Maryland’s 2016 Construction Industry Outlook

51

MARYLAND’S 2016 CONSTRUCTION INDUSTRY OUTLOOK

-

Upload

gross-mendelsohn-associates -

Category

Business

-

view

257 -

download

2

Transcript of Maryland’s 2016 Construction Industry Outlook

MARYLAND’S 2016 CONSTRUCTION

INDUSTRY OUTLOOK

INTRODUCTIONS

Steve Ball, CPA, CVA, CCIFP

Partner and Director of

Gross Mendelsohn’s

Construction Group

32 years of public accounting

experience in the construction

industry

THE SURVEY

SURVEY TOPICS

Outlook and Trends

Human Resources and Personnel Development

Accounting, Finance and Tax

Technology

Exit and Succession Planning

Recommendations

1.

2.

3.

4.

5.

6.

WH

O P

AR

TIC

IPA

TED

Over 200provided responses

Over 1,000asked to participate

WH

O P

AR

TIC

IPA

TED42%Owners/CEOs

18%CFOs/Accountants

40%Other

WH

O P

AR

TIC

IPA

TED

63%Subcontractors

34%General contactors

3%Heavy highway

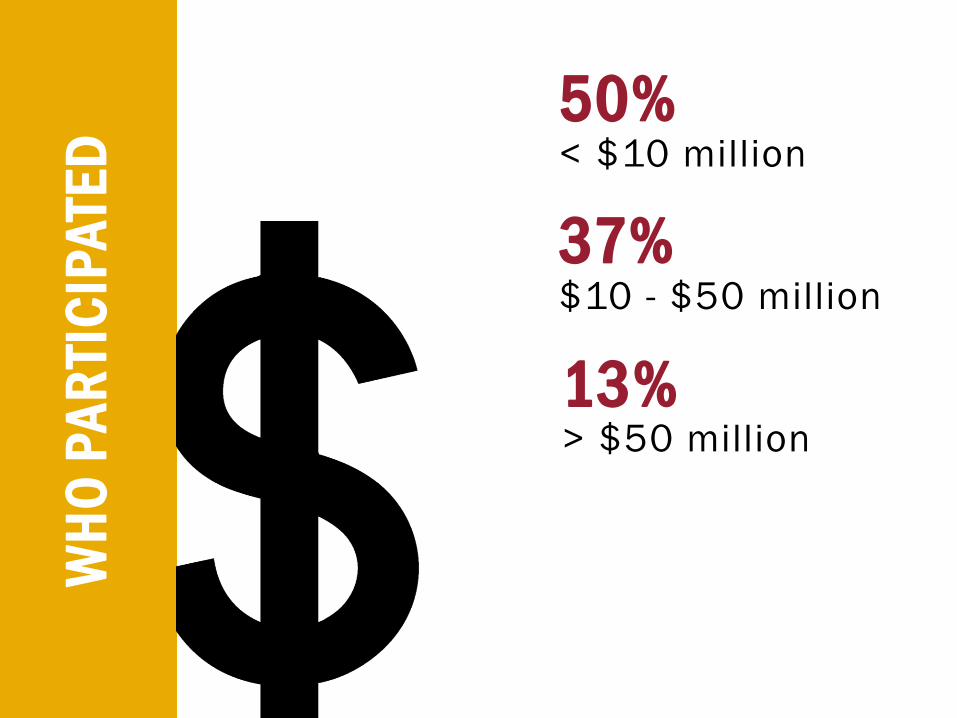

WH

O P

AR

TIC

IPA

TED50%< $10 million

37%$10 - $50 million

13%> $50 million

WH

O P

AR

TIC

IPA

TED

41%< 25 employees

21%26 – 50 employees

38%> 50 employees

OUTLOOK AND TRENDS

YOUR COMPANY’S OUTLOOK FOR 2016

85%More optimistic

15%Less optimistic

INDUSTRY OUTLOOK FOR 2016

50%Better

41%Same

9%Worse

BY ALL PARTICIPANTS

INDUSTRY OUTLOOK FOR 2016BY ROLE

Nearly 60% of CFOs and senior

finance staff say the industry’s

2016 outlook will be better,

compared to only 47% of

