Low Carbon Fuel Standard (LCFS) Analysis … · Low Carbon Fuel Standard (LCFS) Analysis &...

24

Low Carbon Fuel Standard (LCFS) Analysis & Compliance Costs Role of Alternative Fuels in California’ s Role of Alternative Fuels in California s Transportation Energy Future Transportation Committee Workshop November 14, 2011 Gordon Schremp F l dT t ti Di i i Fuels andT ransportation Division California Energy Commission [email protected]

Transcript of Low Carbon Fuel Standard (LCFS) Analysis … · Low Carbon Fuel Standard (LCFS) Analysis &...

Low Carbon Fuel Standard (LCFS) Analysis & Compliance Costs

Role of Alternative Fuels in California’sRole of Alternative Fuels in California s Transportation Energy Future

Transportation Committee Workshop

November 14, 2011

Gordon Schremp

F l d T t ti Di i iFuels and Transportation Division

California Energy Commission

LCFS Compliance Analysis

• Primary intent of this continuation analysis is to evaluate compliance feasibility using various types of biofuels & costs– This scenario analysis should not be considered a forecast– This scenario analysis should not be considered a forecast

• Three cases with varying assumptions– Availability of low carbon intensity fuels increased with each case

M t bi f l tl il bl i i l titi– Most biofuels are currently available in commercial quantities– Only exceptions cellulosic biofuels, especially BTL gasoline

• Biofuel costs are introduced in the analysis– Biofuel selection based on least‐cost, lowest carbon intensity fuels

• Adjustment for biodiesel NOx mitigation– Biodiesel use above 5 percent mitigated with renewable dieselp g

• Primary concern is plausibility of the assumptions

11/14/2011 2

LCFS Analysis – Common Assumptions

• Biofuels with least‐cost, lowest carbon intensity selected first• Development of excess LCFS credits minimized to align with

b h i f i i d l2011 behavior of participants and LRT results• Portion of LCFS credits generated each year are not used in

subsequent years – retained by parties in anticipation of rising q y y p p gvalue– Non‐obligated parties retain larger portion of LCFS credits compared to

obligated parties – electricity and natural gas creditsobligated parties electricity and natural gas credits– Portion of withheld credits diminishes to zero by 2020 – when highest

value of LCFS credits is assumed to be reached in the excess credit market

– No adjustment made to exclude a portion of LCFS credits that have already been generated but my be voided due to use of high carbon intensity crude oil by some obligated parties (refiners) – quantity not known

11/14/2011 3

LCFS Analysis – Case 3 Assumptions

• Cellulosic fuel availability increased to 50 percent of U.S. supply• Brazilian ethanol supply availability increased to 1.5 billion

ll b i i i lgallons beginning in 2014 – lowest CI type• Renewable diesel fuel supply availability

– Raised to 50 percent of U.S. supply by 2017 – 219 million gallons– Carbon intensity of 19.65 gCO2e/MJ

• Biodiesel from corn oil– Raised to 50 percent of U.S. supply by 2017 – 160 million gallonsRaised to 50 percent of U.S. supply by 2017 160 million gallons– Carbon intensity of 5.90 gCO2e/MJ

• Biodiesel from used cooking oilRaised to 200 percent of registered facilities by 2017 155 million– Raised to 200 percent of registered facilities by 2017 – 155 million gallons

