Managing Oil Price Risk with Derivatives - World...

24

1 Managing Oil Price Risk Managing Oil Price Risk with Derivatives with Derivatives Tenzing Sharchok, Senior Financial Officer Ivan Zelenko, Head of Structured Finance and Derivatives The World Bank Treasury Stabilizing Oil Fiscal Revenues over the Short to Medium Term Oil Price Volatility Financial Forum March 11, 2008 Washington, DC 03/23/2008 2 Managing Oil Price Risk Managing Oil Price Risk Agenda Agenda Definition of a Stabilization Policy Risk Management with Derivatives Implementation Case Study: European Airlines

Transcript of Managing Oil Price Risk with Derivatives - World...

1

Managing Oil Price RiskManaging Oil Price Riskwith Derivativeswith Derivatives

Tenzing Sharchok, Senior Financial OfficerIvan Zelenko, Head of Structured Finance and DerivativesThe World Bank Treasury

Stabilizing Oil Fiscal Revenues over the Short to Medium Term

Oil Price Volatility Financial ForumMarch 11, 2008

Washington, DC

03/23/2008 2

Managing Oil Price RiskManaging Oil Price Risk

AgendaAgenda

Definition of a Stabilization Policy

Risk Management with Derivatives

Implementation

Case Study: European Airlines

2

03/23/2008 3

Managing Oil Price RiskManaging Oil Price Risk

AgendaAgenda

Definition of a Stabilization Policy

Risk Management with Derivatives

Implementation

Case Study: European Airlines

03/23/2008 4

Managing Oil Price Risk Managing Oil Price Risk Definition of a Stabilization PolicyDefinition of a Stabilization Policy

Oil price risk challenges fiscal policy

Oil exporting countries may derive a large share of their fiscalrevenues from oil sales

Exposure to oil price challenges fiscal policy:

shelving of planned projects, higher savings and lower investments, wasteful use of oil ‘windfall’

increased vulnerability of governments balance sheet

Exporting countries have set up policies to insulate budgetary revenues from oil price shocks

3

03/23/2008 5

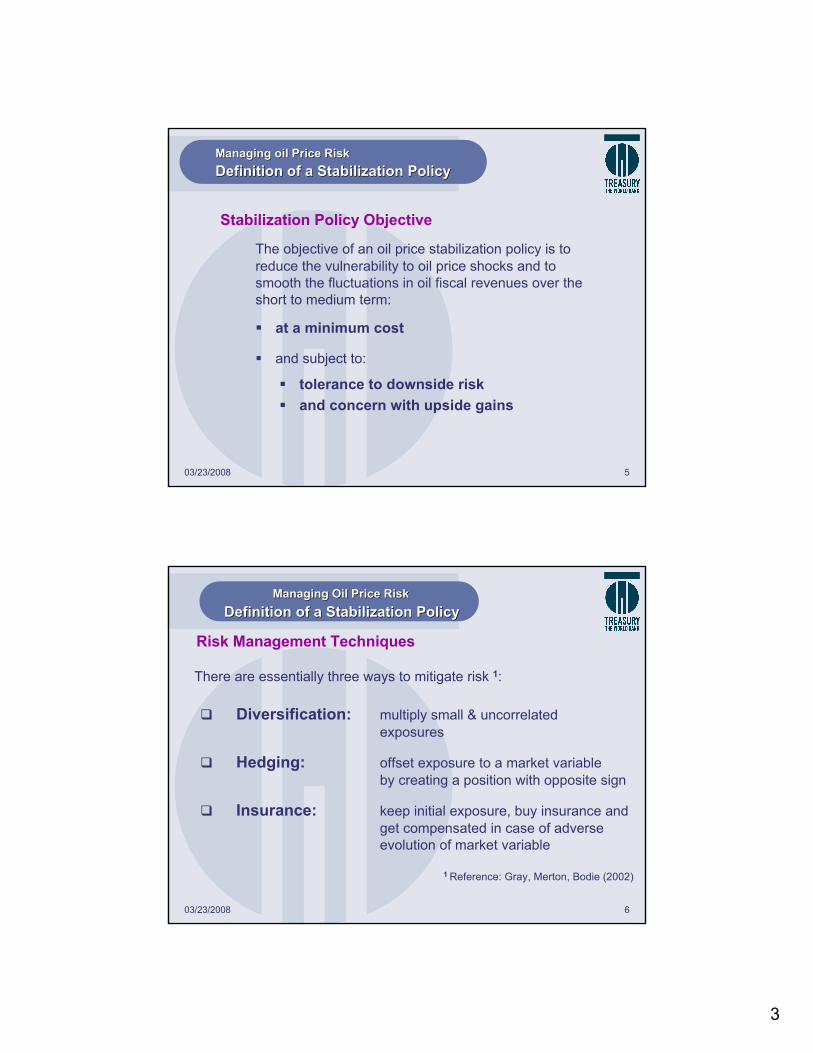

The objective of an oil price stabilization policy is to reduce the vulnerability to oil price shocks and to smooth the fluctuations in oil fiscal revenues over the short to medium term:

at a minimum cost

and subject to:

tolerance to downside riskand concern with upside gains

Managing oil Price RiskManaging oil Price RiskDefinition of a Stabilization PolicyDefinition of a Stabilization Policy

