Master Thesis - Universität Kassel: Aktuelles · This study is a master thesis of Eng. Fadi...

89

Transcript of Master Thesis - Universität Kassel: Aktuelles · This study is a master thesis of Eng. Fadi...

Master Thesis: Large scale RE projects in Syria –

An analysis of the institutional and legal framework In view of the Egyptian experience

Prepared by: Fadi Aljawabra

Supervisors: Prof. Mohamad ElSobki Cairo University Prof. Jürgen schmid Kassel University

February 2011

Master Thesis- REMENA-Fadi Aljawabra

Table of Contents Synopses ....................................................................................................................................... 6 Executive summery ...................................................................................................................... 8 Introduction .................................................................................................................................. 14 Objective ...................................................................................................................................... 14 The Scope and Methodology .................................................................................................... 14 1. Introduction to the energy sector ......................................................................................... 17

1.1 Energy trends in Syria .................................................................................................... 17 1.1.1 Electricity Sector ........................................................................................................... 17 1.1.2 Oil Sector ....................................................................................................................... 19 1.1.3 Gas Sector ..................................................................................................................... 20 1.1.4 Renewable Energy Sources ........................................................................................ 20 1.2 Supply and demand in Syria .......................................................................................... 22 1.2.1 Electricity Demand: ....................................................................................................... 22 1.2.2 Electricity Supply:.......................................................................................................... 24 1.3 Findings: ............................................................................................................................ 26

2. Potentials and Obligations .................................................................................................... 29 2.1 Potential of RE sources ................................................................................................... 29 2.1.1 Solar Energy .................................................................................................................. 29 2.1.2 Wind Energy .................................................................................................................. 32 2.1.3 Hydro Power .................................................................................................................. 34 2.1.4 Biomass .......................................................................................................................... 37 2.1.5 Urban Waste .................................................................................................................. 37 2.1.6. Geothermal Energy ..................................................................................................... 38 2.2 International Conventions and Agreements ................................................................. 38 2.2.1 Environmental agreements: ........................................................................................ 38 2.2.2 The Association Agreement between Syria and the EU ......................................... 39 2.3 National Programmes ...................................................................................................... 40 2.3.1 The 10th five year plan 2006‐2011 .................................................................................... 40 2.3.2 The 11th five year plan 2011-2016 ............................................................................. 40 2.3.3 Master Plan 2010.............................................................................................................. 41 2. 4 Findings ............................................................................................................................... 45

3. Institutional framework ........................................................................................................... 47 3.1 Current institutional framework in Syria ........................................................................ 47 3.1.1 The electricity law No. 32 ............................................................................................ 49 3.2 The role of the RE organisation stakeholders in Syria ............................................... 52 3.4 Comparison with Egypt current institutional set-up ..................................................... 54 3.5 Findings ............................................................................................................................. 58

4. Legal framework ..................................................................................................................... 61 4.1. Public Private Partnership (PPP) in Syria ................................................................... 61 4.1.1 History of PPP ............................................................................................................... 61 4.2 Independent Power Producers (IPP) Laws in Syria ................................................... 62 4.2.1 Tender law ..................................................................................................................... 62 4.2.2 Corporate law ................................................................................................................ 63 4.2.3 The law No. 32 date 14 Nov. 2010 ............................................................................ 63 4.2.4 Investment promotion laws and institutions .............................................................. 64 4.2.5 Tax and customs ........................................................................................................... 66

1/87

Master Thesis- REMENA-Fadi Aljawabra

4.3 Purchase Agreement (PPA) ........................................................................................... 66 4.4 Feed-in Tariff Power ........................................................................................................ 67 4.5 Comparison with Egypt ................................................................................................... 67

5. Conclusion ............................................................................................................................... 71 5.1 RE Institutional Framework: ........................................................................................... 71 5.1.1 Achievements of the Syrian RE- institutional framework ........................................ 71 5.1.2 Obstacles of the Syrian RE-institutional framework ................................................ 72 5.1.3 Suggestions how to overcome the challenges ......................................................... 72 5.2 RE-Legal Framework:...................................................................................................... 74 5.2.1 Achievements of the Syrian RE- legal framework ................................................... 74 5.2.2 Obstacles of the Syrian RE- Legal Framework ........................................................ 75 5.2.3 Suggestions how to overcome the legal challenges ............................................... 75 List of References: .................................................................................................................. 77

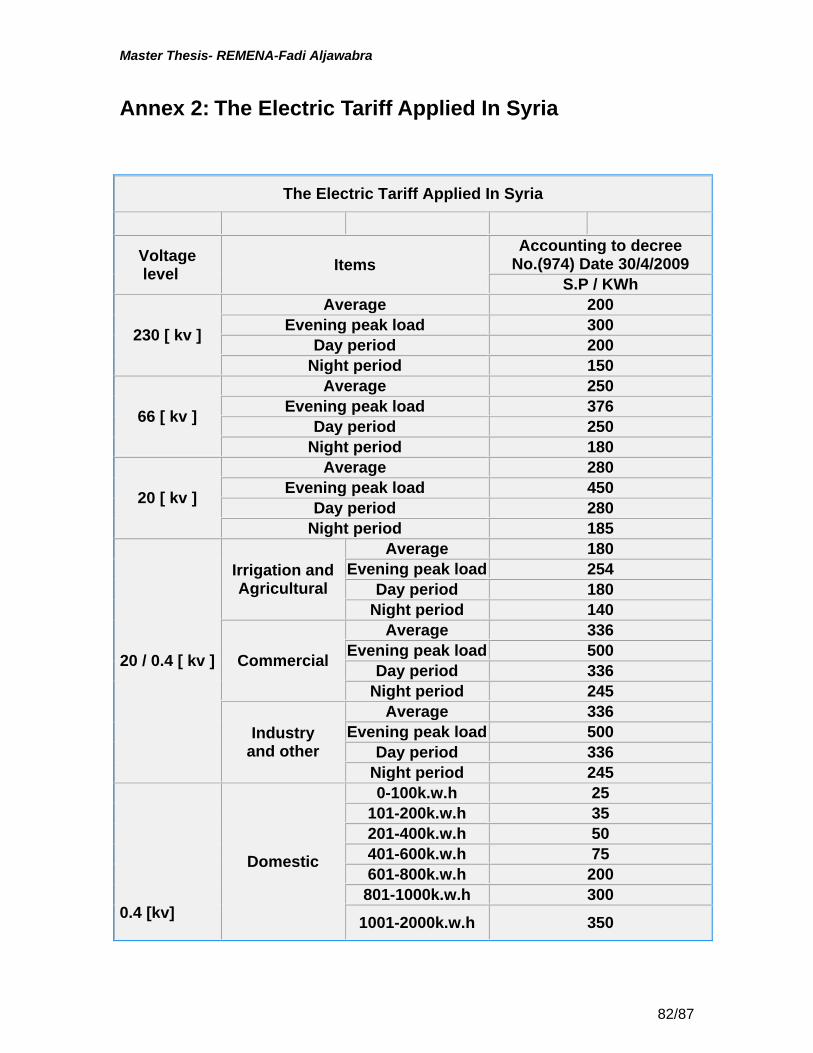

Annex 1: Case study- Expected results (wind energy sector): ............................................ 79 Annex 2: The Electric Tariff Applied In Syria .......................................................................... 82 Annex 3: Organisational chart of the National Energy Research Centre in Syria: ........... 84 Annex 4: Organisational chart of the New & Renewable Energy Authority: ...................... 85 Annex 5: Organisational chart of the Public Establishment of Electricity for Generation and Transmission in Syria: ........................................................................................................ 86 Annex 6: Top 10 wind turbine manufacturers by annual market share in 2009: ............... 88

2/87

Master Thesis- REMENA-Fadi Aljawabra

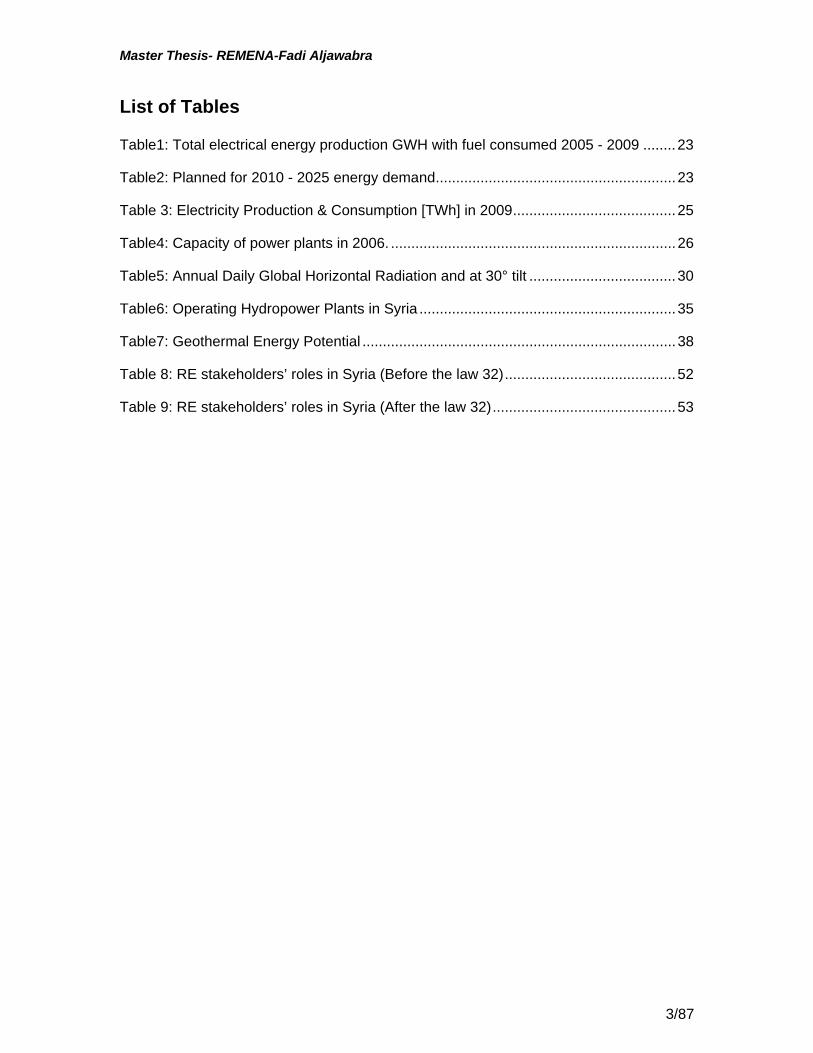

List of Tables

Table1: Total electrical energy production GWH with fuel consumed 2005 - 2009 ........ 23

Table2: Planned for 2010 - 2025 energy demand ........................................................... 23

Table 3: Electricity Production & Consumption [TWh] in 2009 ........................................ 25

Table4: Capacity of power plants in 2006. ...................................................................... 26

Table5: Annual Daily Global Horizontal Radiation and at 30° tilt .................................... 30

Table6: Operating Hydropower Plants in Syria ............................................................... 35

Table7: Geothermal Energy Potential ............................................................................. 38

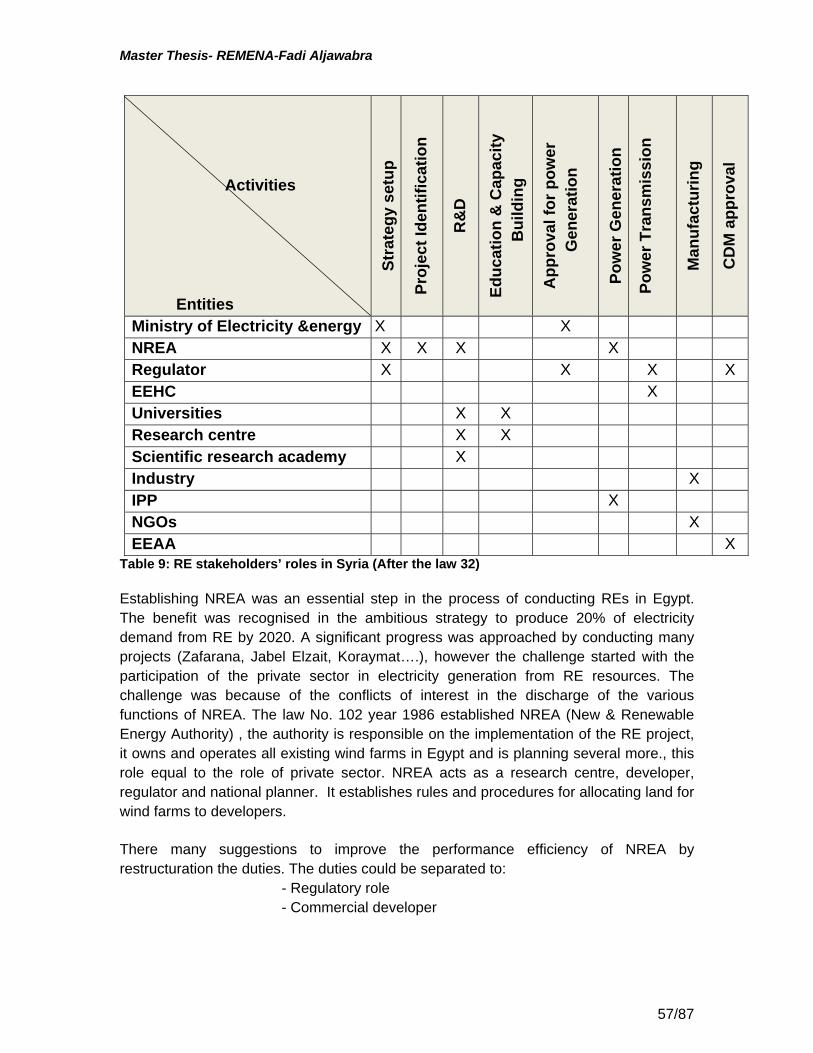

Table 8: RE stakeholders’ roles in Syria (Before the law 32) .......................................... 52

