Margin Squeeze / Refusal to deal - · PDF fileA margin squeeze arises if the spread between...

26

Margin Squeeze / Refusal to deal 12 mars 2010 Valérie MEUNIER Service économique Autorité de la concurrence

Transcript of Margin Squeeze / Refusal to deal - · PDF fileA margin squeeze arises if the spread between...

Margin Squeeze /Refusal to deal

12 mars 2010

Valérie MEUNIER

Service économique

Autorité de la concurrence

Outline

Introduction - Context

Margin squeeze definition

Simple margin squeeze model

Transatlantic divide

Examples

Conditions for a margin squeeze

Margin squeeze test

Links with other infringements

Conclusion

2

Antitrust duty to share property/input?

Should competition law require a firm with market power to share its property/input with its rivals?

Context:

• Physical infrastructure – e.g. telecommunication networks

• Input – e.g. raw material, electricity

• Intellectual property

Does the incumbent firm have a duty to supply?

• Shouldn’t a firm be free to trade with whoever it chooses to?

• If antitrust duty to deal, on what terms?

3

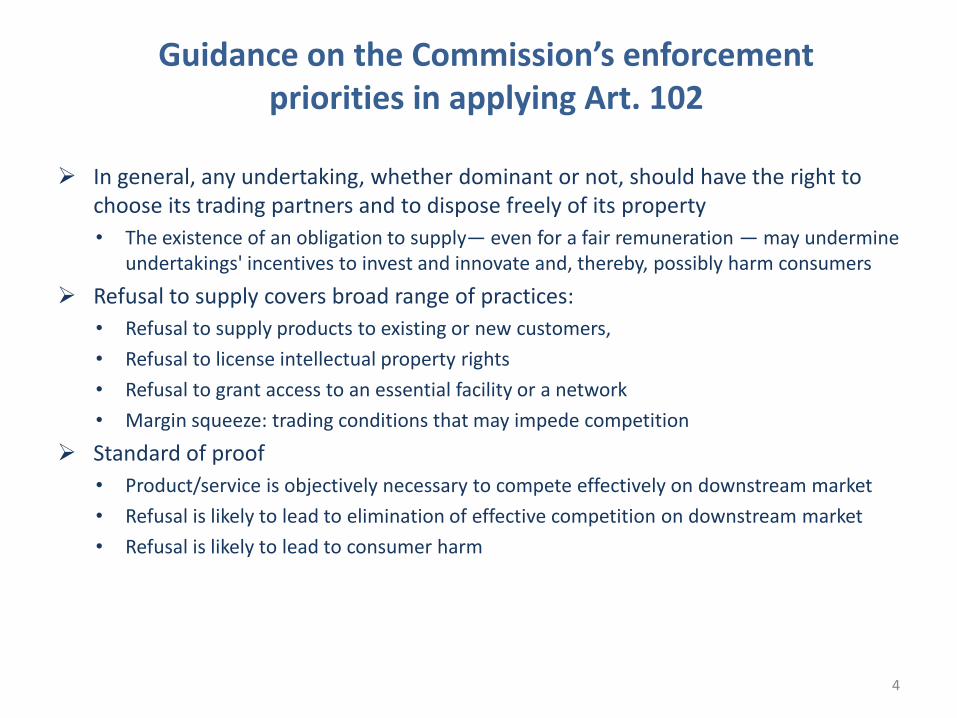

Guidance on the Commission’s enforcement priorities in applying Art. 102

In general, any undertaking, whether dominant or not, should have the right to choose its trading partners and to dispose freely of its property

• The existence of an obligation to supply— even for a fair remuneration — may undermine undertakings' incentives to invest and innovate and, thereby, possibly harm consumers

Refusal to supply covers broad range of practices:

• Refusal to supply products to existing or new customers,

• Refusal to license intellectual property rights

• Refusal to grant access to an essential facility or a network

• Margin squeeze: trading conditions that may impede competition

Standard of proof

• Product/service is objectively necessary to compete effectively on downstream market