– Carbon intensity of 11.76 gCO2e/MJ

11/14/2011 4

7 000

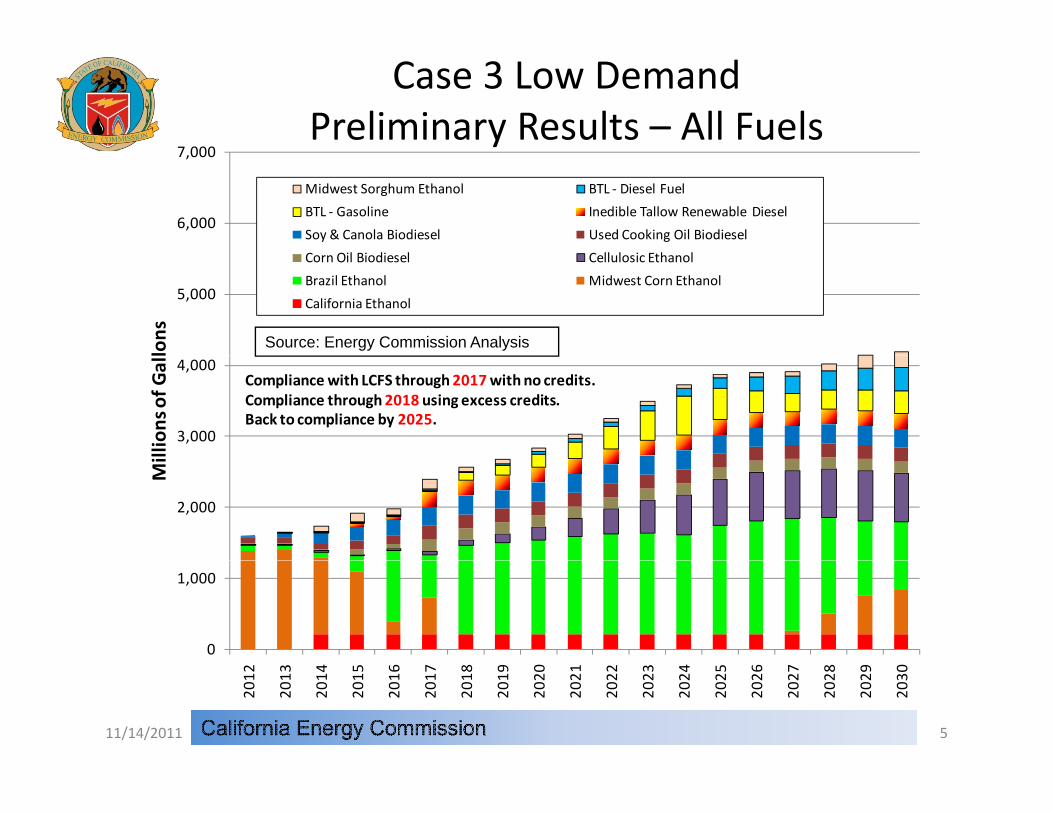

Case 3 Low DemandPreliminary Results – All Fuels

6,000

7,000

Midwest Sorghum Ethanol BTL ‐ Diesel Fuel

BTL ‐ Gasoline Inedible Tallow Renewable Diesel

Soy & Canola Biodiesel Used Cooking Oil Biodiesel

C Oil Bi di l C ll l i E h l

5,000

lons

Corn Oil Biodiesel Cellulosic Ethanol

Brazil Ethanol Midwest Corn Ethanol

California Ethanol

Source: Energy Commission Analysis

3,000

4,000

llion

s of G

all

Compliance with LCFS through2017 with no credits.Compliance through2018 using excess credits.Back to compliance by 2025.