Table 9: RE stakeholders’ roles in Syria (After the law 32) ............................................. 53

3/87

Master Thesis- REMENA-Fadi Aljawabra

List of figures

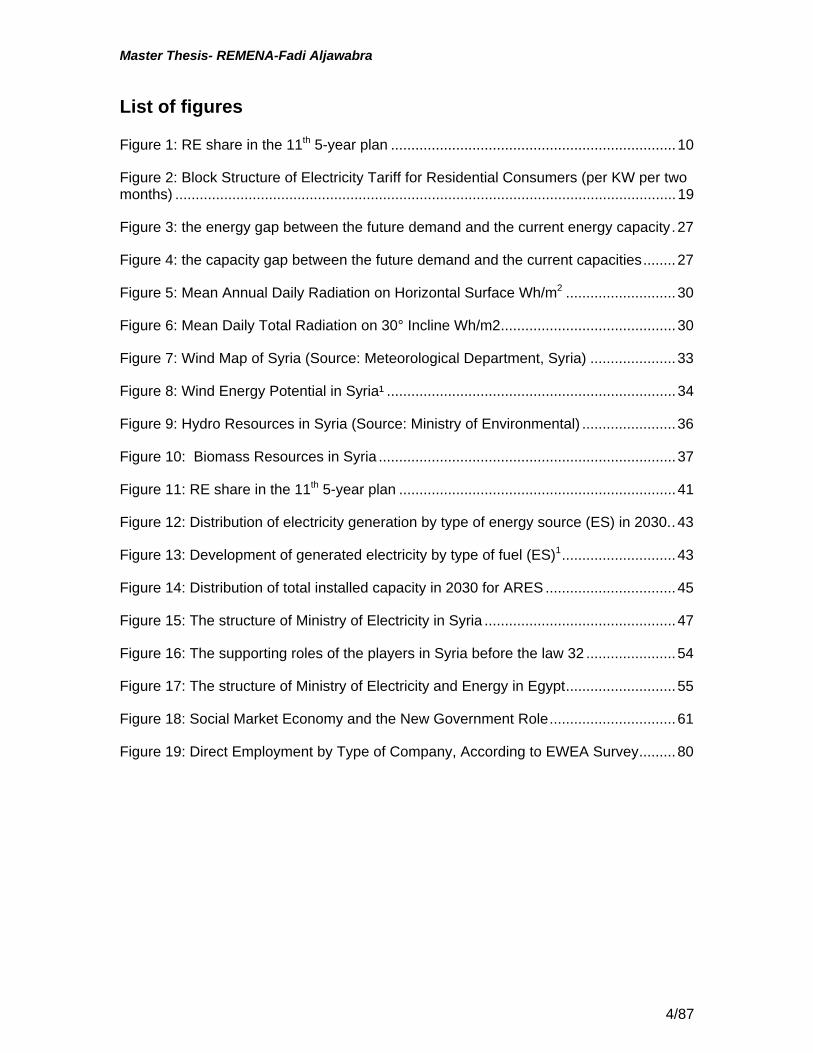

Figure 1: RE share in the 11th 5-year plan ...................................................................... 10

Figure 2: Block Structure of Electricity Tariff for Residential Consumers (per KW per two months) ........................................................................................................................... 19

Figure 3: the energy gap between the future demand and the current energy capacity . 27

Figure 4: the capacity gap between the future demand and the current capacities ........ 27

Figure 5: Mean Annual Daily Radiation on Horizontal Surface Wh/m2 ........................... 30

Figure 6: Mean Daily Total Radiation on 30° Incline Wh/m2 ........................................... 30

Figure 7: Wind Map of Syria (Source: Meteorological Department, Syria) ..................... 33

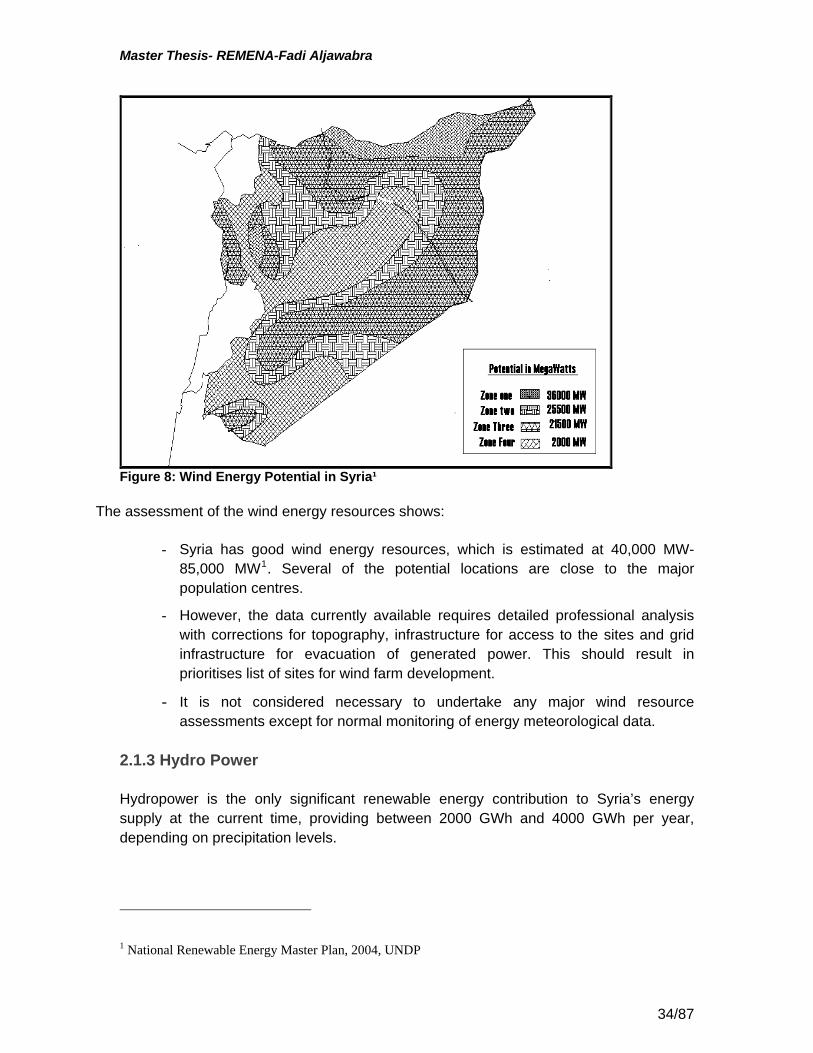

Figure 8: Wind Energy Potential in Syria¹ ....................................................................... 34

Figure 9: Hydro Resources in Syria (Source: Ministry of Environmental) ....................... 36

Figure 10: Biomass Resources in Syria ......................................................................... 37

Figure 11: RE share in the 11th 5-year plan .................................................................... 41

Figure 12: Distribution of electricity generation by type of energy source (ES) in 2030. . 43

Figure 13: Development of generated electricity by type of fuel (ES)1 ............................ 43

Figure 14: Distribution of total installed capacity in 2030 for ARES ................................ 45

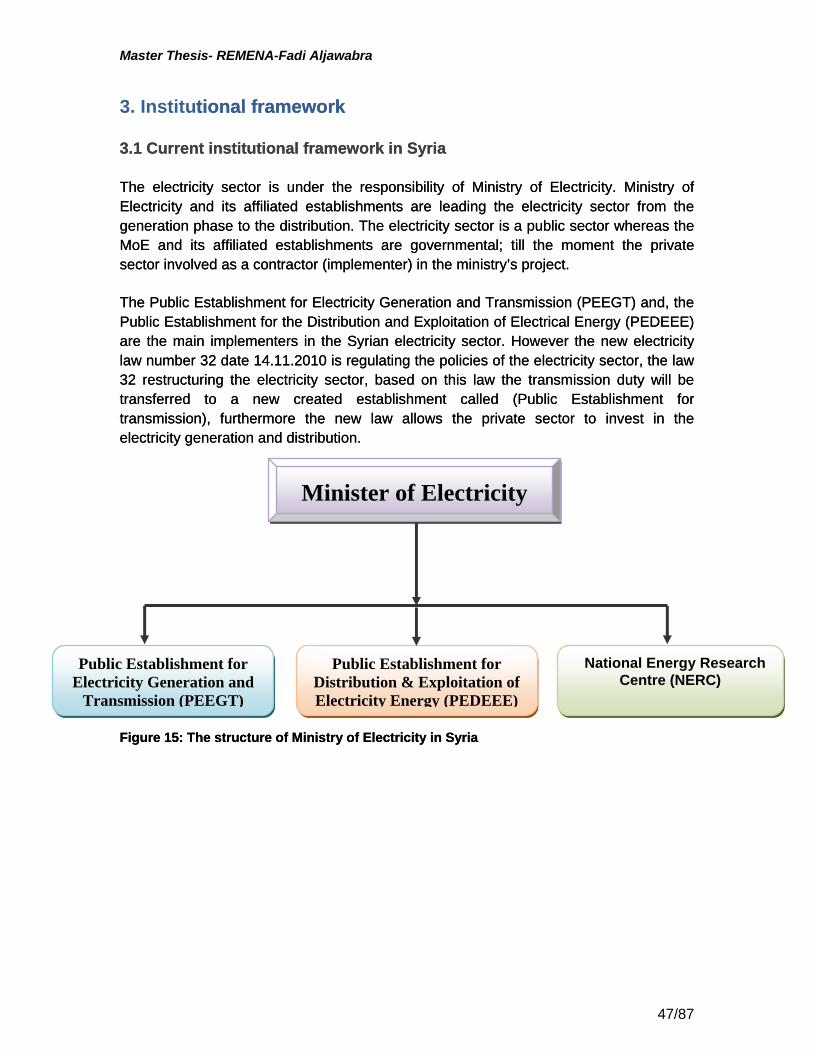

Figure 15: The structure of Ministry of Electricity in Syria ............................................... 47

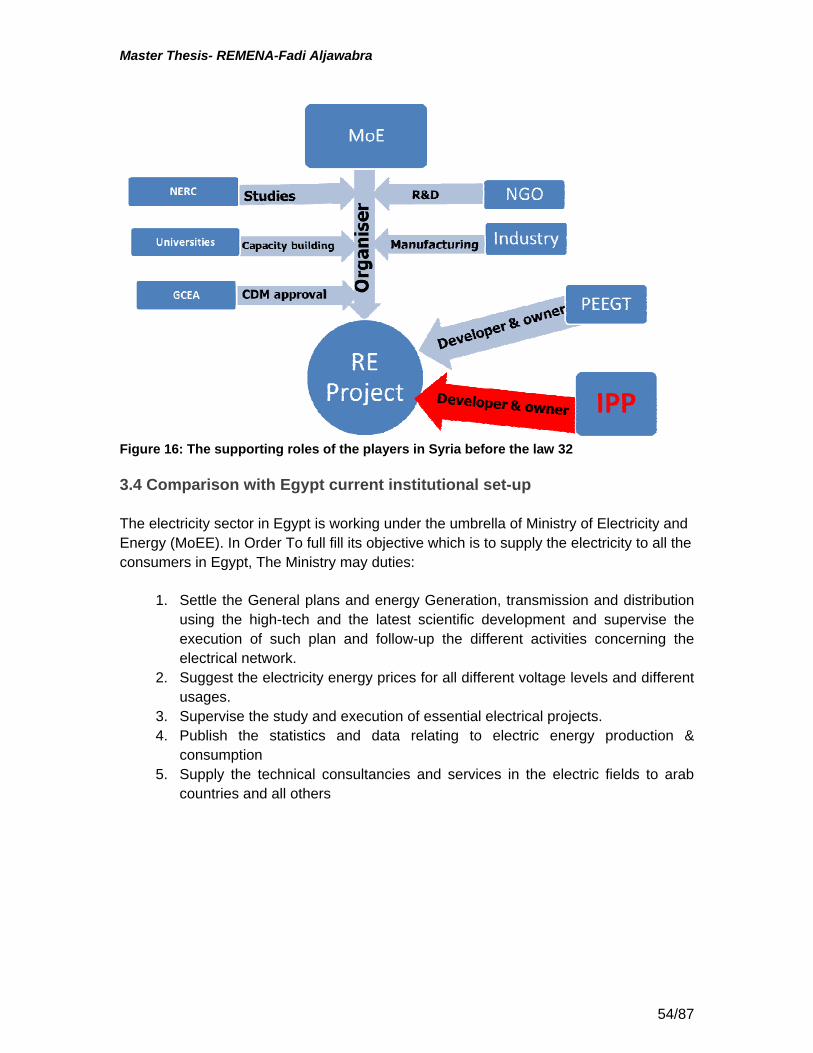

Figure 16: The supporting roles of the players in Syria before the law 32 ...................... 54

Figure 17: The structure of Ministry of Electricity and Energy in Egypt ........................... 55

Figure 18: Social Market Economy and the New Government Role ............................... 61

Figure 19: Direct Employment by Type of Company, According to EWEA Survey ......... 80

