M ANAGERIAL F INANCE I. C OURSE O BJECTIVE To familiarize students with the basic concepts, tools...

33

MANAGERIAL FINANCE I

-

Upload

robyn-flowers -

Category

Documents

-

view

214 -

download

0

Transcript of M ANAGERIAL F INANCE I. C OURSE O BJECTIVE To familiarize students with the basic concepts, tools...

MANAGERIAL FINANCE I

COURSE OBJECTIVE

To familiarize students with the basic concepts, tools and techniques of financial management for decision making.

to develop critical thinking to enable you to think in a broader perspective

COURSE OUTLINE

1. Introduction2. Financial Environment3. Financial Statement, Taxes and Cash-flow4. Time Value of Money5. Working Capital Management6. Cost of Capital7. Capital Investments

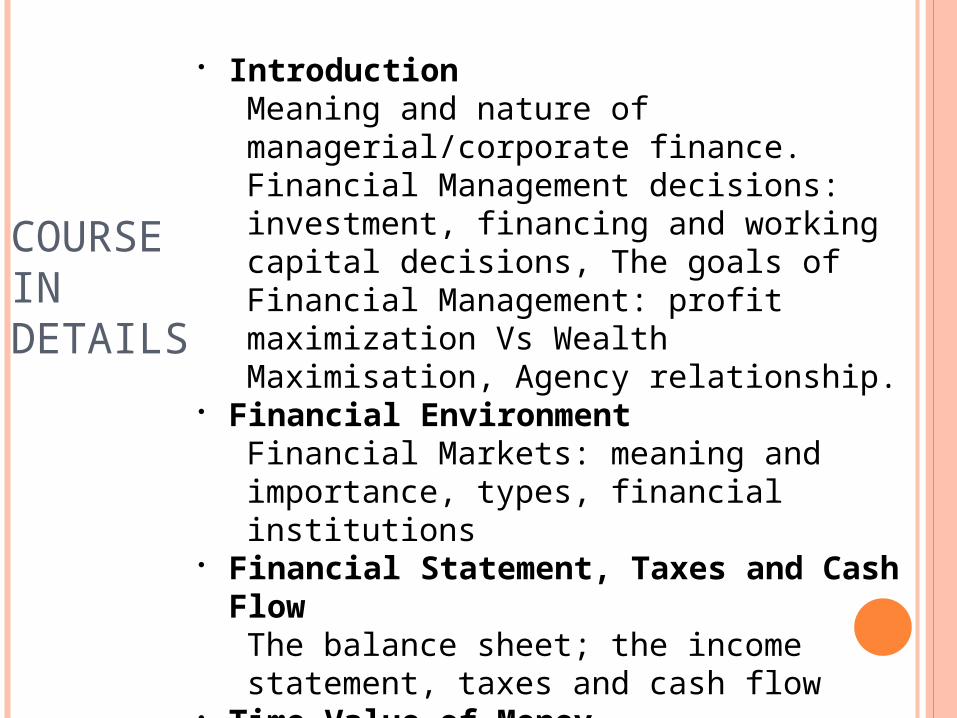

COURSE IN DETAILS

IntroductionMeaning and nature of managerial/corporate finance. Financial Management decisions: investment, financing and working capital decisions, The goals of Financial Management: profit maximization Vs Wealth Maximisation, Agency relationship.

Financial EnvironmentFinancial Markets: meaning and importance, types, financial institutions

Financial Statement, Taxes and Cash FlowThe balance sheet; the income statement, taxes and cash flow

Time Value of MoneyFuture Value, Present value, Future value of annuity, Present value of annuity, annuity dues, uneven cash-flow streams, perpetuities

COURSE IN DETAILS

Working Capital ManagementConcept of Working Capital and Net Working CapitalAlternative Current asset investment policiesCash and liquidity managementCash budgetReceivables managementInventory management (ABC, EOQ)

Cost of CapitalCost of components of capitalWACC

Capital InvestmentsProject classifications, Cash flow estimation, identifying relevant cash flows, Capital budgeting decision criteria. Ranking mutually exclusive projects.

TEXT BOOK AND REFERENCES

We will not be limited to a single text book.

