The Cross – Company Cloud Solution for Managing Returnable ...

Upload

reaz-uddinCategory

view

216download

0

7/29/2019 Managing Company

http://slidepdf.com/reader/full/managing-company 1/39

“How to manage my company?”by Nikolaos Karanassios, Ass. Professor, Dpt. Of Business Administration, TEI of Serres

1 IntroductionManaging a company that you have created needs different skills than entrepreneurship;

needs management.The starting point is to change your perspective; from one deciding person you must turnto be a member of a team, not necessarily the leader, even if you have the right to be,because you own the biggest portion of the company’s capital.Then you have to realize that your team is quite bigger than you think; it includeseveryone depending on the company. First of all are the key persons, then all theworkers, then subcontractors, agents, banks and the general public. Each one hasdifferent expectations from your company, sometimes their interests are conflicting,everyone seeks a bigger stake and your company (not just you) has to balance in this.Your company is founded because you and your partners want to have a permanentlyincreasing income, while your wealth will perpetually increase, not for just theexploitation of an opportunity.

To do this, you have to continuously plan, evaluate and control and for this purpose youmust register, not only what the company is doing, but also the decisions made, as wellas the reasons that led you to these decisions.Your company will be using public money. When you borrow from a bank, you reallyborrow the savings deposited; you are liable for the usage of this money, not just to thebank but the government, which controls the function of the banks, as well. They need toknow how you are using the “public” money and if you are cautious enough. They willnot check you for the decisions themselves, but whether you are diligent enough. Theydon’t give the money to your, but to your company.When your company becomes successful you need more money to fund its activities,then you may invite new partners (shareholders, if your company becomes an SA). It ispossible that you will never know who they are. They will only give their money to your company if they trust the procedures of handling their money. On the other hand, youmay want or need to sell your share. Your share has a value in proportion to the degreeof independence of the persons.Your company is founded to last forever, being profitable. Although people make andgovern a company, they are not permanently bound to it. Co-owners of the companymay change for any reason. The foundations of the company must be solid enough totolerate any such change of ownership. When you decide to found a company youchange from an entrepreneur to an investor.It is not enough to have profits. Your company must have enough cash to pay all theobligations, including the distribution of the profits to the owners.Increasing profitability depends on the procedures that your company is implementing inorder to maximize long term profits, while controlling cash. Profits, even short term or even occasional, do not depend only in maintaining the costs low, but the examination of the factors influencing profitability and choosing the right mix.

All these subjects will be displayed in this booklet and you will be guided to manage your company the best possible way. Yet, there are risks. With this series of booklets theentrepreneurs are guided to diminish the risks. If you consult your booklets about themost important issues of how to start a business (your company will start new activities,as it grows), how to prepare business plans (business planning is a continuousprocedure), how to make marketing plan (concentrating to the consumers) and thepresent one, your risk becomes minimal.

7/29/2019 Managing Company

http://slidepdf.com/reader/full/managing-company 2/39

But.

"Entrepreneurship is risky, mainly because so few of the so-called entrepreneurs know what they are

doing." – Peter Drucker

Let us see the most common reasons why companies fail, as most writers agree:1. Discordance between partners.

2. Cash difficulties.3. Easy money attracted by.4. Overexpansion.5. Lack of preparation for expansion.6. Favoritism.7. Fraud.8. Suspicions of fraud.9. Underestimation of costs.10. Overestimation of the Market niche.11. Overinvestment in equipment and other assets.12. Too much in social relations.13. Too much in partners luxury.

14. Too much power to hired managers.15. Too little attention to government controls.16. Too little attention to bureaucracy.17. Too much confidence in the product / service superiority.18. Too much dependence on massive buyers (distribution chains)19. Dependence on the Public procurements.20. Dependence on subsidies.

In this booklet you will find an easy way to understand how companies work and howthey should be effectively managed. It is not intended to make you a professional or aconsultant, but give you enough guidance to understand and assess consultants andspecialist that will approach you to get a contract or get hired.

2 StatuteIt is a contract between two or more persons that devote a sum of money and / or concede assets of their property, in order to commonly operate in the market.Depending on the type of the company, it has to be edited by a Lawyer or a Notary.It is a series of articles, where all the common activities are governed.You, either as a new entrepreneur or proposing the re-engineering of a company inwhich you are a member, have to indicate to your Lawyer or Notary, some articles thatare not common. These Law persons use patters to write your Statute, they are moreconcerned in the legal completeness of the Statute, than the functionality.You will find in the following chapters a series of suggestions to take into considerationand ask your Lawyer or Notary to include in the Statute.

2.1 The articles of associationIn addition of the patterns of the Lawyers and Notaries, you can dictate the followingarticles:Who is the beneficiary of each partner in case of his inability to continue his participation(death, severe illness, disappearance etc), indicating the partition for each beneficiary or earl.The age until which the members of the company will be able to participate in decisionmaking.

7/29/2019 Managing Company

http://slidepdf.com/reader/full/managing-company 3/39

Most of the companies in Europe suffer succession. If something happens to onemember and his /her share is about to pass to his earls, there are usually legal quarrelswhich practically “freeze” the company and drives it to resolution. Even when this doesnot happen, the remaining members may not have the ability to communicate or beaccepted by the others. When they know the successors, they accept them in advanceand if something happens to one of the members, the company goes on without

problems. An age limit in decision making of a company is very important, because even when theymay be still active, their attention is concentrated in their pension, not the future of thecompany. This makes them very conservative and discordance arises among the rest of the company members. This article must set an age for decision making andrepresentation of the company and also state that they can still participate in decisionmaking sessions and meetings, as advisors, only in preparatory discussions, not invoting time. In the same article, there must be a clause, that their share of profits will notbe invested, unless the aged person agrees. There may be a limit (i.e. 70% of the netprofits may be re-invested without agreement).There must be an article about the change of the Legal Status of the company (i.e. frompartnership to Limited Liability, from Societe Anonyme to the Stock Exchange and other

combinations). Too many companies loose the opportunities of development, becausethe members do not reach a quick decision to change their status. In most cases theyare not prepared, so they are afraid of loosing power.

Another article must rule the entrance of new partners. Unprepared entrepreneurs areafraid of loosing power with new members entrance, while these persons will bring incash and change the percentages distribution of ownership, but in the same time theywill increase the value of the ownership of the old members, since the overall value of the company becomes bigger than the sum of what it was before together with themoney put in by the new members.From a different point of view, there must be included, on one hand the procedures of creating other companies (a company may be a member of another company) and onthe other hand the conditions under which the company may be sold to another

company, merge with another company or participate in cluster of companies. It is oftenseen that successful companies become very vulnerable because they attract newcompetitors, just because they believe that they will become successful as well. Many of these new competitors come from within the company’s staff members. They know thebusiness, they have connections with the clients and they are the key persons. Creatingtheir own business means that they steal the competitive advantage. In such cases, thelegal representative must be delegated, with a specific article, to create a “spin out” (anew company, together with those staff members), provided that they will go to themarket with new products / services, even if they are developed in the company. If suchan article of delegation is missing, those persons will create their company and eat upthe company. A collective decision, as in typical Statutes, takes too long to be taken,while a lawsuit against these staff members, even if it will be accepted by the Court of

Justice, is only a compensation for the damage. It is not the same with mergers or selling out the company. The delegation of such an authority to the legal representativehas to be limited in two ways and also facilitated; there must be a limit of time for consultations with the partners, a specific majority (i.e. 60% of the votes) and a verbaldeclaration of the partners agreeing (or against) the proposal, within a deadline. If thedeadline expires, then delegation must be tacitly given to the legal representative.