4/87

Master Thesis- REMENA-Fadi Aljawabra

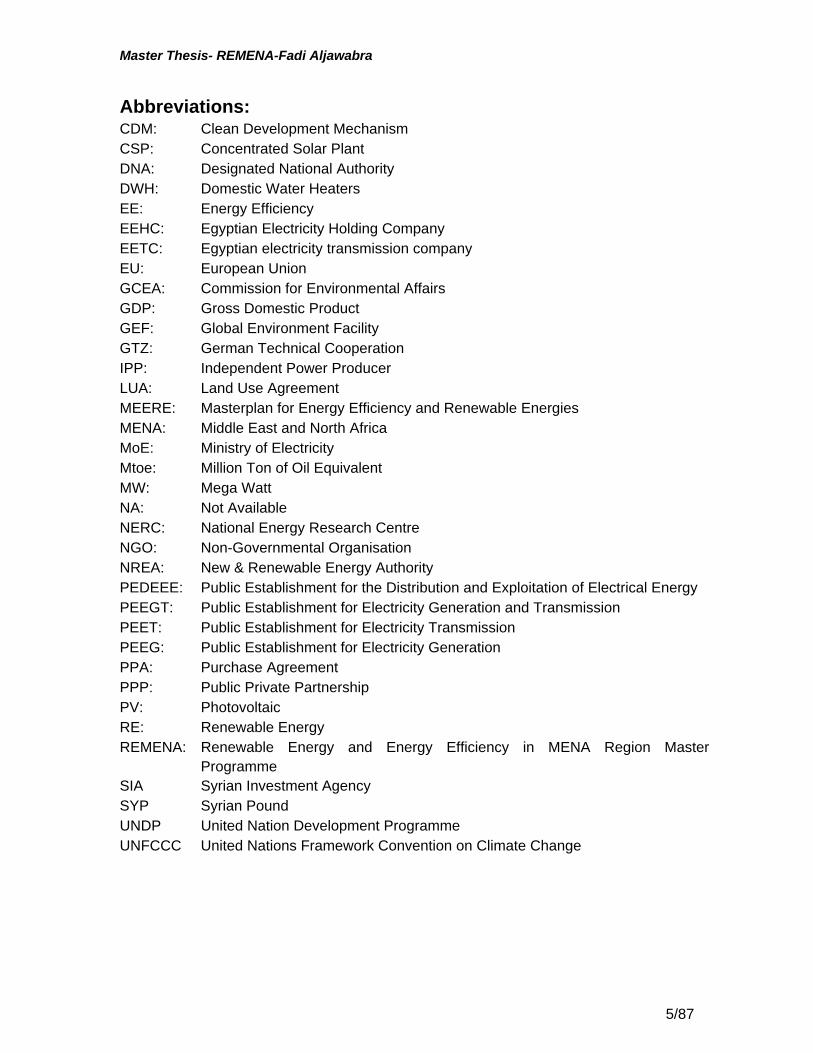

Abbreviations: CDM: Clean Development Mechanism CSP: Concentrated Solar Plant DNA: Designated National Authority DWH: Domestic Water Heaters EE: Energy Efficiency EEHC: Egyptian Electricity Holding Company EETC: Egyptian electricity transmission company EU: European Union GCEA: Commission for Environmental Affairs GDP: Gross Domestic Product GEF: Global Environment Facility GTZ: German Technical Cooperation IPP: Independent Power Producer LUA: Land Use Agreement MEERE: Masterplan for Energy Efficiency and Renewable Energies MENA: Middle East and North Africa MoE: Ministry of Electricity Mtoe: Million Ton of Oil Equivalent MW: Mega Watt NA: Not Available NERC: National Energy Research Centre NGO: Non-Governmental Organisation NREA: New & Renewable Energy Authority PEDEEE: Public Establishment for the Distribution and Exploitation of Electrical Energy PEEGT: Public Establishment for Electricity Generation and Transmission PEET: Public Establishment for Electricity Transmission PEEG: Public Establishment for Electricity Generation PPA: Purchase Agreement PPP: Public Private Partnership PV: Photovoltaic RE: Renewable Energy REMENA: Renewable Energy and Energy Efficiency in MENA Region Master

Programme SIA Syrian Investment Agency SYP Syrian Pound UNDP United Nation Development Programme UNFCCC United Nations Framework Convention on Climate Change

5/87

Master Thesis- REMENA-Fadi Aljawabra

Synopses

This study is a master thesis of Eng. Fadi Aljawabra for Renewable Energy and Energy Efficiency in MENA Region Master Programme. REMENA is a joint Master Programme between Cairo University and Kassel University and subsidised by DAAD (German Academic Exchange Agency).

The main objective of this study is to assess the current situation of the large scale renewable energy projects with review of the institutional roles of relevant entities and the opportunities of private sector participation in Syria. In addition to comparing the anticipated results with the Egyptian experience.

Additionally this study could be considered as a hand out for the outside observer in order to recognise the current situation in Syria, this thesis clarifies the role of the establishments and the current laws which promote the large scale RE projects and pave the road for efficient and successful participation of private sector.

The reasons for choosing the Egyptian experience to compare with are: - The similarity in the institutional, legal, economic, national resources and social

situations in Syria and Egypt - The long experience in Egypt in terms of promoting RE - The achievements were reached in Egypt in order to develop large scale

projects (540MW Wind plants, 20 MW Concentrated Solar Plant (CSP) plant up till year 2011)

- The existence of the ambitious policy for RE in Egypt (20% of the generated electricity from renewable energy by 2020, including a 12% contribution from wind energy).

In purpose of the development of electricity sector, the Syrian government made a major step by issuing the electricity law no. 32 dated 2010. The law regulates and restructures the electricity sector and allows the private sector to invest in the electricity generation and distribution activities.

The big gap between the future demand and the current supply needs to be fulfilled by building new power plants; the RE could be feasible choice to participate in bridging the gap between the supply and demand. Ministry of Electricity aims to increase its capacity from 7500 MW to 12000 MW by the end of the 11th 5 year plan (2011-2016).

The absence of clear strategy for RE and absence of successful RE projects was partly was solved by the electricity law. Moreover the absence of institutional structure for RE sector development in MoE leads to a poor policy making and implementation.

6/87

Master Thesis- REMENA-Fadi Aljawabra

Currently the PEEGT is the governmental power producer and power purchaser; in this case a conflict of interest will be existed while theoretically PEEGT should be the governmental competitor of the IPP from commercial point of view.

One of the main obstacles in the RE-legal framework is the absence of financial mechanisms and guarantee system which ensure the financial sustainability of the projects; it would be required to establish a sustainable fund in order to reduce the cost of the financial risks.

The main suggestions to develop the institutional framework in Syria:

- Carrying out a national Syrian policy for RE sector development.

- Establishing institutional development programmes and projects.

- Establishing RE departments in Ministry of Electricity (MoE), the Public Establishment for Electricity for Generation (PEEG) and the Public Establishment for Electricity Transmission (PEET).

- Establish PPP department in MoE.

- Restructure the Public Establishment for Electricity Generation and Transmission (PEEGT) to two establishments PEEG and PEET.

The main suggestions to develop the legal framework in Syria: - Applying commercial management tools in the contractual process and bidding

system, and applying the marketing tools and developing the financial system.

- Establishing incentives system based on performance contracts linked to performance indicators.

- Establishing tariff systems based on cost figures.

- Issuing technical studies and standards.

7/87

Master Thesis- REMENA-Fadi Aljawabra

Executive summery

This study is a master thesis of Eng. Fadi Aljawabra for Renewable Energy and Energy Efficiency in MENA Region Master Programme (REMENA). REMENA is a joint course between Cairo University-Egypt and Kassel University- Germany and subsidised by DAAD (German Academic Exchange Agency).

The overall objective of REMENA MSc programme is to educate specialists in the field of renewable energy and energy efficiency who are able to manage complex projects for international institutions and companies operating in the MENA region.

The main objective of this study is to assess the current situation of the large scale renewable energy projects with review of the institutional roles of relevant entities and the opportunities of private sector participation. In addition to compare the results with the Egyptian experience.

Additionally this study could be considered as a hand out for the outside observer to recognise the current situation in Syria, this study gives an overview for the role of the establishments and the current laws which promote the large scale RE projects and pave the road for efficient and successful participation of private sector.

The government of Syrian Arab Republic stats its desire to establish a developed RE sector, however there are no tangible results for any RE project yet. This study is trying to cover the institutional and legal barriers for RE development in Syria. The RE technical researches are required for sector growth, nevertheless, the existence of advanced institutional framework which leads the sector through the development process (policy making, strategy making, implementation and monitoring & evaluation) is essential, this clear framework with clear role for each player in the sector should be harmonised with laws and legal system in purpose of translating the sector strategy.

This thesis scans the challenges in the current institutional framework and laws which don’t support RE sector development. Syria was aware of the importance of these components of development and took crucial steps building a sustainable RE sector, in the last two months of the year 2010 Syria issued the electricity law no. 32 which regulates the electricity sector and allows the private sector to invest in electricity projects. Another step was taken by Syria by setting a nominal target for RE projects which was missed before.

The growth of RE sector in Egypt was obvious through the ambitious target which was set and the installed capacity, this capacity is the highest installed capacity from RE resources in MENA region. There are many reasons for this development, one of these reasons was the existence of the New & Renewable Energy Authority (NREA) which lead the RE sector and is responsible for the sector development, the Egyptian experience approves that the institutional and legal development should be in parallel

8/87

Master Thesis- REMENA-Fadi Aljawabra

with the technical one, moreover establishing sustainable advanced sector encourages for more technical research and development.

This study don’t not try to assess the Egyptian experience neither detailed comparison with the Syrian situation, however the study develops suggestions for possible Syrian RE programme based on the lesson learned from the Egyptian experience.

- The reasons for choosing the Egyptian experience are: - The big similarity in the institutional, legal, economic, national resources and

social situations in Syria and Egypt - The long experience in Egypt in terms of promoting RE, and establishing

institutional structure for RE development, for instance (NREA) which was established since 1986.

- The achievements were reached in Egypt in order to develop a large scale projects (for instance: Zafarana wind farms 540MW current capacity, Kuraymat CSP plant 20 MW).

- The existence of the ambitious policy, this policy was approved by the Supreme Council of Energy in February 2008 in order to satisfy 20% of the generated electricity from renewable energy by 20201, including a 12% contribution from wind energy. This figure translates into about 7200 MW of grid-connected wind farms and 8% contribution from other sources, mainly hydro and solar energy.

The research started with the description of energy trends in Syria in the first chapter, this description includes electricity, oil, gas and renewable energy sectors, and additionally the chapter contains the demand and supply in Syria. The approximate annual increase of the electricity demand in Syria is 6%. The total installed power generating capacity in Syria was about 8,359 MW in 2009, of which 7,518 MW was actually available with 67% average system load factor. The need to increase the supply capacity is urgent as Syria faced a lack of electricity power supply in 2010. The big gap between the future demand and the current supply needs to be fulfilled by building new power plants; the RE could be feasible choice to participate in bridging the gap between the supply and demand. Ministry of Electricity aims to increase its capacity to 12000 MW (currently 7500 MW) by the end of the 11th 5 year plan (2011-2016).

The second chapter was important to verify the potentials for the large scale RE projects. These potentials were technical as national sources (Wind, Solar, Biomass, Hydro and wastewater), and legislative potential such as obligations and agreements (international and regional agreements) and existence national policies.

1 NREA Annual Report 2009

9/87

Master Thesis- REMENA-Fadi Aljawabra

Syria has tremendous solar energy resources which are available in a largely uniform manner across the geographical spread of the country, based on the Syrian atlas the global radiation at 30° tilt is approximately 115 KWh/m². Syria has good wind energy resources, which is estimated to be 40,000-85,0001 MW. Several of the potential locations are close to the major population centres.

The national Syrian 11th 5-year plan 2011-2016 of the Ministry of Electricity stats a specific target of RE plants that should be built in the plan duration. The strategic plan mainly focus on wind and photovoltaic energy plants in the supply side, the numeral target of this policy is to reach 2% of the total electricity supply generated from wind and PV by 2016. The planed RE power plants as governmental projects in the 11th 5-year plan are:

- 150 MW wind plants - 5 MW photovoltaic plants - 10 MW CSP

Figure 1: RE share in the 11th 5-year plan

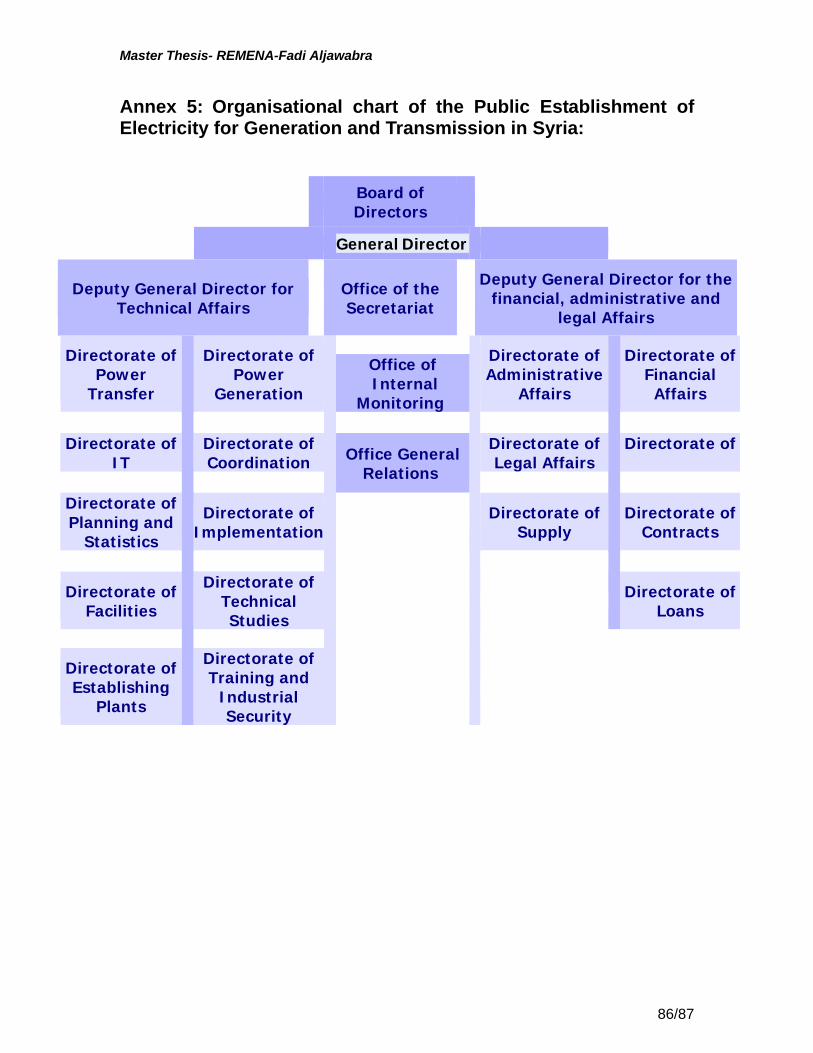

The 3rd chapter of the study discussed the institutional framework of RE sector in Syria by analysing the role of each sector player based on the establishing decrees. The institutions in Egypt were described by the strengths and weaknesses of the current situation. The electricity sector in Syria comes under the responsibility of the Ministry of Electricity (MoE) who controls Public Establishment for Electricity Generation and Transmission (PEEGT) and the Public Establishment for the Distribution and Exploitation of Electrical Energy (PEDEEE). In Syria, the law no. 32 clearly determined MoE as a regulator for the

