Master Class Session Hedging Bullion Price Exposure using ... Group - Options... · Master Class...

21

Anindya A. Boral Director – Metals Products Master Class Session Hedging Bullion Price Exposure using Options 9th India International Gold Convention – Hyderabad, India August 24, 2012

Transcript of Master Class Session Hedging Bullion Price Exposure using ... Group - Options... · Master Class...

Anindya A. BoralDirector – Metals Products

Master Class Session

Hedging Bullion Price Exposure using Options

9th India International Gold Convention – Hyderabad, IndiaAugust 24, 2012

2Copyright © 2012 CME Group Inc. All rights reserved.

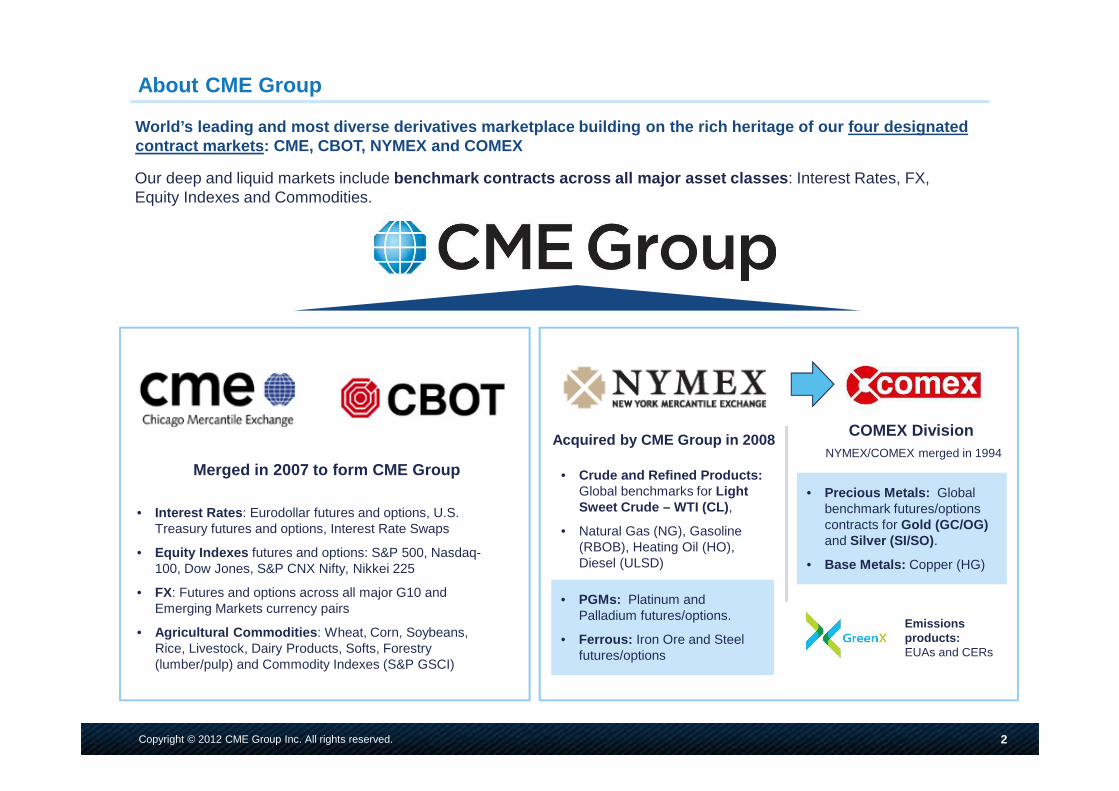

About CME Group

Merged in 2007 to form CME Group

World’s leading and most diverse derivatives market place building on the rich heritage of our four des ignated contract markets: CME, CBOT, NYMEX and COMEX

Acquired by CME Group in 2008NYMEX/COMEX merged in 1994

COMEX Division

Our deep and liquid markets include benchmark contracts across all major asset classes : Interest Rates, FX, Equity Indexes and Commodities.

Emissions products: EUAs and CERs

• Interest Rates : Eurodollar futures and options, U.S. Treasury futures and options, Interest Rate Swaps

• Equity Indexes futures and options: S&P 500, Nasdaq-100, Dow Jones, S&P CNX Nifty, Nikkei 225

• FX: Futures and options across all major G10 and Emerging Markets currency pairs

• Agricultural Commodities : Wheat, Corn, Soybeans, Rice, Livestock, Dairy Products, Softs, Forestry (lumber/pulp) and Commodity Indexes (S&P GSCI)

• Crude and Refined Products: Global benchmarks for Light Sweet Crude – WTI (CL) ,

• Natural Gas (NG), Gasoline (RBOB), Heating Oil (HO), Diesel (ULSD)

• Precious Metals: Global benchmark futures/options contracts for Gold (GC/OG)and Silver (SI/SO) .

