Major revenue and expenditure trends for counties and municipalities. G.R.E.A.T. “T EMPLATE ”

29

Major revenue and expenditure trends for counties and municipalities. G.R.E.A.T. “TEMPLATE”

-

Upload

jayson-sherman-kennedy -

Category

Documents

-

view

215 -

download

2

Transcript of Major revenue and expenditure trends for counties and municipalities. G.R.E.A.T. “T EMPLATE ”

Major revenue and expenditure trends for counties and municipalities.

G.R.E.A.T. “TEMPLATE”

Focus on 4 Key Areas:

ExpendituresRevenues

TaxesTax Base

KEY OBSERVATIONS

• To what extent is your community’s spending similar/different to the average?

• To what extent does spending shift over time?

TRENDING G.R.E.A.T. DATA OVER TIME

A couple of points to consider:

1. What are basic/external factors that should be considered to account for when trending data?1. Population2. Inflation

2. What is the timeframe you want to trend?1. Use all GREAT data?2. Since 2000?

3. Any issues with the data analyzed?1. GREAT data include capital; possibly use sub-totals

that exclude capital

Two Sets of Data

• Comparisons of counties and municipalities

• Example of a template for the city of Titanville

Spending distribution

• Years 1987, 1998 and 2009 (most current)

• The key observation for the following four bar charts is the consistency in relative spending by service.

Half of city general purpose spending is on three services: administration, protective services (police, fire and ambulatory) and, roads and transportation

Town spending (see below) is dominated by roads, debt service and protective services (largely fire prevention)

Village spending is comparable to cities. Unlike other forms of local government, debt service is becoming a larger share of spending. Debt service accounted for 16 percent of spending in 1987 and was 24 percent in 2009.

Counties are largely responsible for the provision of social services; other major expenses are for protective services and administration.

Proportions of Real Per Capita Revenue: 1987, 1998 and 2009.

The “story” in each of these bar charts is the growth in reliance on property

taxes in place of shared revenues.

In 1987, property taxes accounted for 32 percent of revenues and in 2009 the proportion rose to 36 percent. Conversely, Shared Revenues as a share of total GF revenues dropped from 7 percent to 3 percent.

The levy share for cities was 27 percent in 1987 and 34 percent in 2009. Shared Revenues for cities fell from 23 percent in 1987 to 10 percent in 2009.

Reliance on levies increased 5 percentage points over these 22 years; at the same time, Shared Revenues dropped 12 percentage points.

For villages: the story is the same, less reliance on Shared Revenues (from 17 percent in 1987 to 6 percent in 2009) and increased reliance on property taxes (from 23 percent to 29 percent).

Tax Base

• The following pie charts break out property by valuation class: residential, commercial, manufacturing, personal property and agriculture.

• Trends in tax base help explain the distribution of property taxes, thus if a community's residential tax base is growing at a rate higher than manufacturing and/or commercial, home owners will be paying more of the tax burden.

• The data are broken out into two sets of pie charts, property class as a percentage in 2000 and 2009.

Villages: on average, the distribution of tax base shifted by only a couple of percentage points. Manufacturing’s share dropped from 7 percent in 2000 to 5 percent in 2009. Conversely, residential property increased from 71 percent to 73 percent.

Towns: interestingly, agricultural land decreased as a proportion of total valuation from 5 percent in 2000 to 1 percent in 2009. Residential value jumped from 77 percent to 83 percent.

For cities, there was little change in the relative distribution of property valuation by class

Similar to cities, the distribution of property by class for counties changed little between 2000 and 2009.

