MARINE - Willis - Global Risk Advisor, Insurance and ... Marine Market Review August 2008 1 Foreword...

48

Sailing close to the wind August 2008 MARINE MARKET REVIEW

Transcript of MARINE - Willis - Global Risk Advisor, Insurance and ... Marine Market Review August 2008 1 Foreword...

Sailing close to the windAugust 2008

MARINEMARKETREVIEW

Willis Limited, Registered number: 181116 England and Wales. Registered address: 51 Lime Street, London, EC3M 7DQ.A Lloyd's Broker. Authorised and regulated by the Financial Services Authority.

6637/08/08

Willis Marine contact addresses

The Willis Building51 Lime StreetLondon EC3M 7DQTelephone: +44 (0)20 3124 6000Fax: +44 (0)20 3124 8223

One World Financial Center200 Liberty Street, 7th FloorNew York, NY 10281-1003Telephone: +1 212 915 8888

Suite 200, 505 Union Station505 Fifth Avenue SouthSeattle Washington98104Telephone: +1 206 386 7400

Suite 900One Bush StreetSan FranciscoCalifornia94104Telephone: +1 415 981 1141

43155 Main StreetSuite 2200BNoviMichigan48375Telephone: +1 248 735 7580

11240 Waples Mill RoadSuite # 301FairfaxVirginia22030Telephone: +1 703 591 0093

Suite 1600,The Poydras Center650 Poydras StreetNew OrleansLouisiana70130Telephone: +1 504 581 6151

78 Shenton Way# 23-02/03Singapore079120Telephone: +65 6221 9877

3502 The Lee Gardens33 Hysan AvenueCauseway BayHong KongTelephone: +852 282 70111

Lilleakerveien 6DOsloNorwayNO-0283Telephone: +47 2329 6000

Herrlichkeit 1Bremen28199GermanyTelephone: +49 4215 9010

10/F, UC Tower500 Fushan RoadPudong New Area Shanghai200122ChinaTelephone: +86 21 3887 9988

Corporate PlazaRua Alexandre Dumas 2100, 4 AndarChacara Santo AntonioSão Paulo04717-004Brazil Telephone: +55 11 2161 6000

Piazza Dante, 7GenovaItaly Telephone: +39 0105 46711

www.willis.com

6637_MMR_Covers_FINAL FOR PRINT:Layout 1 06/08/2008 15:50 Page 1

Editorial CommitteeRichard Close-SmithCatherine CartwrightKatherine Parsons

ContributorsBen AbrahamSally BramallAndy BuglerPatrick ChowMark FelthamBrian FullerLewis HartDavid KeyesOdd Christian KrohnTrevor McGarryTom PrestAlistair RiversDarren RowlandNicholas RubenChris Taylor

DesignMaria Valeria Mazzitelli

6637_MMR_Covers_FINAL FOR PRINT:Layout 1 06/08/2008 15:50 Page 2

Willis Marine Market Review August 2008 1

Foreword 2

Introduction 4

Hull and Machinery 7

Superyachts 10

Protection and Indemnity 12

Liabilities 19

Cargo 22

Claims 29

Reinsurance 32

Letters from Overseas: 35

– New York 36

– Norway 37

– Singapore 38

– Hong Kong 40

Willis Quality Index® 41

Conclusion 43

CONTENTS

6637_MMR_Inners_FINAL:Aviation Market Review Inners2 07/08/2008 09:21 Page 1

FOREWORD

6637_MMR_Inners_FINAL:Aviation Market Review Inners2 07/08/2008 09:21 Page 2

Willis Marine Market Review August 2008 3

This time last year few commentators andanalysts were forewarning us of the truefinancial implications of the collapse of thesub-prime market. Here we are, twelvemonths later in an extremely challengingeconomic environment, having witnessedthe slowdown in the economies of mostWestern countries. Many of theinternational banks have been obliged to strengthen their balance sheets and some well-known financial institutionshave failed.

Against this background the marine industryhas continued to thrive. Shipyards andShipowners have continued to out-perform,with innovation driving many projects togreater heights and lengths! Commodityprices have remained high as therecontinues to be concern over the availabilityof a number of raw materials and worldtrade values have continued to increase.

Prompted by the economic climate, thoseserving the marine industry are now tacklingold issues and inefficiencies. The insurancemarket is providing new products andservices, struggling for greater operationalefficiencies and there is more discussion ofindustry-wide problems such as the globalcrew shortage. We at Willis are playing ourpart to drive these improvements.

The continued trend towards a softeningmarket in many countries has been fuelledby new entrants and general maritimeresults. However, over the next 12 monthswe will see more insurers changing theirunderwriting philosophies as the cost ofcapital impacts the insurance industry.

Therefore, in order to analyse the impactof these changing and challengingcircumstances, my colleagues and I arepleased to offer you this latest Willis Marine Market Review.

Alistair RiversAugust 2008

6637_MMR_Inners_FINAL:Aviation Market Review Inners2 07/08/2008 09:21 Page 3

INTRODUCTION

6637_MMR_Inners_FINAL:Aviation Market Review Inners2 07/08/2008 09:21 Page 4

Willis Marine Market Review August 2008 5

The business of underwriting is both capital and skillintensive. Neither of theseassets can be simply switchedoff or even put to one side andreactivated at a more attractivepoint in the underwriting cycle.Before concentrating on theindividual Marine markets wemust first look at the biggerpicture summed up so well bythe Chief Executive Officer ofAMLIN, Charles Philipps:

“On the plus side, the London Market hasnever been so well positioned to manage the cycle. In particular, the Lloyd’s markethas made huge progress over the last decade. Having clawed its way back,battered and bloodied, in the 1990s from a solvency crisis that few, initially, wouldhave predicted it would survive; it hasslowly, steadily and methodically rebuiltits brand in global markets. It has grownits capacity, brought new investors intothe U.K. insurance sector, achieved thefirst ever insurance market rating, hasbuilt on that position and has gripped the issue of market process reform.

In underwriting terms, key differencesbetween now and the last soft marketinclude a radical improvement in thedepth, breadth and quality of managementinformation within the market. Combinedwith such initiatives as the U.K.’s move to risk based capital and the successfulimplementation of Lloyd’s FranchisePerformance regime, the market’s abilityto manage the cycle has improved out ofall recognition.

Such developments have been furtherunderpinned by increased divergence inthe cyclical position between classes, theincreased scrutiny by rating agencies andthe greater involvement of capital marketsin the sector.

What has yet to be truly tested, however, is the ‘human factor’. Now, as neverbefore, it is vital that those within theLondon Market – both at board and theunderwriter level – resist the pressure of softening markets to slip back into the bad underwriting habits of the past.

Abandoning underwriting discipline at thispoint would be disastrous and not just forresults. The very progress that has beenmade over recent years means the markethas run out of excuses for getting it wrong.There will be no easy market processscapegoats to blame, no compellingarguments for why the market will do betternext time – and there will be no secondchance for the London Market’s futurecredibility and reputation.”

When Marine underwriters in Londonraised prices in late 2001 and 2002 following‘9/11’, the Scandinavian underwriters sawthis as an overreaction. By offering stablepricing they increased their market share at the expense of the London market.

Today, while all Marine underwriterswould prefer higher premiums, it seems to be the Scandinavian market which feels that it cannot survive without them.Unusually the leading Scandinavian hull underwriters are actually turningaway business in their determination toraise prices.

In the words of Paul Springman of Markel“this is the first time in three or four years we’ve heard about any product linemoving anywhere other than down”.

6637_MMR_Inners_FINAL:Aviation Market Review Inners2 07/08/2008 09:21 Page 5

6637_MMR_Inners_FINAL:Aviation Market Review Inners2 07/08/2008 09:22 Page 6

HULL ANDMACHINERY

6637_MMR_Inners_FINAL:Aviation Market Review Inners2 07/08/2008 09:22 Page 7

8 Willis Marine Market Review August 2008

Shipping market

Despite the looming recession thatthreatens the global economy, so far theshipping market has remained buoyant.The emerging economies of China andIndia continue to lead demand, as theyimport raw materials to drive theirexpanding economies. This demand forkey raw materials has bolstered the drybulk sector, particularly Capesize, pushingprices and freight rates to all-time highs.

In recent years, the demand-drivenshipping market has led to a boom in thenumber of newbuildings ordered. Many ofthese newbuildings will be delivered in2010. These additions may flood the market,especially if there is not adequate scrappingof old vessels. Recently newbuilding ordershave fallen, yet shipyards are still so busythat repairs are costly and often delayed.Exorbitant metal prices have also pushed up the cost of repairs. In order to avoid timeoff hire, repairs are being delayed andshipowners are keener than ever toeliminate accidents. However, the globalcrew shortage means it is difficult to ensurethat crew are always experienced and welltrained. This leads to an increase inaccidents due to human error. Inevitably,the global crew shortage will be exacerbatedby the launch of further newbuildings andthe increase in the world fleet.

In order to fund newbuildings, shippingcompanies are looking at various financeoptions. In light of the U.S. sub-primechaos, banks have limited lending but thetangible nature of shipping has resulted in it being a more favoured asset. Due tocurrent market conditions, companiesmay no longer opt for public share issues.Recently, both Wah Kwong MaritimeTransport Holdings and ZIM IntegratedShipping Services postponed IPOs infavour of alternative financing optionsbecause of the uncertainty and instabilityin the global capital markets.