• Base Metals: Copper (HG)

• PGMs: Platinum and Palladium futures/options.

• Ferrous: Iron Ore and Steel futures/options

3Copyright © 2012 CME Group Inc. All rights reserved.

PART 1QUICK INTRODUCTION TO OPTIONS

4Copyright © 2012 CME Group Inc. All rights reserved.

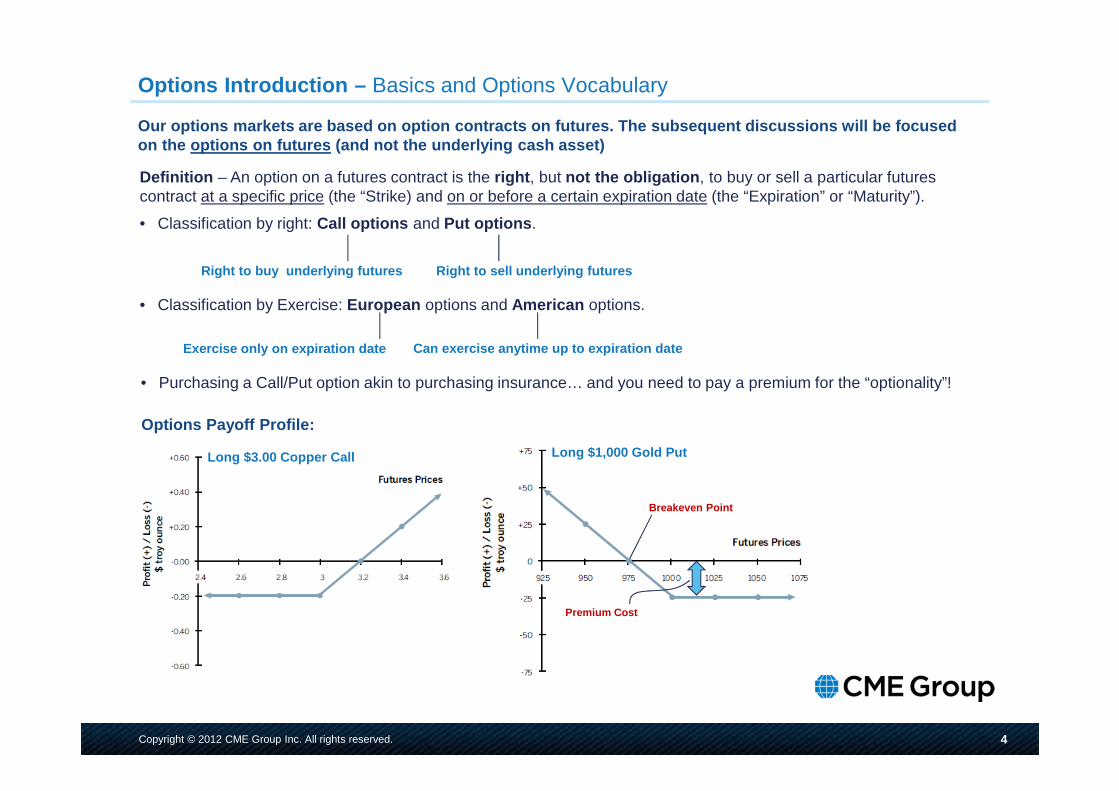

Options Introduction – Basics and Options Vocabulary

Definition – An option on a futures contract is the right , but not the obligation , to buy or sell a particular futures contract at a specific price (the “Strike) and on or before a certain expiration date (the “Expiration” or “Maturity”).

• Classification by right: Call options and Put options .

• Classification by Exercise: European options and American options.

Our options markets are based on option contracts o n futures. The subsequent discussions will be focus ed on the options on futures (and not the underlying ca sh asset)

Right to buy underlying futures Right to sell under lying futures

Premium Cost

• Purchasing a Call/Put option akin to purchasing insurance… and you need to pay a premium for the “optionality”!

Exercise only on expiration date Can exercise anytime up to expiration date

Breakeven Point

Options Payoff Profile:

Long $1,000 Gold PutLong $3.00 Copper Call

5Copyright © 2012 CME Group Inc. All rights reserved.

Option Prices – Introduction to Volatility

Option Premium = Time Value + Intrinsic Valu e

Based on difference between current futures prices and the option strike. Only for “in-the-money” options.

Depends on:

• Time remaining to Expiration

• “Moneyness” of the option (i.e., how far is the futures prices from the Strike?)

• Volatility of the underlying futures prices

An option’s premium can be made up of one or both o f two components:

Volatility is a function of price movement…

• Measure of uncertainty of asset returns / degree of price fluctuation

• When prices are rising or falling substantially, volatility is said to be high. When a futures contract shows little price movement, volatility is said to be low.