2,000

Mi

0

1,000

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

11/14/2011 5

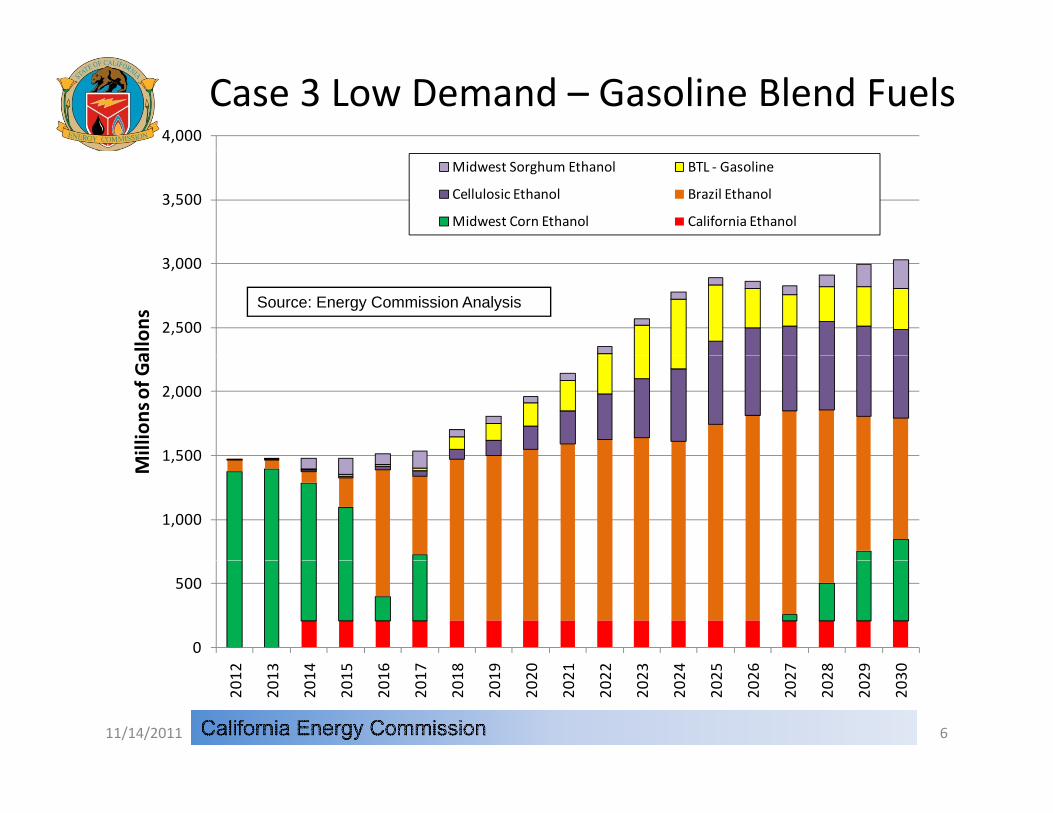

4,000

Case 3 Low Demand – Gasoline Blend Fuels

3,500

Midwest Sorghum Ethanol BTL ‐ Gasoline

Cellulosic Ethanol Brazil Ethanol

Midwest Corn Ethanol California Ethanol

2,500

3,000

allons

Source: Energy Commission Analysis

1 500

2,000

Millions of G

a

1,000

1,500

M

0

500

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

11/14/2011 6

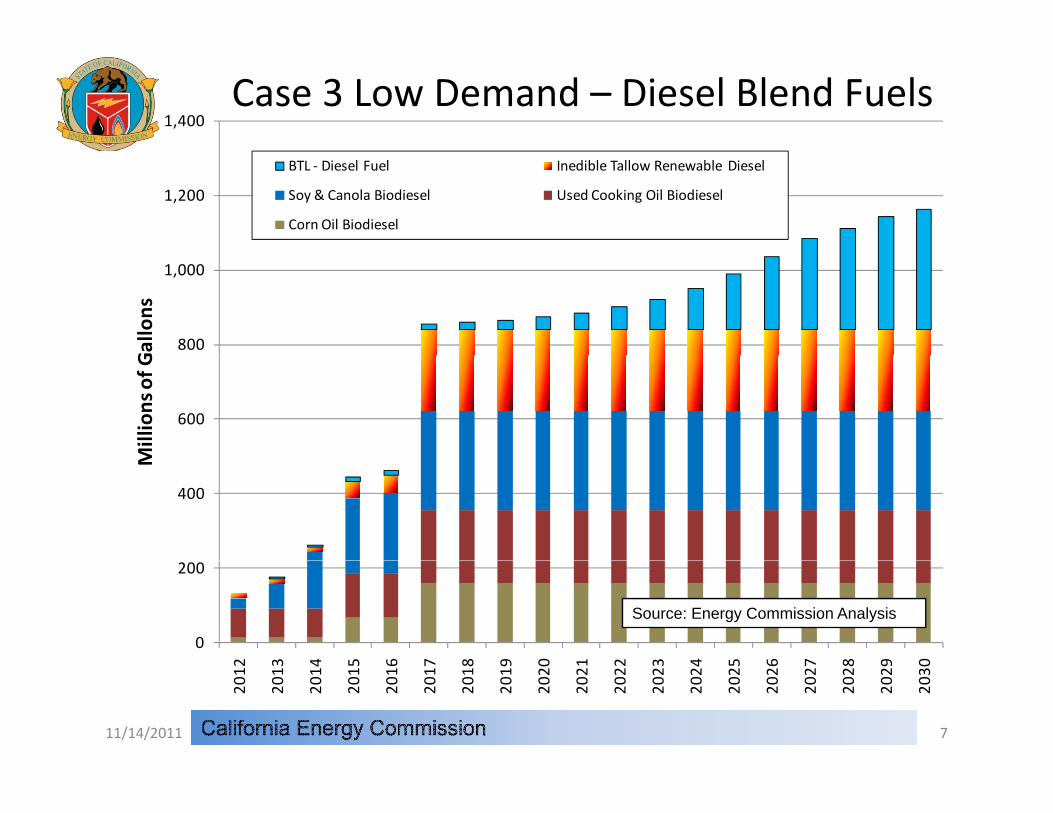

1,400Case 3 Low Demand – Diesel Blend Fuels

1,200

BTL ‐ Diesel Fuel Inedible Tallow Renewable Diesel

Soy & Canola Biodiesel Used Cooking Oil Biodiesel

Corn Oil Biodiesel

800

1,000

Gallons

600

Millions of G

400

M

0

200

2 3 4 5 6 7 8 9 0 1 2 3 4 5 6 7 8 9 0

Source: Energy Commission Analysis

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

11/14/2011 7

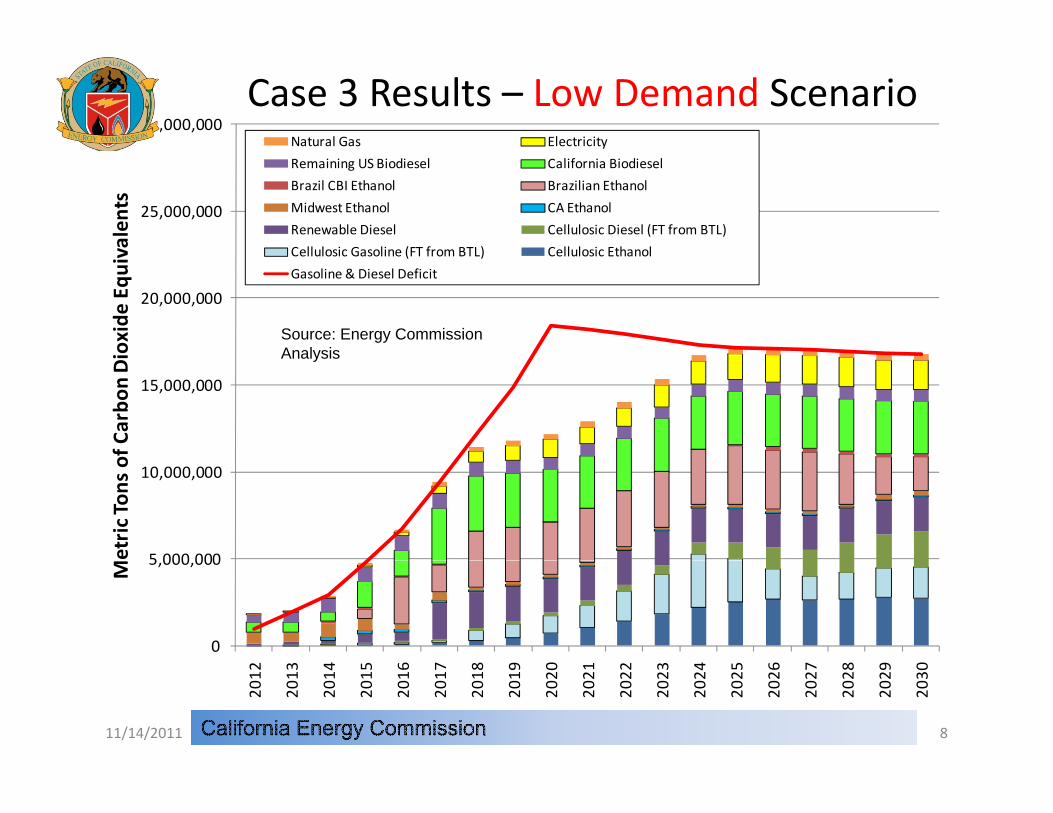

30,000,000Natural Gas Electricity

Case 3 Results – Low Demand Scenario

25,000,000

valents

Remaining US Biodiesel California Biodiesel

Brazil CBI Ethanol Brazilian Ethanol

Midwest Ethanol CA Ethanol

Renewable Diesel Cellulosic Diesel (FT from BTL)

Cellulosic Gasoline (FT from BTL) Cellulosic Ethanol

20,000,000

ioxide

Equ

iv Cellulosic Gasoline (FT from BTL) Cellulosic Ethanol

Gasoline & Diesel Deficit

Source: Energy Commission Analysis

15,000,000

of Carbo

n Di Analysis

5 000 000

10,000,000

etric Tons o

0

5,000,000

2 3 4 5 6 7 8 9 0 1 2 3 4 5 6 7 8 9 0

M

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

11/14/2011 8

30,000,000Natural Gas Electricity

Case 3 Results – High Demand Scenario

25,000,000

alen

tsNatural Gas ElectricityRemaining US Biodiesel California BiodieselBrazil CBI Ethanol Brazilian EthanolMidwest Ethanol CA EthanolRenewable Diesel Cellulosic Diesel (FT from BTL)Cellulosic Gasoline (FT from BTL) Cellulosic Ethanol

20,000,000

oxide Eq

uiva Gasoline & Diesel Deficit

Source: Energy Commission Analysis

