LOCAL MARKET TRENDS IMPACTING AFFORDABLE HOUSING Portland-Vancouver Metropolitan Area Jerry Johnson...

22

LOCAL MARKET TRENDS IMPACTING AFFORDABLE HOUSING Portland-Vancouver Metropolitan Area Jerry Johnson Principal Johnson Reid, LLC

-

Upload

clifford-douglas -

Category

Documents

-

view

213 -

download

0

Transcript of LOCAL MARKET TRENDS IMPACTING AFFORDABLE HOUSING Portland-Vancouver Metropolitan Area Jerry Johnson...

LOCAL MARKET TRENDSIMPACTING AFFORDABLE

HOUSING

Portland-Vancouver Metropolitan Area

Jerry Johnson

Principal

Johnson Reid, LLC

THE GREAT RECESSION

-8%

-7%

-6%

-5%

-4%

-3%

-2%

-1%

1%

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 31 33 35 37 39 41 43 45 47 49 51 53 55 57 59 61 63 65 67 69

PERC

ENTA

GE

CHA

NG

E FR

OM

PEA

K

MONTHS SINCE PEAK

1948-50

1953-55

1957-59

1960-61

1969-71

1974-76

1980

1981-83

1990-93

2001-05

2008-12

CURRENT RECESSION RELATIVE TO SIMILAR FINANCIAL CRISIS

RECESSIONS

EMPLOYED POPULATION RATIOAges 25-54 Years

PART TIME EMPLOYMENT

LONG TERM UNEMPLOYED

UNEMPLOYED SHIFTING TO DISABLED

FAMILY INCOME TRENDS BY QUINTILE

Family Income Down

Net Worth Down 40% from 2007

EMPLOYMENT TRENDS BY SECTORPortland Metro Area – 2001-2011

OLMIS and Johnson Reid

-30%

-20%

-10%

0%

10%

20%

30%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

PERCENTAGE EMPLOYMENT CHANGE BY INDUSTRY FROM 2001

Construction

Other Durable Goods Manufacturing

Computer and Electronics

Transportation Equipment

Nondurable Goods Manufacturing

Wholesale Trade

Retail Trade

Transportation, Warehousing, and utilities

Information

Financial Activities

Professional and Business Services

Leisure and Hospitality

Other Services

Government

EMPLOYMENT TRENDS BY SECTORPortland Metro Area – 2001-2011

-3% -3% -2% -2% -1% -1% 0% 1% 1% 2%

Construction

Other Durable Goods Manufacturing

Computer and Electronics

Transportation Equipment

Nondurable Goods Manufacturing

Wholesale Trade

Retail Trade

Transportation, Warehousing, and …

Information

Financial Activities

Professional and Business Services

Leisure and Hospitality

Other Services

Government

(15,

000)

(10,

000)

(5,0

00)

-

5,00

0

10,0

00

15,0

00

Construction

Other Durable Goods Manufacturing

Computer and Electronics

Transportation Equipment

Nondurable Goods Manufacturing

Wholesale Trade

Retail Trade

Transportation, Warehousing, and utilities

Information

Financial Activities

Professional and Business Services

Leisure and Hospitality

Other Services

Government

OLMIS and Johnson Reid

GENERAL MARKET TRENDS• REAL ESTATE MARKETS ARE CYCLICAL, NOT

LINEAR

HOMEOWNERSHIP RATENational Trends

PRICE TO RENT RATIONational Trends

CASE SHILLER HOME PRICE INDEX TRENDS

50

100

150

200

250

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

20 City Composite

Seattle, WA

Portland, OR

POPULATION GROWTH BY TYPE2000-2010

SOURCE: Oregon Office of Economic Analysis, Washington Office of Financial Management, and JOHNSON REID

SHARE OF 10-YEAR POPULATION GROWTH

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

Popu

latio

n

Natural Increase

Net Migration

22.4%

24.9%14.5%

38.3%

Clackamas Clark Multnomah Washington

MAJOR DEMOGRAPHIC SHIFTS

• AGING BABY BOOMERS– Less affluent than expected– Lost Equity/Negative Positions

• YOUNG BABY BOOMERS– Changing retirement plans– Kids later, high income demands

• CHILDREN OF BABY BOOMERS– Generation Y, Millennials, Echo

Boom– It’s all about them

1,300,000

170,000

1,500,009

4,100,000

5,400,000

5,000,000

3,500,000

(400,000)

(1,900,000)

(1,500,000)

1,000,000

2,600,000

1,600,000

(200,000)

85+

80-84

75-79

70-74

65-69

60-64

55-59

50-54

45-49

40-44

35-39

30-34

25-29

20-24

PROJECTED POPULATION GROWTH BY AGE / 2010-2020

RESIDENTIAL IMPACTS OF DEMOGRAPHIC SHIFTS

• INCREASED INTEREST IN HIGHLY AMENITIZED LOCATIONS– Willingness to swap space and

price for amenities– Urban amenities with a practical

impact

• VALUE ADDED STRATEGY IN PRIME LOCATIONS– Small units carefully sited– No parking?

