MAHiNDRA & MAHiNDRA FiNANciAL SeRViceS LiMiteD Notice

384

1 NOTICE MAHINDRA & MAHINDRA FINANCIAL SERVICES LIMITED Registered Office: Gateway Building, Apollo Bunder, Mumbai - 400 001. Corporate Office: Mahindra Towers, ‘A’ Wing, 4th Floor, Worli, Mumbai – 400 018. Corporate Identity Number: L65921MH1991PLC059642 Tel: +91 22 66526000 | Fax: +91 22 24984170 Website: www.mahindrafinance.com | Email: [email protected] THE THIRTIETH ANNUAL GENERAL MEETING OF MAHINDRA & MAHINDRA FINANCIAL SERVICES LIMITED will be held on Monday, the 10th day of August, 2020, at 3.00 p.m. (IST), through Video Conferencing (“VC”) / Other Audio Visual Means (“OAVM”) facility to transact the business mentioned below. The proceedings of the Annual General Meeting (“AGM”) shall be deemed to be conducted at the Registered Office of the Company at Gateway Building, Apollo Bunder, Mumbai - 400 001 which shall be the deemed venue of the AGM. ORDINARY BUSINESS 1. To receive, consider and adopt the Audited Standalone Financial Statements of the Company for the Financial Year ended 31st March, 2020 together with the Reports of the Board of Directors and Auditors thereon. 2. To receive, consider and adopt the Audited Consolidated Financial Statements of the Company for the Financial Year ended 31st March, 2020 together with the Report of the Auditors thereon. 3. To appoint a Director in place of Mr. V. S. Parthasarathy (DIN: 00125299), who retires by rotation and, being eligible, offers himself for re-appointment. SPECIAL BUSINESS 4. Increase in borrowing limits from Rs. 80,000 Crores to Rs. 90,000 Crores under Section 180(1)(c) of the Companies Act, 2013 (“the Act”) and creation of charge on the assets of the Company under Section 180(1)(a) of the Act To consider and, if thought fit, to pass the following Resolution as a Special Resolution: “RESOLVED that in supersession of the Special Resolution passed by the Shareholders at the 29th Annual General Meeting of the Company held on 23rd July, 2019 and pursuant to the provisions of Section 180(1)(a), 180(1)(c) and all other applicable provisions of the Companies Act, 2013 read with such Rules as may be applicable (including any statutory modification(s) or amendment(s) thereto or re-enactment thereof for the time being in force) and in terms of the Memorandum and Articles of Association of the Company, approval of the Members of the Company be and is hereby accorded to the Board of Directors of the Company (hereinafter referred to as “the Board” which term shall be deemed to include any Committee thereof which the Board may have constituted or hereinafter constitute to exercise its powers including the powers conferred by this Resolution) to borrow moneys from time to time and, if it thinks fit, for creation of such mortgage, charge and/or hypothecation as may be necessary, in addition to the existing charges, mortgages and hypothecations, if any, created by the Company, on such of the assets of the Company, both present and future, and/or on the whole or substantially the whole of the undertaking or the undertakings of the Company, in such manner as the Board may direct, in favour of financial institutions, investment institutions, banks, insurance companies, mutual funds, trusts, other bodies corporate or any other person(s) (hereinafter referred to as the “Lending Agencies”) and Trustees for the holders of debentures/bonds and/or other instruments which may be issued on private placement basis or otherwise, to secure rupee term loans/ foreign currency loans, debentures, bonds and other instruments, including but not restricted to securing those facilities which have already been sanctioned, including any enhancement therein, even though the moneys to be borrowed together

Transcript of MAHiNDRA & MAHiNDRA FiNANciAL SeRViceS LiMiteD Notice

1

Notice

MAHiNDRA & MAHiNDRA FiNANciAL SeRViceS LiMiteDRegistered office: Gateway Building, Apollo Bunder, Mumbai - 400 001.

corporate office: Mahindra Towers, ‘A’ Wing, 4th Floor, Worli, Mumbai – 400 018.

corporate identity Number: L65921MH1991PLC059642

tel: +91 22 66526000 | Fax: +91 22 24984170

Website: www.mahindrafinance.com | email: [email protected]

tHe tHiRtietH ANNUAL GeNeRAL MeetiNG oF

MAHiNDRA & MAHiNDRA FiNANciAL SeRViceS

LiMiteD will be held on Monday, the 10th day

of August, 2020, at 3.00 p.m. (iSt), through

Video conferencing (“Vc”) / other Audio Visual

Means (“oAVM”) facility to transact the business

mentioned below.

The proceedings of the Annual General Meeting (“AGM”)

shall be deemed to be conducted at the Registered

Office of the Company at Gateway Building, Apollo

Bunder, Mumbai - 400 001 which shall be the deemed

venue of the AGM.

oRDiNARY BUSiNeSS1. To receive, consider and adopt the Audited

Standalone Financial Statements of the Company

for the Financial Year ended 31st March, 2020

together with the Reports of the Board of

Directors and Auditors thereon.

2. To receive, consider and adopt the Audited

Consolidated Financial Statements of the Company

for the Financial Year ended 31st March, 2020

together with the Report of the Auditors thereon.

3. To appoint a Director in place of Mr. V. S.

Parthasarathy (DIN: 00125299), who retires

by rotation and, being eligible, offers himself for

re-appointment.

SPeciAL BUSiNeSS4. increase in borrowing limits from Rs. 80,000

crores to Rs. 90,000 crores under Section

180(1)(c) of the companies Act, 2013 (“the

Act”) and creation of charge on the assets of

the company under Section 180(1)(a) of the Act

to consider and, if thought fit, to pass the

following Resolution as a Special Resolution:

“ReSoLVeD that in supersession of the Special

Resolution passed by the Shareholders at the 29th

Annual General Meeting of the Company held on

23rd July, 2019 and pursuant to the provisions of

Section 180(1)(a), 180(1)(c) and all other applicable

provisions of the Companies Act, 2013 read

with such Rules as may be applicable (including

any statutory modification(s) or amendment(s)

thereto or re-enactment thereof for the time being

in force) and in terms of the Memorandum and

Articles of Association of the Company, approval

of the Members of the Company be and is hereby

accorded to the Board of Directors of the Company

(hereinafter referred to as “the Board” which

term shall be deemed to include any Committee

thereof which the Board may have constituted

or hereinafter constitute to exercise its powers

including the powers conferred by this Resolution)

to borrow moneys from time to time and, if it

thinks fit, for creation of such mortgage, charge

and/or hypothecation as may be necessary, in

addition to the existing charges, mortgages and

hypothecations, if any, created by the Company, on

such of the assets of the Company, both present

and future, and/or on the whole or substantially

the whole of the undertaking or the undertakings

of the Company, in such manner as the Board may

direct, in favour of financial institutions, investment

institutions, banks, insurance companies, mutual

funds, trusts, other bodies corporate or any

other person(s) (hereinafter referred to as the

“Lending Agencies”) and Trustees for the holders

of debentures/bonds and/or other instruments

which may be issued on private placement basis

or otherwise, to secure rupee term loans/

foreign currency loans, debentures, bonds and

other instruments, including but not restricted to

securing those facilities which have already been

sanctioned, including any enhancement therein,

even though the moneys to be borrowed together

2

Annual Report 2019-20

Notice

with the moneys already borrowed by the Company

may exceed at anytime, the aggregate of the

paid-up share capital, free reserves and securities

premium reserve of the Company, upto a limit of

an outstanding aggregate value of Rs. 90,000

Crores (apart from temporary loans obtained from

the Company’s Bankers in the ordinary course of

business), together with interest thereon at the

agreed rates, further interest, liquidated damages,

premium on pre-payment or on redemption, costs,

charges, expenses and all other moneys payable by

the Company to the Trustees under the Trust Deed

and to the Lending Agencies under their respective

Agreements/Loan Agreements/Debenture Trust

Deeds entered/to be entered into by the Company

in respect of the said borrowings.

FURtHeR ReSoLVeD that the Board be and is

hereby authorised and empowered to do all such

acts, deeds, matters and things, arrange, give

such directions as may be deemed necessary or

expedient, or settle the terms and conditions of

such instrument, securities, loan, debt instrument

as the case may be, on which all such moneys

as are borrowed, or to be borrowed, from time

to time, as to interest, repayment, security or

otherwise howsoever as it may think fit, and to

execute all such documents, instruments and

writings as may be required to give effect to this

Resolution and for matters connected therewith

or incidental thereto, including intimating the

concerned authorities or other regulatory bodies

and delegating all or any of the powers conferred

herein to any Committee of Directors or Officers

of the Company.”

Notes:

1. In view of the outbreak of COVID-19 pandemic, the

Ministry of Corporate Affairs (“MCA”) has vide its

General Circular No. 20/2020 dated 5th May,

2020 read together with General Circular Nos.

14/2020 & 17/2020 dated 8th April, 2020

and 13th April, 2020 respectively, (collectively

referred to as “MCA Circulars”) and Securities

and Exchange Board of India (“SEBI”) Circular No.

