“Macro Analysis of Chemical Industry in...

110

DATE :- 8 th Dec. 2014 A Study On “Macro Analysis of Chemical Industry in India” Management Research Project -I Submitted In the partial fulfillment of the Degree of Master of Business Administration Semester-III By Name En. No. Specialization Bhalani Vishal 13044311008 Marketing Bhanushali Hardik 13044311009 Finance Chaudhary Kundan 13044311014 Marketing Desai Jayesh 13044311023 HR Joshi Arpi 13044311029 Finance Nayee Naresh 13044311045 Finance Under the Guidance of: Prof. (Dr.) Mahendra Sharma Prof. & Head, V. M. Patel Institute of Management. & Dr. Harsha Jariwala Dr. Abhishek Parikh Faculty Members V. M. Patel Institute of Management. Submitted To: V. M. Patel Institute of Management, Ganpat University, Kherva.

Transcript of “Macro Analysis of Chemical Industry in...

DATE :- 8th

Dec. 2014

A

Study On

“Macro Analysis of Chemical Industry in India”

Management Research Project -I

Submitted

In the partial fulfillment of the Degree of

Master of Business Administration

Semester-III

By

Name En. No. Specialization

Bhalani Vishal 13044311008 Marketing

Bhanushali Hardik 13044311009 Finance

Chaudhary Kundan 13044311014 Marketing

Desai Jayesh 13044311023 HR

Joshi Arpi 13044311029 Finance

Nayee Naresh 13044311045 Finance

Under the Guidance of:

Prof. (Dr.) Mahendra Sharma

Prof. & Head,

V. M. Patel Institute of Management.

&

Dr. Harsha Jariwala

Dr. Abhishek Parikh

Faculty Members

V. M. Patel Institute of Management.

Submitted To:

V. M. Patel Institute of Management,

Ganpat University,

Kherva.

I page

CERTIFICATE BY THE GUIDE

This is to certify that the contents of this report entitled “A Macro Analysis of Chemical

Industry” by Bhalani Vishal (13044311008), Bhanushali Hardik (13044311009), Desai Jayesh

(13044311025), Joshi Arpi (13044311029), Nayee Naresh (13044311045), Chaudhary Kundan

(13044311014) submitted to V. M. Patel Institute of Management for the Award of Master of

Business Administration (MBA Semester -III) is original research work carried out by them

under my supervision.

This report has not been submitted either partly or fully to any other University or Institute for

award of any degree or diploma.

Prof. (Dr.) Mahendra Sharma,

Professor & Head,

V. M. Patel Institute Of Management,

Ganpat University.

Kherva.

Date : 8th

Dec. 2014

Place : Ganpat Vidyanagar

II page

CANDIDATE’S STATEMENT

We hereby declare that the work incorporated in this report entitled “A Study of Macro

Analysis on Chemical Industry” in partial fulfillment of the requirements for the award of

Master of Business Administration (Semester - III) is the outcome of original study undertaken

by us and it has not been submitted earlier to any other University or Institution for the award of

any Degree or Diploma.

Vishal Bhalani

Hardik Bhanushali

Chaudhary Kundan

Jayesh Desai

Arpi Joshi

Naresh Nayee

Date :- 8th

Dec. 2014

Place :- Ganpat Vidyanagar

III page

PREFACE

One can deny for importance of the practical exposure of the problem for its better understanding

and better grip of coming out with industrially acceptable solution.

Being the management student and performing small practical even is in itself and experience of

responsibility on our head. The project is certainly the best chance to work in the management

field and have practical understanding of management strategic planning and his implementation.

This exposure has really added a supplement and nourishment to our growing tree of

management knowledge-just like the fertilizer does to the plants.

In view of above, this report has been completed as a part of syllabus prescribed for the master of

business administration. This had been made in order to know Chemical industry overview and

its strategic tools and its planning. This will help us to understand how made strategic tools for

particular industry, which factor affected to Chemical industry. We also know the strengths,

weakness, opportunities and threats. This will help to understand financial overview of Chemical

industry. We also know the political, economical, social, technology factor which affected to the

Chemical industry.

IV page

ACKNOWLEDGEMENTS

It is indeed of Great moment to pleasure to express our sense of per found gratitude and

ineptness to all the people who have been instrumental in making our learning a rich experience.

We got the opportunity to do a challenging project in Management Research Project. The project

is the important part of our study and gives us a practical exposure to strategic tools its

implementation and it is almost impossible to do the same without the guidance of people in and

around us.

It gives me immense pleasure to acknowledge strategic tools which has been nice enough to give

our chance to do our report and providing us support throughout our report period and afterword.

We hereby take the pleasure of thanking all who have contributed to the making of this report.

Firstly we would like to thank Dr. M. S. Sharma, professor & Head, V.M. Patel institute of

Management, Ganpat University, Kherva, Mehsana. Who provided the major driving force and

incentive behind this study. He has been always generous with his time, resources, and advices.

We wish to express our sincerest gratitude to Professor Harsha Jariwala and Abhisek Parikh,

Assistant professor, V.M.P.I.M., Ganpat University, Kherva, for their continuous guidance,

support, and encouragement throughout our report work.

We are very grateful to Atish Barot for their support and generosity with their time and

Resources during our work. We are also thankful to Librarian, Friends, and family for their

continuous support to make the report.

Thank you.

V page

Executive Summary

The chemical industry is critical for the economic development of any country, providing

products and enabling technical solutions in virtually all sectors of the economy. Global

chemical production growth slowed down from 4.4% p.a. in 1999-2004 to 3.6% p.a. in 2004-

2009, with global chemical sales in FY10 valued at $3.4 trillion. The industry is increasingly

moving eastwards in line with the shift of its key consumer industries (e.g. automotive,

electronics, etc.) to leverage greater manufacturing competitiveness of emerging Asian

economies and to serve the increasing local demand. This has led to share of Asia in the global

chemical industry increasing from 31% in 1999 to 45% in 2009. With Asia’s growing

contribution to the global chemical industry, India emerges as one of the focus destinations for

chemical companies worldwide. With the current size of approximately $108 billion1, the Indian

chemical industry accounts for ~3% of the global chemical industry. Two distinct scenarios for

the future emerge, based on how effectively the industry leverages its strengths and manages

challenges. In the base case scenario, with current initiatives of industry & government, the

Indian chemical industry could grow at 11% p.a. to reach size of $224 billion by 2017. However,

the industry could aspire to grow much more and its growth potential is limited only by its

aspirations. In such an optimistic scenario, high end–use demand based on increasing per capita

consumption, improved export competitiveness and resultant growth impact for each sub-sector

of the chemical industry could lead to an overall growth rate of over 15% p.a. and a size of $290

billion by 2017 (~6% of global industry). This has a potential for further upside in the future

considering India’s increasing competitiveness in manufacturing.

The draft manufacturing policy recently approved by the Cabinet targets increasing the share

of manufacturing in GDP to at least 25% by 2025 (from current 16%). It aims to create 100

million additional jobs through creation of National Investment and Manufacturing Zones

(NIMZs) as mega investment regions, equipped with world class infrastructure. These zones

will enjoy fast track clearances from the environment ministry and state pollution boards,

special policy regimes, tax concessions and more favorable labour laws. Investments in

manufacturing in the chemical sector are absolutely essential to ensure growth of the Indian

chemical industry.

VI page

Focused growth and planning for the chemical sector would enhance our global

competitiveness further, increase domestic value addition, provide technological depth and

promote sustained economic growth. In order to realize the growth envisaged above and

leverage the India opportunity effectively, the chemical industry would require significant

investments in capacity creation, technology development, access to feedstock and a larger

pool of skilled human resources. This could translate into additional investment of $110-150

billion2. Pro-active action by the Government and nodal agencies of PCPIR zones through

encouraging anchor tenants to establish facilities, making feedstock available for downstream

plants and creating a favorable ecosystem in terms of infrastructure and other facilities will

help them become true chemical manufacturing competence centers and also send a positive

message to the global investing community. The chemical industry’s R&D spends would

need to go up significantly from current levels of less than 0.5% of sales to reach closer to

global benchmarks of 4% of sales (implying R&D spends of ~$12 billion by 20173). On the

human resources front, adequate educational infrastructure would be required to impart

vocational training to develop additional 4.5 to 5 million skilled workers by 20172. Over 15

years, employment potential could range between 8-9 million jobs.

The Indian chemical industry can deliver on an accelerated growth phase, provided a clearly

defined vision along with a strategic roadmap is developed to enable it. If this is not done, we

may see the growing market increasingly being served through manufacturing done outside

India. The various segments of the chemical industry (such as organic chemicals, specialty

chemicals, chlor-alkali, pesticides, colorants and alcohol based chemicals) have their own

unique set of challenges. The industry can grow only if these individual segments overcome

their challenges and move swiftly along the growth path. The performance of these segments

has been studied in the subsequent chapters and targets/ goals have been set for the XIIth five

year plan along with concrete action plans consisting of levers that will help overcome

challenges and drive growth. The industry and government will have to work in tandem to

achieve the ambitious targets set for the chemical industry.

VII page

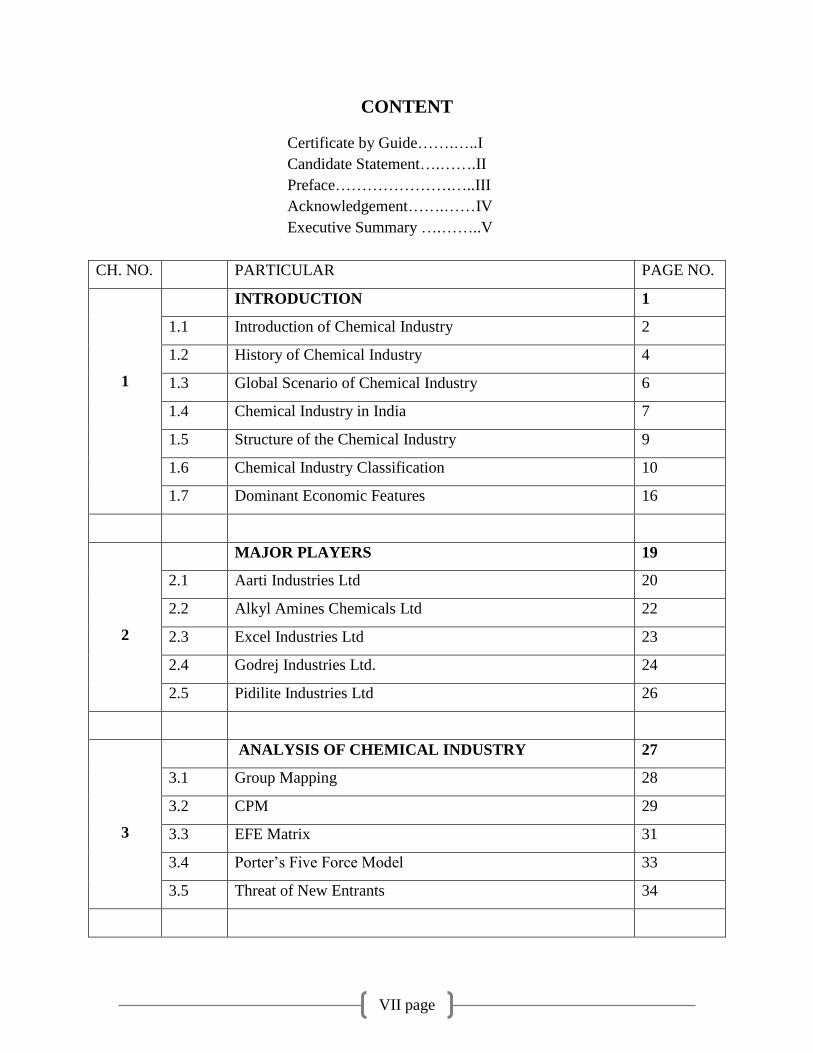

CONTENT

Certificate by Guide…….…..I

Candidate Statement….…….II

Preface………………….…..III

Acknowledgement…….……IV

Executive Summary ….……..V

CH. NO. PARTICULAR PAGE NO.

