Marijuana: Clearing the Smoke - CPCU Society · 2015-09-30 · – Requires very little water –...

90

-

Upload

truonghanh -

Category

Documents

-

view

214 -

download

0

Transcript of Marijuana: Clearing the Smoke - CPCU Society · 2015-09-30 · – Requires very little water –...

Marijuana: Clearing the Smoke Robert S. May Kilmer, Voorhees & Laurick, P.C.

Brenda Wells, PhD, CPCU, AAI East Carolina University/Risk Education Strategies

Theresa Young, MBA, CPCU, ARC, ARe CSAA Insurance Group

“Marijuana will never be taken seriously as long as you put up pictures of stoners in your presentation.” —Anonymous

HISTORY OF MARIJUANA USE AND SOCIAL ACCEPTABILITY

•One acre of hemp – As much fiber as two to three acres of cotton – Produces as much paper as three to four acres of trees

•Fibers are stronger and softer than cotton

•Easily and quickly grown – Frost-tolerant – Requires very little water – Grows in all 50 states – Ready to harvest in 120 days

Known Benefits of Hemp

•Seeds produce a protein similar to soy protein. – Not intoxicating – More nutritious

•Hemp seed oil can be used to produce nontoxic diesel fuel, paint, varnish, detergent, ink and lubricating oil.

•Cheap, easy source for ethanol production.

•Woody inner core can be used in housing production.

Known Benefits of Hemp

•Used as medicine in 2000 BC

•“Found a large stash of cultivated cannabis belonging to a shaman of the Gushi people in the Gobi desert, dating from 2700 BC”

How Long Have We Used It?

Thomas C. Slater Compassion Center, “History of Medicinal Uses of Cannabis,” www.slatercenter.com/about-cannabis/about-history#.

•Shiva is said to have brought cannabis to India. – Shiva is also known as the Lord of Bhang. – Bhang is a socially important liquid refreshment made with cannabis,

spices and milk.

B(H)ANG!

•Farmers in Virginia were required to grow hemp!

•Guess who? – Diaries show he grew hemp for 30 years. – Especially interested in medicinal use of marijuana. – Diary entries also show he grew marijuana with a high THC content.

1700s

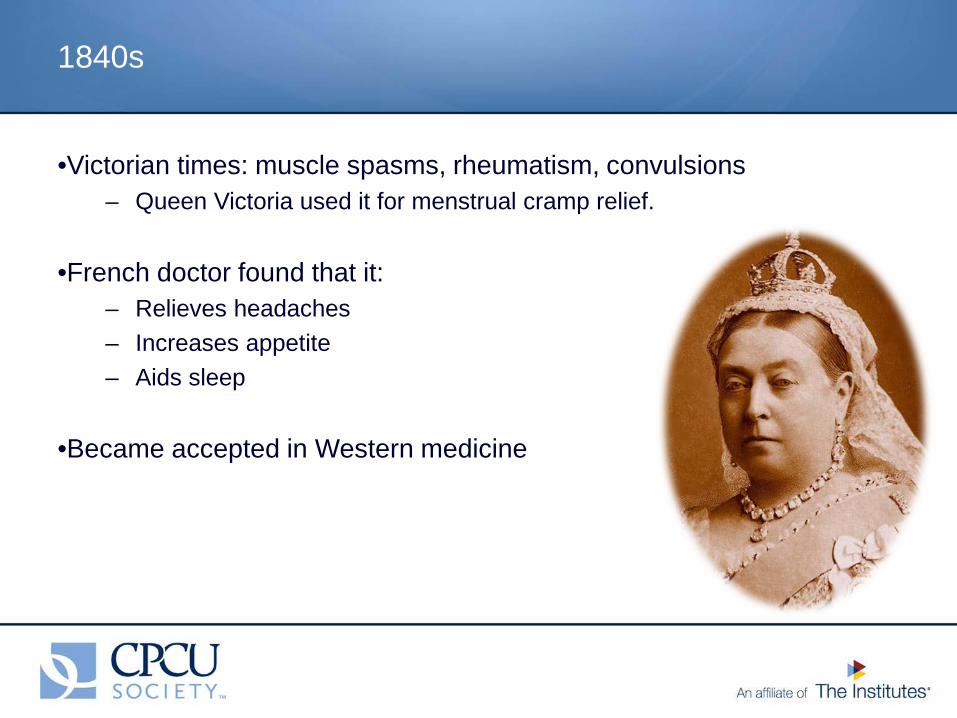

•Victorian times: muscle spasms, rheumatism, convulsions – Queen Victoria used it for menstrual cramp relief.

•French doctor found that it:

– Relieves headaches – Increases appetite – Aids sleep

•Became accepted in Western medicine

1840s

•Marijuana put in United States Pharmacopeial

•Treatment for: – Neuralgia – Tetanus – Typhus – Cholera – Rabies – Dysentery – Alcoholism – Opiate addiction – Anthrax

1850

– Leprosy – Incontinence – Gout – Convulsive disorders – Tonsillitis – Insanity – Excessive menstrual bleeding – Uterine bleeding – Many others

