Macroeconomic Policy in the Asia- Pacific GECO 6400 Monetary Policy Monetary Policy.

55

Macroeconomic Policy in Macroeconomic Policy in the Asia-Pacific the Asia-Pacific GECO 6400 GECO 6400 Monetary Policy Monetary Policy

-

Upload

william-harrison -

Category

Documents

-

view

232 -

download

3

Transcript of Macroeconomic Policy in the Asia- Pacific GECO 6400 Monetary Policy Monetary Policy.

Macroeconomic Policy in the Macroeconomic Policy in the Asia-PacificAsia-Pacific

GECO 6400 GECO 6400

Monetary PolicyMonetary PolicyMonetary PolicyMonetary Policy

ReviewReview

Last lecture we defined the concept of Last lecture we defined the concept of money.money.

We looked at how banks can create We looked at how banks can create deposits and expand the money supply.deposits and expand the money supply.

We introduced the money multiplier.We introduced the money multiplier.

This weekThis weekThe major focus is on Monetary Policy (MP).The major focus is on Monetary Policy (MP).

New concepts include:New concepts include:– Exchange Settlement Accounts;Exchange Settlement Accounts;– Open Market Operations; andOpen Market Operations; and– Cash Rate. Cash Rate.

We will evaluate MP & FP.We will evaluate MP & FP.

Let’s start with money market … Let’s start with money market …

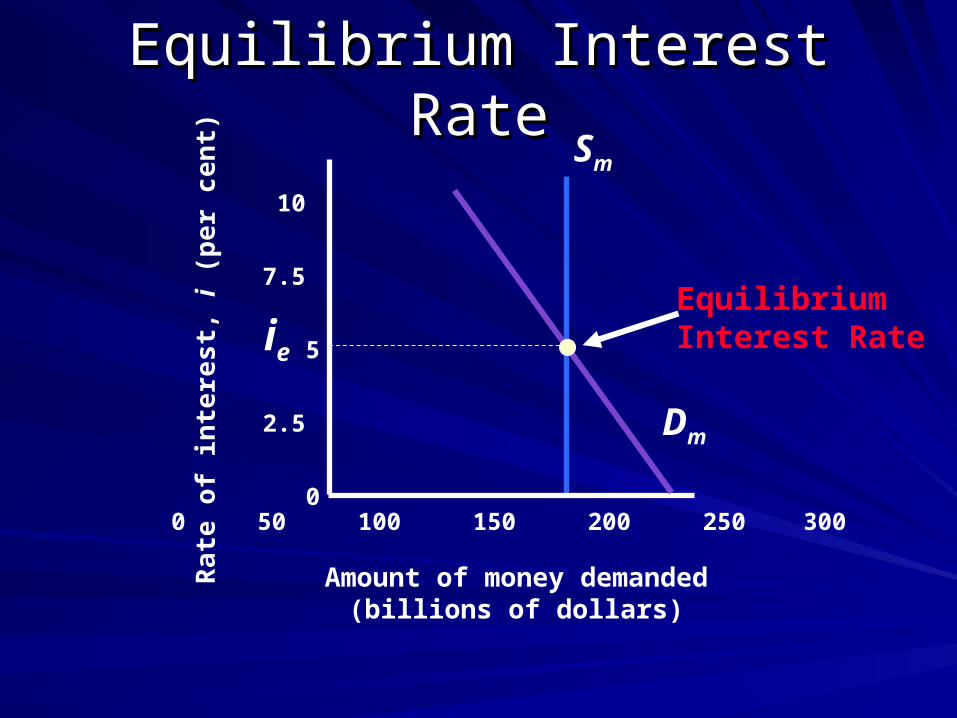

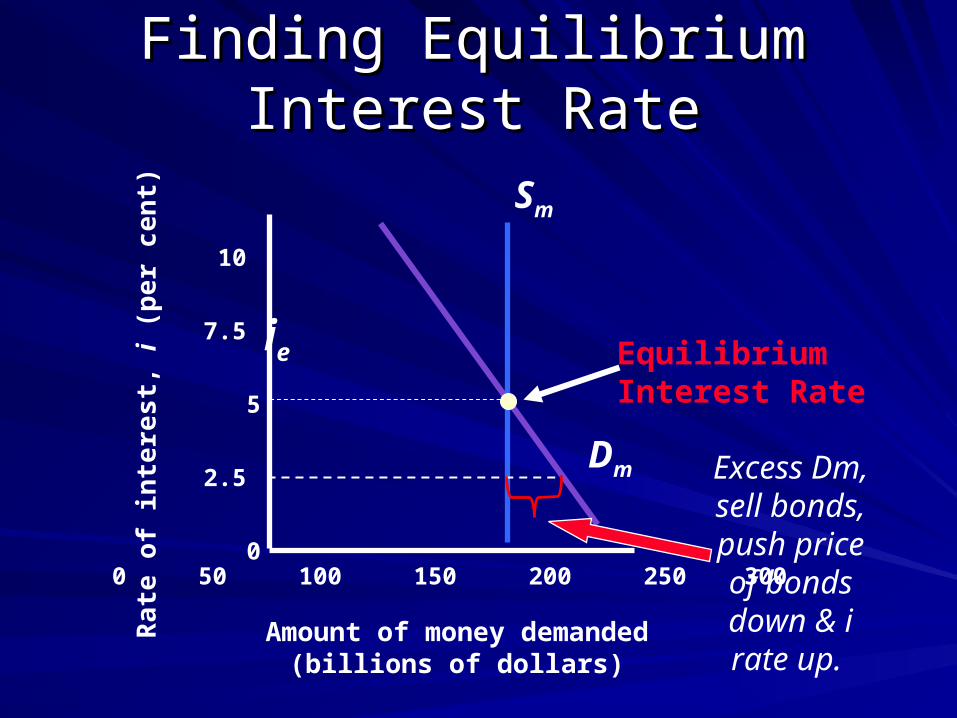

Last week discussed money supply & introduced Last week discussed money supply & introduced money demand. money demand.

Achieved equilibrium at that interest rate where Achieved equilibrium at that interest rate where money demand equals money supply.money demand equals money supply.

Saw that we hold money as an asset when Saw that we hold money as an asset when interest rate is low but what assets might we interest rate is low but what assets might we hold when interest rate is high?hold when interest rate is high?

Sm

Equilibrium Interest RateEquilibrium Interest Rate

Ra

te o

f in

tere

st,

i (p

er c

en

t)

Amount of money demanded(billions of dollars)

10

7.5

5

2.5

0

Dm

ie

0 50 100 150 200 250 300

Equilibrium Interest Rate

BondsBondsCentral banks use bonds in the operation of Central banks use bonds in the operation of Monetary Policy.Monetary Policy.

A bond represents a promise by the issuer of the A bond represents a promise by the issuer of the bond to make a sequence of future payments & bond to make a sequence of future payments & eventually redeem the bond.eventually redeem the bond.

The return on a bond in percentage terms is called The return on a bond in percentage terms is called the Yield. This is the interest rate paid on the the Yield. This is the interest rate paid on the investment in a bond.investment in a bond.

Bond Yield = Annual PaymentBond Price

x 100

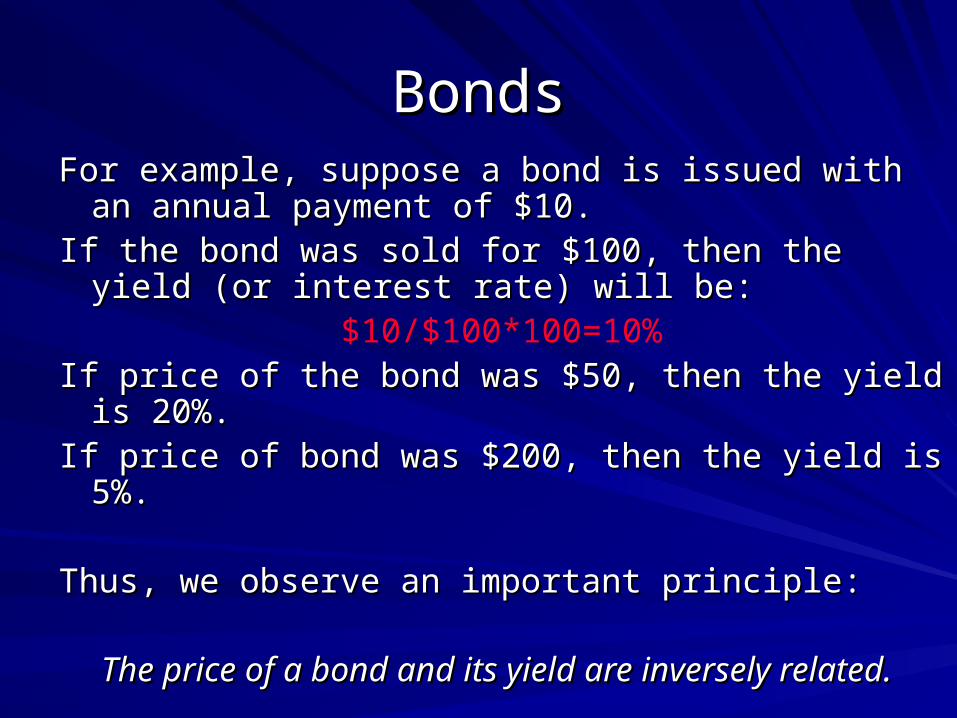

BondsBondsFor example, suppose a bond is issued with an For example, suppose a bond is issued with an

annual payment of $10.annual payment of $10.If the bond was sold for $100, then the yield (or If the bond was sold for $100, then the yield (or

interest rate) will be: interest rate) will be: $10/$100*100=10%

If price of the bond was $50, then the yield is 20%.If price of the bond was $50, then the yield is 20%.If price of bond was $200, then the yield is 5%.If price of bond was $200, then the yield is 5%.

Thus, we observe an important principle:Thus, we observe an important principle:

The price of a bond and its yield are inversely The price of a bond and its yield are inversely related. related.

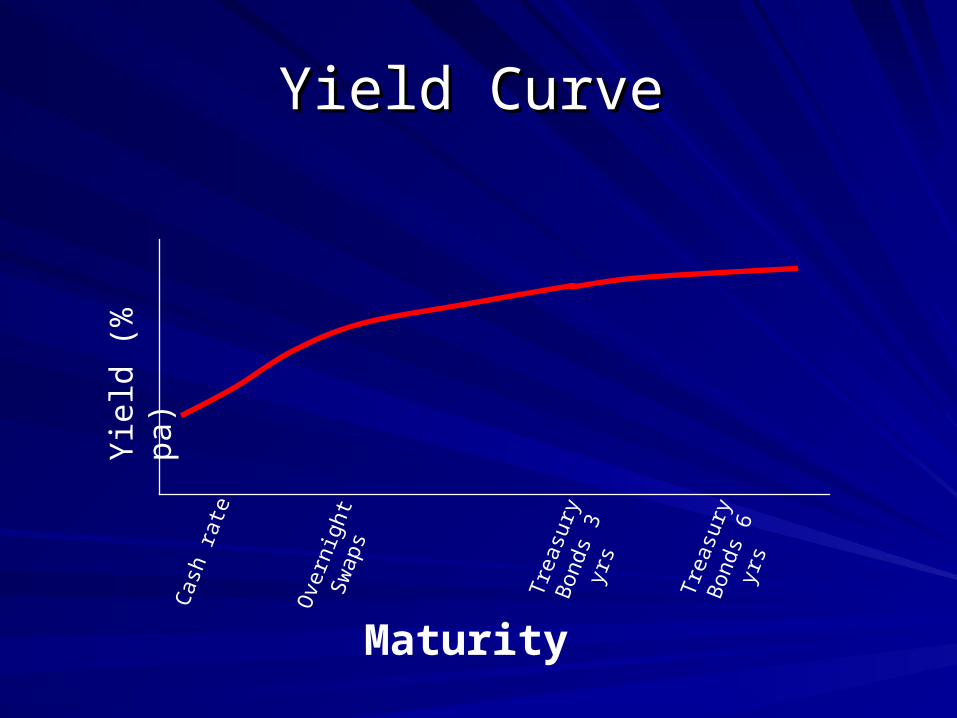

The Yield CurveThe Yield CurveYield curve plots the interest rates that apply at a Yield curve plots the interest rates that apply at a

point in time to securities of similar risk but point in time to securities of similar risk but different terms. different terms.