Another economic factor to consider is thesoaring price of oil; this has necessarily had aknock-on effect on the cost of bunker fuel.

According to industry sources, bunkerprices have tripled within the last threeyears and bunkers now constitute nearlyhalf of total vessel costs, thus seriouslyeroding the profit margins of shippingcompanies and increasing pressure to cutother costs such as insurance premiums.

Overall the current market appears buoyant.However, the performance of the shippingsector is linked with the health of the globaleconomy. Therefore, the rising price of oiland the threat of a global recession may lead to more careful consumer spending, an economic slow-down, and lower tradevolume. This would result in decreaseddemand for tonnage. Nevertheless, in theface of the current demands of China andIndia, such a global downturn seems only a distant concern.

Hull rates

Shipowners are benefiting from relatively‘flat’ insurance rates, with ‘as expiry’premium levels common. Some fleets and accounts with good records have beenachieving improved terms by means of enhanced performance relatedcontinuity credits.

Owners always have the option of switchinginsurers, especially as there is plenty ofcapacity in the market for all but the veryhighly valued cruise ships. Those who doseek alternatives to their incumbentinsurer can sometimes secure significantsavings as underwriters find it easier toassess new business, rather than rewardexisting clients with better terms,irrespective of their relative merits.

Inevitably, one of the outcomes ofinadequate premiums is that all claims are heavily scrutinised. In addition, thecurrent high values of vessels mean thatunderwriters’ exposures have grown.According to CEFOR, the average claimper vessel has doubled since 2003. Withinsome underwriting organisations largeclaims have to be referred upwards by theunderwriter which at best causes delayand at worst can mean that a claim is

6637_MMR_Inners_FINAL:Aviation Market Review Inners2 07/08/2008 09:22 Page 8

Willis Marine Market Review August 2008 9

contested for commercial rather thantechnical reasons. This makes theselection of leaders vitally important.

The increases in vessel values requireadditional premiums. However, thishigher exposure has until recently beenpurchased by owners very cheaply. Nowunderwriters are trying to achieve moreproportional adjustments to ensure theyreceive an appropriate level of premiumfor the increased risk.

Since the beginning of 2008, there hasbeen a divergence in underwriters’behaviour: all aspire to higher premiumsbut only some are insistent upon them.

The hardening market trend ispredominantly being led by mono-linemarine hull underwriters. Theseunderwriters are under particularlyintense pressure and are thereforedesperate to increase rates. In contrast,the composite syndicates in Lloyd’s seem to be under less strain.

A number of the leading Lloyd’s andCompany underwriters, led by SimonStonehouse, Joint Hull Chairman and hull underwriter from the Brit Syndicate have publicly made speeches calling forincreased deductibles, but the market has never done exactly as it is told!

So far, rates have remained low and themarket has remained stable. However, it is likely that over the coming year themarket will begin to harden especially forthose with less than immaculate records.

Underwriting markets

Norwegian Hull Club has led the chargefor increased premium by trying to imposeincreases on all Hull business. In order to push this through, they have beenprepared to lose 35% of their book, albeitnot their core favoured domestic clients.

Gard has followed suit but to a lesserextent and are being very selective on new business.

Bluewater has had very disappointingresults and this has led to the ratingagencies downgrading their security.

The Swedish Hull Club has pushed forincreases on all business. They have issueda report focusing on increased repair costsand claims levels, and have contrasted thiswith the low level of premiums. This is the justification behind their argument for the need for premium increases.Furthermore, the Club are not currentlyinterested in pursuing new clients.

Thomas Miller has withdrawn its hullvehicle DEX from the market and thecurrent portfolio will be handled byGroupama Transport who are already the capital providers for DEX.

MSMI have had a difficult year from aclaims perspective. As a consequence, they have been requesting premiumincreases from their members. In general,the members have been willing toaccommodate such requests in light of the specialist service provided.

The London Market has seen very littlenew capacity apart from Wurttemburgischebeing re-launched in Lloyd’s as Antares Syndicate.

Far Eastern markets we would suggest havenot fared well following their aggressiveentry into international business, over thepast three to four years, at very competitivepremium levels. Hong Kong, Korea andJapan are not the force they were.

However, Singapore is a strong emergingmarket, where a number of operationshave started up, many backed by Lloyd’ssyndicates. This market can be verycompetitive on the right businessparticularly where there is any ‘local management’.

6637_MMR_Inners_FINAL:Aviation Market Review Inners2 07/08/2008 09:22 Page 9

SUPERYACHTS

6637_MMR_Inners_FINAL:Aviation Market Review Inners2 07/08/2008 09:22 Page 10

Willis Marine Market Review August 2008 11

The expansion in the Superyacht industryhas shown no sign of abating over the past 12 months. The builders’ order books are still full for the next four to five years, valuesare increasing and the ‘global credit crunch’ has not yet had any adverse effect, as seen in the graph below.

Due to the extremely good loss ratio enjoyedby the specialist insurers over the past fiveyears or so, 2008 has so far seen many newmarkets wanting to write this business. The new markets with the most capacityinclude: Fortis, Norwegian Hull Club, Gard,Groupama and Axa. These insurers havejoined the traditional ‘players’ such as LeadYacht, Underwriting Risk Services and theGSC Syndicate in Lloyd’s.

The USD 10-30 million market is nowextremely competitive and this has led to a significant softening of hull rates. We estimate that there has been a reductionof between 15% and 20% since this time last year. Rates have remained a littlesteadier for USD 30 million+ yachts.

There are still few brokers specialising inthis niche. This is due to the fact that thesevessels are their owners’ pride and joy and so require special care and attention.Brokers would sooner sub-broke theirclient’s business through a specialist suchas Willis, rather than placing the riskthemselves and making mistakes.

The popularity of large yacht ownership isgrowing on an almost monthly basis, largely

due to the emerging demand from Russia andthe Far East. However, the more traditionalowners from Western Europe and NorthAmerica are also purchasing bigger and moreopulent vessels. In 2008, the world’s mostvaluable yacht to date was launched – it is said to be valued at EUR 500 million!

Yacht management companies remainvery influential and the major companiesare now offering their owners thecomplete package including sales, charter,management (both yacht and financial),newbuild project management, crewhiring and firing and other services.

The issues which remain outstanding withinthe industry are the same as 12 months ago,only now they have been exacerbated by theincreased demand. There is a severe shortageof good crew: it is easy to understand why this is a growing problem when the newlarger Superyachts require over 100 crew.Build times are another problem, as they areincreasing due to the very high demands and expectations of owners. There is alimited number of berths, particularly in theMediterranean. Other problems the industryfaces include environmental issues, such asthe type of paint used.

As previously mentioned, so far the globaleconomic slowdown has not yet impacted theSuperyacht market. However, it is likely thatat some point there will be a knock-on effect,not at the very top end of the market but inthe USD 5-10 million range. The chartermarket may also begin to suffer.

1000

900

800

700

600

500

400

300

200

100

0

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Num

ber

of Y

acht

s

Global Order Book Growth

6637_MMR_Inners_FINAL:Aviation Market Review Inners2 07/08/2008 09:22 Page 11

PROTECTIONANDINDEMNITY

6637_MMR_Inners_FINAL:Aviation Market Review Inners2 07/08/2008 09:22 Page 12

Willis Marine Market Review August 2008 13

Background - Renewal at February 20, 2008

The background to the 2008 Protection andIndemnity (P&I) renewal was fairly bleak.

The Pool claims record for the 2006/07policy year was the worst ever. The 2007/08year was still undeveloped but all the signs indicated it was heading towards asimilar level.

Retained claims performance showedsome variance between Clubs, but largelymirrored the adverse Pool development.

Adding to these underwriting problems,the investment climate in 2007/08 wasalso extremely uncertain. In the previousyear exceptional investment incomeresults had offset the record underwritingdeficits, in 2007/08 however a moremarginal contribution from investmentincome was expected.

The above factors led to a range of GeneralIncreases being announced, averaging at the highest level for five years (+16.15%+ International Group reinsuranceadjustments).

‘Cash Was King’ –Negotiation of Renewal at February 20, 2008

The renewal discussions themselves wereuncharacteristically confrontational.

It was clear that the underwriters’ need to obtain premium increases conflictedwith the ship operators’ need to limitfurther increases to their cost base. These contradictory forces lead to themost adversarial renewal negotiations for over 10 years.

This may seem surprising as the generalincreases announced were materially lowerthan in the early 1990s and 2000s. Theadverse claims development was evident,and it was obvious that the underwritingdeficits were unsustainable in a mutualmarket. However, while acknowledging this,

ship operators were faced with increasingcosts in all areas (bunkers, crew wages,maintenance, dry-docking etc.) and sonaturally fought hard to mitigate anypremium rises for their fleets.

The combination of these issues led todelayed renewal offers and generally amuch later conclusion of negotiationsthan normal.

The other key trait of the 2008 renewalwasthat for the Clubs ‘cash was king’. It wasclear that securing premium increases was the fundamental consideration acrossthe market. Clubs resisted entering intodebates about deductible structures. As a result, there was little value offered in terms of premium savings in exchangefor increased retentions.