15,000,000

of Carbo

n Dio Analysis

5 000 000

10,000,000

Metric Tons o

0

5,000,000

2 3 4 5 6 7 8 9 0 1 2 3 4 5 6 7 8 9 0

M

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

11/14/2011 9

Case 3 – Demand Observations

• Compliance until 2017 through increased use of cellulosic fuels• Excess credits can extend compliance an additional years (2018)

– Due to increased supply of renewable diesel and corn oil biodiesel

• Compliance through deficit portion of the Low Demand forecast period (2019‐2024) would require generation of additional credits from:– Use of additional quantities of drop‐in biofuels greater than 50 percent of

total U.S. supplypp y• Biomass‐to‐liquids (BTL) gasoline and diesel

• Deficit portion of the forecast period (2019‐2027) under the High Demand scenario would require even greater generation ofHigh Demand scenario would require even greater generation of additional credits

11/14/2011 10

Case 3 – Additional Concerns

• Heavy dependence on Brazilian ethanol lessens somewhat– Similar to previous cases

• Biodiesel use would need to rapidly increase to B5– Similar to previous cases– Feasibility of corn oil biodiesel supply increase in 2017 uncertain

• Use of renewable diesel significantly increased– Feasibility of supply increase to 219 million gallons in 2017 uncertain

• Use of cellulosic fuels significantly increased beginning in 2018Use of cellulosic fuels significantly increased beginning in 2018– Feasibility of using half of the U.S. cellulosic fuel supply questionable,

even if the volumes forecast by EIA actually become available

11/14/2011 11

More Expensive Biofuels

• Previous LCFS analysis by Energy Commission staff did not incorporate costs of biofuels but recognized that severalincorporate costs of biofuels but recognized that several different types of biofuels selected for use in the cases are currently more expensive than corn‐based ethanolSt ff d l d bi f l i f LCFS l i• Staff developed biofuel prices for LCFS analysis

