Looking Ahead: Financial Reporting Ottawa Finance Team Meeting November 3, 2010 Sheraton Hotel 150...

65

Looking Ahead: Financial Reporting Ottawa Finance Team Meeting November 3, 2010 Sheraton Hotel 150 Albert Street, Ottawa O’Connor Room

-

Upload

emily-kelly -

Category

Documents

-

view

215 -

download

0

Transcript of Looking Ahead: Financial Reporting Ottawa Finance Team Meeting November 3, 2010 Sheraton Hotel 150...

Looking Ahead: Financial Reporting

Ottawa Finance Team MeetingNovember 3, 2010

Sheraton Hotel

150 Albert Street, Ottawa

O’Connor Room

- 2 -- 2 -

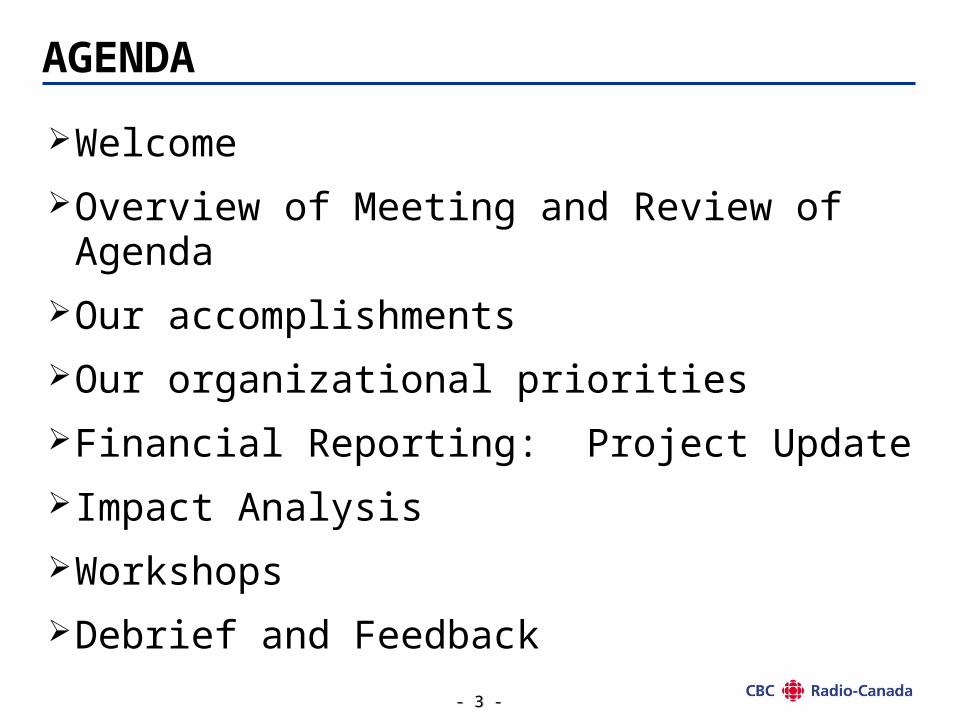

Agenda

- 3 -- 3 -

AGENDA

Welcome

Overview of Meeting and Review of Agenda

Our accomplishments

Our organizational priorities

Financial Reporting: Project Update

Impact Analysis

Workshops

Debrief and Feedback

- 4 -- 4 -

FINANCE AND IT ORGANIZATION

- 5 -- 5 -

Our Achievements

Roles and ResponsibilitiesAchievementsOngoing Activities

- 6 -- 6 -

Finance and Administration

- 7 -- 7 -

Corporate Controller

- 8 -- 8 -

Capital Process and Portfolio Management

- 9 -- 9 -

Supply Management Services

- 10 -- 10 -

Our Mission is to provide CBC/Radio-Canada with the goods and services required for its operations at the

most advantageous price and through the most effective process

Our Vision is for CBC/Radio-Canada to be recognized as an organization that procures its goods and services

through an open, fair and transparent process and ensures that best value is realized

Supply Management Services

- 11 -- 11 -

Who we are:Who we are:

Part of Corporate Finance & Administration, located in Ottawa, Montreal & Toronto, the Supply Management team consists of:

• Strategic Sourcing

• Procurement

• Program Management

• Travel Management

• Fleet Management

• Other Corporate Agreements

Supply Management Services

- 12 -- 12 -

Jeanne BuithieuStrategic Sourcing

Manager

Mario GionetCorporate Fleet

Manager

Richard WiebeStrategic Sourcing

Manager & Team Lead

James CoulmanStrategic Sourcing

Manager

Pauline ValiquetteCorporate Travel

Manager

Philippe Audet-LapointeSenior Director Supply Management

Lynda GreavesProcurement Officer

Manon LacombeProcurement Officer

Newsha Neishaboory

Procurement Officer

France BinetteStrategic Sourcing

Manager & Team Lead

Normand BussieresProcurement Officer

Carole HebertProcurement Officer

Janice PrymakStrategic Sourcing

Officer

Ferdinand Sison *Procurement Officer

Daisy Wong *Procurement Officer

Travis JanzenProcurement Officer

Ana ChangAdmin Assistant

Alicia GuilmetteProcurement Officer

* Contract Position replacing either Marija Kuran or Vince Colozza or Ami Adi Goshi

Supply ManagementSept, 2010

Helene Varin **Admin Assistant

** Contract Position Cellular Transition

Supply Management Services

- 13 -- 13 -

In 2009-2010In 2009-2010: :

20,800 purchase orders were issued to our 10,000 current supplier base

80% of our spend was with 5% of our suppliers

80% of our suppliers received 1 or 2 P/Os

35% of our procurement is done using purchase orders

43% of the purchase orders issued were below 100$

89% of the purchase orders issued were below 5000$

A few numbers…

- 14 -- 14 -

Key Challenges & Implications

• Increasing pressure from suppliers to increase prices

• Changing Technology

• Providing fuel for sustainability and making every dollar count

• We need to team together to create a sustainable, competitive base for CBC while achieving cost containment / reduction objectives

We need to balance stakeholder relationships with the best total cost of ownership

Key Challenges for CBC Radio-Canada

Key Challenges for CBC Radio-Canada

Implications for SMSand Stakeholders

Implications for SMSand Stakeholders

- 15 -- 15 -

Supply Management Intranet Site

- 16 -- 16 -

French Services

- 17 -- 17 -

English Services

- 18 -- 18 -

Who We Are.

What We Do.

- 19 -- 19 -

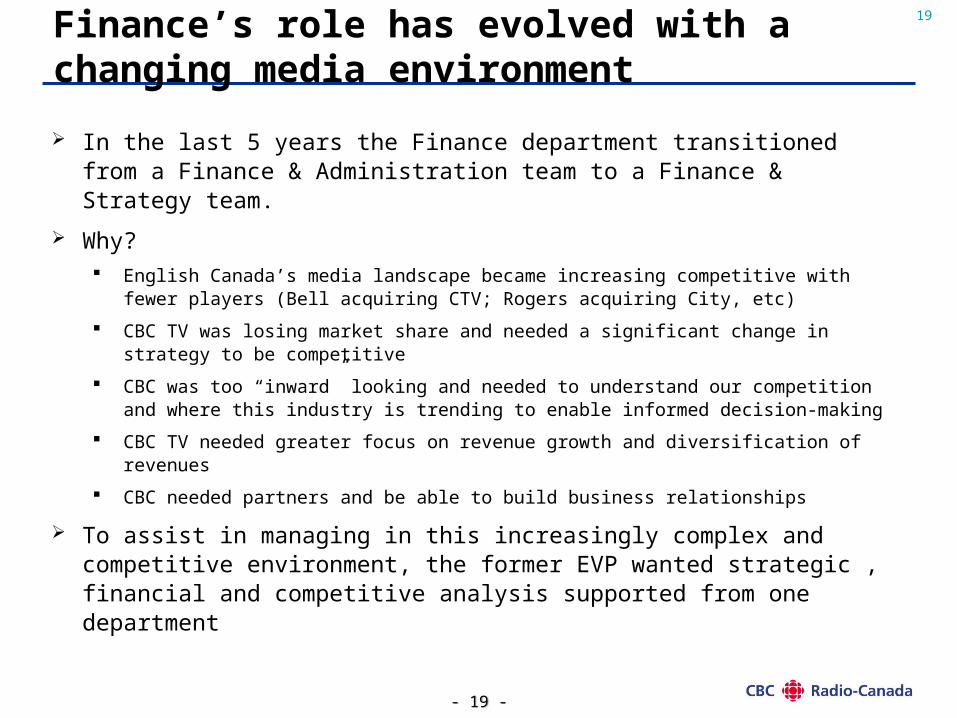

19Finance’s role has evolved with a changing media environment

In the last 5 years the Finance department transitioned from a Finance & Administration team to a Finance & Strategy team.