Fundamentals of Corporate Finance by Ross, Westerfield and Jordon.

Essentials of Managerial Finance by Weston, Besley and Brigham

Fundamentals of Financial Management by Brigham and Houston

Principles of Managerial Finance by Lawrence J. Gitman. Principles of Corporate Finance by Richard A. Brealey: and

Stewart C. Myers

Other reference books and literatures will always be the added advantage.

MANAGERIAL FINANCE

Learning Unit 1

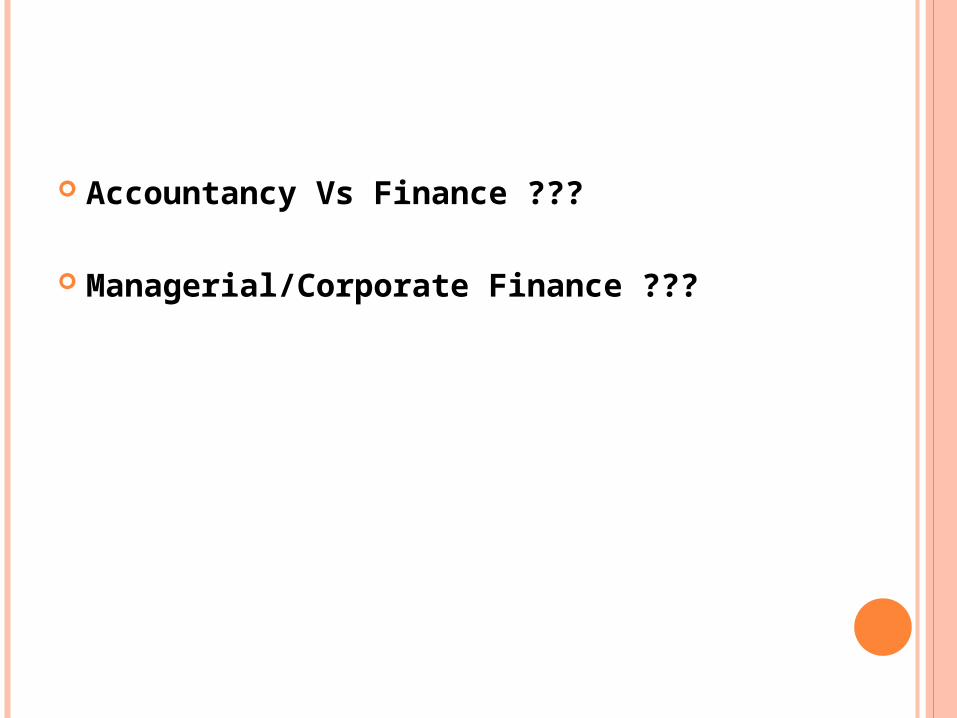

Accountancy Vs Finance ???

Managerial/Corporate Finance ???

FINANCE

The art and science of managing money.

MEANING AND NATURE OF MANAGERIAL/CORPORATE FINANCE

Corporate or managerial finance is the study of ways to answer these three questions.

MEANING AND NATURE OF MANAGERIAL/CORPORATE FINANCE

Corporate or managerial finance is the study of ways to answer these three questions.