1

INTRODUCTION 1

1.1 Introduction of Chemical Industry 2

1.2 History of Chemical Industry 4

1.3 Global Scenario of Chemical Industry 6

1.4 Chemical Industry in India 7

1.5 Structure of the Chemical Industry 9

1.6 Chemical Industry Classification 10

1.7 Dominant Economic Features 16

2

MAJOR PLAYERS 19

2.1 Aarti Industries Ltd 20

2.2 Alkyl Amines Chemicals Ltd 22

2.3 Excel Industries Ltd 23

2.4 Godrej Industries Ltd. 24

2.5 Pidilite Industries Ltd 26

3

ANALYSIS OF CHEMICAL INDUSTRY 27

3.1 Group Mapping 28

3.2 CPM 29

3.3 EFE Matrix 31

3.4 Porter’s Five Force Model 33

3.5 Threat of New Entrants 34

VIII page

4

FINANCIAL ANALYSIS 36

4.1 INTRODUCTION OF FINANCIAL ANALYSIS 37

4.2 TREND ANALYSIS 39

4.3 Ratio Analysis 48

5

BUSINESS PLAN 70

5.1 Objectives 72

5.2 Mission 72

5.3 Company Summary 72

5.4 SWOT Analysis 74

5.5 Market Segmentation 77

5.6 Target Market Segment Strategy 79

5.7 Industry Analysis 80

5.8 Sales Strategy 81

5.9 Milestones 82

5.10 Personnel Plan 82

5.11 Break-even Analysis 83

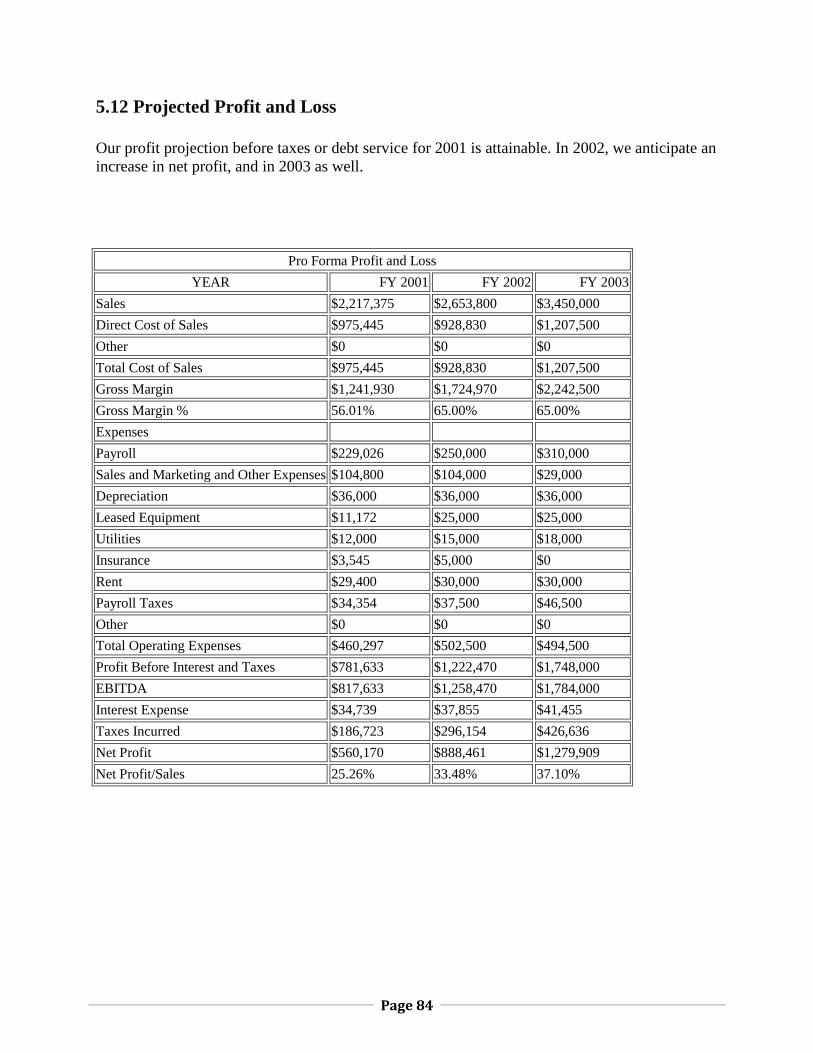

5.12 Projected Profit and Loss 84

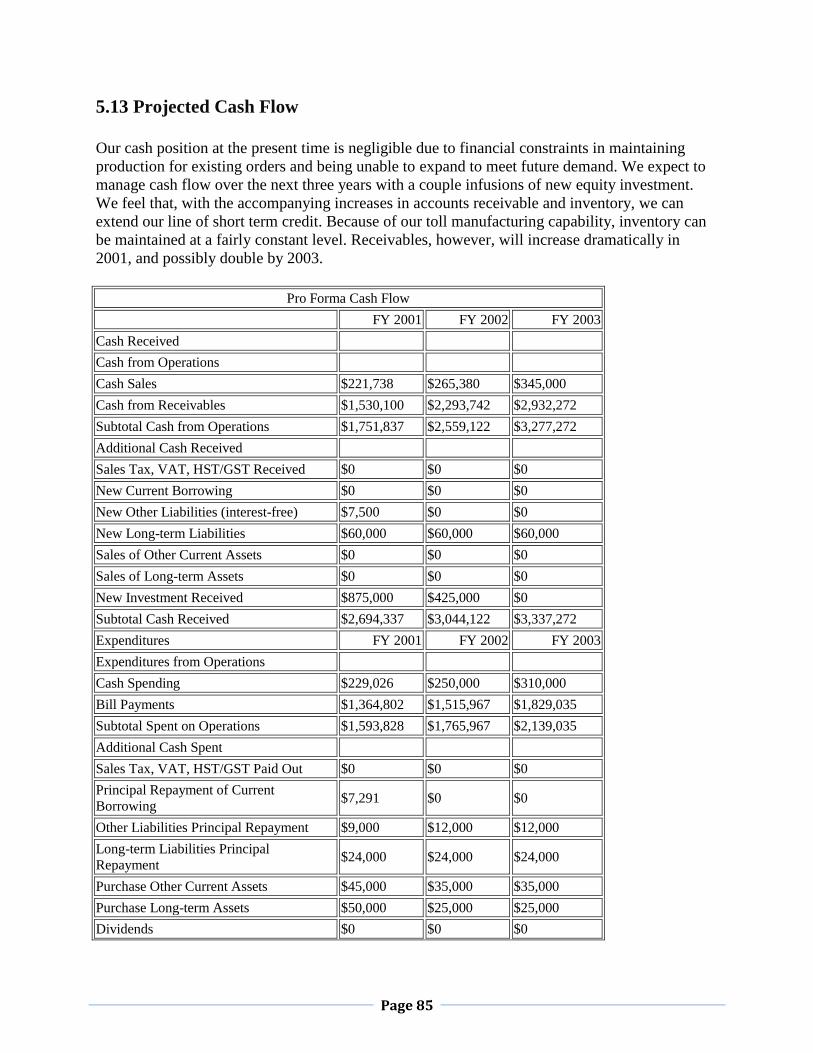

5.13 Projected Cash Flow 85

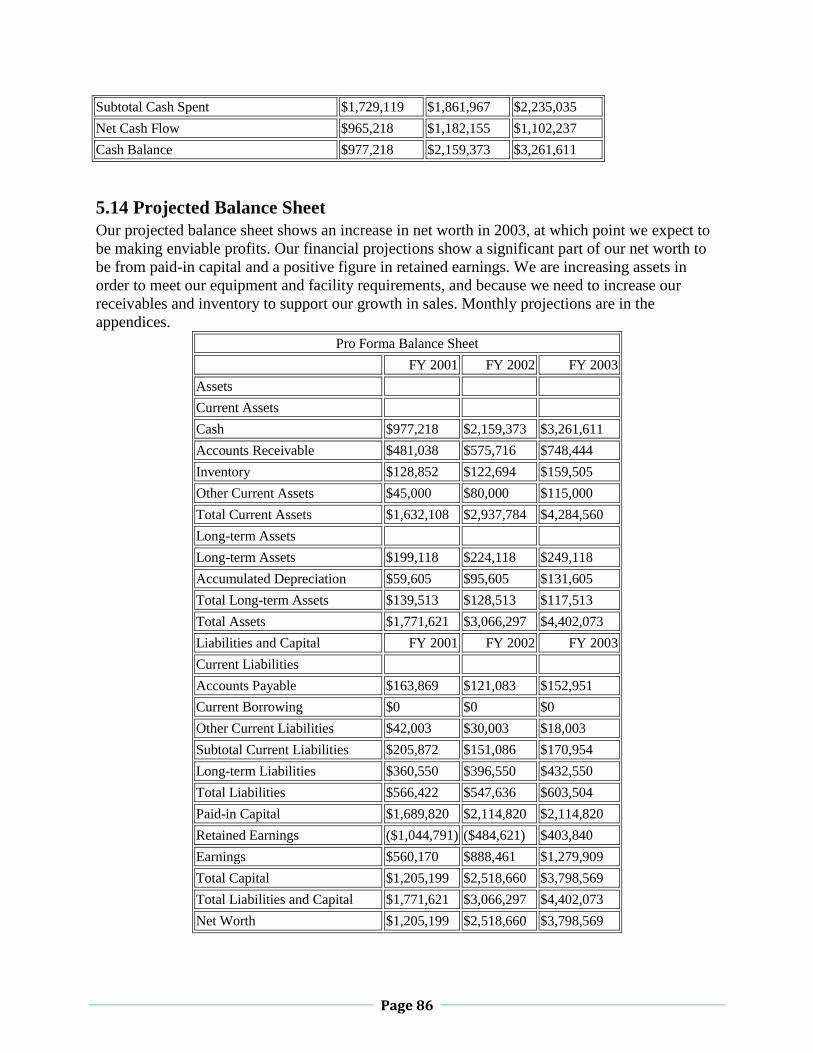

5.14 Projected Balance Sheet 86

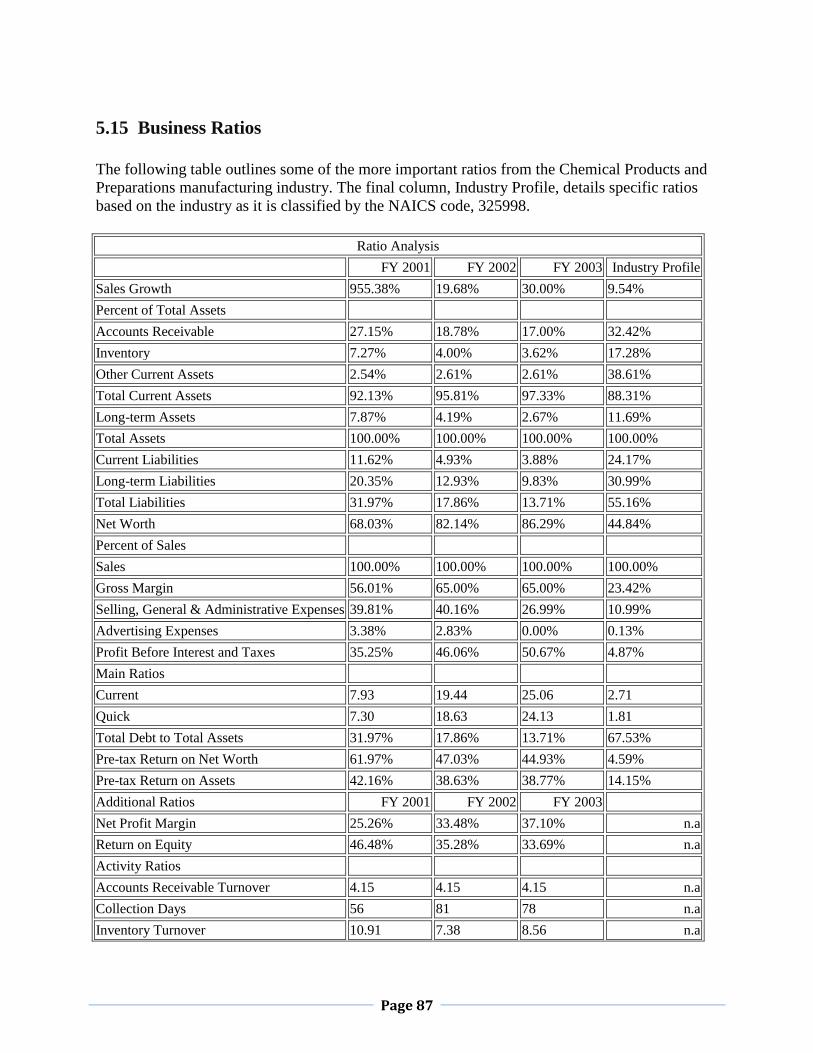

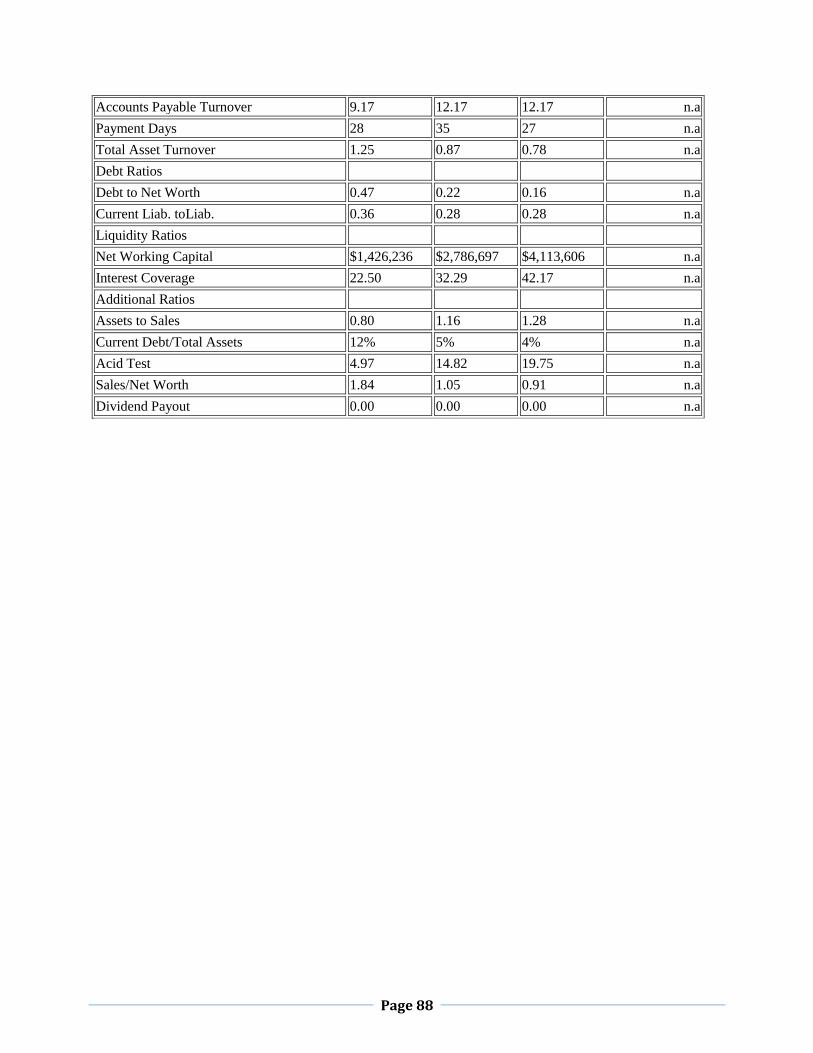

5.15 Business Ratios 87

6 CONCLUSION 89

7 BIBLOGRAPHY 100

Page 1

CHAPTER 1

INTRODUCTION

Page 2

1.1 Introduction of Chemical Industry

Chemical industry is an integral component of the Indian economy, which contributes around 7

% of the Indian GDP. It touches our lives in several different ways. Whether it is thermoplastic

furniture we use, or a synthetic garment we wear, or a drug we take – we are inextricably

associated to it.

