Magic Quadrant for European Offshore Application Services · PDF fileMagic Quadrant for...

13

Magic Quadrant for European Offshore Application Services Gartner RAS Core Research Note G00161624, Ian Paul Marriott, Gianluca Tramacere, Allie Young, Helen Huntley, Partha Iyengar, Arup Roy, 20 November 2008 The Magic Quadrant for European Offshore Application Services positions companies involved in globally delivered application service initiatives and presents the current provider landscape. WHAT YOU NEED TO KNOW Please read “Findings: Recent Satyam Events and Their Impact on Published Gartner Magic Quadrants” for recent information about Satyam’s financial status that may impact the analysis contained in this Magic Quadrant. The Magic Quadrant for European Offshore Application Services analyzes the market for application services delivered in a global delivery model (GDM). The relative positioning of service providers in this year’s Magic Quadrant is based on factors that Gartner has determined to be most relevant to this market and model. For 2008, Gartner has again analyzed service providers of globally delivered (offshore) application services in two separate Gartner Magic Quadrants, one for North America and the other for Europe. Some providers appear on only one Magic Quadrant; other providers appear on both the North American and European Magic Quadrants. We believe that two reports are needed because we continue to see variances in these two markets regarding the maturity of the respective markets, buyer adoption levels and vendor competition levels. Therefore, although providers strive for globally common processes and methodologies, a provider’s placement may be different on one Magic Quadrant than on the other. In addition, as this market continues to evolve, future analysis may offer one global perspective versus regional perspectives, as we have done this year. Expertise in the global delivery of application services requires a combination of technical skills and competencies in the life cycle of application services (architecture, design, development and management) via a labor resource pool that is strategically located to offer clients holistic, integrated access to on-site, onshore, “nearshore” and offshore service delivery. A service provider’s GDM relies on processes, methodologies, and project and program management to effectively leverage geographically dispersed resources in performing core technical application service skills on behalf of clients. Additionally, a service provider’s sales and marketing strategies are essential to communicate to the marketplace; current and prospective clients must understand the unique skills and relationship approaches that differentiate a provider in a fast-evolving and hypercompetitive application service market. To assist application service buyers, Gartner developed the Magic Quadrant for European Offshore Application Services (see Figure 1). Application service buyers must assess which service providers bring the appropriate application competencies, global service locations, institutional and business cultures, and skill bases that meet their specific business and application service needs. Each year, we emphasize that buyers shouldn’t simply evaluate service providers that appear in the Leaders quadrant. All selection processes are enterprise- specific; consequently, providers positioned in each of the different quadrants — Leaders,

Transcript of Magic Quadrant for European Offshore Application Services · PDF fileMagic Quadrant for...

Magic Quadrant for European Offshore Application Services

Gartner RAS Core Research Note G00161624, Ian Paul Marriott, Gianluca Tramacere, Allie Young, Helen Huntley, Partha Iyengar, Arup Roy, 20 November 2008

The Magic Quadrant for European Offshore Application Services positions companies involved in globally delivered application service initiatives and presents the current provider landscape.

WHAT YOU NEED TO KNOWPlease read “Findings: Recent Satyam Events and Their Impact on Published Gartner Magic Quadrants” for recent information about Satyam’s financial status that may impact the analysis contained in this Magic Quadrant.

The Magic Quadrant for European Offshore Application Services analyzes the market for application services delivered in a global delivery model (GDM). The relative positioning of service providers in this year’s Magic Quadrant is based on factors that Gartner has determined to be most relevant to this market and model.

For 2008, Gartner has again analyzed service providers of globally delivered (offshore) application services in two separate Gartner Magic Quadrants, one for North America and the other for Europe. Some providers appear on only one Magic Quadrant; other providers appear on both the North American and European Magic Quadrants. We believe that two reports are needed because we continue to see variances in these two markets regarding the maturity of the respective markets, buyer adoption levels and vendor competition levels. Therefore, although providers strive for globally common processes and methodologies, a provider’s placement may be different on one Magic Quadrant than on the other. In addition, as this market continues to evolve, future analysis may offer one global perspective versus regional perspectives, as we have done this year. Expertise in the global delivery of application services requires a combination of technical skills and competencies in the life cycle of application services (architecture, design, development and management) via a labor resource pool that is strategically located to offer clients holistic, integrated access to on-site, onshore, “nearshore” and offshore service delivery. A service provider’s GDM relies on processes, methodologies, and project and program management to effectively leverage geographically dispersed resources in performing core technical application service skills on behalf of clients. Additionally, a service provider’s sales and marketing strategies are essential to communicate to the marketplace; current and prospective clients must understand the unique skills and relationship approaches that differentiate a provider in a fast-evolving and hypercompetitive application service market.

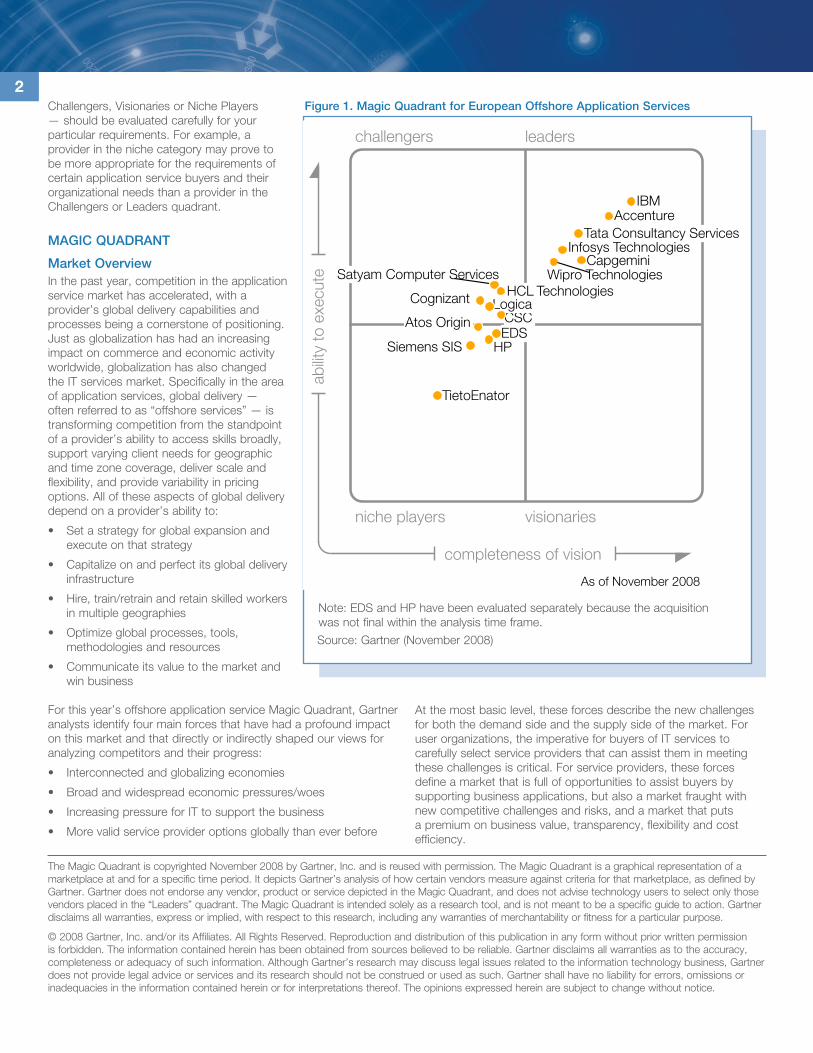

To assist application service buyers, Gartner developed the Magic Quadrant for European Offshore Application Services (see Figure 1). Application service buyers must assess which service providers bring the appropriate application competencies, global service locations, institutional and business cultures, and skill bases that meet their specific business and application service needs. Each year, we emphasize that buyers shouldn’t simply evaluate service providers that appear in the Leaders quadrant. All selection processes are enterprise-specific; consequently, providers positioned in each of the different quadrants — Leaders,

2Challengers, Visionaries or Niche Players — should be evaluated carefully for your particular requirements. For example, a provider in the niche category may prove to be more appropriate for the requirements of certain application service buyers and their organizational needs than a provider in the Challengers or Leaders quadrant.