1 Reference: National Renewable Energy Master Plan, 2004, UNDP

10/87

Master Thesis- REMENA-Fadi Aljawabra

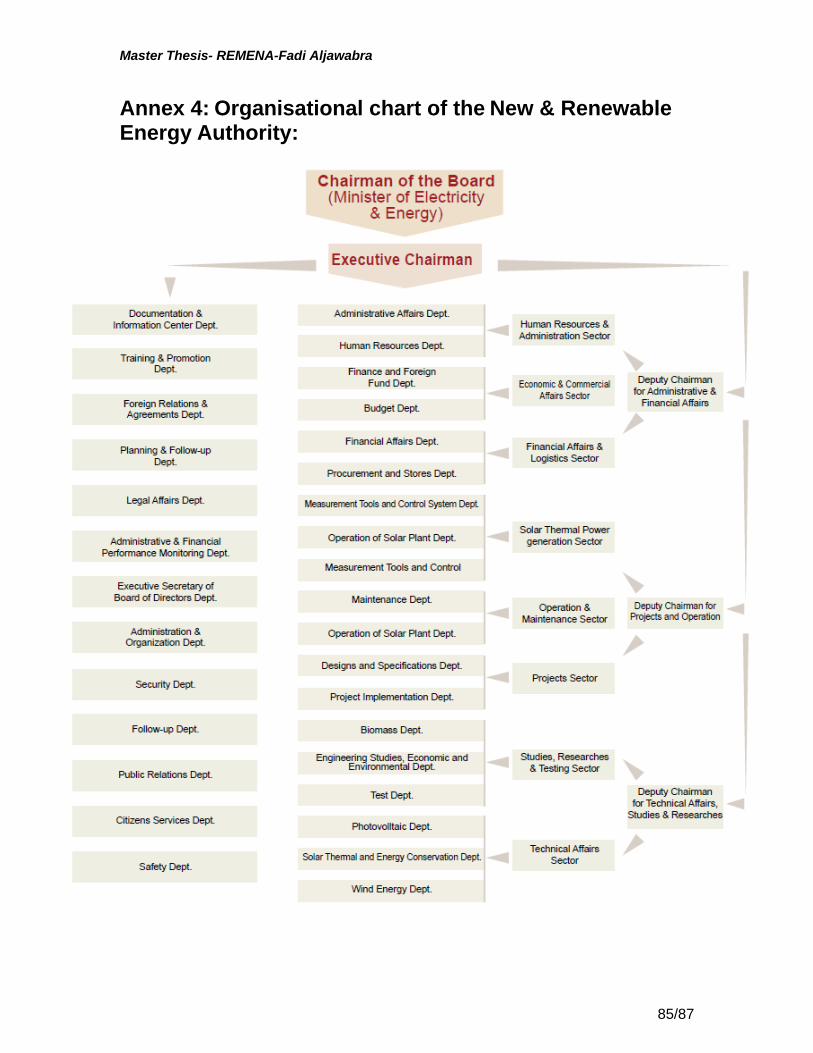

sector; additionally PEEGT was mandated as a developer. The separation between the regulating role and the developing role is a subjective point which prevents the conflict of interests. However the organisation who has the capacity to work daily with REs is the National Energy Research Centre (NERC), NERC is mandated to cover the researches and supporting the decision makers by studies, NERC should support MoE in the RE technical staff while MoE have good experience in contracts and tenders

The Egyptian RE sector framework were special in the region, at a very early stage a specific body for RE development which is the National Renewable Energy Authorities (NREA, the authority is responsible for the implementation of the RE projects, it owns and operates all existing wind farms in Egypt and is planning several more. Currently NREA act as a research centre, developer, regulator and national planner. It establishes rules and procedures with the electricity regulatory agency for allocating land for wind farms to developers. The role of NREA needs to be revisited to avoid the conflict of interest.

The absence of clear strategy for RE and absence of successful RE projects was partly was solved by the electricity law. Moreover the absence of institutional structure for RE sector development in MoE leads to a poor policy making and implementation. As a regulator, MoE has no previous experience in attracting the private sector in the generation sector; this could lead to a poor private sector participation in electricity sector

Currently the PEEGT is the governmental power producer and power purchaser; in this case a conflict of interest will be existed while theoretically PEEGT should be the governmental competitor of the IPP from commercial point of view.

Chapter 4 discussed the legal situation including the laws of developing RE projects and investment incentives in Syria (Contracts Law, Tax taw, Investment law and private sector participation law). Based on the law no 32 year 2010 private investors could be involved in the electricity sector in deferent ways:

Investor: Pay the investment cost and be paid back by the plant operator from the revenues.

The operator: Operate the plant and be paid back according to the pre-agreed electricity tariff

The distributor: Buy the electricity from the operator and sell it to consumers.

The Syrian Investment Agency (SIA) enjoys legal personality, financial and administrative autonomy; however it is linked directly to the prime Minister. SIA has a vision to create an investment environment which is suitable for sustainable development in Syria. SIA duty is to encourage and facilitate the inflow of foreign direct investment by contributing to the development of the socio-economic performance.

11/87

Master Thesis- REMENA-Fadi Aljawabra

The Legislative Decree (law no.8) includes the sectors that benefit from the advantage and incentives granted according to this Decree. Electricity sector was mentioned in the decree as the sector which shall benefit from the exemptions stipulated in the effective Income Tax Law and all the advantages and guarantees stipulated in this legislative decree. One of the main obstacles in the RE-legal framework is the absence of financial mechanisms and guarantee system which ensure the financial sustainability of the projects; it would be required to establish a sustainable fund in order to reduce the cost of the financial risks.

Chapter 5 summarised the findings in each chapter in accordance with the institutional and legal frameworks achievements, obstacles and the recommendations of development to overcome the challenges.

The main suggestions to develop the institutional framework in Syria: - Carrying out a national Syrian policy for RE sector development - Establishing institutional development programmes and projects. These

programmes and projects should lead to efficient institutional and legal mechanisms, since these mechanisms pave the road for sustainable RE projects through sustainable and transparent financial mechanisms.

- Establishing RE department in MoE responsible for: Planning and policy making Issuing projects proposals Preparation of feasibility studies for a pipeline of generating projects that

could be offered to private investors Assessment (in cooperation with Ministry of Finance) the need for

guarantee packages or other credit enhancement instruments Preparation for IPP bidding packages for the selected generating plants

and carry out a transparent bidding process. Giving the sophistication and experience of private investors.

- Establishing a department for Renewable Energy at PEEGT responsible for: RE resources planning for utilisation Implementation of RE matured technologies Rendering of consultancy services in the field of RE exploitation, Training, information dissemination and capacity building Transfer of technology and the development of local industry.

- Establish a governmental PPP unit in the ministry of electricity to be in charge of: Management of private sector participation development Implementation of necessary regulations and Communication with

private sector

12/87

Master Thesis- REMENA-Fadi Aljawabra

- Establishing transmission establishment in order to avoid the conflict of interest which will be exist in the PEEGT, while theoretically it should be a competitor of the IPP from a commercial point of view.

The main suggestions to develop the legal framework in Syria: - Applying commercial management tools in the contractual process and bidding

system, and applying the marketing tools and developing the financial system. - Establishing incentives system based on performance contracts linked to

performance indicators. - Establishing tariff systems based on cost figures (renewable energy production

costs or avoided costs of conventional supply) or premium systems based on market prices for electricity (e.g. electricity wholesale prices) and a specific additional premium.

- Issuing technical documents conclude: Electricity Generation Code Electricity Transmission Code Performance Indicators System Technical conditions for licensing Third part access regulations

- Studying the proposed initiative to establish a Fund in order to subsidise the RE

sector. This Fund would target to compensate the losses of PEET. The law determined the financial sources of the fund as follow:

The saving from the kW electricity produced from RE sources instead of the fuel

The governmental grants from the public budget The non-governmental grants The revenues of the fund investment

A rough case study for the possible results of applying the recommendations was prepared (Annex 1). It is estimated to reach 500 MW wind plants.

Benefit of installing 500 MW wind plant 1. Diversify the fuel sources

and enhance its security of energy supply

2 TWh per annum (0.03 % of needed electricity)

2. Extend the life of the fossil fuel reserves

- 1.5 Million tone of CO2 per annum - Annual price of CO2 credit is 13.5 Million

3. Generate local employment and local market

400 full time job opportunities

4. Diversify the Syrian fuel sources and enhance its security of energy supply

450,000 Toe (0.03 % of needed Fuel)

13/87

Master Thesis- REMENA-Fadi Aljawabra

Introduction

This study is a master thesis of Eng. Fadi Aljawabra for Renewable Energy and Energy Efficiency in MENA Region Master Programme (REMENA). REMENA is a joint Master Programme between Cairo University-Egypt and Kassel University- Germany and subsidised by DAAD (German Academic Exchange Agency).

The overall objective of REMENA MSc programme is to educate specialists in the field of renewable energy and energy efficiency who are able to manage complex projects for international institutions and companies operating in the MENA region.

Objective

To assess the current situation in syria of the large scale renewable energy projects with review of the institutional roles of relevant ministries and the opportunities of private sector participation. In addition to compare the anticipated results with the Egyptian experience.

Additionally this study could be considered as a hand out for the outside observer to recognise the current situation in Syria, this study gives an overview for the role of the establishments and the current laws which promote the large scale RE projects and pave the road for efficient and successful participation of private sector.

The Scope and Methodology

The government of Syrian Arab Republic stats its desire to establish a developed RE sector, however there are no tangible results for any RE project yet. This study is trying to cover the institutional and legal barriers for RE development in Syria. The RE technical researches are required for sector growth, nevertheless, the existence of advanced institutional framework which leads the sector through the development process (Policy making, strategy making, implementation and monitoring & evaluation) is essential, this clear framework with clear role for each player in the sector should be harmonised with laws and legal system in purpose of translating the sector strategies.

This thesis scans the challenges in the current institutional framework and laws which don’t support RE sector development. Syria was aware for the importance of this components of development and took a crucial steps in purpose of building a sustainable RE sector, in the last two months of the year 2010 Syria issued the law 32 which regulates the electricity sector and allows the private sector to invest in electricity projects, the other step was taken by Syria was setting a nominal target for RE projects which was missed before.

14/87

Master Thesis- REMENA-Fadi Aljawabra

Renewable energy sector development would support the governmental efforts in:

- Diversify the Syrian’s fuel sources and enhance its security of energy supply - Reduce its greenhouse gas emissions and enable it to profit from Clean

Development Mechanism (CDM) credits and potential project financing from the Clean Technology Fund

- Generate local employment; - Extend the life of its fossil fuel reserves. - RE cannot displace large conventional power plants, but it can substantially

reduce the need for more fossil fuel fired generating capacity.

The growth of RE sector in Egypt was obvious through the ambitious target which was set and the installed capacity which is the highest installed capacity from RE resources in MENA region. There are many reasons for this development, one of these reasons was the existence of NREA which lead the RE sector and is responsible for the sector development, the Egyptian experience proves that the institutional and legal development should be in parallel with the technical one, moreover establishing sustainable advanced sector encourage for more technical research and development.

This study is not trying to assess the Egyptian experience neither carry out detailed comparison with the Syrian situation, however the study develops the suggestions based on the lesson learned from the Egyptian experience.

There are many reasons for choosing the Egyptian experience:

- The big similarity in the institutional, legal, economic, national resources and social situations in Syria and Egypt

- The long experience in Egypt in terms of promoting RE, and establishing institutional structure for RE development

- The achievements were reached in Egypt in order to develop a large scale projects (for instance: Zafarana wind farms 540MW current capacity, Kuraymat CSP plant 20 MW).

- The existence of the ambitious policy, this policy was approved by Supreme Council of Energy in February 2008 in order to satisfy 20% of the generated electricity from renewable energy by 2020, including a 12% contribution from wind energy. This figure translates into about 7200 MW of grid-connected wind farms and 8% contribution from other sources, mainly hydro and solar energy.