• High volatility generally causes options premiums to increase – sometimes very dramatically. Lower volatility environments generally cause options premiums to decline.

• Relatively easy to calculate “historic” volatility based on the time-series futures price data.Futures Price Daily Return

Technically speaking, Volatility is the standard deviation of daily returns…expressed in annualised terms.

σσσσ

Option value is higher for >>> longer time to expiry, futures price closer to Strike, and Higher Volatility (Vol)

Moneyness terms >>> At-the-money (ATM), In-the-money (ITM), Out-of-the-Money (OTM)

6Copyright © 2012 CME Group Inc. All rights reserved.

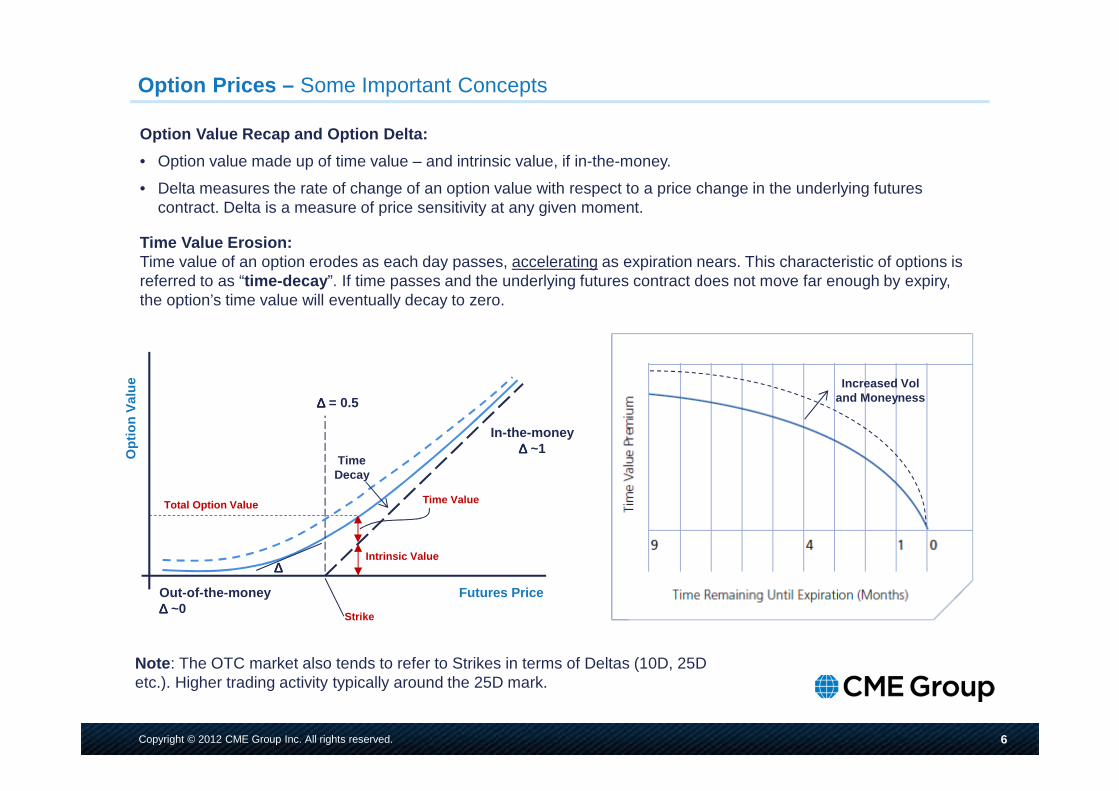

Option Prices – Some Important Concepts

Note : The OTC market also tends to refer to Strikes in terms of Deltas (10D, 25D etc.). Higher trading activity typically around the 25D mark.

Option Value Recap and Option Delta:

• Option value made up of time value – and intrinsic value, if in-the-money.

• Delta measures the rate of change of an option value with respect to a price change in the underlying futures contract. Delta is a measure of price sensitivity at any given moment.

Time Value Erosion:Time value of an option erodes as each day passes, accelerating as expiration nears. This characteristic of options is referred to as “time-decay ”. If time passes and the underlying futures contract does not move far enough by expiry, the option’s time value will eventually decay to zero.

Increased Voland Moneyness

Intrinsic Value

Time ValueTotal Option Value

Futures Price

Opt

ion

Val

ue

Strike

In-the-money∆∆∆∆ ~1

Out-of-the-money∆∆∆∆ ~0

∆∆∆∆ = 0.5

∆∆∆∆

Time Decay

7Copyright © 2012 CME Group Inc. All rights reserved.