• Refusal is likely to lead to elimination of effective competition on downstream market

• Refusal is likely to lead to consumer harm

4

Definition

A margin squeeze is an exclusionary abuse of dominance

Context: A vertically integrated firm that has a dominant position on the upstream market (bottleneck input)

• uses the input for the production of the good or service sold on the downstream market

• sells the input to rival firms that compete on the same downstream market

A margin squeeze arises if the spread between (i) the price at which the vertically integrated firm sells the final good on the downstream market, and (ii) the price at which it sells the upstream input to its rivals is “too small” to allow an efficient downstream rival to effectively compete

Theory of harm: The integrated firm could use (leverage) its dominant position on the upstream market to exclude downstream rivals, in order to monopolize the downstream market

5

Definition

6

Consumers

Vertically integrated firm – Firm 1 Downstream competitor – Firm 2

D2

U

D1

Price P1Price P2

Input price a

D1 operates at

variable cost c1

D2 operates at

variable cost c2

U operates at

variable cost c0

Margin squeeze if P1 – a < c1 (“as efficient competitor”)

Simple price squeeze model

Vertically integrated firm, Firm 1, faces a competitor (Firm 2) on the retail market (homogenous good)

Final demand: D(P1, P2)

If Firm 1 had no competitor: monopoly profit 1M=(P1

M-c0-c1)D(P1M)

Firm 2 will make a non-negative profit if P2 – a – c2 ≥ 0 and P2 ≤ P1

• i.e. if a + c2 ≤ P2 ≤ P1

7

p1

p2

a+c2

P2M

a+c2

P2= P1

Firm 2’s best response function

p2(p1)

Model (2)

Firm 1’s choice of retail price and access charge

• 1(p1, a) = (a-c0)D(p2M) if p1 > p2

M (1)

• 1(p1, a) = (a-c0)D(p1) if a + c2 ≤ p1 < p2M (2)

• 1(p1, a) =(p1-c0-c1)D(p1) if p1 < a + c2 (3)

In case (1), Firm 1 exits the downstream market, and lets Firm 2 choose its monopoly price.

In case (2), Firm 2 is active but sets a lower price – constrained monopoly.

• Note that, since p1< p2M D(p1)> D(p2

M)

Firm 1 is better off constraining Firm 2’s price

• Therefore, in this range, Firm 1 sets p1 = a + c2

In case (3), Firm 2 is not active. Only Firm 1 serves demand

8

),(),( 2111 apap M

Model (3)

If c1 < c2 (Firm 1 is more efficient), then Firm 1 sets monopoly retail price (P1

M that maximizes (P1-c0-c1)D(P1)), and input/access price at a = P1

M – c2

• In that case, a = P1M – c2 < P1

M – c1 : no margin squeeze

If c1 ≥ c2 (Firm 2 is more efficient), then Firm 1 lets Firm 2 serve the retail market:

• Firm 1 sets access price at aM that maximizes (a – c0)D(a + c2),

• Firm 2 sets its price P2 (=P1) = aM + c2

• In that case, a = P1 – c2 > P1 – c1 P1 – a < c1 : margin squeeze even though no intention of exclusion !!

• Vertically integrated firm extracts all Firm 2’s profit through access charge a

9

European Commission versus the US

Debate between EU and US about liability of margin squeeze under antitrust laws

• Chicago school: only one monopoly profit. The vertically integrated firm has no incentives to restrict downstream competition, as long as it can extract monopoly rents on the upstream market

Margin squeeze antitrust liability may do more harm than good:

• Either the vertically integrated firm will charge higher retail prices

• Or it will exit the downstream market, letting potentially less efficient firms serve final demand, which also may lead to higher retail prices

US Supreme court judgment in LinkLine: No margin squeeze antitrust liability. One should demonstrate

• Either a refusal to deal on the upstream market

• Or a predatory conduct on the downstream market

10

Margin squeeze liability?