Stabilization Policy Objective

03/23/2008 6

There are essentially three ways to mitigate risk 1:

Diversification: multiply small & uncorrelated exposures

Hedging: offset exposure to a market variable by creating a position with opposite sign

Insurance: keep initial exposure, buy insurance and get compensated in case of adverse evolution of market variable

1 Reference: Gray, Merton, Bodie (2002)

Managing Oil Price RiskManaging Oil Price RiskDefinition of a Stabilization PolicyDefinition of a Stabilization Policy

Risk Management Techniques

4

03/23/2008 7

Managing Oil Price RiskManaging Oil Price Risk

Definition of a Stabilization PolicyDefinition of a Stabilization Policy

Approaches for a Stabilization Policy

Hedging

Self Insurance

Hedging and/or

Insurance

Issue oil Denominated Liabilities

Set up a Stabilization Fund

Transfer Risk to Markets

using Derivatives

03/23/2008 8

Stabilization Funds have been set up to immunize budgets

Oil revenues above a certain reference price are saved in the Fund. The Fund pays to the budget to ensure stable oil fiscal revenues based on the reference price.

BudgetOil Price sensitive Fiscal Revenues

Managing Oil Price RiskManaging Oil Price RiskDefinition of a Stabilization PolicyDefinition of a Stabilization Policy

Fluctuate

StabilizationFund

Stable

5

03/23/2008 9

Two categories of Funds with distinct objectives

Short to Medium Term Stabilization: “Stabilization Funds”

Savings and Stabilization over the Very Long Run: “Funds for the Future”

Smooth fiscal oil revenues & insulate budget against oil price shocks and volatility.

Transform depleting oil wealth into permanent & stable income through a diversified portfolio of financial assets

Managing Oil Price RiskManaging Oil Price RiskDefinition of a Stabilization PolicyDefinition of a Stabilization Policy

03/23/2008 10

Stabilization Funds have shortcomings

The initial capitalization of and the reference price should be properly set to avoid either exhaustion or over-accumulation

The reference price is difficult to determine as oil prices do not exhibit a natural long term average. It could, however, be defined as a moving average.

The accumulated savings may raise the question of their use.But the Fund may include a “Fund for the Future” tranche

Stabilization Funds require robust governance rules

Cost of carry if invested in short term liquid $ assets

Managing Oil Price RiskManaging Oil Price RiskDefinition of a Stabilization PolicyDefinition of a Stabilization Policy

6

03/23/2008 11

Transfer Risk to Markets using Oil Derivatives

Oil Derivatives enable hedging or insurance RM strategies. They do not require immobilization of capital. They can be combined with the Stabilization Fund approach.

Managing Oil Price RiskManaging Oil Price RiskDefining a Stabilization PolicyDefining a Stabilization Policy

BudgetStabilization Fund

Oil Price sensitive Fiscal Revenues

Transfer of Risk

Fluctuate Derivativestransaction

Stable

03/23/2008 12

Derivatives can increase efficiency in Risk Management

The use of derivatives in Risk Management has become much safer since the second half of the 90s

There are now standard rules and methods for safely setting up a derivatives trading platform with the appropriate procedures and controls

Derivatives such as swaps or forwards have become commoditized products that are increasingly used by central banks or government debt agencies

Hedging or buying insurance from the market should improve on a savings policy. But the safe use of derivatives requires an appropriate platform

Managing Oil Price RiskManaging Oil Price RiskDefinition of aDefinition of a Stabilization PolicyStabilization Policy

7

03/23/2008 13

Managing Oil Price RiskManaging Oil Price Risk

Definition of a Stabilization PolicyDefinition of a Stabilization Policy

ObjectiveGovernanceApproachTime HorizonRisk ToleranceBudgetInstrumentsImplementation infrastructure

Formulation of a Risk Management Policy

03/23/2008 14

Managing Oil Price RiskManaging Oil Price Risk

AgendaAgenda

Definition of a Stabilization Policy

Risk Management with Derivatives

Implementation

Lessons learned: Case Study of European Airlines

8

03/23/2008 15

Managing Oil Price Risk Managing Oil Price Risk RM with DerivativesRM with Derivatives

Basic Derivatives Instruments

Forward A Forward sale contract with a commodities dealer bank is the agreement to deliver oil in the future at a pre-determined price. Physically or cash settled.

Futures A Futures is a Forward contract with an exchange (NYMEX, IPE)

Swap A swap is a stream of [multiple] Forward contracts.