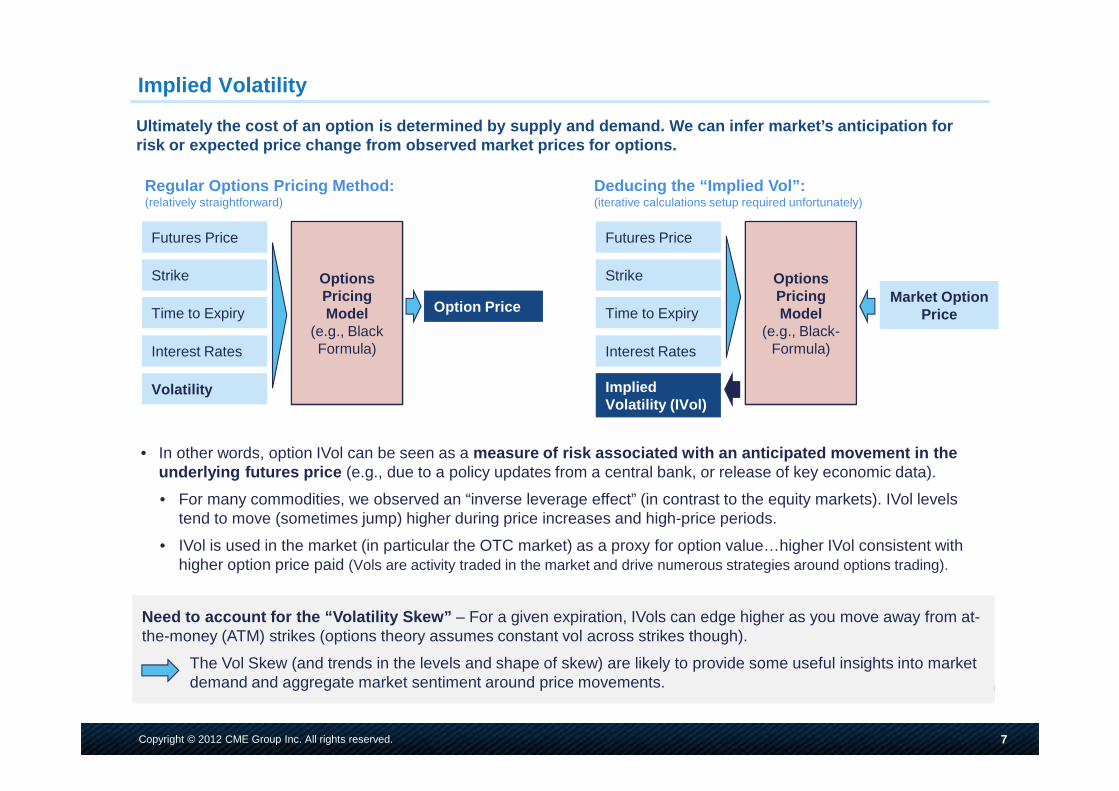

Implied Volatility

Futures Price

Strike

Time to Expiry

Interest Rates

Volatility

Options Pricing Model

(e.g., Black Formula)

Option Price

Futures Price

Strike

Time to Expiry

Implied Volatility (IVol)

Interest Rates

Options Pricing Model

(e.g., Black-Formula)

Market Option Price

Regular Options Pricing Method:(relatively straightforward)

Deducing the “Implied Vol”:(iterative calculations setup required unfortunately)

Ultimately the cost of an option is determined by s upply and demand. We can infer market’s anticipatio n for risk or expected price change from observed market prices for options.

• In other words, option IVol can be seen as a measure of risk associated with an anticipated movement in the underlying futures price (e.g., due to a policy updates from a central bank, or release of key economic data).

• For many commodities, we observed an “inverse leverage effect” (in contrast to the equity markets). IVol levels tend to move (sometimes jump) higher during price increases and high-price periods.

• IVol is used in the market (in particular the OTC market) as a proxy for option value…higher IVol consistent with higher option price paid (Vols are activity traded in the market and drive numerous strategies around options trading).

Need to account for the “Volatility Skew” – For a given expiration, IVols can edge higher as you move away from at-the-money (ATM) strikes (options theory assumes constant vol across strikes though).

The Vol Skew (and trends in the levels and shape of skew) are likely to provide some useful insights into market demand and aggregate market sentiment around price movements.

8Copyright © 2012 CME Group Inc. All rights reserved.

