Market hypotheses 2016

20

Market Hypotheses and Models

-

Upload

david-keck -

Category

Economy & Finance

-

view

217 -

download

0

Transcript of Market hypotheses 2016

Market Hypotheses and Models

The Five Pillars 2

Nobel Prize winner and former Univ. of Chicago professor, Merton Miller, published a paper called the “The History of Finance”

Miller identified five “pillars on which the field of finance rests” Miller-Modigliani Propositions• Merton Miller 1990 and Franco Modigliani 1985

1. Capital Asset Pricing Model• William Sharpe 1990

2. Efficient Market Hypothesis• Eugene Fama 2013

Paul Samuelson, Harry Roberts, Benoit Mandelbrot 3. Modern Portfolio Theory

• Harry Markowitz 19904. Options

• Myron Scholes and Robert Merton 1997

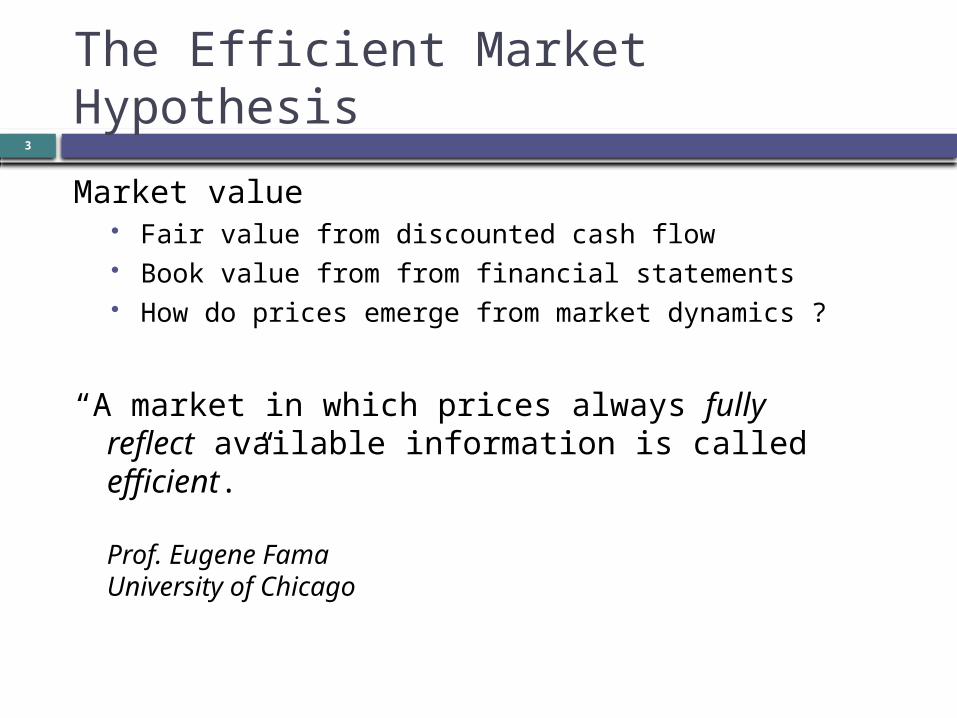

The Efficient Market Hypothesis

Market value Fair value from discounted cash flow Book value from from financial statements How do prices emerge from market dynamics ?

“A market in which prices always fully reflect available information is called efficient.”

Prof. Eugene FamaUniversity of Chicago

3

Hypotheses and Models Explanations of

phenomenon Hypothesis

A proposed explanation for a phenomenon

Law Statement of cause and

effect without explanation Newton’s Universal Law of

Gravitation Theory

A well-established explanation for a phenomenon

Einstein’s theory of gravity

A model is a mathematical or physical representation of a hypothesis, theory, or law The “Bohr

atomic model” Newton’s

inverse square law of gravity

Einstein’s Theory of General Relativity

4

EMH Commentary

“There is an impressive body of empirical evidence which indicates that successive price changes in individual common stocks are very nearly independent. Recent papers by Mandelbrot and Samuelson show rigorously that independence of successive price changes is consistent with an ‘efficient’ market i.e., a market that adjusts rapidly to new information.”

