Marfin s.r.l. CODE OF ETHICS s.r.l. CODE OF ETHICS Contents DEFINITIONS 4 REFERENCES 7

A n n u a l R e p o r t

2009A n n u a l R e p o r t

2009

Prepared in accordance

with the International Financial

Reporting Standards

The financial report has been translated from the

original financial report that has been prepared in the

Greek language. In the event that differences exist

between this translation and the original Greek language

financial report, the Greek language financial statements

will prevail over this document.

February 2010

Annual financial statements as at 31 December 2009

1. Statement of comprehensive income 4

2. Statement of financial position 5

3. Statement of changes in Equity 6

4. Statement of cash flows 7

5. Board of Director’s report for the year 2009 8

6. General Information 11

7. Basis of preparation 12

7.1 Statement of compliance 12

7.2 Basis of presentation 12

7.3 New accounting principles 12

7.4 Estimates 15

8. Basic Accounting Principles 16

8.1 Foreign currency transactions 16

8.2 Investments in Financial Instruments 16

8.3 Property, Plant and Equipment 16

8.4 Intangible assets 17

8.5 Cash and cash equivalents 17

8.6 Impairment of financial assets 17

8.7 Financial liabilities 18

8.8 Employee benefits 19

8.9 Provisions 20

8.10 Leased agreements 20

8.11 Offsetting financial instruments 20

8.12 Interest income and expenses 20

8.13 Fees and commisions 21

8.14 Net trading income 21

8.15 Income Tax and Deferred Tax 21

8.16 Share Capital 21

9. Management estimations and assumptions 22

MARFIN FACTORS & FORFAITERS

ANNUAL REPORT 2009

2

Contents

10. Notes to the Financial Statements 23

10.1 Net interest income 23

10.2 Net fee and commission income 23

10.3 Net trading income 23

10.4 Other income-expenses 24

10.5 Staff costs 24

10.6 Administrative expenses 25

10.7 Impairment of advances and receivables 25

10.8 Taxes 26

10.9 Cash and cash equivalents 26

10.10 Cash advances to Factoring customers 27

10.11 Non recourse Factoring 28

10.12 Forfaiting Portfolio 28

10.13 Intangible Assets 30

10.14 Property, Plant and Equipment 31

10.15 Deferred Tax 32

10.16 Other assets 32

10.17 Due to banks 33

10.18 Dept securities in issue and other borrowed funds 33

10.19 Non recourse Factoring liabilities 34

10.20 Provision for post-employment benefits 34

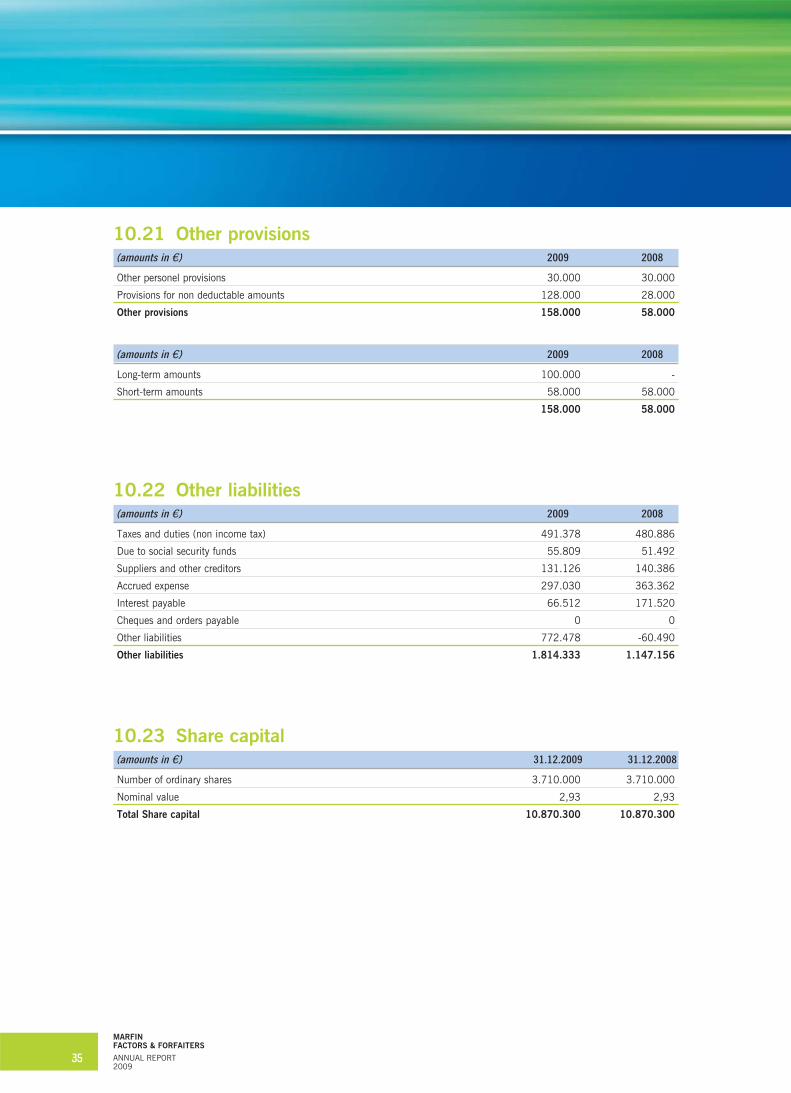

10.21 Other provisions 35

10.22 Other liabilities 35

10.23 Share capital 35

10.24 Reserves 36

11. Related parties transaction 37

12. Fair value of financial assets and liabilities 38

13. Financial risk management 39

13.1 Credit risk 39

13.2 Interest rate risk 42

13.3 Currency risk 43

13.4 Liquidity risk 45

13.5 Operational risk 46

14. Capital Adequacy 47

15. Contingent liabilities 48

16. Subsequent events 49

17. INDEPENDENT AUDITORS’ REPORT 50

MARFIN FACTORS & FORFAITERS

ANNUAL REPORT 2009

3

Contents

(amounts in ú) Note 2009 2008

Interest and similar income 10.1 7.301.162 9.979.848

Interest and similar expense 10.1 -3.699.623 -7.007.860

Net interest income 10.1 3.601.539 2.971.988

Fee and commission income 10.2 3.229.765 2.581.587

Fee and commission expense 10.2 -330.246 -435.611

Net fee and commission income 10.2 2.899.519 2.145.976

Net trading income / expenses 10.3 0 0

Other income 10.4 -32.623 110.972

Operating income 6.468.435 5.228.936

Staff costs 10.5 -2.059.377 -2.207.557

Administrative expenses 10.6 -974.567 -1.061.546

Depreciation and amortization 10.13 & 10.14 -102.775 -119.313

Impairment of advances and receivables 10.7 -1.923.799 -1.198.834

Profit (Loss) before taxes 1.407.917 641.685

Taxes 10.8 -685.982 -280.937

Profit (Loss) after Taxes (∞) 721.936 360.748

Other comprehensive income and expense (μ) 0 0

Other comprehensive income and expense after Tax (∞)+(μ) 721.936 360.748

Profit (Loss) after taxes per share 0,19 0,10

Athens, March 4th 2010

The Chairman The Chief Executive The Manager The Manager

Ôf the Board Officer and Vice President of the Finance of Accounting

of Directors Ôf the Board of Directors Department Department

Konstantinos π. Vassilakopoulos Panagiotis D. Papatheodorou George Sourgiadakis Aggelos Simonetatos

I.D. No ª 310696 I.D. No ™ 573982 I.D. No ∞∂ 107169 License No. 3601

MARFIN FACTORS & FORFAITERS

ANNUAL REPORT 2009

4

Statement of comprehensive income1.

(amounts in ú) Note 2009 2008

ASSETS

Cash and cash equivalents 10.9 3.342.448 1.681.430

Advances to customers 10.10 240.479.066 172.727.714

Non recource factoring assets 10.11 12.720.260 14.342.111

Forfaiting receivables from customers 10.12 19.668.948 42.114.078

Intangible assets 10.13 73.042 50.492

Property plant & equipment 10.14 353.122 425.500

Deferred tax asset 10.15 37.747 37.747

Other assets 10.16 583.133 193.311

Total Assets 277.257.765 231.572.383

LIABILITIES

Banks & financial institutions 10.17 112.933.367 75.120.434

Debt securities in issue and other borrowed funds 10.18 132.633.625 126.256.449

Non recource factoring liabilities 10.19 14.070.505 14.342.111

Provision for post employment benefits 10.20 58.849 46.190

Other provisions 10.21 158.000 58.000

Deferred tax liability 10.15 63.310 63.310

Current tax 511.689 289.920

Other liabilities 10.22 1.814.333 1.147.156

Total liabilities 262.243.679 217.323.570

Share capital 10.23 10.870.300 10.870.300

Reserves 10.24 467.588 400.187

Retained earnings 3.676.199 2.978.326

Total equity 15.014.086 14.248.814

Total equity and liabilities 277.257.765 231.572.383

MARFIN FACTORS & FORFAITERS

ANNUAL REPORT 2009

5

Statement of financial position2.