Why? English Canada’s media landscape became increasing competitive with fewer

players (Bell acquiring CTV; Rogers acquiring City, etc)

CBC TV was losing market share and needed a significant change in strategy to be competitive

CBC was too “inward” looking and needed to understand our competition and where this industry is trending to enable informed decision-making

CBC TV needed greater focus on revenue growth and diversification of revenues

CBC needed partners and be able to build business relationships

To assist in managing in this increasingly complex and competitive environment, the former EVP wanted strategic , financial and competitive analysis supported from one department

- 20 -- 20 -

20The department has evolved to include strategic and business services

Finance & Strategy is now a “one stop shop”, working with other departments, providing them with strategic, financial and competitive advice and information, and supporting corporate priorities.

Finance & Strategy consists of 4 different groups:

Finance (Travers Chow).

Strategic & Competitive Analysis (Betty Chiu).

Strategy & Planning (Stephen Hudovernik).

Business Development (Jonathan Soon-Shiong)

- 21 -- 21 -

21Finance & Strategy Provides Guidance That Is Aligned With CBC’s Key Priorities Via Critical Intel

CBC’s Key Objectives

Roles And Responsibilities

• Assessing and Interpreting The Evolution Of The Media Industry

• Anticipating Opportunities, Solutions, and Action Plans

• Facilitating Long and Short Term Business Activities

• Planning/managing English Services’s business planning processes

• Reporting Metrics

• Supporting Corporate Finance in preparing the Annual Report, Corporate Business Plans filed with the Government

• Supporting requests and analysis from the Board of Directors

• Budgeting, managing, forecasting and reporting all financial activity

• Re-evaluating financial performance

• Contingency planning

• External reporting

• Corporate governance (e.g. CRTC, Annual Reports)

Grow Audience Share

TV, Radio, News Renewal

Invest For The Future

New Platforms

Regional initiatives

•Content Company•Multi-platform•Engage with Canadians

•Deeply rooted in the regions

SCA S&P Finance

• Supports and manages strategic relationships with content and technological partners

• Develop new business activities through various internal stakeholders

Tactical Group -BD

- 22 -- 22 -

2222Finance & Strategy works closely with the rest of ES providing strategic advice & services

BD

- 23 -- 23 -

Successful initiatives

Successes as a “Finance family” include: Corporate Finance Triangle

– Now expanded to Controller Triangle

Recovery Plan

Coordinated planning: operating and capital

Strategic Review Plan

Towards 2015 Strategic Plan

Improved financial reporting (CRTC, Flash reports, IFRS, monthly financial statements, cashflow, information for the Board, etc)

STIP in partnership with Human Resources

23

- 24 -- 24 -

Areas of Focus/Successes

Areas of focus/successes in Network: Stronger reporting (revenues, performance indicators,

MD and A, departmental and regional financial reports, etc)

Alignment of strategic and business planning

Provide business and revenue modeling for all major strategic initiatives. Examples include:

– Significant acquisitions (foreign acquisitions, sports properties, etc)

– Specialty channel strategies: Current TV, Sports specialty channel

24

- 25 -- 25 -

Areas of focus/Successes

Areas of focus/successes in Network – cont’d:

– Local/hyper local strategies

– News wire service

– BDU bundling strategies (new Rogers and Bell contracts)

– Music strategy

– Sports online

– Digital opportunities (Podcasts, VOD, etc)

Partnering opportunities via Business Development

25

- 26 -- 26 -

Areas of focus/Successes

Areas of focus/successes in Network – cont’d:– Competitive and industry analysis (all available via livelink)

– Macro environmental scans (Revenues, TV, Radio,

– Competitor performance (fact sheets, profiles, points of view, etc)

– Product knowledge and information sharing (news of the day, industry reports, competitive SWOT’s major ownership groups, etc)

26

- 27 -- 27 -

QUESTIONS

Questions?

