ÒMarket leader w i t h innovative productsimg2.kbstar.com/obj/eng/2000_kcc_annual.pdf · Kookmin...

59

ANNUAL REPORT 2 0 0 0 “Market leader with innovative products ”

Transcript of ÒMarket leader w i t h innovative productsimg2.kbstar.com/obj/eng/2000_kcc_annual.pdf · Kookmin...

A N N U A L R E P O R T 2 0 0 0

“Market leader w i t h

innovative products”

P r o f i l e

Kookmin Credit Card Company dates to 1987 when the credit card division of

Kookmin Bank, Korea's largest commercial bank, became an independent

business entity. In its comparatively brief history, the Company has experienced

phenomenal growth in quality and in quantity. Its flagship product, the Kookmin

Pass Card, is the most widely used credit card in Korea, with a membership that

exceeded three million by the end of 2000. Mainly because of its market

leadership and the growth potential, the Company successfully carried out an

initial public offering, regardless of market environments and became the first

one in the domestic credit card industry to list its shares on the KOSDAQ.

In addition to its substantial growth potential, the Company also benefits from

sound business management. In 2000, the Company turned in the best profit

performance in its history. In recognition of its business performance and

potential growth, Asiamoney included the Company in its annual list of "Best-

Managed Companies in the Asia-Pacific region."

Financial Highlights

Vision & Strategy

Message from the Management

Highlights of the Year

Kookimn Card Products

Financial Sectoin

Organization Chart

Board of Directors

Corporate Data

1

2

4

7

11

21

54

55

56

1999 2000 1999 2000

Net Income 43 301 34,049 238,581

Operating Revenue 897 1,461 711,853 1,159,482

Credit Card 592 1,218 470,201 966,923

Card Loan 157 167 124,406 132,732

Others 148 76 117,246 59,827

Total Assets 4,225 8,181 3,353,884 6,494,781

Shareholders’ Equity 346 803 274,541 637,079

R O A 1.03% 4.84% 1.03% 4.84%

R O E 14.57% 52.36% 14.57% 52.36%

Notes : 1) Fiscal year 2000 ended on December 31, 2000 .

2) Won amounts have been translated at the rate 1,259.70=US$ 1, the rate prevailing on December 31, 2000.

(in Billions of Korean Won) (in Thousands of U.S. Dollars)

1Kookmincard Annual Report 2 0 0 0

Total Asset(In Billions of Korean Won)

Net Income(In Billions of Korean Won)

‘99 ‘00

Shareholder’s Equity(In Billions of Korean Won)

‘98 ‘99 ‘00 ‘98 ‘99 ‘00

F i n a n c i a l H i g h l i g h t s

www.kookmincard.co.kr2

Vis ion &

VISION

Kookmin Card's vision is to become "the

customer's main card and the industry's major

card." The Company's strategic objectives focus on

transforming itself into a customer-oriented,

value-driven institution managed by first-class

human resources and supported by advanced

corporate governance.

MANAGEMENT STRATEGY

Each strategic objective is built upon specific,

measurable goals, as outlined in the following

paragraphs.

Customer-orientedoperations

Develop products and services suited to

customer needs.

Align all business processes toward improving

customer service.

Develop a comprehensive evaluation system

to monitor customer satisfaction.

Adopt an advanced Customer Relationship

Management (CRM).

Value-driven managementAggressively pursue strategic alliances with

mutually compatible businesses.

Improve credit risk management .

Develop value-added products and market them

through various marketing channels including

Kookmin Bank's extensive branch network.

“ The customer’s Main Card ,

the industry’s Major Card ”

3Kookmincard Annual Report 2 0 0 0

S t r a t e g y

Advanced corporategovernance

Develop a corporate structure that is more

responsive to environmental changes.

Constantly upgrade a decision support system that

will create a more information-based planning

process.

First-class human resourcesExtend employee training programs.

Develop a performance-based compensation

system and adopt a comprehensive evaluation

system.

Foster a work atmosphere that encourages

self improvement and information sharing.

CORE BUSINESS STRATEGY

Credit Card BusinessApproach each customer segmentation with a

unique combination of products using CRM

system that meet customer needs:

Pass Card.

e-Queens Card.

Platinum Card.

Co-branded Card

Financing BusinessCover niche markets by expanding the service line

into areas such as:

Personal card loans.

Auto loans.

Corporate financing.

e-BusinessMake an all-out effort to establish a leading

position in the following areas:

B2B.

B2C.

Electronic money

Cross-sell BusinessCross-sell such products designed to make life

more convenient as :

Insurance and related products.

Travel and related products.

On-line shopping

www.kookmincard.co.kr4

“Historic record of net income represents a sixfold increase over the last year. ”

Dear Shareholders,

Fiscal 2000 was an outstanding year for Kookmin Credit Card Company . We

achieved our long-held goal of becoming a publicly-listed company and we

posted the best annual business performance since our inception. At the same

time, we continued to earn distinguished industry endorsements.

On the fourth of July, we took a momentous step and went public with a listing

on the KOSDAQ. With this public offering, we became the first and only credit

card company to list its shares in Korea. The success of this effort is evident

from the fact that we has attained the second largest market capitalization

among KOSDAQ-listed companies, and has garnered enthusiastic recognition

from domestic and foreign investors alike.

Over the past year, we has achieved industry-leading business results. Our net

income was W301 billion, the largest in the Company's history. This record

income represents a sixfold increase over the previous year's results. Return on

assets (ROA) and return on equity (ROE) likewise jumped- from 1.03 to 4.84%

and from 14.57 to 52.36%, respectively. Cardholders rose 2.7 million to 8.2

million. Total business volume soared 172% to W38 trillion. Our delinquency

ratio was reduced to less than 3%, the lowest in the history.

Youn-Ki KimPresident and Cheif Executive Officer

Our outstanding business performance was capped by some coveted industry

accolades. For the third consecutive year, we were named the best credit card

company in an annual customer satisfaction survey by the Korean

Management Association. A new level of recognition was achieved when the

widely respected financial journal Asiamoney named us to its Year 2000 list of

best-managed companies in the Asia-Pacific region. In selecting us, it cited our

Card gross volume(In Billions of Korean Won)

‘98 ‘99 ‘00

M e s s a g e f r o m t h e M a n a g e m e n t

5Kookmincard Annual Report 2 0 0 0

"stronger market position through an aggressive operating strategy and focus on

reducing delinquency." Kookmin Credit Card was the first one of three newly

listed companies to be included on the Asiamoney list.

As the journal pointed out, we have maintained its delinquency ratio low

despite a huge increase in total business volume, thanks mainly to its

strengthened credit risk management system. In particular, the improved credit

scoring system was instrumental in bringing the delinquency ratio to the

industry's lowest level. As credit card business is heavily exposed to credit risk,

we will continue to improve upon its credit scoring system.

R O A(%)

R O E(%)

‘98 ‘99 ‘00

‘98 ‘99 ‘00

Although last year was favorable to credit card business, this year will present

several daunting new challenges. Major economic indicators continue to point

downward, and consumption is on a steady decline. In addition, several new

players are expected to enter the credit card market.

However challenging the business environment may be, we are confident that

we will continue to make the best out of what's given and grow into Korea's best

credit card company. Following is the detailed action plan we have drawn up for

the coming year.

First, we will continue to focus on enhancing shareholder value. We plan to

listen carefully to customer needs, in order to develop new best-selling products.

We will bolster our business base by rearranging our sales network and adopting

new marketing systems. Our asset quality will continue to improve, while our

net interest spread is forecast to widen.

Second, we will increase long-term investments in order to secure the number

one position in e-business sector. To position ourselves for greater growth, we

will expand our infrastructure for e-business. Our goal is to lead the industry by

adopting innovative online products and services.

Third, we will step up its efforts to improve customer relations. Specifically, we

will establi sh a new unit dedicated to the management of customer

relationships. As we improve and enlarge the customer database, we will be

equiped with advanced customer management systems to ensure continued

attention to these valued relationships.

“Kookmin Credit Card was named oneof best-managed companies in theAsia-Pacific region by Asiamoney.”

www.kookmincard.co.kr6

Fourth, we will continue to foster a corporate culture where all Company

members can share and enjoy the fruits of their hard work. To this end, we will

bring transparency to all aspects of the business, including personnel

management. At the same time, we will adopt a performance-based

compensation system, which is backed by an advanced performance evaluation

system.

Our vision is simple and realistic: to become the most-recognized credit card

brand in Korea. And we have what it takes to be the best: a well-respected brand

identity, a wide range of competitive products, a hard-working work force

dedicated to customer care, and a quality customer base. While cultivating our

high-net-worth customers with superior services and products, we will focus on

strengthening our e-business base and developing niche markets.

Fiscal 2000 evinced the capability of our making the top brand in the Korean credit card

market and I am sure fiscal 2001, regardless of market environment, will bring us a step

closer to that vision. It was a real pleasure to report to you last year's outstanding business

performance, and it is equally exciting to look forward to sharing with you another great

business report the same time next year.

Sincerely,

Youn-Ki KimPresident and Cheif Executive Officer

E P S(In Korean Won)

‘98 ‘99 ‘00

7Kookmincard Annual Report 2 0 0 0

H i g h l i g h t s o f t h e Ye a r

www.kookmincard.co.kr8

1. KOSDAQ ListingOn the fourth of July, the Company became the

first domestic credit card company to list its shares

on the KOSDAQ. The listing of the Company was

a long-waited event for domestic and foreign

investors alike. The domestic credit card market

has long been regarded as a highly desirable

investment opportunity, and analysts now view

Kookmin Credit Card as a company to watch. By

the end of 2000, the Company had the second

largest market capitalization among KOSDAQ-

in the industry. The card became an instant hit

when it was introduced in April 1997, because of

its convenience and customer-oriented feature.

Cardholders can use the card as a pass to ride

public transportation systems such as the subway

and buses, and then pay for the fares as part of

their monthly credit card payment.

3. No. 1 in Customer SatisfactionThe Company's years-long dedication to customer

service earned the Company another coveted

Becoming the first domesticcredit card company to list onthe KOSDAQ

listed companies. With this public offering, the

Company's paid-in capital rose to W366 billion

and Kookmin Bank's stake in the Company was

reduced from 92.96% to 74.27%, while the

combined free floated share increased to 20.3%.

2. Pass Card PatentThroughout 2000 and 2001, the Company

obtained patent r ights to an automated fare

control system, which utilizes Radio Frequency

(RF) technology for debit and credit card

products, thereby further consolidating its leading

position in the domestic public transportation

smart card market. At year-end, cardholders of the

Kookmin Pass Card, a multi-functioning credit

card, exceeded three million, making it the largest

industry recognition in 2000. The Company was

named the best credit card company for the

third consecutive year in an annual customer

satisfaction survey sponsored by Korea

Management Association and also named the

best crdit card company in service quality in

annual Korean Standard-Service Quality Index

Survey sponsored by Korea Standard

Association. Three years ago, the Company set

out to offer the best customer service of any

credit card companies and, to this end, it

launched an extensive customer satisfaction

campaign. Since then, a strategic unit has been

formed to bolster new product development

and marketing, an e-business unit was

For the third consecutive year,the best company in an annualcustomer satisfaction surveysponsored by KMA

9Kookmincard Annual Report 2 0 0 0

established for the first time in the industry to

offer more convenient services, and a Customer

Satisfaction Center was created to better respond

to customer questions and needs.

