Manufacturing of Aniline - indextb.com · “Gujarat ranked first in ease of doing business as per...

18

Establishment of Aniline Manufacturing Unit Chemicals and Petrochemicals Government of Gujarat

Transcript of Manufacturing of Aniline - indextb.com · “Gujarat ranked first in ease of doing business as per...

Establishment ofAniline ManufacturingUnit

Chemicals andPetrochemicalsGovernment of Gujarat

Page 2

Contents

Project Concept 3Market Potential 4Growth Drivers 6Gujarat – Competitive Advantage 7Project Information 9- Location/ Size

- Infrastructure Availability/ Connectivity

- Raw Material/ Manpower

- Key Players/ Machinery Suppliers

- Potential Collaboration Opportunities

- Key Considerations

Project Financials 14Approvals & Incentives 16Key Department Contacts 18

Page 3

What is aniline?� Aniline is an aromatic amine which is mainly used as feedstock for polyurethanes.� It ignites readily, burning with a smoky flame characteristic of aromatic compounds.� Aniline is colourless, but it slowly oxidizes in air, giving a red-brown tint to aged samples.� It is used to manufacture dyes, drugs, photographic and rubber chemicals, explosives and

plastics.

Project Concept

Aniline applications� Methylene di phenyl di isocyanate (MDI) dominates the aniline market based on application.� MDI is used to manufacture PU foams. Its non-foam applications include paints, coatings,

adhesives, sealants and elastomers.

Aniline end uses� Insulation sector is the largest end-user of aniline as aniline enhances the electrical strength of

insulation materials.

45.5%

11.5%

10.7%

6.9%

4.0%4.0%

15.1%

Aniline global market share byend use, 2014

Insulation

Rubber products

Consumer

Transportation

Packaging

Agriculture

Others

45.6%

11.5%

10.3%

6.6%

6.4%

3.7%

15.9%

Aniline global market share byend use, 2019

Insulation

Rubber products

Consumer

Transportation

Packaging

Agriculture

Others

19.9%

80.1%

20.7%

79.3%

Others

MDI

Aniline global market share by application

2019 2014

Source: Technavio Report

Source: Technavio Report

Aniline production process

Benzene AnilineNitro benzeneNitrationExothermic catalytic

hydrogenation

Source:“Global aniline market 2015-19”, Technavio reporthttps://pubchem.ncbi.nlm.nih.gov/compound/aniline#section=Top

Page 4

1.2 1.21.3

1.41.5

1.7

2014 2015 2016e 2017e 2018e 2019e

Global consumption of other anilineapplications and forecast (MT),

2014-19

4.7 5.05.3

5.66.0

6.4

2014 2015 2016e 2017e 2018e 2019e

Global MDI consumption and forecast(MT), 2014-19

Global Market Potential

Global aniline consumption and forecast

Global aniline applications market

5.86.2

6.67.1

7.58.1

2014 2015 2016e 2017e 2018e 2019e

Global aniline consumption and forecast (MT),2014-19

� Global aniline consumption is estimated to reach 8.1 Million Tons (MT) in 2019 from 5.8 MT in2014, growing at a Compounded Annual Growth Rate (CAGR) of 6.8%.

� Aniline market is expected to grow at a steady rate owing to growth in automotive andinfrastructure industries.

� MDI accounts for ~45% of aniline applicationmarket.

� Global MDI consumption is estimated toreach 6.4 MT in 2019 from 4.7 MT in 2014,growing at a CAGR of 6.6% driven byincreasing demand in packaging andinsulation markets

� Global consumption of other anilineapplications is estimated to reach 1.7 MT in2019 from 1.2 MT in 2014, growing at aCAGR of 7.6%.

� Market is expected to grow steadily due toincreasing demand from agricultural sectorand dyes and pigments industry.

Source: Technavio report

Source: Technavio report

Sources:“Global aniline market 2015-19”, Technavio report

Page 5

Indian Market Potential

Aniline demand supply gap in India� Aniline demand in India is expected to reach 90,000 tons in FY20 from 52,500 tons in FY09,

growing at a CAGR of 5%.� Aniline demand growth is driven by manufacture of dye intermediates, rubber processing

chemicals and herbicides.� Demand for aniline is met through a mixture of domestic production and import.

52.5 58.2 63.954.5

63.572.3 70.5 74.0 77.7 81.6 85.7 90.0

34.7 39.4 41.1 40.148.2

40.6 34.5

FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16e FY17e FY18e FY19e FY20e

Aniline demand supply gap in India (‘000’ ton),FY09-20e

Demand Supply

Demand supply gap: 36,000 ton

Indian aniline export and import

Source: Chemicals and petrochemicals statistics, Government of India

Source: Chemicals and petrochemicals statistics, Government of India

� Indian aniline export has declined at a rate of 55% annually between FY12-15, whereas Indiananiline import has increased at a CAGR of 33% between FY12-15.

