Maciej Bukowski, Urszula Siedlecka, Aleksander...

56

Maciej Bukowski, Urszula Siedlecka, Aleksander Śniegocki

Transcript of Maciej Bukowski, Urszula Siedlecka, Aleksander...

Maciej Bukowski, Urszula Siedlecka, Aleksander Śniegocki

.wise

-euro

pa.eu

The WiseEuropa Institute is an independent think-tank, specialising

in European and foreign policies and economics.

The mission of WiseEuropa is to improve the quality of domestic and European policies and

the economic environment by basing them on sound economic and institutional analyses, independent

research and assessments of the impact of policies on the economy. The Institute invites citizens,

entrepreneurs, experts and authors of public policies, at home and abroad, to share their ideas about the

modernisation of Poland and Europe and their role in the world.

WiseEuropa holds the highest competencies in areas such as: European and global economic and political

affairs, macroeconomic, industrial, energy and institutional policy, innovation and digital economy, the

labour market and social policy. WiseEuropa has solid analytic expertise in quantitative and qualitative

research methods: statistics and econometrics, macroeconomic and system modelling, social and political

research, institutional and sociological analyses. Everything supported by the Institute’s high quality

communication and PR activities.

Al. Jerozolimskie 99/18 | 02-001 Warsaw | t.: +48 22 400 93 03 | f.: +48 22 350 63 12 | [email protected]

Coalapse – will fusion with the energy sector save Polish mining?

Authors:

Maciej Bukowski,

Urszula Siedlecka,

Aleksander Śniegocki

Warsaw Institute for Economic Studies

Aleje Jerozolimskie 99 lok. 18

02-001 Warszawa

www.wise-europa.eu

WiseEuropa would like to thank the Greenpeace Polska Foundation for assistance in preparing this report.

Cover design, typesetting, DTP: Studio graficzne TEMPERÓWKA s.c. and key.waw.pl

Copying or distributing with credit to the source.

© Copyright by Warszawski Instytut Studiów Ekonomicznych, Warsaw, 2016

ISBN: 978-83-64813-20-7

Free copy

The Warsaw Institute for Economic Studies, using the WiseEuropa brand, have exercised utmost care to ensure that all information contained herein is

accurate and true as at the date of publication. However, WiseEuropa and its employees are not liable for their accuracy or completeness and are not

liable for any losses that may occur as a result of using this publication or information found herein.

This publication has been prepared for information purposes only and does not constitute an investment recommendation or offer to purchase or sell any

financial instrument, within the meaning of the Civil Code, Act of 29 July 2005 on Public Offering, Conditions Governing the Introduction of Financial

Instruments to Organised Trading, and Public Companies (Journal of Laws [Dz.U.] 2005, No. 184, item 1539) or the Act of 29 July 2005 on Trading in

Financial Instruments (Journal of Laws [Dz.U.] 2005, No. 183, item 1538). No part of this report is or shall be construed as a “recommendation” within the

meaning of the Regulation of the Minister of Finance dated 19 October 2005 on information constituting recommendations concerning financial

instruments or their issuers (Journal of Laws [Dz.U.] 2005, No. 206, item 1715).

WiseEuropa, especially through information found in this publications, does not provide advisory services in connection with any transactions made by the

reader of this report and does not provide any investment advice or recommendations for making such transactions. WiseEuropa specifically excludes

liability for any consequences of use by readers of the information found in this report or for the consequences of investment decisions that were taken on

its basis. Concluding any transaction, the reader of this report makes independent and autonomous decisions, acting on their own account and at their

own risk.

Executive Summary 5

Recommendations 7

1. Introduction 10

2.

Methodology

11

2.1. Scope of the analysis 11

2.2. Mining restructuring process 12

2.3. Impact of the consolidation on energy companies and

investors

15

2.4. Impact on consumers and taxpayers 16

3.

Outlook for Polska Grupa Górnicza

20

3.1. Restructuring scenarios 20

3.2. PGG’s impact on energy companies 25

3.3. PGG’s impact on consumers and taxpayers 28

4.

Sectoral integration

31

4.1. Restructuring scenarios 31

4.2. Impact of sectoral integration on energy companies 35

4.3. Impact of sectoral integration on consumers and taxpayers 38

5.

Consolidation during permanent stagnation on the coal

market 41

5.1. Forecasted stagnation of coal prices 41

5.2. Outlook for PGG under stagnation of coal prices 42

5.3. Sectoral integration under stagnation of coal prices 47

6.

Summary

50

Bibliography 52

List of figures 53

Coalapse – will fusion with the energy sector save Polish mining?

5

Executive Summary

• Integration of the mining industry and the energy sector will have negative impact on

the economy, unless it is accompanied by closing down of the permanently unprofitable mines and by a

significant improvement in mining productivity. This means limiting coal production

in the top three Polish mining companies by over 40% and reducing employment by half

by 2018. Making a swift decision to transfer the unprofitable mines to the Mine Restructuring Company

in order to phase them out will limit the social cost of restructuring, stretching it over

a period of 2 to 3 years. After this period, the EU regulations will make it impossible to support the

liquidation of unprofitable mines, which may lead to uncontrolled bankruptcies and sudden lay-offs of

all miners.

• Polska Grupa Górnicza (PGG), formed in accordance with the agreement concluded in April 2016

between the government and the investors together with trade unions, has little chance

of becoming profitable. PGG’s initial business plan assumed supporting its operations on

the condition that the prices of coal rise and that the productivity improvement scheme to be

consistently deployed in the coming years is successful. However, the implied return on capital was not

attractive enough for investors. The April agreement further deteriorated the outlook for the Group:

even if the prices of coal increase and the assumed improvement in productivity is achieved, the Group

will require further recapitalisation at the beginning of the next decade.

A persistent stagnation of prices and failure of the restructuring process would result in PGG facing

bankruptcy in 2020 at the latest, and perhaps as early as in 2018. Only a permanent closure of

unprofitable mines (around half of the mining capacity) and an appropriate reduction in employment

will give PGG investors a real chance to generate a profit when the prices of coal rebound and to reduce

losses if they are stagnant.

• Direct acquisition of mines by energy companies is unprofitable and may result in multi-billion zloty

losses. A less risky option for the energy sector is equity interest in mining companies, which makes it

more difficult to indefinitely transfer losses of unprofitable mines onto energy companies. However, just

as in the case of the PGG investment, only an approach that assumes a prompt discontinuation of

unprofitable mining operations and focusing on the most productive mines would allow energy

companies to generate an appropriate return on investment, one that will ensure time for more

profound restructuring in times of unfavourable market conditions.

• If restructuring in the mining industry fails, the potential transfer of the costs of upkeep

of unprofitable mines from the energy sector onto citizens would mean that every

household would spend an additional PLN 220-360 (ca. EUR 50-85) a year. If the costs

of the permanent deficit were to be financed by consumers of electricity or coal, their prices would

need to increase by PLN 20-30 (ca. EUR 5-7) per MWh and PLN 180-290 (ca. EUR 40-70) per tonne.

However, this would probably involve breaching EU regulations not only in the area of energy and

climate but also state aid rules. That is why making citizens cover the costs

of maintaining the mining industry by consolidating the energy and mining sectors is neither

a desirable, nor a realistic alternative to the actual restructuring of Polish mines.

Coalapse – will fusion with the energy sector save Polish mining?

6

• In the next two decades, energy companies will need to invest several hundred billion zloty

in modernising infrastructure. Otherwise, they will not only become uncompetitive and lose their

market position but may also become a threat to the energy system and the entire economy. Their

investment capacity is also limited and covers 40% to 70% of the investment needs of the Polish energy

sector. In this situation, engagement in unprofitable mining operations may materially deteriorate the

development outlook for the state-owned energy companies. Moreover, if restructuring the mines that

have been taken over is unsuccessful, this may pose a threat to the survival of some of the energy

companies.

• Losses anticipated by the owners of energy companies involved in saving the mining industry are likely

to range between a few percent of market capitalisation, if coal prices increase and

the restructuring process is successful, and over 50% (or 100% in the worst case scenario)

if the prices of this commodity remain low or if the restructuring process is unsuccessful. Also from this

perspective, a viable, ambitious restructuring strategy is crucial.

Coalapse – will fusion with the energy sector save Polish mining?

7

Recommendations

• The plans of restructuring mining companies should assume closing down the most unprofitable mines.