The research started with the description of energy trends in Syria in the 1st chapter, the second chapter was important to verify the potentials for the large scale RE projects. These potentials were technical as national sources (Wind, Solar, Biomass, Hydro and wastewater), and legislative potential such as obligations and agreements (international and regional agreements) and existence national policies. The 3rd chapter of the study discussed the institutional framework of RE sector in Syria by analysing the role of each

15/87

Master Thesis- REMENA-Fadi Aljawabra

sector players based on the establishing decrees. The institutions in Egypt were described by the strengths and weaknesses of the current situation. Chapter 4 discussed the legal situation including the laws of developing RE projects and investment incentives in Syria (Contracts Law, Tax taw, Investment law and private sector participation law). Chapter 5 summarised the findings in each chapter in accordance with the institutional and legal frameworks achievements, obstacles and the recommendations of development to overcome the challenges. A rough case study for the possible results of applying the recommendations was prepared

16/87

Master Thesis- REMENA-Fadi Aljawabra

1. Introduction to the energy sector

1.1 Energy trends in Syria

Syria is an Eastern Mediterranean country with 23 million inhabitants of which almost 20% live in the capital Damascus. The annual per capita income on a purchasing power parity basis was 3,300 € in 2009 and 1,700 € in nominal terms. The Gross Domestic Product growth (GDP) has slowed to 2.2% in 2009 from 5.1% in 2008 and yet higher values before. The population is growing at an annual rate of 2.3%1.

Syria is the only Eastern Mediterranean country with significant hydrocarbon deposits and in 2007 some 94% of the total final electricity energy usage was based on oil (71.4%) and gas (22.4%), the rest being supplied by hydropower (3.7%) and biomass (2.5%). The exports of crude oil and petroleum products (in 2007 amounting in total to 7.6 million tons) contribute significantly to the state budget, but they are offset by the import of 7.4 million tons of petroleum products. The oil sector is still an important part in the Syrian economy, but its share is decreasing, because crude oil production is hampered by dwindling oil resources.

In the past, Syria has always been a net exporter of energy, ,at present time Syria can be considered self-sufficient in energy. At the rate of growth in final energy usage Syria experienced in the past five years (about 6% per annum), Syria is becoming a net energy importing country. The Syrian government pursues the policy to increase the share of natural gas in domestic consumption in particular in power generation so that the net export of crude oil and petroleum products can be maximised.

In this context the Syrian government has also realised that energy efficiency (EE) and the use of renewable energy resources (RE) can play an important role, because both depend on domestic resources.

1.1.1 Electricity Sector

The electricity sector comes under the responsibility of the Ministry of Electricity (MoE) who controls the Public Establishment of Electricity for Generation and Transmission (PEEGT) and the Public Establishment for the Distribution and Exploitation of Electrical Energy (PEDEEE). These two agencies are the main operators in the Syrian electricity sector. However a new electricity law number 32 date 14.11.2010 reorganised the policies of the electricity sector, the law no. 32 restructures the electricity sector, based on this law the transmission duty will be transferred to a new created establishment

1 Reference: Masterplan for Energy Efficiency and Renewable Energies (MEERE)-2010 – prepared by

GTZ and NERC

17/87

Master Thesis- REMENA-Fadi Aljawabra

called (Public Establishment for transmission), furthermore the new law allows the private sector to invest in the electricity generation and distribution.

In 2008, electricity usage in Syria grew by 4% and amounted to 42 TWh. At the same time domestic generation grew by 6% and amounted to 41 TWh, which means that Syria still depended on electricity imports to the extent of some 2% of usage. Peaks demand are in winter when electricity is widely used for space heating and still to a somewhat lesser degree in summer, when it is needed for air conditioning. The load shedding is still common and stand by generators are visible in many locations.

Syria has interconnections at the 400 kV level with Turkey, Jordan and Lebanon and is a part of the regional grid which includes also Egypt and Libya. Interconnections at the 400 kV level with Iraq is under construction. PEDEEE's distribution lines reach nearly 100% of the population.

In 2007 the fuel needs for the Syrian thermal power stations were covered to 65% by oil and to 35% by natural gas. As mentioned above, a further movement towards the use of natural gas is to be expected.

Hydropower contributed 6% to electricity generation in 2009. There is no additional potential for hydropower in Syria.

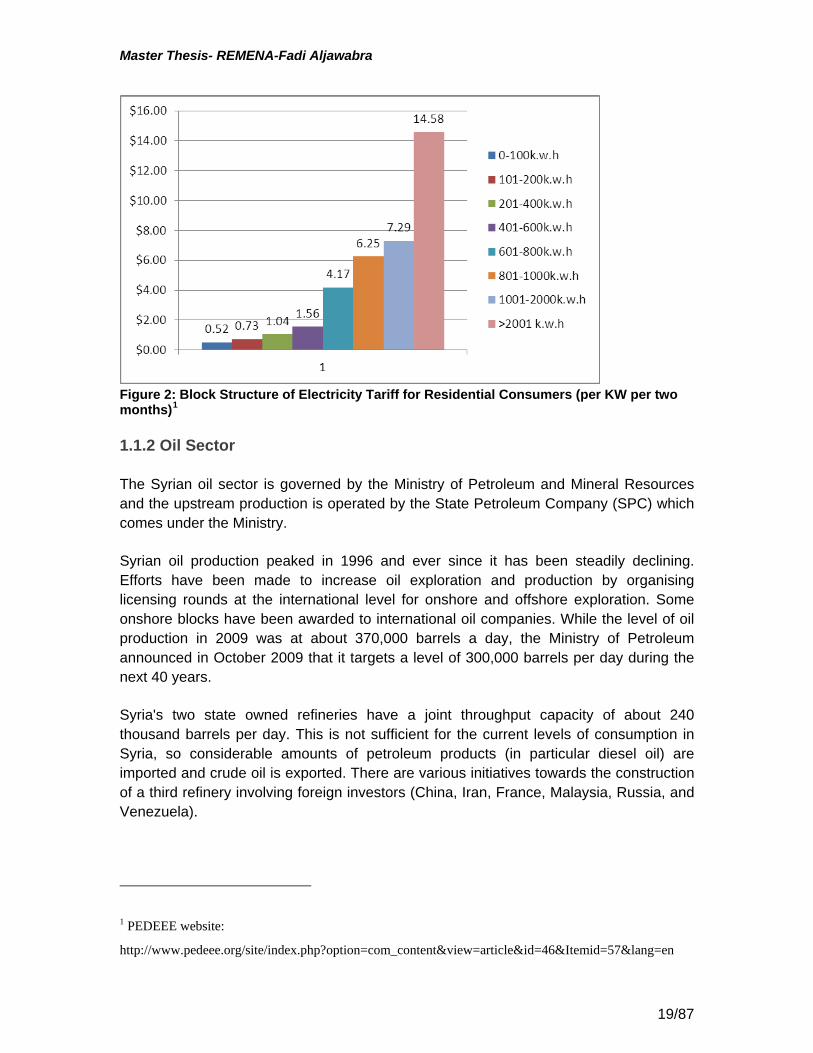

Low electricity prices during the past years have contributed to the rapid growth in electricity demand and to some extent to inefficient electricity use. The government has realised this and in 2007 started to increase the electricity tariffs. Presently there is a block tariff system, where the price depends on the quantity consumed. It consists of eight blocks with the price ranging from as low as 0.25 SYP per kWh(less than 0.5 cents€) for low consumers (with less than 100 KWh usage in two months) to 7 cents€ per kWh for high consumers (above 2,000 kWh usage in two months). The average price paid for electricity by household clients in 2009 was 1.26 SYP/kWh, which is about 0.02 €/kWh. For industrial customers the average price was 2.8 SYP/kWh, equivalent to about 0,045 €/kWh. Added to this price there is a tax of about 10%.

By international standards these prices are still quite low, but in the Syrian economic context they are meaningful and set signals about the scarcity of electricity.

18/87

Master Thesis- REMENA-Fadi Aljawabra

Figure 2: Block Structure of Electricity Tariff for Residential Consumers (per KW per two months)1

1.1.2 Oil Sector

The Syrian oil sector is governed by the Ministry of Petroleum and Mineral Resources and the upstream production is operated by the State Petroleum Company (SPC) which comes under the Ministry.

Syrian oil production peaked in 1996 and ever since it has been steadily declining. Efforts have been made to increase oil exploration and production by organising licensing rounds at the international level for onshore and offshore exploration. Some onshore blocks have been awarded to international oil companies. While the level of oil production in 2009 was at about 370,000 barrels a day, the Ministry of Petroleum announced in October 2009 that it targets a level of 300,000 barrels per day during the next 40 years.

Syria's two state owned refineries have a joint throughput capacity of about 240 thousand barrels per day. This is not sufficient for the current levels of consumption in Syria, so considerable amounts of petroleum products (in particular diesel oil) are imported and crude oil is exported. There are various initiatives towards the construction of a third refinery involving foreign investors (China, Iran, France, Malaysia, Russia, and Venezuela).

1 PEDEEE website:

http://www.pedeee.org/site/index.php?option=com_content&view=article&id=46&Itemid=57&lang=en

19/87

Master Thesis- REMENA-Fadi Aljawabra

Syria's fuel prices were subsidised for many years and the IMF estimated the total sum of all energy subsidies (petroleum products and natural gas) in 2007 to amount to some 13% of GDP. The rather high price subsidies gave rise to significant black marketeering, which meant that a substantial part of the subsidies did not reach the originally intended beneficiaries. The government reacted to this problem and took steps to overcome it. Fuel prices were increased several times during the past three years and now have reached international price levels for petroleum products. Diesel (heating oil) is sold at 20 SYP/l (0.31 €/l) and gasoline at 40 SYP/l (0.62 €/l). Rather than subsidising the fuel prices, the government has shifted to handing out direct subsidies to households, helping them pay for the increased heating oil bill.

1.1.3 Gas Sector

The Syrian gas sector comes also under the Ministry of Petroleum and Mineral Resources and is operated by the Syrian Gas Company belonging to the Ministry. There are significant gas reserves which at present rates of production would last for more than 35 years. Roughly one quarter of the natural gas production is re-injected for enhanced oil recovery or flared; of the remaining three quarters some 80% are used in power production and the rest in industry. Only little gas is used in the domestic or service sector; there is only a very limited gas distribution system.

Syria is connected to the Arab gas pipeline and participates actively in the Europe-Arab Mashreq Gas Market Project, which aims to support the reforms and modernisation of the gas industry with emphasis on gas market and network development, strengthening of the legal and regulatory framework, and transfer of knowhow and expertise to the administrations, institutions and companies of the Mashreq region. The Europe-Arab Mashreq Gas Cooperation Centre has been established in the context of this project. It is located in Damascus and underlines Syrian aspirations to become a regional gas hub.

Presently Syria neither imports nor exports significant amounts of natural gas, but it is expected that on the basis of the policy to replace the use of petroleum products as much as possible by the use of natural gas, Syria will become an important importer of natural gas. The gas imports could come from Egypt through the Arab Gas Pipeline, or in reverser flow from Turkey, once the Arab pipeline is extended into Turkey. Syria also is conducting negotiations in other directions. There are plans for Syria to assist in the development of gas fields in western Iraq and connecting these fields with the Arab Gas Pipeline.

1.1.4 Renewable Energy Sources

Syria has tremendous national resources of renewable energy. The direct use of solar energy for domestic hot water (DHW) is the wider use of renewable energy in Syria. Institutionally there is many parties which play different roles in the renewable energy sector, the renewable energy project is dealt as the conventional energy project,

20/87

Master Thesis- REMENA-Fadi Aljawabra

however the national centre for renewable energy (NREC) is responsible for carrying out the comprehensive studies and research, which help to put in place the proper strategies, polices and long term plans in order to optimise the use of the available energy recourse, and proposing alternatives energies, in coordination with other energy- related organisations in Syria.

During the years 2001- 2004, UNDP sponsored the elaboration of a Renewable Energy Masterplan. It developed a roll out plan for RE investments over the time period up to 2011 amounting to some 1.4 billion USD.

The roll out plan has been implemented only to a very limited extent. Major emphasis was given to the development of wind energy and a serious measurement campaign was conducted at fifteen sites during 2004 and 2005. It confirmed the good potential for wind energy in Syria. Unfortunately this master plan wasn’t applied; however in 2010 The Ministry of Electricity is pursuing various projects for the installation of wind parks.

Syria offers a very good potential for solar energy, in particular for solar thermal applications. It is surprising that only very limited use has been made of this source. There are no effective policies or programmes in place promoting solar thermal applications, but as a consequence of rising prices for traditional heating fuels, a market for solar thermal collectors has been spontaneously developing during the past two years.

Syria represented by NREC with cooperation with GTZ (German Technical Cooperation) prepared a Masterplan for Energy Efficiency and Renewable Energies (MEERE), the MEERE project is the first to analyse the previous studies in a comprehensive framework and develop scenarios till 2030 for the energy demand development under full consideration of EE options and supply scenarios for the same time frame considering the relevant RE options (the scenarios is detailed in MEERE is presented in chapter 2). In addition to the identification of the EE and RE potentials and their integration into a consistent energy planning framework, concrete policy measure were identified and discussed with relevant stakeholders.

21/87

Master Thesis- REMENA-Fadi Aljawabra

1.2 Supply and demand in Syria

1.2.1 Electricity Demand: During the last 5 year plan 2006-2010, the demand for electricity in Syria increased on an average by a very high rate of 6.5% per year, caused by:

1. Strong economic growth 2. Electricity tariffs that are below cost recovery level and that do not

encourage energy efficiency; 3. High technical and non-technical network losses.

During the same period, the power system experienced increasing difficulties in meeting demand. The peak load in 2008 was 6.7 GW; the available generation capacity was 7.1 GW. The shortfall in domestic supply can partly be balanced through electricity imports. Moreover, in 2010 (February & August) the peak load reached an unprecedented amount to reach 7500 MW.

