Market Valuation Analysis - hecweb.org Valuation Analysis ... Valuation Considerations Property...

29

Transcript of Market Valuation Analysis - hecweb.org Valuation Analysis ... Valuation Considerations Property...

1 | P a g e

Market Valuation Analysis

Diminishment Factor involving the properties located at

3581 West 350 North, Danville, Indiana (Himsel, Richard & Janet) 3868 West 350 North (Lannon, Robert & Susan)

Introduction My name is Nick A. Tillema. I am a Certified General Appraiser (CG 69100358) in the State of Indiana and have been involved in the valuing of property with environmental contamination for over fifteen years. I have written a seminar for a national professional organization (The Appraisal Institute) that was marketed on a nationwide basis and is called “Introduction to Environmental Issues for Real Estate Appraisers.” I have taught this seminar and “Appraising Environmentally Contaminated Properties: Understanding and Evaluating Stigma,” “Analyzing the Effects of Environmental Contamination on Real Property,” and “Valuation of Detrimental Conditions in Real Estate,” nationally. A copy of my curriculum vitae is attached as Exhibit A.

I have been retained by Ms. Kim Ferraro, Senior Attorney at the Hoosier Environmental Council, as an appraiser consultant to provide an opinion as to the diminished value, if any, of the residential properties located at 3581 West County Road 350 North, Danville, Indiana and 3868 West County Road 350 North, Danville, Indiana. The sites are adjacent to a Confined Animal Feeding Operation (CAFO) situated at 3042 North 425 West, Danville, Indiana.

Historical Data The area of concern is the properties within the immediate radius of the CAFO located at 3042 North 425 West, Danville, Indiana. It is generally located within the northwestern part of Hendricks County – approximately 6 miles southeast of North Salem, Indiana; 6.5 miles northwest of Danville and approximately 35 miles due west of Indianapolis. The immediate neighborhood is agricultural in nature and is more specifically defined as being bound by the McCloud Nature Park to the west; the Hendricks County Line to the north; U.S. 36 to the south; and State Road 39 to the east. Home sites and farming operations within the defined neighborhood range in age from those built in the early 1900’s to the late-1900’s – many of which have been remodeled within the last decade. The CAFO in question is located near the center of the defined neighborhood. There are no formal records within Indiana Department of Environmental Management (IDEM) regarding either of the subject residential properties. However, there are IDEM records pertaining to the CAFO including an application dated April 19, 2013 to IDEM requesting permission to construct a “new confined feeding operation” at 3042 North County Road 425 West, Danville in Hendricks County. The application indicates that all manure concrete structures would be built in accordance with the NRCS National Engineering Manual and Conservation Practice Standards. The application also indicates that the operation includes two 33,500 square foot buildings holding 4,000 hogs each – both with slatted floors and ventilation fans. It also includes two concrete pits underneath the buildings to collect and store over four million gallons of liquid hog waste. The operation also includes sufficient land to spread the waste through the “drag line” or “hose” method – a technique by which manure is pumped to a nearby field and injected 4 to 6 inches into the ground with knives mounted on a bar behind a tractor.

2 | P a g e

Such an operation would come under the classification of a Confined Animal Feeding Operation (CAFO). A notarized copy of the Confined Feeding Operation Completed Construction Affidavit was filed on September 23, 2013. And, according to IDEM inspection reports, the first round of pigs was introduced on October 6, 2013 and the first annual manure spread was planned October 6, 2014. Unfortunately, the site is approximately 1,400 feet southwest of the home site of Martin R. and Janet L. Himsel located at 3581 West County Road 350 North – a 26-acre farm where Richard Himsel was born and where Richard and Janet Himsel have been living since 1994. It is also approximately 2,500 feet southwest of the residence owned by Robert J. and Susan M. Lannon situated at 3868 West County Road 350 North, Danville, IN where the Lannons have lived since 1971. Prevailing winds in this area are from southwest to northeast thereby placing both residences not only within extremely close proximity but downwind to the odor of 8,000 hogs’ waste. Litigation involving the stench, contamination, and nuisance of the facility was filed with the Hendricks Superior Court on October 6, 2015. Part of the allegations expressed within the filings is that the value of the two residential properties located at 3581 West County Road 350 North, Danville, Indiana and 3868 West County Road 350 North Danville, Indiana have been damaged by the existence of the CAFO.

Issue As of the effective date of this appraisal, are the contamination problems associated with the CAFO substantial enough to lessen the property values of the Himsels’ and Lannons’ residential properties and, if so, to what degree.

General Considerations Livestock farming has undergone a dramatic transformation in the past several decades. Although much

of the production had centered on smaller, family-owned farms, it has now shifted to large farms that

often have corporate contracts. Most meat and dairy products now are produced on large farms with

specially designed buildings. In the process, livestock, dairy, poultry and egg production has apparently

become more efficient. General improvements to mechanical devices, animal breeding, and the specially

formulated feeds have all increased the efficiency and productivity of animal agriculture.

Paramount within that shift is the introduction of the Concentrated Animal Feeding Operation (CAFO) - a

specific type of large-scale industrial livestock production facility that raises animals, usually in high

numbers and at high-density. To be considered a CAFO, a farm must first be categorized as an animal

feeding operation (AFO) - a lot or facility where animals are kept confined and fed or maintained for 45

or more days per year. (Environmental Protection Agency [EPA], 2009). AFOs that meet the definition

of CAFO under federal regulations are considered "point sources" and subject to permitting requirements

of the Clean Water Act's National Pollution Discharge Elimination System (NPDES).1 In Indiana, IDEM has

authority to implement and enforce the federal NPDES permitting programs including those requirements

applicable to CAFO's. Generally, under EPA regulation, a CAFO is defined to include any AFO that confines

more than a specified number of animals or, regardless of the animal threshold, is designated a “significant

contributor of pollutants” to waters of the U.S. by the NPDES permitting authority.2

1 40 CFR 122.23 2 Id.

3 | P a g e

Although CAFOs can provide an economical basis for eggs, meat and milk, they have done so at

considerable expense. Pollutants include large measures of biological waste, air pollutants – including

ammonia, hydrogen sulfide, methane, nitrous oxide, and volatile organic compounds. Such farms are

notorious for noxious odors. Daily manure production from a facility of 8,000 hogs can generate about

38,000 gallons of waste and a concentration of odor that can be dramatic. Air emissions from CAFOs

usually come from one of three main sources: the ventilation stacks of the barns, manure lagoons, and

from the manure spread on fields. However, agriculture is exempt under the Clean Air Act from having

to comply with air quality standards and Indiana does not regulate odors or air emissions from CAFOs.

Spreading manure over nearby fields has long been a recognized as a basic fertilization technique and, within the last several decades, has been considered preferable in an effort by farmers to contain fertilizer costs, move away from chemical applications, designate a specific use for the waste product, and increase crop productions. However, manure applied too frequently or in too large of a quantity, will allow the nutrients to overwhelm the absorptive capacity of the soil. Such conditions lead to either a run off to neighboring properties or the pollutants are leached into the groundwater.

Basically, the dilatory effects on the immediate neighboring properties include:

Groundwater leaching because of improperly spread manure, runoff from land applications,

and/or leaking containments facilities.

Surface Water in which CAFOs pollute lakes, rivers, and reservoirs by runoff and floods.

Typical air borne pollutants surrounding CAFOs include ammonia, hydrogen sulfide, methane,

and particulate matter – all of which have varying health risks.

Depending on such things as weather conditions, prevailing winds, and farming techniques, CAFO

odors can reach as far as 5 or 6 miles.

House flies, stable flies, and mosquitoes are common insects associated with CAFOs and generally

breed in decaying material and standing water. Residence units that are close to the feeding

operations experience a much higher fly population than average homes.

CAFOs are major source of pathogens which consist of parasites, bacterium, and/or viruses – all

of which are capable of causing disease or infection in animals or humans. There are over 150

pathogens in manure that could impact human health. Many of these pathogens are concerning

because they can cause severe diarrhea.

Antibiotics are commonly administered to animal feed to reduce the livestock’s chance for

infection and to help reduce sickness disease in situations in which large numbers of animals are

contained within close quarters. Continued use seems to contribute to an increase in antibiotic-

resistant microbes causing antibiotics to be less effective in humans.

Property values – There is evidence that property values drop significantly with the most certain

fact being that the closer a home is to a CAFO, the more certain will be the value loss.

Property value losses vary based on several criteria but proximity and whether upwind or downwind are

the two major factors. Generally, a safe property and a contaminated property perceived as safe can be

sold at full market value. But both contaminated and non-contaminated properties may lose value or

marketability when the public perceives there to be a physical or financial threat. Whether this public

perception is founded or reasonable is irrelevant because the public’s apprehension drives market value.

4 | P a g e

Properties perceived to be contaminated create an uncertainty over future additional cleanup obligations.

Properties within close proximity to a CAFO is typically perceived to be subject to odor problems –

especially if downwind from such a facility.

“The exact impact of CAFOs fluctuates depending on location and local specifics. Studies have

found differing results of rates of property value decrease. One study shows that property value

declines can range from a decrease of 6.6% within a 3-mile radius of a CAFO to an 88% decrease

within 1/10 of a mile from a CAFO (Dakota Rural Action, 2006). Another study found that

negative effects are largest for properties that are downwind and closest to livestock (Herriges,

Secchi, & Babcock, 2005). The size and type of the feeding operation can affect property value

as well. Decreases in property values can also cause property taxes to drop, which can place

stress on local government budgets.”3

Valuation Considerations Property damage resulting from CAFO’s has been a topic of professional journalism for many years. One

of the premier works on property value damage is by Randall Bell, PhD, MAI in his book, Real Estate Damages. The work classifies such pollutants as an external condition which value loss is determined

by paired sales analysis or regression analysis. Unfortunately, sales of residential properties within

proximity to such facilities are rare.

John A. Kilpatrick, PhD, MAI, the managing director of Greenfield Adviser, has produced an article for the

Appraisal Institute’s The Appraisal Journal in the Winter Edition of 2015 entitled Animal Operations and Residential Property Values, in which he details dozens of national studies that indicate the

existence and extent of property damage associated with a CAFO. He further presents a series of case

studies that document the impacts of such operations.

Kilpatrick indicates that property values are impacted as market participants view the CAFO as a negative externality that, unlike other forms of obsolescence, cannot be remediated by the property owner. It is not typically considered economically curable under generally accepted appraisal theory and practice. His studies conclude that “Overall, the empirical evidence indicates that residences near AOs are significantly affected and data seems to suggest a valuation impact of up to 26% for nearby properties, depending on distance, wind direction, and other factors. Further, there has been some suggestion that properties immediately abutting an AO can be diminished as much as 88%.” 4

3 ©2010 National Association of Local Boards of Health, Bowling Green, Ohio. By Carrie Hribar, MA, 4 Animal operations and Residential Property Values, by John A. Kilpatrick, Phd, Mai, The Appraisal Journal, Winter 2015, p 41.

