Made of Money Project in a Box

21

Made of Money Made of Money Made of Money Made of Money Supporting Vulnerable Women to Rebuild Their Finances Project In A Box A toolkit for running financial education work for women accessing domestic violence services In 2012 - 13 QSA received funding from NIACE through the Community Learning Innovation Fund (CLIF) to pilot running Made of Money with women accessing domestic violence services and staff within these organisations. All grant recipients were asked to produce a ‘Project in a Box’—a toolkit to reproducing their project. This is ours, which outlines the aims of the project, how it was run, and a selection of resources, as well as details on how to access further trainings.

description

The Made of Money Project in a Box toolkit provides ideas and learning from the pilot of our Women's Project.

Transcript of Made of Money Project in a Box

Made of MoneyMade of MoneyMade of MoneyMade of Money Supporting Vulnerable Women to Rebuild Their Finances

Project In A Box A toolkit for running financial education work for women

accessing domestic violence services

In 2012 - 13 QSA received funding from NIACE through the Community Learning Innovation Fund (CLIF) to pilot running Made of Money with women accessing domestic violence services and staff within these organisations. All grant recipients were asked to produce a ‘Project in a Box’—a toolkit to reproducing their project. This is ours, which

outlines the aims of the project, how it was run, and a selection of resources, as well as details on how to access further trainings.

All photos are from our capacity building workshops. Photos by Dena Younkin and Quaker Social Action. Images by Sebastien Braun The creation of new material by Quaker Social Action for the Made of Money learning community has been financed by the Skills Funding Agency through the Community Learning Innovation Fund managed by NIACE. Copyright in this material is vested in the Crown but it is made freely available for others to use under the terms of the Open Government Licence. Full details are available at http://www.nationalarchives.gov.uk/doc/open-government-licence/.

Summary of the project

Made of Money is an established family learning project which brings groups of low-income parents together to share and learn new skills, knowledge and build confidence about managing family finances. We help parents and their children understand and minimise the stress and fear which accompany living on a low income, and we help them recognise and challenge advertising and consumerist pressures. Parents practise and learn to communicate better about money with family and with institutions like banks and energy suppliers. For the past four years we’ve shared Made of Money with other organisations across the U.K. They are now using our methodology to support individuals and households across the country. We’ve now successfully adapted this approach to support women accessing domestic violence support. We have delivered workshops to 59 women and supported 29 workers in these settings through capacity building trainings, to learn new skills and knowledge which they are now using to support their clients on a daily basis. In total, through our main grant and additional funding from NIACE, we worked with 12 organisations in east London and trained one partner visiting QSA from Los Angeles. The women who participated reported feeling more confident, less stressed and more knowledgeable about their money situations. The staff we trained have already worked with over 230 clients, and report being ready to share what they’ve learned with colleagues, as well as continuing to use this approach in the future. As an organisation we now have gained the skills, knowledge and experience in working with people learning difficulties through our pilot group at a refuge for women with learning difficulties, and those making the transition to independence. We are confident that we will be able to use this experience to reach more groups of women and staff through other refuges and domestic violence organisations across London and the U.K.

A short summary of the project

timetable

The programme began in September 2012. The initial phase was spent meeting partners who had expressed an interest in the project as well as potential new partners, to discuss the programme. As part of this we assessed the needs of the organisation, staff, and clients to support the development of the programme. In November we began to run a series of three focus groups through refuges, with a total of 23 women within refuges, and five staff members. Later in the month we ran our pilot group with Beverly Lewis House, a refuge for women with learning difficulties. At the same time, based upon our meetings and focus groups, we adapted our client and staff trainings for the programme. This consisted of pairing down our six week parent workshops into a three week programme, and the two day facilitator training into a one day capacity building training for staff. In January we began delivery of the main programme, with two capacity building trainings and two sets of workshops for women accessing domestic violence services. Between January and May we delivered a total of four capacity building trainings—three through our primarily programme and one through additional funding by NIACE. From January to July we ran nine sets of workshops for clients. Review of the programme took place throughout, alongside impact collection for both strands of the programme. In July we were able to more thoroughly analyse the data we had collected, to review the work and prepare the final reporting.

