MARKET PULSE QUARTER 3, 2015 - Worldwide | Nielsen · Vietnam Asia Pacific OOH Consumer Confidence...

19

Prepared by Nielsen November 2015 MARKET PULSE QUARTER 3, 2015

-

Upload

hoangxuyen -

Category

Documents

-

view

212 -

download

0

Transcript of MARKET PULSE QUARTER 3, 2015 - Worldwide | Nielsen · Vietnam Asia Pacific OOH Consumer Confidence...

Prepared by Nielsen November 2015

MARKET PULSE QUARTER 3, 2015

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

2

55% 51%

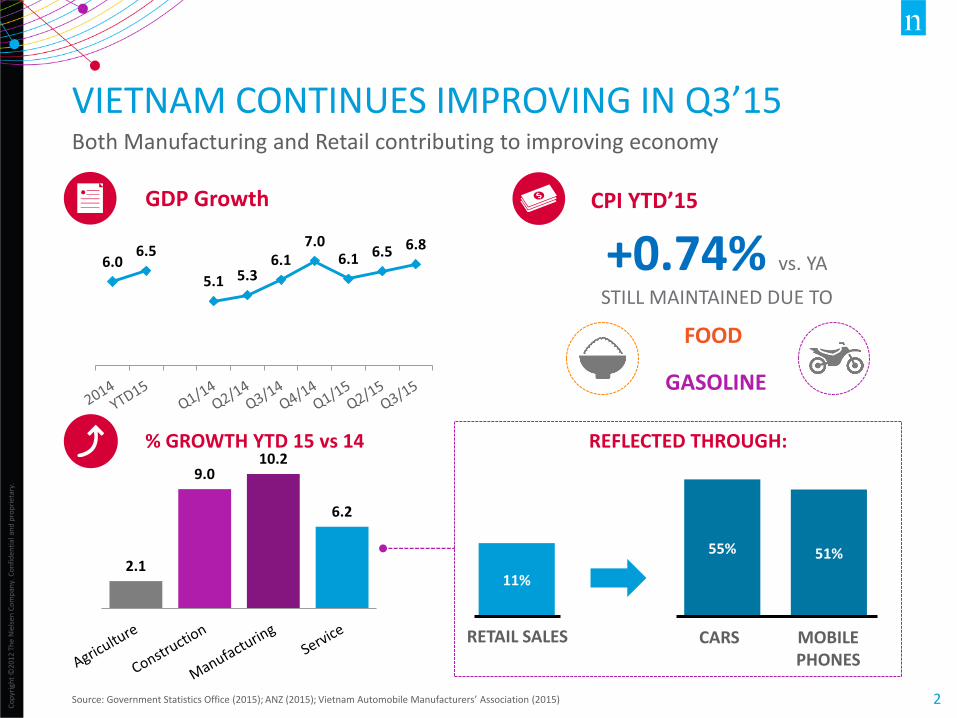

VIETNAM CONTINUES IMPROVING IN Q3’15 Both Manufacturing and Retail contributing to improving economy

Source: Government Statistics Office (2015); ANZ (2015); Vietnam Automobile Manufacturers’ Association (2015)

6.0 6.5

5.1 5.3 6.1

7.0 6.1 6.5 6.8

GDP Growth

+0.74% vs. YA

STILL MAINTAINED DUE TO

CPI YTD’15

FOOD

GASOLINE

RETAIL SALES

11%

CARS

% GROWTH YTD 15 vs 14

2.1

9.0 10.2

6.2

MOBILE PHONES

REFLECTED THROUGH:

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

3

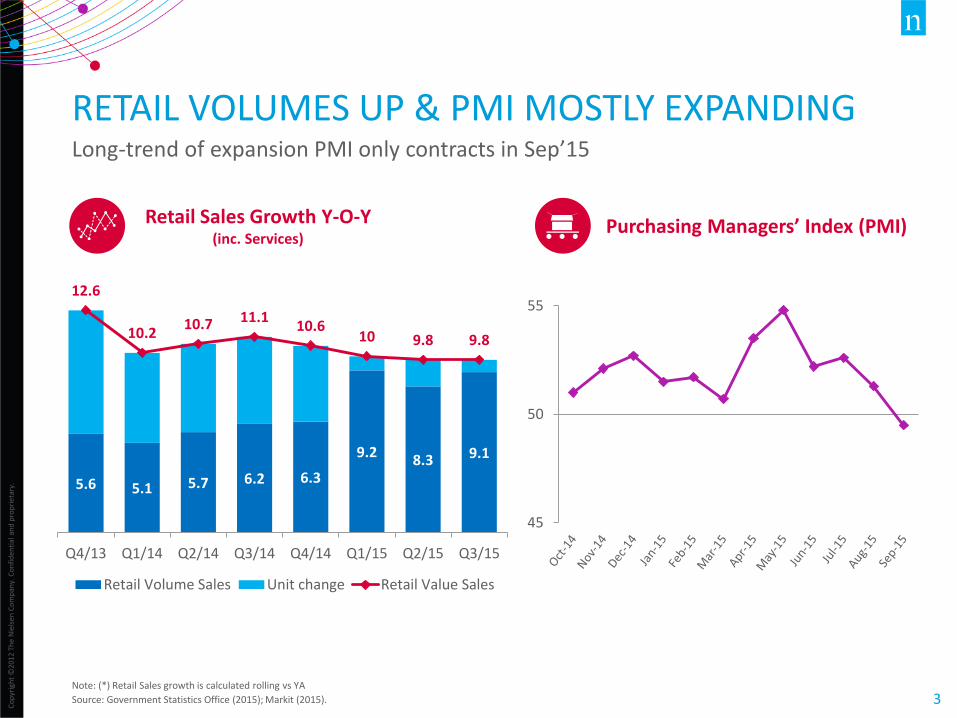

RETAIL VOLUMES UP & PMI MOSTLY EXPANDING Long-trend of expansion PMI only contracts in Sep’15

Note: (*) Retail Sales growth is calculated rolling vs YA

Source: Government Statistics Office (2015); Markit (2015).

45

50

55

Purchasing Managers’ Index (PMI) Retail Sales Growth Y-O-Y (inc. Services)

5.6 5.1 5.7 6.2 6.3

9.2 8.3 9.1

12.6

10.2 10.7 11.1

10.6 10 9.8 9.8

Q4/13 Q1/14 Q2/14 Q3/14 Q4/14 Q1/15 Q2/15 Q3/15

Retail Volume Sales Unit change Retail Value Sales

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

4

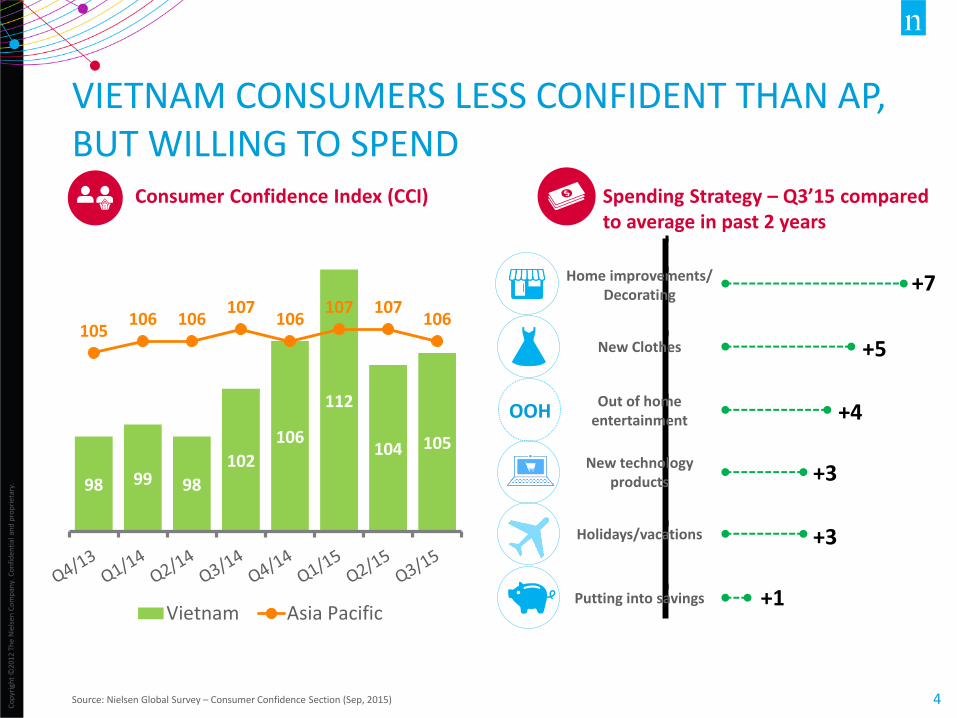

Putting into savings

Holidays/vacations

New technology products

Out of home entertainment

New clothes

Homeimprovements/decorating

Chg in Q3 vs Avg

+7

+5

+4

+3

+3

+1

VIETNAM CONSUMERS LESS CONFIDENT THAN AP, BUT WILLING TO SPEND

Source: Nielsen Global Survey – Consumer Confidence Section (Sep, 2015)

98 99 98

102

106

112

104 105

105 106 106

107 106

107 107 106

Vietnam Asia Pacific

OOH

Consumer Confidence Index (CCI) Spending Strategy – Q3’15 compared to average in past 2 years

