MANAGEMENT’S DISCUSSION AND ANALYSIS AND CONSOLIDATED ... · management’s discussion and...

80

MANAGEMENT’S DISCUSSION AND ANALYSIS AND CONSOLIDATED FINANCIAL STATEMENTS For the Years Ended December 31, 2016 and 2015 WORLDWIDE KNOWLEDGE - LOCAL SOLUTIONS ™

Transcript of MANAGEMENT’S DISCUSSION AND ANALYSIS AND CONSOLIDATED ... · management’s discussion and...

MANAGEMENT’S DISCUSSION AND ANALYSIS AND CONSOLIDATED FINANCIAL STATEMENTS

For the Years Ended December 31, 2016 and 2015

WORLDWIDE KNOWLEDGE - LOCAL SOLUTIONS™

Page left intentionally blank

Trican Well Service Ltd.

MD&A Years Ended December 31, 2015 & 2016 | 03

CONTINUING OPERATIONS - FINANCIAL REVIEW

Three months ended Twelve months ended

($ millions, except per share amounts, unaudited)

Dec. 31, 2016

Dec. 31, 2015

Sept. 30, 2016

Dec. 31, 2016

Dec. 31, 2015

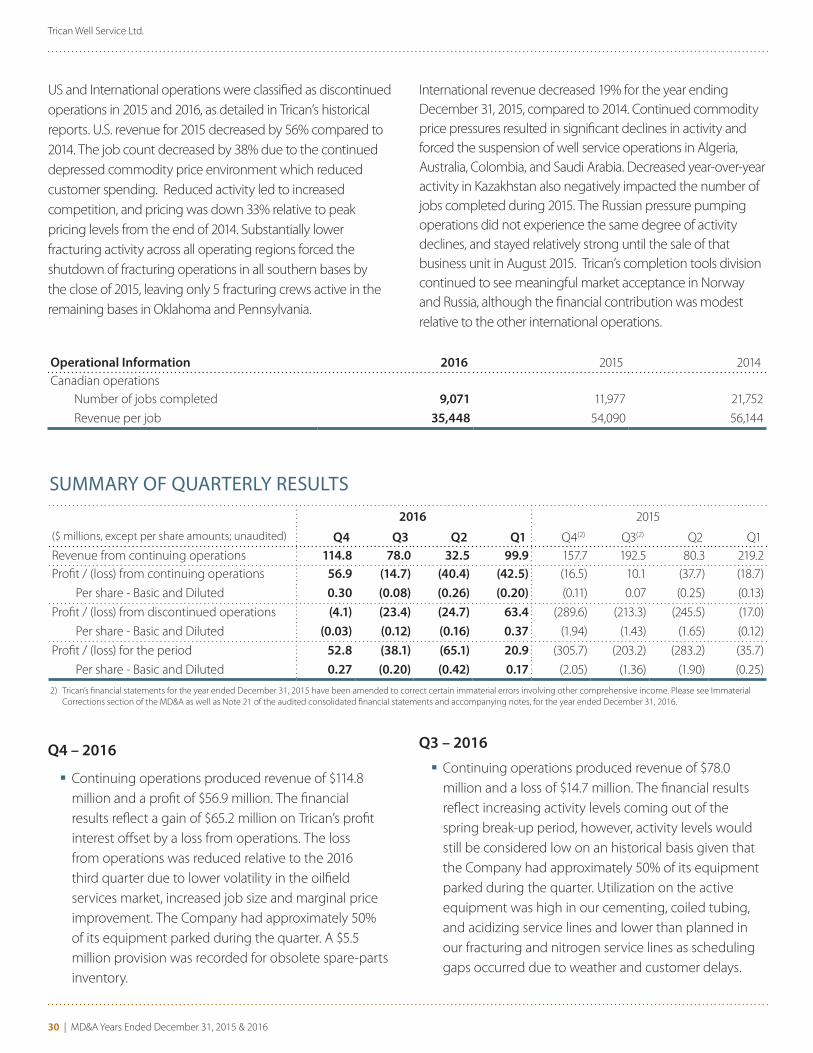

Revenue 114.8 157.8 78.0 325.2 649.7

Operating income / (loss) (1) (7.4) 14.7 (6.8) (69.8) 16.0

Adjusted operating income / (loss) (1) 1.1 19.4 (3.2) (37.4) 34.9

Gross profit / (loss) (10.1) (7.2) (13.7) (83.5) (26.7)

Net income / (loss) 56.9 (16.5) (14.7) (40.7) (62.8)

Per share - basic and diluted 0.29 (0.11) (0.08) (0.24) (0.42)

Notes:

(1) Trican makes reference to operating income / (loss), adjusted operating income / (loss), adjusted general and administrative expenses. These measures are not recognized under International

Financial Reporting Standards (IFRS) and are considered non-GAAP measures. Management believes that, in addition to gross profit / (loss) and profit / (loss), operating income / (loss), adjusted

operating income / (loss); and adjusted general and administrative expenses, adjusted corporate expenses are useful supplemental measures.

� Operating income / (loss) provides investors with an indication of profit / (loss) before depreciation and amortization, foreign exchange gains and losses, asset impairment, other

(income) / loss, finance costs and income tax expense / (recovery).

� Adjusted operating income / (loss) provides investors with an indication of operating income before equity-settled share-based compensation, amortization of debt costs, severance

costs and excludes items that are significant but not recurring in the normal course of operations. It provides investors with an indication of comparable operating income / (loss)

between periods and provides an indication of measures used for debt covenant calculations.

� Adjusted general and administrative expenses combined with adjusted corporate expenses provides investors with an indication of total overhead costs before equity-settled share-

based compensation, amortization of debt costs and severance costs.

Investors should be cautioned that operating income / (loss) and adjusted operating income / (loss) should not be construed as an alternative to gross profit / (loss) or profit / (loss) determined in

accordance with IFRS as an indicator of Trican’s performance. Trican’s method of calculating operating income / (loss), adjusted operating income / (loss), adjusted general and administrative ex-

penses and adjusted corporate expenses may differ from that of other companies and accordingly may not be comparable to measures used by other companies. See also “Non-GAAP Disclosure”

section of this report.

MANAGEMENT’S DISCUSSION AND ANALYSISAND CONSOLIDATED FINANCIAL STATEMENTSFor the Years Ended December 31, 2016 and 2015

The following Management’s Discussion and Analysis (“MD&A”) of the financial condition and results of operations of Trican Well Service Ltd. (“Trican” or “the Company”) has been prepared as at and for the year ended December 31, 2016, taking into consideration information available to February 22, 2017, and should be read in conjunction with the audited annual consolidated financial statements and accompanying notes.

OVERVIEWHeadquartered in Calgary, Alberta, Trican has continuing operations in Canada, which provide a comprehensive array of specialized products, equipment and services that are used during the exploration and development of oil and gas reserves provided by a highly-trained workforce

dedicated to safety and operational excellence. The Company also has minority ownership interests in Keane Group Holdings, LLC in the United States. The following MD&A focuses on the financial and operating results for Trican’s continuing operations.

For further details related to Trican’s discontinued operations in Canada (related to the completions tools services), Russia (related to pressure pumping operations and completions tools services), United States (related to pressure pumping operations and completions tools services), Australia, Algeria, Colombia, Kazakhstan, Norway and Saudi Arabia, please refer to the discontinued operations section of the MD&A and the consolidated financial statements and accompanying notes, as at and for the year ended December 31, 2016.

Trican Well Service Ltd.

4 | MD&A Years Ended December 31, 2015 & 2016

FOURTH QUARTER HIGHLIGHTSConsolidated revenue from continuing operations for the fourth quarter of 2016 was $114.8 million, an increase of 47% compared to the 2016 third quarter. Adjusted operating income for the quarter was $1.1 million which is $4.3 million higher than adjusted operating income for Q3 2016. The revenue increase was primarily due to an increase in activity combined with larger job sizes. An increase in the number of frac stages and proppant pumped per job was experienced during the quarter and were the primary drivers of the larger job sizes.

Utilization of our active equipment was below expectations at the start of the quarter due to wet weather and a delayed freeze up, however, it increased rapidly in mid November when freeze up occurred and remained high throughout the second half of the quarter. December activity remained high as more work was performed during the Christmas break and the break was shorter than anticipated. The Company continued to operate approximately 50% of its equipment during the quarter. Our headcount increased as we converted two fracturing crews from twelve hour crews to twenty-four hour crews which expanded our fracturing capacity coming into the 2017 first quarter. Three cementing crews were also added by reactivating parked equipment during the quarter. Hiring qualified personnel to activate parked equipment has become the most significant challenge to meeting current industry demand.

Average pricing for our customers marginally increased between Q3 2016 and Q4 2016. Pricing for most of our anchor customers slightly increased; however, pricing for spot work is estimated to have increased by approximately 10%. 2017 first quarter average pricing is expected to increase approximately 10% relative to Q3 2016 exit levels.

The Company has been focused on adjusting its cost structure to the level of activity and pricing environment experienced during the cyclical lows experienced during

the past two years. There was some additional consolidation of facilities in the quarter which resulted in meaningful severance costs being incurred. Management believes that we have exited the 2016 fourth quarter with an efficient cost structure from a cost perspective and we believe this cost structure can handle the level of work being performed during the 2017 first quarter. Management’s current expectations are that activity will continue to increase after spring break-up and our cost structure will likely increase at that time to handle the demands of increased activity; however, management believes maintaining a disciplined and efficient cost structure as activity increases will be critical to improving profitability during 2017.