The financial resources required to run the programme

The financial resources for delivery would depend upon the scope of the project and the

organisation running the programme. In running this as part of Made of Money’s work, we

had the equivalent of 3 day a week dedicated worker for management and delivery of the

programme.

In addition, our budget covered:

� Publicity—much of the initial publicity to recruit partners too place over

phone, email, and through meetings. We produced publicity for the client

workshops which were circulated to organisations to use. In addition the

project was publicised on our website and using social media.

� Resources for clients—we gave each woman attending the workshop

relevant handouts, which we printed in house.

� Additional client costs—we covered travel where needed, refreshments for

training, childcare, and translation. This varied between groups, with some

needing no additional support, whilst for others we ran a crèche or provided

a dedicated translation. We also hired a space for one set of workshops.

The cost of this would vary depending upon need and local rates for

services.

� Resources for staff training. Each organisation attending the training

received a box of session plans and resources, which cost £47 in stationary

alone, and were produced

in house. We also

supplied facilitator packs

to everyone who

attended, again produced

in house at minimal cost.

Refreshments were also

provided.

� Travel would depend

upon the location and cost

of local travel.

� In addition the budget

covered central costs

which again would

depend upon the

organisation running the

programme and volunteer

expenses for

administrative support.

Made of Money workshops will be run here on Thursdays

January 17, 24, and 31 from 10am to 12pm

Please join us for all three sessions!

Session plans and learning resources developed through the programme

The session plans and resources used in the delivery of the programme have been

adapted form Made of Money’s core sessions and 2 day facilitator programme. A sample

of resources and session plans, adapted for the project, are found here. To find out more

about our programme, including how to access our full trainings and resources, please

contact us on 020 8983 5043, or by emailing [email protected]. More

information is on our website, www.quakersocialaction.com/madeofmoney,

Made of Money Session 1: Budgeting

Session Plan (2 Hours)

Objectives of the Session: • Doing a Money Plan: how and why? • Examine our spending habits and spending triggers • Look at our emotions around money

Activity Materials Time (mins) 1 Welcome & Taste Test

(e.g. Jaffa Cakes)

- Test items - Taste Test Cards

15 (15)

2 Group Contract (if you do not have a set one for the group)

-Flip chart -Markers -Blu Tack

10 (25)

3 Jelly-Bear Money Trees—how do we feel about our financial situation?

- Jelly Bear Money Tree handouts

- Coloured pencils/pens

10 (35)

4 How do we get there? What are the key elements to managing our money well?

- Flip chart - Flip chart pens - Managing Money Cheat Sheet

10 (45)

5 Element 1: Make a Money Plan Why do a budget? Give out Money Plans (budgets)

- Doing a Money Plan handouts - Budget Cheat Sheet

20 (1h 25)

Break if needed 10 minutes (1hr 05mins)

6 Element 2: Keep Track of Your Spending Spending Diaries

- Spending Diaries - Spending Diaries Cheat Sheet

10 (1h 35)

7 Element 3: Understand why you spend money the

way you do What Influences our Spending?

-What Influences our Spending? cards

15 (1h 50)

8 Wrap up

10 (2h)