MARIJUANA ILLEGALIZATION

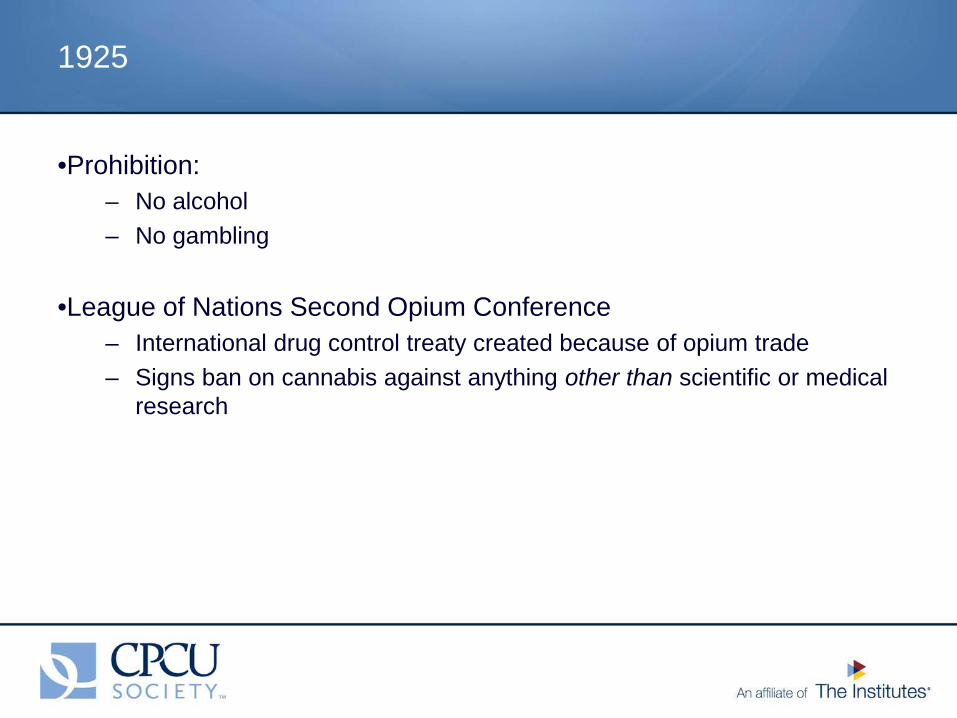

•Prohibition: – No alcohol – No gambling

•League of Nations Second Opium Conference

– International drug control treaty created because of opium trade – Signs ban on cannabis against anything other than scientific or medical

research

1925

•Aspirin and other analgesics are supplanting cannabis.

•All states outlaw it for anything other than a prescribed medical purpose.

1936

1936

•Cannabis is made illegal in the U.S. via the Marijuana Tax Act. – Introduced by Rep. Robert L. Doughton of North Carolina – Opposed by the American Medical Association

•Who was so antihemp? Speculation suggests….

1937

Paper Timber

William Randolph Hearst

DuPont Family

Nylon

Invested in DuPont

Andrew Mellon

•In the early 1900s, the western states developed significant tensions regarding the influx of Mexicans. •The depression came and increased tensions as jobs and welfare resources became scarce. •One of the differences seized upon during this time was the fact that many Mexicans smoked marijuana and had brought the plant with them.

Racial Prejudice: Mexicans

•Newspapers in 1934 editorialized:

“Marijuana influences Negroes to look at white people in the eye, step on white men’s shadows and look at a white woman twice.”

Racial Prejudice: African Americans

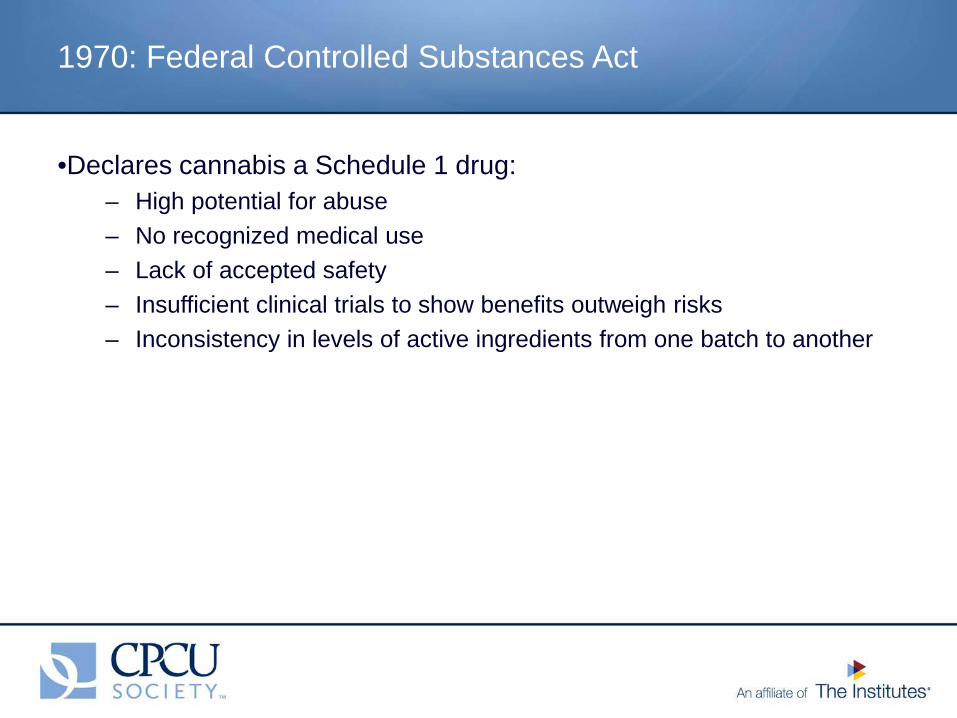

•Declares cannabis a Schedule 1 drug: – High potential for abuse – No recognized medical use – Lack of accepted safety – Insufficient clinical trials to show benefits outweigh risks – Inconsistency in levels of active ingredients from one batch to another

1970: Federal Controlled Substances Act

•Heroin

•LSD

•Ecstasy

•Peyote

What Else is Schedule I?