Fama, Fisher, Jensen, and Roll, “The Adjustment of Stock Prices to New Information”, International Economic Review, Feb. 1969.

5

EMH Commentary

“I believe there is no other proposition in economics which has more solid empirical evidence supporting it than the Efficient Market Hypothesis. That hypothesis has been tested and, with very few exceptions, found consistent with the data in a wide variety of markets...”

Prof. Michael C. JensenSome Anomalous Evidence Regarding Market Efficiency, 1978

6

EMH Commentary

“ … the Efficient Markets Hypothesis (EMH), one of the most controversial and well-studied propositions in all the social sciences. It is disarmingly simple to state, has far-reaching consequences for academic pursuits and business practice, and yet is surprisingly resilient to empirical proof or refutation. Even after three decades of research and literally thousands of journal articles, economists have not yet reached a consensus about whether markets – particularly financial markets - are efficient or not.“

Prof. Andrew Lo, MIT, 1997

7

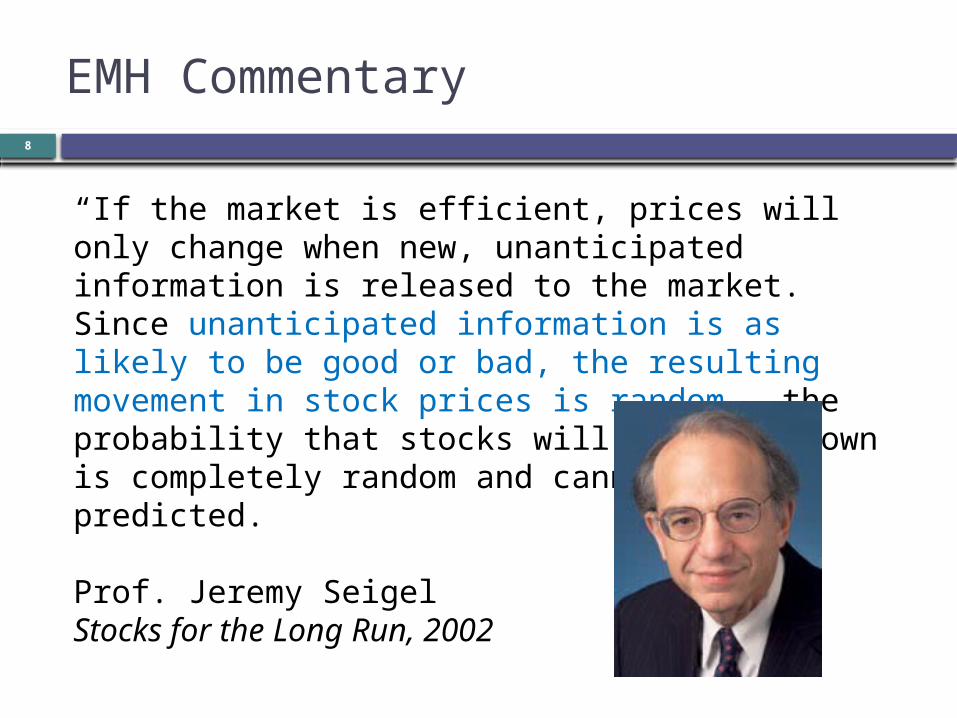

EMH Commentary 8

“If the market is efficient, prices will only change when new, unanticipated information is released to the market. Since unanticipated information is as likely to be good or bad, the resulting movement in stock prices is random … the probability that stocks will go up or down is completely random and cannot be predicted.

Prof. Jeremy SeigelStocks for the Long Run, 2002

EMH Commentary

“The more efficient the market, the more random the sequence of price changes generated by the market, and the most efficient market of all is one in which price changes are completely random and unpredictable.”

Campbell, Lo, MacKinlayThe Econometrics of Financial

Markets, 1997

9

Example Mis-interpretations

The EMH says something very simple, which is that shares are always correctly priced. p. 57.

The EMH states that every security’s price equals its investment value at all times. p. 204

If markets are efficiently priced, then sharesmust always be at fair value and it follows that there can be no difference between price and value. p. 59.

Andrew Smithers, Wall Street Revalued, 2009.

