M Lynch_Multi PB

12

The Multi-Prime Broker Environment Ovr cong h Chang an Rang h Bn June 2008

-

Upload

genie-song -

Category

Documents

-

view

218 -

download

0

Transcript of M Lynch_Multi PB

8/3/2019 M Lynch_Multi PB

http://slidepdf.com/reader/full/m-lynchmulti-pb 1/12

The Multi-PrimeBroker Environment

Ovrcong h Chang

an Rang h Bn

June 2008

8/3/2019 M Lynch_Multi PB

http://slidepdf.com/reader/full/m-lynchmulti-pb 2/12

For or nforaon, a conac:

AmeRiCAs

Cary Gon

222 Broaway

Nw York, Nw York 10038

212.670.2564

euROpe, middle eAst, & AFRiCA

Ana N

2 Kng ewar sr

lonon eC1A 1HQ

+44 20 7996 2475

AsiA

prn Ko

iCBC towr

3 Garn Roa

Cnra, Hong Kong

+852 2161 7124

Merrill Lynch Global Markets Financing & Services

8/3/2019 M Lynch_Multi PB

http://slidepdf.com/reader/full/m-lynchmulti-pb 3/12

The Multi-Prime Broker Environment —Overcoming the Challenges and Reaping the Benets

Historically, it has been common or a hedge und to utilize multiple executing

brokers and a single prime broker. oday, many hedge unds have discovered the

benets o working with multiple prime brokers, as well. Given the value that

investment banks place on nancing ees, prime broker balances play a signicant

role in determining access to the scarce resources that investment banks oer hedgeunds: alpha-generating trade ideas, deal origination, research, calendar access,

capital introduction, etc. By spreading balances across multiple prime brokers,

a hedge und can eectively leverage its access to these valuable resources rom

multiple providers.

ransitioning to a multi-prime operating environment does have its challenges;

a signicant one being the need to aggregate position, cash balance and risk data

into consolidated reports. However, these operational challenges are usually not

insurmountable. Additionally, the process o going multi-prime can oen be a catalyst

or reducing the dependence on outside service providers, giving the und greater

control over its operations. Tis may assist in growing the und, especially given theincreasingly global trend o institutional investors demanding “best-practices” back-

and middle-oce environment beore investing.

Te research indicates that the majority o large unds are using multiple prime

brokers. A 2006 study conducted by Greenwich Associates indicates that three

quarters o hedge unds with more than $1 billion in AUM utilize at least two prime

brokers, and more than 35% o those unds use our or more. Many o the smaller

unds surveyed utilized multiple prime brokers as well.

Figure 1: Number of Prime Brokerage Relationships by Fund Size1

1 Greenwich Associates study commissioned on behalf of Merrill Lynch, 2006

Funds with less than $100 million in AUM

Funds with $100 million to $1 billion AUM

Funds with more than $1 billion in AUM

Prime brokerage is a

currency which can be

used to obtain scarce

resources from theinvestment banks.