4. e-Business ExpansionIn response to the fast-growing use of credit cards

as the main means of paying for online

transactions, the Company introduced a line of

innovative products and services, including cyber

branches, exclusive for online transactions in

5. ezLoanAs a leader in the development of innovative

products, the Company has introduced a new

product that is certain to trigger a new industry

trend. Called "ezLoan", this product allows

Kookmin credit card customers to borrow loans

with just one phone call or few clicks in the

Company's web site. Available to some 3.5 million

customers with a good credit record, the ezLoan is

a pre-approved service that features three "no's":

no collateral, no document, and no visit to a

cooperation with leading online service businesses.

The new products and services are both safer and

easier to use than conventional credit cards, which

require the user to reveal personal information

over the Net. They are safer because they employ

the latest encryption technology and easier

because they require only a password for

authorization. Some of the most advanced

products and services are:

Other newly introduced e-business-related

services include online card application, billing via

e-mail, Internet loans, Internet cash advances,

online shopping and online travel services.

office. As soon as a qualified customer requests a

loan over the phone or internet, the money is

credited to his/her account. Annual interest rates

range from the industry's lowest (9.5%) up to

17.9%, depending on the borrower's credit record.

A sliding system is also applied to readjust the

interest rate according to the borrower's

repayment status. The borrower can select a loan

term ranging from 3 to 36 months.

6. Record Net Income PerformanceThe Company's business performance in 2000 was

outstanding. The Company posted a net income of

W301 billion, the largest in the Company history.

The figure represents a sixfold increase over the

previous year. The stellar performance can be

The new e-business productsand services are both saferand easier to use thanconventional credit cards

www.kookmincard.co.kr10

ascribed to favorable market developments: a fast-

rising use of plastic money on the back of a

government promotional campaign and falling

funding costs . The Company's aggressive

marketing also played a major contributing role.

Likewise, return on assets (ROA) jumped from

1.03% to 4.84% and return on equity (ROE) rose

from 14.57% to 52.36%.

7. Best-managed Company in KoreaThe Company's industry-leading business

performance was endorsed by a leading industry

journal. the Company made Asiamoney's Year

2000 list of best-managed companies in Asia-

Pacific. In selecting the Company, the journal

pointed to the Company's "stronger market

position through an aggressive operating strategy

in line with the rapid growth of the credit card

industry."

8. Risk ManagementThe Company's credit risk management system

substantially improved last year, playing a decisive

role in bringing down the delinquency ratio to the

industry's lowest level. The system consists of a

model for making credit policy and a credit

scoring system for setting and adjusting credit

limit on individual borrowers. The credit scoring

system was particularly upgraded and

strengthened. This analyzes new applicants' credit

status and current customers' credit status by

using the credit database. The system not only has

accumulated a vast amount of internal credit card

information, but also is connected with credit

bureaus for constant updating of credit data.

‘ezLoan’ allows customers toborrow loans with just onephone call or few clicks

11Kookmincard Annual Report 2 0 0 0

K o o k m i n C a r dP r o d u c t s

Market Overview

In 2000, the Korean credit card market more than

doubled in size. The Government's incentives-based

promotional campaign and a mounting public

preference for plastic money combined to grow the

market by 148%; many experts agree that the market

will continue to post gradually increasing rates in the

next few years.

“One card does it all !”

www.kookmincard.co.kr12

Kookmin Pass CardThanks in part to the push of government incentives

and the pull of consumer demand for plastic currency,

the Company enjoyed robust business growth last year.

Total credit card transaction volume soared 172% over

the previous year. This better-than-market growth rate,

however, should be credited to the Company's main

product-the Kookmin Pass Card.

When the Pass Card was introduced a few years ago, it

became an instant hit because of its innovative features.

With convenient and innovative benefits, this credit

card can be used as a mode of payment for subway and

Kookmin Pass Card

other public transportation systems. In fact, it is the

only credit card in Korea that doubles as a public

transportation pass with a deferred payment system:

The radio frequency (RF) technology of the card, in

conjunction with the automated fare control (AFC)

system, allows the cardholder to use public

transportation by simply holding the card near the

sensor; the user then pays the fares on a monthly basis.

This, the world's first contactless, deferred-payment

system, has been patented in the U.S., Australia, and

Canada. Because of its convenience, the Pass Card has

enjoyed explosive growth in acquisition since its rollout.

Card Holders(in Thousands)

‘98 ‘99 ‘00

M e r c h a n t s(in Thousands)

‘98 ‘99 ‘00

1Kookmincard Annual Report 2 0 0 0

As of the year-end, the Pass Card had the largest

enrollment of any credit card product in Korea.

The Company's dominance of the domestic

transportation card market is expected to continue for

some time, although other credit card companies are

gearing up to capture a slice of the lucrative market. the

Company has recently secured patent rights to the

automated fare control technology, which is the standard

technology used in the card-based transportation fare

collection in the Seoul Metropolitan area.

Encouraged by the success o f the Pass Card, the

Company is aggressively exploring ways to add to its

diversity. While enriching its bonus point program with

bigger discount rates and an expanded merchant

network, the Company has recently been pursuing joint

promotion through several business alliances.

Free Pass Card

Lump-sum purchase(in Billions of Korean Won)

‘98 ‘99 ‘00

Installment purchase(in Billions of Korean Won)

‘98 ‘99 ‘00

Cash advance(in Billions of Korean Won)

‘98 ‘99 ‘00

www.kookmincard.co.kr14

Asiana Club CardAsiana Bonus Club is a co-branding credit card

developed jointly with a leading airline. Promoted and

marketed by the airlines, this co-branding card can also

be used as the Pass Card for public transportation. In

addition to being used to purchase goods and services,

the card also offers special bonus mileages for ticketing

through the airlines, buying goods and services, and

staying at affi l iated hotels a t home and abroad.

Accumulated mileages can be redeemed in free air

tickets. Another convenient feature of this card is its

automated airline ticketing service. By placing the card

in contact with the airlines' automated t icketing

machines at the airport, the customer with a flight

reservation can have ticketing done without help of

airline employees.

Asiana Club Card

“ Providing exclu s ivem i l ea ge progra m s”

15Kookmincard Annual Report 2 0 0 0

e-Queens is a multipurpose credit card exclusively

for women. As women constitute an important

part of the credit card market, the Company has

introduced this credit card to offer a variety of

services designed to meet the particular needs of

women customers. In addition to the

transportation features of the Pass Card, the e-

Queens card offers an installment payment service

with no interest charge for up to three months, as

well as various discount services at major

department stores. Other features designed to

appeal to women include discount services from

major beauty parlor chains and marriage

information agencies. The introduction of the e-

Queens card was in line with the Company's new

marketing strategy to segment the customer and

develop new products for each segment. To

consolidate its position in this increasingly

important market segment, the Company will

continue to add new features that anticipate

women's needs.

e-Queens

e-Queens Card

“Offering what women want”

www.kookmincard.co.kr16

e-BusinessYahoo-Kookmin CardThe Yahoo-Kookmin Card is a credit card developed in

cooperation with Yahoo Korea, the biggest Korean

portal. This Internet-oriented card is very popular with

younger generations. Cardholders have been more than

doubled over the previous year to more than 150,000 at

of the end of 2000. In addition to normal credit card

functions, the Yahoo-Kookmin Card offers "cyber

cash"-a point accumulation and redemption system and

email-based services such as daily stock reports and

other stock market-related information.

Tellsign ServiceThis service allows the customer to purchase goods

at online shopping malls without a complicated

authentication process. When a customer

purchases a good or service and makes an

electronic payment transaction using his/her

Tellsign ID and password, a short message is sent

out to the buyer via his/her cellu lar phone

informing the transaction. If the buyer confirms

the transaction by responding to the message via

the phone, the transaction receives approval from

the credit card company and the purchase is

carried out as in the case of normal credit card use.

Yahoo-Kookmin Card

“Leading the era of digital

credit cards”

17Kookmincard Annual Report 2 0 0 0

CD CashIn a strategic alliance with an online payment solution

provider, the Company introduced Kookmin CD Cash,

an exclusive online payment system. Designed to be

used with a personal computer, this credit card-shaped

compact disk (CD) contains links to some 3000 online

shopping malls. By placing the product into the

computer's CD drive and activating the system, the

customer can enjoy online shopping with a simple

password.

Virtual CardA password is all it takes to use this virtual credit

card, which contains an advanced, embedded

authentication certificate technology.

e-MarketplaceThe Company has created an online marketplace for

businesses that cannot afford their own B2B electronic

transaction system. Called K-B2B e-Marketplace, this

system allows small businesses to host their own B2B or

B2C mall for free of charge. Sellers and buyers can

conduct business transactions using the Company's

corporate purchasing card.

Online-Service Membership(in Thousands)

‘99 ‘00

CD Cash

www.kookmincard.co.kr18

Platinum CardThe Platinum Card is the Company's premier-

class credit card for its high-net-worth customers.

To be worthy of the contribution of the customers

to the Company, this prestigious credit card offers

a wide range of services and benefits not available

with other cards. First of all, the minimum

spending limit is set at W20 million, the highest of

any credit card in the company. The Platinum

Cardholders are also entitled to VIP treatment at

Kookmin Bank, Korea's largest commercial bank.

Other desirable benefits and services include

discounted lodging at some 45,000 hotels in 140

countries, cut rates at major auto rental chains,

and a 10% to 50% reduction at some 3000

affiliated merchants around the world. In addition

to these discount services, a free medical check-up

and life insurance policy come with the card. Its

bonus point program is also top-of-the-line,

awarding five times the number of points available

from regular credit cards. The company also

publishes a newsletter for platinum cardholders.

Platinum cardholders(in Thousands)

‘99 ‘00

Platinum Card

“Offering theluxuries of life

to those who deserve”

19Kookmincard Annual Report 2 0 0 0

Commercial CardsCorporate CardThe corporate card is issued to qualified

corporates. The credit limit is set based on the

corporate customer's size of revenues and capital

and the type of business. This card can be used for

procurement, travel, entertainment, training and

other activit ies related to business. As only

entertainment activities paid for with corporate

cards are regarded as legitimate business expenses,

corporate cards are gaining a wider acceptance

among businesses.

Purchasing CardThe Kookmin Purchasing Card is another product

gaining a bigger customer base thanks in part to a

supportive government policy. Designed primarily

for transactions among businesses, this card is fast

establishing as part of a main settlement medium

for B2B transactions, replacing the promissory

note system.

Corporate Card

Purchasing Card

“Meeting various needs of corporate

customers”

www.kookmincard.co.kr20

Installment Financing

Card loans grew an impressive 141% over the year

to W944billion. To better meet such a growing

demand for easy cash the company supplies

diversified card loan products.

ez LoanThe Company has made it easy to borrow small

amounts. The ezloan, which is available to

customers with good credit ratings, a llows

customers to borrow up to W5 million through an

Interactive Voice Response (IVR) system and

Internet, which eliminates collateral and paper

work.

Home loanAlthough termed as home loans, these are

essentially multi-purpose loans. Available to

customers with a regular source of income, the

average limit of Home Loan program is W5

million for non-collaterized loans.