(amounts in ú) Share Statutory Other Retained Total

Capital Reserves Reserves earnings Net Equity

Balance as at January 1, 2008 10.870.300 182.946 161.429 2.617.578 13.832.254

Net profit/(loss) for the year 360.748 360.748

Total results recognised in 2008 360.748 360.748

Stock Options 55.812 55.812

Balance as at December 31, 2008 10.870.300 182.946 217.241 2.978.326 14.248.814

Balance as at January 1, 2009 10.870.300 182.946 217.241 2.978.326 14.248.813

Net profit/(loss) for the year 721.936 721.936

Total results recognised in 2009 721.936 721.936

Statutory reserve 24.063 -24.063 0

Stock Options 43.337 43.337

Balance as at December 31, 2009 10.870.300 207.009 260.578 3.676.199 15.014.086

MARFIN FACTORS & FORFAITERS

ANNUAL REPORT 2009

6

Statement of changes in Equity3.

(amounts in ú) 2009 2008

Cash flows from operating activities

Profit/Loss before taxes 1.407.917 641.685

Adjustments for non-cash items

Depreciation 102.775 119.313

Impairment loss and provisions 1.923.799 1.198.834

Other provisions 100.000 58.000

Employee benefits 55.996 313.200

Transfer to investing activities -798.963 -1.118.750

2.791.524 1.212.282

Changes in operating assets

Loans and advances to banks

Forfaiting portfolio 23.244.093 30.991.575

Loans and advances to customers -68.053.300 -50.063.540

Other Assets -389.822 12.942

Changes in operating liabilities

Due to Banks 44.190.110 26.840.759

Due to Customers -271.606 -5.946.254

Other Liabilities 667.178 -2.004.315

Net cash flow from operating activities before taxes 2.178.177 1.043.450

Tax paid -464.213 -125.452

Net cash flow from operating activities 1.713.965 917.997

Cash flows from investing activities

Purchase of Assets -52.946 -102.654

Sale of assets 0 0

Net Cash flows from Investing Activities -52.946 -102.654

Total net Cash Flows 1.661.019 815.343

Net cash flow increase (decrease) 1.661.019 815.343

Cash and cash equivalents, opening balance 1.681.430 866.086

Cash and cash equivalents, closing balance 3.342.448 1.681.430

MARFIN FACTORS & FORFAITERS

ANNUAL REPORT 2009

7

Statement of cash flows4.

To the annual General Assembly of the shareholders of “Marfin Factors & Forfaiters S.A.”

Dear shareholders,

We hereby present information concerning the Company’s activity during the financial year 2009.

General OverviewLast year has been characterized quite peculiar with regards to international business. In essence, there was no

business or industry that was not affected, while it led some to serious restructuring. Even though Marfin Factors

& Forfaiters did not remain unaffected by the international crisis, we have nevertheless succeded in achieving

increased profitability in 2009 results through a most suitable management process. We have stood by our

clients; we have extended and managed the existing collaborations based on their changing needs. At the same

time, we have continued to service the needs of the marked with complex, specially structured financing

solutions. This effort has paid off by increased turnover, close to ú 1 billion in forfeited receivables, thus proving

in action the increased trust of the market towards our company.

Financial Position and resultsIn 2009, Marfin Factors & Forfaiters bought and managed receivables increased by 23.2% in comparison to the

previous year, significantly higher that the average of the Greek market (increase of approximately 8-10%). This

increase came mainly from domestic factoring; whole turnover came to ú 794m, increased by 32% in

comparison with 2008. In this specific service product, major sectors of the Greek market are represented, such

as wholesale food products, clothing, automobiles, electrical, electronics and technology, manufacturing, courier

services, fish farms, advertising, media etc. Even though the general market tendency showed decrease in sales,

something that was further confirmed by our clients’ turnover, the increased revenue of Marfin Factors &

Forfaiters was based both on the systematic expansion of existing collaborations (turn over of more debtors by

creditor, new products), as well as to new clientelle.

During 2009, Greek exports noted significant decrease, thus affecting departments of international factoring of

most companies. The International factoring of our company developed its business, accomplishing increased

turnover by 12% as compared to that of 2008. This result was based on our intensive efforts through new export

collaborations and better exploitation of existing, as well as on the strengthening of our import markets, through

the systematic relations development with factoring companies of exporting countries. This targeted activity lead

Marfin Factors & Forfaiters into the 3rd place in the greek market’s international factoring, holding a total market

share of 15.33% (data from Factors Chain International), while in the import sector it ranked 2nd, holding a 40%

market share and achieving increase of 57,6% reaching ú 43.20 m in total as compared to ú 27.42m in 2008.

Due to the international financial situation and the ambiguity that continued to define international markets

during 2009, the company continued to apply the policy of business decrease of secondary forfaiting mainly,

thus causing the turnover from this specific business segment to barely reach ú 13.3m compared to ú 44.2m

in 2008 and ú 100.6m in 2007.

The Advance balances of the company at 31.12.2009 amounted to ú 260.15m, increased by 21.1% as

compared to 2008.

The Net Operating Turnover amounted to ú 6.5m while the Profit before Taxes to ú 1.4m, increased by 23.7%

Î·È 119% respectively.

MARFIN FACTORS & FORFAITERS

ANNUAL REPORT 2009

8

Board of Director’s report for the year 20095.

The net commission revenue, which constitutes a basic course index for factoring companies, increased by 35%,

reaching ú 2.89m, while the net interest revenue noted an increase of 21.2% and amounted to ú 3.6m. thus

resulting in a 27% increase of Gross Turnover. On an Operating Results level, (ú 3.35m) the increase reached

79%. Provisions are significantly lower due to the write-off or previous years’ receivables (before 2007) and

constitute 1.22% of the company’s total open receivables. The Net Profit before taxes increased to ú 1.40m in

2009 compared to ú 0.64m in 2008. It is also noted that despite the negative situation in the markets, the

Serbian Branch Office was actively operated in September 2009, after the return to a fairly normal local market.

On an index level, the ratio of Operating Expenses to Operating Revenue (Cost-to-Income ratio) was restrained

to 48.7% against a previous 64.8%.

Risk ManagementThe risk management policy of the company, as well as its exposure to market risk, interest rate risk,

counterparty risk, liquidity risk and operational risk are being described analytically in the relative section of the

Notes to Financial Statements. The company has limited foreign currency and its assets do not include bills or

real estate property.

Transactions with related partiesAll transactions with related parties, are being carried out within the frame of the usual business processes,

performed according to market terms and conditions, and are being approved by the authorized officers of the

Company. These transactions are presented in the respective notes to the Financial Statements, the most

important one being that of loan transactions with the parent company Marfin Egnatia Bank which covers 100%

of the company’s loan payables.

ProspectsIn 2010, the company aims to achive a further increase of turnover, as a higher rate than that of the market,

thus increasing simultaneously its market share. The company also aims to further develop and enhance the

branch office in Serbia, as well as to reinforce its relations with foreign Factors and increase business of

international Factoring, despite estimated decrease of Greek exports in 2010, through better positioning in

selective sectors of export activities.

Post balance sheet eventsThe tax audit for fiscal years 2007-2008 was completed in February, imposing additional taxes and penalties

corresponding to the provision of accounting differences included in previous years’ taxes (see note 10.8).

MARFIN FACTORS & FORFAITERS

ANNUAL REPORT 2009

9

StatementThe members of the Board of Directors state that the attached company financial statements for the fiscal period

starting from 1st of January 2009 and ending on 31st of December 2009, which were prepared according to

effective International Accounting Standards and the International Financial Reporting Standards, fairly depict

the assets and the liabilities, the equity as well as the profit and loss of the company and that the Board of

Directors annual report clearly depicts in a fair way the development, the performance and financial position of

Marfin Factors & Forfaiters including the description of the most significant risks and uncertainties that the

company faces.

Athens, March 4 2010

By commission of the Board of Directors

Panos Papatheodorou

Managing Director & Vice-Precident BoD

MARFIN FACTORS & FORFAITERS

ANNUAL REPORT 2009

10

«MARFIN FACTORS & FORFAITERS S.A.» (former LAIKI FACTORING S.A. and from now on “the Company”),

has its domicile in Greece, and has been registered in the Societes Anonymes Register under number

41316/01/μ/981428.

The company is a member of the “MARFIN EGNATIA BANK S.A.” group. The Marfin Egnatia Bank group of

companies mainly operates in the financial sector providing a broad range of financial services to companies and

individuals.

Δhe Company’s main purpose is to conduct recourse and non-recourse Factoring operations in Greece and

abroad. The branch in Serbia is already operating and the expansion of its operations to other countries of South-

East Europe in the near future is a primary goal for the Company.

The Company makes business in the field of domesic and international Factoring with or without recourse as

well as Forfaiting in cross border transactions.

The Company’s head office is in Marousi 20, Kifisias Avenue.

ManagementAccording to the General Assembly of the shareholders on 26.10.2010 the body of the Board of Directors was

reorganized as follows:

The Chairman (Non executive member): Konstantinos π. Basilakopoulos

The Vice Chairman (Executive member): Panagiotis D. Papatheodorou

Executive members: Dimitrios ∞. Zouzoukis

Non executive members: Dionysios ∫. Papatheodorou

Efthymios T. Bouloutas

Kyriakos D. Mageiras

Heracles G. Kounadis

The auditors of the annual financial statements are as follows:

Regular: John G. Leos (SOEL Reg. No 24881)

Deputy: Athena ∫. Moustaki (SOEL Reg. No 28871)

Of the auditing firm: Grant Thornton S.A. (SOEL Reg. No 127)

MARFIN FACTORS & FORFAITERS

ANNUAL REPORT 2009

11

General Information6.