SEBI/HO/CFD/CMD1/CIR/P/2020/79 dated

12th May, 2020, permitted the holding of this

AGM through VC/OAVM, without the physical

presence of the Members at a common venue. In

compliance with the provisions of the Companies

Act, 2013 (“the Act”), SEBI (Listing Obligations

and Disclosure Requirements) Regulations,

2015 (“Listing Regulations”) and the MCA & SEBI

Circulars, the AGM of the Company is being held

through VC/OAVM, without the physical presence

of the Members at a common venue.

KFin Technologies Private Limited, Registrar &

Transfer Agents of the Company, (earlier known

as Karvy Fintech Private Limited) (“KFintech”) shall

be providing facility for voting through remote

e-voting, for participation in the AGM through VC/

OAVM facility and e-voting during the AGM. The

procedure for participating in the meeting through

VC/OAVM is explained at Note No.19 below.

2. In compliance with applicable provisions of

the Act read with the MCA and SEBI Circulars

and the Listing Regulations, the AGM of the

Company is being conducted through VC/

OAVM. In accordance with the Secretarial

Standard on General Meetings (“SS-2”) issued

by the Institute of Company Secretaries of

India (“ICSI”) read with Clarification/Guidance

on applicability of Secretarial Standards - 1

and 2 dated 15th April, 2020 issued by the ICSI,

the proceedings of the AGM shall be deemed to be

conducted at the Registered Office of the Company

which shall be the deemed venue of the AGM. Since

the AGM will be held through VC/OAVM, the Route

Map is not annexed to this Notice.

3. A. The Explanatory Statement pursuant to

Section 102 of the Companies Act, 2013

setting out material facts in respect of the

business under Item No. 4 above is annexed

hereto. Further, the relevant details, pursuant

to Regulations 26(4) and 36(3) of the

Listing Regulations and Clause 1.2.5 of the

Secretarial Standard on General Meetings

3

Notice

("SS-2") by ICSI, with respect to Item No. 3 is

also annexed hereto.

The Board of Directors has considered and

decided to include the Item No. 4 given above

as Special Business in the forthcoming AGM,

as it is unavoidable in nature.

B. Messrs. B S R & Co. LLP, Chartered

Accountants, were appointed as Statutory

Auditors of the Company at the Twenty-

seventh AGM held on 24th July, 2017.

Pursuant to the Notification issued by the

Ministry of Corporate Affairs on 7th May,

2018 amending Section 139 of the Act and

the Rules framed thereunder, the mandatory

requirement for ratification of appointment

of Auditors by the Members at every AGM

has been omitted, and hence the Company

is not proposing an item on ratification of

appointment of Auditors at this AGM.

The Statutory Auditors have given a

confirmation to the effect that they are eligible

to continue with their appointment and that

they have not been disqualified in any manner

from continuing as Statutory Auditors.

The remuneration payable to the Statutory

Auditors shall be determined by the Board of

Directors based on the recommendation of

the Audit Committee.

4. PURSUANT TO THE PROVISIONS OF THE ACT, A

MEMBER ENTITLED TO ATTEND AND VOTE AT

THE AGM IS ENTITLED TO APPOINT A PROXY TO

ATTEND AND VOTE ON HIS/HER BEHALF AND

THE PROXY NEED NOT BE A MEMBER OF THE

COMPANY. SINCE THIS AGM IS BEING HELD

PURSUANT TO THE MCA AND SEBI CIRCULARS

THROUGH VC/OAVM, THE REQUIREMENT OF

PHYSICAL ATTENDANCE OF MEMBERS HAS BEEN

DISPENSED WITH. ACCORDINGLY, IN TERMS

OF THE MCA CIRCULARS, THE FACILITY FOR

APPOINTMENT OF PROXIES BY THE MEMBERS

WILL NOT BE AVAILABLE FOR THIS AGM AND

HENCE THE PROXY FORM AND ATTENDANCE SLIP

ARE NOT ANNEXED TO THIS NOTICE.

5. Corporate/Institutional Members are entitled to

appoint authorised representatives to attend the

AGM through VC/OAVM on their behalf and cast

their votes through remote e-voting or at the AGM.

Corporate/Institutional Members (i.e. other than

individuals/HUF, NRI, etc.) are required to send a

scanned copy of the Board Resolution/Authority

Letter, etc., authorising their representative

to attend the AGM through VC/OAVM on their

behalf and to vote through remote e-voting or

during the AGM.

The said Resolution/Authorisation shall be sent to

the Scrutinizer by email through its registered email

address to [email protected] with a copy

marked to [email protected] and to the Company

Members of the Company under the category

of Institutional Shareholders are encouraged to

attend and participate in the AGM through VC/

OAVM and vote thereat.

6. In view of the massive outbreak of the COVID-

19 pandemic, social distancing has to be

a pre-requisite.

Pursuant to the above mentioned MCA Circulars,

physical attendance of the Members is not

required at the AGM, and attendance of the

Members through VC/OAVM will be counted

for the purpose of reckoning the quorum under

Section 103 of the Act.

7. The Company’s Registrar and Transfer Agents for

its Share Registry Work (Physical and Electronic)

are M/s. KFin Technologies Private Limited

having their office at Selenium Building, Tower

B, Plot No. 31-32, Gachibowli, Financial District,

Nanakramguda, Ser i l ingampall y Mandal,

Hyderabad – 500 032.

4

Annual Report 2019-20

Notice

8. eLectRoNic DiSPAtcH oF Notice AND

ANNUAL RePoRt:

In line with the MCA General Circular dated 5th

May, 2020 and SEBI Circular dated 12th May,

2020, the Notice of the AGM alongwith the Annual

Report for the Financial Year 2019-2020 is being

sent only through electronic mode to those

Members whose email addresses are registered

with the Company/KFintech/ Depositories.

A copy of the Notice of this AGM alongwith the

Annual Report is available on the website of the

Company at www.mahindrafinance.com, websites

of the Stock Exchanges where the Equity Shares

of the Company are listed, viz. BSE Limited at

www.bseindia.com and the National Stock

Exchange of India Limited at www.nseindia.

com, respectively, and on the website of

KFintech at https://evoting.karvy.com. For any

communication, the Members may also send

a request to the Company’s investor email id:

[email protected]. The

Company will not be dispatching physical copies

of the Annual Report for the Financial Year

2019-2020 and the Notice of AGM to any Member.

9. tRANSFeR to iNVeStoR eDUcAtioN AND

PRotectioN FUND:

(i) Pursuant to Sections 124 and 125 of the

Companies Act, 2013, read with the Investor

Education and Protection Fund Authority

(Accounting, Audit, Transfer, and Refund)

Rules, 2016 (“the IEPF Rules”) notified by

the Ministry of Corporate Affairs with effect

from 7th September, 2016, as amended, all

unclaimed/unpaid dividend, application money,

debenture interest and interest on deposits

as well as principal amount of debentures

and deposits remaining unpaid or unclaimed

for a period of 7 years from the date they

became due for payment, are required to be

transferred to the Investor Education and

Protection Fund (“IEPF”) administered by the

Central Government.

Further, pursuant to Section 124 of the Act

read with the IEPF Rules all shares on which

dividend has not been paid or claimed for

seven consecutive years or more shall be

transferred to IEPF Authority as notified by

the Ministry of Corporate Affairs.

In accordance with the aforesaid IEPF

Rules, the Company has regularly sent

communication to all such shareholders whose

dividends are lying unpaid/unclaimed against

their name for seven consecutive years or

more and whose shares are due for transfer

to the IEPF Authority and has also published

notice(s) in leading newspapers in English and

regional language having wide circulation. The

Company has sent communications to the

Fixed Deposit holders informing them about

their unclaimed matured Fixed Deposits/

unclaimed interest accrued on the Deposits.

The details of such dividends/shares and

other unclaimed moneys to be transferred

to IEPF are uploaded on the website of

the Company at the web-link https://

mahindrafinance.com/investor-zone/

corporate-governance#Policies.

(ii) Due dates of transferring unclaimed and

unpaid dividends declared by the Company for

the Financial Year 2012-13 and thereafter to

the IEPF are as under:

Financial Year ended

Date of declaration of dividend

Last date for claiming unpaid/ unclaimed dividend

Proposed period for transfer of unclaimed dividend to iePF

31st March, 2013

25th July, 2013

24th August, 2020

25th August, 2020 to 23rd September, 2020

5

Notice

Financial Year ended

Date of declaration of dividend

Last date for claiming unpaid/ unclaimed dividend

Proposed period for transfer of unclaimed dividend to iePF

31st March, 2014

24th July, 2014

23rd August, 2021

24th August, 2021 to 22nd September, 2021

31st March, 2015

24th July, 2015

23rd August, 2022

24th August, 2022 to 22nd September, 2022

31st March, 2016

22nd July, 2016

21st August, 2023

22nd August, 2023 to 20th September, 2023

31st March, 2017

24th July, 2017

23rd August, 2024

24th August, 2024 to 22nd September, 2024

31st March, 2018

27th July, 2018

26th August, 2025

27th August, 2025 to 25th September, 2025

31st March, 2019

23rd July, 2019

22nd August, 2026

23rd August, 2026 to 21st September, 2026

The Company urges all the Members to encash/

claim their respective dividend during the

prescribed period. Members who have not

encashed the dividend warrants so far in respect

of the aforesaid period(s), are requested to make

their claim to KFin Technologies Private Limited

(“KFintech”) well in advance of the above due dates.