Our estimate of the actual premiumincrease pushed through by the market wasbetween 13% and 14% on mutual P&I.Within this average figure, possibly becauseof the style of the renewal, there was anotably wider range of individual resultsdepending on fleet, record and Club thanwould normally be expected.

In contrast, Fixed Premium P&I, CharterersLiability, Energy Related P&I and FreightDemurrage and Defence areas of businesswere far more stable. If increased at all itwas only by ‘inflationary’ rises.

Winners and Losers - Renewal at February 20, 2008

As ever, immediately post-renewal, thereis an almost obsessive analysis of tonnagemovements between Clubs. In a mutualenvironment this is not necessarily thebest measure of performance, but it is atangible benchmark.

February 2008 saw slightly moremovement between Clubs than normal. In total, more than seventy fleets wereinvolved in some sort of tonnageredistribution, but in the majority of casesthese were only partial movements oftonnage and/or consolidations of fleets.

6637_MMR_Inners_FINAL:Aviation Market Review Inners2 07/08/2008 09:22 Page 13

14 Willis Marine Market Review August 2008

The North of England and Standard Clubtopped the tables for the number ofwinning fleet movements.

At the other end of the table, perhaps asexpected, the American Club and West ofEngland experienced net losses. Rather moreunusually these Clubs were in good company,with Britannia and the Shipowners’ Club whowould normally be towards the top of thetable, also losing tonnage.

The Gard was notable for making goodgains, but also for losing one of theirbiggest premium contributors (RCCL).

It is too simplistic to view the above as thefinancial winners and losers in the market.Only time will tell whether the tonnagemovements were wise or not.

For example, it is arguable that Britannia’shard line on their large general increasemay well leave them better placedfinancially than a number of theircompetitors going forward, although it lost them tonnage at this renewal.Similarly, those Clubs which rapidlyincreased in size must exercise caution in order to ensure that their financialstrength grows by at least the same rate.

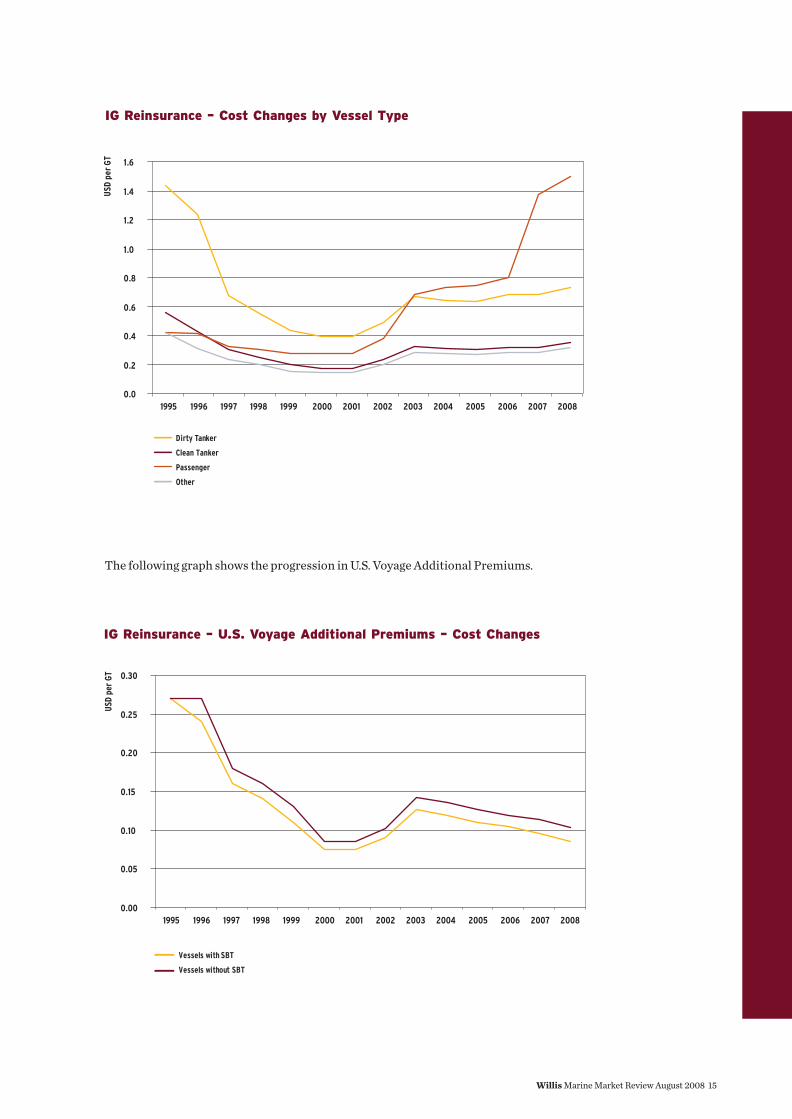

Changes in InternationalGroup Reinsurance – Renewalat 20 February 2008

As expected there were no materialchanges to the Retentions or Structure ofthe International Group (IG) reinsuranceprogramme at 20 February 2008.

The key issue for the reinsurance renewalwas also cost.

Despite a relatively flat reinsurancemarket, the reinsurance rates wereincreased by an average of 9.77% and alltypes of ships were impacted. The largestpercentage increase was on dry cargoships (+12.65%), dirty tankers faced thesmallest percentage increase (+7.4%)while clean tankers and passenger shipsincreased by 9.76% and 9.27% respectively.

Even though when translated to directpremiums the reinsurance increases wererelatively modest (average direct premiumsincreased between 1% and 2%) they cametowards the end of a challenging season.The increases were therefore perceived asan unexpected ‘sting in the tail’ of analready difficult renewal.

As implied above, the driving factorbehind the reinsurance increases was notthe reinsurance market itself but therequirement to address the losses of theInternational Group Captive (Hydra).

Hydra reinsures each Club’s share of theupper Pooling layer (USD 20 million excessof USD 30 million), together with eachClub’s 25% share of the first layer of the IG’sreinsurance programme (USD 500 millionexcess of USD 50 million). Unlike the costsof the IG Pool itself, Hydra is funded by aproportion of the IG reinsurance premiumallocated to each vessel.

The surge in large claims in 2006 wouldhave effectively wiped out Hydra’sreserves: the projected total claims cost on Hydra for the 2005 and 2006 yearscombined was USD 162 million, whereasnet premiums into Hydra totalled USD 119 million.

In order to avoid potential insolvency, an unplanned refinancing was effected in April 2007 through a USD 50 millioncapital call shared across all the IG Clubs.This refinanced the captive, but did not prepare it for the continuing highclaims levels as experienced in 2006.With similar claims levels developing in2007, the decision was taken to increaseannual premiums into Hydra fromFebruary 20, 2008. This had the obviousknock on effect of increasing the IGreinsurance rates per vessel.

One of the very few ‘bright spots’ in thereinsurance results was the reduction inU.S. Voyage Additional Premiums (-10%).

The impact on the reinsurance cost bytype of vessel is outlined overleaf.

6637_MMR_Inners_FINAL:Aviation Market Review Inners2 07/08/2008 09:22 Page 14

Willis Marine Market Review August 2008 15

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

USD

per

GT

Dirty Tanker

Clean Tanker

Passenger

Other

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

0.00

0.05

0.10

0.15

0.20

0.25

0.30

USD

per

GT

Vessels with SBT

Vessels without SBT

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

IG Reinsurance – Cost Changes by Vessel Type

IG Reinsurance – U.S. Voyage Additional Premiums – Cost Changes

The following graph shows the progression in U.S. Voyage Additional Premiums.

6637_MMR_Inners_FINAL:Aviation Market Review Inners2 07/08/2008 09:22 Page 15

16 Willis Marine Market Review August 2008

2007/08 Financial Results

At the time of writing, all of the 13 IG Clubshave provided at least some form of initialindications of their 2007/08 financial yearresults, pending publication of their fullReports and Accounts later in the year.

These early ‘tasters’ from the Clubs provideonly the briefest summary of the financialhighlights, but they are not entirely useless. Of the 13 Clubs, seven have indicated that they will report overall surpluses(including investment income) for the 2007/08 financial year, while theremaining six have suggested that theysuffered overall deficits.

Widespread underwriting deficits remain,but in most cases investment incomeresults do not look as dire as some feared.

A full analysis of the actual financialresults of all the Clubs will be included in the Willis P&I Review later in the year when all of the Clubs have actuallypublished their Reports and Accounts and the initial indications can be double checked.

