Luxury Goods Worldwide Market Study: Spring 2010 Update · Bain Luxury Market Update (April...

15

Luxury Goods Worldwide Market Study: Spring 2010 Update April 16, 2010

Transcript of Luxury Goods Worldwide Market Study: Spring 2010 Update · Bain Luxury Market Update (April...

Luxury Goods Worldwide Market Study: Spring 2010 Update

April 16, 2010

Bain Luxury Market Update (April 16, 2010)

• 2009 was the worst year ever for the luxury market with a -8% decrease

• Results began to improve only at the end of the year, after 3 negative quarters

- Holiday season better than expected- Inventory reduction: end of de-stocking

• The crisis is structurally changing the market- Market is concentrating: larger brands gaining market share- New wave of M&A and IPO operations - No compromise on quality and top-of-mind brands

• Bain forecasts +4% for 2010 (current exchange rates)- Growth spread across all geographies except Japan- Asia and especially China driving growth - All categories recovering after a terrible 2009- Retail becoming more and more important over wholesale- Online channel speeding up its growth

“Tell me the fairytale about the

economy”

2009: Luxury market saw severe shrinking

0

40

80

120

160

€200B

1995

77

1996

84

1997

93

1998

97

1999

109

2000

129

2001

134

2002

133

2003

129

2004

136

2005

147

2006

160

2007

170

2008

166153

Worldwide Luxury Goods Market trend (1995-2009)

2009

CAGR 95-0011%

CAGR 00-041,4%

11% 10% 4% 12% 18% 0% -3%

CAGR:5%

5% 8%

-2%

8%

BOOM (DEMOCRATIZATION)

CONSOLIDATION EXPANSION CRISIS

6%4% -8%

CAGR 04-078%

CAGR 07-09-5%

America and Europe hit hardest, Japan continues its unrelenting decrease

2008

32%

39%

12%

5%

13%

€166B

2009

29%

38%

12%

6%

15%

€153B

Worldwide Luxury Goods Market by Area

-16%

-8,5%

-10%

+10%

-8%

YoY ‘09E vs ‘08

+1%

Americas

Europe

Japan

Asia-Pacific

Rest of World

2008

4%

21%

22%

23%

28%

€166B

2009

4%

19%

24%

24%

27%

€153B

Hard luxury deeply impacted by consumer spending reduction and channel de-stocking

Worldwide Luxury Market by Category

-4,5%

-10,5%

-1,5%

-17%

Accessories

Hard Luxury

Apparel

Perfume and Cosmetics

Art de la table-9%

-8%

YoY ‘09E vs ‘08

Tenth circle: Ladies Shoes

# Brands

30%

50%

18%

220

Luxury Goods Market2009

35%

20%

10%

35%

€153B2%

Crisis is confirming that big is better!

Average brand size

€1,4 B

€0,25 B

€0,8 B

Winners (>+5%)

Neutral (-5/+5%)

Stressed (-15/-5%)

Losers (<-15%)

“I just wanted to say I’ve always been a big fan”

Worldwide luxury market by growth rate ranges

€3,5B

Holiday season showed first signals of recovery

Consumption performance Main Trends (Industry Quotes)

Holiday dollar

-13,0%

-10,0% -10,0%

0,0%

0,0%-3,4% -2,3% -2,6% 0,0%-3,4% -2,3% -2,6%

Luxury Goods Market growth by quarter (2009, QoQ growth)

1Q 2Q 3Q 4QBuild-up of2009 growthBuild-up of2009 growth

“On Christmas Eve we went home with big smiles on our faces.”

“New York's Fifth Avenue, like much of the Northeast, was a wet, sloppy sea of shoppers dodging umbrellas and skipping over puddles to get into gift destinations. ”

“November and December were so strongthat I see them as a harbinger for 2010.”

“It was so busy on our shoe floor that we actually had to close it for awhile to reorganize the assortment. It was a good day, a strong day.”

-8,3%

“Was anyone working? Cyber Monday seen bigger than 2008.”

2010: results to date are very positive

Sell-out 1Q 2010 Sell-in FW 2010

“We are optimistic for FW, and have increased budgets accordingly. Our business is most buoyant in the top-end luxury.”

“We are predicting business will come back strong in the fall. We are seeing the return of our classic customer.”