owners and CEOs

INDUSTRY OUTLOOK FOR 2016BY FIRM SIZE

Firms between $2.5M and $5M

had the lowest industry

outlook, with 42% reporting the

industry’s outlook would be

worse for 2016

REVENUE EXPECTATIONS FOR 2016

68%Increase

21%Same

11%Decrease

$4M

$5M

$6M

$7M$

7.4

M

$7.3

M

$5

M

$6

M

$6

.1M

$6

.3M

$7.1

M

$5

.1M

$5

.6M

AV

ER

AG

E S

ALE

S

Start of great recession

GROSS MENDELSOHN CONSTRUCTIONINDUSTRY BAROMETER

ORGANIC GROW TH

15%

18%

20%

23%

25%

28%2

6.7

%

27.0

%

23

.3%

20

.4% 17.4

%

18

.3%

22

.9%

17.0

%

19

.8%

Start of great recession

AV

ER

AG

E G

P%

GROSS MENDELSOHN CONSTRUCTIONINDUSTRY BAROMETER

PROFITABILIT Y

TOP CONCERNS FOR 2016

Finding and retaining good employees

Competition for experienced labor &the economy

Profitability38%

42%

54%

IMPACT OF ELECTION ON BUSINESS

26%Positive

63%Neutral

11%Negative

HUMAN RESOURCES AND PERSONNEL DEVELOPMENT

#1 REASON EMPLOYEES LEAVE

30%of respondents say the

#1 reason employees

leave their company is

because they can get

more money elsewhere

TOP THREE BENEFITS OFFERED

83%Medical

insurance

74%401(k)/profit sharing plan

71%Dental

insurance

21%Not giving increases

79%Giving increases

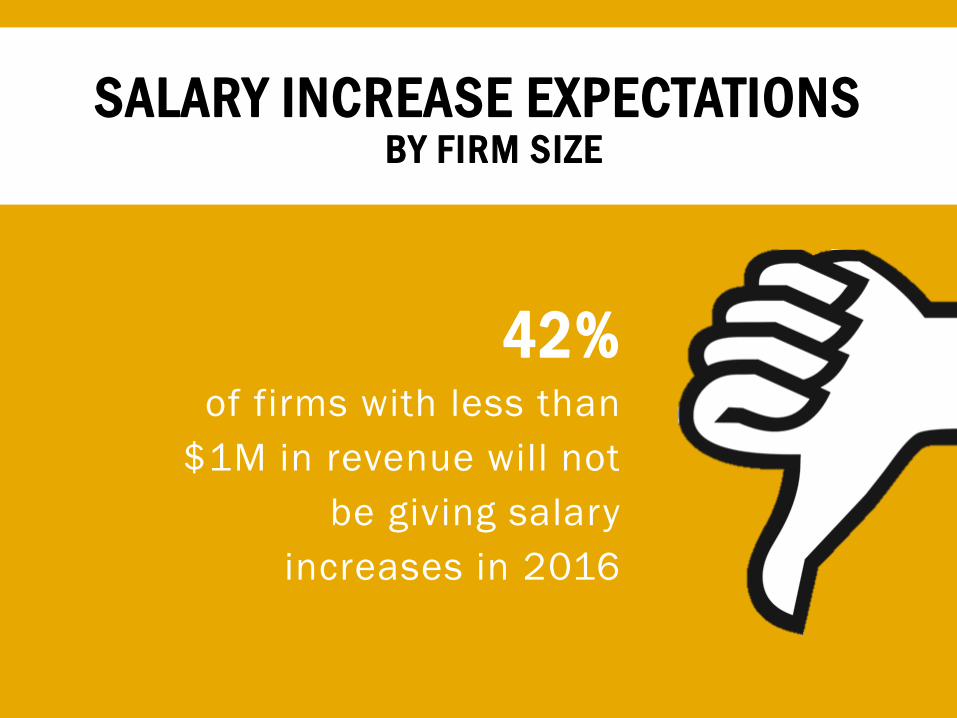

SALARY INCREASE EXPECTATIONSBY ALL PARTICIPANTS

42%of firms with less than

$1M in revenue will not

be giving salary

increases in 2016

SALARY INCREASE EXPECTATIONSBY FIRM SIZE