� This is mainly because of lack of local manufacturers of aniline in India.� GNFC and HOCL are the only manufacturers of aniline in India; HOCL aniline plant became

dysfunctional in 2015.

15310 15441

31742

36095

953 193 94 86

FY12 FY13 FY14 FY15

Indian aniline import and export (tons), FY12-15

Import Export

Note: At present, GNFC and HOCL are the only manufacturers of aniline in India. Supply forecast would depend on the set up of new anilinemanufacturing facilities in the country.

Sources:http://indianpetrochem.com/report/anilinereporthttp://www.thehindu.com/news/cities/Kochi/hocl-facilities-to-be-leased-out/article7657742.ece

Page 6

Growth Drivers

0.7 0.7 0.8 0.8 0.9 0.93

2014 2015 2016e 2017e 2018e 2019e

Aniline for rubber market growth(million tons), 2014-19e

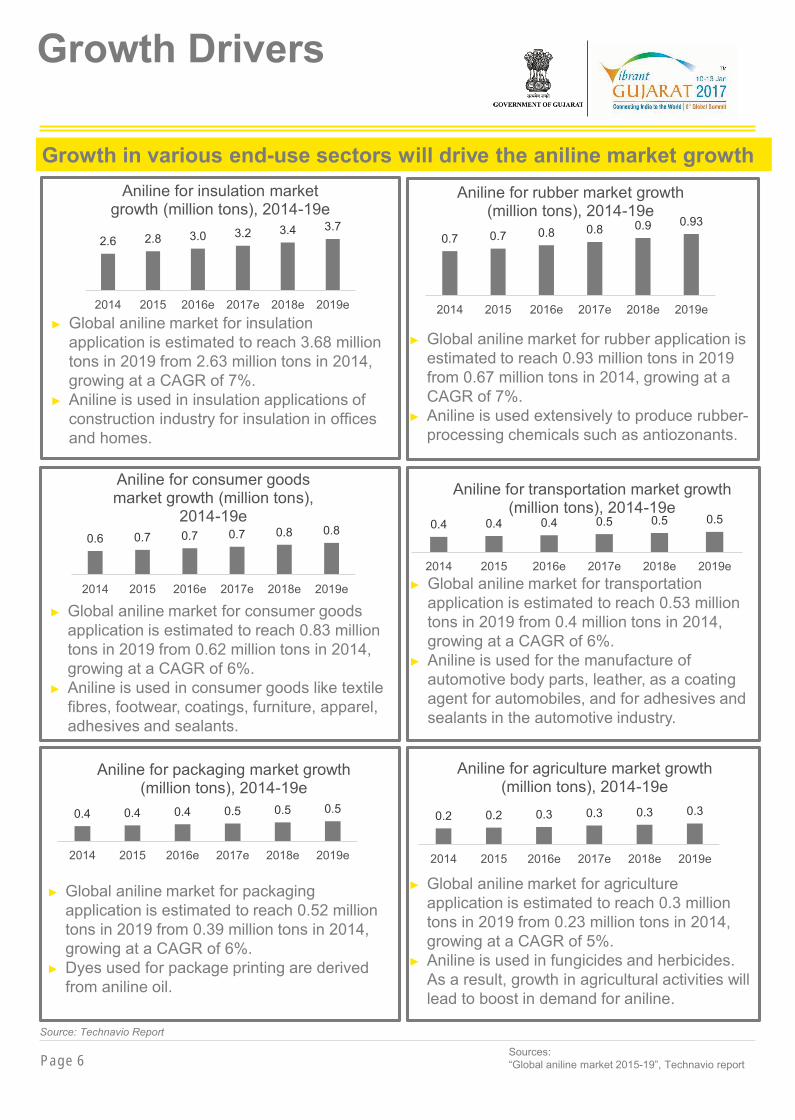

Growth in various end-use sectors will drive the aniline market growth

� Global aniline market for rubber application isestimated to reach 0.93 million tons in 2019from 0.67 million tons in 2014, growing at aCAGR of 7%.

� Aniline is used extensively to produce rubber-processing chemicals such as antiozonants.

� Global aniline market for consumer goodsapplication is estimated to reach 0.83 milliontons in 2019 from 0.62 million tons in 2014,growing at a CAGR of 6%.

� Aniline is used in consumer goods like textilefibres, footwear, coatings, furniture, apparel,adhesives and sealants.

2.6 2.8 3.0 3.2 3.4 3.7

2014 2015 2016e 2017e 2018e 2019e

Aniline for insulation marketgrowth (million tons), 2014-19e

� Global aniline market for insulationapplication is estimated to reach 3.68 milliontons in 2019 from 2.63 million tons in 2014,growing at a CAGR of 7%.

� Aniline is used in insulation applications ofconstruction industry for insulation in officesand homes.

