Market Positioning and Pricing Analysis...Marcus & Millichap has been chosen to exclusively market...

41

Market Positioning and Pricing Analysis 1 VERO BEACH REDEVELOPMENT 965 E Causeway Blvd • Vero Beach, FL 32963

Transcript of Market Positioning and Pricing Analysis...Marcus & Millichap has been chosen to exclusively market...

Market Positioning and Pricing Analysis

1

VERO BEACH REDEVELOPMENT

965 E Causeway Blvd • Vero Beach, FL 32963

VERO BEACH REDEVELOPMENT

Vero Beach, FL

ACT ID Y0391019

N O N - E N D O R S E M E N T A N D D I S C L A I M E R N O T I C E

Non-Endorsements Marcus & Millichap Real Estate Investment Services of Florida, Inc. ("Marcus & Millichap") is not affiliated with,

sponsored by, or endorsed by any commercial tenant or lessee identified in this marketing package. The presence of

any corporation's logo or name is not intended to indicate or imply affiliation with, or sponsorship or endorsement by,

said corporation of Marcus & Millichap, its affiliates or subsidiaries, or any agent, product, service, or commercial

listing of Marcus & Millichap, and is solely included for the purpose of providing tenant lessee information about this

listing to prospective customers.

ALL PROPERTY SHOWINGS ARE BY APPOINTMENT ONLY.

PLEASE CONSULT YOUR MARCUS & MILLICHAP AGENT FOR MORE DETAILS.

Disclaimer THIS IS A BROKER PRICE OPINION OR COMPARATIVE MARKET ANALYSIS OF VALUE AND SHOULD NOT BE

CONSIDERED AN APPRAISAL. This information has been secured from sources we believe to be reliable, but we

make no representations or warranties, express or implied, as to the accuracy of the information. References to

square footage or age are approximate. Buyer must verify the information and bears all risk for any inaccuracies.

Marcus & Millichap is a service mark of Marcus & Millichap Real Estate Investment Services, Inc. © 2017 Marcus &

Millichap. All rights reserved.

2

P R E S E N T E D B Y

Ahmed Kabani

First Vice President Investments

Senior Director - National Hospitality

Group

Miami Office

Tel: (786) 522-7000

Fax: (786) 522-7010

License: FL SL3115103

Garrick Benabe

Agent Candidate

Miami Office

Tel: (786) 522-7000

Fax: (786) 522-7010

License: FL SL3385321

Jesse Bajaj

SIP

Member - National Hospitality Group

Miami Office

Tel: (786) 522-7026

Fax: (786) 522-7010

License: FL SL3385910

3

TABLE OF CONTENTS

SECTION

INVESTMENT OVERVIEW 01 Property Overview

Regional Map

Local Map

Aerial Photo

FINANCIAL ANALYSIS 02 STR

Historical P&L

5 Year Pro Forma

5 Year Return

MARKET COMPARABLES 03 Sales Comparables

MARKET OVERVIEW 04 Market Analysis

Demographic Analysis

VERO BEACH REDEVELOPMENT

4

VERO BEACH REDEVELOPMENT

5

INVESTMENT

OVERVIEW

PROPERTY DETAILS

VERO BEACH REDEVELOPMENT

PROPERTY DETAILS

Steps From the Ocean

Upside in Room Revenue by Adding 8-10 Rooms

Walkable Vero Beach Neighborhood

Unencumbered by Brand and Management

Rare Opportunity, Ideal for Owner-Operators

6

• Name: Sea Spray Inn

• Price: $3,400,000

• Cap Rate: 8.58%

• Address: 965 E Causeway Blvd. Vero Beach, FL 32963

• APN: 33-40-05-00009-0040-00003.0

• County: Indian River County

• Number of Rooms: 17

• Building Area: 9,042 SF

• Lot Area: 14,810 SF (0.34 Acres)

• Building/Lot Ratio: 0.61

• Year Built: 1987

• Zoning: RM-13

• Property Taxes: $13,414 (2016)

