MARKET TRENDS IN RENEWABLE ENERGY AND ENERGY ACCESS · ONSHORE WIND LCOE BY COUNTRY ($/MWH) 0 100...

80

MARKET TRENDS IN RENEWABLE ENERGY AND ENERGY ACCESS SREP Pilot Countries Meeting Takehiro Kawahara 1 February 2017

Transcript of MARKET TRENDS IN RENEWABLE ENERGY AND ENERGY ACCESS · ONSHORE WIND LCOE BY COUNTRY ($/MWH) 0 100...

MARKET TRENDS IN RENEWABLE ENERGY AND ENERGY ACCESS

SREP Pilot Countries Meeting

Takehiro Kawahara

1 February 2017

1

LEVERAGING THE POWER OF BLOOMBERG

Since 1981

Over 15,000 employees

in 192 locations

Generating 5,000 news stories

per day from 150 bureaus

320,000 global clients

Since 2004

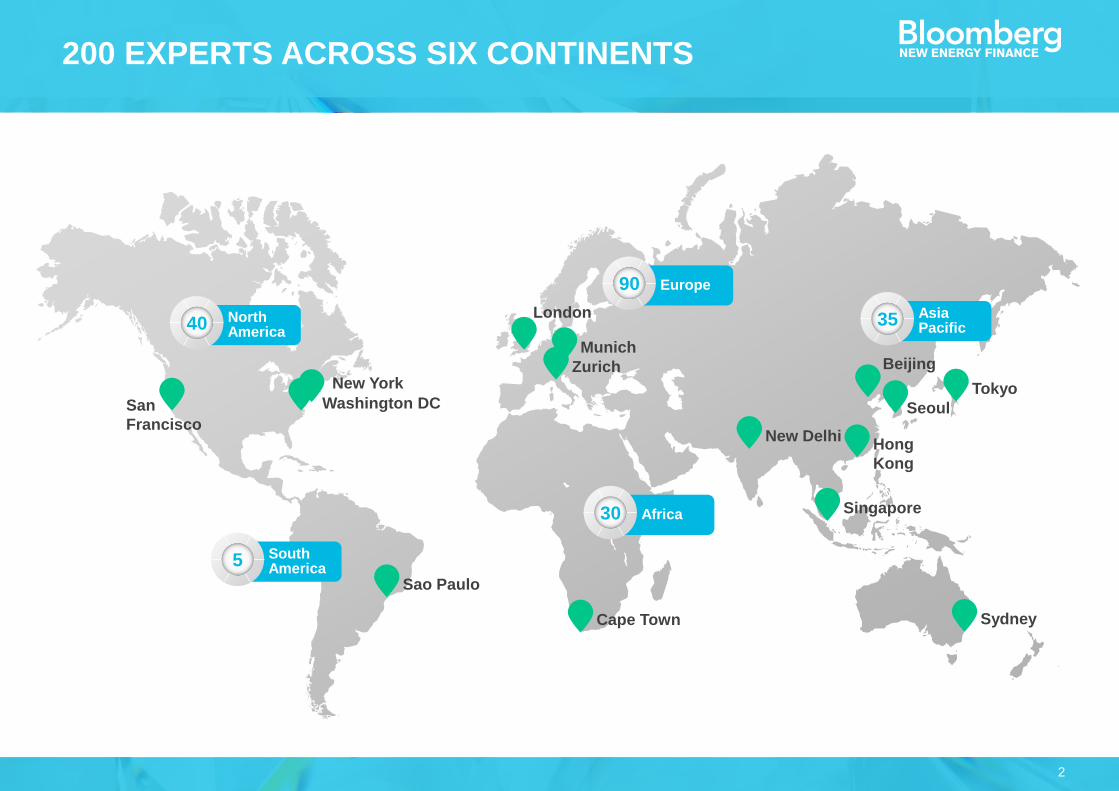

200 employees

in 15 locations on six continents

Generating over 700 Insight

reports annually

2,500 global clients

2

200 EXPERTS ACROSS SIX CONTINENTS

San

Francisco

Washington DC

Sao Paulo

Cape Town Sydney

Singapore

Zurich

Munich

London

New DelhiHong

Kong

Tokyo

Beijing

Seoul

New York

North America

40

SouthAmerica

5

Europe90

Africa30

AsiaPacific

35

3

Europe, Middle East

& Africa

Asia PacificAmericas

PRODUCTS TO HELP YOU UNDERSTAND THE FUTURE OF ENERGY

Solar WindOther

Renewables

Advanced

Transport

Energy Smart

TechnologiesGas

Carbon &

RECs Markets

4

TABLE OF CONTENTS

Renewable energy market trend in emerging countries

Off-grid solar

Policy

Summary

1. RENEWABLE ENERGY MARKET TREND IN EMERGING COUNTRIES

KEY FINDINGS FROM CLIMATE SCOPE PROJECT

7

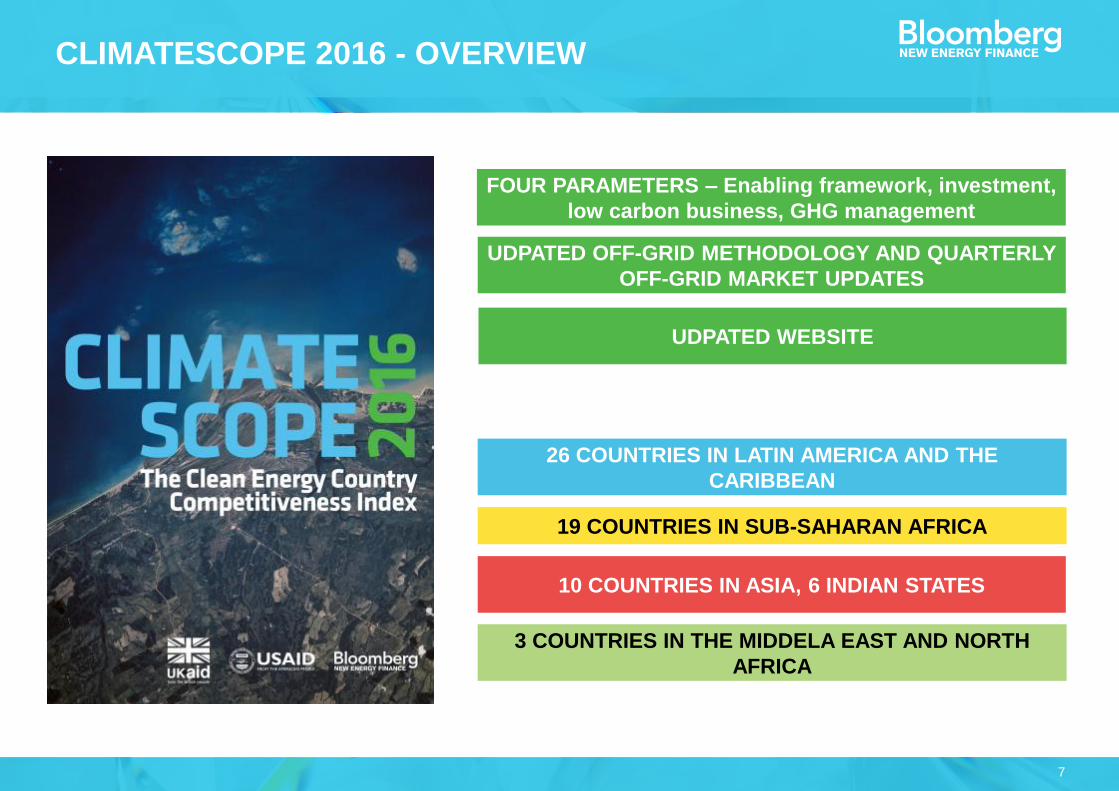

CLIMATESCOPE 2016 - OVERVIEW

FOUR PARAMETERS – Enabling framework, investment,

low carbon business, GHG management

26 COUNTRIES IN LATIN AMERICA AND THE

CARIBBEAN

19 COUNTRIES IN SUB-SAHARAN AFRICA

10 COUNTRIES IN ASIA, 6 INDIAN STATES

UDPATED OFF-GRID METHODOLOGY AND QUARTERLY

OFF-GRID MARKET UPDATES

3 COUNTRIES IN THE MIDDELA EAST AND NORTH

AFRICA

UDPATED WEBSITE

8

CLIMATESCOPE COUNTRY COVERAGE

58 developing nations and 6 Indian states

9

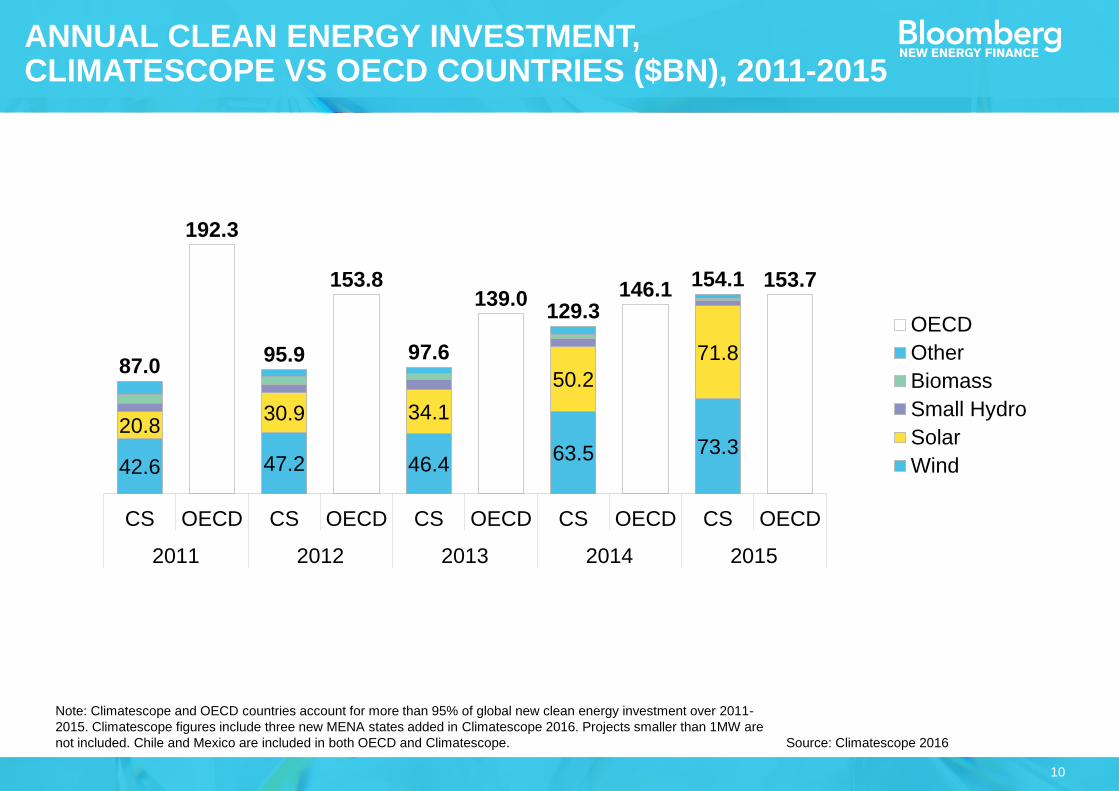

Note: Climatescope and OECD countries account for more than 95% of global annual Source: Climatescope 2016

ANNUAL CLEAN ENERGY CAPACITY ADDITIONS, CLIMATESCOPE VS OECD COUNTRIES (GW), 2011-2015

20.5 18.5 17.928.2

39.52.3 2.111.6

13.4

19.63.2

8.0

29.7

47.5

27.6

56.5

37.244.3

48.451.6

69.8

59.2

CS OECD CS OECD CS OECD CS OECD CS OECD

2011 2012 2013 2014 2015

OECD

Other

Biomass

Small hydro

Solar

Wind

10

Note: Climatescope and OECD countries account for more than 95% of global new clean energy investment over 2011-

2015. Climatescope figures include three new MENA states added in Climatescope 2016. Projects smaller than 1MW are

not included. Chile and Mexico are included in both OECD and Climatescope. Source: Climatescope 2016

ANNUAL CLEAN ENERGY INVESTMENT, CLIMATESCOPE VS OECD COUNTRIES ($BN), 2011-2015

42.6 47.2 46.463.5 73.3

20.830.9 34.1

50.2

71.887.0

192.3

95.9

153.8

97.6

139.0129.3

146.1154.1 153.7

CS OECD CS OECD CS OECD CS OECD CS OECD

2011 2012 2013 2014 2015

OECD

Other

Biomass

Small Hydro

Solar

Wind

11

Source: Climatescope 2016

NON-OECD VS OECD SHARE OF CLEAN ENERGY INVESTMENT INTO CLIMATESCOPE COUNTRIES (%), EXCLUDES INVESTMENT IN CHINA), 2010-2015