0.4 0.4 0.4 0.5 0.5 0.5

2014 2015 2016e 2017e 2018e 2019e

Aniline for transportation market growth(million tons), 2014-19e

� Global aniline market for transportationapplication is estimated to reach 0.53 milliontons in 2019 from 0.4 million tons in 2014,growing at a CAGR of 6%.

� Aniline is used for the manufacture ofautomotive body parts, leather, as a coatingagent for automobiles, and for adhesives andsealants in the automotive industry.

� Global aniline market for packagingapplication is estimated to reach 0.52 milliontons in 2019 from 0.39 million tons in 2014,growing at a CAGR of 6%.

� Dyes used for package printing are derivedfrom aniline oil.

� Global aniline market for agricultureapplication is estimated to reach 0.3 milliontons in 2019 from 0.23 million tons in 2014,growing at a CAGR of 5%.

� Aniline is used in fungicides and herbicides.As a result, growth in agricultural activities willlead to boost in demand for aniline.

0.4 0.4 0.4 0.5 0.5 0.5

2014 2015 2016e 2017e 2018e 2019e

Aniline for packaging market growth(million tons), 2014-19e

0.2 0.2 0.3 0.3 0.3 0.3

2014 2015 2016e 2017e 2018e 2019e

Aniline for agriculture market growth(million tons), 2014-19e

Source: Technavio Report

0.6 0.7 0.7 0.7 0.8 0.8

2014 2015 2016e 2017e 2018e 2019e

Aniline for consumer goodsmarket growth (million tons),

2014-19e

Sources:“Global aniline market 2015-19”, Technavio report

Page 7

'Petro Capital' of India, contributing significantly to the country's production ofPetrochemicals (62%), Chemicals (53%) and pharmaceuticals (45%).

Gujarat has World’s Largest grass root petroleum refinery at Jamnagar by RelianceIndustries Limited with a crude processing capacity of 1.24 million Barrels PerStream Day (BPSD)

Gujarat credited with India’s First LNGchemical port terminal at Hazira

“Gujarat ranked first inease of doing business as

per DIPP report 2015”

Gujarat is one of the leading Industrialized States in India and theState has attracted cumulative FDI worth US$ 12 billion from April2000 to March 2015

Ease of Doing Business: Only state which comply 100% withEnvironmental procedures. Gujarat fares highly when it comes tosetting up a business, allotment of land and obtaining aconstruction permit

Flourishing Economy: State contributes 7.2% of the Nation GDP and shows leadership in manyareas of manufacturing and infrastructure sectors. Gujarat’s SDP (State Domestic Product) atcurrent price registered a growth of 11% during the year 2014-15.

Key Industries: Gujarat is the leader in key industrial sectors such as chemical, petrochemical,auto and its allied sector, pharmaceuticals, engineering, textile, jewellery etc.

18%

45%

51%

62%

70%

75%

Engineering

Pharmaceuticals

Chemicals

Petrochemicals

DiamondProcessing

Salt Processing

Strategic location and excellent infrastructure: Located on the west coast of India, Gujarat iswell connected to the major cities of the world by air and sea routes. The state has 45 ports, 12domestic airports and 1 international airport in addition to an extensive rail and road network

Geographical advantage due to locationon the west coast of IndiaWell connected to the major cities of theworld by air and sea routes. The statehas 45 operational ports, 12 domesticairports and 1 International airport inaddition to an extensive rail and roadnetwork.

