M&A UPDATE - KPMG Institutes · M&A Update Devon Bodoh, KPMG LLP Aaron Feinberg, General Motors...

45

M&A Update Devon Bodoh, KPMG LLP Aaron Feinberg, General Motors January 14, 2016 Detroit, MI

Transcript of M&A UPDATE - KPMG Institutes · M&A Update Devon Bodoh, KPMG LLP Aaron Feinberg, General Motors...

M&A Update

Devon Bodoh, KPMG LLPAaron Feinberg, General Motors

January 14, 2016Detroit, MI

© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

2

Agenda

Interesting Market Transactions and Developments

New Section 367 and Section 482 Guidance

New F Reorganization Regulations

Inversions – Notices and Regulations

Interesting Market Transactions and Developments

4© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Interesting Market Transactions and Developments

Merger of Equals with Planned Dispositions

Inversions

Shareholder Level Taxation

Continuing Viability

Spin-offs

Leveraged Spin-offs

Taxable Spin-offs

Elimination of REIT Spin-offs

Small Active Trade or Businesses

IRS Ruling Practice

New Section 367 and Section 482 Guidance

6© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

New Treasury Regulations Under Section 367 and 482Overview

In September 2015, the Treasury Department (“Treasury”) released new guidance with respect to the application of Section 367 and Section 482:

• Proposed Regulations (1) eliminating the foreign goodwill exception in the context of recognition of gain upon outbound transfers of intangibles and (2) limiting the scope of property that is eligible for the active trade or business exception. REG-139483-13.

• Temporary Regulations that clarify the application of the arm's-length standard and the best method rule under section 482 with other tax code provisions. T.D. 9738.

• Final Regulations relating to the treatment of “outbound F reorganization”, i.e., a transaction where a corporation changes from a U.S. to a non-U.S. corporation. T.D. 9739.

Section 367

8© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

New Treasury Regulations Under Section 367 and 482Current Law – Outbound Property Transfers

Section 367(a)

• Section 367(a) generally requires gain recognition where a U.S. person transfers built-in gain property to a foreign corporation in a transaction that otherwise qualifies for tax-free treatment.

• There are a number of exceptions to this rule. In particular, Section 367(a) does not apply where the property is transferred for use by the foreign corporation in the active conduct of a trade or business outside the U.S. (the “ATB Exception”). Section 367(a)(3).

• The ATB Exception is only applicable to transfers of certain types of property.

• In that regard, the statute lists specific categories of assets to which the ATB Exception does not apply. Section 367(a)(3)(B).

• Included among those assets is intangible property with the meaning of section 936(h)(3)(B) (which does not specifically mention goodwill or going concern value).

9© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

New Treasury Regulations Under Section 367 and 482Current Law – Outbound Transfers of IP

Section 367(d)• Section 367(d) includes a specific rule for the outbound transfer of intellectual property

(within the meaning of Section 936(h)(3)(B)) in an otherwise tax free transfer.• Intended to address abuses whereby a U.S. company incurred deductions relating to research

and experimentation expenses associated with the development of IP but transferred at the point of profitability.

• If Section 367(d) applies, the transferor is deemed to receive royalty payments (that are commensurate with income) over the useful life of the property (generally capped at 20 years under current law).

• Note that Section 367(d) specifically states that if Section 367(d) applied, then Section 367(a) does not apply. Section 367(d)(1)(A),(B).

• Legislative history states that the transfer of foreign goodwill or going concern value developed by a foreign branch to a foreign corporation was unlikely to result in an abuse of the U.S. tax system. See S. Rep. No. 169, 98th Cong., 2d Sess., at 362; H.R. Rep. No. 432, 98th Cong., 2d Sess., at 1317.

• This position is reflected in Temporary Regulations in place prior to September 2015 which explicitly remove foreign goodwill from the deemed royalty regime of section 367(d). Treas. Reg. Section 1.367-1T(d)(5)(iii).

• “Foreign goodwill or going concern value” is defined as the residual value of a business operation conducted outside the U.S. after all other tangible and intangible assets have been identified and valued. Treas. Reg. § 1.367(a)-1T(d)(5)(iii).

10© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

New Treasury Regulations Under Section 367 and 482Current Law - Issues with Respect to Foreign Goodwill and Going Concern

• In order to avoid or minimize tax on the outbound transfer of a business (that includes foreign goodwill and going concern), taxpayers have generally been taking a number of positions:

(1) Goodwill and going concern are not included in the definition of intellectual property under Section 936(h)(3)(B) does not include a specific reference to goodwill and going concern. As a result,

(i) goodwill and going concern are not subject to Section 367(d), and

(i) goodwill and going concern are not included in the categories of property to which the ATB Exception is inapplicable (i.e., the ATB Exception may apply) and therefore, an outbound transfer of goodwill and going concern may occur tax-free, nonwithstanding Section 367(a).

(2) Goodwill and going concern are included in the definition of intellectual property for Section 367(d) purposes but Section 367(d) specifically does not apply to foreign goodwill and going concern. In addition, Section 367(a) does not apply to the outbound transfer of foreign goodwill either because

(i) Section 367(d)(1)(A) implicitly provides that Section 367(d) is the sole provision governing outbound transfers of all IP (including goodwill and going concern) or

(i) Section 367(a) applies but the transfer is subject to the ATB Exception

11© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

New Treasury Regulations Under Section 367 and 482New Proposed Regulations – Reasons for the Rule

• For the foregoing reasons, taxpayers were incentivized to (i) attempt to shift value to foreign goodwill or going concern value in a manner contrary to section 482, and/or (ii) broadly interpret foreign goodwill and going concern value to include goodwill or going concern value that may be attributable to activities in the U.S.