7.1 Statement of complianceThe financial statements of the Company have been prepared in accordance with International Financial

Reporting Standards (I.F.R.S) and all amendments which have been adopted by the European Union. The

financial statements were approved for publication by the Board of Directors on 4 March 2010 and are subject

to final approval of the Ordinary Assembly of the shareholders.

7.2 Basis of presentationThe financial statements are presented in euro which is the reported currency and they are prepared on a historic

cost basis.

7.3 New accounting principlesThe current financial statement were prepared in full compliance with the International Financial Reporting

Standards (IFRS) as well as the amendments that have been adopted by the European Union, whose adoption

is mandatory for the preparation of the financial statements covering the periods after 1.1.2009.

The accounting principles followed by the Company for the preparation of its annual Financial Statements as at

31/12/2009, are consistent to those described in the publicized financial statements for the year ended as at

31/12/2008, taking into account the following amendments to International Accounting Standards and new

Interpretations issued by IASB whose application is mandatory as starting from 1/1/2009.

(i) Standards, amendments and interpretations effective from January 1st 2009

The Company adopted for first time the following standards, amendments and interpretations were issued:

(a) IAS 1: (Revised) “Presentation of Financial Statements”:

IAS 1 has been revised to enhance the usefulness of information presented in the financial statements. The

revised standard prohibits the presentation of items of income and expenses (that is “non-owner changes in

equity”) in the statement of changes in equity, requiring “non-owner changes in equity” to be presented

separately from owner changes in equity. Entities can choose whether to present one performance statement

(the Statement of Comprehensive income) or two statements (the Income Statement and Statement of

Comprehensive Income). The Company has elected to present one Statement.

(b) IAS 23: (Revised) "Borrowing Costs" (effective from January 1st, 2009):

The revised standard requires that an entity capitalises borrowing costs directly attributable to the acquisition,

construction or production of a qualifying asset (an asset for which a significant period of time is required in

order to become ready for use or sale) as part of asset’s cost.

(c) IAS 32: (Amendment) “Financial Instruments: Presentation and IAS 1 Presentation of Financial

Statements (Amendment), (effective from January 1st, 2009):

The amendment to IAS 32 requires certain puttable financial instruments and obligations arising on liquidation

to be classified as equity if certain criteria are met:

Financial instruments which provide the right to the owner to claim their payment.

Means or components of means impose a liability to the Company to provide to a third party portion

of the equity in case of liquidation.

MARFIN FACTORS & FORFAITERS

ANNUAL REPORT 2009

12

Basis of preparation7.

(d) IAS 39: “Financial instruments: Recognition and Measurement (effective from July 1st, 2009):

This amendment clarifies how the principles that determine whether a hedged risk or portion of cash flows is

eligible for designation should be applied in particular situations. This amendment does not impact the

Company’s financial statements.

(e) IFRS 7: “Financial instruments: Disclosures” (amended in March 2009), (effective from January 1st, 2009):

The amendment requires enhanced disclosures about fair value measurement and liquidity risk.In particular, the

amendment requires disclosure of fair value measurement through a three level hierarchy. The adoption of the

amendment had no significant impact on the Company’s financial statements.

(f) IFRS 8: "Operating segments", (effective from January 1st, 2009):

The new IFRS requires a “management approach” to the Group’s presentation of financial information under

segment reporting. Information disclosed is basically information that the Management uses for internal

reporting so as to assess the productivity of segments, as well as the manner in which resources are allocated.

Such reporting might differentiate from information used during the preparation of the balance sheet and the

income statement. Furtheremore, the standard requires that explanatory notes on the basis of preparation of

segment reporting, as well as traces to entries in financial statements should also be disclosed.

(g) IFRS 2: “Share-based Payment: Vesting Conditions and Cancellations (Amendment), (effective from

January 1st, 2009):

This amendment clarifies that only service conditions and performance conditions are vesting conditions, while

all other features need to be included in the grant date fair value.The adoption of the amendment had no impact

on the Company’s financial statements.

(g) IFRIC 13 “Customer Loyalty Programmes”, (effective from July 1st, 2009):

IFRIC 13 is applied on customer loyalty programmes. This Interpretation addresses the accounting by entities that

provide their customers with incentives to buy goods or services by providing awards (called ‘award credits’ in the

Interpretation) as part of a sales transaction. This interpretation is not relevant to the Company’s operations.

(h) IFRIC 15 “Agreements for the Constriction of Real Estate”, (effective from January 1st, 2009):

This interpretation addresses the diversity in accounting for real estate sales. Some entities recognize revenues

in accordance with IAS 18 (i.e. when risks and rewards in the real estate are transferred) and others recognize

revenue as the real estate is developed in accordance with IAS 11. The interpretation clarifies which standard

should be applied to particular. This interpretation is not applicable to the Company’s activities.

(i) IFRIC 16 “Hedges on a Net Investment in a Foreign Operation”, (effective for annual periods beginning on

or after 1st October 2008):

This interpretation applies to an entity that hedges the foreign currency risk arising from its net investments in

foreign operations and qualifies for hedge accounting in accordance with IAS 39. The interpretation provides

guidance on how an entity should determine the amounts to be reclassified from equity to profit of loss for both

the hedging instrument and the hedged item. This interpretation is not applicable to the Company’s activities.

(j) IFRIC 18: “Transfers of Assets from Customers”, (effective for annual periods beginning on or after 1st July 2009):

IFRIC 18 is aimed at clarifying the requirements of IFRSs pertaining to agreements under which an entity

receives from a client a segment of fixed assets that the entity shall use either when a client constitutes a part

of a network or a client shall obtain constant access to provision of goods or services (such as, for instance,

provision of electricity or water). The IFRIC is applied mainly to utility entities and is not applicable to the

Company’s activities.

MARFIN FACTORS & FORFAITERS

ANNUAL REPORT 2009

13

(ii) New standards, amendments and interpretations that are not yet effective

(a) IFRS 3: “Business Combinations” (Revised) and IAS 27 “Consolidated and Separate Financial Statements”

(Amended), (effective for annual periods beginning on or after 1st July 2009)

The revised IFRS introduces a number of changes in the accounting for business combination which will impact

the amount of goodwill recognized, the reported results in the period that an acquisition occurs, and future

reported results. Such changes include the expensing of acquisition related costs and recognizing subsequent

changes in fair value of contingent consideration in the profit and loss. The amended IAS 27 requires that a

change in ownership interest of a subsidiary to be accounted for as an equity transaction. Furthermore the

amended standard changes the accounting for losses incurred by the subsidiary as well as the loss of control of

a subsidiary. The adoption of the revised standards will have no significant impact on the Company’s financial

statements.

(b) IFRS 9: “Financial Instruments”, (effective for annual periods beginning on or after 1st January 2013)

IFRS 9 is the first part of Phase 1 of the Board’s project to replace IAS 39. The IASB intends to expand IFRS 9

during 2010 to add new requirements for classifying and measuring financial liabilities, derecognition of

financial instruments, impairement and hedge accounting. IFRS 9 states that financial assets are initially

measured at fair value plus, in the case of a financial asset not a fair value through profit and loss, particular

transaction costs. Subsequently financial assets are measured at amortised cost or fair value and depend on the

basis of the entity’s business model for managing the financial assets and the contractual cash flows

characteristics of the financial assets.

IFRS 9 prohibits reclassifications except in rare circumstances, when the entity’s business model changes. In

this case, the entity is required to reclassify affected financial assets prospectively. IFRS 9 classification

principles indicate that all equity investments, should be measured at fair value.

However management has the option to present in other comprehensive income unrealized and realized fair

value gains and losses on equity investments that are not held for trading. Such designation is available on initial

recognition on an instrument-by –instrument basis and is irrevocable. There is no subsequent recycling of fair

value gains and losses to profit and loss: however dividends from such investments will continue to be

recognized in profit and loss. IFRS 9 removes the cost excemption for unquoted equities and derivatives on

unquoted equities but provides guidance on when cost may be an appropriate estimate of fair value. IFRS 9 can

not be early adopted, as it has not been endorsed by the E.U.

(c) IFRIC 17 ”Distribution of Non-Cash Assets to Owners”, Owners (effective for annual periods beginning on

or after 1st July 2009.

When an entity announces distribution of non-cash assets to owners, it shall recognize a liability for the

distributed dividends. The Interpretation provides guidelines pertaining to when an entity shall recognize

dividends payable, how they shall be measured and how it shall account for the difference between the carrying

amount of distributed assets and the carrying amount of the dividends paid in case the entity settles dividends

payment. The Interpretation is not applicable to the Company’s activities.

MARFIN FACTORS & FORFAITERS

ANNUAL REPORT 2009

14

7.4 EstimatesThe preparation of the financial statements in conformity with IFRS requires management to make judgments,

estimates and assumptions that affect the reported amount of assets and liabilities, income and expenses. Actual

results may differ from these estimates.

The estimates and associated assumptions are based on historical experience and various other factors that are

believed to be reasonable under the circumstances, the results of which form the basis of making judgments

about carrying values of assets and liabilities that are not readily apparent from other sources.