59.0%65.4% 59.2% 54.9%

47.0% 45.8%

13.6%10.2%

8.9%7.5%

6.9% 5.2%

20.7% 18.2%24.9%

24.1%31.2% 40.9%

6.8% 6.2% 7.0%13.5% 14.9%

8.0%

2010 2011 2012 2013 2014 2015

Development banks - OECD

OECD

Development banks non-OECD

Non-OECD

12

Source: Climatescope 2016

AVERAGE DISCLOSED CAPEX FOR ONSHORE WIND AND PV PROJECTS IN CLIMATESCOPE COUNTRIES ($M/MW)

1.77 1.892.15 2.23 2.18 2.02

5.52

4.104.54

2.68 2.72

2.15

2010 2011 2012 2013 2014 2015

Solar PV

Onshore wind

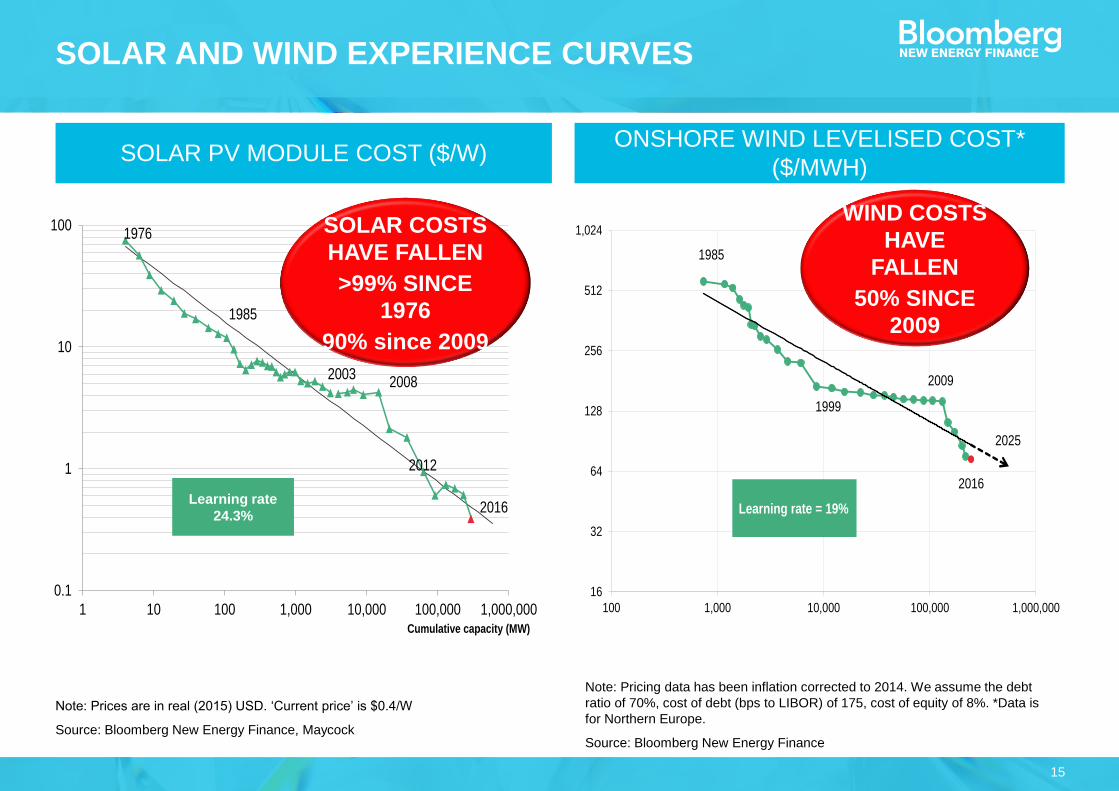

COST OF RENEWABLES

14

LEVELISED COST OF ELECTRICITY (LCOE): DEFINITION

15

y = 3,582.42x-0.30

R² = 0.91

16

32

64

128

256

512

1,024

100 1,000 10,000 100,000 1,000,000

1985

2025

2016

Learning rate = 19%

1999

2009

WIND COSTS

HAVE

FALLEN

50% SINCE

2009

SOLAR AND WIND EXPERIENCE CURVES

Note: Prices are in real (2015) USD. ‘Current price’ is $0.4/W

Source: Bloomberg New Energy Finance, Maycock

Note: Pricing data has been inflation corrected to 2014. We assume the debt

ratio of 70%, cost of debt (bps to LIBOR) of 175, cost of equity of 8%. *Data is

for Northern Europe.

Source: Bloomberg New Energy Finance

0.1

1

10

100

1 10 100 1,000 10,000 100,000 1,000,000

1976

1985

2003

2012

Cumulative capacity (MW)

2016

2008

Learning rate

24.3%

SOLAR COSTS

HAVE FALLEN

>99% SINCE

1976

90% since 2009

SOLAR PV MODULE COST ($/W)ONSHORE WIND LEVELISED COST*

($/MWH)

16

FORECAST OF INTEGRATED PRODUCTION COST FOR C-SI MODULE (US CENT/W)

17

Note: The reduction magnitude is our best indicative estimate of the potential impact. The magnitude could vary

depending on the technological advancements and efficiency improvements. Source: Bloomberg New Energy Finance

WIND PROJECT CAPITAL EXPENDITURE COST (PER MW NAMEPLATE CAPACITY) REDUCTION DRIVERS (%)

Rotor Drivetrain, nacelle Tower BoP & development cost

100% -0.3% -6%1% -4%

91%

2015 Rotor Drivetrain, nacelle Tower Balance of plant &development cost

2025

18

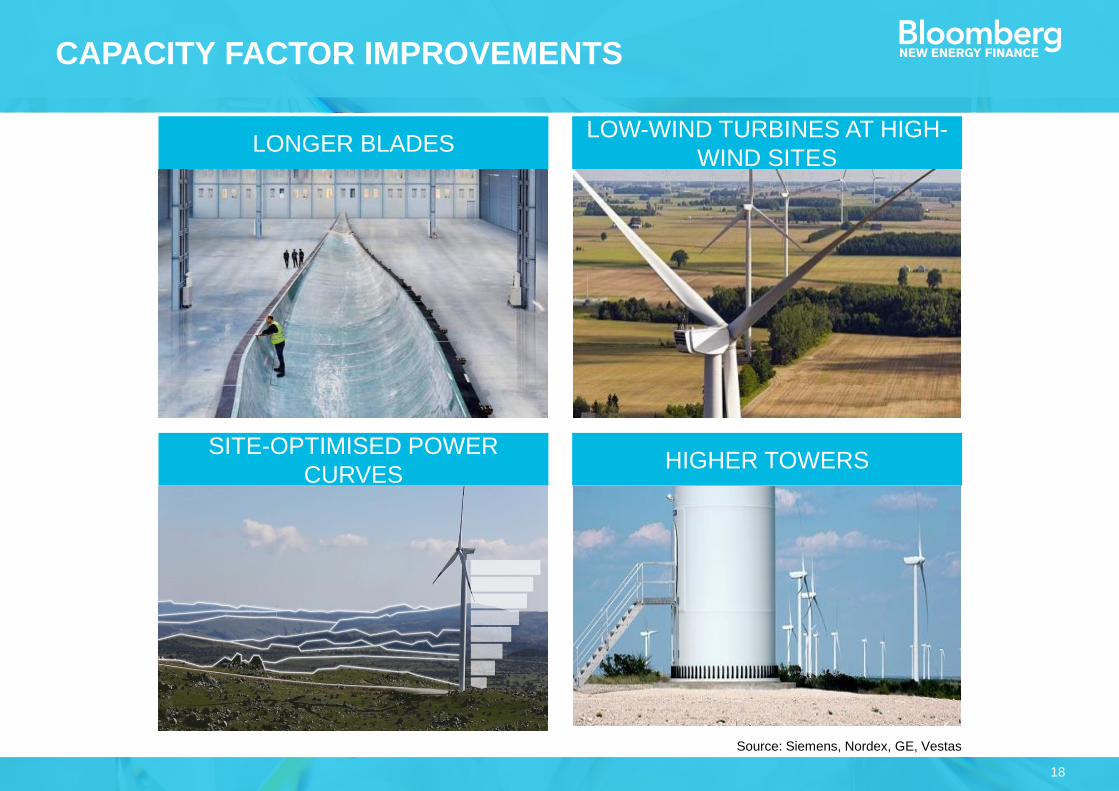

CAPACITY FACTOR IMPROVEMENTS

LONGER BLADESLOW-WIND TURBINES AT HIGH-

WIND SITES

SITE-OPTIMISED POWER

CURVESHIGHER TOWERS

Source: Siemens, Nordex, GE, Vestas

19

Note: Averages are capacity-weighted. We calculate the capacity factor with our proprietary Wind Farm

Capacity Factor Tool using real project data and wind resource data provided by 3TIER by Vaisala. We

assume P90 value in the capacity factor tool.

Source: Bloomberg New Energy

Finance

GLOBAL (EX. CHINA) ONSHORE WIND CAPACITY FACTOR IMPROVEMENTS, 1997-2015 (%)

0%

10%

20%

30%

40%

50%

60%

1980 1984 1988 1992 1996 2000 2004 2008 2012 2016 2020

Germany Denmark UK Spain US Canada

299MW

20

ONSHORE WIND LCOE BY COUNTRY ($/MWH)

0 100 200 300 400 500 600

IndiaSouth AfricaMozambique

MalawiKyrgyzstan

EthiopiaYemen

SomaliaZimbabwe

ZambiaTajikistanTanzania

LiberiaGhana

PakistanNepal

MyanmarAfghanistan

DRCNigeriaKenya

UgandaSudan

PalestineSouth SudanBangladesh

RwandaSierra Leone

LCOE Range Mid

21

SOLAR PV LCOE BY COUNTRY ($/MWH)

0 100 200 300 400 500 600 700

IndiaSouth Africa

PakistanMyanmar

YemenEthiopia

UgandaZimbabweTanzania

Kenya

NepalBangladesh

NigeriaGhana

ZambiaMalawi

Tajikistan

KyrgyzstanSudan

RwandaSierra Leone

Liberia

South SudanMozambique

Somalia

PalestineDRC

Afghanistan

LCOE Range Mid

22

SMALL HYDRO LCOE BY COUNTRY ($/MWH)

0 50 100 150 200 250

IndiaNepal

MyanmarTajikistanTanzania

South AfricaGhana

DRCBangladesh

UgandaMozambique

ZimbabweKyrgyzstan

KenyaMalawiYemenZambiaNigeria

AfghanistanLiberia

PakistanSierra Leone

RwandaSudan

EthiopiaSouth Sudan

SomaliaPalestine

LCOE Range Mid

23

BIOMASS INCINERATION LCOE BY COUNTRY ($/MWH)