• As a result of these concerns, Treasury adopted proposed regulations relating to the outbound transfer of foreign goodwill and going concern in September 2015.

• The preamble states “the Treasury Department and the IRS have determined that allowing intangible property to be transferred outbound in a tax-free manner is inconsistent with the policies of section 367 and sound tax administration.”

• These proposed regulations generally apply to transaction occurring on or after September 14, 2015 and are intended to cause foreign goodwill or going concern value to be taxed under section 367(a) or section 367(d), thus limiting incentives to shift value to or broadly interpret foreign goodwill or going concern value

12© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

New Treasury Regulations Under Section 367 and 482New Proposed Regulations – Changes to Current LawThe proposed regulations

• Remove the provision from the temporary regulations which had made a specific exception to the application of Section 367(d) for the outbound transfer of foreign goodwill and going concern value.

• Note that the proposed regulations do not address whether goodwill and going concern are Section 936(h)(3)(B) intangibles.

• Narrow the ATB Exception by providing an exclusive list of property that is eligible for the ATB Exception (rather than listing property that is not eligible for the ATB Exception) (discussed further below).

• Defining “useful life” to mean the period during which the exploitation of the property is reasonably anticipated to occur and removing the 20 year cap on useful life;

• Provide taxpayers with an election to apply section 367(d) rather than section 367(a) to certain transfers of property that would otherwise be subject to Section 367(a) (discussed further below); and

• Explicitly require value to be determined in accordance with section 482 in the case of a “controlled transaction” within the meaning of Treas. Reg. § 1.482-1(i)(8).

13© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

• Under the proposed regulations, the modified ATB Exception only applies to “eligible property” that is transferred to a foreign corporation for use in the active conduct of a trade or business outside the U.S. Prop. Reg. § 1.367(a)-2(a)(2).

• “Eligible property” means (i) tangible property, (ii) a working interest in oil and gas property, and (iii) a financial asset. Prop. Reg. § 1.367(a)-2(b)(3).

• A financial asset include (i) a cash equivalent, (ii) a security within the meaning of section 475(c)(2) (without certain modifications), (iii) a commodities position within the meaning of section 475(e)(2)(B), (e)(2)(C), or (e)(2)(D), or (iv) a notional principal contract within the meaning of Treas. Reg. § 1.446-3(c)(1). Prop. Reg. §1.367(a)-2(b)(3).

• Further, the following types of property are specifically excluded from the definition of eligible property: (i) inventory, (ii) installment obligations, (iii) foreign currency or certain foreign currency-denominated property, and (iv) certain leased tangible property. Prop. Reg. § 1.367(a)-2(c).

• The exception for certain foreign currency-denominated property in Treas. Reg. §1.367(a)-5T(d)(2) has also been removed.

New Treasury Regulations Under Section 367 and 482New Proposed Regulations – Changes to ATB Exception

14© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

• The net effect of the modified ATB Exception is to exclude intangible property from qualifying for the ATB Exception without regard to the taxpayer’s position with respect to the treatment of certain intellectual property under Section 963(h)(3)(B).

• This eliminates the incentive for taxpayers to undervalue intellectual property that would otherwise be taxed under Section 367(d).

New Treasury Regulations Under Section 367 and 482New Proposed Regulations – Changes to ATB Exception (cont.)

15© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

New Treasury Regulations Under Section 367 and 482New Proposed Regulations – Electivity of Section 367(d)

• As discussed above, if a taxpayer takes the position that goodwill and going concern value are not intangible property within the meaning of section 936(h)(3)(B), then section 367(a), and not section 367(d), will apply to cause the transferor to recognize gain under the proposed regulations.

• However, the proposed regulations provide the taxpayer with the choice to apply the provisions of section 367(d) (instead of section 367(a)) to the outbound transfer of goodwill and going concern value.

• Note that the proposed regulations do not speak one way or another to the issue of whether goodwill and going concern are intangible property within the meaning of Section 936(h)(3)(B).

• Instead, intangible property is defined either as that described in Section 936(h)(3)(B) or property to which a taxpayer specifically applies Section 367(d) (rather than Section 367(a)).

Section 482

17© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

New Treasury Regulations Under Section 367 and 482New Proposed Regulations – Coordination of Section 367 and Section 482

• As noted, one of the goals of the proposed regulations is to remove the incentives to shift value to foreign goodwill and going concern value.

• The preamble to the proposed regulations notes that the Treasury Department is aware that taxpayers value property in a manner contrary to section 482 in order to minimize the value of property that is subject to section 367(d) under the current regulations.

• Specifically, the preamble says that taxpayers (i) use valuation methods that value items of intangible property on an item-by-item basis, where valuing the items on an aggregate basis would provide a more reliable result under the arm’s length standard, or (ii) do not properly perform a factual and functional analysis of the business in which the intangible property is employed.

• Under the current regulations, the amount of gain to be recognized under Section 367(a) was limited to the gain that would have been recognized on a taxable sale of those items of property if sold individually and without offsetting individual losses against individual gains.

• The preamble to the proposed regulations notes that this language has been removed because it may cause taxpayers to interpret the provision as inconsistent with the new temporary regulations under section 482 (discussed below).

• Instead, Prop. Reg. § 1.367(a)-1(b)(3) now provides that in the case of any controlled transaction (as defined in Treas. Reg. § 1.482-1(i)(8)), the value of the property transferred must be determined in accordance with section 482 and the regulations thereunder.

18© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

New Treasury Regulations Under Section 367 and 482New Proposed Regulations – Coordination of Section 367 and Section 482 (Cont.)

• Temporary regulations under section 482 address coordination of section 482 with other provisions of the Code. Specifically, the temporary regulations address coordination of section 482 and section 367.