The industry is integral to the development of agricultural and industrial development in India

and has key linkages with various other downstream, such as automotive, consumer durables,

engineering, food processing and more. Globalization possesses many challenges to the industry,

which has predominantly developed in a protected environment. With World Trade Organization

assuming an increasing role in global economics, there is an inevitable move towards an inter-

linked international economy. However, there have been cases where particular segments of the

industry, such as pharmaceuticals and biotechnology have performed exceedingly well even at

the world level. During 2005-06, the industry contributed 17.6% of the manufacturing sector.

However the country continues to be a net importer in 2005-06, with exports of US$ 5.95 billion

and imports of US$7.92 billion. The worth of Indian chemicals industry during 2005-06 was

US$30.59 billion, which reflected a growth of 10.23% over the previous year and a CAGR of

8.68% during the last 3 years1.

Comprising basic, specialty and knowledge chemicals, the industry caters to a wide range of end-

user industries producing various commodities such aspharmaceuticals, fertilizers, textiles,

plastic, polymers, agrochemicals, and paints and dyes, among others.

Basicchemicals:India has been making remarkable progress as a manufacturer of basic

chemicals - a segment dominated by petrochemicals. With petrochemicals finding use in

almostall user industries, growth prospectsof the segment remain strong. Moreover, with plastic

being widely used in manufacturing a host of commodities,polymer processing is steadily

becoming an organized business. Considering the rising demand for petrochemicals, most

1http://www.india-exports.com/chemical.html (07/09/2014)

Page 3

chemical companies dealing in the commodity are increasing their plant size to ensure greater

production capacity. Notably, India now boasts of having the world’s largest polypropylene

plant.

Specialty chemicals: Heavily dependent on end-user industries, this segment has recorded more

or less uniform growth over the years. During the economic recession, specialty chemicals used

in certain specific export- oriented industries suffered major losses. Post-recession, however,

with a surging demand in key consumer industries such as construction, automobiles and textiles,

among others, specialty chemicals have been able to record pre-downturn growth rate. Coupled

with growth, customized demands from consumers have also moved northward. Now, specialty

chemicals have to be manufactured keeping in mind consumer requirements. The need of the

hour, therefore, is continuous innovation at low costs to maintain a competitive edge.

Knowledge chemicals: This segment remained largely insulated during the global economic

downturn. Comprising mainly agrochemicals and pharmaceuticals, knowledge chemicals hold

bright future prospects. The segment has made prominent headway in the area of R&D and

technological innovation. On the back of a cheap yet intellectual workforce, knowledge-based

chemicals are now manufactured as per global standards. In fact, Indian generics are now in

great demand across the world.

Page 4

1.2 History of Chemical Industry

Indian Chemical Council started out in the year 1938 to promote the interests of the

nascent Chemical Industry. Pioneers of the chemical industry in India such as

Acharya P. C. Ray brought together a group of industrialists including Rajmitra B. D.

Amin, founder of the Alembic Group of Baroda.

What began as a vision, emerging from foresight and aspirations, became the Indian

Chemical Manufacturers Association and was again rechristened the Indian

Chemical Council. It became the representative body of the Rs.500 billion / US $ 16

billion chemical industry in India2

Its members include both Indian companies with a global presence as well as

subsidiaries of multinationals.

Over the years the Indian Chemical Council (earlier as Indian Chemical

Manufacturers Association) went from strength to strength and has evolved into a

movement embodying the goals, concern and achievements of the chemical industry

in India.

In keeping with the dramatically paced growth of the industry in the latter half of this

century, the ICC has striven to give an impetus to the objectives of the industry.

Realizing the power of information, ICC has consciously worked as a bridge for the

many that forms the Indian Chemical Industry.

The chemical industry is one of the earliest domestic industries in India, contributing

considerably to both the industrial as well as economic growth of the country since it achieved

independence in 1947. The industry presently produces around 70,000 commercial products,

which range from toiletries and cosmetics, to plastics and pesticides.

The wide and diverse range of products can be broken down into several categories, which

include Inorganic and organic (commodity) chemicals, plastics and petrochemicals, drugs and

2http://www.india-exports.com/chemical.html (07/09/2014)

Page 5

pharmaceuticals, dyes and pigments, pesticides and agrochemicals, fine and specialty chemicals,

and fertilizers.

With primary focus on modernization, the Govt. of India has taken an active role in promoting

the growth and development of Indian domestic chemical industry. The Department of

Chemicals & Petro-Chemicals that has been part of the Ministry of Chemicals and Fertilizers

since 1991 is responsible for making policy making, planning, development, and regulation of

the industry. In the private sector, several organizations, including the Indian Chemical

Manufacturers Association, the Chemicals and Petrochemicals Manufacturers Association, and

the Pesticides Manufacturers and Formulators Association of India, all work with the prime

objective of promoting the growth of industry and the export of Indian chemicals. For example,

the Indian Chemical Manufacturers Association represents a large number of Indian companies,

which produce and export a variety of chemicals, which have legitimate commercial

applications, but also can be used as precursors and intermediates for production of chemical

weapons.

Page 6

1.3 Global Scenario of Chemical Industry

Global chemical production is growing and the growth is contributed by the chemical industry of

developing countries. Growth in demand for chemicals in developing countries is high leading to

substantial cross-border investment in the chemical sector. Global sales of chemicals in the year

2005 were estimated to be around US$ 1.75 trillion.

USA is the single largest country with a share of 22% (US$ 380 billion) in world chemical sales,

followed by Japan (10% - US$ 194 billion), China (9% - US$ 163 billion), Germany (7% - US$

122 billion) and France (5% - US$ 90 billion). In terms of regions, Asia-Pacific tops the list with

a share of 35% in global sales followed by Europe (34%), NAFTA (25%) and Latin America

(4%). World export of chemicals is estimated to be US$ 832 billion in 2005. The share of

chemicals in world merchandise trade and global trade of manufactures is estimated to be 11%

and 15% respectively, in 2005.

The growth in world chemicals trade has averaged out to around 12% during the period 2000-

2005. Leading chemical exporters are Germany (11% - US$ 95 billion), USA (11% - US$ 94

billion), France (6% - US$ 51 billion), Japan (6% - US$ 49 billion), and China (4% - US$ 32

billion). The joint framework agreement for tariff harmonization in the Uruguay Round

(Chemical Tariff Harmonization Agreement), has led to a substantial reduction in tariffs in the

signatory countries. However, in many countries reduction in tariff hasbeen substituted by

increase in nontariff barriers. Dumping of chemicals and anti-dumping actions by countries has

become part of the game plan of many firms / countries.

Globalizationof chemical industry has led to national markets being supplied from an increasing

number of locations, while individual companies have increased the geographic scope of their

operations. Chemical companies in the world are now merging their business processes,

including their supply chain, to reduce risks and to create sustainable competitive advantage. The

global chemical industry is continuously working towards reduction of environmental impactof

its activities. The industry is committed to contribute to the sustainable development of the

society as a whole, through its ‘Responsible Care Initiative’, and has developed systems for

improving the health, safety and environmental performance of its products and processes.

Page 7

1.4 Chemical Industry in India

Chemical industry is one of the oldest industries in India. It is estimated that the size of Indian

chemical industry is around US$ 30 billion. Volume of production in chemical industry positions

India as third largest producer in Asia (next to China and Japan), and twelfth largest in the world.

The industry, comprising both smallscale and large units (including MNCs) produces several

thousands of products and bi-products, ranging from plastics and petro-chemicals to cosmetics

and toiletries. A significant share (around one-third) of production by chemical industry is

consumed by itself. The chemical industry accounts for about 13% share in the manufacturing

output and around 5% in total exports of the country.

The chemical industry contributes around 20% of national revenue by way of various taxes and

levies. The chemical industry produced around 8 million metric tonnes each of basic chemicals

and basic petrochemicals, and around 10 million metric tonnes of petrochemical intermediaries

in 2005-06.

Gujarat is the major contributor to the basic chemical as well as petrochemical production with

54% and 59% share in all India production, respectively. Other major states producing basic

chemicals include Maharashtra (9%), Tamil Nadu andUttar Pradesh (6% each). Other major

states producing petrochemicals include Maharashtra (18%), West Bengal (12%), Uttar Pradesh

(4%), and Tamil Nadu (3%).

India’s export of basic chemicals amounted to over US$ 7 billion in 2005-06. India exported

US$ 4.85 billion worth of organic chemicals, US$ 775 million worth of inorganic chemicals,

US$ 847 million worth of tanning and coloring materials, and US$ 649 million worth of

pesticides, in the year 2005-06. In addition, India exported petrochemicals valued nearly US$ 4

billion. India is also an importer of basic chemicals and the import value amounted to over US$ 8

billion in 2005-06.

Page 8

The composition of India’s chemical imports includes organic chemicals (63%), inorganic

chemicals (28%), dyes (6%) and pesticides (3%). China, USA and Saudi Arabia are the leading

source countries for India’s chemical imports. In addition, India imported petrochemicals valued

over US$ 2 billion.

The Indian chemical industry has been receiving significant investment intentions, including

foreign direct investment (FDI). Since August 1991, and till November 2006, chemical industry

has received investment proposals worth Rs.274486 cores, a share of 11.3% in total investment

proposals received during this period.

FDI, which is very essential for modern manufacturing of chemicals, has also been flowing into

the chemical sector significantly. During the period August 1991 to October 2006, FDI inflows

into the chemicals sector amounted to US$ 2.2 billion, a share of around6% in total FDI inflows

into the country.

Page 9

1.5 Structure of the Chemical Industry

Ownership pattern of companies include: proprietary firms 30%, partnership firms 25%,

private limited companies 34% and public limited companies 11%.

The total sample is from 15 states; the highest coming from the Western region. The

companies in the West are entirely from Gujarat and Maharashtra and account for 74.5%

of the total sample. Around 11.4% companies are located in the North, 8.5% in the

South and 5.5% in the East.

Around 89% of the companies in the sample are small scale enterprises with investments

less than Rs 50 mn in plant and machinery. The rest are medium sized enterprises.

Close to 77% of the companies in the sample operate in a single segment. The Organic

and Inorganic manufacturers constitute 65% of the sample, organic companies at 37%

and inorganic 28%. The next largest segment is Dyes and Dyestuff accounting for 22%.

Representation of Alkali and Pesticide companies is 1.2% each.

Depicting the long-established nature of the industry, around 49% of the companies in

the sample were established prior to 1990. Another 42% began operations during the

1990s, while only 9% began operations post-2000.

In terms of IT penetration, around 39% of the companies have a website3

3https://sites.google.com/site/chemicalindustry001/the-characteristics-of-fine-chemicals

Proprietary firms

30%

Partnership firms

25%

Private limited

34%

Public limited

11%

Chemical Industry

Page 10

1.6 Chemical Industry Classification

The chemical industry Classified into 4 key segments, based on a detailed analysis of various

industry classifications followed by several domestic & international bodies. The key segments

are:

1. Chemical sector: It includes basic organic chemicals (methanol, acetic acid etc.), basic

inorganic chemicals (caustic soda, chlor alkali etc.) along with the specialty chemicals

(colorants, water treatment etc.) and agrochemicals (pesticides etc.).

2. Petrochemical sector: Petrochemicals includes polymers, synthetic fibers, surfactants and

elastomers.

3. Fertilizers: Include all types of N,P& K based fertilizers like Urea, DAP etc.

4. Pharmaceuticals: It includes formulations, APIs, biotechnology etc.

(However pharmaceutical section, Fertilizers, And Petrochemical sectors are not a part of this

report) Indian chemical sector is the largest followed by fertilizers and then Petrochemicals. In

terms of growth also, chemical sector is fastest growing closely followed by petrochemicals.

Chemical sector high growth estimate is based on high growth potential of specialty chemicals.

