Marine Harvest Seafood Investor Forum London 19 November 2013.

22

Marine Harvest Seafood Investor Forum London 19 November 2013 Click icon to add picture

-

Upload

kathryn-page -

Category

Documents

-

view

214 -

download

0

Transcript of Marine Harvest Seafood Investor Forum London 19 November 2013.

Marine HarvestSeafood Investor ForumLondon 19 November 2013

Click icon to add picture

Implied protein consumption driven by population growth only

Sources: FAO (2009); FAOstat Food Balance Sheets, United Nations population data; World Population Prospects: the 2012 Revision

Assumption: Constant consumption of protein per capita

3

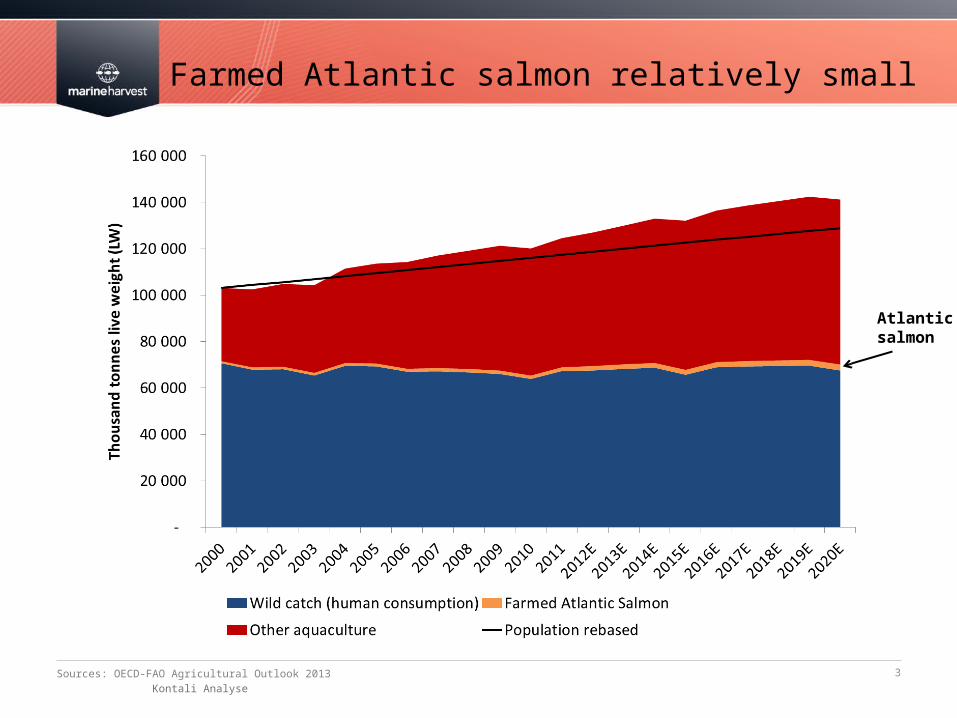

Farmed Atlantic salmon relatively small

Sources: OECD-FAO Agricultural Outlook 2013

Kontali Analyse

Atlantic salmon

4

Large opportunities within aquaculture species

Source: Kontali Analyse

5

Examples of protein co’s and area of potential

6

A unique nutritional package

Proteins:

High quality, easy digestable

proteins

Omega-3:

High content of Omega-3 fatty

acids

Vitamins:

Rich in A, D og B12 vitamins

Mineral:

High content of iodine & selen,

taurin og sterols

7

Farmed salmon - Highly efficient use of resources

8

Value CAGR of 8% - Volume CAGR of 6%

9

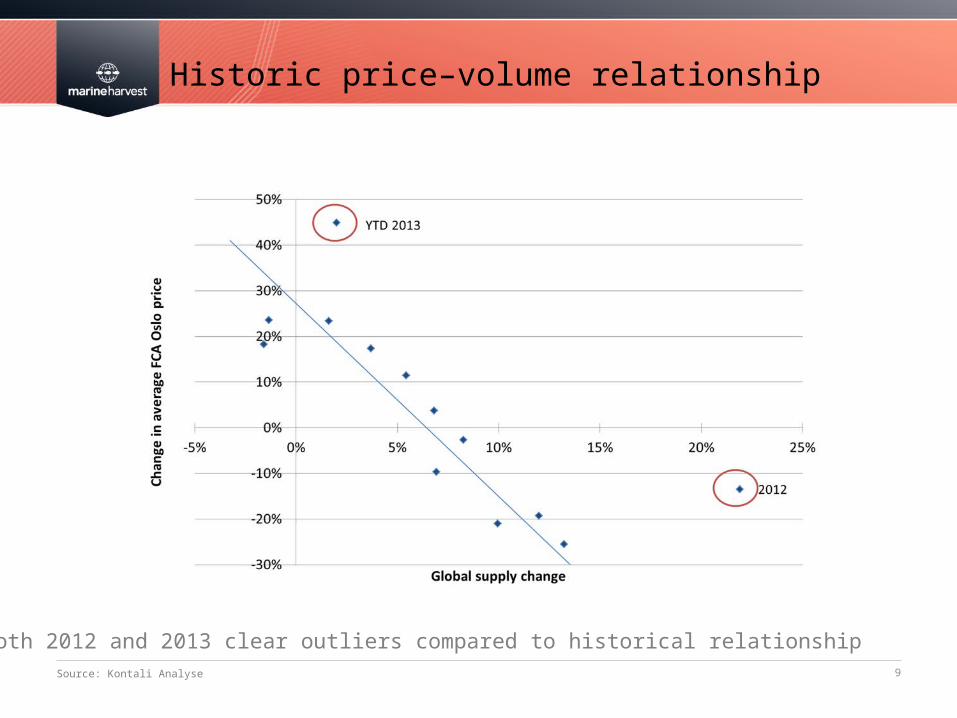

Historic price–volume relationship

Source: Kontali Analyse

Both 2012 and 2013 clear outliers compared to historical relationship

10

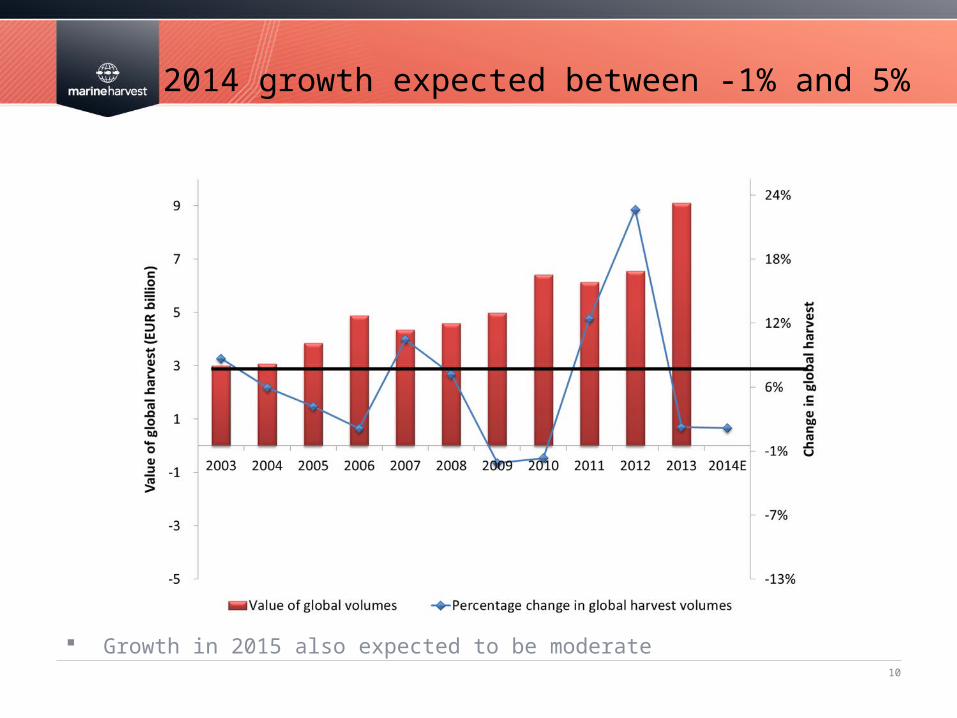

2014 growth expected between -1% and 5%

Growth in 2015 also expected to be moderate

