March 2014 BofAML 2014 Brazil Conference - Fibria ... · 432 448 471+ 473 505 2009 (2) 2010 (2)...

38

BofAML 2014 Brazil Conference March 2014

Transcript of March 2014 BofAML 2014 Brazil Conference - Fibria ... · 432 448 471+ 473 505 2009 (2) 2010 (2)...

BofAML 2014 Brazil Conference March 2014

The information contained in this presentation may include statements which constitute forward-looking statements, within the meaning of Section 27A of the U.S. Securities Act of 1933, as amended, and Section 21E of the U.S. Securities Exchange Act of 1934, as amended. Such forward-looking statements involve a certain degree of risk and uncertainty with respect to business, financial, trend, strategy and other forecasts, and are based on assumptions, data or methods that, although considered reasonable by the company at the time, may turn out to be incorrect or imprecise, or may not be possible to realize. The company gives no assurance that expectations disclosed in this presentation will be confirmed. Prospective investors are cautioned that any such forward-looking statements are not guarantees of future performance and involve risks and uncertainties, and that actual results may differ materially from those in the forward-looking statements, due to a variety of factors, including, but not limited to, the risks of international business and other risks referred to in the company’s filings with the CVM and SEC. The company does not undertake, and specifically disclaims any obligation to update any forward-looking statements, which speak only for the date on which they are made.

Disclaimer

2

Agenda

Financial Highlights 1 Pulp and Paper Market 2 Final Remarks 3

Financial Highlights

1,370 1,347 1,358 1,510

1,301 1,441

4Q12 3Q13 4Q13

Production Sales

4Q13 Results

5

EBITDA (R$ million) and EBITDA Margin (%) Production Cash Cost (R$/t)

Pulp Production and Sales (‘000 t) Net Revenue (R$ million)

1,853 1,841 1,958

4Q12 3Q13 4Q13

Record

446

501 466

4Q12 3Q13 4Q13

+5% 41% 41% 42%

753 762

823

4Q12 3Q13 4Q13

Record

Indebtness

6

Net Debt (Million)

3.4 3.0 2.8

3.3 2.9 2.6

10,768 9,487 9,773

5,269 4,254 4,172

Dec/12 Sep/13 Dec/13

R$ US$

Debt Amortization Schedule (R$ million) – Dec./13 (1)

Gross Debt (Million)

7,745 8,240 7,849

6,946

3,790 3,695 3,351 2,965

Dec/12 Sep/13 Dec/13

R$ US$

Net Debt/EBITDA (US$) Net Debt/EBITDA (R$)

Dec/13 (Pro forma)

2.5

2.3

After Bond 2020

Repurchase

3,482

- 21% - 34%

1,471

903

1,924

4,298

1,474

834 830 1,256

976 762

2,169

1,441

26 5

Liquidity 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

Pre-Payment BNDES ECN Trade Finance (ST) Finnvera Bond

Revolver

Land sale (2)

Cash

(1) Does not consider the reclassification of the bond 2020 to the short term. (2) Pending payment related to the land sale.

Fibria delivered the most significant leverage reduction in the LTM

Net Debt/EBITDA (x)

3.9 3.6

2.9

3.2

4.2

4.8 5.2

4.7

4.5 3.4

3.1

3.3 3.0 2.8

4.7 4.7 5.0 5.1 5.1 5.2

2.4 2.6

2.9 3.0

2.8

3.7

3.1

3.8

Sep/10 Dec/10 Mar/11 Jun/11 Sep/11 Dec/11 Mar/12 Jun/12 Sep/12 Dec/12 Mar/13 Jun/13 Sep/13 Dec/13

Fibria Arauco CMPC Klabin Suzano

S&P BB+/Stable BBB-/Stable BBB/Negative BBB-/Stable BB/Negative

Moody’s Ba1/Positive Baa3/Negative Baa3/Negative - Ba2/Stable

Fitch BBB-/Stable BBB/Stable BBB+/Stable BBB-/Stable BB-/Positive

(1) 2013 projection by Citibank.

Ratings

7

Net Results (R$ million) – 4Q13

823 (444)

(185)

810

(5) (118)

(506)

(713) (32)

Adjusted EBITDA

Rev. (Exp.) non-recurring /

non-cash

Debt Exchange Variation /

MtM Hedge Debt

MtM Operational

Hedge

Net Interest Depreciation, amortization and depletion

IR/CS Other Net Profit (Loss)

Non-recurring impacts

(1) Include non-recurring expenses /non-cash, other exchange and currency variation and other financial incomes and expenditures.