Options [Purchase of an Option (Put or Call) gives its owner the right but not the obligation to buy (Call) or sell (Put) oil in the future at a pre-determined price.]

03/23/2008 16

Generic Strategies with Derivatives

Remove uncertainty. Fix future oil prices. Low cost (but implied costs of margin calls). Do not permit upside gains

An insurance strategy placing a floor on future oil prices. Purchase payments (premiums) for buying puts is the cost of insurance. Permit upside gains.

Managing Oil Price Risk Managing Oil Price Risk RM with DerivativesRM with Derivatives

Forward sales

Purchase of puts

Hedging

Insurance

9

03/23/2008 17

Managing Oil Price RiskManaging Oil Price RiskRM with DerivativesRM with Derivatives

Forward

Initial exposure

Forward Oil Price

Revenues

Forward Sale

Initial exposure

Forward Oil Price

Net exposure

Revenues

Put

Floor future oil price at a costFix future oil priceHedging Insurance

Put

Cost of insurance

Net exposure

03/23/2008 18

Managing Oil Price RiskManaging Oil Price RiskRM with DerivativesRM with Derivatives

Buy Put + Sell Call

Initial exposure

Forward Oil Price

Revenues Initial exposure

Forward Oil Price

Revenues

Buy Put + Sell Put

But protection is lessenedBut upside gains are capped

PutNet exposure

Call

Forward Oil Price

Put

Net exposureSell Put

10

03/23/2008 19

Oil Prices have increased markedly since 2003

Managing Oil Price Risk Managing Oil Price Risk RM with DerivativesRM with Derivatives

WTI Oil Prices (monthly)

0

10

20

30

40

50

60

70

80

90

100

1995 1997 1999 2001 2003 2005 2007 2009

USD

/BB

L

03/23/2008 20

Oil Prices exhibit high volatility

Managing Oil Price Risk Managing Oil Price Risk RM with DerivativesRM with Derivatives

WTI Oil Prices (daily)

40

50

60

70

80

90

100

Jan-

05

Apr

-05

Jul-0

5

Oct

-05

Jan-

06

Apr

-06

Jul-0

6

Oct

-06

Jan-

07

Apr

-07

Jul-0

7

Oct

-07

US

D/B

BL

Vol = 31.62%

Vol = 38.67%

Vol = 32.38%

Vol = 26.40%

Vol = 31.24%

Vol = 29.12%

11

03/23/2008 21

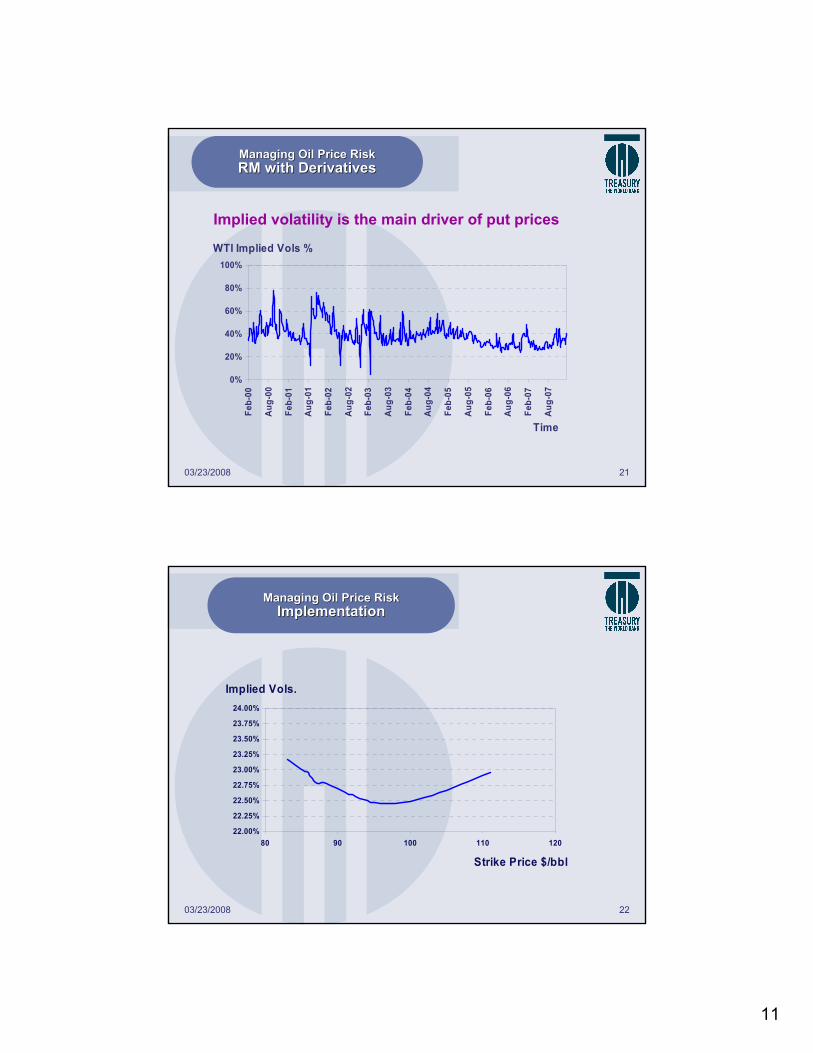

Implied volatility is the main driver of put prices

Managing Oil Price Risk Managing Oil Price Risk RM with DerivativesRM with Derivatives