As has been demonstrated previously, success is more dangerous than stability or decline. Success must be funded and one possible way is to bring in Venture Capital(cash brought in by investors intending to take it back after a period of time, with or

7/29/2019 Managing Company

http://slidepdf.com/reader/full/managing-company 4/39

without a combination with sharing profits). Those investors may ask to participate (or even dominate) decision making. Venture capital opportunities are rare and are safer than bank loans, because the company returns to the venture capitalist only profits andthe increment of the value of the company; if not successful has no liability of themembers with their personal property. An article facilitating fast decisions about theacceptance of a venture capital proposal, must be included. At the Statute formation

time, company members are not afraid of loosing power, since they don’t have power yet. In later time, they may oppose, so a limit of majority must be included, while easier delegation to the legal representative must be considered, while venture capital is notpermanent (as it is with mergers and acquisitions).Finally, an article about the obligation to elaborate an Internal Regulation within a limitedtime (usually one year) must be included.

2.2 The RegistrationThe Statute must be registered at the appropriate authorities. They are supposed toexamine it about the conformity with the Law. They usually reject it when the minoritypartners are not well protected.Even when the Statute is not registered, the company exists as a contract between themembers. Third parties do not make transactions with the company, but with themember.

3 Internal RegulationThe Internal Regulation is a contract as it is the Statute. For the big companies whoseshares are traded at the stock exchange market, there is European Directive which iscommonly called “Corporate Governance”, as well as all OECD member States haveagreed to promote the relative regulation.The Corporate Governance is meant to protect the anonymous shareholders fromfraudulent actions of the Management of the companies they become shareholders. Thisdoes not concern the Small and Medium Size companies, especially the new once.

What makes it a useful tool to such companies, is that it also regulates the way acompany is managed, as “Business Ethics” are best thought to be served.In this section, the ethical issues are avoided, while we concentrate our efforts to whatmakes a company avoid the most common mistakes.The Internal Regulation may be an amendment to the Statute, so it may be alsoregistered. This means that temporary majorities cannot change it, unless it becomes anew amendment. This gives enough time to examine the regulation as a long lastingdocument.It is better to assign the task of the preparation of such a regulation to professionals (i.e.your NGO consultant), while your Lawyer must see it in the end, for possible legalinfringements.The Internal Regulation is adding bureaucracy to the Management and Administration of

your company. In the same time, following the procedures set in it, saves your companyfrom a possible crash.

3.1 Decision Making Both managerial and administrative decisions should be coherent, so that the companyproceeds prosperously. It is thought that these decisions are being taken in favor of thecompany; but what if they are being taken in favor of one partner or a group of

7/29/2019 Managing Company

http://slidepdf.com/reader/full/managing-company 5/39

executives? What if a democratic (majoritary) decision is made on a difference of information among the decision making board or committee?Management and Administration have to make decisions on an equal information basis.They also have the time to reflect, or even get external advice, if they think that theyneed it. Managerial and Administrative decisions are not the same.

3.1.1 Managerial DecisionsManagerial Decisions are the once concerning the company as a legal entity. As such, isresponsive to all third party interested institutions (Fiscal Authorities, Banks, Governmentauthorities of all levels and nature, insurance institutions, European or Public fundingand the alike).Such decisions should be taken under an agenda, timely communicated to themembers, as all the legal systems set. Such formalities are usually followed. Thedecisions are being taken informally, while evident majority participants meet andprepare their vote, not in respect of the company’s benefit, but as a distribution of personal benefits, even if those benefits are not relative to the personal profits.

A well regulated system should set that:Together with the agenda, a proposal is also communicated.The proposal, as communicated, has been approved as being beneficiary to thecompany, by either internal (specialized staff members) or external (NGO consultants)as appropriate, together with their comments.There in an adequate time for submitting different proposals and that there is enoughtime for the members to study them before the meeting. A proposal, for example, toextend the manufacturing equipment, should be delivered three weeks before themeeting, leaving two weeks to the members to prepare a different proposal and deliver itto all the members, so they all have one week to study them both. This is not a Law, but

just a functional system, as we think of it.No discussion of proposals is possible unless all the participants received them at leastan adequate time in anticipation of the meeting (one week?). The members may agreeto postpone the decision, until all proposals have been communicated to all of themembers. Only one time is possible to postpone a decision.The proposing member may ask a staff member to present his proposal.

All proposals are registered in the Verbal. All the members explain their vote.The discussion is not registered in the Verbal.

A vote with hesitation is a vote against a proposal.The secretary (the one who is registering the verbal), is not present during thediscussion.The Secretary is not a voting member of the decision making board.The verbals are registered in three levels; the public, the internal and the restricted. Alldecisions have the same classification; A restricted decision contains all of theproposals, while the same decision, without any argumentation, may be communicated

(i.e. it may become public that the company decided to merge with another company,internal in regard to what this company is, restricted in regard to how such an event isassessed).

3.1.2 Administrative Decisions

Administrative decisions are usually taken by one person, not a committee or a board,as they have been delegated the authority to do so. For example, the legalrepresentative may have been given the authority to take a bank loan, a member of the

7/29/2019 Managing Company

http://slidepdf.com/reader/full/managing-company 6/39

board may have been delegated to contract an external selling agent, an executive toapprove discounts to clients etc. Such decisions do not change the shape of thecompany, as managerial decisions do. It is everyday operations that need fast decisionmaking and, most of all, personal responsibility of the person in charge.While “democratic” management is quite widespread (making decisions in meetings),responsibility is lost. There is a tendency to go back to “consultative” management,

where one person decides and other persons responsible for other activities arediscussing the impact of a decision to their sectors of responsibility. When the companygrows enough to assign responsibilities to staff members, instead of partners, it is wiseto distribute authority of decision making, because the board is not bound to previouslytaken decisions and is free to change policy and even the staff members.The usual decisions that create dispute and discordance, are described bellow.

3.1.2.1 Hiring

Every immediate superior has to be assigned the right to hire the persons he / sheconsiders most appropriate. For example, staff members must be assumed by the boardof directors, while they will be placed in responsible positions, answering to the board(as board we mean the partners or their representatives).The internal Regulation has to be very strict in hiring, by prohibiting the enrolment of relatives until second degree, to all levels, with one and only exception; if these personsare already in the Articles of Association as indicated to succeed a partner.The hiring procedure has to delegate absolute power, restricted only by hiring relatives,to the person they will work for. For example, the Sales Manager must select his salespeople, without the interference of anyone else, the head of the transportation unit mustselect the drivers himself, not his boss; the Sales Manager in this case.The hiring procedures must be very flexible. There must be suggestions aboutadvertising open positions, about the usage of external services (a specialized company)or else, but the person who is going to be the immediate boss of an employee must befree to grab an unemployed person that he thinks will best work for him, so he willperform better and present better results to his superiors.Reminder 1:Hiring is the main cause of trouble in most companies.Reminder 2:However a procedure of hiring is scientifically important (for example the usepsychologists) every person, assuming responsibilities, has his / her own style and thereis no method to predict conformity with this style.Reminder 3:

As a partner, you may be tempted to impose hiring of persons, as a favor to politicians,friends, important clients and any kind of others. Remember that, after you have satisfiedtheir petition, they forget it, until their next petition!

3.1.2.2 FiringEvery immediate superior to an employee has to be assigned the power to fire. Thispower must be restricted by:

A yearly percentage of possible firing. A written statement of the causes that occurred, signed by the dismissed person,

to verify that he / she knows the reasons claimed by his superior (not that he /she agrees).

A hearing from the firing person’s superior, so that the dismissed employee’spoint of view is heard.