Card Loan(in Billions of Koeran Won)

‘98 ‘99 ‘00

Card Loans

Installment loanIn response to a fast-growing housing loan

market, the Company provides a wide selection of

loan products designed to help customers enjoy

life's material comforts.

Auto financingA leading credit card company, the Company

offers auto financing plans with up to 60 months

to pay and W25 million on credit. The interest

rates charged are very competitive, ranging from

10.8% to 12.5%. The financing plans cover just

about every type of passenger car, including

imported cars and some trucks.

21Kookmincard Annual Report 2 0 0 0

F i n a n c i a lS e c t i o n

www.kookmincard.co.kr22

Operating results

Operating revenue 1 , 4 6 0 . 6 8 9 6 . 7 7 5 3 . 8

Operating expense 7 6 6 . 9 5 5 4 . 1 4 9 1 . 6

Operating income 4 3 8 . 0 8 4 . 7 - 5 1 . 8

Net income 3 0 0 . 5 4 2 . 9 - 3 0 . 7

Per share data(won)

Earning per common share 4 , 5 7 7 7 8 8 - 1 , 1 4 0

Dividend per common share* 7 5 0 2 5 0 0

Profitability ratios

Return on assets 4 . 8 4 1 . 0 3 - 0 . 8 2

Return on stockholders' equity 5 2 . 3 6 1 4 . 5 7 - 1 5 . 5 8

Net interest spread 1 2 . 4 9 8 . 8 7 9 . 1 9

Balance sheet data at year end

Total assets 8,181.5 4 , 2 2 4 . 9 4 , 1 2 6 . 0

Credit card assets 7 , 0 8 0 . 3 3 , 3 9 8 . 8 2 , 5 7 5 . 0

D e b e n t u r e s 4 , 5 6 1 . 0 2 , 1 4 0 . 9 2 , 1 6 7 . 3

Common stocks 3 6 6 . 0 2 9 2 . 4 2 4 2 . 4

Asset quality ratios

NPL ratio 3 . 0 5 7 . 5 4 1 5 . 2 0

Capital adequacy ratio 1 0 . 1 9 9 . 1 1 5 . 7 9

(In billion won,%)

Key Financial Data

2000 1999 1998

December 31, 2000 and 1999

Management Discussion & Analysis

Overvi ew

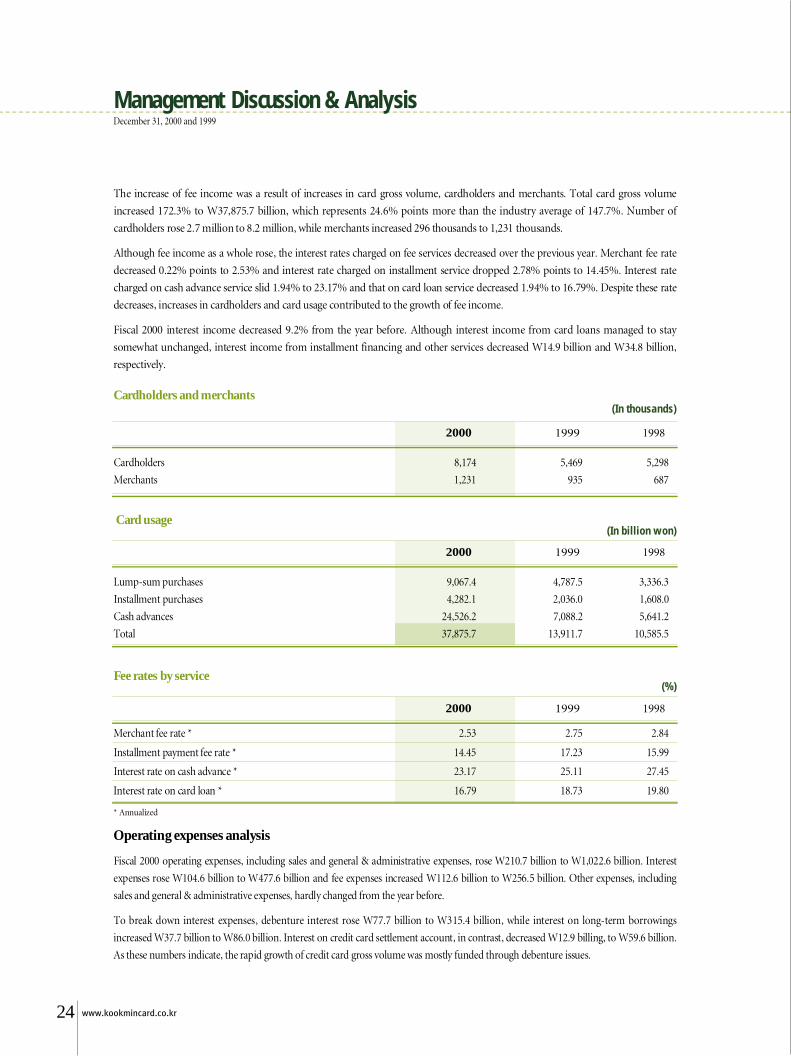

Kookmin Credit Card Company's 2000 business performance markedly improved over the previous year. Operating income

soared 62.9% over the year to W1,460.6 billion and net income jumped 600.5% to W300.5 billion. Reflecting the impressive

growth of net income, ROA and ROE rose 3.81% points and 37.79% points over the year to 4.84% to 52.36%, respectively.

Meanwhile, total assets swelled W3,956.6 billion to W8,181.5 billion, thanks mainly to a huge increase in credit card assets.

Shareholders equity increased by W73.6 billion thanks to the initial public offering in 2000, while CAR(capital adequacy ratio)

improved 1.08% points to 10.19%.

Profit and loss analys i s

Fiscal 2000 revenues rose 62.9% over the previous year to W1,460.6 billion, while business expenses increased 38.4% to W766.0

billion. Sales and general administrative expenses, however, decreased, albeit slightly. As a result, operating income swelled W353.2

billion to W438.0 billion and net income jumped W257.6 billion to W300.5 billion.

Operating income and net income rose substantially over the year mainly because of a rising credit card-based consumption

encouraged by a recovering economy after the financial crisis. Another contributing factor is that the government actively

* 1999 dividend per share reflects the stock split of 2000

23Kookmincard Annual Report 2 0 0 0

encouraged the use of credit cards as a way to raise taxes while bringing transparency to business transactions. The public, seeing

the benefits of using the plastic money, also increasingly preferred credit cards. In step with the government campaign and the

growing public preference of credit cards, the Company launched efforts to expand its market share.

In addition to these external factors, internals factors played an important role as well. The Company's stable business

infrastructure, price competitiveness, excellent risk management system & information technology, funding power, synergy from

sharing Kookmin Bank's network and pioneering e-commerce-related card business are some of the internal factors that led to the

rapid growth.

Opera ting income analys i s

As mentioned earlier, 2000 revenues rose substantially over the year 1999. To break down revenues, fee income rose 105.4% to

W1,245.3 billion, while interest income decreased 9.2% to W207.5 billion. The other income category took a less part of total

income.

Of total revenues, fee income, which is almost all credit card related, accounted for 85.3%, a 17.7% point increase compared with

the year before. Of fee income, the cash advance part was the most prominent growth category, increasing W388.6 billion to

W589.4 billion. The second biggest growth category was merchant fees which rose W134.8 billion to W320.8 billion. Installment &

Late Payment fees also rose W51.1 billion to W187.3 billion.

December 31, 2000 and 1999

Management Discussion & Analysis

R e v e n u e s 1 , 4 6 0 . 6 8 9 6 . 7 7 5 3 . 8

e x p e n s e s 7 6 6 . 9 5 5 4 . 1 4 9 1 . 6

Sales & general administrative expenses 2 5 5 . 7 2 5 7 . 9 3 1 4 . 0

Operating income 4 3 8 . 0 8 4 . 7 - 5 1 . 8

Ordinary income 4 3 5 . 7 8 5 . 9 - 2 7 . 9

Net income 3 0 0 . 5 4 2 . 9 - 3 0 . 7

(In billion won,%)

2000 1999 1998

Profit and loss

Fee income 1 , 2 4 5 . 3 6 0 5 . 2 5 4 2 . 8

Cash advance fees 5 8 9 . 4 2 0 0 . 8 1 9 5 . 5

Merchant fees 3 2 0 . 8 1 8 6 . 0 1 2 8 . 0

Installment & late payment fees 1 8 7 . 3 1 2 2 . 7 1 6 1 . 7

Other fees 1 4 7 . 8 9 6 . 7 5 7 . 6

Interest income 2 0 7 . 5 2 2 8 . 6 1 9 7 . 9

Card loans 1 5 0 . 1 1 4 9 . 0 1 5 8 . 0

Installment financing 1 2 . 0 2 6 . 9 1 4 . 4

Dividend from securities 2 7 . 6 0 . 1 0 . 2

Other interest income 4 5 . 4 5 2 . 7 2 5 . 5

Other revenues 7 . 8 6 2 . 9 1 3 . 1

Total revenues 1 , 4 6 0 . 6 8 9 6 . 7 7 5 3 . 8

(In billion won)

2000 1999 1998

Revenue breakdown

www.kookmincard.co.kr24

The increase of fee income was a result of increases in card gross volume, cardholders and merchants. Total card gross volume

increased 172.3% to W37,875.7 billion, which represents 24.6% points more than the industry average of 147.7%. Number of

cardholders rose 2.7 million to 8.2 million, while merchants increased 296 thousands to 1,231 thousands.

Although fee income as a whole rose, the interest rates charged on fee services decreased over the previous year. Merchant fee rate

decreased 0.22% points to 2.53% and interest rate charged on installment service dropped 2.78% points to 14.45%. Interest rate

charged on cash advance service slid 1.94% to 23.17% and that on card loan service decreased 1.94% to 16.79%. Despite these rate

decreases, increases in cardholders and card usage contributed to the growth of fee income.

Fiscal 2000 interest income decreased 9.2% from the year before. Although interest income from card loans managed to stay

somewhat unchanged, interest income from installment financing and other services decreased W14.9 billion and W34.8 billion,

r e s p e c t i v e l y .

Opera ting expenses analys i s

Fiscal 2000 operating expenses, including sales and general & administrative expenses, rose W210.7 billion to W1,022.6 billion. Interest

expenses rose W104.6 billion to W477.6 billion and fee expenses increased W112.6 billion to W256.5 billion. Other expenses, including

sales and general & administrative expenses, hardly changed from the year before.

To break down interest expenses, debenture interest rose W77.7 billion to W315.4 billion, while interest on long-term borrowings

increased W37.7 billion to W86.0 billion. Interest on credit card settlement account, in contrast, decreased W12.9 billing, to W59.6 billion.

As these numbers indicate, the rapid growth of credit card gross volume was mostly funded through debenture issues.