0 50 100 150 200 250 300 350 400

IndiaTajikistan

BangladeshPakistan

South AfricaGhana

KyrgyzstanDRC

ZimbabweKenya

NigeriaEthiopia

LiberiaTanzaniaMyanmar

Sierra LeoneNepal

SudanMozambique

YemenMalawi

South SudanZambiaUganda

AfghanistanRwandaSomalia

Palestine

LCOE Range Mid

24

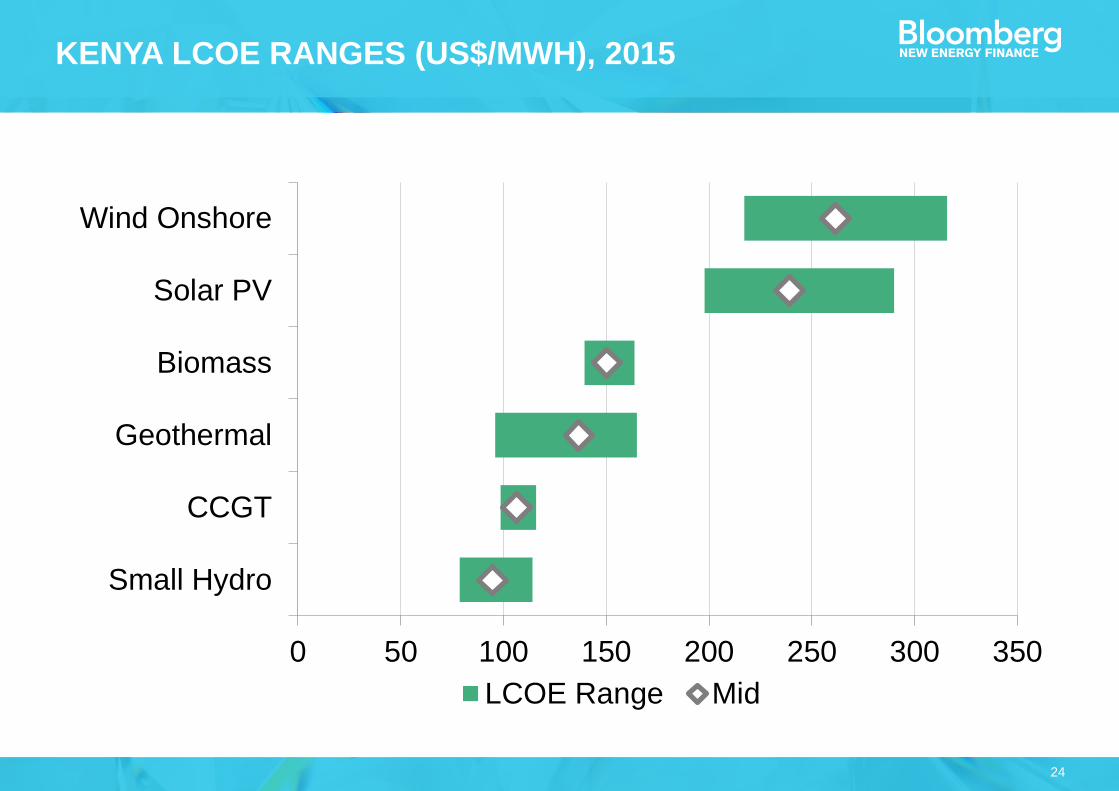

KENYA LCOE RANGES (US$/MWH), 2015

0 50 100 150 200 250 300 350

Small Hydro

CCGT

Geothermal

Biomass

Solar PV

Wind Onshore

LCOE Range Mid

25

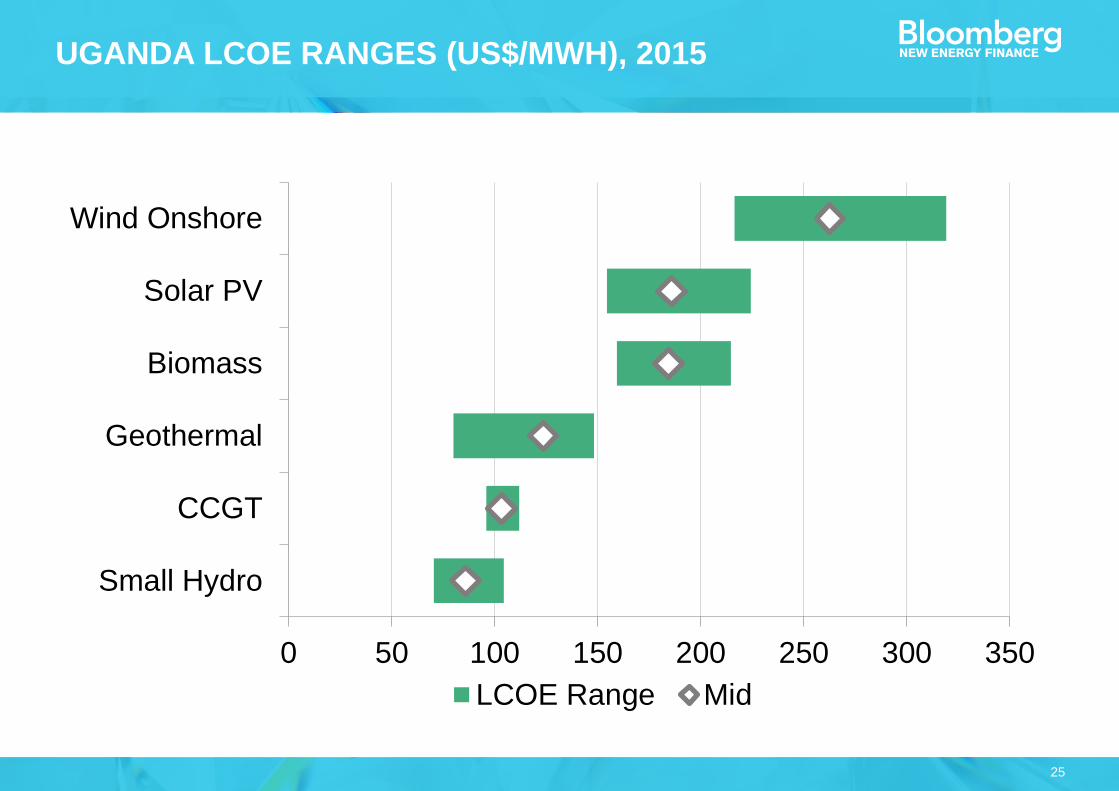

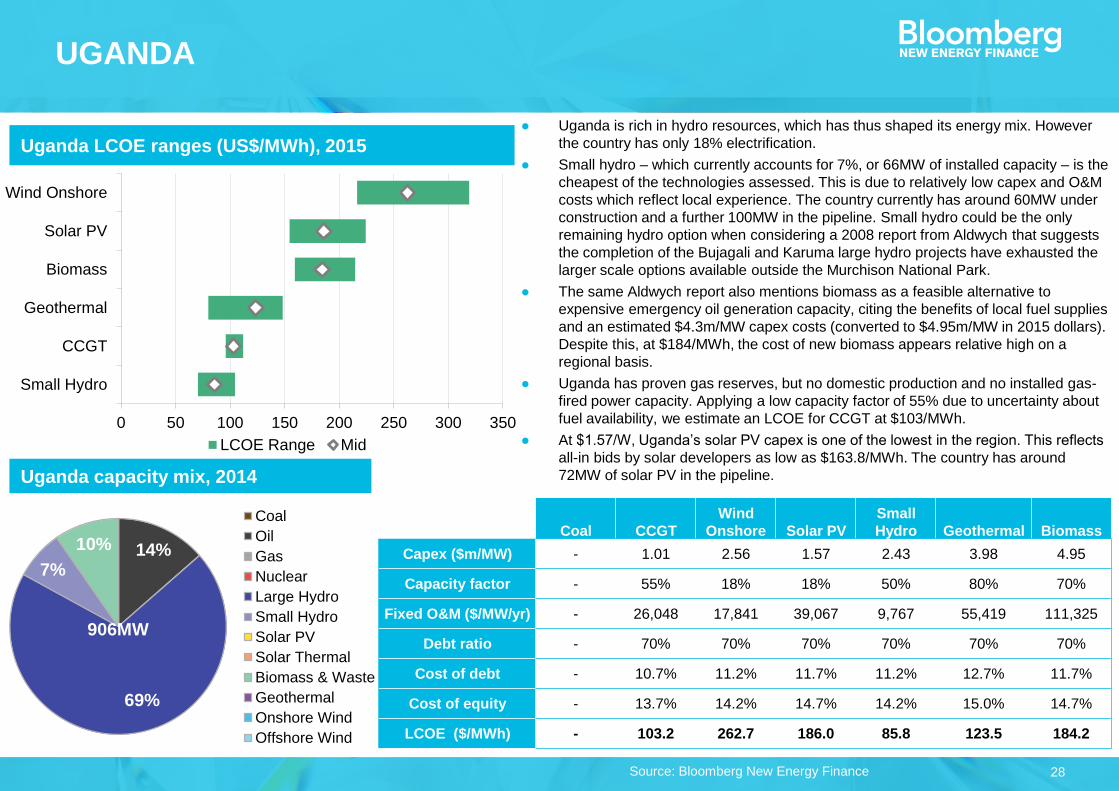

UGANDA LCOE RANGES (US$/MWH), 2015

0 50 100 150 200 250 300 350

Small Hydro

CCGT

Geothermal

Biomass

Solar PV

Wind Onshore

LCOE Range Mid

26

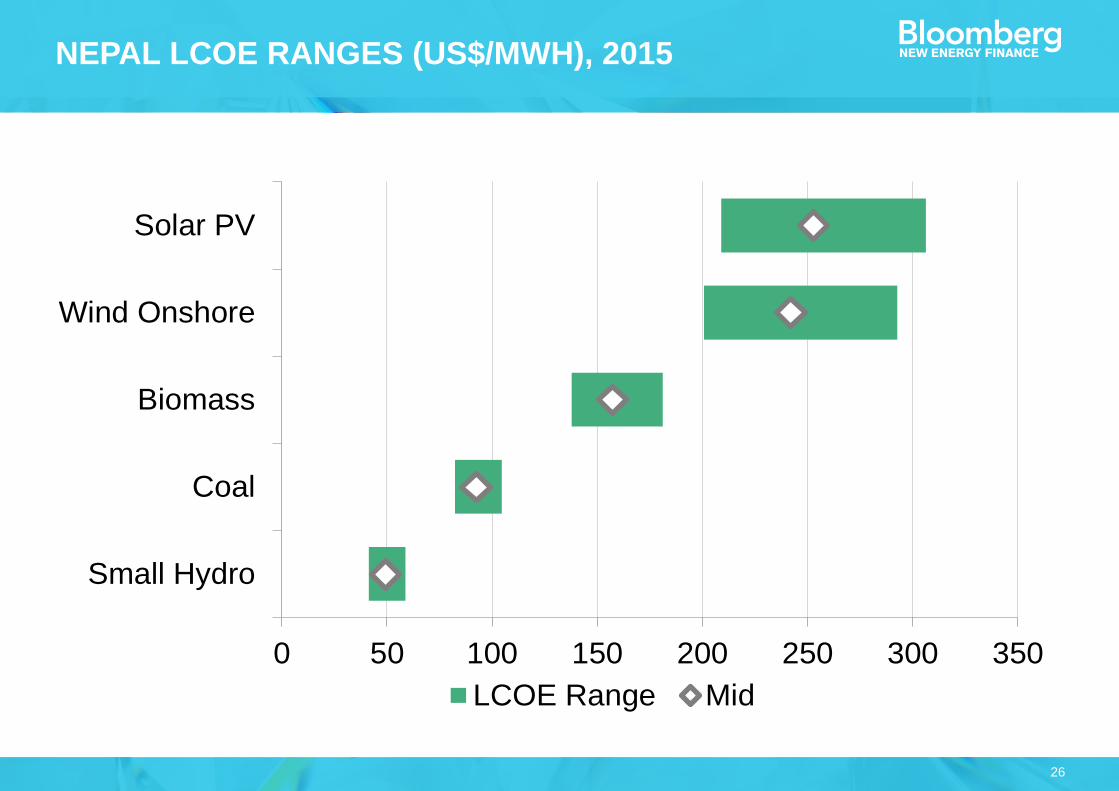

NEPAL LCOE RANGES (US$/MWH), 2015

0 50 100 150 200 250 300 350

Small Hydro

Coal

Biomass

Wind Onshore

Solar PV

LCOE Range Mid

27

Kenya LCOE ranges (US$/MWh), 2015

KENYA

Source: Bloomberg New Energy Finance

Kenya capacity mix, 2014

● Around 32% of Kenya's installed capacity comes from oil. These plants were

commissioned in the 1980s and 1990s when diesel was relatively cheap. As

oil prices rose, other technologies such as geothermal (25%) and hydro

(38%) and more recently wind have been developed.

● Kenya plans to make clean energy a significant part of its ambitious 'Least

Cost Power Development Plan' which targets 22.7GW of capacity by 2033

● Capex for wind is still high in Kenya at around $2.6m/MW. This figure is

based on disclosed data from the Isiolo I wind farm. Recently a number of

other projects were financed, including the 310MW Lake Turkana wind farm.

● The country has good potential for small hydro as well as significant

geothermal resources (estimated at 10GW) which is to undergo a fast track

development plan by the government owned Geothermal Development

Company (GDC).

● Solar has struggled to gain a footing in Kenya despite the country’s feed-in-

tariff, as the rate offered has proven to be too low for project developers.

● Kenya has no proven domestic reserves of natural gas or coal however it

does have some existing natural gas capacity which suggests supply is

available.