The operating loss from continuing operations was $7.4 million and adjusted operating income was $1.1 million for the quarter. A $5.5 million write-down of obsolete spare parts inventory combined with severance costs of $1.6 million, amortization of debt issuance costs of $0.7 million and an additional $0.7 million in equity-settled share-based compensation expense accounts for the difference between the operating loss from continuing operations and adjusted operating income.

In January 2017, Trican sold its shares in National Oilwell Varco (“NOV”) and monetized a portion of its Investments in Keane(1) for net proceeds of approximately USD $20.7 million and USD $28.4 million, respectively. The proceeds were used to further pay down Trican’s outstanding long-term debt. The partial monetization of the Investments in Keane was a result of Keane’s initial public offering on January 20, 2017. Keane’s IPO valuation was significantly higher than its valuation as a private company and, as a result, Trican has increased the value of its Investments in Keane to $231.0 million.

(1) “Investments in Keane” is a defined term that collectively refers to Trican’s direct investments in Keane Group Holdings, LLC which was converted into Trican’s direct investments in Keane Investor Holdings, LLC just prior to the initial public offering (“IPO”) of Keane Group, Inc. Please refer to the “Investments in Keane” section of this MD&A for a detailed description of Trican’s Investments in Keane.

Trican Well Service Ltd.

MD&A Years Ended December 31, 2015 & 2016 | 5

CONTINUING OPERATIONS - COMPARATIVE QUARTERLY INCOME STATEMENTS ($thousands, unaudited) Three months ended

Dec. 31, 2016

% of Revenue

Dec. 31, 2015

% of Revenue

Sept. 30, 2016

% of Revenue

Revenue 114,769 100% 157,752 100% 78,045 100%Expenses Materials and operating 109,546 95% 145,519 92% 76,552 98% General and administrative 4,404 4% 2,411 2% 3,837 5%Operating income / (loss) - Canadian Operations (1) 819 1% 9,822 6% (2,344) (3%)Corporate expenses 8,208 7% (4,840) (3%) 4,425 6%Operating income / (loss) - Continuing Operations (1) (7,389) (6%) 14,662 9% (6,769) (9%) Finance costs 4,655 4% 15,725 10% 4,334 6% Depreciation and amortization 16,281 14% 19,215 12% 16,423 21% Foreign exchange (gain) / loss (331) 0% 7,221 5% 394 1% Asset impairment 3,136 3% 4,996 3% 1,999 3% Finance and other (income) / expense (66,524) (58%) 1,621 1% (2,905) (4%)Income / (loss) before income taxes 35,394 31% (34,116) (22%) (27,014) (35%)Income tax expense / (recovery) (21,539) (19%) (17,613) (11%) (12,268) (16%)Net income / (loss) - Continuing Operations 56,933 (50%) (16,503) (10%) (14,746) (19%)

Adjusted operating income / (loss) - Canadian Operations (1) 7,829 7% 12,312 8% (369) (0%)Adjusted operating income / (loss) - Continuing Operations (1) 1,111 1% 19,418 12% (3,212) (4%)Gross profit / (loss) (1) (10,064) (9%) (7,201) (5%) (13,650) (17%)Job count 2,780 2,887 2,515Revenue per job 40,745 54,390 30,634

(1) See the first page of this report for a description of operating income / (loss) and adjusted operating income / (loss). Gross profit / (loss) has been presented in this table as it is the most directly comparable measure calculated in accordance with IFRS to operating income / (loss).

Sales Mix

(unaudited)Three months ended, Dec. 31, 2016 Dec. 31, 2015 Sept. 30, 2016% of Total RevenueFracturing 57% 64% 56%

Cementing 26% 18% 28%

Industrial Services 5% 3% 5%

Coiled Tubing 3% 2% 3%

Acidizing 4% 2% 4%

Nitrogen 3% 9% 2%

Other 2% 2% 2%

Total 100% 100% 100%

Trican Well Service Ltd.

6 | MD&A Years Ended December 31, 2015 & 2016

Q4 2016 versus Q4 2015

Revenue for the fourth quarter of 2016 decreased by 27% compared to the fourth quarter of 2015. Demand for most of our services was comparable to 2015 fourth quarter demand. However, pricing for all of our services and demand for nitrogen services was substantially lower relative to the 2015 fourth quarter. The job count and revenue per job decreased 4% and 25%, respectively, as compared to last year. The decrease in revenue per job was largely a result of lower pricing for our services combined with a shift in sales mix

towards the cementing service line which typically generates a lower revenue per job relative to the fracturing service line.

Materials and operating expenses increased to 95% of revenue compared to 92% for the same period in 2015 and includes the impact of a $5.5 million write-down of obsolete spare parts inventory recorded in 2016. Materials and operating expenses as a percentage of revenue is consistent with Q4 2015 levels after excluding the write-down. The reductions realized to our fixed and variable cost structure during 2016 have largely offset the significant pricing declines experienced since the 2015 fourth quarter.

General & Admin. Corporate Expense

($ thousands; unaudited)Three months ended,

Dec. 31, 2016

Dec. 31, 2015

Dec. 31, 2016

Dec. 31, 2015

Total Expenses 4,404 2,411 8,208 (4,840)

Adjusted for:

2015 Amended Credit Agreement transaction costs (2) - - - (7,995)

Transaction costs re-classed to Discounted Operations (5,396)

Equity-settled shared-based compensation 293 231 383 434

Amortization of debt issuance costs - - 653 990

Severance 25 182 454 843

Adjusted Expenses (1) 4,086 1,998 6,718 6,284

Cash-settled share-based compensation 1,084 (192) 3,562 156

(1) See first page of this report.

(2) debt issuance costs incurred during 2015 relating to the 2015 Amended Credit Agreements were accounted for as a deduction of long-term debt on the balance sheet at December 31, 2015.

However, these costs were expensed throughout the year but reclassified entirely during the 2015 fourth quarter when the agreements were finalized.

(3) transaction costs incurred during 2015 relating to the sale of Trican’s Russian Operations were accounted for as part of the calculation of the gain on disposal of the Russian Operations as at

December 31, 2015. As a result, costs that had been expensed in prior quarters were reclassified as the sale occurred during the 2015 fourth quarter.

Overhead Expenses

Adjusted general and administrative costs for the 2016 fourth quarter increased $2.1 million compared to the same period last year. This increase is mainly a result of a $1.3 million increase in cash-settled share-based compensation as a result of the share price increase and a $0.4 million bad debt recovery recorded during the 2015 fourth quarter. Cash-settled share-based compensation includes restricted share units expenses, deferred share units expenses and performance share unit expenses which are correlated to the number of vested units and the change in Trican’s share price during the quarter.

During the 2016 fourth quarter, adjusted corporate expenses totaled $6.7 million which compares to the adjusted corporate expenses of $6.3 million for the same period last year. This increase is a result of a $3.7 million increase in cash-settled share-based compensation offset by significant reductions in salaries and professional fees. Adjusted operating income in Q4 2016 was 1% of revenue compared to adjusted operating income of 12% in Q4 2015.

Trican Well Service Ltd.

MD&A Years Ended December 31, 2015 & 2016 | 7

Q4 2016 versus Q3 2016

Fourth quarter revenue increased by 47% compared to the third quarter of 2016 and is consistent with the 47% increase in rig count experienced during the quarter. Activity levels and utilization of active equipment were below expectations at the start of the quarter due to wet weather and a delayed freeze up, however, it increased rapidly in mid November when freeze up occurred and remained highly utilized in the second half of the quarter as customers worked to catch up on their programs. December activity remained high as more work was performed during the Christmas break and the break was shorter than anticipated. Total job count increased 11% sequentially.

Revenue per job has increased 33% largely as a result of larger fracturing and cement jobs. Pricing during the quarter marginally increased with pricing increases for most large customers taking effect at the start of January.

Fracturing and cementing average job sizes have increased relative to the 2016 third quarter. Increases in number of stages and proppant volume per frac job are indicative of the industry trend toward more stages per well and larger sand volumes pumped per stage. These factors largely account for the increase in fracturing job size. An increase in cement tonnage pumped per cement job during the quarter accounts for the increase in the cementing job size.

As a percentage of revenue, fourth quarter materials and operating expenses were 95% compared to 98% during the third quarter of 2016 and includes the impact of a $5.5 million write-down of obsolete spare parts inventory. Materials and operating expenses as a percentage of revenue reduced to 91% from 95% excluding the write-down. This improvement was primarily due to increased equipment utilization combined with some marginal improvements to pricing. Variable and fixed costs generally remained consistent with Q3 2016 levels.

General & Admin. Corporate Expense

($ thousands; unaudited)Three months ended,

Dec. 31, 2016

Sept. 30, 2015

Dec. 31, 2016

Sept. 30, 2015

Total Expenses 4,404 3,837 8,208 4,425

Adjusted for:

Equity-settled shared-based compensation 293 285 383 385

Amortization of debt issuance costs - - 653 656

Severance 25 60 454 542

Adjusted Expenses (1) 4,086 3,492 6,718 2,842

Cash-settled share-based compensation 1,084 324 3,562 295

(1) See first page of this report.