Home improvements/ Decorating

New Clothes

Out of home entertainment

New technology products

Holidays/vacations

Putting into savings

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

5

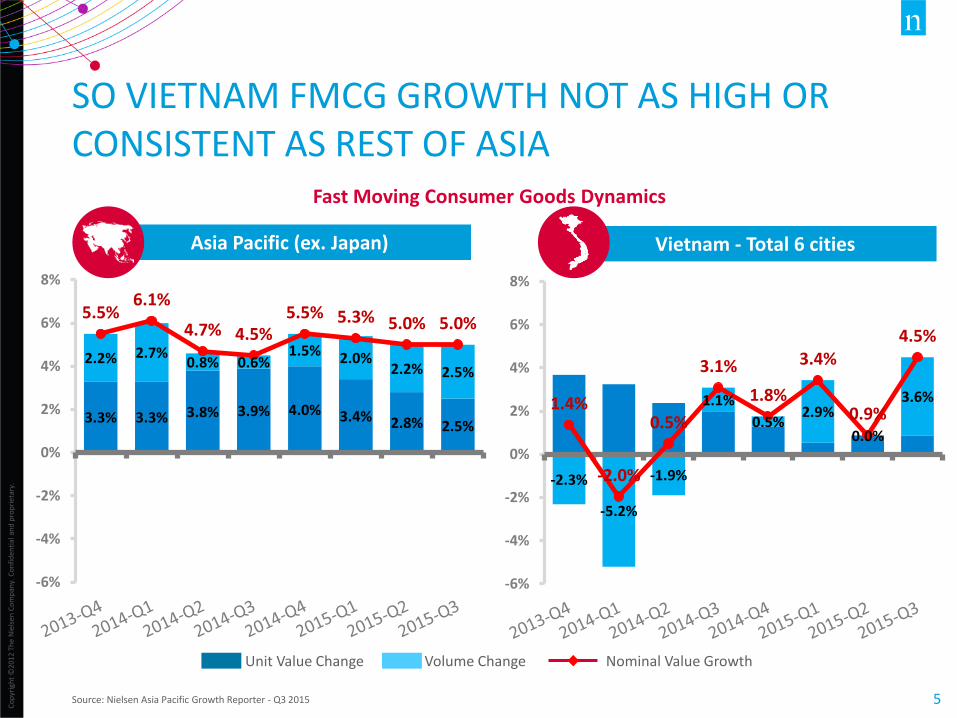

SO VIETNAM FMCG GROWTH NOT AS HIGH OR CONSISTENT AS REST OF ASIA

Source: Nielsen Asia Pacific Growth Reporter - Q3 2015

-2.3%

-5.2%

-1.9%

1.1%

0.5% 2.9%

0.0%

3.6% 1.4%

-2.0%

0.5%

3.1%

1.8%

3.4%

0.9%

4.5%

-6%

-4%

-2%

0%

2%

4%

6%

8%

Vietnam - Total 6 cities

3.3% 3.3% 3.8% 3.9% 4.0% 3.4% 2.8% 2.5%

2.2% 2.7% 0.8% 0.6%

1.5% 2.0% 2.2% 2.5%

5.5% 6.1%

4.7% 4.5% 5.5% 5.3% 5.0% 5.0%

-6%

-4%

-2%

0%

2%

4%

6%

8%

Fast Moving Consumer Goods Dynamics

Asia Pacific (ex. Japan)