(1)

∆

∆

Refis

Debt Hedge

Debt exchange variation

Excluding the non-recurring effects , profit would

reached approximately R$ 323 million at 4Q13.

8

9

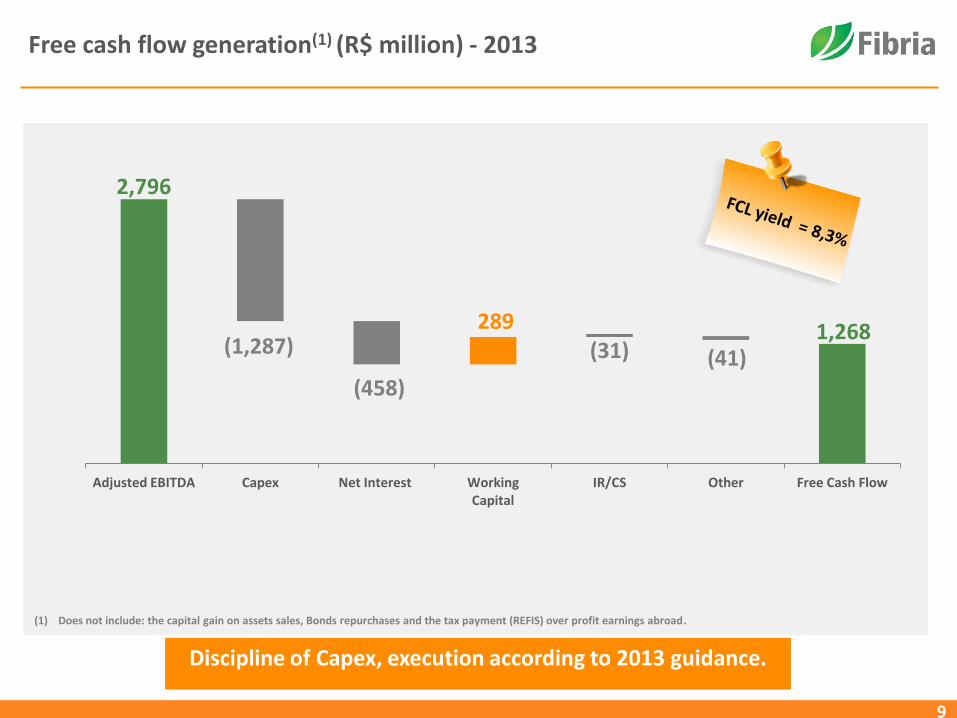

Free cash flow generation(1) (R$ million) - 2013

Discipline of Capex, execution according to 2013 guidance.

2,796

1,268 (1,287)

(458)

289 (31) (41)

Adjusted EBITDA Capex Net Interest Working Capital

IR/CS Other Free Cash Flow

(1) Does not include: the capital gain on assets sales, Bonds repurchases and the tax payment (REFIS) over profit earnings abroad.

Positive Free Cash Flow (1) (R$ million)

10

2013: R$ 1,268 million

230

-402

-149 -12

221 57 157

399

167 234

122

746

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13

1.64 1.59 Average 1.80 1.77 2.03 2.06 2.28 2.07 1.96 2.00

FX(R$/US$)

2.28 1.67

2012: R$ 836 million 2011: R$ -333 million

(1) Does not include: the capital gain on assets sales, Bonds repurchases and the tax payment (REFIS) over profit earnings abroad.

538

244

(248) (-88)

56

(6) (8)

Adjusted EBITDA Capex Net Interest Working Capital

IR/CS Other Free Cash Flow

11

Free Cash Flow per ton

Fibria delivers one of the highest EBITDA/t and FCF/t of the industry

2013 Results (R$/ton)

2.00 1.76 1.67

1.95 2.16

562

844 810 751 791

FX and Pulp Price explain 80% of Fibria’s EBITDA Margin

12

Average Price FOEX (US$/t)

Exchange Rate Average (R$/US$)

EBITDA Margin

EBITDA (R$ million)

29%

40%

34% 36% 40%

1,522

2,526

1,964 2,253

2,796

2009 (1) 2010 (1) 2011 (1) 2012 2013

(1) Excludes Conpacel

0%

5%

10%

15%

20%

25%

30%

5% 10% 15% 20% 25%

Exp

ect

ed

Re

turn

(%

p.a

.)

Volatility (% a.a.)