Overhead Expenses

Adjusted general and administrative expenses increased $0.6 million sequentially from the 2016 third quarter primarily as a result of the increase in cash-settled share-based compensation expense which is highly correlated to the movement in Trican’s share price.

Adjusted corporate expenses incurred during the fourth quarter increased sequentially by $3.9 million largely due to the increase in cash-settled share-based compensation combined with insignificant increases in a handful of other corporate expenses. Removing cash-settled share-based compensation, adjusted operating income for the quarter would have been $5.8 million or 5.0% of revenue.

Operating loss as a percentage of revenue was 6% during the fourth quarter compared to an operating loss as a percentage of revenue of 9% in the third quarter of 2016. Adjusted operating income in Q4 2016 was 1% of revenue compared to an adjusted operating loss of 4% in Q3 2016. The $8.5 million difference between the Q4 2016 adjusted operating income and the Q4 2016 operating loss is largely a result of a $5.5 million write down of obsolete spare parts inventory combined with $1.6 million of severance costs, $0.7 million of amortized debt issuance costs and $0.7 million of equity-settled share-based compensation expense.

Trican Well Service Ltd.

8 | MD&A Years Ended December 31, 2015 & 2016

Discontinued Operations

Discontinued operations include the results of pressure pumping operations in the United States, Russia, Algeria, Australia, Colombia, Kazakhstan, and Saudi Arabia, which were suspended or sold throughout 2015 and 2016. Additionally, discontinued operations include the completions tools business which was sold in July 2016. The completions tools business had operations in Canada, the United States, Norway and Russia. The decisions to discontinue pressure pumping operations in the United States, Russia and other international regions, along with the completions tools business are not anticipated to have a significant effect on the continuing operations of the Company.

Discontinued operations for the fourth quarter of 2016 include revenues of nil compared to $3.9 million for the third quarter of 2016. The net loss from discontinued operations was $4.2 million in the fourth quarter of 2016, compared to net loss of $23.2 million for the three months ended September 30, 2016.

For the year ended December 31, 2016, management continued its efforts to wind up foreign operations resulting in assets being classified as held for sale. At December 31, 2016, the net carrying value of the assets and liabilities located in these regions was $5.5 million and $0.3 million respectively. The Company also had asset held for sale with a net carrying value of $3.2 million in continuing operations.

Results from discontinued operations have not been included in the tables above. For information related to Trican’s discontinued operations, please see the annual consolidated financial statements as at and for the year ended December 31, 2016.

OTHER EXPENSES AND INCOMEFinance costs for the fourth quarter of 2016 increased by 7% compared to the third quarter of 2016. This increase is mainly due to higher interest expense as a result of a higher average debt balance. This higher debt balance is due to increased working capital that results from higher level of activities.

Depreciation and amortization expense for continuing operations decreased during the fourth quarter of 2016 by 1% due to a lower average gross book value of property and equipment being depreciated.

A foreign exchange gain of $0.3 million has been recorded in the fourth quarter of 2016, compared to a loss of $0.4 million for the prior quarter. This gain is due to an unrealized gain on USD denominated marketable securities and Trican’s Profit Interest in Keane as the U.S. dollar strengthened relative to the Canadian dollar. This gain was partially offset by an unrealized loss on the unhedged portion of the USD denominated debt. The translation of the assets and liabilities of international entities that are dependent on the Canadian Operations are reported in discontinued operations.

An impairment loss of $3.1 million on the carrying amount of property and equipment was recorded in the fourth quarter as a result of classifying and measuring certain Canadian properties as assets held for sale at the lower of cost and fair value less cost of disposal.

Finance and other income of $66.5 million for the fourth quarter of 2016 includes an unrealized gain of $65.2 million on Trican’s Profit Interest in Keane and includes approximately $2.3 million relating to interest income and gains on disposal of assets.

INCOME TAXESThe Company recorded an income tax recovery, related predominantly to Canadian operations, of $21.5 million during the fourth quarter of 2016 compared to $12.3 million for third quarter of 2016. The difference in the income tax recoveries is largely due to the difference between the taxable losses incurred in the two periods by our Canadian operations. $4.3 million of the Q4 2016 expense related to losses from Canadian operations and the remaining $25.8 million of the recovery related to recognition of previously unrecognized operating losses of the U.S. entities that offset the taxable gain on the appreciation of the value of the Equity Interest in Keane.

Trican Well Service Ltd.

MD&A Years Ended December 31, 2015 & 2016 | 9

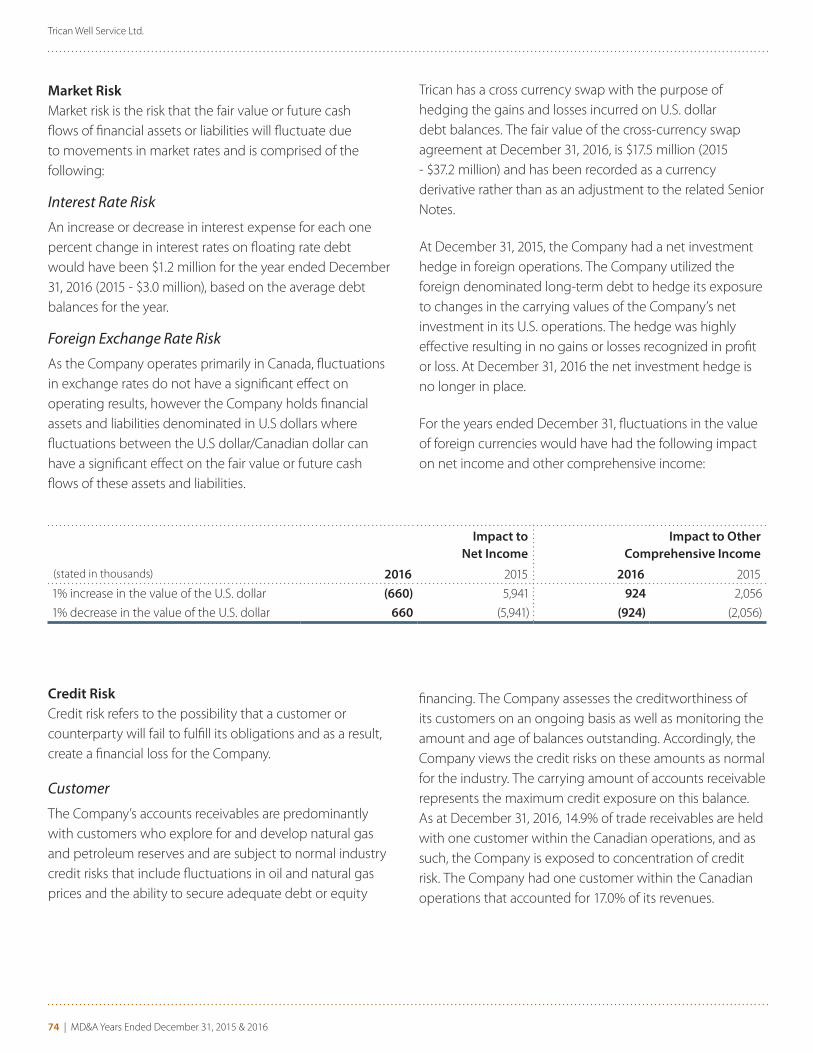

OTHER COMPREHENSIVE INCOME Other comprehensive income includes the effects of foreign currency translation (“FCTA”), the reclassification of FCTA to the income statement for entities that have been sold or substantially disposed of and the unrealized gains and losses on Trican’s Equity Interest in Keane.

The Company had total other comprehensive gain of $84.5 million during the fourth quarter of 2016, compared to a loss of $294.6 million in the fourth quarter of 2015. FCTA differences resulted in $1.1 million net movement during

the fourth quarter of 2016, compared to a gain of $16.4 million during the same period in 2015. The unrealized gain on Trican’s Equity Interest in Keane was $31.6 million in the fourth quarter of 2016 which is calculated net of a tax expense of $40.5 million. The Company obtained 10% of the Class A shares (“Equity Interest in Keane”) in Keane Group Holdings, LLC (“Keane”) on the close of the sale of its U.S. pressure pumping business. These securities were initially recognized at fair value. Subsequent changes in the fair value are recognized through other comprehensive income (OCI).

COMPARATIVE YEAR-TO-DATE INCOME STATEMENTS ($thousands, unaudited) Twelve months ended

Dec. 31, 2016

% of Revenue

Dec. 31, 2015

% of Revenue

Year- Over-

Year Change

% Change

Revenue 325,179 100% 649,735 100% (324,556) (50%)

Expenses Materials and operating 341,275 105% 592,276 91% (251,001) (42%)

General and administrative 14,909 5% 12,168 2% 2,741 23%

Operating income / (loss) - Canadian Operations (1) (31,005) (10%) 45,291 7% (76,296) (168%)

Corporate expenses 38,755 12% 29,270 5% 9,485 32%

Operating income / (loss) - Continuing Operations (1) (69,760) (21%) 16,021 2% (85,781) (535%)

Finance costs 26,016 8% 43,000 7% (16,984) (39%)

Depreciation and amortization 70,440 22% 74,725 12% (4,285) (6%)

Foreign exchange (gain) / loss 3,058 1% (20,652) (3%) 23,710 (115%)

Asset impairment 5,135 2% 4,996 1% 139 3%

Finance and other income (70,455) (22%) (2,127) (0%) (68,328) 3,212%

Loss before income taxes (103,954) (32%) (83,921) (13%) (20,033) 24%

Income tax expense / (recovery) (63,225) (19%) (21,140) 3% (42,085) 199%

Net loss - Continuing Operations (40,729) (13%) (62,781) (10%) 22,052 (35%)

Adjusted operating income / (loss) - Canadian Operations (1) (10,858) (3%) 56,085 9% (66,943) (119%)

Adjusted operating income / (loss) - Continuing Operations (1) (37,369) (11%) 34,893 5% (72,265) (207%)

Gross loss (1) (83,533) (26%) (26,744) (4%) (56,789) 212%

Job count 9,071 11,977 (2,906) (24%)

Revenue per job 35,448 54,090 (18,642) (34%)

(1) See first page of this report.