PROPERTY OVERVIEW

VERO BEACH REDEVELOPMENT

PROPERTY OVERVIEW

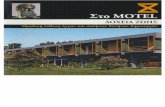

Marcus & Millichap has been chosen to exclusively market for sale the Sea Spray Inn Vero Beach, a charming 17 room motel located just a block from one of the best

beaches in Florida. The Inn consists of 17 exterior-corridor studio and one bedroom suites, and is conveniently located right between A1A and Ocean Drive. Amenities include

a heated pool, large rooftop deck, tropical courtyard, fully equipped kitchens, barbecue grill, complimentary WiFi and HBO, and guest laundry facilities.

The Sea Spray Inn is ideally located in a very walkable Vero Beach neighborhood, just a short distance from boutique shops as well as plenty of dining options. Vero Beach,

known for its beautiful beaches and water sport activities, also attracts tourists because of the town's unique dining and boutique shopping options. Tourists also have the

opportunity to see a show at the nearby Riverside Theater, visit the Vero Beach Museum of Art, or stop by a number of local art galleries filled with famous and local artists

alike.

The Sea Spray Inn is unencumbered by brand and management, making it ideal for an owner-operator. In addition, an owner has the opportunity to significantly boost the

Sea Spray's room revenue by adding 8 to 10 more rooms, without completely redeveloping the entire motel itself.

PROPERTY OVERVIEW

Steps From the Ocean

Upside in Room Revenue by Adding 8-10 Rooms

Walkable Vero Beach Neighborhood

Unencumbered by Brand and Management

Rare Opportunity, Ideal for Owner-Operators

7

REGIONAL MAP

VERO BEACH REDEVELOPMENT

8

LOCAL MAP

VERO BEACH REDEVELOPMENT

9

AERIAL PHOTO

VERO BEACH REDEVELOPMENT

10

PROPERTY PHOTOS

VERO BEACH REDEVELOPMENT

11

ROOM PHOTOS

VERO BEACH REDEVELOPMENT

12

Vero Beach Photo

VERO BEACH REDEVELOPMENT

13

VERO BEACH REDEVELOPMENT

14

FINANCIAL

ANALYSIS

FINANCIAL ANALYSIS

VERO BEACH REDEVELOPMENT

STR

15

FINANCIAL ANALYSIS

VERO BEACH REDEVELOPMENT

HISTORICAL P&L

16

FINANCIAL ANALYSIS

VERO BEACH REDEVELOPMENT

HISTORICAL P&L

17

FINANCIAL ANALYSIS

VERO BEACH REDEVELOPMENT

5 YEAR PRO FORMA

18

FINANCIAL ANALYSIS

VERO BEACH REDEVELOPMENT

5 YEAR PRO FORMA

19

VERO BEACH REDEVELOPMENT

20

MARKET

COMPARABLES

VERO BEACH REDEVELOPMENT

SALES COMPARABLES MAP

21

VERO BEACH REDEVELOPMENT

(SUBJECT)