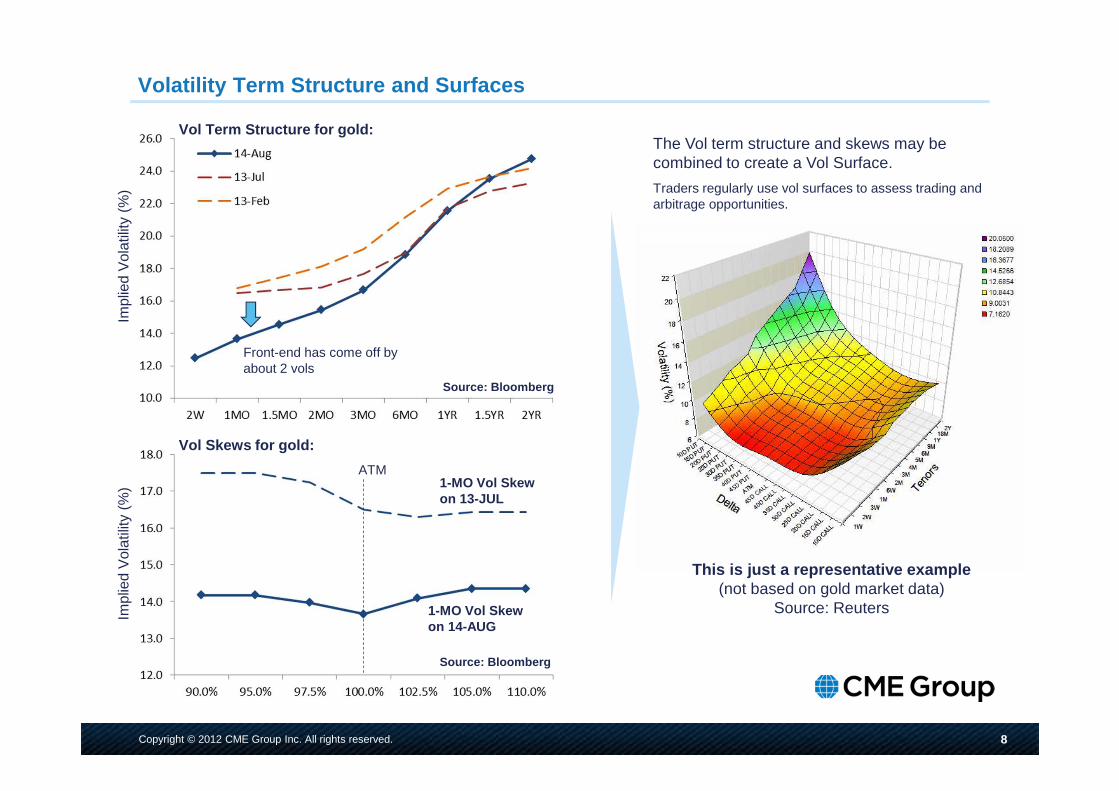

Volatility Term Structure and Surfaces

The Vol term structure and skews may be combined to create a Vol Surface.

Traders regularly use vol surfaces to assess trading and arbitrage opportunities.

This is just a representative example(not based on gold market data)

Source: Reuters

Source: Bloomberg

Front-end has come off by about 2 vols

Impl

ied

Vol

atili

ty (

%)

Impl

ied

Vol

atili

ty (

%)

ATM1-MO Vol Skew on 13-JUL

1-MO Vol Skew on 14-AUG

Source: Bloomberg

Vol Term Structure for gold:

Vol Skews for gold:

9Copyright © 2012 CME Group Inc. All rights reserved.

Tracking Volatility in the Gold Markets

From the CME Risk Management Handbook – “IVol is forward-looking assessment of underlying futures price risk, whereas HVol is backward-looking assessment of where price risk has been.”

Key Takeaway: Market’s assessment of volatility can shift quite a bit.

Source: Bloomberg

U.S. Fed QE2 ($600bn) ends; U.S. credit downgrade in Aug; deepening Eurozone worries and signs of a severe economic slowdown. Gold’s emergence as a safe-haven asset that drives front-month gold futures prices toward the $1,900 mark.

Gold futures front-month prices ($/oz)

30-day Historic Vol

1-Mo ATM Implied Vol

3-Mo ATM Implied Vol

Eurozone worries re-emerge; signs of Asian slowdown; disappointing U.S. economic indicators. “Risk-off” environment takes hold.

Eurozone worries persist; Italian debt concerns emerge

10Copyright © 2012 CME Group Inc. All rights reserved.

PART 2COMEX OPTIONS MARKETS AND STRATEGIES

11Copyright © 2012 CME Group Inc. All rights reserved.

COMEX Options Markets – Volumes and Open Interest

Options on metals futures products provide the liquidity, flexibility and market depth needed to achieve market participants trading objectives…

…from the simple to the most sophisticated of trading strategies.

COMEX has one of the most liquid precious metals futures and options markets in the world.

Option contracts based on our flagship futures contracts that are global benchmarks.

• 2012 Daily volumes:

• Gold Options: 40,000 contractsGold Futures: 190,000 contracts

• Silver Options: 7,000 contractsSilver Futures: 55,000 contracts

• 2012 Open Interest:

• Gold Options: 1.2 million contractsGold Futures: 425,000 contracts

• Silver Options: 190,000 contractsSilver Futures: 115,000 contracts

12Copyright © 2012 CME Group Inc. All rights reserved.