Efficient Frontier (1) with and w/o BHKP

Com Minério de Ferro Com BHKP e Minério de Ferro (1) Since 2009 (2) Considering the expected return of a portfolio comprised of: DJ, Ibovespa Index , Oil, Copper, Niquel, Libor 3M in US Dollar and BHKP.

Without Pulp With pulp and others

Pulp vs Other Commodities

10%

0% -2%

14%

0%

2%

-3% -6% -5%

-20%

-10%

0%

10%

20%

30%

40%

50%

Ibovespa LME Metals

WTI Crude Oil

Iron Ore Sugar Soy Cattle CPI Brazil CPI US

38%

32% 30%

26% 25% 21%

16%

8%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Sugar Iron Ore WTI Crude Oil

Soy LME Metals

Ibovespa Cattle FOEX PIX BHKP

Pulp price has the lowest historical volatility(1) among all commodities.

Considering pulp price in US$, a low correlation with hard commodities and traditional assets is observed.

With a low correlation the inclusion of BHKP in the portfolio expands the efficient frontier of a commodities portfolio(2).

Commodities Historical Volatility BHKP Correlation (USD)

13

Maintenance CAPEX (R$ Million)

1,416

1,078

1,287

1,520

2011 2012 2013 Land Deal:

Rural

Partnership

Non recurring

wood

purchase

Inflation FX Rate Modernization Others 2014E

Approx.

18% increase

14

Cash Production Cost saw an increase of 17% over the past 5 years

Cash Production Cost (1) (R$/ton)

432 448

471 473

505

2009 (2) 2010 (2) 2011 2012 2013

CAGR: + 17%

Inflation in the period : IPCA: +31%

Fibria’s Cash Cost: +17%

2014 Cash Production Cost:

• Wood costs will represent the main impact

• Non recurring increase mainly due to third party wood

• Operating excellence actions focused on keeping cash cost below inflation

• In 2015 the wood impact will be structurally eliminated

(1) Constant Currency (2) Excludes Conpacel

Target to have the cash cost increase below inflation

15

Fibria’s tax structure

Tax benefits (R$ million)

Fiscal - annual adjustment

Benefit Amount Maturity

Goodwill

(Aracruz

acquisition)

Annual tax deduction:

~R$85 million

Remaining Balance Dec./13:

R$ 1,35 billion (base)

2018

Forestry Capex in

Mato Grosso do

Sul state

2013’s tax deduction related

to depletion: R$29 million Undefined

Tax loss carry forward and tax credits

Benefit Amount

Tax loss

carryforward Balance up to Dec./13:

R$507 million (base)

Accumulated tax

credits

Balance Dec./2013:

-PIS/COFINS: R$542 million

- withholding tax (IR and

CSLL): R$226 million

Actual tax payment (cash basis)

16

2009 2010 2011 2012 2013

R$ 7 million R$ 16 million R$ 4 million R$ 15 million R$ 31 million

PULP

- Growth with discipline

- Best portfolio of projects

BIO-ENERGY

- Complementary to pulp

- Ensyn

INDUSTRY

CONSOLIDATION ?

OTHER OPPORTUNITIES

- Portocel

- Land and forest

Potential Growth

Prospects

17

Fibria is seeking value creation for its shareholders with capital discipline

Pulp and Paper Market

Today, according to public information, there will be a 9% increase

of the market pulp capacity between 2013 and 2015

(1) Source: PPPC Special Research Note November 2013 – does not include Sulphite and UKP (2) Projects included: Ilim Group (490kt)| Closures: Resolute Forest (75kt) ; Domtar (125kt) ; Rayonier (280kt); Sodra Tofte (240kt) (3) Projects included: Eldorado (1.5 mt); UPM Fray Bentos (100kt); Maranhão (1.5mt); Montes del Plata (1.3 mt); Oji Nantong (700kt); Guaíba II (1.3 mt) | Closures: Jari (410kt); Cellulose du

Maroc (140kt); Ilim Group (100kt); Double A (85kt); Sappi Cloquet (270kt); Sodra Tofte (180kt); April Rizhao (130kt)

SOFTWOOD(1)

25.0 MT

HARDWOOD(1)

30.3 MT

MARKET PULP(1)

55.3 MT + =

2013-2015(3):

• New capacities: 6.4 mt • Announced Closures: (1.3) mt

Net: 5.1 mt

2013-2015(2): • New capacities: 0.5 mt

• Announced Closures: (0.7) mt

Net: (0.2) mt

2013-2015:

• New capacities: 6.9 mt • Announced Closures: (2.0) mt

Net: 4.9 mt

19

Pulp Market

Shipments of Eucalyptus Pulp (1)

(1) Source: PPPC World 20 – December/2013

Sales Distribuition 2013 - Fibria

Producer Stocks – Hardwood(1)

(1) Source: PPPC World 20 – December/2013

NBSK vs. BHKP - Prices(1)

Europe 39%

North America

28%

Asia 25%

Others 9%

Per region

Tissue 53% Printing

& Writing 29%

Specialty 17%

Daily production

39 days

Nov/13: 40 days | Dec/12: 35 days

Per end use

400

500

600

700

800

900

1,000

1,100

0

50

100

150

200

250

jan

-08

mai

-08

set-

08

jan

-09

mai

-09

set-

09

jan

-10

mai

-10

set-

10

jan

-11

mai

-11

set-

11

jan

-12

mai

-12

set-

12

jan

-13

mai

-13

set-

13

Gap NBSK/BHKP Average Spread NBSK BHKP

Spread Dez/13: US$ 136

(1) Source: FOEX

Average Spread: US$ 88

0

10

20

30

40

50

60

05 06 07 08 09 10 11 12 13

20

6%

12%

-1%

23%

Total North America Western Europe China

+844kt

-37kt

+674kt

2013 vs. 2012

+196kt

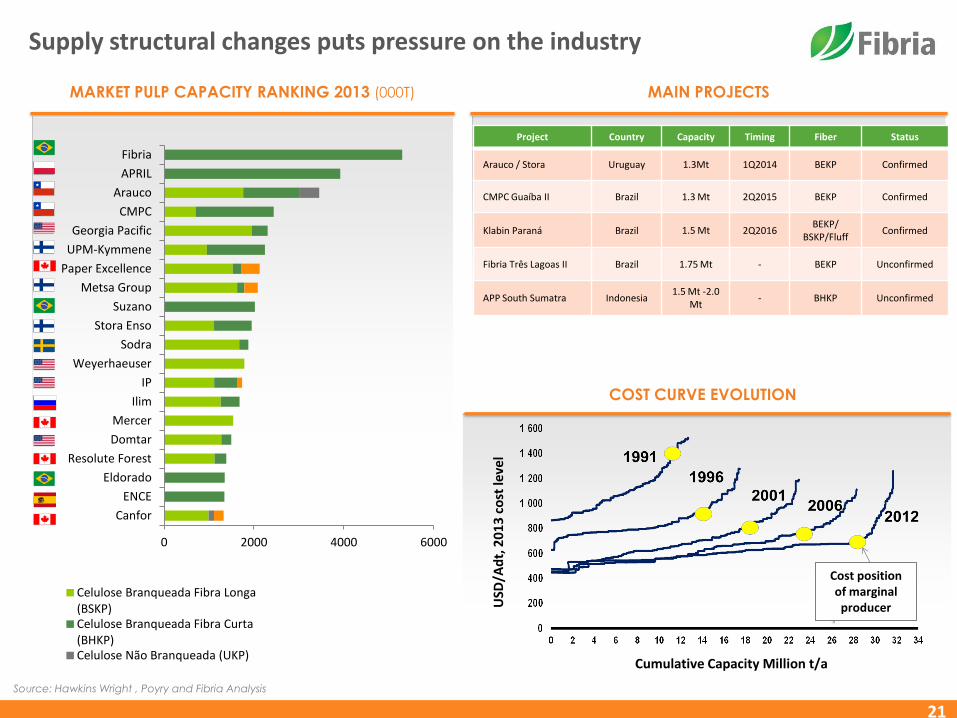

Supply structural changes puts pressure on the industry

21

MARKET PULP CAPACITY RANKING 2013 (000T) MAIN PROJECTS

Project Country Capacity Timing Fiber Status

Arauco / Stora Uruguay 1.3Mt 1Q2014 BEKP Confirmed

CMPC Guaíba II Brazil 1.3 Mt 2Q2015 BEKP Confirmed

Klabin Paraná Brazil 1.5 Mt 2Q2016 BEKP/

BSKP/Fluff Confirmed

Fibria Três Lagoas II Brazil 1.75 Mt - BEKP Unconfirmed

APP South Sumatra Indonesia 1.5 Mt -2.0

Mt - BHKP Unconfirmed

COST CURVE EVOLUTION

USD

/Ad

t, 2

01

3 c

ost

leve

l

Cumulative Capacity Million t/a

Cost position of marginal

producer

Source: Hawkins Wright , Poyry and Fibria Analysis

0 2000 4000 6000

Canfor

ENCE

Eldorado

Resolute Forest

Domtar

Mercer

Ilim

IP

Weyerhaeuser

Sodra

Stora Enso

Suzano

Metsa Group

Paper Excellence

UPM-Kymmene

Georgia Pacific

CMPC

Arauco

APRIL

Fibria

Celulose Branqueada Fibra Longa (BSKP) Celulose Branqueada Fibra Curta (BHKP) Celulose Não Branqueada (UKP)