1. What long-term investments should you take on? - Buildings, machinery, and equipments… - Capital budgeting

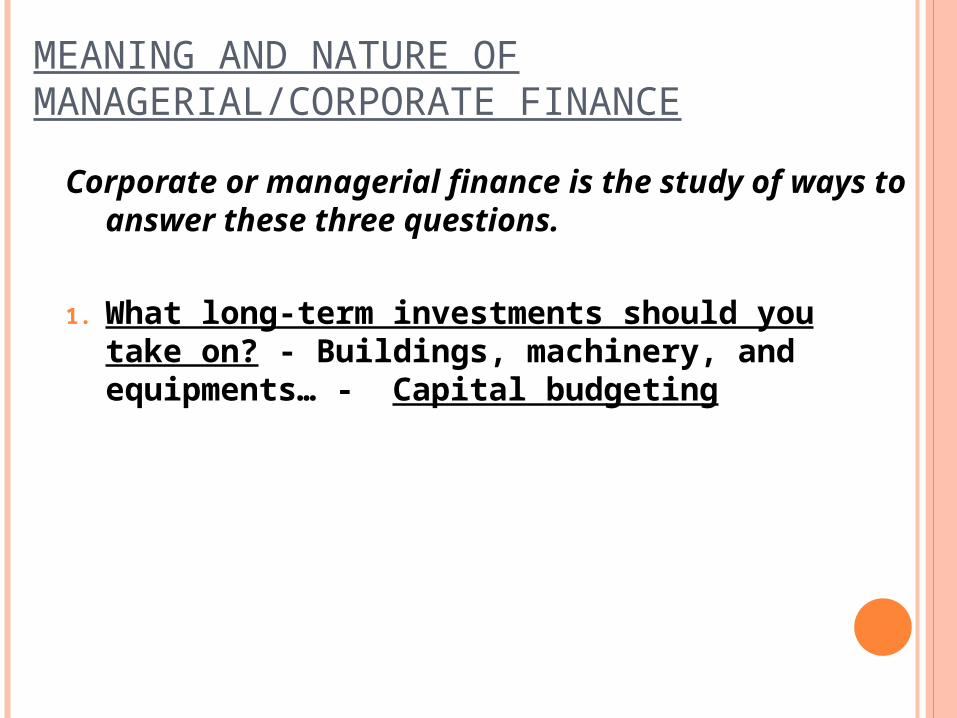

MEANING AND NATURE OF MANAGERIAL/CORPORATE FINANCE

Corporate or managerial finance is the study of ways to answer these three questions.

1. What long-term investments should you take on? - Buildings, machinery, and equipments… - Capital budgeting

2. Where will you get the long-term financing to pay for your investment? Will you bring in other owners or will you borrow the money? Capital Structure – the mixture of debt and equity

MEANING AND NATURE OF MANAGERIAL/CORPORATE FINANCE

Corporate or managerial finance is the study of ways to answer these three questions.

1. What long-term investments should you take on? - Buildings, machinery, and equipments… - Capital budgeting

2. Where will you get the long-term financing to pay for your investment? Will you bring in other owners or will you borrow the money? Capital Structure – the mixture of debt and equity

3. How will you manage your everyday financial activities such as collecting from customers and paying suppliers? Working capital management

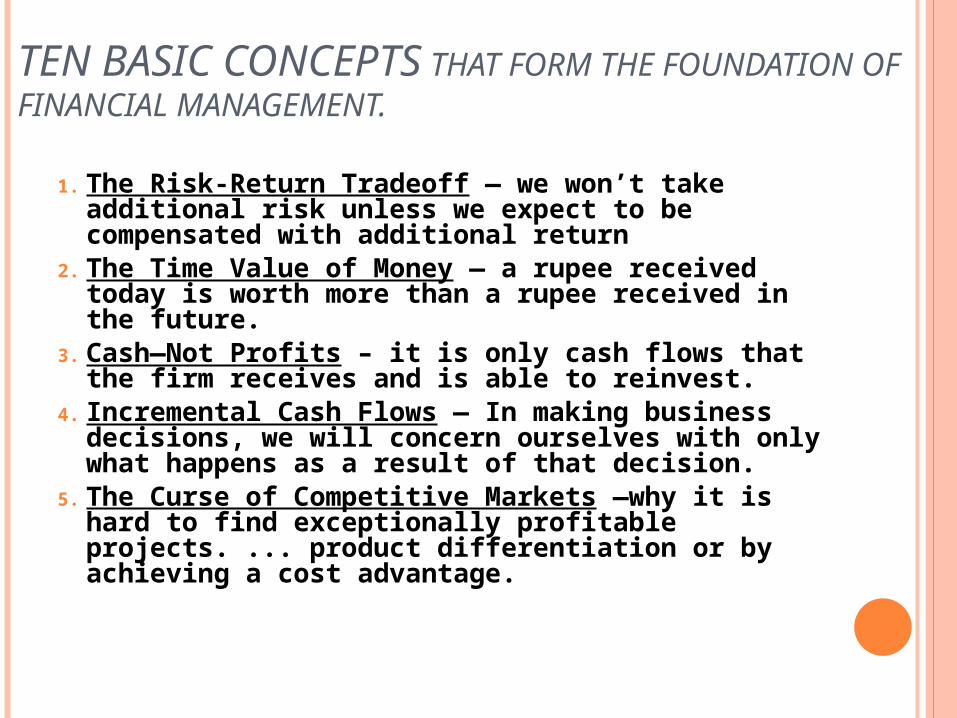

TEN BASIC CONCEPTS THAT FORM THE FOUNDATION OF FINANCIAL MANAGEMENT.