Trican Well Service Ltd.

10 | MD&A Years Ended December 31, 2015 & 2016

Canadian revenue for year ended December 31, 2016, was 50% lower than the year ended December 31, 2015. Low commodity prices over the first half of 2016 led to substantial declines in activity for the majority of our Canadian service lines throughout the year with the largest impact on our fracturing business. The average rig count in Canada has decreased approximately 50% over 2016 compared to 2015. The job count decreased 24% on a year-over-year basis and reflects weak activity during the first half of the year and increasing activity during the second half of the year. Revenue per job decreased 34% on a year-over-year basis and has largely decreased due to a significant reduction in pricing combined with a shift in sales mix towards the cementing service line partially offset by larger

fracturing jobs which is consistent with industry trends experienced during the year.

As a percentage of revenue, materials and operating expenses increased to 105% from 91% for the year ended December 31, 2016 compared to the year ended December 31, 2015. In addition, the gross loss as a percentage of revenue was 26% compared to gross loss as a percentage of revenue of 4% in 2015. The majority of these weak financial results occurred during the first half of the year as low commodity prices resulted in anemic activity levels and significantly reduced pricing for our services. Meaningful reductions in our fixed and variable cost structure partially offset the decline in revenue due to lower activity levels and weak pricing.

General & Admin. Corporate Expense

($ thousands; unaudited)Twelve months ended,

Dec. 31, 2016

Dec. 31, 2015

Dec. 31, 2016

Dec. 31, 2015

Total Expenses 14,909 12,168 38,755 29,270

Adjusted for:

Equity-settled shared-based compensation 1,110 1,475 1,699 2,761

Amortization of debt issuance costs - - 3,776 1,644

Severance 642 349 6,647 2,972

Professional fees - - 122 700

Adjusted Expenses (1) 13,157 10,344 26,511 21,193

Cash-settled share-based compensation 2,368 (1,725) 8,018 (3,381)

(1) See first page of this report.

Overhead Expenses

Adjusted general and administrative expenses increased $2.8 million year over year primarily as a result of the increase in cash-settled share-based compensation expense based on improved share performance. This increase was partially offset by a $0.5 million and $0.6 million decrease in personnel and office costs, respectively.

Adjusted corporate expenses for the twelve months ended December 31, 2016, increased by $5.3 million when compared to the same period last year mainly resulting from an $11.4 million increase in cash-settled share-based compensation partially offset by significant reductions in personnel costs, IT expenses and office costs.

OTHER EXPENSES AND INCOMEFor the twelve months ended December 31, 2016, finance costs decreased by 39% compared to the same period in 2015 due to decreased average debt balances partially offset by an increase in interest rates on the revolving facility and the outstanding notes payable.

Depreciation expense decreased by 6% due to a net decrease in average gross book value of assets by 3% for continuing operations due to disposals of equipment in Canada and due to a lower number of major component disposals recorded in accelerated depreciation.

Trican Well Service Ltd.

MD&A Years Ended December 31, 2015 & 2016 | 11

Foreign exchange losses of $3.1 million have been recorded for the twelve months ended December 31, 2016, compared to gains of $20.7 million for the same period in 2015. Foreign exchange gains recorded during 2015 related to unrealized gains on USD denominated net current asset balances due to a stronger USD relative to the Canadian dollar. The foreign exchange losses recorded in 2016 are due to a stronger Canadian dollar relative to the U.S. dollar on net USD denominated financial assets, when compared to exchange rates in 2015.

An impairment loss of $5.1 million on the carrying amount of property and equipment was recorded in 2016 as a result of measuring the Canadian division’s microseismic assets and other properties as held for sale at the lower of cost and fair value less cost of disposal.

Finance and other income in 2016 was a gain of $70.5 million compared to a gain of $2.1 million for the same period of 2015. The gain recorded in 2016 comprises of an unrealized gain of $65.2 million on Trican’s Profit Interest in Keane. Finance and other income is largely comprised of gains or losses recorded on the Profit Interest in Keane, gains or losses on asset sales and interest income on cash balances.

INCOME TAXESTrican recorded an income tax recovery of $63.2 million for the twelve months ended December 31, 2016, versus a recovery of $21.1 million for the same period in 2015. The difference in the income tax recoveries is largely due to the difference between the taxable losses incurred in the two periods by our Canadian operations. $31.8 million dollars of the recovery related to losses from Canadian operations and the remaining $31.4 million of the recovery related to recognition of previously unrecognized operating losses of the US entities that offset the taxable gain on the appreciation of the value of the Equity Interest in Keane.

OTHER COMPREHENSIVE INCOME Other comprehensive income includes the effects of FCTA, the reclassification of FCTA to the income statement for entities that have been sold or substantially disposed of and the unrealized gains and losses on Trican’s Equity Interest in Keane.

FCTA differences resulted in a gain of $1.0 million during 2016, compared to a gain of $43.1 million during the same period in 2015. In 2016, reclassification of FCTA to the income statement was $67.5 million due to the sale of the U.S. operations, the Completions operations, the Kazakh operations and the disposal of remaining operational assets in Colombia. The unrealized gain on Trican’s Equity Interest in Keane was $41.2 million for the year ended December 31 2016, which is calculated net of the tax expense of $46.1 million. The Company obtained an Equity Interest in Keane on the close of the sale of its U.S. pressure pumping business. These securities were initially recognized at fair value. Subsequent changes in the fair value are recognized through other comprehensive income.

LIQUIDITY, CAPITAL RESOURCES AND FUTURE OPERATIONSOperating Activities

Cash flow used in operating activities for continuing operations was $15.1 million during Q4 2016, compared to cash flow used by continuing operations of $8.6 million during Q4 2015. The net decrease in cash flow provided by continuing operations was largely due to the higher operating income from continuing operations during Q4 2015 as activity and operating conditions were better during the last quarter of 2015 than the comparable period in 2016.

For the twelve months ended December 31, 2016, cash flow used in total operations was $93.9 million versus cash flow used in total operations of $119.8 million for the year ended December 31, 2015. The year-over-year decrease in cash flow from continuing operations between 2015 and 2016 is the result of activity levels and operating conditions that worsened year-over-year leading to larger losses in 2016.

At December 31, 2016, Trican had working capital of $114.1 million compared to $203.1 million at the end of 2015. The decrease is largely due to the sale of the U.S. pressure pumping and the Completions operations in combination with lower levels of activity in Canada, which has led to a significant decrease in trade accounts receivable and inventory, offset partially by a decrease in trade payables. The change in working capital between the current quarter and the prior quarter was small as continuing operations have been more consistent on a quarter over quarter basis.

Trican Well Service Ltd.

12 | MD&A Years Ended December 31, 2015 & 2016

Trican anticipates that cash flow from operating activities and available credit facilities will provide the required resources to fund ongoing operating, investing and financing activities for the foreseeable future including the discharge of its existing liabilities and commitments and compliance with future financial covenants as specified in the amended terms of the applicable credit agreements (“Second 2016 Amended Credit Agreements”) with its bank lenders under its revolving credit facility (“RCF”) and the holders of its senior notes (“Senior Notes”).

For the fiscal years ended December 31, 2016 and December 31, 2015, the Company incurred net losses of $29.3 million and $829.9 million, respectively. Although current economic climate has improved in the last six months, a negative change in the economy could lead to adverse changes in cash flow, working capital levels or long-term debt balances, which may also have a direct impact on our results and financial position.

Based on currently available information, we expect to comply with all covenants during 2017, however our estimated leverage and interest coverage ratios in the Second 2016 Amended Credit Agreements during the first half of 2017 are expected to be near the minimum amounts necessary to comply with the financial covenants. If the Company does not comply with the financial covenants, the RCF and Senior Notes may become due on demand. If future profitability or available liquidity is not sufficient to meet Trican’s operating and debt servicing obligations as they come due, management’s plans include reducing expenditures and pursuing additional asset dispositions or alternative financing arrangements.

Subsequent to year end, Trican sold its NOV shares and monetized a portion of its Investments in Keane for net proceeds of approximately USD $20.7 million and USD $28.4 million, respectively, and used the proceeds to pay down debt.

Investing ActivitiesOn March 16, 2016, Trican closed the sale of its United States pressure pumping business to Keane Group Holdings, LLC, a privately-held U.S.-based well completion services company. The transaction involved the sale of all pressure

pumping and select related assets, and the assumption of certain liabilities, of Trican Well Service, L.P., Trican's wholly-owned subsidiary, for cash proceeds of USD$200 million, or approximately $265 million, with working capital adjustments providing Trican with an additional $4.9 million in proceeds. Trican applied the net cash proceeds from this transaction to reduce its outstanding debt. As part of this transaction, Trican has also received 10% of the Class A shares of Keane (the Equity Interest in Keane) as well as certain economic interests in Keane that represent up to an additional 20% economic participation above certain thresholds upon a Keane liquidity event (the Profits Interest in Keane).