This would increase the chances of success of the entire process and ensure that energy companies

benefit from the consolidation initiatives. The goal of restructuring should not be maintaining the

current production volumes, but rather establishing a new permanent balance in the Polish mining

industry for the next 20 years. The new balance should assume a much smaller scale of mining

operations, which would be based on solid economic foundations.

• It is important to avoid direct acquisitions of unprofitable mines by energy companies. Capital

involvement of energy companies in mining enterprises (i.e. taking part in their recapitalisation) limits

the extent of potential losses, provided that it is one-off, relatively small and accompanied by an

economically sound restructuring scheme. Considering the negative experiences so far with the

functioning of state-owned mining companies and the risk of a permanent stagnation of coal prices, it is

worth considering the privatisation of the restructured mining enterprises. In this scenario, the energy

sector could act as a temporary investor overseeing the restructuring process and reselling

(with a profit) profitable mining assets to private investors.

• The potential recapitalisation of mining companies by the energy sector or any other investor should be

conditional on presenting a realistic profitability improvement plan, going beyond

the one presented during the PGG negotiations. It is important that the execution of the plan

by the company should be monitored and additional remedial actions should be taken, if needed (e.g.

further production reduction, deeper restructuring of employment or closing down the unprofitable

mines).

• Poland’s energy policy should aim for adjusting the production of electricity from coal to reflect the

declining potential of profitable coal mining. A paradigm in which energy security has to be based on

domestic mining needs to be confronted with the reality: the scale of economically justified mining

operations is already much below the level actually maintained, which translates to huge losses. The

problem will get worse in the future, as employees will put more pressure on wage raises and suppliers

will increase their prices.

• This will call for a gradual technological diversification of power and heat generation. The pace

of changes should reflect the declining hard coal production in Poland. According to the presented

estimates, hard coal mining is expected to become uneconomical in Poland in the next 20 years. Given

the various options for ensuring energy security with own resources, it is important to consider the

potential of domestic renewable energy sources and investing in improving energy efficiency.

Coalapse – will fusion with the energy sector save Polish mining?

8

bill

ion

PLN

'15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

20

28

20

29

20

30

20

31

20

32

20

33

20

34

20

35

20

36

bill

ion

PLN

'15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

20

28

20

29

20

30

20

31

20

32

20

33

20

34

20

35

20

36

Assumptions for mining and employment in the PGG restructuring scenario

Scenario

Production, in million tonnes

Employment, in thousands

Permanent change in salaries?

2015

2018

2036

2015

2018

2036

No restructuring

26

26

28

36

39

39

No

April agreement

30

22

No

Initial business plan

30

22

Yes

Deep restructuring

15

15

13

10

Yes

Source: WiseEuropa, own calculations

PGG’s equity capital by restructuring scenario and coal price forecasts

Gradual increase in coal prices 14

12

Stagnation of coal prices 6

5

r=3%

10

r=7% 4

8

3

6 r=3%

2 4

2 .. r=0% 1

r=0%

0 0

— No restructuring — April agreement — Initial business plan — Deep restructuring

Source: WiseEuropa, own calculations

Coalapse – will fusion with the energy sector save Polish mining?

9

Ch

ange

s in

mar

ket

cap

of

ener

gy c

om

pan

ies

Ch

ange

s in

mar

ket

cap

of

ener

gy c

om

pan

ies

Assumptions for mining production and employment in the scenario assuming restructuring of PGG, JSW and KHW mines

Scenario

Production, in million tonnes

Employment, in thousands

Permanent change in salaries?

2015

2018

2036

2015

2018

2036

No restructuring

54

56

49

76

79

68

No

Shallow restructuring

65

42

No

Moderate restructuring

65

41

Yes

Deep restructuring

32

31

33

23

Yes

Source: WiseEuropa, own calculations

Estimated impact of the takeover of PGG, JSW and KHW mines on the market capitalisation of energy

companies by mining industry restructuring scenario and the coal price projections

20%

Gradual increase in coal prices

+10%/+15%

Stagnation of coal prices

0%

0%

-20%

-40%

-60%

-80%

-100%

-78%

/-53%

No

restructuring

-17%/-11%

Shallow

restructuring

-5%/-3%

Moderate

restructuring

Deep restructuring

-20%

-40%

-60%

-80% -100%

-85%

/-100%

No

restructuring

-65%/-44%

Shallow

restructuring

-49%/-33%

Moderate

restructuring

-10%/-7%

Deep

restructuring

Source: WiseEuropa, own calculations

Coalapse – will fusion with the energy sector save Polish mining?

10

1. Introduction

2016 is a crucial year for the Polish mining industry.

The end of the commodity boom on the global market and the EU

regulations that prevent subsidising unprofitable mines revealed

the massive scale of structural problems the industry faces, forcing decision-

makers to make the effort and restructure it. Since late 2014, a few of the

less productive mines were transferred to the Mine Restructuring Company

and employment in the industry dropped significantly, which triggered a

noticeable increase in productivity.

However, the actions taken so far are far from satisfactory. Regaining financial stability by the sector requires

making major investments and cutting costs. As the mining sector has no available resources, energy

companies are to become involved in the restructuring process. The Polish energy sector needs to face the

challenge of financing the capital-intensive modernisation of the ageing electricity and heat generation and

distribution infrastructure as also needs to comply with the climate, energy and environmental requirements

of the European Union.

In this report we attempt to present the results of merging the coal mining and the energy sectors

in Poland. To this end, we evaluate the perspectives ahead of the just established Polska Grupa Górnicza,

which is to take over the assets of Kompania Węglowa, and we consider the results

of the broader consolidation scenario, assuming vertical integration of also the mines that are currently

owned by Jastrzębska Spółka Węglowa and Katowicki Holding Węglowy. We also consider various

restructuring scenarios, analysing how they may affect the investment capacity of energy companies and

their valuations, and indirectly the wallets of consumers and taxpayers.

The analysis starts with a brief overview of the methodology. In the next three chapters we describe the

outcomes of the individual scenarios of consolidating the coal mining and energy sectors and

we also analyse the sensitivity of the obtained results to changing market conditions. The last chapter

contains a summary of the analysis and recommendations.

Coalapse – will fusion with the energy sector save Polish mining?

11

2. Methodology

2.1. Scope of the analysis

This report is an analysis of the possible options for consolidating the coal mining and energy sectors. The

first scenario assumes taking over mines by a special purpose vehicle (SPV) whose shares are acquired by

energy companies. This scenario corresponds to restructuring of Kompania Węglowa (KW) by forming Polska

Grupa Górnicza (PGG) and recapitalising the new entity by state-controlled energy concerns, which became

its shareholders. As the key elements of this transaction are publicly known, it was possible to run an analysis

focused on companies involved in it. An alternative approach to consolidation of the domestic energy and

mining sectors is taking over individual mines and mining companies by energy companies. It is important

to stress that the establishment of the PGG does not exclude this step in the future. It may be introduced in

the event of restructuring of the JSW or the KHW, or even the recently formed PGG, if the project fails. Given

the variety of consolidation options in this scenario (individual mines may be acquired

by different energy companies), we have analysed its effects for the entire sector. The results serve as an

estimate of the potential long-term burden of Polish mining on energy companies.

Box 1. Analysed scenarios of integrating the coal mining and energy sectors

Relying on the information about coal mining restructuring which was publicly available in early May 2016, we

have identified two consolidation scenarios:

• BASIC SCENARIO assuming acquisition of Kompania Węglowa mines by Polska Grupa Górnicza, recapitalised,

among others, by PGE, Energa and PGNiG Termika,

• ALTERNATIVE SCENARIO assuming acquisition of individual mines operated in April 2016

by Kompania Węglowa, Katowicki Holding Węglowy and Jastrzębska Spółka Węglowa by PGE, Energa, Tauron

and Enea.

Source: WiseEuropa research

We began our analysis with the evaluation of the impact of restructuring initiatives in mining on the

financial performance of mines and mining companies. That is why for every consolidation scenario (see Box

1) we have considered various changes in the profitability of assets acquired by the energy sector. The next

step was the evaluation of the impact of the consolidation process on the financial performance of energy

companies, including their investment potential. We have narrowed our analysis to the four leading Polish

energy groups: PGE, Energa, Tauron and Enea as well as three mining companies: PGG (formed from the

former Kompania Węglowa), KHW and JSW.

Coalapse – will fusion with the energy sector save Polish mining?