In 2007 the Public Establishment for the Distribution and Exploitation of Electrical Energy (PEDEEE) had about 4.6 million customers and 99% of the population had access to electricity. About 75 % of delivered energy was billed; the remaining 25% consisted of technical (15%) and non-technical (10%)1 losses. About 5% of billed energy was not collected, mainly due to low payment levels by government entities. Assuming more commercially acceptable loss levels, the equivalent financial loss to PEDEEE on account of these three factors was about US$278 million in 2007 alone.

Residential and industrial consumers are the largest categories, constituting 47% and 37%, respectively, of 2007 total electricity consumption. In contrast, the commercial sector constituted only 9% of the electricity consumption¹. Compared to other intermediate income countries, the demand from industry is high and the demand from commercial activities is relatively low. In terms of capacity demand and during system peak, residential users had by far the largest peak demand with 4,760 MW, followed by industry with 1,016 MW. Residential consumers typically use a great deal of capacity but only during relatively short periods, while industry uses a given capacity on a more continuous basis throughout the day. Hence it i s very important to manage the demand of the residential sector by reducing its demand for peak capacity

1 Reference: annual report 2007, PEEGT.MoE

22/87

Master Thesis- REMENA-Fadi Aljawabra

Table1: Total electrical energy production GWH with fuel consumed 2005 - 2009

Years Total production (GWh)

Growth percentage per year

Import (GWH)

Export (GWH)

local consumption (GWH)

fuel needed (million TOE)

2005 34653.40 101 926 33828.4 8.75

2006 37503.60 8% 310 1099 36714.6 9.47

2007 38644.50 3% 1480 1006 39118.5 9.76

2008 41023.40 6% 607 1064 40566.4 10.36

2009 43317.20 5.6% 557 617 43257.2 10.94 2009

Without Hydropower

41257.2 43257.2 9.293

Reference: annual report 2009, PEEGT.MoE

Table2: Planned for 2010 - 2025 energy demand

Years Total production (GWh)

Growth percentage per year

Fuel needed (Mtoe)

Fuel available (Crude +Gas)

Deficit in fuel (Mtoe)

Total cost of deficit

M US$

2010 45916 6% 10.3 13.725 - -

2011 48671 6% 11.0 13.725 - -

2012 51591 6% 11.6 13.725 - -

2013 54687 6% 12.3 13.725 - -

2015 61446 6% 13.8 13.725 0.1 49.7

2020 82227 6% 18.5 13.725 4.8 2062.4

2025 107200 6% 24.1 13.725 10.4 4481.1

2030 136817 6% 30.8 13.725 17.1 7349.7

Reference: annual report 2009, PEEGT.MOE

23/87

Master Thesis- REMENA-Fadi Aljawabra

1.2.2 Electricity Supply: The total installed power generating capacity in Syria was about 8,359 MW in 2009, of which 7,518 MW was actually available with 67% average system load factor1; Although available capacity increased by 5.6% from 2008 to 2009, it is projected that in the period 2011 to 2020 there will be a shortfall in available capacity due to growing demand. The shortfall is expected to continue to rise during 2011 to 2020 due to retirement of an estimated 2,476 MW of older generating units.

Base case demand forecast projects a 67% increase in electricity demand during 2009-20202.

This would require the addition of about 7000 MW of new generation capacity during the same period. The investments in new generating capacity and in expansion of the transmission and distribution networks would cost an estimated US$ 10.5 billion¹, of which US$ 7.0 billion for generation and US$ 3.5 billion for rehabilitation and expansion of the transmission and distribution networks.

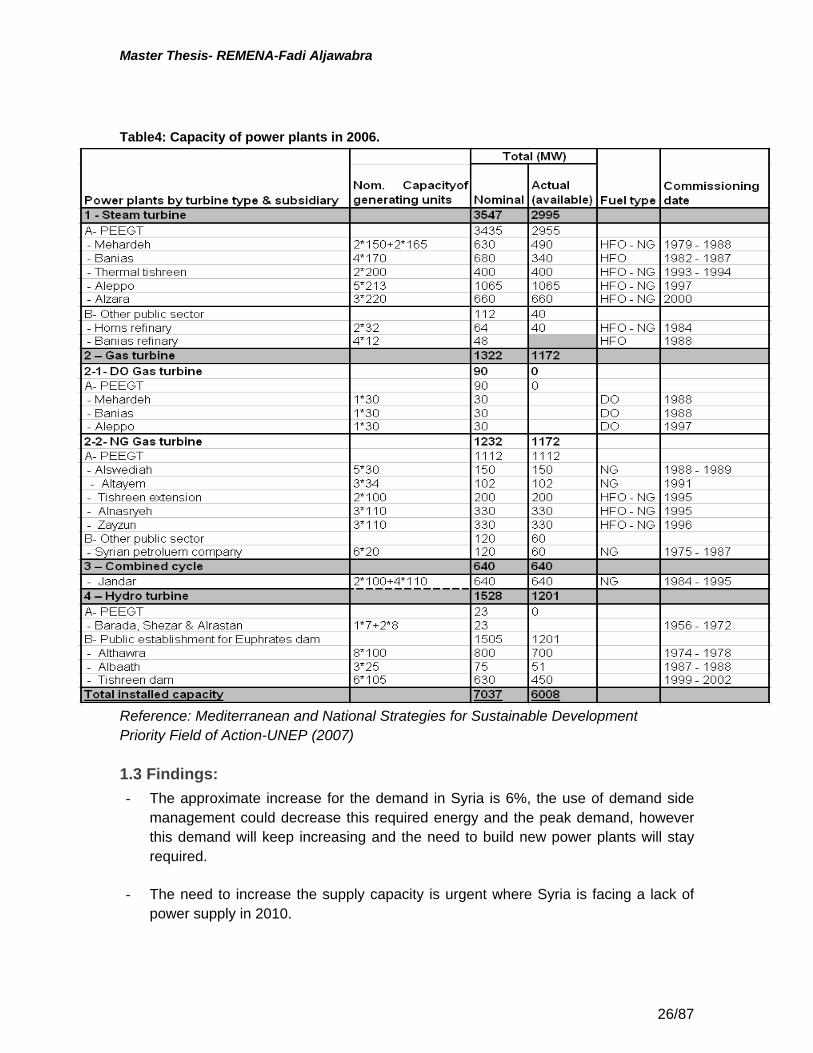

The following table indicates nominal & actual capacity of power plants in Syrian power system by turbine type & subsidiary at the end of 2006.

The transmission system in Syria is planned, operated, and maintained by PEEGT. The main transmission network consists of 5,912 km of 230 kV lines and 1,409 km of 400 kV lines, plus associated substations and transformers

Ministry of Electricity aims to increase its capacity from 7500 MW to 12000 MW by the end of the 11th 5-year plan 2011-2016. However MoE is planning to allow to the private sector to invest in the electricity generation sector, MoE announced three projects according to BOT contract.

The new electricity law number 32 dated 14.11.2010 allows the private sector to invest in generation and distribution, IPPs could have a license from MoE based on financial and technical conditions, this law allows the IPP to establish a power plant which serve their on activities or selling the electricity to the PEET.

1Reference: Nasserieh IPP project, preliminary information memorandum, 2010 2 Reference: Annual report 2009, PEEGT.MOE

24/87

Master Thesis- REMENA-Fadi Aljawabra

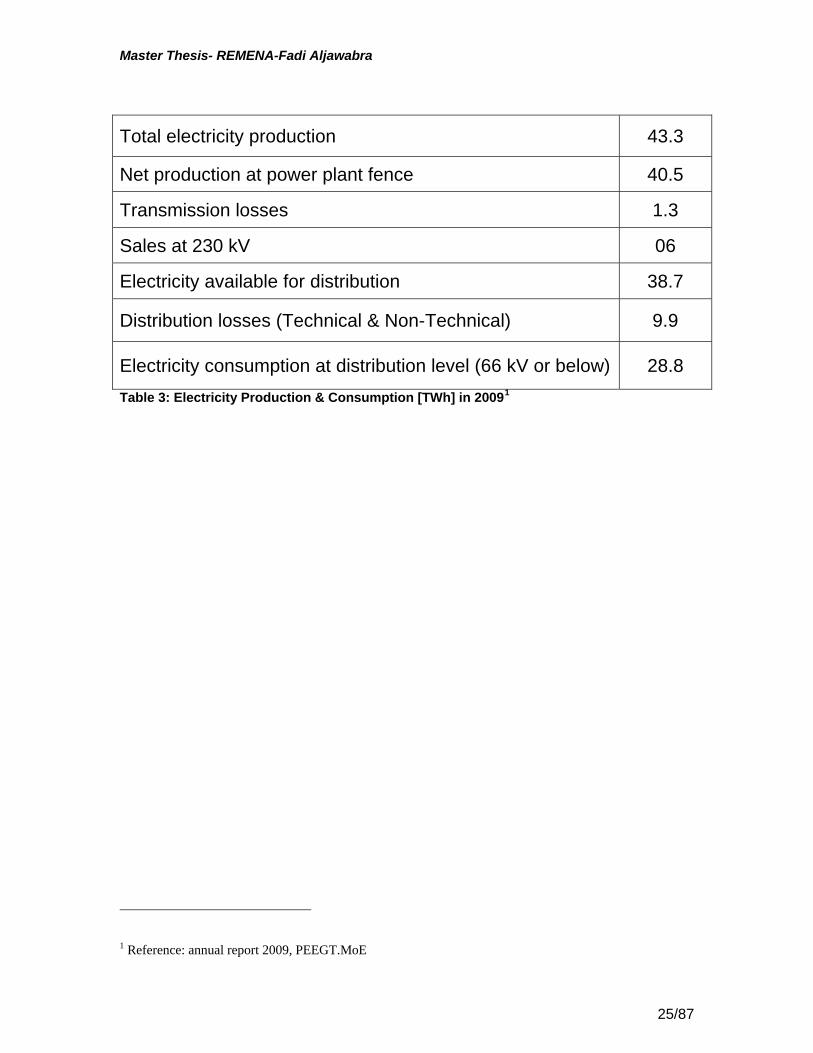

Total electricity production 43.3

Net production at power plant fence 40.5

Transmission losses 1.3

Sales at 230 kV 06

Electricity available for distribution 38.7

Distribution losses (Technical & Non-Technical) 9.9

Electricity consumption at distribution level (66 kV or below) 28.8 Table 3: Electricity Production & Consumption [TWh] in 20091 1 Reference: annual report 2009, PEEGT.MoE

25/87

Master Thesis- REMENA-Fadi Aljawabra

Table4: Capacity of power plants in 2006.

Reference: Mediterranean and National Strategies for Sustainable Development Priority Field of Action-UNEP (2007)

1.3 Findings: - The approximate increase for the demand in Syria is 6%, the use of demand side

management could decrease this required energy and the peak demand, however this demand will keep increasing and the need to build new power plants will stay required.

- The need to increase the supply capacity is urgent where Syria is facing a lack of power supply in 2010.

26/87

Master Thesis- REMENA-Fadi Aljawabra

- The regional electricity grid connection gives Syria an opportunity to sell the electricity in commercial price which support the financial feasibility of RE plants

- The big gap between the future demand and the current supply needs to be fulfilled by building new power plants; the RE could be feasible choice to participate in bridging the gap between the supply and demand.

Figure 3: the energy gap between the future demand and the current energy capacity

Figure 4: the capacity gap between the future demand and the current capacities

27/87

Master Thesis- REMENA-Fadi Aljawabra

- By international standards the electricity prices are still quite low, but in the Syrian economic context they are meaningful and set signals about the scarcity of electricity, electricity tariff restructuring is essential in order to subsidise RE initiatives especially in the lunching period till it become more economically feasible.

- Syria's fuel prices were subsidised for many years and the International Monetary Fund (IMF) estimated the total sum of all energy subsidies in 2007 to amount to some 13% of GDP. Moreover the transaction of Syria from fuel exporting country to importing one can be inspiration for the Syrian government to include RE in its plans to pave the road for RE investments by modernised entities and laws.

28/87

Master Thesis- REMENA-Fadi Aljawabra

2. Potentials and Obligations

2.1 Potential of RE sources

Syrian Arab Republic is well endowed with renewable energy resources such as sun and wind and to a lesser extent with biomass and hydro resources. Syria also has significant fossil fuel resources such as oil and gas which currently dominate its energy supply.

2.1.1 Solar Energy

Syria has good solar energy resources like other countries in the Middle East and on the Mediterranean coast. The average global horizontal solar radiant flux in Syria is approximately 5 KWh/m2/day or 1.8 MWh/m2/Year. The average daily radiant flux varies from 4.4 KWh/m2/day in the mountainous areas in the west to 5.2 KWh/m2/day in the desert regions in the Badia. The annual sunshine hours also vary between 2,820 hours to 3,270 h. A report on the institutional framework for renewable energy in 19981 estimated that the total possible contributions from all solar renewable energy resources in 2010 could be 0.5 Mtoe or 2 TWh/Year.

Solar meteorological data has been collected from four meteorological stations at Kharabo, Raqqa, Messelmiyeh and Jabla over a period (1966-1975) and in 1994 the Meteorological Department and Scientific Studies and Research Centre (SSRC) issued the Solar Atlas of Syria. The atlas is based on tabulated data and maps of theoretical values of different components of solar irradiation for twenty two sites in the various regions of Syria.

The European Solar Radiation Atlas also includes global horizontal solar irradiance values from three of the four stations in the solar atlas of Syria, which are Kharabo, Raqqa and Messelmiyeh. The data in the atlas is taken from monitored data from between 1966-1975 and the radiation figures are generally higher than those in the Syrian Solar Atlas.