In practice there are many different financial assets In practice there are many different financial assets that vary in their term to maturity, their liquidity and that vary in their term to maturity, their liquidity and their risk.their risk.

In general, the longer the term, the less liquid and In general, the longer the term, the less liquid and the more risky, the higher will be the interest rate.the more risky, the higher will be the interest rate.

The interest rates shown on yield curves are The interest rates shown on yield curves are connected to one another.connected to one another.

Yield CurveYield Curve

Maturity

Yie

ld (

% p

a)

Cas

h ra

te

Ove

rnig

ht

Swap

s

Tre

asur

y B

onds

3 y

rs

Tre

asur

y B

onds

6 y

rs

Money Market and Interest RatesMoney Market and Interest Rates

Most central banks focus their Monetary Policy on the cash Most central banks focus their Monetary Policy on the cash rate and this rate in turn influences all other interest rates.rate and this rate in turn influences all other interest rates.

The cash rate and interest rates on other securities tend to The cash rate and interest rates on other securities tend to move together. This is due to 3 factors:move together. This is due to 3 factors:

1.1. Financial assets of similar maturities are substitutable for Financial assets of similar maturities are substitutable for each other. So we would expect them to have similar each other. So we would expect them to have similar interest rates. interest rates.

2.2. A change in the cash rate alters the cost of funds for A change in the cash rate alters the cost of funds for banks & this flows through to a change in the cost of credit banks & this flows through to a change in the cost of credit from banks. from banks.

3.3. If the cash rate is say 4% then any security that is more If the cash rate is say 4% then any security that is more risky or longer term must offer a higher interest rate to risky or longer term must offer a higher interest rate to induce people to hold those securities.induce people to hold those securities.

Finding Equilibrium Interest Finding Equilibrium Interest RateRate

Ra

te o

f in

tere

st,

i (p

er c

en

t)

Amount of money demanded(billions of dollars)

10

7.5

5

2.5

0

Dm

ie

0 50 100 150 200 250 300

Sm

Equilibrium Interest Rate

Excess Dm, sell bonds, push price of bonds down & i rate up.

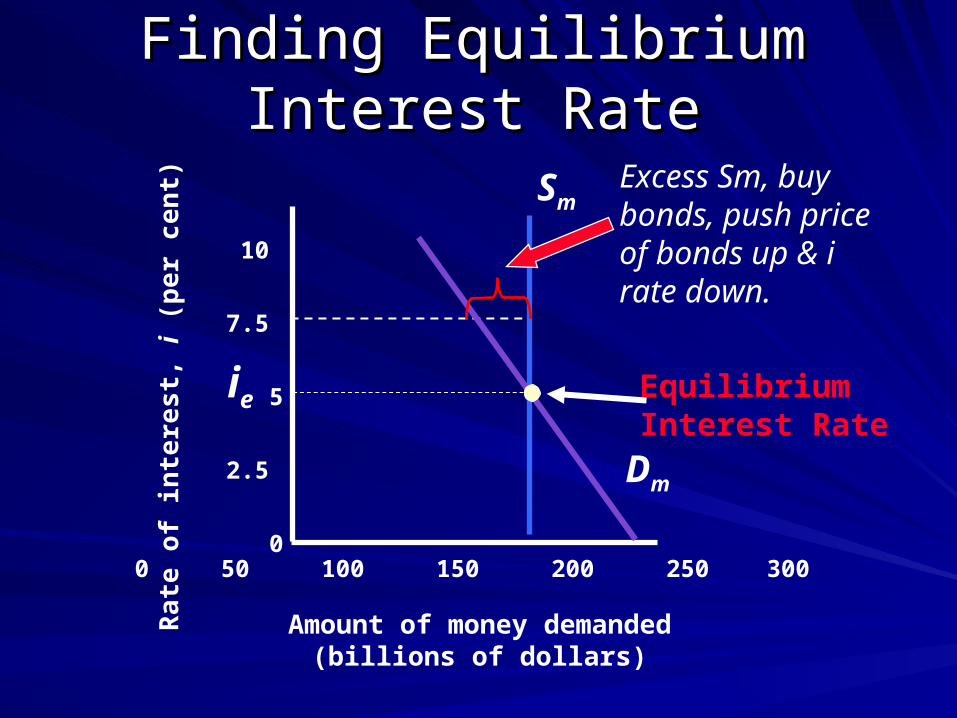

Finding Equilibrium Interest Finding Equilibrium Interest RateRate

Ra

te o

f in

tere

st,

i (p

er c

en

t)

Amount of money demanded(billions of dollars)

10

7.5

5

2.5

0

Dm

ie

0 50 100 150 200 250 300

Sm

Equilibrium Interest Rate

Excess Sm, buy bonds, push price of bonds up & i rate down.

Sm

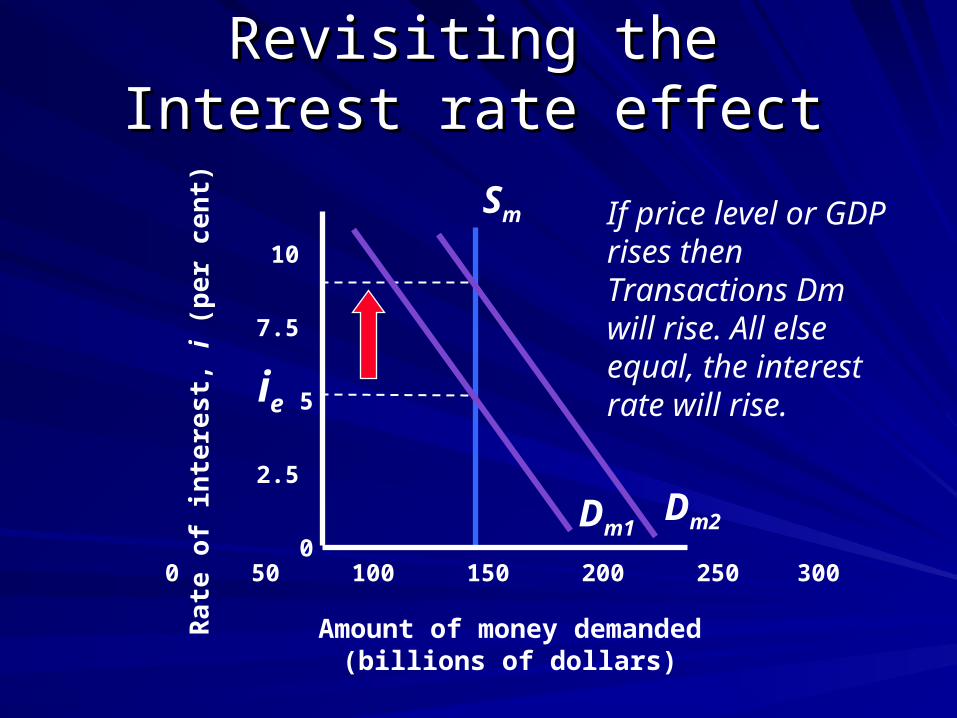

Revisiting the Interest rate Revisiting the Interest rate effecteffect

Ra

te o

f in

tere

st,

i (p

er c

en

t)

Amount of money demanded(billions of dollars)

10

7.5

5

2.5

0Dm1

ie

0 50 100 150 200 250 300

If price level or GDP rises then Transactions Dm will rise. All else equal, the interest rate will rise.

Dm2

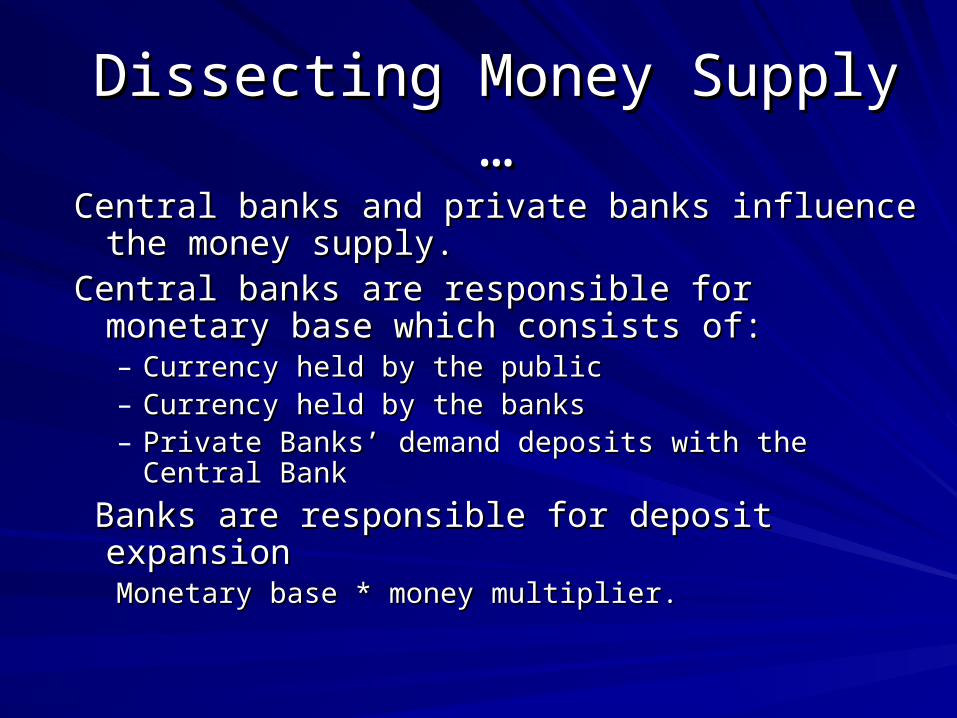

Dissecting Money Supply …Dissecting Money Supply …

Central banks and private banks influence the Central banks and private banks influence the money supply.money supply.

Central banks are responsible for monetary base Central banks are responsible for monetary base which consists of:which consists of:– Currency held by the publicCurrency held by the public– Currency held by the banksCurrency held by the banks– Private Banks’ demand deposits with the Central BankPrivate Banks’ demand deposits with the Central Bank

Banks are responsible for deposit expansionBanks are responsible for deposit expansionMonetary base * money multiplier. Monetary base * money multiplier.