December 31, 2000 and 1999

Management Discussion & Analysis

Lump-sum purchases 9 , 0 6 7 . 4 4 , 7 8 7 . 5 3 , 3 3 6 . 3

Installment purchases 4 , 2 8 2 . 1 2 , 0 3 6 . 0 1 , 6 0 8 . 0

Cash advances 2 4 , 5 2 6 . 2 7 , 0 8 8 . 2 5 , 6 4 1 . 2

T o t a l 3 7 , 8 7 5 . 7 1 3 , 9 1 1 . 7 1 0 , 5 8 5 . 5

(In billion won)

2000 1999 1998

Merchant fee rate * 2 . 5 3 2 . 7 5 2 . 8 4

Installment payment fee rate * 1 4 . 4 5 1 7 . 2 3 1 5 . 9 9

Interest rate on cash advance * 2 3 . 1 7 2 5 . 1 1 2 7 . 4 5

Interest rate on card loan * 1 6 . 7 9 1 8 . 7 3 1 9 . 8 0

(%)

2000 1999 1998

Card usage

Fee rates by service

C a r d h o l d e r s 8 , 1 7 4 5 , 4 6 9 5 , 2 9 8

M e r c h a n t s 1 , 2 3 1 9 3 5 6 8 7

(In thousands)

2000 1999 1998

Cardholders and merchants

* Annualized

Sales and general & administrative expenses remained somewhat unchanged from the year before. By item, salaries rose 41.3% to W51.0

billion and loss from allowance for bad debt inched up 4.1% to W113.6 billion. Other expenses, in contrast, decreased W21.6 billion to

W91.1 billion. Rising prices and the expansion of business led to an increase in just about every expense category.

Fu n d i n g

Total funds raised averaged W6,823.6 billion in 2000, W1,980.3 billion more than 1999. By category, debenture issues made up the largest

portion at 49.2%, up 6.9% points over the year before. Short-term borrowings followed next, at 16.5%, up 5.2% points. The credit card

settlment account, openned at Kookmin Bank dropped 4.5% points to 8.3%. Though shareholders equity increased W55.7 billion due to

the stock listing and the net income, its ratio to total funds raised shrank 0.8% points to 4.9% because of the expansion of business volume.

25Kookmincard Annual Report 2 0 0 0

December 31, 2000 and 1999

Management Discussion & Analysis

Interest expenses 4 7 7 . 6 3 7 3 . 0 3 8 2 . 6

D e b e n t u r e s 3 1 5 . 4 2 3 7 . 7 1 6 9 . 1

Long-term borrowings 8 6 . 0 4 8 . 3 1 0 2 . 7

Credit card settlement account 5 9 . 6 7 2 . 5 9 4 . 0

Other interest expenses 1 6 . 6 1 4 . 5 1 6 . 8

Fee expenses 2 5 6 . 5 1 4 3 . 9 1 0 0 . 8

C o m m i s s i o n s 1 0 9 . 0 6 3 . 0 5 5 . 3

A f f i l i a t i o n s 3 5 . 5 1 7 . 7 1 4 . 0

Card acquisition 2 9 . 6 6 . 0 5 . 1

P r o c e s s i n g 2 0 . 6 1 0 . 0 5 . 2

Other fee expenses 6 1 . 8 4 7 . 2 2 1 . 2

Other operating expenses 3 2 . 8 3 7 . 2 8 . 2

Sales and general expenses 2 5 5 . 7 2 5 7 . 9 3 1 4 . 0

S a l a r i e s 5 1 . 0 3 6 . 1 4 2 . 5

W r i t e - o f f s 1 1 3 . 6 1 0 9 . 1 2 1 2 . 7

Other expenses 9 1 . 1 1 1 2 . 7 5 8 . 8

Total operating expenses 1 , 0 2 2 . 6 8 1 1 . 9 8 0 5 . 6

(In billion won)

2000 1999 1998

Operating expenses

(In billion won, %)

2000 1999 1998

Amount Ratio Amount Ratio Amount Ratio

Short-term borrowings 1 , 1 2 2 . 7 1 6 . 5 5 4 9 . 2 1 1 . 3 8 8 0 . 9 2 4 . 8

Credit card settlement account 5 6 6 . 4 8 . 3 6 1 8 . 1 1 2 . 8 6 7 0 . 9 1 8 . 9

D e b e n t u r e s 3 , 3 6 2 . 4 4 9 . 2 2 , 0 5 0 . 0 4 2 . 3 1 , 1 6 1 . 1 3 2 . 7

Long-term borrowings 2 0 1 . 5 3 . 0 1 4 6 . 6 3 . 0 2 4 . 2 0 . 7

Shareholders equity 3 3 1 . 4 4 . 9 2 7 5 . 7 5 . 7 1 5 4 . 9 4 . 4

Operating income 6 4 2 . 0 9 . 4 4 5 6 . 9 9 . 4 3 5 7 . 7 1 0 . 0

O t h e r 5 9 7 . 2 8 . 7 7 4 6 . 8 1 5 . 5 3 0 1 . 0 8 . 5

T o t a l 6 , 8 2 3 . 6 1 0 0 . 0 4 , 8 4 3 . 3 1 0 0 . 0 3 , 5 5 0 . 7 1 0 0 . 0

Funding-average basis

www.kookmincard.co.kr26

Fund all oc a ti on

In allocation of funds, credit card assets rose most prominently in 2000, increasing W2,590.1 billion over the year. This figure accounted

for 65.9% of total funds operated, up 26.5% points over 1999. Card loans, which increased W141.7 billion, accounted for 14.9% of the

total, down 3.2% points from the year before. Investment assets rose W82.7 billion, or 0.8% points in proportion to total funds operated,

due mainly to undertaking notes related to ABS issuance.

Meanwhile, installment financing and corporate financing decreased W111.4 billion and 141.2 billion, respectively. Accordingly, the ratio

of the two categories to the total decreased from 4.2% and 7.6% in 1999, respectively, to 1.4% and 3.4% in 2000.

Net interest sprea d

Operating rate, which indicates the profit rate of funds in operation, averaged 21.58% in 2000, up 1.61% points from 1999. Funding cost,

on the other hand, decreased 2.01% points to 9.09%. As a result, net interest spread came to 12.49% in 2000, an improvement of 3.62%

points compared with the year before.

As s et s

As of the end of 2000, total assets amounted to W8,181.5 billion, W3,956.6 billion more than the year before. In terms of composition,

card assets came to W7,080.3 billion, constituting 86.5% of total assets. This figure represents a 6.1% point increase over the year.

Current assets and funding assets, on the other hand, decreased W107.5 billion and W80.2 billion, respectively, to W170.5 billion and

W219.2 billion. The decrease of current assets stemmed from securities holdings which fell from W205.3 billion to W4.4 billion. Funding

assets dropped as installment and factoring financing shrank. Investment securities amounted to W420.1 billion, up W14.8 billion from

the year before. The increase of investment securities is mainly related to ABS.

December 31, 2000 and 1999

Management Discussion & Analysis

(In billion won, %)

2000 1999 1998

Amount Ratio Amount Ratio Amount Ratio

Cash and deposits 1 6 . 2 0 . 2 7 3 3 . 3 1 5 . 2 2 9 4 . 5 8 . 3

Credit card assets 4 , 4 9 8 . 4 6 5 . 9 1 , 9 0 8 . 3 3 9 . 4 1 , 9 0 7 . 8 5 3 . 7

Card loans 1 , 0 1 9 . 7 1 4 . 9 8 7 8 . 0 1 8 . 1 8 0 6 . 2 2 2 . 7

Installment financing 9 2 . 5 1 . 4 2 0 3 . 9 4 . 2 5 0 . 7 1 . 4

Corporate financing 2 2 8 . 4 3 . 4 3 6 9 . 6 7 . 6 3 7 . 8 1 . 1

Investment assets 1 4 5 . 9 2 . 1 6 3 . 2 1 . 3 8 9 . 6 2 . 5

Current assets 1 9 7 . 1 2 . 9 1 9 9 . 5 4 . 1 1 2 9 . 4 3 . 6

Operating expenses 3 5 9 . 5 5 . 3 3 8 4 . 9 8 . 0 2 2 1 . 8 6 . 3

O t h e r 2 6 5 . 9 3 . 9 1 0 2 . 6 2 . 1 1 2 . 9 0 . 4

T o t a l 6 , 8 2 3 . 6 1 0 0 . 0 4 , 8 4 3 . 3 1 0 0 . 0 3 , 5 5 0 . 7 1 0 0 . 0

Operating rate 2 1 . 5 8 1 9 . 9 7 2 3 . 2 0

Funding cost 9 . 0 9 1 1 . 1 0 1 4 . 0 1

Net interest spread 1 2 . 4 9 8 . 8 7 9 . 1 9

(%)

2000 1999 1998

Funds allocation

Net interest spread

27Kookmincard Annual Report 2 0 0 0

Credit card asset s

Of total card assets as of the end of 2000, cash advances accounted for 45.4% at W3,211.1 billion, up 7.7% points from the year before.

Card loans, which increased by W133.8 billion over the year, accounted for 13.2%, 10.3% points less than the previous year. Card loans

decreased in proportion for the two consecutive years. Installment purchase assets, in contrast, rose both in proportion and in amount,

increasing 2.1% points to 25.9% and W1,027.5 billion to W1,835.6 billion, respectively. Lump sum purchase assets also rose, up 0.5%

points to 15.5% and W591.6 billion to W1,100.7 billion.

As s et qu a l i ty and loan loss provi s i on

Total credit exposure as of the end of 2000 stood at W7,477.2 billion, W3,555.4 billion more than the year before. Despite this increase,

Non-performing loans decreased W67.7 billion to W228.7billion. Accordingly, the ratio of non-performing loans to total credit was tallied

at 3.06%, which represents 4.50% points and 12.41% points decreases from 1999 and 1998, respectively.

To break non-performing loans into the credit card and credit loan sectors non-performing loans in the credit card sector amounted to

W39.6 billion as of the end of 2000, W14.9 billion and W61.1 billion less than 1999 and 1998, respectively. Accordingly, the NPL ratio in

this sector dropped to 0.64% at 2000-end, 1.40% points and 4.98% points lower than 1999 and 1998, respectively. The NPL ratio in the

card loan sector, also decreased, compared with the two previous years, though higher than that of the credit card sector. The ratio stood at

3.36% at the end of 2000, 3.15 points and 3.07% points less than 1999 and 1998, respectively.

December 31, 2000 and 1999

Management Discussion & Analysis

(In billion won, %)

2000 1999

Amount Ratio Amount Ratio

Current assets 1 7 0 . 5 2 . 1 2 7 8 . 0 6 . 6

Credit Card assets 7 , 0 8 0 . 3 8 6 . 5 3 , 3 9 8 . 8 8 0 . 4

Financing assets 2 1 9 . 2 2 . 7 2 9 9 . 4 7 . 1

Investment securities 4 2 0 . 1 5 . 1 1 4 . 8 0 . 4

Other assets 2 9 1 . 4 3 . 6 2 3 3 . 9 5 . 5

Total assets 8 , 1 8 1 . 5 1 0 0 . 0 4 , 2 2 4 . 9 1 0 0 . 0

(In billion won, %)

2000 1999 1998

Amount Ratio Amount Ratio Amount Ratio

Cash advances 3 , 2 1 1 . 1 4 5 . 4 1 , 2 8 2 . 5 3 7 . 7 6 8 6 . 3 2 6 . 6

Card loans 9 3 2 . 0 1 3 . 2 7 9 8 . 2 2 3 . 5 8 9 0 . 8 3 4 . 6

Installment purchases 1 , 8 3 5 . 6 2 5 . 9 8 0 8 . 1 2 3 . 8 6 4 5 . 6 2 5 . 1

Lump sum purchases 1 , 1 0 0 . 7 1 5 . 5 5 0 9 . 1 1 5 . 0 3 4 9 . 1 1 3 . 6

Other card assets 0 . 9 0 . 0 0 . 9 0 . 0 3 . 2 0 . 1

T o t a l 7 , 0 8 0 . 3 1 0 0 . 0 3 , 3 9 8 . 8 1 0 0 . 0 2 , 5 7 5 . 0 1 0 0 . 0

Asset composition

Card asset composition

* after loan loss provisions

www.kookmincard.co.kr28

These decreases in NPLs led to a significant drop in loan loss provisions, based on the FSS guidelines. Despite this decrease in loan loss

provisions, however, NPL coverage ratio, which is a ratio of loan loss provisions to NPLs, remained not much changed compared with the

two previous years. 2000-end ratio came to 71.71%, compared to 72.17% in 1999 and 69.51% in 1998.