WTI Implied Vols %

0%

20%

40%

60%

80%

100%

Feb-

00

Aug

-00

Feb-

01

Aug

-01

Feb-

02

Aug

-02

Feb-

03

Aug

-03

Feb-

04

Aug

-04

Feb-

05

Aug

-05

Feb-

06

Aug

-06

Feb-

07

Aug

-07

Time

03/23/2008 22

Managing Oil Price Risk Managing Oil Price Risk ImplementationImplementation

Implied Vols.

22.00%

22.25%

22.50%

22.75%

23.00%

23.25%

23.50%

23.75%

24.00%

80 90 100 110 120

Strike Price $/bbl

12

03/23/2008 23

Managing Oil Price RiskManaging Oil Price RiskImplementationImplementation

Capacity of Oil Derivatives Markets

The capacity of derivatives markets caps the maximum volume that can be hedged. The depth of markets has been increasing over the past three years.

As of October 2006, the following volumes of transactions, up to 5-year maturity, can be easily absorbed:

500 Million barrels / per year in forwards/futures 1 Billion barrels / per year in at-the-money puts

Some among the largest producers have fiscal revenues in excess of that capacity

03/23/2008 24

Managing Oil Price RiskManaging Oil Price Risk

AgendaAgenda

Definition of a Stabilization Policy

Derivatives: instruments, strategies and markets

Implementation

Lessons learned: Case Study of European Airlines

13

03/23/2008 25

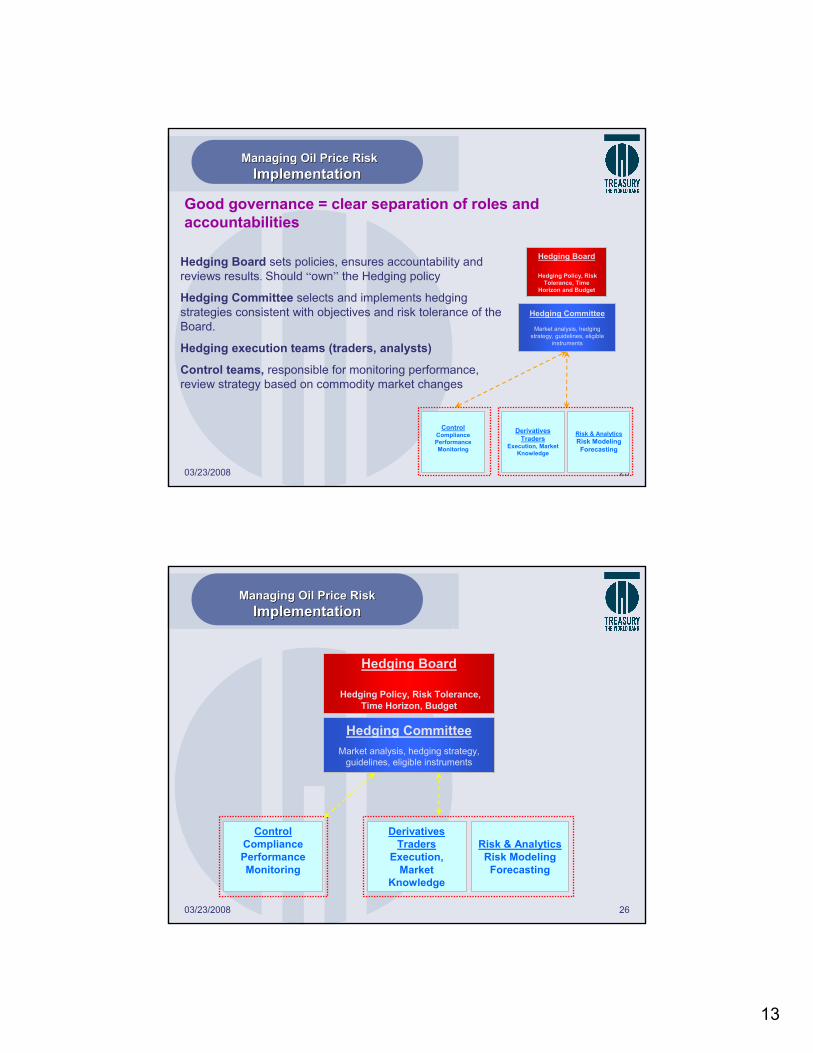

Hedging Board sets policies, ensures accountability and reviews results. Should “own” the Hedging policy

Hedging Committee selects and implements hedging strategies consistent with objectives and risk tolerance of the Board.