27

- 28 -- 28 -

Organizational Priorities

- 29 -- 29 -

Organizational Priorities

Financial Reporting

Compliance

Finance

Budgeting

Supply Management Services

Capital Planning

Government Relationship Management

Employee Engagement

- 30 -- 30 -

Financial Reporting: Project UpdateLooking Ahead: IFRS, Quarterly Financial Reporting, CRTC

- 31 -- 31 -

IFRS Update

- 32 -- 32 -

IFRS UPDATE

On Time

On Budget

No Critical Issues

- 33 -- 33 -

IFRS UPDATE

OPENING BALANCE SHEET – April 1, 2010

The first draft of the opening balance sheet has been prepared. Impacts are as follows:

Financial Statement Category thousands of dollars

Retained earnings March 31, 2010 (Canadian GAAP) (138,056)

IFRS adjustments made:

Deemed cost election – buildings 21,294

Employee benefits and pensions 81,601

Retained earnings (with known adjustments) (35,161)

Potential IFRS adjustments (Decisions remaining to be made)

Deemed cost election – land 159,999

Deemed cost election- Vancouver (16,687)

Provisions (asbestos, PCB’s, AFDA) unknown

Potential adjustments 143, 312

Potential opening retained earnings (IFRS) 108,151

- 34 -- 34 -

IFRS UPDATE

KNOWLEDGE TRANSFER PLAN

2-page technical summaries of each position paper are currently being prepared

Changes from the current procedures to be documented and communicated to stakeholders by November 15

Documentation of procedures which are not changing due to IFRS to be communicated by December 31

- 35 -- 35 -

IFRS UPDATE

KNOWLEDGE TRANSFER PLAN

(cont’d)

Roll out communication of summaries via conference calls, emails and face to face discussions

Develop manual monthly, quarterly and annual sign-off checklists for the December 2010 quarter-end

Automate the checklists via system (SAP GRC) approvals for Q2 2011

- 36 -- 36 -

IFRS UPDATE

OAG

The audit file for the opening balance sheet is currently being prepared for the OAG

The OAG audit of the opening balance sheet is scheduled to commence December 1, 2010;

Completion of the audit is anticipated by January 31, 2011.

- 37 -- 37 -

IFRS UPDATE

WE ARE ON TRACK!

- 38 -- 38 -

Quarterly Reporting Update

- 39 -- 39 -

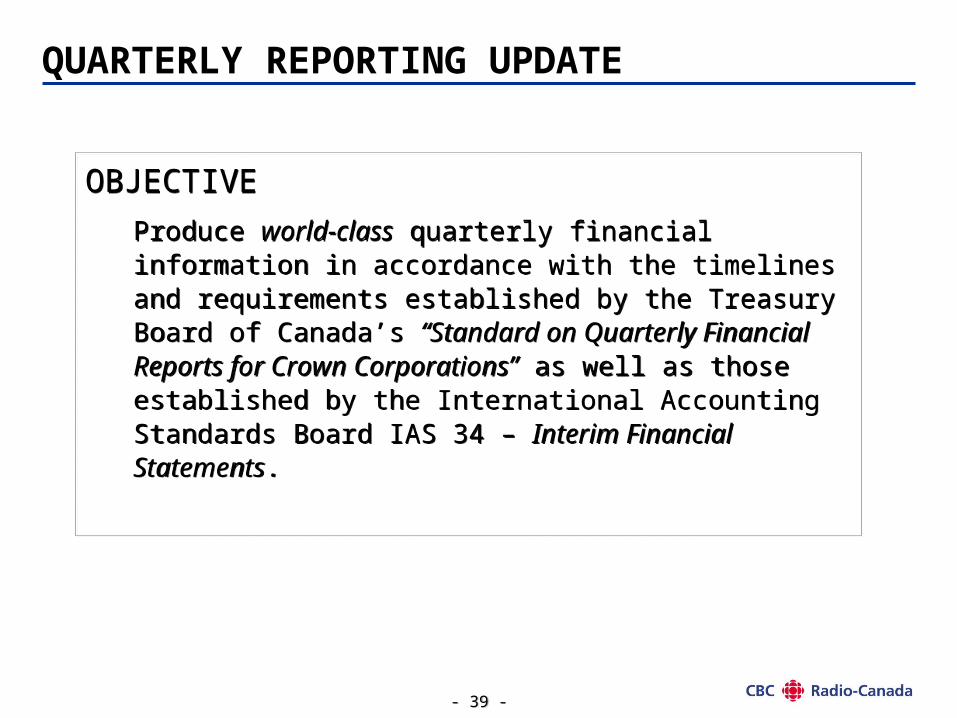

QUARTERLY REPORTING UPDATE

OBJECTIVE

Produce world-class quarterly financial information in accordance with the timelines and requirements established by the Treasury Board of Canada’s “Standard on Quarterly Financial Reports for Crown Corporations” as well as those established by the International Accounting Standards Board IAS 34 – Interim Financial Statements.

OBJECTIVE

Produce world-class quarterly financial information in accordance with the timelines and requirements established by the Treasury Board of Canada’s “Standard on Quarterly Financial Reports for Crown Corporations” as well as those established by the International Accounting Standards Board IAS 34 – Interim Financial Statements.