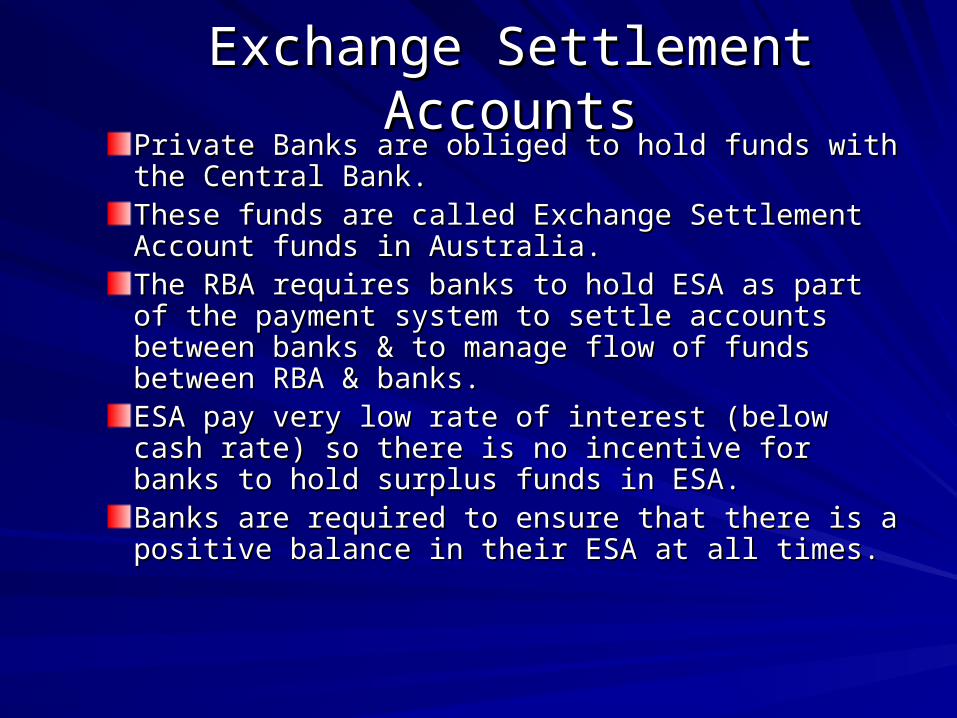

Exchange Settlement AccountsExchange Settlement AccountsPrivate Banks are obliged to hold funds with the Private Banks are obliged to hold funds with the Central Bank.Central Bank.These funds are called Exchange Settlement These funds are called Exchange Settlement Account funds in Australia.Account funds in Australia.The RBA requires banks to hold ESA as part of the The RBA requires banks to hold ESA as part of the payment system to settle accounts between banks payment system to settle accounts between banks & to manage flow of funds between RBA & banks.& to manage flow of funds between RBA & banks.ESA pay very low rate of interest (below cash rate) ESA pay very low rate of interest (below cash rate) so there is no incentive for banks to hold surplus so there is no incentive for banks to hold surplus funds in ESA.funds in ESA.Banks are required to ensure that there is a positive Banks are required to ensure that there is a positive balance in their ESA at all times. balance in their ESA at all times.

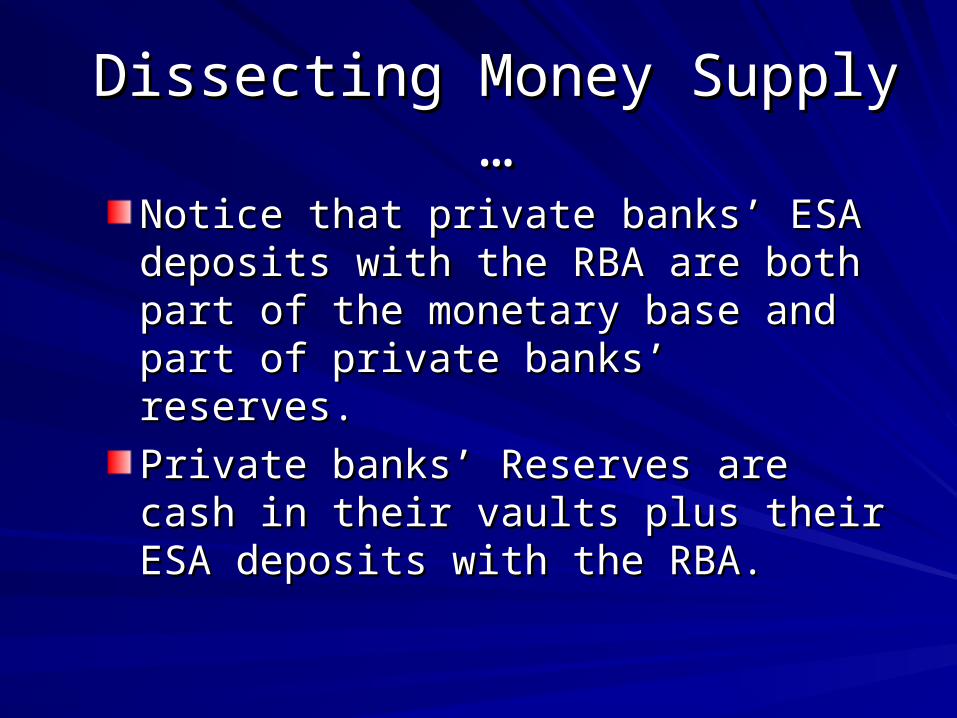

Dissecting Money Supply …Dissecting Money Supply …

Notice that private Notice that private banks’ ESA deposits banks’ ESA deposits with the RBA are both part of the with the RBA are both part of the monetary base and part of private monetary base and part of private banks’ reserves. banks’ reserves.

Private banks’ Reserves are cash in Private banks’ Reserves are cash in their vaults plus their ESA deposits with their vaults plus their ESA deposits with the RBA. the RBA.

Exchange Settlement AccountsExchange Settlement Accounts

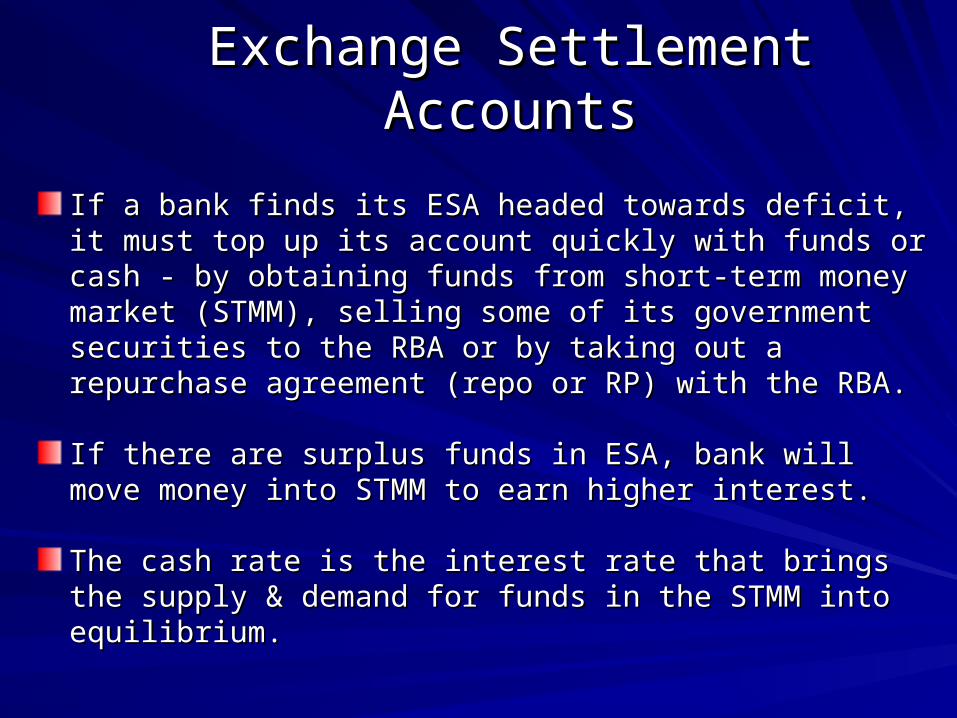

If a bank finds its ESA headed towards deficit, it must top up If a bank finds its ESA headed towards deficit, it must top up its account quickly with funds or cash - by obtaining funds its account quickly with funds or cash - by obtaining funds from short-term money market (STMM), selling some of its from short-term money market (STMM), selling some of its government securities to the RBA or by taking out a government securities to the RBA or by taking out a repurchase agreement (repo or RP) with the RBA. repurchase agreement (repo or RP) with the RBA.

If there are surplus funds in ESA, bank will move money into If there are surplus funds in ESA, bank will move money into STMM to earn higher interest.STMM to earn higher interest.

The cash rate is the interest rate that brings the supply & The cash rate is the interest rate that brings the supply & demand for funds in the STMM into equilibrium. demand for funds in the STMM into equilibrium.

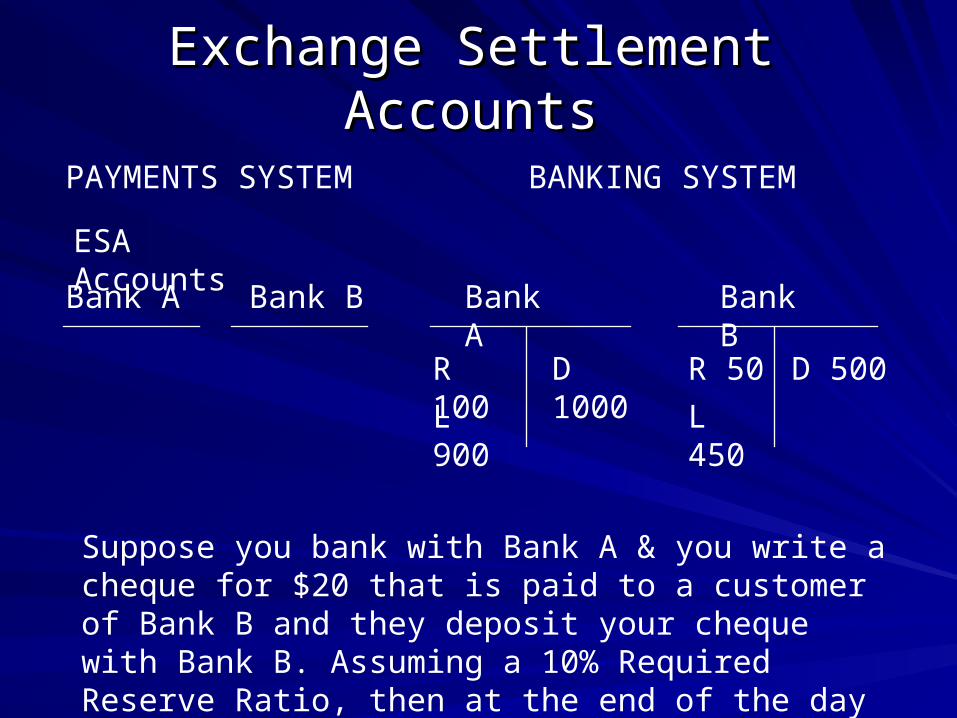

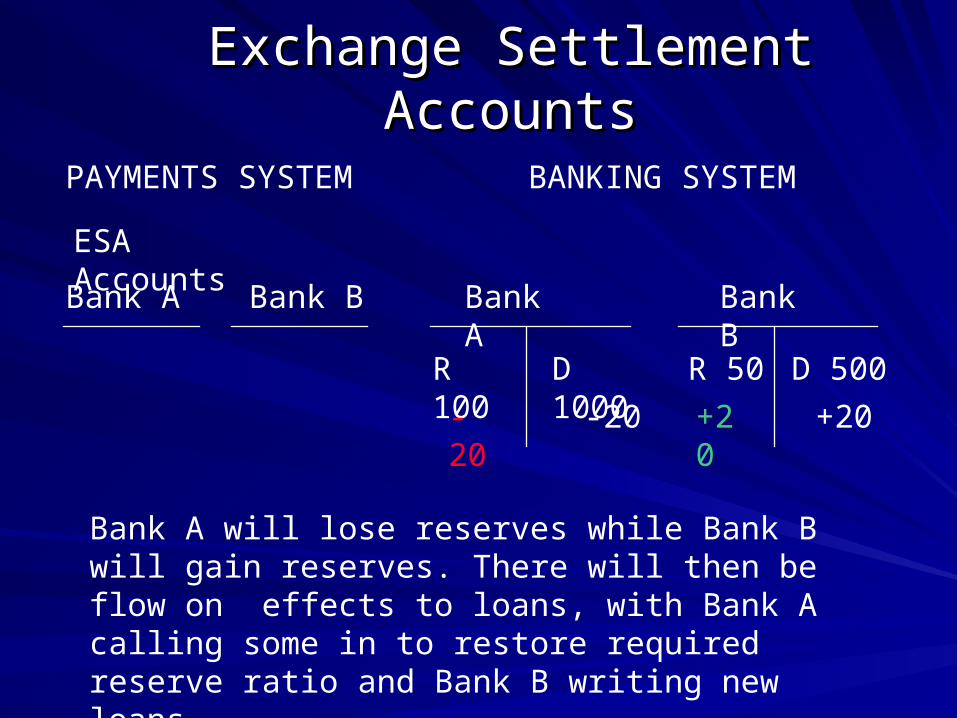

PAYMENTS SYSTEM

ESA Accounts

Bank A Bank B

BANKING SYSTEM

Bank A Bank B

R 100 R 50D 1000 D 500

Suppose you bank with Bank A & you write a cheque for $20 that is paid to a customer of Bank B and they deposit your cheque with Bank B. Assuming a 10% Required Reserve Ratio, then at the end of the day …