Coal CCGT

Wind

Onshore Solar PV

Small

Hydro Geothermal Biomass

Capex ($m/MW) - 1.41 2.60 2.12 2.66 4.04 2.34

Capacity factor - 75% 21% 19% 60% 80% 80%

Fixed O&M ($/MW/yr) - 29,797 38,000 35,000 70,000 60,616 58,000

Debt ratio - 72% 70% 70% 70% 70% 70%

Cost of debt - 11.6% 12.1% 12.6% 12.1% 13.6% 12.6%

Cost of equity - 14.6% 15.1% 15.6% 15.1% 16.6% 15.6%

LCOE ($/MWh) - 106.4 261.6 239.4 94.7 136.8 150.4

0 50 100 150 200 250 300 350

Small Hydro

CCGT

Geothermal

Biomass

Solar PV

Wind Onshore

LCOE Range Mid

32%

33%

5%

25%

Coal

Oil

Gas

Nuclear

Large Hydro

Small Hydro

Solar PV

Solar Thermal

Biomass & Waste

Geothermal

Onshore Wind

Offshore Wind

2,193MW

28

Uganda LCOE ranges (US$/MWh), 2015

UGANDA

Source: Bloomberg New Energy Finance

Uganda capacity mix, 2014

Coal CCGT

Wind

Onshore Solar PV

Small

Hydro Geothermal Biomass

Capex ($m/MW) - 1.01 2.56 1.57 2.43 3.98 4.95

Capacity factor - 55% 18% 18% 50% 80% 70%

Fixed O&M ($/MW/yr) - 26,048 17,841 39,067 9,767 55,419 111,325

Debt ratio - 70% 70% 70% 70% 70% 70%

Cost of debt - 10.7% 11.2% 11.7% 11.2% 12.7% 11.7%

Cost of equity - 13.7% 14.2% 14.7% 14.2% 15.0% 14.7%

LCOE ($/MWh) - 103.2 262.7 186.0 85.8 123.5 184.2

0 50 100 150 200 250 300 350

Small Hydro

CCGT

Geothermal

Biomass

Solar PV

Wind Onshore

LCOE Range Mid

● Uganda is rich in hydro resources, which has thus shaped its energy mix. However

the country has only 18% electrification.

● Small hydro – which currently accounts for 7%, or 66MW of installed capacity – is the

cheapest of the technologies assessed. This is due to relatively low capex and O&M

costs which reflect local experience. The country currently has around 60MW under

construction and a further 100MW in the pipeline. Small hydro could be the only

remaining hydro option when considering a 2008 report from Aldwych that suggests

the completion of the Bujagali and Karuma large hydro projects have exhausted the

larger scale options available outside the Murchison National Park.

● The same Aldwych report also mentions biomass as a feasible alternative to

expensive emergency oil generation capacity, citing the benefits of local fuel supplies

and an estimated $4.3m/MW capex costs (converted to $4.95m/MW in 2015 dollars).

Despite this, at $184/MWh, the cost of new biomass appears relative high on a

regional basis.

● Uganda has proven gas reserves, but no domestic production and no installed gas-

fired power capacity. Applying a low capacity factor of 55% due to uncertainty about

fuel availability, we estimate an LCOE for CCGT at $103/MWh.

● At $1.57/W, Uganda’s solar PV capex is one of the lowest in the region. This reflects

all-in bids by solar developers as low as $163.8/MWh. The country has around

72MW of solar PV in the pipeline.

14%

69%

7%

10%

Coal

Oil

Gas

Nuclear

Large Hydro

Small Hydro

Solar PV

Solar Thermal

Biomass & Waste

Geothermal

Onshore Wind

Offshore Wind

906MW

29

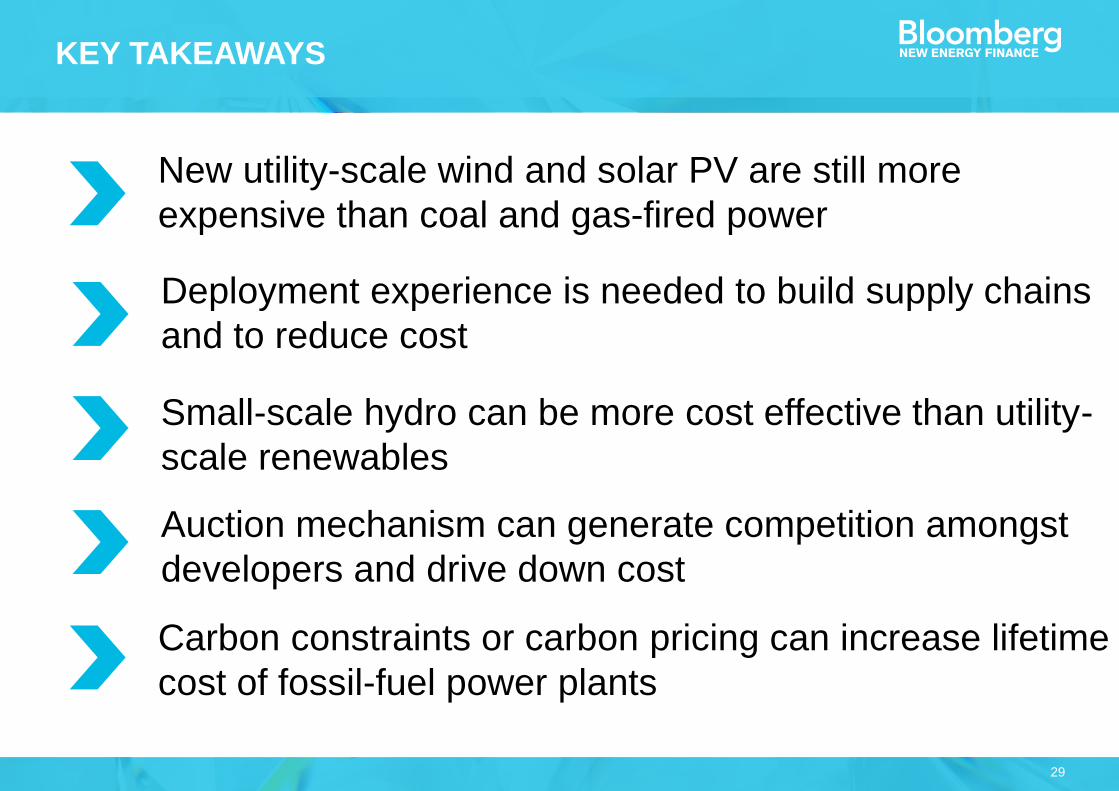

Deployment experience is needed to build supply chains

and to reduce cost

KEY TAKEAWAYS

Small-scale hydro can be more cost effective than utility-

scale renewables

Auction mechanism can generate competition amongst

developers and drive down cost

Carbon constraints or carbon pricing can increase lifetime

cost of fossil-fuel power plants

New utility-scale wind and solar PV are still more

expensive than coal and gas-fired power

2. OFF-GRID SOLAR

31

Note: Figures refer to 2012 data.

Source: Bloomberg New Energy Finance,

World Bank, GOGLA, IFC Lighting Global

SHARE OF POPULATION WITHOUT GRID ACCESS(% OF TOTAL)

0% Lowest

50% Mid

99% Highest

32

Source: Bloomberg New Energy Finance,

Climatescope

NATIONAL ELECTRIFICATION RATES(% OF TOTAL POPULATION)

0

20

40

60

80

100

Uganda Rwanda Kenya Tanzania Ethiopia Senegal Nigeria

0

20

40

60

80

100

Myanmar Nepal Bangladesh Pakistan India Indonesia Sri Lanka

2010 2011 2012 2013 2014 2015

0

20

40

60

80

100

Nicaragua Suriname Guatemala Panama Peru Honduras Colombia

33

Photo credits: Lighting Global, Wikipedia

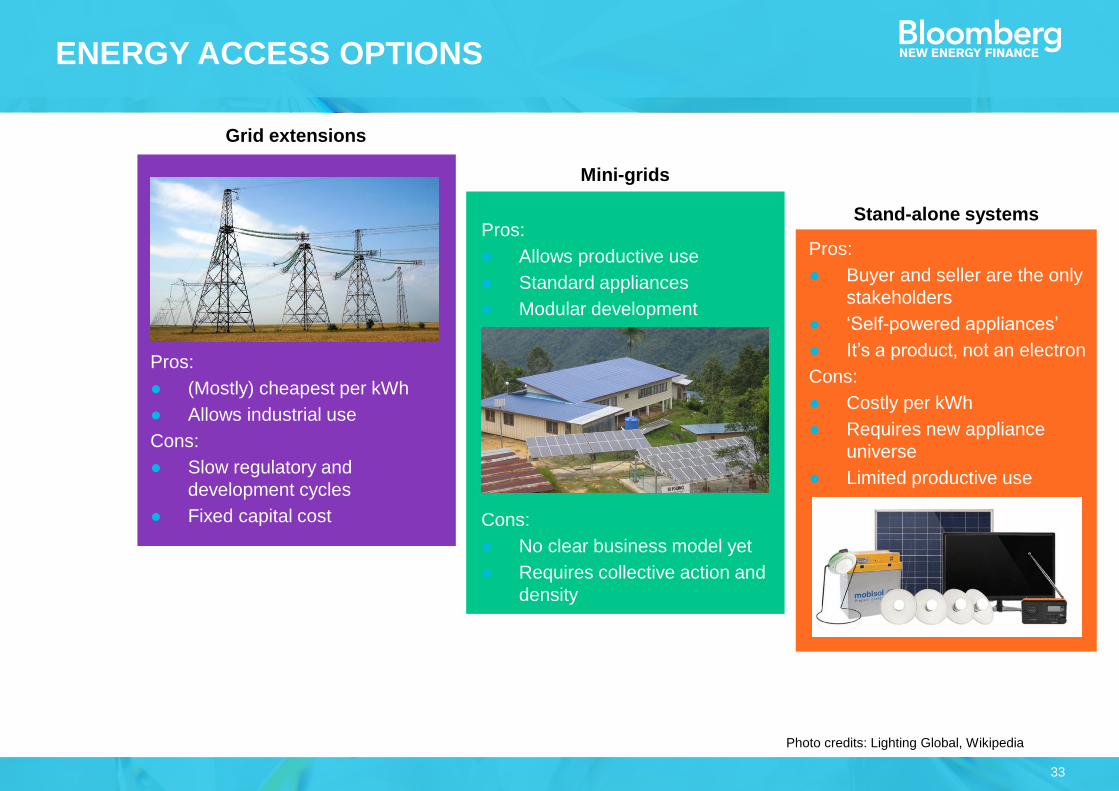

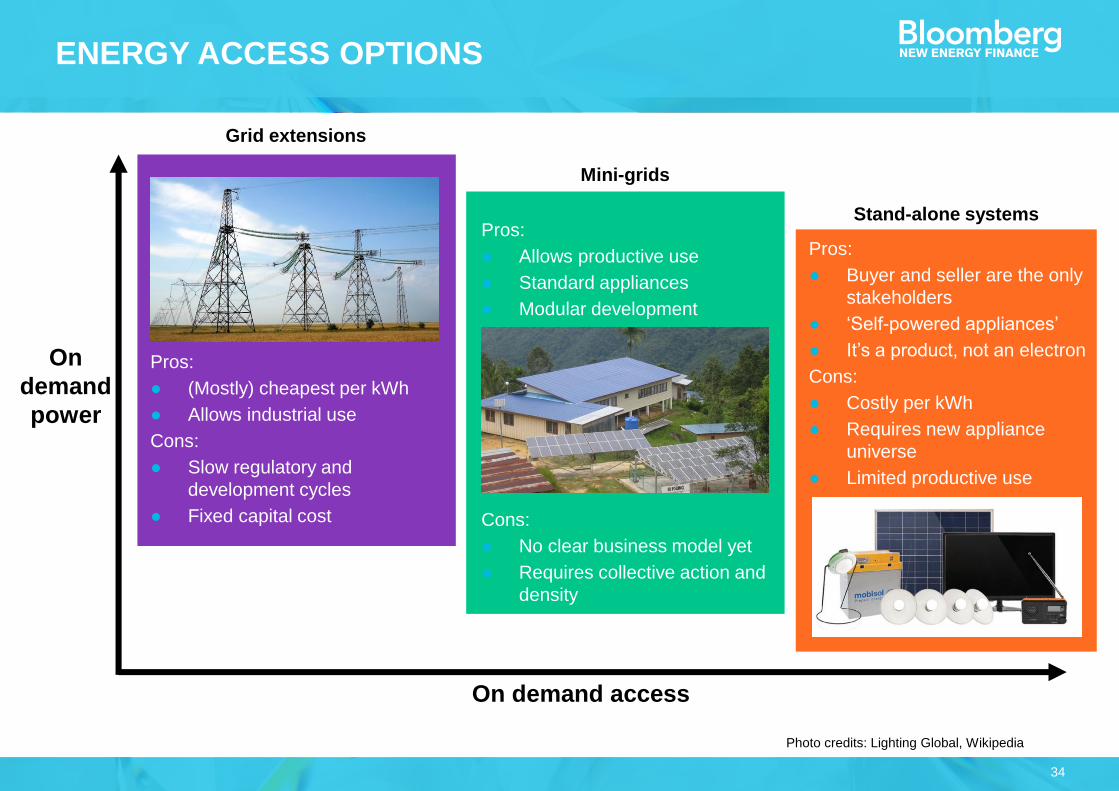

ENERGY ACCESS OPTIONS

Pros:

● Allows productive use

● Standard appliances

● Modular development

Cons:

● No clear business model yet

● Requires collective action and

density

Pros:

● (Mostly) cheapest per kWh

● Allows industrial use

Cons:

● Slow regulatory and

development cycles

● Fixed capital cost

Pros:

● Buyer and seller are the only

stakeholders

● ‘Self-powered appliances’

● It’s a product, not an electron

Cons:

● Costly per kWh

● Requires new appliance

universe

● Limited productive use

Grid extensions

Mini-grids

Stand-alone systems

34

Photo credits: Lighting Global, Wikipedia

ENERGY ACCESS OPTIONS

On demand access

On

demand

power

Pros:

● Allows productive use

● Standard appliances

● Modular development

Cons:

● No clear business model yet

● Requires collective action and

density

Pros:

● (Mostly) cheapest per kWh

● Allows industrial use

Cons:

● Slow regulatory and

development cycles

● Fixed capital cost

Pros:

● Buyer and seller are the only

stakeholders

● ‘Self-powered appliances’

● It’s a product, not an electron

Cons:

● Costly per kWh

● Requires new appliance

universe

● Limited productive use

Grid extensions

Mini-grids

Stand-alone systems

35

Note: Prices are in real (2015) USD. ‘Current price’ is $0.61/W

Source: Bloomberg New Energy Finance, Maycock

PV MODULE COST EXPERIENCE CURVE (USD/W)

0.1

1

10

100

1 10 100 1,000 10,000 100,000 1,000,000

1976

1985

2003

2012

Cumulative capacity (MW)

2016

2008

36

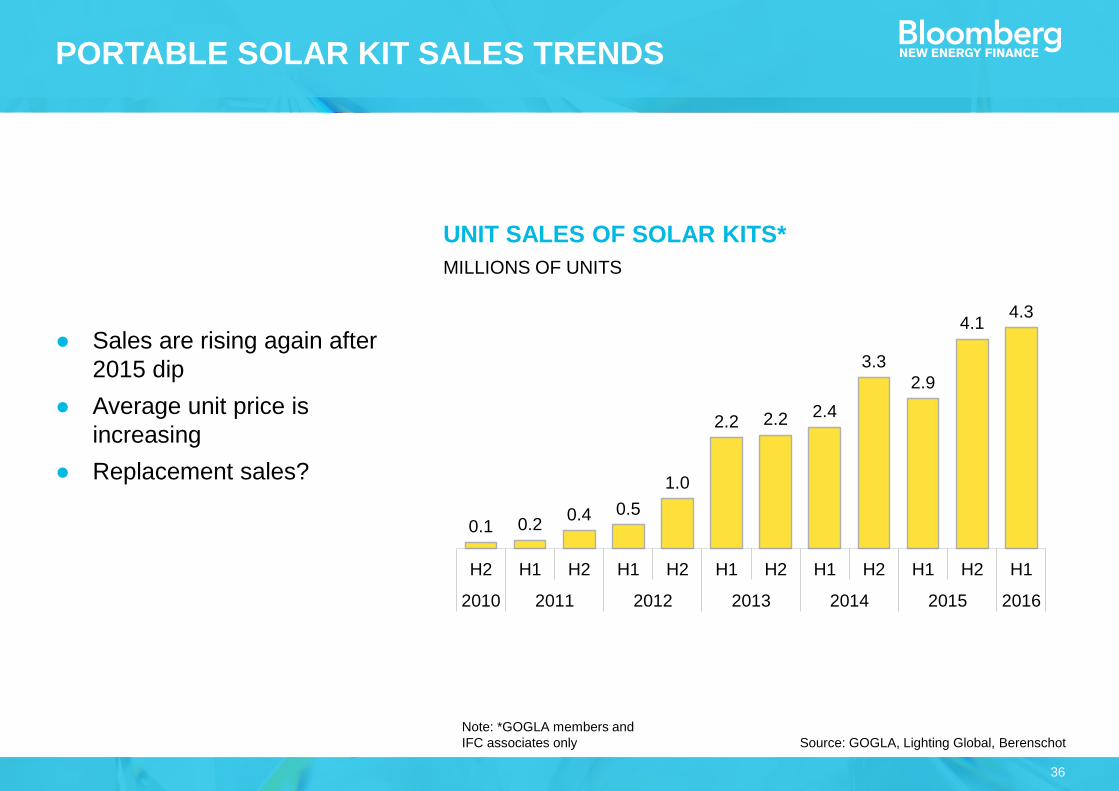

PORTABLE SOLAR KIT SALES TRENDS

● Sales are rising again after

2015 dip

● Average unit price is

increasing

● Replacement sales?

Note: *GOGLA members and

IFC associates only Source: GOGLA, Lighting Global, Berenschot

UNIT SALES OF SOLAR KITS*

MILLIONS OF UNITS

0.1 0.20.4 0.5

1.0

2.2 2.2 2.4

3.3

2.9

4.14.3

H2 H1 H2 H1 H2 H1 H2 H1 H2 H1 H2 H1

2010 2011 2012 2013 2014 2015 2016

37

Source: Ignite Power survey. N=250

WHO BUYS SOLAR HOME SYSTEMS?SURVEY DATA FROM RWANDA

Previously used technology…

17%

26%

35%

22%

Candles Kerosenelamp

Torch Other

3.9

3.6 3.6

4.2

Candles Kerosenelamp

Torch Other

…and its cost (USD/month for

median user)

38

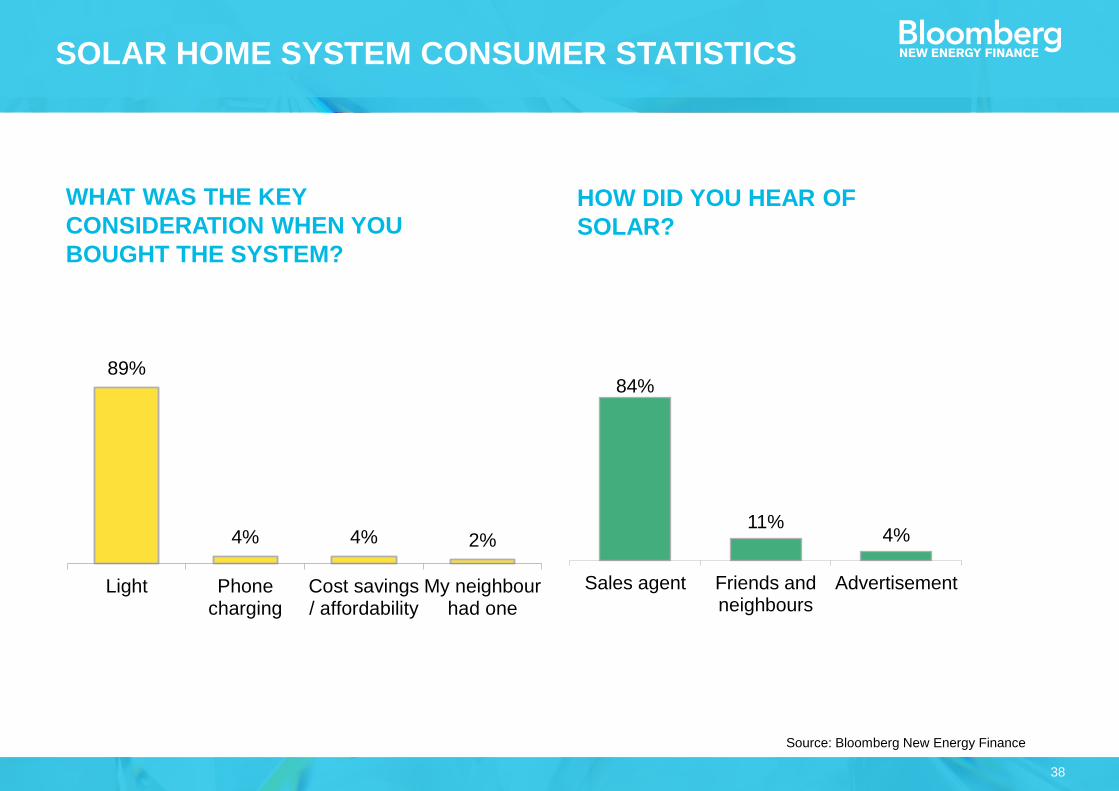

Source: Bloomberg New Energy Finance

SOLAR HOME SYSTEM CONSUMER STATISTICS

HOW DID YOU HEAR OF

SOLAR?

84%

11%4%

Sales agent Friends andneighbours

Advertisement

Total

WHAT WAS THE KEY

CONSIDERATION WHEN YOU

BOUGHT THE SYSTEM?

89%

4% 4% 2%

Light Phonecharging

Cost savings/ affordability

My neighbourhad one

Total

39

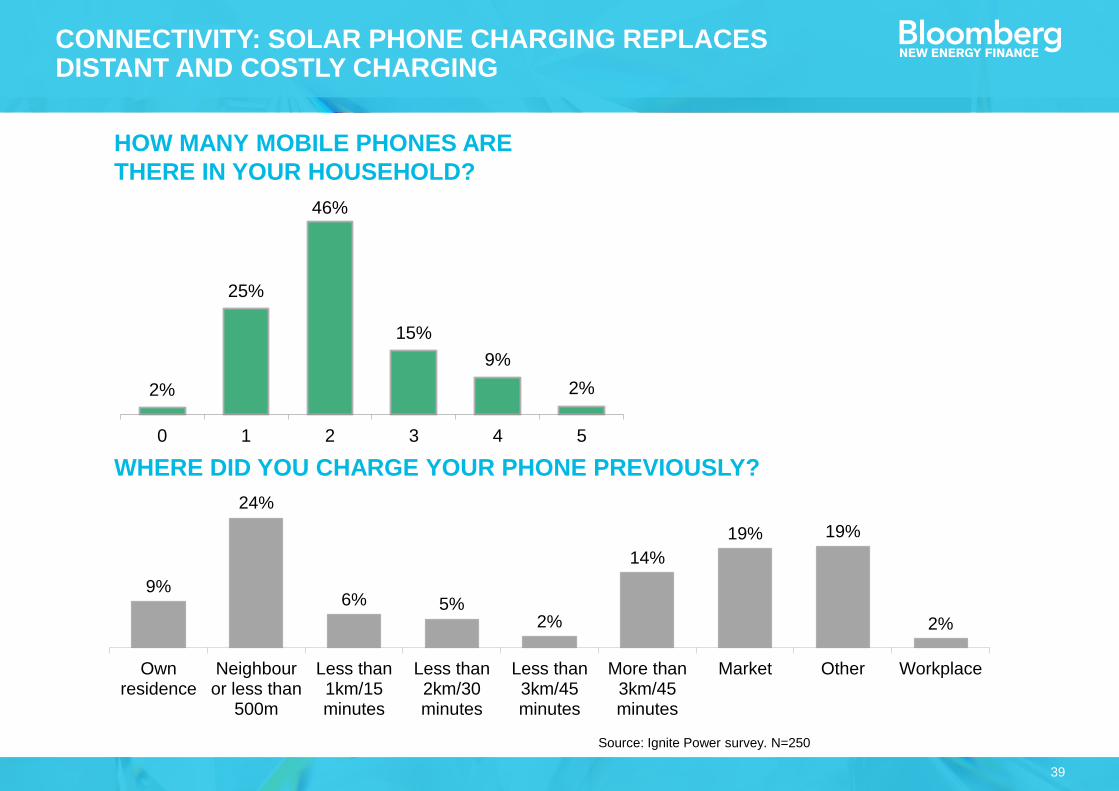

CONNECTIVITY: SOLAR PHONE CHARGING REPLACES DISTANT AND COSTLY CHARGING

HOW MANY MOBILE PHONES ARE

THERE IN YOUR HOUSEHOLD?

Source: Ignite Power survey. N=250

WHERE DID YOU CHARGE YOUR PHONE PREVIOUSLY?