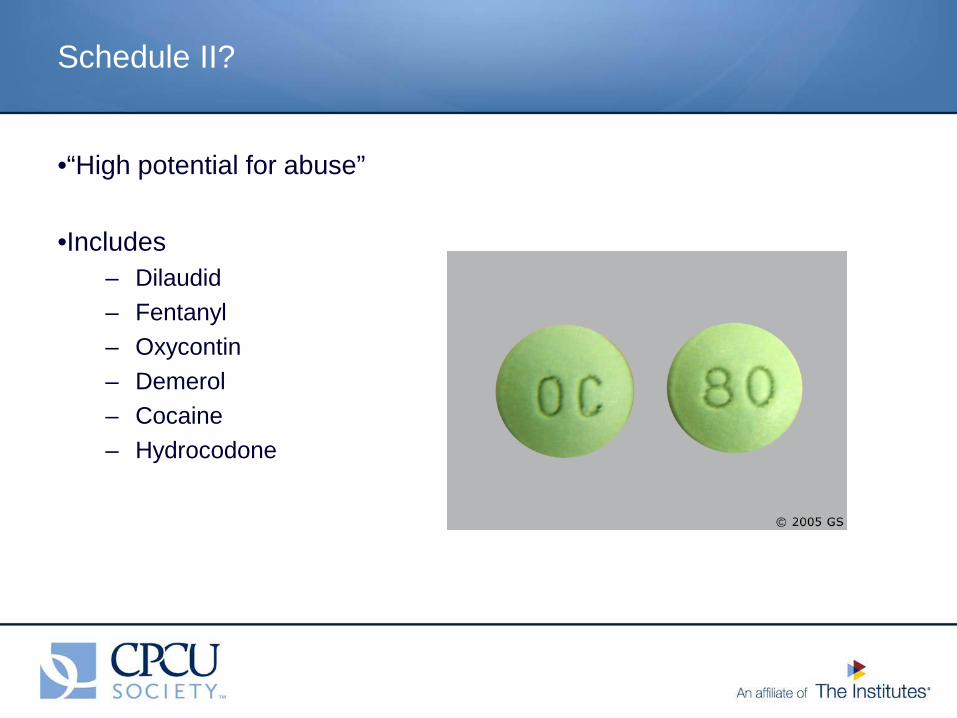

•“High potential for abuse”

•Includes – Dilaudid – Fentanyl – Oxycontin – Demerol – Cocaine – Hydrocodone

Schedule II?

•Less potential for abuse than Schedules I and II

•Includes – Testosterone – Cough syrup with synthetic codeine

Schedule III?

•Less potential for abuse than Schedule III

•Includes – Ativan – Phentermine – Ambien

Schedule IV?

•Less potential for abuse than Schedule IV

•Includes – Lomotil – Lyrica – Phenergan

Schedule V?

ATTEMPTS TO RELEGALIZE

•1972: petition submitted to what is now the DEA to reschedule marijuana to Schedule II, enabling legal physician prescription.

– Court battles ensue for 22 years. – 1994, U.S. Court of Appeals upholds DEA’s decision not to reschedule.

•1995: second petition filed to reschedule it.

•1997: NEJM publishes editorial calling for rescheduling.

Let’s Reschedule

•2003: Canadian HIV-patient Jari Dvorak becomes the first patient to receive government-grown marijuana.

– In response to an Ontario court order for the Canadian government to make a legal supply of marijuana available to authorized patients.

– How it works • Qualified patients are approved through government health care

system (Health Canada). • Marijuana is distributed through the patients' physicians.

In the HIGH-er Latitudes

•Alaska (1998) •Arizona (2010) •California (1996) •Colorado (2000) •Connecticut (2012) •D.C. (2011) •Delaware (2011) •Guam (2014) •Hawaii (2000) •Illinois (2013) •Maine (1999) •Maryland (2014) •Massachusetts (2012)

Michigan (2008) Minnesota (2014) Montana (2004) Nevada (2000) New Hampshire (2013) New Jersey (2010) New Mexico (2007) New York (2014) Oregon (1996) Rhode Island (2006) Vermont (2007) Washington (1998)

Source: http://medicalmarijuana.procon.org/view.resource.php?resourceID=000881

Today, These States/Jurisdictions Allow Medical Marijuana

Legalized Marijuana

Legislation to Legalize Medical Marijuana

http://medicalmarijuana.procon.org/view.resource.php?resourceID=002481

•Pending in 2015: – Pennsylvania

•Failed in 2015:

– Iowa – Alabama – Florida – Georgia – Indiana – Kansas – Kentucky – Mississippi

– Missouri – Nebraska – North Carolina – North Dakota – South Carolina – Tennessee – Texas – Utah – West Virginia