Capital Adequ a c y

The Company's net worth as of the end of 2000 stood at W833.5 billion, which represents a W466.2 billion increase over the previous year.

The increase can be attributed to the initial public offering and the net income. Total assets, compared with the year before, rose W4,146.3

billion, or 102.9%, to W8,177.5 billion. Accordingly, capital adequacy ratio rose 1.08% points over 1999 and 4.40% points over 1998 to

10.19% at the end of 2000. This ratio comfortably exceeds the FSS-recommended 7%. The FSS’s Capital Adequency guideline was

adopted from fiscal year 1999.

December 31, 2000 and 1999

Management Discussion & Analysis

Net worth 8 3 3 . 5 3 6 7 . 3 2 0 6 . 3

Total assets 8 , 1 7 7 . 5 4 , 0 3 1 . 2 3 , 5 6 3 . 5

Capital adequacy ratio 1 0 . 1 9 9 . 1 1 5 . 7 9

(in billion won, %)

2000 1999 1998

Total credit (A) 7 , 4 7 7 . 2 3 , 9 2 1 . 8 3 , 6 7 6 . 9

N o r m a l 7 , 2 4 4 . 9 3 , 5 8 0 . 8 2 , 8 8 8 . 3

p r e c a u t i o n a r y 3 . 6 4 4 . 6 2 2 9 . 8

s u b s t a n d a r d 1 0 7 . 4 9 8 . 8 1 9 4 . 6

d o u b t f u l 3 8 . 9 7 5 . 8 1 1 1 . 0

estimated loss 8 2 . 4 1 2 1 . 8 2 5 3 . 2

NPL (B) 2 2 8 . 7 2 9 6 . 4 5 5 8 . 8

NPL Ratio (C) = (B)/(A) 3 . 0 6 7 . 5 6 1 5 . 2 0

Loan loss reserve (D) 1 6 4 . 0 2 1 3 . 9 3 8 8 . 4

NPL Coverage ratio (D)/(B) 7 1 . 7 1 7 2 . 1 7 6 9 . 5 1

Loan loss reserve ratio (D)/(A) 2 . 1 9 5 . 4 4 1 0 . 5 6

W r i t e - o f f s 2 0 3 . 7 3 1 2 . 0 8 0 . 1

(in billion won, %)

2000 1999 1998

Non-performing loans and loan loss provisions

Capital adequacy ratio

29Kookmincard Annual Report 2 0 0 0

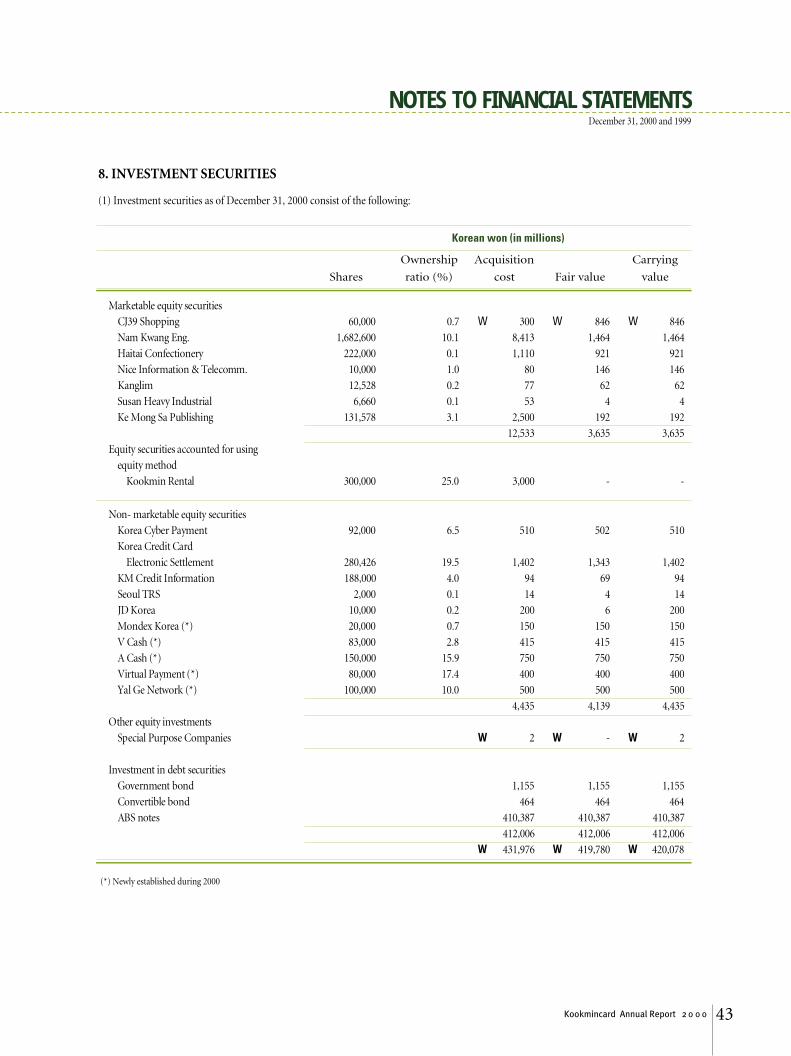

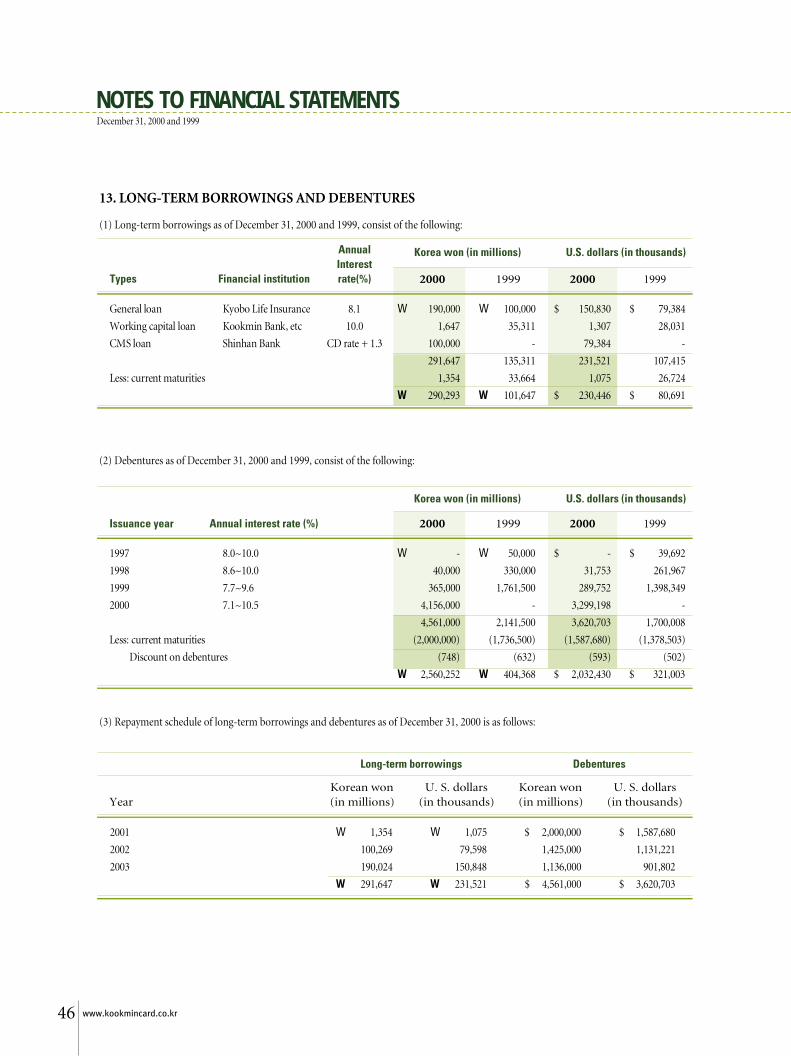

Korean won (in millions) U. S. dollars (in thousands)

ASSETS 2000 1999 2000 1999

December 31, 2000 and 1999

CURRENT ASSETS:

Cash and cash equivalents (Notes 3 and 17) W 4 , 8 8 1 W 2 , 8 7 4 $ 3 , 8 7 5 $ 2 , 2 8 1

Short-term financial instruments (Notes 3 and 17) 7 , 3 9 7 1 2 , 5 7 1 5 , 8 7 2 9 , 9 8 0

Marketable securities (Notes 4 and 17) 4 , 4 2 2 2 0 5 , 3 2 8 3 , 5 1 0 1 6 2 , 9 9 7

Accounts receivable-other, net of allowance for

doubtful accounts of W6,331 million in 2000

and W9,075 million in 1999 (Notes 7 and 17) 2 7 , 6 4 6 1 8 , 2 3 2 2 1 , 9 4 7 1 4 , 4 7 3

Accrued income 9 6 , 8 2 5 2 8 , 0 0 8 7 6 , 8 6 3 2 2 , 2 3 4

Other current assets 2 9 , 3 2 7 1 1 , 0 2 9 2 3 , 2 8 1 8 , 7 5 6

1 7 0 , 4 9 8 2 7 8 , 0 4 2 1 3 5 , 3 4 8 2 2 0 , 7 2 1

CREDIT CARD ASSETS (Notes 5 and 7):

Credit card receivable 2 , 9 6 4 , 8 0 3 1 , 3 5 1 , 5 6 2 2 , 3 5 3 , 5 7 9 1 , 0 7 2 , 9 2 4

Cash in advance 3 , 2 4 9 , 5 4 0 1 , 3 1 4 , 9 9 3 2 , 5 7 9 , 6 1 4 1 , 0 4 3 , 8 9 3

Card loan 9 6 8 , 3 0 0 8 5 6 , 4 4 6 7 6 8 , 6 7 5 6 7 9 , 8 8 1

Less: Allowance for doubtful accounts ( 1 0 2 , 3 8 9 ) ( 1 2 4 , 1 6 0 ) ( 8 1 , 2 8 1 ) ( 9 8 , 5 6 3 )

7 , 0 8 0 , 2 5 4 3 , 3 9 8 , 8 4 1 5 , 6 2 0 , 5 8 7 2 , 6 9 8 , 1 3 5

FINANCING ASSETS (Notes 6 and 7):