• The preamble to the temporary regulations states that, to achieve the purposes of section 367 and section 482, controlled transactions require a consistent and coordinated application of section 367 and section 482.

• The preamble notes that taxpayers may not take into account all of the synergies and interrelated value of economically integrated transactions on the basis that different statutes or regulations apply to the various transactions.

• Under the temporary regulations,

• The arm’s length compensation must be consistent with and account for all of the value provided between the parties, without regard to the form or character of the transaction.

• The combined effect of two or more separate transactions (including transactions that are analyzed under different statutory or regulatory provisions) may be considered if the transactions are economically interrelated such that an aggregate analysis provides the most reliable measure of an arm’s length result.

• A coordinated best method analysis may be required for two or more transactions where one or more provisions of the Code or regulations apply. This includes consistent consideration of the facts and circumstances of the functions performed, resources employed, and risks assumed.

• Allocation of value under a coordinated best method analysis must be allocated under a method that provides the most reliable measure of an arm’s length result for that allocated item.

New F Reorganization Regulations

20© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Overview

In General

• Final regulations released September 18, 2015 generally adopted provisions of the 2004 Proposed Regulations relating to reorganizations under Section 368(a)(1)(F) (“F reorganizations”), with certain specified and clarifying changes. Treas. Reg. § 1.368-2(m).

• Also adopted, without substantive change, the provisions of the 1990 temporary and proposed Section 367(a) regulations regarding outbound F reorganizations. Treas. Reg. § 1.367(a)-1.

Effective Date

• Effective for transactions occurring on or after Monday, September 21, 2015 (i.e., date of publication in the Federal Register).

Overview of Regulations

• Generally affirm F reorganization “in a bubble” principle by retaining Related Events Rule from the 2004 proposed regulations.

• Clarify and expand the list of requirements for a transaction to qualify as an F reorganization.

• Utilize the concept of a “Potential F Reorganization” in evaluating whether the transaction results in a “mere change” that qualifies as an F reorganization.

• Provide coordination rules for transactions that also qualify as a reorganization under other provisions of Section 368(a)(1).

• Provide rules related to distributions occurring concurrently with an F reorganization.

• Provide rules for outbound F reorganizations related to transferor corporation’s taxable year and the deemed mechanics of the reorganization.

21© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

“Mere Change” Requirements

Retained Requirements from 2004 Proposed Regulations

1. Resulting Corporation stock distributed in exchange for Transferor Corporation stock: Immediately after a Potential F Reorganization, all stock of the Resulting Corporation must have been distributed in exchange for stock of the Transferor Corporation in the Potential F Reorganization. Treas. Reg. § 1.368-2(m)(1)(i).

2. Identity of stock ownership: The same person or persons own all the stock of the Transferor Corporation at the beginning of the Potential F Reorganization and all of the stock of the Resulting Corporation at the end of the Potential F Reorganization in identical proportions. (Exceptions for concurrent transactions and de minimis variations). Treas. Reg. § 1.368-2(m)(1)(ii).

3. Prior assets or attributes of Resulting Corporation: The Resulting Corporation does not hold any property or have any tax attributes immediately before the Potential F Reorganization. (Exceptions for borrowings and de minimis variations). Treas. Reg. § 1.368-2(m)(1)(iii).

4. Liquidation of Transferor Corporation: The Transferor Corporation must completely liquidate in the reorganization for federal income tax purposes. (Exception for retaining charter, consistent with existing guidance for 332s, Cs and Ds). Treas. Reg. § 1.368-2(m)(1)(iv).

Additional Requirements

5. Resulting Corporation is the only acquiring corporation: Immediately after the Potential F Reorganization, no corporation other than the Resulting Corporation may hold property that was held by the Transferor Corporation immediately before the Potential F Reorganization, if the other corporation would, as a result, succeed to and take into account the items of the Transferor Corporation described in Section 381(c). Treas. Reg. § 1.368-2(m)(1)(v).

6. Transferor Corporation is the only acquired corporation: Immediately after the Potential F Reorganization, the Resulting Corporation may not hold property acquired from a corporation other than the Transferor Corporation if the Resulting Corporation would, as a result, succeed to and take into account the items of such other corporation described in Section 381(c). Treas. Reg. § 1.368-2(m)(1)(vi).

22© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Special Rules for Related Transactions

1. Series of transactions: A series of related transactions that together result in a mere change of one corporation may qualify as an F reorganization, whether or not isolated steps could be subject to other Code provisions. Treas. Reg. § 1.368-2(m)(3)(i).

2. Mere change within larger transaction: Related events that precede or follow the Potential F Reorganization generally will not cause the reorganization to fail (Related Events Rule). An F reorganization will not alter the character of other related transactions for federal income tax purposes. Treas. Reg. § 1.368-2(m)(3)(ii).

3. Distributions treated as separate transactions: Any concurrent distribution is treated as a separate transaction from the F reorganization. Treas. Reg. § 1.368-2(m)(3)(iii). (See also Treas. Reg. § 1.301-1(l)).

4. Transactions also qualifying under other provisions of section 368(a)(1):

Step transactions: If the Potential F Reorganization or a step thereof involving a transfer of property from the Transferor Corporation to the Resulting Corporation is also a reorganization or part of a reorganization in which a corporation in control of the Resulting Corporation is a party to the reorganization, the Potential F Reorganization does not qualify as an F reorganization. Applies to A and C reorganizations (direct and triangular). Treas. Reg. § 1.368-2(m)(3)(iv)(A).

F reorganization controls: Otherwise, F reorganization treatment will control for overlaps with one or more of A, C, or D reorganizations. Treas. Reg. § 1.368-2(m)(3)(iv)(B).

23© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

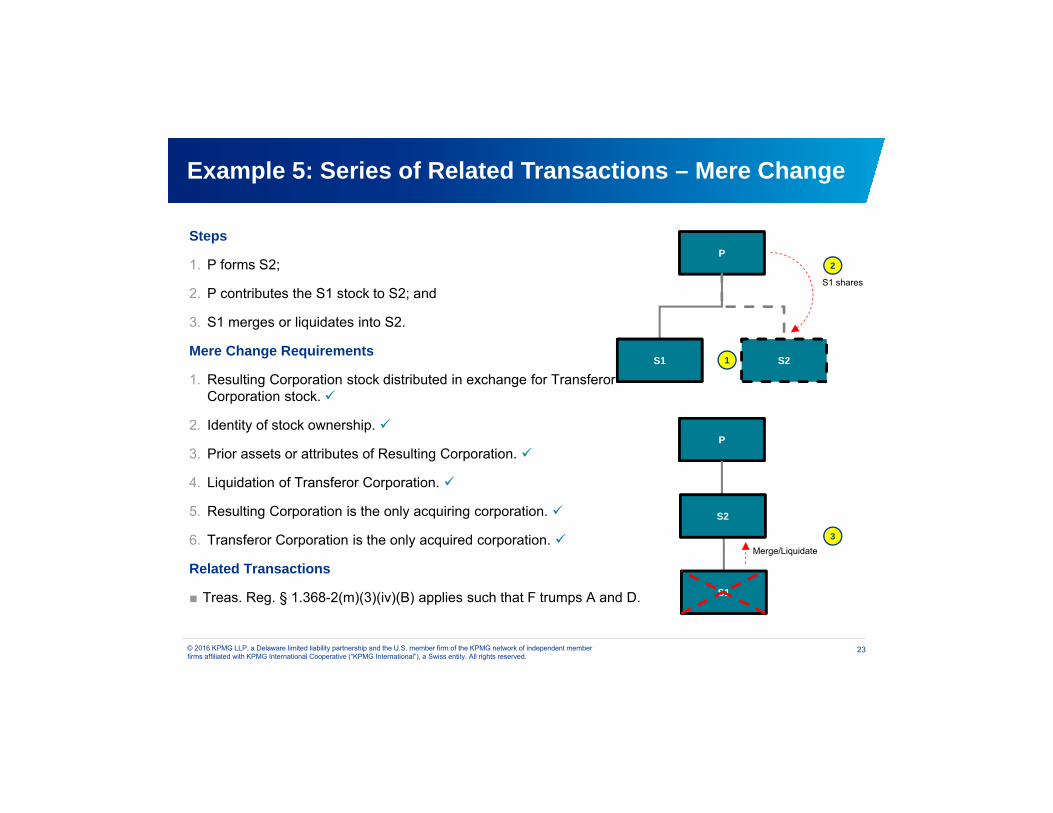

Example 5: Series of Related Transactions – Mere Change

Steps

1. P forms S2;

2. P contributes the S1 stock to S2; and

3. S1 merges or liquidates into S2.

Mere Change Requirements

1. Resulting Corporation stock distributed in exchange for Transferor Corporation stock.

2. Identity of stock ownership.

3. Prior assets or attributes of Resulting Corporation.

4. Liquidation of Transferor Corporation.

5. Resulting Corporation is the only acquiring corporation.

6. Transferor Corporation is the only acquired corporation.

Related Transactions

■ Treas. Reg. § 1.368-2(m)(3)(iv)(B) applies such that F trumps A and D.