*Source: Socio Economic Review of Gujarat 2015-16

GujaratCompetitive Advantage

Page 8

GujaratCompetitive Advantage

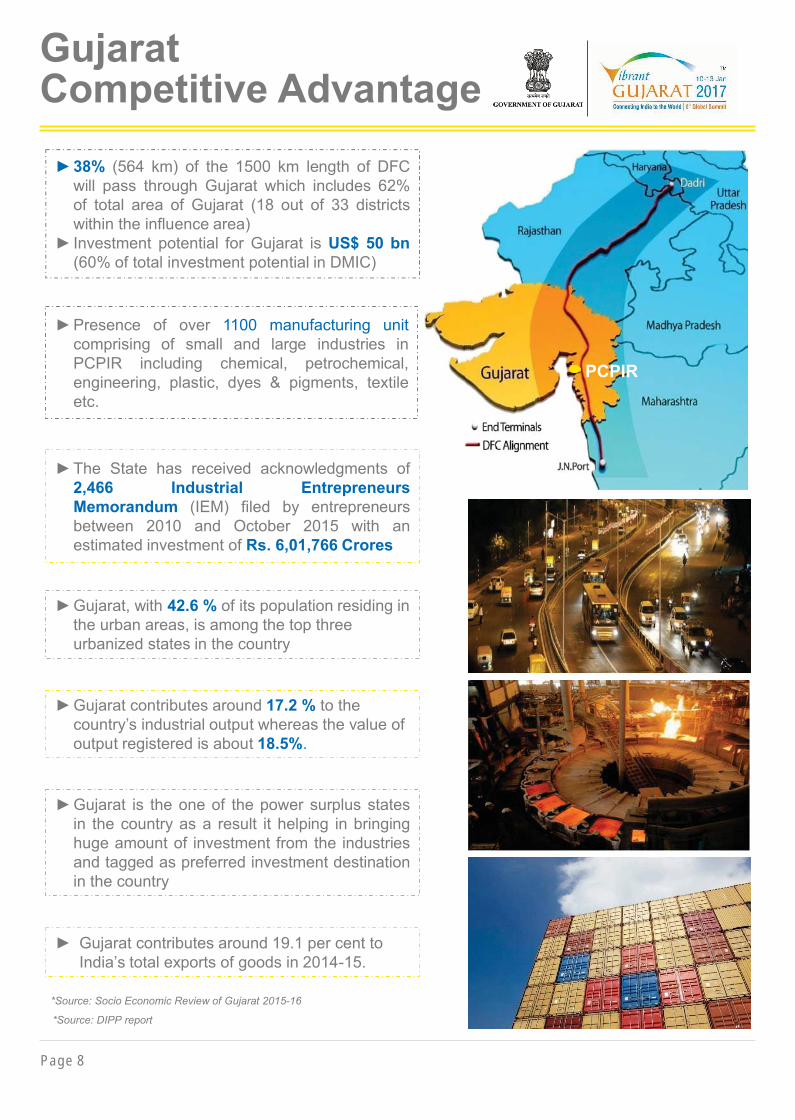

�38% (564 km) of the 1500 km length of DFCwill pass through Gujarat which includes 62%of total area of Gujarat (18 out of 33 districtswithin the influence area)

� Investment potential for Gujarat is US$ 50 bn(60% of total investment potential in DMIC)

*Source: Socio Economic Review of Gujarat 2015-16

PCPIR

� Presence of over 1100 manufacturing unitcomprising of small and large industries inPCPIR including chemical, petrochemical,engineering, plastic, dyes & pigments, textileetc.

� The State has received acknowledgments of2,466 Industrial EntrepreneursMemorandum (IEM) filed by entrepreneursbetween 2010 and October 2015 with anestimated investment of Rs. 6,01,766 Crores

� Gujarat, with 42.6 % of its population residing inthe urban areas, is among the top threeurbanized states in the country

*Source: DIPP report

� Gujarat contributes around 17.2 % to thecountry’s industrial output whereas the value ofoutput registered is about 18.5%.

� Gujarat is the one of the power surplus statesin the country as a result it helping in bringinghuge amount of investment from the industriesand tagged as preferred investment destinationin the country

� Gujarat contributes around 19.1 per cent toIndia’s total exports of goods in 2014-15.