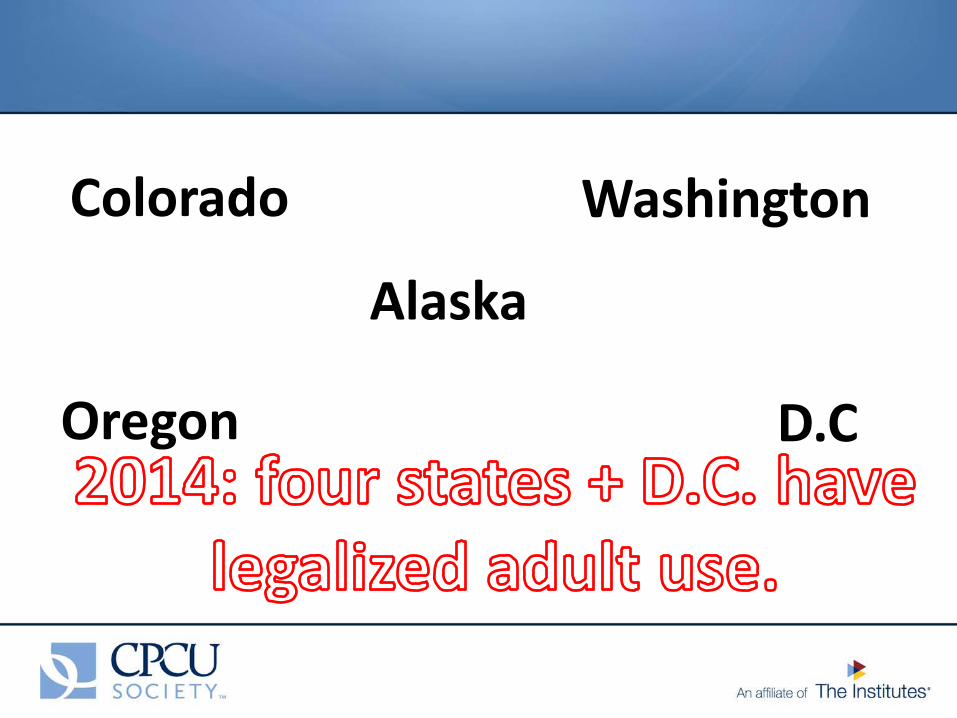

Colorado Washington

Oregon D.C.

Alaska

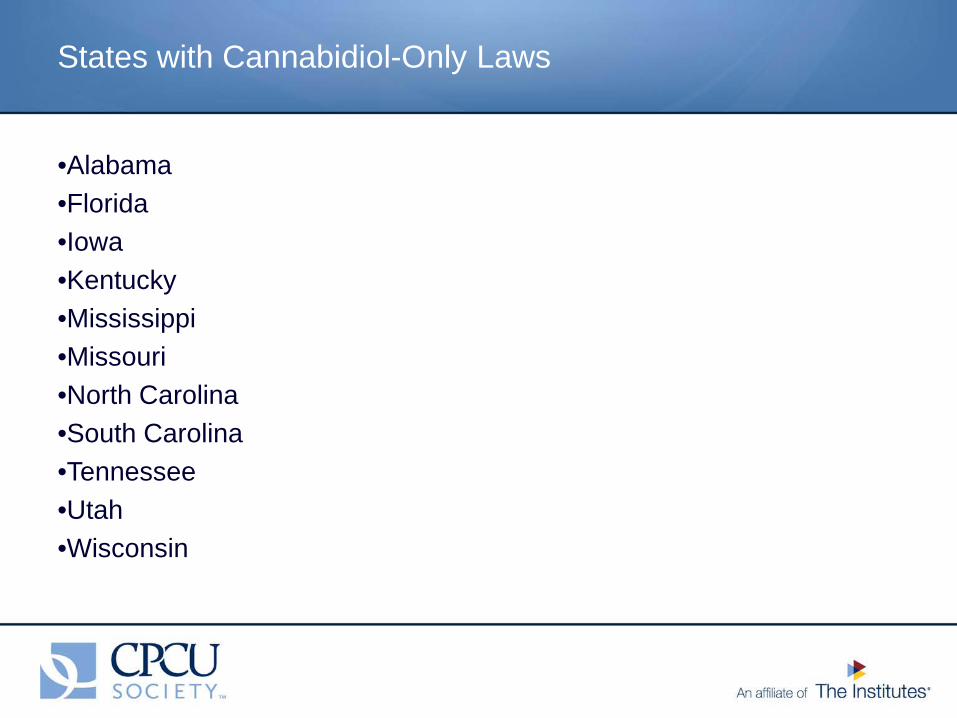

•Alabama •Florida •Iowa •Kentucky •Mississippi •Missouri •North Carolina •South Carolina •Tennessee •Utah •Wisconsin

States with Cannabidiol-Only Laws

•Rhode Island •New Hampshire •Vermont •Maryland •Hawaii •Maine •Missouri •Massachusetts •Nevada •Arizona •California •Delaware

Predicted to Legalize Adult Use Within Five Years

Source: “The State of Legal Marijuana Markets, 2nd Edition,” published by ArcView.

Adult Use Legislation

Public Opinion Regarding Legalization: 1969

“The State of Legal Marijuana Markets, 2nd Edition,” ArcView

Approve

Do not approve

Public Opinion Regarding Legalization: 2015

Legal Illegal

Other

Pew Research

•63 percent of millennials support legalization.

•54 percent of generation Xers support legalization.

•50 percent of baby boomers support legalization.

•27 percent of the silent generation (age 69 to 86) support legalization.

•69 percent of Americans view alcohol as more harmful than cannabis.

Source: The State of Legal Marijuana Markets – 3rd Edition - Arcview

Pew Research

•2011: Canadian judge required auto insurer to pay for greenhouse, soil and plants for man injured in car accident

(Source: Jones, 2011)

A Favorable International Climate

•Obama administration instructs federal prosecutors not to target medical marijuana dispensaries/users in compliance with their respective state laws.