Blue View Resorts

SeaGlass Inn B & B

Sea View Inn

Delmar Motel

The Nevada

1

2

3

4

5

PROPERTY NAME

VERO BEACH REDEVELOPMENT

SALES COMPARABLES

22

SALES COMPARABLES

Avg. $181,626

$0

$30,000

$60,000

$90,000

$120,000

$150,000

$180,000

$210,000

$240,000

$270,000

$300,000

Sea Spray

Inn

Blue View

Resorts

SeaGlass

Inn B & B

Sea View

Inn

Delmar

Motel

The Nevada

Average Price Per Room

PROPERTY NAME

MARKETING TEAM

VERO BEACH REDEVELOPMENT

SALES COMPARABLES

rentpropertyname1

rentpropertyaddress1

rentpropertyname1

rentpropertyaddress1

rentpropertyname1

rentpropertyaddress1

23

rentpropertyaddress1

Interest Fee Simple

Total No. of Rooms 17

Year Built / Renovated 1987

Underwriting Criteria

Room Revenue $587,505 Occupancy 58%

Total Revenue $587,505 ADR $162.00

NOI $291,821 Rev PAR $9,396

SEA SPRAY INN 965 E Causeway Blvd, Vero Beach, FL, 32963

1

Close of Escrow 4/11/2017

Asking Price $2,100,000

Price/Room $140,000

Price/SF $224.74

Total No. of Rooms 15

Year Built / Renovated 1978

BLUE VIEW RESORTS 5815 S Highway A1A, Melbourne Beach, FL, 32951

Close of Escrow 5/1/2017

Asking Price $1,330,000

Price/Room $147,778

Price/SF $323.44

Total No. of Rooms 9

Year Built / Renovated 1915

2

SEAGLASS INN B & B 514 Ocean Ave, Melbourne Beach, FL, 32951

PROPERTY NAME

MARKETING TEAM

VERO BEACH REDEVELOPMENT

SALES COMPARABLES

rentpropertyname1

rentpropertyaddress1

rentpropertyname1

rentpropertyaddress1

rentpropertyname1

rentpropertyaddress1

24

Close of Escrow 4/20/2016

Asking Price $1,042,800

Price/Room $130,350

Price/SF $309.07

Total No. of Rooms 8

Year Built / Renovated 1950

3

SEA VIEW INN 4215 S Highway A1A, Melbourne Beach, FL, 32951

4

Close of Escrow 5/2/2017

Asking Price $3,850,000

Price/Room $256,667

Price/SF $515.67

Total No. of Rooms 15

Year Built / Renovated 1955

DELMAR MOTEL 315 Arthur St, Hollywood, FL, 33019

Close of Escrow 3/4/2017

Asking Price $3,500,000

Price/Room $233,333

Price/SF $272.29

Total No. of Rooms 15

Year Built / Renovated 1970

5

THE NEVADA 322 Nevada St, Hollywood, FL, 33019

VERO BEACH REDEVELOPMENT

25

MARKET

OVERVIEW

MARKET OVERVIEW

VERO BEACH REDEVELOPMENT

26

FLORIDA

Occupancy Rises in Florida Hotels, Bolstering Growth in Revenue Metrics

Orlando drives occupancy and revenue metric growth in Sunshine State. Healthy tourism in the state of Florida and job growth in many of the major metros have

benefited occupancy and spurred increases in statewide revenue metrics during the year ending in June. Nearly all of the state’s largest metros contributed to

occupancy increases, with the Orlando market posting the largest gains. The metro is one of the largest tourist destinations in the United States and received a record

68 million visitors in 2016, underpinning hotel room demand. Additionally, above-average hiring in professional sectors has driven business travel to the area, benefiting

occupancy rates during the workweek. Hiring in office-using sectors rose 4.1 percent during the last 12 months as 12,500 positions were created in Orlando. Healthy

room demand and limited completions not only boosted occupancy rates but accelerated growth in revenue metrics. As a result, investors remained interested in

Orlando’s hotel assets, targeting properties in the Tourist Corridor submarket and near major attractions including Disney World. Many of the hotels that changed hands

are independent or in the upper midscale segment.

Residents take shelter in hotels after hurricane evacuations. Hurricane Irma impacted the entire state of Florida and caused residents and visitors to seek shelter,

elevating occupancy levels in the short term in areas outside of the evacuation zones. Roughly 6.4 million people were ordered to evacuate parts of southeast Florida,

plummeting hotel occupancies and revenue metrics in metros including Miami-Hialeah and Fort Lauderdale as the hurricane made landfall. Occupancy in hotels in

Orlando rose considerably during this time as residents sought shelter farther north and inland. As evacuation orders were lifted, many residents may turn to hotels as

they assess damage or wait for power to be restored, increasing occupancy levels and generating RevPAR growth. FEMA workers and volunteers will also occupy

available hotel rooms as rebuilding occurs, further helping occupancy and revenue growth. Hotel investors will begin assessing their portfolios and determining next

steps. Some owners may elect to place their property on the market in hopes of capturing a higher price amid higher occupancy and revenue growth. Several buyers

will seek damaged properties in hopes of restoring and renovating to capture higher average daily rates.