Page 9

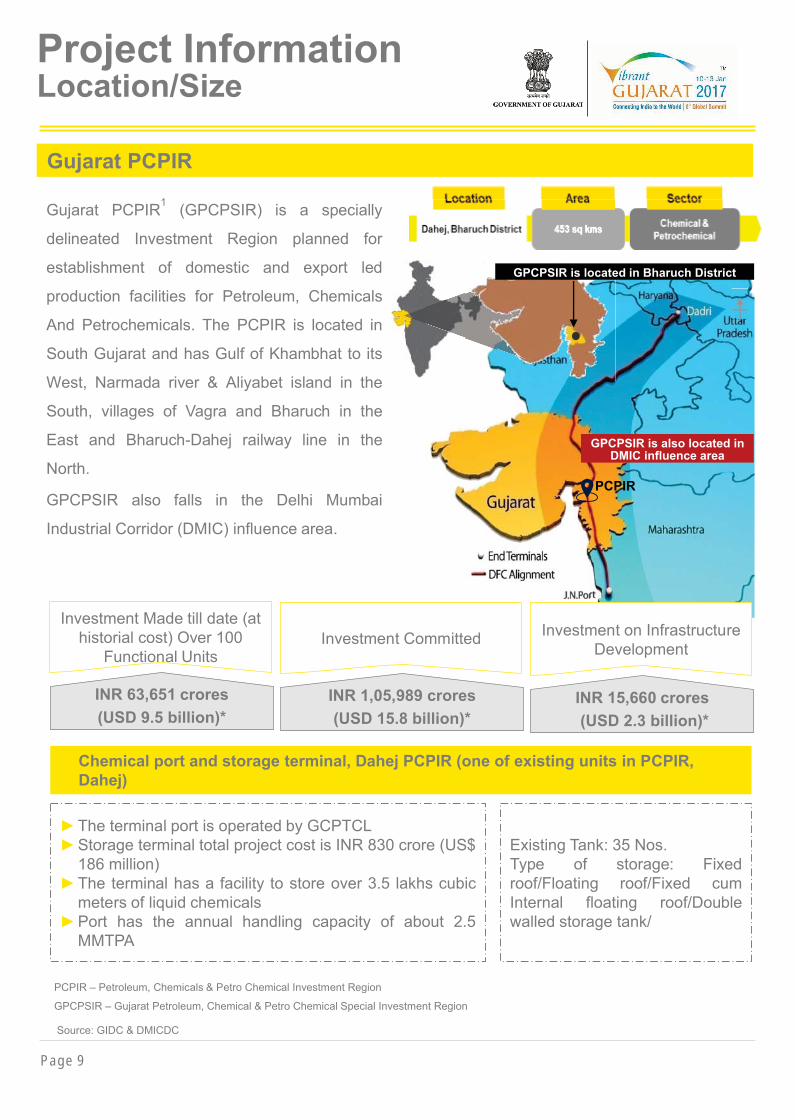

Gujarat PCPIR1 (GPCPSIR) is a specially

delineated Investment Region planned for

establishment of domestic and export led

production facilities for Petroleum, Chemicals

And Petrochemicals. The PCPIR is located in

South Gujarat and has Gulf of Khambhat to its

West, Narmada river & Aliyabet island in the

South, villages of Vagra and Bharuch in the

East and Bharuch-Dahej railway line in the

North.

GPCPSIR also falls in the Delhi Mumbai

Industrial Corridor (DMIC) influence area.

PCPIR – Petroleum, Chemicals & Petro Chemical Investment Region

GPCPSIR – Gujarat Petroleum, Chemical & Petro Chemical Special Investment Region

Source: GIDC & DMICDC

Gujarat PCPIR

GPCPSIR is also located inDMIC influence area

PCPIR

GPCPSIR is located in Bharuch District

Chemical port and storage terminal, Dahej PCPIR (one of existing units in PCPIR,Dahej)

� The terminal port is operated by GCPTCL� Storage terminal total project cost is INR 830 crore (US$

186 million)� The terminal has a facility to store over 3.5 lakhs cubic

meters of liquid chemicals� Port has the annual handling capacity of about 2.5

MMTPA

Existing Tank: 35 Nos.Type of storage: Fixedroof/Floating roof/Fixed cumInternal floating roof/Doublewalled storage tank/

Investment Made till date (athistorial cost) Over 100

Functional Units

INR 63,651 crores(USD 9.5 billion)*

Investment Committed

INR 1,05,989 crores(USD 15.8 billion)*

Investment on InfrastructureDevelopment

INR 15,660 crores(USD 2.3 billion)*

Project InformationLocation/Size

Page 10

Project Information

Existing� Connected to Delhi-Mumbai

Broad Gauge railway line atBharuch

� Bharuch –Dahej rail line (62 km)Proposed� Delhi-Mumbai Dedicated Freight

Corridor (DFC) will touch thePCPIR on the eastern side

� Bharuch –Dahej broad gaugeline to be connected to the DFCat Dayadra Jn. (~50 kms)

Logistics & Connectivity

Existing� 50 Km of six lane Dahej-Bharuch

State Highway connecting sixlane Delhi- Mumbai NationalHighway and NationalExpressway

Proposed� Ahmedabad Vadodara National

Expressway to be extended toMumbai

Existing� 250 km from International

Airport at Ahmedabad� 90 km from Domestic Airport at

Vadodara� 85 km from Domestic Airport at

SuratProposed� Greenfield Airport for PCPIR

Existing� Adani Port (Dahej) - 11.7 MMTPA� GCPTCL Liquid Chemical Terminal

- 1.8 MMTPA� LNG Petronet (Gas Terminal) - 12.5

MMTPA� Reliance liquid fuel jetty - 2.12

MMTPA� Birla Copper bulk cargo jetty - 3.8

MMTPANew Development� Development of jetty for handling

ODC (Over Dimensional cargo) inJoint Venture with Dahej SEZ Ltd

Existing� Three 220 KV sub-stations located at Dahej &

Vilayat & Six 66 KV substations located atDahej, Luna, Bhensali & Vilayat

Utilities

Existing� GIDC supplies 50 MGD

raw water drawn fromNarmada river at Nandand Angareshwar ( 25MGD each)

New Developments� Water supply scheme for

50 MGD water fromMiyagam Branch Canal(130 km)

New Development (in progress)� One 440KV, one 220KV & nine 66KV substations

proposed within PCPIR area� Gujarat Energy Transmission Corporation Limited

(GETCO) of 220 KV substation at Suva Dahej,� 1600 MW gas based power plant by Torrent

Power Ltd. in Dahej SEZ. Operational - 400 MW(1st Phase)

� 2640 MW coal based power plant - Adani Power

Infrastructure Availability

Page 11

Project Information

Aniline manufacturing procedure

Aniline production by exothermic catalytic hydrogenationof nitrobenzene in presence of excess hydrogen

Nitrobenzene production by nitration of benzenein the presence of nitric acid and sulfuric acid

� Feedstock can be sourced from various local manufacturers� Remaining feedstock requirement can be fulfilled by imports from China, US or western Europe.

