Malayan Banking Berhad (Maybank) AGM Chariman's Presentation - Six Month Report - December 2011

Upload

truongnguyetCategory

view

219download

2

The credit rating is not a recommendation to purchase, sell or hold a security, inasmuch as it does not comment on the security’s market price or its suitability for a particular investor, nor does it involve any audit by RAM Ratings. The credit rating also does not reflect the legality and enforceability of financial obligations, transfer and convertibility risks, repatriation risk, currency risk or any other risk apart from credit risk.

JULY 2011

MALAYAN BANKING BERHAD

Financial Institution Ratings

RM1.5 billion Islamic Subordinated Bonds (2006/2018)

RM1.5 billion Subordinated Bonds (2007/2017)

Up to RM4.0 billion Innovative Tier-1 Capital Securities

(2008/2073)

Up to RM3.5 billion Non-Innovative Tier-1 Capital Securities

(2008/2108)

Proposed up to RM3 billion Tier-2 Capital Subordinated

Note Programme

CEKAP MENTARI BERHAD

Up to RM3.5 billion Subordinated Notes (2008/2038)

The credit rating is not a recommendation to purchase, sell or hold a security, inasmuch as it does not comment on the security’s market price or its suitability for a particular investor, nor does it involve any audit by RAM Ratings. The credit rating also does not reflect the legality and enforceability of financial obligations, transfer and convertibility risks, repatriation risk, currency risk or any other risk apart from credit risk.

CREDIT RATING RATIONALE

FINANCIAL INSTITUTION RATINGS

JULY 2011

MALAYAN BANKING BERHAD

– Initial Rating & Rating Update

RAM Ratings has reaffirmed Malayan Banking Berhad’s (“Maybank” or “the

Group”) long- and short-term financial institution ratings at AAA and P1,

respectively. At the same time, the respective issue ratings of Maybank and

Cekap Mentari Berhad (“Cekap Mentari” – a subsidiary set up to issue

subordinated notes) have been reaffirmed while a AA1 rating has been assigned

to Maybank’s proposed up to RM3 billion Tier-2 Capital Subordinated Notes

Programme. All the long-term ratings have a stable outlook.

Table 1: Debt instruments of Maybank and Cekap Mentari

Instrument Rating

Action Rating Outlook

Malayan Banking Berhad

RM1.5 billion Subordinated Bonds (2007/2017) 1 Reaffirmed AA1 Stable

RM1.5 billion Islamic Subordinated Bonds (2006/2018)1 Reaffirmed AA1 Stable

Up to RM4.0 billion Innovative Tier-1 Capital Securities (2008/2073) 2 Reaffirmed AA2 Stable

Up to RM3.5 billion Non-Innovative Tier-1 Capital Securities (2008/2108) 2 Reaffirmed AA2 Stable

Proposed up to RM3 billion Tier-2 Capital Subordinated Note Programme 1 Assigned AA1 Stable

Notes: 1 The 1-notch rating differential between Maybank’s AAA long-term financial institution rating and the AA1 ratings of its Subordinated

Bonds reflect the subordination of the debt facilities to its senior unsecured obligations. 2 The 2-notch rating differential between Maybank’s AAA long-term financial institution rating and the AA2 ratings of its Innovative and

Non-Innovative Tier-1 Capital Securities reflect the deeply subordinated nature and the embedded interest-deferral feature of the

hybrid instruments.

Cekap Mentari Berhad

Up to RM3.5 billion Subordinated Notes (2008/2038) Reaffirmed AA2 Stable

Note:

The up to RM3.5 billion Subordinated Notes are part of the up to RM3.5 billion Non-Innovative Tier-1 Capital Securities transaction.

Each issue of Capital Securities will be stapled to the Subordinated Notes issued by Cekap Mentari. The Subordinated Notes carry

the same rating as the Non-Innovative Tier-1 Capital Securities.

The ratings reflect Maybank’s significant systemic importance, excellent

franchise and sound credit fundamentals. The Group currently commands the

largest share of loans and deposits in the Malaysian banking system, and is

supported by stable funding and liquidity positions as well as sound capitalisation

levels. With an asset base of RM380 billion as at end-March 2011, Maybank is

the largest domestic banking group in Malaysia. While the Group remains the

largest financier in the country in terms of gross loans, commanding

Analysts: Joanne Kek (603) 7628 1163 [email protected] Shireen Ng (603) 7628 1021 [email protected] Principal Activity: Commercial banking Financial Institution Ratings: Long-term: AAA [Reaffirmed] Short-term: P1 [Reaffirmed] Instruments: Malayan Banking Berhad (i) RM1.5 billion

Subordinated Bonds (2007/2017)

(ii) RM1.5 billion Islamic Subordinated Bonds (2006/2018)

(iii) Up to RM4.0 billion Innovative Tier-1 Capital Securities (2008/2073)

(iv) Up to RM3.5 billion Non-Innovative Tier-1 Capital Securities (2008/2108)

(v) Proposed up to RM3 billion Tier-2 Capital Subordinated Note Programme

Cekap Mentari Berhad (vi) RM3.5 billion

Subordinated Notes (2008/2038)

Islamic Contract: (ii) Bai-Bithaman Ajil

Malayan Banking Berhad Cekap Mentari Berhad

2

approximately 18% of the Malaysian market1, it faces keen competition.

Table 2: Maybank’s acquisition of Kim Eng Holdings Limited (“Kim Eng”)

Details Particulars

Acquired stakes and price

tags

At SGD3.10 per Kim Eng share:

Initial 44.6%-stake for SGD798 million

Remaining 55.4%-stake for SGD991 million

Total acquisition cost of SGD1,789 million

Valuation Price to book value (as at December 2010): 1.85 times

Price to earnings (for FY Dec 2010) ratio: 23.3 times

Expected completion date In August 2011

Funding structure Issuance of equity and/or debt and internally generated

funds

RAM Ratings’ estimate of

Maybank’s overall

RWCAR, post-acquisition

Above 12%

Strategic rationales and

synergistic opportunities

The extension of Maybank’s distribution capabilities to

key global financial markets.