1. The Risk-Return Tradeoff — we won’t take additional risk unless we expect to be compensated with additional return

2. The Time Value of Money — a rupee received today is worth more than a rupee received in the future.

3. Cash—Not Profits – it is only cash flows that the firm receives and is able to reinvest.

4. Incremental Cash Flows — In making business decisions, we will concern ourselves with only what happens as a result of that decision.

5. The Curse of Competitive Markets —why it is hard to find exceptionally profitable projects. ... product differentiation or by achieving a cost advantage.

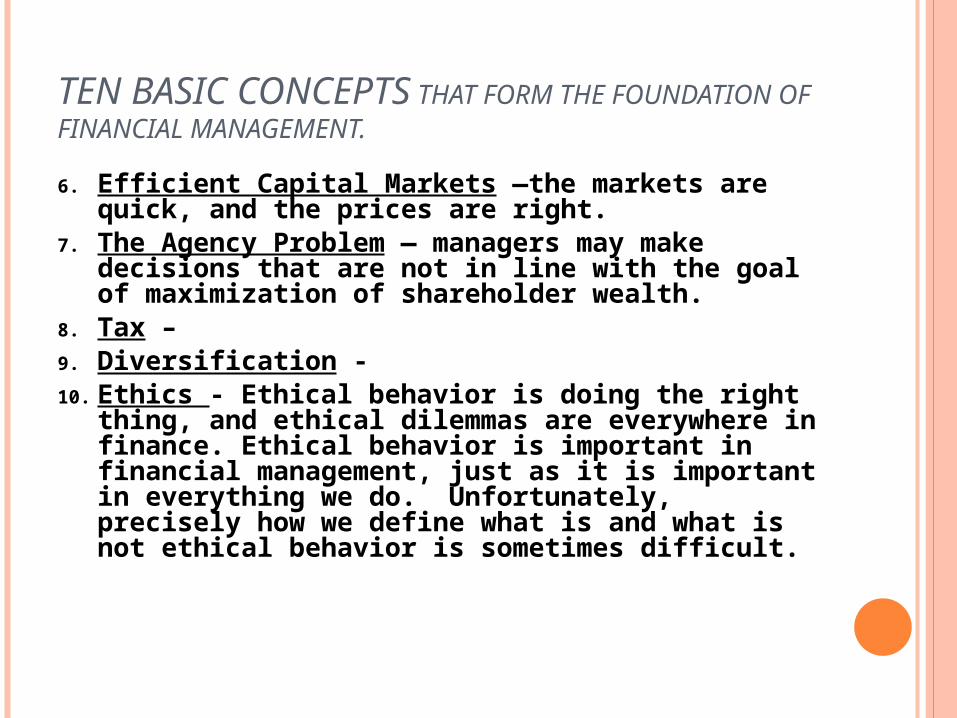

TEN BASIC CONCEPTS THAT FORM THE FOUNDATION OF FINANCIAL MANAGEMENT.

6. Efficient Capital Markets —the markets are quick, and the prices are right.

7. The Agency Problem — managers may make decisions that are not in line with the goal of maximization of shareholder wealth.

8. Tax – 9. Diversification - 10. Ethics - Ethical behavior is doing the right

thing, and ethical dilemmas are everywhere in finance. Ethical behavior is important in financial management, just as it is important in everything we do. Unfortunately, precisely how we define what is and what is not ethical behavior is sometimes difficult.

FIRM AND FINANCIAL MANAGER Those three decisions tend to be more

complex in large corporations than in small single-man businesses.