1.6.1 Basic organic chemicals

Introduction

Organic chemicals are a significant part of Indian chemicals industry. Availability of natural gas

for use as feedstock is a critical part of the entire production process. Formaldehyde and acetic

acid are important methanol derivatives and are used in numerous industrial applications. Phenol

is an aromatic compound and derived from Cumene, a benzene and propylene derivative.

Global production of organic chemicals was around 400 million tonnes during FY11. Major

producers of organic chemicals are USA, Germany, U.K, Japan, China and India. Few Latin

Page 11

American countries, for example Brazil and Chile are increasing their presence in global organic

chemicals market.

Six major chemicals produced in India are Methanol, Aniline, Alkyle Amines and its derivatives

like Formaldehyde, Acetic Acid andPhenol,contributing to nearly 2/3rd of Indian basic organic

chemical industry. The balance 1/3rd of the organic chemical consumption in the country is

accounted for by other wide variety of chemicals.Production of major organic chemicals has

shown a significant decline due to large volume imports taking place from countries like China,

resulting in low utilization rates of ~ 60%.

The demand for organic chemicals in India has been increasing at nearly 6.5% during this period

and has reached the level of 2.8 million tonnes. The domestic supply has however grown at a

slower pace resulting in gradual widening of demand supply gap which was primarily bridged

through imports. Domestic production declined at ~6% per annum and imports grew at a rate of

17-19% between FY06 and FY11.

The key segments of the industry are methanol, formaldehyde, acetic acid, phenol, ethyl acetate

and acetic anhydride.

KEY SEGMENTS

i) Methanol

Methanol, a very versatile chemical is primarily produced from natural gas or naphtha.Demand

for methanol has increased at a CAGR of 8% from 0.87 mmtpa in FY06 to 1.26 mmtpa in FY11.

The domestic production of methanol is not sufficient to meet thedemand of methanol in India.

As a result, in FY11, the net import of methanol was 0.92 mmtpa i.e. ~2.5 times the domestic

production of 0.38 mmtpa. Import of methanol has increased at a high CAGR of 18% from 0.4

mmtpa in FY06 to 0.92 mmtpa in FY11.

The two main end-user industries of methanol are chemicals and energy. In the chemicals

industry, methanol is used mainly to manufacture formaldehyde, acetic acid, di-methyl

terephthalate (DMT) and some solvents.

Page 12

In the energy industry, methanol goes into the manufacture of methyl tertiary butyl ether

(MTBE), tertiary amyl methyl ether (TAME), di-methyl ether (DME) and bio-diesel among

other chemicals. Methanol is also used for blending with petrol.Over the years the usage pattern

of methanol has remained same. Formaldehyde accounts for the largest share of methanol usage

due to demand of formaldehyde from plastic and paints industries.

Domestic methanol production has increased by 13% in FY11, reflecting improvement in

utilization rates by players such as Deepak Fertilizers& Petrochemicals Corporation Ltd (Deepak

Fertilizers), Gujarat Narmada Valley Fertilizers Company Ltd (GNVFC) and Rashtriya

Chemicals & Fertilizers Ltd (RCF).

ii) Acetic Acid

Acetic Acid is the main alcohol based chemical and is primarily used in the production of Vinyl

Acetate Monomer (VAM), Purified Terephthalic Acid (PTA), Acetic Anhydride and Acetate

Esters.Demand for acetic acid has grown at a CAGR of 13% from 0.33 million tons in FY06 to

0.6 million tons in FY11. The demand growth has happened mainly due to increase usage by

manufacturers of PTA which is the basic raw material for polyester & fiber and organic esters

such as RIL and Vinyl Chemicals.

Most of the demand was met through domestic production earlier. However, due to oversupply

of acetic acid in global markets and depressed prices, imports of acetic acid have grown leading

to reduced plant capacity utilization.

Acetic acid is manufactured in India through two routes: the methanol route and the ethyl alcohol

(from molasses) route. Alcohol route in Indian context is gradually becoming unviable due to

high prices and limited availability of this feedstock. At present bulk of acetic acid is imported

with domestic production accounting for less than 30% of demand.

Page 13

iii) Formaldehyde

Unlike methanol, production of its derivative formaldehyde in India is sufficient to meet the

domestic demand. The production of formaldehyde has increased, at a similar pace as has its

demand, at a CAGR of 3% from 0.25 mmtpa in FY06 to 0.30 mmtpa in FY11.Major

formaldehyde producing companies in India are Kanoria Chemicals, Hindustan Organic, Rock

Hard and Asian Paints. The first two companies account for 44% of formaldehyde production in

India. Asian Paints produces formaldehyde for captive consumption.

iv) Phenol

Phenol is a significant type of organic chemical with numerous applications as mentioned in the

table below. Its demand is closely linked to end user industries like the construction and

automobile industries.

More than 70% of demand of phenol is met through imports with no fresh supply addition in last

few years. There are only two manufacturers - Hindustan Organics and S I Group with capacity

of 40 Kilo tonnes per annum each in FY11. As the consumption has grown from 0.15 mmtpa in

FY06 to 0.18 mmtpa in FY11, the imports has grown at a higher CAGR of 10% to meet the

rising demand.

Page 14

1.6.2 Key Challenges of Organic Chemical Industry:

1. Lack of cheaper raw material availability: Feedstock (naphtha and natural gas)and power

are critical inputs for organic chemicals industry. Costs of these raw materials are high in India

compared to countries like China, Middle East and other South East Asian countries such as

Thailand and Indonesia. Given the poor infrastructure with lack of adequate facilities at ports and

railway terminals and poor pipeline connectivity, domestic manufacturers will continue facing

difficulty in procuring raw materials at a cost competitive with the global peers.

2. No domestic price discovery: Domestic prices of organic chemicals are highly correlated

with international prices. Given the small scale of domestic operations, local manufacturers are

more influenced by global demand and supply forces.

3. Large global capacity additions: Apart from the current oversupply in global markets, there

is another cause of concern for domestic manufacturers, with further large capacity additions

happening in global markets. For example, globally, methanol industry is expected to witness

excess capacity in the future due to a spate of capacity additions in gas rich countries such as

Middle East and Russia.

4. Low capacity utilization: Due to oversupply in global markets, prices of major organic

chemicals have taken a steep decline, thereby forcing the domestic companies to underutilize

their plants operating levels. The average capacity utilization has fallen from > 90% in FY04 to

~60% in FY11.

Page 15

1.6.3 Key Opportunities of Organic Chemical Industry:

1. Consolidation: Sincemost of the Indian manufacturers operate on a small scale compared to

global peers, there is a room for consolidation in Indian organic chemicals industry. Domestic

players can take advantage of economies of scale arising from consolidation and become more

competitive thereby preventing cheaper global imports.

2. Improved feedstock supply: Domestic organic chemicals players don't have the advantages

of backward integration and hence, they lack pricing flexibility. However, given the new finds of

natural gas reserves in the country, domestic manufacturers will be able to get supply of

feedstock at stable prices.

3. Wider product portfolio: Commodity chemicals companies can improve their product

portfolio by adding specialty chemicals such as polymers additives, water treatment chemicals,

lubricating additives, etc. This will help in improving their margins but requires significant R&D

efforts.

4. Forward integration: Petrochemical companies producing benzene and propylene can look

for forward integration opportunity given the demand-supply deficit in phenol market. Similarly,

an opportunity exists for companies with better access to natural gas supply to venture into the

methanol market facing continuous supply deficit.

5. Outbound approach: Even successful companies from west are shifting their base to

resource rich nations like Saudi Arabia, Qatar, Russia, etc. Indian organic chemical companies

may also explore opportunities outside the country either through greenfield or brownfield

projects.

Page 16

1.7 Dominant Economic Features

1.7.1 Market size and growth:

Chemical industry has a significant contribution in the overall economy of the country.

The contribution of the chemical industry in the overall GDP of the country financial year

2013-14 is 21%4. The contribution of chemical industry in total export of the country is

13-14% of the financial year 2013-14. While in a total import is 8-9%. The worth of

Indian chemicals industry during 2005-06 was US$30.59 billion, which reflected a

growth of 10.23% over the previous year and a CAGR of 8.68% during the last 3

years5.The Indian advantage lies in the manufacturing of basic chemicals that are also

known as commodity chemicals that account for about 57% of the total domestic

chemical sector6.

1.7.2 Pace of technological change:

Indian chemical industry should strive for continually improving its production processes and

products by investing resources in technology development. Technological development may be

achieved by the chemical industry at two levels. In the bulk products segment, the chemical

industry should undertake process innovation with the objective of reduction in cost of

production. In addition, the industry needs to invest in technological resources that would lead to

specialized product development.

Liberalization process has already increased the possibility of intra-firm transfer of technology

and management practices in the form of consolidation within the economy as also from

developed countries through foreign direct investment.

4http://www.process-worldwide.com/management/markets_industries/articles/304269/

5http://www.india-exports.com/chemical.html

6https://www.dnb.co.in/IndianTelecomIndustry/Chemical%20overview.asp

Page 17

1.7.3 Product Innovation

Based on the observations that new intervention policies and strategies should find its way to

channel societal concerns and environmental externalities into the current closed system of

process innovation on basic chemicals. Some technology-oriented policy initiatives (e.g. EU

directives on integrated pollution and prevention control, best available technologies and

environmental impact assessment) can integrate with other market-oriented initiatives (e.g. EU

directives one missions trading, EU's official technology trading and information service

CORDIS,Innovation Relay Centers for trading technologies across Europe, environmental

funds). Such integration could help set the direct of process innovation to take environmental

externalities into account for innovation in the chemical industry--at least at an explicit level as

chemical policies on health and safety issues. Further research is need to study how to establish a

more open market for technologies where environmental friendly processes compete with

existing processes based on both economic and environmental performances7.

Conclusion:

Use of advanced technology, strong research capabilities, backward and forward linkages and

Development of domestic capacity to reduce dependence on imported raw materials is key

success factors for Indian chemical industry. In addition, safety, health and environment

protection issues are becoming important challenges for the Indian chemical industry. Indian

Manufacturers are addressing such challenges in an organized way. Indian chemical industry has

major strengths in basic research facilities available with CSIR laboratories such as National

Chemical Laboratory, Indian Institute of Chemical Technology, as also corporate R&D centers.

This ensures that development of process knowhow, plant process design, detailed engineering

design, commissioning assistance and even consultancy for re-engineering are available at low

cost. The need for globalization has made many Indian chemical companies enter into strategic

alliances or merge operations to achieve economies of scale. Foreign Collaboration is also

7 Tao Ren, 2005. An Overview of Innovation in the chemical industry: process innovation and product innovation,

Department of science technology and society, Netherlands, p-10

Page 18

bringing solutions for clean technology, process consultancy, and feedstock Linkages, R&D,

waste management, safe manufacture and environmental protection. In addition, Indian chemical

companies are attempting to achieve global standards by improving productivity through various

measures such as better raw material utilization, bi-product reduction and use, energy reduction

and conservation, effluent management, water management, up gradation of plant and

equipment, skill development.

Page 19

CHAPTER 2

MAJOR PLAYERS

Page 20

2.1 Aarti Industries Ltd

Aarti has started its operations in the year 1975 in the name of alchemie labs in a small of

way with a single product namely Dimentylsulphate.

Today Aarti is One of the leading supplier to global manufacturers of Dyes, Pigments,

Agrochemicals, Pharmaceuticals & rubber chemicals. Aarti has acquired world-class

expertise in the development & manufacture of these chemicals. Aarti is amongst the

largest producers of Benzene based basic and intermediate chemicals in India. It has

corporate office in Mumbai & representatives in U.S.A & Europe.

Aarti has 16 manufacturing units spread across Gujarat & Maharashtra and a

strong Research & Development with sophisticated instruments & pool of

scientists.

Aarti has strong Research & Development center with sophisticated instruments

& pool of scientists.

Aarti has customers spread across the globe in 60 countries with major presence

in USA, Europe, Japan & India.

AARTI has attained a group turnover of US $ 5151 million in the year April 2009 – March

2010.

AARTI group is strategically placed to exploit growth opportunities in the Chemical

Industry. In view of its technical expertise and broad base satisfied clientele in India and

abroad, AARTI is looking for global partners and strategic alliances in areas of mutual

interest viz.

1http://www.aartigroup.com/CompanyProfile/Mission_Vision.aspx

Page 21

Development of International markets for AARTI's products.

Toll manufacturing.

Transfer of Technology / Technical know-how.

Mission & Vision

Vision

To emerge as Key source to leading Global consumers of Specialty

Chemicals and Intermediates for Dye stuff, Agro, polymers, Pharma&

Surfactants.

Mission

To constantly strive to set up and maintain global size plant facilities.

To become customer-driven company by providing customized solutions

and service to meet changing customer requirements.

To maintain consistent quality and timely delivery at competitive prices.

To use best cost effective manufacturing methods supported by proven,

eco-friendly and safe technologies.

Commitment to growth by Research & new product developemtn&

progressive increase in Exports.

Continuous focus on people to encourage and nurture winning

organizational culture.

To meet the challenges of competition by dynamic management drive.

Page 22

2.2 Alkyl Amines Chemicals Ltd

Alkyl Amines Chemicals Ltd (AACL) is a public Limited Listed Company promoted in

1979. The Company is in the business of manufacturing and marketing various aliphatic

amines, amine derivatives and other specialty chemicals for the last 30 years.