The estimates and underlying assumptions are reviewed on an ongoing basis. Deviations to accounting estimates

are recognized in the period in which the estimate is revised if the revision effects only that period, or in the

period of the revision and future periods if the revision affects both the current and future periods.

MARFIN FACTORS & FORFAITERS

ANNUAL REPORT 2009

15

The basic accounting principles that were adopted for the preparation of financial statements are as follows:

8.1 Foreign currency transactionsTransactions in foreign currencies are translated to Euro the reporting currency at the foreign exchange rate ruling

at the date of the transaction.

Monetary assets and liabilities denominated in foreign currencies, at the balance sheet date are translated to

Euro at the foreign exchange rate ruling at that date. Foreign exchange differences arising on translation are

recognized in the income statement.

Foreign exchange income and expense from the consolidation of the branch office do not significantly affect the

financial statements.

8.2 Investments in Financial Insruments

(a) Loans and advance to customers

i. Classification

The Company’s financial assets are classified into two categories which are “Advances to Factoring clients” and

“Forfaiting portfolio”.

“Advances to Factoring clients” consist of two subcategories, “Recourse Factoring” and “Non-recourse

Factoring”.

ii. Recognition

Advances are recognized whenever cash is disbursed to the beneficiates of such credit.

iii. Initial Measurement

Financial assets are measured initially at fair value plus transaction costs.

iv. Measurement after the initial

After the initial measurement the financial assets are measured at amortized cost using the effective rate

method.

v. Derecognition

A financial asset is derecognized when the Company loses control on contractual rights that comprise the

financial instrument. This occurs when the rights to receive cash flows from these have been executed, or when

the company has transferred substantially all the risks and rewards of the assets.

8.3 Property, Plant and EquipmentProperty, plant and equipment are stated at cost less accumulated depreciation and accumulated impairment

losses. Depreciation is charged to the income statement on a straight-line basis over the estimated useful lives

of property, plant and equipment. Land is not depreciated.

MARFIN FACTORS & FORFAITERS

ANNUAL REPORT 2009

16

Basic Accounting Principles8.

The estimated useful lives are as follows:

Improvements on non owned properties: over the duration of the lease contract or the estimated

useful life, whichever is the shortest

Furniture and other equipment: 5 years

Computer hardware and software: 3-4 years

Transportation means: 6-7 years

Property, plant and equipment are reviewed for impairment whenever events or changes in circumstances

indicate that the carrying amount at cost may not be recoverable. An asset’s carrying amount is written down

immediately to its recoverable amount if the asset’s carrying amount is greater than its estimated recoverable

amount. The recoverable amount is the higher of the asset’s fair value less costs to sell and value in use.

Subsequent costs are included in the assets carrying amount or recognized as a separate asset, as appropriate

only when it is probable that future economic benefits associated with the item will flow to the Company, and

their cost can be measured reliably. Repairs and maintenance are charged to the income statement during the

financial period in which they take place.

Gains and losses on disposals are determined by comparing proceeds with carrying amounts. These are included

in the income statement.

8.4 Intangible assetsIntangible assets include Company’s software and are stated at cost less accumulated depreciation and

accumulated impairment losses.

Amortization is charged to the income statement on a straight-line basis over the estimated useful life of the

software, which is between 3 to 4 years.

8.5 Cash and cash equivalentsCash and cash equivalents include monetary assets with an original maturity of three months or less, such as

cash balance and amounts due from financial institutions.

8.6 Impairment of financial assetsThe Company assesses at each balance sheet date whether there is objective evidence that a financial asset or

group of financial assets is impaired. A financial asset or group of financial assets is impaired and impairment

losses are incurred and only, and only if there is objective evidence of impairment as a result of one or more

events that occurred after the initial recognition of the asset (a ‘loss event’) and that loss event (or events) has

an impact on the estimated future cash flows of the financial asset or group of financial assets that can be

reliably estimated. Objective evidence that a financial asset or group of assets is impaired includes data that

comes to the attention of the Company about the following loss events:

MARFIN FACTORS & FORFAITERS

ANNUAL REPORT 2009

17

i. Significant financial deterioration of the issuer or obligator;

ii. A breach of contract, such as a default or delinquency in meeting payments;

iii. Strong probability that the borrower will enter bankruptcy stage or other financial restructuring;

iv. Observable data indicating that there is a measurable decrease in the estimated future cash flows

from a group of financial assets since the initial recognition of those assets, although the decrease

cannot yet be identified with the individual financial assets in the group, including:

adverse changes in the payment status of customers; or

national or local economic conditions that correlate with defaults on the assets in a group.

If there is objective evidence that an impairment loss on factoring advances carried, the amount of the loss is

measured as the difference between the assets' carrying amount and the present value of estimated future cash

flows (excluding future credit losses that have already been incurred) discounted at the financial asset's original

effective interest rate. The carrying amount of the asset is reduced through the use of an allowance account and

the amount of the loss is recognized in the income statement. If the factoring advance has a floating interest

rate, the discount rate for measuring any impairment loss is the current effective interest rate determined under

the contract.

The calculation of the present value of the estimated future cash flows of a collateralised financial asset reflects

the cash flows that may result from foreclosure less costs for obtaining and selling the collateral, in case the

foreclosure cannot be carried out.

If, in a subsequent period, the amount of the impairment loss decreases and the decrease can be related

objectively to an event occurring after the impairment was recognized, the previously recognized impairment loss

is reversed by adjusting the allowance account. The amount of the reversal is recognized in the income

statement.

When an advance or receivables is uncollectable, it is written off against the related provision for

advance/receivable impairment. Such advances or receivables are written off after all the necessary procedures

have been completed and the amount of the loss has been determined. Subsequent recoveries of amounts

previously written off are recognized in the income statement.

8.7 Financial liabilitiesFinancial liabilities are measured initially at fair value plus transaction costs. Subsequently they are stated at

amortized cost which occurs by the use of the effective interest method. Any difference between the initial

proceeds and the redemption value is recognized in the income statement, using the effective interest method.

Due to banks, obligations to customers (Non-Recourse Factoring Liabilities) and debt securities in issue are

classified in this category.

MARFIN FACTORS & FORFAITERS

ANNUAL REPORT 2009

18

8.8 Employee benefitsShort-term benefits: Short-term benefits to personnel (except for termination of employment benefits) in cash

and kind are recognized as an expense when considered accrued. Any unpaid amount is recognized as a liability,

whereas in case the amount already paid exceeds the benefits’ amount, the entity identifies the excessive

amount as an asset (prepaid expense) only to the extent that the prepayment shall lead to a future payments’

reduction or refund.

Retirement Benefits: Benefits following termination of employment include lump-sum severance grants, pensions

and other benefits paid to employees after termination of employment in exchange for their service. The

Company’s liabilities for retirement benefits cover both defined contribution schemes and defined benefit plans.

i) Defined contribution plans

For defined contribution plans, the Company pays contributions to publicly administered pension insurance

funds (i.e. Social Security Foundation) and therefore the Company has no obligation to pay further contributions

if the fund does not hold sufficient assets to pay all employees the benefits relating to pension obligations. The

regular contributions constitute net periodic costs for the year in which they are due and as such they are

included in line 'staff costs' of the Income Statement.

ii) Defined benefit plans

The Company’s defined benefit plan regards the legal commitment to pay lump-sum severance grant, pursuant

to L.2112/1920. Typically defined benefit plans define an amount of pension benefit that an employee will

receive on retirement, usually dependent on one or more factors such as years of service and compensation. The

liability recognized in the balance sheet for defined benefit plans is the present value of the liability for the

defined benefit less the plan assets’ fair value (reserve from payments to an insurance company), the changes

deriving from any actuarial profit or loss and the service cost. The defined benefit commitment is calculated on

an annual basis by an independent actuary with the use of the projected unit credit method.

The present value of the liability which incurs from the defined benefit plan is calculated by discounting the

future cash outflows with the long-term Greek bonds’ rate.

Actuarial profits and losses form part of the Company’s commitment to grant the benefit and of the expense

which shall be recognized in the income statement. The adjustments’ outcome based on historical data, if below

or above a 10% accumulated liability margin, is recognized in the income statement within the expected

insurance period of the plan’s participants. The service cost is directly recognized in the income statement except

for the case where plan’s changes depend on employees’ remaining years of service. In such a case, the service

cost is recognized in the income statement using the fixed method during the maturity period.

Employment Termination Benefits: Benefits due to employment termination are paid when employees step

down prior to the retirement date. The Company recognizes these benefits upon committing itself that it

terminate employees’ employment according to a detailed plan for which there is no withdrawal possibility.

Remuneration based on Equity Instruments: The Group, through the Parent Company Marfin Popular Bank,

grants the personnel stock options for the acquisition of Parent Company shares. These benefits are settled by

issuing new shares from the Parent Company, on the condition that the employee fulfils certain vesting

conditions linked to his/her performance and exercises his/her options.

Services rendered by employees are measured according to the fair value of the options granted on the grant

MARFIN FACTORS & FORFAITERS

ANNUAL REPORT 2009

19

date. Option fair value is calculated by using a widely accepted option-pricing model and taking into account

the share’s closing price on grant date. Options’ fair value, following their issue, is readjusted in case there is a

modification in the plan favorable for employees. Employees’ services residual value is recognized as an expense

in the income statement by equal credit amount Èn equity, in the share premium account. The relative amount

is divided throughout the vesting period and is calculated on the basis of the number of options set to vest in

each year.