5 | P a g e

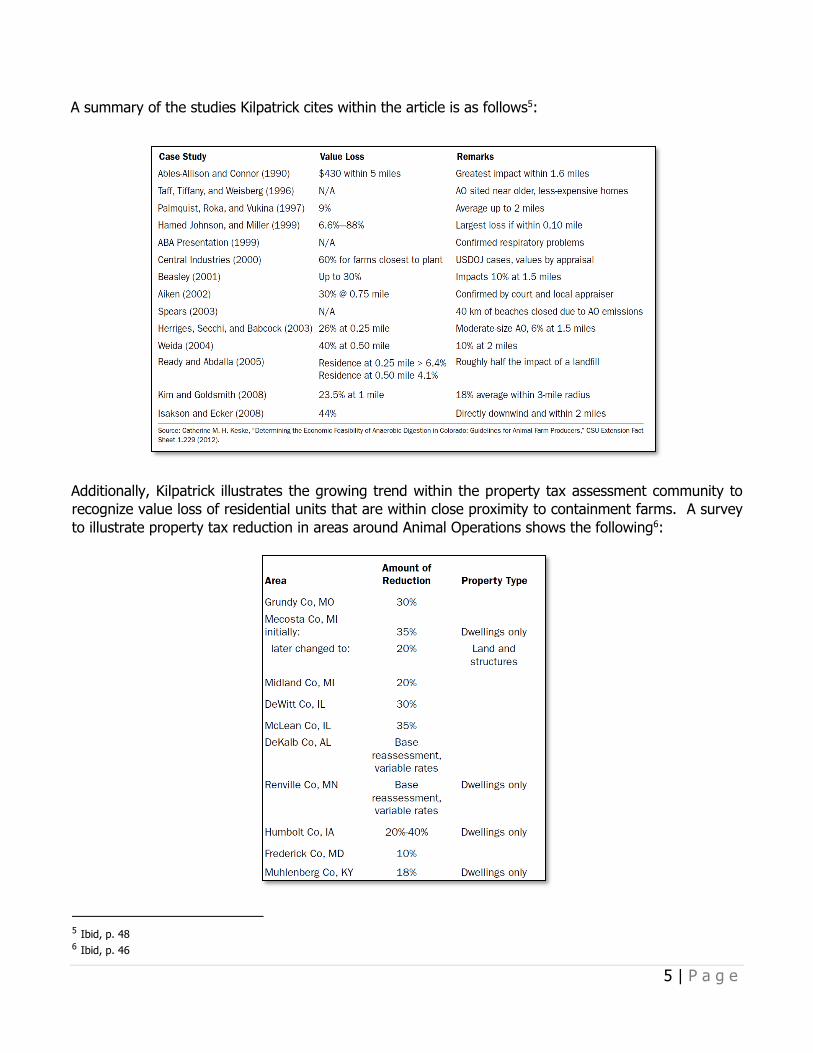

A summary of the studies Kilpatrick cites within the article is as follows5:

Additionally, Kilpatrick illustrates the growing trend within the property tax assessment community to

recognize value loss of residential units that are within close proximity to containment farms. A survey

to illustrate property tax reduction in areas around Animal Operations shows the following6:

5 Ibid, p. 48 6 Ibid, p. 46

6 | P a g e

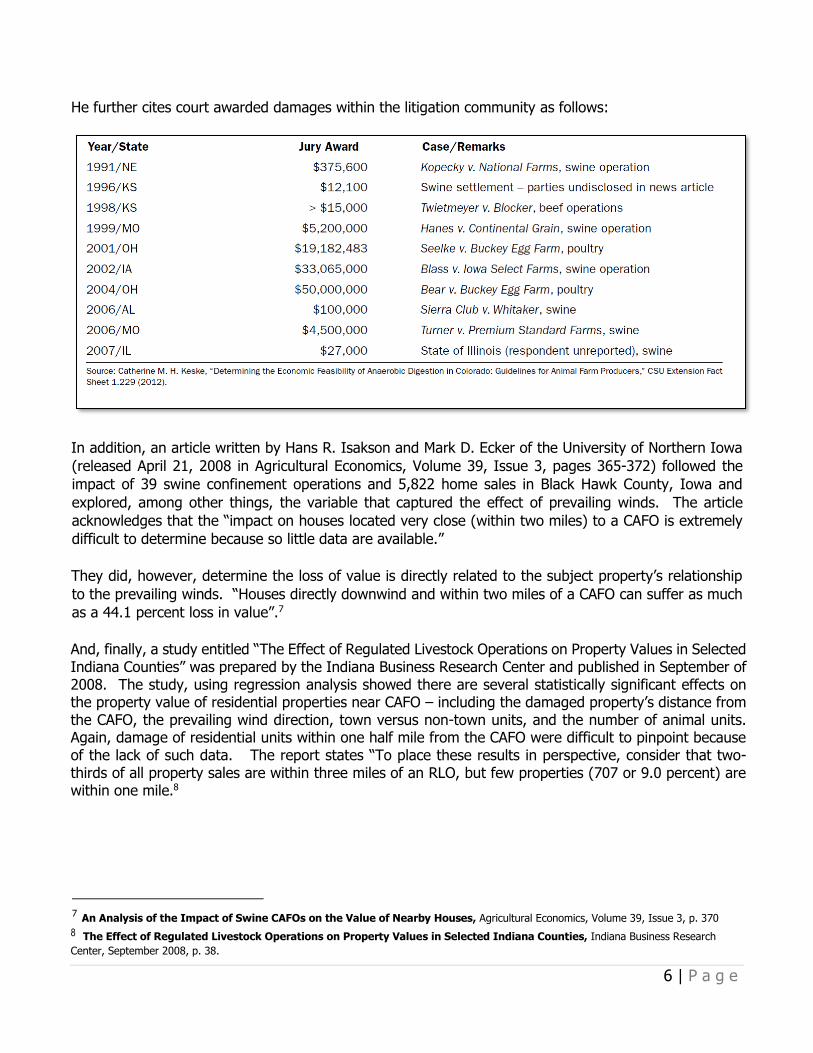

He further cites court awarded damages within the litigation community as follows:

In addition, an article written by Hans R. Isakson and Mark D. Ecker of the University of Northern Iowa

(released April 21, 2008 in Agricultural Economics, Volume 39, Issue 3, pages 365-372) followed the

impact of 39 swine confinement operations and 5,822 home sales in Black Hawk County, Iowa and

explored, among other things, the variable that captured the effect of prevailing winds. The article

acknowledges that the “impact on houses located very close (within two miles) to a CAFO is extremely

difficult to determine because so little data are available.”

They did, however, determine the loss of value is directly related to the subject property’s relationship

to the prevailing winds. “Houses directly downwind and within two miles of a CAFO can suffer as much

as a 44.1 percent loss in value”.7

And, finally, a study entitled “The Effect of Regulated Livestock Operations on Property Values in Selected Indiana Counties” was prepared by the Indiana Business Research Center and published in September of 2008. The study, using regression analysis showed there are several statistically significant effects on the property value of residential properties near CAFO – including the damaged property’s distance from the CAFO, the prevailing wind direction, town versus non-town units, and the number of animal units. Again, damage of residential units within one half mile from the CAFO were difficult to pinpoint because of the lack of such data. The report states “To place these results in perspective, consider that two-thirds of all property sales are within three miles of an RLO, but few properties (707 or 9.0 percent) are within one mile.8

7 An Analysis of the Impact of Swine CAFOs on the Value of Nearby Houses, Agricultural Economics, Volume 39, Issue 3, p. 370

8 The Effect of Regulated Livestock Operations on Property Values in Selected Indiana Counties, Indiana Business Research

Center, September 2008, p. 38.

7 | P a g e

Value Analysis It is evident and acknowledged that the source for the odor problem on the two residential units in

question is the neighboring property at 3042 North County Road 425 West, Danville, Indiana. There

appears to be no alternative uses for either residential units in which the odor is not a concern unless

the CAFO was abandoned and, even then, the stench would prevail for a period of time.

All of the other residential properties in the neighborhood have been affected to one degree or another

but the two subject properties are some of the closest and both are downwind of this area’s prevailing

winds. Based on the perception in the local market, the overall stigma of the neighborhood is considered

as severe.

COST APPROACH

The Cost Approach is where a value indication is derived by adding the estimated current cost of replacing

(or reproducing) the improvement - less any loss in value from depreciation - to the estimated value of

the land as though it were vacant. In this case, land value would have been effected because of the

limitation on the use, i.e., a typical buyer would not purchase the lot as vacant to build a home. And

improvement value would have been diminished because the owners have now realized a limitation of

their right of enjoyment.

Land value in these cases have been diminished because, given the choice between two vacant land

properties that are similar in all respects except that one is a typical unit and the other has an odor

concern like that of the subject properties, a typical buyer would purchase the tract with a clean record.

Diminishment in land value is measured by finding an alternative use that such a property could sustain

and estimating the market value of the tract under such a limitation.

The improvement value diminishment is measured by an increase in depreciation - both physical curable and economic obsolescence. Physical curable is increased because maintenance of the premises requires elimination or containment of the odor and a constant monitoring of the groundwater. Economic obsolescence is increased because a loss has occurred due to the loss of enjoyment based on factors outside of the property line. This report addresses the value loss due to contamination associated with the property. There are improvements on the property but they would not generally be valued via the cost approach, therefore, the cost approach is not applicable.

SALES COMPARISON APPROACH

The Sales Comparison Approach is derived by analyzing recent sales of comparable properties in the market. Evaluating the effects of contamination on value requires a study of the market behavior and a search for signs of evidence in the market. Each comparable situation has a different set of facts that lead to a loss in value conclusion and each must be analyzed as it relates to the circumstances surrounding the subject. The process is similar to that of a location adjustment.

8 | P a g e

Damages from the noxious CAFO waste are made evident by the Sales Comparison Approach although

slightly different for each of the two properties involved. The first unit is the 26.66-acre tract with an old

house and includes several farming outbuildings. It is apparent that the tract was cut from what was

once a large farm leaving an unusually shaped tract with very little tillable acreage. The second is a

typical brick ranch home situated on a small lot that was once part of a farm tract as well. Both are

attractive to the typical buyer but neither are attractive to the same group of typical buyers.

3581 West County Road 350 North, Danville, Indiana:

It is relatively obvious that this 26.6-acre tract was once part of a larger farming operation in which the

productive farm ground was sold leaving this residential tract and outbuildings intact. If valuing this

property under the hypothetical condition that it was not subject to the odor problem, the Highest and

Best Use as if vacant would be for the continued use of its current usage – pasture land with supporting

outbuildings. No alternative use could bear a larger value than how it is currently being employed.

Therefore, the value of the 26.66-acre tract as if it were vacant would be the same whether it had an

odor issue or not. If vacant, an investor would employ the outbuildings and land to cultivate livestock

production. Its value of the land as if vacant, according to the following grid, is approximately $138,619

or $5,211 per acre.

Subject Comparable Sale #1 Comparable Sale #2 Comparable Sale #3

Address 3581 West CR 350 N 3100 South CR 800 West 1701 North CR 300 East 700 North CR 300 East

City Danville, IN Coatsville, IN Danville, IN Danville, IN

Proximity to Subject N/A 10.0 miles 10.2 miles 7.5 miles

Data Source N/A Data Files Data Files Data Files

Verification Source Personal Inspection MLS #21152570 MLS #21378274 MLS #21248582

Sales Price N/A 162,000$ 197,068$ 380,000$

Price Per Acre N/A 5,400$ 5,351$ 9,179$

Rights Transferred Fee Fee Fee Fee

Financing Cash, Conventional Cash Conventional Cash

Condition of Sale Arm's Length Arm's Length Arm's Length Arm's Length

Date of Sale (+ 2% per year) Oct-16 Feb-12 8,910 12/19/21-5 2,625 Oct-13 22,800

Current Cash Equivalent Revised $/Acre 5,697$ 5,422$ 9,729$

Location Rural Hendricks County Rural Hendricks County Rural Boone County Suburban Danville (3,000)

Site Size (acres) 26.66 30.00 36.83 41.40

Tillable Acres 9.00 26.00 (1,000) 29.80 (1,000) 38.00 (1,000)

Zoning Agriculture Acriculture Agriculture Agriculture

Utilities Private Private - Private Private

Topography Flat Flat - Flat - Flat -

Access Average Average - Average Similar -

Flood Zone None (18063C9140D) None (18063C0225D) None (18063C0162D) None (18063C0143D)

Appeal Average Average - Average - Average -

Creek Yes None 250.00 Yes No 250.00

Woods 1 Acre 4 acres 7 acres None

Improvements Farm Outbuildings None 500.00 Farm Outbuildings Superior Buildings (1,000)

Condition Average

Net Adjustment (250) (1,000) (4,000)

Indicated Value/Acre 5,447$ 4,422$ 5,729$

Indicated Value (Site Size x Indicated Value/Acre) 145,217$ 117,891$ 152,748$

Indicated Value 138,619$

The value of the total tract – including the house, outbuildings and the 26.66-acre tract “As-if Not

Contaminated” would be calculated by finding the recent sales of similar type and sized tracts of land

with older homes and outbuildings. The following sales reflect properties with the same factors and

amenities the typical buyers would find in this market.

