Managing chronological objects with =-1 timeDate and = … · timeDate Class timeSeries...

58

timeDate Class timeSeries Class Summary Managing chronological objects with timeDate and timeSeries Yohan Chalabi and Diethelm Wuertz ITP ETH, Zurich Rmetrics Association, Zurich Finance Online, Zurich R/Rmetrics Workshop Meielisalp June 2009

Transcript of Managing chronological objects with =-1 timeDate and = … · timeDate Class timeSeries...

timeDate Class timeSeries Class Summary

Managing chronological objects with timeDate

and timeSeries

Yohan Chalabi and Diethelm Wuertz

ITP ETH, ZurichRmetrics Association, Zurich

Finance Online, Zurich

R/Rmetrics WorkshopMeielisalpJune 2009

timeDate Class timeSeries Class Summary

Outline

1 timeDate ClasstimeDate DefinitionFinancial Center and Holiday Management

2 timeSeries ClasstimeSeres DefinitionPlotting timeSeries ObjectsSubsetting timeSeries ObjectsManipulating a timeSeries@recordIDs Concept

3 Summary

timeDate Class timeSeries Class Summary

Outline

1 timeDate ClasstimeDate DefinitionFinancial Center and Holiday Management

2 timeSeries ClasstimeSeres DefinitionPlotting timeSeries ObjectsSubsetting timeSeries ObjectsManipulating a timeSeries@recordIDs Concept

3 Summary

timeDate Class timeSeries Class Summary

Time and R

There are different date and time classes in R. The most common are

Date : It supports dates without times.

chron : It is a contributed package which provides dates and times.But there are not time zones or notion of daylight saving time(DST).

POSIXt : with its two subclasses POSIXct and POSIXlt. Theseclasses support time zone and DST. But time zone and DSTcalculations are passed to the operating system (OS) and may notwork if the OS has bugs or is not up-to-date!

timeDate Class timeSeries Class Summary

timeDate

timeDate class is for

mixing data collected in different time zones

calendar manipulations for business days, weekends, public andecclesiastical holidays.

and is almost compatible with the same class in S-Plus.

timeDate Class timeSeries Class Summary

timeDate class

The timeDate class represents calendar dates and times as

> library(timeDate)

> showClass("timeDate")

Class "timeDate" [package "timeDate"]

Slots:

Name: Data format FinCenter

Class: POSIXct character character

where @Data are the timestamps in POSIXct, @format is the formattypically applied to @Data and @FinCenter is the financial center.

timeDate Class timeSeries Class Summary

timeDate class

The timeDate class can be summarised as the combination of

POSIXct timestamps objects always in the GMT time zone

in the human readable ISO-8601 format standard which expressesdates as "%Y-%m-%d" and dates/times as "%Y-%m-%d %H:%M:%S"

with a financial center used for the time zone and daylight savingrules (DST).

timeDate Class timeSeries Class Summary

Create a timeDate object

There are different ways to generate a timeDate object.

timeDate()

timeSequence()

timeCalendar()

timeDate Class timeSeries Class Summary

Create a timeDate object, Cont’d

> Dates <- c("2007-01-01","2009-07-01")

> Times <- c( "23:12:55", "10:34:02")

> charvec <- paste(Dates, Times)

> timeDate(charvec, zone = "Zurich", FinCenter = "Tokyo")

Tokyo

[1] [2007-01-02 07:12:55] [2009-07-01 17:34:02]

> timeSequence(from = "2009-01-01", to = "2009-01-05", by = "day")

GMT

[1] [2009-01-01] [2009-01-02] [2009-01-03] [2009-01-04]

[5] [2009-01-05]

> timeCalendar(2009, m=1, d=1:4, h=16, zone = "Tokyo", FinCenter = "Zurich")

Zurich

[1] [2009-01-01 08:00:00] [2009-01-02 08:00:00]

[3] [2009-01-03 08:00:00] [2009-01-04 08:00:00]

timeDate Class timeSeries Class Summary

Operations

Many operations can be performed on timeDate objects.

Math Operations

Lagging

Rounding and Truncating

Subsetting

Logical Test

Coercions and Transformation

Concatentation and Reorderings

timeDate Class timeSeries Class Summary

FinCenter

“Financial Centers” allows mixing data collected in different time zones orhandling historical data recorded in the same time zone but with differentDST rules.