Liberalized markets : Allow entry at downstream level and provide incentives to climb the “investment ladder”

Real life examples not as simple as model:

• Differentiated products

• Fixed / sunk cost of entry on downstream markets

• Dynamics : incentives for (gradual) entry

11

Examples

Raw material: Industrie des poudres sphériques (CFI, 2000)

Napier Brown – British Sugar, DG Comp decision, July 18, 1988

British Sugar is the unique producer of beet sugar in the UK (production quotas); BS is also active at the downstream level on the market for granulated sugar (beet or cane sugar)

Napier-Brown is a wholesaler that buys bulk sugar, re-packages and sells at the retail level.

Beet sugar covers approximately half of British consumption. Importations of beet sugar (5 to 10%). Importation and refining of sugar cane (40%).

BS has 58% market share – dominant position (can fix price independently of competitors, customers and consumers)

(65) “…BS has engaged in a price cutting campaign leaving an insufficient margin for a packager and seller of retail sugar, as efficient as BS itself in its packaging and selling operations, to survive in the long term.”

12

Examples (2/2) Telecommunication sector

Deutsche Telekom (DG Comp decision, May 21, 2003 – CFI, April 10, 2008)

Telefónica (DG Comp decision, July 4, 2007)

Connect ATM (Conseil de la concurrence, 00-MC-01, 04-D-18, 05-D-59)

Upstream market: wholesale access to local networks (local loops)

Vertically integrated firm is the former legal monopoly; Still holds a monopoly position on infrastructure

Downstream market: retail Internet access services

In France

• Telecommunication sector (Connect ATM, Ténor)

Tenor: margin between retail price of fixed-to-mobile calls and (upstream) call termination charges

• Energy sector: Direct Energie

Access to base-load electricity (produced at low marginal cost by nuclear plants operated by EDF)

Context of market liberalization

13

Conditions for a margin squeeze1 - Upstream dominant position

The vertically integrated firm must hold a dominant position on the upstream market

• If not, downstream firms could be supplied by others, and the incumbent’s strategy to restrict downstream competition would fail

• More than often, the vertically integrated firm holds a monopoly position on the upstream market

Deutsche Telekom, Connect ATM, Telefonica: Context of liberalization

Historic operator still has (quasi) monopoly over access to local loop

In cases involving phone services, operator has monopoly position on call terminations

In Direct Energie, EDF is sole producer of nuclear power, which constitutes 80% of total French consumption