Unit Value Change Volume Change Nominal Value Growth

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

7

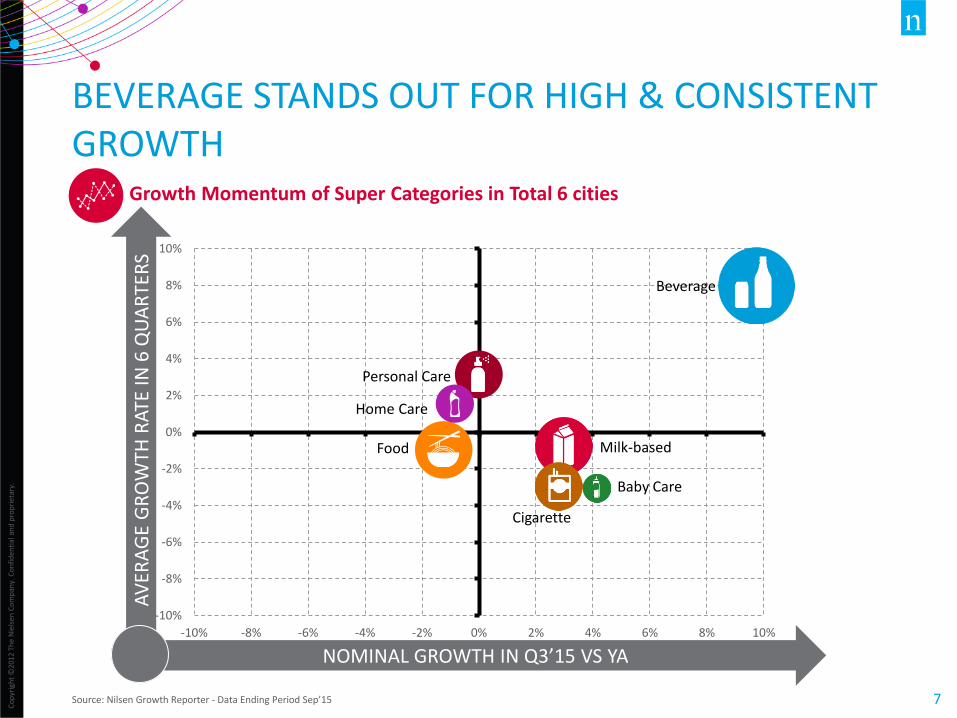

BEVERAGE STANDS OUT FOR HIGH & CONSISTENT GROWTH

Source: Nilsen Growth Reporter - Data Ending Period Sep’15

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

-10% -8% -6% -4% -2% 0% 2% 4% 6% 8% 10%

Beverage

Personal Care

Home Care

Food

Cigarette

Milk-based

Baby Care

Growth Momentum of Super Categories in Total 6 cities

NOMINAL GROWTH IN Q3’15 VS YA

AV

ERA

GE

GR

OW

TH R

ATE

IN 6

QU

AR

TER

S

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

8

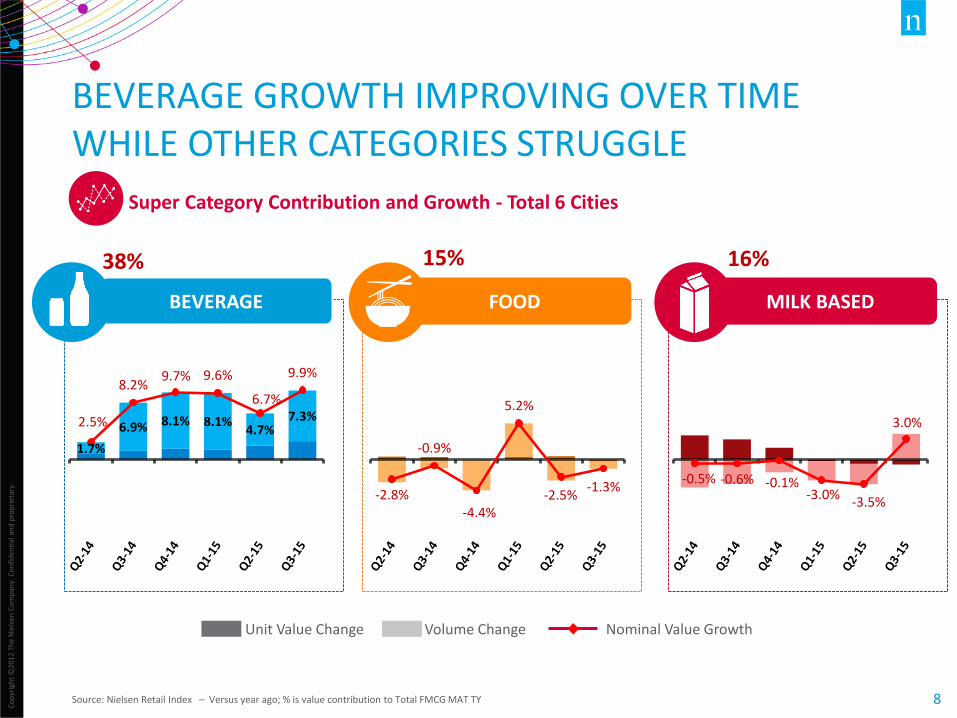

Super Category Contribution and Growth - Total 6 Cities

BEVERAGE GROWTH IMPROVING OVER TIME WHILE OTHER CATEGORIES STRUGGLE

Source: Nielsen Retail Index – Versus year ago; % is value contribution to Total FMCG MAT TY

-2.8%

-0.9%

-4.4%

5.2%

-2.5% -1.3%

1.7%

6.9% 8.1% 8.1% 4.7%

7.3% 2.5%

8.2% 9.7% 9.6%

6.7%

9.9%

-0.5% -0.6% -0.1% -3.0%

-3.5%

3.0%

BEVERAGE FOOD MILK BASED

38% 15% 16%

Unit Value Change Volume Change Nominal Value Growth

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

9

MOST CATEGORIES STRUGGLING DESPITE SHORT-TERM IMPROVEMENT

Source: Nielsen Retail Index – Versus year ago; % is value contribution to Total FMCG MAT TY