(iii) (a) transfer of Unclaimed Dividend:

The Company has transferred an amount

of Rs. 7,82,488 on 11th September, 2019

to the IEPF, being the unclaimed/unpaid

dividend for the Financial Year 2011-12.

The Company has paid to IEPF on 25th

July, 2019, an amount of Rs. 4,45,750.50

towards dividend for the financial year

ended 31st March, 2019 on such Shares

which were transferred to IEPF.

(b) transfer of Unclaimed Matured Fixed

Deposits and interest accrued thereon:

Deposits remaining unclaimed for a

period of seven years from the date

they became due for payment have to be

transferred to the IEPF established by the

Central Government.

During the Financial Year 2019-20, the

Company has transferred to the IEPF

an amount of Rs. 4,10,041 being the

unclaimed amount of matured Fixed

Deposits and Rs. 86,597 towards

unclaimed/unpaid interest accrued

on the Deposits.

(c) transfer of Shares:

Adhering to the various requirements

set out in the IEPF Rules, as amended,

the Company has during the Financial

Year 2019-20 transferred 1,480 Equity

Shares of the face value of Rs. 2 each

to the IEPF Authority in respect of

which dividend had remained unpaid or

unclaimed for seven consecutive years,

on 11th September, 2019.

(iv) Members/Inves tors whose shares,

unclaimed dividend, matured deposit(s),

matured debentures, application money

due for refund, or interest thereon, etc.,

has been transferred to the IEPF, may

claim the shares or apply for refund of the

unclaimed amounts as the case may be, to

the IEPF Authority, by making an electronic

application in e-Form IEPF-5 as detailed on

the website of the Ministry of Corporate

Affairs at the web-link: http://www.iepf.

gov.in/iePF/refund.html. The e-Form can

also be downloaded from the Company’s

website at www.mahindrafinance.com

under the “Investor Zone” Section. No claim

lies against the Company in respect of the

shares/unclaimed amounts so transferred.

6

Annual Report 2019-20

Notice

(v) Details of unclaimed amounts on the

company’s website:

Pursuant to the provisions of the Investor

Education and Protection Fund Authority

(Accounting, Audit, Transfer, and Refund)

Rules, 2016, the Company has uploaded

the details of unpaid and unclaimed

amounts lying with the Company as on 23rd

July, 2019 (date of the previous Annual

General Meeting of the Company) on the

website of the Company at the web-link:

https://mahindrafinance.com/investor-

zone/corporate-governance#Policies

as well as on the website of the Ministry

of Corporate Af fairs at the web- link:

http://www.iepf.gov.in/.

10. tRANSFeR oF SHAReS PeRMitteD iN

DeMAt FoRM oNLY:

As per Regulation 40 of the Listing Regulations,

as amended, securities of listed companies

can be transferred only in dematerialised form

with effect from 1st April, 2019, except in

case of request received for transmission or

transposition of securities.

In view of the above and to eliminate all risks

associated with physical shares and for ease of

portfolio management, Members holding shares in

physical form are requested to consider converting

their holdings to dematerialised form. Members

are accordingly requested to get in touch with any

Depository Participant having registration with SEBI

to open a Demat account or alternatively, contact

the nearest branch of KFintech to seek guidance

with respect to the demat procedure. Members may

also visit the website of depositories viz. National

Securities Depository Limited: https://nsdl.co.in/

faqs/faq.php or Central Depository Services (India)

Limited: https://www.cdslindia.com/investors/

open-demat.html for further understanding of

the demat procedure. Members may also refer to

Frequently Asked Questions (“FAQs”) on Company’s

website at the web-link: https://mahindrafinance.

com/investor-zone/faqs.

11. NoMiNAtioN:

Members can avail of the facility of nomination in

respect of shares held by them in physical form

pursuant to the provisions of Section 72 of the

Companies Act, 2013 read with Rule 19(1) of the

Companies (Share Capital and Debentures) Rules,

2014. Members desiring to avail of this facility

may send their nomination in the prescribed Form

No. SH-13 duly filled in to KFintech having their

office at Selenium, Tower B, Plot No. 31 & 32,

Gachibowli, Financial District, Nanakramguda,

Serilingampally Mandal, Hyderabad – 500 032

or send an email at: [email protected].

Members holding shares in electronic form may

contact their respective Depository Participants

for availing this facility.

If a Member desires to cancel the earlier nomination

and record fresh nomination, he/she may submit

the same in Form No. SH-14. Both the forms are

also available on the website of the Company at

the web-link: https://mahindrafinance.com/

investor-zone/faqs.

12. MeMBeRS ARe ReqUeSteD to:

a) intimate to the KFintech, changes, if any, in

their registered addresses/bank mandates

at an early date, in case of shares held

in physical form;

b) intimate to the respective Depository

Participant, changes, if any, in their registered

addresses/bank mandates at an early

date, in case of shares held in electronic/

dematerialized form;

c) quote their folio numbers/ Client ID and DP ID

in all correspondence;

d) consolidate their holdings into one folio in case

they hold shares under multiple folios in the

identical order of names; and

e) register their Permanent Account Number

(PAN) with their Depository Participants, in

7

Notice

case of Shares held in dematerialised form

and KFintech/Company, in case of Shares

held in physical form, as directed by SEBI.

13. UPDAtioN oF MeMBeRS’ DetAiLS:

The format of the Register of Members prescribed

by the Ministry of Corporate Affairs under the

Companies Act, 2013 requires the Company/

Registrar and Transfer Agents to record additional

details of Members, including their PAN details,

e-mail address, etc. A form for compiling additional

details is available on the Company’s website at the

web-link: https://mahindrafinance.com/investor-

zone/corporate-governance as also attached to

this Annual Report.

Members holding shares in physical form are

requested to submit the form duly completed

to the Company at investorhelpline_mmfsl@

mahindra.com or its Registrar and Transfer

Agents in physical mode, after normalcy is

restored, or in electronic mode at einward.ris@

kfintech.com as per instructions mentioned in

the form. Members holding shares in electronic

form are requested to submit the details to their

respective Depository Participants.

14. UPDAtioN oF PeRMANeNt AccoUNt NUMBeR

(PAN)/BANk AccoUNt DetAiLS oF MeMBeRS:

SEBI vide its Circular No. SEBI/HO/MIRSD/DOP1/

CIR/P/2018/73 dated 20th April, 2018 has

mandated registration of PAN and Bank Account

details for all security holders. Members holding

shares in physical form are therefore, requested

to submit their PAN and Bank Account details to

the Registrar and Share Transfer Agents along

with a self-attested copy of PAN Card and original

cancelled cheque. The original cancelled cheque

should bear the name of the Member. In the

alternative, Members are requested to submit a

copy of bank passbook/statement attested by the

bank. Members holding shares in demat form are

requested to submit the aforesaid information to

their respective Depository Participant(s).

15. Members seeking any information with regard to

the Accounts or any matter to be placed at the

AGM, are requested to write to the Company on

or before Friday, 7th August, 2020, through email

on [email protected]. The

same will be replied by the Company suitably.

16. PRoceDURe FoR iNSPectioN oF DocUMeNtS:

The Register of Directors and Key Managerial

Personnel and their shareholding maintained

under Section 170 of Companies Act, 2013 and

relevant documents referred to in this Notice of

AGM and Explanatory Statement, will be available

electronically for inspection by the Members

during the AGM. All documents referred to in

the Notice will also be available for electronic

inspection without any fee by the Members from

the date of circulation of this Notice up to the date

of AGM, i.e. 10th August, 2020. Members seeking

to inspect such documents can send an email to

Company’s investor email id: investorhelpline_

17. Members are requested to support the Green

Initiative by registering/ updating their e-mail

addresses, with the Depository Participant (in

case of Shares held in dematerialised form) or with

KFintech (in case of Shares held in physical form).

18. PRoceDURe FoR ReGiSteRiNG tHe eMAiL

ADDReSSeS to ReceiVe tHiS Notice

eLectRoNicALLY AND cASt VoteS

eLectRoNicALLY:

i. Those Members who have not yet registered

their email addresses are requested to get

their email addresses registered by following

the procedure given below:

a. Members holding shares in demat

form can get their email ID registered

by con tac t ing the i r respec t i ve

Depository Participant.

b. Members holding shares in physical

form may register their email address

8

Annual Report 2019-20

Notice

and mobile number with the Company’s

Registrar and Transfer Agents, KFin

Technologies Private Limited by sending

an email request at the email ID

[email protected] along with

signed scanned copy of the request

letter providing the email address, mobile

number, self-attested copy of the PAN

card and copy of the Share Certificate

for registering their email address

and receiving the AGM Notice and the

e-voting instructions.

ii. To facilitate Members to receive this Notice

electronically and cast their vote electronically,

the Company has made special arrangements

with Kfintech for temporary registration of

email addresses of the Members in terms of

the MCA Circulars.