Local Manufacturers2 Benzene supply(KTPA)

Reliance Industries 720

Indian Oil Corporation Ltd (IOCL) 125

Haldia Petrochem 132

Bharat Petroleum Corporation Ltd (BPCL) 43Source: Mitsubishi Chemical Holdings, 2014, company websites

Note: 1The list only includes key equipment and suppliers and is not exhaustive2The list of local manufacturers is not exhaustive

Key equipment and suppliers1

� ISGEC Hitachi Zosen,Dahej

� Alfa Engineering andEquipment, BharuchDistrict

� Heatex Industries Ltd,Surat

Key SuppliersKey Equipment

Feedstock requirement and sourcing

� Separator

� Distillation column

� Heat exchanger

� Pumps

� Compressors

� Turbine

� Metal Fab Engineers,Surat

� Ambica Boilers, Vatva,Ahmedabad

� Aero Therm SystemPvt. Ltd, Vatva,Ahmedabad

Source: Technavio report, GNFC prefeasibility report

Sources:“Global aniline market 2015-19”, Technavio reportGNFC prefeasibility report - http://www.ril.com/OurBusinesses/Petrochemicals/Aromatics.aspxhttps://www.iocl.com/aboutus/petrochemicals.aspxhttp://www.haldiapetrochemicals.com/index.php?p=cms&id=13https://bharatpetroleum.com/Our-Businesses/Refineries/Mumbai-Refinery/Product.aspx

Page 12

Project Information

Key Players

Indian Players Global Players

Aniline Technology Providers

Local suppliers of Nitricacid1

Location inGujarat

GNFC Bharuch

Shiv Shakti Acid andChemicals

Valsad

Gujarat State Fertilizers andChemicals Ltd

Vadodara

Local suppliers ofHydrogen1

Location inGujarat

GACL Bharuch

Madhuraj Industrial GasesPvt. Ltd.

Ahmedabad

Verni Gas Tech Pvt. Ltd. Surat

Note: 1The list of local manufacturers is not exhaustive

Page 13

Project Information

Potential collaboration opportunities

Key Considerations

� Volatile feedstock price: Benzene, primary feedstock for aniline production, is a crude oil-based material. In addition, hydrogen (feedstock for aniline manufacture) production requiresnatural gas. Hence, price fluctuation of natural gas and crude oil has a negative impact on theaniline market. The volatility in feedstock prices is reducing the profit margins of anilineproducers.

� Aniline health hazard: Aniline effects eyes, skin, and upper respiratory tract. Chronicexposure may also result in effects on the blood. Exposure to aniline may occur from breathingcontaminated outdoor air, smoking tobacco, or working or being near industries where it isproduced or used. These adverse effects might hinder market growth.

� Negotiation challenge with international technology providers: International chemicalcompanies hold the most advanced aniline manufacturing process technology. Findingmutually acceptable terms of collaboration with the technology providers is a challenge as theinternational companies tend to ask for a majority shareholding in the venture.

� Indian aniline manufacturers can collaborate with global technology providers in order to takeadvantage of their expertise.

� Potential collaborations can be made with key global players like Kellogg Brown & Root Inc. andChematur Engineering AB.

� GNFC has collaborated with Chematur Engineering AB for Aniline technology.

Sources:https://www3.epa.gov/airtoxics/hlthef/aniline.html“Global aniline market 2015-19”, Technavio reporthttp://www.gnfc.in/aboutus/productsales.html

Manpower Requirement1

� Approximately 200-300 skilled manpower would be required for the production unit of 100KTPAof Aniline.

Note: 1Manpower requirement is indicative of a comparable project and may vary by individual project

Page 14

Project Financials

Project specifications INR crore

Land : Area: 30,000 square meters1

Rate: INR1,440 per sq. meter. as of 1 January 201624.3

Building (plant area, office, store, factory shed, lab and packaging,open space)Built-up area: 15,000 sq. metres.Average rate: INR11,200 per sq. metre.

16.8

Machinery, working capital and other miscellaneous expenses 518.9

Total cost 540

The total project cost of setting up an aniline manufacturing facility at Dahej will be ~INR540 croresfor a production capacity of 100 Kilo Ton Per Annum (KTPA) Aniline.

Payback period

1 Area of aniline plant is estimated based on a comparable BASF aniline manufacturing plant2Land rate based on Dahej (rate may vary depending on the location of the site in Dahej PCPIR).3Average capacity utilization of GNFC FY15 is taken for calculation.4Average price per unit is considered by taking average of aniline import price in India.5EBITDA margin of FY14 GNFC is taken for calculation.6Industrial growth rate of 5% is considered taking into consideration the average potential growth of aniline demand inIndia.