In January 2017, Trican monetized a portion of its Investments in Keane for net proceeds of approximately USD $28.4 million and used the proceeds to further pay down debt.

On July 13, 2016, Trican closed its agreement with certain subsidiaries of NOV for the sale of its completion tools business with operations in Russia, Norway, the United States and Canada for aggregate gross proceeds of $53.5 million. The cash consideration received on closing by Trican consisted of $30 million adjusted for working capital estimates of $1.3 million with the final working capital adjustment of $7.2 million finalized during the first quarter of 2017. The share consideration received on closing consisted of 558,221 NOV shares. As at December 31, 2016, the fair value of the shares was $28.1 million. In January 2017, Trican sold its NOV shares for net proceeds of approximately USD $20.7 million and has used the proceeds to further pay down debt.

Capital expenditures related to continuing operations for the year ended December 31, 2016 totaled $1.4 million, compared with $17.1 million for the year ended December 31, 2015. Proceeds from the sale of Property and Equipment totalled $8.4 million during the year ended December 31, 2016, compared with proceeds of $8.9 million for the year ended December 31, 2015. With the decline in commodity prices and North American demand for pressure pumping services, capital expenditures will be kept to a minimum until operating conditions improve. A substantial amount of equipment has been parked in Canada, which will reduce the amount of maintenance capital needed throughout

Trican Well Service Ltd.

MD&A Years Ended December 31, 2015 & 2016 | 13

the current downturn. We expect to continue to minimize capital spending during 2017 with this spending expected to be funded primarily through cash flow from operations and our Revolving Credit Facility. Trican regularly reviews its capital equipment requirements and will continue to follow its policy of adjusting the capital budget on a quarterly basis to reflect changing operating conditions and capital equipment needs.

Financing Activities

2016 Amended Credit Agreements

On March 16, 2016 Trican closed the sale of the U.S. pressure pumping business to Keane. Concurrently the amended terms of the 2016 credit agreements (the “2016 Amended Credit Agreements”) between Trican, its lenders and Senior Noteholders came into effect including:

� an elimination of the minimum EBITDA and liquidity covenants;

� a Cure Amount provision for which 50% of the equity proceeds may be applied in the calculation of adjusted EBITDA for the Leverage and Interest coverage covenant calculations, provided a Cure Amount is not used more than twice in any four quarter period and the aggregate amount of any Cure Amount applied to the quarterly covenant calculations does not exceed $20 million; and;

� Adjusted EBITDA was defined as income before interest, taxes, depreciation and other permitted or non-cash items under the 2016 Amended Credit Agreements.

Second 2016 Amended Credit Agreements

On June 21, 2016, Trican closed a public offering of an aggregate of 43,125,000 common shares at a price of $1.60 per common share for aggregate gross proceeds of $69 million including overallotments (the “Equity Offering”). Concurrently, “Second 2016 Amended Credit Agreements” with its bank lenders under its revolving credit facility (“RCF”) and the holders of its senior notes came into effect which did not change key terms of the 2016 Amended Credit Agreements other than as described below.

Key terms include:

� a reduction in the availability of the RCF from $303 million to $250 million;

� a temporary cap of $175 million on the RCF until Trican has achieved EBITDA (excluding the application of any Cure Amount as defined in the RCF agreement) of at least $25 million in any quarter ended on or after September 30, 2016. The temporary cap remains in place at December 31, 2016;

� a removal of all prior financial covenants until the first quarter of 2017; and,

� new leverage and interest covenant calculations as described below – the covenant thresholds remain unchanged.

Trican Well Service Ltd.

14 | MD&A Years Ended December 31, 2015 & 2016

Senior Notes

Trican had the following notes outstanding:

During 2016, Trican used a portion of the proceeds from the sale of the U.S pressure pumping business, the sale of the completion tools business, and the equity offering to retire in advance Senior Note amounts of USD $130.6 million and $34.3 million. During the second quarter of 2016, Trican fully retired its Senior Notes Series C ($17.3 million) and Series E (USD $25.1 million) on maturity.

Revolving Credit Facility

As at December 31, 2016, Trican has a $250 million (2015 - $410 million) extendible revolving credit facility (“RCF”) with a syndicate of banks that is committed until October 31, 2018. Availability under the RCF is currently capped at $175 million as mentioned above. The RCF is secured and

Canadian $ Amount U.S. $ Denominated Amount(stated in thousands) Maturity Dec. 31, 2016 Dec. 31, 2015 Dec. 31, 2016 Dec. 31, 2015Senior Notes

7.05% (1) Series A November 19, 2017 $8,859 $23,067 $6,598 $16,667

7.05% (1) Series A November 19, 2019 - 5,297 - 3,828

8.22% (1) Series C April 28, 2016 - 33,445 - -

9.11% (1) Series D April 28, 2021 3,368 11,148 - -

7.61% (1)Series E April 28, 2016 - 66,860 - 48,309

8.29% (1)Series F April 28, 2018 25,713 82,289 19,150 59,457

8.90% (1) Series G April 28, 2021 33,448 108,005 24,911 78,038

8.75% (1) Series H September 03, 2024 4,456 14,864 - -

Subordinated Make-Whole Senior Notes

5.96% Series A November 19, 2017 686 703 511 508

5.54% Series D April 28, 2021 458 457 - -

5.55% Series F April 28, 2018 1,224 1,268 912 916

6.28% Series G April 28, 2021 3,317 3,395 2,470 2,453

6.05% Series H September 03, 2024 760 755 - -

PIK Principal 2,075 - - -

Debt issue costs (2) (3,110) (4,977) - -

Senior Notes, net of debt issue costs $81,254 $346,576 $54,552 $210,176

(1) (The interest rate on Senior Notes includes an additional 125 basis point increase payable in cash and a 175 basis point increase of interest payable in kind pursuant to the 2016 and 2015 Amended Credit Agreements.

(2) Includes transaction costs on the 2016 and 2015 Amended Credit Agreements and Original Credit Agreements.

bears interest at the applicable Canadian prime rate, U.S. prime rate, Banker’s Acceptance rate, or at LIBOR, plus 350 to 625 basis points (2015 – Canadian prime rate, U.S. prime rate, Banker’s Acceptance rate, or at LIBOR, plus 350 to 625 basis points), dependent on certain financial ratios of the Company. The undrawn amount of the RCF is $110.0 million of which only $35 million is accessible as at December 31, 2016 (2015 - $214.8 million).

As at December 31, 2016, Trican has a $10 million (2015 - $10 million) Letter of Credit facility with its syndicate of banks. As at December 31, 2016, Trican had $5.1 million in letters of credit outstanding (2015 - $5.2 million).

Trican Well Service Ltd.

MD&A Years Ended December 31, 2015 & 2016 | 15

Covenants

The Company is required to comply with certain covenants under the terms of the Second 2016 Amended Credit Agreements. These covenants are applicable to the RCF and to the Senior Notes:

� no financial covenants are applicable until the first quarter of 2017;

� Trican is required to comply with the following leverage and interest coverage ratio covenants:

For the Quarter Ended Leverage Ratio Interest Coverage Ratio Calculation Basis

December 31, 2016 Not applicable Not applicable Not applicable

March 31, 2017 <5.0x >2.0x Q1 annualized

June 30, 2017 <5.0x >2.0x (Q1 X 3 + Q2)

September 30, 2017 <5.0x >2.0x ((Q1 + Q3) x 3/2) + Q2

December 31, 2017 <4.0x >2.5x Last twelve months

Thereafter <3.0x >3.0x Last twelve months

The leverage ratio is defined as long-term debt excluding Subordinated Make Whole Notes (net of the mark to market value of the cross-currency swaps) minus cash divided by adjusted EBITDA. The interest coverage ratio is defined as adjusted EBITDA divided by interest expense minus payable in-kind interest. Certain expenses such as severance and equity-settled share-based compensation expenses are permitted to be added back to EBITDA to arrive at adjusted EBITDA for covenant calculation purposes. As noted above, no financial covenants are applicable to the Company for the fourth quarter of 2016. However, for illustrative purposes, adjusted EBITDA for covenant calculation purposes for the fourth quarter of 2016 would have been a gain of $2.8 million. This amount is calculated by taking adjusted consolidated operating income of $1.1 million and adding finance and other income of $1.7 million. These amounts do

not include the $20 million equity cure that may be applied to this calculation.

Share Capital

As at February 21, 2017, Trican had 193,617,699 common shares and 8,674,996 employee stock options outstanding.

Other Commitments and Contingencies

Management is satisfied that the Company has sufficient liquidity and capital resources to meet the Company’s future obligations and commitments. The Company has commitments for operating lease agreements, primarily for office space, with minimum payments due as of December 31, 2016, and capital commitments, primarily related to major equipment as follows.

Trican Well Service Ltd.

16 | MD&A Years Ended December 31, 2015 & 2016

Sand Purchase Agreement with Huron Mineral LLC

On November 2, 2016, Trican Well Service L.P. reached an agreement with Huron Minerals LLC to settle its dispute related to a sand purchase agreement. The Company recorded a provision of $8.3 million during 2016 as the parties agreed to settle this claim for USD $6.35 million. The Company will pay USD $4.0 million on January 5, 2017 and USD $2.35 million on April 3, 2017.