11

Tough biological conditions in Chile….

Weighted average EBIT/kg for selected listed companies in Chile and Rest of World

12

…leads to strong cost increases…

Weighted average EBIT/kg for selected listed companies in Chile

13Source: Sernapesca

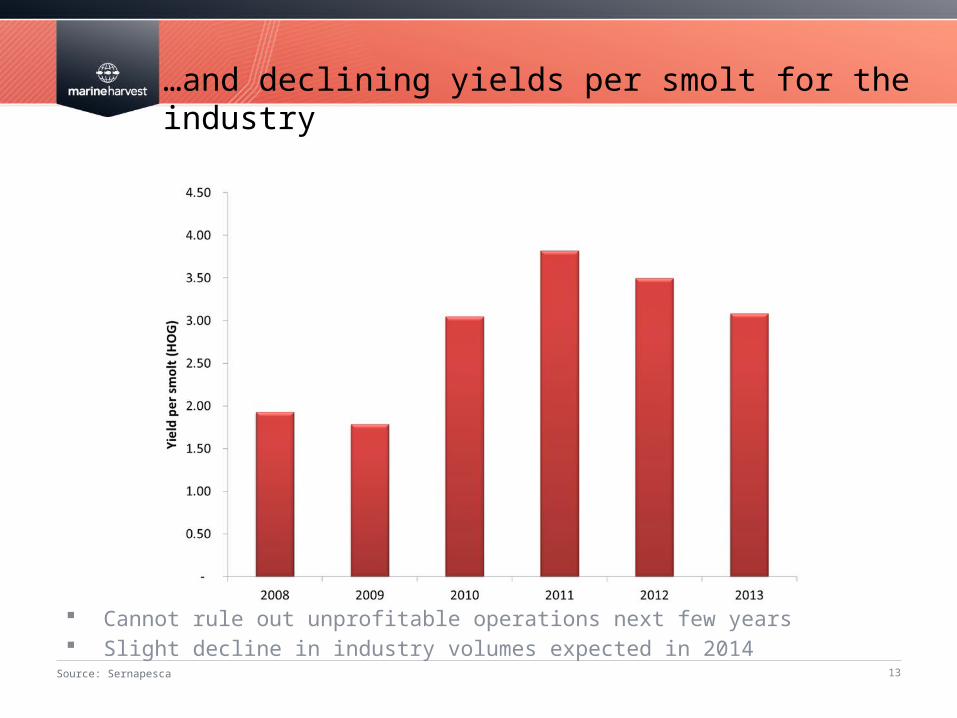

…and declining yields per smolt for the industry

Cannot rule out unprofitable operations next few years Slight decline in industry volumes expected in 2014