Acquisition propels expansion into the Thai market

Cross-selling opportunities, larger client base.

In line with Maybank’s regional profit targets and its

aspiration of becoming a leading ASEAN wholesale

bank.

Salient acquisition terms

Upon the purchase of the 44.6%-stake, Maybank will

make a mandatory general offer for the remaining Kim

Eng shares.

Maybank intends to take Kim Eng private, delisting the

latter’s shares from the Singapore Exchange (or SGX).

Retention programme to be put in place, with the

current chairman continuing to lead Kim Eng for at

least another 3 years.

Source: Maybank’s and Kim Eng’s annual reports, RAM Ratings’ internal estimates and calculations.

In January 2011, Maybank announced the acquisition of Kim Eng, a leading

Singapore-based regional securities and investment broking group. Maybank

completed the acquisition of an initial stake in May 2011 and subsequently

launched a mandatory general offer for the acquisition of the remaining Kim Eng

shares. The transaction is expected to be completed in August 2011, and is

funded through a combination of internal and external funds.

Although Maybank will take some time before it can reap the full benefits from

Kim Eng’s franchise, this acquisition will enable the Group’s subsidiary, Maybank

Investment Bank Berhad (rated AAA/Stable/P1), to gain a strong regional

foothold and allow instant access to the ASEAN market. In fiscal 2010, Kim Eng

chalked up SGD412 million of operating income and SGD113 million of pre-tax

profit. Its operating income was dominated by stockbroking fees (74%). By

1 As at end-March 2011.

Ratings: (i) AA1 [Reaffirmed] (ii) AA1 [Reaffirmed] (iii) AA2 [Reaffirmed] (iv) AA2 [Reaffirmed] (v) AA1 [Assigned] (vi) AA2 [Reaffirmed] Rating Outlook: Stable Last Rating Action: 16 December 2010 Coupon Rates/Profit Margins: (i) 4.00% (ii) 5.00% for Years 1-7;

5.70% for Year 8; 5.90% for Year 9; 6.00% for Years 10-12

(iii) 6.3% for Years 1-10; 3-month KLIBOR + 1.95% thereafter

(iv) 6.85% (v) Determined at issuance (vi) 6.85% Maturity Dates: (i) 13 April 2017 (ii) 15 May 2018 (iii) 25 September 2073 (ii) 27 June 2108 (v) 20 years, from date of

first issuance (vi) 25 June 2038 Lead Arranger: Maybank Investment Bank Berhad Trustee: Malaysian Trustees Berhad Shariah Advisor: Maybank Shariah Committee Security: None

Kim Eng acquisition catalyst for regional investment-banking franchise although full integration benefits will take

time to materialise

Malayan Banking Berhad Cekap Mentari Berhad

3

geographical segment2, Kim Eng’s Singaporean operations make up almost half

(48%) of its revenue, followed by Thailand (32%) and Hong Kong (10%). In

addition to a strong presence in Singapore, Kim Eng also boasts solid positions

in the equity markets of Thailand, the Philippines and Indonesia.

Table 3: Snapshot of Kim Eng’s financials

SGD million FY Dec 2008 FY Dec 2009 FY Dec 2010

Operating income 351.03 366.19 411.75

Brokerage & trading income 245.05 289.02 305.30

Pre-tax profits 91.16 135.74 113.39

Total Assets 1,161.56 1,794.52 1,745.67

Net Assets 967.87 1,046.87 1,088.93

Source: Kim Eng’s annual reports

Post-acquisition, the Group’s investment-banking division will become a larger

business driver, with an estimated pro forma contribution of 8%3 to Maybank’s

pre-tax profits - compared to 2% in the financial year ending June 2010 (“FY

June 2010”). RAM Ratings notes, however, that investment-banking income is

typically volatile, and is subject to the vagaries of the capital markets.

In May 2011, Maybank had announced the receipt of Bank Negara Malaysia’s

approval to commence talks with RHB Capital Berhad and its major shareholders

on a possible merger of their businesses. Negotiations for the potential merger

were terminated in June 2011. Maybank intends to become a regional financial-

services leader by 2015, with its international operations making up 40% of its

pre-tax profits. The Bank’s targeted markets include the Middle East, China and

India, on top of its existing regional operations in Singapore, Indonesia (through

Bank Internasional Indonesia, (“BII”), Pakistan (via MCB Bank Ltd) and Vietnam

(through An Binh Bank). The Group’s strategies include gaining leadership in the

domestic insurance sector and turning its subsidiary, Maybank Islamic Berhad

(rated AAA/Stable/P1), into the largest Islamic bank in ASEAN.

2 Figures for breakdown of revenue by operating segment are for FY Dec 2009.

3 Source: Maybank. Pro forma calculations based on FY June 2010 and FY Dec 2009 results of

Maybank and Kim Eng, respectively.

Profit contributions from investment banking to grow

International operations to contribute to 40% of pre-tax profits

by 2015

Malayan Banking Berhad Cekap Mentari Berhad

4

For FY June 2011, Maybank has set a 12% growth target for its overall loan and

debt securities. Its Malaysian and Singaporean operations have aimed for

respective 12% and 5% growth rates. Meanwhile, BII’s lending portfolio is

expected to augment 24%, reflective of Indonesia’s vastly unbanked population

and favourable growth prospects. In 3Q FY Dec 2011, the Group’s gross loans

expanded an annualised 18% to RM242 billion. The growth had been primarily

driven by an annualised 22% jump in the loan books of BII, and an 25%

annualised loan growth for Maybank Singapore. On the other hand, loans of

Maybank’s domestic operations had increased at a more moderate annualised

rate of 15% (FY June 2010: +10%). Meanwhile, Maybank’s international

operations account for approximately 34% of the Group’s loans; its 2 largest

overseas markets are Singapore and Indonesia, with respective contributions of

20% and 8% to total gross loans.