Sole proprietorships – sole proprietor - no partners or stockholders; Unlimited liability;

Partnerships – partners; unlimited liability Corporations – legally distinct from its

owners; publicly held shares; closely held or widely held shares; legal entity; can sue can be sued; taxes; lend and borrow; stockholders have limited liability;

Shareholders elect a Board of Directors; separation of ownership and management

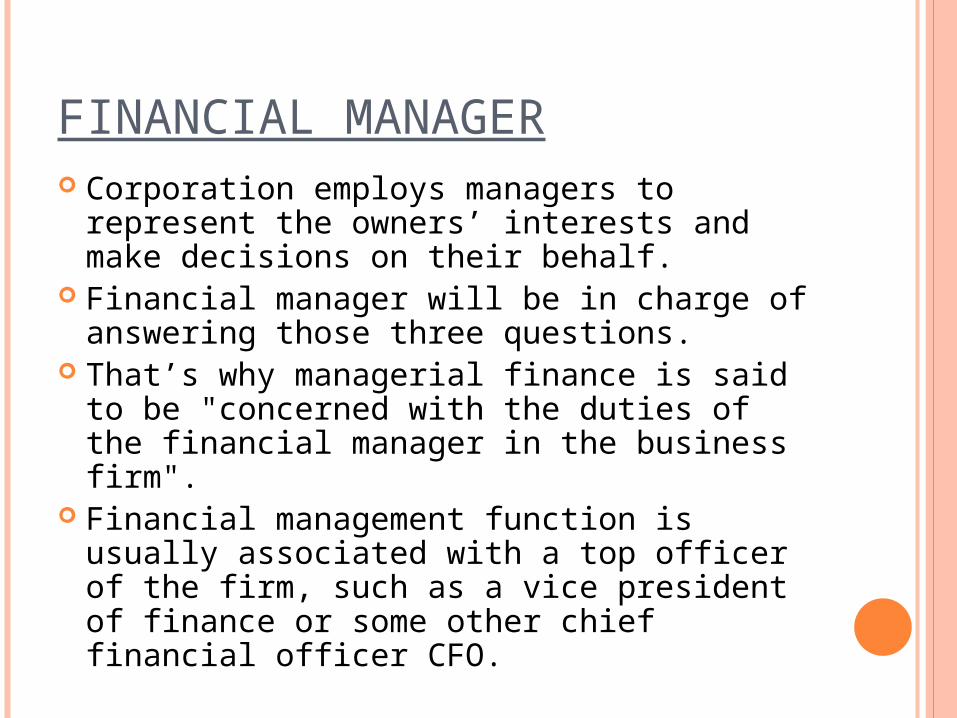

FINANCIAL MANAGER Corporation employs managers to represent

the owners’ interests and make decisions on their behalf.

Financial manager will be in charge of answering those three questions.

That’s why managerial finance is said to be "concerned with the duties of the financial manager in the business firm".

Financial management function is usually associated with a top officer of the firm, such as a vice president of finance or some other chief financial officer CFO.