MAGIC QUADRANT

Market OverviewIn the past year, competition in the application service market has accelerated, with a provider’s global delivery capabilities and processes being a cornerstone of positioning. Just as globalization has had an increasing impact on commerce and economic activity worldwide, globalization has also changed the IT services market. Specifically in the area of application services, global delivery — often referred to as “offshore services” — is transforming competition from the standpoint of a provider’s ability to access skills broadly, support varying client needs for geographic and time zone coverage, deliver scale and flexibility, and provide variability in pricing options. All of these aspects of global delivery depend on a provider’s ability to:

• Setastrategyforglobalexpansionandexecute on that strategy

• Capitalizeonandperfectitsglobaldeliveryinfrastructure

• Hire,train/retrainandretainskilledworkersin multiple geographies

• Optimizeglobalprocesses,tools,methodologies and resources

• Communicateitsvaluetothemarketandwin business

For this year’s offshore application service Magic Quadrant, Gartner analysts identify four main forces that have had a profound impact on this market and that directly or indirectly shaped our views for analyzing competitors and their progress:

• Interconnectedandglobalizingeconomies

• Broadandwidespreadeconomicpressures/woes

• IncreasingpressureforITtosupportthebusiness

• Morevalidserviceprovideroptionsgloballythaneverbefore

At the most basic level, these forces describe the new challenges for both the demand side and the supply side of the market. For user organizations, the imperative for buyers of IT services to carefully select service providers that can assist them in meeting these challenges is critical. For service providers, these forces define a market that is full of opportunities to assist buyers by supporting business applications, but also a market fraught with new competitive challenges and risks, and a market that puts a premium on business value, transparency, flexibility and cost efficiency.

The Magic Quadrant is copyrighted November 2008 by Gartner, Inc. and is reused with permission. The Magic Quadrant is a graphical representation of a marketplace at and for a specific time period. It depicts Gartner’s analysis of how certain vendors measure against criteria for that marketplace, as defined by Gartner. Gartner does not endorse any vendor, product or service depicted in the Magic Quadrant, and does not advise technology users to select only those vendors placed in the “Leaders” quadrant. The Magic Quadrant is intended solely as a research tool, and is not meant to be a specific guide to action. Gartner disclaims all warranties, express or implied, with respect to this research, including any warranties of merchantability or fitness for a particular purpose.

©2008Gartner,Inc.and/oritsAffiliates.AllRightsReserved.Reproductionanddistributionofthispublicationinanyformwithoutpriorwrittenpermissionis forbidden. The information contained herein has been obtained from sources believed to be reliable. Gartner disclaims all warranties as to the accuracy, completeness or adequacy of such information. Although Gartner’s research may discuss legal issues related to the information technology business, Gartner does not provide legal advice or services and its research should not be construed or used as such. Gartner shall have no liability for errors, omissions or inadequacies in the information contained herein or for interpretations thereof. The opinions expressed herein are subject to change without notice.

Figure 1. Magic Quadrant for European Offshore Application Services

Source: Gartner (November 2008)

Note: EDS and HP have been evaluated separately because the acquisition was not final within the analysis time frame.

challengers leaders

niche players visionaries

completeness of vision

abilit

y to

exe

cute

As of November 2008

IBM Accenture

Tata Consultancy Services Infosys Technologies

Capgemini Wipro Technologies

CSC EDS

HP

TietoEnator

Siemens SIS

Atos Origin

Cognizant

Satyam Computer Services

Logica HCL Technologies

3Pertinent to this year’s offshore application service Magic Quadrant, these forces point to the hypercompetition in the application service market.

Global service delivery has become a critical competitive element of service providers to support clients’ business applications and their globalization efforts. Service providers able to deliver greater cost take-out or cost efficiencies, and to leverage a vast global labor pool on behalf of clients’ business needs, will have a competitive advantage. However, with so many service providers pursuing application service opportunities and promoting their “offshore” competencies, the competitive landscape is crowded (for example, the analysis considered more than 100 vendors); skills and scale alone are insufficient to achieve a position of market leadership and the necessary revenue growth to sustain such a position. Therefore, in this year’s Magic Quadrant for European Offshore Application Services, Gartner analysts relied on both quantitative (revenue) and qualitative measures to select the provider list to be considered.

Some providers that appeared in the 2007 Magic Quadrant but are not in this year’s study remain viable players; but with a higher revenue bar for inclusion, these providers did not meet the requirements. Therefore, we emphasize that a change in one service provider’s position does not necessarily indicate weakness in its individual performance or quality of service, but rather in a comparative review, its competition may be making more aggressive moves. For example, a company that has been in the Magic Quadrant in previous years but does not appear on this year’s Magic Quadrant may be performing well for its clients, but it may not have met the higher quantitative targets set for inclusion in this particular research effort. Similarly, an organization that moves from the Challengers to the Niche Players quadrant may be doing well in its own right, but comparatively is not moving as quickly or aggressively as other competition. (see the section below, “Inclusion and Exclusion Criteria”).

Market TrendsThe European market for offshore application services has grown significantly during the past 12 months, and the European market’s growth rates continue to outpace those of the North American market. This provides a significant opportunity to providers, and this has been reflected in the amount of investment made in Europe (by the pure-play offshore providers, in particular) to expand their opportunities for globally delivered application services. Although the U.K. remains the dominant purchaser of globally delivered application services in Europe, enterprises from a growing number ofregions—includingtheNordics,Benelux,GermanyandFrance— are taking advantage of globally delivered services. In addition, as Western European buyers seek the optimum providers for their organizations’ needs, many nearshore — and even “onshore” — countries are emerging as alternative (or additional) locations for service provision.

In the European market, it is essential for providers to not only establish operations in key buying centers but also be able to address the local language and cultural demands of the buyer, in addition to the critical business operating practices of the individual markets. To this end, it has proved beneficial for nondomestic providers to ensure a critical mass of local hires. For some providers, the option of acquiring a European-based organization has to be seriously considered to advance this strategy.

The complexity of supporting Pan-European operations dictates that it is no longer viable to have an India-centric strategy. As a result, although some traditional providers are still trying to build critical mass in India, all providers must invest further in nearshore or possibly low-cost onshore European delivery centers.

In the course of our research for this Magic Quadrant, which included briefings by service providers and input from service providers’ clients, and in our ongoing offshore research, Gartner analysts identified several key forces at work shaping the offshore application service market today. Some of these forces have been present and evolving for some time, whereas others are new or taking on new meaning; we believe these represent the most influential forces that shape the competitive dynamics today.

Hypercompetition and high revenue growth among application service providers: Given the rapid rate of global expansion, double-digit application service revenue growth for providers, and increasing pace of competitive change among service providers in today’s application service market, it is not surprising that service providers’ market position is being constantly challenged. This is reflected in very aggressive competition for new business, but is also seen in some position changes in the Gartner Magic Quadrant from year to year. Despite economic uncertainty and some changes in IT spending, which Gartner tracks closely, the global delivery of application services from external providers continues to grow.