7/29/2019 Managing Company

http://slidepdf.com/reader/full/managing-company 7/39

Reminder 1:Never fire an employee without the appropriate compensation, not even for theft. He willgo to the Court of Justice and you will pay it in the end, while he (may?) sue you for calumniation! He / she will have a Lawyer anyway!Reminder 2:The decision of firing belongs to the immediate boss. It is irrevocable, even if after the

hearing you are convinced that the firing reasons were obviously different, or even illicit!If you are convinced that one of your trusted responsible persons is using his delegatedpower for either personal reasons (sexual included) or as an excuse for failure, you mayfire him!Reminder 3:Never admit, being a partner or legal representative, that there is such a thing asimmoral administration in your company.Reminder 4:Incompatibility is the reason of every person fired, for everyone, whatever the realcause.Reminder 5:Sexual harassment in the working environment exists. There is no gender discrimination.

It exists between persons of the same gender and has been evidence even in the Bible!Never admit it exists! Never accept it as an excuse for firing someone, unless there areother behavioral discrepancies that can justify such an action (for example, there is anevidence of molesting, which is a criminal action). Do not forget that you are running abusiness, not a Court of Justice.Reminder 6:When you fire someone you must replace him / her. You may be suggested to firesomeone, for any reason, because there is an unemployed person waiting for the sameposition.Reminder 7:Never listen to someone who is telling you what his / her co-workers are doing (or evensaying). He / She is waiting for a benefit, usually to get the salary without really working!

3.1.2.3 Promotions

There is no typical system of evaluation. You have to describe one in your InternalRegulation. It will only be functional and long lasting if your system is based on recordingperformance of your employees and then the evaluation comes as the result of anexamination of the records.Reminder 1:Nobody is perfect. People make mistakes. Unless there is a damage to your company,do not give importance to the mistakes. Employees who make mistakes, are risk takingpersons and in most cases are better for higher positions.Reminder 2:

An effective worker may be a very bad director. You may promote such workers, givingthe title and the salary, but not really assign them with leading duties.

3.1.2.4 Subcontracting

Subcontracting is one of the major fields of fraud or suspicion for fraud. You have todescribe the procedures of subcontracting.Reminder 1:

A subcontracting action is never urgent. A random committee can assign it.Reminder 2:

7/29/2019 Managing Company

http://slidepdf.com/reader/full/managing-company 8/39

Set a limit of the annual budget to the managers for services that do not really affectyour business, like painting the office, repairing a photocopying machine and such.

3.1.2.5 Borrowing

Set a procure for borrowing money from the banks.

You must not revert to bank loans unless there is a written justification, including theimpact to profits and examination of alternatives (for example, shortening the credit lineto your clients, minimizing stocks, selling out participations in other companies etc.)This part of the regulation will save you from overborrowing, but it will also save you fromyour creditors, if you delay your payments to the bank. It will also facilitate your borrowing, while the bank will see that you are prepared to pay back.

3.1.2.6 Collecting

Set the procedures and the responsibility for soliciting your clients to pay their debt.Communicate this regulation to your customers, so they also know the procedures.Delegate the authority to extend the credit line to your clients to only one person, other than the legal representative.

Put an exception to the normal procedures for special clients, but the decision must betaken only by the board of directors.

3.1.2.7 Contracting

Delegate the legal representative or the CEO to sign any preliminary agreement or application for grants.Set a procedure for signing the contracts. Such a procedure may include the revision bya Lawyer, but in any case there must be a limit, over which there must be a writtenassessment of the impact of a contract.

3.1.2.8 Pricing Policy

Driven by the desire to increase sales, managers tend to discount prices, while potentialbuyers are pressing for discount, even telling lies about alternative offers, the tend todiscount without taking good care of the impact to overall profits and cash flow.The discount policy is affecting all three of them; sales, profits and cash flow.On the opposite side, managers tend to think profits only as a difference between sellingprice and cost per unit.

Another point of view is examining the discounts as an attraction of clients, being aMARKETING policy element.Yet, another point of view examines the discount policy as a danger to damage thequality image of the company, stating that you cannot sell high quality products anddiscount in the same time; “you cannot buy cheap quality” and consumers know it. If youdiscount quality you may find buyers but not customers (in the sense of frequent

buyers). As a very important issue, it has to be decided by the Board of Directors (a meeting of owners, if the company is small).There must be a clause in the internal Regulation that such a decision must be onlytaken after a series of studies of impact (you may revert to external consultants, if your internal professional resources do not meet the requirements for an appropriateevaluation), such as:

Expected impact on sales in long term and short term. Expected impact on profits after taxes.

7/29/2019 Managing Company

http://slidepdf.com/reader/full/managing-company 9/39

Expected impact on the Cash Flow, for the next three years.Make sure that:

The Advertisement cost of the discounts that you offer has been added to theoverall costs, before you calculate profits and cash flow.

You have taken into consideration that a new discount policy is changing your company’s image.

Pricing (discounts included) competition is always in favor of big companies whocan sell even under their costs, just because they want you and other smallcompanies out of the market; you have examined this occurrence.

You may loose customers (especially “heavy customers”) who already havepurchased from you without a discount.

3.1.2.9 Advertising / Promoting

Advertisement and promotion are very close to aesthetics. All those activities are usingbeauty as a means of “catching the eye” of the consumer. Are you sure that beautifulsells?The most common selling systems for advertisement / promotion agents is to approachthe deciding person of a company (in a small and new company, the legalrepresentative) with beautiful proposals; they usually avoid the selling impact, or theReturn On (your) investment is such a campaign. In order to secure their sales, they will“flatter” the person in charge. They use such arguments as “we are going to advertiseyou in the most popular media” or “you have the first clients who is able to esteembeauty, here are three proposals and we are sure that you will choose the mostbeautiful; yes, we were sure that you would have chosen the most beautiful one!”Your Internal Regulation has to control the procedures of assigning Advertisement andPromotion campaigns, so be sure that, at least:There is calculation of “contact cost per potential buyer”.The “message” that you want to transmit is clear and attractive.You cannot advertise your products and your company in the same time.The more an advertisement is beautiful, the less your potential clients remember your message.Celebrities cost and celebrity has a short life. Do not use them, unless you are preparedto rely on celebrities and not one celebrity, meaning that you are going to use the actualcelebrity every time there is a new one and that your product or service is aiming to sellto market niche attracted by actuality. For example, if you are selling scientific books,celebrities in your advertisement may even damage your sales. If you are sellingindustrial equipment, their usage will not affect your sales. If you are selling fashionitems, you cannot avoid celebrities. Calculate the impact on sales, even in arbitrary way;if you have statistics of your past, use them.You have advertising / promotion proposals of more than one advertising agencies.The proposing agencies accompany their proposal with a cost / benefit analysis.The selection of the best fitting your business proposal is done by the board, not oneperson; it is an investment, after all.

3.1.2.10Setting your own salary

Every person or entity which has interests in your company is also interested in your salary. Those interested parties are:

Your partners. The lower your salary is the higher the profits (their share) will be.

7/29/2019 Managing Company

http://slidepdf.com/reader/full/managing-company 10/39

Your Creditors. Your salary is going out of the company, as a cost element. Theyare afraid of your intentions to increase your personal income at the expense of the company, which you may drive to bankruptcy and never pay them back!

Your employees, which compare their own salaries with yours. The government, while salaries and profits are being taxed differently. Your clients, because they think that you are “stealing” from them, while they

excuse profits.Setting your salary, as a partner (together with the salaries of other partners working inthe company) as well as setting commissions on sales or any other performanceelement, is an internal subject of the company, but it soon becomes public.When you ask for a bank loan, you must declare your salary and other benefits(commission, company car, paid holidays, use of company credit cards, personal loanguarantee by the company, paid personal expenses, Legal assistance paid by thecompany for personal cases, company paid education of your family members and thesimilar). If they exceed normal wages, they may deny you the company loan,considering it a “consumption” loan, with a much higher interest rate, a much smaller amount and much more collateral demanded.Venture capitalists, capital increment invited shareholders and the Stock Exchange (if

you address it for capital raising), they will all turn their back to you if your personalrevenue is considered higher than “normal”.On the other hand, your salary should be the highest in the company (if you are the legalrepresentative) and higher than any of your employees (if you are a member of theboard of directors), so that your subordinates respect your decisions.The Internal Regulation must include a procedure for this salary setting question, while itmust also put limits (both higher and lower) for these salaries, as a comparison to thesalaries of other staff members.