(Source: Barrett, 2009)

Federal Climate 2009

"It would not make sense for us to see a top priority as going after recreational users in states that have determined that it's legal.”

–President Barack Obama

Federal Climate 2014

What Happens Now?

Proh

ibiti

ons &

W

hole

sale

Cos

t

Cons

umpt

ion

Colorado saw retail prices drop 30% over

two years.

$0

$2

$4

$6

$8

$10

$12

2013 2014 2019

Legal Marijuana Market Size ($ Billions)

$10.2

$1.53 $2.7

Legal Marijuana Market

•Multistate licensing by national brands – Branded companies with efficient cost of goods from scale economies

will sell cannabis products in every state. – Today, no true national cannabis companies exist because:

• Individual states require business operators to be state residents. • Interstate commerce in actual cannabis is illegal. • States have unique regulatory environments.

Predictions

•Alternative delivery systems – Viewed as

• Healthier compared with smoking • Offer variable dosage levels to meet patient needs

– Options include • Edibles (candies, chocolates, cookies, brownies) • Vaporization • Tablets • Topicals (balms, oils, lotions, etc., which are nonpsychoactive) • Extractions and concentrates

Predictions

•Growth of ancillary businesses (which are lower risk and not limited by interstate commerce restrictions)

– Real estate providers – Testing labs – Consulting services – Investment firms – Media companies – Technology applications – Banking services – Insurance services

Predictions

•Will Obama order the attorney general to reschedule marijuana?

•Who will win the 2016 presidential election? – 39% of Republicans support legalization. – 63% of Democrats support legalization. – 58% of Independents support legalization.

Two Big What If’s

EMERGING RISKS

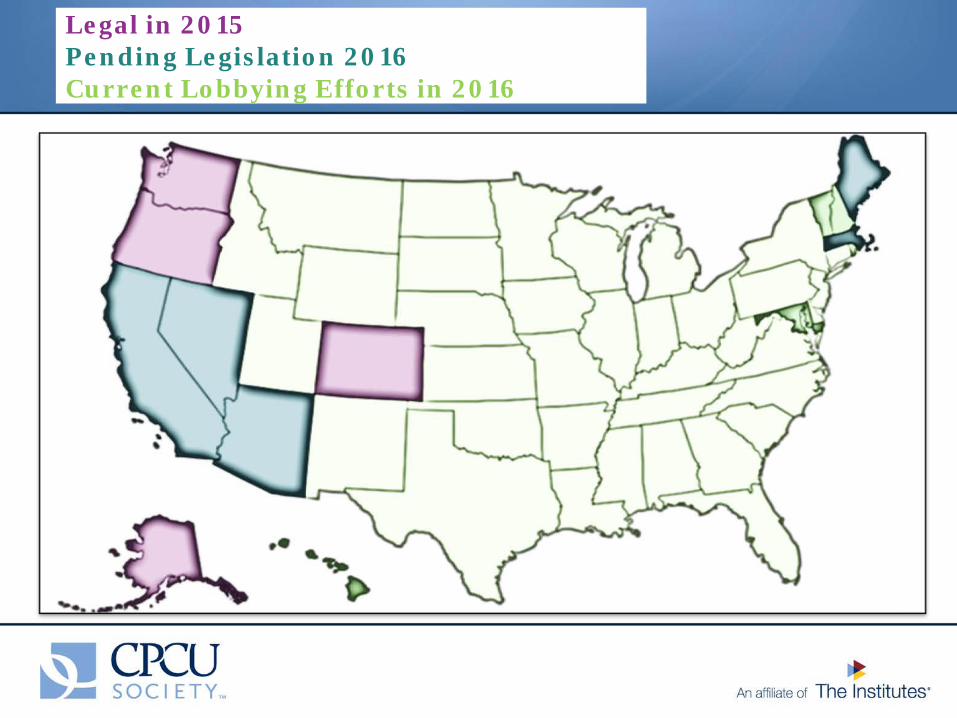

Legal in 2015 Pending Legislation 2016 Current Lobbying Efforts in 2016

Price of Marijuana Per Ounce

McCarran Ferguson Act: • Regulation of insurance is left to the individual states

• Insurers may still deny a claim in reliance on federal illegality—

conflict in laws

Insurance Regulation

• Tracy v. USAA Casualty Insurance Company (2012 WL 928186 U.S. Dist. HI)

– Tracy submitted a claim to USAA for the theft of medical marijuana.

– Court found that Tracy had an insurable interest up to the legal limit of medical marijuana.

– Insurer has no obligation to pay for stolen marijuana plants because the use of marijuana is still illegal under the Federal Controlled Substances Act (even though the policy provided coverage for theft of “trees, shrubs and other plants on the premise”).

– Courts may decline to enforce a contract that is illegal or contrary to public policy (applies where enforcement of the contract would violate federal law). Contract to insure an illegal item made the contract illegal and unenforceable.

Medical Marijuana Claims

RCW 48.18.040: • (1) No contract of insurance on property or of any interest therein

or arising therefrom shall be enforceable except for the benefit of persons having an insurable interest in the things insured. (2) “Insurable interest as used in this section means any lawful and substantial economic interest in the safety or preservation of the subject of the insurance free from loss, destruction, or pecuniary damage.”

• Initiative 502: one ounce is lawful under Washington law and creates an insurable interest.

Insurable Interest

Even with an insurable interest, is coverage available for marijuana if it would be contrary to federal law and federal public policy? Oregon Measure 91: no contract shall be unenforceable on the basis that manufacturing, distributing, dispensing, possessing or using marijuana is prohibited by federal law.