3.0% 4.5%

-0.6%

3.4%

-0.3%

-0.8% 0.8%

5.6% 3.9%

7.1%

2.1%

-0.1% -2.2%

-2.8%

-5.2%

-4.8%

-4.0%

2.8% 4.3%

0.6%

-10.8%

-11.2%

-5.9%

4.0%

HOME CARE PERSONAL CARE CIGARETTE BABY CARE

6% 9% 13% 4%

Super Category Contribution and Growth - Total 6 Cities

Unit Value Change Volume Change Nominal Value Growth

TRENDS FOR CONSISTENT GROWTH

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

11

INNOVATION

HEALTH

CONVENIENCE

BEVERAGE IS LEVERAGING THREE TRENDS TO ACHIEVE CONSISTENT GROWTH

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

12

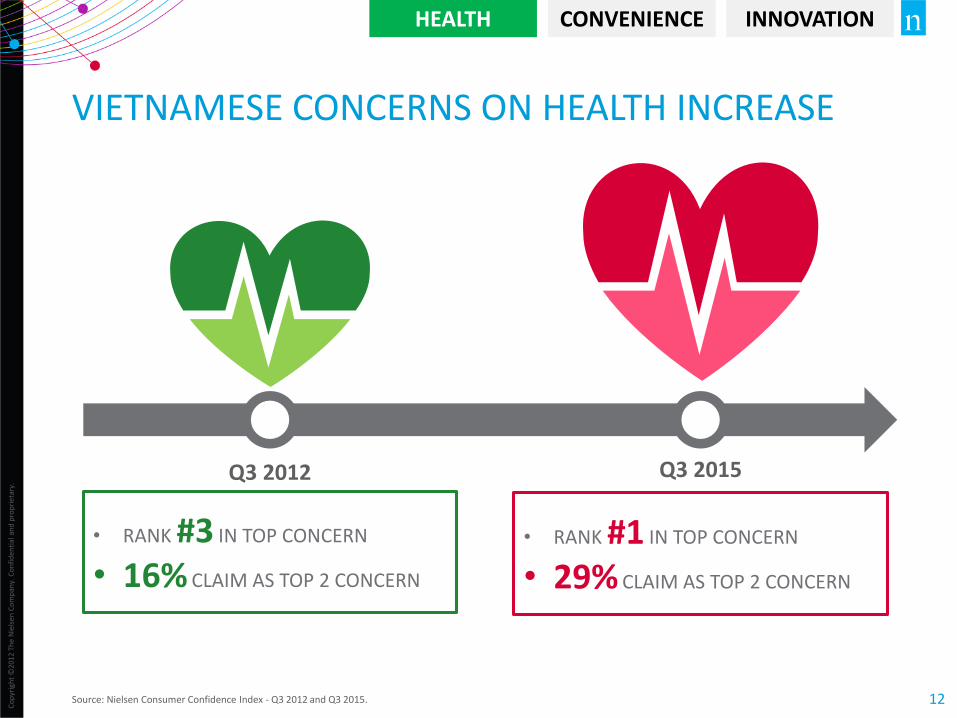

VIETNAMESE CONCERNS ON HEALTH INCREASE

Source: Nielsen Consumer Confidence Index - Q3 2012 and Q3 2015.