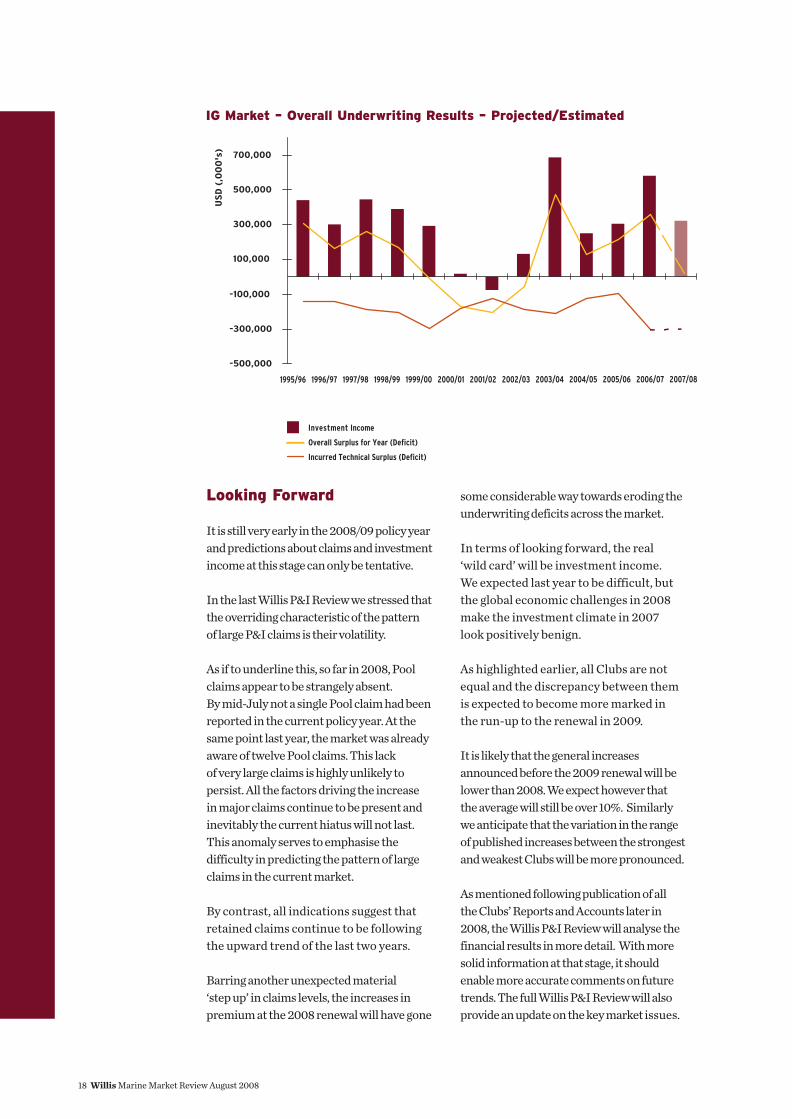

In the meantime the graph below outlinesthe provisional overall results released by the Clubs prior to release of theirformal Accounts.

As mentioned above, seven of the Clubs areexpected to report overall surpluses for the2007/08 financial year. Of these only two(Skuld and Steamship) are expected toshow even modest underwriting surpluses.For the remaining five (American, Gard,Japan, North of England and Standard)investment income was sufficient tocompensate for underwriting losses.

The six Clubs expected to report overalldeficits (Britannia, London, Shipowners,Swedish, U.K. Club and West of England)either experienced extremely adverseunderwriting results or very low investmentincome (or a combination of both).

As continually emphasised by Willispublications, there continues to be amaterial variance between the best andworst performing Clubs in the market.

The above summary of results is obviouslynot the whole story and overallsurpluses/deficits for a single year are easy to misinterpret.

Clubs are of differing sizes and financialstrength to start with. In terms of percentageincrease or decrease in Free Reserves, theSteamship represents the best performingClub in 2007/08 (nearly an 18% increase)whereas the worst performing is the LondonClub (27% reduction).

2.4

-33

32

2.8

-30

30

-6

129

28

-2.3

-34-31

-40

-20

0

20

40

USD

(mill

ions

)

American Britannia Gard Japan London North Shipowners Skuld Standard Steamship Swedish U.K. West of (incl of Club England

Boudicca) England

Club Surpluses/Deficits -2007/08 Overall Surplus/Deficit - Individual Clubs

6637_MMR_Inners_FINAL:Aviation Market Review Inners2 07/08/2008 09:22 Page 16

Willis Marine Market Review August 2008 17

The London Club’s woes stemmed from a USD 30 million underwritingdeficit combined with a terribleinvestment result (almost no investment income).

The Steamship also had a reducedinvestment result (but still managed a 4% return). Their small technicalsurplus resulting largely from acombination of increased premiums and reduced back years’ claims. The Steamship’s entire investment result therefore contributed directly to the Club’s Free Reserves.

The scale of Britannia’s overall deficit is also slightly misleading. Britannia(unlike the majority of the market) does not include their 2007/08 budgeteddeferred call in their reported figures. If the full deferred call for 2007/08 was made this would represent anadditional contribution of USD 45 million.Thus, if Britannia reported as other Clubs and in line with the market normtheir USD 32.5 million deficit would be eradicated.

The Gard surplus mentioned in the graph relates solely to the P&I class of the ‘Gard Group’ (i.e. it excludes the Gard Marine and Energy classes).

IG Market – Financial Summary

In the Willis 2007/08 P&I Review wesuggested that a 6% return on investmentwould be sufficient to offset a similarunderwriting deficit to 2006/07. Feedbackfrom the Clubs following February, 20indicates that, on average, investmentincome may well be close to this level ofreturn. The combined market result istherefore likely to achieve close to (though probably marginally below) an overall break even position.

The Willis 2008/09 P&I Review will includea more complete analysis of the Clubs’positions, but initial results suggest:

– The 2007/08 claims are at a similarhigh level to 2006/07 (though there are some variances in the developmentof back years’ claims).

– The investment income is reduced,but is by no means as disastrous asmany feared.

– There is variation in individual Clubresults, but the International Groupcombined is probably going to show avery marginal deficit overall.

Our estimate of the projected overall marketresult is outlined in the graph overleaf.

6637_MMR_Inners_FINAL:Aviation Market Review Inners2 07/08/2008 09:22 Page 17

18 Willis Marine Market Review August 2008

Looking Forward

It is still very early in the 2008/09 policy yearand predictions about claims and investmentincome at this stage can only be tentative.

In the last Willis P&I Review we stressed thatthe overriding characteristic of the pattern of large P&I claims is their volatility.

As if to underline this, so far in 2008, Poolclaims appear to be strangely absent. By mid-July not a single Pool claim had beenreported in the current policy year. At thesame point last year, the market was alreadyaware of twelve Pool claims. This lack of very large claims is highly unlikely topersist. All the factors driving the increase in major claims continue to be present andinevitably the current hiatus will not last.This anomaly serves to emphasise thedifficulty in predicting the pattern of largeclaims in the current market.

By contrast, all indications suggest thatretained claims continue to be followingthe upward trend of the last two years.

Barring another unexpected material ‘step up’ in claims levels, the increases inpremium at the 2008 renewal will have gone

some considerable way towards eroding theunderwriting deficits across the market.

In terms of looking forward, the real ‘wild card’ will be investment income. We expected last year to be difficult, butthe global economic challenges in 2008make the investment climate in 2007 look positively benign.

As highlighted earlier, all Clubs are notequal and the discrepancy between themis expected to become more marked in the run-up to the renewal in 2009.

It is likely that the general increasesannounced before the 2009 renewal will belower than 2008. We expect however that the average will still be over 10%. Similarlywe anticipate that the variation in the rangeof published increases between the strongestand weakest Clubs will be more pronounced.

As mentioned following publication of all the Clubs’ Reports and Accounts later in2008, the Willis P&I Review will analyse thefinancial results in more detail. With moresolid information at that stage, it shouldenable more accurate comments on futuretrends. The full Willis P&I Review will alsoprovide an update on the key market issues.

-500,000

-300,000

-100,000

100,000

300,000

500,000

700,000

US

D (

,00

0's

)

Investment Income

Overall Surplus for Year (Deficit)

Incurred Technical Surplus (Deficit)

1995/96 1996/97 1997/98 1998/99 1999/00 2000/01 2001/02 2002/03 2003/04 2004/05 2005/06 2006/07 2007/08

IG Market – Overall Underwriting Results – Projected/Estimated

6637_MMR_Inners_FINAL:Aviation Market Review Inners2 07/08/2008 09:22 Page 18

LIABILITIES

6637_MMR_Inners_FINAL:Aviation Market Review Inners2 07/08/2008 09:22 Page 19

20 Willis Marine Market Review August 2008

In the Lloyd’s Annual underwriter Survey(February 2008) the key issue for theindustry in 2008, as identified by thesample of underwriters who responded, was ‘Managing The Insurance Cycle’.

This issue is particularly relevant for the Marine Liability market, whereunderwriters are keen to ensure that the current downturn in premiums andrates does not develop into a collapse.

Marine Liability business has historicallybeen a favoured class for underwriters,having delivered solid profit levels overthe past decade or so.

Marine Liabilities Loss Ratios

YEAR PERCENTAGE

1997 49.40%

1998 70.22%

1999 87.22%

2000 60.89%

2001 82.75%

2002 34.75%

2003 41.34%

2004 73.64%

2005 26.52%

2006 41.78%

2007 45.36%

Source: Lloyd’s Audit Code ‘G.

Underwriters in this sector had, up to mid-2007, been able to maintain a degreeof rating discipline with small reductionsbeing offered on some accounts.

However, during the second half of 2007increased competition betweenunderwriters, additional market capacityand pressure from assureds enabled brokersto obtain larger reductions on accountswhich underwriters had considered to beadequately rated and profitable.

During the January 2008 renewal season,the average reduction being offered was in the region of 10% and there has certainlybeen an increase in the use of other

incentives such as profit and continuitycommissions, prompt payment discountsand long term deals (frequently subject to an annual review clause). Also premiumsavings are often achievable wheredifferent types of coverage are packagedtogether – an example would be whereliability coverage is placed under one policy together with physical damage and business interruption insurance.