Continued strong adoption of the offshore/global delivery model: service providers report record revenues and new contract signingsforapplicationservicesinaGDM.BeyondtraditionalEuropean markets such as the U.K. and the Netherlands, clients are increasingly receptive to offshore delivery and expect a global delivery option to be presented; although a cautious approach is needed, the “offshore stigma” that once prevailed is largely a nonissue, even in countries such as Germany and France. The bar is being raised for all service providers promoting offshore service delivery. While clients initially accepted offshore application services for cost savings, they expect that a provider’s GDM will now also meet high standards for value, quality, skills, predictability and reliability. Service providers are investing in processes, tools and methodologies to make their services seamless. Furthermore, many providers are revamping their approaches for global delivery centersbyaligningcenters/skillsbyverticalexpertise;thiscanafford a “follow the sun” support model as well as diversification of skills and risk in a more leveraged global model.

Market convergence is occurring, but buyers must differentiate the many provider options: Although the tenure, experience and size of traditional service providers give them a significant advantage, the marketplace is also endorsing the “offshore providers’ capabilities” by signing deals of significant size with India-based providers as well as other providers from emerging countries. This leads Gartner to make the bold claim that the offshore service providers have been the catalyst for a major shift in the IT services market and outsourcing competitive landscape. For some time, offshore providers operated “below the radar” of many enterprises, pursuing small-scale project work and staff augmentation services. However, now that the leading Indian providers, in particular, have extended their range of services across the whole spectrum of application services and into infrastructure and have more visibility and expectations from financial analysts, they have been competing boldly for larger

4outsourcing deals — sometimes outside of their original comfort zones. The convergence in the market has resulted in most provider types now offering an offshore value proposition, but the result is a significant challenge for every provider to differentiate itself and have clearly unique value propositions for application services and their GDM. For buyers, this means that lines between traditional service providers and offshore providers are converging.

Looking beyond India to expanding global opportunities and footprints: For service providers, this is the new reality, with significant implications for their business. First, the globalization of economies has broadened service providers’ opportunity to serve more clients in more geographies with application services. This means that many providers are taking concerted steps to systematically build out local presence in more strategic country locations (particularly in Europe), establishing sales and marketing, but also new delivery capabilities that serve those new markets — India is no longer the only delivery source. Second, the shift from an India-centric offshore delivery strategy to a global stage has meant that many providers are already far along in proactively evolving a delivery footprint to become a truly global one by buildingoutdeliverycentersinothercountries/regions—China,RussiaandBrazil,aswellasLatinAmerica,EasternEuropeandAsia. Gartner predicted that the bilateral onshore-offshore model would give way to integrated, global delivery networks. Some providers are trailing in this regard; what we wrote last year in the Magic Quadrant analysis has come true: “Providers that aren’t on the ‘accelerated’ curve to fully integrate and systematically invest in and advance their GDMs are quickly losing ground.” We believe that service providers with concerted investments in strategically building out a multicountry, globally integrated delivery model will dominate in the future. For buyers of services, this means that there is an increasingly complex array of global delivery and country options available.

Greater sophistication in service providers’ sales and marketing strategies and messages for application services/solutions: In a year’s time, it has become apparent which providers have made great strides to refine and hone their client-facing skills. Greater clarity and sophistication in marketing messages, competitive values and vision statements for application services are supported by concrete actions of hiring local sales skills, verticalizing offerings and even reorganizing (often by global vertical competencies) for more-effective reach of clients. Ultimately, this attention to market-facing issues is mandatory to achieve differentiation in this crowded market. Despite investment and senior executive-level attention to this critical aspect of their business, clear differentiation in the market eludes many providers. For buyers, the evaluation process will likely get more complex becausethereislessdifferentiationinthemarket.Buyersofservices will need to interpret more-sophisticated messages to determine where and how service providers can truly assist them.

Greater attention to innovative pricing strategies and options: Service providers in this year’s research reported emphasis on demonstrating new value to clients by offering alternative pricing options, including aligning pricing with business outcomes through outcome-based pricing. This reflects service providers’ success in moving their offshore application service portfolio from a strictly cost-focused value proposition to one of more meaningful business alignment and impact. The past criticisms of the offshore providers being effective only in low-risk, hourly-labor-based pricing schemes are no longer the case; many service providers actively promote

alternative relationship models where they will assume risk and accountability for application performance tied to business metrics.

Accelerating pace of acquisitions and partnering: The “big news” acquisition completed in August 2008 was the HP acquisition of EDS, which has implications for two key providers in the offshore application service market as they will seek to integrate their global delivery centers and position themselves as one of the world’s largest IT services firms. Many other service providers are relying on targeted acquisitions to support their global expansion, gain critical skills, and enter into new vertical markets or solutions areas. The market has matured, but due to the pace of competitive activity, most providers will need to rely on an acquisitive strategy to some extent to move quickly enough to capitalize on growth opportunities. Although partnering and subcontracting will be used to fill skill gaps or address scale requirements, these forms of skills provisioning are less reliable and arguably less satisfactory to clients (higher costs are inevitable when a third party is used).

Continuing evolution of service providers’ service portfolios: The range and depth of service providers’ application skills are impressive and continue to grow. ERP, Web services, consulting, application testing and application modernization services are among the most prominent growth areas in this year’s discussions. However, there is also momentum for application service providers to expand into infrastructure services and business process areas. In contracts where bundling of services is required, these added services are now mandatory; however, they are not covered in this Magic Quadrant.

Research ProcessGartner’s Magic Quadrant process involves conducting primary research, including obtaining client references as well as each service provider’s representation of its organization. Additional analysis is conducted by Gartner analysts’ direct contact with enterprise buyers throughout the year. All these sources of information are carefully analyzed with a heavy emphasis on client feedback. As a result, many individual categories have “client reference” criteria factored into the scoring. Gartner considers client feedback to be one of the most-critical measures of a service provider’s success.

Gartner evaluates service providers on their ability to execute and on their completeness of vision. When the two sets of criteria are evaluated together, the resulting analysis shows how well the provider performs an array of services relative to its peers, and how well it’s positioned for the future. This evaluation is a snapshot in time. Over time, the competitive nature of the offshore application service provider market affects the relative position of the evaluated companies.

In addition to understanding the positions in this Magic Quadrant, enterprises must conduct due diligence and check references. They must ensure that their business cultures are synergistic or at least compatible with the service provider’s culture. The most-critical criteria for project success are a provider’s capability to work within an enterprise’s business culture and to work with an enterprise’s people to effect the organizational changes that are essential to a successful initiative. Evaluation criteria for selecting service providers should reflect your company’s desired business objectives, and should align with your enterprise and sourcing requirements.