S2

P

S1 shares

S1 1

2

P

S1

Merge/Liquidate3

2S2

24© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

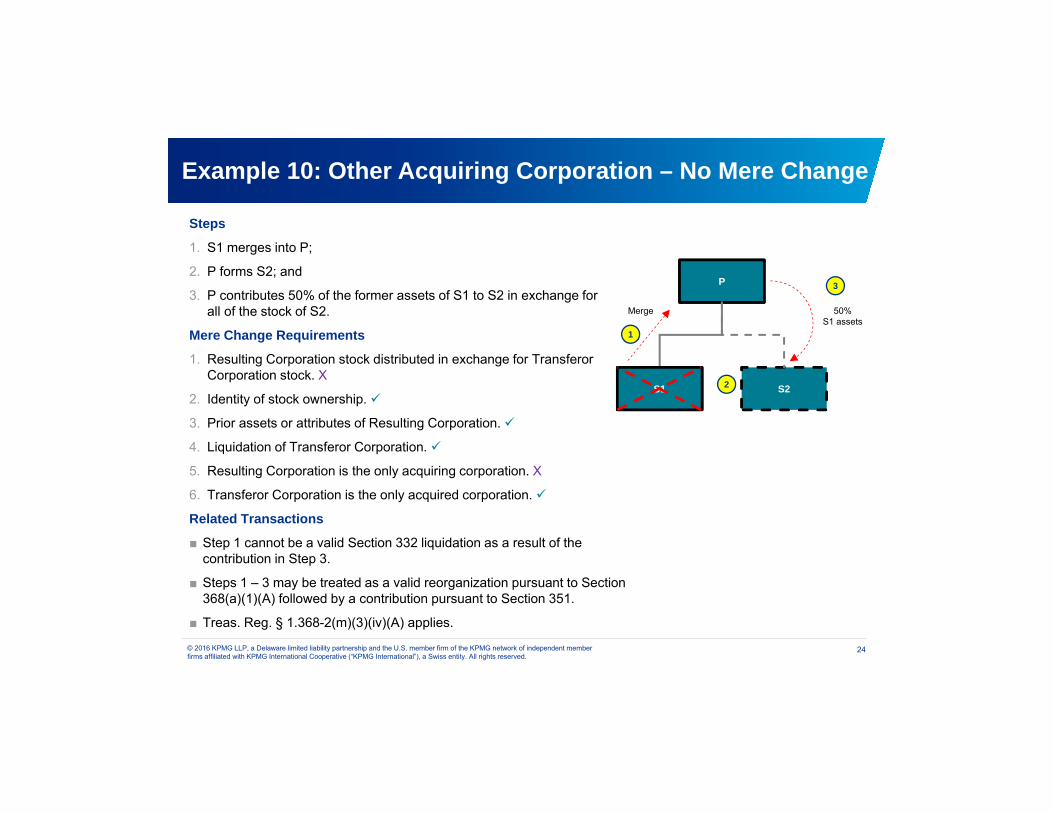

Example 10: Other Acquiring Corporation – No Mere Change

Steps

1. S1 merges into P;

2. P forms S2; and

3. P contributes 50% of the former assets of S1 to S2 in exchange forall of the stock of S2.

Mere Change Requirements

1. Resulting Corporation stock distributed in exchange for Transferor Corporation stock. X

2. Identity of stock ownership.

3. Prior assets or attributes of Resulting Corporation.

4. Liquidation of Transferor Corporation.

5. Resulting Corporation is the only acquiring corporation. X

6. Transferor Corporation is the only acquired corporation.

Related Transactions

■ Step 1 cannot be a valid Section 332 liquidation as a result of the contribution in Step 3.

■ Steps 1 – 3 may be treated as a valid reorganization pursuant to Section 368(a)(1)(A) followed by a contribution pursuant to Section 351.

■ Treas. Reg. § 1.368-2(m)(3)(iv)(A) applies.

S2

P

50%S1 assets

S1

Merge

1

3

2

25© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

X

Example 13: Series of Related Transactions – No Mere Change

Steps

1. P acquires all of the stock of T in exchange for cash and P stock(no Section 338 election);

2. P forms S; and

3. T is merged into S.

Mere Change Requirements

1. Resulting Corporation stock distributed in exchange for Transferor Corporation stock.

2. Identity of stock ownership.

3. Prior assets or attributes of Resulting Corporation.

4. Liquidation of Transferor Corporation.

5. Resulting Corporation is the only acquiring corporation.

6. Transferor Corporation is the only acquired corporation.

Related Transactions

■ Steps 1 – 3 may be treated as a valid reorganization pursuant to Section 368(a)(1)(A) by reason of Section 368(a)(2)(D). P’s momentary ownership of T stock is disregarded.

■ Treas. Reg. § 1.368-2(m)(3)(iv)(A) applies.

ST

P

T Stock

P Stock & Cash

1

2

P

T SMerge

3

26© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

New Treasury Regulations Relating to F ReorganizationsTreatment of Outbound F Reorganizations

• The final regulations also address F reorganizations in which the transferor corporation (the “Transferor Corporation”) is a domestic corporation and the acquiring corporation (the “Resulting Corporation”) is a foreign corporation — an “outbound F reorganization.”

• Specifically, the 2015 Final Regulations provide that where an outbound F reorganization occurs, the taxable year of the Transferor Corporation ends on the date of the transfer and the taxable year of the Resulting Corporation ends with the close of the date the Transferor Corporation’s year would have ended if the transfer had not occurred.

• In addition, the 2015 Final Regulations confirm that (nonwithstanding the single corporation concept for F reorganizations described above and nonwithstanding whether foreign law treats the Resulting Corporation as a continuance of the Transferor Corporation) an outbound F reorganization results in a deemed transfer of assets by the Transferor Corporation to the Resulting Corporation for Resulting Corporation followed by a liquidating distribution of the Resulting Corporation stock by the Transfer Corporationto its shareholders.

Inversions – Notices and Regulations

28© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Anti-Inversion Rule – U.S. Corporate Level Provision

• If, after the inversion transaction,

(i) At least 60% of the stock of the Foreign Acquirer is owned by historic shareholders of the U.S. Target, and

(ii) The Foreign Acquirer (taking into account certain subsidiaries) does not have “substantial business activities” in the jurisdiction of incorporation,

Then U.S. Target is subject to tax on “inversion gain” for 10 years with limited offsets for losses and credits.

• Further, if at least 80% of the stock of Foreign Acquirer is owned by U.S. Target’s historic shareholders, Foreign Acquirer will be taxed as if it were a U.S. corporation.

InversionsBasics of Section 7874

29© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Anti-Inversion Rule – U.S. Corporate Level Provision (Cont.)

• “Inversion Gain” means income or gain recognized by U.S. Target by reason of the transfer of stock or property or by reason of a license

• As part of the inversion transaction, or

• After the inversion transaction, if the transfer or license is to a foreign related person.

InversionsBasics of Section 7874 – Inversion Gain

30© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

• The anti-inversion rule does not apply if Foreign Acquirer has substantial business activities in its jurisdiction of incorporation.

• Substantial Business Activities: At least 25% of employees, assets, and income of Foreign Acquirer located or derived in its country of formation.

• For purposes of applying the substantial business activities test, the business activities of Foreign Acquirer includes the business activities of U.S. Target and their more than 50% owned (directly or indirectly) affiliates.

• IRS regulations exclude items, employees, and assets:

• Transferred to a foreign jurisdiction as part of a plan to avoid the anti-inversion rule; or

• Moved out of a foreign jurisdiction in connection with a plan that existed at the time the inversion transaction occurred.

InversionsBasics of Section 7874 – Substantial Business Activities

31© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

InversionsExcise Tax

■ A 15% excise tax is imposed on the value of certain stock compensation of an “expatriated corporation” that is held by officers, directors and 10% or greater owners.