It has two manufacturing sites with 9 production plants and related utilities at Patalganga

and Kurkumbh in Maharashtra. The company has an R&D center at Hadapsar, Pune.

Over the last decade, the company had added various new product processes which were

developed in the R&D to expand its product range through inhouse technology.

The first plant was commissioned in 1982 at Patalganga to make ethylamines with

technology from Leonard Process Company, USA. Subsequently, the capacity at the site

was expanded to manufacture other amines with technical know-how of Acid Amines

Technologies,USA, and now hosts 2 multipurpose amines plants with a capacity

exceeding 25000 MT/annum. In 1995 it started on its Kurkumbh complex where various

amines and amine derivatives are currently being manufactured in 7 production plants

with a capacity exceeding 30000 MT/annum. In the last decade, the company has added

various facilities to manufacture a wide range of specialty chemicals with its inhouse

developed technologies.

AACL is a global supplier of amines and amine-based chemicals to the pharmaceutical,

agrochemical, rubber chemical and water treatment industries, among others. It has

established a leading position in the domestic market and presence in the international

market with a reputation for reliable service and quality products with annual sales of

Rupees 400 Crores2.

2http://www.alkylamines.com/corporate/index.html

Page 23

2.3 Excel Industries Ltd

We are Excel Industries Ltd., one of India’s first domestic chemical manufacturers. We

are pioneers in indigenous chemical technology and sustainable waste management.

Innovation has always been a key driving force at Excel. Since our inception in 1941, we

have achieved hundreds of chemical process breakthroughs, steadily contributing to the

enhancement of technology knowhow in the nation.

As a corporation, we are committed to growth that is sensitive to the needs of the

environment, community and nation. Taking proactive steps in helping curb urban

pollution we have ventured into the Environmental and Biotechnology sectors where we

have developed novel solutions for Waste Management.

Today, we are all set to embark on a new phase of meaningful growth. We are one of the

India premier manufacturers of Specialty Polymer Additives and high quality Veterinary

APIs. We are also all set to apply our chemical process knowhow in the Pharmaceutical

Intermediates industry while continuing our leadership position in agro chemical

intermediates and phosphorous derivatives.

Even as we change, we take forward with us our core values of “People, Planet, Profit”

and seek to balance the needs of each of these pillars. The future beckons and we look

forward with excitement to developing innovations and breakthrough ideas.

Page 24

2.4 Godrej Industries Ltd.

Godrej industries a part of Godrej group, is India's leading manufacturer of oleochemicals

and makes more than a hundred chemicals for use in over two dozen industries. Godrej

Group was established in year 1897, it entered in security equipment & soaps segment

and is now a $1.875 billion conglomerate.

Godrej group is engaged in chemicals, vegoils& Real Estate. It delivers international

quality product, exports its products to North America, South America, Asia, Europe,

Australia, and Africa. The company was earlier called Godrej Soaps, then it got de-

merged with godrej consumer products & residual and became part of Godrej

industries.The company has its manufacturing plant located at facility at Vikhroli,

Mumbai, and Maharashtra .It has the capabilities of Fat splitting, Fatty Acid distillation,

Fatty Acid fractional distillation, Hydrogenation of Fatty Acids, Sweet water evaporation,

Glycerin distillation and Alfa Olefin Sulphonation. It also has a Co- generation plant

which satisfies partially its requirements of power and steam.

The greatest advantage Godrej Industries (Chemicals Division) enjoys, thanks to the

Vikhroli complex, is a high level of operational flexibility to meet customers'

requirements with a short lead time. The facility is well equipped to deliver the products

of superior Quality, in time and at competitive price.

The company also has a modern, integrated manufacturing facility at Valia in the Indian

state of Gujarat. This faculty uses vegetable oils as the raw material to manufacture Fatty

Acids, Glycerin, Fatty Alcohols & Surfactants such as Sodium Lauryl Sulphate, Sodium

Lauryl Ether Sulphate& Alpha Olefin Sulphonate. The installed capacity for Fatty

Alcohols is 65000 MT per annum which includes a dedicated Export Oriented Unit of

30000 MT.

Godrej Properties: The Company is India’s leading manufacturers of oleo chemicals and

over hundreds of different industrial chemicals. With its global reach spreading wings

across 40 countries, the company was conferred the prestigious exports award by

Chemexcil for 3 consecutive years in 1998-99, 1999-00 and 2000-01.The products in its

Page 25

portfolio are used in a variety of applications: cosmetics, tyres, detergents,

pharmaceuticals, cigarettes, toothpaste and more.

Godrej Consumer Products: Godrej Properties was incepted in 1990 with an aim of

providing ultra-modern townships to discerning customers at affordable prices. It adheres

to a simple philosophy of providing exemplary service based on the optimal use of

available resources.

Godrej Hershey: Godrej Hershey is one of the most respected business conglomerates

established in 2006 with a prime focus on the food division. The range of products from

the house of Godrej Hershey covers a number of popular products in the segment of

Confectionery, Non-Carbonated Beverages, Cooking Aids, Packet Tea and Edible Oil.

Godrej Agrovet: Godrej Agrovet, formerly a division of Godrej Soaps was reformed in

1971 with a focus on the agricultural sector. Over the years this division has developed a

close relationship with farmers with its innovative offerings in the form of animal feed,

oil palm plantations, agrochemicals and poultry.

Page 26

2.5 Pidilite Industries Ltd

Pidilite Industries, a well-known name in adhesives market, was incorporated in 1969.

Pidilite Industries is the market leader in adhesives and sealants, construction chemicals,

hobby colors and polymer emulsions in India.Over two–third of the company’s sales

come from products and segments it has pioneered in India.

The company has diversified in various segments such as adhesives and sealants,

construction and paint chemicals, automotive chemicals, art materials, industrial

adhesives, industrial and textile resins and organic pigments and preparations. It has

created brands like Fevicol, Dr Fixit, Cyclo, hobby ideas, Roff and M–Seal.

To facilitate better global networking, Pidilite Industries has established offices /

subsidiaries in several countries including Singapore, USA, Brazil, UAE, Saudi Arabia,

Indonesia, Egypt, Bangladesh, UK, Kenya, South Africa and Ghana.In India it has

subsidiaries namely Bhimad Commercial Company and Madhumala Traders.

Pidilite also established a state–of–the–art research centre in Singapore that is now a

member of Singapore Chemical Industry Council (SCIC).

Page 27

CHAPTER : 3

ANALYSIS OF CHEMICAL

INDUSTRY

Page 28

No. of Countries

3.1 Group Mapping

Interpretation

In order to visualize the segmentation of strategic groups, it is useful to design a "map"

(Müller-Stewens 2005):

For this purpose we have determine two variables which is helpful in classify the

strategic groups. These criteria form the X axis, where we have sketch as the no of

countries.

Thereafter on Y axis we have took different variable that is R&D exp. are in lacks.

The last step is to divide the companies into strategic groups. The companies which

are closest to each other form a strategic group. In our project group analysis three

companies are close competitors name of the companies are Aarti, Excel, alky

because of they are very near to each other as per R&D exp. and market share.

R & D

Exp.

Godhrej

Aarti

Pidlit

Alky

ll

Excel

Page 29

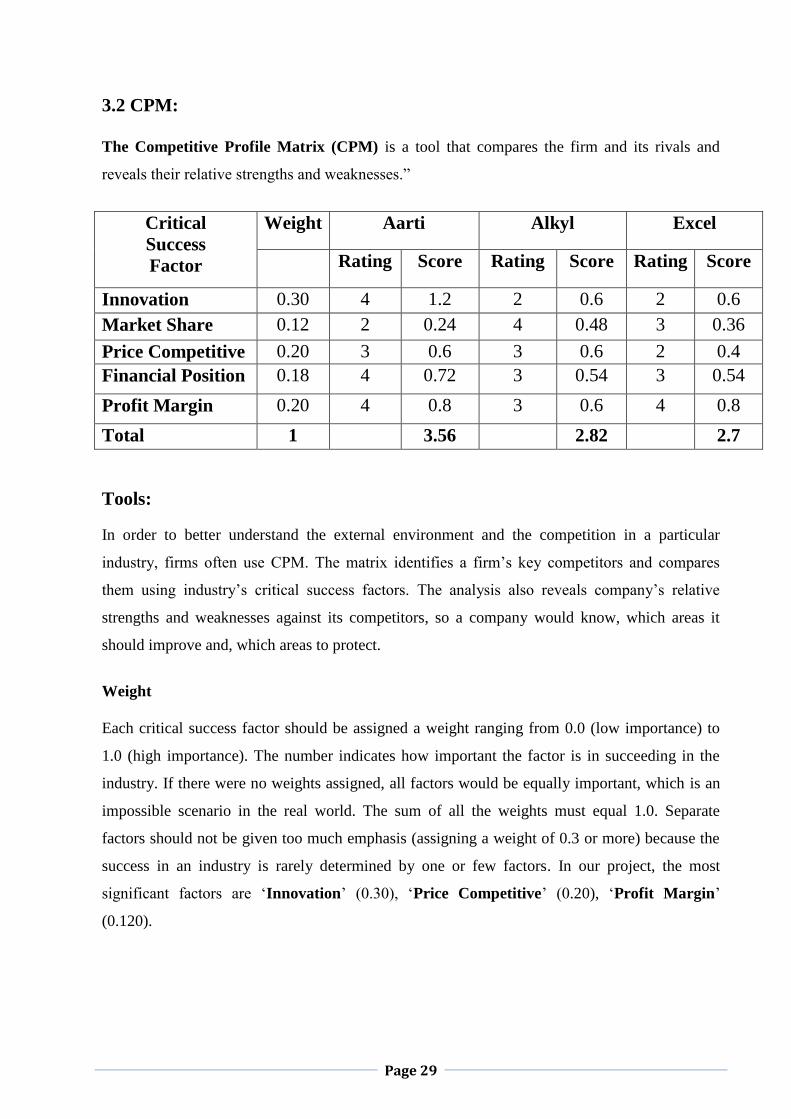

3.2 CPM:

The Competitive Profile Matrix (CPM) is a tool that compares the firm and its rivals and

reveals their relative strengths and weaknesses.”

Critical

Success

Factor

Weight Aarti Alkyl Excel

Rating Score Rating Score Rating Score

Innovation 0.30 4 1.2 2 0.6 2 0.6

Market Share 0.12 2 0.24 4 0.48 3 0.36

Price Competitive 0.20 3 0.6 3 0.6 2 0.4

Financial Position 0.18 4 0.72 3 0.54 3 0.54

Profit Margin 0.20 4 0.8 3 0.6 4 0.8

Total 1 3.56 2.82 2.7

Tools:

In order to better understand the external environment and the competition in a particular

industry, firms often use CPM. The matrix identifies a firm’s key competitors and compares

them using industry’s critical success factors. The analysis also reveals company’s relative

strengths and weaknesses against its competitors, so a company would know, which areas it

should improve and, which areas to protect.

Weight

Each critical success factor should be assigned a weight ranging from 0.0 (low importance) to

1.0 (high importance). The number indicates how important the factor is in succeeding in the

industry. If there were no weights assigned, all factors would be equally important, which is an

impossible scenario in the real world. The sum of all the weights must equal 1.0. Separate

factors should not be given too much emphasis (assigning a weight of 0.3 or more) because the

success in an industry is rarely determined by one or few factors. In our project, the most

significant factors are ‘Innovation’ (0.30), ‘Price Competitive’ (0.20), ‘Profit Margin’

(0.120).

Page 30

Rating

The ratings in CPM refer to how well companies are doing in each area. They range from 4 to 1,

where 4 means a major strength, 3 – minor strength, 2 – minor weakness and 1 – major

weakness. Ratings, as well as weights, are assigned subjectively to each company, but the

process can be done easier through benchmarking

Score & Total Score

The score is the result of weight multiplied by rating. Each company receives a score on each

factor. Total score is simply the sum of all individual score for the company. The firm that

receives the highest total score is relatively stronger than its competitors. In our Project, the

strongest performer in the market is Aarati industries ltd(3.56 points).

Benefits of the CPM:

The same factors are used to compare the firms. This makes the comparison more

accurate.

The analysis displays the information on a matrix, which makes it easy to compare the

companies visually.

The results of the matrix facilitate decision-making. Companies can easily decide which

areas they should strengthen, protect or what strategies they should pursue.