Installment financing assets 7 6 , 6 9 7 1 1 9 , 5 2 7 6 0 , 8 8 5 9 4 , 8 8 5

F a c t o r i n g s 9 8 , 0 8 1 1 5 0 , 6 7 4 7 7 , 8 6 1 1 1 9 , 6 1 1

Property on leases, net of accumulated

depreciation of W7,774 million in 2000 and

W17,637 million in 1999 4 , 6 7 7 8 , 9 8 4 3 , 7 1 3 7 , 1 3 2

Accounts receivable-rental 4 5 9 3 , 5 4 7 3 6 4 2 , 8 1 6

Advance to customers 2 4 6 2 4 6 1 9 5 1 9 5

Other financing assets 9 2 , 1 6 1 9 2 , 4 8 2 7 3 , 1 6 1 7 3 , 4 1 6

Less : Allowance for doubtful accounts ( 5 3 , 0 7 9 ) ( 7 6 , 1 1 0 ) ( 4 2 , 1 3 6 ) ( 6 0 , 4 1 9 )

2 1 9 , 2 4 2 2 9 9 , 3 5 0 1 7 4 , 0 4 3 2 3 7 , 6 3 6

NON-CURRENT ASSETS:

Long-term financial instruments (Notes 3 and 17) 9 0 , 6 6 4 4 8 , 2 3 8 7 1 , 9 7 2 3 8 , 2 9 3

Investment securities (Note 8) 4 2 0 , 0 7 8 1 4 , 7 8 0 3 3 3 , 4 7 5 1 1 , 7 3 3

Guarantee deposits (Note 17) 4 4 , 9 9 5 3 2 , 9 7 8 3 5 , 7 1 9 2 6 , 1 7 9

Other investment assets 2 6 0 1 2 , 5 1 3 2 0 7 9 , 9 3 3

Deferred income tax assets (Note 16) 2 , 3 9 5 4 , 1 5 8 1 , 9 0 1 3 , 3 0 1

Property and equipment, net of accumulated

depreciation of W67,495 million in 2000 and

W55,423 million in 1999 (Notes 9 and 10) 1 5 3 , 0 4 2 1 3 5 , 9 7 3 1 2 1 , 4 9 1 1 0 7 , 9 4 1

Intangible assets 4 8 1 5 3 8 1 2

7 1 1 , 4 8 2 2 4 8 , 6 5 5 5 6 4 , 8 0 3 1 9 7 , 3 9 2

W 8 , 1 8 1 , 4 7 6 W 4 , 2 2 4 , 8 8 8 $ 6 , 4 9 4 , 7 8 1 $ 3 , 3 5 3 , 8 8 4

BALANCE SHEETS

www.kookmincard.co.kr30

CURRENT LIABILITIES:

Call money (Note 12) W 3 6 5 , 2 0 0 W 1 9 0 , 0 0 0 $ 2 8 9 , 9 1 0 $ 1 5 0 , 8 2 8

Short-term borrowings (Notes 12 and 17) 1 , 3 2 4 , 5 0 0 6 0 4 , 2 6 0 1 , 0 5 1 , 4 4 1 4 7 9 , 6 8 6

Credit card (Notes 11 and 17) 3 5 3 , 4 6 7 5 7 8 , 7 7 7 2 8 0 , 5 9 6 4 5 9 , 4 5 6

Accounts payable-other 1 5 , 1 9 3 1 3 , 7 0 8 1 2 , 0 6 1 1 0 , 8 8 2

Advance receipts 1 2 , 6 0 3 - 1 0 , 0 0 5 -

Accrued expense 2 3 8 , 2 2 4 1 2 9 , 6 8 2 1 8 9 , 1 1 2 1 0 2 , 9 4 7

Income taxes payable 1 1 6 , 5 0 9 3 5 , 8 9 6 9 2 , 4 8 9 2 8 , 4 9 6

Dividends payable 5 4 , 5 2 2 3 , 1 3 6 4 3 , 2 8 2 2 , 4 8 9

Current maturities of long-term

debt and debentures, less discount on debentures

(Note 13) 2 , 0 0 1 , 1 2 1 1 , 7 7 0 , 1 6 4 1 , 5 8 8 , 5 6 9 1 , 4 0 5 , 2 2 7

Other current liabilities 3 4 , 1 7 1 2 9 , 8 3 8 2 7 , 1 2 6 2 3 , 6 8 7

4 , 5 1 5 , 5 1 0 3 , 3 5 5 , 4 6 1 3 , 5 8 4 , 5 9 1 2 , 6 6 3 , 6 9 8

LONG-TERM LIABILITIES:

Debentures, less current maturities and discount on

debentures (Note 13) 2 , 5 6 0 , 2 5 2 4 0 4 , 3 6 8 2 , 0 3 2 , 4 3 0 3 2 1 , 0 0 3

Long-term borrowings, less current maturities

(Notes 13 and 17) 2 9 0 , 2 9 3 1 0 1 , 6 4 7 2 3 0 , 4 4 6 8 0 , 6 9 1

Accrued severance indemnities (Note 2) 1 8 , 8 1 9 1 5 , 6 6 5 1 4 , 9 3 9 1 2 , 4 3 6

National Pension payment for employees (Note 2) ( 1 , 3 8 6 ) ( 1 , 7 8 5 ) ( 1 , 1 0 0 ) ( 1 , 4 1 7 )

Individual severance insurance deposits (Note 2) ( 1 2 , 1 1 8 ) - ( 9 , 6 2 0 ) -

Long-term accounts payable-other 7 , 5 7 8 3 , 6 9 3 6 , 0 1 6 2 , 9 3 2

2 , 8 6 3 , 4 3 8 5 2 3 , 5 8 8 2 , 2 7 3 , 1 1 1 4 1 5 , 6 4 5

SHAREHOLDERS’ EQUITY (Note 14):

Common stock 3 6 6 , 0 0 0 2 9 2 , 3 9 8 2 9 0 , 5 4 5 2 3 2 , 1 1 7

Capital surplus 1 4 6 , 5 9 1 - 1 1 6 , 3 7 0 -

Retained earnings

Legal reserve 6 , 9 4 9 1 , 4 4 9 5 , 5 1 6 1 , 1 5 0

Voluntary reserve 2 9 4 , 2 1 0 5 0 , 0 0 0 2 3 3 , 5 5 6 3 9 , 6 9 2

Unappropriated retained earnings (net income of

W300,541 million in 2000 and

W42,891 million in 1999) - 3 , 6 9 2 - 2 , 9 3 1

Capital adjustments (Note 8) ( 1 1 , 2 2 2 ) ( 1 , 7 0 0 ) ( 8 , 9 0 8 ) ( 1 , 3 4 9 )

8 0 2 , 5 2 8 3 4 5 , 8 3 9 6 3 7 , 0 7 9 2 7 4 , 5 4 1

W 8 , 1 8 1 , 4 7 6 W 4 , 2 2 4 , 8 8 8 $ 6 , 4 9 4 , 7 8 1 $ 3 , 3 5 3 , 8 8 4

Korean won (in millions) U. S. dollars (in thousands)

LIABILITIES AND SHAREHOLDERS’ EQUITY 2000 1999 2000 1999

The accompanying notes are an integral part of these financial statements.

December 31, 2000 and 1999

BALANCE SHEETS

31Kookmincard Annual Report 2 0 0 0

Korean won U. S. dollars

(In millions except per share (In thousands except peramount) share amount)

2000 1999 2000 1999

for the year ended December 31, 2000 and 1999

OPERATING REVENUE:

Fees and commissions (Notes 5, 6 and 17) W 1 , 2 4 5 , 3 2 2 W 6 0 6 , 1 6 3 $ 9 8 8 , 5 8 6 $ 4 8 1 , 1 9 7

Interest income (Notes 5, 6 and 17) 2 0 7 , 5 3 2 2 2 8 , 5 5 1 1 6 4 , 7 4 7 1 8 1 , 4 3 2

Gain on disposal of marketable securities 6 8 3 4 4 , 3 5 8 5 4 2 3 5 , 2 1 3

Gain on valuation of marketable securities - 8 , 7 6 4 - 6 , 9 5 7

Rental fee 5 , 7 9 8 7 , 8 3 1 4 , 6 0 3 6 , 2 1 7

Gain on disposal of property on leases - 3 7 0 - 2 9 4

O t h e r 1 , 2 6 5 6 8 4 1 , 0 0 4 5 4 3

1 , 4 6 0 , 6 0 0 8 9 6 , 7 2 1 1 , 1 5 9 , 4 8 2 7 1 1 , 8 5 3

OPERATING EXPENSES:

Interest expense (Note 17) 4 7 7 , 5 9 4 3 7 3 , 0 4 6 3 7 9 , 1 3 3 2 9 6 , 1 3 8

Fees and commissions (Note 17) 2 5 6 , 5 0 8 1 4 3 , 9 0 3 2 0 3 , 6 2 7 1 1 4 , 2 3 6

Loss on disposal of marketable securities 6 , 2 5 4 6 7 4 4 , 9 6 5 5 3 5

Loss on valuation of marketable securities 3 0 1 1 7 , 5 0 0 2 3 9 1 3 , 8 9 2

Depreciation of property on leases 2 , 4 1 9 6 , 1 7 9 1 , 9 2 0 4 , 9 0 5

Loss on disposal of property on leases 1 , 4 7 7 3 7 3 1 , 1 7 3 2 9 6

O t h e r 2 2 , 3 7 3 1 2 , 3 9 2 1 7 , 7 6 0 9 , 8 3 8

7 6 6 , 9 2 6 5 5 4 , 0 6 7 6 0 8 , 8 1 7 4 3 9 , 8 4 0

GENERAL AND ADMINISTRATIVE EXPENSES 2 5 5 , 6 9 1 2 5 7 , 9 0 3 2 0 2 , 9 7 7 2 0 4 , 7 3 4

OPERATING INCOME 4 3 7 , 9 8 3 8 4 , 7 5 1 3 4 7 , 6 8 8 6 7 , 2 7 9

NON-OPERATING INCOME (EXPENSES):

Gain on disposal of investment assets, net 4 , 0 9 1 6 , 9 6 2 3 , 2 4 7 5 , 5 2 7

Loss on disposal of property and equipment, net ( 4 ) ( 1 , 8 4 1 ) ( 3 ) ( 1 , 4 6 1 )

D o n a t i o n ( 2 , 7 9 3 ) ( 2 7 8 ) ( 2 , 2 1 7 ) ( 2 2 0 )

Loss on valuation of equity method - ( 3 , 0 0 0 ) - ( 2 , 3 8 1 )

Miscellaneous, net ( 3 , 5 8 1 ) ( 6 4 7 ) ( 2 , 8 4 2 ) ( 5 1 6 )

( 2 , 2 8 7 ) 1 , 1 9 6 ( 1 , 8 1 5 ) 9 4 9

ORDINARY INCOME 4 3 5 , 6 9 6 8 5 , 9 4 7 3 4 5 , 8 7 3 6 8 , 2 2 8

EXTRAORDINARY ITEMS - - - -

INCOME BEFORE INCOME TAX EXPENSES 4 3 5 , 6 9 6 8 5 , 9 4 7 3 4 5 , 8 7 3 6 8 , 2 2 8

INCOME TAX EXPENSES (Note 16) 1 3 5 , 1 5 5 4 3 , 0 5 6 1 0 7 , 2 9 2 3 4 , 1 7 9

NET INCOME W 3 0 0 , 5 4 1 W 4 2 , 8 9 1 $ 2 3 8 , 5 8 1 $ 3 4 , 0 4 9

ORDINAY INCOME PER SHARE (Note 2) W 4 , 5 7 7 W 1 , 5 7 5 $ 3 . 6 3 $ 1 . 2 5

NET INCOME PER SHARE (Note 2) W 4 , 5 7 7 W 1 , 5 7 5 $ 3 . 6 3 $ 1 . 2 5

The accompanying notes are an integral part of these financial statements.