- 40 -- 40 -

CSANI 51-102

Benchmarking

CSANI 51-102

Benchmarking

Treasury Board of Canada

IASB (IAS 34)

Treasury Board of Canada

IASB (IAS 34)

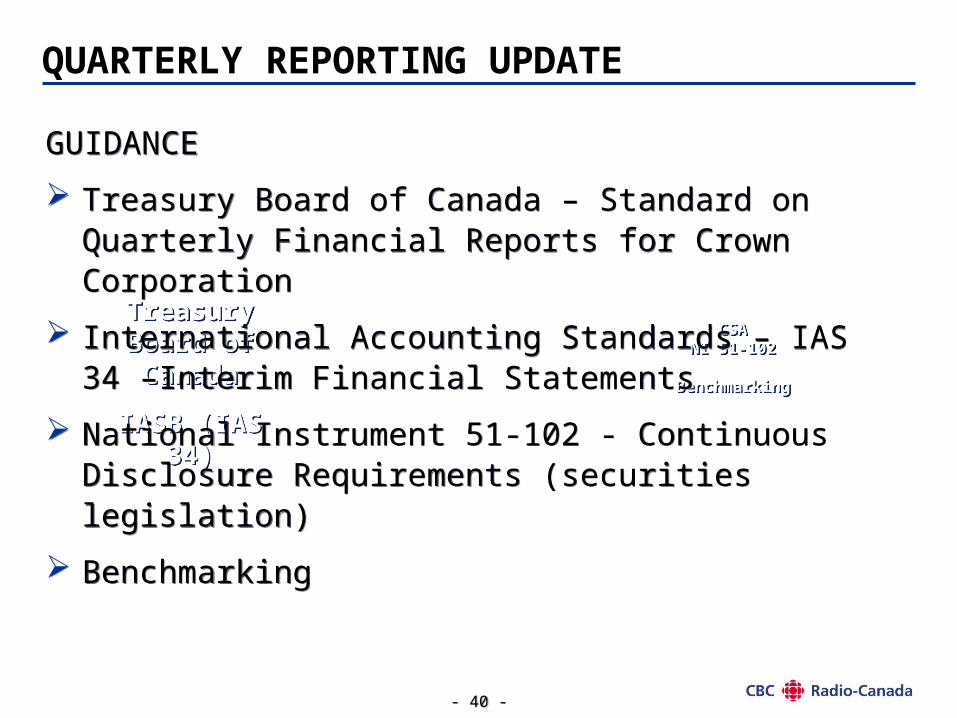

GUIDANCE

Treasury Board of Canada – Standard on Quarterly Financial Reports for Crown Corporation

International Accounting Standards – IAS 34 –Interim Financial Statements

National Instrument 51-102 - Continuous Disclosure Requirements (securities legislation)

Benchmarking

GUIDANCE

Treasury Board of Canada – Standard on Quarterly Financial Reports for Crown Corporation

International Accounting Standards – IAS 34 –Interim Financial Statements

National Instrument 51-102 - Continuous Disclosure Requirements (securities legislation)

Benchmarking

QUARTERLY REPORTING UPDATE

- 41 -- 41 -

Quarterly Financial Reporting

Quarterly Financial Reporting

CRTC ReportsCRTC

Reports

Corporate Plan and Annual Report

Corporate Plan and Annual Report

Monthly Financial

Management Report

Monthly Financial

Management Report

Quarterly Receiver General

Reporting

Quarterly Receiver General

Reporting

QUARTERLY REPORTING UPDATE

Monthly Dashboard

Monthly Dashboard

CURRENT REPORTINGCURRENT REPORTING

- 42 -- 42 -

Developing an efficient process whereby reports and analysis are integrated to avoid reporting redundancies and inconsistenciesDeveloping an efficient process whereby reports and analysis are integrated to avoid reporting redundancies and inconsistencies

Quarterly ReportingQuarterly Reporting

Due Diligence Review

• Role of the Auditor

• Role of the Audit Committee

Due Diligence Review

• Role of the Auditor

• Role of the Audit Committee

60 day timeframe for issuance

• Calendar of events

60 day timeframe for issuance

• Calendar of events

TransparencyTransparencyCertification process

• Role of the CEO

• Role of the CFO

Certification process

• Role of the CEO

• Role of the CFO

QUARTERLY REPORTING UPDATE

CONSIDERATIONS AND CHALLENGESCONSIDERATIONS AND CHALLENGES

- 43 -- 43 -

K a va l P an nuP ro je ct M an a g er

R is k A p p ro p ria tio ns S ys te m s Q u a lita tiveQ u a ntita tive A na lys is