In July 2010, Maybank adopted the FRS 139 recognition criteria for impaired

loans4. As at end-March 2011, its group-level gross impaired-loan (“GIL”) ratio

worked out to 3.7%5 (restated ratio as at end-June 2010: 4.6%) - within RAM

Ratings’ expectations. At the same time, the Group’s net impaired-loan ratio

stood at 2.4% (restated ratio as at end-June 2010: 2.8%). We expect FY Dec

2011 credit costs to be lower than the previous year; credit costs in 9M FY June

2011 came up to an annualised 0.27% of average gross loans (FY Dec 2010:

0.58%). With the adoption of FRS 139, some adjustments to loan impairments

had been made against retained earnings at the start of the current financial

year.

Maybank achieved a pre-tax profit of approximately RM4.5 billion in 9M FY June

2011 (9M FY June 2010: RM4.0 billion), supported by stronger net interest

income contributions from its expanding loan books and lower loan-loss charges.

The Group’s Malaysian operations accounted for the majority of its pre-tax profits

(about 75%), followed by Singapore and Indonesia. Maybank’s net interest

margin clocked in at 1.99% in 9M FY June 2011 (FY June 2010: 2.09%6);

competitive pressures had compressed interest margins on its domestic

mortgage and hire-purchase portfolios. All said, RAM Ratings expects the

Group’s current-year pre-tax profit to surpass the RM5.4 billion achieved in FY

June 2010.

Approximately 67% of the Group’s deposits are sourced domestically. Maybank’s

funding capabilities are viewed to be unrivalled in Malaysia - it commands 15% of

the local banking industry’s deposits (as at end-March 2011), and has a large,

low-cost base of current and savings account deposits (approximately 43% of its

4 The GIL ratio is numerically higher than the previous measure, i.e. gross non-performing-loan ratio,

due to more stringent loan-impairment classification criteria; loans less than 3 months in arrears are classified as impaired if they exhibit signs of impairment.

5 By geographical segment, the GIL ratio of its Malaysian operations stand at 4.5% as at end-March

2011; its international operations record a corresponding GIL ratio of 2%. 6 Net interest margin quoted as a percentage of total assets.

Indonesian loan books to augment

24%

Impaired-loan ratios within expectations

Pre-tax profit anticipated to rise in fiscal 2011

Funding capabilities unrivalled by local

peers

Malayan Banking Berhad Cekap Mentari Berhad

5

total deposits). The Group’s domestic loans-to-deposits ratio of 88.2% as at end-

March 2011 exceeded the Malaysian industry average, but it remains well within

the norm for a bank of its size and market position. Elsewhere, BII’s loans-to-

deposits ratio had climbed up to 94% as at end-March 2011 (end-December

2009: 83%), because loan growth (an annualised +27%) in 9M FY June 2011

had outpaced deposit expansion (+19%, annualised). With a liquid-asset ratio of

25.3% as at end-March 2011, Maybank’s liquidity profile is considered healthy.

Under Maybank’s Dividend Reinvestment Plan (“DRP”), announced in March

2010, the Group’s shareholders can elect to either receive their dividends in cash

or reinvest a portion of it in Maybank shares. RAM Ratings understands that the

election rate for the DRP (on dividends declared for FY June 2010) came up to a

high 88.59%, thus bolstering its capital base. Assuming a conservative full

payout of proposed dividends7 in cash, the Group’s overall and Tier-1 risk-

weighted capital-adequacy ratios (“RWCARs”) would stand at a respective 13.6%

and 11.1% as at end-March 2011. While the acquisition of Kim Eng may dent its

capitalisation levels, we expect Maybank’s overall RWCAR to remain above

12%. In April 2011, Maybank issued SGD1 billion Subordinated Notes under a

USD2.0 billion Multicurrency Medium-Term Note programme; these

Subordinated Notes qualify as tier-2 capital. On the whole, Maybank’s

capitalisation position is viewed to be sound.

7 Interim dividend for FY Dec 2011 of 28 sen per share (21 sen net dividend, of which 3 sen

represents the cash portion while 18 sen is the electable portion).

Overall RWCAR expected to remain sound at above 12%

Malayan Banking Berhad Cekap Mentari Berhad

6

Objectives of the Proposed Issue

Proceeds from the issuance of the Subordinated Notes under the proposed up to

RM3 billion Tier-2 Capital Subordinated Note Programme (“the Programme”) will

be used to fund Maybank’s working capital as well as for general banking and

other corporate purposes. Coupons under the proposed debt facility will be paid

semi-annually, in arrears.

The Subordinated Notes issued under the Programme are expected to be

classified as Tier-2 capital, for inclusion in the calculation of Maybank’s RWCAR.

The Programme has a 20-year tenure, commencing from the date of its first

issuance. Meanwhile, each issuance of Subordinated Notes will be structured to

have one of the following tenures: (i) 10 years, on a non-callable basis; (ii) 15 -

years, on a 15 non-callable 10 basis, (iii) 12-years, on a 12 non-callable 7 basis

or (iv) 10 years, on a 10 non-callable 5 basis. Subordinated Notes with a call

option shall be callable on each coupon payment date in the 5 years prior to the

maturity date.

The aforementioned terms and conditions of the Subordinated Notes issued

under the Programme are not exhaustive. Investors will need to review the Trust

Deed and Programme Agreement for a comprehensive understanding of the

terms and conditions.

