Look Ahead - Q3 2019 - Phillips & Company€¦ · Global Macro Slowdown. 4 The Financial Conditions...

12

Q3 2019 LOOK AHEAD

Transcript of Look Ahead - Q3 2019 - Phillips & Company€¦ · Global Macro Slowdown. 4 The Financial Conditions...

Q3 2019 LOOK AHEAD

DisclaimerCertain information in this presentation constitutes forward-looking statements. Due to various risks, uncertainties, and assumptions made in our analysis, actual events or results or actual performance of the markets covered by this presentation may differ materially from those described. The information herein reflects our current views only, is subject to change, and is not intended to be promissory or relied upon by the reader. There can be no certainty that events will turn out as presented. Data are from sources deemed to be reliable. No representation or warranties either expressed or implied are made as to the accuracy of the information presented.

2

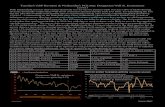

Earnings Recession Maybe

Data Sources: FactSet Earnings Insight - July 2019No representation or warranties either expressed or implied are made as to the accuracy of the information presented.

3

Q2 2019 S&P 500 earnings growth is expected to be negative, which would mark the first time the index has reported two straight quarters of year-over-year declines in earnings since Q1 2016 and Q2 2016.

Analysts have made smaller than average cuts to EPS estimates for Q2 2019 to date. On a per-share basis, estimated earnings for the second quarter have fallen by 2.5% since March 31, 2019. This decline is smaller than both the 5-year (-3.3%) and 10-year (-3.3%) averages for a quarter; however, a larger percentage of companies have lowered the bar for Q2 2019 earnings relative to recent quarters. The percentage of companies issuing negative EPS guidance is 77% (87 out of 113), which is above the 5-year average of 70%.

We expect earnings to increase back to positive growth in the Q3 2019.

Health Care Real Estate ConsumerDisc. Utilities Industrials Financials S&P 500 Consumer

Staples Materials Comm.Services

Info.Technology Energy

Today 9.4% 6.4% 5.3% 4.5% 4.0% 1.9% -0.3% -1.1% -1.6% -5.7% -6.3% -26.9%31-Mar 3.9% 2.6% -6.5% 4.7% 0.2% -3.4% -4.0% -4.2% -10.8% -1.9% -10.6% -18.8%

-30.0%-27.0%-24.0%-21.0%-18.0%-15.0%-12.0%

-9.0%-6.0%-3.0%0.0%3.0%6.0%9.0%

12.0%

S&P 500 Earnings Growth: Q1 2019Today 31-Mar

Source: FactSet as of 6/28/2019

Utilities Health Care Comm.Services Energy Real Estate Financials Industrials S&P 500 Consumer

StaplesConsumer

Disc.Info.

Technology Materials

Today 2.2% 2.1% 1.6% 1.5% 1.3% 0.9% -1.9% -2.6% -3.0% -3.2% -11.9% -14.4%31-Mar 1.8% 2.2% 3.3% -5.2% 2.7% 2.3% 5.5% -0.5% -0.9% 1.7% -10.0% -3.2%

-15.0%

-12.5%

-10.0%

-7.5%

-5.0%

-2.5%

0.0%

2.5%

5.0%

7.5%

S&P 500 Expected Earnings Growth: Q2 2019Today 31-Mar

Source: FactSet as of 6/28/2019

Info.Technology Health Care Consumer

Staples Materials ConsumerDisc. Real Estate Comm.

Services S&P 500 Financials Industrials Energy Utilities

Below 10% 13% 16% 20% 17% 13% 15% 19% 22% 21% 31% 46%In-Line 3% 2% 0% 0% 5% 9% 8% 5% 7% 9% 3% 4%Above 87% 85% 84% 80% 78% 78% 77% 76% 71% 70% 66% 50%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

S&P 500 Earnings Scorecard: Q2 2019

Above In-Line BelowSource: FactSet as of 6/28/2019

Global Macro Slowdown

4

The Financial Conditions Index supports a slowing U.S. economy heading into the second half of 2019 due to tighter financial conditions and a fading fiscal stimulus.

The ISM Manufacturing Index for June checked in at 51.7%, down from 52.1% in May, as manufacturing activity continues to weaken. June was the third straight month in which there was a deceleration in the pace of growth. This should capture the Fed's attention as it contemplates a rate-cut decision at its July FOMC meeting.

Chinese economic growth is back in the cards after a sluggish 2018, but much depends on the outcome of the ongoing trade war and the central bank’s ability to inject flexibility into the economy.