8/3/2019 M Lynch_Multi PB

http://slidepdf.com/reader/full/m-lynchmulti-pb 4/12

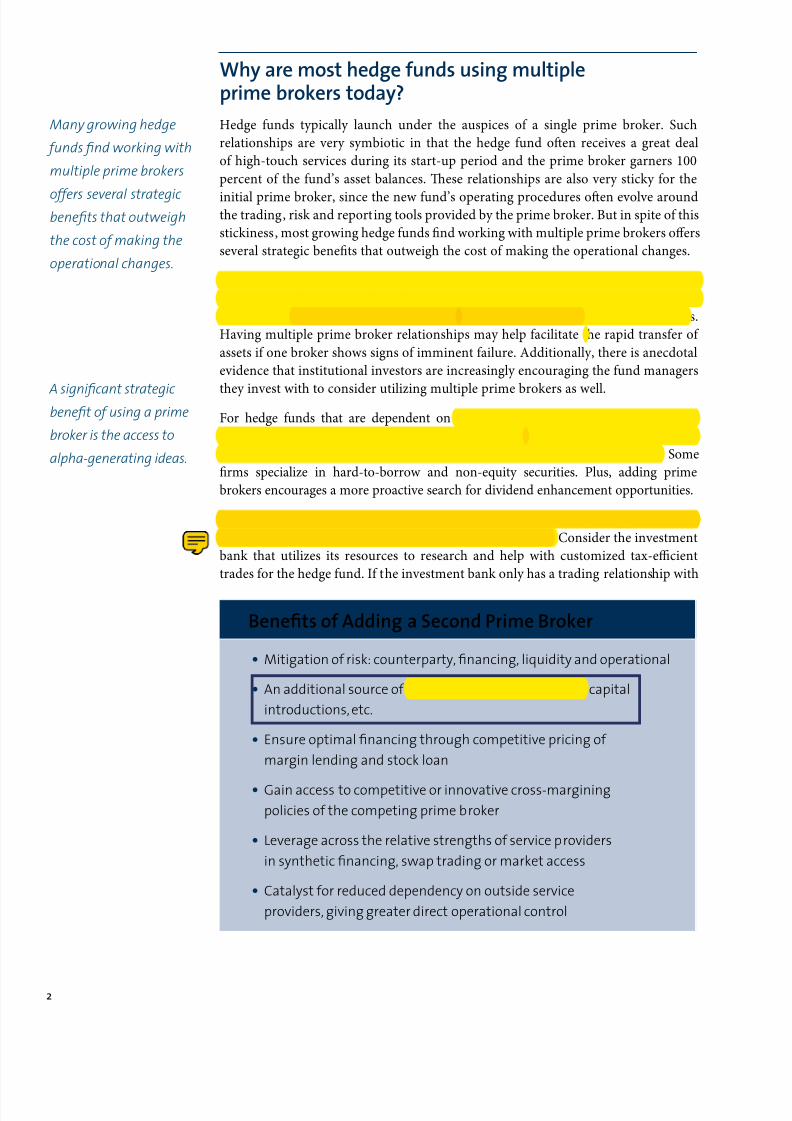

Why are most hedge funds using multipleprime brokers today?

Hedge unds typically launch under the auspices o a single prime broker. Such

relationships are very symbiotic in that the hedge und oen receives a great deal

o high-touch services during its start-up period and the prime broker garners 100

percent o the und’s asset balances. Tese relationships are also very sticky or the

initial prime broker, since the new und’s operating procedures oen evolve aroundthe trading, risk and reporting tools provided by the prime broker. But in spite o this

stickiness, most growing hedge unds nd working with multiple prime brokers oers

several strategic benets that outweigh the cost o making the operational changes.

Tere are many reasons why hedge unds utilize multiple prime brokers, but the recent

turmoil in the nancial markets and the collapse o a bulge bracket prime broker

have driven diversication o counterparty risk to the oreront o those reasons.

Having multiple prime broker relationships may help acilitate the rapid transer o

assets i one broker shows signs o imminent ailure. Additionally, there is anecdotal

evidence that institutional investors are increasingly encouraging the und managers

they invest with to consider utilizing multiple prime brokers as well.

For hedge unds that are dependent on securities lending, multiple prime brokers

means additional sources o borrow and better pricing. Each prime brokerage rm has

a dierent inventory o lendable securities, and some are deeper than others. Some

rms specialize in hard-to-borrow and non-equity securities. Plus, adding prime

brokers encourages a more proactive search or dividend enhancement opportunities.

A signicant strategic benet o using a prime broker is the ability the prime broker

has to make available alpha-generating ideas and strategies. Consider the investment

bank that utilizes its resources to research and help with customized tax-ecient

trades or the hedge und. I the investment bank only has a trading relationship with

Benets of Adding a Second Prime Broker

• Mitigation of risk: counterparty, nancing, liquidity and operational

• An additional source of alpha-generating trade ideas, capital

introductions, etc.

• Ensure optimal nancing through competitive pricing of

margin lending and stock loan

• Gain access to competitive or innovative cross-margining

policies of the competing prime broker

• Leverage across the relative strengths of service providers

in synthetic nancing, swap trading or market access

• Catalyst for reduced dependency on outside service

providers, giving greater direct operational control

Many growing hedge

funds nd working with

multiple prime brokers

offers several strategic benets that outweigh

the cost of making the

operational changes.