Process to be followed for temporary

Registration of e-mail address:

A. the process for registration of email

address with kFintech for receiving

the Notice of AGM and login iD and

password for e-voting is as under:

i. Visit the link: https://ris.kfintech.

com/email_registration/

ii. Select the name of the Company

viz. Mahindra & Mahindra Financial

Services Limited and follow the steps

for registration of email address.

B. the process for registration of email

address with the company for receiving

the Notice of AGM and login iD and

password for e-voting is as under:

Members are requested to v isi t

the website of the Company www.

mahindrafinance.com and click on “click

here for temporary registration of

email-id of Members for AGM 2019-20”

and follow the registration process as

mentioned on the landing page.

iii. After successful submission of the email

address, KFintech will email a copy of

this AGM Notice and Annual Report for

F.Y. 2019-20 along with the e-voting user

ID and password. In case of any queries,

Members are requested to write to kFintech

iV. Those Members who have already registered

their email addresses are requested to keep

their email addresses validated/updated

with their DPs/KFintech to enable servicing

of notices/documents/Annual Reports and

other communications electronically to their

email address in future.

19. iNStRUctioNS FoR MeMBeRS FoR AtteNDiNG

tHe AGM tHRoUGH Vc/oAVM:

i. ATTENDING THE AGM: Members will be

provided with a facility to attend the AGM

through video conferencing platform provided

by KFintech. Members are requested to

login at https://emeetings.kfintech.com

and click on the “Video conference” tab

to join the Meeting by using the remote

e-voting credentials.

ii. Please note that Members who do not have

the User ID and Password for e-voting or have

forgotten the User ID and Password may

retrieve the same by following the instructions

provided in Note No. 20.

iii. Members may join the Meeting through

Laptops, Smartphones, Tablets and Pads

for better experience. Further, Members

will be required to use Internet with a good

speed to avoid any disturbance during the

Meeting. Members will need the latest version

of Chrome, Safari, Internet Explorer 11, MS

Edge or Firefox. Please note that participants

connecting from Mobile Devices or Tablets

or through Laptops connecting via mobile

9

Notice

hotspot may experience Audio/Video loss due

to fluctuation in their respective network. It is

therefore recommended to use stable Wi-Fi

or LAN connection to mitigate any glitches.

Members are encouraged to join the Meeting

through Laptops with latest version of Google

Chrome for better experience.

iv. Members can join the AGM in the VC/OAVM

mode 15 minutes before the scheduled time

of the commencement of the Meeting by

following the procedure mentioned at Note

No. 19 (i) above in the Notice, and this mode

will be available throughout the proceedings

of the AGM. The facility of participation at the

AGM through VC/OAVM will be made available

to atleast 1,000 Members on a first come

first served basis as per the MCA Circulars.

v. In case of any query and/or help, in

respect of attending the AGM through

VC/OAVM mode, Members may refer

the Help & Frequently Asked questions

(“FAqs”) and “AGM Vc/oAVM” user

manual available at the download Section

of https://evoting.karvy.com or contact at

Mr. Suresh Babu D., Deputy Manager – RiS,

KFin Technologies Private Limited at Selenium,

Tower B, Plot No. 31-32, Gachibowli, Financial

District, Nanakramguda, Serilingampally

Mandal, Hyderabad, Telangana – 500 032 or

at the email ID: [email protected] or on

Phone No.: 040-6716 2222 or call Toll

Free No.: 1800-345-4001 for any further

clarifications.

20. PRoceDURe FoR ReMote e-VotiNG

In compliance with the provisions of Section 108

of the Act read with Rule 20 of the Companies

(Management and Administration) Rules, 2014,

as amended and the provisions of Regulation 44

of the Listing Regulations, Members are provided

with the facility to cast their vote electronically,

through the e-voting services provided by KFintech

on all Resolutions set forth in this Notice, through

remote e-voting. It is hereby clarified that it is not

mandatory for a Member to vote using the remote

e-voting facility.

The remote e-voting facility will be available during

the following period:

Day, date and time of Commencement of remote e-voting

From: Thursday, 6th August, 2020 at 9.00 a.m. (IST)

Day, date and time of end of remote e-voting beyond which remote e-voting will not be allowed

To: Sunday, 9th August, 2020 at 5.00 p.m. (IST)

The remote e-voting will not be allowed beyond the

aforesaid date and time and the e-voting module

shall be disabled by KFintech upon expiry of the

aforesaid period.

The remote e-voting module shall be disabled for

voting thereafter. Once the vote on a resolution(s)

is cast by the Member, the Member shall not be

allowed to change it subsequently.

A Member may avail of the facility at his/her/its

discretion, as per the instructions provided herein:

instructions:

a. Member will receive an e-mail from KFintech

[for Members whose e-mail IDs are registered

with the Company/Depository Participant(s)]

which includes details of E-Voting Event

Number (“EVEN”), USER ID and password:

i. Launch internet browser by typing the

URL: https://evoting.karvy.com.

ii. Enter the login credentials (i.e. User ID

and password). In case of physical folio,

User ID will be EVEN (e-voting Event

Number) xxxx followed by folio number.

In case of Demat account, User ID will be

your DP ID and Client ID. However, if you

10

Annual Report 2019-20

Notice

are already registered with KFintech for

e-voting, you can use your existing User

ID and password for casting your vote.

iii. After entering these details appropriately,

click on “LOGIN”.

iv. You will now reach password change

Menu wherein you are required to

mandatorily change your password. The

new password shall comprise minimum 8

characters with at least one upper case

(A-Z), one lower case (a-z), one numeric

(0-9) and a special character (@,#,$,etc.).

The system will prompt you to change

your password and update your contact

details like mobile number, email ID, etc.,

on first login. You may also enter a secret

question and answer of your choice to

retrieve your password in case you forget

it. It is strongly recommended that you do

not share your password with any other

person and that you take utmost care to

keep your password confidential.

v. You need to login again with the

new credentials.

vi. On successful login, the system will prompt

you to select the EVEN for Mahindra &

Mahindra Financial Services Limited.

vii. On the voting page, enter the number of

shares (which represents the number of

votes) as on the cut-off date i.e. Monday,

3rd August, 2020 under “FOR/ AGAINST”

or alternatively, you may partially enter

any number in “FOR” and partially in

“AGAINST” but the total number in “FOR/

AGAINST” taken together should not

exceed your total shareholding as on

the cut-off date.

Pursuant to Clause 16.5.3(e) of

Secretarial Standard on General

Meetings ("SS-2") issued by the Council

of the Institute of Company Secretaries

of India and approved by the Central

Government, in case a Member abstains

from voting on a Resolution i.e., the

Member neither assents nor dissents to

the Resolution, then his/her/ its vote will

be treated as an invalid vote with respect

to that Resolution.

viii. Members holding mult iple folios/

demat accounts shall choose the voting

process separately for each of the folios/

demat accounts.

ix. Voting has to be done for each item of

the Notice separately. In case you do not

desire to cast your vote on any specific

item, it will be treated as abstained.

x. You may then cast your vote by selecting an

appropriate option and click on “Submit”.

xi. A confirmation box will be displayed.

Click “OK” to confirm else “CANCEL” to

modify. Once you confirm, you will not be

allowed to modify your vote. During the

voting period, Members can login any

number of times till they have voted on

the Resolution(s).

xii. Corporate/Inst i tut ional Members

(i.e. other than Individuals, HUF, NRIs,

etc.) are required to send scanned

certified true copy (PDF Format) of the

Board Resolution/Authority Letter,

etc., together with attested specimen

signature(s) of the duly authorized

representative(s), to the Scrutinizer at

e-mail ID: [email protected] with

a copy to [email protected] and

to the Company at investorhelpline_

[email protected]. They may also

upload the same in the e-voting module

in their login. The scanned image of the

above mentioned documents should

11

Notice

be in the naming format “Corporate

Name_EVENT NO”.

It should reach the Scrutiniser and the

Company by email not later than Saturday,

8th August, 2020 (5:00 p.m. IST). In case

if the authorized representative attends

the Meeting, the above mentioned

documents shall be submitted before the

commencement of AGM.

b. In case e-mail ID of a Member is not registered

with the Company/ Depository Participant(s),

then such Member is requested to register/

update their e-mail addresses with the

Depository Participant (in case of Shares held

in dematerialised form) and inform KFintech at

the email ID: [email protected] (in case

of Shares held in physical form):

i. Upon registration, Member will receive

an e-mail from KFintech which includes

details of E-Voting Event Number (EVEN),

USER ID and password.

ii. Please follow all steps from Note. No.

20 (a) (i) to (xii) above to cast your vote by

electronic means.