14

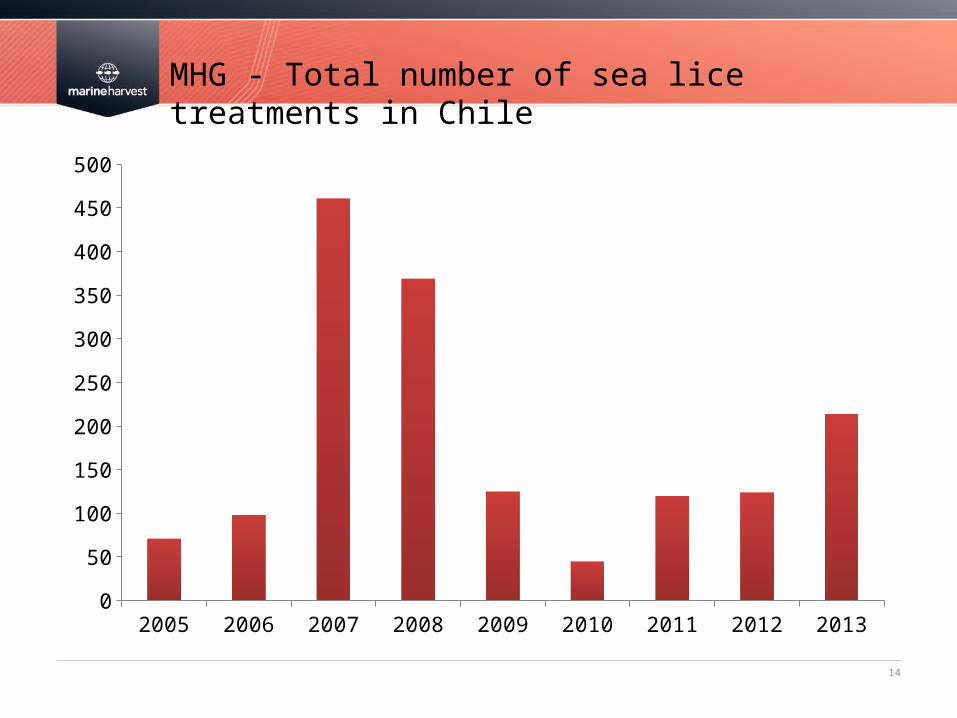

MHG - Total number of sea lice treatments in Chile

2005 2006 2007 2008 2009 2010 2011 2012 20130

50

100

150

200

250

300

350

400

450

500

Initial signals implies more liberal licensing regime Introduction of average Maximum Allowed Biomass constraints Assessment of current licensing system in general

This may lead to increased biological risk and reduced sustainability

Marine Harvest perceives this as a threat due to the industry’s dependency of a well regulated and sustainable framework

Marine Harvest’s recommendation: Continuation of current system with maximum allowed biomass Predictable annual capacity increase of 3-5% for ten years if deemed sustainable Aquaculture Stewardship Council (ASC) certification should be encouraged Establishment of Aquaculture Directorate to secure uniform approach Proceeds from increased capacity directed to host communities

Expectations for new Norwegian government

15

MHG – Leading position across the value chain

16

Feed Farming Sales/VAP

220 thousand tonnes vs. global production of ~2.6m

Marine Harvest business areas

New #1 #1

405 thousand tonnes vs. global production of c.1.85m (22%)

Global sales network

Leading position in VAP

Focus areas:Successful construction and implementation by July 2014

Acquisitive growth in Norway and Chile

Integration of Morpol

Restructuring programme in VAP

Organic growth in VAP

Position:

17

Fish feed project proceeding according to plan

220 thousand tonnes capacity – 60% of MHG requirement in Norway ~NOK 800m investment - Completion July 2014