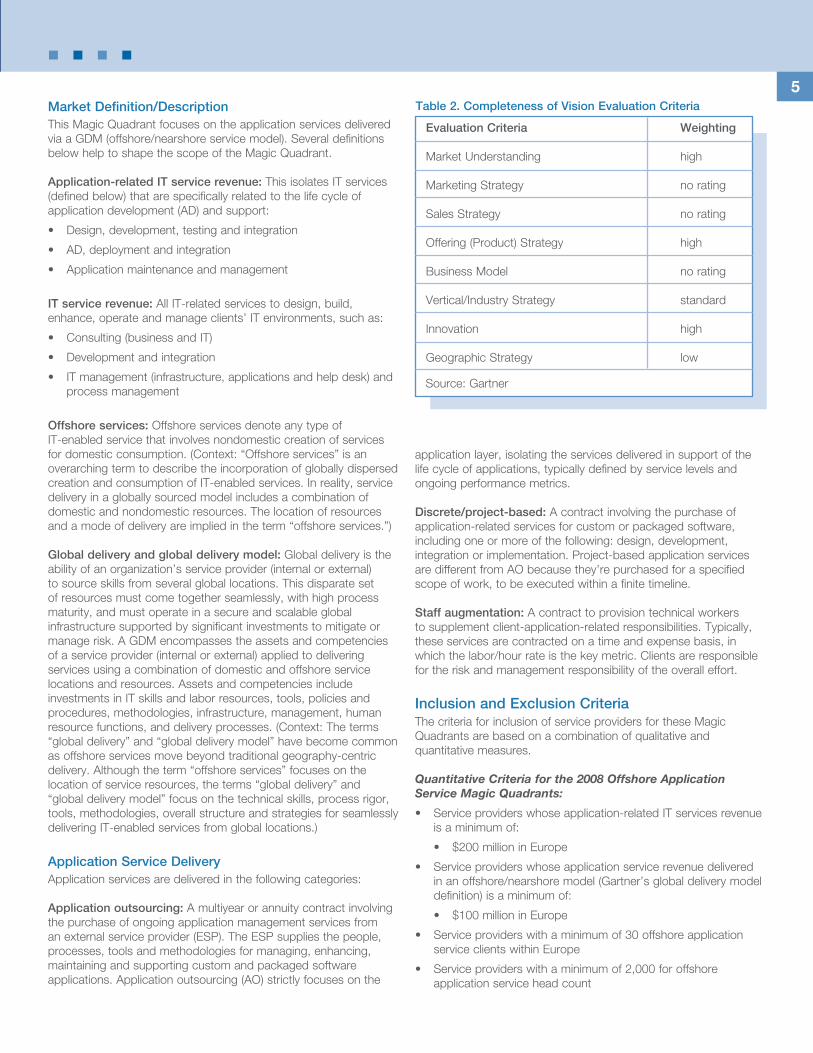

5Market Definition/DescriptionThis Magic Quadrant focuses on the application services delivered viaaGDM(offshore/nearshoreservicemodel).Severaldefinitionsbelow help to shape the scope of the Magic Quadrant.

Application-related IT service revenue: This isolates IT services (defined below) that are specifically related to the life cycle of application development (AD) and support:

• Design,development,testingandintegration

• AD,deploymentandintegration

• Applicationmaintenanceandmanagement

IT service revenue: All IT-related services to design, build, enhance, operate and manage clients’ IT environments, such as:

• Consulting(businessandIT)

• Developmentandintegration

• ITmanagement(infrastructure,applicationsandhelpdesk)andprocess management

Offshore services: Offshore services denote any type of IT-enabled service that involves nondomestic creation of services for domestic consumption. (Context: “Offshore services” is an overarching term to describe the incorporation of globally dispersed creation and consumption of IT-enabled services. In reality, service delivery in a globally sourced model includes a combination of domestic and nondomestic resources. The location of resources and a mode of delivery are implied in the term “offshore services.”)

Global delivery and global delivery model: Global delivery is the ability of an organization’s service provider (internal or external) to source skills from several global locations. This disparate set of resources must come together seamlessly, with high process maturity, and must operate in a secure and scalable global infrastructure supported by significant investments to mitigate or manage risk. A GDM encompasses the assets and competencies of a service provider (internal or external) applied to delivering services using a combination of domestic and offshore service locations and resources. Assets and competencies include investments in IT skills and labor resources, tools, policies and procedures, methodologies, infrastructure, management, human resource functions, and delivery processes. (Context: The terms “global delivery” and “global delivery model” have become common as offshore services move beyond traditional geography-centric delivery. Although the term “offshore services” focuses on the location of service resources, the terms “global delivery” and “global delivery model” focus on the technical skills, process rigor, tools, methodologies, overall structure and strategies for seamlessly delivering IT-enabled services from global locations.)

Application Service DeliveryApplication services are delivered in the following categories:

Application outsourcing: A multiyear or annuity contract involving the purchase of ongoing application management services from an external service provider (ESP). The ESP supplies the people, processes, tools and methodologies for managing, enhancing, maintaining and supporting custom and packaged software applications. Application outsourcing (AO) strictly focuses on the

application layer, isolating the services delivered in support of the life cycle of applications, typically defined by service levels and ongoing performance metrics.

Discrete/project-based: A contract involving the purchase of application-related services for custom or packaged software, including one or more of the following: design, development, integration or implementation. Project-based application services are different from AO because they’re purchased for a specified scope of work, to be executed within a finite timeline.

Staff augmentation: A contract to provision technical workers to supplement client-application-related responsibilities. Typically, these services are contracted on a time and expense basis, in whichthelabor/hourrateisthekeymetric.Clientsareresponsiblefor the risk and management responsibility of the overall effort.

Inclusion and Exclusion CriteriaThe criteria for inclusion of service providers for these Magic Quadrants are based on a combination of qualitative and quantitative measures.

Quantitative Criteria for the 2008 Offshore Application Service Magic Quadrants:

• Serviceproviderswhoseapplication-relatedITservicesrevenueis a minimum of:

• $200millioninEurope

• Serviceproviderswhoseapplicationservicerevenuedeliveredinanoffshore/nearshoremodel(Gartner’sglobaldeliverymodeldefinition) is a minimum of:

• $100millioninEurope

• Serviceproviderswithaminimumof30offshoreapplicationservice clients within Europe

• Serviceproviderswithaminimumof2,000foroffshoreapplication service head count

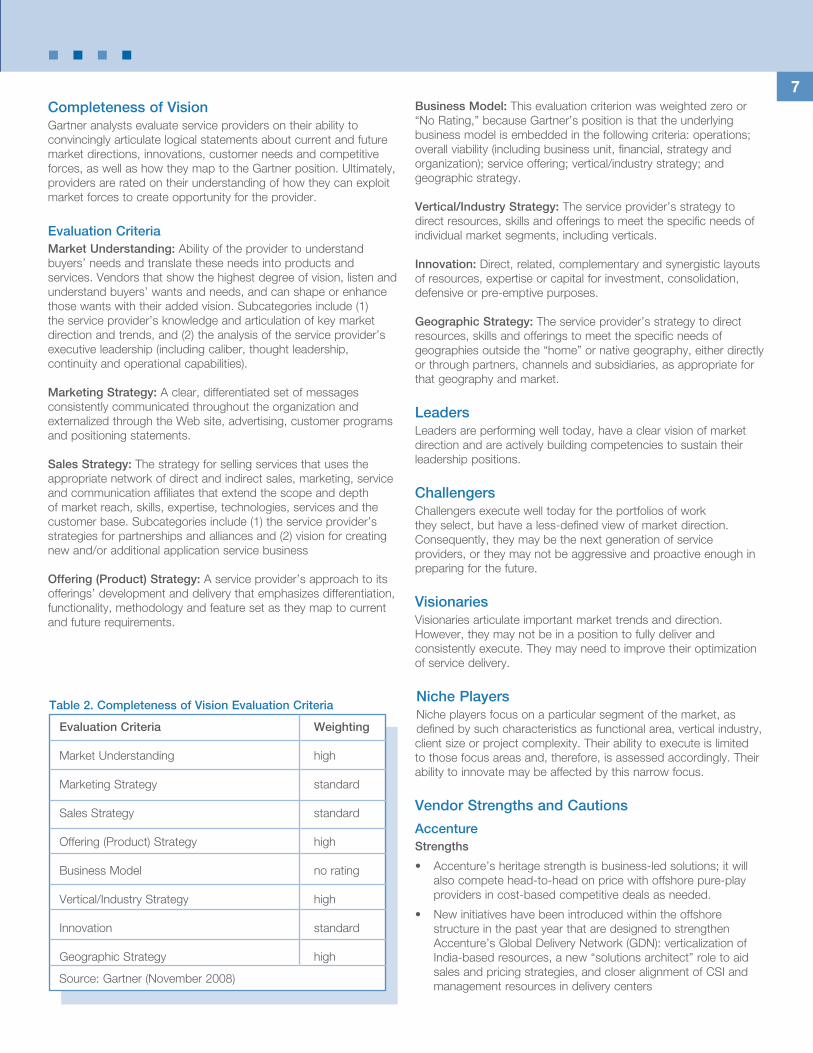

Evaluation Criteria

Market Understanding

Marketing Strategy

Sales Strategy

Offering (Product) Strategy

BusinessModel

Vertical/IndustryStrategy

Innovation

Geographic Strategy

Weighting

high

no rating

no rating

high

no rating

standard

high

low

Table 2. Completeness of Vision Evaluation Criteria

Source: Gartner

6Qualitative Criteria:

• Overallmarketinterestandvisibilityasdeterminedbyseriousconsideration for selection from enterprise clients

• Gartneranalysts’interactionsthatrevealinterestinspecificserviceprovidersforoffshore/globalservicedelivery

• Theserviceproviderservesmultipleindustrieswithabroadbase of application services

AddedVendors added: From the 2007 Magic Quadrant version, no new service providers were added.

DroppedVendors dropped: From the 2007 Magic Quadrant version, the following providers were dropped: Deloitte, Mastek, Perot, T-Systems and Xansa.

Magic Quadrant Evaluation Criteria and WeightsGartner analysts evaluate service providers on the quality and efficacy of the processes, systems, methods or procedures that enable IT provider performance to be competitive, efficient and effective, and to positively affect revenue, retention and reputation. Ultimately, service providers are judged on their ability to successfully capitalize on their vision.

The following are the evaluation criteria for this year’s offshore application service Magic Quadrant along the two primary axes of “Vision” and “Execution,” along with the weights assigned to each parameter.

Evaluation Criteria

Ability to ExecuteGartner analysts evaluate service providers on the quality and efficacy of the processes, systems, methods or procedures that enable IT provider performance to be competitive, efficient and effective, and to positively impact revenue, retention and reputation. Ultimately, technology providers are judged on their ability and success in capitalizing on their vision.

Evaluation Criteria Definitions and WeightsProduct/Service: Core services offered by the provider that competein/servethedefinedmarket.Thisincludescurrentproduct/servicecapabilities,quality,featuresetsandskills,whetherofferednativelyorthroughagreements/partnershipsasdefinedinthe market definition and detailed in the subcriteria.

Subcategories include (1) assessment of specific services in the key application service arena including packaged or custom applications or specialty areas such as testing, and (2) analysis of technical knowledge and skills.

Overall Viability (Business Unit, Financial, Strategy, Organization): Viability includes an assessment of the overall organization’s financial health; the financial and practical success of the business unit; and the likelihood of the individual business unit to continue to invest in the service, offer the service and advance

Evaluation Criteria

Product/Service

OverallViability(BusinessUnit,Financial,Strategy, Organization)

SalesExecution/Pricing

Market Responsiveness and Track Record

Marketing Execution

Customer Experience

Operations

Weighting

high

standard

standard

high

standard

no rating

high

Table 1. Ability to Execute Evaluation Criteria

Source: Gartner (November 2008)

the state of the art in the organization’s portfolio of services. Subcategories include (1) assessment of the service provider’s practice area profile (that is, financials, resources, use and attrition), and (2) analysis of strategy and organization.

Sales Execution/Pricing: The service provider’s capabilities in all presales activities and the structure that supports them. This includes deal management, pricing and negotiation, presales support and the overall effectiveness of the sales channel.

Market Responsiveness and Track Record: Ability to respond, change direction, be flexible and achieve competitive success as opportunities develop, competitors act, customer needs evolve and market dynamics change. This criterion also considers the provider’s history of responsiveness. Subcategories include (1) specific client feedback, and (2) the vendor’s demonstrated ability to adjust to market conditions.

Marketing Execution: The clarity, quality, creativity and efficacy of programs designed to deliver the organization’s message to influence the market, promote the brand and business, increase awareness of the products, and establish a positive identification withtheproduct/brandandorganizationinthemindsofbuyers.This “mind share” can be driven by a combination of publicity, promotions, thought leadership, word of mouth and sales activities.

Customer Experience: This evaluation criterion was weighted zero or “No Rating” because elements of customer experience were included within each of the other evaluation criteria. Gartner research has shown that client feedback is one of the most important indicators of potential success in working with a service provider; hence, collectively, feedback had a high weighting across both axes of this Magic Quadrant analysis.

Operations: The ability of the organization to meet its goals and commitments. Factors include the quality of the organizational structure, including skills, experiences, programs, systems and other vehicles that enable the organization to operate effectively and efficiently on an ongoing basis. Subcategories include (1) the organizational and business model, and (2) the global delivery model (downstream capabilities).

7Completeness of VisionGartner analysts evaluate service providers on their ability to convincingly articulate logical statements about current and future market directions, innovations, customer needs and competitive forces, as well as how they map to the Gartner position. Ultimately, providers are rated on their understanding of how they can exploit market forces to create opportunity for the provider.

Evaluation CriteriaMarket Understanding: Ability of the provider to understand buyers’ needs and translate these needs into products and services. Vendors that show the highest degree of vision, listen and understand buyers’ wants and needs, and can shape or enhance those wants with their added vision. Subcategories include (1) the service provider’s knowledge and articulation of key market direction and trends, and (2) the analysis of the service provider’s executive leadership (including caliber, thought leadership, continuity and operational capabilities).

Marketing Strategy: A clear, differentiated set of messages consistently communicated throughout the organization and externalized through the Web site, advertising, customer programs and positioning statements.

Sales Strategy: The strategy for selling services that uses the appropriate network of direct and indirect sales, marketing, service and communication affiliates that extend the scope and depth of market reach, skills, expertise, technologies, services and the customer base. Subcategories include (1) the service provider’s strategies for partnerships and alliances and (2) vision for creating newand/oradditionalapplicationservicebusiness

Offering (Product) Strategy: A service provider’s approach to its offerings’ development and delivery that emphasizes differentiation, functionality, methodology and feature set as they map to current and future requirements.

Business Model: This evaluation criterion was weighted zero or “No Rating,” because Gartner’s position is that the underlying business model is embedded in the following criteria: operations; overall viability (including business unit, financial, strategy and organization);serviceoffering;vertical/industrystrategy;andgeographic strategy.

Vertical/Industry Strategy: The service provider’s strategy to direct resources, skills and offerings to meet the specific needs of individual market segments, including verticals.

Innovation: Direct, related, complementary and synergistic layouts of resources, expertise or capital for investment, consolidation, defensive or pre-emptive purposes.

Geographic Strategy: The service provider’s strategy to direct resources, skills and offerings to meet the specific needs of geographies outside the “home” or native geography, either directly or through partners, channels and subsidiaries, as appropriate for that geography and market.

LeadersLeaders are performing well today, have a clear vision of market direction and are actively building competencies to sustain their leadership positions.

ChallengersChallengers execute well today for the portfolios of work they select, but have a less-defined view of market direction. Consequently, they may be the next generation of service providers, or they may not be aggressive and proactive enough in preparing for the future.

VisionariesVisionaries articulate important market trends and direction. However, they may not be in a position to fully deliver and consistently execute. They may need to improve their optimization of service delivery.

Niche PlayersNiche players focus on a particular segment of the market, as defined by such characteristics as functional area, vertical industry, client size or project complexity. Their ability to execute is limited to those focus areas and, therefore, is assessed accordingly. Their ability to innovate may be affected by this narrow focus.