2%

25%

46%

15%

9%

2%

0 1 2 3 4 5

9%

24%

6% 5%2%

14%

19% 19%

2%

Ownresidence

Neighbouror less than

500m

Less than1km/15minutes

Less than2km/30minutes

Less than3km/45minutes

More than3km/45minutes

Market Other Workplace

40

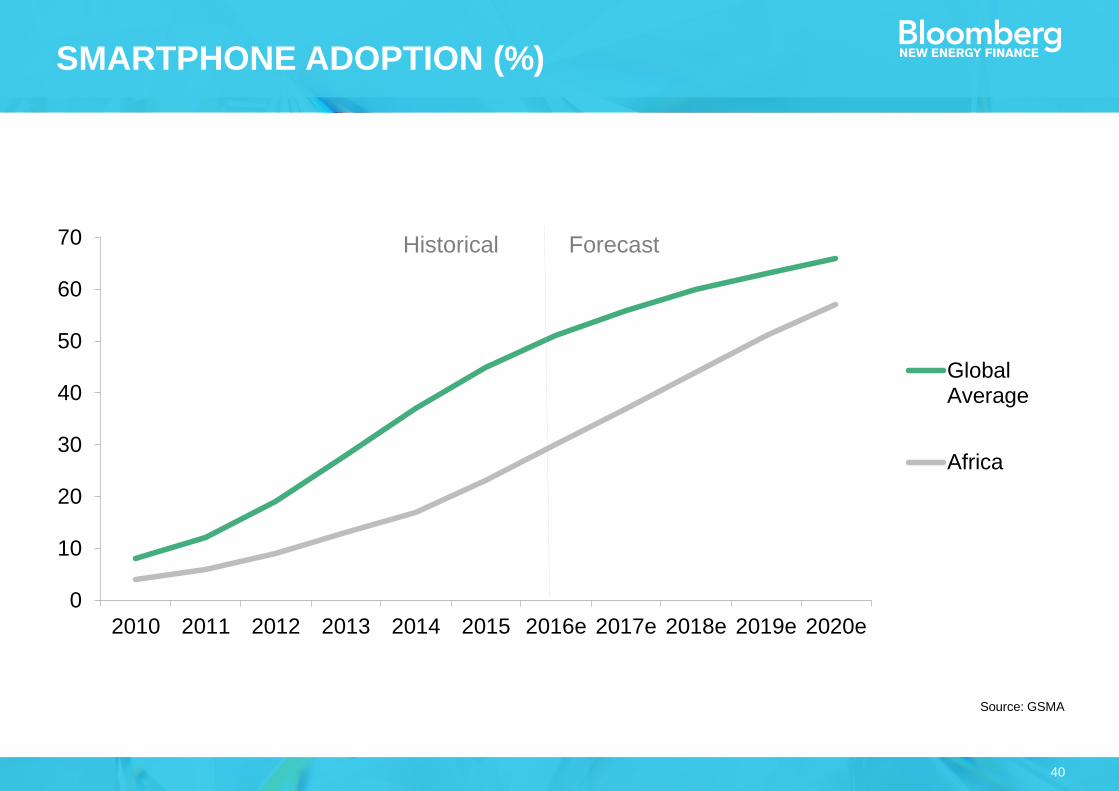

0

10

20

30

40

50

60

70

2010 2011 2012 2013 2014 2015 2016e 2017e 2018e 2019e 2020e

GlobalAverage

Africa

Historical Forecast

SMARTPHONE ADOPTION (%)

Source: GSMA

41

0

100

200

300

400

2014(super-

efficient)

PV Battery Balance ofsystem

Lights Appliances 2020

PRODUCTION COST DEVELOPMENTS, NOMINAL $ PER UNIT

Source: Powering a Home with Just 25 Watts of Solar PV: SuperEfficient Appliances

Can Enable Expanded Off-Grid Energy Service Using Small Solar Power Systems,

Dalberg, EERE Solid-State Lighting Programme, Bloomberg New Energy Finance ,

GOGLA, IFC Lighting Global

0

5

10

15

20

2014 PV Battery Balance ofsystem

Light 2020

Entry-level portable light,

eg d.light S2

Solar home system with

TV, radio, lights

-29%-10% -11%-3%

-50%

-8% -28%

-9% -4%Large portable light,

eg d.light s300

-45%-7%

-7% -3% -3% -26%

-5%

0

1

2

3

4

5

2015 PV Battery Balance ofsystem

LEDs 2020

PAY-AS-YOU-GO

43

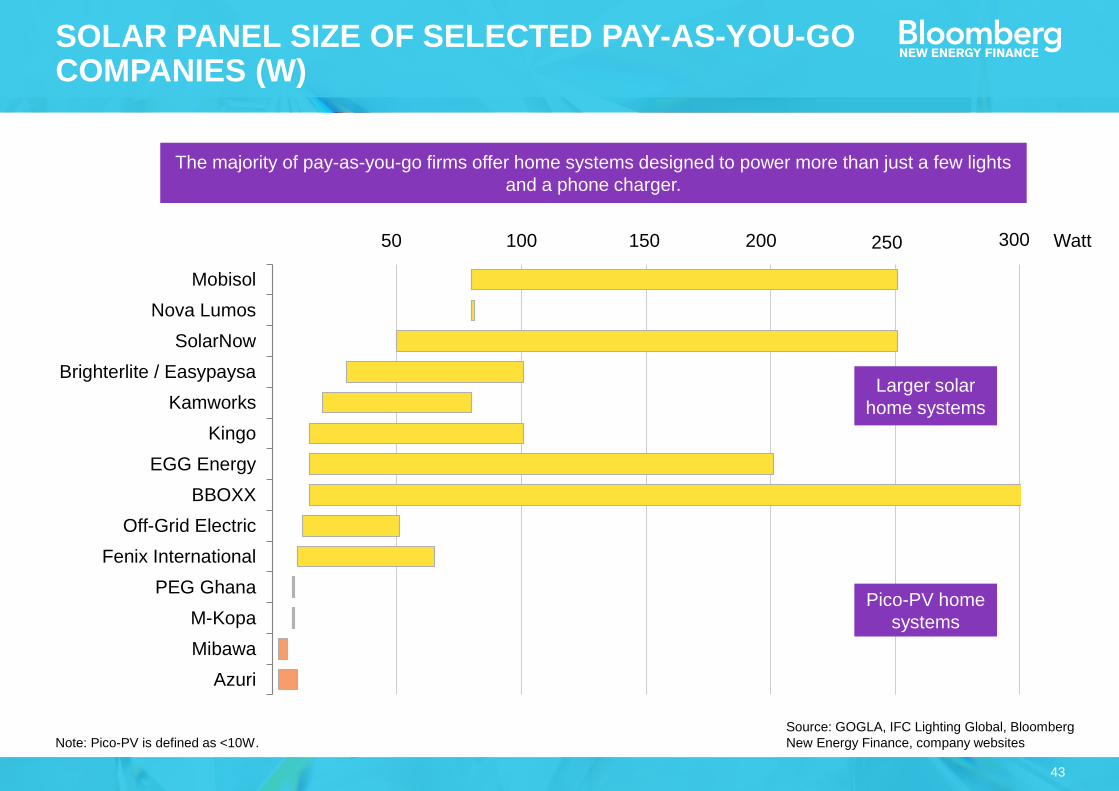

Azuri

Mibawa

M-Kopa

PEG Ghana

Fenix International

Off-Grid Electric

BBOXX

EGG Energy

Kingo

Kamworks

Brighterlite / Easypaysa

SolarNow

Nova Lumos

Mobisol

Note: Pico-PV is defined as <10W.

Source: GOGLA, IFC Lighting Global, Bloomberg

New Energy Finance, company websites

SOLAR PANEL SIZE OF SELECTED PAY-AS-YOU-GO COMPANIES (W)

50 100 150 200 250 300 Watt

The majority of pay-as-you-go firms offer home systems designed to power more than just a few lights

and a phone charger.

Pico-PV home

systems

Larger solar

home systems

44

Note: The list of companies represents a sample and does not claim to be comprehensive.

Source: GOGLA, IFC Lighting Global,

Bloomberg New Energy Finance

THE SHIFT TO PAYG CHANGES THE DYNAMICS BETWEEN THE CUSTOMER AND THE PROVIDER

Technology risk

Data

Higher value

services

Service guarantee

Stronger relationships between customer and provider

Financing

Upsell opportunity

45

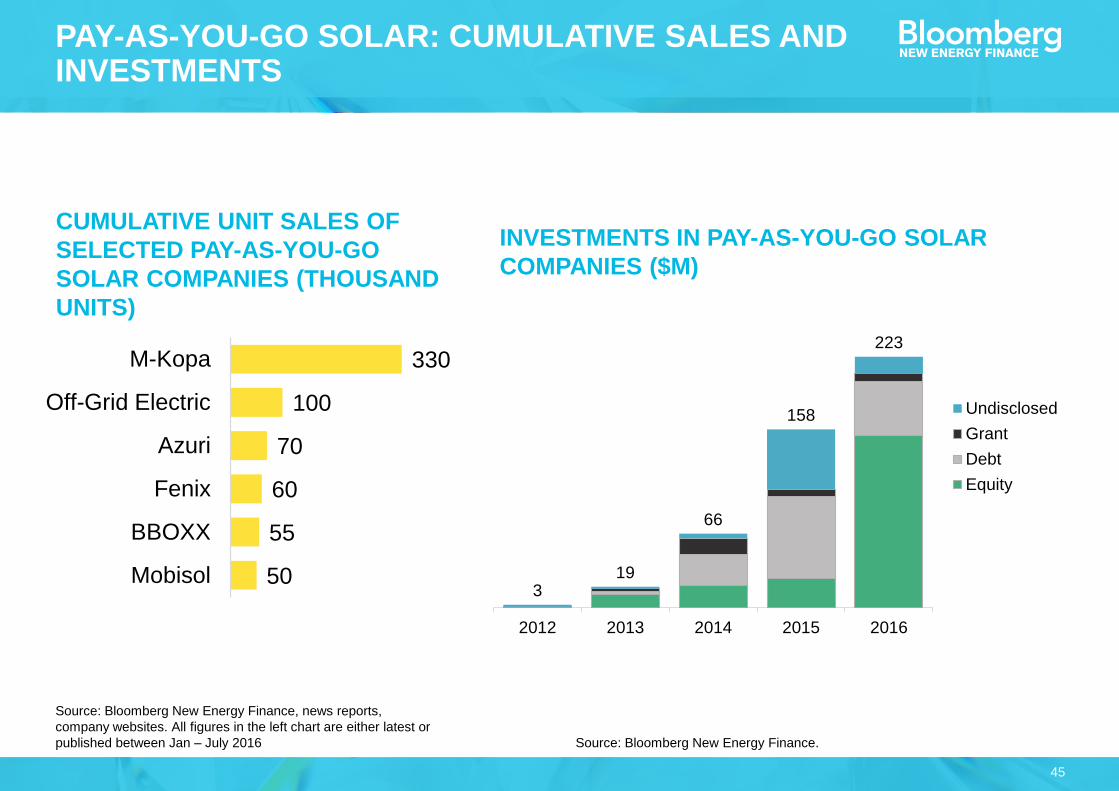

PAY-AS-YOU-GO SOLAR: CUMULATIVE SALES AND INVESTMENTS

50

55

60

70

100

330

Mobisol

BBOXX

Fenix

Azuri

Off-Grid Electric

M-Kopa

Source: Bloomberg New Energy Finance, news reports,

company websites. All figures in the left chart are either latest or

published between Jan – July 2016 Source: Bloomberg New Energy Finance.

CUMULATIVE UNIT SALES OF

SELECTED PAY-AS-YOU-GO

SOLAR COMPANIES (THOUSAND

UNITS)

INVESTMENTS IN PAY-AS-YOU-GO SOLAR

COMPANIES ($M)

319

66

158

223

2012 2013 2014 2015 2016

Undisclosed

Grant

Debt

Equity

46

Product design

OperationsConsumer financing

Retail distribution

Upselling to DC

appliances

Source: GOGLA, IFC Lighting Global,

Bloomberg New Energy Finance

PAY-AS-YOU-GO BUSINESS STRATEGIES

Product developer

Pure-play distributor

Service platform

developers

Integrated service

providers

47

Note: *H1 2016 is estimated at 1.5x data reported up to May 2016. Source: Bloomberg New Energy Finance, IDCOL.