8.9 ProvisionsProvisions are recognized when the Company has a present legal or constructive obligation as a result of past

events, it is probable that an outflow of resources embodying economic benefits will be required to settle the

obligation, and reliable estimates of the amount of the obligation can be made.

Contingent liabilities that cannot possibly incur cash flows are also disclosed, unless they are immaterial.

8.10 Leased agreementsFinancial assets and liabilities are offset and the net amount is reported in the balance sheet when there is a

legally enforceable right to offset the recognized amounts and there is an intention to settle on a net basis, or

realize the asset and settle the liability simultaneously. Offsetting income with expenses is allowed only if they

are part of the same entry.

8.11 Offsetting financial instrumentsFinancial assets and liabilities are offset and the net amount is reported in the balance sheet when there is a

legally enforceable right to offset the recognized amounts and there is an intention to settle on a net basis, or

realize the asset and settle the liability simultaneously. Offsetting income with expenses is allowed only if they

are part of the same entry.

8.12 Interest income and expensesInterest income and expense is recognized in the income statement on an accrual basis for all interest-bearing

instruments, using the effective interest method. The effective interest rate is the one that discounts exactly the

estimated future cash inflows or outflows during the estimated life of the financial instrument or, wherever

deemed appropriate, during a shorter period, on the basis of the net carrying value of the financial asset or

liability. In order to calculate the effective rate, cash flow estimation takes into account the terms of the financial

instrument agreement, but not any future losses from credit risk.

Calculation includes the fees and the basis points paid or collected by the contracting parties and which

constitute an integral part of the effective interest rate, transaction costs, and other premiums and discounts.

MARFIN FACTORS & FORFAITERS

ANNUAL REPORT 2009

20

8.13 Fees and commisionsFee and commission income are recognized on an accrual basis when the relevant service has been provided

unless they influence the effective interest rate.

8.14 Net trading incomeNet trading income comprises gains less losses related to Factoring receivables.

8.15 Income Tax and Deferred TaxThe income tax charge involves current taxes, deferred ones and the differences of preceding financial years’ tax audit.

Income tax is recognized in the financial year’s income statement, except for the tax on transactions recognized

directly in equity, in which case it is recognized accordingly to equity. To assess the annual tax charge, all the

required adjustments on the accounting result are taken into account in order to establish the final taxable

income.

The current income taxes include short-term liabilities or claims vis-à-vis fiscal authorities pertaining to the

payable taxes on the year’s taxable income and any additional income taxes regarding previous financial years.

Current taxes are measured on the basis of tax rates and fiscal regulations in force during the corresponding

financial years, based on the yearly taxable profit.

Deferred taxes are the taxes or the tax relieves from the financial encumbrances or benefits of the financial year

in question, which have been allocated or shall be allocated to different financial years by tax authorities.

Deferred income tax is provided by using the liability method which is determined by the temporary differences

arising between the tax bases of assets and liabilities and their carrying amounts in the financial statements.

However, the deferred income tax is not accounted for if it arises from initial recognition of an asset or liability

in a transaction other than a business combination that at the time of the transaction affects neither accounting

nor taxable profit or loss.

Deferred tax assets and liabilities are measured at the tax rates that are expected to apply to the period when

the asset is realized or the liability is settled, based on tax rates (and tax laws) that have been enacted or

substantively enacted by the balance sheet date. In case it is not possible to clearly determine the time needed

to invert the temporary differences, the tax rate to be applied is the one in force on the financial year after the

balance sheet date.

Deferred income tax assets are recognized to the extent that it is probable that future taxable profit will be

available against which the temporary differences can be utilized.

Most of the changes in the deferred tax assets or liabilities are identified as a part of tax charges in the income

statement.

8.16 Share CapitalOrdinary shares are classified as equity. Incremental costs directly attributable to the issue of new shares or

options are shown in equity as a deduction, free of tax, from the proceeds.

MARFIN FACTORS & FORFAITERS

ANNUAL REPORT 2009

21

The preparation of financial statements in accordance with the I.F.R.S. requires estimates and assumptions

being made by Management during the implementation of the Company’s accounting policies.

The following areas are affected by Management’s estimates and assumptions:

Impairement of Financial assetsFinancial assets and liabilities fair value calculation for which there are no published market prices requires the

use of specific measurement techniques. Fair value calculation calls for various kinds of assessments. The most

important ones involve assessment of various risks an instrument is subject to, such as credit risk, interest rate

risk, currency risk etc.

In the following part the segments in which estimates and assumptions by Management have a significant effect

are assessed:

a. Credit risk provisions

The Company continuously examines total Factoring advances and receivables and Forfaiting prepaid receivables

in order to decide whether their value is impaired or not.

This decision requires an exercise of significant judgment, through which the Company assesses, along with

other factors, whether a fair value of an asset is below cost, a fact that constitutes an objective evidence of

impairment.

b. Estimates on fair value of financial instruments

Financial assets and liabilities fair value calculation for which there are no published market prices requires the

use of specific measurement techniques. Fair value calculation calls for various kinds of assessments. The most

important ones involve assessment of various risks an instrument is subject to, such as credit risk, interest rate

risk, currency risk etc.

c. Defined benefit plans

The liability recognized in the balance sheet for defined benefit plans is the present value of the liability for the

defined benefit less the plan assets’ fair value (reserve from payments to an insurance company), the changes

deriving from any actuarial profit or loss and the service cost. The defined benefit commitment is calculated on

an annual basis by an independent actuary with the use of the projected unit credit method.

d. Income Tax

The Company is subject to income tax in the countries in which it operates. In order to establish the current and

deferred tax, as presented in the balance sheet, significant assumptions are required. For specific transactions

and calculations the ultimate tax determination is uncertain. The Company recognizes liabilities for anticipated

tax issues based on estimates of whether additional taxes will be due. Where the final tax outcome of these

matters is different from the amounts that were initially recorded, such differences will impact the income tax

and deferred tax provisions in the period in which such determination is made.

MARFIN FACTORS & FORFAITERS

ANNUAL REPORT 2009

22

Management estimations & assumptions9.

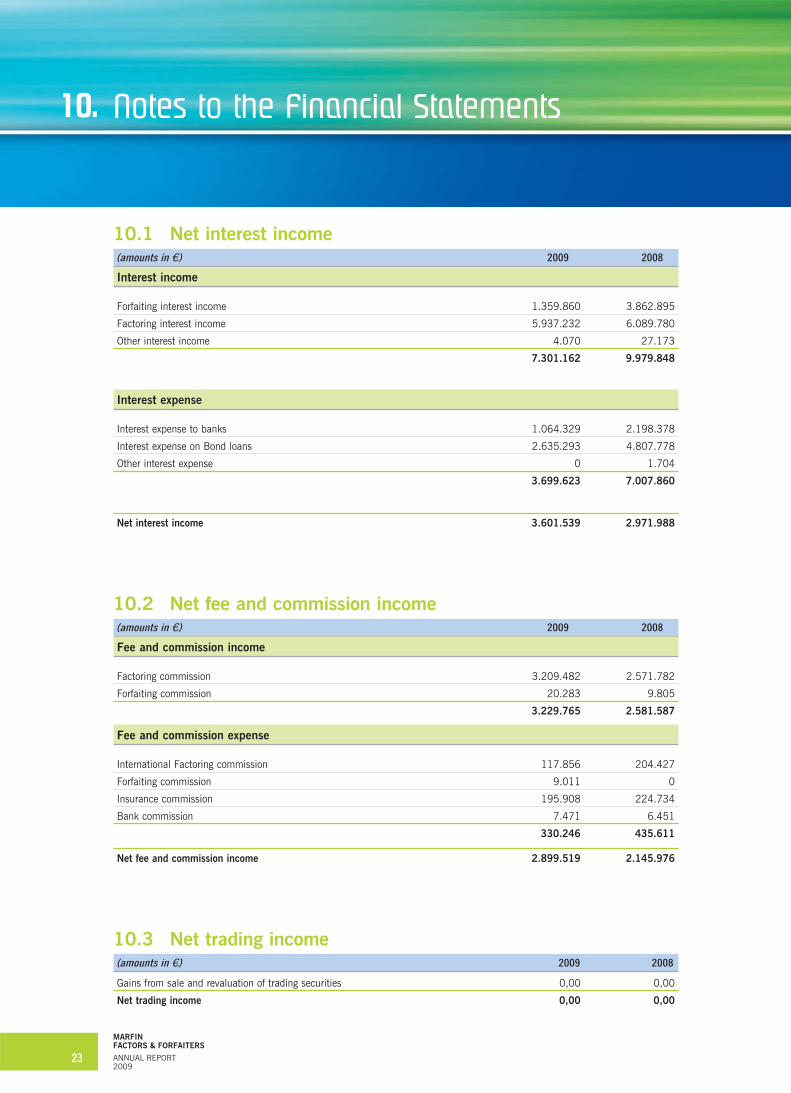

10.1 Net interest income(amounts in ú) 2009 2008

Interest income

Forfaiting interest income 1.359.860 3.862.895

Factoring interest income 5.937.232 6.089.780

Other interest income 4.070 27.173

7.301.162 9.979.848

Interest expense

Interest expense to banks 1.064.329 2.198.378

Interest expense on Bond loans 2.635.293 4.807.778

Other interest expense 0 1.704

3.699.623 7.007.860

Net interest income 3.601.539 2.971.988

10.2 Net fee and commission income(amounts in ú) 2009 2008

Fee and commission income

Factoring commission 3.209.482 2.571.782

Forfaiting commission 20.283 9.805

3.229.765 2.581.587

Fee and commission expense

International Factoring commission 117.856 204.427

Forfaiting commission 9.011 0

Insurance commission 195.908 224.734

Bank commission 7.471 6.451

330.246 435.611

Net fee and commission income 2.899.519 2.145.976

10.3 Net trading income(amounts in ú) 2009 2008

Gains from sale and revaluation of trading securities 0,00 0,00

Net trading income 0,00 0,00

MARFIN FACTORS & FORFAITERS

ANNUAL REPORT 2009

23

Notes to the Financial Statements10.

