Managerial Accounting: An Introduction To Concepts, Methods, And Uses

26

Managerial Accounting: An Introduction To Concepts, Methods, And Uses Chapter 4 Strategic Management of Costs, Quality, and Time Maher, Stickney and Weil

-

Upload

tiger-gonzales -

Category

Documents

-

view

22 -

download

0

description

Managerial Accounting: An Introduction To Concepts, Methods, And Uses. Chapter 4 Strategic Management of Costs, Quality, and Time. Maher, Stickney and Weil. Learning Objectives (Slide 1 of 2). Distinguish between the traditional view of quality and the quality-based view. - PowerPoint PPT Presentation

Transcript of Managerial Accounting: An Introduction To Concepts, Methods, And Uses

Managerial Accounting:

An Introduction To Concepts, Methods, And Uses

Chapter 4

Strategic Management

of Costs, Quality, and Time

Maher, Stickney and Weil

Learning Objectives (Slide 1 of 2)

Distinguish between the traditional view of quality and the quality-based view.

Define quality according to the customer.

Compare the costs of quality control to the costs of failing to control quality.

Explain why firms make trade-offs in quality control costs and failure costs.

Learning Objectives (Slide 2 of 2)

Describe the tools firms use to identify quality control problems.

Explain why just-in-time requires total quality management.

Explain why time is important in a competitive environment.

Explain how activity-based management can reduce customer response time.

Explain how traditional managerial accounting systems require modifications to support total quality management.

Explain Traditional Versus Quality-Based View

What is quality according to the customer?

List Some Examples of Performance Measures

Quality Control

Improving quality may be costly, but failing to improve quality may be equally costly

Costs of controlling and improving quality include what?

Prevention Costs

What are some prevention costs?

Appraisal Costs

Costs to detect individual units of products that do not conform to specifications include:

Costs of Failing to Control

& Improve Quality (Slide 1 of 2)

Internal failure costs - costs of detecting nonconforming products and services before delivery to customers

Scrap

Rework to correct defects

Reinspection/retesting after completing rework

Costs of Failing to Control

& Improve Quality (Slide 2 of 2)

External failure costs - costs of detecting nonconforming products and services after delivery to customers

Warranty repairs

Product liability resulting from product failure

Marketing costs to improve tarnished company image

Lost sales from customer dissatisfaction

Identifying Quality Problems

Signals provided by these tools may be:

Warnings - indicate that something is wrong

Diagnostic- suggest cause of problem and possible solutions

Explain Control Charts

Discuss Pareto Charts

Review Cause-and-Effect Analysis

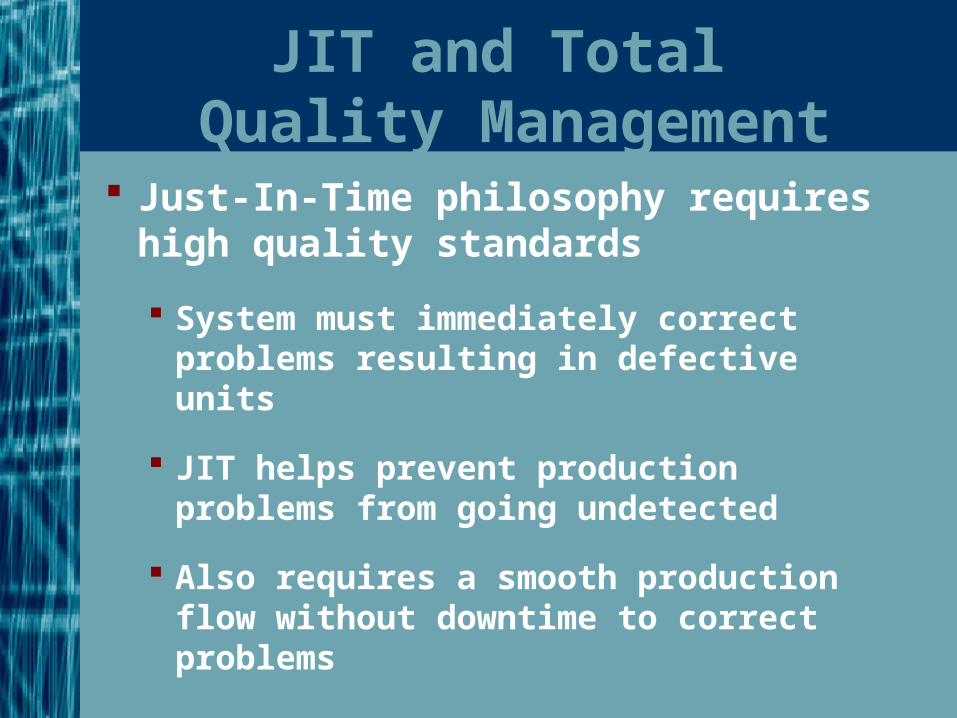

JIT and Total Quality Management

Just-In-Time philosophy requires high quality standards

System must immediately correct problems resulting in defective units

JIT helps prevent production problems from going undetected

Also requires a smooth production flow without downtime to correct problems

Importance of Time in a Competitive Environment

Competitive markets demand shorter new-product development and more rapid response to customers

Customer response time falls into two categories:

New-product development time

Operational measures of time

Comment on New-Product Development Time

What is break-even time?

What are operational measures of time?

Activity-Based Management to Improve Customer Response Time

ABM helps improve customer response time by identifying :

Activities that consume the most resources, both in dollars and time

Non-value-added activities

Describe Customer Response Time

Balanced Scorecard

Reports an integrated group of financial and nonfinancial performance measures, includes the following four areas

Financial

Internal business processes

Learning and Growth

Customer

Draw a Balanced Scorecard & Include

Sample Measures

Review Total Quality Management

If you have any comments or suggestions concerning this PowerPoint Presentation for Managerial Accounting, An Introduction To Concepts, Methods, And Uses, please contact:

Dr. Michael Blue, CFE, CPA, CMA [email protected]

Bloomsburg University of Pennsylvania