MARKET OVERVIEW

VERO BEACH REDEVELOPMENT

27

FLORIDA

2017 Forecast

Revenue jumps in short term. In the aftermath of Hurricane Irma, statewide occupancy will move up

amid recovery efforts. As a result, the average daily rate will climb 5.6 percent to $140.88 and drive a 10

percent increase in RevPAR to $105.04. Occupancy and revenue metrics should adjust back to normal

levels by next year.

Office-using job growth persists. Many of the major Florida markets registered employment gains in

professional sectors above the national rate of growth. Job growth can spur occupancy gains during

weekdays as individuals attend business meetings and interviews. Fort Lauderdale registered the largest

increase in office-using hiring during the last four quarters, rising 5.4 percent as 12,000 positions were

created. Tampa also posted strong growth, climbing 4.2 percent with the addition of 15,300 workers.

Construction rises in Miami. Nearly 12,500 rooms are under construction in Florida and another 15,600

are making their way through the planning stage and expected to break ground in the next 12 months. Of

these deliveries, the Miami-Hialeah metro has 4,900 rooms under construction.

* Forecast

Sources: Marcus & Millichap Research Services; STR, Inc.

Metrics 2016 2017*

Occupancy 71.6% 74.6%

Demand Growth -0.9% 5.9%

Supply Growth 1.5% 1.6%

Average Daily Rate $133.37 $140.88

Annual Change 2.2% 5.6%

RevPAR $96.35 $105.04

Annual Change 1.6% 10.0%

Revenue Growth -2.9% 11.8%

MARKET OVERVIEW

VERO BEACH REDEVELOPMENT

28

FLORIDA

Occupancy Trends

After a 20-basis-point decrease in the prior year, occupancy in Florida climbed 130 basis points during

the last 12 months to 73.2 percent in June. Room nights in the state rose 3.8 percent during this time,

outpacing a supply increase of 1.8 percent.

The majority of major metros in Florida registered occupancy increases during the last four quarters.

Orlando posted the largest gain, with occupancy in the metro rising 330 basis points during the year to

78.9 percent at the end of the second quarter, the highest rate among the major markets. Limited

completions and a 5.2 percent increase in room nights contributed to the spike in year-over-year

occupancy.

Occupancy in Miami-Hialeah and Fort Lauderdale climbed more than 100 basis points in each metro. In

June, occupancy in Miami-Hialeah rested at 72.8 percent while Fort Lauderdale had a 73.9 percent

occupancy rate. The Tampa-St. Petersburg market registered the only decline as the rate fell 110 basis

points to 71.8 percent. Supply additions of 2.9 percent outpaced a room nights increase of 1.6 percent.

Revenue Trends

The average daily rate in Florida rose 3.4 percent during the last four quarters to $125.59 in June. The

increase in ADR coupled with rising occupancy lifted statewide RevPAR up 5.4 percent during this same

time period to $91.98.

The significant jump in occupancy in Orlando aided in a 6.8 percent increase in the metro’s ADR to

$115.85. As a result, RevPAR in Orlando soared 11.5 percent year over year to $91.39. In Fort

Lauderdale, the average daily rate ticked up slightly to $112.78 while RevPAR climbed 3.0 percent

during the last four quarters to $83.34.

Declining occupancy in the Tampa-St. Petersburg metro did not hamper improvement in the area’s

revenue metrics. ADR in the market rose 3.3 percent during the previous 12 months to $117.95 in June.

The increase in the rate drove a 1.8 percent advance in RevPAR to $84.64. In Miami/Hialeah, ADR ticked

down 0.7 percent but rising occupancy led to a 1.2 percent increase in RevPAR to $106.92.