10.4 Other income-expenses(amounts in ú) 2009 2008

Foreign exchange differences -94.542 33.072

Forfaiting trading income 24.118 44.373

Other income 34.801 33.527

Other Income -32.623 110.972

10.5 Staff costs(amounts in ú) 2009 2008

Wages and salaries -1.327.977 -1.278.946

Defined benefit plan expense – Social security contributions -271.380 -247.642

Employee benefits -219.364 -470.557

Provision for post employment benefits -12.678 -12.684

Stock options plan expense -43.337 -55.812

Employee insurance expenses -25.952 -26.908

Vehicle leases -64.786 -62.186

Other expenses -93.903 -52.823

Staff costs -2.059.377 -2.207.557

The number of employees as at the end of the year was 41 (2008: 41)

Some 2008 figures have been reclassified for comparability reasons, having however no significant effect on

financial statements or accounts presented above.

Share based payments

In May, 2007 the Management of the parent company Marfin Popular Bank prepared a stock option provision

plan to the employees of all the companies of the Group, based on the as at 5/4/07 decision of the Extraordinary

General Assembly of its shareholders. Based on the criteria that were established, the options in question are

provided gradually within the five year period of 2007-2011. The Options with an exercise price of ú 10 on the

parent company’s shares and maturity date December 15, 2011 can be exercised by the holders during the

years 2007 to 2011.

The fair value of the options provided to the personnel has been measured as at the provision date based on the

estimation model of Black & Scholes from specialists of the parent Company MARFIN EGNATIA BANK S.A.

The employees of Marfin Factors & Forfaiters can exercise these options, if they want to. During this annual

period no option was exercised.

The total fair value of all the options provided that burden the results of the year 2009, was computed as that

of ú 43.337,04 (2008: ú 55.812,00).

MARFIN FACTORS & FORFAITERS

ANNUAL REPORT 2009

24

10.6 Administrative expenses(amounts in ú) 2009 2008

Rent (operating expense) -239.372 -206.755

Taxes stamps and duties -21.064 -67.471

Repairs and Maintenance -52.032 -27.119

Third party fees (legal, advisory, audits, etc) -345.618 -132.205

Telephone and postage -40.842 -35.157

Promotion and advertisement -23.523 -4.218

Travel and transportation expenses -60.693 -56.326

Subscription – Contribution payment -34.215 -18.146

Office supplies -23.262 -21.568

Conventions Expenses -30.602 -44.135

Prior years expenses -28 -287.186

Other expenses -103.315 -161.259

Administrative expenses -974.567 -1.061.546

Some 2008 figures have been reclassified for comparability reasons, having however no significant effect on

financial statements or accounts presented above.

10.7 Impairment of advances and receivables(amounts in ú) 2009 2008

Impairment of receivables -1.923.799 -1.198.834

Impairment losses -1.923.799 -1.198.834

MARFIN FACTORS & FORFAITERS

ANNUAL REPORT 2009

25

10.8 Taxes(amounts in ú) 2009 2008

Income Tax -511.689 -289.920

Prior years income Tax -174.292 -28.764

Deferred tax 37.747

Income tax -685.982 -280.937

The information concerning the deferred tax is provided in note 10.15.

The reconciliation of the effective tax rate is as follows:

(amounts in ú) % 2009 % 2008

Profits before tax 1.407.917 641.685

Tax based on tax rate 25% -351.979 25% -160.421

Not deductable expenses 11% -159.710 19% -120.516

Prior years income Tax 12% -174.292

Income tax 49% -685.982 44% -280.937

In Greece, the results reported to the tax authorities by an entity are provisional and subject to revision until

such time as the tax authorities examine the books and records of the entity and the related tax returns are

accepted as final. Therefore entities remain contingently liable for additional taxes and penalties, which may be

assessed upon such examination.

10.9 Cash and cash equivalents(amounts in ú) 2009 2008

Deposits in Banks 3.342.238 1.681.240

Cash 210 190

Cash and cash equivalents 3.342.448 1.681.430

MARFIN FACTORS & FORFAITERS

ANNUAL REPORT 2009

26

10.10 Cash advances to Factoring customers(amounts in ú) 2009 2008

Building and Construction companies 857.633 1.628.213

Manufacturing companies 26.710.431 25.188.667

Commercial companies 139.207.884 128.844.828

Services companies 9.928.030 11.911.959

Shipping and Maritime companies 3.681 2.145.420

Agriculture 36.707.995

Transportation 9.854.476

Other 19.223.355 6.853.223

Total Advances to customers 242.493.487 176.572.310

Less: Impairment loss 2.014.421 3.844.596

Advances to customers 240.479.066 172.727.714

Provisions account movements

(amounts in ú) 2009 2008

Balance brought forward 3.844.596 3.202.883

Impairment 1.218.000 1.198.834

Recovered amounts -139.201

Write-off -2.908.975 -557.120

Balance as at 31/12/2009 2.014.421 3.844.596

(amounts in ú) 2009 2008

Short-term advances 241.415.529 175.874.421

Long-term advances 1.077.958 697.889

242.493.487 176.572.310

MARFIN FACTORS & FORFAITERS

ANNUAL REPORT 2009

27

10.11 Non recourse FactoringFactored receivables without recourse are trade receivables that the Company has purchased from third parties

(customers/sellers) during its ordinary course of operation. The Company manages the whole account and

collects these receivables from the various buyers, without however having the right of recourse to the seller, in

the case that the buyer has a financial inability to meet his debt. The respective amounts and their analysis for

the financial period ended at December 31st 2009 and December 31st 2008 are shown in the following table.

(amounts in ú) 2009 2008

Domestic non recourse Factoring 4.460.184 8.533.193

Imported non recourse Factoring 8.260.076 5.808.918

Total 12.720.260 14.342.111

(amounts in ú) 2009 2008

Short-term accounts 12.720.260 14.342.111

Long-term accounts - -

12.720.260 14.342.111

10.12 Forfaiting Portfolio(amounts in ú) 2009 2008

Forfaiting advances to customers 8.805.630 42.114.078

Forfaiting advances to customers under revision for impairement 11.708.318

Total Forfaiting Portfolio 20.513.948 42.114.078

Less: Impairment loss 845.000

Total Forfaiting Portfolio 19.668.948 42.114.078

Provisions account movements

(amounts in ú) 2009 2008

Balance brought forward

Impairment 845.000

Write-off

Balance as at 31/12/2009 845.000 0

(amounts in ú) 2009 2008

Short-term amounts 6.541.678 20.553.415

Long-term amounts 13.972.270 21.560.663

20.513.948 42.114.078

MARFIN FACTORS & FORFAITERS

ANNUAL REPORT 2009

28

Forfaiting is a form of an export trading credit in which the Forfaiter purchase assets from the exporter, without

recourse, at 100% of its value, at full discount. Under the Forfaiting agreement, the exporter, or a Forfaiter sells

to MARFIN Factors & Forfaiters a trade receivable evidenced by a commercial drafts, such as Bill of Exchange,

Promissory Note and Letter of Credit, usually accompanied by a bank guarantee for the foreign buyer. The seller

is only responsible for the actual existence of the transaction. These receivables have a medium-long term

maturity (from 6 months up to 5 years) and can be exchanged between Forfaiting companies in the secondary

market. The total value of the forfaiting assests on the 31st of December 2009 amounted ú 19.668.947,70

while in 2008 the respective value was ú 42.114.077,95.

Forfating receivables under impairment include receivable from banks in Kazakhstan for which an international

effort for debt restructuring is in process. The debt restructuring negotiations are expected to finalize within the

first half of 2010. Upon completion of the process, the aforementioned receivables are expected to be

substituted with a new set of assets that could not be defined at the time of preparation of the financial

statements. The impairment test of the aforementioned receivables has been performed with the information

available and according to management estimates until the date of the publication of the financial statements.