Note: The estimated project financials have been calculated based on the capital requirement/investment of a typicalaniline manufacturing unit. However, they may vary by individual project.

Project cost

Capacity (TPA) 100,000Average capacity utilization in industry (%)3 98.5Production (TPA) 98,500Average price per unit (AR) (INR / ton)4 87,435Industrial average EBITDA margin5 14.23%Forecasting revenues at expected industrial growth rate6

5.00%

Time (years) 1 2 3 4 5 6 7

Revenue (INR crore) 861 904 950 997 1047 1099 1154EBITDA (@14.23% of rev.)4 123 129 135 142 149 156 164Undiscounted cumulative cashflows (INR crore) 123 251 386 528 677 834 998Investment (INR crore) 540

Estimated payback period: 4.1 years

Comparable Project:1. Gujarat Narmada Valley Fertilizers & Chemicals Ltd (GNFC)“Executive Summary of EIA & EMP Report for Expansion of BrownfieldAmmonia, Urea Plant, New Aniline, TDI-MDI Blend, Water Soluble Fertilizers(NPK) and CPSU Plants at GNFC, Narmadanagar, Bharuch, Gujarat”, July2014

Sources:GNFC Annual report“Petrosil Chemical Explorer”, 13 June 2016

Page 15

Project Financials

� Minimum viable size

1EBIT margin of FY14 GNFC is taken for calculation.2 Depreciation cost= %Depreciation of machinery * machinery costIndustry average is used for depreciation% for estimation purposesMachinery cost is considered to be 60% of Machinery, raw materials, component import and other miscellaneousexpenses

3Manpower cost=50% of employee cost; Employee cost=18.3% of total cost(50% of total employee cost is assumed to be fixed, while rest is considered under variable cost.)

Note:1. Exchange rate of 67 is used to convert US$ to INR2. The estimated project financials have been calculated based on the capital requirement/investment of acomparable aniline manufacturing unit. However, they may vary by individual project.

EBIT margin110.57%

Total operating costs (as% of revenues) 89.43%

Total costs (89.43% @ 861) (INR crores) 770.2

Depreciation cost2 (10.5% of PPE cost) crores 32.7Manpower cost (50% of employee cost)Employee cost (18.3% of total cost)3 70.5Finance cost (16% of debt) 31.4Others (including insurance and miscellaneous)(2% of total investment) 10.8

Total fixed cost (FC) (INR crore) 145.3

Variable cost (VC= TC-FC) (INR crore) 624.9Variable cost/Unit (INR crore) 0.006

Average revenue/unit (INR crore) 0.008

Minimum viable size (FC/(AR-VC)) (units) 60,564

Estimated minimum viable size: ~61 KTPA

Estimated industrial average (Debt/equity) 0.57x

Debt raised (INR crore) 196

Equity invested (INR crore) 344

Estimated debt raised (INR crore): 196

Means of finance

Minimum viable size

Sources:GNFC Annual report“Petrosil Chemical Explorer”, 13 June 2016

Comparable Project:1. Gujarat Narmada Valley Fertilizers & Chemicals Ltd (GNFC)“Executive Summary of EIA & EMP Report for Expansion of BrownfieldAmmonia, Urea Plant, New Aniline, TDI-MDI Blend, Water Soluble Fertilizers(NPK) and CPSU Plants at GNFC, Narmadanagar, Bharuch, Gujarat”, July2014

Page 16

Approvals andincentivesClearances/approval required

Approvals/clearance required Department to be approached and consultedIncorporation of company Registrar of companies

Registration/Industrial license “Secretariat of industrial assistance” (SIA) for large andmedium scale industries

Allotment of land State industrial development corporation

No objection certificate (NOC) underair and water pollution control acts

State pollution control board

Approval of construction and countryplanning

� Town and country planning� Municipal and local authorities� Chief inspector of factories� Pollution control board� Electricity board

Finance For loans higher than INR 1.5 crore((~US$ 0.22 million1), allIndia financial institutions like Industrial Development Bankof India(IDBI), Industrial Credit and Investment Corporationof India(ICICI), Industrial Finance Corporation of India(IFCI)etc.