9 | P a g e

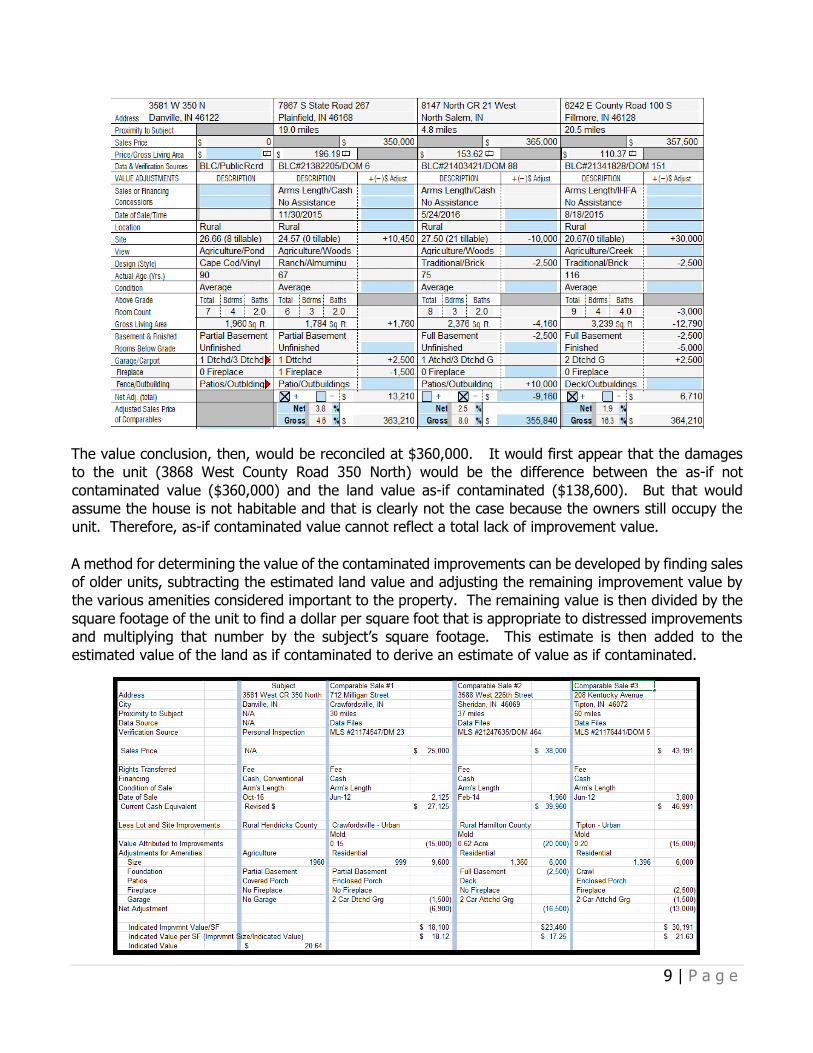

The value conclusion, then, would be reconciled at $360,000. It would first appear that the damages

to the unit (3868 West County Road 350 North) would be the difference between the as-if not

contaminated value ($360,000) and the land value as-if contaminated ($138,600). But that would

assume the house is not habitable and that is clearly not the case because the owners still occupy the

unit. Therefore, as-if contaminated value cannot reflect a total lack of improvement value.

A method for determining the value of the contaminated improvements can be developed by finding sales

of older units, subtracting the estimated land value and adjusting the remaining improvement value by

the various amenities considered important to the property. The remaining value is then divided by the

square footage of the unit to find a dollar per square foot that is appropriate to distressed improvements

and multiplying that number by the subject’s square footage. This estimate is then added to the

estimated value of the land as if contaminated to derive an estimate of value as if contaminated.

10 | P a g e

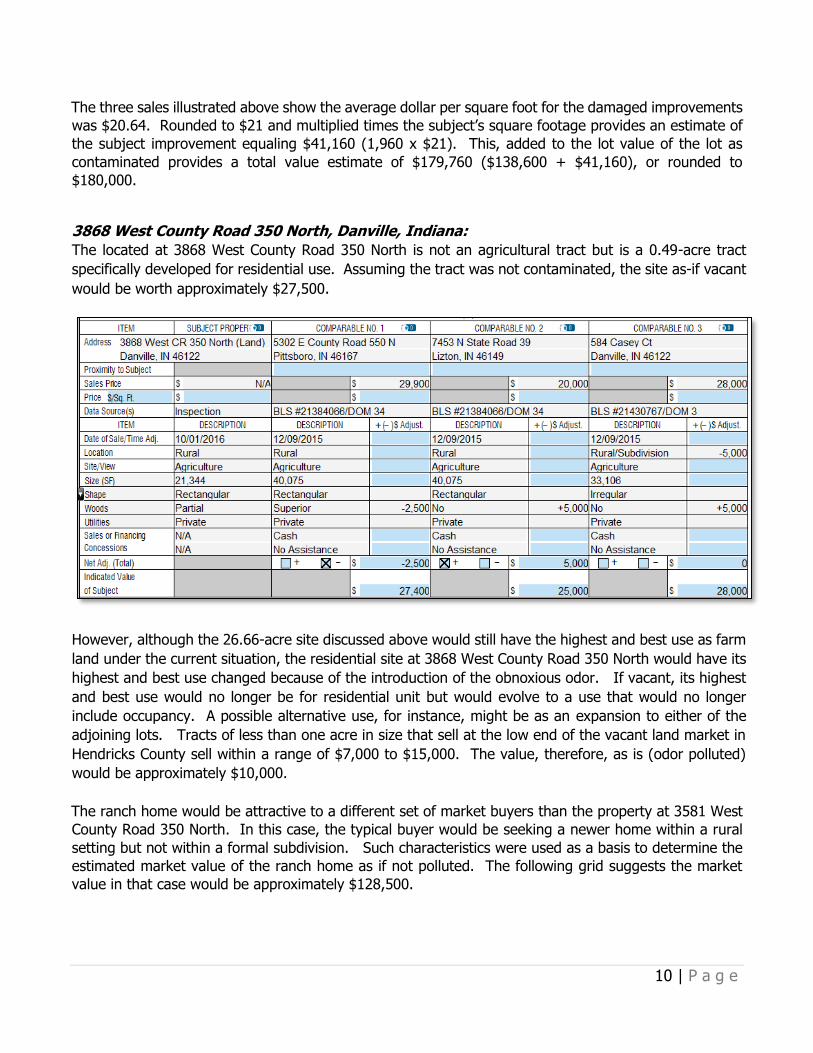

The three sales illustrated above show the average dollar per square foot for the damaged improvements

was $20.64. Rounded to $21 and multiplied times the subject’s square footage provides an estimate of

the subject improvement equaling $41,160 (1,960 x $21). This, added to the lot value of the lot as

contaminated provides a total value estimate of $179,760 ($138,600 + $41,160), or rounded to

$180,000.

3868 West County Road 350 North, Danville, Indiana:

The located at 3868 West County Road 350 North is not an agricultural tract but is a 0.49-acre tract

specifically developed for residential use. Assuming the tract was not contaminated, the site as-if vacant

would be worth approximately $27,500.

However, although the 26.66-acre site discussed above would still have the highest and best use as farm

land under the current situation, the residential site at 3868 West County Road 350 North would have its

highest and best use changed because of the introduction of the obnoxious odor. If vacant, its highest

and best use would no longer be for residential unit but would evolve to a use that would no longer

include occupancy. A possible alternative use, for instance, might be as an expansion to either of the

adjoining lots. Tracts of less than one acre in size that sell at the low end of the vacant land market in

Hendricks County sell within a range of $7,000 to $15,000. The value, therefore, as is (odor polluted)

would be approximately $10,000.

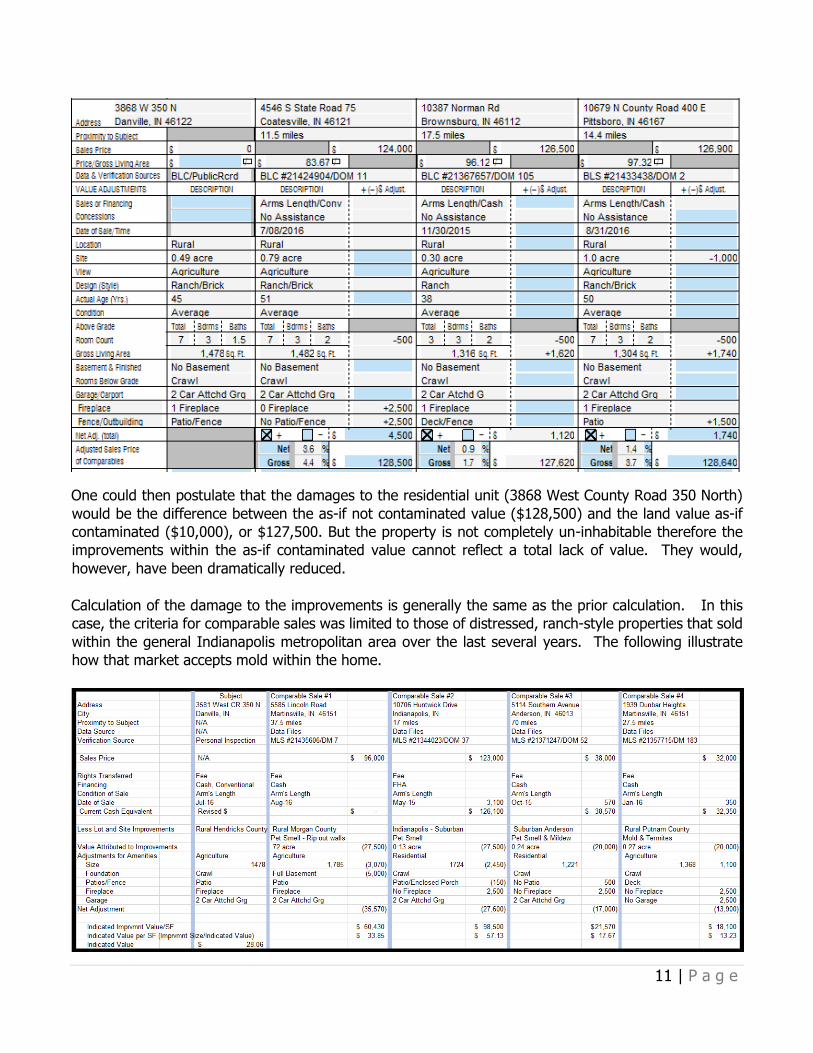

The ranch home would be attractive to a different set of market buyers than the property at 3581 West

County Road 350 North. In this case, the typical buyer would be seeking a newer home within a rural

setting but not within a formal subdivision. Such characteristics were used as a basis to determine the

estimated market value of the ranch home as if not polluted. The following grid suggests the market

value in that case would be approximately $128,500.

