Lean Cash Flow: Simple Steps To Manage Your Startup Cash Flow

Upload

kristinportCategory

view

229download

0

7/27/2019 Marley's Cash Flow

http://slidepdf.com/reader/full/marleys-cash-flow 1/64

7/27/2019 Marley's Cash Flow

http://slidepdf.com/reader/full/marleys-cash-flow 2/64

2

Objectives:1. Describe the purpose of the Cash Flow Statement (how it meets

GAAP’s Objectives of Financial Reporting)

2. Prepare a Statement of Cash flows under both the Direct andIndirect Method.

3. Differentiate between Net Income and Cash from Operations(CFO) and use it to assess a company’s ability to generate future Cash Flows (CFO)

4. Evaluate the company’s quality of earnings by comparing andreconciling net income to cash

5. Determine whether a company is expanding or contracting using the “Investing” section of the Cash Flow Statement

6. Evaluate the company’s financing activity – are they relying oninternal or external financing , and debt or equity financing?

7. Assess a company’s need for external financing and its ability to

pay its debts and dividends

Cash Flow Statement Learning Objectives

7/27/2019 Marley's Cash Flow

http://slidepdf.com/reader/full/marleys-cash-flow 3/64

• What is included in “cash”? • The cash flow statement provides

information for a period of time about: – cash receipts (cash inflows) – uses of cash (cash outflows)

• Inflows and outflows are reported for: – operating – investing – financing activities – Summing to the net increase/decrease in cash over

the period

The Cash Flow Statement

7/27/2019 Marley's Cash Flow

http://slidepdf.com/reader/full/marleys-cash-flow 4/64

4

Cash is King

• Remember the 2nd Objective of FinancialReporting: to “Provide Information that is useful inassessing future ________ flows”. (see the House of GAAP from our first class, and repeated on the next slide)

• A good place to start predicting future cash flowsis the company’s historical cash flows.

• The Statement of Cash Flows provides information

about the cash receipts and cash disbursementsduring a specific time period, the same time periodcovered by the income statement.

4

7/27/2019 Marley's Cash Flow

http://slidepdf.com/reader/full/marleys-cash-flow 5/64

5

HOUSE OF GAAPGAAP’s Objective is to provide Financial Information that is:

1. Useful in investment & credit decisions2. Useful in assessing future ______ flows

3. About the enterprise resources (assets), claims (liabilities& owners’ equity) to resources, and _________ in them

Qualitative CharacteristicsRelevancePredictive or Feedback Value

TimelinessReliability

Comparability

Consistency

Elements AssetsLiabilities

Stockholders’ Equity Other Comprehensive Income

Revenues

Expenses

Assumptions

Economic EntityGoing ConcernMonetary Unit

Periodicity

Principles

Historical CostRevenue Recognition

Matching

Full Disclosure

Constraints

Cost/BenefitMateriality

Industry Practice

Conservatism

7/27/2019 Marley's Cash Flow

http://slidepdf.com/reader/full/marleys-cash-flow 6/64

6

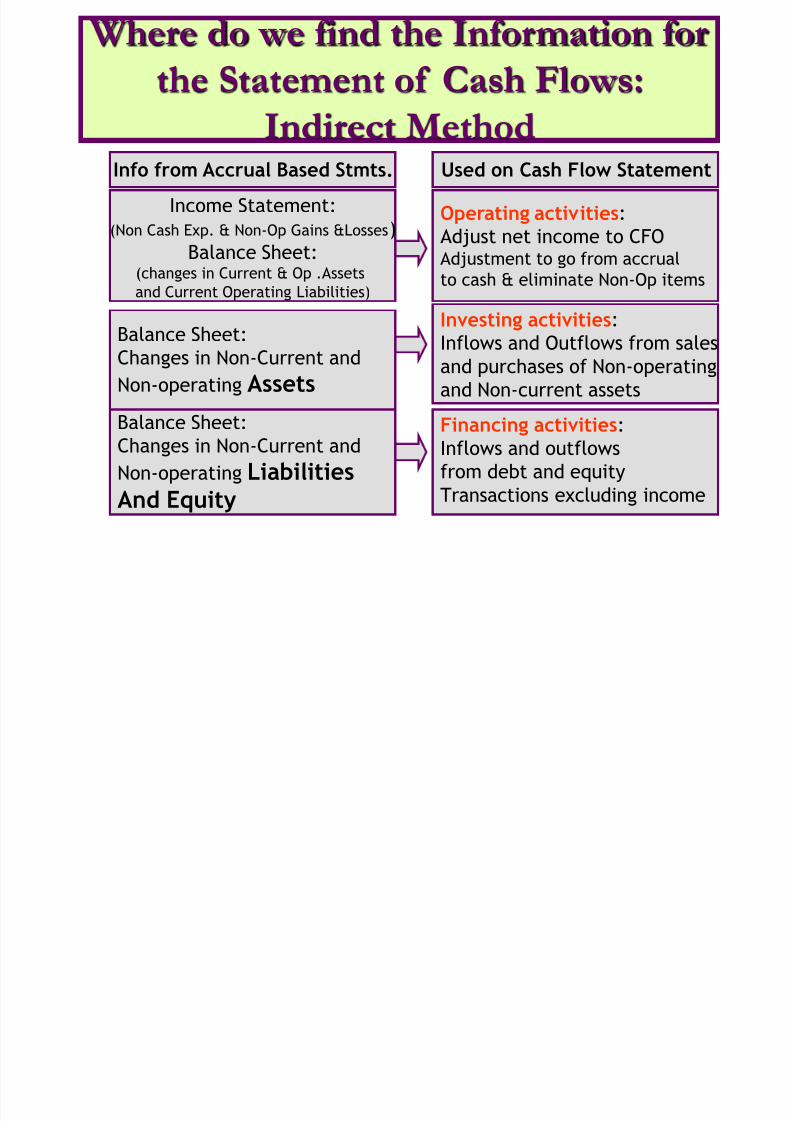

Highlighting Balance Sheet Changes

• The 3rd Objective of Financial Reporting is to “Provide Information about the enterpriseresources (assets), claims (liabilities & owners’ equity) to resources, and _________ in them” (see the House of GAAP Prior slide and first class)

• The Cash Flow Statement also highlights how theBalance Sheet Accounts have changed.

Changes in Balance Sheet Accounts: Located in Cash Flow Statement

1. Most Current Assets and CurrentLiabilities (working capital accts) Operating Section

2. Most Long-term Assets Investing Section

3. Most Non-operating Liabilities

Stockholder’s Equity accounts

Financing Section

7/27/2019 Marley's Cash Flow

http://slidepdf.com/reader/full/marleys-cash-flow 7/64

7/27/2019 Marley's Cash Flow

http://slidepdf.com/reader/full/marleys-cash-flow 8/64

7/27/2019 Marley's Cash Flow

http://slidepdf.com/reader/full/marleys-cash-flow 9/64

9

Using the Statement of Cash Flows

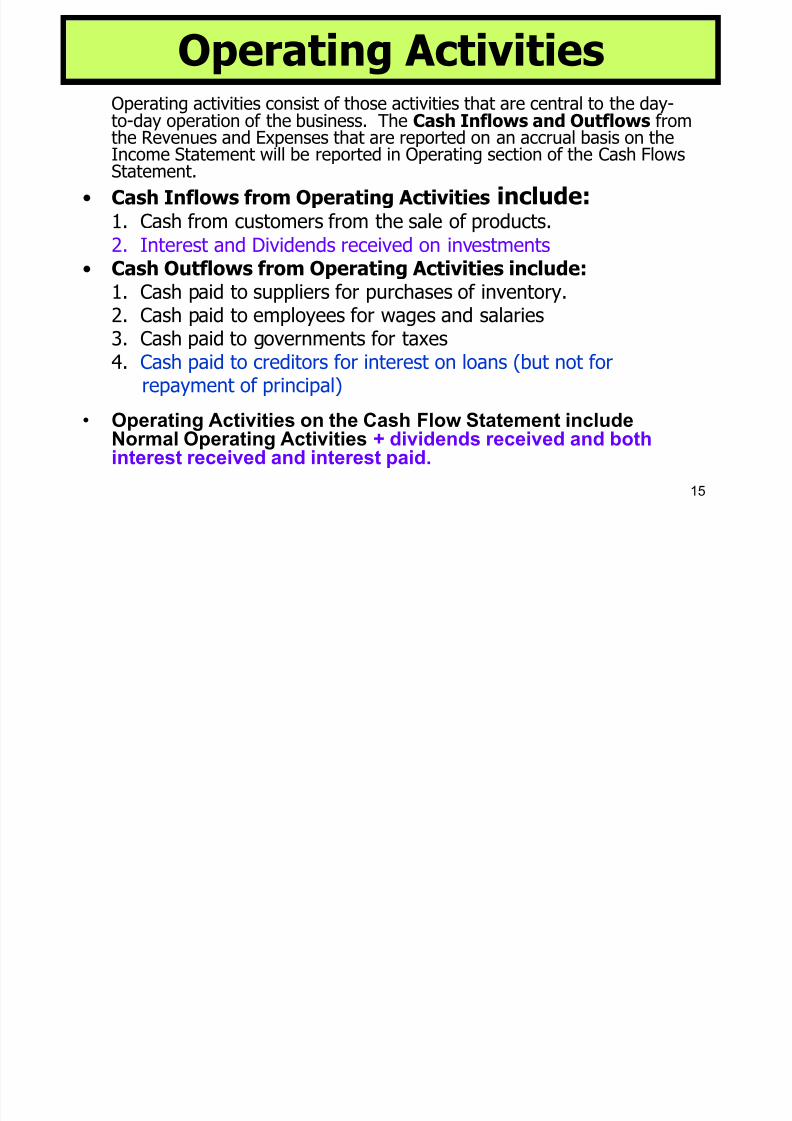

In addition to reporting the changes to each currentoperating asset & liability (accounts receivable, inventory,accounts payable) the Statement of Cash Flows also helps:

• assess a company’s ability to generate positive future

cash flows from operations,• reconcile differences between net income and the change

in the cash balance.

• monitor a company’s investment in property, plant and

equipment – is it more or less than their depreciationexpense? Is the company expanding or contracting?

• assess a company’s need for external financing, source of external financing (debt or equity) and its ability to payits debts and dividends.

7/27/2019 Marley's Cash Flow

http://slidepdf.com/reader/full/marleys-cash-flow 10/64

7/27/2019 Marley's Cash Flow

http://slidepdf.com/reader/full/marleys-cash-flow 11/64

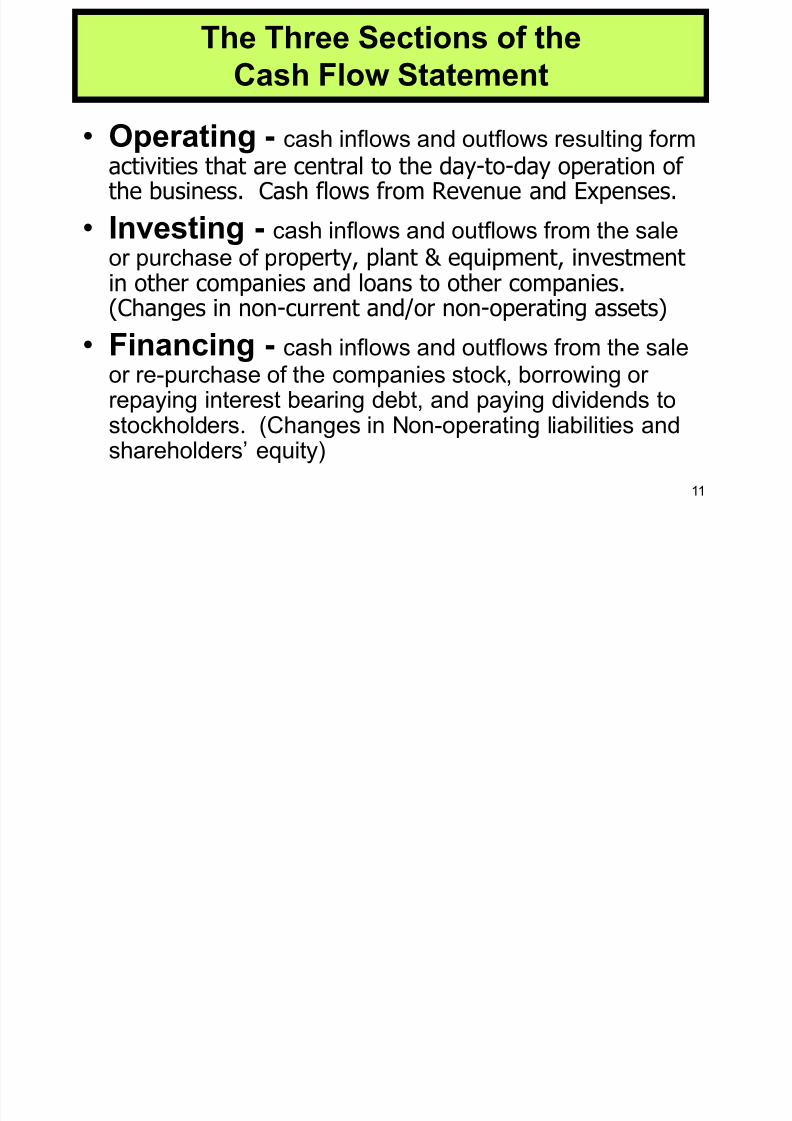

11

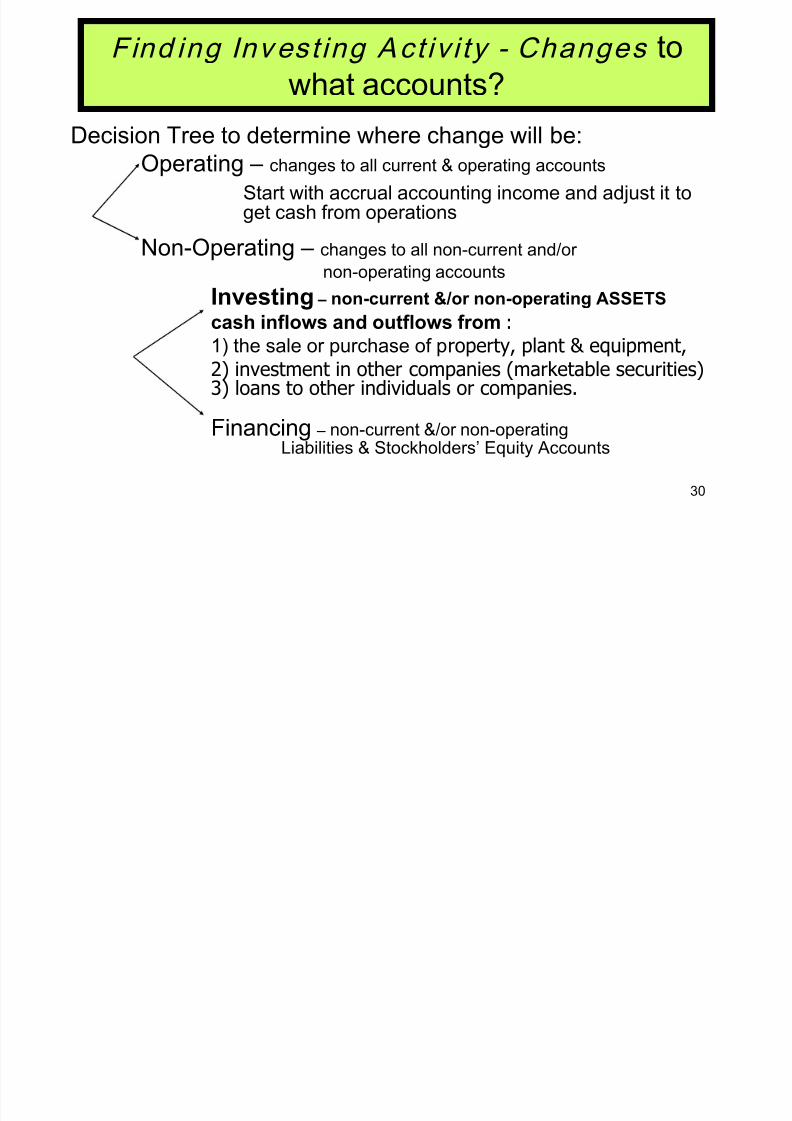

The Three Sections of the

Cash Flow Statement

• Operating - cash inflows and outflows resulting formactivities that are central to the day-to-day operation of the business. Cash flows from Revenue and Expenses.

• Investing - cash inflows and outflows from the saleor purchase of property, plant & equipment, investmentin other companies and loans to other companies.(Changes in non-current and/or non-operating assets)

• Financing - cash inflows and outflows from the sale

or re-purchase of the companies stock, borrowing or repaying interest bearing debt, and paying dividends tostockholders. (Changes in Non-operating liabilities andshareholders’ equity)

7/27/2019 Marley's Cash Flow

http://slidepdf.com/reader/full/marleys-cash-flow 12/64

7/27/2019 Marley's Cash Flow

http://slidepdf.com/reader/full/marleys-cash-flow 13/64

7/27/2019 Marley's Cash Flow

http://slidepdf.com/reader/full/marleys-cash-flow 14/64

7/27/2019 Marley's Cash Flow

http://slidepdf.com/reader/full/marleys-cash-flow 15/64

7/27/2019 Marley's Cash Flow

http://slidepdf.com/reader/full/marleys-cash-flow 16/64

16

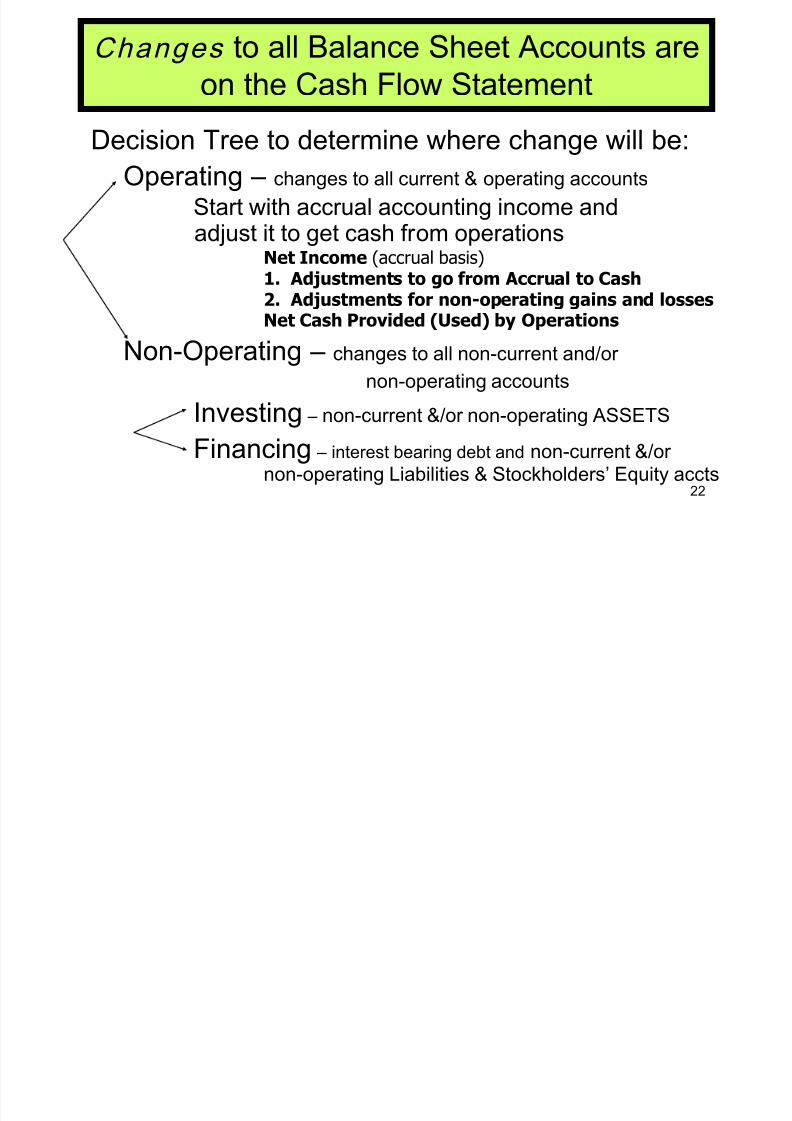

Decision Tree to determine Reporting on theCash Flow Statement

Operating – changes to all current & operating accountsStart with accrual accounting income andadjust it to get cash from operations

Net Income (accrual basis)1. Adjustments to go from Accrual to Cash

a. Changes to all Current & Operating Assetsb. Changes to all Current & Operating Liabilitiesc. Non Cash Expenses

2. Adjustments for non-operating gains and lossesNet Cash Provided (Used) by Operations

Non-Operating – changes to all non-current and/or non-operating accounts

Investing – non-current &/or non-operating ASSETS

Financing – interest bearing debt and non-current &/or non-operating Liabilities & Stockholders’ Equity accts

7/27/2019 Marley's Cash Flow

http://slidepdf.com/reader/full/marleys-cash-flow 17/64

7/27/2019 Marley's Cash Flow

http://slidepdf.com/reader/full/marleys-cash-flow 18/64

7/27/2019 Marley's Cash Flow

http://slidepdf.com/reader/full/marleys-cash-flow 19/64

7/27/2019 Marley's Cash Flow

http://slidepdf.com/reader/full/marleys-cash-flow 20/64

20

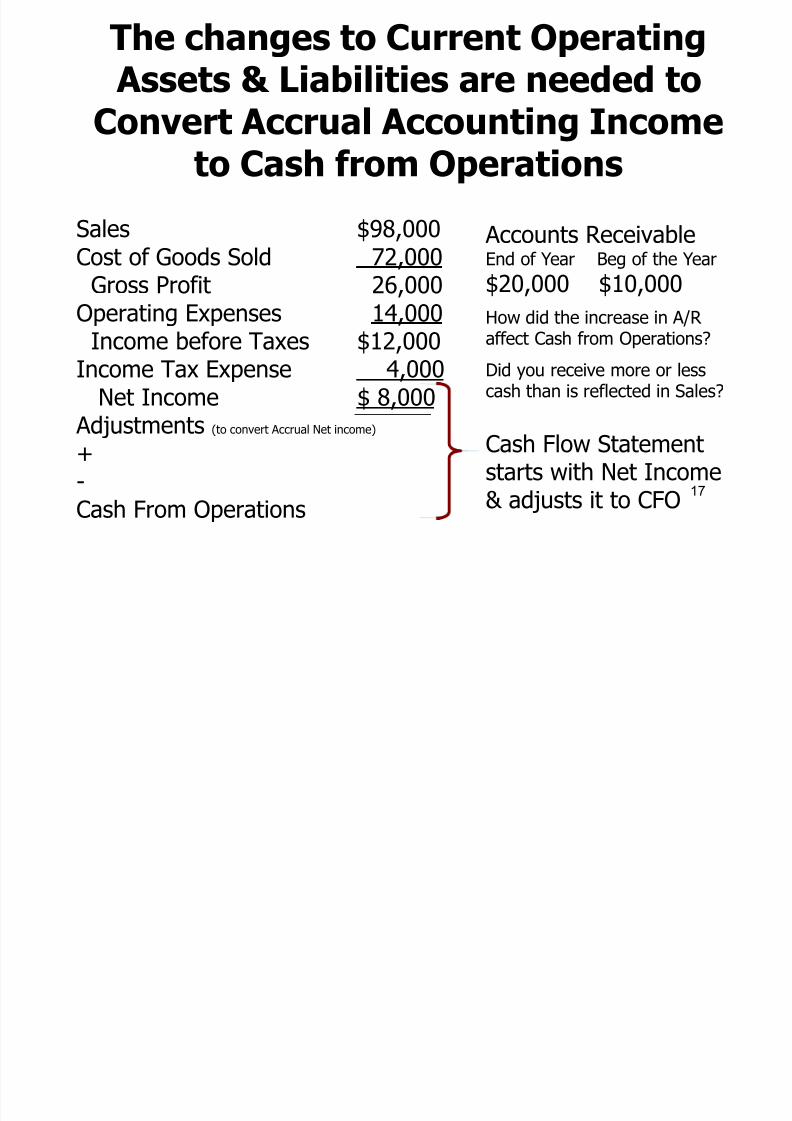

The changes to Current Operating Assets & Liabilities are needed to

Convert Accrual Accounting Incometo Cash from Operations

Sales $98,000

Cost of Goods Sold 72,000Gross Profit 26,000

Operating Expenses 14,000Income before Taxes $12,000

Income Tax Expense 4,000Net Income $ 8,000

Adjustments (to convert Accrual Net income)

+-Cash From Operations

Taxes PayableEnd of Year Beg of the Year

$5,000 $ 3,000

How did the increase in TaxesPayable affect Cash fromOperations?

Did you spend more or less cashthan is reflected in income taxexpense?

Cash Flow Statementstarts with Net Income

& adjusts it to CFO

7/27/2019 Marley's Cash Flow

http://slidepdf.com/reader/full/marleys-cash-flow 21/64

7/27/2019 Marley's Cash Flow

http://slidepdf.com/reader/full/marleys-cash-flow 22/64

7/27/2019 Marley's Cash Flow

http://slidepdf.com/reader/full/marleys-cash-flow 23/64

7/27/2019 Marley's Cash Flow

http://slidepdf.com/reader/full/marleys-cash-flow 24/64

7/27/2019 Marley's Cash Flow

http://slidepdf.com/reader/full/marleys-cash-flow 25/64

7/27/2019 Marley's Cash Flow

http://slidepdf.com/reader/full/marleys-cash-flow 26/64

Lansbury Inc. Balance Sheet

December 31, 2010 increase

(decrease) Assets 2010 2009 Cash $ 32,000 $ 20,000 $ 12,000

Accounts Receivable

41,600 21,200 20,400Investments 20,400 32,000 (11,600)

Plant Assets (net) 70,000 81,000 (11,000)

Land 88,000 40,000 48,000

total assets $ 252,000 $ 194,200 $ 57,800

Liabilities and Stockholders's Equity Accounts payable $ 30,000 $ 30,000 $ -

Notes Payable 25,000 41,000 (16,000)

Bonds Payable 30,000 30,000

Common Stock 120,000 100,000 20,000

Retained Earnings 47,000 23,200 23,800

$ 252,000 $ 194,200 $ 57,800

Prepare Statement of Cash Flows

(Indirect using Ch 5 problem 6)

7/27/2019 Marley's Cash Flow

http://slidepdf.com/reader/full/marleys-cash-flow 27/64

7/27/2019 Marley's Cash Flow

http://slidepdf.com/reader/full/marleys-cash-flow 28/64

7/27/2019 Marley's Cash Flow

http://slidepdf.com/reader/full/marleys-cash-flow 29/64

29

Computing Cash from Operations Start with Net Income and Adjust it to get Cash from Operations.

Net Income (accrual basis) $32,000

1. Adjustments to go from Accrual to Cash: A. Add back non-cash expenses (Expenses that

reduce net income but do not use up any cash)Depreciation Expense $ 11,000

_____________________________ $______

B. Changes in Operating Assets & LiabilitiesIncrease in Accounts Receivable (20,400)

_____________________________ $______

2. Adjustments for non-operating gains and losses:We want only operating cash so add back non-operating losses which have

reduced net income and subtract out gains from non-operating activitiesLoss on disposition of assets

Gain on sale of Investments ( 3,400)

Net Cash Provided by Operations $ 19,200

Computing Cash from Operations

7/27/2019 Marley's Cash Flow

http://slidepdf.com/reader/full/marleys-cash-flow 30/64

7/27/2019 Marley's Cash Flow

http://slidepdf.com/reader/full/marleys-cash-flow 31/64

7/27/2019 Marley's Cash Flow

http://slidepdf.com/reader/full/marleys-cash-flow 32/64

7/27/2019 Marley's Cash Flow

http://slidepdf.com/reader/full/marleys-cash-flow 33/64

7/27/2019 Marley's Cash Flow

http://slidepdf.com/reader/full/marleys-cash-flow 34/64

7/27/2019 Marley's Cash Flow

http://slidepdf.com/reader/full/marleys-cash-flow 35/64

7/27/2019 Marley's Cash Flow

http://slidepdf.com/reader/full/marleys-cash-flow 36/64

7/27/2019 Marley's Cash Flow

http://slidepdf.com/reader/full/marleys-cash-flow 37/64

7/27/2019 Marley's Cash Flow

http://slidepdf.com/reader/full/marleys-cash-flow 38/64

7/27/2019 Marley's Cash Flow

http://slidepdf.com/reader/full/marleys-cash-flow 39/64

LO 2 Identify the major classifications of cash flows.

Typical Company Cash Flow Life Cycle

7/27/2019 Marley's Cash Flow

http://slidepdf.com/reader/full/marleys-cash-flow 40/64

7/27/2019 Marley's Cash Flow

http://slidepdf.com/reader/full/marleys-cash-flow 41/64

41

1. Calculate each company’s cash balance at the end of the year.

2. Would you prefer to own company A, B or C? Why?

3. Which company would you least like to own? Why?

4. Which companies have net income and which have a net loss?

5. Explain what might cause company C’s net cash from financingactivities to be negative.

6. Explain what might cause company A’s net cash from financingactivities to be positive.

Using the Statement of Cash Flows

Co. A Co. B Co. C

Net cash flow from operating activities (300)$ (400)$ 300$

Net cash provided (used) in investing activities (900) 500 (90)

Net cash provided (used) in financing activities 1,200 (10) (240)

Net increase or decrease in cash for the year

Cash balance beginning of year 150 150 150

Ending Cash Balance

7/27/2019 Marley's Cash Flow

http://slidepdf.com/reader/full/marleys-cash-flow 42/64

7/27/2019 Marley's Cash Flow

http://slidepdf.com/reader/full/marleys-cash-flow 43/64

43

Summary story from the Cash Flow Statement

2010 2009 2008

Cash provided by Operations 3,919 7,000 3,670

Cash (required) by Investing Activity (14,031) (4,600) (3,650)

Net effect on Cash from issuing (retiring) debt (6,154) (2,339) 2,876Net effect on Cash from issuing (retiring) stock 23,082 141 639

Effect of exchange rate changes on cash (4) 14 -

Net increase (decrease) in Cash $6,812 $216 $3,535

What is Company’s major source of cash?

Is the company relying upon internal or external financing?

Is the Company generating enough cash to pay its debt obligations?

7/27/2019 Marley's Cash Flow

http://slidepdf.com/reader/full/marleys-cash-flow 44/64

7/27/2019 Marley's Cash Flow

http://slidepdf.com/reader/full/marleys-cash-flow 45/64

7/27/2019 Marley's Cash Flow

http://slidepdf.com/reader/full/marleys-cash-flow 46/64

7/27/2019 Marley's Cash Flow

http://slidepdf.com/reader/full/marleys-cash-flow 47/64

7/27/2019 Marley's Cash Flow

http://slidepdf.com/reader/full/marleys-cash-flow 48/64

Format of the Statement of Cash Flows

7/27/2019 Marley's Cash Flow

http://slidepdf.com/reader/full/marleys-cash-flow 49/64

Format of the Statement of Cash Flows

7/27/2019 Marley's Cash Flow

http://slidepdf.com/reader/full/marleys-cash-flow 50/64

7/27/2019 Marley's Cash Flow

http://slidepdf.com/reader/full/marleys-cash-flow 51/64

7/27/2019 Marley's Cash Flow

http://slidepdf.com/reader/full/marleys-cash-flow 52/64

7/27/2019 Marley's Cash Flow

http://slidepdf.com/reader/full/marleys-cash-flow 53/64

E23-6: Prepare the operating activities section of the statement of

cash flows using the indirect method (Step 2).

Cash flows from operating activities

Net income 90,000$

Adjustment to reconcile net incometo net cash provided by operating activities:

Depreciation expense 60,000

Loss on sale of equipment 26,000

Decrease in accounts receivable 17,000

Increase in accounts payable 10,000

Decrease in income taxes payable (4,500)

Net cash provided by operating activities 198,500

Operating Activities— Indirect Method

7/27/2019 Marley's Cash Flow

http://slidepdf.com/reader/full/marleys-cash-flow 54/64

7/27/2019 Marley's Cash Flow

http://slidepdf.com/reader/full/marleys-cash-flow 55/64

7/27/2019 Marley's Cash Flow

http://slidepdf.com/reader/full/marleys-cash-flow 56/64

Statement of Cash Flows

Cash flow from operating activitiesNet income (loss) (50,000)$

Adjustment to reconcile net income to cash:

Loss on sale 2,700

Depreciation expense 22,000

Gain on sale (9,000)

Cash from operations (34,300)

Cash flow from investing activities

Sale of plant assets 5,300

Sale of land 39,000

Cash from investing activities 44,300

Cash flow from financing activities

Sale of common stock 330,000 Purchase of company stock (47,000)

Cash from financing activities 283,000

Net Change in Cash 293,000$

O

I

F

The Cash Flow Statement

7/27/2019 Marley's Cash Flow

http://slidepdf.com/reader/full/marleys-cash-flow 57/64

7/27/2019 Marley's Cash Flow

http://slidepdf.com/reader/full/marleys-cash-flow 58/64

7/27/2019 Marley's Cash Flow

http://slidepdf.com/reader/full/marleys-cash-flow 59/64

7/27/2019 Marley's Cash Flow

http://slidepdf.com/reader/full/marleys-cash-flow 60/64

LO 7 Identify sources of information for a statement of cash flows.

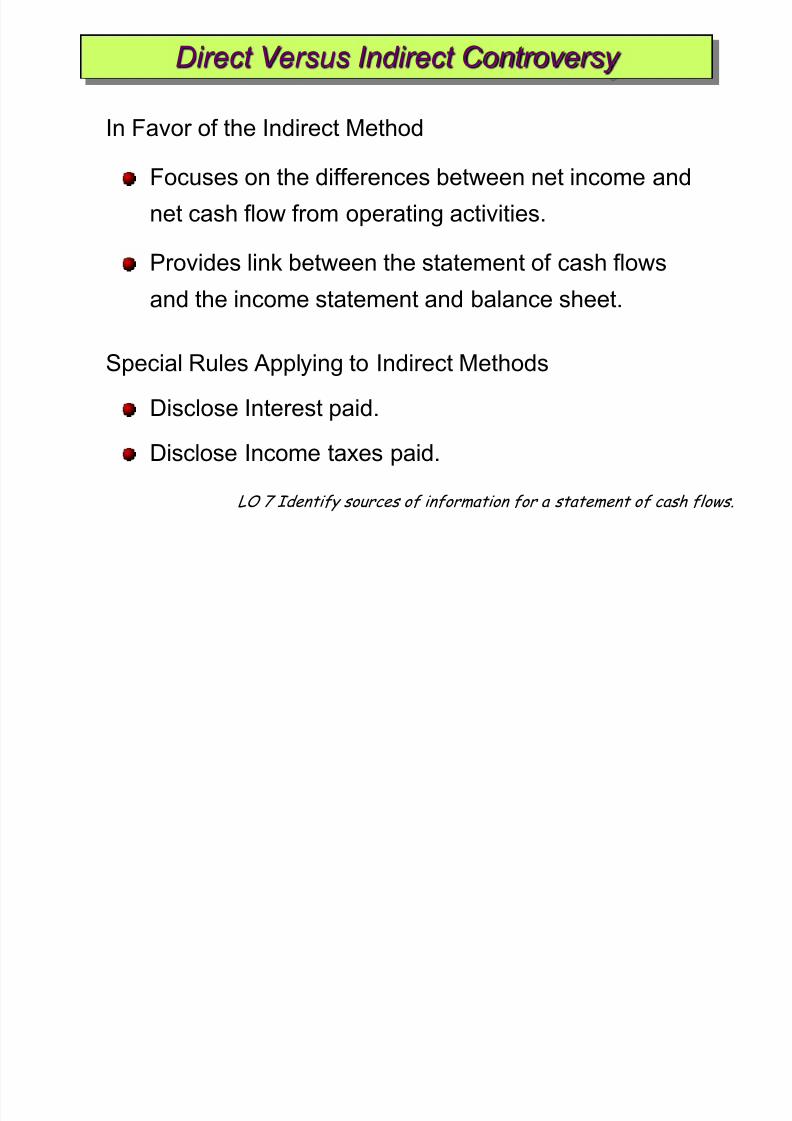

In Favor of the Indirect Method

Focuses on the differences between net income and

net cash flow from operating activities.

Provides link between the statement of cash flows

and the income statement and balance sheet.

Special Rules Applying to Indirect Methods

Disclose Interest paid.

Disclose Income taxes paid.

Direct Versus Indirect Controversy

7/27/2019 Marley's Cash Flow

http://slidepdf.com/reader/full/marleys-cash-flow 61/64

7/27/2019 Marley's Cash Flow

http://slidepdf.com/reader/full/marleys-cash-flow 62/64

7/27/2019 Marley's Cash Flow

http://slidepdf.com/reader/full/marleys-cash-flow 63/64

LO 8 Discuss special problems in preparing a statement of cash flows.

2. Accounts receivable, net3. Other working capital changes

4. Net losses

5. Gains

6. Stock options

7. Postretirement benefits

8. Extraordinary items

9. Significant noncash transactions

Special Problems in Statement Preparation

7/27/2019 Marley's Cash Flow

http://slidepdf.com/reader/full/marleys-cash-flow 64/64