* Forecast

Sources: CoStar Group, Inc.; STR, Inc.; Real Capital Analytics

MARKET OVERVIEW

VERO BEACH REDEVELOPMENT

29

FLORIDA

Sales Trends

Transaction velocity fell 9 percent in Florida during the year ending in the second quarter as fewer

listings were available. The competitive bidding environment for available properties during this time

lifted the average price up 15 percent to approximately 143,000 per key.

Independent hotels comprised a significant chunk of all transactions, particularly in coastal locations

including Miami Beach and oceanside hotels in Tampa-St. Petersburg. Increased competition for

independent hotels lifted the average price up 14 percent statewide to $180,000 per key.

During the last four quarters, transaction volume for hotels in Jacksonville rose notably from the prior

year. Limited service assets were a primary target for investors in the Jacksonville metro.

* Forecast

Sources: Marcus & Millichap Research Services; STR, Inc.

MARKET OVERVIEW

VERO BEACH REDEVELOPMENT

30

HOSPITALITY RESEARCH

Investors Maintain Confidence in Hospitality Market

As Occupancy and Revenue Metrics Improve

Hotel room demand persists. The U.S. hospitality sector has recorded increases in occupancy and revenue

metrics during the year ending in June as room demand remained healthy. Employment growth nationwide and

the rising median household income will support travel in the near future. Both domestic and international travel

continue to rise, further benefiting room demand. Potential headwinds do exist including the growing construction

pipelines in many major markets that may place downward pressure on occupancy, the average daily rate and

RevPAR this year and into 2018.

• During the last 12-month period, hiring in office-using sectors rose 2.4 percent nationwide as 734,000 workers

were added to staffs. Healthy job growth and a tight employment rate of 4.4 percent bolstered medium

household incomes by 2.8 percent during this time. The rising incomes may spur additional leisure travel while

increased jobs may further business travel.

• Domestic and international passenger travel in the United States rose 3.8 percent during 2016. In particular,

international travel provides hotel operators opportunities for stronger demand drivers as passengers more

than doubled in the last three years.

• Texas and California have more than 20,000 rooms each that are expected to break ground in the next 12

months. The increased supply may place downward pressure on occupancy in the coming years.

MIDYEAR 2017

MARKET OVERVIEW

VERO BEACH REDEVELOPMENT

31

HOSPITALITY RESEARCH

Investors increasingly targeting hotels as demand drivers improve. Hotel operations that spur revenue growth

have kept buyers active in this sector. Transaction velocity rose roughly 10 percent nationwide as demand picked

up for properties in many of the country’s smaller markets. On average, hotel assets changed hands for nearly

$100,000 per key, down slightly year over year as fewer properties in upper chain scales changed hands.

Among chain scales, lower-tier hotels garnered significant investor attention. Trades increased considerably

for economy and upper midscale assets during the previous four quarters. Demand for upscale assets held

steady with the majority of trades in Marriott and Hilton branded properties.

Several regions posted significant increases in transaction volume during the last 12 months. The Carolinas

and the Central Midwest region led the nation, with the Mid Atlantic, Mid South and Southwest regions

following. In prior years, coastal regions typically led sales volume.

Sales velocity picked up for independent properties during the year ending in June as buyers widened their

acquisition expectations. The increased demand for soft brand hotels may further intensify bidding for their

properties moving forward as visitors seek experience oriented hotels.

MIDYEAR 2017

MARKET OVERVIEW

HOSPITALITY RESEARCH

32

Hotel construction pipeline on the rise. Roughly 111,000 rooms in more than 950 hotel projects were

completed nationwide during the last 12 months up to June. Moving forward, nearly 187,000 rooms are under

development and an additional 222,000 are expected to break ground in the next four quarters. The growing

supply additions may place downward pressure in occupancy over the coming year.

The metros of Houston and New York City received the largest number of rooms as 4,200 and 5,400 rooms

were completed within July to June, respectively.

Hilton Worldwide and Marriott International boosted their inventory during the last 12 months. Both companies

averaged between 27 percent and 28 percent increases of new hotel rooms over all supply additions.