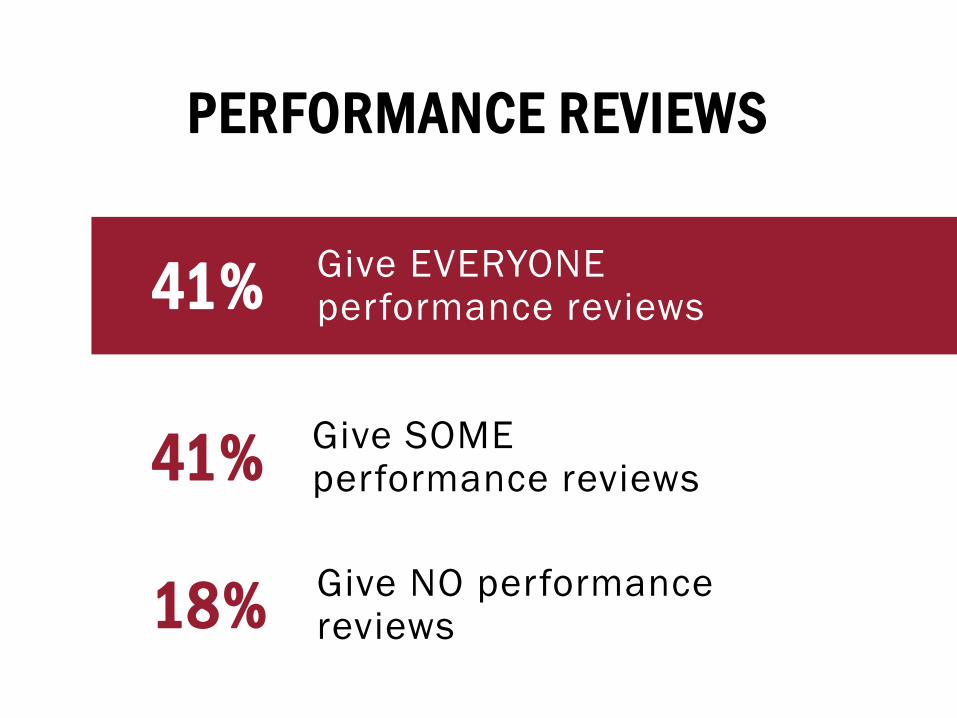

Give EVERYONE performance reviews

Give SOME performance reviews

Give NO performance reviews18%

41%

41%

PERFORMANCE REVIEWS

CO

MP

EN

SA

TIO

N

JUS

TIF

ICA

TIO

N89%Merit/job performance

8%Cost of living

3%Tenure at company

of all survey participants say

they have employees on staff

who should be terminated29%

TERMINATING EMPLOYEESBY ALL PARTICIPANTS

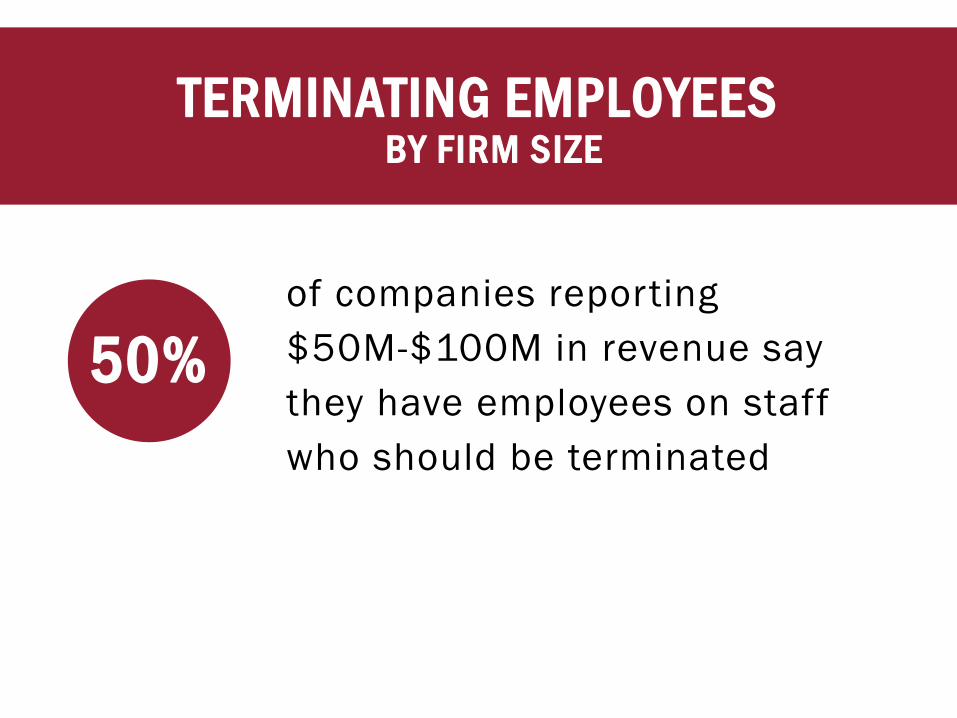

of companies reporting

$50M-$100M in revenue say

they have employees on staff

who should be terminated

50%

TERMINATING EMPLOYEESBY FIRM SIZE

ACCOUNTING, FINANCE AND TAX

75%On target

16%Underestimate

9%Overestimate

ESTIMATE ACCURACYBY ALL PARTICIPANTS

100%Heavy highway

84%General contractors

69%Subcontractors

ESTIMATES ARE RIGHT ON TARGETBY CONTRACTOR T YPE

TAKES ADVANTAGE OF TAX CREDITS

8%

Not sure

82%

Section 179DEnergy Efficiency

6%Section 41 R&D

4%Section 199 DPAD

AVAILABILIT Y OF BANK FINANCING

30%Increasing

63%Same

7%Decreasing

TECHNOLOGY

TOP SOFTWARE PACKAGES

28%QuickBooks

13%Timberline

11%ComputerEase

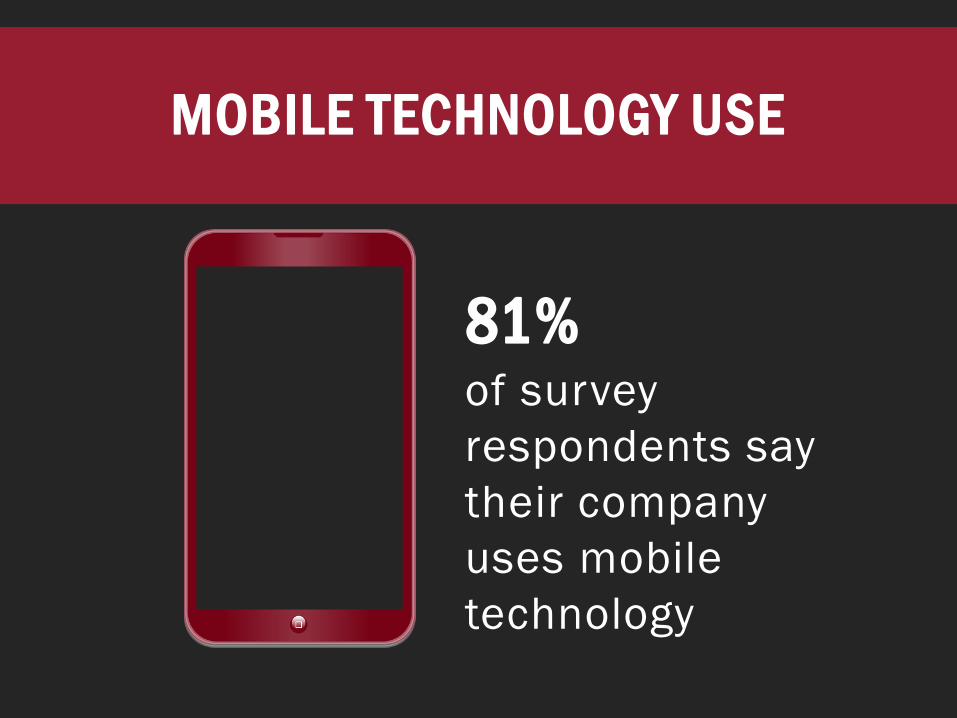

81%of survey

respondents say

their company

uses mobile

technology

MOBILE TECHNOLOGY USE

One fifthof survey participants

were hacked last year

COMPUTER HACKS IN THE PAST YEARBY ALL PARTICIPANTS

Firms making more

than $25M were

twice as likely to be

hacked than

smaller firms

EXIT AND SUCCESSION PLANNING