F in an c ia l S ta te m e nta n d N ote s D isc lo su re

C h an geM a na ge m e nt

M a rie -Jo sée L a co m beP ro jec t L ea d er

Steering CommitteePeter St-Onge Michael Mooney

Neil McEneaney Christopher Flann

Martine Ménard Suzanne Morris

Stan Staple Jerry Zubryckyj

Maryse Vendette (Deloitte)

Steering CommitteePeter St-Onge Michael Mooney

Neil McEneaney Christopher Flann

Martine Ménard Suzanne Morris

Stan Staple Jerry Zubryckyj

Maryse Vendette (Deloitte)

QUARTERLY REPORTING UPDATE

TEAM COMPOSITION

- 44 -- 44 -

Crown Corporation Committee

Deloitte and Touche

External trainers

Crown Corporation Committee

Deloitte and Touche

External trainers

QUARTERLY REPORTING UPDATE

EXTERNAL RESOURCE SUPPORT

- 45 -- 45 -

2010/11

April 1, 2011April 1, 2010 April 1, 2012

IFRS Parallel Reporting Period

April 1, 2011

IFRS Implemented

March 31, 2012

First Audited IFRS Annual Statements

IFRS Fully Implemented

2009/10

New Quarterly Reporting

Legislation

New Quarterly Reporting

Legislation

Q1Proforma

Qrtly

1stTrial

Qrtly FS

2ndTrial

Qrtly FS

Q2

1st

Qrtly FSPreparation

August 2011

Issue 1st Quarterly Financial

Statements

Prepare processes and systems

Prepare processes and systems

Corporate and Network staff training

Corporate and Network staff training

IFRS Transition Project

Q3Q1 Q3 Q1

QUARTERLY REPORTING UPDATE

QUARTERLY REPORTING TIMELINE

- 46 -- 46 -

Within 60 days after the end of the quarter, Crown Corporations are required to make public quarterly financial reports

A. Complete Financial Statements (with comparative data)

C. Risk analysis

B. Narrative Discussion

D. Significant changes

E. Reporting on use of Appropriations

F. Attestations by Senior Officials (i.e. CEO or CFO)

QUARTERLY REPORTING UPDATE

Management Discussion and Analysis (MD&A)Management Discussion and Analysis (MD&A)

QUARTERLY REPORTING REQUIREMENTSQUARTERLY REPORTING REQUIREMENTS

Treasury Board Policy requirements:Treasury Board Policy requirements:

- 47 -- 47 -

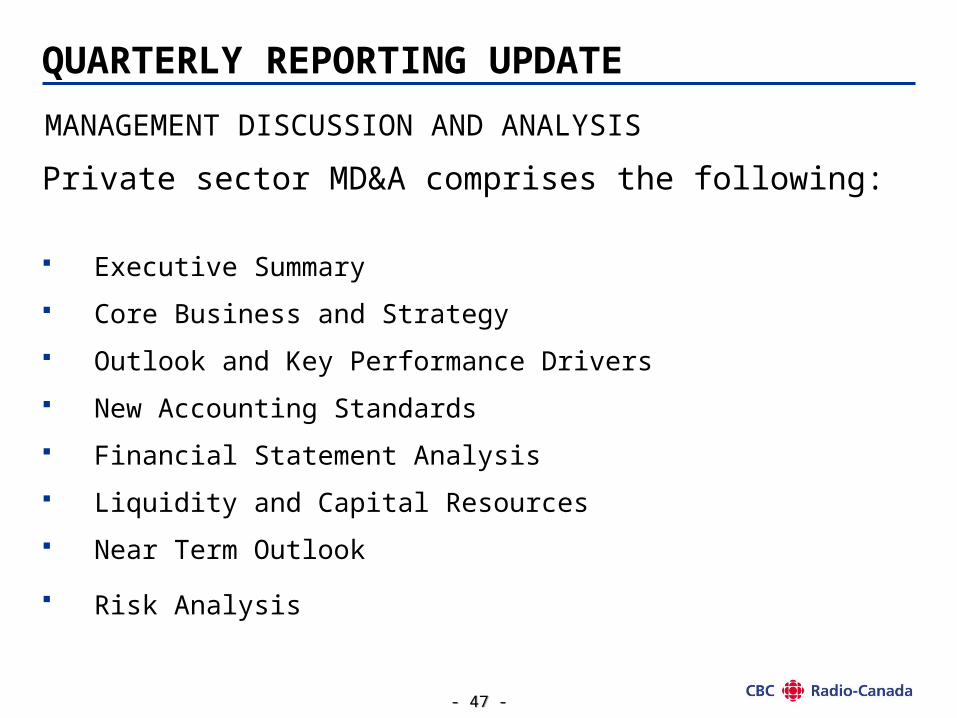

Private sector MD&A comprises the following:

Executive Summary

Core Business and Strategy

Outlook and Key Performance Drivers

New Accounting Standards

Financial Statement Analysis

Liquidity and Capital Resources

Near Term Outlook

Risk Analysis

QUARTERLY REPORTING UPDATE

MANAGEMENT DISCUSSION AND ANALYSIS

- 48 -- 48 -

Outlook and Key Performance Drivers Outlook and Key Performance Drivers

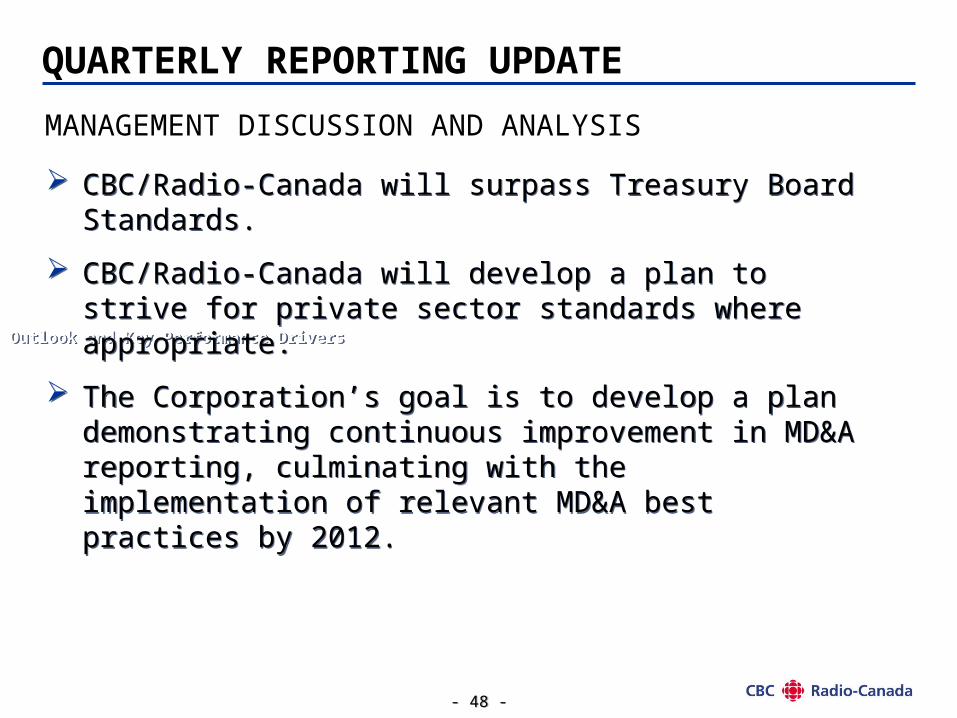

CBC/Radio-Canada will surpass Treasury Board Standards.

CBC/Radio-Canada will develop a plan to strive for private sector standards where appropriate.

The Corporation’s goal is to develop a plan demonstrating continuous improvement in MD&A reporting, culminating with the implementation of relevant MD&A best practices by 2012.

CBC/Radio-Canada will surpass Treasury Board Standards.

CBC/Radio-Canada will develop a plan to strive for private sector standards where appropriate.

The Corporation’s goal is to develop a plan demonstrating continuous improvement in MD&A reporting, culminating with the implementation of relevant MD&A best practices by 2012.

QUARTERLY REPORTING UPDATE

MANAGEMENT DISCUSSION AND ANALYSIS

- 49 -- 49 -

Attend MD&A training (October/November/December) and develop MD&A plan for best practice implementation

Develop full Management Discussion and Analysis for December 31st quarter-end

Continue discussion with Treasury Board and Crown Corporations Quarterly Reporting Committee to clarify standards

Develop plan to obtain assurance on quarterly reports

Conclude by November 30 with Deloitte on technical accounting and disclosure matters (appropriations, materiality, note disclosures)

Attend MD&A training (October/November/December) and develop MD&A plan for best practice implementation

Develop full Management Discussion and Analysis for December 31st quarter-end

Continue discussion with Treasury Board and Crown Corporations Quarterly Reporting Committee to clarify standards

Develop plan to obtain assurance on quarterly reports

Conclude by November 30 with Deloitte on technical accounting and disclosure matters (appropriations, materiality, note disclosures)

QUARTERLY REPORTING UPDATE

NEXT STEPS

- 50 -- 50 -

QUARTERLY REPORTING UPDATE

WHAT DOES THIS MEAN FOR YOU?