11 | P a g e

One could then postulate that the damages to the residential unit (3868 West County Road 350 North)

would be the difference between the as-if not contaminated value ($128,500) and the land value as-if

contaminated ($10,000), or $127,500. But the property is not completely un-inhabitable therefore the

improvements within the as-if contaminated value cannot reflect a total lack of value. They would,

however, have been dramatically reduced.

Calculation of the damage to the improvements is generally the same as the prior calculation. In this

case, the criteria for comparable sales was limited to those of distressed, ranch-style properties that sold

within the general Indianapolis metropolitan area over the last several years. The following illustrate

how that market accepts mold within the home.

12 | P a g e

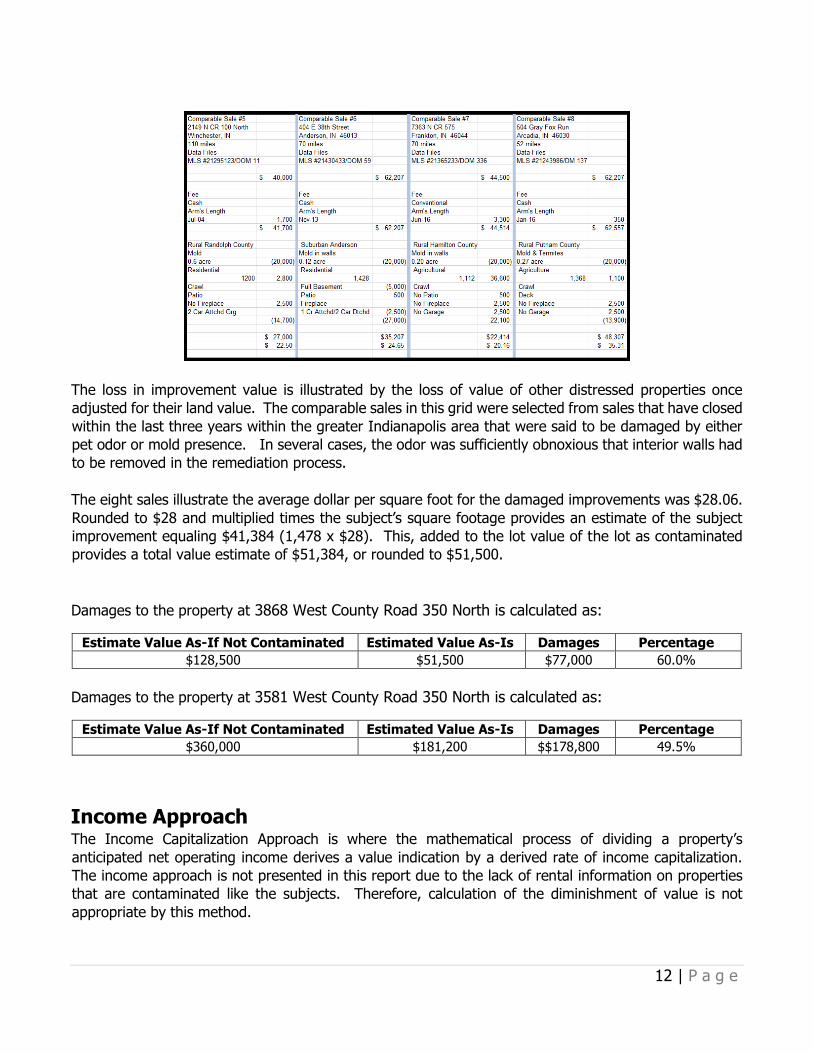

The loss in improvement value is illustrated by the loss of value of other distressed properties once

adjusted for their land value. The comparable sales in this grid were selected from sales that have closed

within the last three years within the greater Indianapolis area that were said to be damaged by either

pet odor or mold presence. In several cases, the odor was sufficiently obnoxious that interior walls had

to be removed in the remediation process.

The eight sales illustrate the average dollar per square foot for the damaged improvements was $28.06.

Rounded to $28 and multiplied times the subject’s square footage provides an estimate of the subject

improvement equaling $41,384 (1,478 x $28). This, added to the lot value of the lot as contaminated

provides a total value estimate of $51,384, or rounded to $51,500.

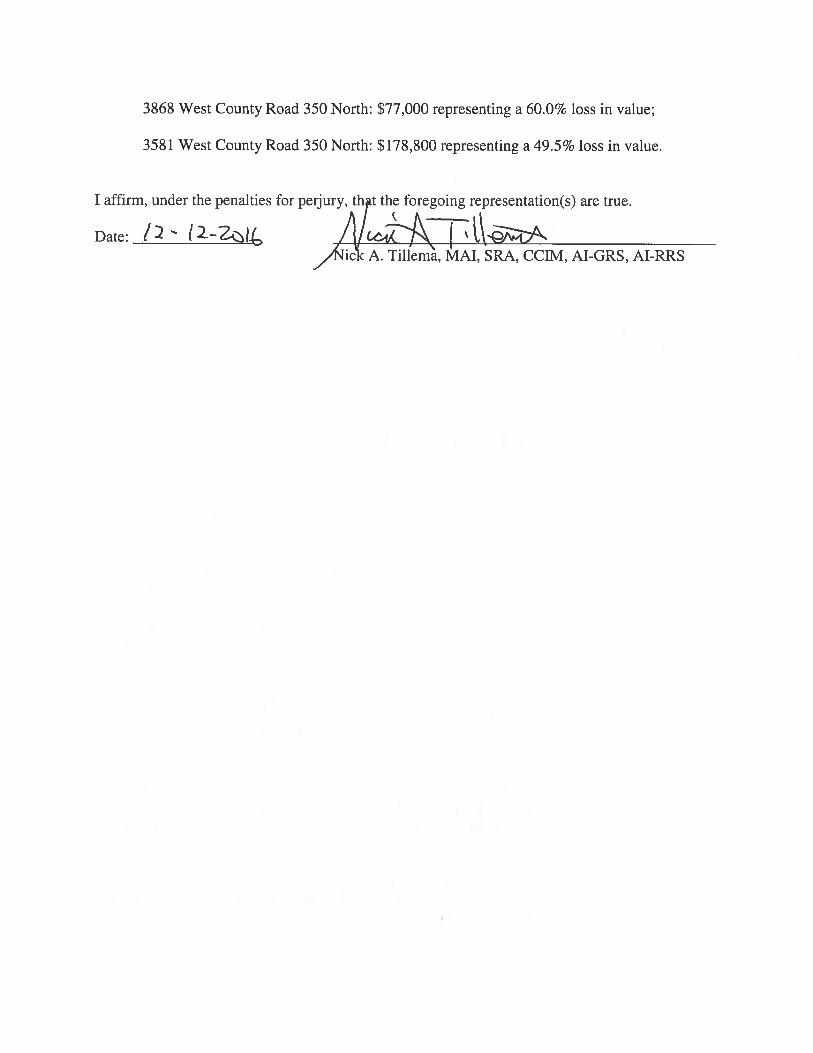

Damages to the property at 3868 West County Road 350 North is calculated as:

Estimate Value As-If Not Contaminated Estimated Value As-Is Damages Percentage

$128,500 $51,500 $77,000 60.0%

Damages to the property at 3581 West County Road 350 North is calculated as:

Estimate Value As-If Not Contaminated Estimated Value As-Is Damages Percentage

$360,000 $181,200 $$178,800 49.5%

Income Approach The Income Capitalization Approach is where the mathematical process of dividing a property’s

anticipated net operating income derives a value indication by a derived rate of income capitalization.

The income approach is not presented in this report due to the lack of rental information on properties

that are contaminated like the subjects. Therefore, calculation of the diminishment of value is not

appropriate by this method.

13 | P a g e

Test of Reasonableness As illustrated in the text above and within the articles from national publications attached in the Addendum, property values of residential units within proximity to CAFOs suffer from a diminution of value. Generally, it has been determined that residential units within one half mile are affected on a higher degree than others – especially those considered downwind from the offending CAFO. Both subject properties suffer from these specific conditions. A damage estimate of 50% and 60% appear to be well within reason.

Reconciliation and Final Value Estimate Determining stigma damage can be difficult. Although sometime considered as speculative, there is no

doubt, either from peer-reviewed literature or actual experience, that obnoxious odors associated with a

typical CAFO operation cause a form of market resistance to local residential units. It has been

determined that the degree of proximity and the direction of the prevailing winds are of importance when

calculating the market resistance in this market.

Note that both subject properties were in existence for several decades prior to the construction of the

CAFO. Had the CAFO been in operation prior to either house being constructed, an argument could be

made that the homeowners had taken on the risk of the loss of value due to the CAFO. The opposite is

not true.

Both properties in question suffer from:

air borne pollutants carrying varying degrees of health risks;

prevailing winds carrying contaminants directly to the property;

insect vectors that house flies, stable flies, and mosquitoes to the properties;

possible groundwater leaching because of nearby manure spreading; and

loss of property value.

In addition, both properties have an extended possibility of receiving potential diseases causing

pathogens like parasites, bacterium, and/or viruses. The source property, along with both subject

properties, are serviced with well and septic so groundwater contamination is a real threat.

Although both the Cost and Income Approaches were addressed within this analysis, market reactions

were best observed through the Sales Comparison Approach. Detailed searches of property sales that

reflect the property values As-If-Not-Contaminated were compared with a rational discussion of property

values As-Is – or As-If Contaminated. The difference reflects the loss of value due to the presence of the

CAFO.

14 | P a g e

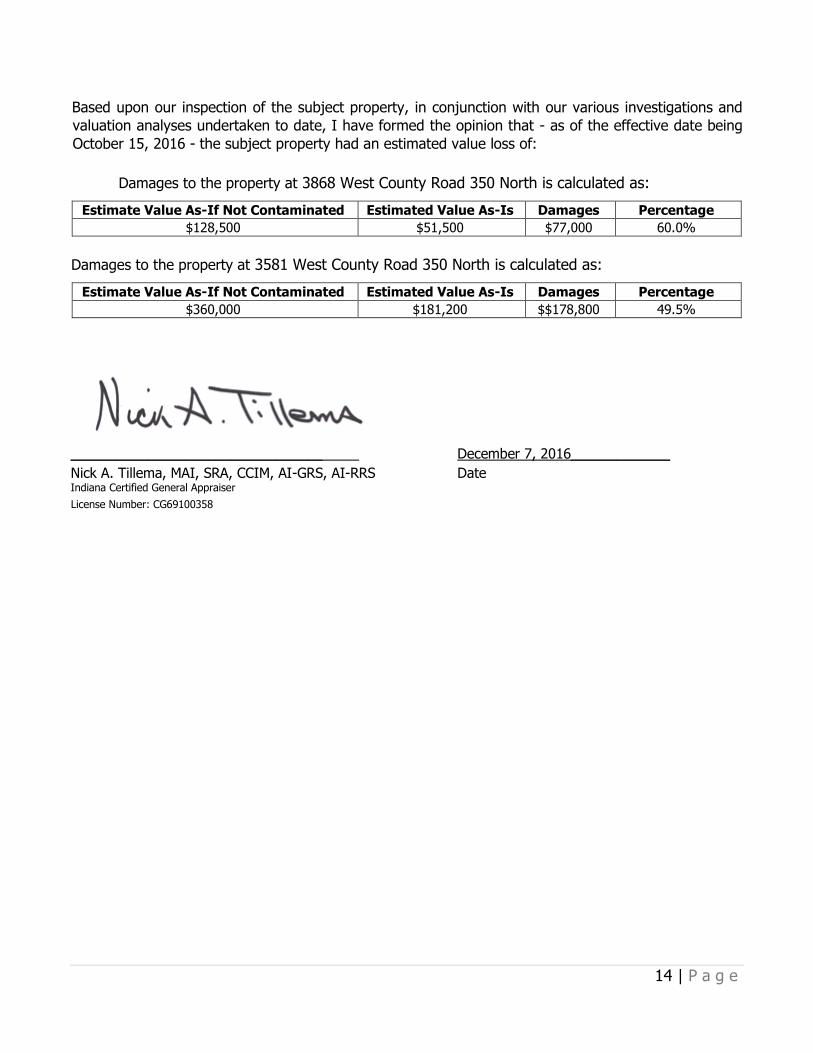

Based upon our inspection of the subject property, in conjunction with our various investigations and

valuation analyses undertaken to date, I have formed the opinion that - as of the effective date being