Data on mean daily irradiance from 15 solar meteorological stations was published in 1997, in the Country Level Study on Renewable Energy Resources.

The figures 5 & 6 shows the locations of the meteorological stations in Syria and the mean annual daily radiation on horizontal surface and 30° incline respectively. 1 Syria-Institutional Framework for Renewable Energy, Hagler Bailly Consulting Ltd, EC DGXV11, Dec

1998

29/87

Master Thesis- REMENA-Fadi Aljawabra

Figure 5: Mean Annual Daily Radiation on Horizontal Surface Wh/m2

Figure 6: Mean Daily Total Radiation on 30° Incline Wh/m21

1 National Renewable Energy Master Plan, 2004, UNDP

30/87

Master Thesis- REMENA-Fadi Aljawabra

The Table 5 presents the deference in the results of the measured radiation on horizontal surface in the available studies (Syrian solar atlas, European Solar atlas, the country level study).

Table 5: Annual Daily Global Horizontal Radiation and at 30° tilt

Station Latitude Longitude

Radiation on Horizontal Surface (Wh/m2)

Syrian Solar Atlas

Radiation on 30° incline

(Wh/m2)

Syrian Solar Atlas

European Solar Atlas

Country Level Study

Idleb 35°56 36°37 4850 NA NA 5249

Palmyra 34°33 38°18 4985 NA 5100 5439

Jableh 35°22 35°57 4750 NA NA 5180

Jarablus 36°49 38°00 4610 NA 4800 5042

Aleppo 36°11 37°13 4792 NA 4900 5160

Hama 35°08 36°43 4926 NA 5100 5303

Homs 34°46 36°42 4886 NA NA 5249

Kharabo 33°30 36°28 5134 5725 5300 5564

Daraa 32°36 36°07 5070 NA NA 5510

Damascus airport

33°26 36°32 5108 NA 5200 5540

Damascus Mezzeh

33°29 36°14 5179 NA 5300 5635

Deir Ezzor 35°17 40°11 4817 NA 5000 5283

Sarghaya 33°49 36°09 4863 NA NA 5187

Hassakah 36°31 40°43 4695 NA 4800 5132

Raqqa 35°55 38°59 4870 5152 4900 5338

Kamishli 37°02 41°13 4572 NA NA 5042

Lattakia 35°33 35°47 4511 NA 4600 4884

Messelmiyeh 36°19 37°14 4696 5026 4800 5114

Ein Elkroum 35°21 36°16 4617 NA NA 4873

31/87

Master Thesis- REMENA-Fadi Aljawabra

Station Latitude Longitude

Radiation on Horizontal Surface Syrian Solar (Wh/m2) Atlas

Radiation on 30° incline

(Wh/m2)

Syrian European Country Solar Atlas Solar Atlas Level Study

El Jayyed 35°33 36°19 4690 NA 4800 5072

Khafseh 36°13 38°02 4802 NA NA ` 5244

Kraem 35°23 36°20 4742 NA NA 5333

The analysing of the Syrian solar resources shows:

- Syria has tremendous solar energy resources which are available in a largely uniform manner across the geographical spread of the country, based on the Syrian atlas the global radiation at 30° tilt is approximately 115 KWh/m²

- The significant availability of solar energy resources for a long period during the year

- Available data resources through the solar atlas of Syria, the European Solar Atlas and the Country level study which provide a good and acceptable summary of solar resources in the country

2.1.2 Wind Energy

Wind monitoring stations have been established around the country, mainly towards the major population centres in the western and southern regions. These monitoring stations have collected between 5 and 12 years’ data at each site, during the period 1965-1993. The data so collected has resulted in developing a Wind Energy Atlas for the country which was published in 1998 through co-operation with Risø National Labs of Denmark. Syrian engineers were also trained on wind resource assessments and wind atlas methodology in the early 1990s.

The Syrian Wind energy atlas is a comprehensive document and presents for each of the sites the measured wind speed data, Weibull parameters for each 30° sector, and a table summarising the calculated mean wind speed (m/s) and power density (W/m2). The wind speeds and wind power density are given at heights of 10 m, 25 m, 50 m, 100 m, and 200 m for four roughness classes. Wind roses and wind speed duration curves are also available for most of the sites.

A wind map of Syria is presented in Figure 7. It illustrates strong wind resources in the central, southern and hilly coastal areas of the country. Some of the attractive areas

32/87

Master Thesis- REMENA-Fadi Aljawabra

include Qattina, Mesiaf, Qunaitera and Palmyra. The Wind Atlas is thoroughly prepared and represents an excellent data source from which a wind energy programme can be planned.

Figure 7: Wind Map of Syria (Source: Meteorological Department, Syria)1 The theoretical technical potential for wind power developments in Syria was calculated based on the data available from the wind energy atlas and based on some assumptions¹:

- Only locations with a minimum wind power density of 250 W/m2 at 50m height was considered suitable for the wind energy generation;

- Air density is taken as 1.184 kg/m2, considering an altitude of sea level and an ambient temperature of 25ºC;

- The orographic features and their effect on wind speeds was ignored;

- The technical specifications of two commercially available wind turbines of 100 kW and 1 MW were used for calculations ;

- A wind farm array spacing of 10 d x 5 d was used for the calculations;

- It will be feasible to develop wind farms in at least 5% of the suitable land area.

Based on the calculations, the technical potential for wind energy developments in Syria is estimated to be 85,000 MW¹.

1 National Renewable Energy Master Plan, 2004, UNDP

33/87

Master Thesis- REMENA-Fadi Aljawabra

Figure 8: Wind Energy Potential in Syria¹

The assessment of the wind energy resources shows:

- Syria has good wind energy resources, which is estimated at 40,000 MW- 85,000 MW1. Several of the potential locations are close to the major population centres.

- However, the data currently available requires detailed professional analysis with corrections for topography, infrastructure for access to the sites and grid infrastructure for evacuation of generated power. This should result in prioritises list of sites for wind farm development.

- It is not considered necessary to undertake any major wind resource assessments except for normal monitoring of energy meteorological data.

2.1.3 Hydro Power

Hydropower is the only significant renewable energy contribution to Syria’s energy supply at the current time, providing between 2000 GWh and 4000 GWh per year, depending on precipitation levels.

1 National Renewable Energy Master Plan, 2004, UNDP

34/87

Master Thesis- REMENA-Fadi Aljawabra

The table 6 presents the installed hydropower plants in Syria which are the Al-Thawra Dam (880 MW) and newly commissioned Teshreen Dam (630 MW), both on the Euphrates, provide around 90 % of the hydro-electric supply. The Al-Baath Dam on the Euphrates (75 MW) and 5 other small hydro plants make up the total of 1620 MW .

Table 6: Operating Hydropower Plants in Syria1

Basin / River Name / Location Installed Capacity (MW)

Typical Output (GWh/year)

Euphrates Al-Thawra 880 2,000 Al-Baath 75 300 Teshreen 630 1,300

Barada Wadi-Barada 8 24 Orontes Al Rastan 8 12

Shaizer 7 4 Afrin 17th of April 10 40 Al-Khabour Hassakeh-West 1.2 3.3 Total 1,619.2 3,683.3

Because priority is given to drinking water supply and irrigation over electricity supply, these growing demands are likely to reduce the potential for existing and future developments. Development on the Tigris and Yarmuk rivers depends on agreement with the respective bordering countries (Turkey and Jordan).

1 Small Hydro Power in the Syrian Arab Republic, Sufian Al-Alao, UNDP Sustainable Energy in the Arab

States RAB/96/005, July 1998

35/87

Master Thesis- REMENA-Fadi Aljawabra

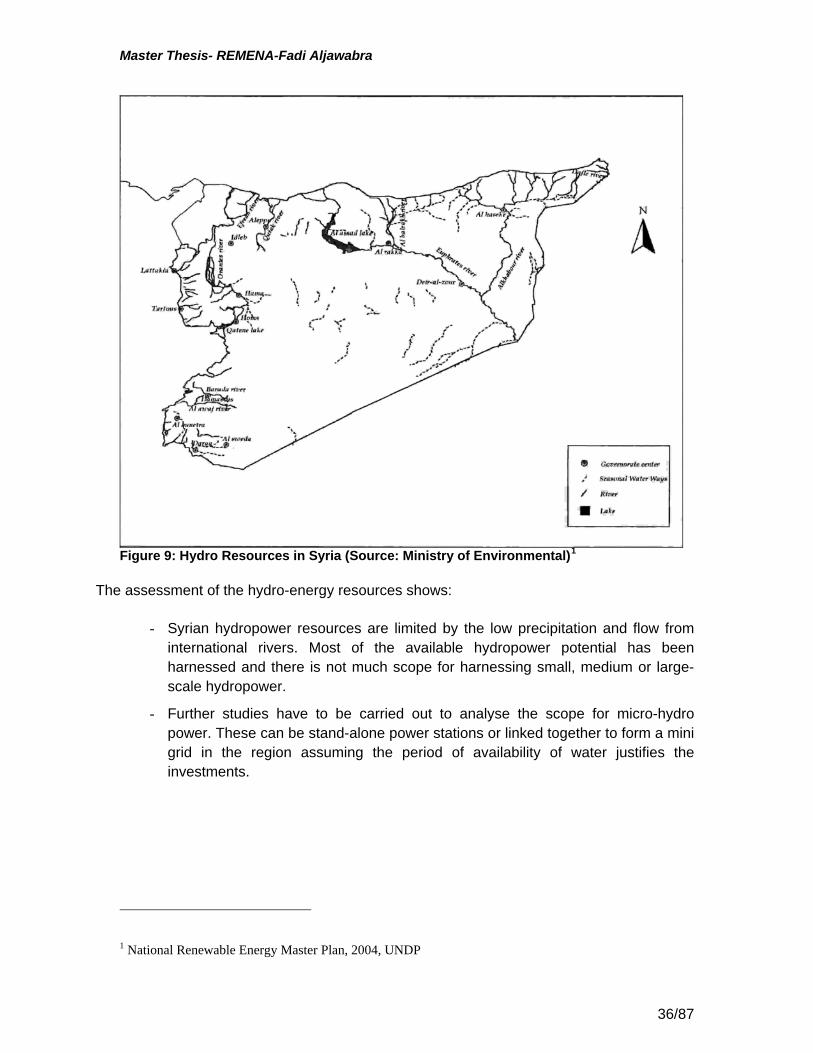

Figure 9: Hydro Resources in Syria (Source: Ministry of Environmental)1

The assessment of the hydro-energy resources shows:

- Syrian hydropower resources are limited by the low precipitation and flow from international rivers. Most of the available hydropower potential has been harnessed and there is not much scope for harnessing small, medium or large-scale hydropower.

- Further studies have to be carried out to analyse the scope for micro-hydro power. These can be stand-alone power stations or linked together to form a mini grid in the region assuming the period of availability of water justifies the investments.

1 National Renewable Energy Master Plan, 2004, UNDP

36/87

Master Thesis- REMENA-Fadi Aljawabra

2.1.4 Biomass

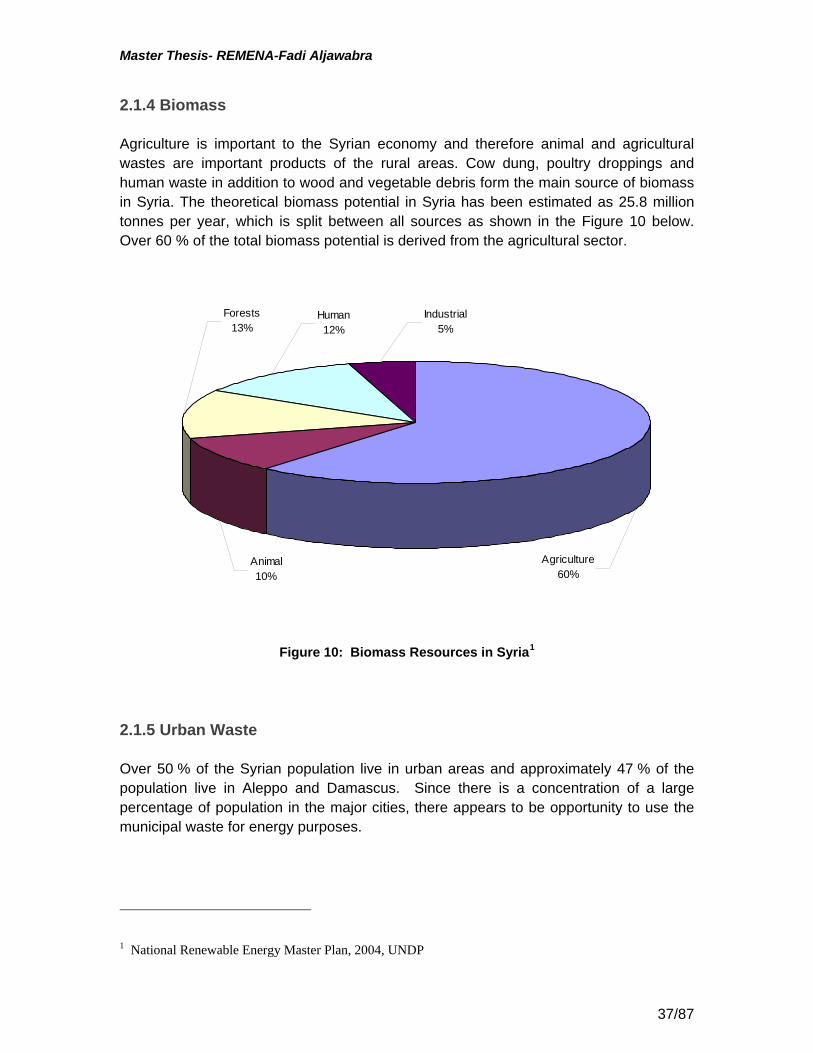

Agriculture is important to the Syrian economy and therefore animal and agricultural wastes are important products of the rural areas. Cow dung, poultry droppings and human waste in addition to wood and vegetable debris form the main source of biomass in Syria. The theoretical biomass potential in Syria has been estimated as 25.8 million tonnes per year, which is split between all sources as shown in the Figure 10 below. Over 60 % of the total biomass potential is derived from the agricultural sector.