Among chain scales, the bulk of new completions were in the upscale and upper midscale segments with a

combined total of 77,000 rooms. Roughly 10,500 unaffiliated rooms were also constructed during this time. * Trailing 12 months through 2Q

MIDYEAR 2017

MARKET OVERVIEW

HOSPITALITY RESEARCH

33

Occupancy climbs amid healthy room demand. Since last June, demand for hotel rooms continued to outpace

supply growth, lifting occupancy in the United States 50 basis points to 73.4 percent at the end of the second

quarter. First half occupancy rose 40 basis points from the same time period last year to 65.3 percent.

Large markets that demonstrated significant occupancy increases from last year include Norfolk-Virginia

Beach, Orlando and Atlanta. On the other hand, mounting supply pressures in metros including Dallas,

Houston and Nashville weighed on vacancy improvement in the last 12 months.

Nearly all hotel chain scales posted occupancy improvements over the year ending in June. Economy chains

boasted the greatest improvement with occupancy increasing 90 basis points to 65.4 percent. The upscale

segment posted the only occupancy decrease as the rate ticked down 20 basis points year over year to 80.5

percent.

Based on location, occupancy in properties in proximity to major thoroughfares climbed 100 basis points

during the previous four quarters to 66.6 percent. Room demand in these hotels typically comes from travelers

passing by. The highest occupancy rate remains in urban hotels at 80.4 percent, up 50 basis points year over

year.

MIDYEAR 2017

MARKET OVERVIEW

HOSPITALITY RESEARCH

34

Room demand drives increases in revenue metrics. Rising occupancy nationwide is driving growth in revenue

metrics. During the year ending in the second quarter, the average daily rate advanced 2.1 percent to $129.12.

The increase in ADR and occupancy generated a 2.8 percent rise in RevPAR during this time to $94.73.

ADR and RevPAR in independent hotels outperformed all other chain scales, rising 2.7 percent and 3.9

percent, respectively. Economy hotels followed as strong occupancy improvement and a 2.2 percent increase

in ADR drove a 3.5 percent climb in RevPAR during the last 12 months.

Despite higher occupancy in urban areas, suburban hotels outperformed their counterparts in ADR and

RevPAR growth during the previous four quarters. ADR in urban hotels rose 0.3 percent while RevPAR inched

up 0.9 percent during this time. In the suburbs, ADR climbed 2.3 percent and RevPAR posted a 2.8 percent

advance.

Major markets with RevPAR growth near or above 10 percent include Norfolk-Virginia Beach, Orlando, and

San Diego.

MIDYEAR 2017

* Trailing 12 months through 2Q

MARKET OVERVIEW

HOSPITALITY RESEARCH

35

Total Airport Passengers in Major Markets

MIDYEAR 2017

2016 International Visitation

Passenger travel in the many of the nation’s largest

airports can highlight up-and-coming travel

destinations and the potential for improvement in hotel

occupancy and revenue metrics. The Los Angeles

International Airport registered an 8 percent increase in

passenger volume in 2016 from the prior year, making it

the second most traveled airport in the nation. During

this same time, hotel occupancy increased 100 basis

points in the Los Angeles metro while RevPAR jumped

10.9 percent year over year. Additionally, hotels located

near airports tend to have some of the highest

occupancy rates, compared with interstate, resort,

suburban and small metro hotels.

One of U.S. largest contributors to international

visitation, Brazil, was battered with political turmoil and

a recession leading to a 24 percent drop in arrivals in

2016. Many Florida markets are impacted from fewer

tourists visiting from the country and several of these

metros, including Orlando, registered occupancy

declines last year. On the other hand, the number of

tourists from China grew 15 percent in 2016 from the

prior year and that number is expected to increase. As

a result, many hotels are customizing amenities to

entice these travelers, including a hotel chain in

California that will now accept Chinese mobile

payments.

Travel Highlights

MARKET OVERVIEW

VERO BEACH REDEVELOPMENT

36

HOSPITALITY RESEARCH

Monetary policy in transition. Despite the Fed raising its benchmark short-term rate three times in seven months and signaling another rise before the end of the year,

long-term rates have remained stable. The yield on the 10-year U.S. Treasury bond remained in the low- to mid-2 percent range throughout the third quarter of 2017.