Indemnity Claim in connection with the sale of Trican’s US operations to Keane Group (“Keane”) on March 16, 2016

During Q2 2016, Keane delivered an Indemnity Claim stating that Trican owes Keane $3.9 million (USD $3.0 million) due to losses incurred by Keane for assets purchased that were not in good operating condition. Management has not recorded any accrual for this contingent liability associated with this claim based on our belief that a liability is not more likely than not and any range of potential future charge cannot be reasonably estimated at this time.

Other Litigation

On August 25, 2015, a class action lawsuit was filed on behalf of 31 plaintiffs against Trican Well Service, L.P. The claim alleges that Trican misclassified the plaintiffs’ position as “exempt” from overtime wages from February 2011 to August 2015, resulting in a loss of overtime wages during this period. Given the information available at these early stages of litigation, management has not recorded any accrual for this contingent liability associated with this claim based on our belief that a liability is not probable and any range of potential future charge cannot be reasonably estimated at this time.

The tax regulations and legislation in the various jurisdictions that the Company operates in are continually changing. As a result, there are usually some tax matters under review. Management believes that it has adequately met and provided for taxes based on the Company’s interpretation of the relevant tax legislation and regulations.

Payments Due by Period

December 31, 2016 1 year or less 1 to 5 years 5 years & thereafter Total

Trade and other payables $87,239 $- $- $87,239Senior Notes (including interest) 14,697 80,493 5,961 101,151RCF (including interest) 10,348 154,020 - 164,368Finance leases 717 264 - 981Operating leases 4,641 9,838 8,324 22,803Total commitments $107,294 $244,615 $14,285 $376,542

December 31, 2015

Trade and other payables $141,212 $- $- $141,212

Senior Notes (including interest) 106,202 269,382 20,103 395,687

RCF (including interest) 29,798 215,873 - 245,671

Finance leases 7,296 13,759 - 21,055

Operating leases 14,159 19,639 5,783 39,581

Inventory purchases 3,019 36,998 - 40,018

Capital commitments 5,559 - - 5,559

Total commitments $307,245 $555,651 $25,886 $888,782

Management is satisfied that the Company has sufficient liquidity and capital resources to meet the Company’s obligations and commitments.

Contractual Obligations

Trican Well Service Ltd.

MD&A Years Ended December 31, 2015 & 2016 | 17

Immaterial Corrections

Subsequent to the issuance of the consolidated financial statements for the year ended December 31, 2015, the Company determined that two immaterial errors occurred in those previously issued financial statements:

� In the fourth quarter of 2015, hedged transactions in a cash flow hedging relationship (being foreign exchange gains and losses on the Company’s Series E and Series F Senior Notes) were no longer probable of occurring based on expectations of disposals being pursued by the Company. As a result, the hedging relationship no longer qualified for hedge accounting and, accordingly, in the fourth quarter of 2015, the cumulative loss of $3.9 million previously recognized in other comprehensive income should have been reclassified to reduce foreign exchange gain and increase loss from continuing operations by the same amount; and

� In the third quarter of 2015, the Company determined that cumulative foreign exchange loss of $1.4 million previously recognized in other comprehensive income should have been reclassified to loss from discontinued operations as a result of the sale of its Russian operation.

The Company concluded that these adjustments are not material to the Company’s consolidated financial statements for the year ended December 31, 2015 and has reflected them as immaterial corrections of the comparative financial information in these annual consolidated financial statements.

Deficit at December 31, 2015 has been increased by $5.3 million.

In addition, the Company has presented the carrying amount of the cross currency swaps of $37.2 million at December 31,

2015 as currency derivatives rather than as an adjustment to the related Senior Notes. Changes in fair value of the cross currency swaps commencing the fourth quarter of 2015 have been recognized in profit and loss.

INVESTMENTS IN KEANEOn March 16, 2016, Trican sold its U.S. pressure pumping operations to Keane Group Holdings, LLC (“Keane Private Company”) for USD $200 million in cash, 10% and 100% of class A and C shares, respectively, in the Keane Private Company. At the time of the sale, Keane Private Company and its subsidiaries performed pressure pumping services for oil and gas companies in the onshore U.S. market.

On January 20, 2017, Keane Group, Inc. (“FRAC”) completed its initial public offering (“IPO”) and its shares became publicly traded on the New York Stock Exchange under the ticker symbol “FRAC”. As a result of the IPO, Trican’s ownership interests in the Keane Private Company have been transferred to Keane Investor Holdings, LLC (“Keane Holding Company”). Effectively, our Class A common shares and Class C profits interest in Keane Private Company are now Class A common shares and Class C profits interests in the Keane Holding Company. At the time of IPO, the Keane Holding Company’s only asset was 87.4 million shares of FRAC and it had no liabilities. Trican’s Investments in Keane have been reorganized as a result of the IPO, but the waterfall calculation used to calculate the cash received by Trican on future liquidity events has not changed.

Future liquidity events will effectively be the future sale of the remaining shares of FRAC currently held by the Keane Holding Company. The proceeds from the future sales will be distributed to the owners of Keane Holding Company. Trican’s portion of the future liquidity events will be calculated based on the following waterfall table:

Liquidity Event Cumulative Proceeds Thresholds (USD $MM)For the Year Ending March 15

Tranche Trican Ownership Interest 2017 2018 2019 2020 2021

First 10% up to $468 $468 $468 $468 $468

Second 9.2% between $468 - 608 $468 - 791 $468 - 1,028 $468 - 1,336 $468 - 1,737

Third 18.3% between $608 - 632 $791 - 853 $1,028 - 1,151 $1,336 - 1,554 $1,737 - 2,098

Fourth 27.4% greater than $632 $853 $1,151 $1,554 $2,098

Trican Well Service Ltd.

18 | MD&A Years Ended December 31, 2015 & 2016

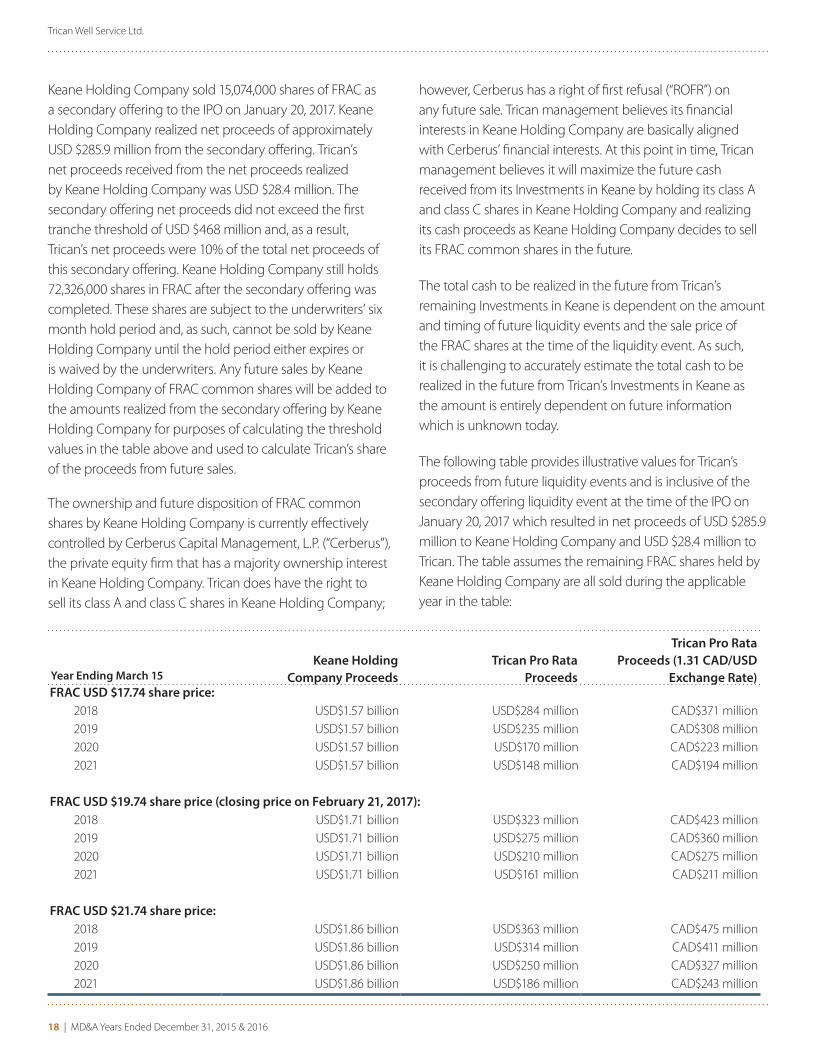

Keane Holding Company sold 15,074,000 shares of FRAC as a secondary offering to the IPO on January 20, 2017. Keane Holding Company realized net proceeds of approximately USD $285.9 million from the secondary offering. Trican’s net proceeds received from the net proceeds realized by Keane Holding Company was USD $28.4 million. The secondary offering net proceeds did not exceed the first tranche threshold of USD $468 million and, as a result, Trican’s net proceeds were 10% of the total net proceeds of this secondary offering. Keane Holding Company still holds 72,326,000 shares in FRAC after the secondary offering was completed. These shares are subject to the underwriters’ six month hold period and, as such, cannot be sold by Keane Holding Company until the hold period either expires or is waived by the underwriters. Any future sales by Keane Holding Company of FRAC common shares will be added to the amounts realized from the secondary offering by Keane Holding Company for purposes of calculating the threshold values in the table above and used to calculate Trican’s share of the proceeds from future sales.