Made of Money Session 1: Budgeting

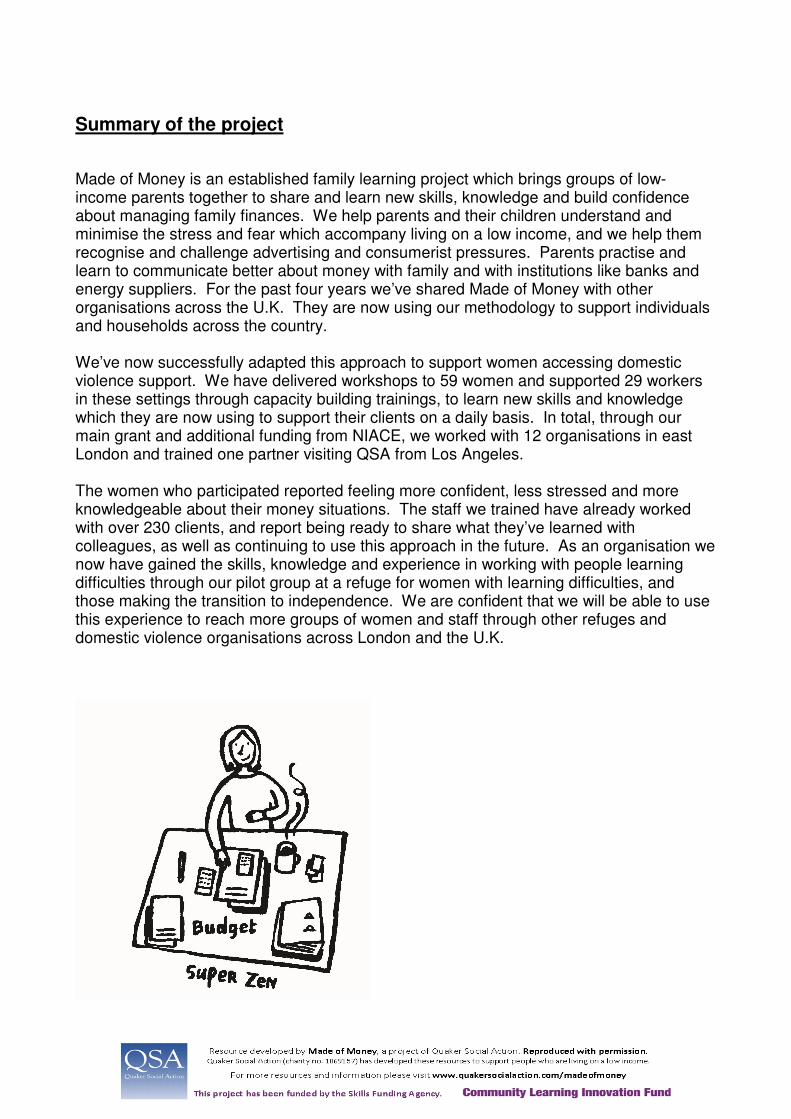

FACILITATOR CHEAT SHEET

Elements to Managing Money Have the group discuss what is needed to manage their money well. Encourage them to think about both practical elements and the emotional side of money. The sessions will then support 7 key elements dealt with in the 3 sessions. Other key elements, such as maximising income, as not covered as require specialist advice. Below are some prompters if needed with the group. Practical Elements

• Make a budget • Know how much you are spending—use a spending diary • Think about ways to save money • Maximise your income—get your benefits checked, look at other options where

possible such as starting / going back to work • Understand credit options if needed • Deal with any debts • Decide if you prefer to use cash or cards

Emotional Elements

• Understand why you spend money • Know your money “triggers”—emotions, or situations, which mean you are more

likely to spend money you don’t need to • Realise the pressures family, friends, and children place on you around money • Be aware of external factors to your spending such as the influences of

advertising • Be aware of the things you need, and those you want but don’t need

8 Key Elements Covered in the Sessions

• Element 1: Make a money plan • Element 2: Keep track of your spending • Element 3: Understand why you spend money the way you do • Element 4: Save money where you can • Element 5: Know your saving options • Element 6: Identify changes we need to make • Element 7: Understand different types of credit • Element 8: Deal with debts

I have no money to spend. I was left with all of

these debts in my name, that I never knew about in the

first place.

What influences our spending? These are additions that were added to our

standard cards for the course I’m used to spending a lot more

than this! I had to give up work to come here, and it’s the first time I’ve ever been on benefits.