L 900 L 450

Exchange Settlement AccountsExchange Settlement Accounts

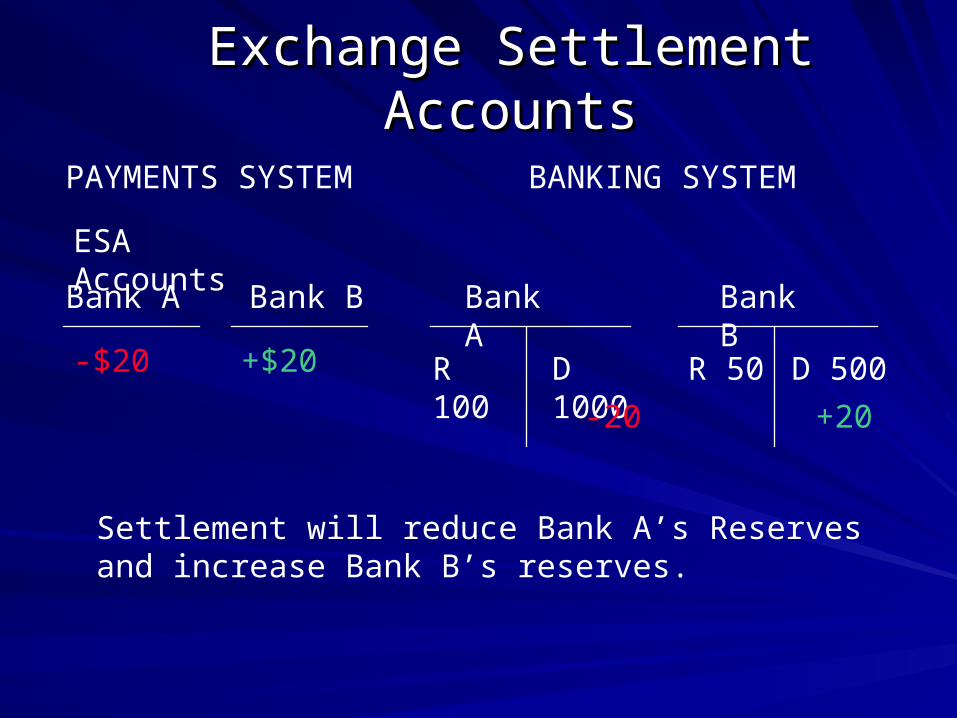

PAYMENTS SYSTEM

ESA Accounts

Bank A Bank B

-$20 +$20

BANKING SYSTEM

Bank A Bank B

R 100 R 50D 1000 D 500

Settlement will reduce Bank A’s Reserves and increase Bank B’s reserves.

-20 +20

Exchange Settlement AccountsExchange Settlement Accounts

PAYMENTS SYSTEM

ESA Accounts

Bank A Bank B

BANKING SYSTEM

Bank A Bank B

R 100 R 50D 1000 D 500

Bank A will lose reserves while Bank B will gain reserves. There will then be flow on effects to loans, with Bank A calling some in to restore required reserve ratio and Bank B writing new loans.

-20 +20-20 +20

Exchange Settlement AccountsExchange Settlement Accounts

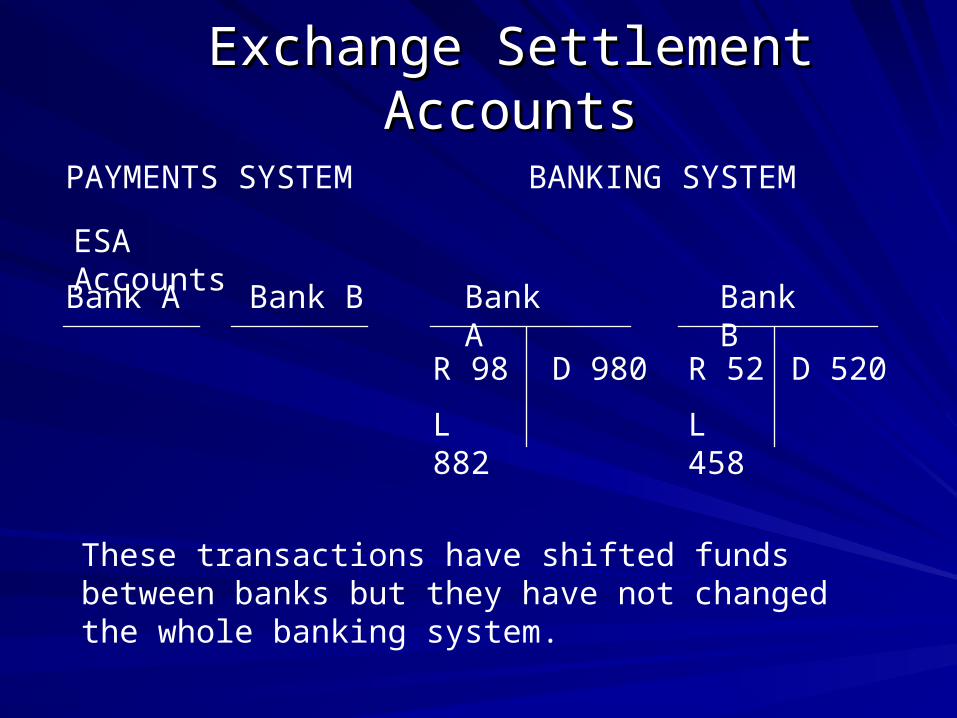

PAYMENTS SYSTEM

ESA Accounts

Bank A Bank B

BANKING SYSTEM

Bank A Bank B

R 98 R 52D 980 D 520

These transactions have shifted funds between banks but they have not changed the whole banking system.

L 882 L 458

Exchange Settlement AccountsExchange Settlement Accounts

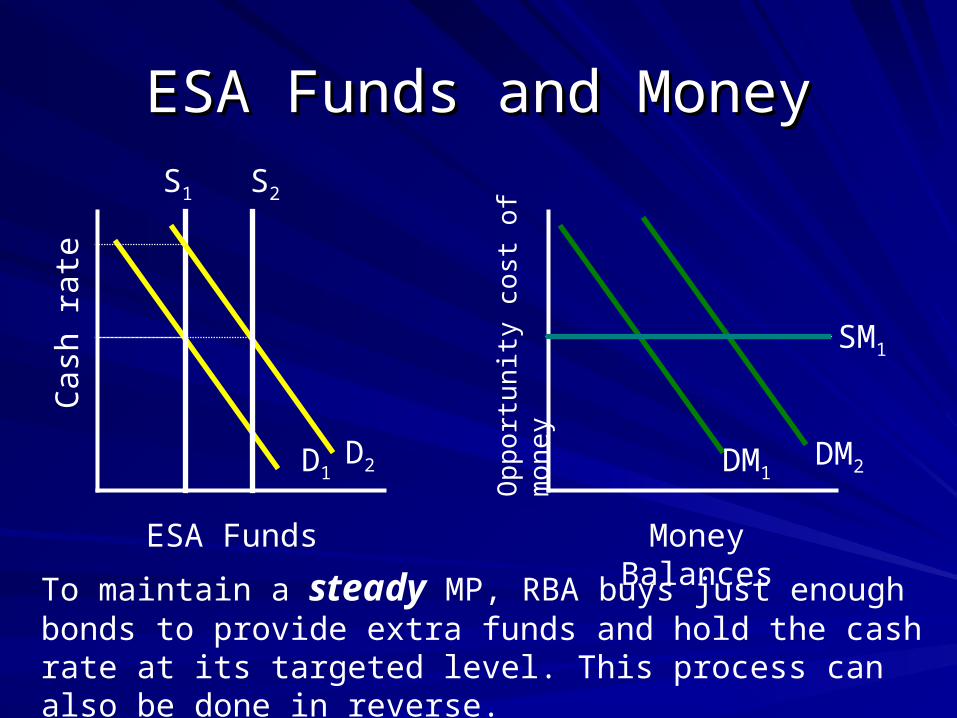

ESA Funds, Money and ESA Funds, Money and Investment FundsInvestment Funds

There is a distinction between ESA funds, money There is a distinction between ESA funds, money & investment funds.& investment funds.

ESA funds are the funds that are the subject of ESA funds are the funds that are the subject of ESA accounts and are closely connected to ESA accounts and are closely connected to money. Recall that ESA are part of monetary base money. Recall that ESA are part of monetary base but not part of M3 or Broad Money.but not part of M3 or Broad Money.

Money here refers to M3 or Broad Money. Money here refers to M3 or Broad Money.

Market for investment funds represents all the Market for investment funds represents all the markets for funds on yield curve. markets for funds on yield curve.

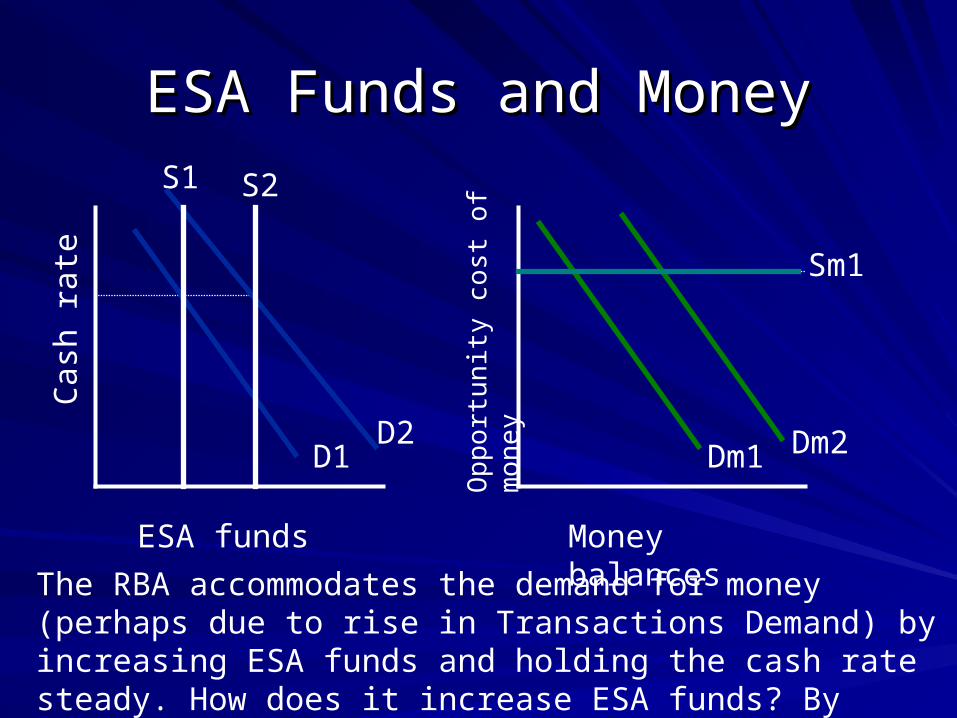

ESA Funds and MoneyESA Funds and Money

ESA funds Money balances

Cas

h ra

te

Opp

ortu

nity

cos

t of

mon

eyD1 Dm1

S1

D2 Dm2

Sm1

The RBA accommodates the demand for money (perhaps due to rise in Transactions Demand) by increasing ESA funds and holding the cash rate steady. How does it increase ESA funds? By buying government securities.