Page 31

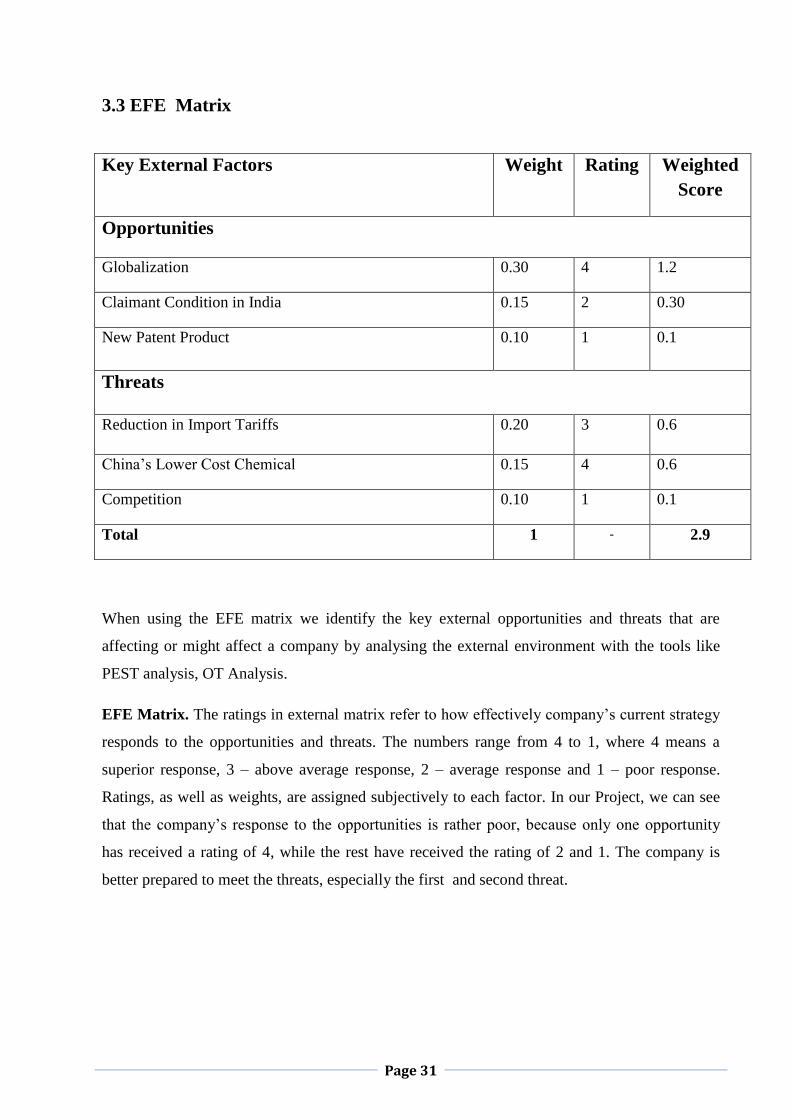

3.3 EFE Matrix

When using the EFE matrix we identify the key external opportunities and threats that are

affecting or might affect a company by analysing the external environment with the tools like

PEST analysis, OT Analysis.

EFE Matrix. The ratings in external matrix refer to how effectively company’s current strategy

responds to the opportunities and threats. The numbers range from 4 to 1, where 4 means a

superior response, 3 – above average response, 2 – average response and 1 – poor response.

Ratings, as well as weights, are assigned subjectively to each factor. In our Project, we can see

that the company’s response to the opportunities is rather poor, because only one opportunity

has received a rating of 4, while the rest have received the rating of 2 and 1. The company is

better prepared to meet the threats, especially the first and second threat.

Key External Factors Weight Rating Weighted

Score

Opportunities

Globalization 0.30 4 1.2

Claimant Condition in India 0.15 2 0.30

New Patent Product 0.10 1 0.1

Threats

Reduction in Import Tariffs 0.20 3 0.6

China’s Lower Cost Chemical 0.15 4 0.6

Competition 0.10 1 0.1

Total 1 - 2.9

Page 32

Weighted Scores & Total Weighted Score The score is the result of weight multiplied by rating. Each key factor must receive a score.

Total weighted score is simply the sum of all individual weighted scores. The firm can receive

the same total score from 1 to 4 in matrix. The total score of 2.9 is an good score. In external

evaluation a low total score indicates that company’s strategies are well designed to meet the

opportunities and defend against threats.

In our project, the company has received total score 2.9, which indicates that company’s

strategies are effective in exploiting opportunities or defending against threats. The company

should improve its strategy and focus more on how takes advantage of the opportunities.

Benefits

The matrixes have the following benefits:

Easy to understand. The input factors have a clear meaning to everyone inside or

outside the company. There’s no confusion over the terms used or the implications of the

matrices.

Easy to use. The matrix do not require extensive expertise, many personnel or lots of

time to build.

Focuses on the key internal and external factors. Unlike EFE only highlight the key

factors that are affecting a company or its strategy.

Multi-purpose. The tools can be used to build SWOT analysis, IE matrix, GE-

McKinsey matrix or for benchmarking.

Limitations

Easily replaced. EFE matrix can be replaced almost completely by PEST analysis,

SWOT analysis, competitive profile matrix and partly some other analysis.

Doesn’t directly help in strategy formation. Both analyses only identify and evaluate

the factors but do not help the company directly in determining the next strategic move

or the best strategy. Other strategy tools have to be used for that.

Too broad factors. SWOT matrix has the same limitation and it means that some

factors that are not specific enough can be confused with each other. Some strengths can

be weaknesses as well, e.g. Changing population psychograph, which can be a strong

and valuable Changing population psychograph or a poor Changing population

psychograph. The same situation is with opportunities and threats. Therefore, each factor

has to be as specific as possible to avoid confusion over where the factor should be

assigned.

Page 33

Industry Rivalry

Large number of competitors all competing for market

share

All are global competitors little room for expansion

All benefiting from economies of scale, so competing on

price

Little differentiation among current players

High fixed costs, and high exit costs

3.4 Porter’s Five Force Model:

Threat of New Entrants

Government regulations and patents

Significant capital requirements

Incumbents have superior efficiency and quality in production that may be difficult to imitate

Intense R&D and human capital requirements

Bargaining Power of Suppliers

Chemical industry relies on supplies from a few large corporations (such as those in petrochemicals industry)

Chemical producers have limited substitutes for inputs

Most suppliers are not dependent on their sales to chemical manufacturers

Bargaining Power of Buyers

Chemicals are important inputs to many industries

Those in chemical industry have many end-customers; don’t rely on one customer

The products (chemicals) are not greatly differentiated

Usually purchased through long-term contracts, so switching costs are high

Threat of Substitutes

Buyers tend to need specific chemicals as inputs

There really are no similar substitutes for chemicals

Even if another chemical can be used, it is most likely produced by the same Industry Players.

Page 34

3.5 Threat of New Entrants

1. Government regulations and patents

Rules under Environment (Protection) Act, 1986

Manufacture, Storage and Import of Hazardous Chemical Rules, 1989, 2000.

Chemical Accidents (Emergency Planning, Preparedness and Response)

Amendment Rules, 1996.

Public Liability Insurance Act, 1991, 1992.

Industrial Activities Covered in the regulations

Production, storages, use and import of the specified hazardous chemicals.

Chemical and petrochemical substances having hazardous (i.e. flammable,

explosive, corrosive, toxic) properties.

Storages of hazardous chemicals not associated with processes.

Bargaining Power of Suppliers

If the suppliers to an industry have strong bargaining power in the market, they can

reduce industry profits and slow industry growth. Some of the factors that can increase

supplier bargaining power include:

The industry being supplied is composed of a large number of competitors.

The supply industry is dominated by a few large firms.

The supply industry experiences little threat from substitutes.

Page 35

Bargaining Power of Buyers

If customers have strong bargaining power in the market, it can reduce industry profits

and slow industry growth. Some of the factors that can increase customer bargaining

power include:

The industry is composed of a large number of competitors.

The customer industry is dominated by a few large firms.

Customers purchase large volumes relative to seller sales.

Customers perceive little product differentiation.

Customers have low switching costs.

The product is unimportant to the cost or quality of the customer's product.

Threat of Substitutes

Substitute products are those products that can perform the same or similar function for

the customer. Substitutes may be very similar to the existing product, for example

substituting an aqueous cleaner for a solvent-based cleaner, or may be very different,

such as eliminating the need for cleaners by using a technology that reduces product

soiling.

Thus, identifying and anticipating potential substitutes requires more than monitoring

new product development by existing competitors. Potential substitutes can come from

almost any industry. Any product, service, or technology that can effectively perform the

same function for a customer may become a significant substitute threat.

Page 36

CHAPTER – 4

FINANCIAL ANALYSIS

Page 37

4.1 INTRODUCTION OF FINANCIAL ANALYSIS

Financial analysis converts raw information of financial statements in useful financial

information. Only after financial analysis, we can use financial statements for decision making.

These financial information are useful for planning. For example, we can estimate our future

ability of earning on advertising if we did financial analysis of our advertising expenses with

direct return on the investment in advertising. Like this, we can do financial analysis of each and

every item of profit and loss account, balance sheet and cash flow statement.

We highlighted the content and importance of the statement of change in financial position.

Management, creditors, investors and other use the information contained in these statements to

form judgment about the operating performance and financial position of the firm. User of

financial statement can get future insight about financial strength and weakness of the firm if

they properly analyse information reported in these statement. Management should be

particularly interested in knowing financial strength of the firm to make their best use and to be

able to spot out financial weakness of the firm to take suitable corrective action. The future plan

of the free should be laid down in view of the firm‘s financial strengths and weakness. Thus

financial analysis is the starting point for making plans, before using any sophisticated

forecasting and planning procedures. Understanding the past is a prerequisite for anticipating the

future.

For doing financial analysis, we use following tools.

4.1.1 Tool of Financial Analysis : Financial Statement Analysis

In financial statement analysis is that tool of financial analysis in which we create and highlight

the significant relationships of different items of financial statement. We also interpret that

relationship in simple words. For example, an investor may be interested to know past earning

data with its relationship with company's investments. Two type of financial statement analysis

are very important. One is horizontal analysis and second is vertical analysis. In horizontal

analysis, we compare all items of balance sheet and profit and loss account with previous years'

balance sheet and profit and loss account's items. In vertical analysis, we convert each element of

the information into a percentage of the total amount of statement so as to establish relationship

with other components of the same statement.

Page 38

4.1.2 Tool of Financial Analysis : Ratio Analysis

Actually, it is also financial statement analysis but for detail study we can make separate topic of

study. We calculate different ratios like revenue ratios, balance sheet ratios and mixed ratios.

Ratio analysis is based on fact, if we create relationship between two accounting figures, we can

get useful information relating to performance, strengths and weakness. For example, we know

that according to rule of thumb, debt equity ratio should not more than 2:1 because it is risky. As

an investor, we calculate debt -equity ratio before invest our money in the form of debt. Here are

two company and we have calculated its debt equity ratio.

Page 39

4.2 TREND ANALYSIS

Trend analysis is an aspect of technical analysis that tries to predict the future movement of a

stock based on past data. Trend analysis is based on the idea that what has happened in the past

gives traders an idea of what will happen in the future.

Method for calculating Trend:

Trend percentage Method:

We have utilized trend percentage method for the calculation of trend. For the trend analysis

index number is advocated. The procedure followed is to assign the number 100 to the item of

the base year and to calculate percentage change in each item of other years in the relation to the

base year. this procedure is called trend percentage method.

Base year for the trend analysis:

For the trend analysis, year dec 2006 is taken as base for the calculation of the trend of different

of balance sheet and income statement.

Page 40

4.2.1 Total income

INTERPRETATION:

The industry has a fluctuating flow of the income over the 5 year. The industry has increase till

2014, decreases in 2012 and rises 2013 as it has good sign for industry and reputed name. Also it

affects the earnings of shareholders.

0

20

40

60

80

100

120

140

2009-10 2010-11 2011-12 2012-13 20013-14

Total Income

Total Income

Year 2010 2011 2012 2013 2014

Aarti Industries Ltd 1320.15 1451.29 1699.69 2171.59 2705.02

Alkyl Amines Chemicals Ltd 211.82 245.21 287.95 372.21 448.89

Pidilite Industries Ltd 1996.13 2454.16 2887.01 3440.45 3963.44

Total 3528.1 4150.66 4874.65 5984.25 7117.35

Average 1176.03 1383.55 1624.88 1994.75 2372.45

100 117.645808 117.4428 122.7629 118.9347

Page 41

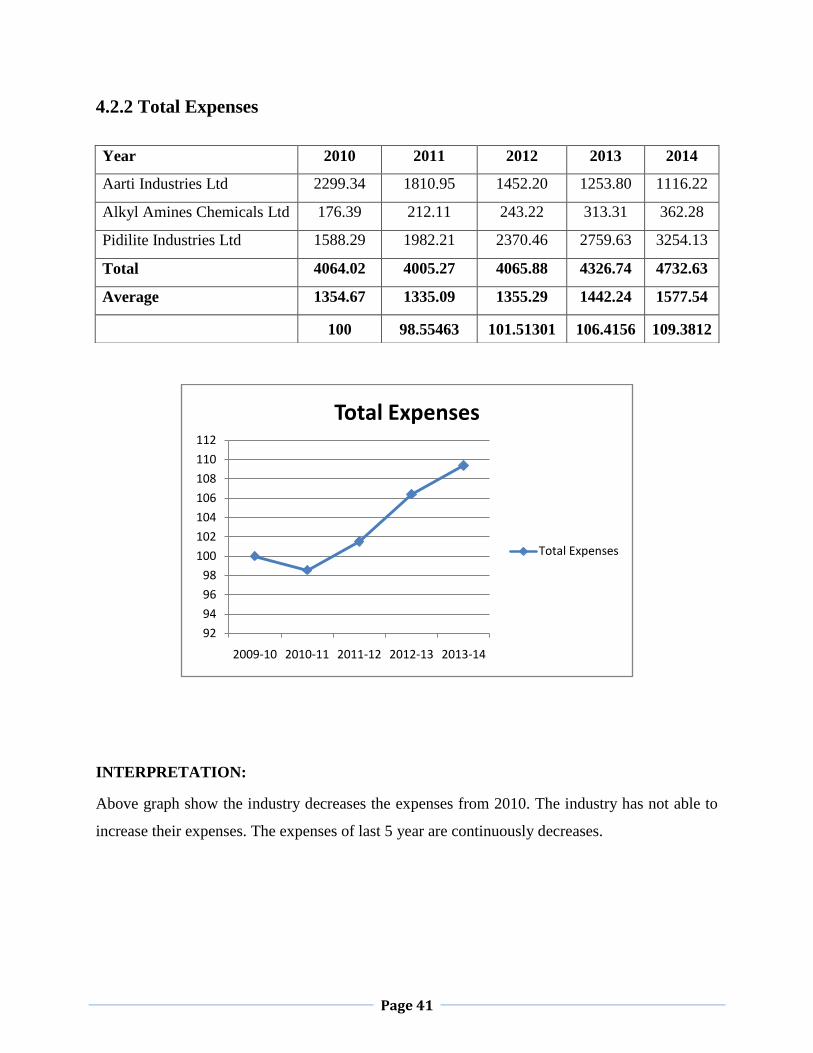

4.2.2 Total Expenses

INTERPRETATION:

Above graph show the industry decreases the expenses from 2010. The industry has not able to

increase their expenses. The expenses of last 5 year are continuously decreases.