Underwriters have been able to maintainprices on some accounts where specialistcoverage is being offered or whereminimum premium levels apply. However,on other large premium income accountsmuch greater reductions have beenachieved where significant reserves of‘clean’ premium have been generated over a number of years and where there is now pressure to achievepremium savings.

It is difficult to see the current situationchanging before the end of 2008 andtherefore it is likely that rates willcontinue to fall up to the end of the year –unless the current soft market is halted as a result of a lack of capacity or byexceptional claim events.

It is clear that concerns relating to theissue of Environmental Pollution coverageare increasing in the minds of bothunderwriters and assureds. With this new focus on environmental issues, theadequacy of current limits and coverageneeds to be carefully considered.

The Lloyd’s Survey also identified‘Increasing Competition From OtherInsurance Centres’ as being a major issuefor underwriters in London. It is certainlythe case that overseas and local marketsare competing on a more regular basis on facultative Marine Liability businessthat would traditionally have been placed in the London market.

To counter this problem, a number ofLloyd’s syndicates and companies have set up their own separate underwritingcentres away from the London market,

6637_MMR_Inners_FINAL:Aviation Market Review Inners2 07/08/2008 09:22 Page 20

Willis Marine Market Review August 2008 21

which are intended to attract domesticbusiness and are able to provide localservicing. Singapore currently appears to be a favourite location – an example of this is Mark Trevitt of Travelers, whomoved in late 2007 from London toSingapore to write a book of MarineLiability/Ports business.

The underwriter merry-go-round hascontinued into 2008 with one of the most high profile moves being StephenBarr’s departure from Talbot Syndicate to start underwriting a new book ofMarine Liability business at Marketform Syndicate.

It is clear that managing the insurancecycle will be the main challenge for the Marine Liability market in 2008 – as 67% of Lloyd’s underwriters believethat insufficient progress was madeduring 2007 in this respect. If MarineLiability rates and premiums continue to fall at the current rate during thesecond half of 2008 and into 2009, thenthis sector may well be in danger of losing its favoured status.

6637_MMR_Inners_FINAL:Aviation Market Review Inners2 07/08/2008 09:22 Page 21

6637_MMR_Inners_FINAL:Aviation Market Review Inners2 07/08/2008 09:22 Page 22

CARGO

6637_MMR_Inners_FINAL:Aviation Market Review Inners2 07/08/2008 09:22 Page 23

24 Willis Marine Market Review August 2008

Market Overview and Trends

In the 2007 Marine Review, we reportedthat the cargo market was experiencingunprecedented rate reductions due toincreasing capacity and competition.

In 2008, there has been a continuation ofthe softening market, with no apparentend in sight. Cargo owners can now obtainwider coverage, reduced deductibles andhigher limits – at the same or even lowerpremiums than in 2007.

Fuelled by a weak U.S. Dollar, commodityprices and world trade volumes continue

to rise. However, from a cargo marketperspective, we have seen a 20%reduction in gross cargo premiums since 2002, against a 25% increase inworld trade volumes.

Despite the falling premiums, cargoinsurance is still showing profitableresults for insurers. We detail below the 10 largest cargo losses advised to Lloyd’s of London for the period April 1, 2007 toMarch 31, 2008. While this only includesclaims where Lloyd’s of London participateon the account, it highlights the fact thatthere have been no losses which wouldimpact the market as a whole:

TYPE OF LOSS LOCATION AMOUNT (USD)

GA AND SALVAGE FOR COPPER AFTER CHILE – INDIA 30,000,000

VESSEL GROUNDED

VESSEL SANK CARRYING STEEL PRODUCTS XINGANG – IRAN 29,800,000

JACK-UP RIG GROUNDED WHILST TOWED USA – ANGOLA 10,000,000

STEEL BARS MISSING FROM WAREHOUSE RUSSIA 9,000,000 +

HURRICANE DAMAGE TO WIND TURBINES TEXAS 8,750,000

SHORTAGE OF OIL FROM RAILCARS KAZAKHSTAN 8,600,000

RISER PIPES LOST OVERBOARD IN HEAVY WEATHER USA – KOREA 6,900,000

CONSTRUCTIVE TOTAL LOSS AS ADVENTURE LOST TAIWAN – RUSSIA 6,100,000

THEFT OF COPPER BETWEEN MINE & PORT TANZANIA 5,700,000

TOTAL LOSS OF GASOLINE FOLLOWING SOUTH AFRICA 5,600,000

LIGHTNING STRIKE

Figures provided by the Joint Cargo Committee on the 25 July 2008 – V Risk Code

The above, together with the lack of any significant losses due to naturalcatastrophes has done little to dent themarket’s confidence. Even the recent hail loss affecting Volkswagen and Porsche vehicles in Emden, Germany, is expected to have little or no impact on the marketplace.

Despite being estimated to be in excess of USD 110 million, the loss is sharedamongst a number of continental insurerswith no involvement of other marketswriting cargo accounts. The fact that such large exposures can be written by a small number of insurers means that even substantial losses only affectsmall pockets of the global marketplace,therefore doing nothing to reverse the downward trend.

The most notable development that theselosses demonstrate is the effect thatincreasing commodity prices are having onunderwriters’ exposures. The largest loss wasa General Average claim for USD 30 million –with little damage to the cargo itself!

In an effort to maintain their premiumincome from cargo business, underwritershave broadened the scope of products on offer. Stock Throughputs have continuedto prove popular, with the boundaries beingpushed even to include additional risks suchas retail exposures.

Package arrangements are becoming morepopular, with cover for businessinterruption, working equipment, tradedisruption, hull, CEND and charterersliability being added to basic cargo policies.

6637_MMR_Inners_FINAL:Aviation Market Review Inners2 07/08/2008 09:22 Page 24

Willis Marine Market Review August 2008 25

While many of the new entrants into the market struggled to meet theirpremium income expectations in 2007, the Asian cargo market remainshealthy and profitable for mostunderwriters.

Combined with the regional companyunderwriters such as AIG, Allianz, AsiaCapital Re, Ace, Chubb, Federal, Groupama,Liberty, QBE and RSA, we estimate that the capacity of the Singaporean cargomarket is now between USD 250 millionand USD 300 million.

Willis International Trade and Logisticsare ideally positioned to take advantage of the opportunities presented by thecurrent market and are at the forefront of innovative program design.

The move to globalise the cargo market is accelerating, with underwriterstransferring capacity away from Londonin an effort to maximise their involvementwith vibrant domestic markets. This hasresulted in the formation of regionalunderwriting hubs in Asia, Europe, LatinAmerica (Miami) and the Middle East.

In light of the above and the perceivedprofitability of cargo business, it is nowonder that we see cargo underwritingcapacity growing worldwide, creating afiercely competitive market and some ofthe lowest cargo premiums on record.

The marketplace

U.S.Capacity continues to grow in the U.S.market. However, there have been nosignificant new entrants over the past six months which perhaps suggests that the appetite of capital providers hasreached a plateau.

Domestic underwriters are widening the scope of their coverage to try andrecapture business being placed overseas.As a reaction to the popularity of StockThroughput policies, property insurersare seeking to include inland marine in their coverage along with import and export.

During the past 12 months the U.S. markethas been offering 50-60% reductions on selected accounts in an attempt to winthem back from overseas markets.

The Council of Insurance Agents andBrokers report that insurance premiumsdeclined by an average of 13.5% during the first quarter of 2008, following afourth quarter decline of 12% in 2007. The major broking houses offer no sign that the market cycle is ready to turn.

AsiaGeorge Street Singapore has become the home of Lloyd’s syndicates in Asia.Amlin is one of the most recent entrantsinto the Singapore cargo market with the following syndicates now activelywriting cargo in the region:

SYNDICATE SINGAPORE HONG KONG

WATKINS SYNDICATE X X

KILN MARINE SINGAPORE X –

SYNDICATE 1965 X –

CATLIN SYNDICATE X X

ALBA SYNDICATE X –

ASCOT UNDERWRITING X –

CHAUCER SINGAPORE X –

TALBOT ASIA X –

TRAVELLERS ASIA X –

AMLIN X –

CV STARR – X

6637_MMR_Inners_FINAL:Aviation Market Review Inners2 07/08/2008 09:22 Page 25

26 Willis Marine Market Review August 2008

So far 2008 has seen a continuation in the movement of personnel. Notably, the transfer of Lee Vanderson, whounderwrote the largest cargo book at Lloyd’s, to head up Reith Singapore,underlines that Syndicate’s commitment to Asia.

In 2007, 20-25% reductions in rates were commonplace, but obviously thissimply cannot continue indefinitely.Already 2008 has seen more moderatereductions of 10-15%, although bigger reductions remain available for the larger accounts.

Middle EastThe transfer of capacity to the Middle East is creating yet another regionalunderwriting hub.

Although still in the early stages ofgrowth, the marketplace is developing,unsurprisingly with a strong focus on oil and construction risks.

The market is still strongly regulated and brokers have only recently gained admission.

No particular country has so far emergedas the front runner and currently themarket is spread between Bahrain, Dubaiand Oman. The market is dominated byinsurance companies but the role ofLloyd’s is expanding. There is no reasonwhy we should not expect a repeat of the Asia experience.

EuropeThe larger European insurance carrierssuch as AXA, Allianz and XL have begun to centralise the underwriting ofinternational cargo business, either back to their European head offices or, in the case of Allianz to London.