S2

Monetary Policy ObjectivesMonetary Policy Objectives

Monetary policyMonetary policyInfluencing interest rates and credit availability to:Influencing interest rates and credit availability to:– Encourage real GDP growth;Encourage real GDP growth;– Promote employment; andPromote employment; and– Stabilise the price level Stabilise the price level

Fundamental objectivesFundamental objectivesfull employmentfull employmentnon-inflationary level of total outputnon-inflationary level of total output

Central banks have responsibility for managing Central banks have responsibility for managing monetary policymonetary policy

Monetary Policy ToolsMonetary Policy Tools

Major financial securities used by Central Major financial securities used by Central Banks to determine the cash rate are:Banks to determine the cash rate are:– Open market operations (OMO)Open market operations (OMO)– Foreign exchange swaps and intervention Foreign exchange swaps and intervention

in the foreign exchange marketin the foreign exchange market– Rediscount rate & repurchase Rediscount rate & repurchase

agreements agreements

Foreign Exchange SwapsForeign Exchange Swaps

RBA may use foreign exchange swaps to RBA may use foreign exchange swaps to supplement or substitute for OMOsupplement or substitute for OMO

Foreign exchange market interventionForeign exchange market intervention——either either selling or buying Australian dollarsselling or buying Australian dollars– purchase/sale of dollars is equivalent to purchase/sale purchase/sale of dollars is equivalent to purchase/sale

of government securities, and has similar impact on of government securities, and has similar impact on banks’ ESA fundsbanks’ ESA funds

Rediscount Rate and Monetary Rediscount Rate and Monetary PolicyPolicy

The rate at which the RBA buys or sells The rate at which the RBA buys or sells short-term securities under repurchase short-term securities under repurchase agreementagreement

Can be used as a central tool of monetary Can be used as a central tool of monetary policypolicy

Open-Market OperationsOpen-Market Operations

Buying and selling of Commonwealth Buying and selling of Commonwealth government securities by the RBA in the government securities by the RBA in the cash or short-term money market cash or short-term money market

The objective of OMOs is to ensure that The objective of OMOs is to ensure that the demand and supply of ESA funds are the demand and supply of ESA funds are such that they are in balance at the target such that they are in balance at the target cash ratecash rate

Open-Market OperationsOpen-Market Operations

Buying and selling of Commonwealth Buying and selling of Commonwealth government securities by the RBA affects the government securities by the RBA affects the cash ratecash rate

Cash rate provides an indication of the RBA’s Cash rate provides an indication of the RBA’s monetary policy stancemonetary policy stance– Sustained increases in cash rate target level: Sustained increases in cash rate target level:

tightening of monetary policytightening of monetary policy

– Sustained decreases in cash rate target level:Sustained decreases in cash rate target level:easing of monetary policyeasing of monetary policy

Open-Market Operations:Open-Market Operations:Buying SecuritiesBuying Securities

Banks sell some of their securitiesBanks sell some of their securities

Expansionary Monetary PolicyExpansionary Monetary Policy

RBA pays for securities by increasing RBA pays for securities by increasing banks’ exchange settlement accounts banks’ exchange settlement accounts (ESAs)(ESAs)

Bank reserves increaseBank reserves increase– Causing the monetary base and the banks’ Causing the monetary base and the banks’

lending ability to increaselending ability to increase

Open-Market Operations:Open-Market Operations:Selling SecuritiesSelling Securities

The RBA sells securities to the banksThe RBA sells securities to the banks

Contractionary Monetary policyContractionary Monetary policy

Banks pay for securities by decreasing Banks pay for securities by decreasing their exchange settlement accounts their exchange settlement accounts (ESAs)(ESAs)

Bank reserves decreaseBank reserves decrease– Causing the monetary base and the banks’ Causing the monetary base and the banks’

lending ability to decreaselending ability to decrease

ESA Funds and MoneyESA Funds and Money

Money Balances

To maintain a steady MP, RBA buys just enough bonds to provide extra funds and hold the cash rate at its targeted level. This process can also be done in reverse.

ESA Funds

Cas

h ra

te

D1

S1

D2

S2

Opp

ortu

nity

cos

t of

mon

ey

DM1DM2

SM1

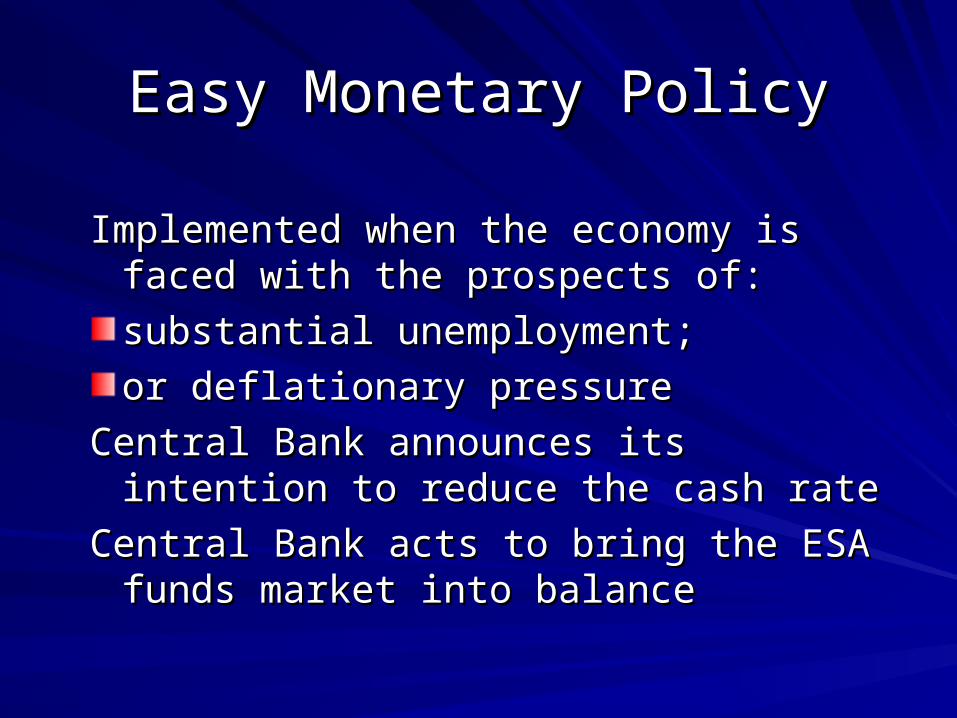

Easy Monetary PolicyEasy Monetary Policy

Implemented when the economy is faced Implemented when the economy is faced with the prospects of:with the prospects of:

substantial unemployment;substantial unemployment;

or deflationary pressureor deflationary pressure

Central Bank announces its intention to Central Bank announces its intention to reduce the cash ratereduce the cash rate

Central Bank acts to bring the ESA funds Central Bank acts to bring the ESA funds market into balancemarket into balance

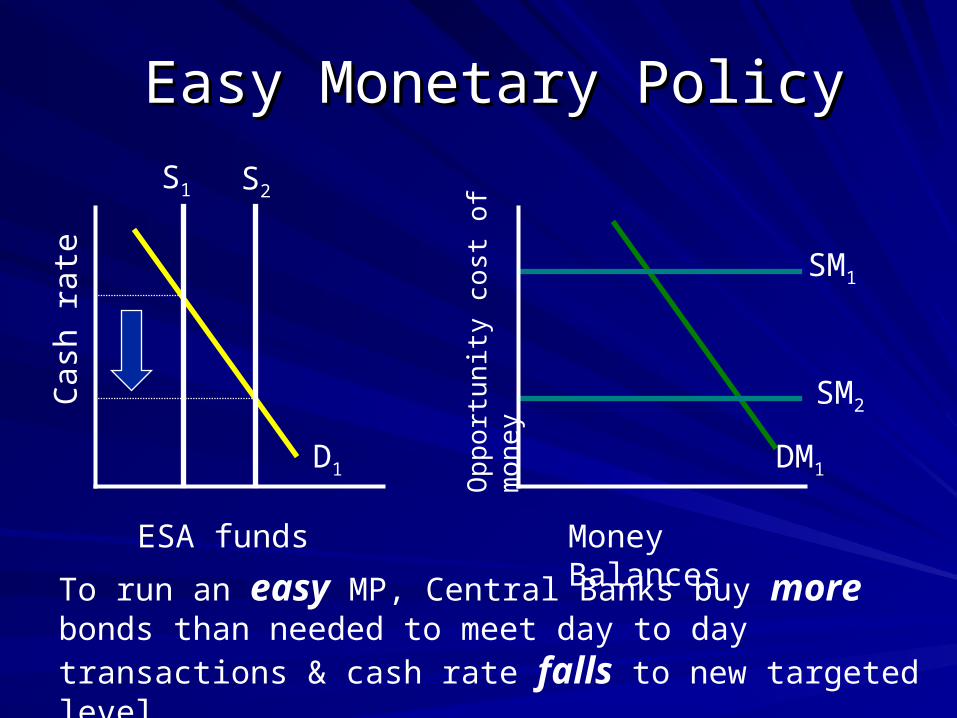

Easy Monetary PolicyEasy Monetary Policy

ESA funds Money Balances

Cas

h ra

te

Opp

ortu

nity

cos

t of

mon

eyD1 DM1

S1

SM1

To run an easy MP, Central Banks buy more bonds than needed

to meet day to day transactions & cash rate falls to new targeted level.