STATEMENTS OF INCOME

www.kookmincard.co.kr32

UNAPPROPRIATED RETAINED EARNINGS:

Unappropriated retained earnings carried over

from prior years W 3 , 6 9 2 W - $ 2 , 9 3 1 $ -

Cumulated effect from accounting changes - 1 4 , 4 1 9 - 1 1 , 4 4 6

Net income 3 0 0 , 5 4 1 4 2 , 8 9 1 2 3 8 , 5 8 1 3 4 , 0 4 9

3 0 4 , 2 3 3 5 7 , 3 1 0 2 4 1 , 5 1 2 4 5 , 4 9 5

A P P R O P R I A T I O N S :

Amortization of stock issuance cost - 8 2 - 6 5

Legal reserve 5 , 5 0 0 4 0 0 4 , 3 6 6 3 1 8

Dividends (Note 15) 5 4 , 5 2 2 3 , 1 3 6 4 3 , 2 8 2 2 , 4 8 9

Voluntary reserve 2 4 4 , 2 1 1 5 0 , 0 0 0 1 9 3 , 8 6 4 3 9 , 6 9 2

3 0 4 , 2 3 3 5 3 , 6 1 8 2 4 1 , 5 1 2 4 2 , 5 6 4

UNAPPROPRIATED RETAINED EARNINGS TO

BE CARRIED FORWARD TO SUBSEQUENT YEAR W - W 3 , 6 9 2 $ - $ 2 , 9 3 1

Korean won (in millions) U. S. dollars (in thousands)

2000 1999 2000 1999

The accompanying notes are an integral part of these financial statements.

for the year ended December 31, 2000 and 1999

STATEMENTS OF APPROPRIATIONS OF RETAINED EARNINGS

33Kookmincard Annual Report 2 0 0 0

Korean won (in millions) U. S. dollars (in thousands)

2000 1999 2000 1999

for the year ended December 31, 2000 and 1999

I. CASH FLOWS FROM OPERATING ACTIVITIES:

Net income W 3 0 0 , 5 4 1 W 4 2 , 8 9 1 $ 2 3 8 , 5 8 1 $ 3 4 , 0 4 9

Adjustments to reconcile net income to net cash

used in operating activities:

Provision for severance indemnities 7 , 7 8 1 4 , 6 4 1 6 , 1 7 7 3 , 6 8 4

Loss on disposal of marketable securities 6 , 2 5 4 6 7 4 4 , 9 6 5 5 3 5

Loss on valuation of marketable securities 3 0 1 1 7 , 5 0 0 2 3 9 1 3 , 8 9 2

Depreciation of property and equipment 1 5 , 3 3 5 1 6 , 6 0 1 1 2 , 1 7 4 1 3 , 1 7 9

Depreciation of property on leases 2 , 4 1 9 6 , 1 7 9 1 , 9 2 0 4 , 9 0 5

Loss on disposal of property and equipment 1 6 1 , 8 8 5 1 2 1 , 4 9 6

Loss on disposal of property on leases 1 , 4 7 7 3 7 3 1 , 1 7 3 2 9 6

Loss on disposal of investment assets 1 , 0 2 5 6 4 8 1 4 5 1

Amortization of intangible assets 1 6 5 0 , 6 6 5 1 3 4 0 , 2 2 0

Amortization of discount on debenture 1 , 2 3 7 2 , 3 5 6 9 8 2 1 , 8 7 1

Loss on valuation of equity method - 3 , 0 0 0 - 2 , 3 8 1

Gain on disposal of marketable securities ( 6 8 3 ) ( 4 4 , 3 5 8 ) ( 5 4 2 ) ( 3 5 , 2 1 3 )

Gain on valuation of marketable securities - ( 8 , 7 6 4 ) - ( 6 , 9 5 7 )

Gain on disposal of property on leases - ( 3 7 0 ) - ( 2 9 4 )

Gain on disposal of investment assets ( 5 , 1 1 6 ) ( 7 , 0 2 6 ) ( 4 , 0 6 1 ) ( 5 , 5 7 8 )

Gain on disposal of property and equipment ( 1 2 ) ( 4 4 ) ( 9 ) ( 3 5 )

Amortization of present value discount - ( 2 ) - ( 2 )

(Increase) decrease in accounts receivable-other ( 9 , 4 1 5 ) 1 1 , 5 9 0 ( 7 , 4 7 4 ) 9 , 2 0 1

(Increase) decrease in accrued income ( 6 8 , 8 1 7 ) 9 , 1 3 2 ( 5 4 , 6 2 9 ) 7 , 2 4 9

(Increase) decrease in other current assets ( 1 8 , 2 9 4 ) 2 2 , 8 5 1 ( 1 4 , 5 2 5 ) 1 8 , 1 3 9

(Increase) in credit card receivable ( 3 , 5 4 7 , 6 2 3 ) ( 9 1 8 , 4 6 3 ) ( 2 , 8 1 6 , 2 4 4 ) ( 7 2 9 , 1 1 2 )

(Increase) decrease in card loan ( 1 3 3 , 7 9 0 ) 9 2 , 5 8 8 ( 1 0 6 , 2 0 8 ) 7 3 , 5 0 0

Decrease in installment financing assets 3 6 , 0 6 4 1 2 5 , 2 4 9 2 8 , 6 2 9 9 9 , 4 2 8

Decrease in factorings 3 2 , 7 9 9 1 5 8 , 9 6 2 2 6 , 0 3 7 1 2 6 , 1 9 0

Decrease (increase) in property on leases 3 5 9 ( 4 , 3 4 9 ) 2 8 5 ( 3 , 4 5 2 )

Decrease in other financing assets 6 , 9 9 0 1 0 0 , 7 4 1 5 , 5 4 9 7 9 , 9 7 2

Decrease in deferred income tax assets 1 , 7 6 3 - 1 , 3 9 9 -

Increase in accounts payable-other 1 , 4 8 5 1 5 , 4 4 6 1 , 1 7 9 1 2 , 2 6 2

Increase in advance receipts 1 2 , 6 0 3 - 1 0 , 0 0 5 -

Increase (decrease) in accrued expense 1 0 8 , 5 4 1 ( 1 8 4 , 7 2 8 ) 8 6 , 1 6 5 ( 1 4 6 , 6 4 5 )

Increase in income taxes payable 8 0 , 6 1 2 4 3 , 0 3 8 6 3 , 9 9 4 3 4 , 1 6 5

Increase (decrease) in other current liabilities 4 , 3 3 4 ( 3 7 7 ) 3 , 4 3 9 ( 2 9 8 )

Increase in long-term accounts payable-other 3 , 8 8 5 3 , 4 7 4 3 , 0 8 4 2 , 7 5 8

Payment of severance benefits ( 4 , 6 2 8 ) ( 4 , 8 8 3 ) ( 3 , 6 7 4 ) ( 3 , 8 7 6 )

Decrease in National Pension payment for employees 3 9 9 1 0 0 3 1 7 7 9

Increase in individual severance insurance deposits ( 3 8 7 ) ( 2 , 3 0 0 ) ( 3 0 7 ) ( 1 , 8 2 6 )

Net cash used in operating activities ( 3 , 1 6 2 , 5 2 9 ) ( 4 4 5 , 6 6 4 ) ( 2 , 5 1 0 , 5 4 1 ) ( 3 5 3 , 7 8 6 )

STATEMENTS OF CASH FLOWS

www.kookmincard.co.kr34

II. CASH FLOWS FROM INVESTING ACTIVITIES:

Collection (purchase) of short-term

financial instruments W 5 , 1 7 4 W ( 9 , 4 9 2 ) $ 4 , 1 0 7 $ ( 7 , 5 3 5 )

Purchase of long-term financial instruments ( 4 2 , 4 2 5 ) ( 4 8 , 0 3 8 ) ( 3 3 , 6 7 9 ) ( 3 8 , 1 3 4 )

Proceeds from sales of marketable securities 1 9 5 , 0 3 3 3 1 9 , 5 5 6 1 5 4 , 8 2 5 2 5 3 , 6 7 6

Proceeds from sales of investment securities 6 , 7 8 2 6 4 7 5 , 3 8 4 5 1 4

Acquisition of investment securities ( 4 1 7 , 1 6 6 ) ( 4 , 1 1 6 ) ( 3 3 1 , 1 6 3 ) ( 3 , 2 6 8 )

Net (increase) decrease of guarantee deposits ( 1 2 , 6 8 0 ) 3 , 4 8 0 ( 1 0 , 0 6 6 ) 2 , 7 6 3

Net decrease of other investment assets 5 9 1 5 5 3 4 7 0 4 3 8

Proceeds from disposal of property and equipment 9 6 4 , 9 5 7 7 6 3 , 9 3 7

Acquisition of property and equipment ( 3 2 , 5 0 4 ) ( 9 , 8 6 4 ) ( 2 5 , 8 0 3 ) ( 7 , 8 3 0 )

Additions to intangible assets ( 4 8 ) ( 1 1 ) ( 3 8 ) ( 9 )

( 2 9 7 , 1 4 7 ) 2 5 7 , 6 7 4 ( 2 3 5 , 8 8 7 ) 2 0 4 , 5 5 2

III. CASH FLOWS FROM FINANCING ACTIVITIES:

Proceeds from call money 1 7 5 , 2 0 0 7 8 , 0 0 0 1 3 9 , 0 8 1 6 1 , 9 1 9

Proceeds from short-term borrowings 7 2 0 , 2 4 0 2 5 7 , 4 6 0 5 7 1 , 7 5 5 2 0 4 , 3 8 2

Repayment of credit card ( 2 2 5 , 3 1 0 ) ( 9 1 , 9 5 2 ) ( 1 7 8 , 8 6 0 ) ( 7 2 , 9 9 5 )

Proceeds from long-term borrowings 1 9 0 , 0 0 0 1 0 0 , 0 0 0 1 5 0 , 8 3 0 7 9 , 3 8 4

Repayment of current maturities of long-term debt ( 1 , 7 7 0 , 1 6 4 ) ( 1 , 9 8 0 , 7 0 5 ) ( 1 , 4 0 5 , 2 2 7 ) ( 1 , 5 7 2 , 3 6 2 )

Proceeds from debenture issuance 4 , 1 5 4 , 4 1 4 1 , 7 6 0 , 8 6 9 3 , 2 9 7 , 9 3 9 1 , 3 9 7 , 8 4 8

Proceeds from stock issuance 2 2 0 , 4 3 9 4 9 , 7 5 4 1 7 4 , 9 9 3 3 9 , 4 9 6

Acquisition of treasury stock - ( 1 , 8 0 9 ) - ( 1 , 4 3 6 )

D i v i d e n d s ( 3 , 1 3 6 ) - ( 2 , 4 8 9 ) -

3 , 4 6 1 , 6 8 3 1 7 1 , 6 1 7 2 , 7 4 8 , 0 2 2 1 3 6 , 2 3 6

IV. NET (DECREASE) IN CASH (I+II+III) 2 , 0 0 7 ( 1 6 , 3 7 3 ) 1 , 5 9 4 ( 1 2 , 9 9 8 )

V. CASH, BEGINNING OF YEAR 2 , 8 7 4 1 9 , 2 4 7 2 , 2 8 1 1 5 , 2 7 9

VI. CASH, END OF YEAR W 4 , 8 8 1 W 2 , 8 7 4 $ 3 , 8 7 5 $ 2 , 2 8 1

Korean won (in millions) U. S. dollars (in thousands)

2000 1999 2000 1999

The accompanying notes are an integral part of these financial statements.

for the year ended December 31, 2000 and 1999

STATEMENTS OF CASH FLOWS

1. GENERAL

KOOKMIN CREDIT CARD CO., LTD. (the “Company”) was incorporated in September 25, 1987 and subsequently acquired credit

card business of KOOKMIN BANK CO., LTD. (“KOOKMIN BANK”). The Company merged with KOOKMIN FINANCE CO.,

LTD. and KLB CREDIT CARD CO., LTD. in August 22, 1998 and December 30, 1998, respectively. With a total number of 51

branch offices nation-wide, the Company is principally engaged in credit card services, factoring, installment financing and leasing.