Hedging execution teams (traders, analysts)

Control teams, responsible for monitoring performance, review strategy based on commodity market changes

Good governance = clear separation of roles and accountabilities

Managing Oil Price RiskManaging Oil Price RiskImplementationImplementation

Hedging Committee

Market analysis, hedging strategy, guidelines, eligible

instruments

Hedging Board

Hedging Policy, Risk Tolerance, Time

Horizon and Budget

Derivatives Traders

Execution, Market Knowledge

Risk & AnalyticsRisk Modeling

Forecasting

ControlCompliancePerformanceMonitoring

03/23/2008 26

Managing Oil Price RiskManaging Oil Price RiskImplementationImplementation

Hedging CommitteeMarket analysis, hedging strategy,

guidelines, eligible instruments

Hedging Board

Hedging Policy, Risk Tolerance, Time Horizon, Budget

Derivatives Traders

Execution, Market

Knowledge

Risk & AnalyticsRisk Modeling

Forecasting

ControlCompliancePerformanceMonitoring

14

03/23/2008 27

Review and monitor Hedging strategy and roll-over

Execute hedging strategy Determine forecasts and scenarios for oil prices. Select hedging strategy.

Establish guidelines for implementation

Hedging policy, time horizon, risk tolerance

Managing Oil Price RiskManaging Oil Price RiskImplementationImplementation

Operational Processes

03/23/2008 28

Managing Oil Price RiskManaging Oil Price RiskImplementationImplementation

Prob.-weighted scenarios

Hedging Strategy Selection Process

……

Hedging

Strategies

No hedge

Puts

…..

Annual Fiscal Oil Revenues net of hedging gains/losses

Present Value of oil revenues over the hedging time horizon

Select strategywith best gain profile subject to Risk Tolerance

Review scenarios

15

03/23/2008 29

A first look at possible strategies (Forward = $58.68)

Managing Oil Price RiskManaging Oil Price RiskImplementationImplementation

and:

$3.70$5.00$51.47Buy out-of-the-money put

$6.08$7.38$58.68Buy at-the-money put

-$1.30$88.02Sell call at 150% of forward

$5.00$5.00$51.47Buy out-of-the-money put

$7.38$7.38$58.68Buy at-the-money put

Total CostCostStrikeStrategy

Maturity for all options: 3 years

03/23/2008 30

Managing Oil Price RiskManaging Oil Price Risk

AgendaAgenda

Definition of a Stabilization Policy

Derivatives: instruments, strategies and markets

Implementation

Case Study: European Airlines

16

03/23/2008 31

Managing Oil Price RiskManaging Oil Price RiskCase StudyCase Study

Who hedges oil risk with derivatives?

Hedgers

Airline Companies: Southwest, Lufthansa

US independent oil producers

Some oil importers (large users in public sector)

Some oil exporters

Utilities

Non- Hedgers

Airline Companies. Some stopped hedging

Most oil exporters

Most oil importers

Oil companies (strategic decision)

Railways (can pass the oil bill on to their customers)

03/23/2008 32

Hedging of Jet fuel purchases among US airline companies

Significant economic impact of higher Jet fuel costs on US Airlines: second largest operating expense with about 1.6 million barrels consumed daily

Airlines found it difficult to raise air fares to reflect higher fuel costs. This lead many to file for bankruptcy. They now lack the cash or the creditworthiness to put on fuel hedges

Some US airlines have been hedging oil price volatility from an early stage, taking a risk management approach. They were able to plan budgets and earnings with greater accuracy

Southwest has been very successful and consistent with its hedging strategy overtime

Managing Oil Price RiskManaging Oil Price RiskLessons learnedLessons learned

Based on congressional hearings February 2006

17

03/23/2008 33

Fuel Hedging Activity of Major U.S. Airlines

0%0%0%0%Continental/Delta/Northwest

0%0%0%4% @$62 per barrelFrontier

0%0%0%13% @$67 per barrelUS Airways

0 %0%0%18% @$60 per barrelAmerican

0%0%0%16% @$68 per barrelJetBlue

0%0%16% @$59 per barrel

25% @$56 per barrelAirTran

0%7% @$49 per barrel

20% @$45 per barrel

45% @$40 per barrelAlaska

30% @$39 per barrel

35% @$37 per barrel

55% @$37 per barrel

70% @$36 per barrelSouthwest

2009200820072006

% of Total Annual Fuel Requirement Hedged and Hedge Level (Source: Air Transport Association )

Managing Oil Price RiskManaging Oil Price RiskCase StudyCase Study

03/23/2008 34

Managing Oil Price Risk Managing Oil Price Risk

Case Study: European AirlinesCase Study: European Airlines

Minimize variability in jet fuel purchase costsTwo years8 million tons of crude/jet fuel p.a. Tighter “cap” on oil price, but reducing the costs by selling out-of-money puts