The local financial center can be defined with the global variablemyFinCenter and refers, by default, to the Greenwich Mean Time (GMT).

Note: By setting the financial center to a continent/city which liesoutside of the time zone used by your computer does not change anytime settings or environment variables used by your computer.

timeDate Class timeSeries Class Summary

list of FinCenters

There are almost 400 financial centers supported thanks to the Olsondata base. They can be listed with listFinCenter().Note: You can search for financial centers with regular expressions.

> FCs <- listFinCenter()

> head(FCs) # the first few

[1] "Africa/Abidjan" "Africa/Accra"

[3] "Africa/Addis_Ababa" "Africa/Algiers"

[5] "Africa/Asmara" "Africa/Bamako"

> str(FCs) # the "overview"

chr [1:397] "Africa/Abidjan" "Africa/Accra" ...

> listFinCenter("Europe/[AB].*") # -> nine

[1] "Europe/Amsterdam" "Europe/Andorra"

[3] "Europe/Athens" "Europe/Belgrade"

[5] "Europe/Berlin" "Europe/Bratislava"

[7] "Europe/Brussels" "Europe/Bucharest"

[9] "Europe/Budapest"

timeDate Class timeSeries Class Summary

DST rules

Each financial center has an associated function which returns its daylightsaving time rule (DST). Theses functions are named as their financialcenter, e.g. Zurich(), and return a data.frame with 4 columns,

> head(Zurich(), 8)

Zurich offSet isdst TimeZone numeric

1 1901-12-14 20:45:52 3600 0 CET -2147397248

2 1941-05-05 00:00:00 7200 1 CEST -904435200

3 1941-10-06 00:00:00 3600 0 CET -891129600

4 1942-05-04 00:00:00 7200 1 CEST -872985600

5 1942-10-05 00:00:00 3600 0 CET -859680000

6 1981-03-29 01:00:00 7200 1 CEST 354675600

7 1981-09-27 01:00:00 3600 0 CET 370400400

8 1982-03-28 01:00:00 7200 1 CEST 386125200

timeDate Class timeSeries Class Summary

Concatenation

Note: The c() method for timeDate objects takes care of the differentfinancial centers of the object to be concatenated.

> ZH <- timeDate("2009-01-01 16:00:00", zone = "GMT", FinCenter = "Zurich")

> NY <- timeDate("2009-01-01 18:00:00", zone = "GMT", FinCenter = "NewYork")

> c(ZH, NY)

Zurich

[1] [2009-01-01 17:00:00] [2009-01-01 19:00:00]

> c(NY, ZH)

NewYork

[1] [2009-01-01 13:00:00] [2009-01-01 11:00:00]

timeDate Class timeSeries Class Summary

Holidays

There are different functions to compute:

the last day in a given month and year,

the n-days before or after a given date,

the n-th occurrences of the n-days for a specified year/month,

or the last n-days for a specified year/month.

timeDate Class timeSeries Class Summary

Holidays

This gives

timeFirstDayInMonth()

timeLastDayInMonth()

timeFirstDayInQuarter()

timeLastDayInQuarter()

timeNthNdayInMonth()

timeLastNdayInMonth()

timeNdayOnOrAfter()

timeDate Class timeSeries Class Summary

Holidays

> tH <- listHolidays()

> # number of holiday days available in timeDate

> length(tH)

[1] 115

> # the first 10

> head(tH, 10)

[1] "Advent1st" "Advent2nd"

[3] "Advent3rd" "Advent4th"

[5] "AllSaints" "AllSouls"

[7] "Annunciation" "Ascension"

[9] "AshWednesday" "AssumptionOfMary"

> # The date of Easter for the next 3 years:

> Easter(2009:(2009+3))

GMT

[1] [2009-04-12] [2010-04-04] [2011-04-24] [2012-04-08]

timeDate Class timeSeries Class Summary

Calendar

The following three functions can be used as model to build new holidaycalendars.

holidayZURICH() : the Zurich holiday calendar,

holidayNYSE() : the NYSE stock exchange holiday calendar

and holidayTSX() : the TSX holiday calendar.