Registration under state sales tax actand Central and State excise act

� Sales tax department� Central and state excise department

Code number for export and import Regional office of director general of foreign trade

Environmental clearance Ministry of environment, forest and climate change afterconducting environment impact assessment (EIA) for anyproject

Hazardous waste import and exportapproval

Ministry of environment, forest and climate change

Exiting business Ministry of corporate affairs

Government of Gujarat (GoG) has introduced single window facilitation portal for investorsproviding undermentioned benefits:� Centralized system to monitor applications� User friendly and simplified application process for investors� System for authorities and investors to check the status of applications� Increased departmental ownership

Source:1. “Gujarat Textile Policy”, Industries and Mines Department, Government of Gujarat, 5 September 20122. Approvals required for setting up plant,

http://dipp.nic.in/English/Investor/Investers_Gudlines/approval_clearances_required_for_new_projects.pdf,accessed 8 July 2016

3. “Environment clearance” http://envfor.nic.in/major-initiatives/environmental-clearances, accessed 8 July2016

4. “Gujarat single window clearance, https://www.ifpgujarat.gov.in/portal/jsp/aboutUs.jsp, accessed 8 July2016

5. “Exiting business, http://www.mca.gov.in/MinistryV2/CloseCompany.html, accessed 9 July 2016

1- USD= 67.67INR

Page 17

Approvals andincentives

Incentives from Government of Gujarat

As per the Gujarat Industrial Policy 2015, following are the key incentives provided to themanufacturing sector:� Capital investment subsidy of 10% loan amount disbursed by Bank/Financial Institution up to a

maximum amount of INR1.5 million (~US$ 22,5001)in municipal corporations areas.� Assistance for technology acquisition from recognized institution for manufacturing products will

be provided by way of 50% of the cost payable subject to a maximum of INR 5 million (~US$75,0001), including royalty payment for first two year.

� Assistance for venture capital to raise promoter contribution in the form of equity or loan throughGujarat Venture Finance Limited (GVFL).

� Interest subsidy scheme: 50 lakh interest subsidy for large scale industrial units.� Assistance scheme for Centre of Excellence: For national level centre of excellence the amount

of assistance will be up to INR20 crore (~US$ 30 million1)while for international level centre ofexcellence the limit will be INR30 crore. Such centre of excellence must encourage forinnovation and entrepreneurship. 70% assistance including recurring expenditure would beavailed.

Sector policy under Make in India initiative� Industrial licensing has been abolished for most sub-sectors except for certain hazardous

chemicals.� A weighted tax deduction of 200% under Section 35 (2AB) of the Income Tax Act for both capital

and revenue expenditure incurred on scientific research and development. Expenditure on landand buildings are not eligible for deductions.

� In the export sector, India has entered into a number of free trade agreements with ASEAN,Japan, Korea, Malaysia, Singapore, and others.

Technology development� SMEs will be given access to the patent pool and/or part of reimbursement of technology

acquisition costs up to a maximum of INR2 million (~US$30,0001) for the purpose of acquiringappropriate technologies up to a maximum of five years.

Green technology & practices:� 5% interest in reimbursement & 10% capital subsidy for the production of

equipment/machines/devices for controlling pollution, reducing energy consumption and waterconservation.

� A grant of 25% to SMEs for expenditure incurred on audit subject to a maximum ofINR1,00,000 (~US$1,5001).

� A 10% one-time capital subsidy for units practising zero water discharge.� A rebate on water cess for setting up wastewater recycling facilities.� Incentives for renewable energy under the existing schemes.

Incentives from Government of India

Source:1. “Exiting business, http://www.mca.gov.in/MinistryV2/CloseCompany.html, accessed 9 July 20162. “Manufacturing Sector – Profile”, Vibrant Gujarat website, 7 October 20143. Industries Commissionerate website, http://ic.gujarat.gov.in/?page_id=3175, accessed on 1 June 20164. “Textile industry welcomes amended TUFS”, Business Standard, 2 January 20165. “Approvals” http://dipp.nic.in/English/Investor/Investers_Gudlines/FAQ_GrantIndustrialLicence.pdf, accessed 27 June

20166. “List of defence equipment requiring industrial license”, http://dipp.nic.in/English/acts_rules/Press_Notes/pn3_2014.pdf

1- USD= 67.67INR

Gujarat Narmada Valley Fertilizers & Chemicals LimitedP.O. Narmadanagar - 392015, Dist. Bharuch, Gujarat.Phone : +91 – 2642 – 202279 Fax : +91 – 2642 – 247063Email: [email protected] ; [email protected]://www.gnfc.in

This project profile is based on preliminary study to facilitate prospective entrepreneurs to assess a prima facie scope.It is, however, advisable to get a detailed feasibility study prepared before taking a final investment decision.

Gujarat Industrial Development Corporation

Office of Industries Commissioner

www.gidc.gov.in

www.ic.gujarat.gov.in

Industrial Extension Bureauwww.indextb.com

Industries & Mines Department

www.imd-gujarat.gov.in

www.gnfc.in

Gujarat Narmada Valley Fertilizers & Chemicals Limited

www.guj-epd.gov.in

Energy and Petro Chemicals Department

Gujarat Narmada ValleyFertilizers & Chemicals Limited

![[(ClImDipp)P P(Dipp)][GaCl4]: a polarized, cationic ...](https://static.fdocuments.us/doc/165x107/625e6fd4eb47b40d4c7551dc/climdippp-pdippgacl4-a-polarized-cationic-.jpg)