Managing my money is new to me, and sometimes I just lose

track of what I’m spending

There isn’t enough money coming in. The benefits still

aren’t being paid to me

I feel really guilty about what the children have been

through, so want to make it up to them

Made of Money Page 1 Session 2: Saving Money

Session Plan (2 Hours)

Objectives of the Session: • Examine spending habits & household finances • Look at ways to save money • Understand basics of switching utility tariffs or providers to save money • Think about changes to make, and ways to go about these

Activity Materials Time (mins)

1 Welcome & Taste Test (e.g. Hula Hoops)

- Test items - Taste Test Cards

10 (10)

2 Group Contract review

-Group contract from last week - Blu-tack

5 (15)

3 Spending Diary & Money Plan Review if running as a follow on session

10 (25)

4 Element 4: Save Money Where You Can Household Finance & Money Saving

- Money Saving Tips cards 15 (40)

5 Saving Money on Utility Bills—True False

- Saving Money on Utility Bills Statements - True and False Cards

15 (55)

Break if needed 10 minutes (1hr 05mins)

6 Element 5: Know Your Saving Options Saving Brainstorm—Where can we save our money? NB: people may want to get advice on best form of saving—we cannot provide this individual advice

- Savings cheat sheet 10 (1h 15)

7 Savings—pros and cons NB: people may want to get advice on best form of saving—we cannot provide this individual advice

- Which Savings Is Best for Me? Activity Cards and Cheat Sheet

15 (1h 25)

8 Element 6: Identify Changes We Need To Make

- Changes I Want to Make handout

15 (1h 40)

9 Wrap up

10 (1h 50m)

Made of Money Session 2: Savings

True or False

Saving Money on Utility Bills Place the True sign on one side of the room, and the False sign on the other. Have the group stand up in the middle of the room. Read out each statement, and ask people to stand by the True sign if they think this is true, or the False sign if False. Ask someone to explain why they are standing where they are, and supplement with additional information if needed. If you do not have space for this, then read out the statements and have people say if they are true or false. The only way to save money on my gas or electricity bills is by using less energy. False: Many people can save money by switching utility provider, or tariff with the same provider. But you can also save money by reducing your usage. If I’m on a low income I can get help with my bills. True: If you are on a low income and in receipt of certain benefits if are eligible for the Warm Home Discount. This is a rebate of £130 off your electricity bill. To find out if you qualify, contact your electricity provider or the Home Heat Helpline. If I switch utility provider my energy supply could be disconnected. False: There is no danger of disconnection if you switch. If I’m on a water meter I could get my bills capped. True for some people: If you are in the Thames Water area, and on a water meter, you might be eligible to have your bills capped. This can be if you have 3 or more children living at home for whom you receive child benefit, or someone in the house has a medical condition which means they use more water than normal. Other water companies may run the same scheme. Contact your water company for details. If I switch utility provider my energy supply I need a new meter. False: Your meter stays the same if you switch. Switching energy provider changes the gas or electricity I receive into my home. False: Only your bill will change if you switch. Turning your thermostat down by only one degree centigrade can cut the cost of your heating by 10 per cent. True: Turning down your heating just one degree can save you up to 10% of your heating bill. If you have a baby, small children, or someone who is ill at home get advice on the ideal temperature. For others, 21 degrees is said to be a good temperature. Putting on extra clothes will ensure you stay warm.

Made of Money Session 2: Savings

I can switch utility providers if I have a debt with them. True depending upon how much debt you have: You can switch even if you have a debt of up to £500. There is no help available if I have utility debts. False: There are grants available to help clear utility, including water, debts. Not everyone is eligible, but it is worth finding out about. Contact a debt advisor to find out if you are eligible to apply. You can also ask your utility provider who may be able to tell you more. I can compare energy prices online. True: There are a number of sites that will help you to compare energy providers’ prices. I can’t switch providers if I’m on a key meter False: You can switch tariffs or providers regardless of your payment method. If we all turned off our TVs instead of keeping them on stand-by, we could shut down a couple of power stations in the UK. True: Appliances left on standby can use as much as three quarters of the energy they use when they are fully switched on. Turn off items on standby, unplug your phone charger when done, and turn off lights when not in use.