As of December 31, 2000, the Company holds 8.17 million of total credit card holders and 1.23 million of franchise account. The

Company was registered on the Korea Association Securities Dealers’ Automated Quotation (KOSDAQ) on July 4, 2000.

As of December 31, 2000, the Company’s common stock is W366,000 million($ 290,545 thousand) and 74.27 percent of shares is

owned by KOOKMIN BANK.

Beginning in 1997, Korea and other countries in the Asia Pacific region experienced a severe contraction in substantially all aspects of

their economies. This situation is commonly referred to as the 1997 Asian Financial Crisis. In response to this situation, the Korean

government and the private sector began implementing structural reforms to historical business practices. Through early 1999, it was

widely accepted that the economic situation had stabilized, but not fully recovered from the 1997 crisis.

The Korean economy is currently experiencing additional difficulties, particularly in the areas of restructuring private enterprises and

reforming the banking industry. The Korean government continues to apply pressure to Korean companies to restructure into more

efficient and profitable firms. The banking industry is currently undergoing forced consolidations and significant uncertainty exists

with regard to the availability of short-term financing during the coming year. The Company may be either directly or indirectly

affected by the situation described above.

The accompanying financial statements reflect management’s current assessment of the impact to date of the economic situation on

the financial position of the Company. Actual results may differ materially from management’s current assessment.

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Basis of Financial Statement Presentation

The Company maintains its official accounting records in Korean won and prepares its statutory financial statements in the Korean

language (Hangul) in conformity with the accounting principles generally accepted in the Republic of Korea. Certain accounting

principles applied by the Company that conform with financial accounting standards and accounting principles in the Republic of

Korea may not conform with accounting principles generally accepted in other countries. Accordingly, these financial statements are

not intended for use by those who are not informed about Korean accounting principles and practices.

The accompanying financial statements have been condensed, restructured and translated into English (with certain expanded

descriptions) from the statutory Korean language financial statements. Some supplementary information included in the statutory

Korean language financial statements, but not required for a fair presentation of the Company’s financial position, results of

operations or cash flows, is not presented in the accompanying financial statements

The US dollar amounts presented in these financial statements were computed by translating the Korean won into US dollars based

on the Bank of Korea Basic Rate of W1,259.7 to US$1.00 at December 31, 2000, solely for the convenience of the reader. This

convenience translation into US dollars should not be construed as a representation that the Korean won amounts have been, could

have been, or could in the future be, converted at this or any other rate of exchange.

The significant accounting policies followed by the Company in the preparation of its financial statements are summarized below.

December 31, 2000 and 1999

NOTES TO FINANCIAL STATEMENTS

35Kookmincard Annual Report 2 0 0 0

Recognition of Fees and Commissions and Interest Income

The Company recognizes the revenue on an accrual basis, except for fees and commissions and interest income on overdue accounts

more than three months.

Allowance for Doubtful Account

The Company provides an allowance for doubtful account based on the results of loan classification. The loans are classified as of

balance sheet date as ‘normal’, ‘precautionary’, ‘substandard’, ‘doubtful’ and ‘loss’ and an allowance is then calculated, as of the

balance sheet date, on the loan balances using the prescribed percentages of 0.5 percent, 2 percent, 20 percent, 50 percent and 100

percent, respectively.

Valuation of Marketable Securities

Marketable securities are recorded at purchase price plus incidental costs. However, if the fair value of marketable securities differs

from the book value determined by the moving average method, the securities are stated at fair value and the valuation gain or loss is

reflected in current operations.

Valuation of Investment Securities

Investment equity securities (excluding non-listed equity securities and investments accounted for using the equity method) are

stated at fair value with the unrealized gain or loss reported as a capital adjustment within shareholders’ equity. Non-listed equity

securities are stated at cost, determined using the moving average method. However, if the investment is in a company whose

financial condition has deteriorated and, accordingly, whose fair value (marketable security) or net equity value (non-listed security)

has declined and is not expected to recover, the acquisition cost is adjusted to the fair value or net equity value and the difference

between the acquisition cost and revalued amount is charged to current operations.

Investments in equity securities of companies in which the Company is able to exercise significant influence over the operating and

financial policies of the investees are accounted for using the equity method. The change in the Company’s portion of an investee’s

net equity resulting from a change in an investee’s net equity is reflected in the Company’s net income (loss), retained earnings and

capital adjustments, in accordance with the causes of the change which consist of the investees’ net income (loss), changes in retained

earnings and changes in capital surplus and capital adjustments.

Investments in debt securities, excluding held-to-maturity securities, are stated at fair value with the unrealized gain or loss recorded

as a capital adjustment. Debt securities that the Company intends to hold to maturity are stated at cost. However, if the fair value has

declined and is not expected to recover, the acquisition cost is adjusted to the fair value and the difference between the acquisition

cost and revalued amount is charged to current operations. If the fair value of these securities recovers, the Company records the

recovery as a capital adjustment. In the case of held-to-maturity securities, the Company records the recovery in current operations

to a maximum of the original acquisition cost.

When the face value of held-to-maturity debt securities differs from their acquisition cost, the difference is amortized over the term of

the securities, using the effective interest method.

Property on Leases and Property and Equipment

Property and equipment are stated at cost, net of accumulated depreciation. Routine maintenance and repairs are expensed as

incurred. Expenditures that result in the enhancement of the value or extension of the useful life of the facilities involved are treated

as additions to property and equipment.

Depreciation is computed using the declining balance method (except that straight-line method is used for buildings) based on the

estimated useful lives of the assets as follows:

December 31, 2000 and 1999

NOTES TO FINANCIAL STATEMENTS

www.kookmincard.co.kr36

Intangibles

Intangible assets are stated at cost, net of amortization computed using the straight-line method over the economic useful lives of the related

assets from the usable date.

Stock Issuance Costs and Debenture Issuance Cost

New stock issuance costs are deducted from capital surplus in excess of paid-in-capital. However, if no sufficient capital surplus in excess of

paid-in-capital exist, stock issuance costs are recorded to stock discounts which are amortized over a period no more than 3 years in equal

amounts beginning in the year of issuance. The amortization amount is charged to retained earnings through an appropriation. Debenture

issuance cost is added to discounts on debenture which are amortized over maturity using the effective interest method. The amortization

amount is charged to operation as interest expenses.

Accounting for Foreign Currency Transactions and Translation

The Company maintains its accounts in Korean won. Transactions in foreign currencies are recorded in Korean won based on the

prevailing rates of exchange on the transaction date. Monetary accounts with balances denominated in foreign currencies are recorded and

reported in the accompanying financial statements at the exchange rates prevailing at the balance sheet dates. The balances have been

translated using the Bank of Korea Basic Rate, which was W1,259.7 and W1,145.4 to US $1.00 at December 31, 2000 and 1999, and the

translation gains or losses are reflected in current operations

Accrued Severance Indemnities

Employees and directors with more than one year of service are entitled to receive a lump-sum payment upon termination of their service

with the Company, based on their length of service and rate of pay at the time of termination. The severance indemnities which would be

payable assuming all eligible employees were to resign as of December 31, 2000 and 1999 are W18,819 million ($14,939 thousand) and

W15,665 million ($12,436 thousand), respectively. Actual payment of severance indemnities amount to W4,628 million ($3,674 thousand)

in 2000 and W4,883 million ($3,876 thousand) in 1999.

Individual severance insurance deposits, in which the beneficiary is a respective employee, are presented as deduction from accrued

severance benefits and as of December 31, 2000, individual severance insurance deposits, which are actually funded through an individual

severance plan, are W12,118 million ($9,620 thousand).

Before April 1999, the Company and its employees paid 3 percent and 6 percent, respectively, of monthly pay (as defined) to the National

Pension Fund in accordance with the National Pension Law of Korea. The Company paid half of the employees’ 6 percent and is paid back at

the termination of service by netting the receivable against the severance payment. Such receivables are presented as a deduction from

accrued severance indemnities. Since April, 1999, according to a revision in the National Pension Law, the Company and its employees each

pay 4.5 percent of monthly pay to the Fund.

Income Tax Expense

The Company recognizes deferred income tax arising from temporary differences between pre-tax accounting income and taxable income.

December 31, 2000 and 1999

NOTES TO FINANCIAL STATEMENTS

37Kookmincard Annual Report 2 0 0 0

B u i l d i n g s 4 0

V e h i c l e s 5

Other property and equipment 5

Property on leases 5

UsefulLives(Years)

Accordingly, income tax expense consists of the total income tax and surtaxes currently payable and the changes in deferred income tax

assets or liabilities during the period. The deferred income tax assets or liabilities will be charged or credited to income tax expense in the

period each temporary difference reverses in the future.

Ordinary Income Per Share and Net Income Per Share

Ordinary income per common share and net income per common share are computed by dividing ordinary income (after deduction for tax

effect) and net income, respectively, by the weighted average number of common shares (65,657,882 shares in 2000 and 27,228,112 shares in

1999 considering stock split) outstanding during the year.

3. CASH AND CASH EQUIVALENTS AND FINANCIAL INSTRUMENTS

Cash and cash equivalents and financial instruments as of December 31, 2000 and 1999 consist of the following:

Included in the above long-term financial instruments are W81,831 million ($64,960 thousand) and W40,000 million ($31,753

thousand), respectively, as of December 31, 2000 and 1999, which are pledged as collateral for bank loans, and are thereby subject to

withdrawal restrictions. In addition, long-term financial instruments include restricted deposits amounting to W7,669 million ($6,088

thousand) and W7,588 million ($6,024 thousand), respectively, as of December 31, 2000 and 1999, which are provided as guarantee for

the storage in cash service machine. Also, as of December 31, 2000 and 1999, W14 million ($11 thousand) of long-term financial

instruments are provided as guarantees for checking accounts.

December 31, 2000 and 1999

NOTES TO FINANCIAL STATEMENTS

www.kookmincard.co.kr38

Cash and cash equivalents

Cash on hand - W 3 5 7 W 5 7 0 $ 2 8 4 $ 4 5 3

Passbook account 1 . 0 4 , 5 2 4 2 , 3 0 4 3 , 5 9 1 1 , 8 2 8

4 , 8 8 1 2 , 8 7 4 3 , 8 7 5 2 , 2 8 1

Short-term financial instruments