AnalysisAnalysis

RigorRigor

TimeTime

- 51 -- 51 -

WE ARE ON TRACK

IN THE EARLY STAGES OF

IMPLEMENTATION!

QUARTERLY REPORTING UPDATE

- 52 -- 52 -

CRTC Update

- 53 -- 53 -

CRTC Financial Reports include:

1. Conventional TV and Radio Annual Return

2. Aggregate Report

3. Local Programming Improvement Fund (LPIF) Report

4. Specialty Services Annual Report

CRTC Financial Reports include:

1. Conventional TV and Radio Annual Return

2. Aggregate Report

3. Local Programming Improvement Fund (LPIF) Report

4. Specialty Services Annual Report

CRTC UPDATE

All Reports reflect financial results for the broadcast year ending August 31.All Reports reflect financial results for the broadcast year ending August 31.

- 54 -- 54 -

One report required per broadcasting license One report required per broadcasting license

CRTC UPDATE

ANNUAL RETURN

Radio TV Total

English Network 50 16 66

French Network 32 13 45

Total 82 29 111

- 55 -- 55 -

Annual Return includes:

Revenues

Expenses

Cost of Programming

Salaries

FTE’s

Other….

(Not a public document)

Annual Return includes:

Revenues

Expenses

Cost of Programming

Salaries

FTE’s

Other….

(Not a public document)

CRTC UPDATE

ANNUAL RETURN

- 56 -- 56 -

The fund was created in 2008 to encourage broadcasters to provide diverse local television programming to smaller Canadian markets.

Represents $ 36M of funding to CBC/Radio-Canada in 2010/11

Enhance Local Programming

Sustain Local Programming

As of November 30, 2010, submitted LPIF Report must be accompanied by audit reports attesting to the fairness of the statement in accordance with the definition of “direct expenses” set out in Paragraph 33 of Broadcasting Policy 2009-406.

The fund was created in 2008 to encourage broadcasters to provide diverse local television programming to smaller Canadian markets.

Represents $ 36M of funding to CBC/Radio-Canada in 2010/11

Enhance Local Programming

Sustain Local Programming

As of November 30, 2010, submitted LPIF Report must be accompanied by audit reports attesting to the fairness of the statement in accordance with the definition of “direct expenses” set out in Paragraph 33 of Broadcasting Policy 2009-406.

CRTC UPDATE

LOCAL PROGRAMMING IMPROVEMENT FUND (LPIF)

- 57 -- 57 -

Newsworld

RDI

bold

Doc Channel

Review engagements

LICENCE RENEWALS

Expected in 2011 or 2012

Newsworld

RDI

bold

Doc Channel

Review engagements

LICENCE RENEWALS

Expected in 2011 or 2012

CRTC UPDATE

SPECIALTY SERVICES ANNUAL REPORT

- 58 -- 58 -

November 30th submission is on track

Audit is progressing on track

November 30th submission is on track

Audit is progressing on track

CRTC UPDATE

CRTC OVERALL

There is pain in this process

Very Tight Timetable!

There is pain in this process

Very Tight Timetable!

- 59 -- 59 -

Questions?

- 60 -- 60 -

Workshops

- 61 -- 61 -

SWOT Analysis

SWOT

=

Strengths

Weaknesses

Opportunities

Threats

- 62 -- 62 -

SWOT Analysis

Strengths – What do we have going for us? What are we doing very well? What are our assets?

Weaknesses – What are our limitations? What prevents us from being successful?

Opportunities – What factors can help us?

Threats – What factors will reduce our ability to achieve?

- 63 -- 63 -

Exercise - Needs

EXERCISE #1 – 40 minutesIn two groups, identify the following elements:What are our needs as a team?Who are our clients?What are their expectations?How can we meet their needs?

EXERCISE #2 – 20 minutesAs a team, we should……STOP START CONTINUE

- 64 -- 64 -

Feedback and Review of Parking Lot

- 65 -- 65 -

Wrap Up