timeDate Class timeSeries Class Summary

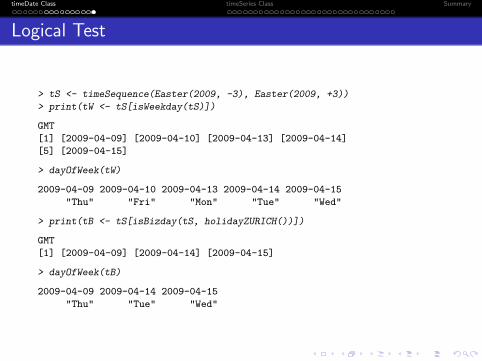

Logical Test

Weekdays, weekends, business days and holidays can be tested with thefunctions:

isWeekday()

isWeekend()

isBizday()

isHoliday()

timeDate Class timeSeries Class Summary

Logical Test

> tS <- timeSequence(Easter(2009, -3), Easter(2009, +3))

> print(tW <- tS[isWeekday(tS)])

GMT

[1] [2009-04-09] [2009-04-10] [2009-04-13] [2009-04-14]

[5] [2009-04-15]

> dayOfWeek(tW)

2009-04-09 2009-04-10 2009-04-13 2009-04-14 2009-04-15

"Thu" "Fri" "Mon" "Tue" "Wed"

> print(tB <- tS[isBizday(tS, holidayZURICH())])

GMT

[1] [2009-04-09] [2009-04-14] [2009-04-15]

> dayOfWeek(tB)

2009-04-09 2009-04-14 2009-04-15

"Thu" "Tue" "Wed"

timeDate Class timeSeries Class Summary

Outline

1 timeDate ClasstimeDate DefinitionFinancial Center and Holiday Management

2 timeSeries ClasstimeSeres DefinitionPlotting timeSeries ObjectsSubsetting timeSeries ObjectsManipulating a timeSeries@recordIDs Concept

3 Summary

timeDate Class timeSeries Class Summary

timeSeries class

The timeSeries class represents time series as

> library(timeSeries)

> showClass("timeSeries")

Class "timeSeries" [package "timeSeries"]

Slots:

Name: .Data units positions

Class: matrix character numeric

Name: format FinCenter recordIDs

Class: character character data.frame

Name: title documentation

Class: character character

Extends:

Class "structure", from data part

Class "vector", by class "structure", distance 2, with explicit coerce

Note: timeSeries extends the virtual class structure

timeDate Class timeSeries Class Summary

timeSeries class

where

@.Data : time series data in numeric matrix form

@positions : date/time stamps as a character vector

@format : format of the character vector in @positions

@FinCenter : the financial center of the data

@units : the column names of the data matrix

@recordsIDs : record identification for additional information as adata.frame

@title and @documentation : descriptive character strings

timeDate Class timeSeries Class Summary

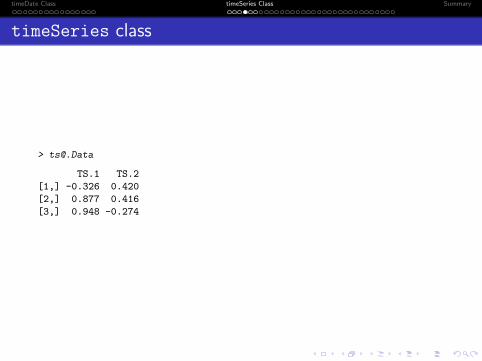

timeSeries class

> data <- matrix(round(rnorm(6), 3), ncol = 2)

> td <- timeCalendar()[1:3]

> ts <- timeSeries(data, td)

> ts

GMT

TS.1 TS.2

2009-01-01 -0.326 0.420

2009-02-01 0.877 0.416

2009-03-01 0.948 -0.274

timeDate Class timeSeries Class Summary

timeSeries class

TS.1 TS.2

[1,] -0.326 0.420

[2,] 0.877 0.416

[3,] 0.948 -0.274

timeDate Class timeSeries Class Summary

timeSeries class

> ts@positions

[1] 1230768000 1233446400 1235865600

> ts@units

[1] "TS.1" "TS.2"

> ts@format

[1] "%Y-%m-%d"

> ts@FinCenter

[1] "GMT"

> ts@title

[1] "Time Series Object"

> ts@documentation

[1] "Tue Jun 30 11:48:08 2009"

timeDate Class timeSeries Class Summary

Creation of timeSeries Objects

The generic function timeSeries() has different methods to generatetimeSeries objects.