3.2 Business EthicsBusiness Ethics are supposed to be an “oxymoron”. Profits are not easily accepted as alegitimate way of money making, by most of the people, worldwide. In the same time thegeneral public admires business persons which become rich!Within this conflicting mindset, all persons dealing with your company need to trust thatyou are not “cheating” them. Since the profits of your company are the result of all theoperations in the end of a year, the only interested parties are the partners (or shareholders) and your staff members. The clients and the creditors, will hardly learnabout your profits and the fiscal authorities will be happy to know that you declare highprofits.Since the shares of your company are not yet being traded at the Stock Exchange, youare not obliged to adopt the “Corporate Governance” directives; yet, reading theguidelines of the “Corporate Governance”, paves the way to the desired “incorporation”that will transform you from an entrepreneur into an investor.

3.3 Social Responsibility Corporate Social Responsibility is not certainly meant for small companies. It concernsbig enterprises, but even they have been small in their past.Social Responsibility means a company operation in such a way that it shows an evidentconcern about:The environment.The development of the society they operate in.The health and safety of people working in the company.

7/29/2019 Managing Company

http://slidepdf.com/reader/full/managing-company 11/39

The company impact on the evolution of innovation and scientific world.The promotion of equal opportunities to all the members of the society.The company has to declare its values, both to the external environment and theemployees, but only if it is determined to serve these values. If, for example, your company is dealing with chemicals without using the appropriate technology to protectthe environment, will prove disastrous for the company, because everyone (including

your competitors, will declare you a liar).

3.4 Professional Code of Conduct For almost every profession there is a code of good conduct, being a manufacturing,commercial or service providing.

Although such codes are not obligatory, you have better read the code, corresponding toyour business and try to implement it in your company. You will find it very difficult, whileyour competitors will be getting most of those clients that are vulnerable to unfair trade,but in the same time you will be getting more and more recognition by the finalconsumers and you will gradually get back the most valuable customers.You must use your Public Relations to frequently communicate that your company isimplementing a professional code, at a level best adapted in your market. Do not includeprinciples that you are not able to follow.Remember: Sooner or later, a similar code will be adopted by your government and willbecome obligatory, because you and your established competitors will try to protect your companies from new competitors and unfair competition among you.

4 Organizational essentialsYou are about to run a company, so before you start anything you have to organize your business. Here is how to start and how to proceed.

4.1 General

Organization is putting persons to work together, co-coordinating the company facilitiesand other means, so that they all go to the same direction. There are several theoriesdating at least two centuries, but the essence remains the same; putting people to worktogether means that they share the same goals, the same means, the same values andthe same objectives.It is obviously impossible to have (or make) people that will put the organization (andyour company) in precedence of their personal desires, ambitions and even beliefs.People compete for power, admiration by others and money, being (as we all are) lazyby nature, so they prefer obtaining it all without effort.

A company can me run without a formal organization. In such a case a strong leader (gifted by nature) is able to transmit his goals and values and mobilize people workingfor him. It only lasts a little.What we need is a formal organization which is clear to everyone, different fromcompany to company, making people work for the same purpose, either they believe in itor not.To do so, there is a little bureaucracy to tolerate, a little power to loose, but in the end,the formal organization makes the company to last and be profitable.People need a program to work and control, so that they know that they have to do the

job they are assigned.Here is how:

7/29/2019 Managing Company

http://slidepdf.com/reader/full/managing-company 12/39

4.2 Programming Programming means have written the future action in advance, so that everyone knowswhat has to be done and when. A program consists of the following:

4.2.1 Targets

A program has to declare a target to achieve, which everyone involved knows andremembers, so:The target has to be brief, so that everyone remembers it.It has to be tangible; using numbers and dates.It has to be coherent and in accordance to the Strategy of the company, to the tactics of the Board of Directors and the policy of the company, in respect of every field of action.It has to be feasible, otherwise people abandon it.Reminder:Use less than 18 words to declare the target.

4.2.2 Procedure Analysis

To reach the targets you need several procedures to be executed; others simultaneouslyand others sequentially.The procedures analysis is a very difficult task, if you are about to write an overallprogram for your company. It becomes much easier if you break down the functions of your company and write a separate program for each function, even if don’t haveseparate units for each. For example, you can write different programs for sales andproduction (when applicable), although production depends on sales. Writing theprograms you will realize that you can declare the targets in conjunction to one another,i.e. production of orders within 20 days, means that you have to write a new program for each new order.

4.2.3 Assignments

Every procedure is assigned to a work position (not the person working in this position)because he / she may be absent or replaced, during the program. Assignments have to balance the work load to the working positions. You will betempted to assign many procedures to the most skilful and productive workers and lessto the untrustworthy. This way you risk loosing your best people. Even if they don’tdismiss themselves, they will change attitude.Reminder:Never accept “this work is not among my duties”. Employees are learning quickly thatthey have to do what they are assigned and do it well. Exercise every possible way youthink to convince them, but never retreat.

4.2.4 Allocation of resources

Your resources are not infinite. You may just have one truck and it is needed both for thetransportation of raw material to your company, the transportation of the sold goods toyour clients and for the transportation of spare parts that the maintenance of your equipment need. You have to allocate the means to the working positions, according totheir assignments.If you don’t allocate resources, you have to expect an excuse for not doing their tasks.Do not expect your employees to ask for the means they need.

7/29/2019 Managing Company

http://slidepdf.com/reader/full/managing-company 13/39

If you have to assign tasks to external parties, assign the task to monitor the progressthat this third party is doing. If you omit this, you risk finding this third party havingforgotten you, creating a delay and disorder.

4.2.5 Budgets

Break down a budget, so that each procedure has enough money to be executed. Adding the particular budgets, you know the overall budget of your program.Subcontracting and external services must be trusted for payments to the person whowill receive and control the “deliverables” of this third party.

4.2.6 Schedule

Writing in a calendar the procedures, the assignments, the deadlines for deliverables,the allocation of resources and the payments, you have the whole picture of your program and you can control it.Putting all these information in a table (using the Gantt table is very helpful) you can alsohave the payments for each time unit (week, month etc).

Reminder:Distribute assignments in written to all working positions and seek a receipt in duplicate,headed by the program target declaration.

4.3 Controlling However your programs are well done, if you don’t control the business, all you have toexpect is excuses.The control consists of organization and observation. It sounds oxymoron, but all your programs need an organization which facilitates reaching the targets and observation of what people are doing and how.

4.3.1 Organization

An organized company is the one where every employee known what and how to do,how to ask and report, as well as his / her higher and lower positions. From whom to getdirectives and who to guide.

4.3.1.1 The Organizational Goals

The company is an organization. The company has been founded for a specific purposeor more than one purposes. These purposes include the way they can be fulfilledthrough competitive advantages.The goals of the organization are those leading to the route to success in the purposesfulfillment. For example, if the company purpose is to produce innovative products, theorganizational goal may be to promote research. If the company purpose is to satisfy the

clients servicing, the organizational goal may be to improve customer treatment.The whole system is affected by the organizational goals, because through thecommunication of these goals to all parties involved, they all know what the priorities areand act accordingly.

4.3.1.2 Co-ordination

Co-ordination is achieved with: A clear hierarchy.

7/29/2019 Managing Company

http://slidepdf.com/reader/full/managing-company 14/39

Unique and clear formal communication. Distinction between Line and Staff members (working positions).