12

The last step was the estimation of the impact of the consolidation processes on investors (assuming that the

energy sector will not be compensated for the potential losses suffered), consumers (if losses are shifted to

end users) and taxpayers (if losses suffered by energy companies were to be covered directly or indirectly

from the state budget).

Diagram 1. Steps in the evaluation of consolidation of the energy and coal mining sectors

Effectiveness of

restructuring the

acquired mines

Impact on energy

companies

Impact on

investors,

consumers and

taxpayers

Source: WiseEuropa research

2.2. Mining restructuring process

The economic restructuring of coal mining is a complex process, whose effects can only be precisely

estimated by examining detailed data on geological conditions and organisation of mining in each mine

separately. If more aggregated data is examined, however, it is still possible to perform

the relevant calculations with a relatively small margin of error. Successful restructuring is mainly

conditioned on strictly economic factors, determining the costs and revenues of mining enterprises. The

former are mainly unit labour costs, which depend on employment level, extraction productivity and miners’

salaries. An important factor on the cost side is also the scale of modernisation investments and the quality

of management that affect all other mining costs (e.g. effective use of outsourced services). Mining revenues

are predominantly conditioned by global and domestic market forces that cause coal price fluctuations, as

well as by changes in demand for this fuel from the energy sector.

Based on these factors we can evaluate the relation between mining profitability and the chosen

restructuring scenario as well as external factors, such as the market price of coal. The calculations require

a limited number of parameters and a few assumptions about their future evolution. The necessary data is

available in the financial statements of mining enterprises and other publicly available sources, disclosed by

the companies or other stakeholders, including unions and the Ministry of Energy. A particularly important

data source is the business plan of Polska Grupa Górnicza (KW 2016) supplemented with information on the

directions of restructuring, expected changes in employment and the anticipated cost reduction in mines.

Coalapse – will fusion with the energy sector save Polish mining?

13

Diagram 2. Estimation of the impact of restructuring and external factors on the profitability of mines

Restructuring External factors

Overall improvement in

management

Other costs

Changes in labour

productivity

Changes in salaries

Labour costs

Coal price

Trends on the global

coal market

Scale of investments Amortisation and depreciation

Profit/loss on coal sales

Financial costs

Liabilities from

previous years

Cost of debt

Pre-tax net profit/loss

Source: WiseEuropa research

Taking into account considerable uncertainty regarding the outcomes of restructuring initiatives in each

option of integrating the energy and mining sector, we analyse four scenarios:

• Moderate restructuring (for PGG – Initial business plan), consistent with the initial plans

of the government regarding the sector’s restructuring. It assumes retaining all mines, salary cuts and

significant improvement in labour productivity, achieved mainly through significant reduction in

employment.

• Shallow restructuring (for PGG – April agreement), assumes taking similar steps as in the moderate

restructuring scenario, yet maintaining the miners’ remuneration scheme, with a temporary withdrawal

from paying the so-called fourteenth salary until 2017.

Coalapse – will fusion with the energy sector save Polish mining?

14

• Deep restructuring assumes a significantly greater improvement in profitability than in

the Moderate restructuring scenario, thanks to closing down of the least efficient mines and investment

in the most productive assets.

• No changes, maintaining status quo ante, i.e. maintaining all mines without any productivity

improvements.

The analysed period is 2016–2036. A number of common assumptions regarding the market

environment of the mines have been made for all the scenarios (Table 1).

Table 1. Common assumptions for all analysed mine restructuring scenarios

Parameters – levels

Depreciation rate

20%

Cost of debt

7%

Parameters – dynamics (average annual growth)

Coal price, 2016–2036

+1.9% (chapters 3 and 4) +0.4% (chapter 5)

Salaries – after completion of restructuring

+3.2%

Other unit mining costs (excluding depreciation) – after completion of restructuring

+2.4%

Labour productivity improvement dynamics* – after completion of restructuring

+1.6%

Source: WiseEuropa research; *not applicable in the “No changes” scenario

The assumed future coal price dynamics is based on the most recent forecasts of the World Bank

(2016a and 2016b) for the global market up to 2025, which we have extrapolated onto

2026–2036. The January forecast has been assumed as the baseline. It predicts a moderate increase in the

prices of coal in the long-term, similarly to other forecasts from last year (e.g. DECC 2015). The forecast

published by the World bank in late April 2016 assumes stagnation of the coal prices

in the long term. It reflects the convictions that are voiced ever more frequently that in the next few years

the supply of coal will exceed demand globally, which should prevent coal prices on the global market to

increase again (e.g. IMF 2016). We assume coal price stagnation until 2036 in order

to perform the sensitivity analysis of the effects of consolidating the energy and mining sectors –

the results are presented in Chapter 5.

We assume that after a couple years of restructuring salaries will start increasing again,

in line with the overall trend of improving productivity in the economy. This assumption

is based on the anticipated wage pressure which will be exerted on the mining sector

by the rest of economy, especially the manufacturing sector, which employs similarly-qualified staff

(see Bukowski et al. 2015). A necessary condition to handle this pressure by the mining sector is to gradually

improve labour productivity in the restructured mines.

Coalapse – will fusion with the energy sector save Polish mining?

15

We assume that this will be achieved by constantly introducing organisational and technical improvements,

coming as a result of the appropriately high investments. This requires reaching

the sufficient EBIT profitability level. Improving labour productivity will slow down the increase

in other costs not associated with the consumption of fixed capital (especially outsourced services), which

will cause them to increase slower than average salaries in the economy.

Subsequent chapters contain more detailed information about the size of the necessary investments,

improving mining productivity, shifts in salaries and the mining output during restructuring in each

of the analysed scenarios of consolidation of the mining and energy sectors.

2.3. Impact of the consolidation on energy companies

and investors

An analysis of the effects of each option of integrating the coal mining industry and the energy sector in the

light of several different restructuring scenarios in the industry allows to determine

the cash flows and Net Present Value (NPV) of the investments in mining companies and mines from the

investor’s perspective. This allows to evaluate the impact of consolidation on the key financial parameters of

energy companies, their investment capacity and capitalisation (and therefore stock prices). The evaluation

includes the following:

• estimation in variants of the ranges of investment capacity of individual energy companies, when they

are not involved in restructuring the mining sector – the range depends, among all,

on restructuring the energy sector itself but also on external conditions, e.g. the shape of future

regulations or the market price of electrical energy,

• calculating the impact of cash flows generated through capital involvement in coal mining on

the investment capacity of energy companies, assuming that 40% of their profit will be allocated for

dividend payments and that the share of external financing reaches 50%,

• calculating the investment capacity of energy companies in different options and scenarios that assume

consolidation with mining.

Estimations are performed based on historical financial data and assumptions for

the development of the Polish energy sector up to 2036. The low option assumes stagnation of unit income

as a result of, among all, the prevailing low bulk prices of electrical energy and the absence

of additional supporting mechanisms, such as capacity markets or green certificates, and also maintaining

the present dividend policy in energy companies. The high option assumes constant increases in unit income

by 3% per annum (this corresponds to the forecasts presented in the draft 2050 Poland’s Energy Policy) and

increasing investments at the expense of dividends.

Coalapse – will fusion with the energy sector save Polish mining?

16

The impact of the consolidation on the capitalisation of energy companies is evaluated by comparing the net

present value of the investment in coal mining (calculated for a discount rate of r=7%) and their present

market value. This is how we estimate the impact that the fusion of the mining and energy sectors may have

on the assets of the shareholders of energy companies. It can be assumed that a part of this impact has

already been reflected in the valuation of energy companies, which has significantly dropped in 2015–2016,

among all under a wave of speculation regarding the prospects of the energy and mining sectors fusion. That

is why we present the impact of consolidation with the mining industry on energy companies’ capitalisation

in two variants: assuming valuations from March 2015 and March 2016. These can be treated as range of

values for the relative impact of the fusion on the stocks of energy companies.

2.4. Impact on consumers and taxpayers

Should the financial results of energy companies deteriorate as a result of consolidation with the mining

sector, there is a risk that some or all losses of the investors will be shifted to consumers or taxpayers. The

state, being at the same time a regulator and the co-owner of energy companies, may make attempts at

compensating for the costs of the failed restructuring of mines incurred by energy companies, motivating its

decisions, e.g., with the concern for the country’s energy security. For the purpose of this analysis, the cost

that meets this definition is the negative Net Present Value (NPV) of the investment, calculated for a discount

rate of 7%.