92

94

96

98

100

102

104

106

108

110

112

2009-10 2010-11 2011-12 2012-13 2013-14

Total Expenses

Total Expenses

Year 2010 2011 2012 2013 2014

Aarti Industries Ltd 2299.34 1810.95 1452.20 1253.80 1116.22

Alkyl Amines Chemicals Ltd 176.39 212.11 243.22 313.31 362.28

Pidilite Industries Ltd 1588.29 1982.21 2370.46 2759.63 3254.13

Total 4064.02 4005.27 4065.88 4326.74 4732.63

Average 1354.67 1335.09 1355.29 1442.24 1577.54

100 98.55463 101.51301 106.4156 109.3812

Page 42

4.2.3 Operating Profit

INTERPRETATION:

Above graph show the industry different year operating profit over the 5 year. The graph

shows that in 2014 operating profit decreases and increases continuously till 2010.

0

20

40

60

80

100

120

140

160

2009-10 2010-11 2011-12 2012-13 2013-14

Operating Profit

Operating Profit

Year 2010 2011 2012 2013 2014

Aarti Industries Ltd 203.93 197.49 243.49 360.64 405.91

Alkyl Amines Chemicals Ltd 35.43 33.1 44.73 58.9 86.6

Pidilite Industries Ltd 407.84 471.95 516.55 680.83 709.32

Total 672.2 702.54 804.77 1100.37 1201.83

Average 215.73 234.18 268.25 366.79 400.61

100 108.55236 114.54864 136.7344 109.2205

Page 43

4.2.4 PBDT

INTERPRETATION:

Above graph show the industry fluctuating of PBDT over the 5 year. The industry has able to

improve their PBDT in current year.

0

20

40

60

80

100

120

140

160

2009-10 2010-11 2011-12 2012-13 2013-14

PBDT

PBDT

Year 2010 2011 2012 2013 2014

Aarti Industries Ltd 107.47 93.61 122.01 183.84 200.94

Alkyl Amines Chemicals Ltd 14.86 13.61 23.68 35.93 64.62

Pidilite Industries Ltd 328.87 397.4 444.12 619.57 631

Total 451.2 504.62 589.81 839.34 896.56

Average 150.4 168.20 196.60 279.78 298.85

100 111.835106 116.885 142.309 106.816

Page 44

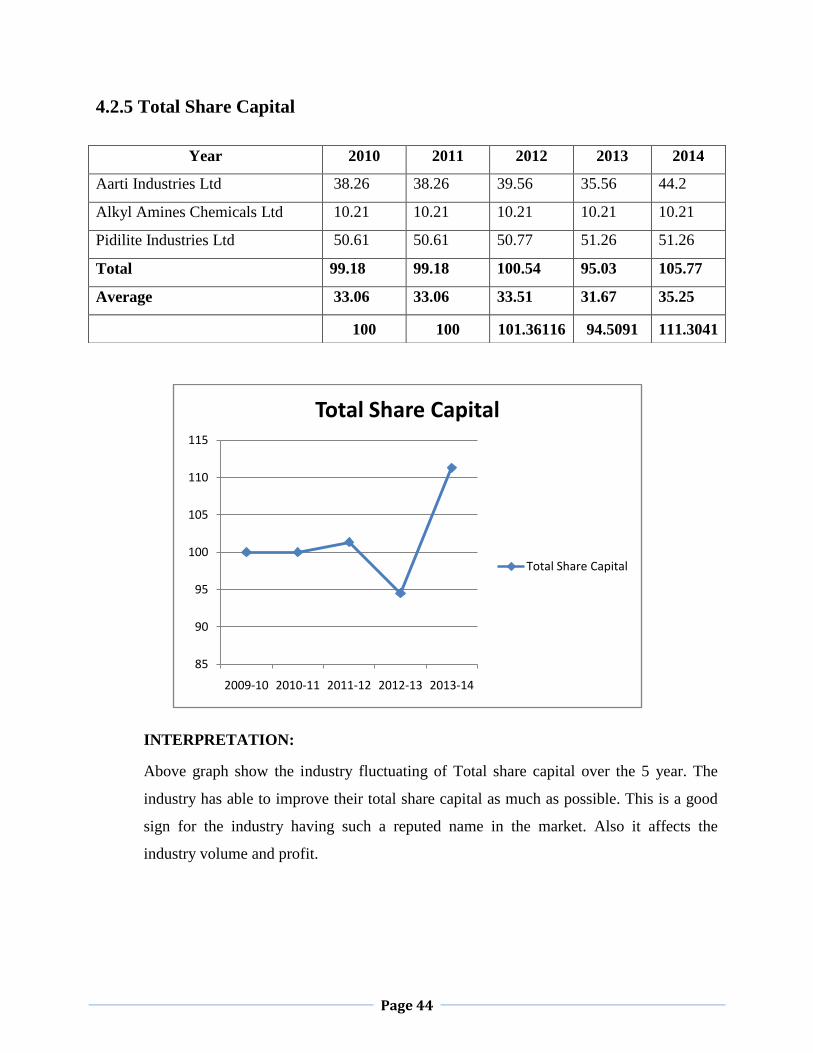

4.2.5 Total Share Capital

INTERPRETATION:

Above graph show the industry fluctuating of Total share capital over the 5 year. The

industry has able to improve their total share capital as much as possible. This is a good

sign for the industry having such a reputed name in the market. Also it affects the

industry volume and profit.

85

90

95

100

105

110

115

2009-10 2010-11 2011-12 2012-13 2013-14

Total Share Capital

Total Share Capital

Year 2010 2011 2012 2013 2014

Aarti Industries Ltd 38.26 38.26 39.56 35.56 44.2

Alkyl Amines Chemicals Ltd 10.21 10.21 10.21 10.21 10.21

Pidilite Industries Ltd 50.61 50.61 50.77 51.26 51.26

Total 99.18 99.18 100.54 95.03 105.77

Average 33.06 33.06 33.51 31.67 35.25

100 100 101.36116 94.5091 111.3041

Page 45

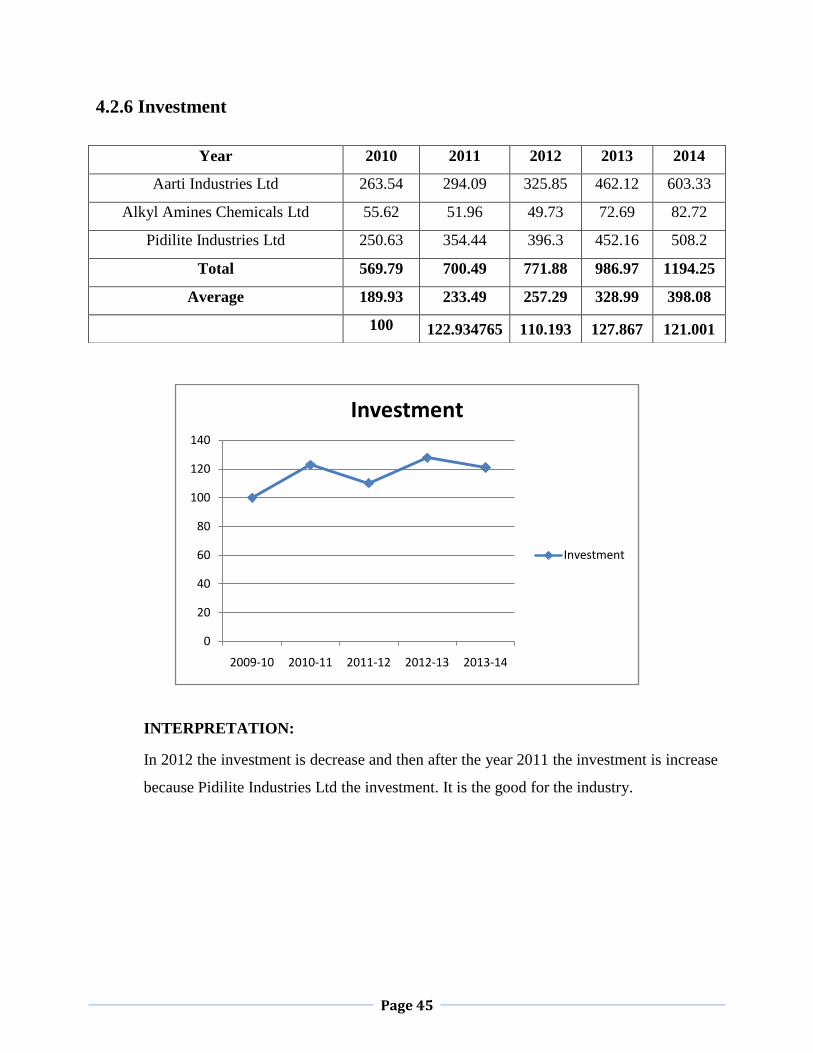

4.2.6 Investment

INTERPRETATION:

In 2012 the investment is decrease and then after the year 2011 the investment is increase

because Pidilite Industries Ltd the investment. It is the good for the industry.

0

20

40

60

80

100

120

140

2009-10 2010-11 2011-12 2012-13 2013-14

Investment

Investment

Year 2010 2011 2012 2013 2014

Aarti Industries Ltd 263.54 294.09 325.85 462.12 603.33

Alkyl Amines Chemicals Ltd 55.62 51.96 49.73 72.69 82.72

Pidilite Industries Ltd 250.63 354.44 396.3 452.16 508.2

Total 569.79 700.49 771.88 986.97 1194.25

Average 189.93 233.49 257.29 328.99 398.08

100 122.934765 110.193 127.867 121.001

Page 46

4.2.7 Total Asset

INTERPRETATION:

From the above trend of total assert of company we can say that company had good

growth rate in 2012 but after that it Increase in 2014.

0

20

40

60

80

100

120

140

2009-10 2010-11 2011-12 2012-13 2013-14

Total Assets

Investment

Year 2010 2011 2012 2013 2014

Aarti Industries Ltd 835.14 1112.66 1309.59 1739.83 079.10

Alkyl Amines Chemicals Ltd 183.21 199.88 214.28 254.9 292.66

Pidilite Industries Ltd 427.87 523.53 609.19 723.24 771.52

Total 1446.22 1836.07 2133.16 2717.97 3143.28

Average 482.07 612.02 711.05 905.99 1047.76

100 126.95667 116.18084 127.4158 115.6481

Page 47

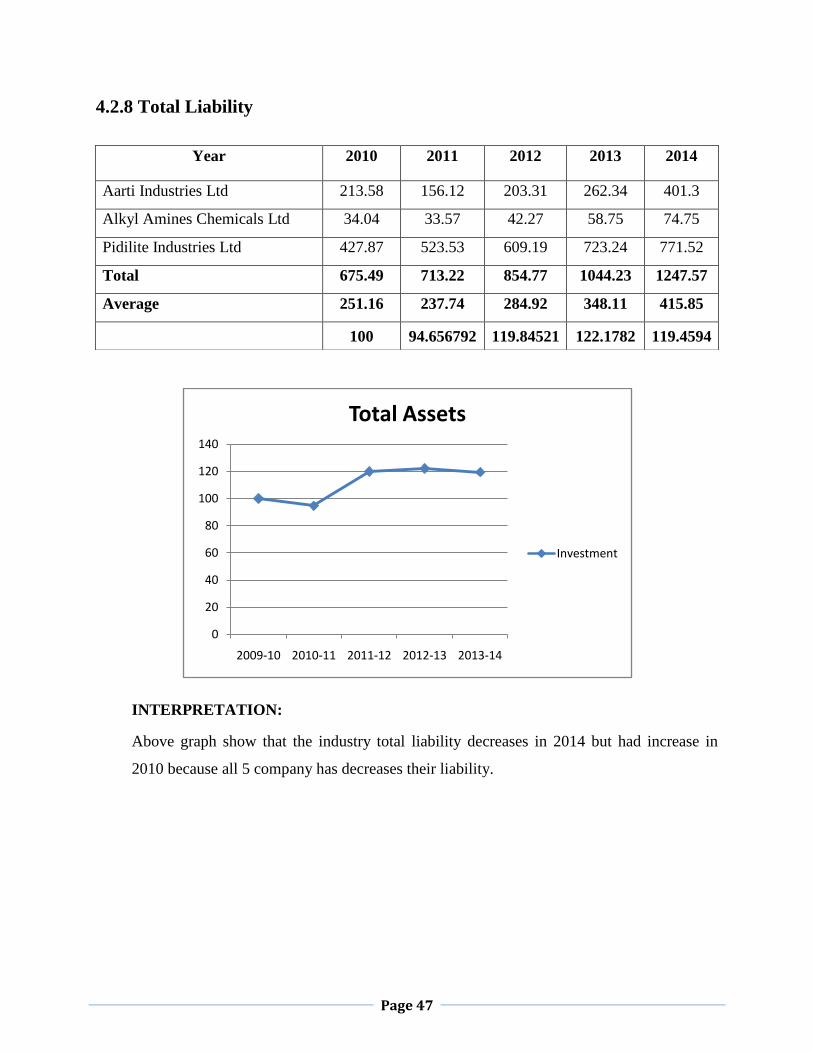

4.2.8 Total Liability

INTERPRETATION:

Above graph show that the industry total liability decreases in 2014 but had increase in

2010 because all 5 company has decreases their liability.