■ An expatriated corporation is a U.S. corporation that undergoes an inversion transaction where between 60-80% of the stock of Foreign Acquirer is owned by the U.S. corporation’s historic shareholders.

■ The stock compensation this excise tax applies to is payment received as compensation from the expatriated entity the value of which is determined by reference to value of the stock of that corporation, e.g., compensatory stock and restricted stock grants, compensatory stock options, and other forms of stock-based compensation.

■ This excise tax applies only if any of the expatriated corporation's shareholders recognize gain on any stock in the corporation by reason of the corporate inversion transaction that caused the expatriation.

32© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

InversionsIllustrative Transaction

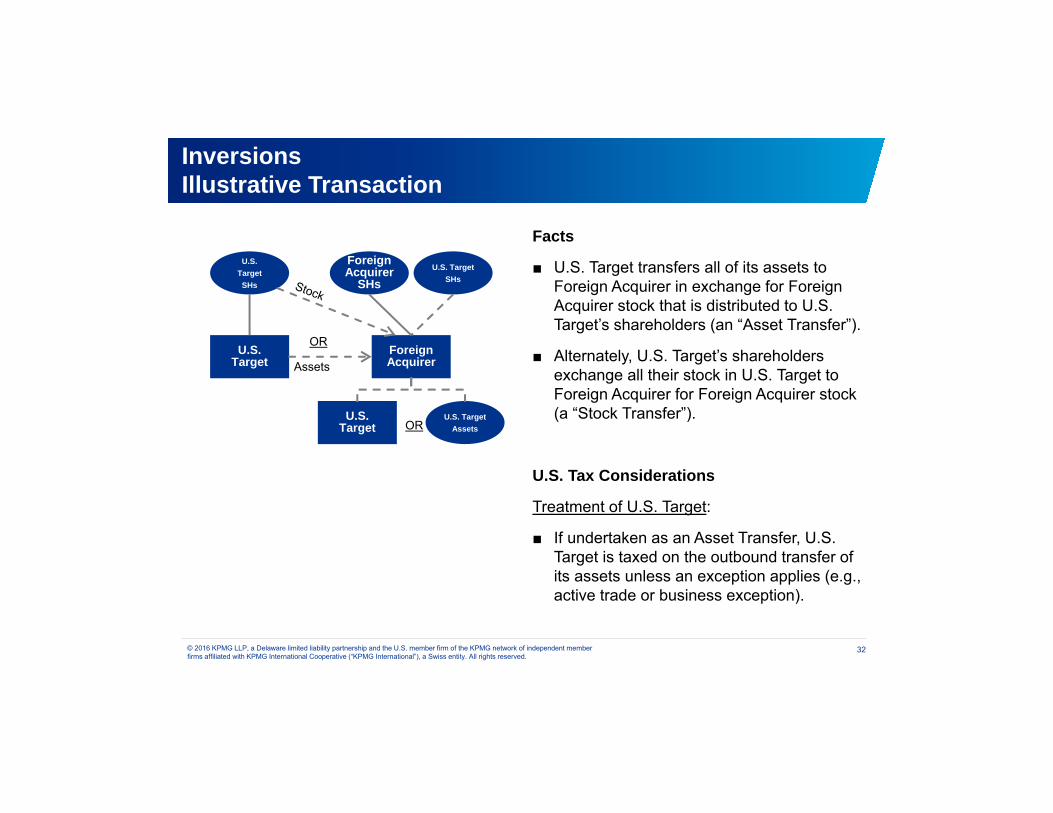

Facts

■ U.S. Target transfers all of its assets to Foreign Acquirer in exchange for Foreign Acquirer stock that is distributed to U.S. Target’s shareholders (an “Asset Transfer”).

■ Alternately, U.S. Target’s shareholders exchange all their stock in U.S. Target to Foreign Acquirer for Foreign Acquirer stock (a “Stock Transfer”).

U.S. Tax Considerations

Treatment of U.S. Target:

■ If undertaken as an Asset Transfer, U.S. Target is taxed on the outbound transfer of its assets unless an exception applies (e.g., active trade or business exception).

U.S.Target

U.S. TargetSHs

Foreign Acquirer

Foreign Acquirer

SHs

OR

U.S. TargetSHs

U.S.Target

Assets

U.S. TargetAssetsOR

Notice 2015-79

34© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Overview

Addressing Transactions Contrary to Section 7874 Purposes

Modifications to the Substantial Business Activities Test.

Third Country Transactions.

Clarification of Reg. § 1.7874-4T Regarding Avoidance Property.

Addressing Post-Inversion Tax Avoidance

Changes to Inversion Gain.

Gain Recognition for Exchanges of Expatriated Foreign Subsidiary Stock.

Corrections to Notice 2014-52

Modification of the General Definition of Foreign Group Nonqualified Property.

Addition of De Minimis Exception to “Shrinking” Distribution Rules.

De-Controlling/Significant Dilution Transactions .

35© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Modifications to the Substantial Business Activities Test

• Treasury and the IRS intend to issue regulations under section 7874 to provide that Foreign Acquirer cannot satisfy the “substantial business activities” test unless Foreign Acquirer is subject to tax as a resident of its country of formation.

• Applies to inversion transactions completed on or after November 19, 2015.

36© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Third-Country Transactions

Stock of Foreign Acquirer that otherwise would be included in the Ownership Test will be excluded from the Ownership Test to the extent the stock of Foreign Acquirer is held byformer owners of a foreign target corporation by reason of holding stock in the foreigntarget corporation if all following requirements are met:

■ In a transaction related to the inversion transaction (the “Foreign Target Acquisition”), Foreign Acquirer directly or indirectly acquires substantially all of the properties held by a foreign target corporation;

■ The gross value of all property directly or indirectly acquired by Foreign Acquirer in the Foreign Target Acquisition exceeds 60% of the gross value of all “foreign group property” other than “foreign group nonqualified property” and as modified by Notice 2015-79;

■ The tax residence of Foreign Acquirer is not the same as that of the foreign target corporation, as determined before the Foreign Target Acquisition and any transaction related to the Foreign Target Acquisition (a change in the foreign target corporation’s management or control is a “transaction”); and

■ The ownership percentage under the Ownership Test is at least 60% but less than 80% (without application of this rule).

Aggregation of multiple foreign target corporations that are tax residents of the same country.

Applies to inversion transactions completed on or after November 19, 2015.

37© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Clarification of Reg. § 1.7874-4T RegardingAvoidance Property

Treasury and the IRS intend to issue regulations that will clarify Treas. Reg. § 1.7874-4T to provide that so-called “avoidance property” means any property (other than specified nonqualified property) acquired with a principal purpose of avoiding the purposes of Section 7874, regardless of whether the property is used to indirectly transfer specified nonqualified property to the foreign acquiring corporation.

Applies to inversion transactions completed on or after November 19, 2015.

38© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Changes to Inversion Gain

Treasury and the IRS have determined that it is inconsistent with the purposes of Section 7874(a)(1) and (e) to exclude from the definition of Inversion Gain income or gain recognized by an expatriated entity from an indirect transfer or license of property in circumstances analogous to the transactions that currently produce Inversion Gain.

As a result, Treasury and the IRS intend to issue regulations that will provide that Inversion Gain includes income or gain recognized by an expatriated entity from an indirect transfer or license of property, such as an expatriated entity’s Section 951(a)(1)(A) gross income inclusions taken into account during the applicable period that are attributable to a transfer of stock or other properties or a license of property, either:

(i) as part of the inversion transaction, or

(ii) after such inversion transaction, if the transfer or license (other than inventory) is to a specified related person.

In addition, regulations will provide that if a partnership that is a foreign related person transfers or licenses property, a partner of the partnership shall be treated as having transferred or licensed its proportionate share of that property for purposes of determining the inversion gain.

Applies to transfers or licenses of property occurring on or after November 19, 2015, but only if the inversion transaction is completed on or after September 22, 2014.

39© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Certain Exchanges of Stock of an ExpatriatedForeign Subsidiary

Treasury and the IRS believe it is appropriate to require the exchanging shareholder to recognize all of the gain in the stock of the expatriated foreign subsidiary that is exchanged, without regard to the amount of the expatriated foreign subsidiary’s undistributed E&P.

Section 367(b) regulations will be amended to provide that, if an exchanging shareholder would be required under the rules announced in Notice 2014-52 to include in income as a deemed dividend the Section 1248 amount (if any) with respect to the stock of an expatriated foreign subsidiary, the exchanging shareholder also must recognize all realized gain with respect to such stock, after taking into account any increase in the basis resulting from a deemed dividend with respect to the exchange provided in Treas. Reg. § 1.367(b)-2(e)(3)(ii).

Conforming changes will be made to Notice 2014-52’s “specified stock” transfer rules.

Applies to specified exchanges occurring on or after November 19, 2015, but only if the inversion transaction is completed on or after September 22, 2014.

40© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Modification of the General Definition of Foreign Group Nonqualified PropertyExclusion for Property that Gives Rise to Income Described in Section 1297(b)(2)(B)

The regulations described in Notice 2014-52 will provide that property that gives rise to income described in the PFIC insurance exception will be excluded from the general definition of foreign group nonqualified property, but such property will be subject to the special rule for substitute property.

Exclusion of Property Held by Certain Domestic Corporations

The regulations described in Notice 2014-52 will provide that the general definition of foreign group nonqualified property does not include property held by a U.S. corporation that is subject to tax as an insurance company under subchapter L, provided that the property is required to support, or is substantially related to, the active conduct of an insurance business.

Foreign group nonqualified property will also not include property held by a U.S. corporation that gives rise to income derived in the active conduct of banking, financing, or similar businesses (as defined in Section 954(h)), with conforming changes to reflect the fact that Section 954(h) will be applied to a U.S. corporation and not a CFC.

This property will be subject to the special rule for substitute property.

Applies to inversion transactions completed on or after November 19, 2015, but taxpayers can elect to apply this rule to acquisitions completed before November 19, 2015.

41© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Addition of De Minimis Exception to “Shrinking” Distribution Rules

The so-called “Shrinking” Distribution rules in Notice 2014-52 could cause Section 7874 to apply to an acquisition even though the former owners of U.S. Target actually own no, or only a de minimis amount of, stock in Foreign Acquirer after the acquisition—an overbroad application.

Notice 2015-79 provides that a de minimis exception will be added to the “Shrinking” Distribution rules and will be available where:

The Ownership Test, determined without regard to Treas. Reg. § 1.7874-4T(b) and the rules in Notice 2014-52, must be less than 5% (by vote and value); and

After the acquisition and all transactions related to the acquisition are completed, former shareholders or former partners of the domestic entity, in the aggregate, must own (applying Section 318 as modified by Section 304(c)(3)(B)) less than 5% (by vote and value) of the stock of (or a partnership interest in) any member of the expanded affiliated group that includes Foreign Acquirer.

Applies to acquisitions completed on or after November 19, 2015, but taxpayers can elect to apply this rule to acquisitions completed before November 19, 2015.

42© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

De-Controlling/Significant Dilution Transactions

Notice 2014-52 provides that regulations will be issued that will recharacterize certain post-inversion transactions that otherwise would de-control or significantly dilute a U.S. shareholder’s ownership of a CFC that is an expatriated foreign subsidiary.