Q3 2012 Q3 2015

• RANK #3 IN TOP CONCERN

• 16% CLAIM AS TOP 2 CONCERN

• RANK #1 IN TOP CONCERN

• 29% CLAIM AS TOP 2 CONCERN

HEALTH CONVENIENCE INNOVATION

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

13

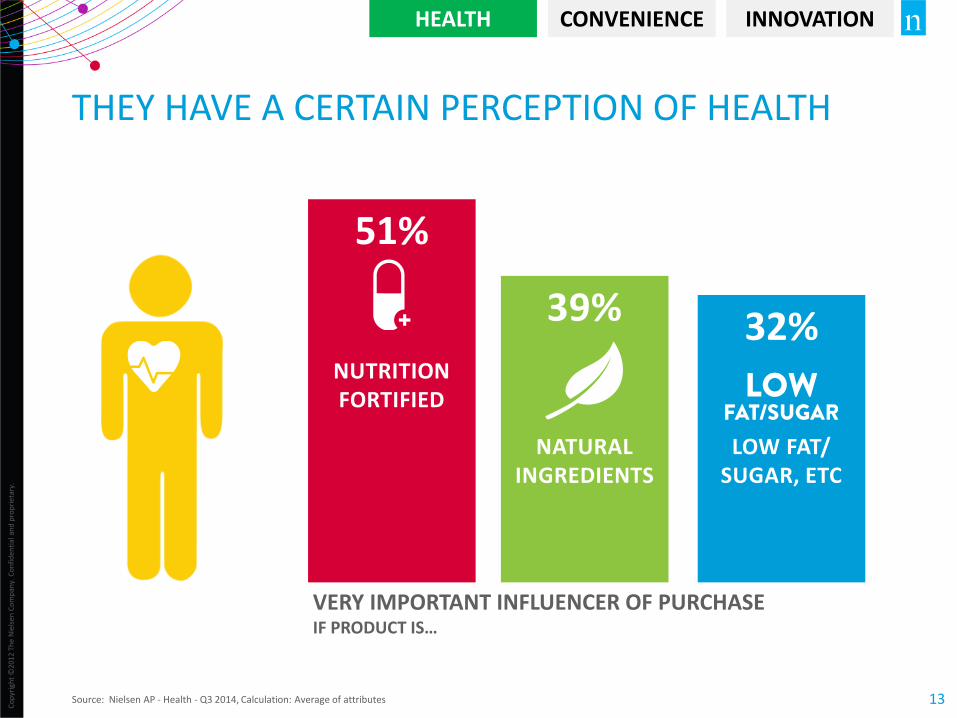

THEY HAVE A CERTAIN PERCEPTION OF HEALTH

Source: Nielsen AP - Health - Q3 2014, Calculation: Average of attributes

39%

51%

NUTRITION FORTIFIED

32%

HEALTH CONVENIENCE INNOVATION

NATURAL INGREDIENTS

LOW FAT/ SUGAR, ETC

VERY IMPORTANT INFLUENCER OF PURCHASE IF PRODUCT IS…

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

15

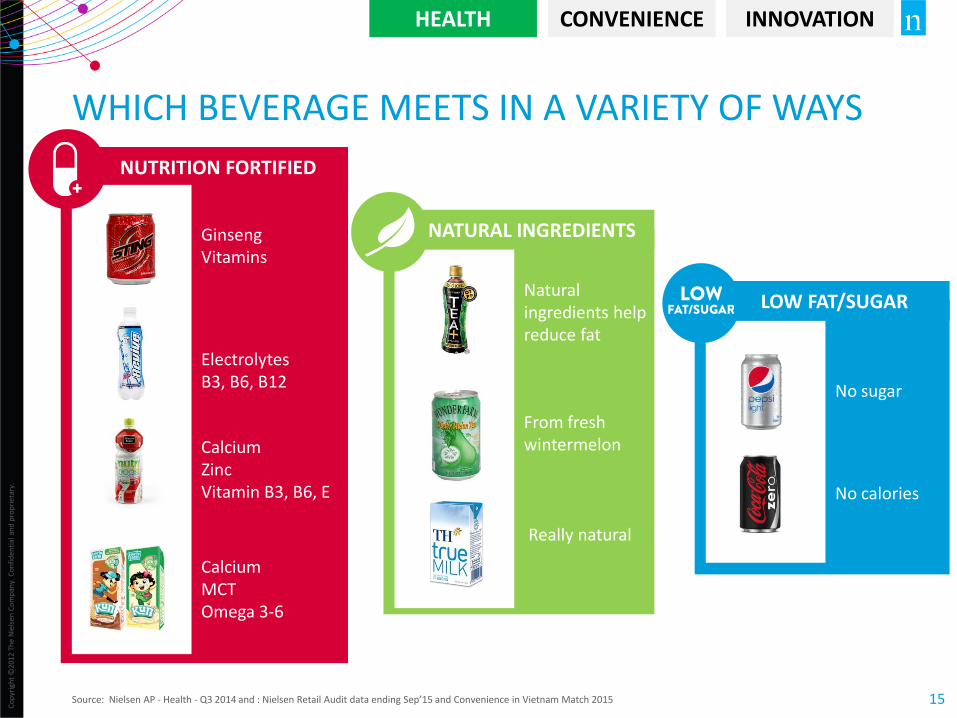

WHICH BEVERAGE MEETS IN A VARIETY OF WAYS

Source: Nielsen AP - Health - Q3 2014 and : Nielsen Retail Audit data ending Sep’15 and Convenience in Vietnam Match 2015