Malayan Banking Berhad Cekap Mentari Berhad

7

Corporate Information – Malayan Banking Berhad

Date of Incorporation:

31 May 1960

Commencement of Business:

12 September 1960

Major Shareholders (as at 20 April 2011):

Amanah Raya Nominees (Tempatan) Sdn Bhd*

Employees Provident Fund Board Permodalan Nasional Berhad * Nominee for Skim Amanah Saham Bumiputera

45.31% 10.88% 5.32%

Directors:

Tan Sri Dato' Megat Zaharuddin Megat Mohd Nor Dato' Mohd Salleh bin Hj Harun Dato' Sri Abdul Wahid bin Omar Tan Sri Datuk Dr Hadenan Jalil Dato' Seri Ismail Shahudin Dato' Dr Tan Tat Wai Zainal Abidin Bin Jamal Alister Maitland Cheah Teik Seng Dato’ Johan Ariffin Sreesanthan Eliathamby

Auditor:

Ernst & Young

Listing:

17 February 1962 (Main Market of Bursa Malaysia)

Key Management:

Dato’ Sri Abdul Wahid Omar Khairussaleh Ramli Lim Hong Tat Dr John Lee Hin Hock Geoffrey Stecyk Ridha Wirakusumah Pollie Sim Tengku Dato’ Zafrul Aziz Muzaffar Hisham Nora Abd Manaf Hans De Cuyper Hazimi Kassim Jerome Hon Kah Cho Mohd Nazlan Mohd Ghazali

President & Chief Executive Officer Group Chief Financial Officer Head, Community Financial Services Group Chief Risk Officer Head, Enterprise Transformation Services President Director, Bank Internasional Indonesia Chief Executive Officer, Maybank Singapore Chief Executive Officer, Maybank Investment Bank Berhad Head, Group Islamic Banking Head, Group Human Capital Head, Insurance & Takaful Head, Strategy & Corporate Finance Chief Audit Executive General Counsel & Company Secretary

Malayan Banking Berhad Cekap Mentari Berhad

8

Corporate Information – Malayan Banking Berhad Major Subsidiaries:

Banking Maybank Islamic Berhad PT Bank Maybank Syariah Indonesia Bank Internasional Indonesia Tbk Maybank International (L) Ltd Maybank (PNG) Limited Maybank Philippines Incorporated Investment Banking Maybank Investment Bank Berhad Insurance & Takaful Mayban Fortis Holdings Berhad ETiQa Insurance Berhad ETiQa Takaful Berhad Mayban Life Assurance Berhad Mayban Life International (L) Ltd Asset Management/Trustees/Custodial Mayban International Trust (Labuan) Berhad Mayban Trustees Berhad Mayban Ventures Sdn Bhd Mayban Investment Management Sdn Bhd

100.00% 96.80% 97.50% 100.00% 100.00% 99.97% 100.00% 69.05% 69.05% 69.05% 69.05% 62.00% 100.00% 100.00% 100.00% 100.00%

Capital History:

Year Remarks Amount (RM million)

Cumulative Total (RM million)

2005 2006 2007 2008 2008 2008 2009 2009 2010

Paid-up capital Employee Share Option Scheme Employee Share Option Scheme Bonus issue Employee Share Option Scheme Employee Share Option Scheme Rights issue Employee Share Option Scheme Issuance of new shares pursuant to Dividend Reinvestment Plan

3,721.05 75.90 92.28 976.05 15.84 0.03

2,196.52 0.32

244.26

3,721.05 3,796.95 3,889.23 4,865.28 4,881.12 4,881.15 7,077.66 7,077.98

7,322.24

Malayan Banking Berhad Cekap Mentari Berhad

9

unaudited

STATEMENT OF FINANCIAL POSITION (RM million) 30-Jun-07 30-Jun-08 30-Jun-09 30-Jun-10 31-Mar-11

ASSETS

Cash & Money At Call 37,597.42 27,644.36 23,607.98 28,707.99 31,988.87

Deposits & Placements With Financial Institutions 17,348.42 8,956.52 6,299.18 8,915.38 8,495.39

Securities Purchased Under Resale Agreements 258.77 0.00 346.46 371.24 483.75

Financial Assets Held for Trading 2,032.63 880.79 1,489.27 2,651.10 7,420.72

Financial Investments Available for Sale 29,124.70 34,484.14 47,877.11 42,576.24 47,512.62

Financial Investments Held to Maturity 2,534.39 1,186.23 8,360.75 8,942.71 9,302.13

Gross Loans & Advances 147,497.27 171,155.46 193,362.79 213,258.44 241,794.31

Collective Impairment Allowances ^ (2,757.32) (3,187.61) (3,725.60) (3,838.54) (4,565.19)

Individual Impairment Allowances ^^ (3,875.22) (3,353.68) (3,854.03) (3,864.83) (3,142.39)

Net Loans & Advances 140,864.74 164,614.18 185,783.17 205,555.07 234,086.73

Statutory Deposits 5,652.23 5,872.41 4,050.93 4,471.38 4,421.18

Investments in Associates and/or Joint Ventures 43.60 2,218.85 2,630.12 2,471.44 2,327.07

Other Assets 20,058.67 22,032.40 28,898.60 30,677.38 32,952.40

Property, Plant & Equipment 1,151.69 1,210.83 1,395.56 1,359.85 1,351.09

TOTAL ASSETS 256,667.28 269,100.70 310,739.12 336,699.77 380,341.94

LIABILITIES

Customer Deposits 163,676.76 187,112.08 212,598.59 236,909.79 260,738.98

Demand 30,890.79 38,634.57 44,730.96 48,779.47 54,163.53

Savings 27,842.62 29,425.90 35,290.82 38,779.00 42,724.05

Fixed 104,462.67 105,735.18 118,733.15 130,645.97 144,619.24

Negotiable Instruments of Deposits 0.00 0.00 0.00 0.00 0.00

Others 480.69 13,316.43 13,843.66 18,705.35 19,232.16

Interbank Deposits 29,534.69 23,136.88 28,781.86 23,257.87 33,962.98

Bills & Acceptances Payable 2,930.07 4,792.30 1,470.06 3,061.59 3,776.25

Securities Sold Under Repurchase Agreements 9,957.07 322.37 0.00 407.06 148.61

Other Borrowings 2,455.76 2,691.30 2,028.58 3,474.84 5,394.18

Debt Securities & Hybrid Capital 6,344.05 8,473.04 14,719.91 14,047.87 14,038.45

Other Liabilities 21,900.73 22,480.97 25,372.14 26,875.82 31,602.87

TOTAL LIABILITIES 236,799.13 249,008.94 284,971.15 308,034.83 349,662.33

Paid-up Capital 3,889.23 4,881.12 7,077.66 7,077.98 7,322.24

Share Premium & Other Reserves 3,333.64 1,717.24 5,167.60 5,319.31 6,490.24

Statutory Reserves 3,921.99 4,573.64 4,664.98 5,554.00 6,192.70

Retained Profits/(Accumulated Losses) 8,052.80 8,130.50 7,988.50 9,925.89 9,870.22