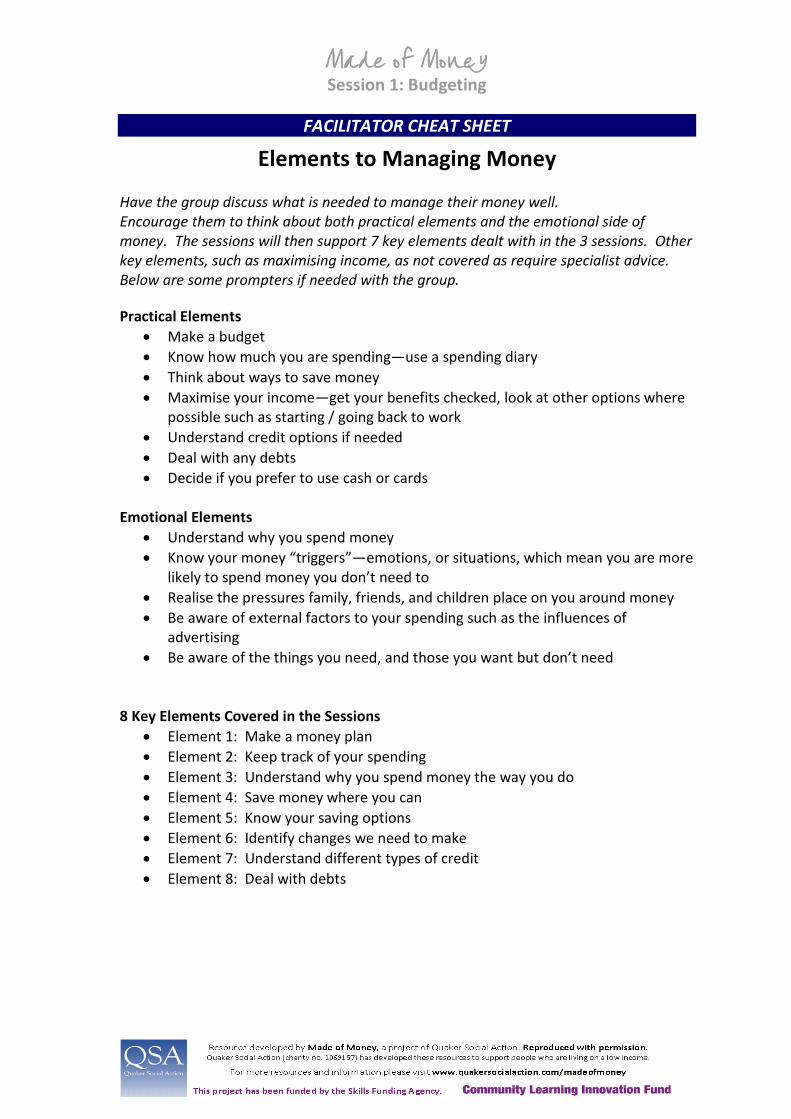

Made of Money Session 2: Savings

Changes I Need To Make

Think about changes you need to or want to make about your finances. They could be something practical, or something related to how you feel about money.

Now choose one change you want to make first:

Now think about what steps you need to take to make this change. Think about who you may need to involve, or ask for help, if needed. Where will you go for this? What do you

need to start doing? What do you need to stop? Which of these will you do first?