“FW10 sell-in is around no more than +1% +2%compared to previous year.”

“She is out stimulating the economy –can I take a message?”

• Strong results in first monthsof 2010 for listed players (LVMH, Dior Couture, Tiffany)

• Luxury retail stores show impressive like-for-like growth (+15-20%)

• US department storespositive sell-out trends: +8%in January, +6% in February, +13% in March

• Inventory de-stocking is over

2010 will be the inflection point for the restart of growth

Bain Forecast at 04/16/10

0

50

100

150

€200B

2009

153

2010F

158

+4%

Source: Bain analysis

Main Assumptions

• First semester average market trend shows strong recovery: 5% - 10% across all regions

• Slower growth in second half of the year

By semester

By channel

• Retail L4L sees strong improvement, especially thanks to traffic increase (10% - 15%)

• New openings will remain cautious, mainly driven by expansion in Asiaand Latin America

• Wholesale regaining momentum after 2009; more controlled mark-down campaigns

ESTIMATES

The recovery will be spread across (almost) all geographies and categories

Geographic areas Product categories

Asia Pacific ex-China

China

Source: Bain analysis

Japan

Americas

Europe

RoW

+3% +4%

+4%

-3%

+10%

+15% +0%

+2% +0%

+4% +4%Total

Art de la table

+5%

+2%Perfume and cosmetics

Leather, Shoes &

Accessories

+4%Watches and Jewelry

Apparel

Other

Total

ESTIMATES

Drivers for 2010 recovery have a twofold root

Hard roots Soft roots

• Macroeconomic indicators recovering worldwide, even if at different speeds

- GDP projections for 2010: +4,3%

- Growth driven by China +10%

• Strong urbanization and infrastructure investments in Asia, especially in China

• International passenger traffic increasing by 4.5% in 2010, after a -4.2% in 2009

• Political stability in US enhancing consumer confidence

• Slight decrease of unemploymentrate

• Consumer attitude improving: Confidence Index expected to increase in 2010

• Recovery in footfall and conversion rates

• Boom of e-commerce sales

• Chinese consumers continue to spend heavily in luxury

“I see your consumer confidence remains undeterred”