-910

-85

-1260

-1180

-540 -500

-105

-1200

-1400

-1200

-1000

-800

-600

-400

-200

0

2006 2007 2008 2009 2010 2011 2012 2013-2015E

Capacity closures DO happen…

22

Source: PPPC and Fibria

Closures of Hardwood Capacity Worldwide 000 ton

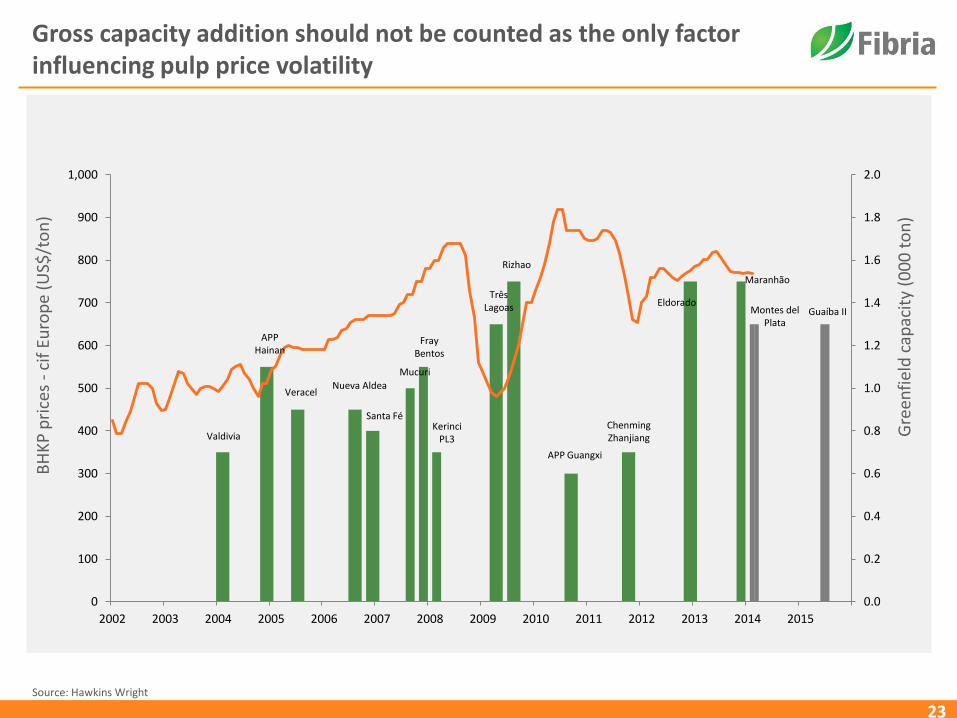

Gross capacity addition should not be counted as the only factor influencing pulp price volatility

Source: Hawkins Wright

BH

KP

pri

ces

- ci

f Eu

rop

e (U

S$/t

on

)

Gre

enfi

eld

cap

acit

y (0

00

to

n)

23

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

0

100

200

300

400

500

600

700

800

900

1,000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Valdivia

APP Hainan

Veracel Nueva Aldea

Santa Fé

Mucuri

Fray Bentos

Kerinci PL3

Três Lagoas

Rizhao

APP Guangxi

Chenming Zhanjiang

Eldorado Montes del

Plata

Maranhão

Guaíba II

Technical Age and Scale in the Market Pulp Industry Further closures are expected due to lack of adequate investments in the industry…