Data Sources: Federal Reserve Bank of Chicago, Institute of Supply Management “June 2019 Manufacturing ISM Report on Business”, International Monetary FundNo representation or warranties either expressed or implied are made as to the accuracy of the information presented.

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

United States and China Real GDP Growth ExpectationsU.S. China

Source: International Monetary Fund as of 7/5/2019

Perc

ent G

row

th (%

)

Forecast

U.S. Consumer Strength

Wage Growth: 3.28%

Total Consumer

Credit Outstanding

Wage growth continues to increase at a rate above 3 percent, further supporting the consumers’ appetite to spend. Consumer Sentiment remains at elevated levels. After seeing a break below trend after Q1, sentiment is once again nearing multi-year highs. We remain cautiously

optimistic, with consumers likely to continue their appetite for spending. After the government change in calculating the Personal Savings Rate, it shows limited declines over the past half decade, further suggesting that the

U.S. consumer has ample room to increase spending; prior to the change in calculation, the Personal Savings Rate matched the lows recorded prior to the Great Financial Crisis.

5

ConsumerSentiment

PersonalSavings

Rate remains range bound

Data Sources: U.S. Bureau of Labor Statistics, The Conference Board Consumer Confidence Survey, University of Michigan, U.S. Bureau of Economic AnalysisNo representation or warranties either expressed or implied are made as to the accuracy of the information presented.

Interest Rates and Trump’s Managed Trade War

6

Data Sources: FactSet Insights “5 U.S. Economic Charts to Watch in H2 2019”, Fidelity Investment “Quarterly Market Update”, Raymond James “Fixed Income Quarterly”No representation or warranties either expressed or implied are made as to the accuracy of the information presented.

Market expectations are calling for lower rates, certainly much lower than the Fed has signaled. Between market expectations and multiple trade wars, Trump will likely get what he wants – a round of monetary stimulus that will help his 2020 campaign.

Our expectation is for a “one and done” 50 basis point rate cut. This anticipated rate cut combined with an economy that – overall – remains in decent shape would temper near-term recession risks and repair the short end of the inverted yield curve.

International Developed Markets

7

Europe is poised for slow growth going forward; southern European countries like Italy are projected to slow GDP growth to under 1.5% by 2023, and the European Central Bank is responding through continued accommodative interest rate policies

Brexit: A hard landing will be disruptive to global equity markets

Earnings in Europe have lagged its global counterparts for much of the last decade; heading into the late innings of the economic cycle, there is no data that supports Europe outperforming its global counterparts

The Trump administration is threatening to introduce new tariffs on EU products worth $4B in a trade war escalation. Fresh off reaching a truce in the China trade war, the U.S. Trade Representative’s office released a list of products made in the EU that are being considered for additional import duties. They include scotch whiskey, ham and pork, olives, pasta, and popular cheeses.

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

European Real GDP Growth ExpectationsGermany Greece Italy Spain

Source: International Monetary Fund as of 7/5/2019

Perc

ent G

row

th (%

)

Data Sources: International Monetary Fund, J. P. Morgan “Guide to the Markets – Q3 2019”, Council on Foreign Relations “Global Monetary Policy Tracker”No representation or warranties either expressed or implied are made as to the accuracy of the information presented.

Forecast

Emerging Markets (EM)

8

39%61%

China added to MSCI indices; the inclusion of China A-Shares to MSCI indices should greatly increase foreign investment, in addition to bolstering corporate governance, as local companies increase the transparency of their reporting practices and adopt strategies that more firmly consider shareholders’ interests.

China has significantly increased social financing levels, which should calm some of the anxiety about weakening credit growth as the Chinese economy slows.

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Mean Reverting the Strength of the U.S. Dollar% Chg Average +1 Std. Dev. -1 Std. Dev.

Source: Federal Reserve Bank of St. Louis as of 6/26/2019

Data Sources: Federal Reserve Bank of St. Louis, Yardeni Research “Money & Credit: China Social Financing”No representation or warranties either expressed or implied are made as to the accuracy of the information presented.

Data continues to support a weakening U.S. dollar in 2019 for two reasons:

1. Using data going back to 1996, the strength of the U.S. dollar has reached a potential inflection point at the one standard deviation level above its mean.

2. The Federal Reserve is no longer anticipating any additional rate hikes in 2019, further supporting the case for a weakening U.S. dollar.

A weakening U.S. dollar will make interest payments cheaper for Emerging Market countries with dollar denominated debt.