Vendor Strengths and Cautions

AccentureStrengths

• Accenture’sheritagestrengthisbusiness-ledsolutions;itwillalso compete head-to-head on price with offshore pure-play providers in cost-based competitive deals as needed.

• Newinitiativeshavebeenintroducedwithintheoffshorestructure in the past year that are designed to strengthen Accenture’s Global Delivery Network (GDN): verticalization of India-based resources, a new “solutions architect” role to aid sales and pricing strategies, and closer alignment of CSI and management resources in delivery centers

Evaluation Criteria

Market Understanding

Marketing Strategy

Sales Strategy

Offering (Product) Strategy

BusinessModel

Vertical/IndustryStrategy

Innovation

Geographic Strategy

Weighting

high

standard

standard

high

no rating

high

standard

high

Table 2. Completeness of Vision Evaluation Criteria

Source: Gartner (November 2008)

8• AccenturecontinuestoevolveitsGDNasintegraltoitsgo-to-

marketsalesanddeliverystrategy:93%ofAccenture’stop100clients utilize Accenture’s GDN for some level of service delivery (upfrom70%oneyearago).

Cautions

• SomeclientsperceivethatAccenturelagsbehinditscompetitionintermsoftypicaloffshore/onshoreresourceratios; greater communication with clients on the leverage of its offshore resource pool for application projects is needed.

• WiththeriseofmultitowerIToutsourcing,Accenturemustdevelopclearermarketing/salesmessagesandofferingstoexplain to clients how it will deliver value with its GDN through integrated applications and infrastructure capabilities.

• Accentureisperceivedinthemarketasalarge,premium-priced service provider that may be inflexible to work with. In cautionary economic times, this opens the door for offshore competitors to aggressively position themselves ahead of Accenture for cost-sensitive buyers seeking “flexible” partners.

Atos OriginStrengths

• Whileitsinvestmentinenhancingtheportfolioofglobaldeliverycapabilities continues, Atos Origin also focuses on migrating its business toward a fixed-price model to support an aggressive leverageofnear/offshoreresources(ideally60%to70%).

• AtosOrigin’sportfolioofapplicationservicesisbalancedtowardboth projects and full management services. It focuses on a wide spectrum of technology.

• CustomersciteAtosOrigin’sflexibleapproachinmanagingthe relationship and understanding the technical and business requirements. This is supported by a focus on process excellence.

Cautions

• AtosOriginmustcontinuetopromoteitsbrandinIndiatofurther reduce staff attrition, which remains higher than its major competitors. While its investment in Morocco is ideally suited to target the French market, Atos Origin also needs to further enhance the depth and breadth of its capabilities outside of India.

• Tosupportitsfuturegrowth,AtosOriginneedstoclearlycommunicate how it can pursue and manage leads related to global deals. Further growth leverage can also be achieved in areas such as application testing.

• Areasforimprovementscitedbycustomersincludetheability to manage resources at the beginning of the offshore delivery project (when a ramp-up is often necessary) and communication around its full capabilities and the benefits delivered.

CapgeminiStrengths

• Capgemini’sstrongEuropeanfocusandcoverage,combinedwith a clear commitment to the development of a fully integrated GDM, gives it a clear appeal for clients with a European presence or preference for an EU-based provider.

• Aggressiveplansexisttodoubleoffshoreresourcesduringthenext two years, through a combination of organic and inorganic means. If executed, this should allow Capgemini to gain critical mass in a number of locations in addition to India.

• Capgeminihasinvestedheavilyinthesalesandmarketingofits Rightshore initiatives, and it has worked hard at instituting consistent tools and methodologies across its delivery centers to ensure more seamless, integrated support for clients.

Cautions

• Capgeministillhasthelargestproportionofits“offshore/nearshore” resources located in India, and many of these are from the Kanbay acquisition. While Capgemini has added scale toeachofitsnon-Indianoffshore/nearshoredeliverylocationsin 2008, its ability to achieve credible scale will be key to its ongoing success.

• Clientscitealackofproactivityinsuggestingalternativeapproaches to improving support and driving down cost (indicative of immaturity in global delivery).

• CapgeminimustbetterleverageitscontinentalEuropeanpresence as a differentiator when compared with its Indian competitors. Growing investments by its competitors in Europe will increasingly dilute Capgemini’s European heritage benefits.

CognizantStrengths

• CognizanthassuccessfullytransferreditsU.S.modeloffocusing on establishing strong and deep relationships with a small(er) number of clients to Europe.

• ThecreationofanearshorecenterinEasternEurope(Budapest)willallowCognizanttobecomemoreattractiveto customers in Continental Europe and address one of its key shortcomings in its European strategy that is a lack of nearshore resources.

• Cognizanthaswonafewblue-chipaccountsinEuropethathave helped it establish its brand awareness as an EU provider of offshore application services.

Cautions

• TheEuropeanpresenceforCognizantisconcentratedintheU.K. and, although growing, the penetration into mainland Europe has not yet been as successful.

• Althoughnotthesolepathtogrowth,anallianceapproachin the largest market in mainland Europe (Germany) is risky. Alliances in the offshore services world have historically been difficult to manage and derive value from.

• Unlessitcontinuestoinvestincapabilitiesdesignedtoaddressthe needs of the European market, it will be a challenge for Cognizant to replicate its U.S. success, which was driven toalargeextentbyits“hybrid”U.S./Indiabusinessmodel,in the diverse European market where it does not enjoy that advantage.

9CSCStrengths

• CSCcanrelyonawideportfolioofapplicationservices.Itsrecent focus on leveraging its technical skills, global delivery capabilities and vertical experience to develop business solutions has the potential to support positive growth in the future.

• Beyondexpandingthesizeofitsnearshore/offshorecapabilities, CSC is focusing on creating a global delivery network aimed at underlining the unique application capabilities of each center. CSC’s aim is to link the delivery centers through common tools, processes and methodologies.

• Customers’feedbackpointedtoCSC’sstrengthinoffshoreapplication service engagements in terms of technical skills, compliance with contracted deliverables, process focus, trust and communication.

Cautions

• Whilethecreationofaglobaldeliverynetworkissound,CSCwill need to ensure that the transition to a “homogeneous” approach to delivering services is executed efficiently and in a timely way. Discipline and rigor are necessary but will also challenge CSC’s reputation for flexibility in the market.

• CSC’sexperience,reputationandskillsingloballydeliveredapplication services are not equally recognized across Europe. As such, to further grow in Europe and mirror its position in countries such as the U.K., CSC needs to focus on investing in sales, marketing and front-end delivery capabilities in some key markets such as Germany or Italy.

• Areasforimprovementmentionedbycustomersincludeinnovation, proactive delivery of service improvements and resource management. Finally, CSC would also benefit from enhancing its brand in application services outside of its key European markets.

EDSStrengths

• EDShasconsolidatedandtransformeditsBestShoreglobaldelivery approach by consolidating offshore centers into industry-aligned Global Competency Centers (GCCs) in various geographies.

• EDSfocusesonthetotalcostofoperations(whichitcalls“EDSDesigned for Run”) and overall quality for client applications as a component of its full stack service integration.

• EDShascreatedhorizontalpracticesinMicrosoft,Oracle,SAPand testing that are integrated with its industry teams. This further supports its vertical integration and orientation strategy and delivery.

Cautions

• EDSneedstofurthermarketanddemonstratespecificapplication capabilities through its integrated “design to run” approach that will aid clients in planning and implementing downstream business agility.

• EDSlargelyappearsonshortlistsforinfrastructure-centricoutsourcing, but clients have been reluctant to consider EDS for large application-only deals, especially implementation services. Continued commitment and focused strategy on the application business is necessary to prove to European clients that EDS is serious about growing its application business.