• Used recent historical values as starting point– Near‐term pricing information

• Brazilian ethanol as one example

– Federal RFS2 RIN values during 2010 & 2011• Biodiesel

C ll l i th l• Cellulosic ethanol• Advanced biofuels

11/14/2011 12

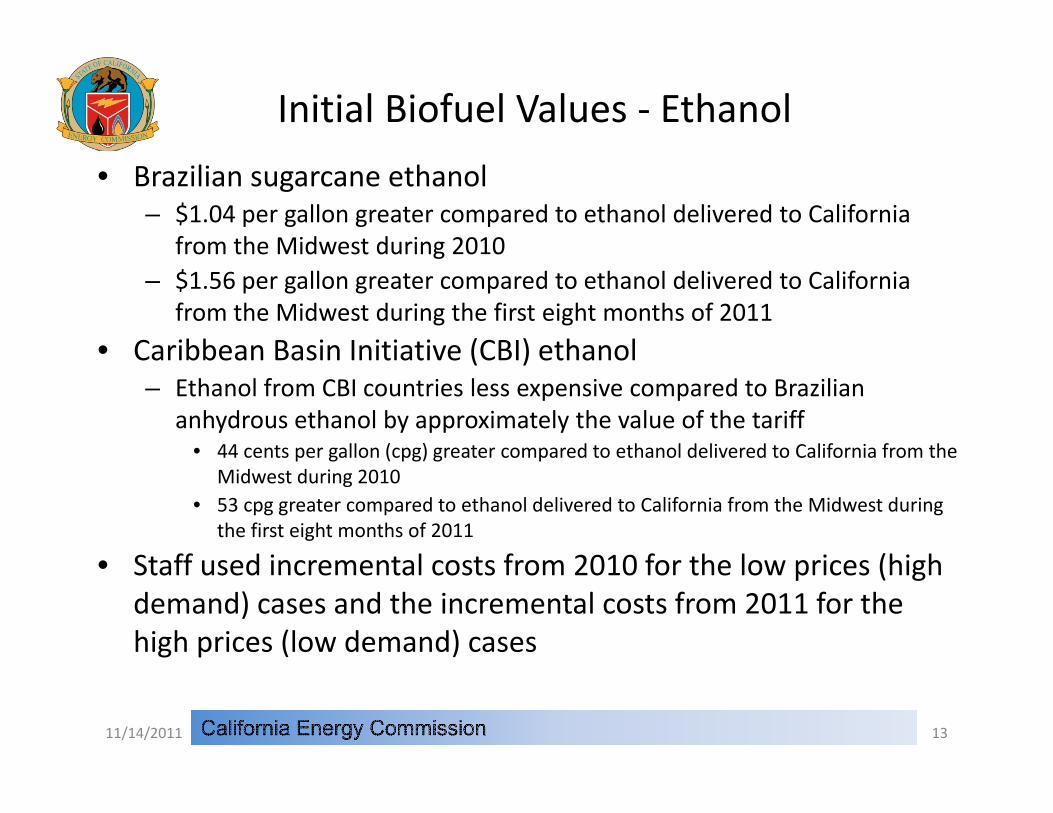

Initial Biofuel Values ‐ Ethanol

• Brazilian sugarcane ethanol – $1.04 per gallon greater compared to ethanol delivered to California

from the Midwest during 2010from the Midwest during 2010– $1.56 per gallon greater compared to ethanol delivered to California

from the Midwest during the first eight months of 2011

• Caribbean Basin Initiative (CBI) ethanolCaribbean Basin Initiative (CBI) ethanol– Ethanol from CBI countries less expensive compared to Brazilian

anhydrous ethanol by approximately the value of the tariff• 44 cents per gallon (cpg) greater compared to ethanol delivered to California from the p g ( pg) g p

Midwest during 2010• 53 cpg greater compared to ethanol delivered to California from the Midwest during

the first eight months of 2011

• Staff used incremental costs from 2010 for the low prices (high• Staff used incremental costs from 2010 for the low prices (high demand) cases and the incremental costs from 2011 for the high prices (low demand) cases

11/14/2011 13

Initial Biofuel Values ‐ Biodiesel

• Biodiesel from soybean oil– Calculated as a premium to wholesale diesel fuel

• Used RIN values multiplied by 1.5p y

• Renewable Identification Number (RIN) credit values– 42 cents per gallon (cpg) for biomass‐based diesel during 2010– 124 cpg for biomass‐based diesel during the first eight months of 2011124 cpg for biomass based diesel during the first eight months of 2011

• Applied 1.5 multiplier to wholesale diesel– $2.88 per gallon calculated biodiesel price for 2010 based on average

$2 25 per gallon CARB diesel wholesale value$2.25 per gallon CARB diesel wholesale value– $4.94per gallon calculated biodiesel price during the first eight months

of 2011 based on an average $3.08 per gallon CARB diesel wholesale valuevalue

• Staff used values from 2010 for the low prices (high demand) cases and the values from 2011 for the high prices (low d d)demand) cases

11/14/2011 14

Initial Biofuel Values – Cellulosic Ethanol

• Cellulosic ethanol prices were derived due to lack of historical data– Calculated as a RIN premium to Brazilian ethanol– Calculated as a RIN premium to Brazilian ethanol

• Renewable Identification Number (RIN) credit values– 30 cents per gallon (cpg) for cellulosic biofuels during 2010

100 f ll l i bi f l d i th fi t i ht th f 2011– 100 cpg for cellulosic biofuels during the first eight months of 2011

• Applied these RIN values as premium to Brazilian ethanol– $2.86 per gallon calculated cellulosic ethanol price for 2010 based on

average $2.56 per gallon Brazilian ethanol value– $4.87per gallon calculated cellulosic ethanol price during the first eight

months of 2011 based on an average $3.87 per gallon Brazilian ethanol lvalue

• Staff used values from 2010 for the low prices (high demand) cases and the values from 2011 for the high prices (low demand) cases