Animal10%

Forests13%

Human12%

Industrial5%

Agriculture60%

Figure 10: Biomass Resources in Syria1

2.1.5 Urban Waste

Over 50 % of the Syrian population live in urban areas and approximately 47 % of the population live in Aleppo and Damascus. Since there is a concentration of a large percentage of population in the major cities, there appears to be opportunity to use the municipal waste for energy purposes.

1 National Renewable Energy Master Plan, 2004, UNDP

37/87

Master Thesis- REMENA-Fadi Aljawabra

2.1.6. Geothermal Energy

The geothermal energy potential1 in Syria has been evaluated based on mathematical models and a number of locations have been identified as offering scope for power generation.

Table7: Geothermal Energy Potential

Name of Well Location Surface Temperature°C

Water Discharge m3/hour

Aldabiat – Sukneh

Aboureah – Gareten

Almauh Swamp

Alyadude

Raas Alain

Alsfera

Palmyra central region

Palmyra central region

Palmyra central region

Daraa – South region

North east region

Aleppo – North region

61

50

45

44

40

38

42

dry air

320

7.72

31.3

980

The assessment of the geothermal energy resources shows:

- There is a high theoretical potential of the geothermal energy in some locations in Syria like in Palmayra, however a feasibility study should be prepared.

- The geothermal potential itself need to be investigated thoroughly to identify regions with prospects and to verify the initial findings. A geothermal resource assessment study is needed.

2.2 International Conventions and Agreements

2.2.1 Environmental agreements:

The Syrian Government considers the environment to be an integral component of all sectoral activities, and will work to achieve an integrated rural development that includes the protection and improvement of use of natural resources. Environmental issues being integrated into major development plans are the responsibility of the Ministry of state for Environmental Affairs, and other relevant ministries that form the Environment Protection Council. In 2002 the Environmental Law (decree 50/2002) has been issued, and forms

1 (Aug-2000), Renewable Energy Country Profile for the Syrian Arab Republic, ESCWA.

38/87

Master Thesis- REMENA-Fadi Aljawabra

the basis for environmental management in Syria. The Government of Syria has ratified the UNFCCC in April 1996 and ratified the Kyoto protocol (Presidential decree 73 dated 4/9/2005).

Syria has nominated the General Commission for Environmental Affairs (GCEA) as the national authority for the Clean Development Mechanism (CDM)-Designated National Authority (DNA).

The main tasks of DNA are to provide approval to the project participants and in case of a host party, confirm, through written approval, that the CDM project activity assists it in achieving sustainable development. Furthermore, GCEA through the National Climate Change Committee is the official focal point for climate change activities in Syria, including CDM projects.

2.2.2 The Association Agreement between Syria and the EU

The Association Agreement between Syria and the EU has been negotiated, but it is not yet in force. It will require Syria to adapt to EU energy market standards (level play field) which means that the Syrian energy market will need further liberalisation and institutional change in accordance with the respective EU directives.

Under the heading "Policy and Legal Reforms" inter alia the following key points are listed1:

- Amend legislations allowing the private sector to produce electricity - Restructuring the electricity sector according to the studies prepared by Euro-

Med Association Area. - Set out pricing and incentive policies for rationing consumption, particularly in

residential application by using energy saving bulbs and to introduce rationed uses in commercial and services sectors such as using automated lighting and appliances that have high efficiency and to monitor manufacturers of electric appliances.

- Adopt regulations that allow Syrian private sector to participate in oil and gas production service operations, transport and final marketing.

- Adopt flexible and transparent financial conditions regarding contracting, domestic sales and foreign marketing.

- Establish an independent governing authority for the energy sector that will supervise contracts, transparent competition, domestic and international marketing and economic pricing of energy carriers.

- Establish higher energy commission that prepares the national energy strategy and branch policies for various sectors, by expanding the functions of the

1 The Association Agreement between Syria and the EU

39/87

Master Thesis- REMENA-Fadi Aljawabra

National Centre for Energy Research currently under Ministry of Electricity, to include the oil and gas sectors.

2.3 National Programmes

2.3.1 The 10th five year plan 2006-2011

There is no official document that states the national policy of renewable energy of the Syrian Government. The 10th five year plan 2006-2011 stated long term objectives to be achieved by 2015:

1. Improve electricity generation efficiency and reduce all types of loses as high priority.

2. Provide electricity to cover expected growth in loads, by doubling combined capacity from presently 7079 MW to 12,000 MW in 2015.

3. Best use of renewable energies, by fully utilising hydro-electricity and benefiting from Syria's climate to use new and renewable energies (solar, wind and biomass).

4. Maximum benefit from available quantities of gas to generate electricity. 5. Reach higher dependability in generating and distributing electricity. 6. Restructure electricity sector according to Syrian European Association

Agreement, intended to be signed soon. Issue electricity law which will allow competition and attract investments in accordance with regional market for energy and electricity by 2015.

2.3.2 The 11th five year plan 2011-2016

In contrast to previous 5-year plan the 11th 5-year plan 2011-2016 of the Ministry of Electricity put a specific target of RE plants should be built in the plan duration. Ministry of Electricity is aiming to increase its capacity from 7500 MW to 12000 MW by the end of the 11th 5 year plan 2011-2016.

The plan included strategies to reach the national objectives, the strategy manly focus on wind and photovoltaic energy plant in the supply side, however the plan focus also on the energy efficiency technologies in the demand side in purpose to reduce the consumption.

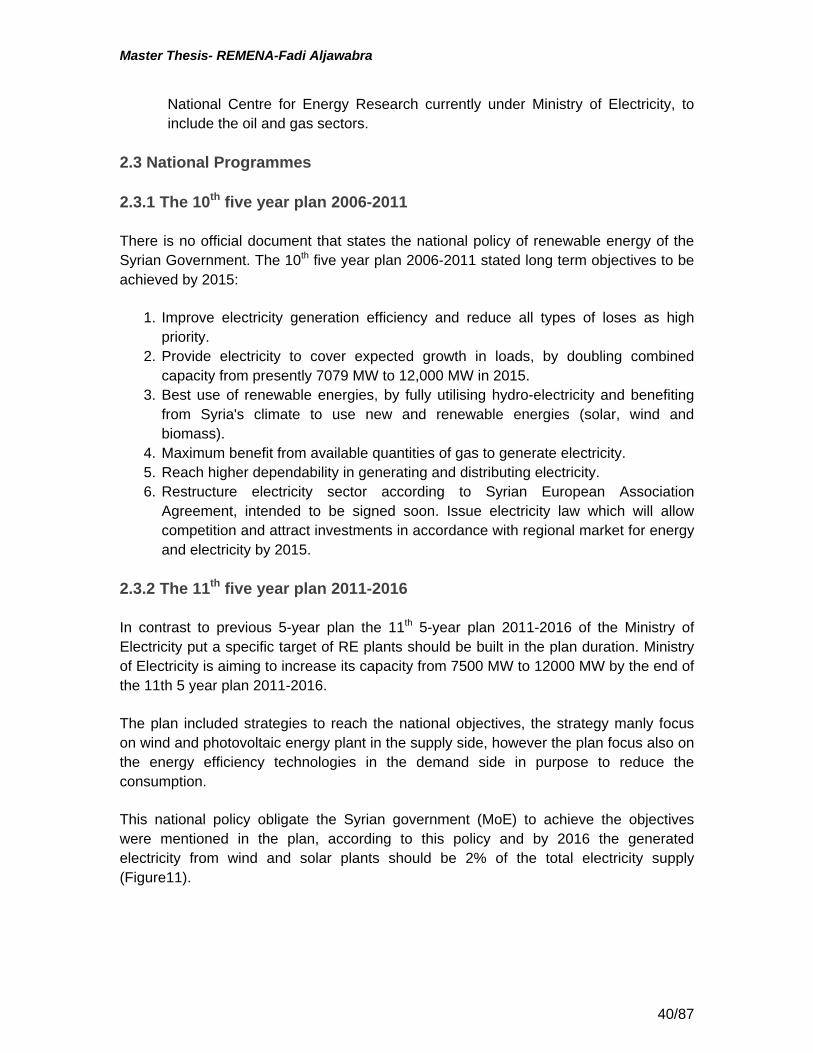

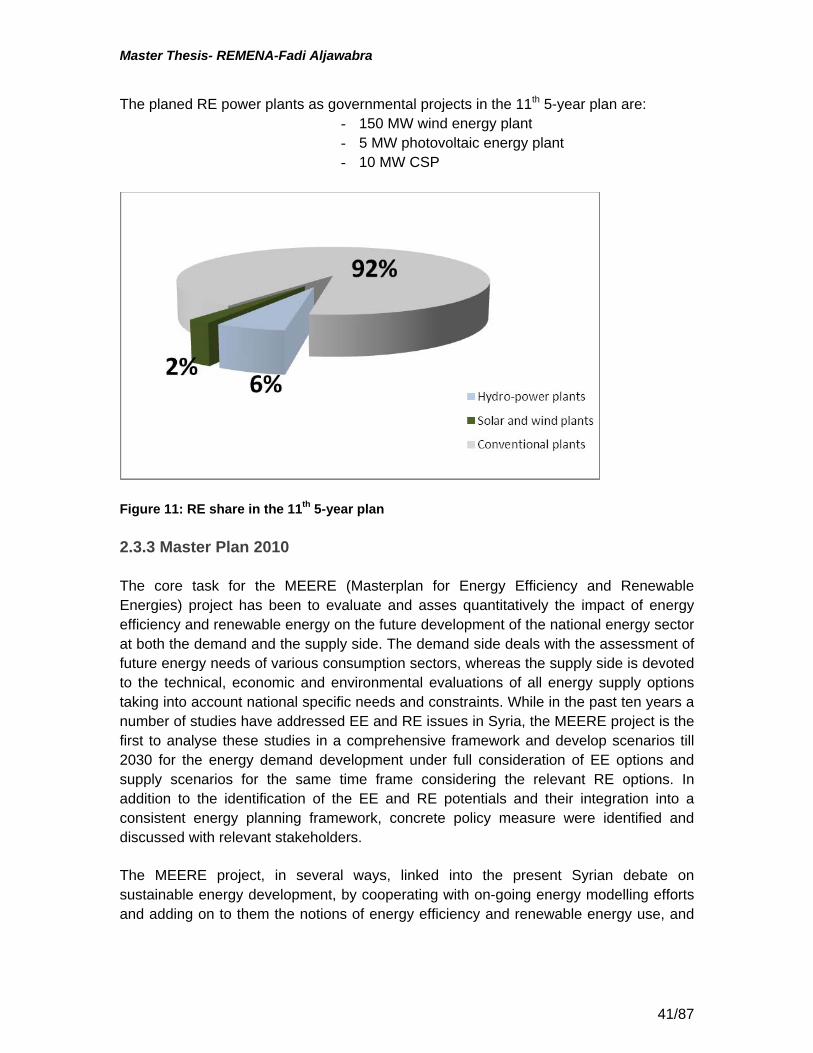

This national policy obligate the Syrian government (MoE) to achieve the objectives were mentioned in the plan, according to this policy and by 2016 the generated electricity from wind and solar plants should be 2% of the total electricity supply (Figure11).

40/87

Master Thesis- REMENA-Fadi Aljawabra

The planed RE power plants as governmental projects in the 11th 5-year plan are: - 150 MW wind energy plant - 5 MW photovoltaic energy plant - 10 MW CSP

Figure 11: RE share in the 11th 5-year plan

2.3.3 Master Plan 2010

The core task for the MEERE (Masterplan for Energy Efficiency and Renewable Energies) project has been to evaluate and asses quantitatively the impact of energy efficiency and renewable energy on the future development of the national energy sector at both the demand and the supply side. The demand side deals with the assessment of future energy needs of various consumption sectors, whereas the supply side is devoted to the technical, economic and environmental evaluations of all energy supply options taking into account national specific needs and constraints. While in the past ten years a number of studies have addressed EE and RE issues in Syria, the MEERE project is the first to analyse these studies in a comprehensive framework and develop scenarios till 2030 for the energy demand development under full consideration of EE options and supply scenarios for the same time frame considering the relevant RE options. In addition to the identification of the EE and RE potentials and their integration into a consistent energy planning framework, concrete policy measure were identified and discussed with relevant stakeholders.

The MEERE project, in several ways, linked into the present Syrian debate on sustainable energy development, by cooperating with on-going energy modelling efforts and adding on to them the notions of energy efficiency and renewable energy use, and

41/87

Master Thesis- REMENA-Fadi Aljawabra

in addition by bringing together several times the national stakeholders of EE and RE issues to discuss options for Syria.

The MEERE project made use of and contributed to on-going national energy modelling efforts using MAED (Model for Analysis of Energy and Electricity Demand) and the optimisation model MESSAGE (Model for Energy Supply Strategy Alternatives and their General Environmental Impacts). They have been applied for the projection of future Syrian final energy demand and the formulation of optimal supply strategies for different scenarios.

2.3.3.1 Reference supply (RS) and energy saving (ES) scenarios: