MARKETBEAT Office Snapshot Q1 2016 - Cushman & …/media/reports/vietnam/Q1 2016 Vietna… ·...

20

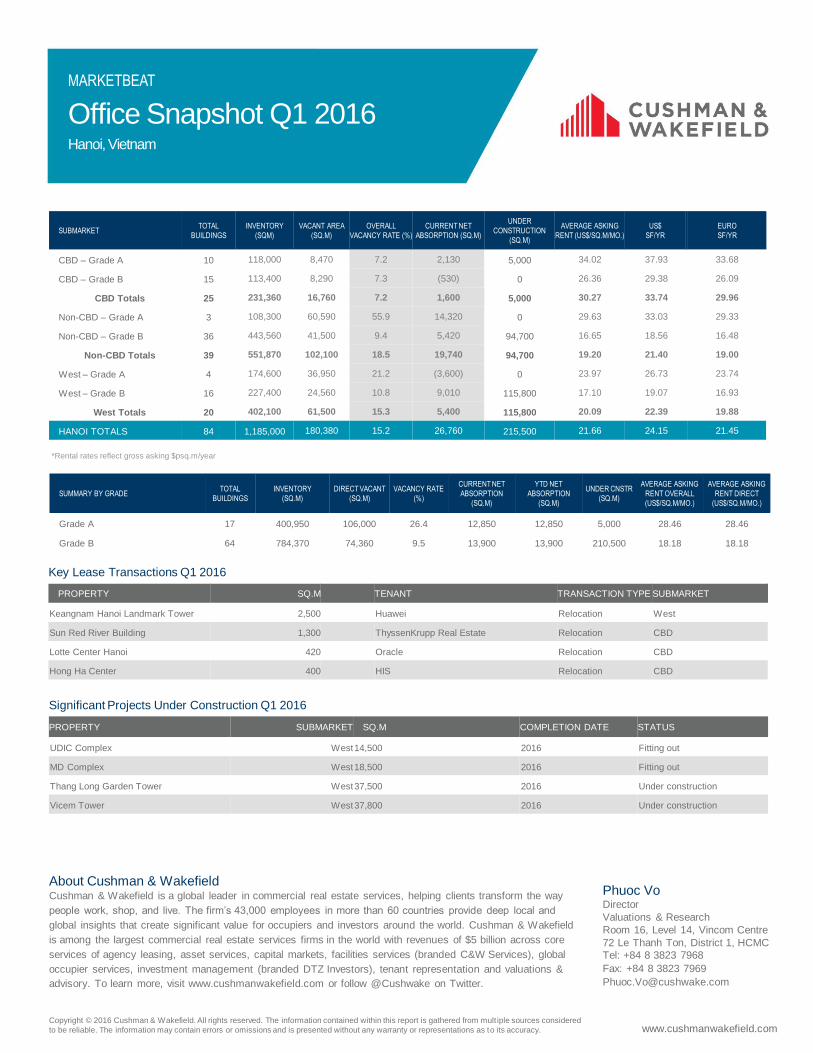

Office Snapshot Q1 2016 Hanoi, Vietnam MARKETBEAT Economic Indicators Market Indicators – Grade A Grade A - Net Absorption/Asking Rent Grade A - Overall Vacancy www.cushmanwakefield.com Economy With an impressive economic growth in 2015, the government has set a more optimistic target of 6.7% in GDP growth and CPI at below 5% in 2016. As of February 2016, total inward FDI into Vietnam reached US$2.80 billion (both newly registered and adjusted), up 135% year-on-year, while implemented FDI was estimated to have reached US$1.5 billion, up 15.4% year-on-year. The manufacturing and processing industry, which accounted for 71.2% of total registered capital, attracted the largest share. Singapore was the leading investor with newly registered FDI in the first two months accounting for 23% of the total investment. Market Overview Two new office buildings were delivered in first quarter 2016, namely TNR Tower (Grade A) and Handico Tower (Grade B), adding over 65,600 square meters (sq.m.) of office space to the market. Currently, there are 17 Grade A and 67 Grade B office buildings, supplying over 1,185,000 sq.m. of office space to the market, registering an increase of 6% quarter-on-quarter and 9% year-on-year. Average asking rent for both Grades in first quarter 2016 trended downward on a yearly basis—down by 6% for Grade A to VND635,000 per square meter per month (/sq.m./mo), equivalent to US$28.46/sq.m/mo; and down by 3% for Grade B to VND405,000/sq.m./mo, equivalent to US$18.18/sq.m./mo respectively. This was mostly due to lower rents in the new projects. Due to substantial new supply delivered this quarter, Grade A experienced a significant fall in average occupancy rate by 6.3 percentage points quarter-on-quarter and 2.2 percentage points year-on-year, to reach 73.6%. Meanwhile, over 90% of Grade B office was occupied in this quarter, remaining stable quarter-on-quarter but registering a significant increase in occupancy rate by 8.3 percentage points year-on-year. Outlook Twelve new projects are expected to be completed this year, providing approximately 170,500 sq.m. of office space to the market. Most of these projects are located in the non-CBD and the Western area, contributing 54% and 44% to the new stock respectively. This implies a tendency to shift from the crowded CBD to nearby districts such as Dong Da, Ba Dinh, and especially to the West, such as Cau Giay and Tu Liem Districts. Half of these projects are currently in the fit-out stage. 2 months 15 2 months 16 12-Month Forecast CPI (%) 0.64 1.03 Inward FDI (billion US$) 1.19 2.80 Trade balance (billion US$) (0.61) 0.86 Q1 15 Q1 16 12-Month Forecast Grade A Overall Vacancy 24.3% 26.4% Grade A Net Absorption 9.3k 12.9k Under Construction 81.8k 5.0k Grade A Average Asking Rent (/sqm/mo.) $30.27 $28.46 0% 5% 10% 15% 20% 25% 30% 35% 40% 2010 2011 2012 2013 2014 2015 2016 HANOI OFFICE Historical Average = 22% $10 $20 $30 $40 $50 -5,000 0 5,000 10,000 15,000 20,000 25,000 2010 2011 2012 2013 2014 2015 2016 Net Absorption, SQ.M Asking Rent, $ PSQ.M

-

Upload

duongkhanh -

Category

Documents

-

view

237 -

download

4

Transcript of MARKETBEAT Office Snapshot Q1 2016 - Cushman & …/media/reports/vietnam/Q1 2016 Vietna… ·...

Office Snapshot Q1 2016Hanoi, Vietnam

MARKETBEAT

Economic Indicators

Market Indicators – Grade A

Grade A - Net Absorption/Asking Rent

Grade A - Overall Vacancy

www.cushmanwakefield.com

Economy

With an impressive economic growth in 2015, the government has

set a more optimistic target of 6.7% in GDP growth and CPI at

below 5% in 2016. As of February 2016, total inward FDI into

Vietnam reached US$2.80 billion (both newly registered and

adjusted), up 135% year-on-year, while implemented FDI was

estimated to have reached US$1.5 billion, up 15.4% year-on-year.

The manufacturing and processing industry, which accounted for

71.2% of total registered capital, attracted the largest share.

Singapore was the leading investor with newly registered FDI in

the first two months accounting for 23% of the total investment.

Market Overview

Two new office buildings were delivered in first quarter 2016,

namely TNR Tower (Grade A) and Handico Tower (Grade B),

adding over 65,600 square meters (sq.m.) of office space to the

market. Currently, there are 17 Grade A and 67 Grade B office

buildings, supplying over 1,185,000 sq.m. of office space to the

market, registering an increase of 6% quarter-on-quarter and 9%

year-on-year.

Average asking rent for both Grades in first quarter 2016

trended downward on a yearly basis—down by 6% for Grade A

to VND635,000 per square meter per month (/sq.m./mo),

equivalent to US$28.46/sq.m/mo; and down by 3% for Grade B to

VND405,000/sq.m./mo, equivalent to US$18.18/sq.m./mo

respectively. This was mostly due to lower rents in the new

projects.

Due to substantial new supply delivered this quarter, Grade A

experienced a significant fall in average occupancy rate by

6.3 percentage points quarter-on-quarter and 2.2 percentage

points year-on-year, to reach 73.6%. Meanwhile, over 90% of

Grade B office was occupied in this quarter, remaining stable

quarter-on-quarter but registering a significant increase in

occupancy rate by 8.3 percentage points year-on-year.

Outlook

Twelve new projects are expected to be completed this year,

providing approximately 170,500 sq.m. of office space to the

market. Most of these projects are located in the non-CBD and the

Western area, contributing 54% and 44% to the new stock

respectively. This implies a tendency to shift from the crowded

CBD to nearby districts such as Dong Da, Ba Dinh, and especially

to the West, such as Cau Giay and Tu Liem Districts. Half of these

projects are currently in the fit-out stage.

2 months 15 2 months 1612-Month

Forecast

CPI (%) 0.64 1.03

Inward FDI (billion US$) 1.19 2.80

Trade balance

(billion US$)(0.61) 0.86

Q1 15 Q1 1612-Month

Forecast

Grade A Overall Vacancy 24.3% 26.4%

Grade A Net Absorption 9.3k 12.9k

Under Construction 81.8k 5.0k

Grade A Average Asking

Rent (/sqm/mo.)$30.27 $28.46

0%

5%

10%

15%

20%

25%

30%

35%

40%

2010 2011 2012 2013 2014 2015 2016

HANOI OFFICE

Historical Average = 22%

$10

$20

$30

$40

$50

-5,000

0

5,000

10,000

15,000

20,000

25,000

2010 2011 2012 2013 2014 2015 2016

Net Absorption, SQ.M Asking Rent, $ PSQ.M

Office Snapshot Q1 2016Hanoi, Vietnam

MARKETBEAT

www.cushmanwakefield.com

About Cushman & WakefieldCushman & Wakefield is a global leader in commercial real estate services, helping clients transform the way

people work, shop, and live. The firm’s 43,000 employees in more than 60 countries provide deep local and

global insights that create significant value for occupiers and investors around the world. Cushman & Wakefield

is among the largest commercial real estate services firms in the world with revenues of $5 billion across core

services of agency leasing, asset services, capital markets, facilities services (branded C&W Services), global

occupier services, investment management (branded DTZ Investors), tenant representation and valuations &

advisory. To learn more, visit www.cushmanwakefield.com or follow @Cushwake on Twitter.

Copyright © 2016 Cushman & Wakefield. All rights reserved. The information contained within this report is gathered from mult iple sources considered

to be reliable. The information may contain errors or omissions and is presented without any warranty or representations as to its accuracy.

SUBMARKETTOTAL

BUILDINGS

INVENTORY

(SQM)

VACANT AREA

(SQ.M)

OVERALL

VACANCY RATE (%)

CURRENT NET

ABSORPTION (SQ.M)

UNDER

CONSTRUCTION

(SQ.M)

AVERAGE ASKING

RENT (US$/SQ.M/MO.)

US$

SF/YR

EURO

SF/YR

CBD – Grade A 10 118,000 8,470 7.2 2,130 5,000 34.02 37.93 33.68

CBD – Grade B 15 113,400 8,290 7.3 (530) 0 26.36 29.38 26.09

CBD Totals 25 231,360 16,760 7.2 1,600 5,000 30.27 33.74 29.96

Non-CBD – Grade A 3 108,300 60,590 55.9 14,320 0 29.63 33.03 29.33

Non-CBD – Grade B 36 443,560 41,500 9.4 5,420 94,700 16.65 18.56 16.48

Non-CBD Totals 39 551,870 102,100 18.5 19,740 94,700 19.20 21.40 19.00

West – Grade A 4 174,600 36,950 21.2 (3,600) 0 23.97 26.73 23.74

West – Grade B 16 227,400 24,560 10.8 9,010 115,800 17.10 19.07 16.93

West Totals 20 402,100 61,500 15.3 5,400 115,800 20.09 22.39 19.88

HANOI TOTALS 84 1,185,000 180,380 15.2 26,760 215,500 21.66 24.15 21.45

Key Lease Transactions Q1 2016

PROPERTY SQ.M TENANT TRANSACTION TYPE SUBMARKET

Keangnam Hanoi Landmark Tower 2,500 Huawei Relocation West

Sun Red River Building 1,300 ThyssenKrupp Real Estate Relocation CBD

Lotte Center Hanoi 420 Oracle Relocation CBD

Hong Ha Center 400 HIS Relocation CBD

Phuoc VoDirector

Valuations & Research

Room 16, Level 14, Vincom Centre

72 Le Thanh Ton, District 1, HCMC

Tel: +84 8 3823 7968

Fax: +84 8 3823 7969

SUMMARY BY GRADETOTAL

BUILDINGS

INVENTORY

(SQ.M)

DIRECT VACANT

(SQ.M)

VACANCY RATE

(%)

CURRENT NET

ABSORPTION

(SQ.M)

YTD NET

ABSORPTION

(SQ.M)

UNDER CNSTR

(SQ.M)

AVERAGE ASKING

RENT OVERALL

(US$/SQ.M/MO.)

AVERAGE ASKING

RENT DIRECT

(US$/SQ.M/MO.)

Grade A 17 400,950 106,000 26.4 12,850 12,850 5,000 28.46 28.46

Grade B 64 784,370 74,360 9.5 13,900 13,900 210,500 18.18 18.18

*Rental rates reflect gross asking $psq.m/year

Significant Projects Under Construction Q1 2016

PROPERTY SUBMARKET SQ.M COMPLETION DATE STATUS

UDIC Complex West14,500 2016 Fitting out

MD Complex West18,500 2016 Fitting out

Thang Long Garden Tower West37,500 2016 Under construction

Vicem Tower West37,800 2016 Under construction

Retail Snapshot Q1 2016Hanoi, Vietnam

MARKETBEAT

Economic Indicators

Market Indicators

Net Absorption/Asking Rent

Overall Vacancy

www.cushmanwakefield.com

EconomyHaving achieved an impressive growth rate in 2015, the government

set a more optimistic GDP growth target of 6.7% and CPI at below

5% in 2016. As of February 2016, total inward FDI into Vietnam

reached US$2.80 billion (both newly registered and adjusted), up

135% year-on-year; while implemented FDI was estimated to have

reached US$1.5 billion, up 15.4% year-on-year. The manufacturing

and processing industry, which accounted for 71.2% of total

registered capital, attracted the largest share. Singapore was the

leading investor with newly registered FDI in the first two months,

accounting for 23% of total investment.

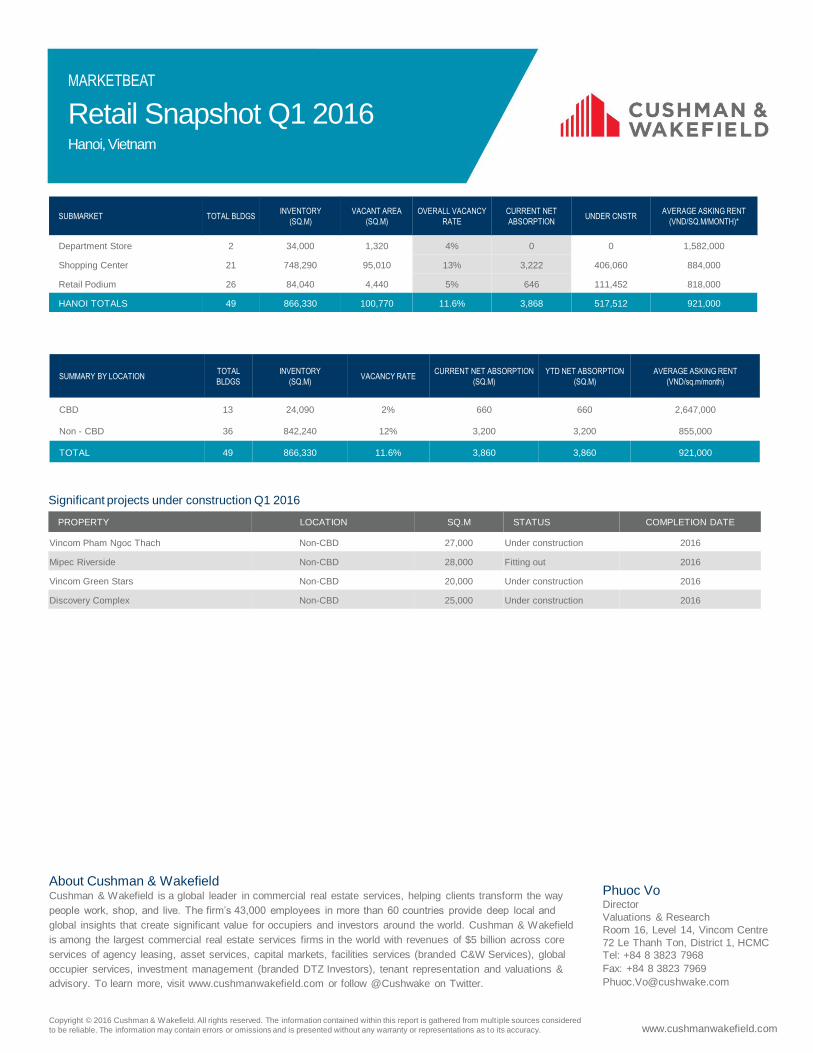

Market OverviewWith no new retail centres entering the market in the first

quarter of 2016, overall supply remained stable quarter-on-quarter

but still higher by 23% year-on-year, at over 866,300 square meters

(sq.m.) of retail space from 49 projects. Non-CBD supply dominated

the market, accounting for nearly 97% of the market as land

available for development in the CBD remains limited.

The overall market performance continued to experience

gradual improvement, with vacancy rate down by 6 percentage

points year-on-year but unchanged on a quarterly basis at nearly

12% in first quarter 2016. There was an improvement in the CBD on

both a quarterly and yearly basis, with vacancy rate down 3

percentage points quarter-on-quarter and 1 percentage point year-

on-year to 2%, while Non-CBD reached 12%, down by 6% year-on-

year but remained unchanged on a quarterly basis.

The overall average asking rent saw a moderate decrease by nearly

1% quarter-on-quarter, but went up by 8.3% year-on-year, mostly

due to the high rents offered by new projects, reaching VND905,000

per square meter per month (/sq.m./mo) or US$40.6/sq.m./mo. In

terms of rent by location, the average rent in the CBD recorded at

VND2,647,000/sq.m./mo (US$118.7/sq.m./mo), triple those in the

Non-CBD. Average rents in both locations remained stable on a

quarterly basis, but down 6% and up 11% year-on-year,

respectively.

OutlookOver 175,000 sq.m. of new supply is expected to be completed in

2016, of which nearly 30% of the total stock will comprise the two

Vincom shopping centres in Cau Giay and Dong Da. No additional

retail space in CBD is expected to be completed in 2016. A large

number of projects will also be concentrated in the Western area of

Hanoi. With WTO commitments, FTA participation and the signing of

TPP, the number of retailers into Vietnam is expected to rise in the

future and consequently, intensify competition between domestic

and foreign retailers.

2 months 2015 2 months 201612-Month

Forecast

CPI (%) 0.64 1.03

Inward FDI (billion US$) 1.19 2.80

Trade balance

(billion US$)(0.61) 0.86

Q1 15 Q1 1612-Month

Forecast

Overall Vacancy 18% 11.6%

Net Absorption (10,716) 3,866

Overall Average Asking

Rent (VND/sq.m/month)807,000 905,000

0%

10%

20%

30%

2010 2012 2014 2016

HANOI RETAIL

Historical Average = 14%

600

800

1,000

1,200

-10,000

10,000

30,000

50,000

70,000

90,000

110,000

130,000

150,000

2010 2011 2012 2013 2014 2015 2016

Net Absorption, SQ.M Asking Rent, thousand VND PSQ.M

(*) Average rent on the ground level is used as a benchmark to represent the rent of each

retail centre. All rents include Service charge and exclude VAT

Retail Snapshot Q1 2016Hanoi, Vietnam

MARKETBEAT

www.cushmanwakefield.com

About Cushman & WakefieldCushman & Wakefield is a global leader in commercial real estate services, helping clients transform the way

people work, shop, and live. The firm’s 43,000 employees in more than 60 countries provide deep local and

global insights that create significant value for occupiers and investors around the world. Cushman & Wakefield

is among the largest commercial real estate services firms in the world with revenues of $5 billion across core

services of agency leasing, asset services, capital markets, facilities services (branded C&W Services), global

occupier services, investment management (branded DTZ Investors), tenant representation and valuations &

advisory. To learn more, visit www.cushmanwakefield.com or follow @Cushwake on Twitter.

Copyright © 2016 Cushman & Wakefield. All rights reserved. The information contained within this report is gathered from mult iple sources considered

to be reliable. The information may contain errors or omissions and is presented without any warranty or representations as to its accuracy.

SUBMARKET TOTAL BLDGSINVENTORY

(SQ.M)

VACANT AREA

(SQ.M)

OVERALL VACANCY

RATE

CURRENT NET

ABSORPTIONUNDER CNSTR

AVERAGE ASKING RENT

(VND/SQ.M/MONTH)*

Department Store 2 34,000 1,320 4% 0 0 1,582,000

Shopping Center 21 748,290 95,010 13% 3,222 406,060 884,000

Retail Podium 26 84,040 4,440 5% 646 111,452 818,000

HANOI TOTALS 49 866,330 100,770 11.6% 3,868 517,512 921,000

Significant projects under construction Q1 2016

PROPERTY LOCATION SQ.M STATUS COMPLETION DATE

Vincom Pham Ngoc Thach Non-CBD 27,000 Under construction 2016

Mipec Riverside Non-CBD 28,000 Fitting out 2016

Vincom Green Stars Non-CBD 20,000 Under construction 2016

Discovery Complex Non-CBD 25,000 Under construction 2016

SUMMARY BY LOCATIONTOTAL

BLDGS

INVENTORY

(SQ.M)VACANCY RATE

CURRENT NET ABSORPTION

(SQ.M)

YTD NET ABSORPTION

(SQ.M)

AVERAGE ASKING RENT

(VND/sq.m/month)

CBD 13 24,090 2% 660 660 2,647,000

Non - CBD 36 842,240 12% 3,200 3,200 855,000

TOTAL 49 866,330 11.6% 3,860 3,860 921,000

Phuoc VoDirector

Valuations & Research

Room 16, Level 14, Vincom Centre

72 Le Thanh Ton, District 1, HCMC

Tel: +84 8 3823 7968

Fax: +84 8 3823 7969

Industrial Snapshot Q1 2016Hanoi, Vietnam

MARKETBEAT

Economic Indicators

Market Indicators

Net Absorption/Asking Rent

Overall Vacancy

www.cushmanwakefield.com

EconomyHaving achieved an impressive growth rate in 2015, the government

set a more optimistic GDP growth target of 6.7% and CPI at below 5%

in 2016. As of February 2016, total inward FDI into Vietnam reached

US$2.80 billion (both newly registered and adjusted), up 135% year-

on-year; while implemented FDI was estimated to have reached

US$1.5 billion, up 15.4% year-on-year. The manufacturing and

processing industry, which accounted for 71.2% of total registered

capital, attracted the largest share. Singapore was the leading investor

with newly registered FDI in the first two months, accounting for 23%

of total investment.

Market OverviewThere was no change in the supply of industrial parks (IPs) in

first quarter 2016. Total net leasable area supplied by 11 IPs in Hanoi

remained the same at more than 1,420 hectares, constituting around

78% of gross land area. Total available land for lease at the end of the

first quarter was 395 hectares, accounting for approximately 28% of

total supply. RBFs were not popular in Hanoi’s IPs.

The overall market performance continued to experience gradual

improvement, with the average occupancy reaching well over 72% in

first quarter 2016, up 2 percentage points year-on-year. Seven out of

11 IPs (54% of the total stock) were fully occupied. Among the

remaining IPs that still had vacant area at the end of this quarter, Hoa

Lac Hi-tech Park recorded the highest vacancy rate (70%) with 346

hectares land available for lease.

The average asking rent of IPs in Hanoi continued to be the

highest compared to all other cities/provinces in the northern region of

Vietnam (about 50% higher than that of Hai Phong and Bac Ninh),

standing at VND2,475,000 per square meter per term (/sq.m./term),

equivalent to US$111/sq.m./term in first quarter 2016, slightly down

1% quarter-on-quarter but still up 12% year-on-year. Management

fees for these IPs averaged at VND9,650/sq.m./month

(US$0.43/sq.m/month) [check if this is in term or month]. Nam Thang

Long Industrial Park offered the highest rent at nearly

VND4,171,000/sq.m./term (US$187/sq.m./term).

* ALL RENTS ARE ASKING RENTS AND VAT EXCLUDED

OutlookAn additional supply of about 6,000 hectares from 14 identified IP

projects is expected to enter the market from now through 2020, which

is equivalent to 400% of current supply. By 2030 with vision to 2050,

Hanoi will have 33 IPs with an area of 8,000 hectares in total. With

labor costs increasing in China, foreign investment in IPs is expected

to grow continually in the medium to long term as manufacturing

companies shift their operations to Vietnam, particularly when the

country has entered into FTAs, AEC and TPP.

2 months 15 2 months 1612-Month

Forecast

CPI (%) 0.64 1.03

Inward FDI (billion US$) 1.19 2.80

Trade balance

(billion US$)(0.61) 0.86

Q1 15 Q1 1612-Month

Forecast

Overall Vacancy 29.6% 27.8%

Net Absorption 0 ha 2.5 ha

Under Construction 0 340

Average Asking Rent

(VND/sq.m/term)2,212,000 2,475,000

20%

25%

30%

35%

40%

2012 2014

HANOI INDUSTRIAL PARK

Historical Average = 31%

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

-15

-10

-5

0

5

10

15

20

25

30

35

2012 2013 2014 2015 2016

Net Absorption, ha Asking Rent, VND PSQ.M

Industrial Snapshot Q1 2016Hanoi, Vietnam

MARKETBEAT

www.cushmanwakefield.comCopyright © 2016 Cushman & Wakefield. All rights reserved. The information contained within this report is gathered from mult iple sources considered

to be reliable. The information may contain errors or omissions and is presented without any warranty or representations as to its accuracy.

About Cushman & WakefieldCushman & Wakefield is a global leader in commercial real estate services, helping clients transform the way

people work, shop, and live. The firm’s 43,000 employees in more than 60 countries provide deep local and

global insights that create significant value for occupiers and investors around the world. Cushman & Wakefield

is among the largest commercial real estate services firms in the world with revenues of $5 billion across core

services of agency leasing, asset services, capital markets, facilities services (branded C&W Services), global

occupier services, investment management (branded DTZ Investors), tenant representation and valuations &

advisory. To learn more, visit www.cushmanwakefield.com or follow @Cushwake on Twitter.

SUBMARKET TOTAL IPs INVENTORY (ha)YTD LEASING ACTIVITY

(ha)

OVERALL VACANCY

RATE

YTD NET OVERALL

ABSORPTION (ha)

UNDER

CONSTRUCTION (ha)NET RENT

(VND/SQ.M/TERM)

Chuong My 1 111 81 27% 0 0 2,341,000

Dong Anh 1 206 206 0% 0 0 2,676,000

Gia Lam 1 78 78 0% 0 0 3,790,000

Long Bien 1 32 32 0% 0 0 3,568,000

Me Linh 1 240 240 0% 0 0 3,568,000

Thach That & Quoc Oai 2 619 270 56% 2.5 0 1,606,000

Tu Liem 1 24 24 0% 0 0 4,171,000

Soc Son 3 114 95 17% 0 340 3,083,000

HANOI TOTALS 11 1423 1028 28% 2.5 340 2,475,000

Significant Future Projects

PROJECT NAME AREA (ha) DISTRICT STATUS

Soc Son Clean IP 340 Soc Son Under construction

North Thuong Tin 430 Thuong Tin Site clearance

Quang Minh II 266 Me Linh Site clearance

Dong Anh IP 300 Dong Anh Planning

Thanh My – Xuan Son 100 Son Tay Planning

Phuoc VoDirector

Valuations & Research

Room 16, Level 14, Vincom Centre

72 Le Thanh Ton, District 1, HCMC

Tel: +84 8 3823 7968

Fax: +84 8 3823 7969

Residential Snapshot Q1 2016Hanoi, Vietnam

MARKETBEAT

Economic Indicators

Market Indicators

Primary Market Performance

Asking Prices of All Segments

www.cushmanwakefield.com

Economy

Having achieved an impressive growth rate in 2015, the government

set a more optimistic GDP growth target of 6.7% and CPI at below 5%

in 2016. As of February 2016, total inward FDI into Vietnam reached

US$2.80 billion (both newly registered and adjusted), up 135% year-

on-year; while implemented FDI was estimated to have reached

US$1.5 billion, up 15.4% year-on-year. The manufacturing and

processing industry, which accounted for 71.2% of total registered

capital, attracted the largest share. Singapore was the leading investor

with newly registered FDI in the first two months, accounting for 23% of

total investment.

Market Overview

The first quarter of 2016 continued to see positive market momentum,

reflected by strong launches across all Grades from both 24 new and

active projects, with nearly 6,200 units launched. Grade B dominated

the market with 68% of marketshare, followed by Grade C (30%) and

Grade A (2%). The total primary supply in this quarter reached over

14,700 units.

Transaction volume of all Grades fell 19% quarter-on-quarter due to

the long Tet holiday but remained stable year-on-year; 74% of sold

units were Grade B, followed by Grade C with 26%. Several Grade B

projects registered impressive sales rate including Time City Phase II,

Imperia Garden and Vinhomes Gardenia. Thanh Xuan District had the

highest share of over 25% of total sales volume this quarter.

Average price saw a significant increase on both a quarterly and yearly

basis, by 6% quarter-on-quarter and 16% year-on-year, reaching

VND28 million per square meter (/sq.m.) or US$1,250/sq.m. Grade A,

with limited remaining stock, saw a marked decrease on both quarterly

and yearly basis of nearly 10% quarter-on-quarter and 22% year-on-

year due to price adjustment from one project, attaining VND47

million/sq.m. (US$2,087/sq.m.). The average price for Grade B stood

at VND32 million/sq.m. (US$1,400/sq.m.), up nearly 3% quarter-on-

quarter but down 6% year-on-year. Price of Grade C increased to

VND18.5 million/sq.m. (US$820/sq.m.), up nearly 8% quarter-on-

quarter and 10% year-on-year.

* ALL PRICES ARE VAT EXCLUDED

Outlook

Market sentiment is expected to remain positive in 2016, in terms of

both the number of newly launched projects and sale performance as

developers’ credibility improves with substantial support from banks

and policies in favor of buyers. The Western area is expected to see

the highest supply of apartments in 2016. The mid to low-end

segments will continue to dominate due to its liquidity. Care needs to

be exercised to prevent excessive speculation from distorting the

market.

2 months 15 2 months 1612-Month

Forecast

CPI (%) 0.64 1.03

Inward FDI (billion US$) 1.19 2.80

Trade balance

(billion US$)(0.61) 0.86

Q1 15 Q1 1612-Month

Forecast

Primary supply 16,200 14,200

Net Absorption 35% 41%

Overall Average Asking

Price (mil. VND/sq.m)24 28.1

0

10,000,000

20,000,000

30,000,000

40,000,000

50,000,000

60,000,000

70,000,000

80,000,000

Grade A Grade B Grade C

Lowest asking price (VND/sq.m) Highest asking price (VND/sq.m)

HANOI APARTMENT

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

Grade A Grade B Grade C

Primary stock Sold units

Residential Snapshot Q1 2016Hanoi, Vietnam

MARKETBEAT

www.cushmanwakefield.com

About Cushman & WakefieldCushman & Wakefield is a global leader in commercial real estate services, helping clients transform the way

people work, shop, and live. The firm’s 43,000 employees in more than 60 countries provide deep local and

global insights that create significant value for occupiers and investors around the world. Cushman & Wakefield

is among the largest commercial real estate services firms in the world with revenues of $5 billion across core

services of agency leasing, asset services, capital markets, facilities services (branded C&W Services), global

occupier services, investment management (branded DTZ Investors), tenant representation and valuations &

advisory. To learn more, visit www.cushmanwakefield.com or follow @Cushwake on Twitter.

Copyright © 2016 Cushman & Wakefield. All rights reserved. The information contained within this report is gathered from mult iple sources considered

to be reliable. The information may contain errors or omissions and is presented without any warranty or representations as to its accuracy.

Key launched projects Q1 2016

PROPERTY MARKET APPROACH DISTRICT GRADE NO. UNITS LAUNCHED

Park Hill Premium (T12) New launch Hai Ba Trung B 682

Goldmark Sapphire (2,4) Added Tu Liem B 346

Ecogreen City Added Tu Liem B 377

VOV Me Tri (CT2E) Added Tu Liem B 110

Comatce New launch Thanh Xuan B 30

Vinhomes Gardenia New launch Tu Liem B 1164

Gold Season New launch Thanh Xuan B 320

B1, B2 CT2 Linh Dam New launch Hoang Mai C 112

Gemek Premium Added Ha Dong C 576

The Golden An Khanh (32T) Added Hoai Duc C 286

Star Tower Added Thanh Xuan C 156

Him Lam Thach Ban New launch Long Bien C 187

Key future projects

PROPERTY LOCATION EST. TOTAL UNITS STATUS COMPLETION YEAR

FLC Twin Tower Cau Giay 486 Foundation 2017

D'Le Roi Soleil Tay Ho 948 Foundation 2017

Legend Tower Thanh Xuan 460 Under construction 2017

Goldmark city - Phase 2 Tu Liem 2,680 Under construction 2017

Phuoc Vo Director

Valuations & Research

Room 16, Level 14, Vincom Centre

72 Le Thanh Ton, District 1, HCMC

Tel: +84 8 3823 7968

Fax: +84 8 3823 7969

SUMMARY BY GRADE TOTAL PROJECTS INVENTORY NET ABSORPTIONAVERAGE PRICE LEVEL*

(mil VND/SQM)

Grade A 4 270 6% 47

Grade B 38 9,600 44% 31.9

Grade C 35 4,300 45% 18.7

TOTAL 76 14,710 41% 28.1

MARKETBEAT

Serviced Apartment Snapshot

Q1 2016Hanoi, Vietnam

Economic Indicators

Market Indicators

Net Absorption/Asking Rent

Overall Vacancy

www.cushmanwakefield.com

Economy

Having achieved an impressive growth rate in 2015, the

government set a more optimistic GDP growth target of 6.7% and

CPI at below 5% in 2016. As of February 2016, total inward FDI

into Vietnam reached US$2.80 billion (both newly registered and

adjusted), up 135% year-on-year; while implemented FDI was

estimated to have reached US$1.5 billion, up 15.4% year-on-year.

The manufacturing and processing industry, which accounted for

71.2% of total registered capital, attracted the largest share.

Singapore was the leading investor with newly registered FDI in

the first two months, accounting for 23% of total investment.

Market Overview

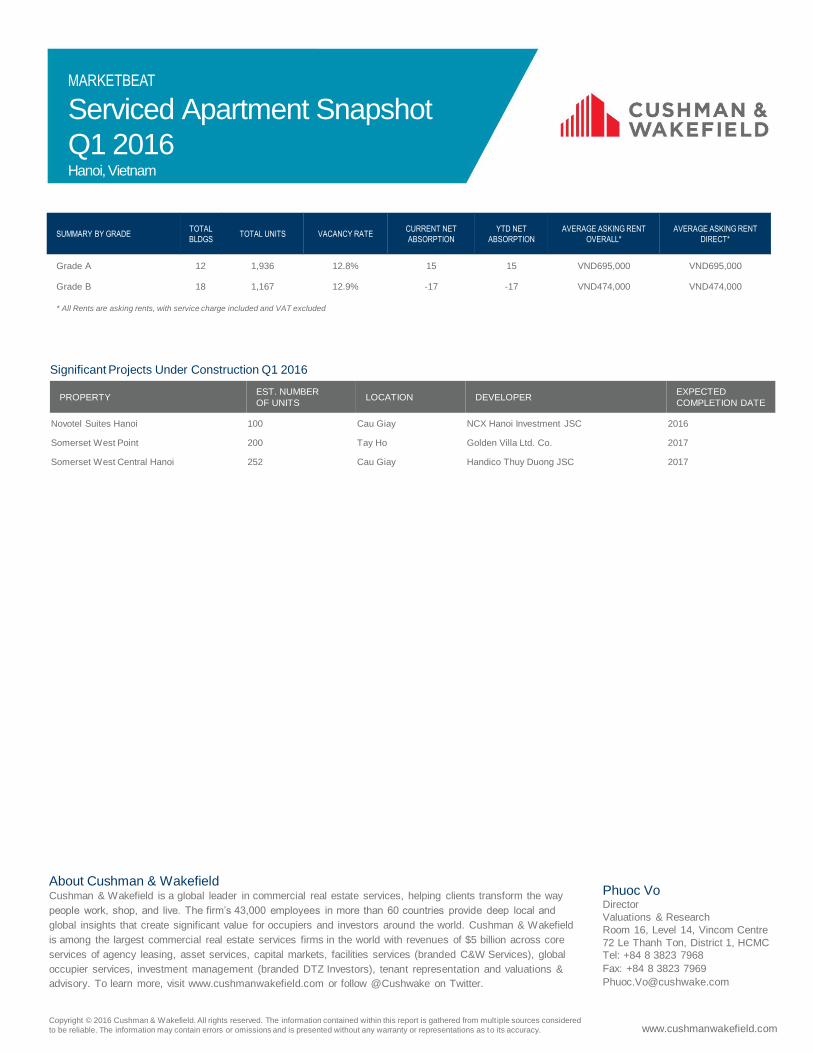

No new project entered Hanoi’s serviced apartment market in

first quarter 2016. Overall, there are 12 Grade A projects and 19

Grade B projects supplying a total of 3,100 units. Grade A still

takes up the larger share of total stock with nearly 1,940 units

(62%). Serviced apartments are mainly located in Ba Dinh and

Tay Ho Districts, accounting for 30% and 29% of the total supply

respectively. There are a few international operators present in

Hanoi with mainly Grade A projects such as IHG, Ascott Group,

Fraser and Keppel Land Hospitality

Overall market performance showed significant improvement

year-on-year, up 7 percentage points but remaining stable

quarter-on-quarter, with average occupancy reaching 87% in the

first quarter of 2016. Specifically, occupancy in Grade A reached

87.2%, up by 6 percentage points year-on-year, while that of

Grade B improved by 10 percentage points to 87.1%.

Overall average rent showed a slight decrease on both a

quarterly and yearly basis, by 2%, to VND612,000 per square

meter per month (/sq.m./month) or US$27.4/sq.m./mo. Asking

rent of Grade A averaged at VND695,000/sq.m./mo

(US$31.2/sq.m./mo), down 2% both on a quarterly and yearly

basis, while that of Grade B was down 2% quarter-on-quarter and

3% year-on-year to VND474,000/sq.m./mo (US$21.2/sq.m./mo).

* ALL RENTS ARE ASKING RENTS, WITH SERVICE CHARGE INCLUDED AND VAT EXCLUDED

Outlook

In 2016, Hanoi’s serviced apartment market is likely to welcome

only one new project, namely Novotel Suites Hanoi in Cau Giay

district with 100 units. This will be the first project of this brand in

Hanoi. The market will experience more competition from future

Grade A buy-to-let apartments besides the current over-supply

status. Therefore, the asking rents are expected to remain stable

or slightly decrease in order to maintain occupancy.

2 months 15 2 months 1612-Month

Forecast

CPI (%) 0.64 1.03

Inward FDI (billion US$) 1.19 2.80

Trade balance

(billion US$)(0.61) 0.86

Q1 15 Q1 1612-Month

Forecast

Grade A Vacancy 18.5% 12.8%

Grade A Average Rent VND708,000 VND695,000

Grade B Vacancy 22.9% 12.9%

Grade B Average Rent VND490,000 VND474,000

5%

10%

15%

20%

25%

2011 2012 2013 2014 2015 2016

HANOI SERVICED APARTMENT

Historical Average = 16%

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

-60

-40

-20

0

20

40

60

80

100

120

140

160

2011 2012 2013 2014 2015 2016

Net Absorption, SQ.M Asking Rent, VND PSQ.M

Serviced Apartment Snapshot

Q1 2016Hanoi, Vietnam

MARKETBEAT

www.cushmanwakefield.com

About Cushman & WakefieldCushman & Wakefield is a global leader in commercial real estate services, helping clients transform the way

people work, shop, and live. The firm’s 43,000 employees in more than 60 countries provide deep local and

global insights that create significant value for occupiers and investors around the world. Cushman & Wakefield

is among the largest commercial real estate services firms in the world with revenues of $5 billion across core

services of agency leasing, asset services, capital markets, facilities services (branded C&W Services), global

occupier services, investment management (branded DTZ Investors), tenant representation and valuations &

advisory. To learn more, visit www.cushmanwakefield.com or follow @Cushwake on Twitter.

Copyright © 2016 Cushman & Wakefield. All rights reserved. The information contained within this report is gathered from mult iple sources considered

to be reliable. The information may contain errors or omissions and is presented without any warranty or representations as to its accuracy.

Significant Projects Under Construction Q1 2016

PROPERTYEST. NUMBER

OF UNITSLOCATION DEVELOPER

EXPECTED

COMPLETION DATE

Novotel Suites Hanoi 100 Cau Giay NCX Hanoi Investment JSC 2016

Somerset West Point 200 Tay Ho Golden Villa Ltd. Co. 2017

Somerset West Central Hanoi 252 Cau Giay Handico Thuy Duong JSC 2017

Phuoc VoDirector

Valuations & Research

Room 16, Level 14, Vincom Centre

72 Le Thanh Ton, District 1, HCMC

Tel: +84 8 3823 7968

Fax: +84 8 3823 7969

SUMMARY BY GRADETOTAL

BLDGSTOTAL UNITS VACANCY RATE

CURRENT NET

ABSORPTION

YTD NET

ABSORPTION

AVERAGE ASKING RENT

OVERALL*

AVERAGE ASKING RENT

DIRECT*

Grade A 12 1,936 12.8% 15 15 VND695,000 VND695,000

Grade B 18 1,167 12.9% -17 -17 VND474,000 VND474,000

* All Rents are asking rents, with service charge included and VAT excluded

Office Snapshot Q1 2016Ho Chi Minh City, Vietnam

MARKETBEAT

Economic Indicators

Market Indicators

Grade A Net Absorption/Asking Rent

4Q TRAILING AVERAGE

Grade A Overall Vacancy

www.cushmanwakefield.com

Economy

With impressive economic growth in 2015, the Government has set a

more optimistic target of 6.7% in GDP growth and CPI to be well under

control at below 5% in 2016.

As of February 2016, total inward FDI into Vietnam reached

US$2.80 billion (both newly registered and adjusted), up 135% year-

on-year (y-o-y); implemented FDI was estimated to have reached

US$1.5 billion, up 15.4% y-o-y. The manufacturing and processing

industry, which accounted for 71.2% of total registered capital,

attracted the largest share. Singapore was the leading investor with

newly registered FDI in the first 2 months, accounting for 23% of total

investment.

Market Overview

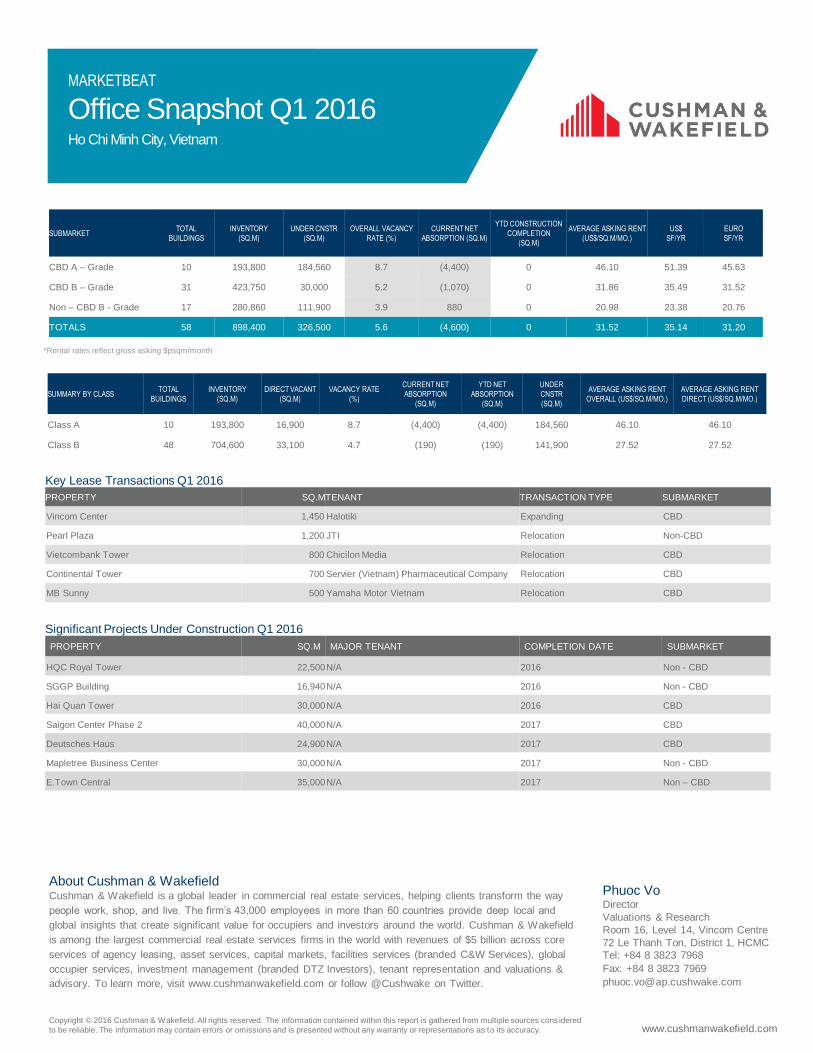

No new office building entered the market in Q1 2016, however,

one Grade B building converted over 3,200 sq.m of space into office for

lease. Currently, there are 10 Grade A and 48 Grade B office buildings,

providing approximately 193,800 square meters (sq.m.) and 704,600

sq.m. of space to the market respectively.

Average occupancy of Grade A saw a moderate decrease by 2

percentage point (ppt) by quarter and remained stable by year, at

91%. As a result, Grade A net absorption was recorded at minus 4,440

sq.m. Grade B occupancy reached 95%, unchanged by quarter but

rose 1 ppt y-o-y, enjoying an unbroken upward trend in the last 11

quarters. Occupancy for non-CBD Grade B buildings remained slightly

higher than those in the CBD over the last seven quarters, reached

96%, whilst those in the CBD achieved 95%.

In terms of rents, the average rents of both grades remained

stable on a quarterly basis, at around VND1,028,000 per square

meter per month (/sq.m./mo), equivalent to US$46.1/sq.m./mo. for

Grade A, and VND613,200/sq.m./mo (US$27.5/sq.m./mo) for Grade B.

However, on a yearly basis, Grade A rent softened by 1% whilst Grade

B remained unchanged. The decrease was mostly due to the lower

rent offered by the new project. The average rent for CBD was 40%

higher than in the non-CBD. 10/12 buildings that recorded an increase

in average rent by year were in the CBD area.

Outlook

Over 51,000 sq.m. of new supply of both grades is expected to be

completed in 2016. Low historical standards as well as a limited supply

of large spaces will keep rents stable with moderate increases likely by

the end of the year. The balance of power is generally still with the

tenants as occupiers continue to look for ways to reduce costs by

renegotiating with their existing landlords or relocating to alternative

more cost-efficient buildings.

2 months 15 2 months 1612-Month

Forecast

CPI (%) 0.64 1.03

Inward FDI (billion US$) 1.19 2.80

Trade balance

(billion US$)(0.61) 0.86

Q1 15 Q1 1612-Month

Forecast

Grade A Overall Vacancy 6.4% 8.7%

Grade A Net Absorption 34.9k (4.4)k

Under Construction 221.6k 184.5k

Grade A Average Asking

Rent$45.94 $46.10

5%

10%

15%

20%

25%

30%

35%

2011 2012 2013 2014 2015 Q1 2016

HCMC OFFICE

Historical Average = 14%

$44

$46

$48

$50

$52

$54

$56

-5,000

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

2011 2012 2013 2014 2015 Q1 2016

Net Absorption, SQM Asking Rent, $ PSQM

Office Snapshot Q1 2016Ho Chi Minh City, Vietnam

MARKETBEAT

www.cushmanwakefield.com

About Cushman & WakefieldCushman & Wakefield is a global leader in commercial real estate services, helping clients transform the way

people work, shop, and live. The firm’s 43,000 employees in more than 60 countries provide deep local and

global insights that create significant value for occupiers and investors around the world. Cushman & Wakefield

is among the largest commercial real estate services firms in the world with revenues of $5 billion across core

services of agency leasing, asset services, capital markets, facilities services (branded C&W Services), global

occupier services, investment management (branded DTZ Investors), tenant representation and valuations &

advisory. To learn more, visit www.cushmanwakefield.com or follow @Cushwake on Twitter.

Copyright © 2016 Cushman & Wakefield. All rights reserved. The information contained within this report is gathered from multiple sources cons idered

to be reliable. The information may contain errors or omissions and is presented without any warranty or representations as to its accuracy.

SUBMARKETTOTAL

BUILDINGS

INVENTORY

(SQ.M)

UNDER CNSTR

(SQ.M)

OVERALL VACANCY

RATE (%)

CURRENT NET

ABSORPTION (SQ.M)

YTD CONSTRUCTION

COMPLETION

(SQ.M)

AVERAGE ASKING RENT

(US$/SQ.M/MO.)

US$

SF/YR

EURO

SF/YR

CBD A – Grade 10 193,800 184,560 8.7 (4,400) 0 46.10 51.39 45.63

CBD B – Grade 31 423,750 30,000 5.2 (1,070) 0 31.86 35.49 31.52

Non – CBD B - Grade 17 280,860 111,900 3.9 880 0 20.98 23.38 20.76

TOTALS 58 898,400 326,500 5.6 (4,600) 0 31.52 35.14 31.20

Key Lease Transactions Q1 2016

PROPERTY SQ.MTENANT TRANSACTION TYPE SUBMARKET

Vincom Center 1,450 Halotiki Expanding CBD

Pearl Plaza 1,200 JTI Relocation Non-CBD

Vietcombank Tower 800 Chicilon Media Relocation CBD

Continental Tower 700 Servier (Vietnam) Pharmaceutical Company Relocation CBD

MB Sunny 500 Yamaha Motor Vietnam Relocation CBD

Significant Projects Under Construction Q1 2016

PROPERTY SQ.M MAJOR TENANT COMPLETION DATE SUBMARKET

HQC Royal Tower 22,500N/A 2016 Non - CBD

SGGP Building 16,940N/A 2016 Non - CBD

Hai Quan Tower 30,000N/A 2016 CBD

Saigon Center Phase 2 40,000N/A 2017 CBD

Deutsches Haus 24,900N/A 2017 CBD

Mapletree Business Center 30,000N/A 2017 Non - CBD

E.Town Central 35,000N/A 2017 Non – CBD

Phuoc VoDirector

Valuations & Research

Room 16, Level 14, Vincom Centre

72 Le Thanh Ton, District 1, HCMC

Tel: +84 8 3823 7968

Fax: +84 8 3823 7969

SUMMARY BY CLASSTOTAL

BUILDINGS

INVENTORY

(SQ.M)

DIRECT VACANT

(SQ.M)

VACANCY RATE

(%)

CURRENT NET

ABSORPTION

(SQ.M)

YTD NET

ABSORPTION

(SQ.M)

UNDER

CNSTR

(SQ.M)

AVERAGE ASKING RENT

OVERALL (US$/SQ.M/MO.)

AVERAGE ASKING RENT

DIRECT (US$/SQ.M/MO.)

Class A 10 193,800 16,900 8.7 (4,400) (4,400) 184,560 46.10 46.10

Class B 48 704,600 33,100 4.7 (190) (190) 141,900 27.52 27.52

*Rental rates reflect gross asking $psqm/month

MARKETBEAT

Retail Snapshot Q1 2016Ho Chi Minh City, Vietnam

Economic Indicators

Market Indicators

Net Absorption/Asking Rent

4Q TRAILING AVERAGE

Overall Vacancy

www.cushmanwakefield.com

EconomyHaving achieved an impressive growth rate in 2015, the government set a

more optimistic GDP growth target of 6.7% and CPI at below 5% in 2016.

As of February 2016, total inward FDI into Vietnam reached US$2.80

billion (both newly registered and adjusted), up 135% year-on-year; while

implemented FDI was estimated to have reached US$1.5 billion, up

15.4% year-on-year. The manufacturing and processing industry, which

accounted for 71.2% of total registered capital, attracted the largest

share. Singapore was the leading investor with newly registered FDI in

the first two months, accounting for 23% of total investment.

Market Overview

Two shopping centres, namely Vincom Plaza Go Vap and Vincom

Plaza Le Van Viet, were completed in the first quarter of 2016 adding

more than 44,000 square meters (sq.m.) of retail space to the market.

This resulted in a net increase of total stock by 4% quarter-on-quarter

and 22% year-on-year. Currently, there are 131 retail centres in the city

with a total area of approximately 1.10 million sq.m. District 1 remains the

most concentrated retail market in the city, accounting for more than 16%

of total supply.

Overall occupancy remained stable on a quarterly basis, but was up

1 percentage point year-on-year, to 92%. The two aforementioned new

completions achieved a high occupancy rate at above 80%. The recent

trend of high profile investments from retailing giants into Non-CBD

areas, establishing large shopping centres and offering aggressive rents,

has paid off with a higher occupancy rate at 93%. This is in contrast to

the CBD, which saw occupancies remaining unchanged quarter-on-

quarter, but down 5 percentage points year-on-year to 86%, due mainly

to the partial renovation of a big shopping centre in District 1.

Average rents continued to trend downwards on both a quarterly and

yearly basis, downed 3% quarter-on-quarter and 6%year-on-year to

VND1.26 million per square meter per month (/sq.m./mo), or

US$56.6/sq.m./mo. due to lower rents at the new projects. All new

projects over the last four quarters were in the non-CBD area. Rents in

the CBD remained stable on a quarterly basis, but fell moderately by 1%

year-on-year, to VND2.37 million/sq.m./mo (US$105/sq.m./mo.). This is

2.5 times higher than in the secondary area and triple those in the

suburban area.

Outlook

Over 150,000 sq.m. of new supply is expected to enter the market by

2016. While demand for CBD retail space is expected to remain high,

limited land for development means that significant future projects will

mainly be located in the non-CBD areas. These will mostly be in the

south and west where much of the infrastructure and residential

developments have been established. Easing tariffs under the TPP,

together with the further liberalization of the retail sector under the

provisions of the WTO, is expected to enhance Vietnam's potential to

international retailers.

2 months 15 2 months 1612-Month

Forecast

CPI (%) 0.64 1.03

Inward FDI (billion US$) 1.19 2.80

Trade balance

(billion US$)(0.61) 0.86

Q1 15 Q1 1612-Month

Forecast

Overall Vacancy 9.3% 8.4%

Net Absorption 22.0k sq.m 36.1k sq.m

Average Asking Rent

(per sq.m. per month)VND1,297k VND1,261k

0%

5%

10%

15%

20%

2011 2012 2013 2014 2015 2016

HCMC OFFICE

Historical Average = 13%

1,000,000

1,100,000

1,200,000

1,300,000

1,400,000

1,500,000

1,600,000

-10,000

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

2011 2012 2013 2014 2015 2016

Net Absorption, SQM Asking Rent, VND PSQM

(*) Average rent on the ground level is used as a benchmark to represent the rent of each retail

centre. All rents include Service charge and exclude VAT

MARKETBEAT

Retail Snapshot Q1 2016Ho Chi Minh City, Vietnam

www.cushmanwakefield.com

About Cushman & WakefieldCushman & Wakefield is a global leader in commercial real estate services, helping clients transform the way

people work, shop, and live. The firm’s 43,000 employees in more than 60 countries provide deep local and

global insights that create significant value for occupiers and investors around the world. Cushman & Wakefield

is among the largest commercial real estate services firms in the world with revenues of $5 billion across core

services of agency leasing, asset services, capital markets, facilities services (branded C&W Services), global

occupier services, investment management (branded DTZ Investors), tenant representation and valuations &

advisory. To learn more, visit www.cushmanwakefield.com or follow @Cushwake on Twitter.

Copyright © 2016 Cushman & Wakefield. All rights reserved. The information contained within this report is gathered from multiple sources cons idered

to be reliable. The information may contain errors or omissions and is presented without any warranty or representations as to its accuracy.

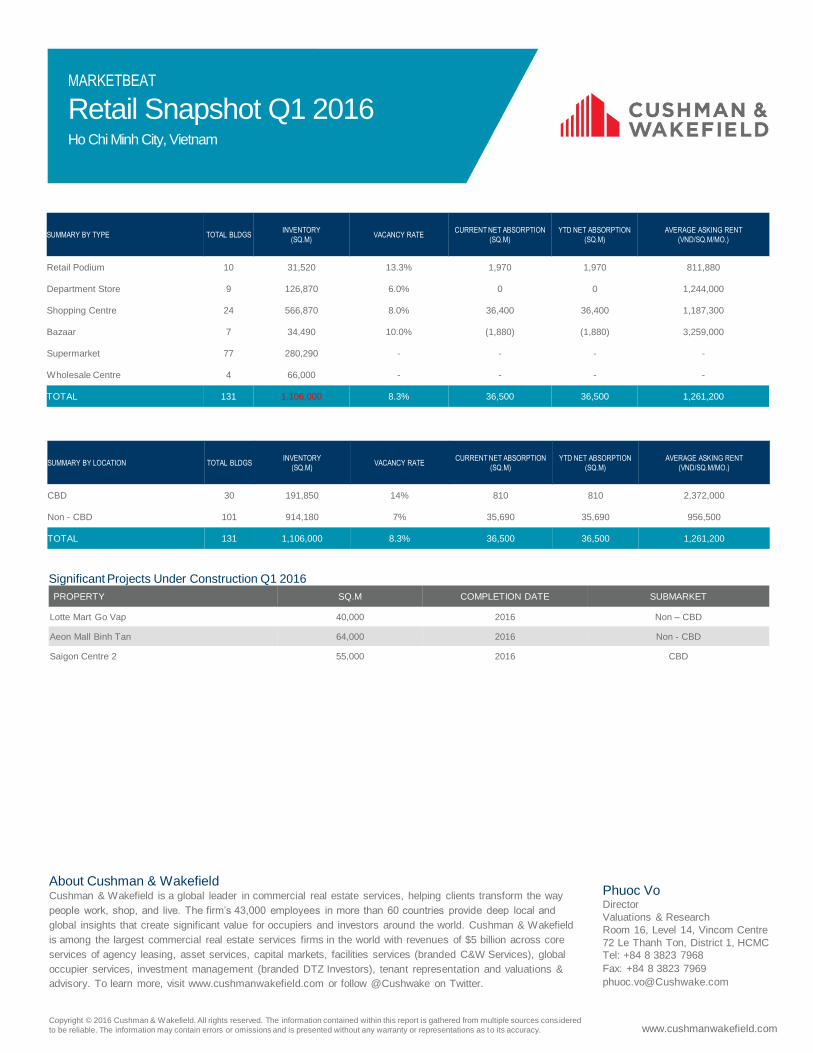

Significant Projects Under Construction Q1 2016

PROPERTY SQ.M COMPLETION DATE SUBMARKET

Lotte Mart Go Vap 40,000 2016 Non – CBD

Aeon Mall Binh Tan 64,000 2016 Non - CBD

Saigon Centre 2 55,000 2016 CBD

Phuoc VoDirector

Valuations & Research

Room 16, Level 14, Vincom Centre

72 Le Thanh Ton, District 1, HCMC

Tel: +84 8 3823 7968

Fax: +84 8 3823 7969

SUMMARY BY TYPE TOTAL BLDGSINVENTORY

(SQ.M)VACANCY RATE

CURRENT NET ABSORPTION

(SQ.M)

YTD NET ABSORPTION

(SQ.M)

AVERAGE ASKING RENT

(VND/SQ.M/MO.)

Retail Podium 10 31,520 13.3% 1,970 1,970 811,880

Department Store 9 126,870 6.0% 0 0 1,244,000

Shopping Centre 24 566,870 8.0% 36,400 36,400 1,187,300

Bazaar 7 34,490 10.0% (1,880) (1,880) 3,259,000

Supermarket 77 280,290 - - - -

Wholesale Centre 4 66,000 - - - -

TOTAL 131 1,106,000 8.3% 36,500 36,500 1,261,200

SUMMARY BY LOCATION TOTAL BLDGSINVENTORY

(SQ.M)VACANCY RATE

CURRENT NET ABSORPTION

(SQ.M)

YTD NET ABSORPTION

(SQ.M)

AVERAGE ASKING RENT

(VND/SQ.M/MO.)

CBD 30 191,850 14% 810 810 2,372,000

Non - CBD 101 914,180 7% 35,690 35,690 956,500

TOTAL 131 1,106,000 8.3% 36,500 36,500 1,261,200

Industrial Snapshot Q1 2016Ho Chi Minh City, Vietnam

MARKETBEAT

Economic Indicators

Market Indicators

Net Absorption/Asking Rent

4Q TRAILING AVERAGE

Overall Vacancy

www.cushmanwakefield.com

Economy

Having achieved an impressive growth rate in 2015, the government

set a more optimistic GDP growth target of 6.7% and CPI at below 5%

in 2016. As of February 2016, total inward FDI into Vietnam reached

US$2.80 billion (both newly registered and adjusted), up 135% year-

on-year; while implemented FDI was estimated to have reached

US$1.5 billion, up 15.4% year-on-year. The manufacturing and

processing industry, which accounted for 71.2% of total registered

capital, attracted the largest share. Singapore was the leading

investor with newly registered FDI in the first two months, accounting

for 23% of total investment.

Market Overview

No new supply was delivered during the quarter. Currently, there

are 18 operating IPs covering a total area of nearly 3,630 hectares.

The leasable area is estimated to be about 62% of the total land area,

while the average remaining LUR years is 35.

The performance of the IP market in HCMC remained stable on

both a quarterly and yearly basis with average occupancy rate

increasing moderately by 1 percentage point both on a quarterly and

yearly basis, to 72%. The majority of the established IPs reported

robust occupancy rates of above 90%.

Average asking rents in this quarter stood at approximately

VND2,808,000 per square meter per term (/sq.m./term), equivalent to

US$126/sq.m./term, remaining stable both on a quarterly and yearly

basis. This rent was about two times higher than that in the

neighboring provinces, such as Binh Duong and Dong Nai.

Ready-Built Factory rents for areas of about 2,000–3,000 sq.m.

ranged from US$2.50–US$3.50 per square meter per month.

* ALL RENTS ARE ASKING, EXCLUDING VAT

Outlook

The total increase in industrial land in HCMC up to 2030 is projected

at approximately 3,000 hectares, increasing by some 85% from the

current stock. Twelve new IPs are expected to be added to the 18 that

are currently in operation by 2020. However, the majority of future

projects are still in the clearance and compensation stage;

construction progress is expected to be protracted; and only three of

these projects are in under-construction stage.

With the TPP and other free trade agreements that Vietnam has

participated in recently, coupled with stable economic conditions,

favorable government policies and low labor cost, Vietnam will attract

more investments from foreign manufacturers as they shift their

operations to Vietnam. With demand for industrial land on the rise, this

segment will remain a compelling investment.

2 months 15 2 months 1612-Month

Forecast

CPI (%) 0.64 1.03

Inward FDI (billion US$) 1.19 2.80

Trade balance

(billion US$)(0.61) 0.86

Q1 15 Q1 1612-Month

Forecast

Overall Vacancy 29% 28.1%

Net Absorption 5 ha 17.4 ha

Under Construction 1,000 ha 1,000 ha

Overall Average Asking

Rent (/sqm/term)VND2,696k VND2,808k

20%

25%

30%

35%

40%

2012 2013 2014 2015 2016

HCMC OFFICE

Historical Average = 33%

2,500,000

2,600,000

2,700,000

2,800,000

2,900,000

0

10

20

30

40

50

60

70

80

2012 2013 2014 2015 2016

Net Absorption, ha Asking Rent, VND PSQM

Industrial Snapshot Q1 2016Ho Chi Minh City, Vietnam

MARKETBEAT

www.cushmanwakefield.comCopyright © 2016 Cushman & Wakefield. All rights reserved. The information contained within this report is gathered from multiple sources cons idered

to be reliable. The information may contain errors or omissions and is presented without any warranty or representations as to its accuracy.

About Cushman & WakefieldCushman & Wakefield is a global leader in commercial real estate services, helping clients transform the way

people work, shop, and live. The firm’s 43,000 employees in more than 60 countries provide deep local and

global insights that create significant value for occupiers and investors around the world. Cushman & Wakefield

is among the largest commercial real estate services firms in the world with revenues of $5 billion across core

services of agency leasing, asset services, capital markets, facilities services (branded C&W Services), global

occupier services, investment management (branded DTZ Investors), tenant representation and valuations &

advisory. To learn more, visit www.cushmanwakefield.com or follow @Cushwake on Twitter.

SUBMARKET TOTAL IPsINVENTORY

(HA)

YTD LEASING ACTIVITY

(HA)OVERALL VACANCY RATE

UNDER CNSTR

(HA)

NET RENT

(VND/SQM/TERM)

District 2 1 72 72 0% 0 VND2,230,000

District 7 1 195 193 1% 0 VND5,797,000

District 12 1 22 22 0% 0 VND2,221,000

Binh Tan District 2 321 321 0% 0 VND4,971,000

Tan Phu District 2 92 92 0% 0 VND4,459,000

Thu Duc District 3 110 110 0% 0 VND3,931,000

Nha Be District 2 506 315 38% 600 VND2,064,000

Binh Chanh District 2 190 110 42% 240 VND2,012,000

Cu Chi District 4 753 378 50% 170 VND1,520,000

TOTAL 18 2,260 1,612 28% 1,000 VND2,808,000

*Rental rates reflect asking $psqm/term

Projects under construction Q1 2016

PROPERTY HECTAREDISTRICT STATUS

Le Minh Xuan – Phase 3 242 Binh Chanh Under Construction

Tay Bac Cu Chi – Phase 2 173 Cu Chi Under Construction

Hiep Phuoc – Phase 2 597 Nha Be Under Construction

Phuoc Vo Director

Valuations & Research

Room 16, Level 14, Vincom Centre

72 Le Thanh Ton, District 1, HCMC

Tel: +84 8 3823 7968

Fax: +84 8 3823 7969

Residential For Sale Snapshot

Q1 2016Ho Chi Minh City, Vietnam

MARKETBEAT

Economic Indicators

Market Indicators

Overall Primary supply/Asking Prices Q1 2016

Primary Stock/Price Range by Grade Q1 2016

www.cushmanwakefield.com

Economy

Having achieved an impressive growth rate in 2015, the government

set a more optimistic GDP growth target of 6.7% and CPI at below 5%

in 2016. As of February 2016, total inward FDI into Vietnam reached

US$2.80 billion (both newly registered and adjusted), up 135% year-on-

year; while implemented FDI was estimated to have reached US$1.5

billion, up 15.4% year-on-year. The manufacturing and processing

industry, which accounted for 71.2% of total registered capital, attracted

the largest share. Singapore was the leading investor with newly

registered FDI in the first two months, accounting for 23% of total

investment.

Market Overview

There was a decrease in new supply in the first quarter of 2016 across

all Grades, totaling over 8,400 units from both new and active projects,

of which more than half are concentrated in the Eastern region. As of

first quarter 2016, there are nearly 21,200 available units for sale

across all Grades in the primary market, of which Grade B accounted

for 40%, while Grade A and Grade C contributed around 33% and 27%

respectively. In this quarter, Districts 2, 7 and Binh Thanh continued to

dominate the market, accounting for around 52% of the total primary

supply.

Transaction volume fell in the residential market, registering a decline

of nearly 10% year-on-year, but rose 6% quarter-on-quarter. Districts

2,7, 8 and Binh Thanh led the market, accounting for nearly a half of

total absorbed units in the quarter. Binh Thanh District continued to

outperform the rest of the other districts, making up 22% in total

transaction volume.

All Grades recorded an increase in price level on a yearly basis, mostly

due to the higher prices offered at new projects. Average price of Grade

B and Grade C increased by 2% and 14% year-on-year respectively but

fell by 1% and nearly 3% quarter-on-quarter to VND30.6 million per

square meter (/sq.m.) or US$1,370/sq.m. for Grade B and VND18.8

million/sq.m. (US$846/sq.m.) for Grade C; Grade A‘s price was up on

both a quarterly and yearly basis, to VND48.5 million/sq.m. (US$2,176/

sq.m.)., up 3% quarter-on-quarter and 7% year-on-year .

Outlook

Small to medium-sized apartments are expected to be the most sought

after. Future supply will largely be in strategic locations which offer easy

access to the CBD such as Districts 2, 4, 7 and Binh Thanh District.

Projects located along the first metro line are attracting more interest.

Buying activity is expected to benefit from lower home loan interest

rates with longer tenures from banks as well as flexible payment terms

from developers. Sentiment in the city’s residential market is expected

to continually improve in the short to medium term.

2 months 15 2 months 1612-Month

Forecast

CPI (%) 0.64 1.03

Inward FDI (billion US$) 1.19 2.80

Trade balance

(billion US$)(0.61) 0.86

Q1 15 Q1 1612-Month

Forecast

Overall Absorption Rate 35% 38%

Overall Average Price VND24,970k VND33,300k

0

1,500

3,000

4,500

6,000

7,500

9,000

0

20

40

60

80

100

120

140

Grade A Grade B Grade C

Primary Stock, UNITS Lowest Price (MIL VND/SQM)

Highest Price (MIL VND/SQM)

HCMC OFFICE

15

20

25

30

35

'-

5,500

11,000

16,500

22,000

2011 2012 2013 2014 2015 2016

Primary Stock, UNITS Aksing Price, MIL VND/SQM

* ALL PRICES ARE VAT EXCLUDED

Residential For Sale Snapshot

Q1 2016Ho Chi Minh City, Vietnam

MARKETBEAT

www.cushmanwakefield.com

About Cushman & WakefieldCushman & Wakefield is a global leader in commercial real estate services, helping clients transform the way

people work, shop, and live. The firm’s 43,000 employees in more than 60 countries provide deep local and

global insights that create significant value for occupiers and investors around the world. Cushman & Wakefield

is among the largest commercial real estate services firms in the world with revenues of $5 billion across core

services of agency leasing, asset services, capital markets, facilities services (branded C&W Services), global

occupier services, investment management (branded DTZ Investors), tenant representation and valuations &

advisory. To learn more, visit www.cushmanwakefield.com or follow @Cushwake on Twitter.

Copyright © 2016 Cushman & Wakefield. All rights reserved. The information contained within this report is gathered from multiple sources cons idered

to be reliable. The information may contain errors or omissions and is presented without any warranty or representations as to its accuracy.

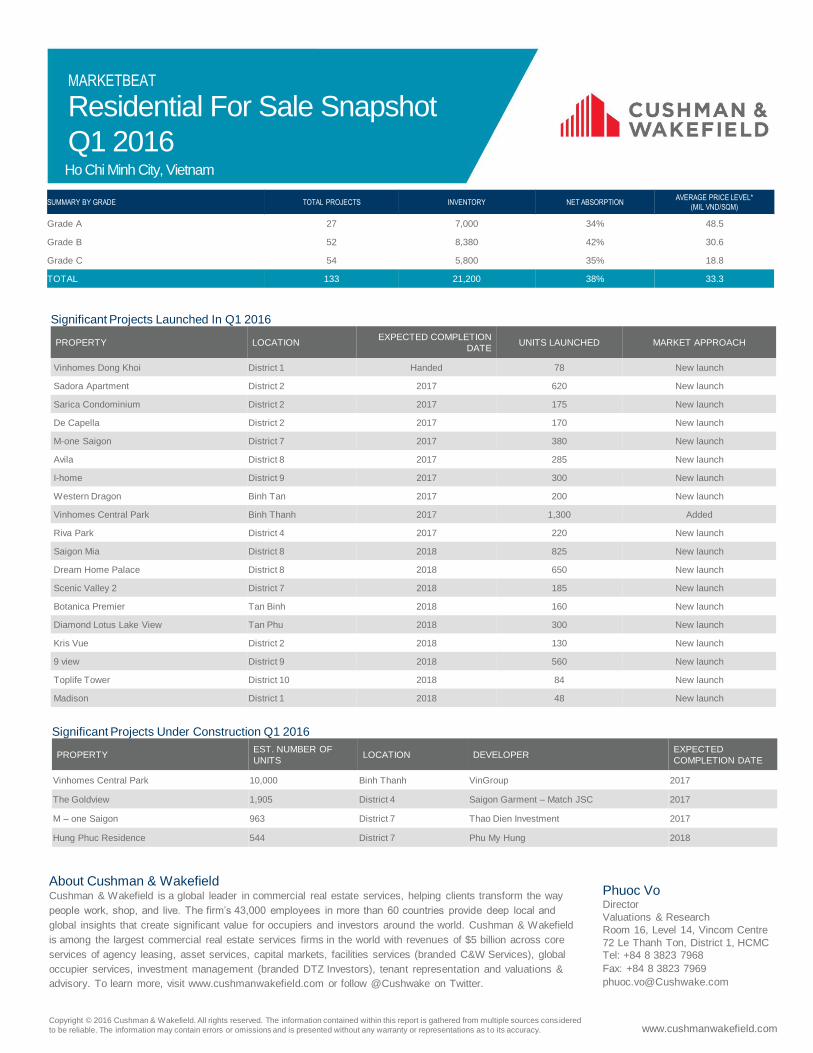

Significant Projects Under Construction Q1 2016

PROPERTYEST. NUMBER OF

UNITSLOCATION DEVELOPER

EXPECTED

COMPLETION DATE

Vinhomes Central Park 10,000 Binh Thanh VinGroup 2017

The Goldview 1,905 District 4 Saigon Garment – Match JSC 2017

M – one Saigon 963 District 7 Thao Dien Investment 2017

Hung Phuc Residence 544 District 7 Phu My Hung 2018

Phuoc VoDirector

Valuations & Research

Room 16, Level 14, Vincom Centre

72 Le Thanh Ton, District 1, HCMC

Tel: +84 8 3823 7968

Fax: +84 8 3823 7969

SUMMARY BY GRADE TOTAL PROJECTS INVENTORY NET ABSORPTIONAVERAGE PRICE LEVEL*

(MIL VND/SQM)

Grade A 27 7,000 34% 48.5

Grade B 52 8,380 42% 30.6

Grade C 54 5,800 35% 18.8

TOTAL 133 21,200 38% 33.3

Significant Projects Launched In Q1 2016

PROPERTY LOCATIONEXPECTED COMPLETION

DATEUNITS LAUNCHED MARKET APPROACH

Vinhomes Dong Khoi District 1 Handed 78 New launch

Sadora Apartment District 2 2017 620 New launch

Sarica Condominium District 2 2017 175 New launch

De Capella District 2 2017 170 New launch

M-one Saigon District 7 2017 380 New launch

Avila District 8 2017 285 New launch

I-home District 9 2017 300 New launch

Western Dragon Binh Tan 2017 200 New launch

Vinhomes Central Park Binh Thanh 2017 1,300 Added

Riva Park District 4 2017 220 New launch

Saigon Mia District 8 2018 825 New launch

Dream Home Palace District 8 2018 650 New launch

Scenic Valley 2 District 7 2018 185 New launch

Botanica Premier Tan Binh 2018 160 New launch

Diamond Lotus Lake View Tan Phu 2018 300 New launch

Kris Vue District 2 2018 130 New launch

9 view District 9 2018 560 New launch

Toplife Tower District 10 2018 84 New launch

Madison District 1 2018 48 New launch

Serviced Apartment Snapshot

Q1 2016Ho Chi Minh City, Vietnam

MARKETBEAT

Economic Indicators

Market Indicators

Net Absorption/Asking Rent

4Q TRAILING AVERAGE

Overall Vacancy

www.cushmanwakefield.com

EconomyHaving achieved an impressive growth rate in 2015, the government set a

more optimistic GDP growth target of 6.7% and CPI at below 5% in 2016.

As of February 2016, total inward FDI into Vietnam reached US$2.80 billion

(both newly registered and adjusted), up 135% year-on-year; while

implemented FDI was estimated to have reached US$1.5 billion, up 15.4%

year-on-year. The manufacturing and processing industry, which accounted

for 71.2% of total registered capital, attracted the largest share. Singapore

was the leading investor with newly registered FDI in the first two months,

accounting for 23% of total investment.

Market Overview

No new projects for either Grades entered the market in the first

quarter of 2016. The remaining units from Reverie Saigon are still under

renovation. In addition, two projects in the CBD have been completed and

are awaiting for inauguration – Ascott Waterfront Saigon and New Pearl

Residence. Currently, the market comprises 700 units from eight Grade A

buildings and 2,290 units from 23 Grade B buildings. Those in District 1

make up 44% of the total supply.

Grade B continued to see gradual improvement with average

occupancy rising on both a quarterly and yearly basis, up nearly 2

percentage points quarter-on-quarter and 5 percentage points year-on-year

to 95%. Meanwhile, Grade A had a softer performance, with occupancy

down moderately by 1 percentage point quarter-on-quarter and nearly 4

percentage points year-on-year to 92%, largely due to the seasonal

fluctuation in short term leases.

District 1 has traditionally outperformed due to its prime location,

accessibility and full range of facilities. However, lower occupancy at the

new project proved a drag as overall occupancy in the district fell to 93%,

while non-CBD occupancy reached 95%.

Average rents of both Grades experienced moderate increases on year.

Grade A rose by 1% quarter-on-quarter and 4% year-on-year, to

VND669,000 per square meter per month* (/sq.m./mo), equivalent to

US$30.0/sq.m./mo, mainly due to the ending of the promotion period of the

new project. Grade B’s rent was stable quarter-on-quarter but up 2% year-

on-year, standing at VND476,000/sq.m./mo. (US$21.3/sq.m./mo). Rents of

1-bedroom units are showing signs of an increase in majority of the projects

in the CBD, indicating increasing demand for such room types in the area.

Outlook

Over 600 units from six projects are expected to enter the market by 2016,

of which more than 60% will be in District 1 as the CBD continues to be the

preferred location of developers. Under the Trans Pacific Partnership

Agreement and the Vietnam-EU Free Trade Agreement, Vietnam ‘s

economic outlook remains positive which will drive prospects n the serviced

apartment market.

2 months 15 2 months 1612-Month

Forecast

CPI (%) 0.64 1.03

Inward FDI (billion US$) 1.19 2.80

Trade balance

(billion US$)(0.61) 0.86

Q1 15 Q1 1612-Month

Forecast

Grade A Vacancy 4.0% 7.8%

Grade A Average Rent VND644k VND669k

Grade B Vacancy 10.5% 5.3%

Grade B Average Rent VND467k VND476k

5%

10%

15%

20%

25%

2010 2011 2012 2013 2014 2015 2016

HCMC SERVICED APARTMENT

Historical Average = 14%

460,000

480,000

500,000

520,000

540,000

560,000

580,000

-40

0

40

80

120

160

200

2011 2012 2013 2014 2015 2016

Net Absorption, units Asking Rent, VND PSQM

* ALL RENTS ARE ASKING RENTS, WITH SERVICE CHARGE INCLUDED AND VAT EXCLUDED

Serviced Apartment Snapshot

Q1 2016Ho Chi Minh City, Vietnam

MARKETBEAT

www.cushmanwakefield.com

About Cushman & WakefieldCushman & Wakefield is a global leader in commercial real estate services, helping clients transform the way

people work, shop, and live. The firm’s 43,000 employees in more than 60 countries provide deep local and

global insights that create significant value for occupiers and investors around the world. Cushman & Wakefield

is among the largest commercial real estate services firms in the world with revenues of $5 billion across core

services of agency leasing, asset services, capital markets, facilities services (branded C&W Services), global

occupier services, investment management (branded DTZ Investors), tenant representation and valuations &

advisory. To learn more, visit www.cushmanwakefield.com or follow @Cushwake on Twitter.

Copyright © 2016 Cushman & Wakefield. All rights reserved. The information contained within this report is gathered from multiple sources cons idered

to be reliable. The information may contain errors or omissions and is presented without any warranty or representations as to its accuracy.

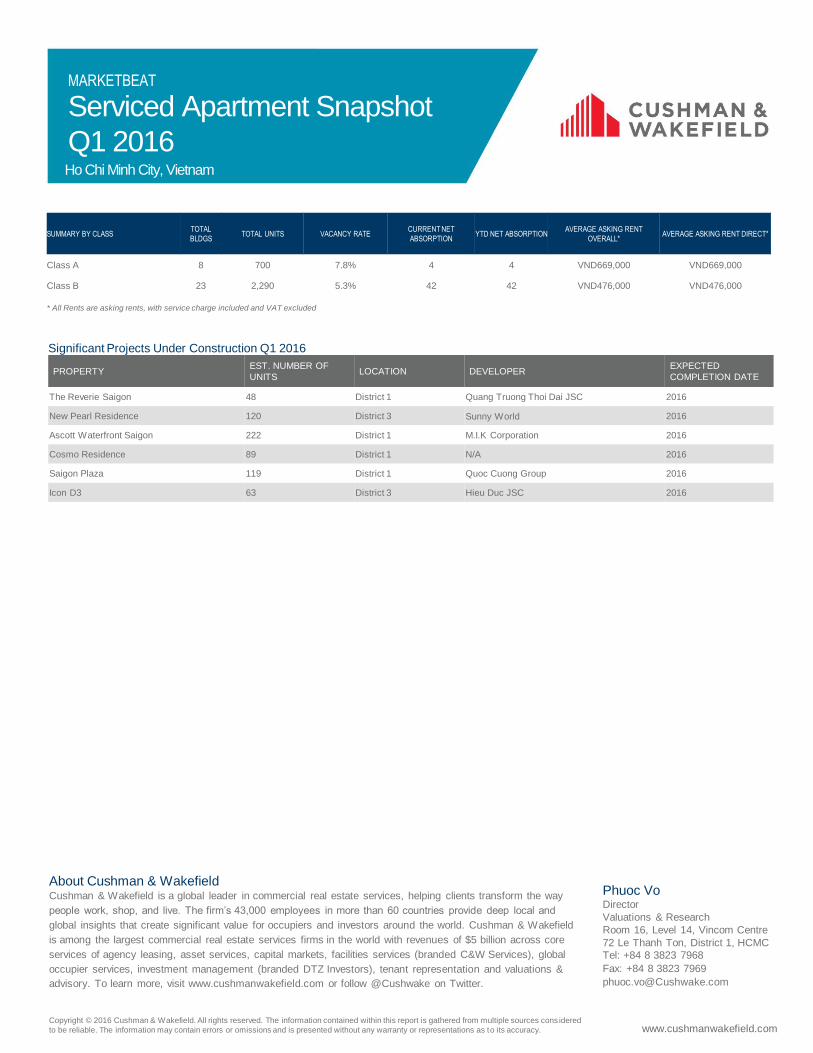

Significant Projects Under Construction Q1 2016

PROPERTYEST. NUMBER OF

UNITSLOCATION DEVELOPER

EXPECTED

COMPLETION DATE

The Reverie Saigon 48 District 1 Quang Truong Thoi Dai JSC 2016

New Pearl Residence 120 District 3 Sunny World 2016

Ascott Waterfront Saigon 222 District 1 M.I.K Corporation 2016

Cosmo Residence 89 District 1 N/A 2016

Saigon Plaza 119 District 1 Quoc Cuong Group 2016

Icon D3 63 District 3 Hieu Duc JSC 2016

Phuoc VoDirector

Valuations & Research

Room 16, Level 14, Vincom Centre

72 Le Thanh Ton, District 1, HCMC

Tel: +84 8 3823 7968

Fax: +84 8 3823 7969

SUMMARY BY CLASSTOTAL

BLDGSTOTAL UNITS VACANCY RATE

CURRENT NET

ABSORPTIONYTD NET ABSORPTION

AVERAGE ASKING RENT

OVERALL*AVERAGE ASKING RENT DIRECT*

Class A 8 700 7.8% 4 4 VND669,000 VND669,000

Class B 23 2,290 5.3% 42 42 VND476,000 VND476,000

* All Rents are asking rents, with service charge included and VAT excluded

![2015 Q1 Marketbeat [РУС/ENG]](https://static.fdocuments.us/doc/165x107/55a661761a28ab65538b4754/2015-q1-marketbeat-eng.jpg)