> showMethods("timeSeries")

Function: timeSeries (package timeSeries)

data="ANY", charvec="ANY"

data="ANY", charvec="missing"

data="matrix", charvec="ANY"

data="matrix", charvec="missing"

data="matrix", charvec="numeric"

data="matrix", charvec="timeDate"

data="missing", charvec="ANY"

data="missing", charvec="missing"

timeDate Class timeSeries Class Summary

Plotting timeSeries Objects

The plot() function of timeSeries is implemented in the same way asthe function plot.ts() for regular time series objects ts in R’s basepackage.

Three different types of plots can be displayed :

Multiple plot : up to 10 subplots can be produced on one sheet of apaper

Single plot : all curves are drawn in one plot on the same sheet,

Scatter plot of two univariate ’timeSeries’ objects.

timeDate Class timeSeries Class Summary

Multiple Plots

> library(fEcofin)

> LPP <- as.timeSeries(data(SWXLP))[,4:6]

> plot(LPP, main = "LPP")

9511

012

5

LP25

9011

013

0

LP40

7090

110

2000−01−03 2001−06−22 2002−12−10 2004−05−30 2005−11−17 2007−05−08

LP60

Time

LPP

timeDate Class timeSeries Class Summary

Single Plots

> plot(LPP, plot.type = "single", col = 2:5, ylab = "Price")

2000−01−03 2001−06−22 2002−12−10 2004−05−30 2005−11−17 2007−05−08

7080

9010

011

012

013

0

timeDate Class timeSeries Class Summary

Subsetting

One can subset a timeSeires object byCountsDate/Time Vectors (timeDate)Logical testsOther common subsetting rules.

> showMethods("[", classes = "timeSeries")

Function: [ (package base)

x="timeSeries", i="ANY", j="index_timeSeries"

x="timeSeries", i="character", j="character"

x="timeSeries", i="character", j="index_timeSeries"

x="timeSeries", i="character", j="missing"

x="timeSeries", i="index_timeSeries", j="character"

x="timeSeries", i="index_timeSeries", j="index_timeSeries"

x="timeSeries", i="index_timeSeries", j="missing"

x="timeSeries", i="matrix", j="missing"

x="timeSeries", i="missing", j="character"

x="timeSeries", i="missing", j="index_timeSeries"

x="timeSeries", i="missing", j="integer"

(inherited from: x="timeSeries", i="missing", j="index_timeSeries")

x="timeSeries", i="missing", j="missing"

x="timeSeries", i="timeDate", j="character"

x="timeSeries", i="timeDate", j="index_timeSeries"

x="timeSeries", i="timeDate", j="missing"

x="timeSeries", i="timeSeries", j="index_timeSeries"

x="timeSeries", i="timeSeries", j="missing"

timeDate Class timeSeries Class Summary

Column Statistics

This functions return a numeric vector of the same length as the numberof columns of the timeSeries.

’colStats’ calculates column statistics,

’colSums’ calculates column sums,

’colMeans’ calculates column means,

’colSds’ calculates column standard deviations,

’colVars’ calculates column variances,

’colSkewness’ calculates column skewness,

’colKurtosis’ calculates column kurtosis,

’colMaxs’ calculates maximum values in each column,

’colMins’ calculates minimum values in each column,

’colProds’ computes product of all values in each column,

’colQuantiles’ computes quantiles of each column.

timeDate Class timeSeries Class Summary

Column Statistics

> colMeans(LPP)

LP25 LP40 LP60

108.353 102.887 95.412

> colQuantiles(LPP)

LP25 LP40 LP60

97.708 88.278 76.036

> colStats(LPP, FUN = "median")