• EDSisinvestingsignificantlyinanindustryapproachviaits GCCs, but application clients largely are still focused on immediate cost savings, which will drive them to do short-term planning focused on cost containment and reduction, not necessarily industry competencies.

HCL TechnologiesStrengths

• HCLcontinuestoleverageitsintegratedoperationsmanagement framework to grow its application service revenue.

• HCLhasatargetedsalesstrategyinpursuingdealsthatfocuson business value delivery — as opposed to driving volume.

• HCL’sclientsrecognizeitforitsflexibilityinadaptingtochanging business needs; this helps in developing a stronger relationship with its clients.

Cautions

• HCLhasbeenslowinbuildingoutanetworkofnearshoredevelopment centers to serve the European market; this will potentially inhibit its speed of growth in situations where a nearshore presence is required or would be a strong differentiator.

• AlthoughHCLispositioningitselfasatransformationpartner,it still needs to gain the confidence of many of its larger clients to execute upstream application services and consulting-type work; to this end, clients believe that HCL should be more proactive and assertive in communicating on potential opportunities to lower costs or to innovate on current solutions.

• HCLhastraditionallybeenviewedasastronginfrastructureservice provider, and its application service revenue has historically been significantly lower than that of its peers. It must aggressively expand its application service marketing, to establish a strong and differentiated value proposition.

HPStrengths

• HPseniorleadershiphasarticulatedanewHPapplicationstrategythatisconsistentwithitsoverallservice/outsourcingstrategy and has a global road map for implementation.

• GlobalservicedeliveryisenhancedbyHPCentersofExcellence (COEs) that are linked, and are aligned with industry or technology domains and initiatives to industrialize HP’s application services in areas like testing, modernization and management services.

• HPhasestablishedabroadandrobustGDMwithasignificantpresenceforEuropeanclients;80%ofHP’sglobaldeliverycenters are in cost-advantaged locations.

10Cautions

• AlthoughHPshowscommitmenttoapplicationoutsourcing,clients are not yet consistently shortlisting HP for “application services only” deals due to lack of market awareness and presence.

• ClientsciteweaknessinHP’sabilitytohaveadequatenumbersof skilled on-site application resources and the need for greater adherence to standardized, repeatable methods for service delivery.

• WhileHP’sservicebusinessispromotinganoffshoreapplication growth strategy, HP’s corporate message emphasizes product before services. This places application services behind HP product services, where it may become lost in the overall HP brand.

IBMStrengths

• Inthepastyear,IBMevolveditsglobalapplicationservicedelivery processes and methodologies to ensure a consistent delivery experience for clients and dedicated industry-specific offshore centers.

• IBM’sfocuson“globallyintegratedcapabilities”hasledtoincreasing levels of industry-specific solution work and technical focus being done in dedicated offshore centers; in the past year,IBM’snearshoreEuropeandeliveryoperationshaveexhibited this dedication and focus on key technologies (SAP and Web development, for example).

• IBM’smarket-ledapproachforserviceshasbeenenhancedbya new application service consultant (ASC) role that helps align clients’businessneedswithIBM’sfullserviceofferingsandoffshore resourcing needs.

Cautions

• IBM’spenetrationandleverageofoffshore/nearshoreservicedelivery for business application solutions is lower overall compared with its competition; opportunities exist to increase its levels of offshore service mix.

• ClientsperceivethatIBMcouldbemoreproactiveinpostimplementation initiatives to leverage automation to enhance reliability, reduce costs and improve efficiency; and to introduce ideas for innovation to consistently drive more value in offshore application service engagements.

• ClientsreportthatIBMisgenerallyslowertorespondandlessflexible in its contracting approaches compared with some of its competitors that have fewer management approval layers, allowing more agility.

Infosys TechnologiesStrengths

• Infosyscontinuestostrengthenitsglobaldeliverycapabilitiesthrough aggressive build-out of delivery centers and improvements in global delivery processes and methodologies.

• ThestrongInfosysbrandimagecoupledwithahighlyscalablehiring process has allowed Infosys to manage the challenges of attrition and competition for resources better than some of its peers.

• InfosyshasreorganizeditsbusinessunitsinEuropetodeepenits vertical-oriented transformational capabilities in an effort to broaden its customer base.

Cautions

• Infosys’inflexibilityinpricingmayslowitsgrowth,especiallyinatightening macroeconomic environment, unless it is successful in pursuing a higher percentage of larger, and higher-value, deals.

• Infosyshasnotyetsuccessfullyleverageditshigh-endconsulting business to support and extend its application service business through its global delivery network.

• Infosyshasbeenslowtotakeadvantageofinorganicgrowthopportunities when compared to its direct competitors; failure to use strategic acquisitions may jeopardize Infosys’ growth requirements.

LogicaStrengths

• Logica’sheritageinawiderangeofapplicationservicesis recognized in Europe, especially in key markets such as the U.K., France and the Netherlands. Its renewed focus on leveraging an industrialized and process-oriented delivery model is likely to cement its position in Europe.

• Logica’sinvestmentincapturingoutsourcingservices,andproactively driving the globalization agenda of its key accounts by leveraging its consulting resources, offers the potential for future growth.

• Customerfeedbackindicatesmotivatedandqualifiedresourcesfocused on addressing the deal while managing customer satisfaction. Customers also report that Logica’s services offer value for money.

Cautions

• Followingorganicandinorganicgrowth,Logicawillbeexpectedto execute its “One Logica” vision in a timely and rigorous way, where standardized tools and processes can support profitability while enhancing a seamless customer experience.

• Logica’splantoenhanceitsglobaldeliverycapabilities(doubling the current head count of 4,000 by the end of 2009) needs to be supported by a focus on branding, and career development aimed at efficiently managing staff attrition. This will be particularly necessary to protect skills in key technologies.

• Customerinteractionpointstoinnovation,resourcemanagement, adherence to the customer security standards, and continuity in management resources as areas for improvement.

11Satyam Computer ServicesStrengths

• Satyamhasatargetedverticalstrategy,anditsdomaincompetency and successful penetration in the manufacturing and automotive sectors distinguish it in the market versus other India pure-play providers.

• Satyamalignstochangingcustomerexpectationsthrougha consulting-led approach for its business solutions and via centers of excellence in specific locations.

• Clientsciteflexibility,experienceandknow-howofenterpriseapplications and commitment toward customer satisfaction as positive attributes.

Cautions

• Transformationandinnovationarenotprimarybrandattributesof Satyam; although Satyam is investing in capabilities to position it as a “transformation” partner, it is still work in progress.

• Satyam’sjointdevelopmentand“gotomarket”approachleveraging partners for developing new service capabilities runs a high risk of failure because of misaligned objectives of the partners and conflicting interests.

• SomeSatyamclientscitealackofproactiveness,lackofinnovation and staffing issues (such as the high turnover of key project people) as common problems. Moreover, Satyam lacks brand visibility in Europe, and it would need to be much more aggressive in order to boost its business in the European region.

Siemens SISStrengths

• SiemensSISmaintainsastrongfocusonapplicationservicesand on the integration of global capabilities within its delivery model. Its global delivery capabilities include valuable and experienced SAP skills.

• SiemensSIS’salignmenttothemainverticalmarketsofitskeyaccounts (including Siemens) offers the potential to position its application services and solutions closer to the business of the customer and, as a consequence, achieve organic growth by upselling.

• Customers’interactionunderlinedSiemensSIS’sabilityinterms of compliance with the contract, technical and process adherence, and willingness to solve problems in a timely manner.