Made of Money Session 3: Credit and Debt

Session Plan (2 Hours) Objectives of the Session:

• Explore the different types of credit • Raise awareness of types of credit and the consequences • Raise awareness of the cost of credit • To discuss the impact of credit and debt on self and family • Raise awareness of types of debt and the consequences • Discuss what one should and shouldn’t do when in debt

Activity Materials Time (mins) 1 Welcome

2 Spending Diary & Money Plan Review if running as a follow on session

10 (10)

3 What is credit? Discussion

- Flipchart - Different Types of Credit cheat

sheet

15 (25)

4 Comparing Cost of Credit & APRs- TV Exercise

- How Much Would You Pay For A Flatscreen TV? Cards and handout

20 (45)

5 Jargon Busters

- Jargon Buster cards and cheat sheet

15 (1h 5)

6 Priority/Non Priority Debt Game

- Priority/Non Priority Game cards and cheat sheet

15 (1h 25)

7 Debt - Dos and Don’ts

-Debt Dos and Don’ts cards and cheat sheet

15 (1h 40)

8 Final Evaluation Forms and Certificates

- Final Evaluation forms - Certificates

15 (1h 55)

9 Wrap up

5 (2h)

Evaluation tools

The methodology and tools used to capture evidence were based upon those that we use in the general Made of Money programme. They are tried and tested, having been honed since the inception of the project and further developed with the support of an external evaluator. We find them to be very effective at capturing the impact as related to our outcomes for both local and national work, as well as in capturing learner satisfaction with our approach and support. Using the same tools will enable us to compare learning between this project and that of our main strands of work.

Top tips for anyone wishing to replicate the project

The key factors for success we identified were:

� Strong partnerships—We had very good

relationships with the partners, all of

whom are organisations doing great

work in the field. They were very

experienced and able to speak

knowledgeably about the needs of their

clients, speak openly about their own

staff needs, and support us where we

had questions about the work.

� Good communication—Communication

was key in working with a wide range of

partners, to ensure that sessions went

according to plan or that changes could

be made in advance where needed.

This was also key for ensuring that the

right people came on the staff training,

who would benefit the most and best be

able to use it with their clients.

� Solid training—Our experience in delivering financial education over the past 7 ½

years was very useful, as it meant we could use this to tailor the workshops to the

client groups. We were able to retain resources we knew worked across a wide

range of groups, whilst developing new resources / tailoring others where needed.

� This same knowledge allowed us to tailor our facilitator training into a 1 day

capacity building training, which the staff we trained found to be fun, engaging, and

useful for them to take forwards in their work.

� Skilled facilitators—QSA’s skilled facilitators with strong experience of delivery

meant that we were able to take on the challenges faced within some groups, and

offer them the best support we were able to, for both clients and staff.

� Funding for translation and childcare—This enabled us to widen access to the

course.

� Funding to offer the staff training and resources for free—this enabled a wide range

of organisations with limited budgets the opportunity to join the programme, and

meant that multiple staff within organisations were able to be trained, something we

know increases use of the learning in the future.

The project objectives and planned outcomes for learners, and the

difference the project made to learners, communities, and other

stakeholders

The primary aims of the programme were:

� To provide tailored financial capability training and support to east London women

leaving abusive relationships, giving them skills and confidence to cope with the

economic challenges they face.

� Leave a sustainable legacy by training partner agencies to provide day to day

support around financial management.

Within these our objectives and outcomes were to:

� Increase financial awareness and control—Improved day-to-day management of spending, saving, paying bills and budgeting.

� Increase financial inclusion—Greater understanding of financial products (bank accounts, affordable credit) and reduced risk of debt.

� Raise confidence and self-esteem—Improved mental wellbeing and greater independence.

� Leave a legacy of skills and capacity in partner agencies and QSA around financial literacy for women with experience of violence—A more capable workforce with specialist knowledge and confidence to support women in crisis around their finances.

� QSA will benefit from establishing a specialist short course and group of partnerships that we can integrate into our portfolio of work in east London, and our national partnership training.