S2

SM2

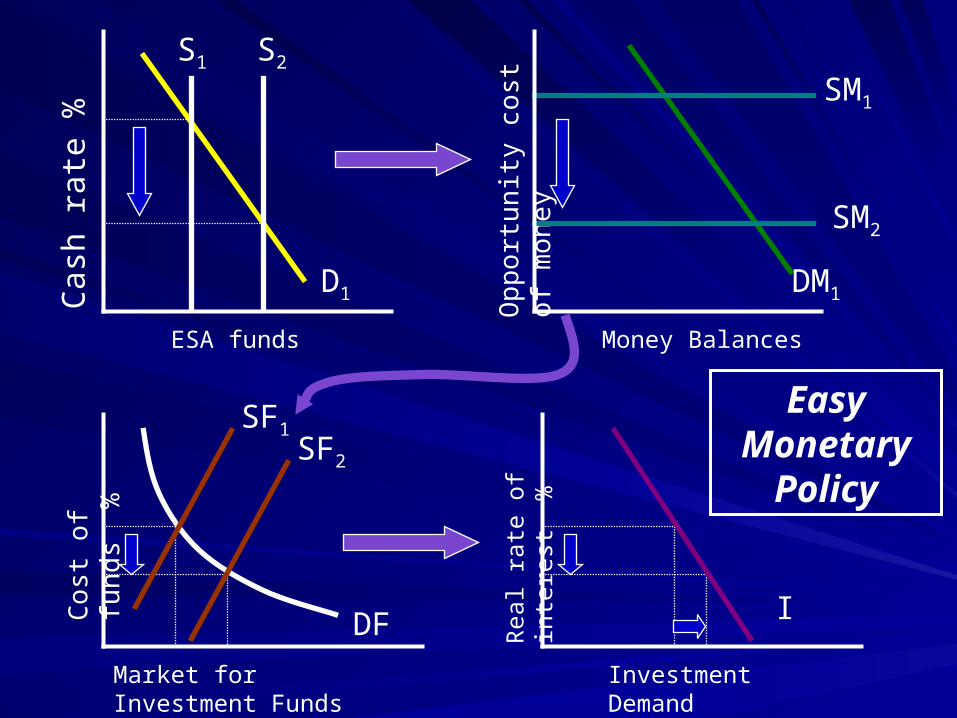

ESA funds Money Balances

Cas

h ra

te %

Opp

ortu

nity

cos

t of

mon

ey

D1

S1 S2

DM1

SM1

SM2

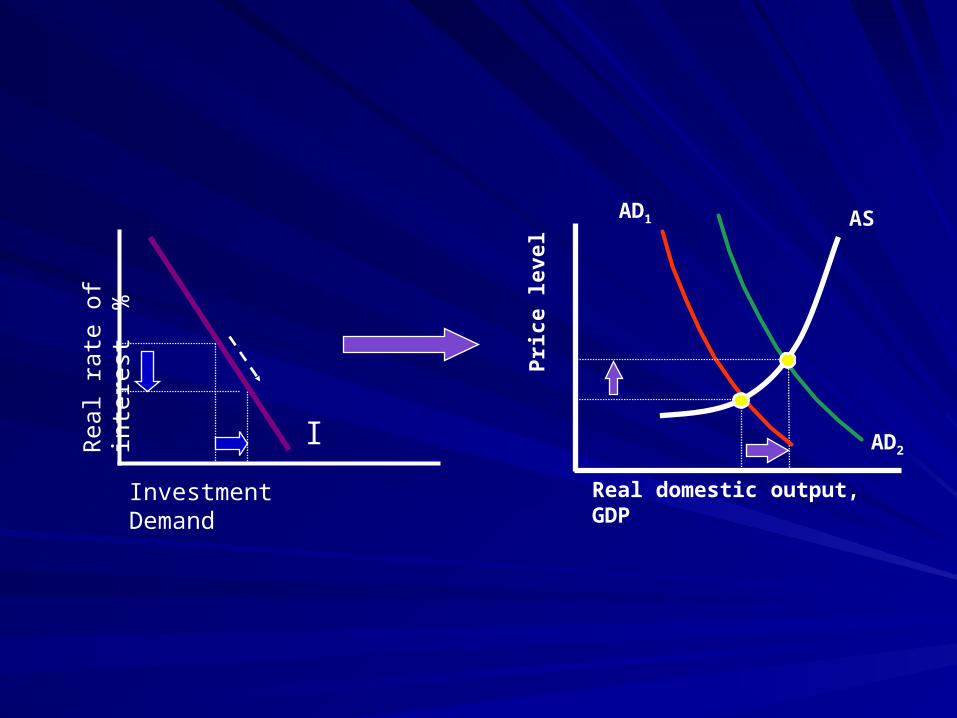

Market for Investment Funds Investment Demand

Cos

t of

fund

s %

DF

SF1SF2

Rea

l rat

e of

inte

rest

%

I

Easy Monetary

Policy

Investment Demand

IRea

l rat

e of

inte

rest

%

Pri

ce le

vel

Real domestic output, GDP

AD1

AD2

AS

Tight Monetary PolicyTight Monetary Policy

Enacted when the economy is facing Enacted when the economy is facing significant inflationary pressuressignificant inflationary pressures

Central Bank announces its intention to Central Bank announces its intention to increase the target cash rateincrease the target cash rate

ESA funds are brought into balance at this ESA funds are brought into balance at this new target cash ratenew target cash rate

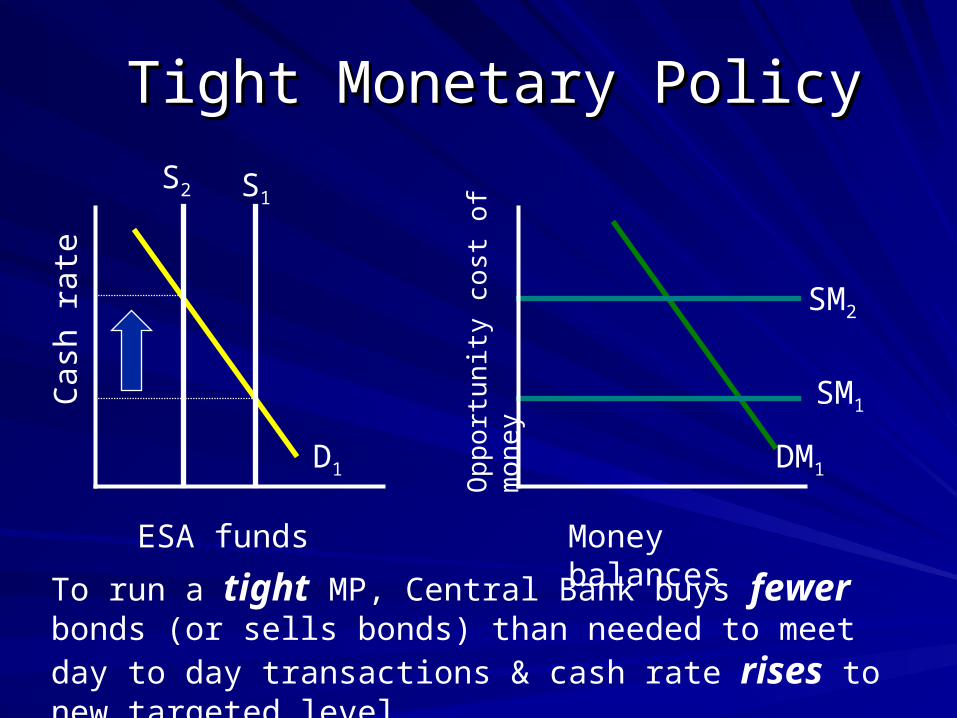

Tight Monetary PolicyTight Monetary Policy

ESA funds Money balances

Cas

h ra

te

Opp

ortu

nity

cos

t of

mon

eyD1 DM1

S2

SM2

To run a tight MP, Central Bank buys fewer bonds (or sells bonds)

than needed to meet day to day transactions & cash rate rises to new targeted level.

S1

SM1

ESA funds Money balances

Cas

h ra

te %

Opp

ortu

nity

cos

t of

mon

ey

D1

S2 S1

DM1

SM2

SM1

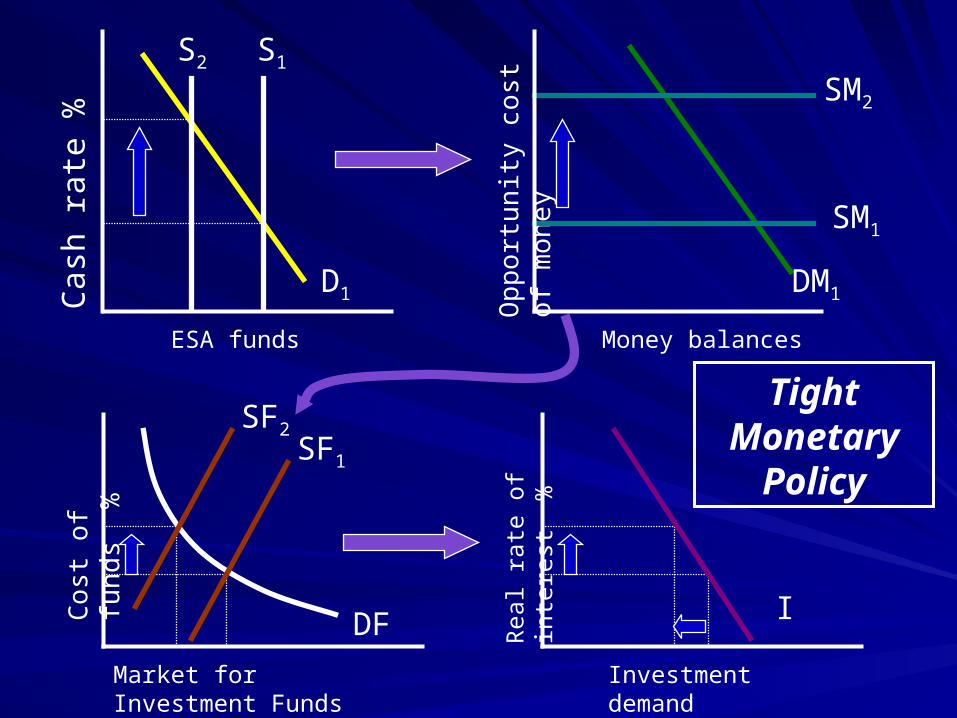

Market for Investment Funds Investment demand

Cos

t of

fund

s %

DF

SF2SF1

Rea

l rat

e of

inte

rest

%

I

Tight Monetary

Policy

Investment Demand

IRea

l rat

e of

inte

rest

%

Pri

ce le

vel

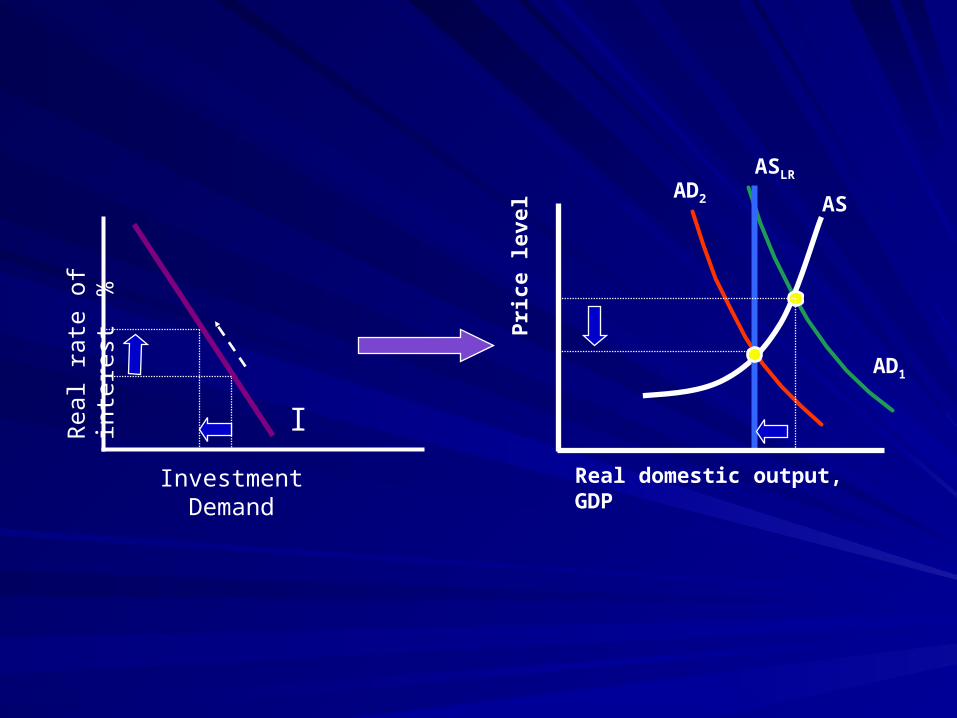

Real domestic output, GDP

AD1

AD2 AS

ASLR

MP and Exchange RatesMP and Exchange RatesInternational capital flows move around the world in International capital flows move around the world in response to interest rate differentials.response to interest rate differentials.

When domestic interest rates rise, the interest rate When domestic interest rates rise, the interest rate differential between domestic & overseas interest ratesdifferential between domestic & overseas interest rates widens and attracts capital inflow.widens and attracts capital inflow.

This causes the value of a freely-floating currency to This causes the value of a freely-floating currency to appreciate making imports more attractive and Net appreciate making imports more attractive and Net Exports fall.Exports fall.

This will reinforce the shift to the left in AD.This will reinforce the shift to the left in AD.

This can also work in reverse.This can also work in reverse.

Expansionary MP & Transmission Expansionary MP & Transmission MechanismMechanism

Central Bank announces cash rate target, buys Central Bank announces cash rate target, buys bonds, increases ESA funds.bonds, increases ESA funds.

Bank reserves increase, deposits created & Bank reserves increase, deposits created & money supply expands.money supply expands.

Interest rates fall currency depreciates. Interest rates fall currency depreciates.

Investment (& consumption) increase; Net Investment (& consumption) increase; Net Exports improve. Exports improve.

AD increases.AD increases.

Equilibrium GDP increases & price level rises.Equilibrium GDP increases & price level rises.