TOTAL EQUITY ATTRIBUTABLE TO EQUITY HOLDERS 19,197.66 19,302.49 24,898.75 27,877.18 29,875.39

Minority Interests 670.49 789.27 869.23 787.76 804.22

TOTAL EQUITY 19,868.15 20,091.76 25,767.98 28,664.94 30,679.61

TOTAL LIABILITIES AND EQUITY 256,667.28 269,100.70 310,739.12 336,699.77 380,341.94

COMMITMENTS & CONTINGENCIES 175,392.45 204,216.76 221,586.70 232,273.34 236,083.13

TIER 1 CAPITAL 16,904.26 19,935.05 24,456.04 24,719.04 26,556.28

CAPITAL BASE 26,010.63 25,166.70 33,492.04 33,543.39 32,604.09

Note:

^ Prior to FY Dec 2010, known as General Loan Loss Reserves

^^ Prior to FY Dec 2010, known as Specific Loan Loss Reserves

* After deducting proposed dividends. Capital figures as at end-March 2011 reflect the assumption that the full electable portion under the Dividend Reinvestment Plan is

paid in cash.

FINANCIAL SUMMARY Malayan Banking Berhad – Group

Malayan Banking Berhad Cekap Mentari Berhad

10

unaudited

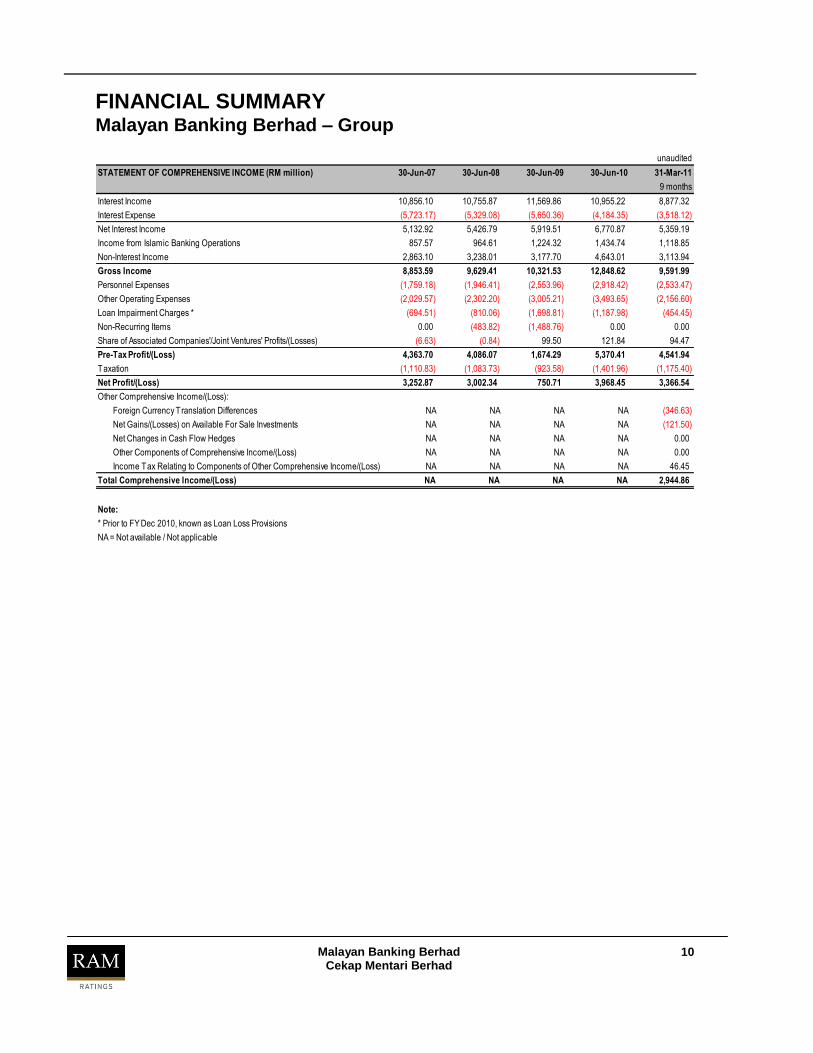

STATEMENT OF COMPREHENSIVE INCOME (RM million) 30-Jun-07 30-Jun-08 30-Jun-09 30-Jun-10 31-Mar-11

9 months

Interest Income 10,856.10 10,755.87 11,569.86 10,955.22 8,877.32

Interest Expense (5,723.17) (5,329.08) (5,650.36) (4,184.35) (3,518.12)

Net Interest Income 5,132.92 5,426.79 5,919.51 6,770.87 5,359.19

Income from Islamic Banking Operations 857.57 964.61 1,224.32 1,434.74 1,118.85

Non-Interest Income 2,863.10 3,238.01 3,177.70 4,643.01 3,113.94

Gross Income 8,853.59 9,629.41 10,321.53 12,848.62 9,591.99

Personnel Expenses (1,759.18) (1,946.41) (2,553.96) (2,918.42) (2,533.47)

Other Operating Expenses (2,029.57) (2,302.20) (3,005.21) (3,493.65) (2,156.60)

Loan Impairment Charges * (694.51) (810.06) (1,698.81) (1,187.98) (454.45)

Non-Recurring Items 0.00 (483.82) (1,488.76) 0.00 0.00

Share of Associated Companies'/Joint Ventures' Profits/(Losses) (6.63) (0.84) 99.50 121.84 94.47

Pre-Tax Profit/(Loss) 4,363.70 4,086.07 1,674.29 5,370.41 4,541.94

Taxation (1,110.83) (1,083.73) (923.58) (1,401.96) (1,175.40)