A signicant strategic benet of using a prime

broker is the access to

alpha-generating ideas.

2

8/3/2019 M Lynch_Multi PB

http://slidepdf.com/reader/full/m-lynchmulti-pb 5/12

the und (and not a prime broker relationship), the investment bank is compensated or

its eorts through the commission on executing trades. However, a ull service prime

broker arrangement may be more nancially enduring and rewarding than only trading

commissions. Since the resources to research such customized trades are limited, the

investment bank may share its alpha generating with the clients that generate higher

revenues. By using prime brokers, the hedge und may benet rom multiple rms with

distinct resources working to help identiy alpha-generating trade ideas.

Another key benet may be the ability or the CFO or COO to ensure that the und is

optimally nanced through competitive pricing. Prime brokers with sole mandates,

particularly the top-tier prime brokers, may charge a premium or their services

(margin nancing, security lending, etc.). A und may assert pricing pressure on its

initial prime by introducing additional prime brokers.

Additionally, the types o services and their relative strength vary across prime brokers.

Not all rms have the same capabilities with regard to synthetic nancing, swap trading,

local market access or direct market access trading tools. Cross-margin policies and

the manner in which o-setting positions can reduce collateral requirements also vary

among dierent prime brokers. Capital utilization may be optimized by custodying a

group o securities with whichever prime broker oers the best margin or collateralrelie or any given position.

Utilizing multiple prime brokers may allow a hedge und to mitigate several types o risk.

Counterparty risk diversication, as mentioned previously, comes rom having multiple

custodians. Funding liquidity risk can be reduced by having nancing relationships

with multiple brokers, which is especially critical at times o market distress. On the

operational side, multiple prime brokers may act as a “check-and-balance” or corporate

action processing, minimizing the likelihood that a corporate action will be missed i a

given security is held at multiple primes. Also, by not relying on a single prime broker,

the hedge und has more options in the event one o its prime brokers experiences a

business interruption scenario. Lastly, splitting a und’s balances across multiple primebrokers ensures no single investment bank can view a hedge und’s entire portolio,

which may give the und manager an additional level o reassurance when working

with a prime broker rm that also conducts proprietary trading.

Implementing a Multi-Prime Broker Environment

Introducing additional prime brokers into a hedge und’s operating environment is

not without its challenges. Te degree o diculty is directly correlated to the level

o reliance on the initial prime broker or tools, such as intra-day P&L, position and

risk reporting, investor reporting, etc. Te more systems that are either maintained

in-house or by a neutral third-party provider, the easier it is to add a prime broker.