October 15, 2016 - the subject property had an estimated value loss of:

Damages to the property at 3868 West County Road 350 North is calculated as:

Estimate Value As-If Not Contaminated Estimated Value As-Is Damages Percentage

$128,500 $51,500 $77,000 60.0%

Damages to the property at 3581 West County Road 350 North is calculated as:

Estimate Value As-If Not Contaminated Estimated Value As-Is Damages Percentage

$360,000 $181,200 $$178,800 49.5%

_________________________________ December 7, 2016_____________

Nick A. Tillema, MAI, SRA, CCIM, AI-GRS, AI-RRS Date Indiana Certified General Appraiser License Number: CG69100358

15 | P a g e

SUMMARY OF SALIENT FACTS AND CONCLUSIONS PROPERTY NAME:

CAFO (HIMSEL/LANNON)

PROPERTY USE TYPE: Residential

REAL PROPERTY:

The subject property consists of two residential units located in a rural

area of northwest Hendricks county. One of the homes is a ±1,960-square foot older home set on an irregularly shaped parcel constituting ±26.66

acres. It is additionally improved with several outbuilding, fences and other farm related buildings. The second unit is a ±1,478-square foot

ranch home set on a ±.49 acres tract situated on a county road. Based

on observed physical appearance during the inspection, the subject appears to be in average condition.

GENERAL LOCATION:

ASSET LOCATION:

It is generally located within the northwestern part of Hendricks County –

approximately 6 miles southeast of North Salem, Indiana; 6.5 miles northwest of Danville and approximately 35 miles due west of Indianapolis.

Mailing Address: 3581 West 350 North and 3868 West 350 North Township & County: Marion Township, Hendricks County City, State & Zip Code:

Danville, Indiana 46122

PARCEL NUMBER:

32-05-24-300-001.000-017 and 32-05-24-100-005.000-017

Owner of Record:

3581 West 350 North, Danville, Indiana (Himsel, Richard & Janet)

3868 West 350 North (Lannon, Robert & Susan)

DEFINITION OF THE PROBLEM:

As of the effective date of this appraisal, are the contamination problems

associated with the CAFO substantial enough to lessen their property values of the two residential units and, if so, to what degree.

PURPOSE OF THIS ANALYSIS:

The purpose of this analysis is to present written evidence to be used as

litigation support. This narrative report presents the data and reasoning

the appraiser has used to form such an opinion.

SCOPE OF THIS ANALYSIS:

The scope is an organized collection and examination of all data from a physical, economic and legal standpoint as they might affect market value.

Each is then analyzed in an orderly fashion to derive an estimate of market value.

The data included in the report represents information collected from

several sources, not limited to, grantors and grantees of properties, real

estate brokers, real estate appraisers, multiple listing associations and real

estate management companies. Unless otherwise noted, the time span

designated as the period for comparable analysis was two years prior to

the valuation date. Sources are quoted were applicable.

Confirmation of all data is made to the extent that confirmation is practical.

The majority of the market data used in this analysis has been developed

through the Metropolitan Indianapolis Board of Realtor – Broker Listing

Coopertive (BLS) – an organization recently organized by the joining of a

number of metropolitan multiple listing services within the central Indiana.

16 | P a g e

Provisions for membership in the computer system require all Realtors to

insert required data concerning a listing within 48 hours after the listing

agreement is signed.

Failure to include all and/or accurate information can be the basis for

suspension from the system, therefore, verification beyond the

information provided by such listings has not been undertaken for this

analysis. Therefore, confirmation past the written information has not

been performed for this assignment.

Data collected is analyzed to determine the subjects’ highest and best use,

then developed through the three approaches to value (when applicable),

and lastly, reconciled into a final value estimate. Exclusion of any approach

(if necessary) is explained and justified elsewhere in this report. In this

case, based on the age of the improvements, the Cost Approach does not

appear to have credibility. And, based on the lack of comparable rental

information concerning properties like the subject, the Income Approach

has also been eliminated from the process.

All of the data collected is not presented in this report. Data collected

during the examination of the subject market, but not considered relevant,

is included in the appraiser’s file. This appraisal report includes all

information considered necessary to illustrate the appraiser’s basis for

forming an estimate of the change in the subject property’s market value.

PERTINENT DATES: The property was last inspected and photographed on July 7, 2016, by the

appraiser, Nick A. Tillema, MAI, SRA, AI-GRS, AI-RRS, CCIM. The effective

date of the appraisal is October 15, 2016The report was prepared in the

intermediate time frame and signed on December 7, 2016.

INTEREST APPRAISED: The real property interest appraised in the before/after analysis is the fee

simple estate interest. It is defined as: "Absolute ownership unencumbered by any other interest

or estate, subject only to the limitations imposed by the

governmental powers of taxation, eminent domain, police

power, and escheat." 9

Fee simple estate is recognized as the highest state of ownership, an

absolute fee, a fee unencumbered by restrictions; a fee without limitations

of use or dispositions to any particular class of heirs; subject only to the

aforementioned limitations.

9 Appraisal Institute, The Dictionary of Real Estate Appraisal, Fifith Edition, (Chicago, Appraisal Institute, 2002), p. 113.

17 | P a g e

COMPETENCY: Nick A. Tillema, MAI, SRA, AI-GRS, AI-RRS, CCIM, is currently a Certified General Appraiser [License number C.G. 691 00358] by the State of

Indiana; is designated as a commercial (MAI) and residential (SRA) appraiser; General Review Appraiser (AI-GRS); and Residential Review

Appraiser (AI-RRS) by the Appraisal Institute; and is designated as a

commercial real estate specialist by the CCIM Institute. Nick A. Tillema, MAI, SRA, AI-GRS, AI-RRS, CCIM has performed and adequately

completed appraisals concerning the analysis and valuation of such improvements similar to the subject since 1978. Adequate study was

made of the local area to make the appropriate area, regional and neighborhood analysis.

DEFINITION OF MARKET VALUE: Fair market value is specifically identified to differentiate the conclusion of

this analysis from other forms of value. The Internal Revenue Service

specifically asks for the fair market value in preparing an analysis for a

conservation easement. Fair market value is defined in this report, per

IRS Publication 561, as: “….Fair market value (FMV) is the price that property would sell

for on the open market. It is the price that would be agreed on

between a willing buyer and a willing seller, with neither being

required to act, and both having reasonable knowledge of the

relevant facts.” 11011

INTENDED USER:

This report is for the use of Ms. Kim Ferraro, Senior Attorney at the Hoosier

Environmental Council, their employees, agents, successors and assigns

may rely upon this report in evaluating the property for settlement analysis. It is mutually agreed that the client shall hold harmless the

appraiser against any legal or governmental inquiry that may evolve involving the subject property.

INTENDED USE:

This presentation centers on an estimate of the market value loss based on accepted appraisal principles and techniques. No attempt is made to

determine “sentimental,” “book,” “historic,” or “investment” value. This report is for the sole and private use of the client.

Acceptance and use of this report shall constitute contractual agreement with an implied consent to all of the definitions, functions, purposes, and

limiting conditions contained in this report. No consideration is given to

conditions reflecting a forced sale, foreclosure, or coerced liquidation of property.

10 Ibid, p. 60. 11 IRS Publication 561 (2007) page 2.

18 | P a g e

Appraisers’ Certification of Value

We hereby certify that, to the best of our knowledge and belief:

The statements of fact contained in this report are true and correct. The reported analyses, opinions and conclusions are limited only by the reported assumptions

and limiting conditions and are our personal, impartial, and unbiased professional analysis, opinions and conclusions.

I have no present or prospective interest in the property that is the subject of this report and no personal interest with respect to the parties involved.

I have no bias with respect to the property that is the subject of this report or to the parties involved with this assignment.

My engagement in this assignment was not contingent upon developing or reporting predetermined results.

My compensation for completing this assignment is not contingent upon the development or reporting of a predetermined value or direction in value that favors the cause of the client, the amount of the value opinion, the attainment of a stipulated result, or the occurrence of a subsequent event directly related to the intended use of this appraisal.

My analyses, opinions, and conclusions have been developed, and this appraisal report has been prepared in conformity with the requirements of the Uniform Standards of Professional Appraisal Practice; Financial Institutions Reform, Recovery, and Enforcement Act of 1989, and the Code of Professional Ethics and Standards of Professional Appraisal Practice of the Appraisal Institute.

Nick A. Tillema, MAI, SRA, AI-GRS, AI-RRS, CCIM, conducted a full inspection of the property that is the subject of this report on July 7, 2016.

Nick A. Tillema, MAI, SRA, AI-GRS, AI-RRS, CCIM, is professionally competent to perform this appraisal assignment by virtue of previous experience with similar assignments and/or research and education regarding the specific property type being appraised.

No one provided significant real property appraisal assistance to the persons signing this certification.

I have performed no other services, as appraisers or in any other capacity, regarding the property that is the subject of this report within the three-year period immediately preceding the acceptance of this assignment.

The use of this report is subject to the requirements of the Appraisal Institute relating to review by its duly authorized representatives.

As of the date of this report, Nick A. Tillema, MAI, SRA, AI-GRS, AI-RRS, CCIM has completed the continuing education program of the Appraisal Institute.

As of the effective date of this report, being: December 7, 2016

______________________________

Nick A. Tillema, MAI, SRA, AI-GRS, AI-RRS, CCIM Certified General Appraiser

Indiana License CG69100358

19 | P a g e

Report Limitations

Scope of Work Underlying Premises and Assumptions

Unless otherwise stated, this appraisal of real estate is made expressly subject to the following: 1. Title: That no opinion is intended to be expressed for matters legal in character, or that would require specialized

investigation or knowledge beyond that ordinarily employed by real estate appraisers, although such

matters may be discussed in the report. No opinion as to title is rendered within this report. Title is

assumed to be marketable and free and clear of all liens, encumbrances and restrictions except those

specifically discussed in the report. The subject property is assumed to be vested in the indicated owner

of record.

2. Responsible Ownership / Management: That value estimate concerning the subject property is appraised assuming it to be under responsible

ownership and competent management.

3. Information Sources: That while the information in this report has been carefully checked and is believed to be reliable, no

warranty is given for the accuracy of information obtained from the owner, from representatives of the

owner, from other informed persons, or from other sources of available information. Data on ownership

and the legal descriptions have been obtained from sources generally considered reliable.

4. Hidden or Unapparent Conditions: This appraisal analysis and subsequent report values the property on an “as-is” basis, and assumes there

are no hidden or unapparent conditions of the property, soil and sub-soil that would render potential

development of the site more or less viable than otherwise comparable properties. While not considered

conclusive, information ascertained - and either presented within this report or maintained within our office

file - is considered consistent with information that would be available to the general public, (i.e., potential

purchasers, real estate brokers and/or other real estate appraisers).