Several of the U.K. insurers see potential for further growth in Europe, especially inlight of over-capacity in the home market.

RSA have commenced a strategy ofdeveloping marine cargo-specific

operations in Belgium, France, Germanyand the Netherlands and furtherexpansion is planned.

Starr Marine have employed SimonPlumridge from AIG to manage theirexpansion in Europe and already theyhave secured the services of SergeVanderstappen and Michael Zanetti as European managers.

From a rating perspective, larger Europeancarriers have become increasinglycompetitive and have won several globalaccounts from the London market.

The large composite companies still havethe advantage over Lloyd’s when it comes to packaging risks and offering truly global programs. This will no doubt changesoon given the competitive nature of themarket and the appetite of Lloyd’s for newsources of income.

LondonWith the growing strength of domesticmarkets and competition for internationalaccounts from both regional hubs and the continental market, London is goingthrough a period of dramatic change.

Insurers and brokers alike, are looking toposition themselves to meet the challengesof the rapidly changing marketplace, whilstmaintaining their budgeted expectations for growth and profitability.

London is increasingly moving away from the smaller transactional risks andfocusing on its strengths of globalexperience, expert knowledge on keyindustries such as automotive,construction, pharmaceutical, metals and oils and a focus on high risk andcapacity exposures.

Whilst the domestic and regional marketsare strong on transactional accounts, they still cannot match the depth ofexperience that London provides oncomplex and problematical accounts. The subscription market provides clientswith a large amount of capacity, with

6637_MMR_Inners_FINAL:Aviation Market Review Inners2 07/08/2008 09:34 Page 26

Willis Marine Market Review August 2008 27

underwriters sharing accounts thatinsurers would not be prepared to accepton a 100% basis.

However, London insurers realise theycan no longer sit at their boxes and waitfor accounts to be shown to them and are increasingly being pro-active indeveloping direct relationships with theassureds and working on a partnershiprather than transactional basis. Riskmanagement and loss prevention servicesare now offered by a large number ofinsurers and are seen as an integral part of the value-added product now being offered.

This drive to improve the service given toclients and the increasing competition togrow premium income has seen anotheryear of changes to the landscape of theLondon cargo market.

AIG have completed their takeover of Reith and whilst not officially announced,there are three new insurers looking to startcargo underwriting before the end of 2008.

The transfer of personnel betweenbrokers and underwriters continues at arapid pace, with perhaps the most notablemove being that of David Roe, previouslyhead of cargo at Marsh London, leaving to join Ascot following the transfer of Lee Vanderson to Singapore.

Other changes include Huw Daviesmoving from Marsh to O’Farrell, HelenSteadman moving from Marsh to Mitsui,Richard Golder from Amlin to Catlin, Tim Garrett from AIG to Beazely, AndrewThorp from AIG to CV Starr, Allan Brooksfrom CNA to Zurich, Johnathon Eatonfrom Aon to AIG.

In summary, there can be no better time for cargo owners to take advantage of thehigh capacity, the broad coverage and thecompetitive pricing.

Our team at Willis is well positioned to take full advantage of the opportunities onoffer in the global marketplace and has theexpertise to deliver innovative productsand solutions to our clients.

6637_MMR_Inners_FINAL:Aviation Market Review Inners2 07/08/2008 09:22 Page 27

6637_MMR_Inners_FINAL:Aviation Market Review Inners2 07/08/2008 09:22 Page 28

Willis Marine Market Review August 2008 29

CLAIMS

6637_MMR_Inners_FINAL:Aviation Market Review Inners2 07/08/2008 09:22 Page 29

30 Willis Marine Market Review August 2008

Recent case law has againhighlighted the importance of warranties, both to assureds and insurers. Our own claimsexpert outlines the issues anddevelopments concerningwarranties and the law thatsurrounds them in the following article:

Warranties: They do whatthey say on the tin!

In recent years there has been much debateabout the role of insurance warrantiesunder English and Scottish law. For manyyears, there has been wide consensuswithin the insurance community thatEnglish Insurance Law may be in need of reform and the impact of warranties is central to these proposals.

Warranties as originally conceived, undercommon law, were promises made by theinsured to insurers to guarantee that therisk had been accurately described to them.The use of warranties in Marine Insurancehas moved far from this original concept. A good example of this would be a premiumwarranty that requires premium to be paidon or before a certain date: this has noconnection to the risk underwritten.

The Marine Insurance Act 1906characterises a warranty as a conditionwhich must be exactly complied with,whether it be material to the risk or not.The remedy for a breach of warranty issevere and again defined within the 1906 Act as “…the insurer is dischargedfrom liability, as from the date of thebreach of warranty”.

It is imperative that a warranty iscompatible with the operation of thevessel and that the consequences of non-compliance are clearly understood by theassured. The breach does not have to bematerial to, or causative of, the loss. Two recent cases to pass through theEnglish courts highlight the pitfalls.

Firstly, G.E. Frankona Reinsurance Limited -v- CMM Trust No.1400 - “The Newfoundland Explorer” [2006]. The Claimant was a Yacht owner, whoseUSD 3 million yacht caught fire due to an overheating generator while safelymoored at a marina in Fort Lauderdale.The Owner was at home 15 miles away and the rest of the crew dismissed as theyacht was laid up. The marine policycontained an express warranty:“warranted fully crewed at all times”. The claim was denied by the insurers onthe basis that the warranty was breached.The courts held that the yacht owner was to keep at least one crew member on board the vessel 24 hours a day (barringone or two emergency situations that would allow the craft to be unmanned).

Secondly, Pratt v Aigaion InsuranceCompany SA (The “Resolute”) [March 2008].Pratt, the claimant, was a trawler owner, who returned from a day’s fishing to North Shields, U.K., safely moored,discharged her catch and the crew readiedthe vessel for the following day’s fishing. TheOwner/Master and crew then made thecraft secure and left to meet family orpartake in a well-earned drink. During theevening a fire was reported on the vessel,investigations concluded that it wascaused by a faulty deep fat fryer or fridge.The insurers declined the claim on thebasis of a breach of an express warranty:“warranted Owner and/or Owner’sexperienced Skipper on board and in chargeat all times and one experienced crewmember.” The claimants argued strongly,that it was obvious that the warranty wasdirected to periods of navigation and, ifapplied literally, would be absurd comparedto the accepted practice in the trawlerindustry as the Skipper and one other crewmember would have to permanently residein a crew cabin measuring 6ft by 9ft. The Court held that there was no ambiguityto the warranty, “on board…at all times”meant “at all times” 24 hours a day, 365 daysa year regardless of the impracticalities of the Owner/Skipper actually strictlycomplying with the warranty. Accordingly,the claim failed.

6637_MMR_Inners_FINAL:Aviation Market Review Inners2 07/08/2008 09:22 Page 30

Willis Marine Market Review August 2008 31

It can be seen from these two legalexamples above that English law may be in need of review. Most other jurisdictionshave accepted, to varying degrees, thatthere must be a clear link between thebreach of warranty and the cause of theloss for insurers to rely solely on a breachof warranty to deny liability.

In July 2007, The Law Commission ofEngland and Wales issued a consultationpaper that dealt with, amongst othermatters, warranties within consumerinsurance. The paper sought responsesfrom consumer groups, lawyers, brokersand insurers. At the end of May this year,the Commission published a summary of responses. These concluded that theCommission’s proposals had little effect on consumer insurance but would have asignificant effect on business insurance and particularly marine insurance,requiring the more extreme provisions ofthe Marine Insurance Act to be repealed.

It is now planned for the Law Commissionto produce a further consultation paper oncommercial/business insurance warrantyreform. These proposals are thereforeunlikely to come before Parliament for afurther three to four years.

A Classification Warranty is a morecommon express warranty on a policy ofmarine insurance; this requires a vessel tobe fully classed and class maintained duringthe entire policy period. Classification is acontinuous process and failure to meetsurvey dates or requirements will result in a vessel losing class status. There can oftenbe an innocent explanation for missing an inspection and the situation may bespeedily resolved. However, the delay insurvey may lead to a break in the continuityof the vessel’s class record enabling atechnical breach of the warranty. Insurerswould then be entitled to dischargethemselves of any future liability under the policy after the date of the breach. In these circumstances it is essential forinsurers to be advised immediately andobtain agreement from them that cover is continued.

Until the law is reformed, assureds shouldremain fully aware of the implied andexpress warranties in their policies,ensuring that they are clear, sensible,workable and relevant. The consequencesof non-compliance should be fullyunderstood and suitable processesemployed to ensure that insurance cover remains complete.

6637_MMR_Inners_FINAL:Aviation Market Review Inners2 07/08/2008 09:22 Page 31

REINSURANCE

6637_MMR_Inners_FINAL:Aviation Market Review Inners2 07/08/2008 09:22 Page 32

Willis Marine Market Review August 2008 33

Following the traumatic events of 2004 and 2005 in the Gulf of Mexico, Marine reinsurershave enjoyed two years without a major Marine-related multi-interest loss incident. For Marine catastrophereinsurers, riding on highpremiums inflated by paybackfor the hurricanes, 2006 and 2007 have been excellentperformers.