MARFIN FACTORS & FORFAITERS

ANNUAL REPORT 2009

29

10.13 Intangible Assets(amounts in ú) Software Total

Acquisition Cost

Balance as at 1 January, 2008 484.261 484.261

Additions 28.417 28.417

Disposals

Balance as at 31 January, 2008 512.678 512.678

Acquisition Cost

Balance as at 1 January, 2009 512.678 512.678

Additions 47.200 47.200

Disposals

Balance as at 31 January, 2009 559.878 559.878

Accumulated amortization

Balance as at 1 January, 2008 440.538 440.538

Amortization 21.648 21.648

Disposals - -

Balance as at 31 January, 2008 462.186 462.186

Accumulated amortization

Balance as at 1 January, 2009 462.186 462.186

Amortization 24.650 24.650

Disposals - -

Balance as at 31 January, 2009 486.836 486.836

Carrying amounts

As at 1 January, 2008 43.723 43.723

As at 31 January, 2008 50.492 50.492

As at 1 January, 2009 50.492 50.492

As at 31 January, 2009 73.042 73.042

MARFIN FACTORS & FORFAITERS

ANNUAL REPORT 2009

30

10.14 Property, Plant and Equipment(amounts in ú) Improvements Furniture PPE

on third party and construction

property equipment projects Other Total

Acquisition Cost

Balance as at 1 January, 2008 352.992 291.038 476 4.610 649.116

Additions - 40.331 1.863 29.804 71.997

Disposals - - - - -

Balance as at 31 January, 2008 352.992 331.368 2.339 34.414 721.114

Acquisition Cost

Balance as at 1 January, 2009 352.992 331.368 2.339 34.414 721.114

Additions - 1.884 3.862 0 5.746

Disposals - - - - -

Balance as at 31 January, 2009 352.992 333.253 6.201 34.414 726.860

Depreciation

Balance as at January 1, 2008 20.828 178.138 - 173 199.140

Annual depreciation 39.074 54.225 - 3.175 96.474

Decreases -

Balance as at 31 December, 2008 59.902 232.363 - 3.348 295.614

Depreciation

Balance as at January 1,2009 59.902 232.363 - 3.348 295.614

Annual depreciation 39.074 34.385 - 4.665 78.124

Decreases -

Balance as at 31 December, 2009 98.976 266.748 0 8.013 373.738

Amounts in the Balance Sheet

As at 1 January, 2008 332.164,17 112.899,26 476,30 4.437,13 449.976,86

As at 31 December, 2008 293.090,13 99.005,08 2.339,30 31.065,67 425.500,18

As at 1 January, 2009 293.090,13 99.005,08 2.339,30 31.065,67 425.500,18

As at 31 December, 2009 254.016,09 66.504,37 6.201,00 26.400,27 353.121,73

MARFIN FACTORS & FORFAITERS

ANNUAL REPORT 2009

31

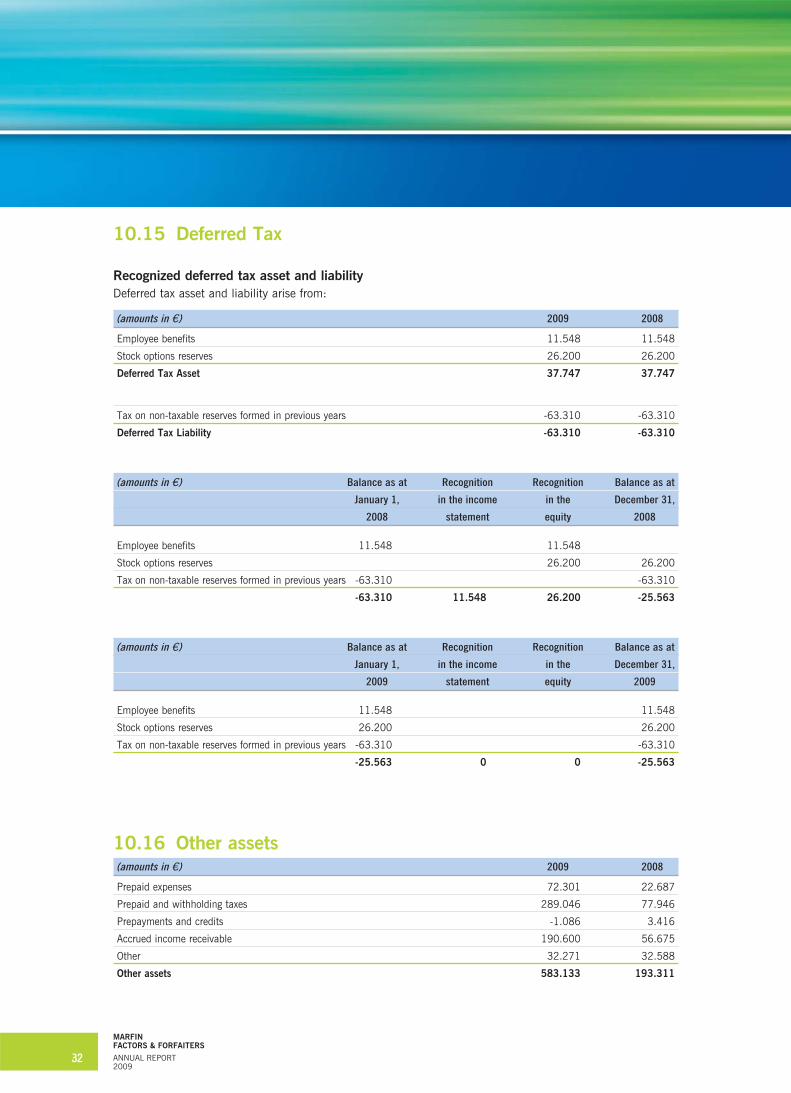

10.15 Deferred Tax

Recognized deferred tax asset and liability

Deferred tax asset and liability arise from:

(amounts in ú) 2009 2008

Employee benefits 11.548 11.548

Stock options reserves 26.200 26.200

Deferred Tax Asset 37.747 37.747

Tax on non-taxable reserves formed in previous years -63.310 -63.310

Deferred Tax Liability -63.310 -63.310

(amounts in ú) Balance as at Recognition Recognition Balance as at

January 1, in the income in the December 31,

2008 statement equity 2008

Employee benefits 11.548 11.548

Stock options reserves 26.200 26.200

Tax on non-taxable reserves formed in previous years -63.310 -63.310

-63.310 11.548 26.200 -25.563

(amounts in ú) Balance as at Recognition Recognition Balance as at

January 1, in the income in the December 31,

2009 statement equity 2009

Employee benefits 11.548 11.548

Stock options reserves 26.200 26.200

Tax on non-taxable reserves formed in previous years -63.310 -63.310

-25.563 0 0 -25.563

10.16 Other assets(amounts in ú) 2009 2008

Prepaid expenses 72.301 22.687

Prepaid and withholding taxes 289.046 77.946

Prepayments and credits -1.086 3.416

Accrued income receivable 190.600 56.675

Other 32.271 32.588

Other assets 583.133 193.311

MARFIN FACTORS & FORFAITERS

ANNUAL REPORT 2009

32

10.17 Due to banks(amounts in ú) 2009 2008

Due to banks 112.933.367 75.120.434

Total liabilities 112.933.367 75.120.434

The Company’s liabilities to Banks refer to the Company’s liabilities to the parent company, Marfin Egnatia Bank.

10.18 Dept securities in issue and other borrowed funds(amounts in ú) 2009 2008

Bonds 132.633.625 126.256.449

Dept securities in issue and other borrowed funds 132.633.625 126.256.449

The Company has contracted six bond loans, three of which (A-C) with its parent company Marfin Egnatia Bank

and the other three (D-F) with its parent company Marfin Egnatia Bank and IBG.

A) A bond amounting to EUR 18,000,000 was issued on December, 2006. It has an interest

rate based on a three-month Euribor (3M) (Year average 1,225%) and maturity three years.

It has been fully paid off during 2009.

B) A bond amounting to Euro 40,000,000 was issued on August, 2007. It has an interest rate

of one-month Euribor (1M) (Year average 0,894%) and maturity two years. It has been fully

paid off during 2009.

C) A bond amounting to USD 13,740,000 was issued on August 2007. It has an interest rate

of one-month Libor/USD (1M) (Year average 0,334%) and maturity two years. It has been

fully paid off during 2009.

D) A bond amounting to EUR 50.000.000 was issued on May, 2008. It has an interest rate of

one-month Euribor (1M) (Year average 0,894%) and maturity two years.

E) A bond amounting to USD 20.000.000 was issued on December, 2008. During 2009

another USD 10.000.000 were added to the existing USD 20.000.000,00. It has an interest

rate of one-month Libor/USD (1M) (Year average 0,334%) and maturity two years. In 2009

the Company paid off USD 18.200.000,00. The effective exchange rate on December 31,

2008 was (1,4406) and the bond was measured at EUR 12.633.624,88.

F) A bond amounting to EUR 70.000.000 was issued on March 2009. It has an interest rate

of one-month Euribor (1M) (Year March-December 0,7%) and maturity two years.

MARFIN FACTORS & FORFAITERS

ANNUAL REPORT 2009

33

10.19 Factoring liabilities The liabilities to customers refer to the Company’s obligations of the third parties, due to its ordinary course of

operation. Such liabilities have been created by the purchase of receivables for which the Company has the right

to manage and collect from the buyer, without however having the right to pursue collection from the seller in

the case that the buyer is unable to pay his debt. The respective amounts and their analysis for the financial

period ended at December 31st 2009 and December 31st 2008 are shown in the following table.