14

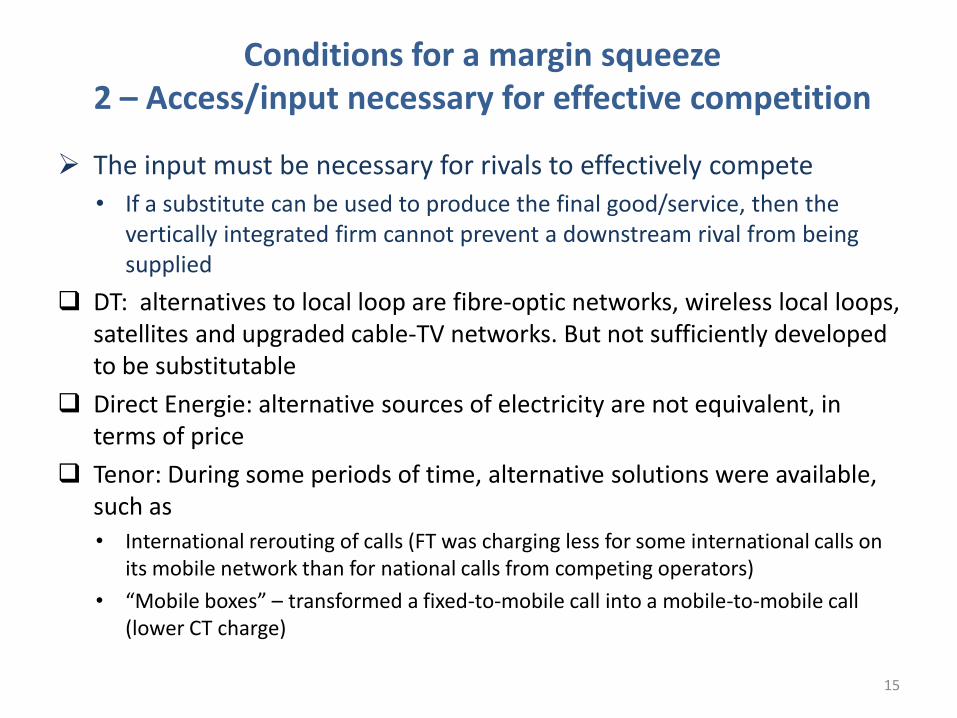

Conditions for a margin squeeze2 – Access/input necessary for effective competition

The input must be necessary for rivals to effectively compete

• If a substitute can be used to produce the final good/service, then the vertically integrated firm cannot prevent a downstream rival from being supplied

DT: alternatives to local loop are fibre-optic networks, wireless local loops, satellites and upgraded cable-TV networks. But not sufficiently developed to be substitutable

Direct Energie: alternative sources of electricity are not equivalent, in terms of price

Tenor: During some periods of time, alternative solutions were available, such as

• International rerouting of calls (FT was charging less for some international calls on its mobile network than for national calls from competing operators)

• “Mobile boxes” – transformed a fixed-to-mobile call into a mobile-to-mobile call (lower CT charge)

15

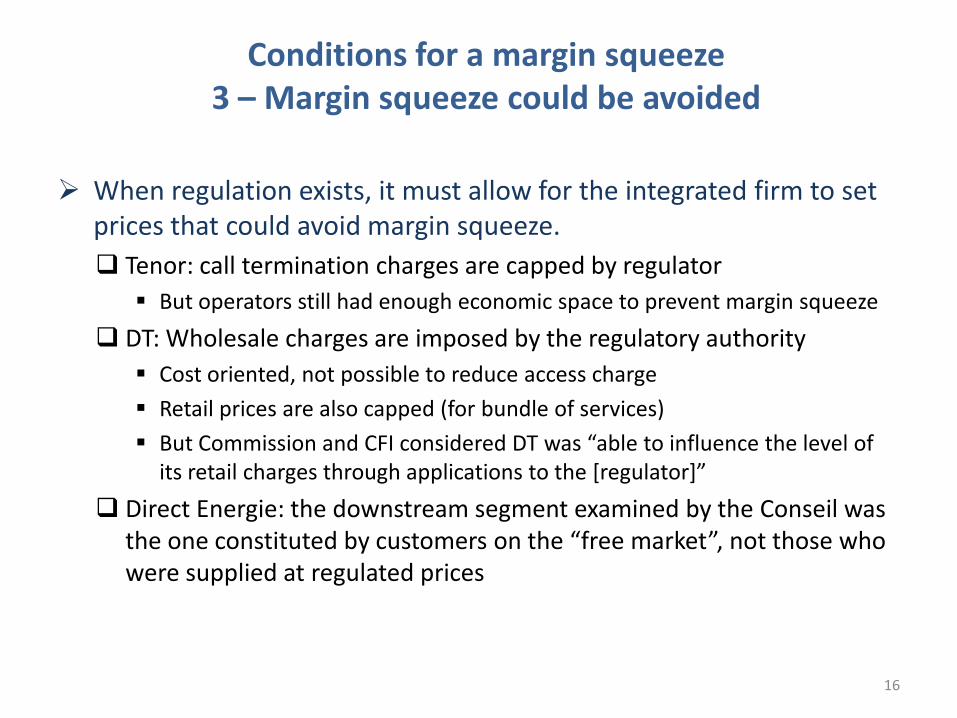

Conditions for a margin squeeze3 – Margin squeeze could be avoided

When regulation exists, it must allow for the integrated firm to set prices that could avoid margin squeeze.