LP25 LP40 LP60

103.86 100.35 93.82

timeDate Class timeSeries Class Summary

Cumulated Column Statistics

Functions to compute cumulated column statistics are

colCumsums returns column cumulated sums

colCummaxs returns column cumulated maximums

colCummins returns column cumulated minimums

colCumprods returns column cumulated products

colCumreturns returns column cumulated returns

timeDate Class timeSeries Class Summary

Manipulating a timeSeries

Additional timeSeries operations include functions for

Sorting and reverting

Aggregation

Lagging

Rolling windows

Binding and merging

Adding new methods

@recordIDs Concept

timeDate Class timeSeries Class Summary

Sorting and Ordering

The time stamps of timeSeries objects can be sampled, sorted, andreverted.> ts <- dummySeries()

> ts

GMT

TS.1 TS.2

2009-01-01 0.634370 0.508988

2009-02-01 0.206838 0.569707

2009-03-01 0.617899 0.138199

2009-04-01 0.954138 0.532224

2009-05-01 0.094575 0.248911

2009-06-01 0.970725 0.366148

2009-07-01 0.397929 0.022207

2009-08-01 0.066369 0.230418

2009-09-01 0.426999 0.921124

2009-10-01 0.512974 0.918697

2009-11-01 0.403992 0.613478

2009-12-01 0.111533 0.209306

timeDate Class timeSeries Class Summary

Sorting and Ordering

> sa <- sample(ts)

> sa

GMT

TS.1 TS.2

2009-07-01 0.397929 0.022207

2009-05-01 0.094575 0.248911

2009-03-01 0.617899 0.138199

2009-09-01 0.426999 0.921124

2009-10-01 0.512974 0.918697

2009-01-01 0.634370 0.508988

2009-06-01 0.970725 0.366148

2009-12-01 0.111533 0.209306

2009-02-01 0.206838 0.569707

2009-08-01 0.066369 0.230418

2009-11-01 0.403992 0.613478

2009-04-01 0.954138 0.532224

timeDate Class timeSeries Class Summary

Sorting and Ordering

> so <- sort(sa)

> so

GMT

TS.1 TS.2

2009-01-01 0.634370 0.508988

2009-02-01 0.206838 0.569707

2009-03-01 0.617899 0.138199

2009-04-01 0.954138 0.532224

2009-05-01 0.094575 0.248911

2009-06-01 0.970725 0.366148

2009-07-01 0.397929 0.022207

2009-08-01 0.066369 0.230418

2009-09-01 0.426999 0.921124

2009-10-01 0.512974 0.918697

2009-11-01 0.403992 0.613478

2009-12-01 0.111533 0.209306

timeDate Class timeSeries Class Summary

Sorting and Ordering

> re <- rev(so)

> re

GMT

TS.1 TS.2

2009-12-01 0.111533 0.209306

2009-11-01 0.403992 0.613478

2009-10-01 0.512974 0.918697

2009-09-01 0.426999 0.921124

2009-08-01 0.066369 0.230418

2009-07-01 0.397929 0.022207

2009-06-01 0.970725 0.366148

2009-05-01 0.094575 0.248911

2009-04-01 0.954138 0.532224

2009-03-01 0.617899 0.138199

2009-02-01 0.206838 0.569707

2009-01-01 0.634370 0.508988

timeDate Class timeSeries Class Summary

Aggregation

> (by <- timeSequence(from = "2003-01-01", to = "2005-01-01", by = "quarter"))

GMT

[1] [2003-01-01] [2003-04-01] [2003-07-01] [2003-10-01]

[5] [2004-01-01] [2004-04-01] [2004-07-01] [2004-10-01]

[9] [2005-01-01]

> aggregate(LPP, by, mean)

GMT

LP25 LP40 LP60

2003-01-01 100.37 97.073 92.658

2003-04-01 97.46 86.600 73.363

2003-07-01 100.43 90.155 77.372

2003-10-01 103.42 94.390 82.812

2004-01-01 104.86 96.218 84.984

2004-04-01 108.08 99.842 88.920

2004-07-01 107.71 99.763 89.154

2004-10-01 107.71 99.238 88.076

2005-01-01 109.85 101.101 89.602

timeDate Class timeSeries Class Summary

Rolling Windows

Rolling windows can be performed with applySeries().