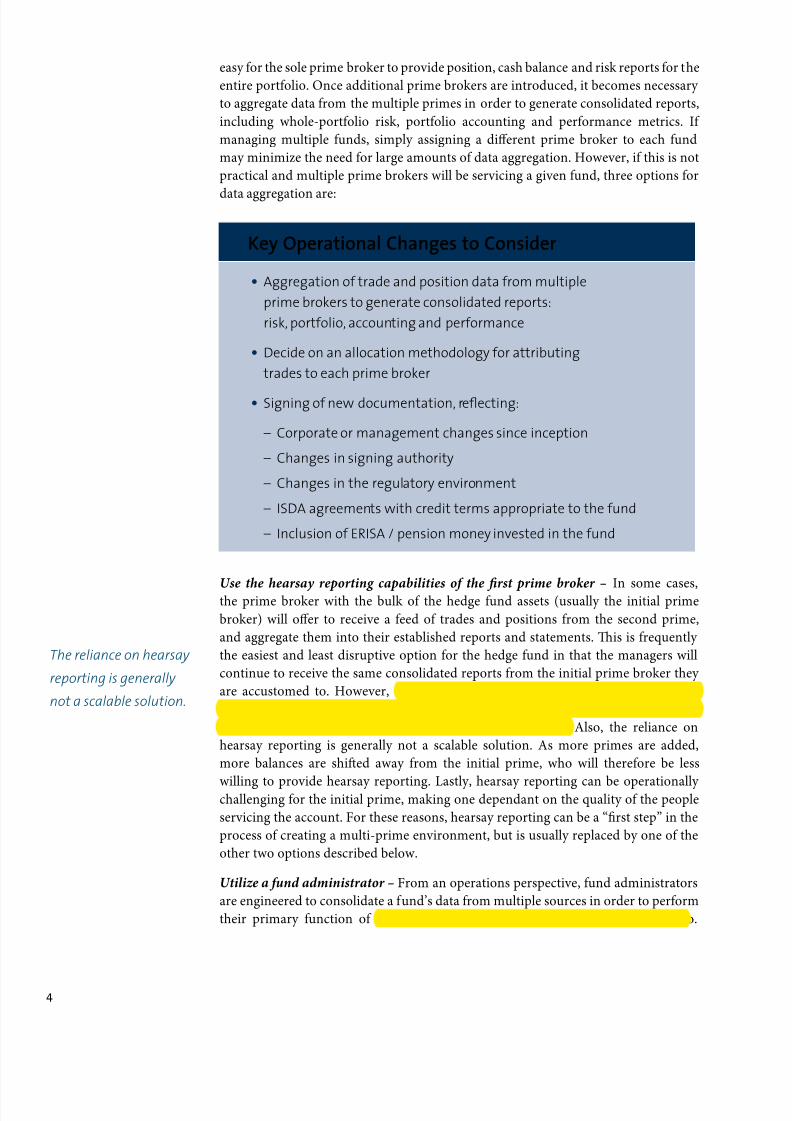

Data Aggregation

ransitioning to a multi-prime environment requires a number o decisions to be made

by the und manager. One signicant decision is the process or daily data aggregation.

When a hedge und uses only one prime broker, that prime broker has visibility to the

entire hedge und’s book. With all trade and position data maintained in one place, it is

Utilizing multiple prime

brokers allows a hedge

fund to mitigate several

types of risk.

Investment strategy

can drive the need for

multiple prime brokersand dictate the

solutions required.

8/3/2019 M Lynch_Multi PB

http://slidepdf.com/reader/full/m-lynchmulti-pb 6/12

easy or the sole prime broker to provide position, cash balance and risk reports or the

entire portolio. Once additional prime brokers are introduced, it becomes necessary

to aggregate data rom the multiple primes in order to generate consolidated reports,

including whole-portolio risk, portolio accounting and perormance metrics. I

managing multiple unds, simply assigning a dierent prime broker to each und

may minimize the need or large amounts o data aggregation. However, i this is not

practical and multiple prime brokers will be servicing a given und, three options or

data aggregation are:

Use the hearsay reporting capabilities o the frst prime broker – In some cases,the prime broker with the bulk o the hedge und assets (usually the initial prime

broker) will oer to receive a eed o trades and positions rom the second prime,

and aggregate them into their established reports and statements. Tis is requently

the easiest and least disruptive option or the hedge und in that the managers will

continue to receive the same consolidated reports rom the initial prime broker they

are accustomed to. However, the use o hearsay reporting negates one o the risk

diversication benets o a multi-prime environment — preventing any one prime

broker rom having ull knowledge o the und’s portolio. Also, the reliance on

hearsay reporting is generally not a scalable solution. As more primes are added,

more balances are shied away rom the initial prime, who will thereore be less

willing to provide hearsay reporting. Lastly, hearsay reporting can be operationally challenging or the initial prime, making one dependant on the quality o the people

servicing the account. For these reasons, hearsay reporting can be a “rst step” in the

process o creating a multi-prime environment, but is usually replaced by one o the

other two options described below.

Utilize a und administrator – From an operations perspective, und administrators

are engineered to consolidate a und’s data rom multiple sources in order to perorm

their primary unction o independently valuing a hedge und’s entire portolio.

Key Operational Changes to Consider

• Aggregation of trade and position data from multiple

prime brokers to generate consolidated reports:

risk, portfolio, accounting and performance

• Decide on an allocation methodology for attributing

trades to each prime broker

• Signing of new documentation, reecting:

– Corporate or management changes since inception

– Changes in signing authority

– Changes in the regulatory environment

– ISDA agreements with credit terms appropriate to the fund

– Inclusion of ERISA / pension money invested in the fund

The reliance on hearsay

reporting is generally

not a scalable solution.