Tenor: call termination charges are capped by regulator

But operators still had enough economic space to prevent margin squeeze

DT: Wholesale charges are imposed by the regulatory authority

Cost oriented, not possible to reduce access charge

Retail prices are also capped (for bundle of services)

But Commission and CFI considered DT was “able to influence the level of its retail charges through applications to the *regulator+”

Direct Energie: the downstream segment examined by the Conseil was the one constituted by customers on the “free market”, not those who were supplied at regulated prices

16

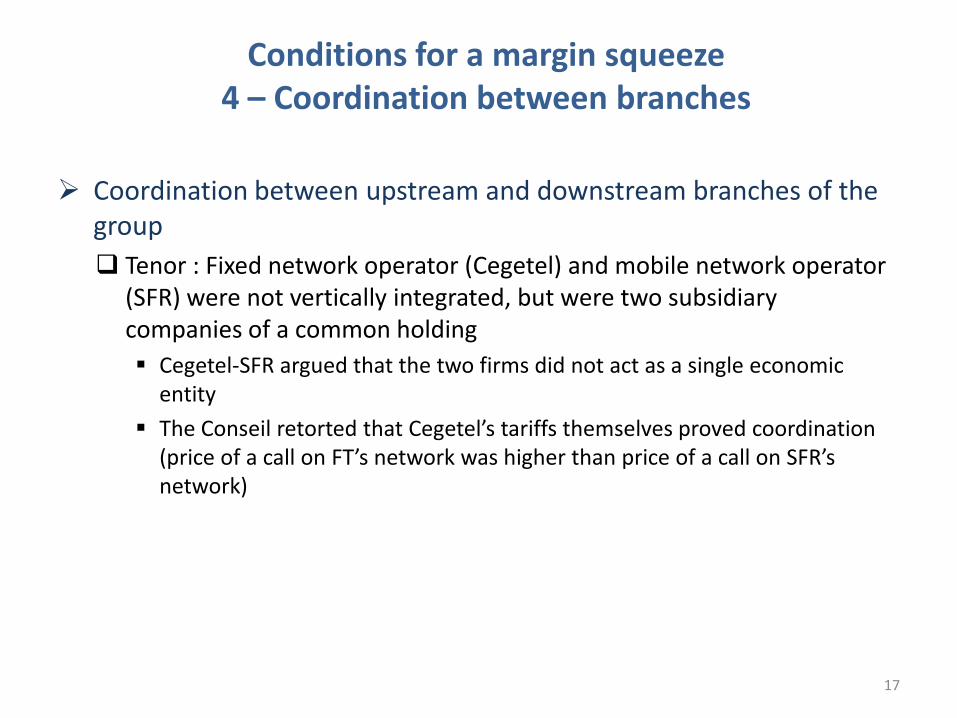

Conditions for a margin squeeze4 – Coordination between branches

Coordination between upstream and downstream branches of the group

Tenor : Fixed network operator (Cegetel) and mobile network operator (SFR) were not vertically integrated, but were two subsidiary companies of a common holding

Cegetel-SFR argued that the two firms did not act as a single economic entity

The Conseil retorted that Cegetel’s tariffs themselves proved coordination (price of a call on FT’s network was higher than price of a call on SFR’s network)

17

Margin squeeze test

“As efficient competitor” test

Check whether the vertically integrated firm’s margin on the downstream market (P1-c1) is high enough to cover the price of the input (a)

The vertically integrated firm knows its cost and can verify the test

Distinguishes between exclusion of efficient competitor and exclusion of less efficient competitors

Link with ECPR rule (efficient component pricing rule)

• Optimal access charge = cost of providing access (production and opportunity cost)

18

Elements of the test

1. Revenues of the integrated firm on the downstream market

2. Costs of the integrated firm on the downstream market

3. Price of the bottleneck input

Which revenues should the test take into account when many services or goods are provided for on the downstream market?