Net Profit/(Loss) 3,252.87 3,002.34 750.71 3,968.45 3,366.54

Other Comprehensive Income/(Loss):

Foreign Currency Translation Differences NA NA NA NA (346.63)

Net Gains/(Losses) on Available For Sale Investments NA NA NA NA (121.50)

Net Changes in Cash Flow Hedges NA NA NA NA 0.00

Other Components of Comprehensive Income/(Loss) NA NA NA NA 0.00

Income Tax Relating to Components of Other Comprehensive Income/(Loss) NA NA NA NA 46.45

Total Comprehensive Income/(Loss) NA NA NA NA 2,944.86

Note:

* Prior to FY Dec 2010, known as Loan Loss Provisions

NA = Not available / Not applicable

FINANCIAL SUMMARY Malayan Banking Berhad – Group

Malayan Banking Berhad Cekap Mentari Berhad

11

unaudited

KEY FINANCIAL RATIOS (%) 30-Jun-07 30-Jun-08 30-Jun-09 30-Jun-10 31-Mar-11

PROFITABILITY

Net Interest Margin 2.13% 2.06% 2.04% 2.09% 1.99% *

Non-Interest Income Margin 1.19% 1.23% 1.10% 1.43% 1.16% *

Cost To Income 42.79% 44.12% 53.86% 49.90% 48.90%

Cost Over Total Average Assets 1.58% 1.62% 1.92% 1.98% 1.74% *

Return On Assets 1.81% 1.55% 0.58% 1.66% 1.69% *

Return On Equity 23.37% 20.45% 7.30% 19.73% 20.41% *

Dividend Payout 64.53% 72.74% 96.23% 25.42% 75.91%

ASSET QUALITY

Gross Impaired Loan Ratio ^ 5.55% 3.76% 3.46% 2.89% 3.67%

Net Impaired Loan Ratio ^ 3.03% 1.85% 1.51% 1.10% 2.40%

Net Impaired Loans To Total Assets ^ 1.71% 1.16% 0.92% 0.69% 1.51%

Individual Impairment Allowance For The Period 1.20% 0.55% 1.14% 1.05% 0.51% *

Gross Impaired Loan Coverage ^ 80.31% 101.06% 112.87% 124.52% 86.90%

Loan Loss Reserve Coverage 4.46% 3.80% 3.91% 3.59% 3.19%

Collective Loan Loss Reserve Coverage 1.90% 1.89% 1.96% 1.82% 1.91%

LIQUIDITY & FUNDING

Liquid Asset Ratio 37.03% 26.49% 25.75% 25.36% 25.25%

Interbank Deposits To Total Interest Bearing Funds 13.74% 10.21% 11.09% 8.27% 10.68%

Customer Deposits To Total Interest Bearing Funds 76.16% 82.60% 81.89% 84.26% 81.98%

Loans To Deposits Ratio 86.06% 87.98% 87.39% 86.77% 89.78%

Loans To Stable Funds Ratio 68.12% 73.74% 72.49% 71.73% 74.16%

CAPITAL ADEQUACY

Total Equity To Total Assets 7.74% 7.47% 8.29% 8.51% 8.07%

Tier 1 Risk Weighted Capital Adequacy Ratio 9.43% 10.08% 10.82% 10.11% 11.09% #

Overall Risk Weighted Capital Adequacy Ratio 14.51% 12.73% 14.81% 13.72% 13.62% #

Internal Rate Of Capital Generation 7.89% 6.17% 1.51% 11.41% 5.06% *

Note :

^ Prior to FY Dec 2010, Impaired Loans were known as Non-Performing Loans

* annualised# Capital Adequacy Ratios assuming full electable portion under the Dividend Reinvestment Plan is paid in cash.

FINANCIAL RATIOS Malayan Banking Berhad – Group

Malayan Banking Berhad Cekap Mentari Berhad

12

KEY FINANCIAL RATIOS FORMULAE

PROFITABILITY

Net Interest Margin Net Interest Income / Average Total Assets

Non-Interest Income Margin Non-Interest Income / Average Total Assets

Cost To Income (Personnel & Other Operating Expenses) / Gross Income

Cost Over Total Average Assets (Personnel & Other Operating Expenses) / Average Total Assets

Return On Assets Pre-Tax Profit/(Loss) / Average Total Assets

Return On Equity Pre-Tax Profit/(Loss) / Average Total Equity

Dividend Payout Dividends / Net Profit/(Loss)

ASSET QUALITY

Gross Impaired Loan Ratio Total Impaired Loans / Gross Loans

Net Impaired Loan Ratio (Total Impaired Loans - Individual Impairment Allowances) / (Gross Loans - Individual Impairment Allowances)

Net Impaired Loan To Total Assets (Total Impaired Loans - Individual Impairment Allowances) / Total Assets

Individual Impairment Allowance For The Period Individual Impairment Allowance For The Period / Average Gross Loans

Gross Impaired Loan Coverage (Collective Impairment Allowances + Individual Impairment Allowances) / Total Impaired Loans

Loan Loss Reserve Coverage (Collective Impairment Allowances + Individual Impairment Allowances) / Gross Loans

Collective Loan Loss Reserve Coverage Collective Impairment Allowances / (Gross Loans - Individual Impairment Allowances)

LIQUIDITY & FUNDING

Liquid Asset Ratio Liquid Assets / Customer Deposits & Short-Term Funds

Loans To Deposits Ratio Net Loans / Customer Deposits

Loans To Stable Funds Ratio Net Loans / (Shareholders' Funds + Total Interest Bearing Funds + Collective Impairment Allowance

- Interbank Funding - Property, Plant & Equipment - Investments in Associates)

Short-Term Funds Interbank Deposits + Bills & Acceptances + Securities Sold Under Repos

Liquid Assets Cash & Short-Term Funds + Securities Purchased Under Repos + Deposits & Placements With

Financial Institutions + Quoted Securities (Excluding Financial Investments Held-To-Maturity)

Total Interest Bearing Funds Customer Deposits + Interbank + Bills & Acceptances + Securities Sold Under Repos + Borrowings + Supplementary Capital

CAPITAL ADEQUACY

Internal Rate Of Capital Generation (Net Profit/(Loss) + Extraordinary Income - Dividend + Collective Impairment Allowances) /

Average Total Equity

FINANCIAL RATIOS Malayan Banking Berhad – Group

Malayan Banking Berhad Cekap Mentari Berhad

13

CREDIT RATING DEFINITIONS

Financial Institution Ratings

Long-Term Ratings

AAA

AA

A

BBB

BB

B

C

D

Short-Term Ratings

P1

P2

P3

NP

D

A financial institution rated AAA has a superior capacity to meet its financial obligations. This is the highest long-term FIRassigned by RAM Ratings.