Hierarchy shows who is the boss in every unit, having the right to “give orders” andmakes decisions and to whom all subordinates report or revert to for guidance, or evenask for something (for example the permission to leave).Formal Communication is distinguished into Vertical (order and report) and Horizontal

(information of the same hierarchical level of other working positions).Line members are those operating in segmented working positions (sales, productionetc), while Staff members are those working for the whole of the company (marketing,accounting, research etc.).

All the above is usually represented in the Organization Chart.Reminder:The lines of the Organization Chart show the unique formal communication route.

4.3.1.3 Authority

Every working position must have a clear and written authorization to perform tasks. Theauthority concerns the right to give orders (describing also the kind of eligible orders andthe limit to give orders) and the authority to handle items (goods, equipment, tools etc.)For example, the Sales Manager may be authorized to send sales persons to a trip for visiting clients but he cannot arrange their meals. He may be authorized to makephotocopies of the price lists, but not to change the prices etc.

4.3.1.4 Responsibility

Authority is connected to responsibility. There is no responsibility without authority, whilethere is responsibility for every authority. If, in the previous example, the Sales Manager is authorized to send sales persons for a visiting trip, he / she is responsible for havingthe visits done and that the sales persons are equipped with enough price lists. If theauthority to make copies of the price lists belongs to the sales persons, then they mustbe responsible for being provided with, before they leave.

4.3.1.5 Delegation

Concentration of authority to the top management creates bottlenecks, while alldecisions have to be taken by the same persons and their working time is limited, never mind their ability and skills to resolve every case. Keeping all decisions to the topmanagement will result to employees waiting in a cue and loosing their time, while thisdiscourages them from taking any initiative, thus to lack of progress.

Authority and responsibility is distributed with a formal written delegation, not to persons,but to working positions (the boxes of the organization chart).

4.3.1.6 Span of Control

As it has been said in the previous section, it is impossible to have under control anextended number of working positions. The same stands for the space extension. It isimpossible to control vast spaces or dispersed company facilities. Space and workingpositions of the control alleged to every working position must be well defined.

4.3.1.7 Unity of Management

Delegating authority, defining responsibility, describing the span of control, may result toundesired results.

7/29/2019 Managing Company

http://slidepdf.com/reader/full/managing-company 15/39

You must examine again all of the above sections, to verify that:Subordinates do not have more authority and responsibilities than their superiors.Subordinate positions do not take orders by more than one superiors.

A working position does not require multiple skills (engineering together with Legal andComputer programming). You may meet such persons, but even if you do, do notdescribe a working position based on such a rarity. Skills required must be

homogeneous.

4.3.1.8 Duties / definition

For every working position there must be produced a small “book of instructions”. In this“manual” you must describe:

What the person occupying the working position is expected to do daily and howto do it.

What this working position is expected to execute periodically (every week, everymonth, every year).

How to handle security (his security and security of the others). What to do in cases of emergency (working accident, physical catastrophes,

external or internal attack, health hazards and similar).Preparing all these books for every working position needs much work and efforts, but itis quite rewarding, because your company will perform well, both in achieving goals andkeeping the employees satisfaction high.

4.3.2 Observation

The previous chapter was paperwork with working positions. This chapter is aboutpeople working in your company.

Although the title of this chapter is observation, you will find out that there is no physicalobservation. Knowing that nobody wants to be watched (we tend to make all themistakes while we are being watched) and keeping in mind that what you want isperformance (quantity and quality), you have to create transparent procedures for your

human Resources.

4.3.2.1 Selection

You already have described the skills and qualifications for every working position, nowyou have to select the best fitting persons. Set the procedures for selection andcommunicate them to the candidates.Reminder 1:Work experience is not always a qualification. It may be indispensable for managerialpositions, but for entry level positions it may bring in bad habits from the previousposition.Reminder 2:Persons selected because they are recommended by relatives, politicians or other

“obligations”, will make you loose control.Reminder 3:Very high academic records are only needed for research positions. The ambition of such persons is to hold an academic position.

4.3.2.2 Training

Life Long Learning (LLL) is a universal tool for personal development and also theevolution of the enterprises and, as a consequence, the society.

7/29/2019 Managing Company

http://slidepdf.com/reader/full/managing-company 16/39

Companies are considered to be the main lever for development and in the same timethe field of action for ambitious persons. As a result, the enterprises are the most fertileground for LLL, being considered as learning organizations and characterized by“Knowledge Management”.In fact, every company is different from any other. A new comer must know his /her environment, the colleagues, the managerial style, the locations, the premises, the

equipment and their use, the “manuals” about his working position and the generalInternal Regulation about his / her service.

As a result, the company needs to train every newly hired person.The same necessity is evident whenever the company is either equipped with newmachinery, adopts new techniques or reengineers the whole management. Thecompany must train the employees again.Whenever the technological or socio-economic environment (even the competitiveenvironment) changes, the company must train its employees, so they are prepared toface the changes.Companies change work positions of the Staff Members, especially when they aredesignated to occupy high rank positions, which need a wider view of the company anda deeper knowledge of its operations. Before they move to another position, in addition

to getting the necessary acquaintances with their new working environment, they needtraining, so that they are able to understand the difficulties of the tasks they will assign toothers and know if they are real or just excuses for non-action.Reminder:Professionals will try to convince you, offering a part of European funding of LLL, to hirethem as “training bodies”. Close your ears to the sirens. If you listen to them, you willend up with getting involved in fraud together with your employees, who become“accomplices”. One time sinners; what do you have to expect? Will you able to ask theman honest behavior?

Academics will make you believe that they are the most appropriate trainers for your personnel. Before accepting them, ask them to show you how they can operate in your technological / cultural / educational / procedural environment. Without such an

examination, you risk making your employees loose their morale, while they will beshown every new scientific achievement, just because it is important.You have to crate an internal education system, as well as an external, facilitating your employees to bring in external knowledge. The internal education system is the onepermitting the employees to change positions, adapt to technological changes in thecompany and improve their skills.

4.3.2.3 Monitoring

Supervising personnel is both costly (the supervisor does not produce income for thecompany) and ineffective. When an employee decides to pretend working, he will. Evenif he really works, he will produce bad quality.Our days are not all the same. The best employee, for personal or even no reason at all,may not be in good mood and perform less than usual. If this causes a bad judgment, hewill be discouraged to cope up with the company expectations.

A fine tuned organization records the production of each employee in a regular basisboth in quantity and quality. Rushing production (or sales, or services) and measuringonly the quantity, you risk destroying material and other resources and even damageyour company image. Concentrated only in quality, you risk incrementing your costs andstaying out of the market. The most desired combination is to have the best quality at themaximum quantity, but such an occurrence is very rare.

7/29/2019 Managing Company

http://slidepdf.com/reader/full/managing-company 17/39

There are many ways to control quality. You should replace supervision with qualitycontrol and record keeping of the productivity of each employee.

4.3.2.4 Evaluation

If you just record productivity (or efficiency, or effectiveness), you already have done a

step forward. If you evaluate each worker in every period (no less than a month at atime) using a system that he knows (for example you may use an average as “normal”and compare it with the individual average performance) in advance, your employeeswill increase their contribution in the revenue making process.It is mandatory that the evaluating system is clear to all employees and it is differentfrom working position to working position. It is also important to have a simple statisticaltool in hand, so that you avoid arbitrary or circumstantial evaluations.

4.3.2.5 Motivation

In 1980 scientists started expressing doubts about the wage increment relatedmotivation. Now most of them believe that “monetary” motivation does not really work.Rewarding productivity (efficiency, effectiveness) is much more important for the workers

when it is related to social recognition.There is no pattern for this, social recognition is different from society to society, even inneighboring places. Let your imagination work!Participation at the distribution of profits may be strongly motivating, if on individual basisand not collective. It is not a matter of justice, but merely common sense. If an employeecan enjoy additional earnings independently from his contribution, he will not bemotivated at all.Promotion is commonly used as an incentive for the best performers. It certainly is, but apromotion without a salary rise seems ridiculous and does not last for long. As it hasalready been explained, it may also put the wrong persons in the wrong positions. Youcan invents other systems, like creating many stages with titles and a rise of wages,without really assigning administrative duties that are often incompatible with a well

performing employee. Selecting the head of employees is not a reward for performance.He or she must lead people and not tune machines or treat customers, while he or shemust make fast, accurate and profitable decisions, taking the risk to fail.