Options (buying calls and selling puts)Hedging committee reporting to the Board

6 staff in Trading, Analytics, Risk Management, M/O & B/O functions, Systems Software bought & customized (~ $1 Mio)

Net price of calls = 5% Jet Fuel purchase costs

Objective:Time Horizon:Size:Risk Tolerance:

Instruments:Governance:ImplementationInfrastructure:

Budget:

Formulation of the Risk Management Policy

18

03/23/2008 35

Managing Oil Price RiskManaging Oil Price Risk

Case Study: European AirlinesCase Study: European Airlines

Generic Risk Management Strategy based on collars

Program: ~ 8 Mio tons purchase of Kerosene per year

Annual Cost: ~ $ 4 Bio

Budget: ~ 4% of purchase ~ $ 160 Mio ~ $3 / bbl

Upside Protection: ~ $ 2 / bbl above forward price

Downside OpportunityRisk: ~ - $ 10 $ / bbl

03/23/2008 36

Managing Oil Price RiskManaging Oil Price Risk

Case Study: European AirlinesCase Study: European Airlines

Basis Risk Management

The Airline Company is mainly exposed to Kerosene price risk.

However, Kerosene futures are much less liquid than Crude oil. An extra liquidity premium has to be paid. Estimated to be around $7 per ton (~ $ 56 Mio).

Kerosene is fairly well correlated with Crude although the two prices may deviate.

The Airline decided to hedge mainly on Crude oil derivatives

19

03/23/2008 37

Managing Oil Price RiskManaging Oil Price Risk

Case Study: European AirlinesCase Study: European Airlines

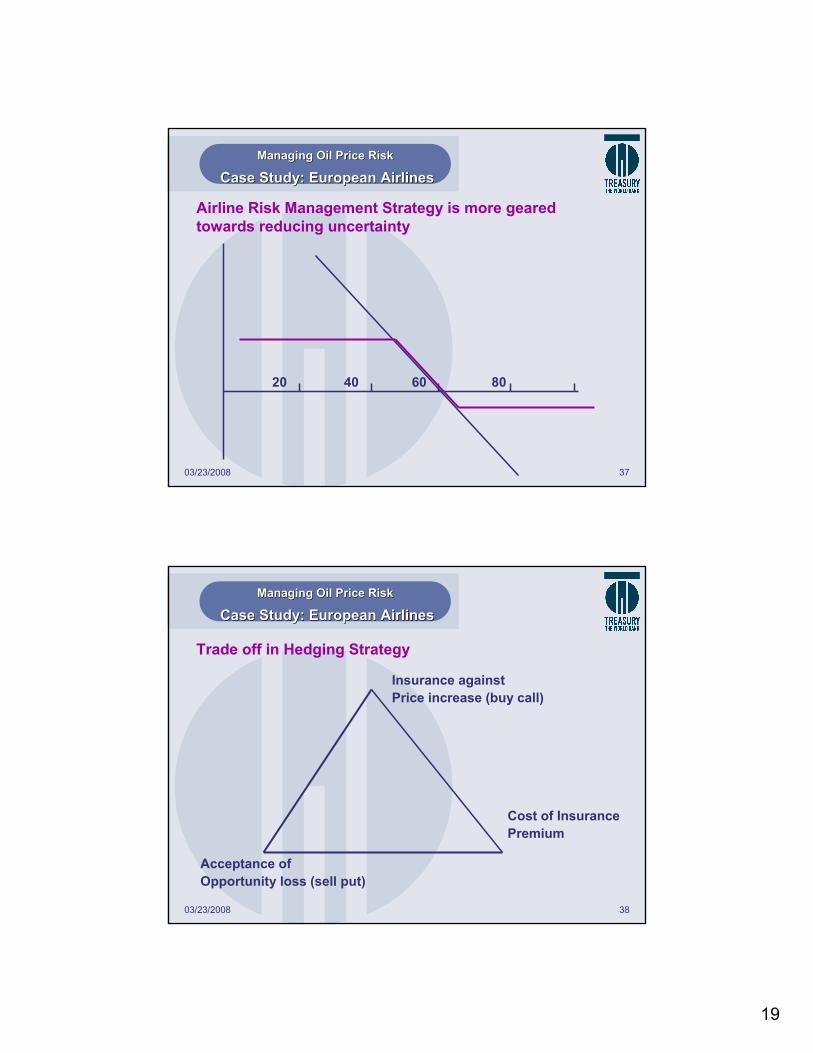

Airline Risk Management Strategy is more geared towards reducing uncertainty

20 40 8060

03/23/2008 38

Managing Oil Price RiskManaging Oil Price Risk

Case Study: European AirlinesCase Study: European Airlines

Trade off in Hedging Strategy

Cost of InsurancePremium

Insurance againstPrice increase (buy call)

Acceptance ofOpportunity loss (sell put)

20

03/23/2008 39

Managing Oil Price RiskManaging Oil Price Risk

Case Study: European AirlinesCase Study: European Airlines

Hedging strategy is implemented over time in 18 layersTarget hedge ratio is 90%

Crude

+24m+23+22

.