The Federal Reserve wants to normalize monetary policy and, in addition to raising its funds (or overnight lending) rate, has announced it will begin to taper its

balance sheet by allowing an initial $10 billion in securities to mature without reinvestment. By reducing its acquisitions of securities, 10-year Treasury rates should

drift upward, thereby widening the spread between short- and long-term rates.

Increase in interest rates over the course of the year, pushing up the cost of capital. While commercial real estate fundamentals remain strong, rising costs

associated with debt financing will tighten the spread between cap rates and lending benchmarks. This environment could weigh on transaction activity as investors

evaluate their yield options. Cap rates have remained relatively stable over the last year, but upward movement in Treasury rates has amplified the expectation gap

between buyers and sellers.

Capital markets remain highly competitive, with a broad assortment of fixed-rate products available. Year to date, CMBS market share has moved from a quarter of

the market up to comprising one-third of hotel lending. Loan-to-value for CMBS typically is in the low-60 percent range. Lending by national and regional/local banks

comprises a quarter of the lending activity this year with smaller loan sizes and LTV averaging from 60 percent to upwards of 90 percent for SBA products.

Capital Markets

MIDYEAR 2017

MARKET OVERVIEW

VERO BEACH REDEVELOPMENT

37

HOSPITALITY RESEARCH

Name State Rooms

Wyndham Garden Hotel Newark NJ 349

Clarion Orlando International Airport FL 330

Surfside Marina TX 281

Clarion Conversion KS 257

Holiday Inn & Suites Beaumont TX 253

Atrium Hotel & Conference Center KS 216

Cabot Lodge Jackson North MS 200

Crowne Plaza OH 200

A2B Budget Hotel GA 196

Fontana Village Resort NC 194

Denver’s Best Inn & Suites CO 190

Ramada Florence Center SC 190

Days Inn Birmingham South AL 159

Red Roof Inn St. Louis Westport MO 158

Holiday Inn & Suites WI 146

Clarion Inn & Suites Syracuse NY 143

Days Inn New Orleans LA 138

The Hotel Blue NM 140

Best Western Plus Westbank LA 138

Roadway Inn FL 125

Suburban Extended Stay South Bend IN 117

Days Inn Knoxville East TN 116

Holiday Inn Yakima WA 114

Motel 6 Tulsa South OK 114

2017 Marcus & Millichap Transactions

MIDYEAR 2017

PROPERTY NAME

MARKETING TEAM

VERO BEACH REDEVELOPMENT

DEMOGRAPHICS

Source: © 2016 Experian

Created on November 2017

POPULATION 1 Miles 3 Miles 5 Miles

2021 Projection

Total Population 2,283 20,929 59,326

2016 Estimate

Total Population 2,255 20,251 56,846

2010 Census

Total Population 2,159 19,540 54,722

2000 Census

Total Population 2,343 20,784 52,566

Daytime Population

2016 Estimate 2,544 33,177 71,395

HOUSEHOLDS 1 Miles 3 Miles 5 Miles

2021 Projection

Total Households 1,133 10,968 27,924

2016 Estimate

Total Households 1,108 10,577 26,598

Average (Mean) Household Size 2.08 1.91 2.10

2010 Census

Total Households 1,050 10,118 25,430

2000 Census

Total Households 1,086 10,866 24,166

HOUSING UNITS 1 Miles 3 Miles 5 Miles

Occupied Units

2021 Projection 1,133 10,968 27,924

2016 Estimate 1,521 14,170 33,649

HOUSEHOLDS BY INCOME 1 Miles 3 Miles 5 Miles

2016 Estimate

$200,000 or More 25.56% 8.11% 7.03%

$150,000 - $199,000 10.04% 3.51% 3.60%

$100,000 - $149,000 19.39% 10.72% 10.99%

$75,000 - $99,999 7.69% 7.17% 8.50%

$50,000 - $74,999 13.80% 14.18% 16.87%

$35,000 - $49,999 6.68% 11.77% 12.79%

$25,000 - $34,999 3.64% 12.58% 12.23%

$15,000 - $24,999 7.43% 17.11% 15.39%

Under $15,000 5.77% 14.84% 12.60%

Average Household Income $175,754 $83,706 $81,531

Median Household Income $111,948 $41,375 $46,069