4

8/3/2019 M Lynch_Multi PB

http://slidepdf.com/reader/full/m-lynchmulti-pb 7/12

Tereore, they requently provide consolidated versions o the common reports

prime brokers generate (position, cash balance, risk reports, etc.). As a solution to

the data aggregation problem, use o a und administrator does not suer the same

scalability issue that hearsay reporting does. It also has the advantage o ensuring

that each prime broker can only view their portion o the hedge und’s portolio.

Some und administrators also oer outsourced middle oce services. In addition to

data aggregation, these services may include much o the daily processing necessary

to support a und (P&L calculation, reconciliation, collateral management, etc.).

Tere are some challenges with this approach, most notably the need or hedge und

sta to manage the process. Fund administration and/or middle oce outsourcing

is an additional expense that will have to be borne by the und, as many domestic

unds do not use a und administrator or their onshore entities. Further, not all und

administrators have the ability to service the complex asset classes that are now being

employed by many und managers.

Build in-house capabilities – Te most fexible (and generally most costly) solution

may be to implement internal systems that will consolidate the data across all prime

brokers and generate all the necessary reports internally. Such implementations

requently start out with a vendor-supplied order management system to controlthe allocation o trades across multiple primes (see below). Requirements or control

over in-house data aggregation requirements, internal and investor reporting

requirements, and accounting control, lead to the use o a third-party accounting

solution. Tese systems usually require customized integration with the other existing

soware packages and data present within the und. While this approach does entail

signicant cost, both in terms o the vendor soware and the I services/personnel

required to implement and maintain the system, the benet is sel-suciency and

Consolidated Reporting Options

O P T I O N S P R O S C O N S

Haray by

pr Brokr

wh Bk of

A

• Easiest implementation

• Least expensive option

• Already familiar with reportformats

• Not scalable – hard to add athird or fourth Prime Broker

• “Prime” Prime Broker can still view entire portfolio

• Dependency on “Prime” PrimeBroker’s release schedule, willingnessto accommodate hearsay, etc.

Fn

Anraor

• Scalable up to any numberof Prime Brokers

• Each Prime Broker only views

its portion of the portfolio• Usually more cost eective

than doing all aggregation

and reporting in-house

• Additional expense (to the fund)

• Some have diculty withexotic products

• Must get familiar with new report formats

B in-Ho

Caab

• Most exible

• Each Prime Broker only viewsits portion of the portfolio

• All data remains in house

• Most costly in both time

and expense (usually borne bythe management company)

An in-house solution

ensures that there is

no dependency on any outside providers or

vendors for custom

reporting, data

extracts, etc.

8/3/2019 M Lynch_Multi PB

http://slidepdf.com/reader/full/m-lynchmulti-pb 8/12

complete control over the und’s data. Te importance o this can’t be overstated. A

common complaint rom unds in the multi-asset class arena is the inability to access

“our data” rom external vendors and service providers. An in-house solution may

remove the hedge und’s dependency on any outside providers or vendors or custom

reporting, data extracts, etc. Additionally, each prime broker will continue to have

access to only their portion o the portolio.