Mean Reversion DashboardStyle Current P/E as a % of 20-Yr Avg. P/E

Regional Fwd P/E as a % of 10-Yr Avg. Fwd P/E

Sector Fwd P/E as a % of 20-Yr Avg. Fwd P/E

9

Value Blend Growth

Larg

e

103.3% 106.8% 107.7%

Mid 102.4% 106.0% 107.3%

Smal

l

88.5% 103.7% 123.3%

ACW

I

EAFE

Inde

x

EM In

dex

Unit

ed S

tate

s

Germ

any

Unit

ed

King

dom

Chin

a

Braz

il

Indi

a

Russ

ia

104.2% 97.6% 99.1% 110.5% 99.4% 97.2% 91.5% 96.1% 105.0% 78.5%

Mat

eria

ls

Indu

stri

als

Fina

ncia

ls

Ener

gy

Cons

umer

D

iscr

etio

nary

Tech

nolo

gy

Com

m.

Serv

ices

Real

Est

ate

Hea

lth

Care

Cons

umer

St

aple

s

Utili

ties

124.5% 99.4% 94.4% 93.1% 118.4% 95.0% 97.3% 125.3% 93.3% 114.3% 131.5%

Data Sources: Bloomberg, J. P. Morgan “Guide to the Markets – Q3 2019”No representation or warranties either expressed or implied are made as to the accuracy of the information presented.

Economic Dashboard

10

Data Sources: Bloomberg, Federal Reserve Bank of St. LouisNo representation or warranties either expressed or implied are made as to the accuracy of the information presented.

As of 12/31/2018 U.S. Treasury Spread 2-Yr vs. 10-Yr Spread As of 6/30/2019

Latest Level 3.0 Latest Level 26.0

Change from Prior Quarter 0.2 Change from Prior Quarter 7.0

Latest Direction Improving Latest Direction Steepening

Frequency Quarterly Frequency Monthly

U.S Inflation As of 12/31/2018 S&P 500 P/E Ratio As of 6/30/2019

Latest Level 1.6 Latest Level 22.1

Change from Prior Quarter -0.6 Change from Prior Month 1.7

Latest Direction Decreasing Latest Direction Increasing

Frequency Quarterly Frequency Monthly

U.S. U-6 Unemployment Rate As of 3/31/2019 Schiller Home Value Index As of 4/30/2019

Latest Level 7.2 Latest Level 215.7

Change from Prior Quarter -0.1 Change from Prior Month 0.7

Latest Direction Decreasing Latest Direction Increasing

Frequency Quarterly Frequency Monthly

Retail Sales As of 3/31/2019 Credit: Revolving / Non-Revolving As of 4/30/2019

Latest Level 0.3 Latest Levels 1064.5 3005.4

Change from Prior Month -1.6 Changes from Prior Month 7 10.5

Latest Direction Decreasing Latest Direction Expanding

Frequency Monthly Frequency Quarterly

U.S. GDP Growth

-6%-4%-2%0%2%4%6%

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

-2%

0%

2%

4%

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

0%

5%

10%

15%

20%

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

0

300

BPS

-6%

0%

6%

500

2,965

-2%

5%

1,500

4,000

800

1,800

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Billi

ons U

SD

Billi

ons U

SD

Revoling Credit (L) Non-Revolving Credit (R)

0

300

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

BPS

-4%

-2%

0%

2%

4%

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

125145165185205225

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

-2%

5%

10

15

20

25

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Our View and RecommendationsOur View

Expect risk assets to start pricing in better Q3 earnings-per-share growth.

A rally in Chinese equities should recommence as the Trade War overhang is lifted.

Expect a “one and done” 50 basis point cut to the Federal Funds Rate.

We expect to see the Quantitative Easing policies of the last decade being re-examined.

Developed Markets will continue to languish, with Brexit and slowing economies being the dominant forces.

Emerging Market economies should strengthen on better earnings and forward-looking valuations.

Central banks around the world will continue to act as a safety net for slowing economies.

With forward-looking returns getting smaller by the day, investors are likely to stretch for return through private equity and other U.S. growth assets.

Recommendations

Investors should maintain a slight overweight allocation to Emerging Markets and Chinese equities.

We recommend shortening overall bond durations in relation to benchmarks, as the short-end of the yield curve normalizes.

U.S. Small Cap Value stocks should offer compelling mean-reverting opportunities compared to Mid and Large Cap names.

Continue to tilt to yield as rate cuts will support the Utilities, Energy, and Telecom sectors of the economy.

11

Data Source: Phillips & Co.