5. Subsurface Rights: That no opinion is expressed as to the potential value of subsurface oil, gas or mineral rights. It is assumed

that the subject property is not subject to surface entry for the exploration or removal of such materials

except as may be expressly stated herein.

6. Improvement's Compliance with various Legal Jurisdictions: That, unless stated, described, and considered within this report, the appraisal is based upon the premise

that the subject property's site and improvement development (and proposed improvements), have been

developed in full conformance with all applicable federal, state, and local building development and

environmental regulations and laws. This includes (but is not limited to), all applicable zoning, building use

and development regulations, and development /restrictions of all types. No responsibility is assumed for

hidden defects or lack of conformity with specific government requirements, such as fire, building and

safety, flood hazard development, earthquake, occupancy codes, or general conformance with the

Americans with Disabilities Act. It is assumed that proof of conformance, (in the form of required licenses,

certificates of occupancy, consents, and/or permits), with various requirements of federal, state, and local

legislative or administrative authorities, (as well as those of concerned private entities, or organizations),

can readily be obtained. Any improvements developed upon the subject property that is found to be

developed without such permits shall invalidate all value estimate(s) presented within this appraisal report.

7. Exhibits - Graphics:

20 | P a g e

That all maps, plats, sketches, photographs and other graphic exhibits included herein are for illustrative

purposes only and included as an aid in visualizing matters discussed within the report. The absolute

accuracy is not assumed of any graphic representations included, referred to, or which have been made

by others. They are not to be considered or relied upon for any other purpose.

8. Encroachment: That the use of the land is confined within the boundaries or the property lines of the property described

and that there is no encroachment or trespass upon the subject property unless noted otherwise within

this report.

9. Financing: That it is recognized a potential purchaser will likely take advantage of the maximum available financing.

The effects of such financing on the probable selling price have been considered within the valuation

analysis.

10. Highest and Best Use: That the subject property is appraised assuming it is to be available for its highest and best use.

Stipulations and Limiting Conditions

In addition to the preceding underlying premises and assumptions, this appraisal report is presented for

use based upon the following stipulations and limiting conditions:

That the term "market value," as herein used, is defined as delineated within the Definition of

Market Value sub-section of this appraisal report.

That the date of value to which the opinions expressed in this report apply is set forth in the letter of

transmittal, as well as delineated under the section titled "Effective Date of the Appraisal." Our office

assumes no responsibility for economic or physical factors occurring at some later date that may

affect the opinions stated herein.

That the market value estimated and the costs used are as of the effective date of the estimate of

value. Unless stated otherwise, all dollar amounts are based on the purchasing power and price of

the dollar as of the indicated effective date of the value estimate.

That the value estimate in the appraisal report is not based in whole or in part upon race, color,

religion, or national origin of the present owners, or occupants of the properties in the vicinity of the

property appraised.

That the estimated market value is subject to change with market changes over time; value is highly

related to exposure, time, promotional effort, terms, motivation, and conditions surrounding the

offering. The value estimate considers the productivity and relative attractiveness of the property

both physically and economically in the marketplace. This report does not consider the potential

discounting required to reflect a motivated or "forced sale" due to bankruptcy or foreclosure.

That disclosure of the contents of this report is governed by the by-laws and regulations of the

Appraisal Institute and Uniform Standards of Professional Appraisal Practice, (USPAP).

That this appraisal consists of "trade secrets and commercial, or financial information," all of which is

privileged and confidential, and exempted from disclosure, under 5 U.S.C. 552 (b) (4).

That no environmental or impact studies, special market study or analysis, highest and best use

analysis study, or feasibility study has been requested or made unless otherwise specified in an

agreement for services, or in this report.

That, unless otherwise noted within this report, any value estimate set forth within this report applies

only to the subject property analyzed within this report. Additionally, unless a specifically identified

proration or division is set forth within this appraisal report, any proration or division of the total into

fractional interests will invalidate the value estimate.

21 | P a g e

That, by reason of this appraisal report, our office’s representatives are prepared to give testimony in

court with reference to the property in question, and the interest therein, provided satisfactory

negotiations have been made for payment of services, for attendance in court, while under

subpoena, or in any other pretrial work requested by the attorney for either party.

That possession of this report, or any copy thereof, does not carry with it the right of publication, nor

may it be used for any other reason other than its specifically intended use. The physical report

remains the property of our office. This report is for the sole intended use of the client exclusively.

The fee is compensation for analytical service only.

That this appraisal report may not be used, except in its entirety, by anyone but the principals

identified in the cover letter / letter of transmittal. Such other use is specifically unauthorized.

Possession of this report, or any authorized copy thereof, does not carry with it the right of

publication, nor may it be used for any purpose other than its intended use. Duplication of this report

is unauthorized unless the principle appraiser signing this report has been notified and consented in

writing to the request for duplication.

That the projections included in this report are utilized to assist in the valuation process and are based

on current market conditions, anticipated short term supply and demand factors, and a continued

stable economy. Therefore, the projections are subject to changes in future conditions that cannot be

accurately predicted by representatives of our office and could affect the future income or value

projections.

That our office representatives reserve the unlimited right to alter, amend, revise or rescind any of the

statements, findings, opinions, values, estimates or conclusions upon any subsequent study, analysis

or previous study subsequently becoming known to this office.

That much of the information and analysis presented within this report, as well as the physical

appraisal report itself, was generated by way of electronic means. While our office representatives

assume the responsibility for mathematical calculations, spelling, and grammar, we depend heavily

upon the accuracy of all software and hardware employed. Our office representatives do not assume

responsibility for any software deficiencies that are beyond the scope of knowledge of a typical

software user.

That - while Federal Emergency Management Agency (FEMA) Flood Insurance Rate Maps (FIRM) were

used to determine if the property is located in or near a high probability flood area - our office

representatives are not qualified to give an opinion as to the subject property's mean elevation above

sea level. Because FIRM maps are revised without notice to the public, it is suggested that a second

source of flood hazard data, (i.e. a recent survey), be used to verify flood data provided herein.

Extraordinary Assumptions and Hypothetical Conditions None used.

22 | P a g e

Nick A. Tillema, MAI, SRA, AI-GRS, AI-RRS, CCIM

Attorney at Law Nick has been involved in the real estate/finance industry since 1972. His education includes a Bachelor's of Finance

from Indiana University, a Masters of Business Administration from Arizona State University and a Doctorate of

Jurisprudence from Indiana University - Indianapolis. His background includes leasing and management with a Chicago-

based, regional, shopping center owner; mortgage banking (origination, underwriting, secondary marketing &

management), title company (co-owner); property management, real estate development (residential condominiums);

investment, consulting and appraising (residential, commercial, easements and diminutive damages).

His experience in teaching includes real estate broker and appraiser pre-licensing classes, continuing education seminars

and real estate college classes for private schools, professional organizations, Indiana University and Butler University.

He has written numerous seminars for both law and real estate professionals. He is currently the chair of both the board

of directors of the Appraisal Institute Relief Foundation and the Appraiser Liability Insurance Program. He has also served

on the national board of directors for the Appraisal Institute and has served on the board of directors of the Hoosier State

Chapter of the Appraisal Institute, the Indiana CCIM chapter, the Indiana Association of Realtors, the Realtor Foundation,

and the Metropolitan Indianapolis Board of Realtors.

As an attorney, he has both prosecuted and defended real estate appraisers. As an appraiser, he has reviewed both

residential and commercial appraisals as part of a litigation team. His background and education allow him to speak

intelligently on today’s appraisal issues.

As an appraiser, his experience includes appraising farms, local and regional shopping centers, conventional and HUD

apartment facilities, steel mills, oil refineries, and mega-warehouses. His experience with special purpose properties

includes mega-church facilities, school buildings, cemeteries, airports, the Detroit RiverWalk and an abandoned U.S. Air

Force Base. Specialty appraisal assignments have included forensic appraising for litigation purposes, conservation

easements, pipeline easements and properties affected by environmental contamination, construction defects and partial

interests.

23 | P a g e

Nick A. Tillema, MAI, SRA, AI-GRS, AI-RRS, CCIM 9247 North Meridian, Suite 260

Indianapolis, IN 46260

Indiana Certified General Appraiser #CG69100358 317.571.8800 – Office

Indiana Principal Real Estate Broker #IB51247724 317.581.9553 – Facsimile

[email protected] – e-mail 317.581.0400 – Cellular

PROFESSIONAL EXPERIENCE: ACCURITY VALUATION (1/16 to present)

Valuation, Consulting & Litigation (Indiana Representative)

ACCESS GROUP, LLC - (1/04 to present)

Valuation, Education, Consulting & Litigation Support

NICK A. TILLEMA AND ASSOCIATES - (1/82 to present)

Appraisal/Research

THE FORRESTAL GROUP – (11/95 to present)

Environmental Consulting/Appraisals

SYCAMORE TREE DEVELOPMENT, INC. – (1/92 to present)

Real Estate Development

FRONTIER TITLE COMPANY – (1-91 TO 7-93)

President

MEDLEY, SMITH, KOLAS & TILLEMA - (6/90 to 1/94)

Attorneys at Law

MERIDIAN MORTGAGE COMPANY, INC. – (4/75 to 6/82)

Senior Vice President – Administration

LANDAU, HEYMAN & CLAY - (7/72 TO 3/75)

Commercial Leasing (Indiana)

FORMAL EDUCATION: INDIANA UNIVERSITY SCHOOL OF LAW

Doctor of Jurisprudence (JD) - (9-81 to 1-87)

ARIZONA STATE UNIVERSITY

Masters of Business Administration – MBA - (9-71 to 7-72)

INDIANA UNIVERSITY

Bachelors of Science (BS – Finance) - (9-68 to 8-71)

PROFESSIONAL EDUCATION AND SEMINARS (partial listing): SOCIETY OF REAL ESTATE APPRAISERS

Principles of Real Estate Appraising

Narrative Report Writing Seminar

Condominium Appraising Seminar

R-41B & Professional Practice Seminar

Instructor Course (101)

Appraising with the URAR Form

Marshall & Swift Cost Seminar

Legal Liability

AMERICAN INSTITUTE OF REAL ESTATE APPRAISERS

Basic Valuation Procedures 1A-1 & 1A-2

Capitalization Theory 1B-a & 1B-2

Case Studies & Report Writing

Standards of Professional Practice

APPRAISAL INSTITUTE

Standards of Professional Practice

RECOGNITION 1991 – Dick Snyder Award (Indiana Association of Realtors) 2005 – Ed White Award (Hoosiers State Chapter, Appraisal Institute) 2006 – Extra Mile Award (Hoosiers State Chapter, Appraisal Institute) 2009 – Fellow of REAL (Metropolitan Indianapolis Board of Realtors) 2011 – Richard E. Nichols Lifetime Achievement Award (Hoosiers State Chapter, Appraisal Institute)

24 | P a g e

PROFESSIONAL ORGANIZATIONS: APPRAISAL INSTITUTE (combined with the Society of Real Estate Appraiser in 1991)

Designated Member of the Appraisal Institute (MAI - June, 1992 & SRA – March, 1985))

Hoosier State Chapter

Indianapolis Sub-Chapter Appraisal Institute – Past Chairman (1999)

Hoosier State Chapter Appraisal Institute – President (2004)

Region V

Regional Representative – Region 5 - (1994 to 1998)

Regional Chairperson (2007-2010)

National Ethics Committee – Past Assistant Regional Member

National

Appraisal Institute – National Nomination Committee (2005 – Alternate)

Appraisal Standards and Guidance Committee (2005-2006)

Board of Directors (2007-2010)

Publications Review Panel (2010 – 2012)

Appraisal Institute Relief Fund - Board of Directors (2009 – 2012)(Chair 2011) & (2014 – 2016)(Chair – 2016)