A financial institution rated AA has a strong capacity to meet its financial obligations. The financial institution is resilientagainst adverse changes in circumstances, economic conditions and/or operating environments.

A financial institution rated A has an adequate capacity to meet its financial obligations. The financial institution is moresusceptible to adverse changes in circumstances, economic conditions and/or operating environments than those in

higher-rated categories.

A financial institution rated BBB has a moderate capacity to meet its financial obligations. The financial institution is morelikely to be weakened by adverse changes in circumstances, economic conditions and/or operating environments than

those in higher-rated categories. This is the lowest investment-grade category.

A financial institution rated BB has a weak capacity to meet its financial obligations. The financial institution is highlyvulnerable to adverse changes in circumstances, economic conditions and/or operating environments.

A financial institution rated B has a very weak capacity to meet its financial obligations. The financial institution has alimited ability to withstand adverse changes in circumstances, economic conditions and/oroperating environments.

A financial institution rated C has a high likelihood of defaulting on its financial obligations. The financial institution ishighly dependent on favourable changes in circumstances, economic conditions and/or operating environments, the lack

of which would likely result in it defaultingon its financial obligations.

A financial institution rated D is currently in default on either all or a substantial portion of its financial obligations, whetheror not formally declared. The D rating may also reflect the filing of bankruptcy and/or other actions pertaining to the

financial institution that could jeopardise the payment of financial obligations.

A financial institution rated P1 has a strong capacity to meet its short-term financial obligations. This is the highest short-term FIR assigned by RAM Ratings.

A financial institution rated P2 has an adequate capacity to meet its short-term financial obligations. The financialinstitution is more susceptible to the effectsof deteriorating circumstances than thosein the highest-rated category.

A financial institution rated P3 has a moderate capacity to meet its short-term financial obligations. The financialinstitution is more likely to be weakened by the effects of deteriorating circumstances than those in higher-rated

categories. This is the lowest investment-grade category.

A financial institution rated NP has a doubtful capacity to meet its short-term financial obligations. The financial institutionfaces major uncertainties that could compromise its capacity for payment of financial obligations.

A financial institution rated D is currently in default on either all or a substantial portion of its financial obligations, whetheror not formally declared. The D rating may also reflect the filing of bankruptcy and/or other actions pertaining to the

financial institution that could jeopardise the payment of financial obligations.

For long-term ratings, RAM Ratings applies subscripts 1, 2 or 3 in each rating category from AA to C. The subscript 1 indicates that thefinancial institution ranks at the higher end of its generic rating category; the subscript 2 indicates a mid-ranking; and the subscript 3

indicates that the financial institution ranks at the lower end of its generic rating category.

A Financial Institution Rating ("FIR") is RAM Ratings' current opinion on the overall capacity of a financial institution to meetits financial obligations. The opinion is not specific to any particular financial obligation, as it does not take into account theexpressed terms and conditions of any specific financial obligation.

Malayan Banking Berhad Cekap Mentari Berhad

14

CREDIT RATING DEFINITIONS

Issue Ratings

Long-Term Ratings

AAA

AA

A

BBB

BB

B

C

D

Short-Term Ratings

P1

P2

P3

NP

D

An issue rated AAA has superior safety for payment of financial obligations. This is the highest long-term Issue Ratingassigned by RAM Ratings.

An issue rated AA has high safety for payment of financial obligations. The issuer is resilient against adverse changes incircumstances, economic conditions and/or operating environments.

An issue rated A has adequate safety for payment of financial obligations. The issuer is more susceptible to adversechanges in circumstances, economic conditions and/or operating environments than those in higher-rated categories.

An issue rated BBB has moderate safety for payment of financial obligations. The issuer is more likely to be weakened byadverse changes in circumstances, economic conditions and/or operating environments than those in higher-rated

categories. This is the lowest investment-grade category.

An issue rated BB has low safety for payment of financial obligations. The issuer is highly vulnerable to adverse changesin circumstances, economic conditions and/oroperating environments.

An issue rated B has very low safety for payment of financial obligations. The issuer has a limited ability to withstandadverse changes in circumstances, economic conditions and/oroperating environments.

An issue rated C has a high likelihood of default. The issuer is highly dependent on favourable changes in circumstances,economic conditions and/or operating environments, the lack of which would likely result in it defaulting on a particular

debt issue.

An issue rated D is either currently in default or faces imminent default on its financial obligations, whether or not formallydeclared. The D rating may also reflect a distressed exchange, the filing of bankruptcy and/or other actions pertaining to

the issuer that could jeopardise thepayment of a particular debt issue.

An issue rated P1 has high safety for payment of financial obligations in the short term. This is the highest short-termIssue Rating assigned by RAM Ratings.

An issue rated P2 has adequate safety for payment of financial obligations in the short term. The issuer is moresusceptible to the effects of deteriorating circumstances than those in the highest-rated category.

An issue rated P3 has moderate safety for payment of financial obligations in the short term. The issuer is more likely tobe weakened by the effects of deteriorating circumstances than those in higher-rated categories. This is the lowest

investment-grade category.

An issue rated NP has doubtful safety for payment of financial obligations in the short term. The issuer faces majoruncertainties that could compromise its capacity for payment of a particulardebt issue.