RENTAL APARTMENT MARKET TRENDSPortland Metro Area

10-Year Average Annual Supply 2,32110-Year Average Annual Absorption 2,54710-Year Average Annual Rental Increase: 3.6%10-Year Average Annual Vacancy Rate: 4.9%

SOURCE: Johnson Reid

-4%

-2%

0%

2%

4%

6%

8%

10%

-3,000

-2,000

-1,000

0

1,000

2,000

3,000

4,000

5,000

6,000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

NEW RENTAL SUPPLY

NET ABSORPTION

VACANCY RATE

RENT ESCALATION

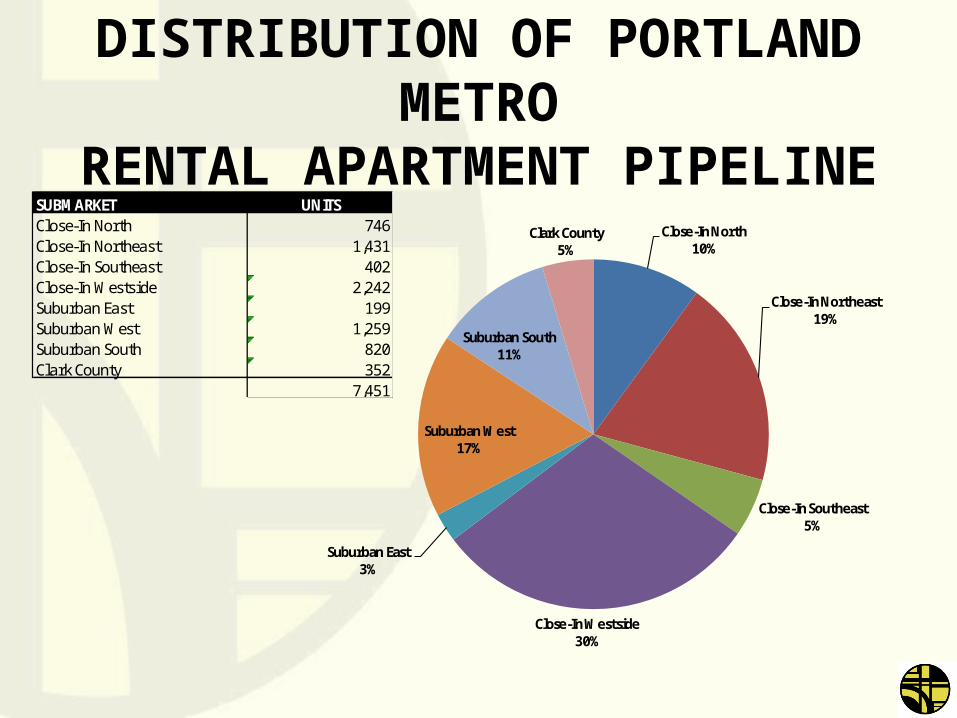

DISTRIBUTION OF PORTLAND METRORENTAL APARTMENT PIPELINE

SUBMARKET UNITSClose-In North 746Close-In Northeast 1,431Close-In Southeast 402Close-In Westside 2,242Suburban East 199Suburban West 1,259Suburban South 820Clark County 352

7,451

Close-In North10%

Close-In Northeast19%

Close-In Southeast5%

Close-In Westside30%

Suburban East3%

Suburban West17%

Suburban South11%

Clark County5%

PIPELINE AS APERCENT OF CURRENT BASE

SOURCE: 2010 Census and Johnson Reid LLC

0% 10% 20% 30% 40%

Close-In North

Close-In Northeast

Close-In Southeast

Close-In Westside

Suburban East

Suburban West

Suburban South

Clark County

EXISTING BASE AND PIPELINEPERCENT OF METRO TOTAL

Existing Base

Pipeline

6.0%

10.6%

1.3%

7.4%

0.2%

1.6%

6.6%

0.7%

0% 5% 10% 15%

Close-In North

Close-In Northeast

Close-In Southeast

Close-In Westside

Suburban East

Suburban West

Suburban South

Clark County

IDENTIFIED PIPELINE AS A PERCENT OF CURRENT RENTER HOUSEHOLD BASE

HOUSING MARKET DYNAMICS• DEMAND INCREASING

– Losses to tenure split ending– Rising rental pricing– Continued low interest rates

• PIPELINE DRY– Very little new construction– Lot supply limited– Pricing must rise to replacement

cost

LOCAL RENTAL APARTMENTS• NO LONGER A CAN’T MISS

MARKET– Production Cycle Well Underway– Attention Needs to be Paid to Pipeline– Infill, Understand Micro Markets– Quality Locations– Urban Amenity Profile– “Sustainable Competitive Position”

• DEATH OF SUBURBS OVERSOLD

![Jeffrey Johnson v Ryan Reid - Supreme Court · Statement of Jeffrey Johnson). [3] The Defendant filed a Defence and in that Defence, it was admitted that there had, on the relevant](https://static.fdocuments.us/doc/165x107/60bcf53a7900a4278700a5d8/jeffrey-johnson-v-ryan-reid-supreme-court-statement-of-jeffrey-johnson-3-the.jpg)