A systematic knowledge and analysis of the desires of the employees will give you ideasof motivation. An incentive that you think is plausible, may not be interesting at all to your employees and other (to you irrelevant) things may be strong incentives (for example,paid excursion with the family, may result a wrong incentive, while the expedition to atrade fair alone, may be a strong incentive).

4.4 Organizational toolsYou can use simple tools to help you organize your company better. There is a lot of free

software in the internet, but you can simply use MS-Office.Computer use is not necessary, but it helps you doing the same job faster and moreaccurately.

4.4.1 The GANNT matrix (enhanced)

The Gannt table is a very simple tool. Here is an example:Imagine that your company is planning to increase sales by 10% in 6 weeks.

7/29/2019 Managing Company

http://slidepdf.com/reader/full/managing-company 18/39

To cope up with increased sales, you need to get raw material, increase production,move sales persons, advertise and pack.Here is the Chart.Code Task Week 1 wek 2 Week 2 wek 3 Week 3 wek 4 Week 4 wek 5 Week 5 wek 6 Cost

1 Marketing 1.100

1.1 Brochure Creation 250 250

1.2 Brochure reproduction 500 500

1.3 Brochure distribution 350 350

2 Sales 3.340

2.1 Sales Persons Tour 400 400 400 400 1.600

2.2 Orders Received 0

2.3 Orders Executed 50 60 100 120 145 170 195 840

2.4 Clients follow-up 100 120 140 160 180 200 900

3 Provision 6.600

3.1 Raw Material 800 1.000 1.500 1.700 5.000

3.2 Packaging 250 300 500 550 1.600

4 Distribution 300 350 400 450 500 550 600 3.150

Cost 250 500 1.800 2.050 910 620 2.710 1.205 3.150 995 14.190

Payments 100 400 1.000 1.825 680 540 1.435 1.878 903 2.745

ASSIGNMENTS

Sales Director

Production Assistant

Assistant Accountant

Secretary

Company Car

Office Equipment

The original Gannt Chart had only the shadowed areas, to show when a procedure(task) starts, when it ends, how several tasks can be executed simultaneously and how

the tasks follow one another.This proposed enhancement, includes also the cost for each task at the time it occursand also the payments.Payments differ from the cost, because you can buy on credit, but this credit must bepaid in a later time. This example assumes that you pay the credit the following week infull. In a real case, there are different credit lines for each purchase.It is a simplified chart. There should be also the involvement of sales position (per territory, type of clients, type of products).

As you can see, there are no names of persons, but just working positions. This isbecause the work must go on and executed in time, never mind the absence of aperson.

4.4.2 The Organization Chart

President

Accountant Marketing

Secretary

Production

Assistant Maintainance

Supplies Sales

Some observations:

7/29/2019 Managing Company

http://slidepdf.com/reader/full/managing-company 19/39

The boss is only one. He may represent the Board of Directors. The members of theBoard are not represented in the chart, although they may fill in positions (for example,there may be a Sales Vice President, a Marketing Director, who is also a member of theBoard, or even an Assistant at the Production). As a member of the Board, participatesin the Decision Making meetings, has a voting right and may be assigned with other tasks, like the representation of the company in trade Fair, sign contracts with banks and

similar high rank authority, or even delegated the power to evaluate the employees,among them, his superiors!The “boss” (in this example the President, but it may be Chief Executive Officer, or differently called) has three duties; implement the decisions of the Board, Coordinate hissubordinates and resolve everyday implications. His duty is also to bring in the Boardevery matter that needs a Board Decision (when the subject is so serious as to affect thecompany) as in charge to compile the Agenda and Call the Board in a meeting.

Accounting, Marketing and Secretary cannot give orders, but only through the President.They are Staff Members.Production position can give orders (in fact he prepares programs) to the Assistant andMaintenance positions and receives Reports from them. If the Production Assistantneeds a change in Raw Material supply, he must refer it to the Production position. The

Production responsible, then, may ask the Supplies responsible to make this change. If the Supplies responsible does not agree, even if he thinks that this change is major for the company, their disagreement will be resolved by the President. If the Presidentthinks that this change is in fact major to the company, he will put in the Agenda of anOrdinary meeting, or Call an Extraordinary Meeting of the Board, to decide upon.

5 Human Resources essentialsWhen the work gets to be too much, you may find yourself toying with the idea of addingstaff to help out. But do you really need help? First, ask yourself if you need to hiresomeone or just be better organized. If you're having trouble getting organized, try locallibraries, community centers, or colleges for information or seminars on time

management.Can you afford an employee? Even if you know that you need the extra help, you'll stillneed to consider whether you can afford to hire a new employee. How do you know howmuch you can afford to pay? There's a tension between how much the employee'ssalary and benefits will drain your business's budget and how much extra money theemployee's presence will bring in.Look at your operating budget. How much slack is there in it? How much money couldbe cut from other areas, so you could use it to pay an extra person? Remember thatyou'll need to pay at least the minimum wage, not only under the law, but under thedanged to have your business boycotted. Don't forget about payroll taxes and legally

mandated employee benefits, like workers' compensation.Now, try to estimate how much extra income that employee would generate in the first

year. It's not always easy. If the employee is going to sell your product or services, it willbe easier to figure out how much extra income he or she would bring in than if theperson is going to perform data entry or cashier duties.But in the absence of a "cause and effect" relationship, consider other ways that anemployee could generate extra income:

• With an extra employee, would you have more time to market your services andexpand your business?

7/29/2019 Managing Company

http://slidepdf.com/reader/full/managing-company 20/39

• Would an extra employee allow you a chance to produce more products or servemore clients?

• Would an extra employee allow you to give your customers more efficient serviceor quicker delivery, with the result that higher quality would lead to morecustomers?

If the answer is "yes" to any of these, try to estimate how much extra business would begenerated by more, faster, and better delivery of your product or service.The math is simple. If you're fairly sure that the extra business would amount to morethan the minimum salary of the employee, then you are in a good position to hiresomeone. If the added business does not outweigh the minimum salary that you wouldhave to pay, then look for other alternatives to hiring a permanent employee.Will you really save time? Once you've got someone to help out, you'll have all thisextra time, right? Well, maybe. But don't forget, when you hire someone - especiallywhen you hire for the first time - you have to invest a lot of time in the hiring process, intraining the worker to get them up to speed, and in managing records.

5.1 Organizational Behavior basicsOrganizational behavior deals with the sociological and psychological attitude of theemployees, such as work satisfaction, leadership, conflicts in team work and the similar.For a small company, especially in early stages, it is a waste of resources to analyze theorganizational behavior, while your organization is not yet established, there is nostruggle for power, other than the one among partners, there is no disappointment, yet,there is no establishment to block the ambitions.

5.2 Human Resources Management basicsPeople working for you (employees or externals) will do their best for your company if you treat them as humans. They need to be paid, respected and cared about.First of all, there are laws protecting work and workers. Most of the Constitutions oblige

the Parliaments to make Laws in favor of the workers. These are legal obligations thatyou have to follow, as well as all bureaucracy that goes with it. Your accountant isusually able to guide you. Hiring a person is not a simple thing. You must follow all therules, otherwise you risk to loose money and time to remediate. Look at followingchecklist:

What authority (or more than one) must be notified about hiring and in whatform?

Is the Salary that you have agreed, over minimal wage? Is the Insurance Authority notified and how? Does the person hired belong to a Profession with special obligations (like

notification of his Professional Association, special insurance, additionalpayment)?