An issue rated D is either currently in default or faces imminent default on its financial obligations, whether or not formallydeclared. The D rating may also reflect a distressed exchange, the filing of bankruptcy and/or other actions pertaining to

the issuer that could jeopardise thepayment of a particular debt issue.

For long-term ratings, RAM Ratings applies subscripts 1, 2 or 3 in each rating category from AA to C. The subscript 1 indicates that theissue ranks at the higher end of its generic rating category; the subscript 2 indicates a mid-ranking; and the subscript 3 indicates that the

issue ranks at the lower end of its generic rating category. In addition, RAM Ratings applies the suffixes (bg) or (s) to ratings which havebeen enhanced by a bank guarantee or other supports, respectively.

An Issue Rating is RAM Ratings' current opinion on the creditworthiness of a particular debt issue. It reflects the overallcapacity and willingness of an issuer to meet the financial obligations on a particular debt issue on a full and timely basis,taking into account its expressed terms and conditions.

Malayan Banking Berhad Cekap Mentari Berhad

15

CREDIT RATING DEFINITIONS

Issue Ratings - Debt-Based Sukuk

Long-Term Ratings

AAA

AA

A

BBB

BB

B

C

D

Short-Term Ratings

P1

P2

P3

NP

D

A sukuk rated AAA has superior safety for payment of financial obligations. This is the highest long-term Issue Ratingassigned by RAM Ratings to a debt-based sukuk.

A sukuk rated AA has high safety for payment of financial obligations. The issuer is resilient against adverse changes incircumstances, economic conditions and/or operating environments.

A sukuk rated A has adequate safety for payment of financial obligations. The issuer is more susceptible to adversechanges in circumstances, economic conditions and/or operating environments than those in higher-rated categories.

A sukuk rated BBB has moderate safety for payment of financial obligations. The issuer is more likely to be weakened byadverse changes in circumstances, economic conditions and/or operating environments than those in higher-rated

categories. This is the lowest investment-grade category.

A sukuk rated BB has low safety for payment of financial obligations. The issuer is highly vulnerable to adverse changesin circumstances, economic conditions and/oroperating environments.

A sukuk rated B has very low safety for payment of financial obligations. The issuer has a limited ability to withstandadverse changes in circumstances, economic conditions and/oroperating environments.

A sukuk rated C has a high likelihood of default. The issuer is highly dependent on favourable changes in circumstances,economic conditions and/or operating environments, the lack of which would likely result in it defaulting on a particular

sukuk.

A sukuk rated D is either currently in default or faces imminent default on its financial obligations, whether or not formallydeclared. The D rating may also reflect a distressed exchange, the filing of bankruptcy and/or other actions pertaining to

the issuer that could jeopardise thepayment of a particular sukuk.

A sukuk rated P1 has high safety for payment of financial obligations in the short term. This is the highest short-termIssue Rating assigned by RAM Ratings to a debt-based sukuk.

A sukuk rated P2 has adequate safety for payment of financial obligations in the short term. The issuer is moresusceptible to the effects of deteriorating circumstances than those in the highest-rated category.

A sukuk rated P3 has moderate safety for payment of financial obligations in the short term. The issuer is more likely tobe weakened by the effects of deteriorating circumstances than those in higher-rated categories. This is the lowest

investment-grade category.

A sukuk rated NP has doubtful safety for payment of financial obligations in the short term. The issuer faces majoruncertainties that could compromise its capacity for payment of a particularsukuk.

A sukuk rated D is either currently in default or faces imminent default on its financial obligations, whether or not formallydeclared. The D rating may also reflect a distressed exchange, the filing of bankruptcy and/or other actions pertaining to

the issuer that could jeopardise thepayment of a particular sukuk.

For long-term ratings, RAM Ratings applies subscripts 1, 2 or 3 in each rating category from AA to C. The subscript 1 indicates that theissue ranks at the higher end of its generic rating category; the subscript 2 indicates a mid-ranking; and the subscript 3 indicates that the

issue ranks at the lower end of its generic rating category. In addition, RAM Ratings applies the suffixes (bg) or (s) to ratings which havebeen enhanced by a bank guarantee or other supports, respectively.

An Issue Rating for a debt-based sukuk is RAM Ratings' current opinion on the creditworthiness of a particular debt-basedsukuk. It reflects the overall capacity and willingness of an issuer to meet the financial obligations on a particular debt-based sukuk on a full and timely basis, taking into account its expressed terms and conditions. RAM Ratings’ sukuk ratingsare, however, not a measure of compliance with Shariah principles or the role, formation, practices, legitimacy andsoundness of the Shariah advisors’ recommendations and decisions.

Malayan Banking Berhad Cekap Mentari Berhad

16

RAM Ratings receives compensation for its rating services, normally paid by the issuers of such securities or the rated entity, and sometimes

third parties participating in marketing the securities, insurers, guarantors, other obligors, underwriters, etc. The receipt of this compensation has

no influence on RAM Ratings’ credit opinions or other analytical processes. In all instances, RAM Ratings is committed to preserving the

objectivity, integrity and independence of its ratings. Rating fees are communicated to clients prior to the issuance of rating opinions. While RAM

Ratings reserves the right to disseminate the ratings, it receives no payment for doing so, except for subscriptions to its publications.

RAM Ratings, its rating committee members and the analysts involved in the rating exercise have not encountered and/or are not aware of any

conflict of interest relating to the rating exercise. RAM Ratings will adequately disclose all related information in the report if there are such

instances.

Published by RAM Rating Services Berhad

Reproduction or transmission in any form is prohibited except by

permission from RAM Ratings.

Copyright 2011 by RAM Ratings

RAM Rating Services Berhad

Suite 20.01, Level 20

The Gardens South Tower

Mid Valley City, Lingkaran Syed Putra

59200 Kuala Lumpur

Tel: (603) 7628 1000 / (603) 2299 1000 Fax: (603) 7620 8251

E-mail: [email protected] Website: http://www.ram.com.my