.

.

.

+1 +2 +6

Kerosene

5%

10%15%

20%25%

7,5%

15,0%

22,5%

30,5%

03/23/2008 40

Managing Oil Price RiskManaging Oil Price RiskCase Study: European AirlinesCase Study: European Airlines

Implementation of Risk Management Policy

Mandatory/Automatic Trading

Computer-generated automatic trading program (works as a benchmark)Given budget and insurance parameter solves for the last value (strike of sold put)Price averaging approach

6 months 18 months (7th-24th)

90%

85% - 5%

Active Management•Can deviate from the mandatory hedging program to take advantage of market conditions •Provides flexibility to the hedging program•Within the pre-determined parameters such as stop-loss limits and tolerance range of the hedge ratio

6 months 18 months (7th-24th)

90%

85% - 5%

Deviation

+

21

03/23/2008 41

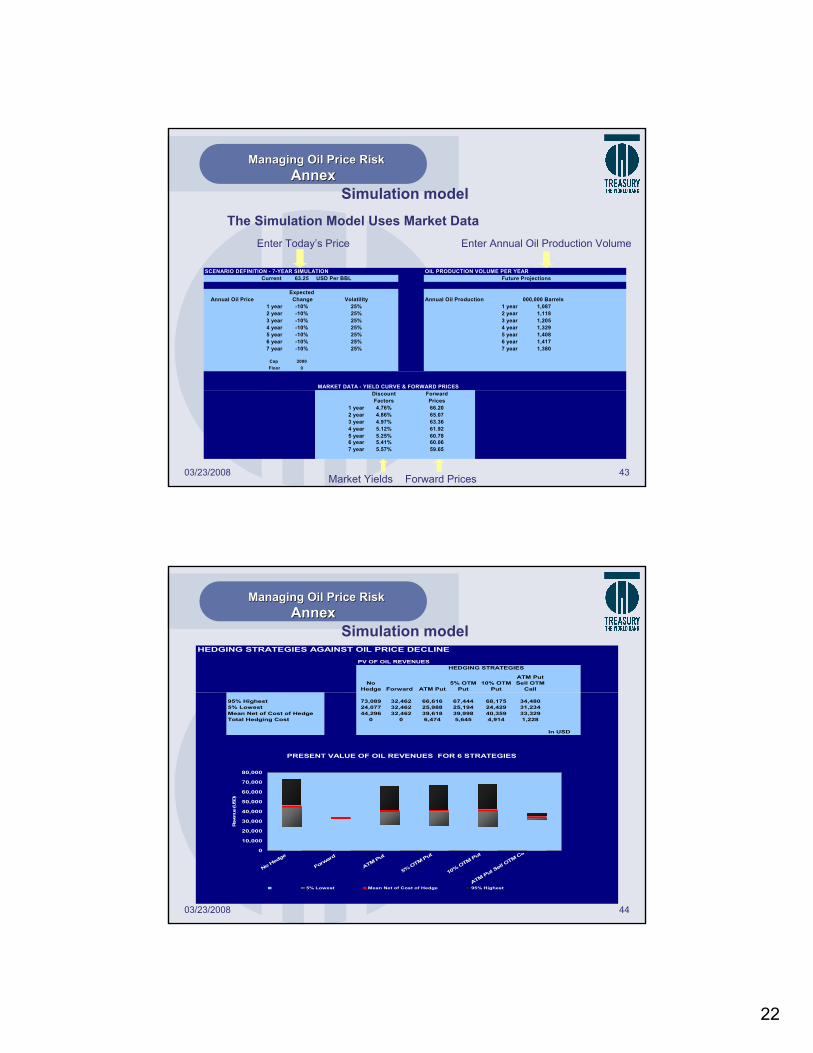

Managing Oil Price RiskManaging Oil Price RiskAnnexAnnex

Simulation model

7-year horizon. Annual data. Simulates future random oil prices. Enables to run scenarios for oil price evolutions and volatilities

The model uses market data: yield curve, oil forward rates, oil options volatilities

The present value of future oil sales net of hedging costs is computed for each 7-year oil price path

The model computes performance indicators. For each strategy, for each simulation, the mean and the 5% and 95% fractiles are computed.