PROPERTY COVERAGE AND RISKS

• Fire

• Water damage, rot, mold and insects from increased humidity

• Theft

• Pollution and odor from residual THC, hydroponic waste, fertilizer and insecticides

Increased Risk

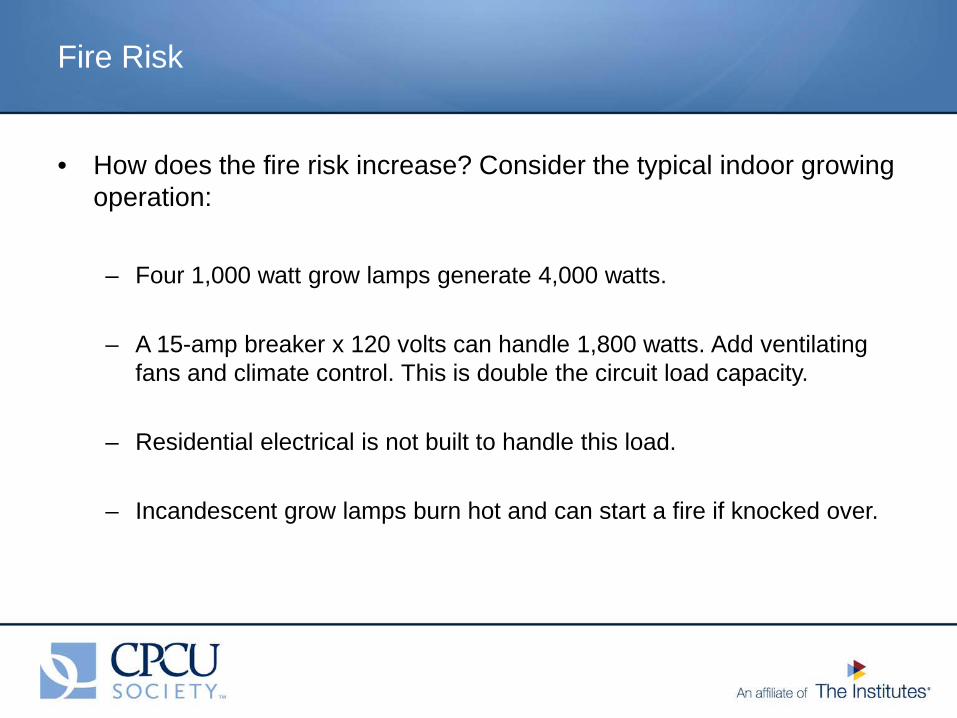

• How does the fire risk increase? Consider the typical indoor growing operation:

– Four 1,000 watt grow lamps generate 4,000 watts.

– A 15-amp breaker x 120 volts can handle 1,800 watts. Add ventilating

fans and climate control. This is double the circuit load capacity.

– Residential electrical is not built to handle this load.

– Incandescent grow lamps burn hot and can start a fire if knocked over.

Fire Risk

“I’ve never met anybody who grows marijuana who’s not been robbed—not just once, but robbed multiple times.” —Grower Noah Stokes in Willamette Week • Colorado, Oregon and Alaska: at current prices, a household may

have home-grown marijuana valued well over $10,000.

• By law, this is an insurable interest.

• By volume, one pound worth about $4,000 will fit in a freezer bag.

• Six pounds will fit in a backpack.

Theft Risk

•Valuation—“fair value:” replacement cost is the same as ACV.

•Loss of product preharvest: growers only.

•Insurable interest: not an issue.

•Loss of business income: grower/retailer must show loss of retail sales during the “period of restoration.”

Adjusting a Claim for Marijuana Plants/Products

• Insured has an indoor marijuana grow operation. Insured is also reducing marijuana leaves to hash oil using propane cook stoves.

• Explosion at house caused by propane gas.

• Insured claims $60,000 for value of plants, harvested marijuana and his personal property including grow equipment.

What If?

Adjust This Claim

• Before legalization: – No insurable interest in

marijuana. – Possible coverage for

equipment and other personal property, but…

– Exclusion for “illegal activity” by “insured”?

• After legalization – Insurable interest in

marijuana up to the legal limit.

– Grow equipment and personal property are both covered.

– Possible denial for “illegal activity” because the rendering of hash oil is illegal?