COMEX Options Markets – Electronic Trading Activity

We have seen a remarkable growth in our options mar kets driven by an increase in electronic trading vo lumes via our Globex platform.

• Gold option volumes grew almost 4-fold over the past 5 years to average around 40,000 contracts changing hands daily in first half of 2012.

• Almost 45% of our gold option volumes come via our Globex electronic trading platform.

• It is noteworthy that electronic trading activity in gold options was virtually non-existent back in early-2007.

• However, the open outcry and off-exchange (ClearPort) venues still important for options -especially when it comes to executing complex option strategies.

13Copyright © 2012 CME Group Inc. All rights reserved.

COMEX Options Products – Contract Specifications

Short-Term Gold Options

Our ST Gold Options are physically-settled options with expiries over the next 5 business days. These are European-style options with automatic exercise on expiration.

14Copyright © 2012 CME Group Inc. All rights reserved.

Margins

• An option buyer must only put up the amount of the premium, in full, at the time of the trade. However, because option selling involves more risk, an option seller or writer will be required to post performance bond.

• Once an options position is exercised into a futures position, performance bond is required, just as for any other futures position.

COMEX Options Products – Some Important Information

Gold Option Specs Recap

• One standard monthly option contract (OG) delivers into one futures contract.

• One Gold futures contract (GC) constitutes a contract for delivery of 100 troy oz. of Gold to an Exchange-approveddepository at a specific date in the future.

• One options contract would allow the buyer or assign the seller to take or give possession of one corresponding underlying futures contract the specific date of each contract.

Options Expiration Procedure / monthly options

Settlement is based on the COMEX close at 1:30 p.m. Eastern Time (ET). Abandonments and assignments must be submitted to the Exchange by 4:30 p.m. ET.

Option Buyers exercise and sellers get assigned.

Notice of exercise and abandonments are generally given by 8:00 p.m. ET.

Cycle Months

Gold options settle into underlying futures contracts on a cycle-month schedule.

For example, a November options contract exercises into a December futures contract. Since the December futures price is generally different from the November futures price, the option must be valued with the December (Cycle Month) price in mind.

15Copyright © 2012 CME Group Inc. All rights reserved.

Choose Venue

Choose Underlying futures

Choose Options Expiration

Tools Available on CME Metals Website – Delayed Quotes

16Copyright © 2012 CME Group Inc. All rights reserved.

Tools Available on CME Metals Website – Open Interest Profile

Our Metals Options Open Interest Profile provides p owerful insights into open interest patterns for ou r core option contracts.

Open Interest Profile for Dec-12 Gold Option Contra ct (OG) • Why is this valuable? Options incorporate Calls/Puts, variety of contract months, and a wide range of Strikes.

• Market participants can assess market sentiment and liquidity pools in the option markets.

• Can also help market participants draw inferences around likely support and resistance levels.

• Can also help identify “pin risk” potential around certain strikes.

$1800

$2200

$2000

$2300

$1400

$1200

GCZ2 Dec-12 GC futures16- Aug Settle: $1619.2

$1500

17Copyright © 2012 CME Group Inc. All rights reserved.