How many hours per week? What are the minimal allowances per day for a business trip? Is this person eligible for commuting reimbursement (because of distance or

profession)? Are the duties of the position corresponding with the actual duties? Do the actual duties oblige you for additional compensation, insurance, less

working hours, other obligations?

Reminder 1:

7/29/2019 Managing Company

http://slidepdf.com/reader/full/managing-company 21/39

You may sign a contract with an employee in which some terms are such that they omitthe legal minimal. Such contracts cannot stand before Court.

Reminder 2:Fully legal work costs less than any low cost work, in mid term.

Reminder 3:You save money when you pay all your obligations to the employees. They producemore value for your company than what you save from the payment.

Reminder 4:Pay your employees first. All the others can wait (at a cost).

Reminder 4:Remind your employees at any chance you have, that they are paid in due time at theLegal standards. If someone gets more than that, remind him /her that he /she has toearn it.

Reminder 5:If an employee neglects to perform a task assigned because he does not know how,arrange training for him / her. If he / she does not get trained or after training does notperform as expected, do not hesitate to fire.

5.3 Work-force costsThe arithmetic of the cost of an employee is simple. Since you are calculating the costson a production (or working hours) basis, you must calculate his / her hourly cost.Take the basic (or nominal) wage, add insurance (without the retained part), addbonuses, add the cost of other benefits (coffee break offers, commuting, company car costs etc) on a yearly basis and divide the sum with the real yearly working hours.Remember to subtract the working hours corresponding to the yearly leave for holidaysand other holidays.Wages are admittedly low. Your employees will try to find a second employment. It isbetter to keep them in your own work “overtime”, even if the cost is elevated.

Reminder:Do not calculate extraordinary bonuses and travel allowances as work-force costs. Theyare overheads.

5.3.1 Internal work

You may hire full time or part time. The cost of part-timers is not half the fully workingpersons cost but reaches 2/3.

You must create a working position when you have calculated what this position isexpected to do and how much time is needed.Managerial positions are created when you have 5 or more working positions and theyneed coordination. If they become more than 10, you need a second managerialposition. The more employees you have, the more managerial positions you will need,because they are working positions as well and if they exceed 5 they will need acoordinator. As the number of employees increases you will need to add morehierarchical levels.You may “Lease” workers (whenever this becomes valid), but only for auxiliary works.

7/29/2019 Managing Company

http://slidepdf.com/reader/full/managing-company 22/39

Reminder 1:You cannot create portions of working positions. You may hire only full time or part time(which is half a persons working hours). It is better to employ overtime.

Reminder 2:

Part time working needs a very well organized company, with too many workers thatpermit detailed specialization.

Reminder 3:Special agreements with the employees about overtime compensation are extremelyrarely denounced or complained about, as long as what you have promised you keep,even with a delay.

Reminder 4:You may hire your children, at any age, without fear of legal procedures. It is mostunlikely that the authorities will press charges. But beware; your partners may not likethis.

5.3.2 Outsourcing

Instead of hiring employees, you may assign the same tasks to independentprofessionals. You may be tempted to assign tasks instead of hiring. There is a danger that the Government will not accept it and charge you with fines and other penalties.

In general, you may only use external contractors, when: They have or will create an enterprise. They have premises of their own, even if they work in your premises. They do not have a working program, even when they are paid by the hour. They are proficient in a specific specialty, mentioned in their contract. They issue an invoice for their services.

In general terms, Staff tasks may be assigned to externals (outsourcing), but not linework position tasks.

5.3.3 Employment Liability

When you hire someone and he / she, during the execution of his duties, harmssomeone else with his doings or negligence, you have the full responsibility.Under this general rule, this harmed third party may sue you and win a compensation or even press charges on you, through the penal procedures.You never know what your employees are doing. They may harm a third party and claimthat they were just following the orders of the company to avoid their own liability.You never know what third parties may “invent” and ask for compensation, claiming thatan employee has harmed them.

If you ever receive a legal document of such a kind, however obvious it is that your company has no responsibility, call a Lawyer.What you can do to protect your company, is to describe the duties of each employee ina contract in which you limit the duties to the content of this document and give the rightto the employee to ask for written instructions for additional tasks you may assign tothem. If possible, make this documents unique, by either depositing the documents to anauthority (Tax Office, for example), or with a registration in your Books.It is bureaucratic, but if your company becomes very profitable, you will face suchoccurrences.

7/29/2019 Managing Company

http://slidepdf.com/reader/full/managing-company 23/39

5.3.4 Work Health and Safety

Employees feeling safe at work, perform better, are regular at work (minimizingabsenteeism) and rarely dismiss.The Ministry of Labor has a set of Health and Safety regulations, following the EuropeanStandards. Those regulations are minimal and even if you follow them, you are not safe

at all from potential accidents. Even when accidents happen, if you have taken allprecautions and you were ready to affront it, you are safe from being asked for enormous recompense.Here are some additional guidelines:Gather specific facts about your situation. Before you make any changes in your safety and health operations, you will want togather as much information as possible about the current conditions at your workplaceand about business practices that are already part of your safety and health program.This information can help you identify any workplace problems and see what's involvedin solving them.The assessment of your workplace should be conducted by the person responsible for the safety and health program and/or a professional safety and health consultant.

Request a consultation visit covering both safety and health to get a full survey of the hazards that exist in your workplace and those that could develop.

Establish a system, such as vendor consultations, to get expert help when youmake changes and to be sure that the changes are not introducing new hazardsinto your workplace. Also, find ways, such as through trade groups, to keepcurrent on newly recognized hazards in your industry.

Make a commitment to look carefully at each type of job done in your workplacefrom time to time, taking it apart step-by-step to see if there are any hiddenhazards in the equipment or procedures. Some initial instructions from aconsultant may be necessary.

Set up a system of checking to make sure that your hazard controls haven't failedand that new hazards haven't appeared. This is usually done by routine self-inspections.

Provide a way for your employees to let you know when they see things that lookharmful to them and encourage them to use the process.

Learn how to do a thorough investigation when things do go wrong and someonegets sick or hurt. This will help you find ways to prevent recurrences.

If you've been in business for a while, take the time to look back over severalyears of injury or illness experience to identify patterns that can lead to moreeffective prevention. Thereafter, periodically look back over several months of experience to determine if any new patterns are developing.

Once you know what your hazards and potential hazards are, you are ready to put inplace the systems that prevent or control those hazards. Your state or private consultantcan help you do this. Whenever possible, you will want to eliminate those hazards.Sometimes that can be done through substitution of a less toxic material or throughengineering controls that can be built in. When you cannot eliminate hazards, systemsshould be set up to control them.

Here are some actions to take:

Set up safe work procedures, based on the analysis of the hazards in your employees' jobs, and make sure that employees understand the job procedures

7/29/2019 Managing Company

http://slidepdf.com/reader/full/managing-company 24/39

and follow them. This may be easier if employees are involved in the analysisthat results in those procedures.

Be ready, if necessary, to enforce the rules for safe work procedures by askingyour employees to help you set up a disciplinary system that will be fair andunderstood by everyone.

Where necessary to protect your employees, provide, at your own cost, personal

protective equipment (PPE) according to published standards and be sure thatyour employees know why they need it, how to use it, and how to maintain it.

Provide for regular equipment maintenance to prevent breakdowns that cancreate hazards.

Plan for emergencies, including fire and natural disasters, and drill everyonefrequently so that if the real thing happens, everyone will know what to do, evenunder stressful conditions.

You must ensure the ready availability of medical personnel for advice andconsultation on matters of employee health. This does not mean that you mustprovide health care. But if health problems develop in your workplace, you areexpected to get medical help to treat them and their causes.