21. VotiNG DURiNG tHe AGM:

i. The procedure for remote e-voting during the

AGM is same as the instructions mentioned

for remote e-voting since the Meeting is being

held through VC/OAVM.

ii. The e-voting window shall be activated upon

instructions of the Chairman of the Meeting

during the AGM.

iii. E-voting during the AGM is integrated with the

VC platform and no separate login is required

for the same. The Members shall be guided

on the process during the AGM.

iv. Onl y those Members/Shareholders,

who will be present in the AGM through

VC/OAVM facility and have not cast their vote

on the Resolutions through remote e-voting

and are otherwise not barred from doing

so, shall be eligible to vote through e-voting

system in the AGM.

v. Members who have cast their vote by remote

e-voting prior to the AGM will also be eligible

to participate at the AGM but shall not be

entitled to cast their vote again.

22. GeNeRAL iNStRUctioNS/iNFoRMAtioN FoR

MeMBeRS FoR VotiNG oN tHe ReSoLUtioNS:

i. A Member can opt for only a single mode

of voting i.e. through remote e-voting or

e-voting at the AGM.

ii. The voting rights of Members shall be in

proportion to the paid-up value of their shares

in the Equity Share capital of the Company as

on the cut-off date i.e. Monday, 3rd August,

2020. Members are eligible to cast their

vote either through remote e-voting or in the

AGM only if they are holding Shares as on that

date. A person who is not a Member as on the

cut-off date is requested to treat this Notice

for information purposes only.

iii. In case a person has become a Member of

the Company after dispatch of AGM Notice

but on or before the cut-off date for E-Voting,

i.e. Monday, 3rd August, 2020, he/she/it

may obtain the User ID and Password in the

manner as mentioned below:

a. If the mobile number of the Member is

registered against Folio No./ DP ID Client ID,

the Member may send SMS:

MYEPWD<space> e-voting

Event Number + Folio No. or DP ID Client

ID to +91-9212993399

12

Annual Report 2019-20

Notice

example for NSDL:

MYEPWD<SPACE>IN12345612345678

example for cDSL:

MYEPWD<SPACE>1402345612345678

example for Physical:

MYEPWD<SPACE>XXXX1234567890

b. If e-mail address or mobile number of the

Member is registered against Folio No./

DP ID Client ID, then on the home page of

https://evoting.karvy.com, the Member

may click “Forgot Password” and enter

Folio No. or DP ID Client ID and PAN to

generate a password.

c. Member may call KFintech’s Toll free

number 1800-345-4001.

d. Member may send an e-mail request

to [email protected]. However,

KFintech shall endeavor to send User ID

and Password to those new Members

whose e-mail IDs are available.

iv. In case of any query pertaining to e-voting,

please visit Help & FAQs section and E-voting

User Manual available at the download section

of KFintech’s website https://evoting.karvy.

com or contact at investorhelpline_mmfsl@

mahindra.com or at [email protected]

or on Phone No. +91 40 6716 2222 or call

KFintech’s Toll Free No. 1800-345-4001, for

any further clarifications.

23. ScRUtiNizeR FoR e-VotiNG AND DecLARAtioN

oF ReSULtS:

Mr. S. N. Ananthasubramanian (Membership

No. 4206) or failing him, Ms. Malati Kumar

(Membership No. 15508) of M/s. S. N.

Ananthasubramanian & Co., Company Secretaries,

have been appointed as Scrutinizer to scrutinize

the e-voting process as well as e-voting during the

AGM, in a fair and transparent manner.

The Scrutinizer will, after the conclusion of the

e-voting at the Meeting, scrutinise the votes cast

at the Meeting and votes cast through remote

e-voting, make a consolidated Scrutinizer’s Report

and submit the same to the Chairman of the

Company or any other person of the Company

authorised by the Chairman, who shall countersign

the same. The Results shall be declared not

later than forty-eight hours from conclusion

of the Meeting.

The Results declared along with the consolidated

Scrutinizer’s Report shall be hosted on the website

of the Company at www.mahindrafinance.com

and on the website of KFintech at https://evoting.

karvy.com immediately after the Results are

declared and will simultaneously be forwarded

to BSE Limited and the National Stock Exchange

of India Limited, where Equity Shares of the

Company are listed.

The Resolutions shall be deemed to be passed on

the date of the Meeting, i.e. Monday, 10th August,

2020, subject to receipt of the requisite number

of votes in favour of the Resolutions.

24. SUBMiSSioN oF qUeStioNS / qUeRieS

PRioR to AGM:

a. Members desiring any additional information

or having any question or query pertaining to

the business to be transacted at the AGM

are requested to write from their registered

e-mail address, mentioning their name,

DP ID and Client ID number/folio number and

mobile number to the Company’s investor

email - id i.e. investorhelpline_mmfsl@

mahindra.com at least 48 hours before

the time fixed for the AGM i.e. by 3:00 p.m.

(IST) 8th August, 2020, so as to enable the

Management to keep the information ready.

The queries may be raised precisely and in

brief to enable the Company to answer the

same suitably depending on the availability of

time at the AGM.

13

Notice

b. Alternatively, Members holding shares

as on the cut-of f date may also visit

https://evoting.karvy.com and click on the

tab “Post Your Queries Here” to post their

queries/views/questions in the window

provided, by mentioning their name, demat

account number/folio number, email ID and

mobile number. The window shall be activated

during the remote e-voting period and shall be

closed 48 hours before the time fixed for the

AGM at 3:00 p.m. (IST) on 8th August, 2020.

c. Members can also post their questions during

AGM through the “Ask A question” tab, which

is available in the VC/OAVM Facility.

The Company will, at the AGM, endeavour

to address the queries received t i l l

3.00 p.m. (IST) on 8th August, 2020, from

those Members who have sent queries

from their registered email IDs. Please note

that Members’ questions will be answered

only if they continue to hold shares as on

the cut-off date.

25. SPeAkeR ReGiStRAtioN BeFoRe AGM:

Members of the Company, holding shares

as on t he cu t - o f f da t e i .e. Monday,

3rd August, 2020 and who would like to speak

or express their views or ask questions during

the AGM may register as speakers by visiting

https://emeetings.kfintech.com, and clicking

on “Speaker Registration” during the period

from Wednesday, 5th August, 2020 (9:00

a.m. IST) upto Friday, 7th August, 2020 (5:00

p.m. IST). Those Members who have registered

themselves as a speaker will only be allowed to

speak/express their views/ask questions during

the AGM. The Company reserves the right to

restrict the number of speakers depending on

the availability of time at the AGM.

26. Members can also provide their feedback on the

services provided by the Company and its Registrar

& Transfer Agents by filling the "Shareholders

Satisfaction Survey" form available on the website

of the Company at https://mahindrafinance.

com/investor-zone/investor-information. This

feedback will help the Company in enhancing

Shareholder Service Standards.

27. kPRiSM – MoBiLe SeRVice APPLicAtioN

BY kFiNtecH:

Members are requested to note that KFintech

has launched a mobile application – KPRISM and

a website https://kprism.kfintech.com for online

service to Shareholders.

Members can download the mobile application,

register themselves (one time) for availing host

of services viz., view of consolidated portfolio

serviced by KFintech, Dividend status, request for

change of address, change/update Bank Mandate.

Through the Mobile application, Members can

download Annual Reports, standard forms and

keep track of upcoming General Meetings and

dividend disbursements. The mobile application

is available for download from Android Play

Store. Members may alternatively visit the link

https://kprism.kfintech.com/app/ to download

the mobile application.

By order of the Board

Arnavaz M. Pardiwalla

Company Secretary

Registered office:

Gateway Building,

Apollo Bunder,

Mumbai – 400 001.