An exception to this general rule applies if:

■ (i) the expatriated foreign subsidiary is a CFC immediately after the specified transaction and all related transactions, and

■ (ii) the amount of stock (by value) of the expatriated foreign subsidiary that is owned, in the aggregate, directly or indirectly by the Section 958(a) U.S. shareholders of the expatriated foreign subsidiary immediately before the specified transaction and all related transactions does not decrease by more than 10%.

When applying this exception, Treasury and the IRS are concerned that taxpayers are measuring the value of stock of an expatriated foreign subsidiary owned by a section 958(a) U.S. shareholder immediately before a specified transaction with the value of the stock owned by the Section 958(a) U.S. shareholder immediately after the specified transaction, rather than comparing the percentage of the stock owned (by value) by the Section 958(a) U.S. shareholder before and after the specified transaction.

The regulations will clarify the application of the small dilution exception by substituting the phrase “the percentage of stock (by value)” for the phrase “the amount of stock (by value).”

Applies to specified transactions and specified exchanges completed on or after November 19, 2015, but only if the inversion transaction is completed on or after September 22, 2014.

43© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Devon M. BodohPrincipal

Professional and Industry ExperienceDevon M. Bodoh is the leader of KPMG International’s Global Complex Transactions Group. In addition, Mr. Bodoh is the Principal-in-Charge of KPMG US’s Washington National Tax International M&A Group. Mr. Bodoh is on KPMG’s global leadership group for International Tax and Deal Advisory (M&A) Tax.

Mr. Bodoh advises clients on cross border mergers, acquisitions, inversions, spin-offs, other divisive strategies, restructurings, bankruptcy and non-bankruptcy workouts, the use of net operating losses, foreign tax credits, deficits and other tax attributes, and consolidated return matters.

Prior to joining KPMG, Mr. Bodoh was a partner in the international law firm of Dewey & LeBoeuf LLP (as well as its predecessor firm Dewey Ballantine LLP).

Publications and Speaking EngagementsMr. Bodoh is a frequent speaker on subjects in his practice area for various groups, including the Tax Executives Institute, the Practising Law Institute, the American Bar Association, the DC Bar Association, the American Law Institute/American Bar Association, the American Institute of Certified Public Accountants, BNA/Center for International Tax Education, the International Tax Institute and the Law Education Institute.

Representative TransactionsBurger King’s acquisition of Tim Hortons, Horizon’s acquisition of Vidara, eBay’s potential spin-off of PayPal, The Walt Disney Company’s spin-off of ABC Radio, Darden’s potential spin-off of its real estate, Pfizer’s spin-off of its animal health business, SES’s spin-off of various businesses to GE, Elan’s spin-off of Neotope, Nextera’s Yieldco public offering, The Walt Disney Company’s acquisition of Pixar, Marvel and Fox Family, and NCR’s acquisition of Retalix Ltd

DEVON M. BODOHPrincipal-in-ChargeInternational M&AWashington National TaxKPMG LLP

Washington DC Office1801 K Street, NWWashington, DC 20006

Tel +1 202-533-5681Fax +1 202-609-8969Cell +1 [email protected]

Function and SpecializationCross border mergers, acquisitions, spin-offs, divestitures, liquidating and nonliquidating corporate distributions, corporate reorganization, and consolidated returns

Education, Licenses & Certifications• LLM, Taxation, New York University of Law• JD, University of Detroit Mercy School of Law

School• BBA, University of Michigan Stephen M. Ross

School of Business

44© 2016 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Aaron FeinbergGeneral Motors Company – Senior Tax Counsel

Background

Aaron Feinberg

Senior Tax Counsel, General Motors Company

Tower 300, Office B44300 Renaissance CenterDetroit, Michigan 48265

Tel +1 313-667-9616Fax +1 313-665-5125Email: [email protected]

Education, Licenses & Certifications

• LL.M. in Taxation, Georgetown University School of Law

• J.D., Boston University School of Law• B.A., Michigan State University

Aaron joined General Motors Company in December 2014 as Senior Tax Counsel, where he focuses on domestic and cross-border transactions and internal restructurings and tax controversy matters with taxing authorities. Prior to joining General Motors, Aaron served as a Tax Managing Director and Mid-Americas practice leader for KPMG’s Mergers & Acquisitions Tax practice in Detroit.

Prior to joining KPMG in 2011, Aaron was an attorney with the international law firm of Skadden, Arps, Slate, Meagher & Flom, LLP, in Washington, D.C., and a partner at Honigman, Miller, Schwartz & Cohn in Detroit, Michigan. Aaron has significant experience with the U.S. and local tax consequences of cross-border mergers and acquisitions and restructurings.

Professional and Industry Experience

Aaron’s experience includes assisting various forms of business entities on tax matters critical to domestic and cross-border mergers and acquisitions, internal restructurings and financially distressed companies. His background includes the provision of tax advice relating to transaction and financing structures, due diligence, post-merger integration strategies, debt modifications and the preservation of net operating losses and other tax attributes.

Aaron has experience in a broad category of transactions and industries, including the following:

Advising U.S. and foreign business entities and private equity funds on the U.S. tax aspects of structuring acquisitions of U.S. and non-U.S. businesses, including tax-free reorganizations of publicly-traded target companies.

Providing advice in connection with internal, cross-border restructurings, including the local tax implications of the various organizational structures.

Representation of debtor corporations in connection with tax issues arising from insolvency and filings, including issues arising from the cancellation of existing indebtedness, the post-emergence preservation of tax attributes and tax planning for bankruptcy emergence transactions.

Thank you