(amounts in ú) 2009 2008

Domestic non recourse Factoring 5.140.343 8.533.193

Imported non recourse Factoring 8.473.032 5.808.918

Domestic recourse Factoring 241.440

Domestic recourse Factoring 215.690

Total 14.070.505 14.342.111

(amounts in ú) 2009 2008

Short-term amounts 14.070.505 14.342.111

Long-term amounts - -

14.070.505 14.342.111

10.20 Provision for post-employment benefits(amounts in ú) 2009 2008

Obligation as at 1st January 46.190 31.802

Expenses recognized in income statement 12.659 14.388

Obligation as at December 31st 58.849 46.190

(amounts in ú) 2009 2008

Expenses recognized in income statement

Service costs (payroll and staff cost) 10.393 12.684

Interest and related expenses 2.285 1.704

12.678 14.388

Principal actuarial assumptions used for 2009 and 2008 were as follows:

2009 2008

Discount rate 5.50% 5.50%

Salary increases 4.00% 4.00%

MARFIN FACTORS & FORFAITERS

ANNUAL REPORT 2009

34

10.21 Other provisions(amounts in ú) 2009 2008

Other personel provisions 30.000 30.000

Provisions for non deductable amounts 128.000 28.000

Other provisions 158.000 58.000

(amounts in ú) 2009 2008

Long-term amounts 100.000 -

Short-term amounts 58.000 58.000

158.000 58.000

10.22 Other liabilities(amounts in ú) 2009 2008

Taxes and duties (non income tax) 491.378 480.886

Due to social security funds 55.809 51.492

Suppliers and other creditors 131.126 140.386

Accrued expense 297.030 363.362

Interest payable 66.512 171.520

Cheques and orders payable 0 0

Other liabilities 772.478 -60.490

Other liabilities 1.814.333 1.147.156

10.23 Share capital(amounts in ú) 31.12.2009 31.12.2008

Number of ordinary shares 3.710.000 3.710.000

Nominal value 2,93 2,93

Total Share capital 10.870.300 10.870.300

MARFIN FACTORS & FORFAITERS

ANNUAL REPORT 2009

35

10.24 Reserves(amounts in ú) 2009 2008

Statutory reserve 207.009 182.946

Untaxed reserves 981 981

Reserves from specially taxed income (1999) 55.847 55.847

Reserves from specially taxed income (2000) 10.739 10.739

Reserves from specially taxed income (2001) 1.705 1.705

Reserves from discounts on one-off tax payments 33.765 33.765

Stock options reserves 148.135 104.798

Special reserves 9.406 9.406

Reserves 467.588 400.187

Statutory reserve: Under the provisions of corporate law, entities are required to transfer 5% of their annual

profits to a statutory reserve until the reserve equals one third of the issued capital. This reserve is not available

for distribution but may be applied to cover losses.

Untaxed reserves: In the event that the reserves are distributed they will be taxed at the rate applicable on the

date of distribution.

MARFIN FACTORS & FORFAITERS

ANNUAL REPORT 2009

36

Group of the parent Marfin Egnatia Bank(amounts in ú) 31.12.2009 31.12.2008

ASSETS

Loans and advances to banks 2.584.114 1.223.100

Total assets 2.584.114 1.223.100

LIABILITIES

Due to Banks 245.566.992 201.376.882

Total liabilities 245.566.992 201.376.882

(amounts in ú) 1.1-31.12.2009 1.1-31.12.2008

INCOME

Interest and similar income 3.704 27.173

Commission income 2.385 84

Total income 6.089 27.257

EXPENSES

Interest and similar expenses 3.609.514 6.805.925

Commission expenses 8.191 192.205

Other expenses 25.943 5.300

Total expenses 3.643.648 7.003.429

Some 2008 figures have been reclassified for comparability reasons, having however no significant effect on

financial statements or accounts presented above.

(amounts in ú) 2009 2008

Key management compensation

Salaries & Social Insurance payments 308.392 301.308

Extraordinary payments 120.000 342.320

Stock options 29.470 38.000

Total 457.862 681.628

MARFIN FACTORS & FORFAITERS

ANNUAL REPORT 2009

37

Related parties transaction11.

The fair value represents the amount for which an asset could be exchanged, or a liability settled, between

knowledgeable, willing parties in an arm’s length transaction. Differences might arise between the carrying

amount and the fair value of financial assets and liabilities.

Receivables and other advances and financial liabilities are presented at amortized cost. The carrying amount

of the aforementioned items, as presented in the financial statements, does not materially differ from their fair

value. In particular:

(a) Cash and cash equivalents

Loans and advances to bank mainly include short tern interbank placements and other collectibles. The fair

value of those placements and collectibles is quite similar to their carrying amount

(b) Recourse Factoring

Recourse Factoring is presented following the deduction of the corresponding provision for impairment. All the

receivables have a fluctuating interest.

(c) Non-recourse Factoring

Non recourse Factoring is measured at amortized cost. All such receivables have a fluctuating interest and are

measured at amortized cost.

(d) Forfaiting Portfolio

Forfaiting portfolio is measured at amortized cost. Such receivables may have a fluctuating interest or a fixed

interest.

(e) Debt securities and other borrowed funds.

All bonds and loans bear fluctuating interest rate. Therefore, the fair value of the bonds is quite similar to their

carrying amount.

MARFIN FACTORS & FORFAITERS

ANNUAL REPORT 2009

38

Fair value of financial assets and liabilities12.

As every credit institution, the Company is exposed to many kind of risks, such as credit risk, currency risk,

interest rate risk, as explained below. Those risks are constantly monitored in various ways in order to avoid

undue risk concentrations. Primarily, they are monitored by the company’s Management, and secondarily by the

relevant Division of the mother Bank, Marfin Egnatia Bank. Below, further information on the description of

extent and nature of financial risks faced by the Company together with the comparative data concerning the

prior period, is presented.

13.1 Credit riskCredit risk is the risk of loss resulting from counter party default, or when counterparty fails to meet their

contractual obligations. The counterparties may be buyers or sellers. The undertaking of credit risk is based on

international recognized practices and Factoring criteria whose purpose is the transparency of transactions and

the recognition of risk.

Credit risk management

The company structures the levels of acceptable credit risk based on the financial analysis of the borrower or

the group of borrowers, their industry, their position in the market and the dispersion of their credit risks.

The company structures the levels of acceptable credit risk based on the financial analysis of the borrower or

the group of borrowers, their industry, their position in the market and the dispersion of their credit risks.

The determination of credit limits and charges to the customers is affected primarily by the type of factoring

service that will be provided. Factoring services are classified in terms of risk, as follows:

Recourse Factoring

In Recourse Factoring the Company has the right to go back to the seller (borrower) to collect its claims. This

way, the credit risk the company assumes against the debtor is mitigated.

Non recourse Factoring

The provision of non-recourse factoring services implies that the credit risk has been assumed by the Factoring

Company, in the case that the debtor (customer) becomes insolvent.

For non-recourse Factoring Services provided to its customers, Marfin Factors & Forfaiters after examining each

case accordingly, obtains insurance coverage for credit risk.

The Company reassesses the credit and advance limits approved on the basis of the customer’s creditworthiness

at regular intervals.

Forfaiting

The aforementioned procedures about Non recourse Factoring apply accordingly to Forfaiting operations with the

substitution, at some cases, of insurance coverage with bank coverage (e.g. avalised Promisory note).

Internationally recognized methods are applied to monitor the creditworthiness of the Bank providing coverage

or/and the debtor.

MARFIN FACTORS & FORFAITERS

ANNUAL REPORT 2009

39

Financial risk management13.

Highest exposure to credit risk prior to calculation of collaterals and other credit risk protection

measures

The table below presents the highest exposure of the Company to credit risk arising from trade receivables as

presented in the balance sheet. As far as the trade receivables presented in the balance sheet are concerned,

the exposure to credit risk equals their carrying amount

(amounts in ú) 2009 2008

Highest exposure

Exposure to credit risk of the Balance Sheet items:

Forfaiting portfolio 20.513.948 42.114.078

Less: Impairement loss -845.000

(a) Total forfaiting Portfolio 19.668.948 42.114.078

(b) Non recourse Factoring 12.720.260 14.342.111

(c) Advances to customers (after provisions)

Construction companies 857.633 1.628.213

Industries 26.710.431 25.188.667

Commercial companies 139.207.884 128.844.828

Service companies 9.928.030 11.911.959

Shipping and Maritime companies 3.681 2.145.420

Agriculture/Fishing 36.707.995

Transportation/Communication 9.854.476

Other 19.223.355 6.853.223

Impairment 2.014.421 -3.844.596

Advances to customers 240.479.066 172.727.714

Total Assets (a+b+c) 272.868.273 229.183.903

Cash advances to customers and non recourse Factoring

The table below presents the nature of advances and receivables of the Company, as well as the non-recourse

Factoring activity.

(amounts in ú) 2009 2008

Advances Non-recourse Advances Non-recourse

to customers Factoring to customers Factoring

Receivables Receivables

Cash advances without delay and impairment (i) 238.323.151 12.720.260 171.331.935 14.342.111

Delayed but not impaired (ii) 1.077.958 0 697.889 0

Impaired (iii) 3.092.378 0 4.542.486 0

Cash advances before provisions 242.493.487 0 176.572.310 0

Provision for impairment 2.014.421 0 3.844.596 0

Total Cash advances after provisions 240.479.066 12.720.260 172.727.714 14.342.111

MARFIN FACTORS & FORFAITERS

ANNUAL REPORT 2009

40

Cash advances and Factoring past but not impaired

The total Cash advances and Factoring receivables past due but not impaired for the year ended on 31st

December 2009 has a maturity over 6 months and is amounted ú 1.077.958. For the year ended on 31st