> by <- periods(time(LPP), period = "24m", by = "6m")

> applySeries(LPP, from = by$from, to = by$to, FUN = "colMeans")

GMT

LP25 LP40 LP60

2001-12-31 100.911 99.438 97.310

2002-06-30 101.209 98.476 94.639

2002-12-31 100.252 95.199 88.487

2003-06-30 99.437 92.248 83.037

2003-12-31 100.420 92.120 81.543

2004-06-30 102.222 93.126 81.524

2004-12-31 104.943 95.920 84.295

2005-06-30 108.678 100.223 89.070

2005-12-31 112.648 104.784 94.170

2006-06-30 116.179 109.216 99.525

2006-12-31 120.190 114.424 105.964

timeDate Class timeSeries Class Summary

Merging and Binding

There are four functions to bind time series together. These are, withincreasing complexity, c(), cbind(), rbind() and merge().

> (ts1 <- timeSeries(matrix(rnorm(4), ncol = 2), c("2009-01-01", "2009-03-01")))

GMT

TS.1 TS.2

2009-01-01 0.065859 -0.84444

2009-03-01 -1.434893 0.11602

> (ts2 <- timeSeries(matrix(rnorm(4), ncol = 2), c("2009-02-01", "2009-04-01")))

GMT

TS.1 TS.2

2009-02-01 1.31517 -0.97362

2009-04-01 0.99981 -0.97810

timeDate Class timeSeries Class Summary

c()

> c(ts1, ts2)

[1] 0.065859 -1.434893 -0.844442 0.116023 1.315173

[6] 0.999811 -0.973622 -0.978103

timeDate Class timeSeries Class Summary

cbind()

> cbind(ts1, ts2)

GMT

TS.1.1 TS.2.1 TS.1.2 TS.2.2

2009-01-01 0.065859 -0.84444 NA NA

2009-02-01 NA NA 1.31517 -0.97362

2009-03-01 -1.434893 0.11602 NA NA

2009-04-01 NA NA 0.99981 -0.97810

timeDate Class timeSeries Class Summary

rbind()

> rbind(ts1, ts2)

GMT

TS.1_TS.1 TS.2_TS.2

2009-01-01 0.065859 -0.84444

2009-03-01 -1.434893 0.11602

2009-02-01 1.315173 -0.97362

2009-04-01 0.999811 -0.97810

timeDate Class timeSeries Class Summary

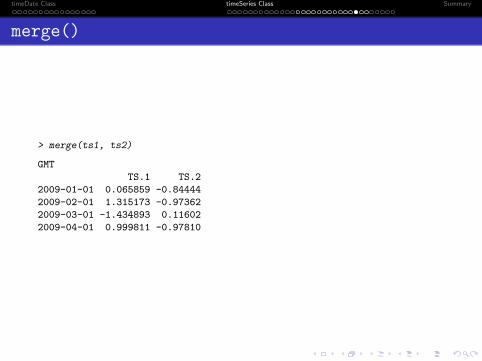

merge()

> merge(ts1, ts2)

GMT

TS.1 TS.2

2009-01-01 0.065859 -0.84444

2009-02-01 1.315173 -0.97362

2009-03-01 -1.434893 0.11602

2009-04-01 0.999811 -0.97810

timeDate Class timeSeries Class Summary

Adding new methods

Since timeSeries is an S4 class, we can use the functionsetMethod() to create new methods for a generic function whichhas can not handle by default the class.

In this example, we write a method for the lowess() function fromthe stats package.

> setMethod("lowess", "timeSeries",

function(x, y = NULL, f = 2/3, iter = 3)

{

stopifnot(isUnivariate(x))

series(x) <- stats::lowess(x = x, y, f, iter)$y

x

})

[1] "lowess"

timeDate Class timeSeries Class Summary

Adding new methods

> LP60 <- LPP[,"LP60"]

> LP60low <- lowess(LP60, f = 0.08)

> plot(LP60)

> lines(LP60low, col = "brown", lwd = 2)

2000−01−03 2001−06−22 2002−12−10 2004−05−30 2005−11−17 2007−05−08

7080

9010

011

012

0

timeDate Class timeSeries Class Summary

@recordIDs Concept

The slot @recordIDs is meant for additional information that wewant to keep for each time entries but which is not part of data part.