Strategic Planning Committee (2012-2013)

Government Relations Committee (2005-2007 & 2011-2013) (Chair 2012/2013)

Appraiser’s Liability Insurance Program – Board of Directors (2014 – 2016) (Chair – 2016)

SOCIETY OF REAL ESTATE APPRAISERS (CHAPTER 5)

(Past President ['89], Secretary ['84], Director ['85-'87])

(Chairman of Standards of Professional Practice, 1987-1990)

Designated as Senior Residential Appraiser (SRA) 1985 CCIM INSTITUTE

Designated Member of the CCIM (October 2004)

Indiana Chapter of CCIM – Board of Directors (2010-2012)

NATIONAL, STATE, AND LOCAL BOARD OF REALTORS

Designated as Realtor (1978)

Past Chairperson – Appraisal Committee of Indiana Association of Realtors

Past Chairperson - Broker/Appraiser Committee MIBOR

Board of Directors - MIBOR (1998 – 2000)

Board of Directors - Indiana Association of Realtors (2000 – 2006 and 2010 - 2012)

Board of Directors – Realtors Foundation (2007 – 2012)

INDIANAPOLIS BAR ASSOCIATION

Real Estate/Probate Committee (2005 to Present)

INDIANA BAR ASSOCIATION

Indiana Bar Ethics Committee (2006-2009) & (2010-2013)

INDIANAPOLIS BUILDER'S ASSOCIATION (Inactive)

Past Member (1980 – 1984)

NATIONAL ASSOCIATION OF ENVIRONMENTAL RISK AUDITORS (Inactive)

Past Legal Counsel & Member of Board of Directors – National Organization

INDIANA INSTITUTE OF REAL ESTATE EDUCATORS (Inactive)

Designated as Certified Real Estate Instructor – CREI (Charter Member)

INDIANAPOLIS MORTGAGE BANKERS ASSOCIATION (Inactive)

(Past President - 1979)

OTHER ACTIVITIES: ACCESS EDUCATION, INC.

Principal (Pre-licensing & Continuing Education for Real Estate Appraisers and Brokers)

APPRAISAL INSTITUTE

Instructor – See attached

INDIANA UNIVERSITY PURDUE UNIVERSITY AT INDIANAPOLIS (I.U.P.U.I.)

Part-time Instructor – course R-305, R-440 & R-443 (1993 to present)

REAL ESTATE RECERTIFICATION PROGRAM

Instructor – Real Estate Appraiser and Broker Licensing Courses (1979 to 2010)

RESOURCE EDUCATION

Instructor – Pre-licensing and Continuing Education Seminars (1998 to 2010)

BUTLER UNIVERSITY

Instructor – Principles of Real Estate Law (1976 to 1978)

SOCIETY OF REAL ESTATE APPRAISERS (1985 to 1989)

Instructor – Principles of Real Estate Appraising (101)

Instructor – Seminar “Appraising for Underwriters”

NATIONAL ASSOCIATION OF ENVIRONMENTAL RISK AUDITORS

Instructor – Environmental Effects of Real Estate (1989 to 2002)

CERTIFIED AUCTIONEER INSTITUTE

Instructor – Real Estate Appraisal & Auctioneering (1989 to 1993)

INDIANA REAL ESTATE EDUCATION ADVISORY COMMISSION

Vice Chairman (1998 – 2007)

25 | P a g e

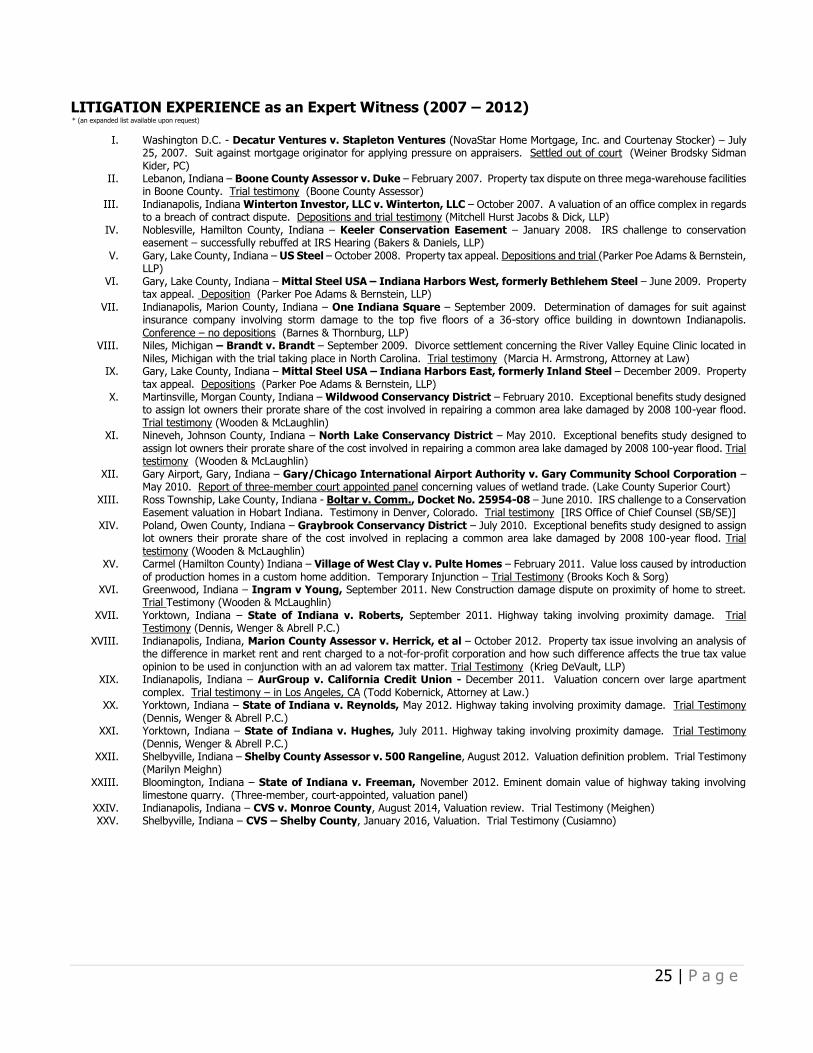

LITIGATION EXPERIENCE as an Expert Witness (2007 – 2012) * (an expanded list available upon request)

I. Washington D.C. - Decatur Ventures v. Stapleton Ventures (NovaStar Home Mortgage, Inc. and Courtenay Stocker) – July 25, 2007. Suit against mortgage originator for applying pressure on appraisers. Settled out of court (Weiner Brodsky Sidman Kider, PC)

II. Lebanon, Indiana – Boone County Assessor v. Duke – February 2007. Property tax dispute on three mega-warehouse facilities in Boone County. Trial testimony (Boone County Assessor)

III. Indianapolis, Indiana Winterton Investor, LLC v. Winterton, LLC – October 2007. A valuation of an office complex in regards to a breach of contract dispute. Depositions and trial testimony (Mitchell Hurst Jacobs & Dick, LLP)

IV. Noblesville, Hamilton County, Indiana – Keeler Conservation Easement – January 2008. IRS challenge to conservation easement – successfully rebuffed at IRS Hearing (Bakers & Daniels, LLP)

V. Gary, Lake County, Indiana – US Steel – October 2008. Property tax appeal. Depositions and trial (Parker Poe Adams & Bernstein, LLP)

VI. Gary, Lake County, Indiana – Mittal Steel USA – Indiana Harbors West, formerly Bethlehem Steel – June 2009. Property tax appeal. Deposition (Parker Poe Adams & Bernstein, LLP)

VII. Indianapolis, Marion County, Indiana – One Indiana Square – September 2009. Determination of damages for suit against insurance company involving storm damage to the top five floors of a 36-story office building in downtown Indianapolis. Conference – no depositions (Barnes & Thornburg, LLP)

VIII. Niles, Michigan – Brandt v. Brandt – September 2009. Divorce settlement concerning the River Valley Equine Clinic located in Niles, Michigan with the trial taking place in North Carolina. Trial testimony (Marcia H. Armstrong, Attorney at Law)

IX. Gary, Lake County, Indiana – Mittal Steel USA – Indiana Harbors East, formerly Inland Steel – December 2009. Property tax appeal. Depositions (Parker Poe Adams & Bernstein, LLP)

X. Martinsville, Morgan County, Indiana – Wildwood Conservancy District – February 2010. Exceptional benefits study designed to assign lot owners their prorate share of the cost involved in repairing a common area lake damaged by 2008 100-year flood. Trial testimony (Wooden & McLaughlin)

XI. Nineveh, Johnson County, Indiana – North Lake Conservancy District – May 2010. Exceptional benefits study designed to assign lot owners their prorate share of the cost involved in repairing a common area lake damaged by 2008 100-year flood. Trial testimony (Wooden & McLaughlin)

XII. Gary Airport, Gary, Indiana – Gary/Chicago International Airport Authority v. Gary Community School Corporation – May 2010. Report of three-member court appointed panel concerning values of wetland trade. (Lake County Superior Court)

XIII. Ross Township, Lake County, Indiana - Boltar v. Comm., Docket No. 25954-08 – June 2010. IRS challenge to a Conservation Easement valuation in Hobart Indiana. Testimony in Denver, Colorado. Trial testimony [IRS Office of Chief Counsel (SB/SE)]

XIV. Poland, Owen County, Indiana – Graybrook Conservancy District – July 2010. Exceptional benefits study designed to assign lot owners their prorate share of the cost involved in replacing a common area lake damaged by 2008 100-year flood. Trial testimony (Wooden & McLaughlin)

XV. Carmel (Hamilton County) Indiana – Village of West Clay v. Pulte Homes – February 2011. Value loss caused by introduction of production homes in a custom home addition. Temporary Injunction – Trial Testimony (Brooks Koch & Sorg)

XVI. Greenwood, Indiana – Ingram v Young, September 2011. New Construction damage dispute on proximity of home to street. Trial Testimony (Wooden & McLaughlin)

XVII. Yorktown, Indiana – State of Indiana v. Roberts, September 2011. Highway taking involving proximity damage. Trial Testimony (Dennis, Wenger & Abrell P.C.)

XVIII. Indianapolis, Indiana, Marion County Assessor v. Herrick, et al – October 2012. Property tax issue involving an analysis of the difference in market rent and rent charged to a not-for-profit corporation and how such difference affects the true tax value opinion to be used in conjunction with an ad valorem tax matter. Trial Testimony (Krieg DeVault, LLP)

XIX. Indianapolis, Indiana – AurGroup v. California Credit Union - December 2011. Valuation concern over large apartment complex. Trial testimony – in Los Angeles, CA (Todd Kobernick, Attorney at Law.)

XX. Yorktown, Indiana – State of Indiana v. Reynolds, May 2012. Highway taking involving proximity damage. Trial Testimony (Dennis, Wenger & Abrell P.C.)

XXI. Yorktown, Indiana – State of Indiana v. Hughes, July 2011. Highway taking involving proximity damage. Trial Testimony (Dennis, Wenger & Abrell P.C.)