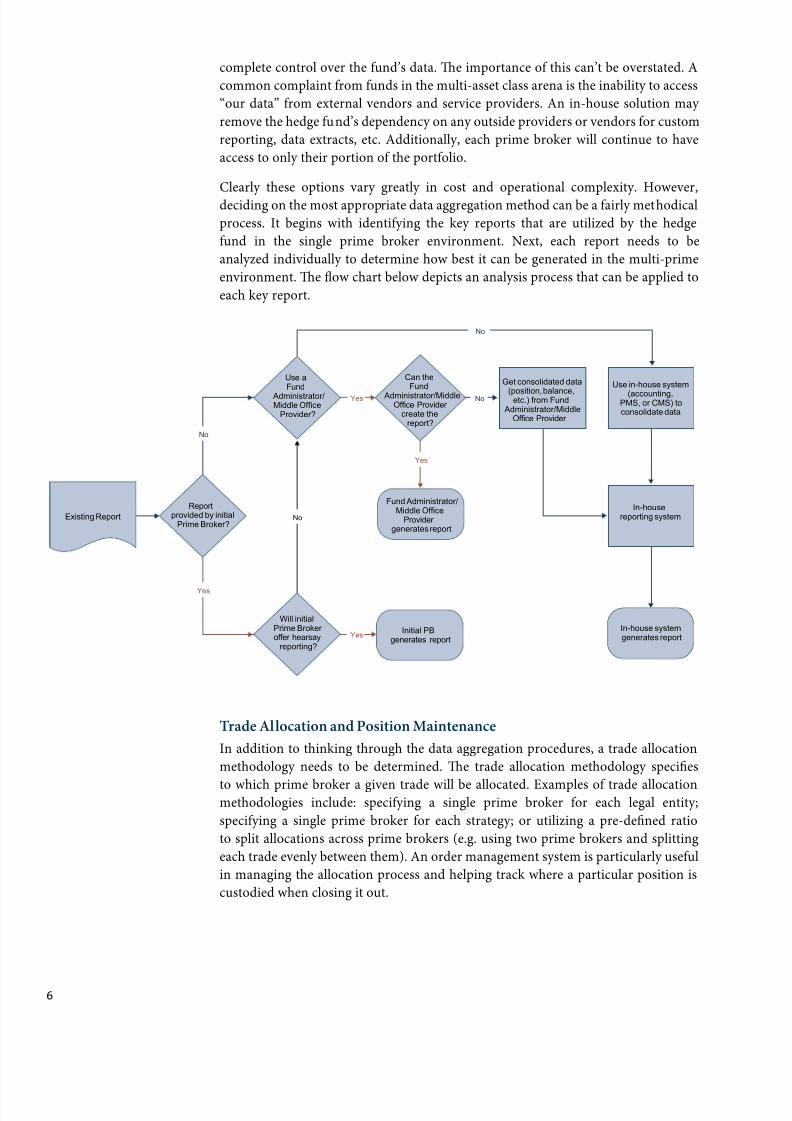

Clearly these options vary greatly in cost and operational complexity. However,

deciding on the most appropriate data aggregation method can be a airly methodical

process. It begins with identiying the key reports that are utilized by the hedge

und in the single prime broker environment. Next, each report needs to be

analyzed individually to determine how best it can be generated in the multi-prime

environment. Te fow chart below depicts an analysis process that can be applied to

each key report.

Trade Allocation and Position Maintenance

In addition to thinking through the data aggregation procedures, a trade allocation

methodology needs to be determined. Te trade allocation methodology species

to which prime broker a given trade will be allocated. Examples o trade allocationmethodologies include: speciying a single prime broker or each legal entity;

speciying a single prime broker or each strategy; or utilizing a pre-dened ratio

to split allocations across prime brokers (e.g. using two prime brokers and splitting

each trade evenly between them). An order management system is particularly useul

in managing the allocation process and helping track where a particular position is

custodied when closing it out.

Existing Report

Reportprovided by initial

Prime Broker?

Will initialPrime Broker offer hearsay

reporting?

Initial PBgenerates report

Fund Administrator/Middle Office

Provider generates report

Use aFund

Administrator/Middle Office

Provider?

Can theFund

Administrator/MiddleOffice Provider

create thereport?

Get consolidated data

(position, balance,etc.) from Fund

Administrator/MiddleOffice Provider

In-house systemgenerates report

In-housereporting system

Use in-house system

(accounting,PMS, or CMS) toconsolidate data

Yes

No

No

Yes

Yes

Yes

No

No

6

8/3/2019 M Lynch_Multi PB

http://slidepdf.com/reader/full/m-lynchmulti-pb 9/12

When choosing a trade allocation process, it is also important to consider the

impact o cross-margining. I the hedge und is trading o-setting positions that canpotentially reduce collateral requirements at a prime broker, it is critical that the o-

setting trades be allocated to the same prime broker. I the trades are sent to dierent

prime brokers, no margin relie will be realized.

Recommended Documentation Practices To Help with theMulti-Prime Broker Implementation

I it has been more than a couple o years since the initial prime broker relationship

was established, the managers o the hedge und should expect a more involved

documentation process. o ensure the documentation process or adding a prime

broker proceeds as smoothly as possible, it is important to rst review the und and

management company’s ormation documents. Any corporate or management changes

that have occurred since the inception o the und must be properly documented.