CIN: L65921MH1991PLC059642

Tel: +91 22 66526000/6156

Fax: +91 22 24984170

Email: [email protected]

Website : www.mahindrafinance.com

Place : Mumbai

Date : 20th June, 2020

14

Annual Report 2019-20

Notice

ADDitioNAL iNFoRMAtioN WitH ReSPect to iteM No. 3Details of Director(s) seeking re-appointment at the forthcoming Annual General Meeting

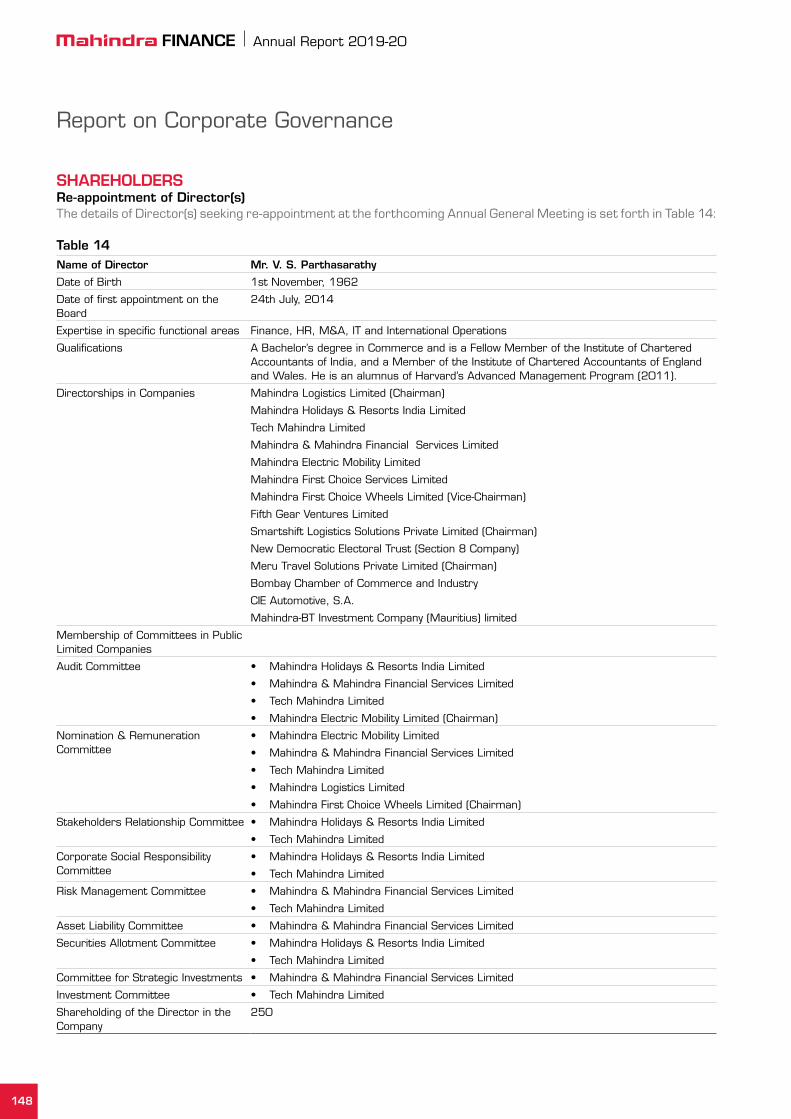

Mr. V. S. Parthasarathy, Non-Executive Non-Independent Director of the Company, retires by rotation

and, being eligible, has offered himself for re-appointment. Mr. V. S. Parthasarathy has confirmed that he

satisfies the criteria of ‘fit and proper’ as prescribed by the Reserve Bank of India vide Master Direction No.

DNBR.PD.008/03.10.119/2016-17 dated 1st September, 2016. Mr. V. S. Parthasarathy is not debarred

from holding the office of Director by virtue of any SEBI Order or any other such authority pursuant to circulars

dated 20th June, 2018 issued by BSE Limited and the National Stock Exchange of India Limited pertaining to

Enforcement of SEBI Orders regarding appointment of Directors by listed companies.

Information as required under Regulations 26(4) and 36(3) of the Securities and Exchange Board of India (Listing

Obligations and Disclosure Requirements) Regulations, 2015 and Clause 1.2.5 of the Secretarial Standard on

General Meetings ("SS-2") is given hereunder:

Name of Director Mr. V. S. ParthasarathyDIN 00125299Age 57 yearsDate of first appointment on the Board

24th July, 2014

Brief Resume,Qualification(s), Experienceand Nature of expertise in specific functional areas, Recognition or awards.

Mr. V. S. Parthasarathy is a much awarded professional, a thought leader and a votary of transformational changes with over 3 decades of experience.

With effect from 1st April, 2020, Mr. Parthasarathy was appointed as the President of the newly created Mobility Services Sector of the Mahindra Group. He is a member of the ‘Group Executive Board’ of the Mahindra Group.

Mr. V. S. Parthasarathy is the Chairman of Mahindra Logistics Limited, Smartshift Logistics Private Limited and a Director on Board of other listed companies of the Mahindra Group (including Tech Mahindra Limited, Mahindra Holidays and Resorts India Limited) and CIE Automotive S.A. Spain.

He is the President of BCCI (Bombay Chamber of Commerce & Industry) and Chairman of FICCI CFO Council.

Mr. Parthasarathy began his career with Modi Xerox as a Management Trainee. Before joining Mahindra & Mahindra Limited ("M&M") in 2000, he was the Associate Director at Xerox. Mr. Parthasarathy’s journey at M&M began with an HR stint where he brought about organisational transformation – performance management system, policy deployment, strategic planning – and journeyed through Deming Prize. He later spearheaded functions like Finance, M&A, IT and International Business, prior to being the Group CFO and the Group CIO at M&M until March 31, 2020. His areas of expertise include organisational transformation, leadership, strategic planning, finance, international operations, etc.

He is a well-recognised speaker in the fields of Finance and IT. He was awarded with the Lifetime Achievement awards for both his CFO and CIO roles. He is also the recipient of the BusinessWorld - Yes Bank Hall of Fame Award, Best CFO of India Award by IMA, Corporate Excellence Awards and Digital Icon of India Award by HPE.

15

Notice

Mr. Parthasarathy holds a Bachelor’s degree in Commerce and is a Fellow Member of the Institute of Chartered Accountants of India, and a Member of the Institute of Chartered Accountants of England and Wales. He is an alumnus of Harvard’s Advanced Management Program (2011).

Terms and conditions of appointment/ re-appointment

Liable to retire by rotation.

Details of remuneration sought to be paid

Not Applicable

Details of remuneration last drawn (F.Y. 2019-20)

Not Applicable

Shareholding in the Company

250 Equity Shares of Rs. 2 each. For other persons on a beneficial basis : Nil

Relationship with other Directors and Key Managerial Personnel

None of the Directors of the Company is inter-se related to each other or with the Key Managerial Personnel of the Company.

Number of Board Meetings attended during the Financial Year 2019-20

7 (out of 7 Meetings held)

Directorships held in other Companies

Mahindra Logistics Limited (Chairman)*

Mahindra Holidays & Resorts India Limited*

Tech Mahindra Limited*

Mahindra Electric Mobility LimitedMahindra First Choice Services LimitedMahindra First Choice Wheels Limited (Vice-Chairman)Fifth Gear Ventures Limited Smartshift Logistics Solutions Private Limited (Chairman)New Democratic Electoral Trust (Section 8 Company)Meru Travel Solutions Private Limited (Chairman)Bombay Chamber of Commerce and IndustryCIE Automotive, S.A.*

Mahindra-BT Investment Company (Mauritius) LimitedChairmanship/ Membership of Board Committees of other Companies

Mahindra Logistics Limited• Nomination and Remuneration Committee - Member

Mahindra electric Mobility Limited• Audit Committee - Chairman• Nomination and Remuneration Committee - Member

Mahindra Holidays & Resorts india Limited

• Audit Committee - Member• Stakeholders Relationship Committee - Member• Corporate Social Responsibility Committee - Member• Securities Allotment Committee - Member

tech Mahindra Limited

• Audit Committee - Member• Nomination and Remuneration Committee - Member• Stakeholders Relationship Committee - Member• Corporate Social Responsibility Committee - Member• Risk Management Committee - Member• Securities Allotment and Investment Committee - MemberMahindra First choice Wheels Limited

• Nomination and Remuneration Committee - Chairman*Listed entities

16

Annual Report 2019-20

Notice

explanatory Statement in respect of the Special

Business pursuant to Section 102 of the

companies Act, 2013

iteM No. 4

As per the provisions of Section 180(1) (c) of the

Companies Act, 2013, as amended, the Board of

Directors of the Company cannot borrow moneys in

excess of the amount of the paid-up share capital, free

reserves and securities premium reserve, (apart from

temporary loans obtained from the Company’s bankers

in the ordinary course of business), without the approval

of the Members, by way of a Special Resolution.

The Members by a Special Resolution passed at the

29th Annual General Meeting of the Company held

on 23rd July, 2019, had empowered the Board of

Directors of the Company to borrow moneys upto Rs.

80,000 Crores even though such borrowing would be

in excess of the paid-up share capital and free reserves

of the Company.

The moneys so borrowed by the Company and

outstanding as at 31st March, 2020 amounted to

Rs. 50,719.17 Crores. During the year 2019-20, the

estimated value of assets financed was Rs. 42,388.19

Crores and the Company plans to disburse over

Rs. 52,000 Crores during the current year, for

financing the Mahindra range of vehicles and tractors

and for other products like Cars, Commercial Vehicles,

Construction Equipment, Pre-owned Vehicles, etc.,

of reputed automobile manufacturers, for Invoice

Discounting, SME Financing, Personal Loans and

consumer durables.

In order to further expand its business and to

meet increased financial needs for the budgeted

disbursements, it is proposed to enhance the

borrowing limits of the Company to Rs. 90,000 Crores.

The Company may be required to secure some of the

borrowings by creating mortgage/charge on all or any

of the movable or immovable properties of the Company

in favour of the lender(s) in such form, manner and

ranking as may be determined by the Board of Directors

of the Company from time to time, in consultation with

the lender(s). In terms of Section 180(1)(a) of the Act

any proposal to sell, lease or otherwise dispose of the

whole, or substantially the whole of the undertaking of

the Company or where the Company owns more than

one undertaking, of the whole or substantially the whole

of any of such undertaking(s), requires the approval of

the Members by way of a Special Resolution.