XXII. Shelbyville, Indiana – Shelby County Assessor v. 500 Rangeline, August 2012. Valuation definition problem. Trial Testimony (Marilyn Meighn)

XXIII. Bloomington, Indiana – State of Indiana v. Freeman, November 2012. Eminent domain value of highway taking involving limestone quarry. (Three-member, court-appointed, valuation panel)

XXIV. Indianapolis, Indiana – CVS v. Monroe County, August 2014, Valuation review. Trial Testimony (Meighen) XXV. Shelbyville, Indiana – CVS – Shelby County, January 2016, Valuation. Trial Testimony (Cusiamno)

26 | P a g e

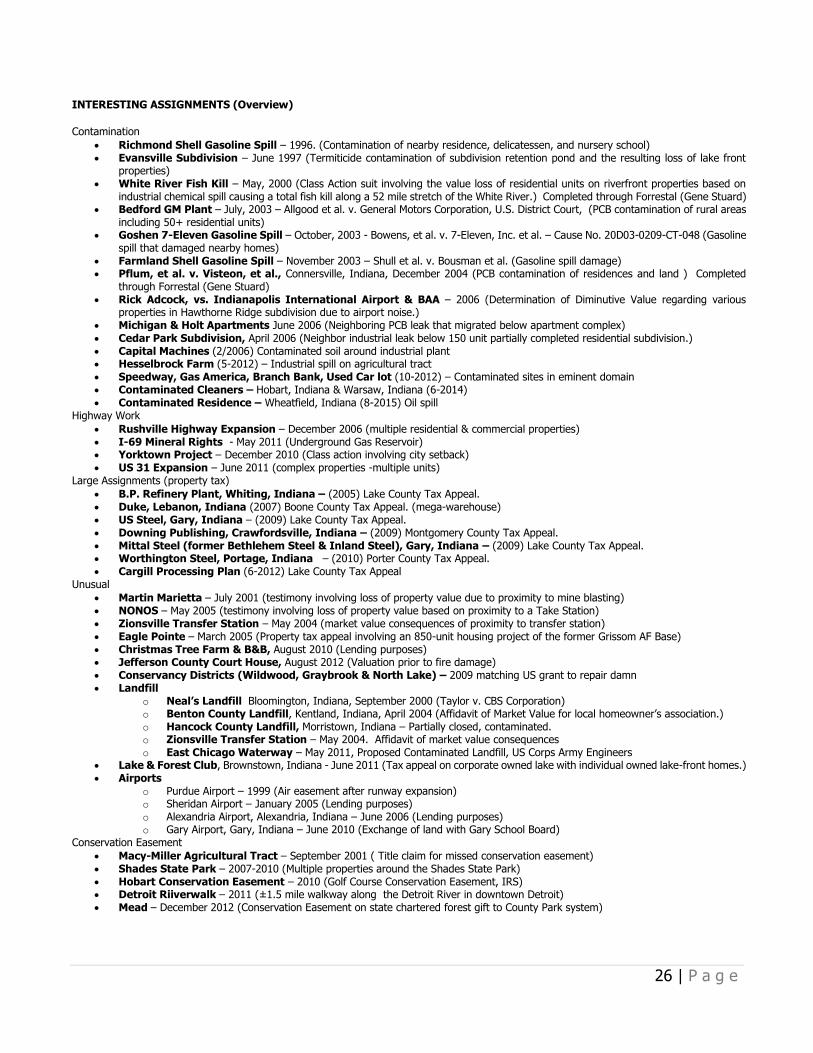

INTERESTING ASSIGNMENTS (Overview)

Contamination

Richmond Shell Gasoline Spill – 1996. (Contamination of nearby residence, delicatessen, and nursery school) Evansville Subdivision – June 1997 (Termiticide contamination of subdivision retention pond and the resulting loss of lake front

properties) White River Fish Kill – May, 2000 (Class Action suit involving the value loss of residential units on riverfront properties based on

industrial chemical spill causing a total fish kill along a 52 mile stretch of the White River.) Completed through Forrestal (Gene Stuard) Bedford GM Plant – July, 2003 – Allgood et al. v. General Motors Corporation, U.S. District Court, (PCB contamination of rural areas

including 50+ residential units) Goshen 7-Eleven Gasoline Spill – October, 2003 - Bowens, et al. v. 7-Eleven, Inc. et al. – Cause No. 20D03-0209-CT-048 (Gasoline

spill that damaged nearby homes) Farmland Shell Gasoline Spill – November 2003 – Shull et al. v. Bousman et al. (Gasoline spill damage) Pflum, et al. v. Visteon, et al., Connersville, Indiana, December 2004 (PCB contamination of residences and land ) Completed

through Forrestal (Gene Stuard) Rick Adcock, vs. Indianapolis International Airport & BAA – 2006 (Determination of Diminutive Value regarding various

properties in Hawthorne Ridge subdivision due to airport noise.) Michigan & Holt Apartments June 2006 (Neighboring PCB leak that migrated below apartment complex) Cedar Park Subdivision, April 2006 (Neighbor industrial leak below 150 unit partially completed residential subdivision.) Capital Machines (2/2006) Contaminated soil around industrial plant Hesselbrock Farm (5-2012) – Industrial spill on agricultural tract Speedway, Gas America, Branch Bank, Used Car lot (10-2012) – Contaminated sites in eminent domain Contaminated Cleaners – Hobart, Indiana & Warsaw, Indiana (6-2014) Contaminated Residence – Wheatfield, Indiana (8-2015) Oil spill

Highway Work

Rushville Highway Expansion – December 2006 (multiple residential & commercial properties) I-69 Mineral Rights - May 2011 (Underground Gas Reservoir) Yorktown Project – December 2010 (Class action involving city setback) US 31 Expansion – June 2011 (complex properties -multiple units)

Large Assignments (property tax)

B.P. Refinery Plant, Whiting, Indiana – (2005) Lake County Tax Appeal. Duke, Lebanon, Indiana (2007) Boone County Tax Appeal. (mega-warehouse) US Steel, Gary, Indiana – (2009) Lake County Tax Appeal. Downing Publishing, Crawfordsville, Indiana – (2009) Montgomery County Tax Appeal. Mittal Steel (former Bethlehem Steel & Inland Steel), Gary, Indiana – (2009) Lake County Tax Appeal. Worthington Steel, Portage, Indiana – (2010) Porter County Tax Appeal. Cargill Processing Plan (6-2012) Lake County Tax Appeal

Unusual

Martin Marietta – July 2001 (testimony involving loss of property value due to proximity to mine blasting) NONOS – May 2005 (testimony involving loss of property value based on proximity to a Take Station) Zionsville Transfer Station – May 2004 (market value consequences of proximity to transfer station) Eagle Pointe – March 2005 (Property tax appeal involving an 850-unit housing project of the former Grissom AF Base) Christmas Tree Farm & B&B, August 2010 (Lending purposes) Jefferson County Court House, August 2012 (Valuation prior to fire damage) Conservancy Districts (Wildwood, Graybrook & North Lake) – 2009 matching US grant to repair damn Landfill

o Neal’s Landfill Bloomington, Indiana, September 2000 (Taylor v. CBS Corporation) o Benton County Landfill, Kentland, Indiana, April 2004 (Affidavit of Market Value for local homeowner’s association.) o Hancock County Landfill, Morristown, Indiana – Partially closed, contaminated. o Zionsville Transfer Station – May 2004. Affidavit of market value consequences o East Chicago Waterway – May 2011, Proposed Contaminated Landfill, US Corps Army Engineers

Lake & Forest Club, Brownstown, Indiana - June 2011 (Tax appeal on corporate owned lake with individual owned lake-front homes.) Airports

o Purdue Airport – 1999 (Air easement after runway expansion) o Sheridan Airport – January 2005 (Lending purposes) o Alexandria Airport, Alexandria, Indiana – June 2006 (Lending purposes) o Gary Airport, Gary, Indiana – June 2010 (Exchange of land with Gary School Board)

Conservation Easement

Macy-Miller Agricultural Tract – September 2001 ( Title claim for missed conservation easement) Shades State Park – 2007-2010 (Multiple properties around the Shades State Park) Hobart Conservation Easement – 2010 (Golf Course Conservation Easement, IRS) Detroit Riiverwalk – 2011 (±1.5 mile walkway along the Detroit River in downtown Detroit) Mead – December 2012 (Conservation Easement on state chartered forest gift to County Park system)

27 | P a g e

AUTHORSHIP (Courses & Seminars) Book:

Indiana Real Estate Law and Practice Manual (1990; Revised – 1993) Courses:

Introduction to Real Estate Appraising Principles & Procedures (1/2004) – Access Education (IUPUI) Appraising the 2-4 Family Residence (1/2004) – Access Education (IUPUI) The Calculator Class (6/2004) – Access Education Appraising Complex Properties (2/2008) - Access Education (IFA – Russian Contingency)

Seminars:

Real Estate Appraisals in Indiana (1995) Indiana Continuing Legal Education Foundation (ICLEF) Litigation Skills for the Appraiser: An Overview (6/1997) – Appraisal Institute Introduction to Environmental Issues for Real Estate Appraisers (2001) – Appraisal Institute Appraising Environmentally Contaminated Properties (2001) – Appraisal Institute Crossing the Line: Home Mortgage Fraud (9/2002) – Appraisal Institute Civil Rights, Real Estate and Valuation (1/2004) – Access Education (Realtors – Austrian Tour) Recognizing Relevant Environmental Issues (1/2004) – Access Education (Realtors – Austrian Tour) Indiana Agency Law and Buyer Agency (1/2004) – Access Education (Realtors – Austrian Tour) Creating the Right List Price (1/2004) – Access Education (Realtors – Austrian Tour) A Professional’s Perspective on Predatory Lending (1/2004) – Access Education (Realtors – Austrian Tour) Laws, Ethics & Standards (5/2004) – Access Education (Wisconsin Online Appraisal CE) Procedures for the Unusual Residential Appraisal (5/2004) – Access Education (Wisconsin Online Appraisal CE) The Economics of Residential Finance (5/2004) – Access Education (Wisconsin Online Appraisal CE) Environmental and Disclosure Issues (5/2004) – Access Education (Wisconsin Online Appraisal CE) USPAP Basics for Clients (11/2006) – Access Education Valuation of Real Property in a Business Value Context (2005) ICLEF CMA, BPO, Appraisal – What’s the Diff? (3/2006) – Access Education (Realtors – Italian Tour) Pricing Issues in Unusual Properties (3/2006) – Access Education (Realtors – Italian Tour) Current issues in Real Estate Brokerage (3/2006) – Access Education (Realtors – Italian Tour) Recognizing the Mold Issues in Listing Real Estate (3/2006) – Access Education (Realtors – Italian Tour) Introduction to Conservation Easement (2007) Access Education (The Nature Conservancy) Agricultural Conservation Easements (2009) Access Education (The Nature Conservancy) Real Estate Valuations (2008) Indiana Continuing Legal Education Foundation (ICLEF) Income Approach: Strengths, Weaknesses and Areas of Concern for Indiana Tax Appeals (2010) ICLEF Diversity in the Valuation Industry (2011) Appraisal Institute

APPROVED INSTRUCTOR (Courses & Seminars)

Indiana University (Part-time Instructor)

Introduction to Real Estate Analysis (R-305) Real Estate Appraisal (R-440) Real Estate Finance/Investment Analysis (R-443)

Appraisal Foundation

15-hour USPAP 7-hour USPAP

Appraisal Institute

Partial List of Seminars Currently Authorized To Teach

Litigation Skills for the Appraiser; Appraisal Curriculum Overview; Uniform Appraisal Standards for Federal Land Acquisitions (Yellow Book); Introduction to Conservation Easement Valuation, and Analyzing the Effects of Environmental Contamination on Real Property

Partial List of Courses Currently Authorized To Teach

Basic Procedures Basic Principles Business Practices and Ethics

Professional Certificate Programs

Review Designations o Appraisal Review – Residential Instructor o Appraisal Review – General Instructor

Valuation of Conservation Easements: Litigation Appraising

o The Appraiser as an Expert Witness: Preparation and Testimony o Litigation Appraising: Specialized Topics and Applications o Condemnation Appraising: Principles and Applications

o Complex Litigation Appraisal Case Studies