As starting from timeSeries version ’2100.84’ we have added amethod for the operator ’$’ to access the @recordIDs as well asthe data part.

by default show() will print the data part with the @recordIDs.Note the ’*’ in the column names of @recordIDs in the output.

@recordIDs can be used to give a data.frame behavior to yourtime series.

> ts$id <- "id"

> head(ts)

GMT

TS.1 TS.2 id*

2009-01-01 0.634370 0.508988 id

2009-02-01 0.206838 0.569707 id

2009-03-01 0.617899 0.138199 id

2009-04-01 0.954138 0.532224 id

2009-05-01 0.094575 0.248911 id

2009-06-01 0.970725 0.366148 id

> cov(ts)

TS.1 TS.2

TS.1 0.094909 0.017982

TS.2 0.017982 0.084142

timeDate Class timeSeries Class Summary

@recordIDs Example

A good example is to include turnpoints of the smoothed index tothe time series.

We can use the turnpoints() function from the R packagepastecs1.

The function determines the number and the positions of extrema,i.e. the turning points, either peaks or pits, in a regular time series.

> library(pastecs)

> setMethod("turnpoints", "timeSeries", function(x)

{

stopifnot(isUnivariate(x))

tp <- turnpoints(as.ts(x))

x$peaks <- tp$peaks #-> need timeSeries >= 2100.84

x$pits <- tp$pits

x

})

[1] "turnpoints"

1Ibanez, Grosjean & Etienne, 2009

timeDate Class timeSeries Class Summary

@recordIDs Example

> head(LP60low <- turnpoints(LP60low))

GMT

LP60 peaks* pits*

2000-01-03 97.730 FALSE FALSE

2000-01-04 97.767 FALSE FALSE

2000-01-05 97.805 FALSE FALSE

2000-01-06 97.842 FALSE FALSE

2000-01-07 97.880 FALSE FALSE

2000-01-10 97.917 FALSE FALSE

timeDate Class timeSeries Class Summary

@recordIDs Example

We plot the original index series and the smoothed series and add pointsfor the peaks and pits in green and red respectively.

> plot(LP60)

> lines(LP60low, col = "brown", lwd = 2)

> points(LP60low[LP60low$peaks,], col = "green3", pch = 24)

> points(LP60low[LP60low$pits,], col = "red", pch = 25)

Note: the use of the operator ’$’.

timeDate Class timeSeries Class Summary

@recordIDs Example

2000−01−03 2001−06−22 2002−12−10 2004−05−30 2005−11−17 2007−05−08

7080

9010

011

012

0

timeDate Class timeSeries Class Summary

Outline

1 timeDate ClasstimeDate DefinitionFinancial Center and Holiday Management

2 timeSeries ClasstimeSeres DefinitionPlotting timeSeries ObjectsSubsetting timeSeries ObjectsManipulating a timeSeries@recordIDs Concept

3 Summary

timeDate Class timeSeries Class Summary

Summary

timeSeries is meant to have a matrix like behavior

With some aspects of a data.frame,

It can handle ordered/unordered data and display them in any order.

It takes care of financial centers when merging/binding.

And has facilities to manage calendars thanks to the timeDatepackage.

timeDate Class timeSeries Class Summary

References I

D. Wuertz, Y. Chalabi, W. Chen, A. Ellis,Portfolio Optimization with R/Rmetrics.Finance Online, 2009.

D. Wuertz, Y. Chalabi, A. Ellis,FAQ - Time Series Objects for R in Finance

timeDate Class timeSeries Class Summary

> toLatex(sessionInfo())

R version 2.10.0 Under development (unstable) (2009-06-23r48824), i686-pc-linux-gnu

Locale: LC_CTYPE=en_US.UTF-8, LC_NUMERI ...

Base packages: base, datasets, graphics, grDevices, methods, stats,utils

Other packages: boot 1.2-37, fEcofin 2100.77, pastecs 1.3-8,timeDate 2100.86, timeSeries 2100.84

Loaded via a namespace (and not attached): tools 2.10.0

timeDate Class timeSeries Class Summary

Managing chronological objects with timeDate

and timeSeries

Yohan Chalabi and Diethelm Wuertz

ITP ETH, ZurichRmetrics Association, Zurich

Finance Online, Zurich

R/Rmetrics WorkshopMeielisalpJune 2009