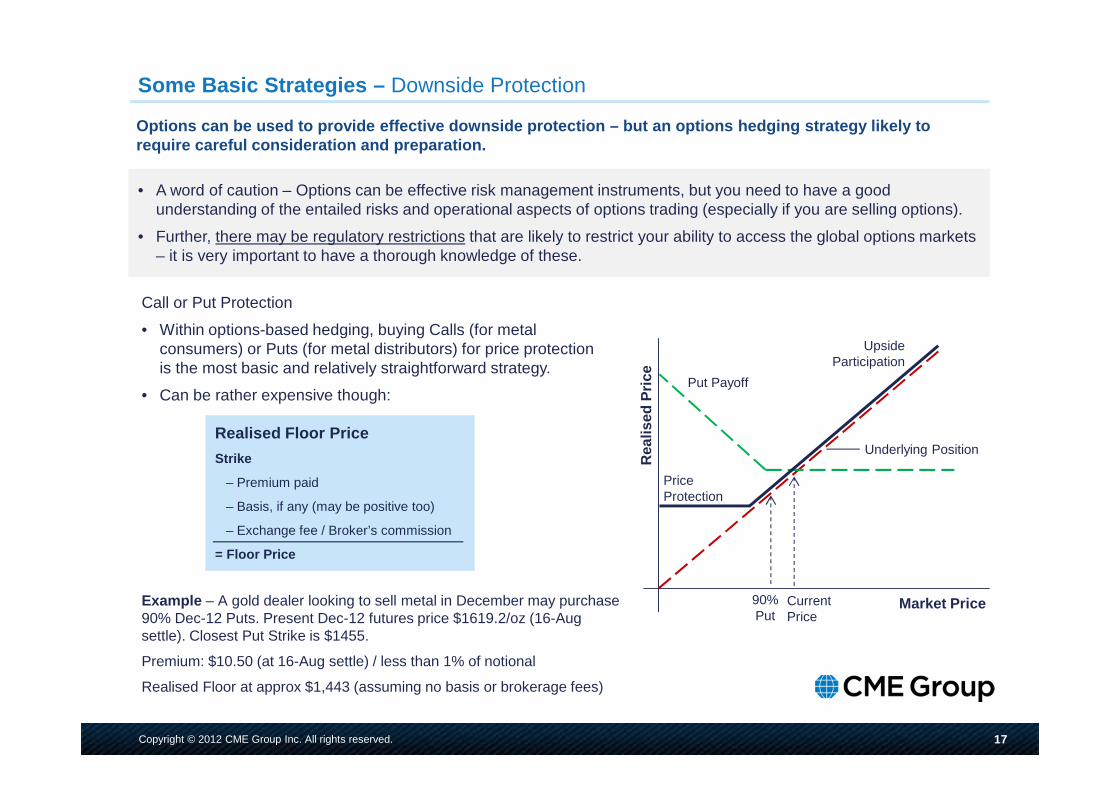

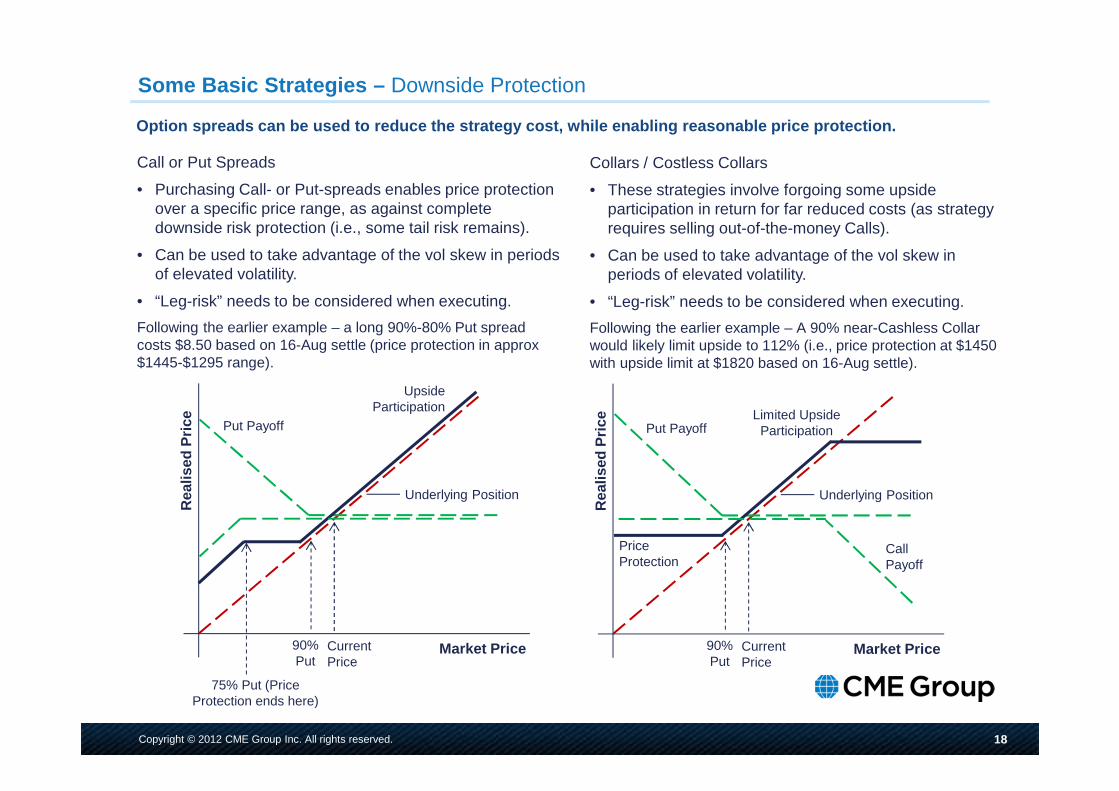

Some Basic Strategies – Downside Protection

Options can be used to provide effective downside p rotection – but an options hedging strategy likely t o require careful consideration and preparation.

• A word of caution – Options can be effective risk management instruments, but you need to have a good understanding of the entailed risks and operational aspects of options trading (especially if you are selling options).

• Further, there may be regulatory restrictions that are likely to restrict your ability to access the global options markets – it is very important to have a thorough knowledge of these.

90% Put

Current Price

Upside Participation

Market Price

Rea

lised

Pric

e

Price Protection

Put Payoff

Underlying PositionRealised Floor Price

Strike

– Premium paid

– Basis, if any (may be positive too)

– Exchange fee / Broker’s commission

= Floor Price

Call or Put Protection

• Within options-based hedging, buying Calls (for metal consumers) or Puts (for metal distributors) for price protection is the most basic and relatively straightforward strategy.