The ownership and future disposition of FRAC common shares by Keane Holding Company is currently effectively controlled by Cerberus Capital Management, L.P. (“Cerberus”), the private equity firm that has a majority ownership interest in Keane Holding Company. Trican does have the right to sell its class A and class C shares in Keane Holding Company;

however, Cerberus has a right of first refusal (“ROFR”) on any future sale. Trican management believes its financial interests in Keane Holding Company are basically aligned with Cerberus’ financial interests. At this point in time, Trican management believes it will maximize the future cash received from its Investments in Keane by holding its class A and class C shares in Keane Holding Company and realizing its cash proceeds as Keane Holding Company decides to sell its FRAC common shares in the future.

The total cash to be realized in the future from Trican’s remaining Investments in Keane is dependent on the amount and timing of future liquidity events and the sale price of the FRAC shares at the time of the liquidity event. As such, it is challenging to accurately estimate the total cash to be realized in the future from Trican’s Investments in Keane as the amount is entirely dependent on future information which is unknown today.

The following table provides illustrative values for Trican’s proceeds from future liquidity events and is inclusive of the secondary offering liquidity event at the time of the IPO on January 20, 2017 which resulted in net proceeds of USD $285.9 million to Keane Holding Company and USD $28.4 million to Trican. The table assumes the remaining FRAC shares held by Keane Holding Company are all sold during the applicable year in the table:

Year Ending March 15Keane Holding

Company ProceedsTrican Pro Rata

Proceeds

Trican Pro Rata Proceeds (1.31 CAD/USD

Exchange Rate)FRAC USD $17.74 share price:

2018 USD$1.57 billion USD$284 million CAD$371 million2019 USD$1.57 billion USD$235 million CAD$308 million2020 USD$1.57 billion USD$170 million CAD$223 million2021 USD$1.57 billion USD$148 million CAD$194 million

FRAC USD $19.74 share price (closing price on February 21, 2017):2018 USD$1.71 billion USD$323 million CAD$423 million2019 USD$1.71 billion USD$275 million CAD$360 million2020 USD$1.71 billion USD$210 million CAD$275 million2021 USD$1.71 billion USD$161 million CAD$211 million

FRAC USD $21.74 share price:2018 USD$1.86 billion USD$363 million CAD$475 million2019 USD$1.86 billion USD$314 million CAD$411 million2020 USD$1.86 billion USD$250 million CAD$327 million2021 USD$1.86 billion USD$186 million CAD$243 million

Trican Well Service Ltd.

MD&A Years Ended December 31, 2015 & 2016 | 19

OUTLOOKDemand for our services steadily increased from the 2016 third quarter into the 2016 fourth quarter. This trend has intensified at the start of the 2017 first quarter with activity significantly picking up during the first week of January and continuing to the date of this report. All our active pressure pumping equipment is expected to be at or near full utilization until spring break-up in March. We activated one 12-hour 30,000 HP fracturing crew midway through the first quarter and will work to convert this to a twenty-four hour crew as we hire additional people. We also activated six cementing crews in the latter part of Q4 and early in Q1. Cementing demand remains very high at the start of 2017 and we anticipate it will remain high throughout the year based on current commodity prices. First quarter financial results are expected to reflect a meaningful increase in activity. The timing of break-up in March remains the only question regarding total activity levels expected during the quarter.

The high level of demand being experienced during the 2017 first quarter has resulted in some customers increasing their work programs during the second quarter. As a result, we expect second quarter activity levels to be considerably higher on a year-over-year basis. The second quarter work was priced at a discount relative to first quarter pricing; however, the incremental revenue from the increased workload is expected to cover a meaningful portion of our fixed cost structure which should allow us to improve our second quarter financial results and maintain our headcount in anticipation of activity picking up coming out of Spring break-up.

The increased activity levels and equipment utilization during the 2016 fourth quarter resulted in a pressure pumping market that became meaningfully undersupplied with manned equipment. These conditions allowed management to increase pricing by approximately 10% by the beginning of the 2017 first quarter. While the activity and pricing increases obtained to date have improved Trican’s EBITDA from negative to positive territory, management believes additional pricing increases are necessary to allow the company to continue to increase its margins to acceptable levels that allow us to run a sustainable business.

The increased activity currently being experienced is a positive indicator that additional pricing increases may be obtained as we emerge from the second quarter activity slowdown due to spring break-up conditions. However, the increased activity levels are resulting in inflationary pressures relating to personnel, proppant, chemicals and third-party hauling costs. If demand continues to increase, we expect the undersupply conditions currently being experienced to persist into the second half of 2017. Difficulties activating parked equipment are expected due to challenges in hiring qualified personnel. We will continue to push for increased pricing from our customers assuming the undersupply conditions persist.

Trican has retired 18,000 HP of fracturing capacity. This HP was older pre-2003 light duty equipment and was sold into the US market. This leaves the Company with approximately 250,000 HP active today and 172,000 HP parked. Parked HP remains in good shape and can be reactivated as activity increases. We continue to run approximately 50% of our cement, coil and other pressure pumping equipment.

Estimates regarding re-activating parked equipment are not possible at this time. Meaningful discussions with our customers regarding expected work programs during the 2017 second half have yet to occur. Management anticipates demand for our services to continue to increase during 2017 assuming oil and gas prices remain constructive. We anticipate making decisions during April regarding equipment re-activation for the second half of the year based on committed customer work programs and our ability to attract and hire qualified personnel to man the equipment.

Keane IPO

On January 20, 2017, FRAC completed its initial public offering (“IPO”) and its shares became publicly traded on the New York Stock Exchange. Trican received net proceeds of approximately USD $28.4 million from the secondary offering of the IPO. At a USD $19.00 IPO share price, Keane received a strong valuation for its business and its shares have traded positively increasing approximately 4% since the IPO. As a result, the value of Trican’s Investments in Keane has significantly increased. Trican’s ownership interest is subject to a six month hold period after the IPO and the timing of further liquidity events are impossible to predict at this time.

Trican Well Service Ltd.

20 | MD&A Years Ended December 31, 2015 & 2016

NEW ACCOUNTING STANDARDS AND INTERPRETATIONS NOT YET ADOPTED

A number of new standards and amendments to standards and interpretations are not yet effective for the year ended December 31, 2016, and have not been applied in preparing these consolidated financial statements.

In July, 2014 the IASB issued the complete IFRS 9, Financial Instruments, (IFRS 9 (2014)). Under the new standard financial assets are classified and measured based on the business model in which they are held and the characteristics of their contractual cash flows. It also amends the impairment model by introducing a new ‘expected credit loss’ model for calculating impairment. Further, IFRS 9 (2014) includes a new general hedge standard that is better aligned with companies’ risk management, expands the scope of the hedging strategies, and introduces more judgement to assess the effectiveness of the hedge relationship. The amendments to IFRS 9 (2014) are effective for annual periods beginning or after January 1, 2018, and are available for early adoption. The Company expects IFRS 9 will impact the Company’s current policies and procedures regarding provisions on trade receivables. Trade receivables are recorded at its original invoice less any amounts estimated to be uncollectable. Under IFRS 9, the expected loss impairment model replaces the current incurred loss model and is based on forward looking approach which includes earlier recognition of losses. Given the short-term nature of these receivables, the Company does not anticipate these changes to have a material financial impact. IFRS 9 also contains a new model to be used for hedge accounting. The Company does not currently apply hedge accounting.

IFRS 15, Revenue from Contracts with Customers, was issued on May 28, 2014. The Standard contains a single model that applies to contracts with customers and two approaches to recognising revenue: at a point in time or over time. The model features a contract-based five-step analysis of transactions to determine whether, how much and when revenue is recognized. New estimates and judgmental thresholds have been introduced, which may affect the amount and/or timing of revenue recognized. The Standard replaces IAS 11, Construction Contracts, IAS 18, Revenue, IFRIC 13, Customer Loyalty Programmes, IFRIC

15, Agreements for the Construction of Real Estate, IFRIC 18, Transfer of Assets from Customers, and SIC 31, Revenue – Barter Transactions Involving Advertising Services. The new standard is effective for annual periods beginning on or after January 1, 2018. Early adoption is also permitted. The Company is currently in the process of reviewing its revenue streams to determine the impact, if any, that the adoption of IFRS 15 will have on its financial statements, as well as the impact that adoption of the standard will have on disclosure.

IASB issued IFRS 16, Leases, in January 2016. The new standard replaces IAS 17, Leases. It is in effect for accounting periods beginning on or after January 1, 2019. Early adoption is permitted only if the Company has adopted IFRS 15, Revenue from Contracts with Customers. Under the new standard, more leases will come on-balance sheet for lessees, with the exception of leases with a term not greater than 12 months and “small value” leases. Lease accounting for lessors remains substantially the same as existing guidance. In 2017, the Company will complete an assessment documenting the potential impacts of IFRS 16 on its consolidated financial statements.

The Company’s initial assessments on the IFRS 9, IFRS 15, and IFRS 16 are based on work completed to date and may be subject to change as the assessments continue.