Accordingly, the consent of the Members is being

sought for the enhancement of the borrowing limits

and to secure such borrowings by mortgage/charge

on any of the movable and/or immovable properties

and/or the whole or any part of the undertaking(s) of

the Company as set out in Resolution No. 4 appended

to this Notice.

The Memorandum and Articles of Association of the

Company are available for inspection by the Members

in electronic form as per the instructions provided in

Note No. 16 of this Notice.

The Board recommends the Special Resolution set out

at Item No. 4 of the Notice for approval of the Members.

None of the Directors, Key Managerial Personnel of the

Company and their relatives are in any way, concerned

or interested, financially or otherwise, in the Resolution

set out at Item No. 4 of the Notice except to the extent

of their shareholding interest, if any, in the Company.

By order of the Board

Arnavaz M. Pardiwalla

Company Secretary

Registered office:

Gateway Building,

Apollo Bunder,

Mumbai – 400 001.

CIN: L65921MH1991PLC059642

Tel: +91 22 66526000/6156

Fax: +91 22 24984170

Email: [email protected]

Website : www.mahindrafinance.com

Place : Mumbai

Date : 20th June, 2020

Mahindra & Mahindra Financial Services LimitedMahindra Towers, ‘A’ Wing, 4th Floor, Dr. G.M. Bhosale Marg,P. K. Kurne Chowk, Worli, Mumbai - 400 018CIN: L65921MH1991PLC059642www.mahindrafinance.com

Stock Exchange CodesNSE: M&MFINBSE: 532720Bloomberg: MMFS:IN

Annual Report 2019-20

Goodcompanies do.

Tough timesdon’t last.

Stea

df

ast

Mature Agile

Ready

Trans

pare

nt

Corporate Overview Introducing Mahindra Finance 2

Product Portfolio 4

Presence 6

Operational Highlights 7

Financial Highlights 8

Strategic Review Operating Environment 10

Value Creation Model 12

Strategic Priorities 14

The Secret of a Good Company Steadfast - Changing the financial landscape of rural India 18

Mature - A mature company with strong industry relationships 20

Agile - Staying light on our feet, lean and mean on strategy 22

Ready - Future-focused on the Power of One 24

Transparent - We do what we say, we mean what we say 26

People 28

Accountability and Growing Responsibly Corporate Social Responsibility 30

Environmental Impact 32

Awards and Accolades 34

Board of Directors 36

Summary of Results 37

COVID-19 Response 38

Corporate Information 39

Statutory Reports Board’s Report 40

Management Discussion and Analysis 115

Report on Corporate Governance 130

Financial StatementsStandalone Financials 165

Consolidated Financials 269

Form AOC-1 362

Contents

2019-20 key highlights

Total income

Rs. 10,245 crore 16% 12%

Asset under management

Rs. 77,160 crore

y-o-y growth

Tough times, they say, test one’s true character.For more than two-and-a-half decades, we have built a formidable ecosystem of semi-urban and rural financing by identifying key trends early, gathering deep local insight, making relevant investments, and steadily growing our footprint nationally.

FY 2019-20 tested the soundness of our business model, the wide arc of our foresight and the distance that we can travel with fortitude. During the year, we continued to stay close to our customers across the length and breadth of India, allayed their concerns with faster and empathetic response, crafted need-based solutions, and built on our rich culture of teamwork, transparency and ethical business practices. We also fostered new partnerships, accelerated our digital outreach, and continued to support vulnerable communities.

Concurrently, we rationalised our cost structure, made time-critical provisioning to tide over the crisis, enhanced our liquidity buffer and evolved a feasible business continuity plan. We are also exploring different avenues to bolster our Tier-1 capital base to offer diverse and innovative solutions to our customers and grow our scale.

We firmly believe semi-urban and rural India will drive India’s economic recovery with prospects of good monsoon and improved farm cashflow, going forward. The Government of India’s strong commitment to enhance rural income will also augur well for our business.

Our time-tested fundamentals, Group strength and the abiding trust of all our stakeholders will hold us in good stead - we believe in being SMART: Steadfast, Mature, Agile, Ready and Transparent. As we navigate the new normal, ever more confident and committed to creating lasting value.

4%

Book value per share

Rs. 184 Gained market share in many product lines, however in view of declining sales of vehicles and tractors, the disbursements have been lower

Assigned AAA by rating agencies (India Ratings, CARe Ratings, Brickwork and CRISIL)

Strong risk-focused practices in Asset Liability Management (ALM) and liquidity management

Introducing Mahindra Finance

A strong ecosystem of rural financing

The Mahindra Group is a federation of companies bound by one purpose - to Rise. For over seven decades, the Group has made many transformational changes, but remains grounded to its core purpose of challenging conventional thinking, and innovatively use resources to drive positive impact in the lives of its stakeholders and communities globally; and enable them to Rise.

Headquartered in Mumbai, the Group employs 2,50,000+ people across 100+ countries. It operates in key industries that propel economic growth, such as tractors, utility vehicles, information technology, financial services and vacation ownership. The Group has a strong presence in agribusiness, aerospace, components, consulting services, defence, energy, industrial equipment, logistics, real estate, retail, steel, commercial vehicles and two-wheelers.

Mahindra & Mahindra Financial Services Limited (Mahindra Finance or MMFSL) is one of the leading Non-Banking Finance Companies (NBFCs), with customers primarily in the rural and semi-urban markets of India. It belongs to the Mahindra Group, a global, innovation-led conglomerate, offering a wide range of products, services and possibilities to people worldwide.

For close to three decades since inception, Mahindra Finance is primarily engaged in financing new and pre-owned auto and utility vehicles, tractors, cars and commercial vehicles. It also provides housing finance, personal loans, financing to small and medium enterprises, insurance broking and mutual fund distribution services. MMFSL also offers wholesale inventory-financing to dealers and retail-financing to customers in the United States (USA) for the purchase of Mahindra Group products through Mahindra Finance USA LLC, its joint venture with a subsidiary of the Rabobank Group.

MMFSL benefits from its close relationships with dealers and its long-standing relationships with Original Equipment Manufacturers (OEMs), which allow it to provide on-site financing at dealerships. During the reporting year, it entered into a Joint Venture (JV) with Ideal Finance Limited (IFL), Sri Lanka. This JV will provide a diversified suite of financial products to the Sri Lankan market.

VisionTo be a leading financial services provider in semi-urban and rural India.

About Mahindra Group

Who we are

What we do

Rise tenets

MissionTo transform rural lives and drive positive change in the communities.

Core values• Professionalism • Good Corporate Citizenship • Customer First • Quality Focus • Dignity of the Individual

• Accepting No Limits• Alternative Thinking• Driving Positive Change

Core purposeWe will challenge conventional thinking and innovatively use all our resources to drive positive change in the lives of our stakeholders and communities across the world, to enable them to Rise.

Vehicle & Tractor Financing

Personal Loans

Housing Finance

SMe Financing

Insurance Broking

Mutual Funds

Investment Products

2

Annual Report 2019-20

Mahindra & Mahindra Limited

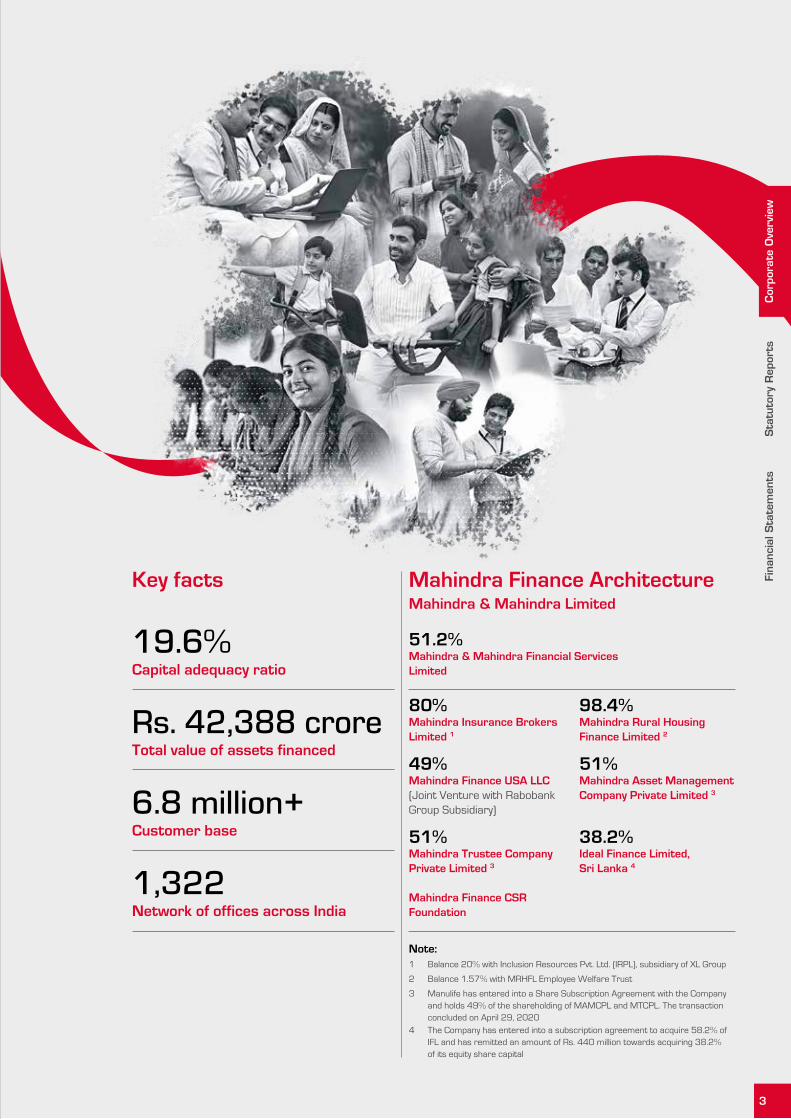

Note:

Mahindra Finance Architecture

Mahindra & Mahindra Financial Services Limited

51.2%

Key facts

Customer base

Capital adequacy ratio

Network of offices across India

6.8 million+

Total value of assets financedRs. 42,388 crore

19.6%

1,322

Mahindra Insurance Brokers Limited 1

Mahindra Asset Management Company Private Limited 3

Mahindra Rural Housing Finance Limited 2

Mahindra Trustee Company Private Limited 3

Mahindra Finance CSR Foundation

Mahindra Finance USA LLC (Joint Venture with Rabobank Group Subsidiary)

Ideal Finance Limited, Sri Lanka 4

80%

51%

98.4%

51%

49%

38.2%

1 Balance 20% with Inclusion Resources Pvt. Ltd. (IRPL), subsidiary of XL Group

2 Balance 1.57% with MRHFL Employee Welfare Trust

3 Manulife has entered into a Share Subscription Agreement with the Company and holds 49% of the shareholding of MAMCPL and MTCPL. The transaction concluded on April 29, 2020

4 The Company has entered into a subscription agreement to acquire 58.2% of IFL and has remitted an amount of Rs. 440 million towards acquiring 38.2% of its equity share capital

Cor

pora

te O

verv

iew

Sta

tuto

ry R

epor

tsFi

nanc

ial S

tate

men

ts

3

Product Portfolio

Thinking afresh and supporting aspirationsOur offerings include a wide range of financing, investment and insurance solutions. Product development is a key focus area for us. Through innovative products and solutions, we strive to fulfil the evolving needs of our customers in semi-urban and rural India.

Vehicle & Tractor Financing Mahindra Finance is primarily engaged in asset financing of vehicles, which are divided into five categories: (a) auto and utility vehicles, (b) tractors, (c) cars, (d) commercial vehicles and construction equipment and (e) pre-owned vehicles and others. The customers include transport operators, farmers, small businesses and self-employed and salaried individuals.

Personal LoansMahindra Finance provides personal loans primarily to its existing customers and Mahindra Group employees. Customers seek personal loans for weddings, children’s education, medical treatment or working capital for a small or medium-sized enterprise. These loans are typically repayable in monthly or quarterly instalments.

SMe FinancingMahindra Finance provides loans for varied purposes such as project finance, equipment finance, working capital finance, vehicle finance and bill discounting services to SMEs. The Company intends to leverage the existing customer base and the strengths of the Mahindra Group to target the auto ancillary, engineering and food and agri-processing sectors through our SME business.

Project Finance  Equipment Finance

Working Capital Finance

AUM of MSMe as on March 31, 2020

Rs. 2,723 crore

New contracts financed Increase in loan book7,57,463 6%

Competitive advantages  First choice for Mahindra

vehicles  Strong OEM tie-ups  Expanding network  Ability to offer customised

financing solutions  Handholding customers through

all stages of the project lifecycle

Efficient and technology-enabled delivery channel

Robust processes to deliver faster Turnaround Time (TAT)

Primary focus on the rural and semi-urban markets of India

Competitive advantages  Robust risk-management

framework  Use of artificial intelligence and

analytics

Proven ability to scale rapidly  Efficient and technology-enabled

delivery channel

Competitive advantages  Proven ability to support Small

and Medium-sized Enterprises (SMEs) through adverse cycles

Ability to offer differentiated and relevant solutions for varied customer needs

Robust risk management framework

Optimal usage of both traditional and non-traditional data to enhance credit delivery

4

Annual Report 2019-20

Insurance BrokingMahindra Finance provides insurance broking solutions to individuals and corporates through its subsidiary, Mahindra Insurance Brokers Ltd. (MIBL). MIBL has a ‘composite broking licence’ from the Insurance Regulatory and Development Authority of India, which allows MIBL to undertake broking of life, non-life and reinsurance products.

Housing FinanceMahindra Finance provides housing finance to individuals through its subsidiary, Mahindra Rural Housing Finance Limited (MRHFL), a registered housing finance company. MRHFL grants housing loans for purchase, construction, extension and renovation of property.

Mutual Fund SchemesMahindra Mutual Fund offers the rural and semi-urban India a secured means to move from simple saving instruments to investing in mutual funds. The Company’s distribution team provides end-to-end solutions for simple and safe ways to invest, including Equity Mutual Funds, Tax Saver Mutual Funds, Monthly Income Funds and other similar investment schemes.

Serviced insurance cases

Loan disbursements as on March 31, 2020

New customers

Assets Under Management (AUM) as on March 31, 2020

Percentage increase in distributors in 2019-20

~2.23 million

Rs. 1,876 crore 95,523

Rs. 4,771 crore

Flagship product Mahindra Loan Suraksha (MLS) cases registered

6,84,186

19%

Investments and Advisory  Fixed Deposits  Mutual Fund Distribution

Competitive advantages  Multi-channel distribution backed

by strong technology platform  Simple and innovative solutions

adding value to customers

Competitive advantages  Enriched offerings to attract

self-employed customers  Introduced door-to-door services

to ensure maximum convenience of customers

Streamlined processes to deliver faster sanctions and disbursement TAT to customers

Competitive advantages  Robust performance of the

Fund’s equity schemes  Diversified and ever-expanding

reach across distribution channels

Cor

pora

te O

verv

iew

Sta

tuto

ry R

epor

tsFi

nanc

ial S

tate

men

ts

5

Presence

Driving impact, deep and wide

Total number of villages 3,82,689

Lakshadweep

Madhya Pradesh

Maharashtra

Manipur

Meghalaya

Mizoram

Nagaland

Odisha

Puducherry

Punjab

Rajasthan

Sikkim

Tamil Nadu

Telangana

Tripura

Uttar Pradesh

Uttarakhand

West Bengal

19

20

20

21

21

22

22

23

23

24

24

25

25

26

26

27

27

28

28

29

29

30

30

31

31

32

32

33

33

34

34

35

35

36

36

Andaman & Nicobar Islands

Andhra Pradesh

Arunachal Pradesh

Assam

Bihar

Chandigarh

Chhattisgarh

Dadra & Nagar Haveli

Daman and Diu

Delhi

Goa

Gujarat

Haryana

Himachal Pradesh

Jammu and Kashmir

Jharkhand

Karnataka

Kerala

1

2

2

3

3

4

4

5

5

6

6

7

7

8

8

9

9

10

10

11

11

12

12

13

13

14

14

15

15

16

16

17

17

18

18

328

14,776

373

6,359

30,624

22

13,633

69

26

313

18

15,917

6,212

11,335

2,956

13,441

19,774

1,646

2

36,268

28,942

67

1,978

263

6

23,588

90

9,466

27,359

325

13,994

9,721

673

62,783

4,997

24,345

States/Union Territories Number of Villages Note: Numbers in the map above correspond to the name of the respective state in the table.

19

1

Zonal offices

Branches

Regional offices

8

1,322

36

We have presence across 3.83 lakh villages

6

Annual Report 2019-20

Operational Highlights

Number of employees engaged

2019-20

2018-19

2017-18

2016-17

2015-16

21,862

21,789

18,733

17,856

15,821

estimated Value of Assets Financed(Rs. in crore)

2019-20

2018-19

2017-18

2016-17

2015-16

42,388

46,210

37,773

31,659

26,706

Number of Contracts

2019-20

2018-19

2017-18

2016-17

2015-16

68,58,082

61,00,619

53,39,238

47,13,066

41,56,944

Progress made during the yearOpened more rural branches Mahindra Finance established new branches in rural areas to remain close to customers, to understand better their cash flows and to approach them for recovery when they have the money. These branches will seize new opportunities when the economic cycle and farm cycle improves.

Used analytics and Artificial Intelligence (AI)Mahindra Finance adopted the use of AI to understand the behavioural pattern of customers to offer better and more tailored products and services.

Internal customer programmes Internal customer programmes, coupled with growing reach helped Mahindra Finance build strong relationships with OEMs and dealerships.