Additionally, signing authority documentation should be current. While going

through the process o adding a second prime broker, save all required constitutional

documents and other background inormation in a single place so they will be easily

accessible i any prime brokers are added aer the rst two. Lastly, once the process

has started, the und’s documentation contacts should be committed to providing all

inormation in a timely manner. I there are any questions about the process or the

documents themselves, quickly seek guidance rom the documentation specialists at

the new prime broker so as not to lose time or momentum.

When negotiating the prime broker relationship terms, the most critical initial actorsto consider are timing, cost and risk tolerance. Clear communication o the und

managers’ priorities, and views on these topics to both internal and external counsel

is essential. Tat said, the terms will vary among prime brokers as a result o their

dierent and evolving credit and risk tolerance levels, legal perspectives and business

models.

While going through

the process of adding a

second prime broker, save

all required constitutional

documents and other

background information

in a single place so they

will be easily accessible

if any prime brokers are

added after the rst two.

Methodologies For Allocating Trades

to Multiple Prime Brokers

s / sac • By Fund

• By Market

• By Strategy

Easiest to implement, but canbe dicult to adjust in order tomaintain target asset levels witheach Prime Broker

Granar / dynac • By Security

• On a pro rata basis

• Arbitrary method

More complex to implement,but can be recalibrated whentarget allocations of balancesacross prime brokers arereviewed and changed

Oornc • By borrow availability

• By executing Broker

Used in conjunction with oneof the others as a “ne-tuning”method to optimize nancingbenets

8/3/2019 M Lynch_Multi PB

http://slidepdf.com/reader/full/m-lynchmulti-pb 10/12

ISDA and Master Conrm Agreements

For hedge unds transacting in over-the-counter derivative markets, ISDA docu-

mentation must be negotiated (i.e. the ISDA Master Agreement and Credit Support

Annex, collectively “an ISDA Agreement”). While a prime broker relationship is

not a prerequisite or establishing an ISDA Agreement, hedge unds trading OC

derivatives will typically have an ISDA Agreement with each o their prime brokers

at a minimum.

Te main structure o an ISDA Agreement is dened by the International Swaps and

Derivatives Association, Inc. which acts as a clearinghouse o industry standards, but

each dealer can modiy the schedules/annexes to the ISDA Agreement to refect their

particular views on legal, credit, business and other risks. One critical issue or the

und manager to consider in the ISDA Agreement (and prime broker agreements as

well) is whether the credit terms are appropriate or the und’s strategy. Also, und

managers should be aware that the presence o ERISA/pension money in the und

may lead to a more extended negotiation process.

Related to the ISDA Agreement certain products use a Master Conrmation which

sets orth and governs specic transaction terms, as opposed to the overarching

contractual relationship established in the main document. While not required or

trading, it is recommended or any und trading large volumes o OC derivatives. A

Master Conrmation which is negotiated once at the beginning o the relationship,

along with the process o negative armation minimizes the amount o documentation

that must be generated, tracked and signed with each OC transaction, and thereore

reduces the strain on legal/documentation resources and back oce operations.

Transition to the Multi-Prime Broker Environment

Logistics o Transerring Securities and Cash Between Prime Brokers

When adding an additional prime broker, a hedge und has two options regarding the

establishment o accounts at the new prime broker:

• Open accounts at the new prime broker and initially fund with cash only

• Open accounts at the new prime broker and transfer existing positions/cash

in rom the original prime broker.

Te rst option is simpler rom a logistics perspective. Cash is wired into the account

(street-wide practice is to require a $500,000 minimum). Te hedge und manager will

then establish positions in the account trough new trading activity.

I the hedge und manager wishes to transer existing positions between prime brokers,

the integration team rom the new prime broker may work with the hedge und client

and the existing prime broker to dene an orderly transition plan. For US securities, thiswill most likely be done through the Automated Customer Account ranser Service

(ACAS). ACAS is an automated system managed by the DC. Although reliable,

ACAS makes use o the standard settlement process, which means the transer can

take several days to complete. Alternatively, “ree delivery/ree receive” can sometimes

be perormed or overnight delivery, but this process is manual and may expose the

prime brokers to settlement risk. For international securities, the transer process

between prime brokers will vary, depending on the issuing country o the security being

transerred, and what correspondent banks the prime brokers use in that country.