Per Capita Income $86,356 $43,893 $38,250

POPULATION PROFILE 1 Miles 3 Miles 5 Miles

Population 25+ by Education Level

2016 Estimate Population Age 25+ 1,859 16,349 43,958

Elementary (0-8) 0.07% 2.24% 2.47%

Some High School (9-11) 0.77% 6.26% 7.31%

High School Graduate (12) 10.52% 24.64% 25.74%

Some College (13-15) 19.90% 22.36% 23.50%

Associate Degree Only 4.84% 6.75% 7.82%

Bachelors Degree Only 39.06% 23.06% 20.35%

Graduate Degree 24.75% 13.64% 11.66%

38

Income

In 2016, the median household income for your selected geography is

$111,948, compare this to the US average which is currently $54,505.

The median household income for your area has changed by 5.91%

since 2000. It is estimated that the median household income in your

area will be $124,578 five years from now, which represents a change

of 11.28% from the current year.

The current year per capita income in your area is $86,356, compare

this to the US average, which is $29,962. The current year average

household income in your area is $175,754, compare this to the US

average which is $78,425.

Population

In 2016, the population in your selected geography is 2,255. The

population has changed by -3.76% since 2000. It is estimated that

the population in your area will be 2,283.00 five years from now,

which represents a change of 1.24% from the current year. The

current population is 49.58% male and 50.42% female. The median

age of the population in your area is 60.53, compare this to the US

average which is 37.68. The population density in your area is 718.58

people per square mile.

Households

There are currently 1,108 households in your selected geography. The

number of households has changed by 2.03% since 2000. It is

estimated that the number of households in your area will be 1,133

five years from now, which represents a change of 2.26% from the

current year. The average household size in your area is 2.08 persons.

Employment

In 2016, there are 709 employees in your selected area, this is also

known as the daytime population. The 2000 Census revealed that

89.27% of employees are employed in white-collar occupations in

this geography, and 15.14% are employed in blue-collar occupations.

In 2016, unemployment in this area is 1.18%. In 2000, the average

time traveled to work was 16.00 minutes.

Race and Ethnicity

The current year racial makeup of your selected area is as follows:

97.79% White, 0.20% Black, 0.00% Native American and 0.88%

Asian/Pacific Islander. Compare these to US averages which are:

70.77% White, 12.80% Black, 0.19% Native American and 5.36%

Asian/Pacific Islander. People of Hispanic origin are counted

independently of race.

People of Hispanic origin make up 3.07% of the current year

population in your selected area. Compare this to the US average of

17.65%.

PROPERTY NAME

MARKETING TEAM

VERO BEACH REDEVELOPMENT

Housing

The median housing value in your area was $450,267 in 2016,

compare this to the US average of $187,181. In 2000, there were 959

owner occupied housing units in your area and there were 126 renter

occupied housing units in your area. The median rent at the time was

$677.

Source: © 2016 Experian

DEMOGRAPHICS

39

8

VERO BEACH REDEVELOPMENT

DEMOGRAPHICS

40

www.MarcusMillichap.com

Ahmed Kabani

First Vice President Investments

Senior Director - National Hospitality Group

Miami Office

Tel: (786) 522-7000

Fax: (786) 522-7010

License: FL SL3115103

Garrick Benabe

Agent Candidate

Miami Office

Tel: (786) 522-7000

Fax: (786) 522-7010

License: FL SL3385321

Jesse Bajaj

SIP

Member - National Hospitality Group

Miami Office

Tel: (786) 522-7026

Fax: (786) 522-7010

License: FL SL3385910

P R E S E N T E D B Y

41