03/23/2008 42

Managing Oil Price RiskManaging Oil Price RiskAnnexAnnex

22

03/23/2008 43

Managing Oil Price Risk Managing Oil Price Risk AnnexAnnex

Simulation model

SCENARIO DEFINITION - 7-YEAR SIMULATION OIL PRODUCTION VOLUME PER YEARCurrent 63.25 USD Per BBL Future Projections

Expected Annual Oil Price Change Volatility Annual Oil Production 000,000 Barrels

1 year -10% 25% 1 year 1,0872 year -10% 25% 2 year 1,1183 year -10% 25% 3 year 1,2054 year -10% 25% 4 year 1,3295 year -10% 25% 5 year 1,4086 year -10% 25% 6 year 1,4177 year -10% 25% 7 year 1,380

Cap 2000Floor 0

MARKET DATA - YIELD CURVE & FORWARD PRICESDiscount ForwardFactors Prices

1 year 4.76% 66.202 year 4.86% 65.073 year 4.97% 63.364 year 5.12% 61.925 year 5.25% 60.786 year 5.41% 60.067 year 5.57% 59.65

Enter Annual Oil Production Volume

Market Yields Forward Prices

Enter Today’s Price

The Simulation Model Uses Market Data

03/23/2008 44

Managing Oil Price RiskManaging Oil Price RiskAnnexAnnex

Simulation modelHEDGING STRATEGIES AGAINST OIL PRICE DECLINE

PV OF OIL REVENUES HEDGING STRATEGIES

No Hedge Forward ATM Put

5% OTM Put

10% OTM Put

ATM Put Sell OTM

Call

95% Highest 73,089 32,462 66,616 67,444 68,175 34,4805% Lowest 24,077 32,462 25,988 25,194 24,429 31,234Mean Net of Cost of Hedge 44,296 32,462 39,618 39,998 40,359 33,329Total Hedging Cost 0 0 6,474 5,645 4,914 1,228

In USD

PRESENT VALUE OF OIL REVENUES FOR 6 STRATEGIES

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

No Hedge

Forward

ATM Put

5% OTM Put

10% OTM Put

ATM Put Sell O

TM Ca

Rev

enue

(USD

)

5% Lowest Mean Net of Cost of Hedge 95% Highest

23

03/23/2008 45

Managing Oil Price RiskManaging Oil Price RiskAnnexAnnex

Simulation modelHEDGING STRATEGIES AGAINST OIL PRICE DECLINE

STRATEGY 1 : NO HEDGE AVERAGE ANNUAL OIL REVENUES in USD PV in USD

1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year

95% Highest 8,713 10,441 12,178 13,862 15,718 18,063 19,406 73,0895% Lowest 4,502 4,071 3,838 3,727 3,644 3,570 3,492 24,077Mean 6,397 6,842 7,324 7,847 8,392 8,983 9,575 44,296

HEDGING COST in USD

Total 0Per BBL 0

STRATEGY 2 : FORWARD SALES AVERAGE ANNUAL OIL REVENUES in USD PV in USD

1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year

95% Highest 6,129 5,937 5,746 5,591 5,491 5,427 5,415 32,4625% Lowest 6,129 5,937 5,746 5,591 5,491 5,427 5,415 32,462Mean 6,129 5,937 5,746 5,591 5,491 5,427 5,415 32,462

HEDGING COST in USD

Total 0Per BBL 0

STRATEGY 3 : ATM PUTS AVERAGE ANNUAL OIL REVENUES in USD PV in USD

1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year

95% Highest 7,930 9,535 11,229 12,901 14,764 17,103 18,445 66,6165% Lowest 5,347 5,031 4,798 4,629 4,537 4,468 4,454 25,988Mean Net of Cost of Hedge 5,995 6,295 6,705 7,180 9,628 10,208 8,875 39,618

PUT STRIKES = FORWARD PRICES HEDGING COST in USD

Total 6,474Per BBL 64.74

03/23/2008 46

Managing Oil Price RiskManaging Oil Price RiskAnnexAnnex

Simulation modelPRESENT VALUE OF OIL REVENUES

HISTOGRAMS FOR 4 GENERIC STRATEGIES 7-YEAR SIMULATION

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

12,15

1

20,82

1

29,49

1

38,16

1

46,83

1

55,50

1

64,17

1

72,84

1

81,51

1

90,18

0

98,85

0

107,5

20

116,1

90

Oil Revenues (USD) Net of Hedging Costs

Prob

abili

ty o

f Occ

urrin

g

Forward Expected Revenues-No Hedge No Hedge ATM Put ATM Put - OTM Call

24

03/23/2008 47

Managing Oil Price Risk Managing Oil Price Risk AnnexAnnex

Simulation modelANNUAL OIL REVENUES FOR DIFFERENT HEDGING STRATEGIES

NO HEDGE

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

1 2 3 4 5 6 7Years

USD

95% Highest 5% Lowest Mean

ATM PUTS

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

1 2 3 4 5 6 7Years

USD

95% Highest 5% Lowest Mean Net of Cost of Hedge

10% OTM PUTS

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

1 2 3 4 5 6 7Years

USD

95% Highest 5% Lowest Mean Net of Cost of Hedge

5% OTM PUTS

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

1 2 3 4 5 6 7Years

USD

95% Highest 5% Lowest Mean Net of Cost of Hedge