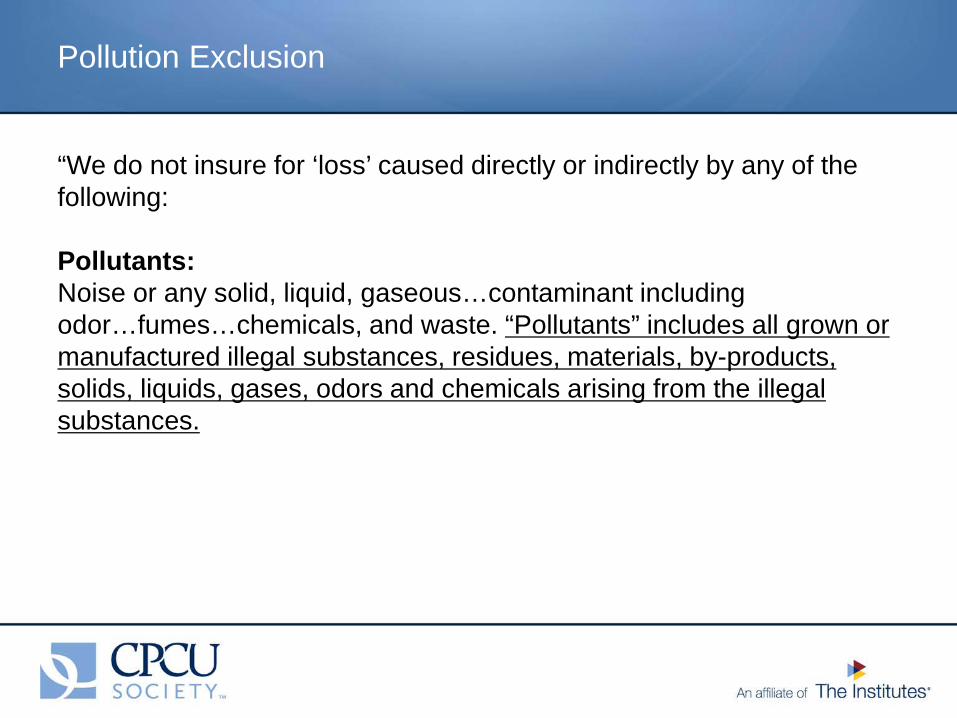

“We do not insure for ‘loss’ caused directly or indirectly by any of the following: Pollutants: Noise or any solid, liquid, gaseous…contaminant including odor…fumes…chemicals, and waste. “Pollutants” includes all grown or manufactured illegal substances, residues, materials, by-products, solids, liquids, gases, odors and chemicals arising from the illegal substances.

Pollution Exclusion

“Trees, Shrubs and Other Plants” are typically limited to $500 per plant.

Cause of loss limited to theft, fire or vandalism. However, after the buds are removed, it becomes personal property.

Trees, Plants, Shrubs Or Lawns

• Bundles both general liability and property insurance • What does a BOP cover?

• Business personal property • Stock in trade: inventory you hold for sale • Business interruption • Liability arising out of your business operations

Businessowners Policy (BOP)

LIABILITY COVERAGE

• Intentional Act/Criminal Act

• Workers Compensation

• Employer Liability (optional coverage)

• Pollution (optional coverage)

• Government Action/Seizure

• Wrongful Eviction

Commercial Liability Exclusions

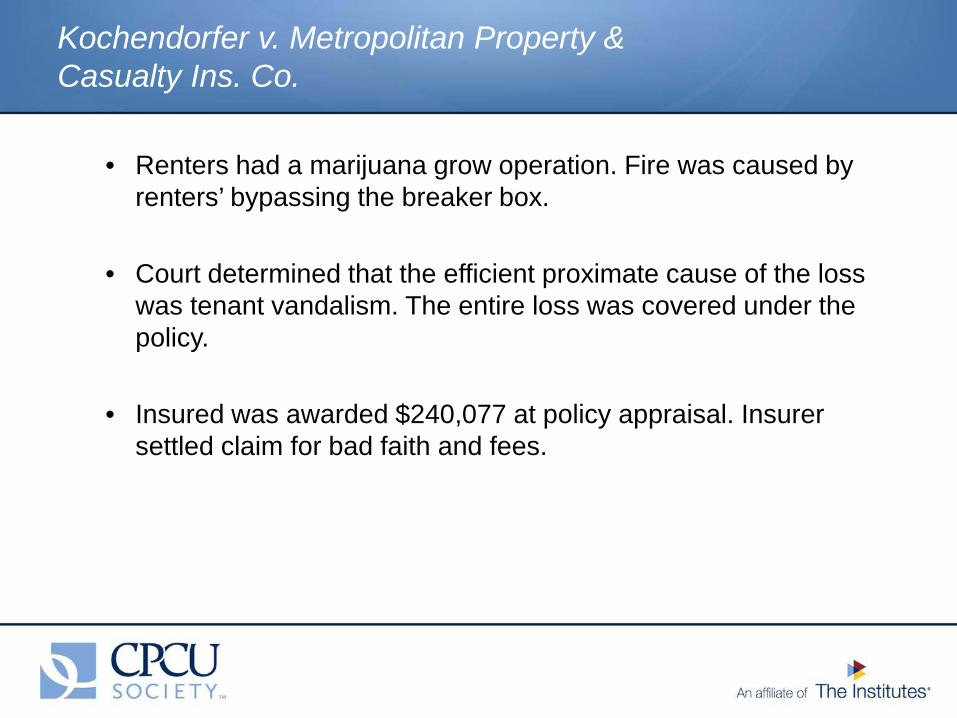

• Renters had a marijuana grow operation. Fire was caused by renters’ bypassing the breaker box.

• Court determined that the efficient proximate cause of the loss

was tenant vandalism. The entire loss was covered under the policy.

• Insured was awarded $240,077 at policy appraisal. Insurer settled claim for bad faith and fees.

Kochendorfer v. Metropolitan Property & Casualty Ins. Co.

Homeowners: Homeowners may give away, but not sell, the marijuana they grow. A homeowner may be liable to a third party injured by a guest if that injury can be linked to the marijuana the homeowner provided.

Issues for Consideration

• A landlord may expressly prohibit growing marijuana at a rental or specify a drug-free rental. Still, termination of a tenancy for these reasons may lead to increased risk of litigation.

• Wrongful eviction is covered under the Personal Injury endorsement.

– “Personal Injury means…wrongful eviction, wrongful entry…invasion of privacy.”

• A restaurant located near the insured’s property sues both the insured and tenant for trespass and nuisance because of odors from the tenant’s grow operation.