By contrast there has been an abundanceof small and medium-sized losses, whichhave affected reinsurers’ results to varyingdegrees, always depending on the level ofthe original insurer’s (i.e. the reassured’s)retention. Vessels are running to capacity,as are shipbuilding and shiprepair yards.Oil has never been more expensive,political situations and tensions are oftenunpredictable, and earthquake activity ismuch publicised in China, Japan, andIceland (and in Market Rasen in the U.K.!)These are all factors which are keepinginsurers occupied and emphasising theneed for insurance and reinsurance. The threat of a meaningful claim is everpresent, especially as recent claimsactivity has been bubbling just below the (reinsurance) surface.

This contrasting claims picture hasinevitably led to a range of expectationsand pressures. The reassureds have paid substantial increases in the pastfew years to recompense the large losses(sometimes in spite of having littleinvolvement in the losses themselves) and to satisfy reinsurers’ re-evaluation of the cost of catastrophe coverage. As profit margins are being squeezed bysmaller claims, reassureds are seekingimproved terms (in the form ofmeaningful premium/cost reductions).Their ambitions are often at odds withreinsurers’ approach: requests for hugelyenhanced information, broad applicationof modelling tools, pressure for internalcapital allocations, constant management,

supervision, and control, and Solvency IIare all creating a less sympathetic –perhaps somewhat more defensive –reinsurance market.

In general, at the beginning of 2008 therewere premium reductions of about 5-7.5%for the larger multi-class programmesand, 10-15% for specific, local, indigenousaccounts. These reductions were alwayssubject to past claims experience and tothe renewal information: there was littletolerance for a poorly performing lowerExcess of Loss layer, which was eroding a major proportion of a programme’sprofitability. Reinsurers are seeking asensible retention level, as well as pricing,to ensure that the insurer (reassured) is not merely passing all or most of theliability to reinsurers.

As an example, pre-set monetary budgets,set in the latter half of 2007, were in somecases so optimistic that retentions had to be increased several fold to ensure thatfinancial targets were met. The prevailingfocus on performance for all classes iscompelling Excess of Loss reinsurers todifferentiate their interests, and thereforetheir underwriting, from the needs of their clients, the insurers. Hence, we seeexcellent reinsurance results (in so far as Marine reinsurance results arediscernable within the accounts ofmultiline reinsurance companies), whilethe results of the Marine insurancebusiness are often marginal at best.

Retrocessional coverage (retro) continuesto be limited and expensive. Whereas retro may have once offered a tradingadvantage to its reinsuring clients, it is now purchased as a necessity, either forinternal management requirements or for external balance sheet, and hence ratingconsiderations. Likewise as the Energyreinsurance market softens, Gulf of Mexico coverage is being included to an ever greater degree – within Whole Account programmes. The number of Gulf of Mexico hurricane Energy specificprotections are reducing – whether writtenon an orthodox or parametric/finite basis or as a sidecar.

6637_MMR_Inners_FINAL:Aviation Market Review Inners2 07/08/2008 09:22 Page 33

34 Willis Marine Market Review August 2008

Reinsurance prices are not reducing in linewith the original business and the WholeAccount or Limited General markets havebecome more tolerant.

The core focus for insurers in 2008 is the management of attritional losses. There are many enquiries for low-levelprotection and there is a distinct dearth of sympathetic or innocent reinsurancecapacity. Rates and terms (specifically thelevel of annual aggregate deductibles) arebeing related to claims experience, riskexposure and current worldwide Marineconditions. A good example is Protectionand Indemnity coverage, which hascustomarily been well supported at low levels (as a true thermometer of a

genuinely wet Marine portfolio); the resultshave been indifferent in the recent past, asclaims activity has increased markedly. It is increasingly apparent that reinsurersare seeking to maintain profitability andresults are now a core focus at the expenseof some long-term relationships.

For 2009 reinsurance will continue toreact firmly to any deterioration incontract performance, any large loss and also to increased exposure (higherhull values and oil prices), but willcontinue, in the absence of a large Marine catastrophe loss, to come underpressure to reduce pricing. Reinsurers are certainly showing a firmer resolve and are likely to continue to do so.

6637_MMR_Inners_FINAL:Aviation Market Review Inners2 07/08/2008 09:23 Page 34

LETTERS FROM OVERSEASMarine is inherently a global business from both a shipping and a cargo perspective. As a result of this, we have Marine Associates based all over the world. Several of ourcolleagues have contributed with Letters from their Region, giving us a snapshot of the local markets and current trends.

6637_MMR_Inners_FINAL:Aviation Market Review Inners2 07/08/2008 09:23 Page 35

36 Willis Marine Market Review August 2008

Letter from New York

Well, another year has passed and it is moreof the same: rates very competitive, coveragebeing enhanced, new capacity entering themarket and everyone fighting over the samebusiness. All very positive for the assureds.

With rates so competitive one would havethought that it was not the right time fornew capacity to enter the market. We have,as advised in last year’s review, had newcapacity enter the market and ratesbecame soft as they fought to establishtheir positions. These carriers have donean excellent job of solidifying theirpositions and are now firmly established.

This year we have three new entries intoour marine market. The first is MaxSpecialty which is made up of a senior groupwho left the Firemen’s Fund and is headedup by Michael Miller. The second entry isValiant Insurance which is lead by JosephO’Connor and the third is Catlin InsuranceU.S. with Vincent Liotta at the helm.

These entries complement each other asthey are, at least in the initial stage,targeting different lines. Max Specialty islooking to the Inland Marine and OceanCargo placements, although they do havethe capabilities to write Hull, P&I andMarine Liabilities. Valiant Insurance isconcentrating on Hull, P&I and MarineLiabilities whereas they do have thecapability to write Ocean Cargo. CatlinInsurance U.S. is looking to write all lines of marine business, excluding bluewaterhull. Their aim is to target that businessthat stays in the U.S. and is not seen inLondon where Catlin is a major player in the marine market.

Major changes in management positions seeHarry Yerkes joining the American HullSyndicate as Chief Operating Officer, to takeover from Fred Robertie when he retireslater in the year. Raymond Stahl left Aceafter many years to join AIG Global Marineto start up their recreation group. JohnBarnwell has now been made the NationalCargo Manager at the Firemen’s Fund.

The year in general saw ocean cargo ratescontinuing to drop as competition forbusiness grew, with rates dropping by upto 50% for those accounts which had notbeen re-marketed in recent years. Ratesgenerally dropped 10-15% on top of themajor reductions of recent years.

The U.S. Marine Liability market continuesto remain stable. The first quarter of 2008saw the majority of primary and excesspolicies renewed at the expiring premiumswith rate reductions few and far between.The second quarter is starting to see somevery minor reductions (5% or less) onpremium accounts with clean loss records.The Marine Liability market tends to lagbehind other marine markets in terms ofrate fluctuations, due to the “long tail”nature of liability business.

Hull and Machinery rates vary withbluewater accounts renewing ‘as expiry’ or with minor reductions. Brown wateraccounts are seeing reductions in the rangeof 5-10%. However these percentages arediscarded when the renewal is subject to aserious remarketing exercise: the accountcan be considered as new business andunderwriters are aggressive when pricingthose specific accounts they have targeted.

We do not know what the rest of the yearwill bring, but we have recently seen theU.S. Marine Liability market be veryaggressive in taking an account which has been placed in the London marketfor several years.

6637_MMR_Inners_FINAL:Aviation Market Review Inners2 07/08/2008 09:23 Page 36

Willis Marine Market Review August 2008 37

Letter from Norway

We have the following active underwriterswriting international hull business.

– Norwegian Hull Club– Gard– Codan– Nemi– Gerling– Trygg Vesta– Swedish Club– Inter-hanover– Markel, Stockholm

Norwegian Hull Club is leading the chargein their push for increases on marine hullbusiness, and they have taken a tough line resulting in the loss of a number ofaccounts. We see ‘general increases’ from NHC in the region of 10-15% onaccounts with good statistics.

Gard has gained a number of new claimslead positions as a result of NHC’s firmstance on increases. Gard’s growth is wellfounded and they appear to be in a strongposition going forward. Unlike otherUnderwriters, Gard do not impose blanketgeneral increases though they are seekingrises. Instead, Gard examine the fleet’sindividual record before applying any increases.

Bluewater is struggling as it has beendowngraded. Reports suggest that theywill try to continue as an agency with anew carrier but this might be difficult.

Nemi has also encountered somedifficulties. The rating agencies areconcerned with the financial health of their ultimate parent company.

Codan has re-staffed their office in Bergenafter many of their key employees left for Vega insurance last year. They havebrought in Geir-Arne Heggeland fromNHC as their General Manager andGeirmund Sangedal from Royal Sun assenior underwriter. Codan remains animportant underwriter and they areconsidering further expansion.

Swedish Club has adopted a similarposition to NHC, imposing increases onhull business. They are not as active in2008 as they were last year and they are reviewing their strategies. They havejust appointed a new Managing Director,which may lead to a change inunderwriting policy.

Markel has opened an office in Stockholmwith well known people such as StaffanSahlin and Ove Staaf heading up the operation.

Vega is still not up and running althoughthey hope to be operational by September.However, with the current difficulties inthe capital markets, they may struggle to reach their target of USD 120 million.Already they have lost three employees,and more may follow if they are notoperational soon.

In conclusion, the Scandinavian marinemarket continues to flourish, albeit with a determination to raise premiumssufficiently to meet increased claims.