Hardwood (BHKP) Market Pulp Softwood (BSKP) Market Pulp

Source: Poÿry & Fibria

24

0

500

1,000

1,500

2,000

2,500

3,000

0 5 10 15 20 25 30

PM Capacity, 1000 t/a

Technical Age, years

STRONG

2013/IQ

Weighted average

technical age 14.2 years

Weighted average

capacity 1184 000 t/a

Aracruz

Três Lagoas

Veracel

Jacareí

0

500

1,000

1,500

2,000

2,500

3,000

0 5 10 15 20 25 30

PM Capacity, 1000 t/a

Technical Age, years

WEAK

STRONG Weighted average

technical age 21.2 years

Weighted average

capacity 503 000 t/a

2013/IQ

North American Pulp Mills Other Pulp Mills Closures Grade Switch On & Off

Total delivered cash cost will also have an influence on bottom prices

25

Total Cash Cost of BHKP

delivered to Europe

(US$/t)

458 532 498 487 484

475 449 426 403 359 324

301

308 262

234

134 58 76

55 52 57 81 97 41

62 56 71 59 88

69

55 6

115

41 26

Cash Cost (US$/t) Delivery (US$/t)

Source: Hawkins Wright (Outlook for Market Pulp, December 2013) | Fibria’s 2013 considering a FX of R$/US$2.16.

592 546

SG&A

Others

CAPEX

Interest Working Capital

Capacidade (k tons): 1.125 660 1.700 570 355 565 690 2.045 2.430 3625 11.385 = 30.300 365 945 3755

26

China: Paper capacities expansion continues to go on

China corresponds to 2/3 of global tissue capacity expansion

Ktons 2012 2013 2014E 2015E Total

P&W (woodfree) 720 -25 0 550 1,245

Tissue 1,540 1,184 1,518 903 5,145

Cartonboard 2,210 2,428 1,300 300 6,238

Total 4,470 3,587 2,818 1,753 12,628

Source: Fibria and Independent Consultants

Strong internal consumption will drive tissue demand in China

24.3

14.8 14.6

11.1

6.3 6.1 4.4

2.2 0.8 0.6

N. A

mer

ica

W. E

uro

pe

Jap

an

Oce

ania

E. E

uro

pe

L. A

mer

ica

Ch

ina

N&

M E

ast

Asi

a Fa

r Ea

st

Afr

ica

Kg/capita

Per Capita Consumption of Tissue by Region, 2012(1)

Growth Potential

0

5

10

15

20

25

30

35

1991 1996 2001 2006 2009 2010 2011 2012

N.America W.Europe E.Europe L.America Middle East

Japan China Asia FE Oceania Africa

Average Growth Rate

+3.5% p.a.

Million tons

World Tissue Consumption, 1991-2012(1)

27

(1) Source: RISI

Internal Consumption and Urbanization

China’s private consumption vs. exports (CNY trillion and annual % change) (1)

Chinese Urbanization Driver of Long-Term Growth

(UN Population Projections, Millions)(2)

28

Sources: (1) the Economist. (2) RISI China Pulp Market Study.

Shift from exports to private consumption;

Positive effects on households income and rising standards of living.

Different from other commodities, China accounts for 26% of hardwood demand compared to around 60% in other basic materials sectors

12% 15%

17%

19%

26%

20%

26% 25%

14% 15%

16%

18%

25%

21%

26% 26%

0

2,000

4,000

6,000

8,000

2005 2006 2007 2008 2009 2010 2011 2012

Eucalyptus ('000 t) Hardwood ('000 t)

Latin America is the main

supplier of pulp to China

(1) Source: PPPC Global 100 Report 2012

China’s Market Share of Market Pulp Shipments (%)(1)