10

Implications of the EMH

• “Always fully reflected” implies that all new information is immediately reflected in the price

• Information about risk and return drives supply and demand for a security • But what is ‘information’ ? What is noise? What

information is relevant? • Type of information

• Technical information • Prices, volume, correlation, volatility

• Fundamental information • Free cash flow growth, cost of capital

• Public and private information

• Might imply that information is rationally “reflected”• but doesn’t define rational other than maybe as a

tautology

11

Implications of the EMH

Markets are almost surely ‘complex systems’ Laws or general theories of markets seem improbable Markets might be modeled as complex systems to gain insights

How can a result emerging from a complex system be defined as ‘correct’ ?

How can a random variable in a stochastic system be defined as ‘correct’ ?

Price change rates in an efficient market are not predictable which means the rates are uncorrelated, but not necessarily independent

The EMH does imply that a trading strategy will not consistently outperform a buy and hold strategy

12

EMH Testing: Original Taxonomy Prices are information efficient with respect to what

information?

”The 1970 review divides work on market efficiency into three categories: (1) weak-form tests

How well do past returns predict future returns?, (2) semi-strong form tests

How quickly do security prices reflect public information announcements?,

(3) strong-form tests Do any investors have private information that is not fully

reflected in market prices?”

Note that there is no mention of “correct price” or “price equal to (fair) value” in any test

Prof. Eugene Fama, 1991

13

EMH Testing: Updated Taxonomy “Instead of weak-form tests, which are only concerned

with the forecast power of past returns, the first category now covers the more general area of tests for return predictability …

For the second and third categories, I propose changes in title, not coverage.

Instead of semi-strong form tests of the adjustment of prices to public announcements, I use the now common title, event studies.

Instead of strong-form tests of whether specific investors have information not in market prices, I suggest the more descriptive title, tests for private information.”

Note that there is no mention of “correct price” or “price equal to (fair) value” in any test

Prof. Eugene Fama, 1991

14

Event Studies 15

http://freerisk.org/wiki/index.php/Efficient-markets_hypothesis

Fair Game 16

Return rate in a fair game is a stationary process The expected value your capital, S, does not change The distribution of rates over time is not necessarily IID The EMH can be modeled as