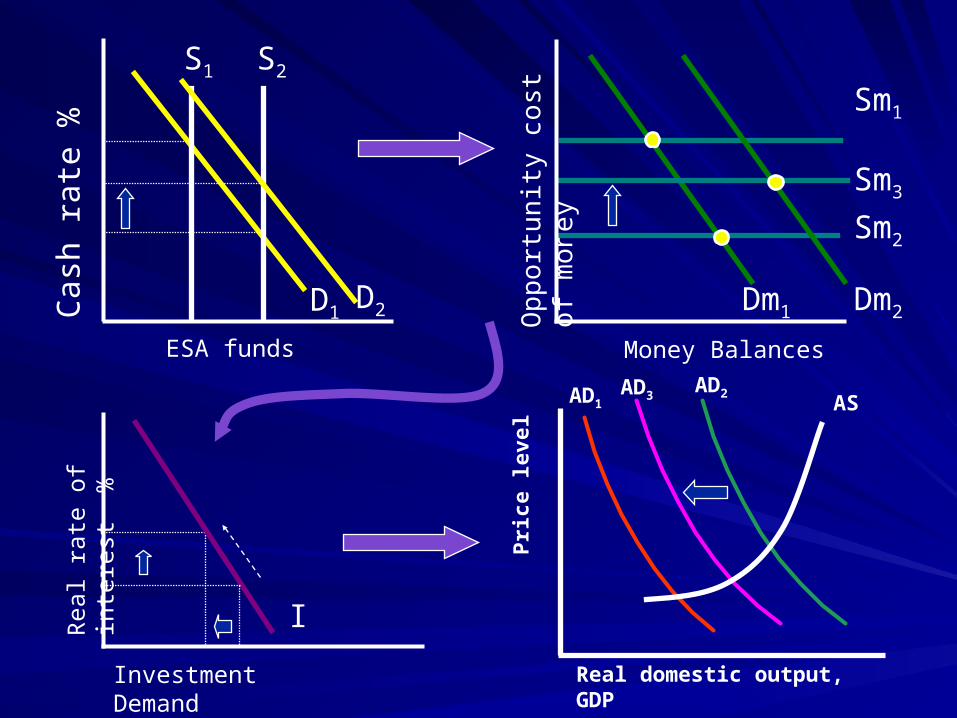

Second Round or Feedback EffectsSecond Round or Feedback Effects

The expansionary MP will shift AD to the right The expansionary MP will shift AD to the right as outlined but now we need to consider the as outlined but now we need to consider the consequences of the rise in GDP. consequences of the rise in GDP. Recall that the transactions demand for Recall that the transactions demand for money shifts to the right as GDP rises. money shifts to the right as GDP rises. This increase in demand for money will This increase in demand for money will generate an increased demand for ESA generate an increased demand for ESA funds.funds.What will central bank do? It can do nothing & What will central bank do? It can do nothing & allow the cash rate to rise OR it can allow the cash rate to rise OR it can accommodate the change to keep the cash accommodate the change to keep the cash rate at target.rate at target.

Investment Demand

IRea

l rat

e of

inte

rest

%

Pri

ce le

vel

Real domestic output, GDP

AD1AD2

ASAD3

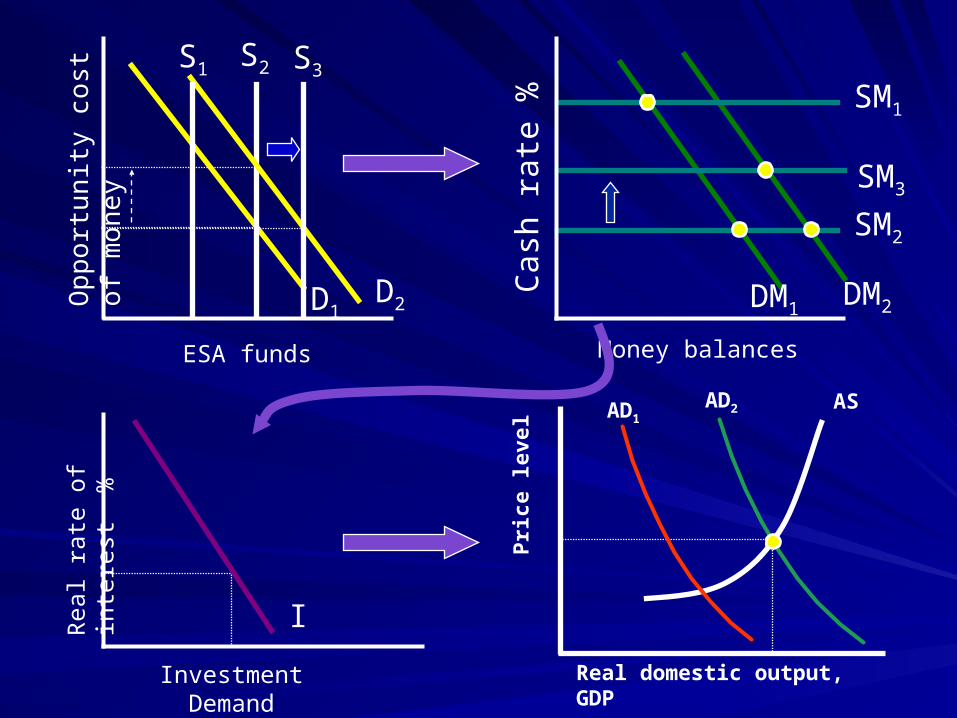

ESA funds

Cas

h ra

te %

D1

S1 S2

D2

Money Balances

Opp

ortu

nity

cos

t of

mon

ey

Dm1

Sm1

Sm2

Dm2

Sm3

ESA funds Money balances

Opp

ortu

nity

cos

t of

mon

ey

D1

S1 S2

Investment Demand

IRea

l rat

e of

inte

rest

%

Pri

ce le

vel

Real domestic output, GDP

AD2 AS

D2

S3

Cas

h ra

te %

DM1

SM2

DM2

SM1

SM3

AD1

Second Round Effects & FPSecond Round Effects & FPNow we are in a better position to understand the Now we are in a better position to understand the finance implications of budget deficits & crowding out. finance implications of budget deficits & crowding out. Expansionary FP has a first round effect of shifting Expansionary FP has a first round effect of shifting AD to the right.AD to the right.Second round effects cause transactions demand to Second round effects cause transactions demand to shift to the right as GDP rises. shift to the right as GDP rises. This increase in demand for money will generate an This increase in demand for money will generate an increased demand for ESA funds.increased demand for ESA funds.What will central bank do? It can accommodate the What will central bank do? It can accommodate the change to keep the cash rate at target OR it can do change to keep the cash rate at target OR it can do nothing & allow the cash rate to rise. nothing & allow the cash rate to rise.

AD1

AD2

AS

Money balances

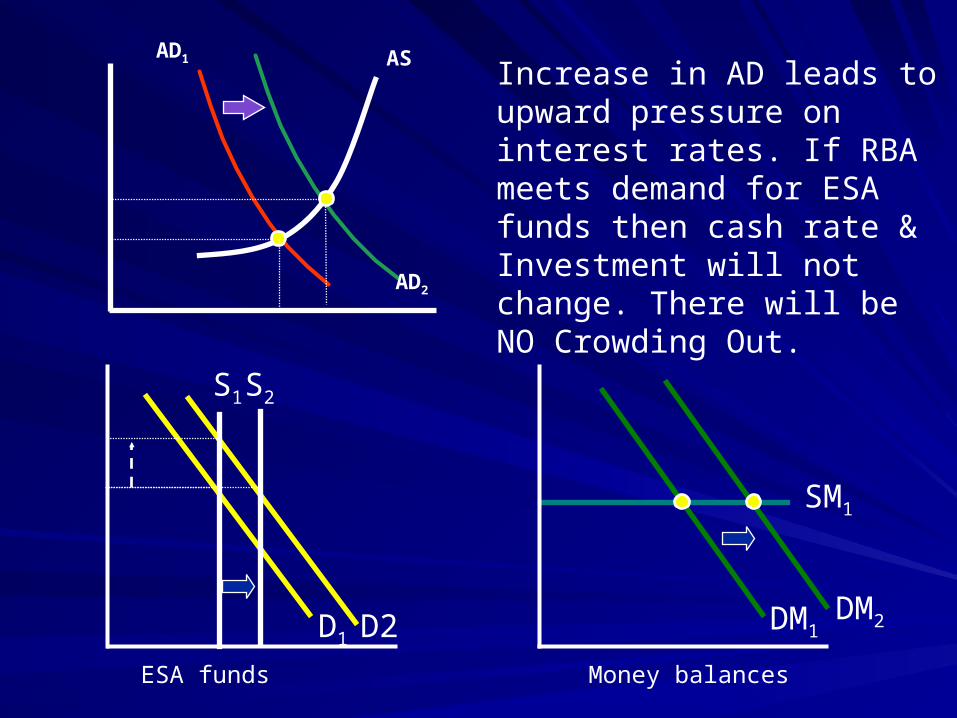

Increase in AD leads to upward pressure on interest rates. If RBA meets demand for ESA funds then cash rate & Investment will not change. There will be NO Crowding Out.

ESA funds

D1

S1 S2

DM1

SM1

DM2D2

ESA funds

D1

S1

Dm1

SM1

Dm2

SM2

I

Real domestic output, GDP

AD1

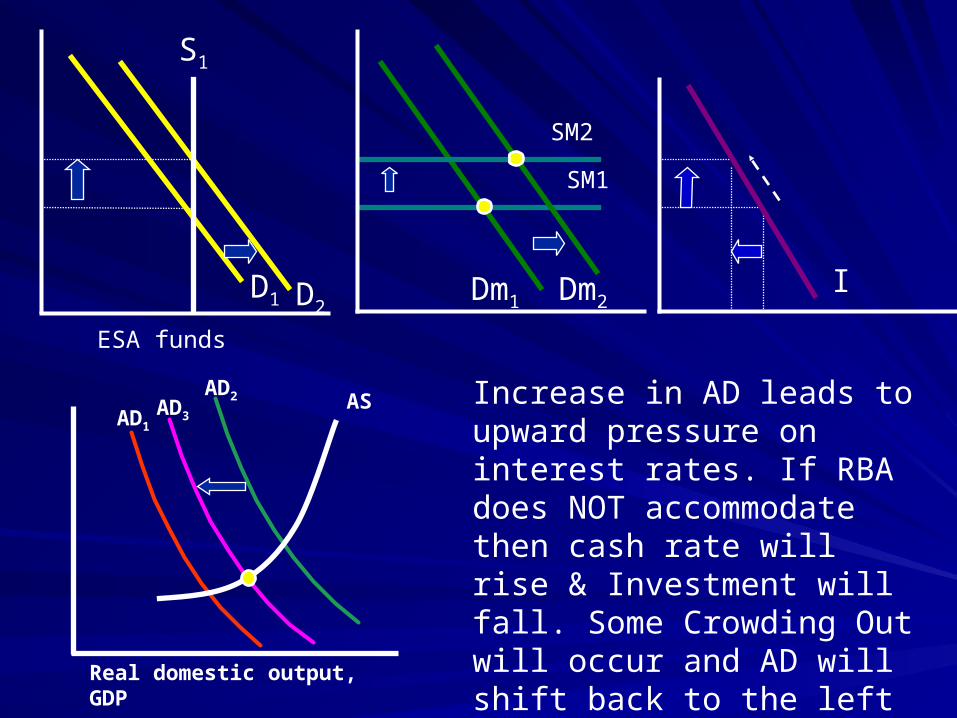

AD2 ASAD3Increase in AD leads to upward pressure on interest rates. If RBA does NOT accommodate then cash rate will rise & Investment will fall. Some Crowding Out will occur and AD will shift back to the left causing output and prices to fall.