SALES OF SHS UNDER THE IDCOL PROGRAMME BY COMPANY, H1 2006–H1 2016* (UNITS)

17k 20k 32k 38k53k 51k

64k

104k

142k

183k

244k225k

313k330k

453k

400k404k

321k

284k

167k

120k

0m

1m

2m

3m

4m

5m

0.0m

0.1m

0.2m

0.3m

0.4m

0.5m

H1 H2 H1 H2 H1 H2 H1 H2 H1 H2 H1 H2 H1 H2 H1 H2 H1 H2 H1 H2 H1

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 '16*

Other

AVA

SRIZONY

RDF

BGEF

SEF

HFSKS

RSF (Rahimafrooz)

Grameen Shakti

Total, cumulative(right-hand axis)

48

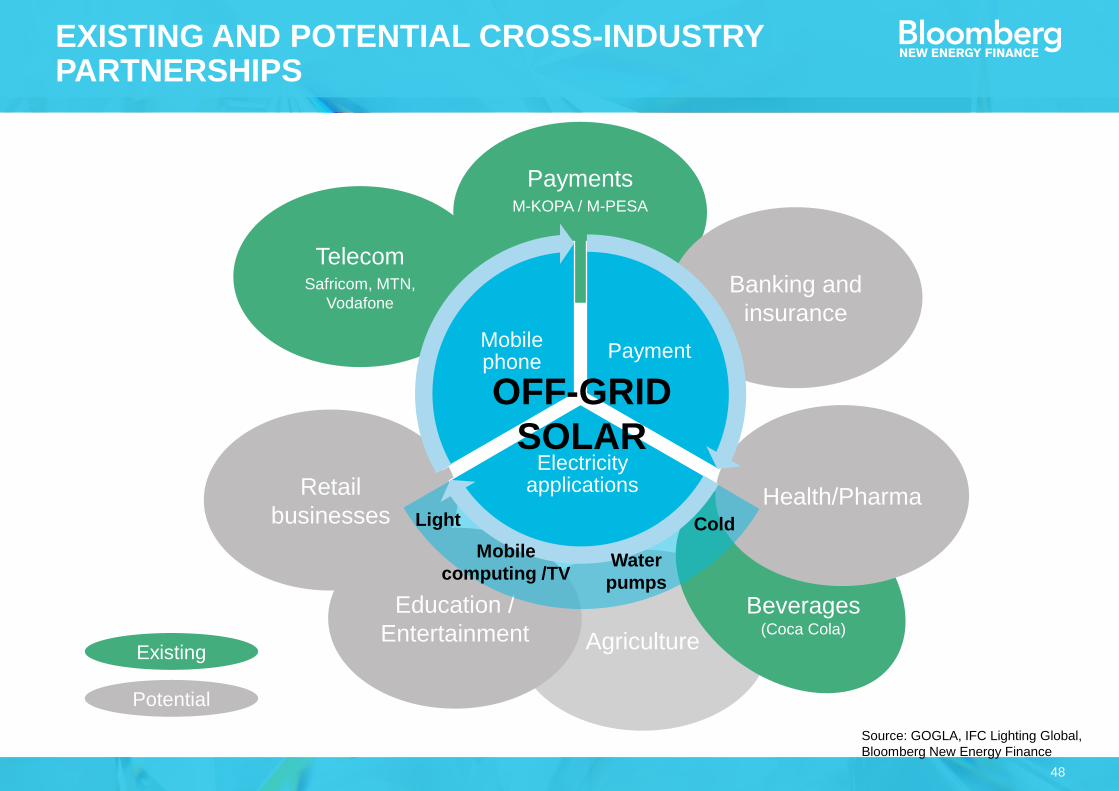

Agriculture

EXISTING AND POTENTIAL CROSS-INDUSTRY PARTNERSHIPS

PaymentsM-KOPA / M-PESA

Education /

Entertainment

Retail

businessesHealth/Pharma

Banking and

insurance

TelecomSafricom, MTN,

Vodafone

Payment

Electricity applications

Mobile phone

Cold

Mobile

computing /TV

Light

Beverages(Coca Cola)

OFF-GRID

SOLAR

Existing

Potential

Water

pumps

Source: GOGLA, IFC Lighting Global,

Bloomberg New Energy Finance

49

CHALLENGES TO THE PAYG INDUSTRY

● Long lead time for building the company infrastructure

● Geographical differences in terms of business environment (eg.,

mobile-money infrastructure)

● Demand for debt financing will continue to outstrip supply for the

foreseeable future

MINI-GRID

51

MINI-GRID DEVELOPMENT MODELS

Grid-quality power

Partial power

Top-down

developmentBottom-up

development

Characteristics:

● DC power

● Grid uptime <24/7

● Grant financed through

government development

agencies

● Focus on residential rural

customers

Characteristics:

● 24/7 AC power

● Formal agreement with

government agency or utility

● Anchor or dominant off-taker

common

● Steady cash flows

● Grid connection/ distribution grid

may already be established

● Diesel replacement common

Characteristics:

● DC power

● Grid uptime <24/7

● Solar + storage assets

● Company manages all aspects

of mini-grid value chain and

develops retail network

● Focus on residential rural

customers

● High exposure to payment risks

Characteristics:

● 24/7 AC power

● Solar + storage + diesel

generator assets

● Company manages many

aspects of mini-grid value chain

and develops retail network

● Focus on productive consumers /

businesses to balance exposure

to payment risks from residential

customers

Source: Bloomberg New Energy Finance

52

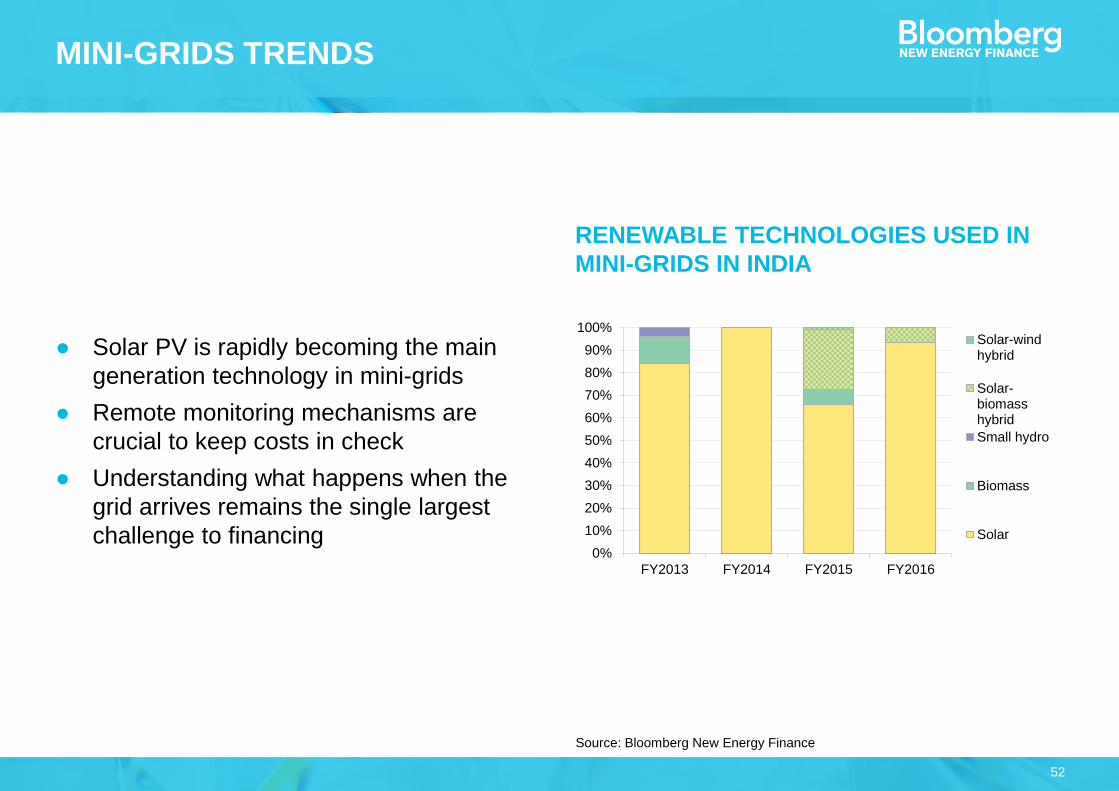

MINI-GRIDS TRENDS

● Solar PV is rapidly becoming the main

generation technology in mini-grids

● Remote monitoring mechanisms are

crucial to keep costs in check

● Understanding what happens when the

grid arrives remains the single largest

challenge to financing

Source: Bloomberg New Energy Finance

RENEWABLE TECHNOLOGIES USED IN

MINI-GRIDS IN INDIA

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY2013 FY2014 FY2015 FY2016

Solar-windhybrid

Solar-biomasshybrid

Small hydro

Biomass

Solar

53

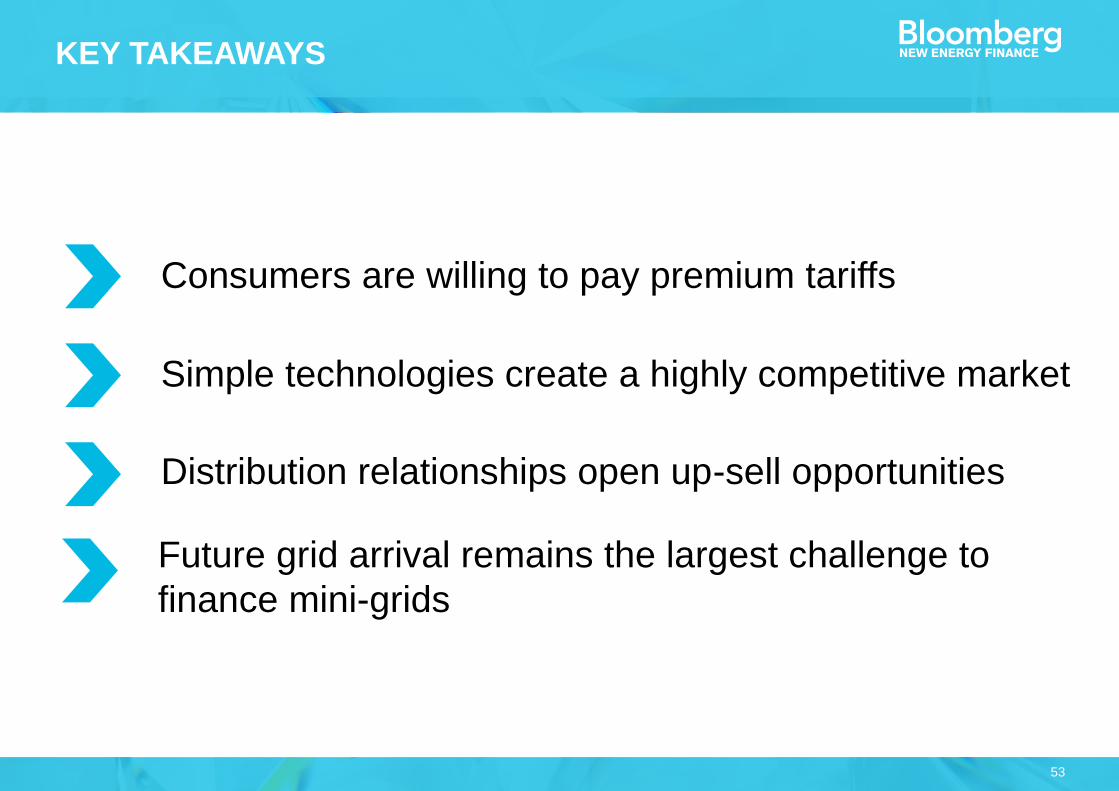

Consumers are willing to pay premium tariffs

KEY TAKEAWAYS

Simple technologies create a highly competitive market

Distribution relationships open up-sell opportunities

Future grid arrival remains the largest challenge to

finance mini-grids

3. SUCCESSFUL POLICY CASES

CASE 1: RENEWABLE ENERGY AUCTION

56

Note: bids are reflective of lowest bid in each country. China’s auction programme is currently on hold but may be re-

introduced in the near future. Tenders have been used infrequently at a state level rather than nationwide in the US and

Australia. Dollar values are nominal and converted using exchange rate on the day of the result announcement. Source: Climatescope 2016

COUNTRIES WITH CLEAN ENERGY TENDER PROGRAMMES AND SELECT RECENT LOWEST CLEARING PRICES, H1 2016

57

ONSHORE WINDSOLAR PV

Location:

Bidder:

Signed:

Construction:

Price:

Morocco

Enel Green Power

January 2016

2018

US$ 3.0 c/kWh

Location:

Bidder:

Signed:

Construction:

Price:

Peru

Enel Green Power

February 2016

2017

US$ 4.8 c/kWh

2016 UNSUBSIDISED CLEAN ENERGY 2016WORLD RECORDS

Source: Bloomberg New Energy Finance; ImagesSiemens; Wikimedia Commons

58

ONSHORE WIND

Location:

Bidder:

Signed:

Construction:

Price:

Morocco

Enel Green Power

January 2016

2018

US$ 3.0 c/kWh

Location:

Bidder:

Signed:

Construction:

Price:

Coahuila, Mexico

Enel Green Power

March 2016

2018

US$ 3.6 c/kWh

2016 UNSUBSIDISED CLEAN ENERGY 2016WORLD RECORDS

Source: Bloomberg New Energy Finance; ImagesSiemens; Wikimedia Commons

SOLAR PV

59

ONSHORE WINDSOLAR PV

Location:

Bidder:

Signed:

Construction:

Price:

Morocco

Enel Green Power

January 2016

2018

US$ 3.0 c/kWh

Location:

Bidder:

Signed:

Construction:

Price:

Dubai

Masdar Consortium

May 2016

2019

US$ 2.99 c/kWh

2016 UNSUBSIDISED CLEAN ENERGY 2016WORLD RECORDS

Source: Bloomberg New Energy Finance; ImagesSiemens; Wikimedia Commons

60

ONSHORE WINDSOLAR PV

Location:

Bidder:

Signed:

Construction:

Price:

Morocco

Enel Green Power

January 2016

2018

US$ 3.0 c/kWh

Location:

Bidder:

Signed:

Construction:

Price:

Chile

Solarpack Corporation

August 2016

2019

US$ 2.91 c/kWh

2016 UNSUBSIDISED CLEAN ENERGY 2016WORLD RECORDS

Source: Bloomberg New Energy Finance; ImagesSiemens; Wikimedia Commons

61

Source: Bloomberg New Energy Finance

PRICE IMPACT OF SWITCH FROM FIT TO AUCTIONS, SELECTED COUNTRIES (NORMALISED)

SOLAR PV

(unit price normalised to 100 at date of first auction)

ONSHORE WIND

(unit price normalised to 100 at date of first auction)

: non-tariff

price signals

: tariffs

: auctions

KEY

EMEA

Other LatAm

Brazil

India

South Africa0

20

40

60

80

100

120

140

160

+3+2+10-1-2-3

- 30% - 50%

0

20

40

60

80

100

120

140

160

+3+2+10-1-2-3

- 35% - 60%

62

PRICE AND COMPETITION LEVEL OF SOUTH AFRICA’S RENEWABLE ENERGY AUCTIONS ($/KWH)

R1

R2R3

R4

Round (R) 1

R2

R3

R4

0

5

10

15

20

25

30

35

40

0 1 2

Wind

PV

Undersubsribed / low competition Oversubsribed / high competition

63

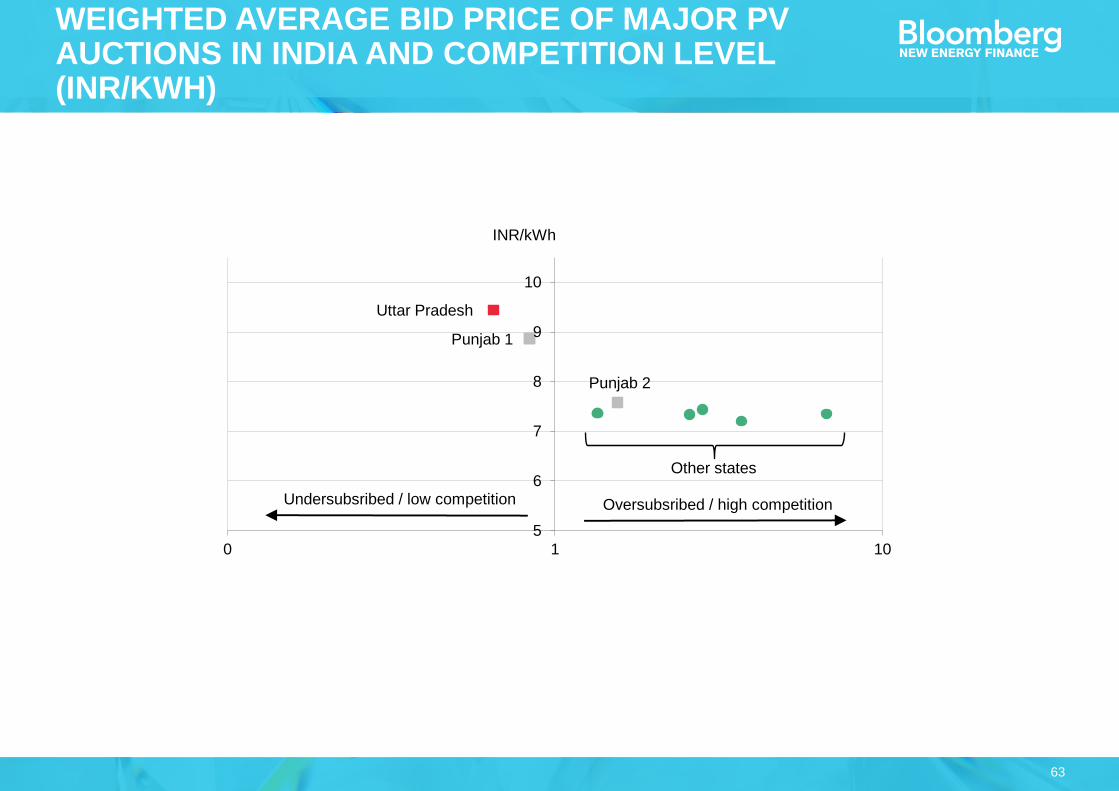

WEIGHTED AVERAGE BID PRICE OF MAJOR PV AUCTIONS IN INDIA AND COMPETITION LEVEL (INR/KWH)

Punjab 1

Uttar Pradesh

Punjab 2

5

6

7

8

9

10

0 1 10

Undersubsribed / low competition Oversubsribed / high competition

Other states

INR/kWh

CASE 2: ELECTRIFICATION PROGRAMME IN PERU

65

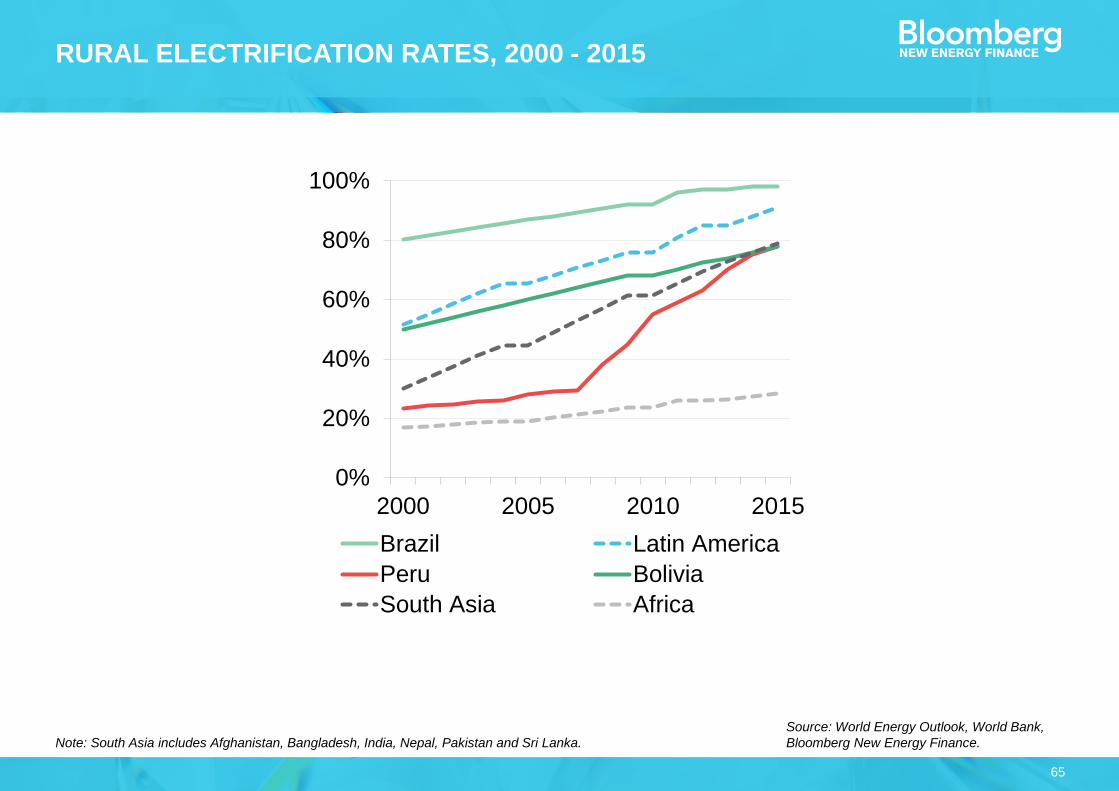

RURAL ELECTRIFICATION RATES, 2000 - 2015

Note: South Asia includes Afghanistan, Bangladesh, India, Nepal, Pakistan and Sri Lanka.

Source: World Energy Outlook, World Bank,

Bloomberg New Energy Finance.

0%

20%

40%

60%

80%

100%

2000 2005 2010 2015

0%

100%

2000 2005 2010 2015

Brazil Latin America

Peru Bolivia

South Asia Africa

66

PERU’S RURAL ELECTRIFICATION BUDGET AND ELECTRIFICATION RATES, 2000-2025

Note: 2006-2015 budget break down was estimated based on PNER 2004-2013 and PNER 2009-2018.

Source: OSINERGMIN, Bloomberg New

Energy Finance.

41 45

13

44 38 4736

8498

176

223

183

149 154

116 113

403

279

178 186

101

4464

25 25 26

Rural electrification rate

National eletrification rate

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

-

50

100

150

200

250

300

350

400

450

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022 2024

Total invested - mix of technologies Mini-grids Grid extension PV systems Small hydro plants Wind Investment in utilities

Pre General Rural Electrification Law

Post General Rural Electrification Law

67

HOUSEHOLDS ELECTRIFIED PER $1M INVESTED BY THE GOVERNMENT, 2006 - 2025

Source: OSINERGMIN, Bloomberg New

Energy Finance

68

Auction can be an effective tool to reduce cost of

renewables

KEY TAKEAWAYS

Lowering risk can lead more developers to participate

auction

Rural electrification can be accelerated at achievable

cost through determined action.

Technical regulations that do not fit consumer

preference may need reconsideration.

SUMMARY

70

SUMMARY

● Utility-scale

renewables

A new utility-scale solar and wind projects are still more expensive than

thermal power projects. A lack of local experience and supply chain is a

major factor. Deployment experience with support of development banks

is a key to reduce LCOE. A small-hydro could be a cost effective option.

In auction programmes, lowering risks for developers is a key to

generate competition in market and to reduce cost. Rural electrification

can be accelerated at achievable cost through determined action.

Consumers are willing to pay premium tariffs for better energy services.

Simple technologies can generate fierce competition amongst market

players and lead them to deploy higher-valued products and services.

● Off-grid

solar

● Policy

BNEF COVERAGE OF FRONTIER POWER

72

FURTHER READING

Sample reports

73

RESEARCH SCOPE FOR BNEF FRONTIER POWER

Solar lanterns

Solar home systems

DC micro grids

Irrigation and agriculture mechanisation

(Back-up) diesel replacement

C&I energy in emerging markets

Grid improvements

Off-grid Weak grid

24/7 AC mini-grids

Grid extensions

Communication and critical infrastructure

Uninterrupted power supply

74

How much kit is

sold?

How will countries

electrify?

Who will own the

customer relationship?

What role can

institutional investors

play?

Can clean energy

replace diesel

generators?

Who is investing in

what?

RESEARCH SCOPE FOR BNEF FRONTIER POWER

7530 January 2017

THE TEAM

Itamar Orlandi

Head of Frontier

Power

Michael Wilshire

Head of Strategy

Takehiro Kawahara

Lead Analyst

Raksha Gosai

Data researcher

Isabelle Edwards

Analyst

Ankit Agarwal

Analyst

76

REFERENCE

Climate Scope 2016

(http://global-climatescope.org/en/)

UK DFID LCOE Study

(https://www.gov.uk/dfid-research-outputs/levelised-cost-of-electricity)

Off-grid Solar Market Trend 2016

(https://about.bnef.com/blog/off-grid-solar-market-trends-report-2016/)

Off-Grid and Mini-Grid: Q1 2017 Market Outlook

(https://about.bnef.com/blog/off-grid-mini-grid-q1-2017-market-outlook/)

78

This publication is the copyright of Bloomberg New Energy Finance. No portion of this document may be photocopied,

reproduced, scanned into an electronic system or transmitted, forwarded or distributed in any way without prior consent of

Bloomberg New Energy Finance.

The information contained in this publication is derived from carefully selected sources we believe are reasonable. We do

not guarantee its accuracy or completeness and nothing in this document shall be construed to be a representation of such

a guarantee. Any opinions expressed reflect the current judgment of the author of the relevant article or features, and does

not necessarily reflect the opinion of Bloomberg New Energy Finance, Bloomberg Finance L.P., Bloomberg L.P. or any of

their affiliates ("Bloomberg"). The opinions presented are subject to change without notice. Bloomberg accepts no

responsibility for any liability arising from use of this document or its contents. Nothing herein shall constitute or be

construed as an offering of financial instruments, or as investment advice or recommendations by Bloomberg of an

investment strategy or whether or not to "buy," "sell" or "hold" an investment.

COPYRIGHT AND DISCLAIMER

Unique analysis, tools and data for decision-makers

driving change in the energy system

MARKETS Renewable Energy

Energy Smart Technologies

Advanced Transport

Gas

Carbon and RECs

SERVICESAmericas Service

Asia Pacific Service

EMEA Service

Applied Research

Events and Workshops

Takehiro Kawahara