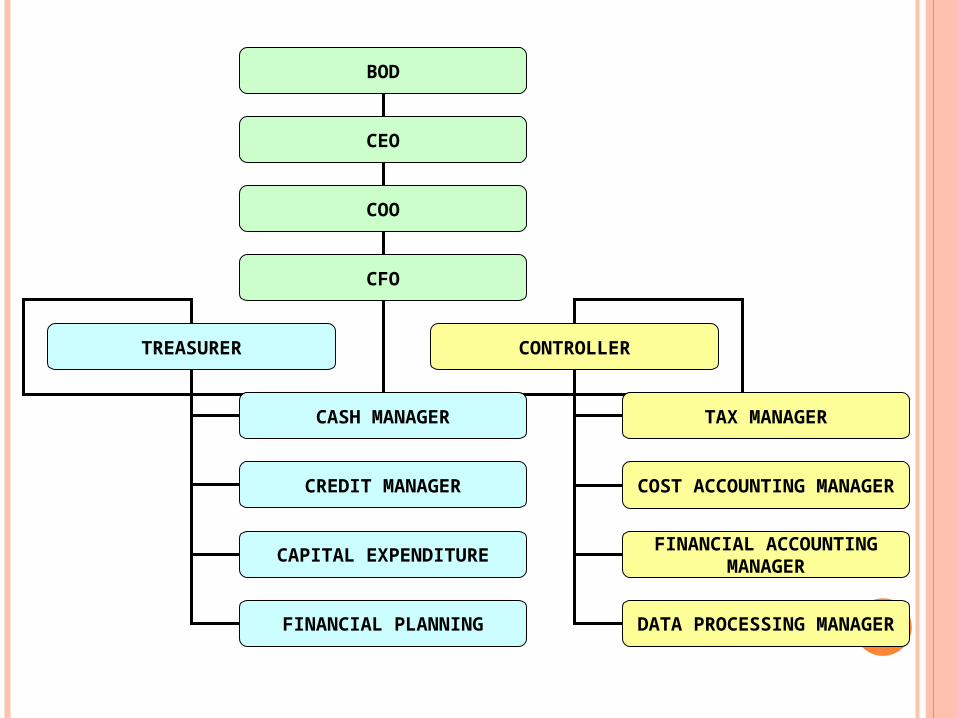

BOD

CEO

COO

CFO

TREASURER CONTROLLER

CASH MANAGER

CREDIT MANAGER

CAPITAL EXPENDITURE

FINANCIAL PLANNING

TAX MANAGER

COST ACCOUNTING MANAGER

FINANCIAL ACCOUNTING MANAGER

DATA PROCESSING MANAGER

FINANCIAL MANAGEMENT DECISIONS1. Investment decisions: long-term

investments.

Capital budgeting decisions. Financial manager tries to identify

investment opportunities that are worth more to the firm than they cost to acquire.

Varies with the nature of business. How much cash they expect to receive,

when they expect to receive it and how likely they are to receive it? Evaluating the size, timing, and risk of future cash flows is the essence of the capital budgeting.

FINANCIAL MANAGEMENT DECISIONS2. Financing Decisions: how to obtain the

long term finance? Ways in which the firm obtain and manages

the long-term financing which it needs to support its long term investments.

Determination of capital structure – the mixture of long-term debt and equity the firm uses to finance its operations.

How much should the firm borrow? Or what should be the mixture of debt and equity? What are the least expensive sources of funds for the firm?

This decision affects, What percentage of firm’s cash flow goes to creditors and what percentage goes to shareholders?

FINANCIAL MANAGEMENT DECISIONS

3. Working capital decisions Concerned with short term assets and liabilities –

cash, inventory, receivables, payables… ensures that the firm has sufficient resources to

continue its operations and avoid costly interruptions.

Level of cash, inventory, … ; Credit policy …; Short term financing … (ST borrowings)

How much cash and inventory should we keep on hand? Should we sell on credit? If so, what terms will we offer, and to whom will we extend them? How will we obtain any needed short-term financing? Will we purchase on credit or will we borrow in the short term and pay cash? If we borrow in the short term, how and where should we do it?

GOALS Survive Avoid financial distress and bankruptcy Beat the competition Maximize the sales or market share Minimize costs Maximize profits Maintain steady earnings growth

The goals involving sales, market share, and cost control all relate, to different ways of earning or increasing profits.

The goals like bankruptcy avoidance, stability and safety, relate in some way to controlling risk.

But these two types of goals are somewhat contradictory. The pursuit of profit normally involves some element of risk, so it isn’t really possible to maximize both safety and profit.

GOAL OF FINANCIAL MANAGEMENT For the profit-oriented businesses, the goals

of financial management are to make money or add value for the owners. Profit maximization would probably be the most commonly cited goal, but even this is not a very precise objective. (controversies: Long run or short run, average or total, accounting net income or earning per share, ….)

GOAL The goal of financial management is to

maximize the current value per share (maximization of shareholder wealth) of the existing stock. They should act in the shareholders’ best interests.