0

20

40

60

80

100

120

140

2009-10 2010-11 2011-12 2012-13 2013-14

Total Assets

Investment

Year 2010 2011 2012 2013 2014

Aarti Industries Ltd 213.58 156.12 203.31 262.34 401.3

Alkyl Amines Chemicals Ltd 34.04 33.57 42.27 58.75 74.75

Pidilite Industries Ltd 427.87 523.53 609.19 723.24 771.52

Total 675.49 713.22 854.77 1044.23 1247.57

Average 251.16 237.74 284.92 348.11 415.85

100 94.656792 119.84521 122.1782 119.4594

Page 48

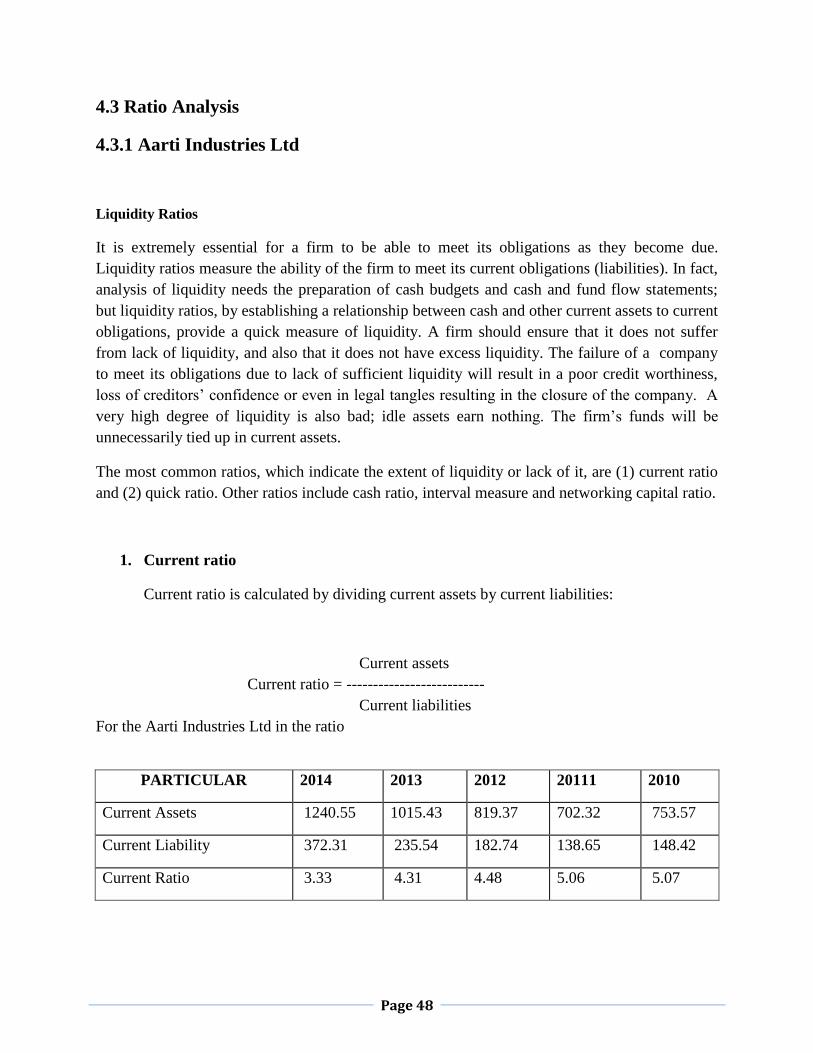

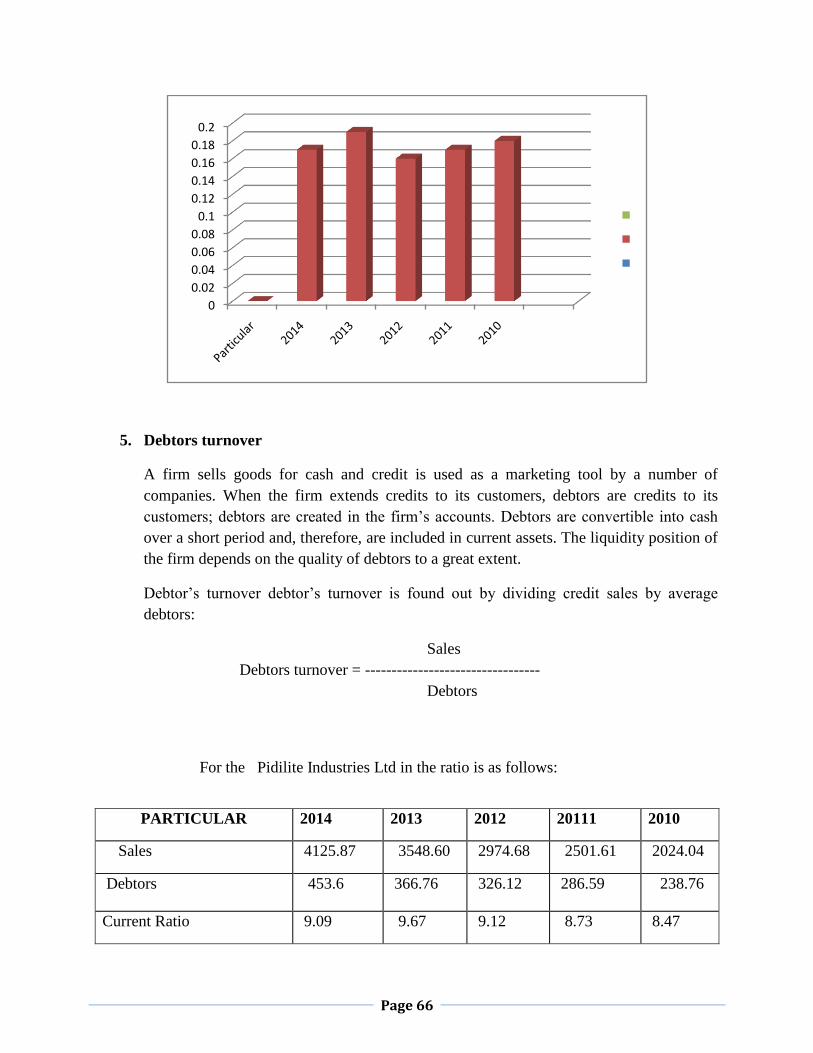

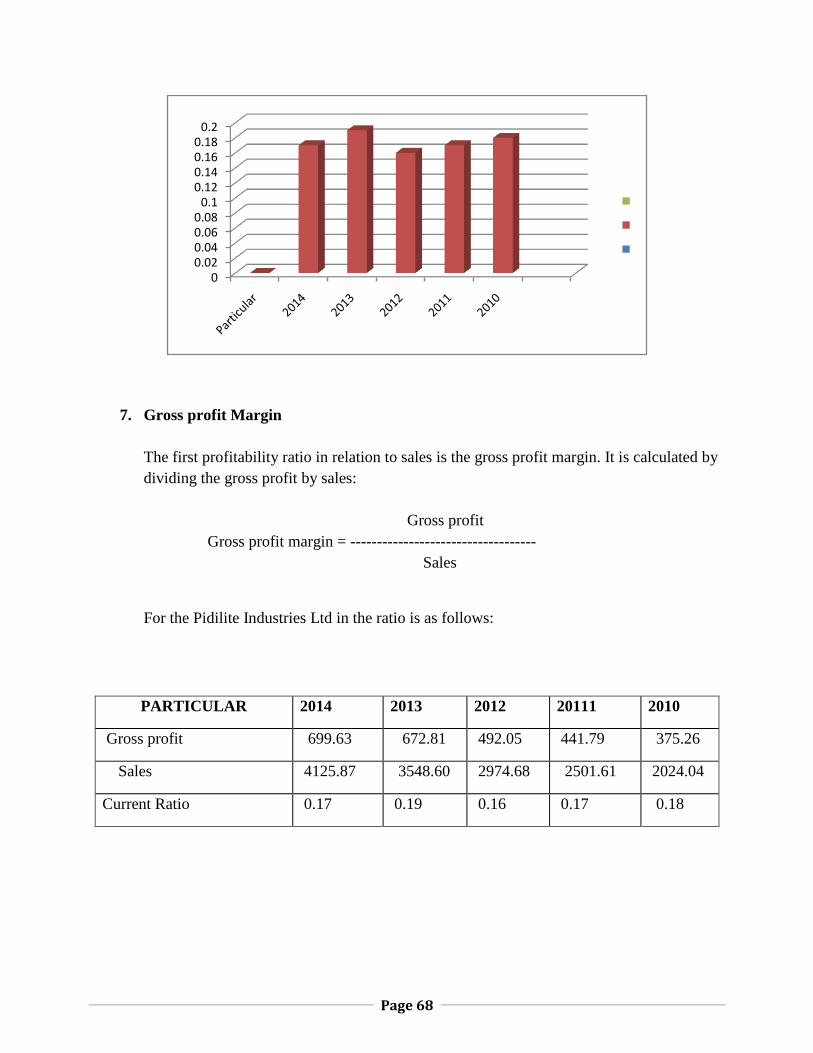

4.3 Ratio Analysis

4.3.1 Aarti Industries Ltd

Liquidity Ratios

It is extremely essential for a firm to be able to meet its obligations as they become due.

Liquidity ratios measure the ability of the firm to meet its current obligations (liabilities). In fact,

analysis of liquidity needs the preparation of cash budgets and cash and fund flow statements;

but liquidity ratios, by establishing a relationship between cash and other current assets to current

obligations, provide a quick measure of liquidity. A firm should ensure that it does not suffer

from lack of liquidity, and also that it does not have excess liquidity. The failure of a company

to meet its obligations due to lack of sufficient liquidity will result in a poor credit worthiness,

loss of creditors’ confidence or even in legal tangles resulting in the closure of the company. A

very high degree of liquidity is also bad; idle assets earn nothing. The firm’s funds will be

unnecessarily tied up in current assets.

The most common ratios, which indicate the extent of liquidity or lack of it, are (1) current ratio

and (2) quick ratio. Other ratios include cash ratio, interval measure and networking capital ratio.

1. Current ratio

Current ratio is calculated by dividing current assets by current liabilities:

Current assets

Current ratio = --------------------------

Current liabilities

For the Aarti Industries Ltd in the ratio

PARTICULAR 2014 2013 2012 20111 2010

Current Assets 1240.55 1015.43 819.37 702.32 753.57

Current Liability 372.31 235.54 182.74 138.65 148.42

Current Ratio 3.33 4.31 4.48 5.06 5.07

Page 49

2. Quick Ratio

Quick ratio, also called acid –test ratio, establishes a relationship between quick, or

liquid, assets and current liabilities. An asset is liquid if it can be converted into cash is

the most liquid asset.

Current assets – inventories

Quick ratio = ---------------------------------------------

Current liabilities

For the Aarti Industries Ltd in the ratio

PARTICULAR 2014 2013 2012 20111 2010

Current Assets - inventories 637.22 553.31 412.42 408.23 490.03

Current Liability 372.31 235.54 182.74 138.65 148.42

Current Ratio 1.72 2.35 2..26 2.95 3.31

0

0.02

0.04

0.06

0.08

0.1

0.12

Particular 2014 2013 2012 2011 2010

Page 50

3. Cash Ratio

Since cash is the most liquid asset, a financial analyst may examine cash ratio and its

equivalent to current liabilities. Trade investment or marketable securities are equivalent

of cash; therefore, they may be included in the computation of cash ratio:

Cash + Marketable securities

Cash ratio = -------------------------------------------------

Current liabilities

For the Aarti Industries Ltd in the ratio is as follows:

PARTICULAR 2014 2013 2012 20111 2010

Cash 12.35 9.71 8.81 7.77 11.41

Current Liability 372.31 235.54 182.74 138.65 148.42

Current Ratio 0.033 0.041 0.048 0.057 0.076

0

0.02

0.04

0.06

0.08

0.1

0.12

Page 51

4. Debt Ratio

Several debt ratios may be used to analyze the long-term solvency of a firm. The firm

may be interested in knowing the proportion of the interest-bearing debt in the capital