D2

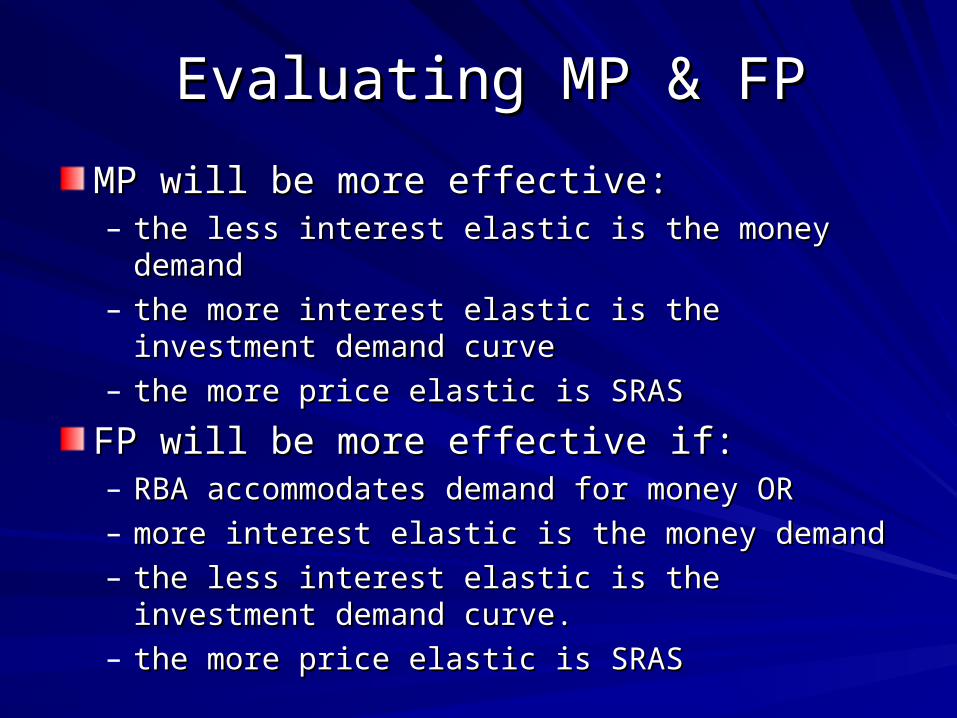

Evaluating MP & FPEvaluating MP & FP

MP will be more effective:MP will be more effective:– the less interest elastic is the money demand the less interest elastic is the money demand – the more interest elastic is the investment demand the more interest elastic is the investment demand

curvecurve– the more price elastic is SRASthe more price elastic is SRAS

FP will be more effective if:FP will be more effective if:– RBA accommodates demand for money ORRBA accommodates demand for money OR– more interest elastic is the money demandmore interest elastic is the money demand– the less interest elastic is the investment demand the less interest elastic is the investment demand

curve.curve.– the more price elastic is SRASthe more price elastic is SRAS

Evaluating MP & FPEvaluating MP & FP

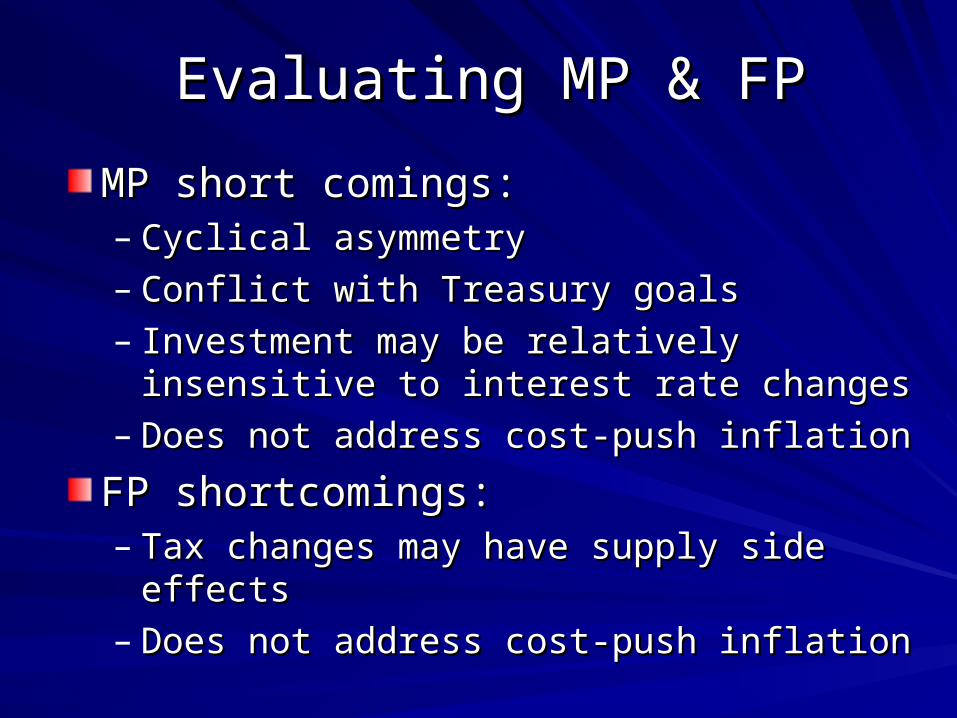

MP short comings:MP short comings:– Cyclical asymmetry Cyclical asymmetry – Conflict with Treasury goalsConflict with Treasury goals– Investment may be relatively insensitive to Investment may be relatively insensitive to

interest rate changesinterest rate changes– Does not address cost-push inflationDoes not address cost-push inflation

FP shortcomings:FP shortcomings:– Tax changes may have supply side effectsTax changes may have supply side effects– Does not address cost-push inflationDoes not address cost-push inflation

Evaluating MP & FPEvaluating MP & FP

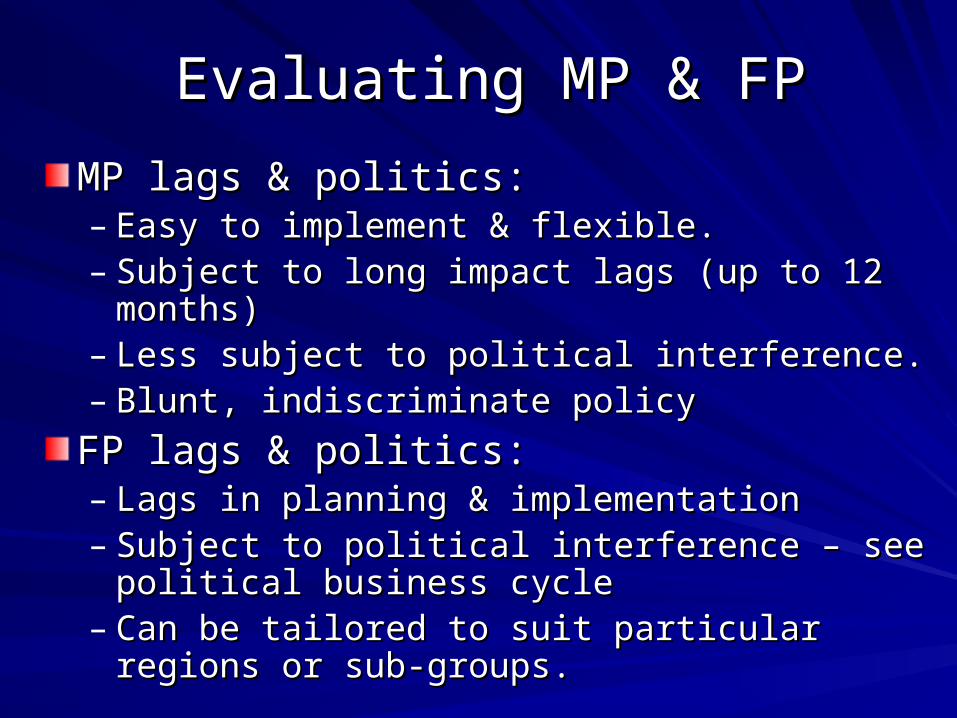

MP lags & politics:MP lags & politics:– Easy to implement & flexible.Easy to implement & flexible.– Subject to long impact lags (up to 12 months)Subject to long impact lags (up to 12 months)– Less subject to political interference.Less subject to political interference.– Blunt, indiscriminate policy Blunt, indiscriminate policy

FP lags & politics:FP lags & politics:– Lags in planning & implementationLags in planning & implementation– Subject to political interference – see political Subject to political interference – see political

business cycle business cycle – Can be tailored to suit particular regions or sub-Can be tailored to suit particular regions or sub-

groups. groups.

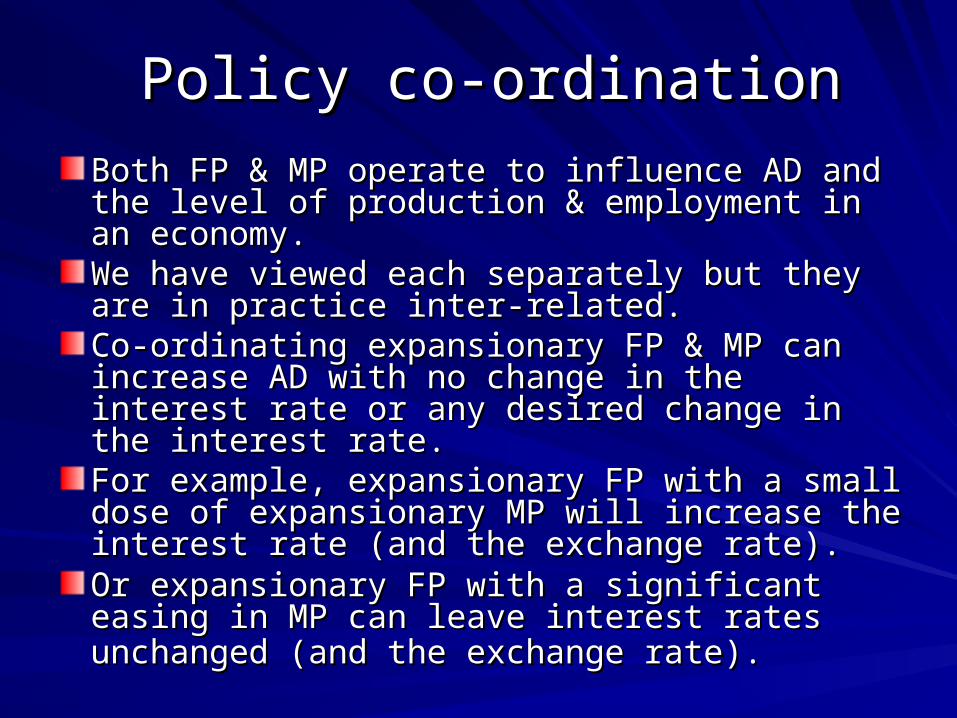

Policy co-ordinationPolicy co-ordination

Both FP & MP operate to influence AD and the Both FP & MP operate to influence AD and the level of production & employment in an economy.level of production & employment in an economy.We have viewed each separately but they are in We have viewed each separately but they are in practice inter-related. practice inter-related. Co-ordinating expansionary FP & MP can Co-ordinating expansionary FP & MP can increase AD with no change in the interest rate or increase AD with no change in the interest rate or any desired change in the interest rate.any desired change in the interest rate.For example, expansionary FP with a small dose For example, expansionary FP with a small dose of expansionary MP will increase the interest rate of expansionary MP will increase the interest rate (and the exchange rate).(and the exchange rate).Or expansionary FP with a significant easing in Or expansionary FP with a significant easing in MP can leave interest rates unchanged (and the MP can leave interest rates unchanged (and the exchange rate).exchange rate).

Policy conflictPolicy conflict

Sometimes the political imperatives that Sometimes the political imperatives that governments respond to & the objectives of governments respond to & the objectives of central banks diverge.central banks diverge.Governments tend to have shorter (re-election) Governments tend to have shorter (re-election) time horizons. While central banks have longer time horizons. While central banks have longer time frame centred on price stability.time frame centred on price stability.Govt pursuing expansionary FP might desire Govt pursuing expansionary FP might desire expansionary MP (to lower interest rates and expansionary MP (to lower interest rates and the currency) but if central bank is concerned the currency) but if central bank is concerned about inflation, it will not ease MP unless FP is about inflation, it will not ease MP unless FP is restrained.restrained.

Policy objectives & policy toolsPolicy objectives & policy tools

MP objective is to ‘assist the economy to MP objective is to ‘assist the economy to achieve full-employment, non-inflationary level achieve full-employment, non-inflationary level of total output’.of total output’.Actually 2 objectives here – full employment & Actually 2 objectives here – full employment & price stability. Sometimes these objectives pull price stability. Sometimes these objectives pull in opposite directions. in opposite directions. Further MP has essentially one tool to achieve Further MP has essentially one tool to achieve its objectives – OMO.its objectives – OMO.A rule of thumb says that should have one A rule of thumb says that should have one objective per tool.objective per tool.Most recently MP, with its long lags, has focused Most recently MP, with its long lags, has focused on achieving an inflation target.on achieving an inflation target.

ReferencesReferences

Mc Taggart et al. Chapter 27 Mc Taggart et al. Chapter 27

Jackson & McIverJackson & McIver, Chapter 12., Chapter 12.