Diagram 3. Assessed possibilities of shifting the losses of the energy sector onto the citizens and

indicators of the potential support intensity

Support for the energy sector

Increase in coal

prices for

individuals

Additional fees for

electricity

Immediate

support from

the budget

PLN/tonne PLN/MWh PLN/household per

annum

Source: WiseEuropa research

Coalapse – will fusion with the energy sector save Polish mining?

17

We consider three possible options of shifting the losses of the integrated mining and energy concerns onto

the citizens. The first option is increasing the prices of coal for individuals, possibly through limiting the

import of coal from outside the European Union and competition on the domestic market. The second

option is to introduce additional fees in the prices of electrical energy by the regulator. The third option is to

provide support to the mining and energy companies directly from the budget. It is important to stress that

in all of the presented options, there is a major risk of breaching EU regulations on state aid and competition

protection. An attempt at introducing them would entail not only costs for the citizens but could also give

rise to a legal dispute with EU institutions.

Box 2. Key problems of the Polish hard coal mining industry

The crisis of the Polish hard coal mining industry results from a combination of supply-side and demand-side

factors, particularly the organisational and geological problems (as coal deposits are harder to reach), as well as

the slump on the global market for this commodity and the potential loss of significance in

the European and global energy mix. It is structural, not cyclical in nature, so restoring profitability to

the industry requires a deep restructuring, not only weathering the cyclical slump on the coal market.

Low mining productivity

The majority of Polish mines are several times less productive than mining companies successfully competing on

the global market. Extraction per employee is similar to the deeply unprofitable mines from Western Europe,

which are earmarked for liquidation. This results from organisational and technical issues as well as the absence of

investments in modernising coal extraction. What is more, the negative impact of the high labour intensity on the

profitability of Polish mining will only deteriorate with time. This results from the wage pressure, corresponding to

the gradual increase in salaries in the entire economy. The wealthier the country, the more productive mining

must be to help draw employees with appropriately high salaries while maintaining the profitability of operations.

The United States, having good geological conditions and boasting a very high extraction productivity, remain an

important coal producer (despite the current crisis and a series of bankruptcies of the local mining enterprises),

while coal mining in Western Europe has nearly disappeared.

Chart 1. Productivity in underground coal mines in Europe and the United States

USA 2012 –the worst 20%

USA 2012

United Kingdom 1981

United Kingdom 1991

United Kingdom 2012

Spain 2012

Germany 2012

France 1996–2000

Poland 2005–2012

Poland 2015

0 1000 2000 3000 4000 5000

extraction per employee (tonnes per year)

Source: Bukowski et al. (2015) and data of the Ministry of Economy

Coalapse – will fusion with the energy sector save Polish mining?

18

met

res

cont'd Box 2. Key problems of the Polish coal mining industry

Geological barriers – mining depth and coal quality

Despite the considerable coal deposits in Poland, its recoverable resources are much smaller. Given

the current production in Polish mines, their coal resources will quickly start depleting after 2020.

As the deposits are depleted, it will be necessary to mine coal at greater depths, even up to 1 km.

The average mining depth in Poland increases with time, reducing productivity and increasing costs.

Chart 2. Average mining depth in underground coal mines

0

250

500

750

1,000

1,250

Poland USA United Kingdom Germany

1989 2000 2011 2009 2009 2009

Source: Bukowski et al. (2015)

The quality of the extracted coal is also an issue. This particularly concerns the quality of fuel delivered to private

individuals. For example, the Polish Coal Retailers Chamber of Commerce estimates that only around 15% of the

commodity produced in Poland is of better quality than imported coal. Domestic coal contains much more total

sulphur than its Russian counterpart and also has more ash (Ney et al. 2004). This makes it more difficult to

compete on the market but also to limit import through quality regulations. At the same time, the rising

awareness of the high health costs associate with air pollution in Poland translates to falling social acceptance for

the usage of low-quality coal for heating.

Low prices of coal on the global market

Structural problems of the coal sector surfaced with the systematically falling coal prices on the global market.

They are presently at under 50$ per tonne. This puts pressure on the domestic market on which

a downward trend is visible. In accordance with the Industrial Development Agency data, the price of steam coal

sold to utility and industrial power plants in March 2016 was PLN 194 per tonne

(8.75 PLN/GJ), while it was 264 PLN per tonne three years ago (11.9 PLN/GJ). Global outlook assumes

no rebound of the coal prices any time soon, but instead permanent stagnation is considered possible

(see Chapter 5.1). This means that a boom on the domestic market of this commodity should not be expected as

well, and the only way to make mines profitable again is through cost reduction.

Coalapse – will fusion with the energy sector save Polish mining?

19

PLN

/GJ

Jan

'11

Jun

'11

No

v'1

1

Ap

r'12

Sep

'12

Feb

'13

Jul'1

3

Dec

'13

May

'14

Oct

'14

Mar

'15

Au

g'15

Jan

'16

mill

ion

to

nn

es

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

cont'd Box 2. Key problems of the Polish coal mining industry

Climate policy and energy sector transformation

In the long term, the main factor affecting the competitiveness of mining is the gradual tightening of

the climate policy coupled with the progressing transformation of the energy sector, not only on the domestic or

European but also global scale. Investments in low-emission energy sources and improving energy efficiency will

continue to limit the demand for coal. If the global demand for coal fails to increase dynamically, only the mines

with the lowest operating costs will manage to stay in the market. The Polish mines which will not be able to

radically improve mining productivity will remain permanently unprofitable.

Chart 3. Prices of Polish and Australian coal, 2011–2016

Chart 4. Hard coal production and consumption in Poland, 1990–2015

18 150

125 16

100

75

50

25

0

8 -25

— Polish Steam Coal Market Index

– sale to the energy sector

— Polish Steam Coal Market Index

– sale to the heat generation sector — Prices of Australian coal

n Domestic consumption

n Import

n Export — Domestic production

Source: own research based on Industrial Development Agency (ARP) and International Monetary Fund data

Source: own research based on Central Statistical Office (GUS) and Industrial Development Agency (ARP) data

Source: WiseEuropa research

14

12

10

Coalapse – will fusion with the energy sector save Polish mining?

20

extr

acti

on

per

em

plo

yee

(to

nn

es p

er y

ear)

in t

ho

usa

nd

s

3. Outlook for Polska Grupa Górnicza

3.1. Restructuring scenarios

The main parameter differentiating the four scenarios of how the Polska Grupa Górnicza (PGG) should

function in the future is employment dynamics. In the deep restructuring scenario we assume a nearly three-

fold drop in employment by 2018. It will primarily be a result of discontinuing extraction in certain mines,

where a permanent improvement in productivity is not possible. Afterwards it will continue to drop as a

result of the gradual increase in capital intensity of extraction in other locations, which entails a successive

improvement in labour productivity – it is expected to double by 2036. A similar, long-term upward trend in

productivity is also assumed in the April agreement and Initial business plan scenarios. However, in these

cases the scale of employment restructuring in the initial period is much lower, no mines are closed down

and the production remains high (28 million tonnes versus 15 million tonnes in the Deep restructuring

scenario). This comes at a price of much lower mining productivity and profitability. On the opposite end is

the No restructuring scenario, in which both coal extraction and employment are maintained

on a steady level, while labour productivity does not change.

Chart 5. Assumed improvement in mining productivity by PGG restructuring scenario

Chart 6. Employment by PGG restructuring

scenario

1500

1250

1000

750

500

250

718

1465

1262

718

40 39 39 39 36

35

30 30 30

26 26 25 20 15 13

12

10

5

22 22

10

0

2015 2018 2026 2036

0

2015 2018 2026 2036

• No restructuring

• April agreement

• Initial business plan

• Deep restructuring

n No restructuring

n April agreement

n Initial business plan

n Deep restructuring

Source: PGG business plan, WiseEuropa own calculations Source: WiseEuropa own calculations

Coalapse – will fusion with the energy sector save Polish mining?

21

In addition to the number of employees, the individual scenarios also differentiate between unit labour

costs. In the Deep restructuring and Initial business plan there is a one-off reduction in salaries in 2016–2017,

which will allow to better align remuneration and productivity. Additionally, assumed improvement in supply

management allows to bring down other units costs, mostly associated with outsourced services. The costs

of labour are also cut in the April agreement scenario, yet in this case the reduction in salaries has a

temporary character and only spans 2016–2017. This is a modification of the initial government plan to

restructure Kompania Węglowa, after negotiations with the trade unions: in accordance with the agreement

concluded in April 2016, salary cuts are only temporary and assume suspending the so-called fourteenth

salaries for two years.