• Can be rather expensive though:

Example – A gold dealer looking to sell metal in December may purchase 90% Dec-12 Puts. Present Dec-12 futures price $1619.2/oz (16-Aug settle). Closest Put Strike is $1455.

Premium: $10.50 (at 16-Aug settle) / less than 1% of notional

Realised Floor at approx $1,443 (assuming no basis or brokerage fees)

18Copyright © 2012 CME Group Inc. All rights reserved.

Some Basic Strategies – Downside Protection

90% Put

Current Price

Upside Participation

Market Price

Rea

lised

Pric

e Put Payoff

Underlying Position

75% Put (Price Protection ends here)

90% Put

Current Price

Limited Upside Participation

Market Price

Rea

lised

Pric

e

Price Protection

Put Payoff

Underlying Position

Call Payoff

Option spreads can be used to reduce the strategy c ost, while enabling reasonable price protection.

Call or Put Spreads

• Purchasing Call- or Put-spreads enables price protection over a specific price range, as against complete downside risk protection (i.e., some tail risk remains).

• Can be used to take advantage of the vol skew in periods of elevated volatility.

• “Leg-risk” needs to be considered when executing.

Following the earlier example – a long 90%-80% Put spread costs $8.50 based on 16-Aug settle (price protection in approx$1445-$1295 range).

Collars / Costless Collars

• These strategies involve forgoing some upside participation in return for far reduced costs (as strategy requires selling out-of-the-money Calls).

• Can be used to take advantage of the vol skew in periods of elevated volatility.

• “Leg-risk” needs to be considered when executing.

Following the earlier example – A 90% near-Cashless Collar would likely limit upside to 112% (i.e., price protection at $1450 with upside limit at $1820 based on 16-Aug settle).

19Copyright © 2012 CME Group Inc. All rights reserved.

Accessing Information

CME Group Metals Page

http://www.cmegroup.com/trading/metals/

Click on OPT to see options quotes

20Copyright © 2012 CME Group Inc. All rights reserved.

Contact Information

Thank You!

Some Useful Links:

Fee Schedule – http://www.cmegroup.com/company/clearing-fees/index.html

Open Interest Profile – http://www.cmegroup.com/trading/metals/options-open-interest/main.html

Margins – http://www.cmegroup.com/clearing/margins/

Options Exercise Months – http://www.cmegroup.com/trading/metals/files/PM236_Metals_Option_Exercise.pdf

Brokers Directory – http://www.cmegroup.com/tools-information/find-a-broker/broker-directory-as.html

If you require further details regarding our markets, please do not hesitate to get in touch. We very much look forward to your feedback on our products/services and your questions.

Contact Details:

Anindya A. Boral (LON) / Miguel Vias (NY)

E-mails: [email protected]; Miguel.Vias@cm egroup.com

Desk Tel: +44 20 3379 3738 (Anindya); +1 212 299 23 58 (Miguel)

Mobile: +44 7912 581 181 (Anindya)

21Copyright © 2012 CME Group Inc. All rights reserved.

Important Information

DISCLAIMER

Futures trading is not suitable for all investors, and involves the risk of loss. Futures are a leveraged investment, and because only a percentage of a contract’s value is required to trade, it is possible to lose more than the amount of money deposited for a futures position. Therefore, traders should only use funds that they can afford to lose without affecting their lifestyles. And only a portion of those funds should be devoted to any one trade because they cannot expect to profit on every trade. All references to options refer to options on futures unless otherwise stated.

The Globe Logo, CME®, Chicago Mercantile Exchange®, and Globex® are trademarks of Chicago Mercantile Exchange Inc. CBOT® and the Chicago Board of Trade® are trademarks of the Board of Trade of the City of Chicago. NYMEX, New York Mercantile Exchange, and ClearPort are trademarks of New York Mercantile Exchange, Inc. COMEX is a trademark of Commodity Exchange, Inc. CME Group is a trademark of CME Group Inc. All other trademarks are the property of their respective owners.

The information within this presentation has been compiled by CME Group for general purposes only. CME Group assumes no responsibility for any errors or omissions. Although every attempt has been made to ensure the accuracy of the information within this presentation, CME Group assumes no responsibility for any errors or omissions. Additionally, all examples in this presentation are hypothetical situations, used for explanation purposes only, and should not be considered investment advice or the results of actual market experience.

All matters pertaining to rules and specifications herein are made subject to and are superseded by official CME, CBOT, NYMEX and CME Group rules. Current rules should be consulted in all cases concerning contract specifications.

This presentation is issued by the Chicago Mercanti le Exchange Inc.