Titanville Template

$-

$200.00

$400.00

$600.00

$800.00

$1,000.00

$1,200.00

$1,400.00

$1,600.00

$1,800.00

TITANVILLE AVERAGE

19871989

19911993

19951997

19992001

20032005

20072009

$-

$20.00

$40.00

$60.00

$80.00

$100.00

$120.00

$140.00

$160.00

TITANVILLE

AVERAGE

19871989

19911993

19951997

19992001

20032005

20072009

$-

$50.00

$100.00

$150.00

$200.00

$250.00

$300.00

$350.00

$400.00

$450.00

TITANVILLEAVERAGE

$-

$50.00

$100.00

$150.00

$200.00

$250.00

$300.00

$350.00

TITANVILLEAVERAGE

General Operating and Capital Expenses

General Government

Law Enforcement

Fire Prevention

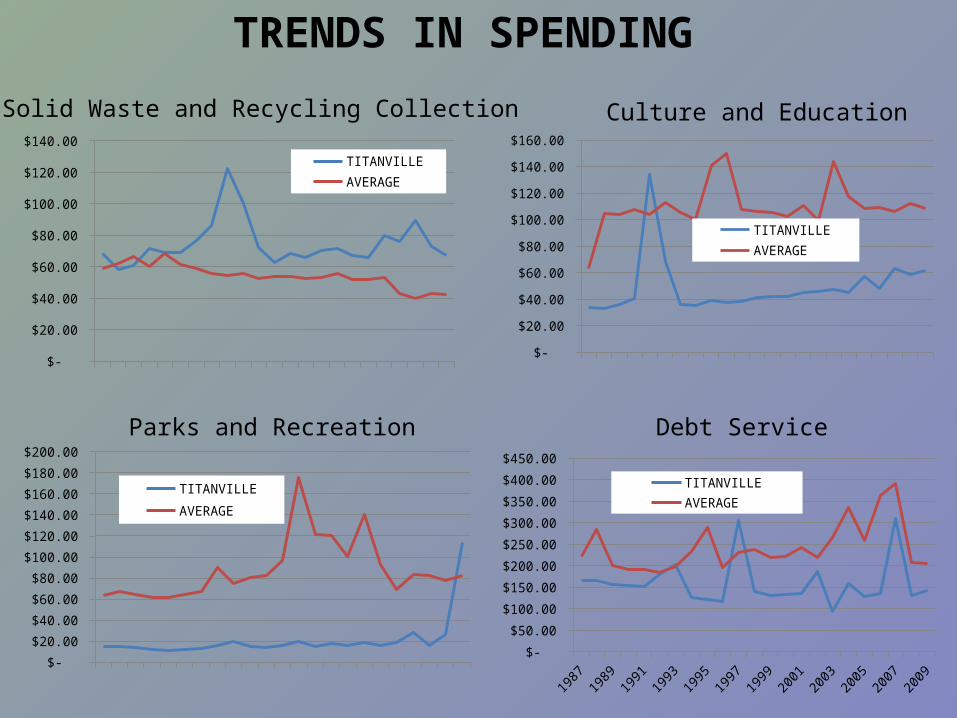

TRENDS IN SPENDING

$-

$20.00

$40.00

$60.00

$80.00

$100.00

$120.00

$140.00

TITANVILLEAVERAGE

$-

$20.00

$40.00

$60.00

$80.00

$100.00

$120.00

$140.00

$160.00

$180.00

$200.00

TITANVILLE

AVERAGE

$-

$20.00

$40.00

$60.00

$80.00

$100.00

$120.00

$140.00

$160.00

TITANVILLEAVERAGE

19871989

19911993

19951997

19992001

20032005

20072009

$-

$50.00

$100.00

$150.00

$200.00

$250.00

$300.00

$350.00

$400.00

$450.00

TITANVILLE AVERAGE

TRENDS IN SPENDING

Solid Waste and Recycling Collection Culture and Education

Parks and Recreation Debt Service

DISTRIBUTION OF REVENUES

REAL PER CAPITA REVENUES

19871988

19891990

19911992

19931994

19951996

19971998

19992000

20012002

20032004

20052006

20072008

2009 $-

$200.00

$400.00

$600.00

$800.00

$1,000.00

$1,200.00

$1,400.00

$1,600.00

$1,800.00

TITANVILLE AVERAGE

Total General Revenue

REAL PER CAPITA REVENUES

19871989

19911993

19951997

19992001

20032005

20072009

$-

$100.00

$200.00

$300.00

$400.00

$500.00

$600.00

$700.00

$800.00

$900.00

TITANVILLE

AVERAGE

19871989

19911993

19951997

19992001

20032005

20072009

$-

$100.00

$200.00

$300.00

$400.00

$500.00

$600.00

TITANVILLE

AVERAGE

Municipal Property Tax Total Intergovernmental Aid

19871989

19911993

19951997

19992001

20032005

20072009

$-

$50.00

$100.00

$150.00

$200.00

$250.00

$300.00

$350.00

TITANVILLE AVERAGE

19871989

19911993

19951997

19992001

20032005

20072009

$-

$20.00

$40.00

$60.00

$80.00

$100.00

$120.00

$140.00

$160.00

$180.00 TITANVILLE

AVERAGE

State Shared RevenuesCharges for Services

DISTRIBUTION OF LEVIES BY SOURCE

PROPERTY VALUATION BY CLASS

In Conclusion

• Historical trends provide means by which to put current and future budgeting discussions in context

• You have access to statewide trends by municipal type and county; and group comparisons

• Importance of “controlling” for environmental factors such as population and inflation

• THE story over the past 22 years is: spending patterns are remarkably stable; revenues are shifting away from decreasing state aids

• Changes in distribution of tax base may help explain shifts in property tax burdens