Table 2. Cost assumptions by PGG restructuring scenario

Scenario

Labour cost in thousand PLN'15/employee

per year

Other costs (excluding depreciation),

PLN’15/tonne

2015

2018

2036

2015

2018

2036

No restructuring

81

81

142

110

110

169

April agreement

81

142

100

153

Initial business plan

70

123

100

153

Deep restructuring

70

123

100

153

Source: WiseEuropa, own calculations

In all scenarios, after 2018 both salaries and other costs of mining will gradually pick up, driven by the

rising pressure on company costs from the broader economic environment. This is valid both for mining as

well as all other sectors of the economy, none of which is isolated from the other ones. A gradual increase in

efficiency (the volume of coal extracted per employee) is therefore a necessary condition to offset the

external pressure on costs in the sector. In all of the scenarios, this will require investing in modernisation of

mining. We assume that the target volume of investments per tonne of coal will be significantly higher than

at Kompania Węglowa, reaching over PLN 50 per tonne a year, consistent with the PGG business plan as well

as the experience of private mining enterprises (Bogdanka). We assume that the initial PGG capital will

amount to PLN 2.9 billion and that the company will take over and will be servicing the debt of Kompania

Węglowa in the amount of PLN 3 billion.

Improving labour productivity at PGG will not be limited to improving technical efficiency

(coal extraction per employee) but will also cover economic productivity. The latter will be influenced by the

price of coal on the global markets, which in the baseline price scenario will be gradually increasing as a

result of foreign companies limiting their production, adjusting supply to the global demand for coal.

However, the increase is relatively low, keeping the unit price in the entire assessed period near the multi-

decade average. This statement is of key significance for PGG’s ratio between income and costs, and thus for

its profitability in the medium term, as well as for the impact that the Group’s operations might have on

energy companies with equity interest in it.

Coalapse – will fusion with the energy sector save Polish mining?

22

PLN

'15/

ton

ne

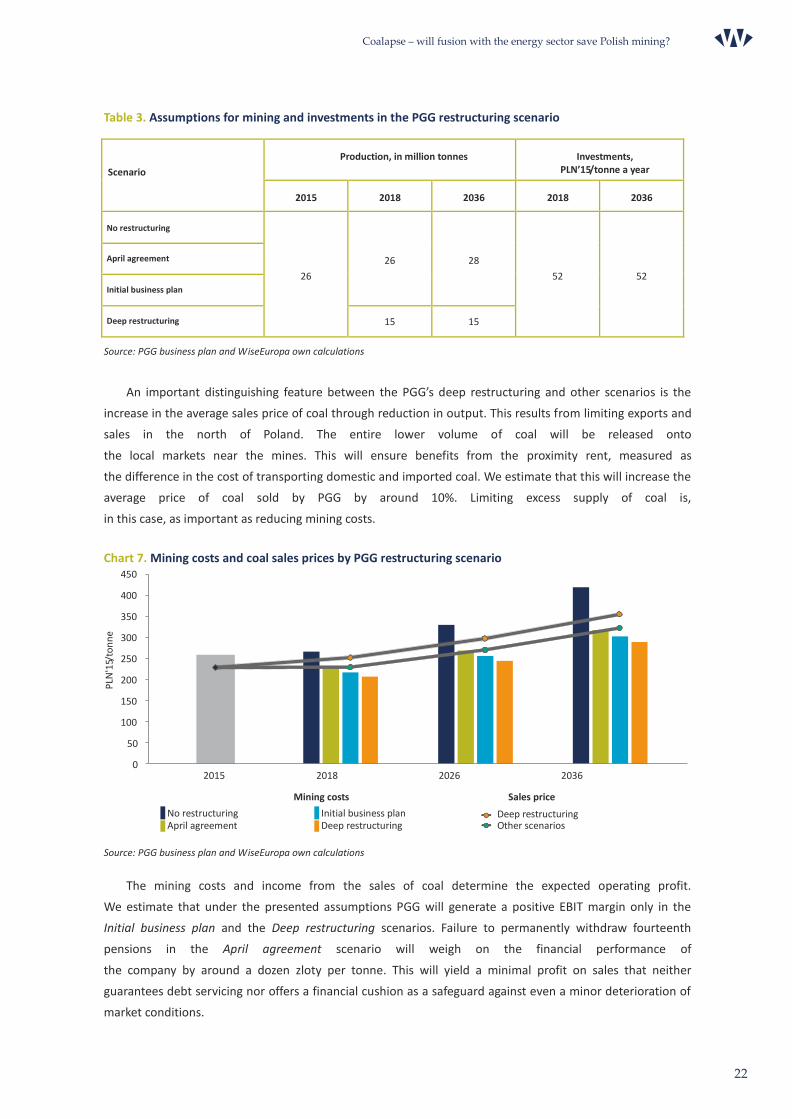

Table 3. Assumptions for mining and investments in the PGG restructuring scenario

Scenario

Production, in million tonnes

Investments, PLN’15/tonne a year

2015

2018

2036

2018

2036

No restructuring

26

26

28

52

52

April agreement

Initial business plan

Deep restructuring

15

15

Source: PGG business plan and WiseEuropa own calculations

An important distinguishing feature between the PGG’s deep restructuring and other scenarios is the

increase in the average sales price of coal through reduction in output. This results from limiting exports and

sales in the north of Poland. The entire lower volume of coal will be released onto

the local markets near the mines. This will ensure benefits from the proximity rent, measured as

the difference in the cost of transporting domestic and imported coal. We estimate that this will increase the

average price of coal sold by PGG by around 10%. Limiting excess supply of coal is,

in this case, as important as reducing mining costs.

Chart 7. Mining costs and coal sales prices by PGG restructuring scenario

450

400

350

300

250

200

150

100

50

0

2015 2018 2026 2036

Mining costs

Sales price

n No restructuring n Initial business plan • Deep restructuring n April agreement n Deep restructuring

—l

Other scenarios

Source: PGG business plan and WiseEuropa own calculations

The mining costs and income from the sales of coal determine the expected operating profit.

We estimate that under the presented assumptions PGG will generate a positive EBIT margin only in the

Initial business plan and the Deep restructuring scenarios. Failure to permanently withdraw fourteenth

pensions in the April agreement scenario will weigh on the financial performance of

the company by around a dozen zloty per tonne. This will yield a minimal profit on sales that neither

guarantees debt servicing nor offers a financial cushion as a safeguard against even a minor deterioration of

market conditions.

Coalapse – will fusion with the energy sector save Polish mining?

23

2015

2018

2026

2036

Deep restructuring

-30

45

53

66

Initial business plan

12

14

20

April agreement

1

1

5

No restructuring

-37

-59

-97

In the event of no restructuring, PGG’s operating loss will increase from around 13% of income

to 30% in two decades. Zero or negative EBIT will require the company to receive permanent capital

injections from its owners or the company will be liquidated in a few years (or a few months,

in the absence of restructuring) due to depleting equity. In subsequent parts of the analysis we assume that

PGG shareholders will be systematically filling the potential financial gaps from their own profits. This

illustrates the case in which operating problems of today’s Kompania Węglowa are shifted to the companies

investing in PGG and how they are potentially multiplied as a result of market processes (beyond the

company’s control).

Table 4. EBIT per tonne of coal by PGG restructuring scenario

Chart 8. EBIT to sales ratio by PGG restructuring scenario

30%

20%

10%

18% 18% 19%

5% 5% 6%

0%

-10%

-20%

-30%

-13%

0% 0% 1%

-16%

-22%

-40%

-30%

2015 2018 2026 2036

— No restructuring

—l April agreement

—l Initial business plan —l Deep restructuring

Source: WiseEuropa, own calculations

On the opposite extreme is the Deep restructuring scenario, which, given the assumed market conditions

(increasing coal prices), will involve quick labour productivity improvement and a permanently positive

extraction profitability. This will be a result of focusing on the best deposits, reducing output and

employment as well as mechanising production. Companies investing in PGG restructured in such a way can

expect a high rate of return from the risk taken, given moderately positive price developments on the global

market. A prolonged downturn on the commodities market is a risk factor and, as we show in Chapter 5, it is

of key significance for the economic viability of the investment in coal mining in Poland after 2025, even

following a deep restructuring in the sector.