18

CanadaVolume: 28 000

ChileVolume: 56 000

Faroe IslandsVolume: 9 000

ScotlandVolume: 50 000

IrelandVolume: 8 000

NorwayRegion NorthVolume: 62 000

NorwayRegion MidVolume: 59 000

NorwayRegion WestVolume: 77 000

NorwayRegion SouthVolume: 56 000

Marine Harvest farming regions

19

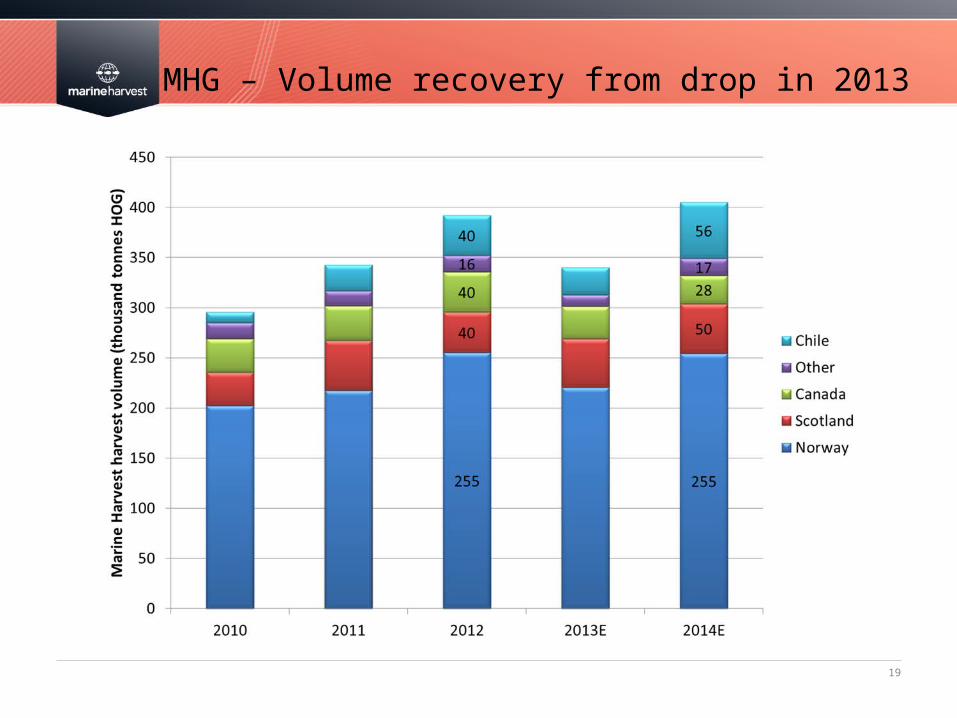

MHG – Volume recovery from drop in 2013

Marine Harvest sales & marketing structure

20

Europe, Sales & Marketing:• VAP Processing: 60,000MT

finished product, turnover 4,5BN NOK (VAP)

• VAP Production: France, Belgium, Holland, Poland, Czech Rep

• 2500FTE• Sales to retail, food service

and industry• Sales office: France, Belgium,

Spain, Italy, Czech Rep, Norway, Scotland and Ireland

Asia, Sales & Marketing:• Sales 1,1BN NOK. 25,000MT

finished products• VAP Processing: Tokyo &

Shanghai• 115FTE• Sales Office in: Japan, China,

Korea, Taiwan, Thailand and Singapore

America, Sales & Marketing:• VAP Processing: 13,400MT

finished product, turnover 1,0BN NOK

• VAP Processing: USA & Chile• Sales to retail, food service

and industry• 485FTE• Sales Office in: Miami, LA and

Puerto Montt (Chile)

Note: Figures in Europe excluding Morpol

21

Morpol – Competition clearance obtained

Major step in becoming a leading integrated protein player The leading secondary processing entity in Europe Complementary market position to Marine Harvest

~30 thousand tonnes HOG farming assets ~18 thousand tonnes in Orkneys and Shetland to be divested ~12 thousand tonnes to be integrated Norway and Scotland Location in Northern Norway where MHG is not currently present Well positioned for further licences in this region in 2013 licencing round

About 4,000 employees

22

Outlook

Strong market poses attractive 2014 net cash flow opportunity Forward prices of NOK 38 per kg in 2014 and 35 in 2015 Significantly reduced level of investment

Strategic focus areas Successful development of green-field feed capacity Acquisitions in Norway and Chile Integration of Morpol

Expected impact from the higher than normal investments in 2013 65 000 tonnes increase in 2014 harvest volumes Significant feed capacity in Norway from 2H 2014