6637_MMR_Inners_FINAL:Aviation Market Review Inners2 07/08/2008 09:23 Page 37

38 Willis Marine Market Review August 2008

Letter from Singapore

Tiger Tiger Burning Bright -View from a Topical IsleLast year’s letter from Singapore focused on the steady stream of international interestand subsequent establishment of new marineventures: from underwriters to brokers andP&I clubs to adjusters. The concern from the‘old school’ underwriting fraternity here, thatthe new influx of ‘kids’ would drive the ratesdown, has now largely subsided. It happenedand it was inevitable but it has dramaticallyimproved the responsiveness and servicelevels of most underwriters.

There is an increasing appetite to leadbusiness here. This was dramatically andvery publically demonstrated when ACRtook the lead from Gard on the massiveEvergreen account. Also, it is reflected inthe movement of key personnel: severalmain players have been transferred, oftenfrom Lloyd’s – enabling more importantunderwriting decisions to be made here.

So, now we are on the map and the recentTradewinds Marine Risk Forum in Mayattracted a global mix of speakers. Strangelynoticeable was the distinct lack of Lloyd’sAsia underwriting representation, especiallygiven their appetite for marine business.London underwriters were well represented.Delegates from Brit and RSA eloquentlyunveiled a series of concerning statistics,challenging the current deductible andpricing levels, and the lack of qualified crew.The consensus was clear: if underwriterscannot force a change, they will becomevictims of their own policies.

However, one particular broker (strugglingeither with the heat or the local Tiger Beer)claimed despite his client’s atrocious figures he had successfully managed tonegotiate a reduction that he openlydescribed as “so ridiculous” that it wasclearly “underwriting suicide” and heseemed genuinely perplexed as to what was going on. Could one argue brokers aresimply becoming too good at driving therates down or has underwriters’ hunger beento the detriment of their technical rating?

The continuing ‘high’ throughout theshipping industry is obviously boostingoverall world tonnage but even though the premium base is increasing, SimonStonehouse (of Brit Insurance andChairman of the London market’s Joint HullCommittee) pointed out to the Tradewindsdelegates that current insurance rates are35% of what they were in 1994.

So it would seem that for now we doremain in a buyers’ market. This wasespecially pleasing for the local shippingcommunity who were represented byMISC, NOL and PCL to name a few.

Simon Wilson, Managing Director ofLloyd’s Asia, is pleased with the growthof the market ‘hub’ here. The market hasgrown from three to fifteen syndicates inthe last 18 months but Marine still onlyrepresents a small share of the overallpremium base: 10% for cargo and 3% forhull. Wilson predicts there will be fewernew entrants into this market – only onefurther syndicate is currently in thepipeline for 2008/9. This trend clearlyreflects the soft market and is likely tocontinue throughout 2009. Last year,Lloyd’s Asia’s gross received premiumstopped USD 126 million. It is still too earlyto tell but 2007 figures are looking veryhealthy at present – around 10% loss ratio.

One of Wilson’s aims this year has been topromote the Lloyd’s brand and to attract a quality skill base into the market. We saw a successful road show in Kuala Lumpurrecently which attracted all the majorinsurance companies and brokers. Manysyndicates were represented with thepurpose not only to promote the syndicatesbut also the Lloyd’s Asia market as a whole.

Working with GIS, insurance companies,and brokers, Lloyd’s Asia is heavilypromoting local graduates into theindustry with the hope of creating futurefoundations. Although Lloyd’s syndicateshave been criticised in the past for raisinglocal salaries, this initiative will hopefullymake insurance a more attractive careerproposition in the future.

6637_MMR_Inners_FINAL:Aviation Market Review Inners2 07/08/2008 09:23 Page 38

Willis Marine Market Review August 2008 39

Wilson feels the key to success in thismarket will be in its ability to mature intoa fully independent hub. In general,Singapore is not particularly claimsefficient. Therefore, claims leadership and efficient servicing is key to themarket’s success. With only two of thecurrent syndicates having dedicatedmarine claims directors, there is clearlyroom for improvement.

As mentioned above, the biggest impact on the effectiveness of Lloyd’s Asia, seemsto have been the arrival of genuine marketleaders who have the ability and authorityto lead business. The arrival of establishednames such as Chris Wildee (Chaucer),Mark Trevitt (Travelers) and recently Lee Vanderson (Ascot) are likely to furtherenhance the Asia position.

Trevitt is the first dedicated MarineLiability underwriter at Lloyds and recentlyAIG appointed Catherine Mangan as VicePresident for Regional Marine Liability.Trevitt feels that while other classes haveestablished themselves, this is largely as aresult of a similar build up on the brokingside. He believes that the marine liabilitiesmarket has the biggest potential in theregion with an estimated USD 750 million of Asia Pacific liability business available and currently very little is written here. By 2013 China will have 6 of the 10 largestports in the world. Closer to home,Malaysia’s increasing port infrastructurewill give Singapore a run for its money.

The players outside Lloyd’s who havetraditionally written marine liabilitieshere such as AIG, Swiss Re, Munich Re and QBE are now joined by the likes ofWatkins, AMS, Catlin, Ascot and Talbotwho are predominantly writing asfollowing markets.

Currently the market capacity isestimated at USD 150 million locally withnet loss ratios at about 45%. While Trevittfeels there is regional competition fromthe likes of the TT Club in Hong Kong and ACE in Australia, the success of themarkets here will depend on the support

and build up of dedicated regional brokersspecialising in the sector.

Last year’s feeling was that the cargomarket could not fall any lower. Everincreasing demand for higher limits havecontinued to force rates down further.

Lee Vanderson of Ascot is bullish in hisattitude that Ascot will increase theircargo book here by a further 30% in 2008,despite the current position in the cycle.Cargo represents 30% of his overall bookhere and he is keen to expand othermarine lines. Particularly sceptical thatIndian oil cargoes will remain at theircurrent levels, he sees major opportunitiesin the Chinese market. Vandersonpredicts that rates are going to get thinner,even though there is little meat on thebone to sustain a claim, let alone a pack of hungry underwriters it needs to feed.

The General Insurance Association’s (GIA)total premium income statistics for cargohave remained worryingly stagnant for the last four years. The vastly increasedthroughput, oil, steel and other commodityprices have in part hidden these percentagereductions. It certainly seems that buyerswill continue to gain from attractive rates in2009, albeit lower in percentage terms thanthe last 12 months. Statistically cargo figuresprove it is still a profitable account given agross loss ratio here of only 25% for 2007.

Marine construction rates remaincompetitive although there have beenseveral losses in the region. There wasnotably a spate of launch problems inVietnam but most of these losses have beenpicked up in the treaty markets and hadlittle effect on facultative rates. Probablywe are at the bottom of the cycle but we will have to wait for a major loss beforeyards need to worry about increases.

The Hull and Machinery account, aspredicted last year, has continued tosoften. A few 25% reductions at the start of the year did not become the norm.On average, Jonathan Ranger of WatkinsSyndicate says, he has seen rates slide

6637_MMR_Inners_FINAL:Aviation Market Review Inners2 07/08/2008 09:23 Page 39

40 Willis Marine Market Review August 2008

between 10% and 12.5% in 2008. Yet, henotes that over June and July the trendhas seen signs of changing, where severaloffers for regional facultative RI have gone unsupported.

GIA statistics for hull and machinery alsoshow premiums down by 12.5% and grossloss ratios for 2007 at 43%, so on a netbasis the class is marginal. The clear pushfrom some European markets, especiallyNorway, to increase rates is likely tospread East eventually. However, whileloss levels remain low and capacity isstable, our advice would be to negotiatehard now and lock in as far as possiblebecause a hardening hull market in Asia is almost within sight.

A note from Hong Kong

The insurance market in Asia continues to grow in line with the ever increasingvolume of trade coupled with the thirst of China, particularly in the shipbuildingsector. Arguably Hong Kong has missedout on this growth as Lloyd’s hubs haveestablished themselves in Singapore andmore recently Shanghai. However, HongKong remains well positioned to servicethe Pearl River Delta in Southern China,Taiwan and South Korea.

The conservative view is that Singapore and Shanghai will remain the epicentre of the Asian insurance market. It is foolishhowever to underestimate the ‘thirst of the Dragon’ and to this end global insurershave so far continued to feel the need tohave a presence in Hong Kong. Not onlybecause this is often where the riskoriginates but also because manyshipowners like to correspond with localinsurers to provide a local claims service.

Due to this demand, in 2008 the marketcapacity in Hong Kong has increased. Asia Insurance restarted their bluewaterhull underwriting cautiously andconservatively. Starr Marine and ACR(Asian Capital Reinsurance) have set upoffices in Hong Kong – expanding theirmarketing activities.

Following the success of its operation in Singapore, Catlin has also spread theirwings and has opened in Hong Kong.Other Lloyd’s vehicles such as Kiln havefollowed. Ming An continue to have astrong presence but only in facultativereinsurance. Axa and Groupama havemuch more autonomy and unlike someother underwriters they are not required to refer risks to their parent companies.

Even though there has been significantexpansion in Hong Kong, obviously the more complex and high capacityprogrammes will still be spread globallywith the more established markets leading such placements.

Although the market capacity hasincreased there has been a hardening of the market with Swiss Re, Groupama and Swedish Hull Club all restricting the business they write, and chargingincreased rates.