The Initial business plan scenario, which mirrors the government’s publicly voiced initial expectations of PGG,

allows to generate a positive operating result in 2017. The necessity to finance the investment and to service

debt makes the economic viability of the undertaking doubtful in the long term. The proposal offered a

positive net present value (NPV) to the investors only at very low discount rates (under 3%), which can be

considered acceptable from the social perspective but not from the investor’s point of view: as opposed to

bank deposits that offer a similar yield, this investment involves substantial risk.

Coalapse – will fusion with the energy sector save Polish mining?

24

NP

V, in

bill

ion

PLN

'15

b

illio

n P

LN'1

5

20

16

2

01

7

20

18

2

01

9

20

20

2

02

1

20

22

2

02

3

20

24

2

02

5

20

26

2

02

7

20

28

2

02

9

20

30

2

03

1

20

32

2

03

3

20

34

2

03

5

20

36

bill

ion

PLN

'15

N

PV,

in b

illio

n P

LN'1

5

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

20

28

20

29

20

30

20

31

20

32

20

33

20

34

20

35

20

36

What is more, a small scale of restructuring ultimately accepted in the April agreement scenario means that

energy company shareholders can expect the net present value of the investment in PGG to be negative

irrespective of the assumed discount rate. In Chapter 5 we show that this result will worsen if the downturn

on the global coal market proves permanent.

Chart 9. Cash flows from the investors’ perspective by PGG restructuring scenario

0.0

-0.5

-1.0

-1.5

-2.0

-2.5

-3.0

-3.5

n No restructuring

n April agreement

n Initial business plan

n Deep restructuring

Source: WiseEuropa, own calculations

Chart 10. Net present value of the investment in PGG from the investors’ perspective by restructuring

scenario

0

-10

-20

Discount rate

0% 5% 7% 9%

-

-13

-17

Discount rate

0% 5% 7% 9%

10 9.2

8

6

4 3.3

-30

-40

-50

-24 2.2 2

0

-2 -4

2.1

1.2

Source: WiseEuropa, own calculations

-42

-5 -4 -3 -3

-0,6 -1,5 -1,1

Coalapse – will fusion with the energy sector save Polish mining?

25

In P

LN b

ilio

n

in P

LN b

illio

n

3.2. PGG’s impact on energy companies

To analyse the economic impact of investing in PGG for the major energy companies involved (PGE and

Energa), we assume that their share in the profits of the new entity or participation in loss coverage will be

proportionate to the initial contribution, namely PLN 500 million each. In the case of scenarios that assume

no or limited restructuring of the mines, PGG’s equity of PLN 2.9 billion (PLN 500 million of initial

contribution from Węglokoks and a PLN 2.4 billion capital injection by PGE, Energa, PGNiG Termika,

Węglokoks, TF Silesia and Fundusz Inwestycji Polskich Przedsiebiorstw) will not suffice to ensure sustained

operation. This means that it will be necessary to either continue subsiding PGG by energy companies or to

withdraw from maintaining all mines (or most of them) in the near future (deeper restructuring than

assumed in PGG’s business plan or the April agreement scenario). In this chapter we consider the outcome of

the first variant, namely permanently burdening the energy companies with maintaining coal extraction and

employment in PGG. In the second variant (no support from the energy sector), PGG will go bankrupt in

2023 if the April agreement is implemented, or in 2017 if not restructuring is carried out at all.

Chart 11. Estimated investment capacity of PGE and Energa in 2016–2036 by PGG restructuring scenario and developments on the energy market

200

180

120

160

140

100

80

60

40

20

0

PGE

Low variant High variant

PGE investment capacity in 2016–2036

Energa 50

45

40

35

30

25

20

15

10

5

0 Low variant High variant

Energa’s investment capacity 2016–2036

n n No investments in PGG — No restructuring — April agreement — Initial business plan — Deep restructuring

Source: WiseEuropa, own calculations

We estimate that investing in PGG without any restructuring initiatives being introduced would lower the

investment capacity of both PGE and Energa by around PLN 12 billion. Relative burden for each entity would

be different in view of the different scale of operations. PGE’s investment capacity for 2016–2036 without

involvement in the mining sector is estimated at around PLN 110 billion in the low variant (stagnation of the

company’s income, limited restructuring of costs and maintaining the current dividend policy), and PLN 180

billion in the high variant (increase in income by about 3% p.a., e.g. as a result of a capacity market

introduction, restructuring the costs of producing and distributing energy, increasing investments at the

expense of the dividend).

Coalapse – will fusion with the energy sector save Polish mining?

26

Ch

ange

in P

GE'

s in

vest

men

t ca

pac

ity

Ch

ange

in E

ner

ga's

inve

stm

ent

cap

acit

y

Analogous assumptions for Energa yield an investment capacity of PLN 31–43 billion by 2036. Therefore,

permanently absorbing some of the losses of unrestructured PGG would reduce PGE’s investment capacity

by 7–11% by 2036 and even up to 28%–39% in the case of Energa.

In the more optimistic scenario, the April agreement, PGG would be a lesser burden for the investors. We

estimate that investment capacity of both companies in this case would drop by around

PLN 1.4 billion (1% of the total capacity of PGE and 3–5% of Energa). The Initial business plan would be close

to neutral for both companies, but this result is subject to considerable risk: even if market conditions

deteriorate only slightly, the drop in investment capacity of both entities would be noticeable. Only Deep

restructuring, which assumes focusing on PGG assets that offer good prospects, allows both PGE and Energa

to achieve a positive return on capital and enables a slight increase in their own investment capacity by PLN

0.7 billion in a 2036 perspective. At the same time, this scenario leaves a relatively high safety margin,

reassuring investors from the energy sector that involvement in mining, provided a deep restructuring is

carried out, will not become a completely failed investment, even if coal prices do not rebound in the long

term (see Chapter 5.2).

Chart 12. Estimated impact of PGG on the investment capacity of PGE and Energa in 2016-2036 by restructuring scenario and developments on the energy market

PGE 2%

Energa

-2%

-4%

-6%

-8%

-10%

-12%

-1

-5%

-10%

-15%

-20%

-25%

-30%

-35%

-40%

-45%

-39%

-5%

-1% -28%

-1%

Low variant High variant Low variant High variant

n No restructuring n April agreement n Initial business plan n Deep restructuring

Source: WiseEuropa, own calculations

Greater impact of the assessed investment on Energa than on PGE results from the fact that both energy

companies contribute equally to recapitalisation of Polska Grupa Górnicza, despite the fact that PGE is

several times larger than Energa, has more profitable assets and generates better financial results. It is

interesting to note that the relatively good financial standing of PGE compared to the rest of the sector

entails greater investment capacity, which is why investing in PGG is much less risky for this company than for

Energa. PGE’s investment capacity would be considerably reduced only if no restructuring initiatives were to

be undertaken at PGG. Comparing the historical and current capitalisation of both energy companies with

the net present value (NPV) of the investment in PGG offers the same conclusion.

-11%

-1% -0,3%

0,6%

-7%

-1%

2%

-0,2% 0,4% 2%

-5% 0%

0%

5%

Coalapse – will fusion with the energy sector save Polish mining?

27

Ch

ange

in P

GE'

s ca

pit

alis

atio

n

Cap

ital

isat

ion

of

PG

E

Ch

ange

in E

ner

ga's

cap

ital

isat

ion

N

PV

of

the

inve

stm

ent

in P

GG

Ener

ga's

cap

ital

isat

ion

NP

V o

f th

e in

vest

men

t in

P

GG

Chart 13. Present capitalisation of PGE and Energa and net present value of the investment in PGG by restructuring scenario

PGE

Energa

March 2015 March 2015

March 2016

Deep

restructuring

Initial business

plan

April

agreement

No

restructuring

March 2016

Deep

restructuring

Initial business

plan

April

agreement

No restructuring

-0,2

-0,7

5

0,3

-10 0 10 20 30 40 PLN

billion

Source: WiseEuropa, own calculations

-8 -6 -4 -2 0 2 4 6 8 10 PLN

billion

One is led to believe that the significantly milder decrease in price of PGE stocks over the past 12 months

compared to Energa’s valuation reflects to some extent the fact that investors are less concerned that

permanent involment in PGG, even in the worst-case scenario, may threaten the existence of the enterprise.