Cautions

• SiemensSIS’salignmenttoitskeyaccountscouldhinderthepotential for new business because new potential customers will remain cautious about the quality of capabilities made available to them. This may challenge Siemens SIS’s ability to compete for deals with new accounts outside of its core markets.

• WhileSiemensSIScanrelyonawidesetofapplicationservicecapabilities, these are often known only to existing customers. Customer-centric initiatives around marketing and innovation are not likely to create awareness and growth outside of the established customer base.

• Areasforimprovementmentionedbycustomersincludeunderstanding of the client business pressure points, the management of skills and continuity of management resources.

Tata Consultancy ServicesStrengths

• TCShascontinuedtowinlargenewcontractsinapplicationservices and application outsourcing on a global basis. Combined with its depth and breadth of capability, this has ensured continued revenue leadership among the Indian providers.

• TCScontinuestomaketargetedacquisitionstogrowitspresence in new markets and supplement its skills in industry domains, and it has recently reorganized to strengthen its vertical growth strategy.

• CustomersciteTCS’sresponsiveness,flexibilityinengagements, commercial arrangements and service delivery as strengths of TCS.

Cautions

• Clientsindicatesomeinconsistencyinproactivelyofferingalternative delivery approaches, such as increased automation, and in taking steps to improve efficiency and drive down cost.

• TCSmustdemonstrategreaterabilitytoprovidedeepindustry/domain expertise across a broad range of industry verticals; while, in some areas, domain expertise was strong, clients in some industries cite gaps in market understanding or depth of resources with vertical understanding.

• Withcontinuedstronggrowthandrecentorganizationalchanges, TCS will face challenges in maintaining consistency and quality across its broad industry, service and geographical coverage areas. Hiring and training the sheer amount of resources it needs to sustain and grow the business will also be challenging.

TietoEnatorStrengths

• Despiteitsrelativelysmallsize,TietoEnatorhasastrong,established presence in offshore application services in the Nordic market.

• TheintroductionofanewCEOhasreinvigoratedTietoEnator’sfocus around global delivery, now seen as a key strategic area for investment. Recent results of this investment are the acquisition of Fortuna Technologies, an Indian telecom engineering company and the opening of a new delivery site in Belorussia.

• TietoEnatormaintainsastrongreputationforcustomerintimacyand focus on service delivery quality, key elements to achieve customer satisfaction in TietoEnator’s domestic market.

Cautions

• BeyonditscoreNordicmarket,TietoEnatorhasverylowEuropean market penetration. Future growth will need to be supported by an aggressive marketing and branding investment.

12• Althoughitsplantotransformtheorganizationintoaglobal

deliveryentityissound,thisjourneyhasstartedlate.Beyondgrowingtheheadcountinnear/offshorelocations,TietoEnatorwill need to focus on “internal change management” in order to fully leverage the newly created nearshore and offshore capabilities.

• Initstransformationtowardagloballyintegratedcompany,TietoEnator must focus on achieving a seamless alignment of service delivery tools, processes and methodologies.

Wipro TechnologiesStrengths

• Wiprohasmadestronginvestmentsinitsindustry-verticalfocus, and it now has a significant number of domain consultants across its broad vertical coverage area.

• Continuedinvestmentsinabroadrangeofcountriesarenowbuilding a balanced portfolio of GDN locations from which to support clients. These investments include an additional drive to establish delivery centers in Europe, the Middle East and Africa, often as a direct result of contract awards.

• Wiprohasextendeditslocalhiringpracticesinbothconsultingand sales to boost its local presence, knowledge and appeal.

Cautions

• AlthoughstrongprocesscapabilityunderpinsWipro’sappealas a provider, an overly rigid approach to process quality raises concerns regarding its ability to deliver flexibility to its clients; some clients also cite a lack of proactive communication on project plans and delivery issues.

• Wipro’snewexecutivestructure,whichincludesjointCEOs(announced in April 2008) will take time to perfect and demonstrate effectiveness.

• AlthoughWiprohassuccessfullyestablisheditstechnologyand process credentials in the market, more work is required to build the perception of its business acumen with C-level executives.

Vendors Added or DroppedWe review and adjust our inclusion criteria for Magic Quadrants and MarketScopes as markets change. As a result of these adjustments, the mix of vendors in any Magic Quadrant or MarketScope may change over time. A vendor appearing in a Magic Quadrant or MarketScope one year and not the next does not necessarily indicate that we have changed our opinion of that vendor. This may be a reflection of a change in the market and, therefore, changed evaluation criteria, or a change of focus by a vendor.

13

Evaluation Criteria Definitions

Ability to ExecuteProduct/Service: Coregoodsandservicesofferedbythevendorthatcompetein/servethedefinedmarket.Thisincludescurrentproduct/servicecapabilities,quality,featuresetsandskills,whetherofferednativelyorthroughOEMagreements/partnershipsasdefined in the market definition and detailed in the subcriteria.

Overall Viability (Business Unit, Financial, Strategy, Organization): Viability includes an assessment of the overall organization’s financial health, the financial and practical success of the business unit, and the likelihood that the individual business unit will continue investing in the product, will continue offering the product and will advance the state of the art within the organization’s portfolio of products.

Sales Execution/Pricing: The vendor’s capabilities in all pre-sales activities and the structure that supports them. This includes deal management, pricing and negotiation, pre-sales support and the overall effectiveness of the sales channel.

Market Responsiveness and Track Record: Ability to respond, change direction, be flexible and achieve competitive success as opportunities develop, competitors act, customer needs evolve and market dynamics change. This criterion also considers the vendor’s history of responsiveness.

Marketing Execution: The clarity, quality, creativity and efficacy of programs designed to deliver the organization’s message to influence the market, promote the brand and business, increase awareness of the products, and establish a positive identification withtheproduct/brandandorganizationinthemindsofbuyers.This“mindshare”canbedrivenbyacombinationofpublicity,promotional initiatives, thought leadership, word-of-mouth and sales activities.

Customer Experience:Relationships,productsandservices/programsthatenableclientstobesuccessfulwiththeproductsevaluated. Specifically, this includes the ways customers receive technical support or account support. This can also include ancillary tools, customer support programs (and the quality thereof), availability of user groups, service-level agreements and so on.

Operations: The ability of the organization to meet its goals and commitments. Factors include the quality of the organizational structure, including skills, experiences, programs, systems and other vehicles that enable the organization to operate effectively and efficiently on an ongoing basis.

Completeness of VisionMarket Understanding: Ability of the vendor to understand buyers’ wants and needs and to translate those into products and services. Vendors that show the highest degree of vision listen to and understand buyers’ wants and needs, and can shape or enhance those with their added vision.

Marketing Strategy: A clear, differentiated set of messages consistently communicated throughout the organization and externalized through the Web site, advertising, customer programs and positioning statements.

Sales Strategy: The strategy for selling products that uses the appropriate network of direct and indirect sales, marketing, service and communication affiliates that extend the scope and depth of market reach, skills, expertise, technologies, services and the customer base.

Offering (Product) Strategy: The vendor’s approach to product development and delivery that emphasizes differentiation, functionality, methodology and feature sets as they map to current and future requirements.

Business Model: The soundness and logic of the vendor’s underlying business proposition.

Vertical/Industry Strategy: The vendor’s strategy to direct resources, skills and offerings to meet the specific needs of individual market segments, including vertical markets.

Innovation: Direct, related, complementary and synergistic layouts of resources, expertise or capital for investment, consolidation, defensive or pre-emptive purposes.

Geographic Strategy: The vendor’s strategy to direct resources, skills and offerings to meet the specific needs of geographies outside the “home” or native geography, either directly or through partners, channels and subsidiaries as appropriate for that geography and market.