CRITICAL ACCOUNTING ESTIMATES AND JUDGEMENTSThe preparation of these consolidated financial statements in accordance with IFRS requires management to make judgments and estimates that could materially affect the amounts recognized in the financial statements. By their nature, judgments and estimates may change in light of new facts and circumstances in the internal and external environment. The following judgments and estimates are those deemed by management to be material to the Company’s consolidated financial statements.

Judgments

Depreciation and AmortizationDepreciation and amortization methods are based on management’s judgment of the most appropriate method to reflect the pattern of an asset’s future economic benefit

Trican Well Service Ltd.

MD&A Years Ended December 31, 2015 & 2016 | 21

expected to be consumed by the Company. Among other factors, these judgments are based on industry standards and company-specific history and experience.

Impairment

Assessment of impairment indicators is based on management’s judgment of whether there are internal and external factors that would indicate that a non-financial asset is impaired. The determination of a cash generating unit is also based on management’s judgment and is an assessment of the smallest group of assets that generate cash inflows independently of other assets.

Estimates

Investments in Keane The Company uses a discounted cash flow model to determine the fair value of the Investments in Keane. Inputs to the model are subject to various estimates relating to the timing and size of liquidity events, the price at which shares are sold, the discount rate and volatility of the share price. Fair value inputs are subject to market factors as well as internal estimates. The Company uses a waterfall table to calculate estimated proceeds in accordance with the operating agreement between Trican Well Service Ltd. and Keane Holding Company.

Assets Held for Sale Assets held for sale contains estimates that the property and equipment classified in this category meet the criteria as “assets held for sale”. As at the end of the reporting period these assets are recorded at the lower of cost or fair value less cost to sell.

Allowance for Doubtful Accounts An allowance for doubtful accounts is recorded when there is objective evidence that the collection of the full amount is no longer probable under the terms of the original invoice. Impaired receivables are derecognized when they are assessed as uncollectible. Amounts estimated represent management’s best estimate of probability of collection of amounts from customers.

Impairment of Inventories The Company regularly reviews the nature and quantities of inventory on hand and evaluates the net realizable value of items based on historical usage patterns, known changes to

equipment or processes and customer demand for specific products. Significant or unanticipated changes in business conditions could impact the magnitude and timing of impairment recognized.

Depreciation and Amortization

Depreciation and amortization are calculated to write off the cost, less estimated residual value, of assets on a systematic and rational basis over their expected useful lives. Estimates of residual value and useful lives are based on data and information from various sources including industry practice and historic experience. Expected useful lives and residual values are reviewed annually for any change to estimates and assumptions. Although management believes the estimated useful lives of the Company’s property and equipment are reasonable, it is possible that changes in estimates could occur, which may affect the expected useful lives and salvage values of the property and equipment.

Income taxes

Deferred tax assets and liabilities contain estimates about the nature and timing of future permanent and temporary differences as well as the future tax rates that will apply to those differences. Changes in Canadian and foreign tax laws and rates as well as changes to the expected timing of reversals may have a significant impact on the amounts recorded for deferred tax assets and liabilities. Management closely monitors current and potential changes to Canadian and foreign tax law and bases its estimates on the best available information at each reporting date.

Fair Value of Equity-Settled Share-Based Payments

The Company uses an option pricing model to determine the fair value of equity-settled share-based payments. Inputs to the model are subject to various estimates relating to volatility, interest rates, dividend yields and expected life of the units issued. Fair value inputs are subject to market factors as well as internal estimates. The Company considers historic trends together with any new information to determine the best estimate of fair value at the date of grant.

Impairment of Non-Financial Assets

In determining the recoverable amount of assets subject to impairment testing, the Company measures the recoverable amount of non-financial assets as the higher of a fair value less costs of disposal and its value in use. Recoverable

Trican Well Service Ltd.

22 | MD&A Years Ended December 31, 2015 & 2016

amounts of the non-financial assets are evaluated and calculated using various factors and assumptions. The factors and assumptions used in the estimates are assessed for reasonableness based on the information available at the time the estimates are prepared. As circumstances change and new information becomes available, the estimates could change.

BUSINESS RISKS

Our business is subject to a number of risks and uncertainties, some of which are summarized below. We encourage you to review and carefully consider the risks described below, as well as those described elsewhere in this report and in our other publicly disclosed reports and materials. If any such risks were to materialize, our business, financial condition, results of operations, cash flows or prospects could be materially adversely affected. In turn, this could have a material adverse effect on the trading price of our securities. Additional risks and uncertainties not currently known to us or that we currently deem immaterial may also adversely affect our business and operations.

Demand for Trican’s Services is Dependent Upon the Price of Oil and Natural Gas and Oilfield Services Industry Conditions, which can be Volatile

The demand, pricing and terms for Trican's services depend significantly upon the level of expenditures made by oil and gas companies on exploration, development and production activities. Expenditures by oil and gas companies are typically directly related to the demand for, and price of, oil and gas. Generally, when commodity prices and demand are predicted to be, or are relatively high, demand for Trican's services is high. The converse is also true.

The prices for crude oil and gas have fluctuated widely during recent years and may continue to be volatile in the future. Crude oil prices have decreased significantly since mid-2014 and have fluctuated in response to a variety of factors beyond Trican's control, including: global energy supply, production and policies, including the ability of the Organization of Petroleum Exporting Countries ("OPEC") to set and maintain production levels in order to influence prices for oil; oil and gas production

by non-OPEC countries; the level of consumer demand; political conditions, including the risk of hostilities in the Middle East and global terrorism; global and domestic economic conditions, including currency fluctuations; cost of exporting, producing and delivering oil and gas; technological advances affecting energy consumption; weather conditions; the effect of world-wide energy conservation and greenhouse gas reduction measures and the price and availability of alternative energy sources; and government regulations.

In addition to current and future oil and gas prices, the level of expenditures made by oil and gas companies are influenced by numerous factors over which the Company has no control, including but not limited to: general economic conditions; the cost of exploring for, producing and delivering oil and gas; the discovery rates of new oil and gas reserves; cost and availability of drilling equipment; availability of pipeline and other oil and gas transportation capacity; North American natural gas storage levels; taxation and royalty changes; government regulation; environmental regulation; ability of oil and gas companies to obtain credit, equity capital or debt financing; and currency fluctuations in the jurisdiction where we operate. A decline in expenditures by oil and gas companies caused by a decrease in crude oil prices and/or natural gas prices or otherwise, could have a material adverse effect on Trican's business, financial condition, results of operations and cash flows.

Trican’s May Exceed its Debt Covenants Under the Credit Agreements and May Not be Successful in Negotiating Covenant Relief with its Lenders

Trican is required to comply with certain covenants under the Credit Agreements, which were amended as of November 12, 2015, and January 26, 2016, with the most recent amendments having become effective June 21, 2016 upon closing of an equity offering.

Trican is required to comply with the covenants under the Credit Agreements, which, among others, include leverage ratios and interest coverage covenants, which from time to time either affect the availability or price of additional funding and, in the event that the Company does not comply with these covenants, restrict the Company's access to capital or require a repayment. In addition, if the Company's financial performance results in a breach of

Trican Well Service Ltd.

MD&A Years Ended December 31, 2015 & 2016 | 23

any future financial covenants, access to financing could be restricted and/or all or a portion of the Company's debt could become due on demand. Events beyond the Company's control may contribute to the failure of the Company to comply with such covenants. Even if the Company is able to obtain new financing, it may not be on commercially reasonable terms or terms that are acceptable to the Company. If the Company is unable to negotiate further covenant relief and is required to repay amounts owing under the Bank Facility or the Senior Notes, the lenders thereunder could proceed to foreclose or otherwise realize upon our assets. The acceleration of the Company's indebtedness under one agreement permits acceleration of indebtedness under other agreements that contain cross default or cross-acceleration provisions.

In addition, the Credit Agreements impose operating and financial restrictions on the Company, including restrictions on payment of dividends, repurchase or making of other distributions with respect to the Company's securities, incurring of additional indebtedness, the provision of guarantees, the assumption of loans, making of capital expenditures, entering into of amalgamations, mergers, take-over bids or disposition of assets, among others.

Trican Would be Adversely Affected Should Access to a Credit Facility or Additional Financing be Unavailable to Trican or its Customers

Trican's ability to maintain and potentially expand its current operations is subject to the availability of additional financing that may not be available, or may not be available on terms acceptable to Trican. Trican's current and future activities may also be financed partially or wholly with debt, which may increase its debt levels above industry standards. The level of Trican's indebtedness from time to time could impair its ability to obtain additional financing on a timely basis to take advantage of business opportunities that may arise. If the Company's cash flow from operations is not sufficient to fund its capital expenditure requirements, there can be no assurance that additional debt or equity financing will be available to meet these requirements or, if available, on acceptable terms.

In addition, many of our customers access the credit and financial markets to finance their oil and natural gas drilling activity. If the availability of credit to our customers is

reduced, they may reduce their drilling and production expenditures, thereby decreasing demand for our products and services. Any such reduction in spending by our customers could adversely impact our operating results and financial condition.

The Oilfield Services Industry is Highly Competitive

We compete with multinational, national and regional competitors in each of our current service lines. Certain of our competitors may have financial, technical, manufacturing and marketing advantages and may be in a stronger competitive position than Trican as a result.