29

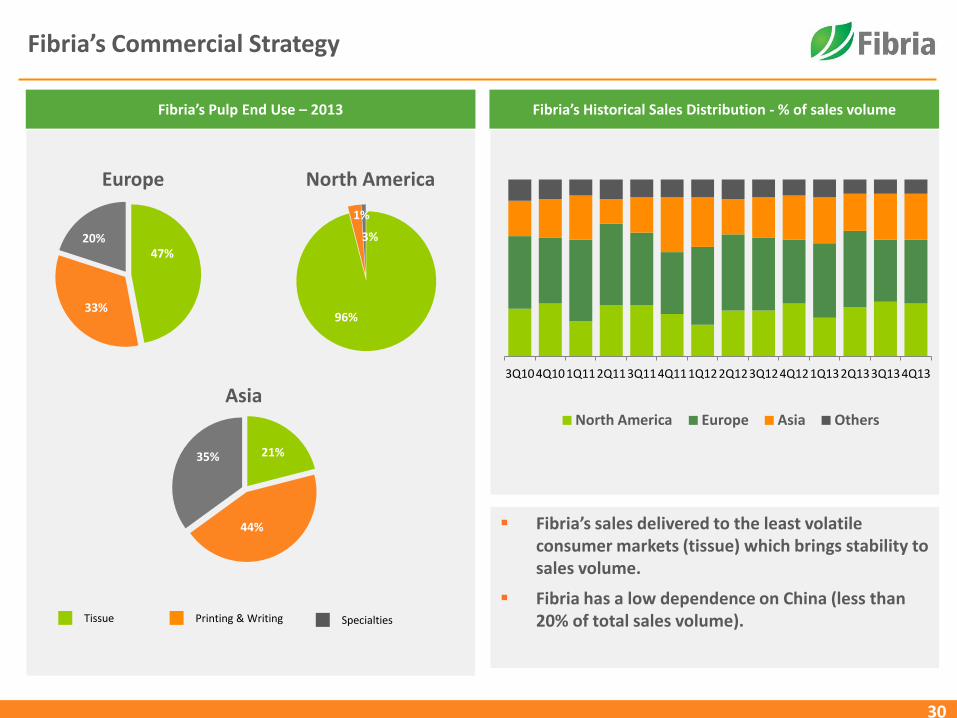

Fibria’s Commercial Strategy

30

47%

33%

20%

Fibria’s Pulp End Use – 2013 Fibria’s Historical Sales Distribution - % of sales volume

Europe

96%

3%

1%

21%

44%

35%

North America

Asia

Specialties Tissue Printing & Writing

3Q10 4Q10 1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13

North America Europe Asia Others

Fibria’s sales delivered to the least volatile consumer markets (tissue) which brings stability to sales volume.

Fibria has a low dependence on China (less than 20% of total sales volume).

Final Remarks

Fibria was elected as 1st place in

the pulp & paper sector in the

corporate governance and future's vision categories

Fibria is one of the 5 Brazilian

companies nominees to the Best

Corporate Governance

Award from London.

Acknowledgments in Governance, Transparency and Profitability

32

Company of the year,

among all industries,

according to Valor

Econômico.

Valor 1000

XVII ANEFAC-FIPECAFI - SERASA

EXPERIAN Prize

Fibria is among the most

transparent public

companies in Brazil,

recognized for the

quality of its 2012

financial statements.

Fibria was ranked for the forth

consecutive year (2010, 2011,

2012 and 2013).

In 2013 Fibria was ranked in four

categories: CEO, CFO, IR Team

and IR Professional

2013 Institutional Investor Latam

Ranking - P&P Sector

Fibria was selected as one of

the 10 best companies in

transparency.

The only one in

the pulp & paper

sector.

CDP Brasil 100 – Climate

Change 2013 Report

Época Negócios 360º

International Recognition by

Corporate Governance Report

Fibria was elected as 2nd place.

The prize highlights the

business profitability,

share profitability,

liquidity, corporate

governance and sustainability.

The Best Companies to the Shareholders

Prize of Capital Aberto Magazine

33

Fibria is the only Latin America company selected by RobecoSAM (responsible for DJSI) as one of the 10 worldwide leaders in SRI magazine’s “The 10

Game Changers – Changing the industry through sustainability”.

RobecoSAM - Sustainability Investing Magazine

Selected to Dow Jones World and Emerging Markets Sustainability Indices for 2013/14 as the industry leader of Forestry Resources and Paper sector.

DJSI World and DJSI Emerging Markets

Acknowledgments in Sustainability

Fibria was selected again to ISE, the corporate sustainability Index of BM&F Bovespa.

ISE – Corporate Sustainability Index (Bovespa)

THANK YOU

Investor Relations

E-mail: [email protected]

Phone: +55 11 2138-4565

Website: www.fibria.com.br/ir

Back up

Global Paper Consumption

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Developed Markets Emerging Markets

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Developed Markets Emerging Markets

CAGR 1996 – 2006 Developed Markets: + 1.7% Emerging Markets : + 6.0%

85,291

117,611

15,548

37,474

P&W Consumption (000 tons)(1)

Tissue Consumption (000 tons)(1)