PROFIT MAXIMIZATION VS WEALTH MAXIMIZATIONProfit maximization ... microeconomics … Maximizing

EPS (example) While the goal of profit maximization stresses the

efficient use of capital resources, it assumes away many of the complexities of the real world 1. Timing - timing differences of returns. ...the timeframe over

which profits are to be measured (with in a year or some longer period?)... current profits by cutting down costs like routine maintenance and R&D expenditures

2. Cash flows - profits do not necessarily result in cash flows available to stockholders

3. Risk - alternatives are compared by examining their expected values or weighted average profit. Whether one project is riskier than another! does not enter into these calculations.

Thus a more realistic goal is needed, which we consider to be Maximization of Shareholder Wealth

EXAMPLE

Expected EPS

Investment Year 1 Year 2 Year 3 Total (1-3)

X Rs 1.4 Rs 1 Rs 0.4 Rs 2.8

Y 0.60 1 1.4 3

In terms of the profit maximisation goal, Y would be preferred over X, because it results in higher total EPS over the 3-year period.

<<

PROFIT MAXIMIZATION VS WEALTH MAXIMIZATIONMaximization of shareholder wealth There is no ambiguity in this criterion, and there is

no short-run versus long run issue. We explicitly mean that our goal is to maximize the current stock value.

Stockholders are the residual owners. If the stockholders are winning in the sense that the leftover, residual portion is growing, it must be true that everyone else is winning also.

The challenge is, how to identify those investments and financing arrangements that favorably impact the value of the stock, and this is what the corporate finance deals with. Corporate finance is the study of the relationship between business decisions and the value of the stock in the business.

PROFIT MAXIMIZATION VS WEALTH MAXIMIZATION However, financial manager should not take illegal

or unethical actions in the hope of increasing the value of the equity in the firm.

Financial manager best serves the owners of the business by identifying goods and services that add value to the firm because they are desired and valued in the free market place.

In order to employ this goal, we need not consider every price change to be the worth of our decisions. Other factors, such as changes in the economy, also affect stock prices. What we do focus on, is the effect that our decision should have on the stock price if everything were held constant.

AGENCY PROBLEM The possibility of conflict of interest

between the stockholders and management of a firm.

The relationship between stockholders and management is called an agency relationship. Such a relationship exists whenever someone (the principal) hires another (the agent) to represent his/her interests.

Stockholders/ owners – principal Managers – agents Will management necessarily act in the best

interests of the stockholders? Might not management pursue its own goals at the stockholders’ expense?

AGENCY COST

The term agency costs refers to the costs of the conflict of interest between stockholders and management.

These costs can be indirect or direct. An indirect agency cost is a lost opportunity.

Suppose, the firm is considering a new investment. The new investment is expected to favorably impact the share value, but it is also a relatively risky venture. The owners of the firm will wish to take the investment (because the stock will rise), but management may not because there is the possibility that things will turn out badly and management jobs will be lost. If management does not take the investment, then the stockholders may lose a valuable opportunity. This is one example of indirect agency cost.

Direct agency costs come in two forms. The first type is a corporate expenditure that

benefits management but costs the stockholders. Perhaps the purchase of a luxurious and unneeded corporate jet would fall under this heading.

The second type of direct agency cost is an expense that arises from the need to monitor management actions. Paying outside auditors to assess the accuracy of financial statement information could be one example.

Do managers act in the stockholders’ interest? Two factors: How closely the management goals aligned with

stockholder goals? (managerial Compensation) Can management be replaced if they do not pursue

stockholder goals? (control of the firm) Compensation (economic incentive to increase share

value) Top managerial compensation is tied to financial

performance and often to share value. Managers are frequently given the option to buy stock

at a bargain price. The more the stock is worth, the more valuable is this option.

Job prospects: better performers within the firm will tend to get promoted. More generally, those managers who are successful in pursuing stockholder goals will be in greater demand in the labor market and thus command higher salaries.

Control of the firm Control of the firm ultimately rests with stockholders. They elect

the board of directors, who, in turn, hire and fire management. (An important mechanism by which unhappy stockholders can act to replace existing management is called a proxy fight.)

Another way that management can be replaced is by takeover. Those firms that are poorly managed are more attractive as acquisitions than well-managed firms because a greater profit potential exists. Thus, avoiding a takeover by another firm gives management another incentive to act in the stockholders’ interests.

Even so, often management goals are pursued at the expense of the stockholders, at least temporarily.