Fund managers should

be aware that the

presence of ERISA/pension

money in the fund may

lead to a more extended

negotiation process.

8

8/3/2019 M Lynch_Multi PB

http://slidepdf.com/reader/full/m-lynchmulti-pb 11/12

Use O Consulting Services

Te prime brokers recognize that the process o adding an additional relationship can

be taxing to a hedge und and its back oce sta. As a result, they requently oer

assistance in the orm o consulting services to help mitigate these pressures. Consulting

service oerings can include assistance with vendor and service provider selection,

project management, and process fow reengineering. Te consulting teams can also

provide guidance when making the decisions outlined above (trading methodology, data

aggregation, etc.) It is advisable to engage with the new prime broker’s consulting servicesas early as possible in order to help smooth the new prime broker integration process.

Reaping the Benets of theMulti-Prime Broker Environment

Clearly the decision to evolve to a multi-prime broker environment carries with it a

number o challenges to be aced and decisions to be made. While this decision will

have an impact on the daily operations o the hedge und, it is important to keep

in mind that the multi-prime decision is ultimately a strategic one. Just evaluating

the impact o an additional prime may highlight operational ineciencies (manual

processes, critical data residing in spreadsheets, etc.) that are present in many evolving

hedge unds. Since back-oce procedures may need to be modied to accommodate

the additional prime broker, the multi-prime transition may be an opportunity to

address those day-to-day ineciencies and move the und’s operations closer to

“institutional caliber.” Tis in turn may lead to better risk controls and may even

improve the und’s attractiveness to institutional investors. But ultimately, utilizing

the services o multiple prime brokers may allow hedge und managers to extract the

most value out o the prime brokerage community.

Tese materials are intended or inormational purposes only and should not be construed as investmentadvice. Tis document is designed to serve as a general summary o the trading services and products thatMerrill Lynch may oer rom time-to-time. Tis document is not intended to constitute advertising or adviceo any kind, and it should not be viewed as an oer or a solicitation to buy or sell securities, utures or any other nancial instrument. Merrill Lynch makes no representation, warranty or guarantee, express or implied,concerning this document and its contents, including whether the document and its contents (which may include inormation and statistics obtained rom third party sources) are accurate, complete or current. Te in-ormation in this document is subject to change at any time, and Merrill Lynch has no duty to provide you withnotice o such changes. In addition, Merrill Lynch will not be responsible or liable or any losses, whether direct,indirect or consequential, including loss o prots, damages, costs, claims or expenses, relating to or arising romyour reliance upon any part o this document. Te descriptions in this document are not a guarantee that any particular service or product will be available or your use, nor are the descriptions a guarantee that any serviceor product will perorm in accordance with such descriptions or help you to achieve particular results. Beoredetermining to use any service or product oered by Merrill Lynch, you should consult with your independent

advisors to review and consider any associated risks and consequences. For example, the risk o loss associatedwith utures and options trad¬ing (whether electronic or manual) can be substantial. Tis document has beenprepared without regard to the specic investment objectives, nancial situation and needs o any particularrecipient. Merrill Lynch does not render any opinion regarding legal, accounting, regulatory or tax matters.Tis document does not constitute an oer or agreement, or a solicitation o an oer or agreement, to enter intoany particular contractual relationship with Merrill Lynch. Any use o the trading services and products oeredby Merrill Lynch must be preceded by your acceptance o binding legal terms and conditions. Tis document iscondential, or your private use only, and may not be shared with others. Any reproduction or distribution o the document by you must be authorized in advance by Merrill Lynch in writing.© 2008, Merrill Lynch & Co.,Inc. Views expressed herein are current opinions as o the original publication date appearing on this materialonly, and the inormation is subject to change without notice. Tis document, including all trademarks andservice marks relating to Merrill Lynch, remains the intellectual property o Merrill Lynch. For other importantlegal terms governing the use o this document please see: http://www.ml.com/legal_ino.htm

8/3/2019 M Lynch_Multi PB

http://slidepdf.com/reader/full/m-lynchmulti-pb 12/12

©2008 mrr lynch, prc, Fnnr & sh incorora