114,507

CAGR 2007 – 2016 Developed Markets: - 4.0% Emerging Markets : + 4.1%

CAGR 1996 – 2006 Developed Markets: + 2.4% Emerging Markets : + 6.9%

CAGR 2007 – 2016 Developed Markets: + 1.4% Emerging Markets : + 6.7%

26,877

36

Source: RISI

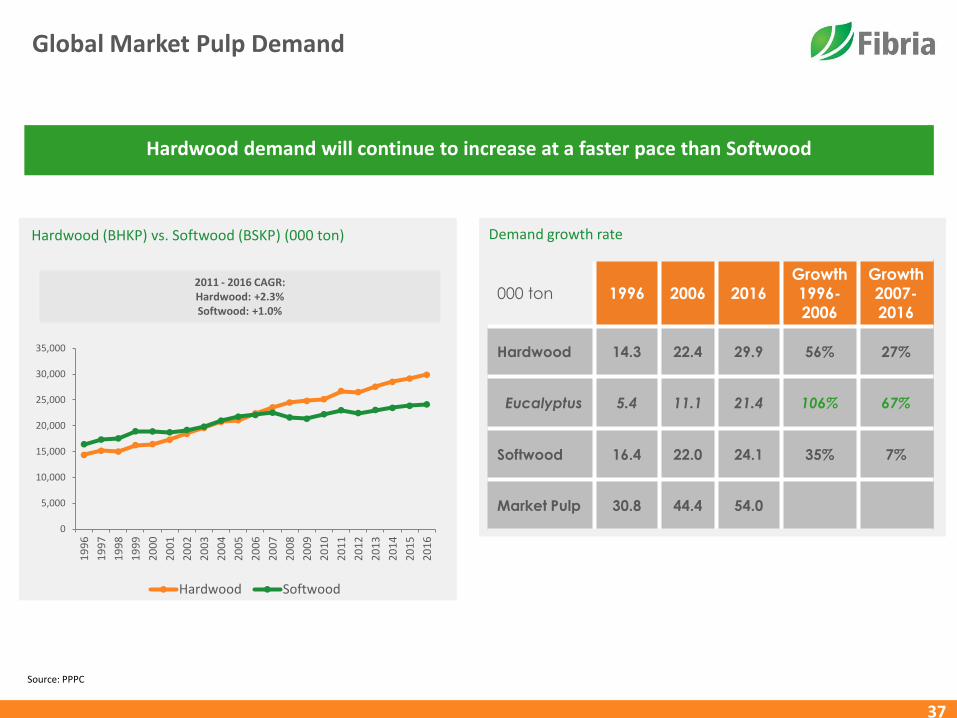

Global Market Pulp Demand

000 ton 1996 2006 2016

Growth

1996-

2006

Growth

2007-

2016

Hardwood 14.3 22.4 29.9 56% 27%

Eucalyptus 5.4 11.1 21.4 106% 67%

Softwood 16.4 22.0 24.1 35% 7%

Market Pulp 30.8 44.4 54.0

Demand growth rate Hardwood (BHKP) vs. Softwood (BSKP) (000 ton)

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

Hardwood Softwood

Hardwood demand will continue to increase at a faster pace than Softwood

2011 - 2016 CAGR: Hardwood: +2.3% Softwood: +1.0%

37

Source: PPPC

38

Pg. Slide

4 Financial Highlights

5 4Q13 Results

6 Indebtness

7 Fibria delivered the most significant leverage reduction in the LTM

8 Net Results (R$ million) – 4Q13

9 Free cash flow generation(1) (R$ million) - 2013

10 Positive Free Cash Flow (1) (R$ million)

11 Fibria delivers one of the highest EBITDA/t and FCF/t of the industry

12 FX and Pulp Price explain 80% of Fibria’s EBITDA Margin

13 Pulp vs Other Commodities

14 Maintenance CAPEX (R$ Million)

15 Cash Production Cost saw an increase of 17% over the past 5 years

16 Fibria’s tax structure

17 Fibria is seeking value creation for its shareholders with capital

18 Pulp and Paper Market

19 Today, according to public information, there will be a 9% increase of the market pulp capacity between 2013 and 2015

20 Pulp Market

21 Supply structural changes puts pressure on the industry

Pg. Slide

22 Capacity closures DO happen…

23 Gross capacity addition should not be counted as the only factor influencing pulp price volatility

24 Technical Age and Scale in the Market Pulp Industry

25 Total delivered cash cost will also have an influence on bottom prices

26 China: Paper capacities expansion continues to go on

27 Strong internal consumption will drive tissue demand in China

28 Internal Consumption and Urbanization

29 Different from other commodities, China accounts for 26% of hardwood demand compared to around 60% in other basic materials sectors

30 Fibria’s Commercial Strategy

31 Final Remarks

32 Acknowledgments in Governance, Transparency and Profitability

34 Acknowledgments in Sustainability

35 Back up

36 Global Paper Consumption

37 Global Market Pulp Demand