• In Telecom sector, many services can be sold thanks to broadband access

Scope of services to take into account

• Energy sector: consumers can have many different consumption profiles

Downstream costs can be difficult to evaluate when upstream and downstream operations are tightly linked

• Lack of separation between upstream and downstream levels of the group

Non linear relationship between costs or revenues and consumption

• Need for segmentation before aggregation

19

Elements of the test1 – The “as efficient competitor” test

The test must refer to the situation of the vertically integrated firm

• Costs and revenues of the vertically integrated firm

• Structure of the demand addressed by the vertically integrated firm

A competitor should not be restricted to address specific niches

Legal safety: if the incriminated firm had to compute margin squeeze test on its competitors’ data, it could not verify the legality of its conduct.

Cost concept: Long-run average incremental cost (LRAIC) [CMILT in French]

• Total downstream costs incurred to produce all goods/services – downstream costs that would be incurred if all goods/services were produced but for the ones under scrutiny

• Take into account possible economies of scope that can be passed on to consumers

20

Elements of the test2 – Scope of costs and revenues

In principle, costs and revenues for an as efficient firm if it replicates the vertically integrated firm’s offers on the retail market

In Deutsche Telekom, the Commission (approved by the CFI)

Only took into account revenues from provision of telephone lines to end-users

Did not take into account DT’s revenues from local or long-distance calls, call termination and sending, and other higher-value services.

Justification: historically, high price of long-distance calls compensated low subscription prices. Several Directives recommended tariff rebalancing, to terminate cross subsidy effects, and to ensure full competition on the market. Margin squeeze test should then be consistent with Directives principles, and should not allow for compensations between call and connection charges

21

Elements of the test3 – Segmentation and aggregation

Complex relationship between quantities, costs and revenues

• E.g. think of the many different mobile services offered

• E.g. Electricity consumption differs widely; depending on activity, size of industry or household,…

• Non-linear tariffs

In Tenor, the Conseil identified 19 consumption profiles.

In Connect ATM, set of assumptions regarding the number of subscribers, the cost incurred depending on population density,…

The test must be verified not on subcategories of consumers, but on the total portfolio of consumer groups

An “as efficient competitor” should be able to replicate the structure of the offers made by the vertically integrated firm, i.e. to address the same demand structure, not just some niches

22

Elements of the test4 – Time consideration

The Conseil has computed its margin squeeze tests on a period by period basis

In Telefonica, the Commission also presented a dynamic test, based on the net discounted value of the operator’s activity over several years

• Appropriate in nascent markets (or in rapid development): reasonable to assume that the operator, when setting its tariffs, anticipates future cost reductions (due to economies of scale, learning, innovations)

• But how to agree ex post on the ex ante anticipations of market growth?

• Maybe market growth resulted from anticompetitive behavior of incumbent?

23

Link with other infringements1 – Refusal to deal

Very similar approach

Liability should not undermine firms’ incentives to invest and innovate

But the Commission considers that in certain circumstances, imposing an obligation to supply clearly does not undermine those incentives (regulatory obligations; dominant position on infrastructure resulting from special or exclusive rights or has been financed by state resources)

Connect ATM :

First decision: The Conseil fined FT for not complying with injunction (interim measures), since offers to access “virtual network” were squeezing

Second decision (on the merits): the Conseil concluded that FT had infringed competition law, by refusing to deal with rival operators

Telefonica:

Company argued the Commission should have followed a refusal-to-deal standard of proof

24

Link with other infringements2 – Predation

In a margin squeeze, the vertically integrated firm sacrifices part of its profit in order to exclude downstream rivals. However, this sacrifice does not necessarily result in net losses; the vertical structure can still be profitable

Margin squeeze conduct is one of several strategies aiming at raising rivals’ costs• Two strategic levers: upstream access price and retail price

Predation

• The predator incurs losses first, and then recoups when rivals have exited -dynamic strategy

• The prey’s profits are eroded until it has to exit – Its costs are not directly affected by the predator

25

Conclusion

Margin squeeze test: verify that an as efficient competitor has enough economic space to operate on downstream market.

Balances willingness to allow new operators to enter markets and incentives to “climb the investment ladder”

Many important cases in context of liberalization

• Competition authorities may have legal instruments that regulators lack that can facilitate markets’ opening

26