Increase financial awareness and control-- Improved day-to-day management of spending, saving, paying bills and budgeting. Through the programme we delivered workshops directly to 59 women. Workshops lasted for three sessions, and covered budgeting, saving, credit, and debt, whilst also supporting learners to explore their values and attitudes towards money, set goals, and build confidence regarding managing their finances. Of women who filled in the final evaluation form:

• 95% said they were more in control of their finances

• 92% said they were managing money better

• 65% were budgeting and keeping a spending diary, and 35% planned to

• 96% were better off financially each week

• 61% had cut their spending, 39% planned to

“I learned how to save money. I know I need to save and how to manage my money better after everything I’ve learned”

“I feel good to know how I can wisely spend my money.” “I feel better since I have been saving my money-each week I have been saving £10-£12. I have been saving a lot of money for weekly shopping and groceries” We ran four capacity building training for 29 workers. In the post course evaluation, all workers agreed or strongly agreed that:

• The training has given me new skills and information to support my clients;

• The course has increased my confidence to help my clients around their finances;

• I expect the course will give my clients better control over their finances;

• I expect the course will be able to give my clients a better understanding of money management

19 people responded to a follow up survey in July—1 and 6 months after the trainings were run. Between them they had used the information with 230 clients. As a result of this:

• 79% felt the clients they had worked with were managing money better

• 58% felt the clients they had worked with were less stressed about money

• 53% felt the clients they had worked with were more in control of their money

“The women at the refuge have become savvy shoppers. I noticed women buying supermarket own brand items. As staff we have done the same too. The women are able to visualise where each penny is spent. Women have a better understanding of managing money and choices around money.” “We used the program in conjunction with our job training course, so this information has help these women prepare for employment and prepare to move off benefits.”

Increase financial inclusion--Greater understanding of financial products (bank accounts, affordable credit) and reduced risk of debt. Of women who attended our course and filled in the final evaluation form:

• 87% said they were more confident to deal with banks / businesses;

• 9% were opening a new account, 57% planned to (for most this was a savings account as refuges had helped them to sort out a basic account)

• 65% were saving, 35% planned to—helping to reduce the risk of debt in the future.

• 14% of women were getting advice regarding debts (most likely through support by the refuge) but importantly 52% now planned to get advice on debts (the remaining did not indicate a need to)

• The same number indicated they were, or planned to, pay off / reduce debts

“It has given me motivation for other areas of my life, and to correct my debts and borrowing.” “I didn’t have a great start in life but I feel there is hope for everyone in debt.” “I have learned how to deal with debt.”

For more information on this project, and our Made of Money facilitator trainings, please contact us:

Made of Money, Quaker Social Action

www.quakersocialaction.com 020 8983 5043

Project Partners

Aanchal Women's Aid An east London based women's organisation that assists women across the UK affected by physical as well as mental, financial, sexual and emotional domestic abuse. Beverley Lewis House a unique and specialist housing project run by East Thames, which provides a safe environment for women with learning disabilities, who might also have additional or complex needs. Downtown Women’s Project provide permanent supportive housing in Los Angeles and a safe and healthy community fostering dignity, respect, and personal stability, and to advocate ending homelessness for women. Hackney Asian Women's Aid Provides refuge accommodation to Asian women and children fleeing domestic violence.

Hestia Housing Association. Hestia provide support to women experiencing domestic violence across 12 London boroughs including Hackney where we worked with them. Latin American Women's Aid supports women from Latin America or other Spanish/Portuguese speaking countries and their children who are fleeing from domestic violence through advice, advocacy and emergency accommodation. NIA provides high quality services to women, children and young people who have experienced gender-based violence and abuse. We ran workshops through their general services and with the Emma Project, providing refuge and outreach services to women with substance misuse problems who have experienced gender based violence. Newham Action Against Domestic Violence is a small charity supporting adults and children to leave abusive relationships, working in Newham for over 20 years, providing access to shelter and safety, legal advice and representation, counselling and support. Tower Hamlets Parental Engagement Team Newham Women's Refuge is a shared supported housing scheme run by East Thames, for women fleeing domestic violence in a personal or family relationship. Solace A London based charity with a primary focus supporting women and children affected by domestic and sexual violence. Tower Hamlets Refuge provides refuge accommodation in Tower Hamlets, run by Hestia Housing Association. Tower Hamlets Asian Women’s Aid, a refuge for Asian Women, run by Hestia Housing Association.