11/14/2011 15

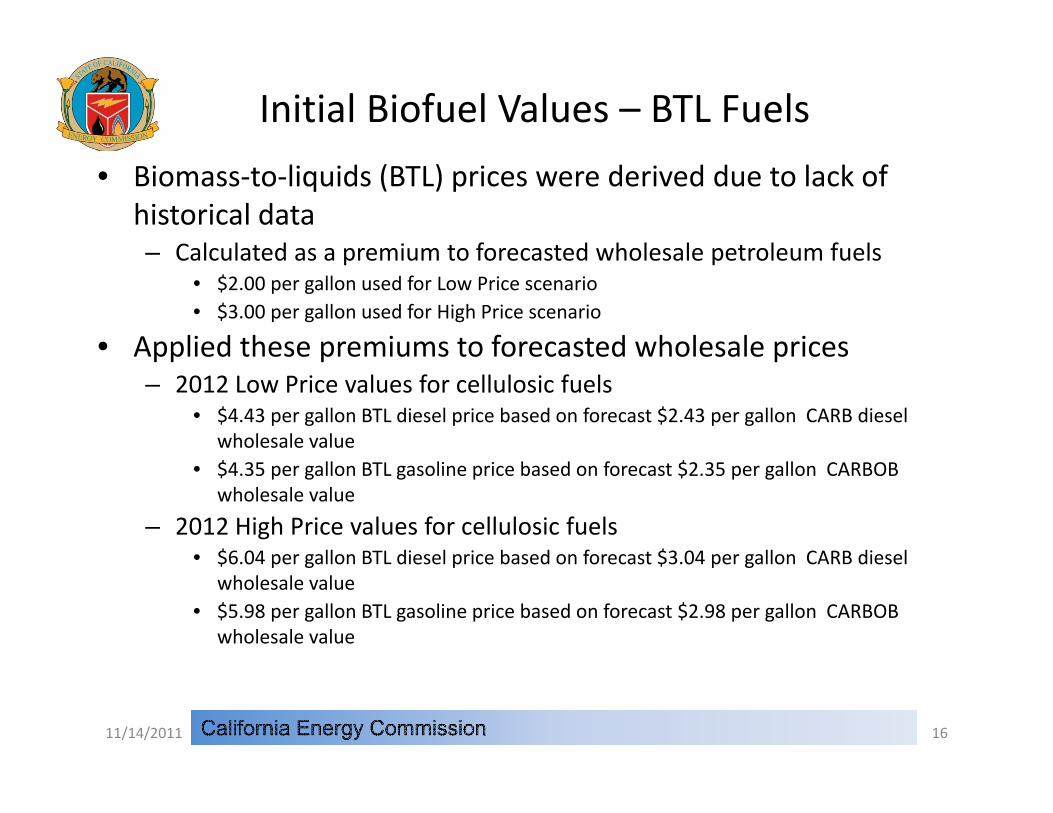

Initial Biofuel Values – BTL Fuels

• Biomass‐to‐liquids (BTL) prices were derived due to lack of historical data– Calculated as a premium to forecasted wholesale petroleum fuels– Calculated as a premium to forecasted wholesale petroleum fuels

• $2.00 per gallon used for Low Price scenario• $3.00 per gallon used for High Price scenario

• Applied these premiums to forecasted wholesale pricesApplied these premiums to forecasted wholesale prices– 2012 Low Price values for cellulosic fuels

• $4.43 per gallon BTL diesel price based on forecast $2.43 per gallon CARB diesel wholesale value

• $4.35 per gallon BTL gasoline price based on forecast $2.35 per gallon CARBOB wholesale value

– 2012 High Price values for cellulosic fuels• $6 04 per gallon BTL diesel price based on forecast $3 04 per gallon CARB diesel$6.04 per gallon BTL diesel price based on forecast $3.04 per gallon CARB diesel

wholesale value• $5.98 per gallon BTL gasoline price based on forecast $2.98 per gallon CARBOB

wholesale value

11/14/2011 16

700

2012 Fuel Prices – No CI Adjustment

600

Low Price ‐ High Demand Scenario

High Price ‐ Low Demand Scenario

Source: Energy Commission Analysis

400

500

Gallon

300

Cents P

er G

100

200

0

RFG Ex

ax Diesel

Tax

dwest

ybean

odiesel

dwest

hano

l

CBI

arcane

hano

l

zilian

arcane

hano

l

lulosic

hano

l

lulosic

soline

lulosic

iesel

Rack R Ta

CARB

Ex T

Mid

Soy

Bio

Mi

Et CSuga Eth

Bra

Sug a Eth

Cell

Eth

Cell

Gas

Cell D

11/14/2011 17

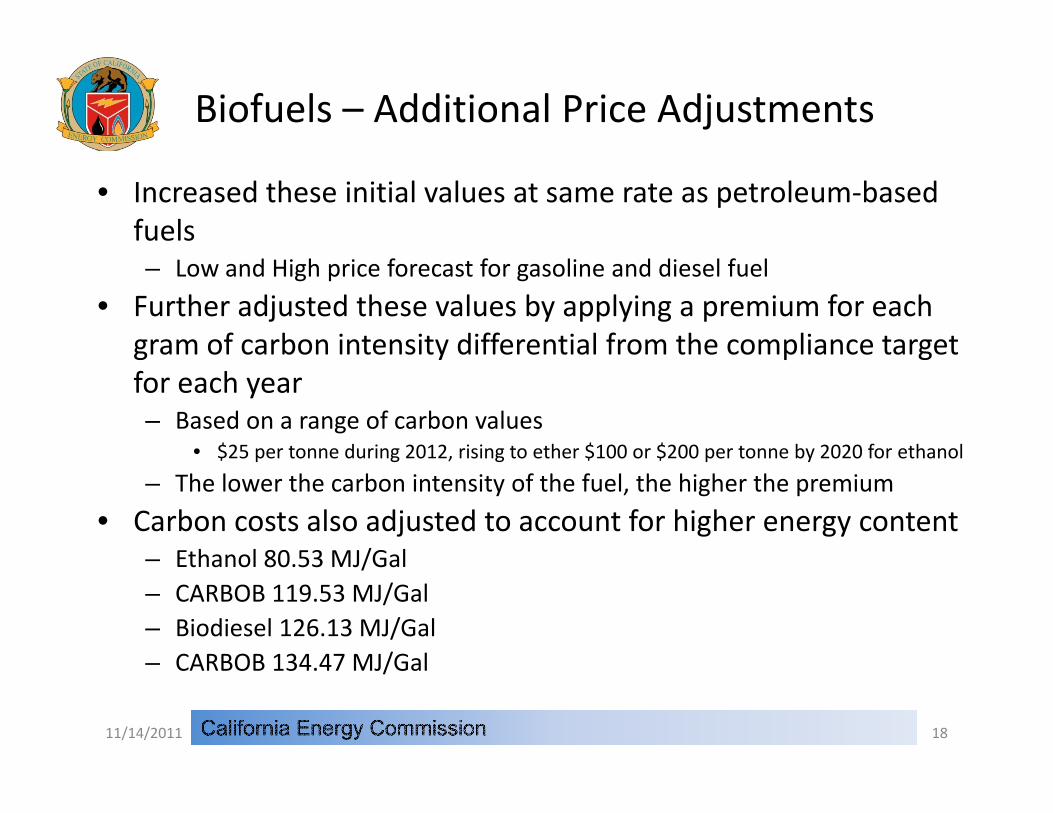

Biofuels – Additional Price Adjustments

• Increased these initial values at same rate as petroleum‐based fuels– Low and High price forecast for gasoline and diesel fuel

• Further adjusted these values by applying a premium for each gram of carbon intensity differential from the compliance target g y p gfor each year– Based on a range of carbon values

• $25 per tonne during 2012, rising to ether $100 or $200 per tonne by 2020 for ethanol$25 per tonne during 2012, rising to ether $100 or $200 per tonne by 2020 for ethanol

– The lower the carbon intensity of the fuel, the higher the premium

• Carbon costs also adjusted to account for higher energy content– Ethanol 80 53 MJ/Gal– Ethanol 80.53 MJ/Gal– CARBOB 119.53 MJ/Gal– Biodiesel 126.13 MJ/Gal– CARBOB 134 47 MJ/Gal– CARBOB 134.47 MJ/Gal

11/14/2011 18

600CornOil Biodiesel (5.90 grams)

CI Premium Adjustment – Diesel SubstitutesSource: Energy Commission Analysis

500

Corn Oil Biodiesel (5.90 grams)

UCO ‐No Cooking Biodiesel (11.76 grams)

Inedible Tallow Renewable Diesel (19.65 grams)

Cellulosic Diesel Fuel (37.20 grams)

Source: Energy Commission Analysis

400

llon

NA Canola Oil Biodiesel (62.99 grams)

Midwest Soybean Biodiesel (83.25 grams)

Premium to CARB diesel

300

ents Per Ga

200

Ce

100

02012 2015 2020

11/14/2011 19

600

CI Premium Adjustment – Gasoline Substitutes

500

BTL Gasoline (37.20 grams)

Cellulosic Ethanol (37.20 grams)

Brazil Anhydrous Ethanol ‐ Cogen + Mechanized Harvest (58.40 grams)

Brazil Hydrous Ethanol ‐ CBI El Salvador (58.40 grams)

il h d h l ( )

400

on

Brazil Anhydrous Ethanol ‐ Cogen (66.40 grams)

Brazil Anhydrous Ethanol ‐ Average (73.40 grams)