NUTRITION FORTIFIED

HEALTH CONVENIENCE INNOVATION

Ginseng Vitamins

Electrolytes B3, B6, B12

Calcium Zinc Vitamin B3, B6, E

Calcium MCT Omega 3-6

NATURAL INGREDIENTS

Natural ingredients help reduce fat

From fresh wintermelon

Really natural

LOW FAT/SUGAR

No sugar

No calories

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

16

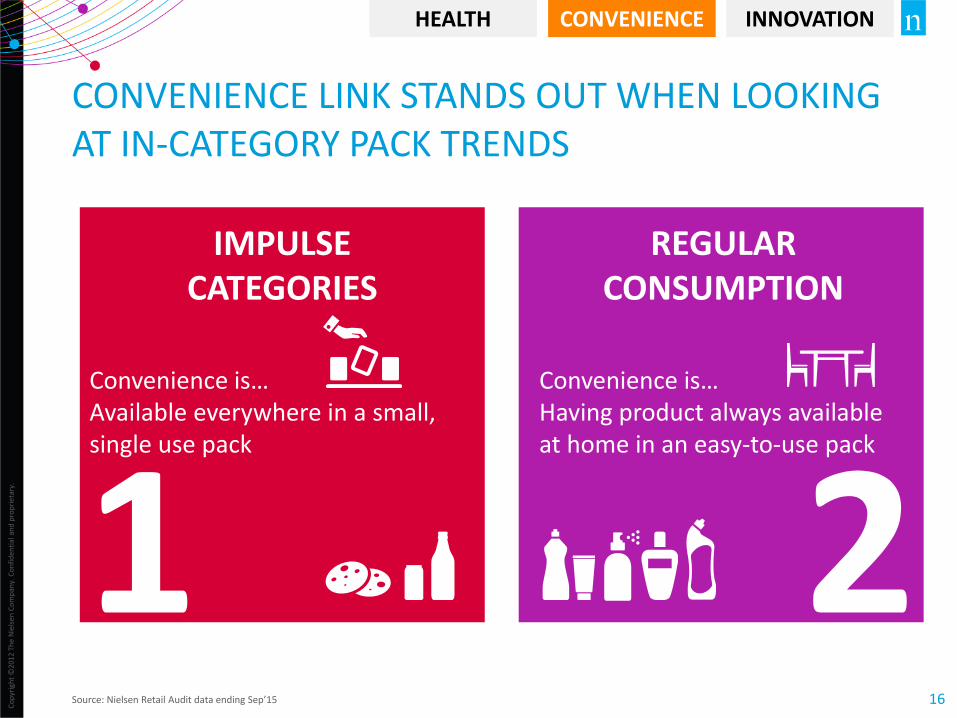

CONVENIENCE LINK STANDS OUT WHEN LOOKING AT IN-CATEGORY PACK TRENDS

Source: Nielsen Retail Audit data ending Sep’15

IMPULSE CATEGORIES

REGULAR CONSUMPTION

Convenience is… Having product always available at home in an easy-to-use pack

2

HEALTH CONVENIENCE INNOVATION

1 Convenience is… Available everywhere in a small, single use pack

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

17

FOOD

BEVERAGE

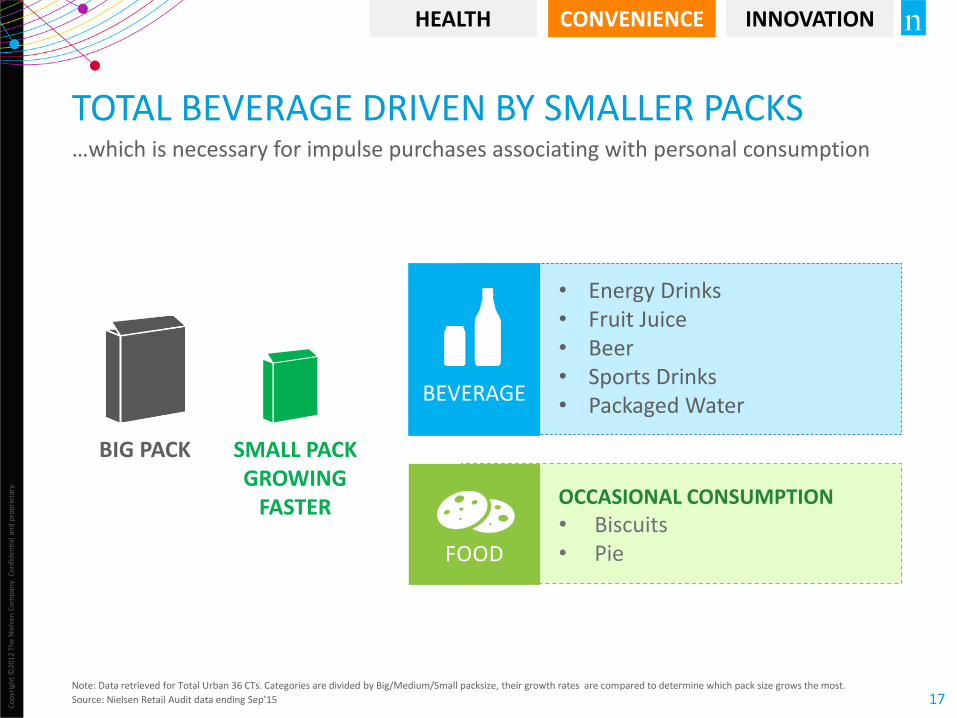

TOTAL BEVERAGE DRIVEN BY SMALLER PACKS …which is necessary for impulse purchases associating with personal consumption

Note: Data retrieved for Total Urban 36 CTs. Categories are divided by Big/Medium/Small packsize, their growth rates are compared to determine which pack size grows the most.

Source: Nielsen Retail Audit data ending Sep’15

• Energy Drinks • Fruit Juice • Beer • Sports Drinks • Packaged Water

OCCASIONAL CONSUMPTION • Biscuits • Pie

BIG PACK SMALL PACK GROWING

FASTER

HEALTH CONVENIENCE INNOVATION

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

18

HOME CARE

FOOD

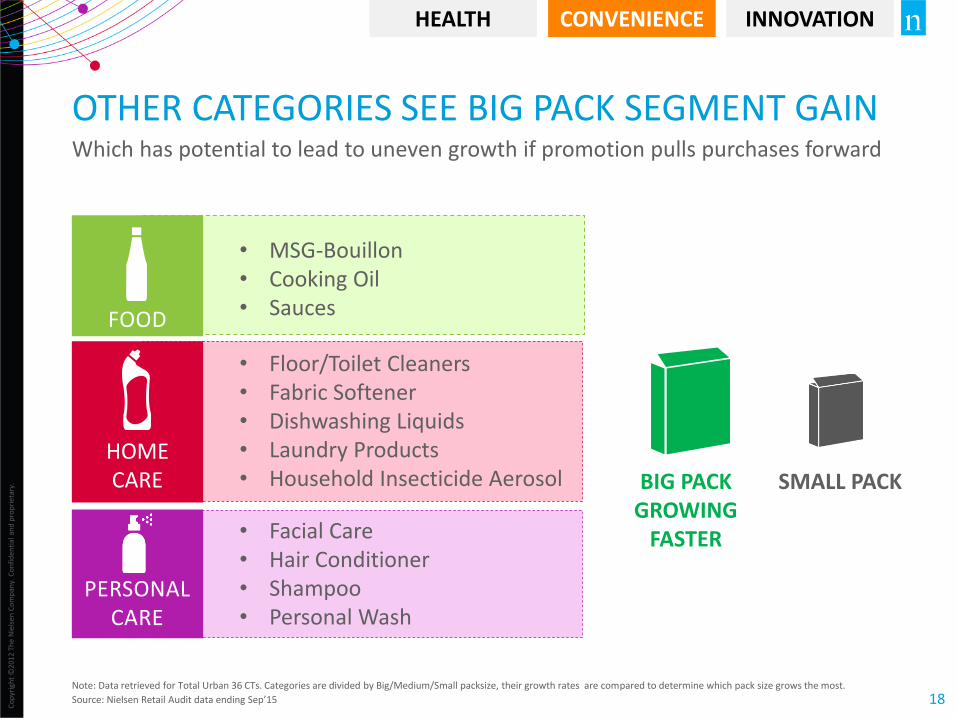

OTHER CATEGORIES SEE BIG PACK SEGMENT GAIN Which has potential to lead to uneven growth if promotion pulls purchases forward

Note: Data retrieved for Total Urban 36 CTs. Categories are divided by Big/Medium/Small packsize, their growth rates are compared to determine which pack size grows the most.