Biased Game

Sub-martingale 17

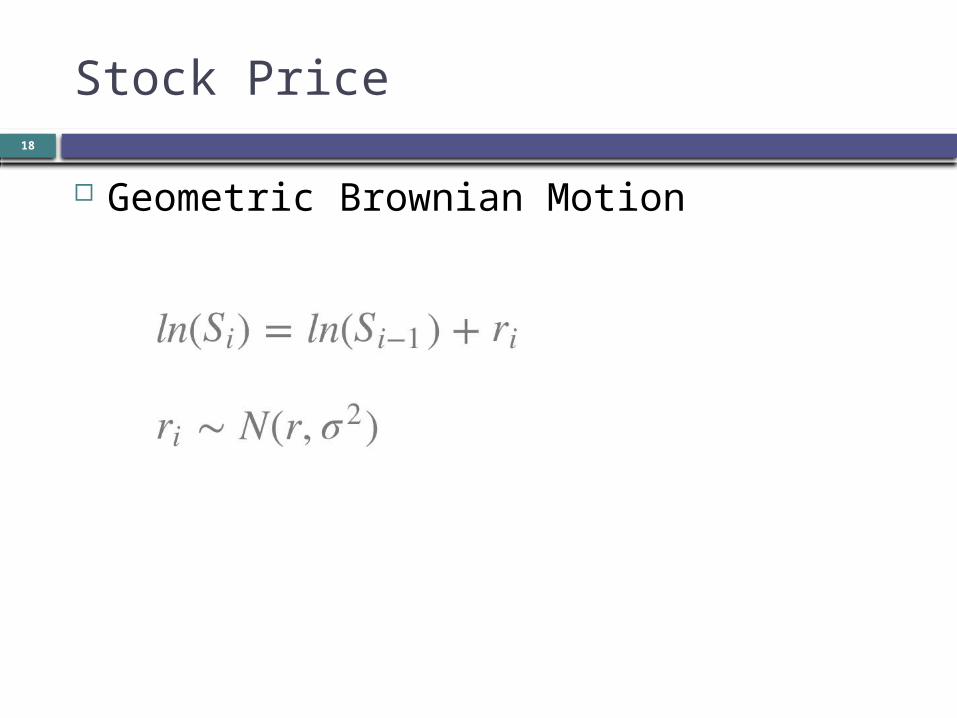

Stock Price

Geometric Brownian Motion 18

The Rational Market Hypothesis

“One of the central tenets of modern financial economics is the necessity of some trade off between risk and expected return, and although the martingale hypothesis places a restriction on expected returns, it does not account for risk in any way. If an asset’s expected price change is positive, it may be the reward necessary to attract investors to hold the asset and bear the associated risks. Therefore despite the intuitive appeal that the fair game interpretation might have, it has been shown that the martingale property is neither necessary nor sufficient condition for rationally determined asset prices. “

Campbell, Lo, MacKinlayThe Econometrics of Financial Markets, 1997

19

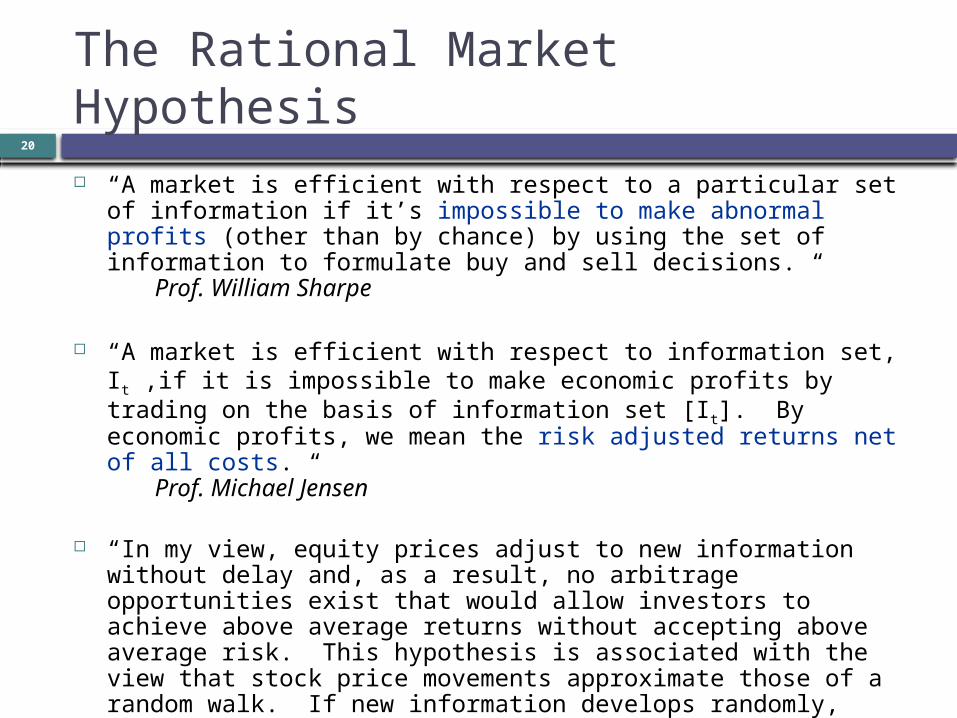

The Rational Market Hypothesis

“A market is efficient with respect to a particular set of information if it’s impossible to make abnormal profits (other than by chance) by using the set of information to formulate buy and sell decisions. “

Prof. William Sharpe

“A market is efficient with respect to information set, It ,if it is impossible to make economic profits by trading on the basis of information set [It]. By economic profits, we mean the risk adjusted returns net of all costs. “

Prof. Michael Jensen

“In my view, equity prices adjust to new information without delay and, as a result, no arbitrage opportunities exist that would allow investors to achieve above average returns without accepting above average risk. This hypothesis is associated with the view that stock price movements approximate those of a random walk. If new information develops randomly, then so will market prices, making the stock market unpredictable apart from its long-run uptrend.”

A Random Walk Down Wallstreet, Prof. Burton Malkiel

20