-20

-15

-10

-5

0

5

10%

Apr

-08

May

-08

Jun-

08

Jul-

08

Aug

-08

Sep

-08

Oct

-08

Nov

-08

Dec

-08

Jan-

09

Feb-

09

Mar

-09

Apr

-09

May

-09

Jun-

09

Jul-

09

Aug

-09

Sep

-09

Oct

-09

Nov

-09

Dec

-09

Jan-

10

Feb-

10

Mar

-10

-20

-15

-10

-5

0

5

10%

Apr

-08

May

-08

Jun-

08

Jul-

08

Aug

-08

Sep

-08

Oct

-08

Nov

-08

Dec

-08

Jan-

09

Feb-

09

Mar

-09

Apr

-09

May

-09

Jun-

09

Jul-

09

Aug

-09

Sep

-09

Oct

-09

Nov

-09

Dec

-09

Feb-

10

Jan-1

0 -20

-15

-10

-5

0

5

10%

Apr

-08

May

-08

Jun-

08

Jul-08

Aug

-08

Sep

-08

Oct

-08

Nov

-08

Dec

-08

Jan-

09

Feb-

09

Mar

-09

Apr

-09

May

-09

Jun-

09

Jul-09

Aug

-09

Sep

-09

Oct

-09

Nov

-09

Dec

-09

Jan-

10

Feb-

10

-40

-35

-30

-25

-20

-15

-10

-5

0

5

10%

Apr

-08

May

-08

Jun-

08

Jul-

08

Aug

-08

Sep

-08

Oct

-08

Nov

-08

Dec

-08

Jan-

09

Feb-

09

Mar

-09

Apr

-09

May

-09

Jun-

09

Jul-

09

Aug

-09

Sep

-09

Oct

-09

Nov

-09

Dec

-09

Jan-

10

Feb-

10

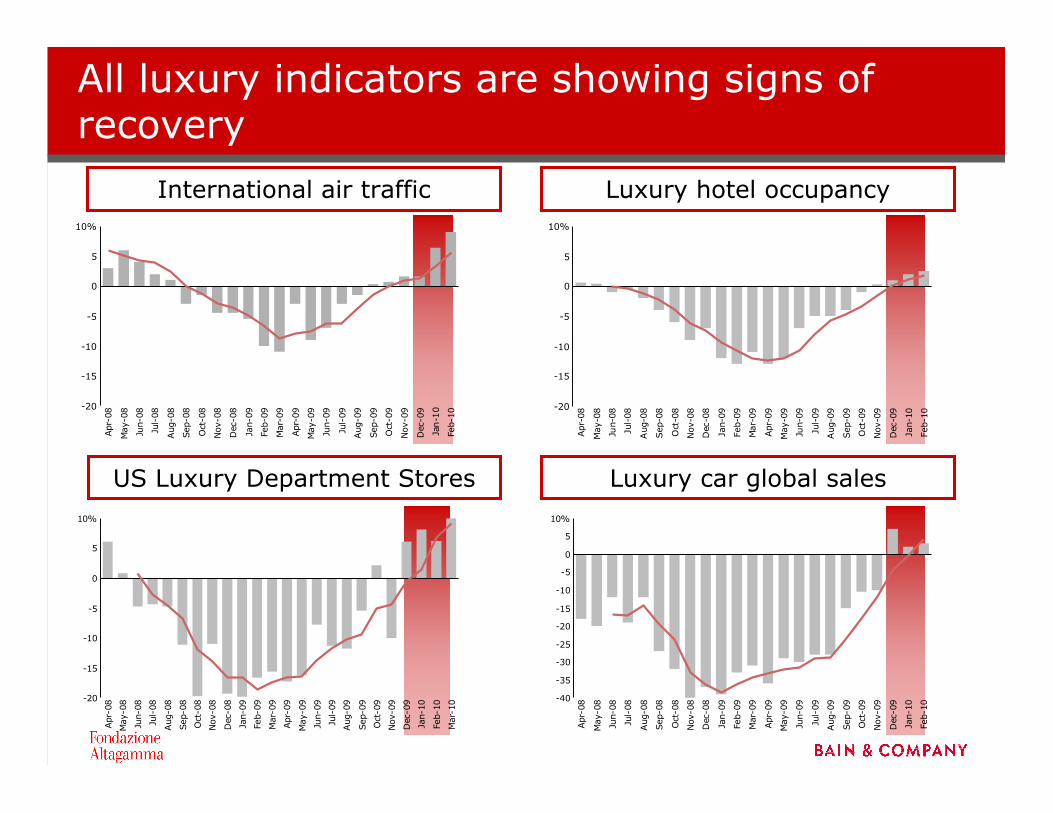

All luxury indicators are showing signs of recovery

International air traffic

US Luxury Department Stores

Luxury hotel occupancy

Luxury car global sales

The good news: consumers are shopping again!

• Recovery in footfall andconversion rates thanks to marketing and promotional activities

• End of luxury shame for local consumers in mature markets: luxury brands are gaining appeal again

• Asia “optimism”boosted Europeand US market as well: consumers are spending heavily abroad

• New channels are bringing vitality to luxury environment:online sales booming!

“Most successful suit sale we ever had, I

should say”

“She’ll have to get back to you- she’s off

shopping now”

“New timetable... all in Cantonese!”

“Post-war” we are assisting to some structural changes in the market

Competition• Polarization and concentration...

-Mega-brands taking share-Failures and bankruptcies (but brands do not disappear)-Restart of M&A activity and IPOs-Acceleration in generational shifts and managerialization

• ...but consumers always want and need newness

Channels• Retail overperforming wholesale but not still at full potential• Concentration of wholesale distribution • Strategic rethinking of Department Stores formats• New opportunities from web and digitalization of experience

Consumer behaviour

• Increasing attention for value for money but new and diverse value drivers:

-Cheap & chic not still at full potential-Customization widely spread across categories and products-Customer experience and service-Innovation -Need to “justify” the premium price... brand is not enough

• Huge consumer diversity along all segmentation axes

Geography• Asia becoming the key market• Chinese consumers driving global market growth• Japan structurally deflating

Strategic pay-offs going forward!

Year of the Tiger

Breakfast @ Tiffany.com

Store sweet store!

Because they are worth it!

Winners take it all