Source: Nielsen Retail Audit data ending Sep’15

• Floor/Toilet Cleaners • Fabric Softener • Dishwashing Liquids • Laundry Products • Household Insecticide Aerosol

• Facial Care • Hair Conditioner • Shampoo • Personal Wash

PERSONAL CARE

HEALTH CONVENIENCE INNOVATION

• MSG-Bouillon • Cooking Oil • Sauces

BIG PACK GROWING

FASTER

SMALL PACK

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

19

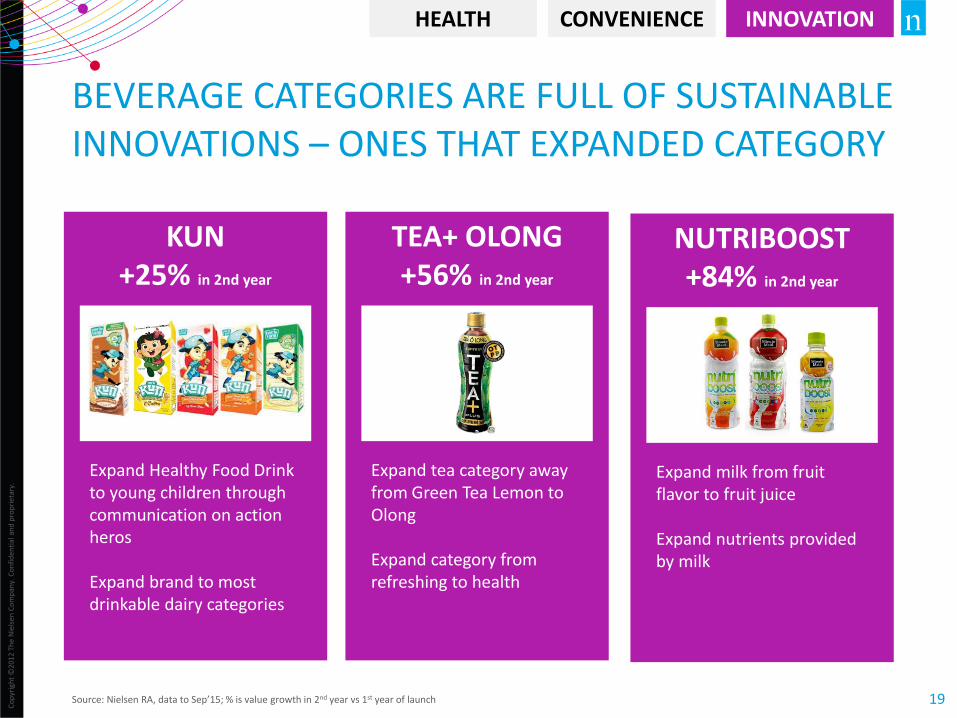

NUTRIBOOST +84% in 2nd year

Expand milk from fruit flavor to fruit juice Expand nutrients provided by milk

KUN +25% in 2nd year

BEVERAGE CATEGORIES ARE FULL OF SUSTAINABLE INNOVATIONS – ONES THAT EXPANDED CATEGORY

Source: Nielsen RA, data to Sep’15; % is value growth in 2nd year vs 1st year of launch

HEALTH CONVENIENCE INNOVATION

Expand Healthy Food Drink to young children through communication on action heros Expand brand to most drinkable dairy categories

TEA+ OLONG +56% in 2nd year

Expand tea category away from Green Tea Lemon to Olong Expand category from refreshing to health

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

20

KEY TAKEAWAYS - Q3 2015

POSITIVE GROWTH BUT STILL VOLATILE

AND 0.74% 6.5%

GDP GROWTH YTD SEP15 VS YA

CPI VS YA LOW INFLATION

MANUFACTURING

+10.2% EXPORTS DRIVING

ECONOMY

TREND FOR CONSISTENT GROWTH

FMCG GROWTH

+4.5% HIGHEST GROWTH RATE IN THE LAST 8

QUARTERS

CCI 105 GOOD, BUT LAGGING REST OF ASIA

FMCG GROWTH RATE IMPROVING BUT STILL SEEKING SUSTAINABLE GROWTH

BEVERAGE CATEGORIES THE ONLY ONES ABLE TO SUSTAIN GROWTH

HEALTH INNOVATION CONVENIENCE

• NUTRITION FORTIFIED • NATURAL INGREDIENT • LOW FAT/SUGAR

SUSTAINABLE INNOVATION

• GO SMALL FOR OCCASIONAL PURPOSE

• GO BIG FOR REGULAR CONSUMPTION PURPOSE

THANK YOU