Premium to CARBOB

200

300

ts Per Gallo

100

200

Cent

02012 2015 2020

‐100Source: Energy Commission Analysis

11/14/2011 20

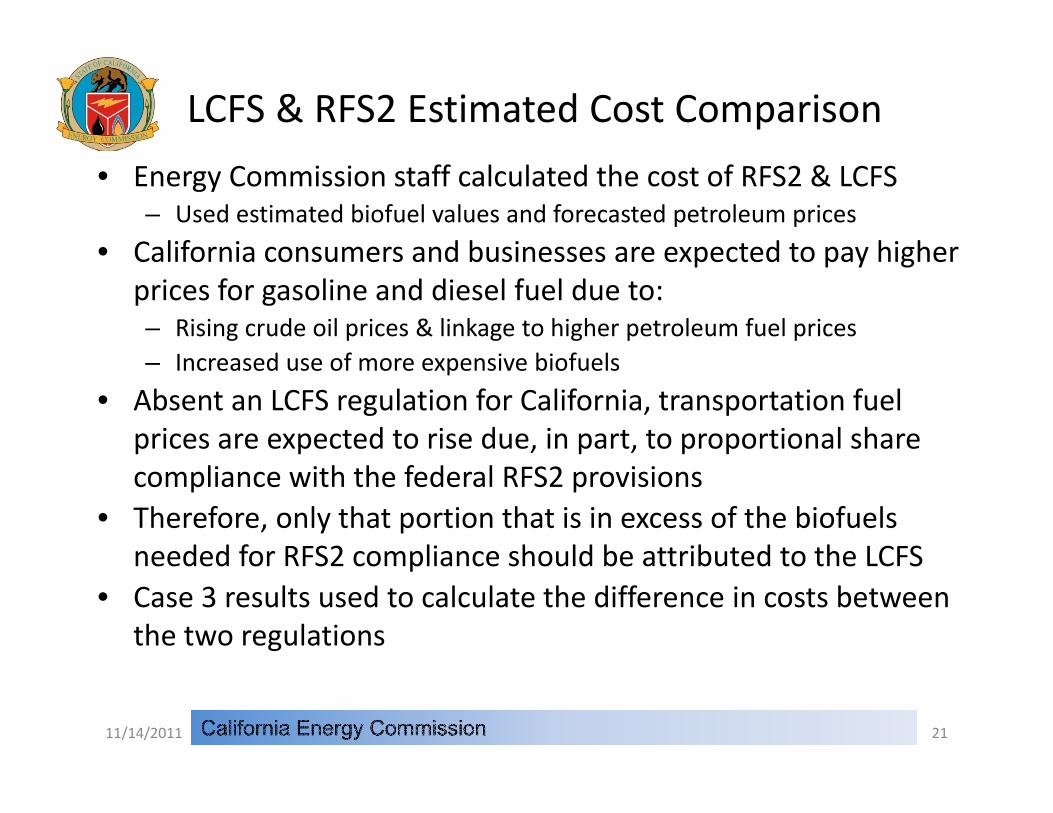

LCFS & RFS2 Estimated Cost Comparison

• Energy Commission staff calculated the cost of RFS2 & LCFS– Used estimated biofuel values and forecasted petroleum prices

• California consumers and businesses are expected to pay higher• California consumers and businesses are expected to pay higher prices for gasoline and diesel fuel due to:– Rising crude oil prices & linkage to higher petroleum fuel prices

I d f i bi f l– Increased use of more expensive biofuels

• Absent an LCFS regulation for California, transportation fuel prices are expected to rise due, in part, to proportional share compliance with the federal RFS2 provisions

• Therefore, only that portion that is in excess of the biofuels needed for RFS2 compliance should be attributed to the LCFSneeded for RFS2 compliance should be attributed to the LCFS

• Case 3 results used to calculate the difference in costs between the two regulations

11/14/2011 21

Case 3 Low Demand – LCFS less RFS2Preliminary Initial Results

10,000

y

Energy Commission staff will continue to work with Air Board t ff th d l f d

6 000

8,000 staff on methodology for and prices used in calculating these regulatory compliance differences

4,000

6,000

s of D

ollars

Low CI ‐ High Price ‐ Low Demand

d e e ces

2,000Millions

Source: Energy Commission Analysis

0

012

013

014

015

016

017

018

019

020

021

022

023

024

025

026

027

028

029

030

‐2,000

20 20 20 20 20 20 20 20 20 20 20 20 20 20 20 20 20 20 20

11/14/2011 22

Continuing Efforts

• Energy Commission staff will continue to analyze LCFS compliance cases, including:– New compliance targets proposed by the Air Resources Board in

response to revised high carbon intensity crude oil provisions– Additional sensitivities suggested during today’s workshop or detailed in

subsequent comments– More detailed assessment of the differences between Energy

Commission and Air Resources Board respective LCFS compliance l ianalysis

• This additional LCFS analysis will be published in the Final Staff Report

11/14/2011 23

LCFS Outside of California

• 22 other states are developing or considering adoption of LCFS programs similar to California

• The incremental demand for the same type of biofuels used to comply with California’s LCFS program that would result if any other region of the United States carried out implementation ofother region of the United States carried out implementation of an LCFS‐like program would, at a minimum, increase competition and raise the market‐clearing prices of these biof elsbiofuels

• States considering implementation of LCFS‐like regulations equate to 3.7 times the quantity of gasoline consumed in California and 7.2 times the quantity of diesel fuel consumed in California during 2009

11/14/2011 24