In the case of Energa, the costs of permanently supporting ineffective mining operations at PGG would

exceed the present market value of the company. That is why introducing restructuring measures at PGG

is particularly important from Energa shareholders’ point of view. They should take into account that PGG

restructuring may fail and that continuing extraction at the expense of its owners would be very risky

for them, as the possible loss ranges between 65% and 100% of the company value. Keeping the mine

in the April agreement scenario is, from their perspective, problematic, exposing Energa shareholders to the

risk of losing 7–13% of the value of the company. In the Initial business plan scenario (one-off capital

injection in a fairly successful PGG restructuring), Energa’s market cap may drop by 2–4%. Yet, initiating

the process of deep restructuring at PGG mines may increase Energa’s value by even 4–6%.

Chart 14. Estimated impact of PGG on the market capitalisation of PGE and Energa in 2016-2036 by

restructuring scenario 5%

0%

-5%

-3%/-2%

+1%

20%

0%

-4%/-2%

+4%/+6%

-10%

-15%

-20%

-25%

-24%

/-17%

-40%

-60%

-100% /-65%

No restructuring

April

agreement

Initial business plan

Deep restructuring

No

restructuring

April agreement

Initial business plan

Deep restructuring

Source: WiseEuropa, own calculations

-1%

-13%/-7%

-80%

-100%

-20%

-30%

36

25

0,3

-0,2

-0,7

-6 -6

9

Coalapse – will fusion with the energy sector save Polish mining?

28

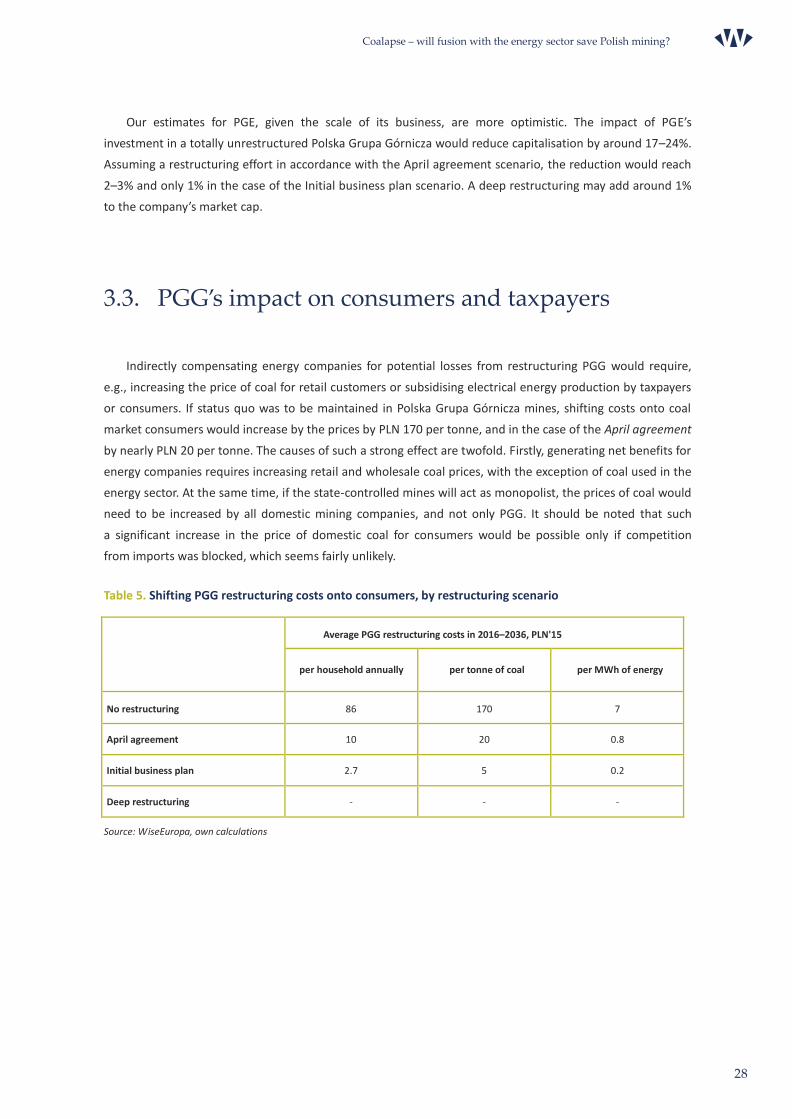

Our estimates for PGE, given the scale of its business, are more optimistic. The impact of PGE’s

investment in a totally unrestructured Polska Grupa Górnicza would reduce capitalisation by around 17–24%.

Assuming a restructuring effort in accordance with the April agreement scenario, the reduction would reach

2–3% and only 1% in the case of the Initial business plan scenario. A deep restructuring may add around 1%

to the company’s market cap.

3.3. PGG’s impact on consumers and taxpayers

Indirectly compensating energy companies for potential losses from restructuring PGG would require,

e.g., increasing the price of coal for retail customers or subsidising electrical energy production by taxpayers

or consumers. If status quo was to be maintained in Polska Grupa Górnicza mines, shifting costs onto coal

market consumers would increase by the prices by PLN 170 per tonne, and in the case of the April agreement

by nearly PLN 20 per tonne. The causes of such a strong effect are twofold. Firstly, generating net benefits for

energy companies requires increasing retail and wholesale coal prices, with the exception of coal used in the

energy sector. At the same time, if the state-controlled mines will act as monopolist, the prices of coal would

need to be increased by all domestic mining companies, and not only PGG. It should be noted that such

a significant increase in the price of domestic coal for consumers would be possible only if competition

from imports was blocked, which seems fairly unlikely.

Table 5. Shifting PGG restructuring costs onto consumers, by restructuring scenario

Average PGG restructuring costs in 2016–2036, PLN'15

per household annually

per tonne of coal

per MWh of energy

No restructuring

86

170

7

April agreement

10

20

0.8

Initial business plan

2.7

5

0.2

Deep restructuring

-

-

-

Source: WiseEuropa, own calculations

Coalapse – will fusion with the energy sector save Polish mining?

29

It is a slightly more probable scenario, albeit still difficult to implement, to subsidise energy companies

indirectly by increasing the price of energy. We estimate that if support measures financed from electricity

bills were introduced for energy companies investing in PGG, the prices of electricity would rise by PLN 0.2–

7.0 per MWh, depending on the restructuring scenario. The option assuming support for energy companies

directly from the budget would increase its expenses by PLN 86 per household in the worst-case scenario.

It is important to stress that the presented estimates assume compensation only for PGE and Energa.

Compensating for the losses of all shareholders involved in PGG could consume nearly

PLN 140 annually per household, if no restructuring initiatives are taken.

Box 3. Financial viability of investments of energy companies in coal mines

In the public debate on restructuring the mining industry, the success criterion is often assumed to be driving

down the mining costs below the sales price of coal (obtaining a positive EBIT). However, from

the owner’s perspective, this does not mean generating a satisfactory return on the investment. A mining

enterprise not only bears the costs associated with its operating activity (extraction and sale of coal) but also

financial costs associated with commitments from previous years and new investment loans, taken on account of

restructuring. A sufficiently high rate of return needs to be obtained by the owner as well. Private investors

compare the return on capital employed against alternative investments (e.g. investments in competitive mining

enterprises, other sectors of the economy or other asset classes). When the state is the owner, it may accept a

lower rate of return in view of non-economic factors (e.g. intention to maintain status quo on the labour market in

the region or exercise direct control over primary energy sources). In the case of state-owned energy companies,

accepting a low rate of return is problematic for two main reasons:

• State Treasury is not the only owner of energy companies – they are listed on the stock exchange, so a

vast portion of their shares is held by private entities, including individual investors.

• EU regulations prohibit subsiding hard coal mining (see Box 4), which also includes companies controlled

by the State Treasury becoming involved in investments that are unattractive

for private investors.

Accepting a low, “social” rate of return by energy companies is not in the interest of energy company shareholders

and may be considered unlawful state aid by the European Commission. This means that not only the April

agreement, which yields losses, but also the profitable Initial business plan may be treated as unviable in

economic terms. What is more, investors do not base their decisions on one scenario of developments in the

industry but rather consider the opportunities and threats that any investment project needs to address. In the

case of mining, this means that it is necessary to take into account the real threat of a long-term stagnation of coal

prices (see Chapter 5), the risks of technical problems or rejection of labour cost cutting initiatives by trade unions.

Coalapse – will fusion with the energy sector save Polish mining?