• Pollution exclusion includes “odors.”

• Federal DEA agents raid the insured location, confiscate all property, remove all fixtures and seize the building.

Potential Landlord/Tenant Liability

“Nothing in this section is intended to require an employer to permit or accommodate the use…of marijuana in the workplace or affect …policies restricting the use of marijuana by employees.” Colorado Statute C.R.S. 12-43.3 – 101 (2014).

• Employers can still enforce drug-free workplaces, including

prohibiting the use of marijuana for medicinal purpose.

• This presents potential wrongful termination issues under state unlawful employment statutes.

Impact on Employers and Employees

• Employee uses marijuana to treat anxiety and nausea.

• Employee fails mandatory drug test for permanent employment and is terminated.

• Employee sues for violation of state unlawful employment practices. • • Employer wins. State law cannot authorize use of marijuana, but

state can legalize marijuana use. Federal law states marijuana has no recognized medicinal purpose. Therefore, employee’s use of marijuana cannot be for the treatment of his medical condition.

What If…?

“Are there any traps that are used for security on the property?” “Is there any barbed wire, razor wire or electrified fencing…?” “Are there any dogs on the premises?” “Are there any firearms on the property?” “Any products not FDA approved?”

Actual Questions From Grower/Dispensary Application

• Disclosure in the application?

• Optional coverages?

• Special limits?

Underwriting Issues

DRAFTING POLICY LANGUAGE

• Twenty states in the Union offer some sort of legalization or decriminalization of marijuana possession/usage.

• Colorado medical marijuana statistics for registered users: • 67 percent male • Average age: 40 (male: 40; female: 45) • Leading cause: severe pain • 60 percent reside in Denver metro area (including Boulder)

• Typical medicinal user is not the 20-something snowboarder dude.

• As of 2009, there were 730,000 registered marijuana users nationwide.

– Government asserts that 24.8M would be eligible.

• Like it or not, trend is increasing acceptance and legalization is likely.— So you need to think about what your strategy is as an insurance organization.

Looking High and Wide

Overview

• Currently, four states ( AK, CO, OR, WA) and Washington D.C. have legalized recreational use of marijuana.

• It is projected that six additional states will introduce ballot measures that

could expand legalized marijuana usage in 2016 ( AZ, CA, MA, ME, MO, NV), with another state to introduce similar legislation (MI).

• By 2017: MA, MD, NH, TX, RI and VT will also address the issue. • Like it or not—the public and legislative views are changing on this issue.

Variance of Outcomes

• Nationally, one joint can get you: • Nothing—as long as you are old enough and in an accepted

location. • 15 years and a $250,000 fine. • In WY, simply being high can get you 90 days and $1,000 fine.

• DEA—seizure of assets

• RICO laws (Racketeer Influenced and Corruption Organizations Act) • Two acts • $25K fine and up to 20 years imprisonment per act • Includes controlled substance trafficking and money laundering

• Banks have federal charters.

• Accepting deposits from marijuana business is a violation of the RICO Act.

– These business have had to resort to an all-cash business. – Recent Department of Justice memorandums has provided

guidelines and eased the ability for the industry to utilize the banking industry.

– These are DOJ guidelines and could be revoked at any time.

Federal Laws That Could Affect Personal Lines

• Business risk • Home growers • Cash business—increased crime hazard • Driver impairment

• Liability risk

• Adults allowed to give away an ounce to other adults • Increase in children consuming accidently, usually when in care of grandparents (also

day care/adult care/pet care) • DUI risk

• Personal property risk

• DEA seizure of assets • Paying for covered marijuana • Business vs. self-grower

• RICO risk

• If we pay claims or accept premiums from those involved in this business, could we fall under the RICO statute?

Personal Lines Possible Exposures

• Personal property • Plant limit (5% of coverage A/C); $500 for plants (limited peril) • Treated like any other personal property • Exclusions for government seizures

• Business property

• Business property limit

• Exclusions under liability for: • Business • Controlled substance by licensed provider

• Rental property

• Possible exposure resulting from tenant’s misdeeds

Current Insurance Services Office, Inc. (ISO) Home Coverages

• Underwrite against the exposure • Exclude the coverage entirely • Invoke a special limit of liability • Give back narrower coverage after excluding • Provide an additional coverage after excluding • Define precisely business versus personal • Liability coverage:

• Business • Accidental ingestion • Nuisance • “Marijuana” host liability

Insurance Mitigation Strategies

•CSAA Insurance Group

• Excluded medicinal use and business crops

• Marijuana provider excluded

• Criminal acts exclusions

• Removal of state law condition

• Sublimit for state allowed marijuana

• Underwriting rules against home-growers here aren’t licensed by states

• Underwriting rules against home-growers if grown for others

• Exclusion of marijuana entirely

Personal Lines Industry Response

•Handout

Examples of Language

Questions?

Robert S. May Theresa Young, MBA, CPCU, ARC, ARe, ARM, AIC Kilmer, Voorhees and Laurick, PC CSAA Insurance Group 732 NW 19th Avenue 3055 Oak Road Portland, OR 97209 Walnut Creek CA 94575 (503) 224-0055 (925) 279-2596 [email protected] [email protected] www.KilmerLaw.com www.AAA4Insurance.com Brenda Wells, PhD, CPCU, AAI East Carolina University / Risk Education Strategies 2815 Madison Grove Rd Greenville, NC 27858 (252) 481-2777 [email protected] www.RiskedStrategies.com