EXIT PLANNING

?57%of owners say they don’t

have or don’t know if

they have an exit plan

SUCCESSOR

70%of survey respondents

say their firm has not

identified a successor

BUSINESS VALUE

30%Less than

of owners say they

know how much their

business is worth

of survey respondents say their

company doesn’t have a

stockholders’ agreement that has

buy-sell provisions

STOCKHOLDERS’ AGREEMENT

62%

More strategic planning and

developmental work relative to employee

issues and concerns

RECOMMENDATIONS

Take a closer look at f irm culture issues

Revisit compensation and benefits

Implement a company-wide employee

review program

RECOMMENDATIONS

Attempt to increase pricing modestly

Ensure profitability of new work by

enforcing fundamental business principles

Take advantage of tax minimization

opportunities through deductions and

credits

RECOMMENDATIONS

Choose the right software by looking for a

product that reflects your firm’s wants and

expectations

Engage the ser vices of IT specialists who

can assess your system and put in

safeguards to protect your firm’s critical

data

RECOMMENDATIONS

Make an exit plan

Know what your business is actually

wor th

FIELD NET PERFORMANCE RATING FORM

QUESTIONS

?

CO

NTA

CT

ME

410.685.5512

www.gma-cpa.com

FOLLOW US

GET THE 2016 MARYLAND CONSTRUCTION INDUSTRY SURVEY EXECUTIVE SUMMARY

Get data from over 200

Maryland construction

contractors

Download your copy now