30

bill

ion

PLN

'15

20

16

2

01

7

20

18

2

01

9

20

20

2

02

1

20

22

2

02

3

20

24

2

02

5

20

26

2

02

7

20

28

2

02

9

20

30

2

03

1

20

32

2

03

3

20

34

2

03

5

20

36

bill

ion

PLN

'15

20

16

20

17

2

01

8

20

19

2

02

0

20

21

2

02

2

20

23

2

02

4

20

25

2

02

6

20

27

2

02

8

20

29

2

03

0

20

31

2

03

2

20

33

2

03

4

20

35

2

03

6

cont'd Box 3. Financial viability of investments of energy companies in coal mines

Chart 15. PGG’s equity in various restructuring scenarios Baseline coal price scenario

14

12

Stagnation of coal prices 6

5

10

4

8

3

6

2 4

2 1

r=0%

0 0

— No restructuring — April agreement — Initial business plan — Deep restructuring

Source: WiseEuropa, own calculations; detailed description of the coal price stagnation scenario is presented in Chapter 5

In the light of these factors, only Deep restructuring of PGG and its assets is an opportunity for success of this

project, even in unfavourable market conditions. According to our calculations, given the baseline coal prices

scenario and implementation of the Deep restructuring scenario, the project would ensure a market rate of return

to the investors, and in a pessimistic scenario it would give then the necessary time to decide on deeper

adjustments. Less ambitious restructuring initiatives involve a high risk of not only generating low rates of return,

but also making the company insolvent within 2 to 7 years.

Source: WiseEuropa, own calculations

r=3%

r=7%

r=0%

r=3%

Coalapse – will fusion with the energy sector save Polish mining?

31

extr

acti

on

per

em

plo

yee

(to

nn

es p

er y

ear)

in t

ho

usa

nd

s

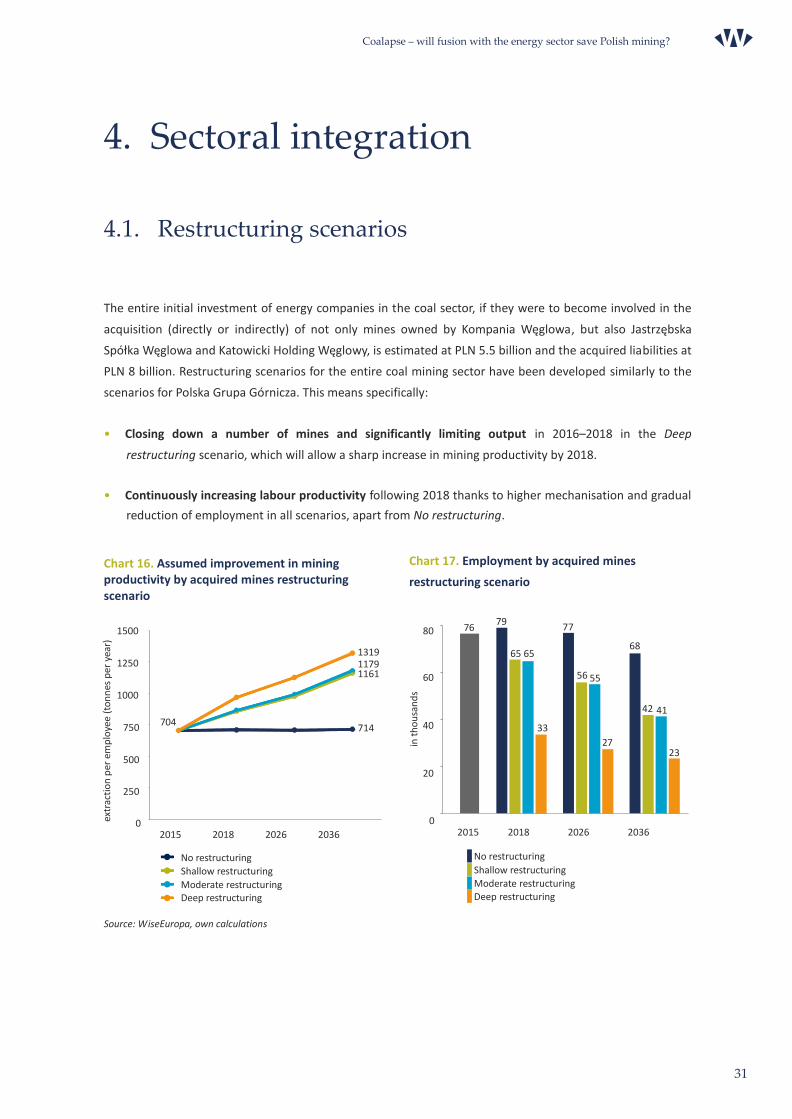

4. Sectoral integration

4.1. Restructuring scenarios

The entire initial investment of energy companies in the coal sector, if they were to become involved in the

acquisition (directly or indirectly) of not only mines owned by Kompania Węglowa, but also Jastrzębska

Spółka Węglowa and Katowicki Holding Węglowy, is estimated at PLN 5.5 billion and the acquired liabilities at

PLN 8 billion. Restructuring scenarios for the entire coal mining sector have been developed similarly to the

scenarios for Polska Grupa Górnicza. This means specifically:

• Closing down a number of mines and significantly limiting output in 2016–2018 in the Deep

restructuring scenario, which will allow a sharp increase in mining productivity by 2018.

• Continuously increasing labour productivity following 2018 thanks to higher mechanisation and gradual

reduction of employment in all scenarios, apart from No restructuring.

Chart 16. Assumed improvement in mining productivity by acquired mines restructuring scenario

Chart 17. Employment by acquired mines

restructuring scenario

1500

1250

1000

750

500

250

704

1319 1179 1161 714

80

60

40

20

65 65

33

0 2015 2018 2026 2036

0 2015 2018 2026 2036

—l No restructuring

—l Shallow restructuring

—l Moderate restructuring —l Deep restructuring

n No restructuring

n Shallow restructuring

n Moderate restructuring n Deep restructuring

Source: WiseEuropa, own calculations

76 79

77

56 55

27

68

42 41

23

Coalapse – will fusion with the energy sector save Polish mining?

32

Table 6. Cost assumptions by acquired mines restructuring scenario

Scenario

Labour costs, in thousand PLN’15/employee per year

Other costs (excluding depreciation),

PLN’15/tonne

2015

2018

2036

2015

2018

2036

No restructuring

84

88

152

113

113

174

Shallow restructuring

88

152

104

159

Moderate restructuring

79

136

104

159

Deep restructuring

76

135

105

160

Source: WiseEuropa, own calculations

We also assume that in the Moderate and Deep restructuring scenarios, in 2016–2018 remuneration will

be aligned with actual productivity in the sector by limiting other benefits paid to the miners.

Thereafter, the gradual increase in real salaries in the industry will follow the wage pressure from other

sectors of the economy, making it necessary to adequately increase productivity in the mining sector.

As in the case of PGG, it will be crucial to increase the scale of investment up to around PLN 55 per tonne

and introduce organisational changes to improve labour productivity. Major investments in the machines will

result in the growing mechanisation of production and a gradual reduction of employment in this sector.

Without these measures, assuming fixed mining output, achieving productivity levels that ensure increasing

real salaries would not be possible.

Table 7. Assumptions for mining and investments by acquired mines restructuring scenario

Scenario

Output, in million tonnes

Investments, PLN’15/tonne a year

2015

2018

2036

2018

2036

No restructuring

54

56

49

56

55

Shallow restructuring

Moderate restructuring

Deep restructuring

32

31

55

56

Source: WiseEuropa, own calculations

According to our calculations, if energy companies were to acquire the entire state-controlled hard coal

mining sector, they would need to accept that extraction profitability is only achievable in Moderate and

Deep restructuring scenarios. At the same time, only in the second case would it reach a level typical

for commercial entities operating in the sector. Our calculations indicate that chances for energy companies

to obtain a high operating margin (EBIT) through their involvement in restructuring coal mining are very slim.

Coalapse – will fusion with the energy sector save Polish mining?

33

2015

2018

2026

2036

Deep restructuring

-28

49

64

79

Moderate restructuring

10

19

26

Shallow restructuring

-1

6

10

No restructuring

-29

-46

-83

PLN

’15/

ton

ne

In the baseline coal price scenario, a positive EBIT may be expected in all variants that assume

a more or less far-reaching cost restructuring at the level of individual mines, yet only in the Deep

restructuring scenario the margin is a two-digit one and reaches the level expected by the investors and

lenders (see Box 3).

Chart 18. Mining costs and coal sales prices by acquired mines restructuring scenario 500

450

400

350

300

250

200

150

100

50

0

2015 2018 2026 2036

Mining costs

Sales price

n No restructuring n Moderate restructuring —l Deep restructuring