To fulfill the above requirements, consider the following:

Have an emergency medical procedure for handling injuries, transporting ill or injured workers, and notifying medical facilities with a minimum of confusion.Posting emergency numbers is a good idea.

Survey the medical facilities near your place of business and make arrangementsfor them to handle routine and emergency cases. Cooperative agreements couldpossibly be made with nearby plants that have medical personnel or facilities on-site.

If your business is remote from medical facilities, you are required to ensure thata person or persons be adequately trained and available to render first aid.

Adequate first aid supplies must be readily available for emergency use.

Arrangements for this training can be made through your local Red Crosschapter, your insurance carriers, your local safety council, and others.

Reminder:The employees working in production or other hazardous environments will try toconvince you that they can take care of themselves without all these PPE (helmets,boots, gloves, ear protection devices, masks etc.) equipment. Impose your will toprotection procedures with disciplinary actions. Soon they will get used to the use of PPE and safety procedures. It usually takes some weeks. After starting to use PPE theyfeel that they belong to a well organized company and they increase fidelity andperformance.

6 Financial essentials

6.1 Your Basic Bookkeeping To succeed in business, one of your most important tools is financial analysis, based onyour business records. Accurate financial records will help you answer some veryimportant questions. Are you making money, or losing it? How much? Is your businesson sound financial ground, or are troubles lurking ahead? A sound bookkeeping systemis the foundation on which all of this valuable financial information can be built.

7/29/2019 Managing Company

http://slidepdf.com/reader/full/managing-company 25/39

As a small business owner, you probably rely on an outside accountant to do your taxesand prepare financial statements. However, like many small business owners, you mayfind that it's too expensive to pay an accountant to do routine bookkeeping chores.Someone in your organization must take on the responsibility of keeping an accurate setof financial records. Fortunately, you may find this task easier than you thought,especially if you use your computer.

You are not going to become an accountant, especially if you choose to use “double-entry” book keeping (which is most advisable). You must understand some simpleprinciples of accounting.

6.2 Accounting BasicsThis is not an accounting guide, but yet you must understand how accounting works, sothat you know how your company is doing.

Accounting is a system of recording transactions of your company, so that all theproperty transformations can inform you about what your property is at any time. To doso, property is classified in “Accounts” and all the transactions are recorder there. Those

Accounts are registered in a book called “General Ledger”.In order to facilitate control, every transaction or property transformation is alsoregistered in a sequential manner one after the other, day after day) in another bookcalled “Journal”.Every year (called fiscal year) starts and ends with a Balance Sheet.

6.2.1 Balance Sheet

A Balance sheet is an account where Assets and Liabilities are put together. As in allaccounts, there is a left hand part and a right hand part. The two parts are equal.The left hand part contains the value of the property of the company, the right hand partcontains the financial sources that permitted the acquisition of this property.

6.2.2 Assets (Active)

They represent the current value of the property which the company owns. In case thatthe company holds property of others (even your personal property), it is not representedin the Assets part of the Balance.

At the end of the fiscal year the company counts all the possessions in an Inventory andevaluates them, so that they will be represented with their value.

6.2.2.1 Fixed Assets

Fixed Assets are those that are not items of trade, but they are used by the company for its operation. For example, a company car is a fixed asset, if the company sells cars,those cars are not fixed assets.Fixed assets loose their value as time passes by, except the land.

Studies on which the company foundation and development is based upon, are fixedassets, as long as they can be sold (together with the company) to a new owner.

6.2.2.2 Current Assets

Current assets are those commercialized by the company, or used in propertytransformation. Cash is one of them. The value of what your clients (or others) owe toyou, are current assets as well.

7/29/2019 Managing Company

http://slidepdf.com/reader/full/managing-company 26/39

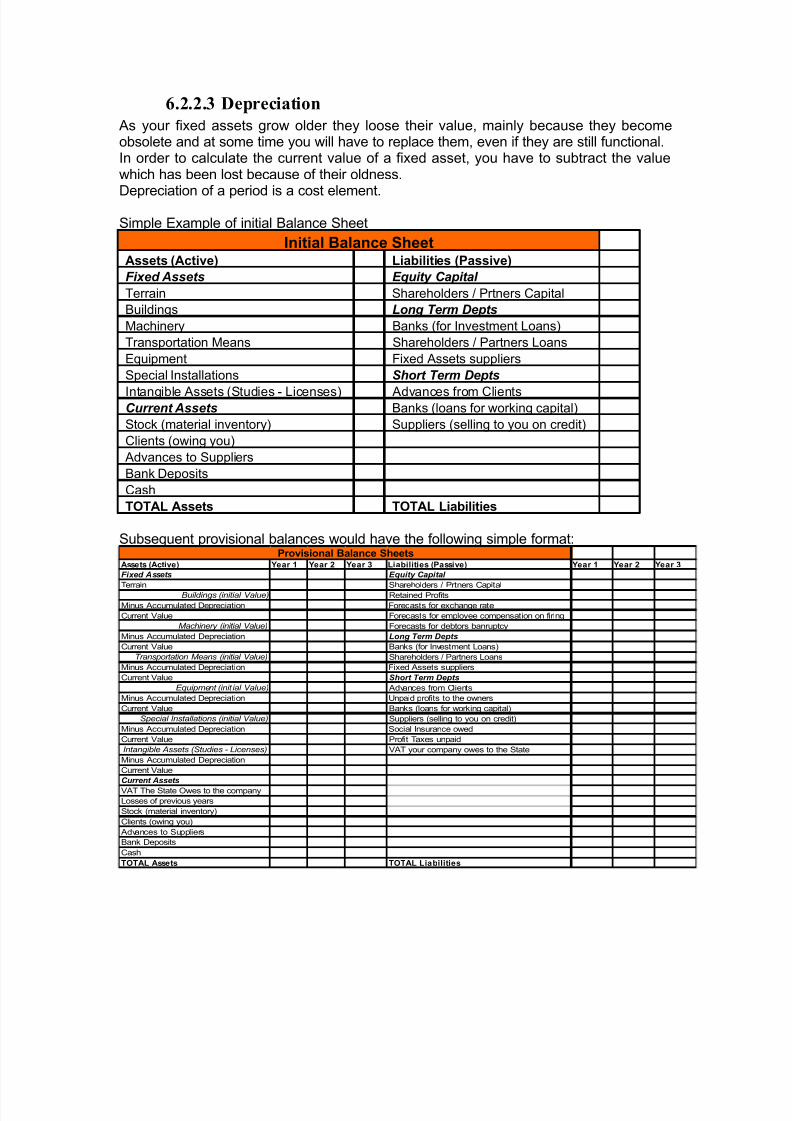

6.2.2.3 Depreciation

As your fixed assets grow older they loose their value, mainly because they becomeobsolete and at some time you will have to replace them, even if they are still functional.In order to calculate the current value of a fixed asset, you have to subtract the valuewhich has been lost because of their oldness.

Depreciation of a period is a cost element.

Simple Example of initial Balance Sheet

Initial Balance Sheet

Assets (Active) Liabilities (Passive)

Fixed Assets Equity Capital

Terrain Shareholders / Prtners Capital

Buildings Long Term Depts

Machinery Banks (for Investment Loans)

Transportation Means Shareholders / Partners Loans

Equipment Fixed Assets suppliers

Special Installations Short Term Depts

Intangible Assets (Studies - Licenses) Advances from ClientsCurrent Assets Banks (loans for working capital)

Stock (material inventory) Suppliers (selling to you on credit)

Clients (owing you)

Advances to Suppliers

Bank Deposits

Cash

TOTAL Assets TOTAL Liabilities

Subsequent provisional balances would have the following simple format:

Assets (Active) Year 1 Year 2 Year 3 Liabilities (Passive) Year 1 Year 2 Year 3

Fixed Assets Equity Capital

Terrain Shareholders / Prtners Capital