LITIGATION RISK, AUDIT FEES AND ... - assets.csom…assets.csom.umn.edu/assets/37726.pdf ·...

44

LITIGATION RISK, AUDIT FEES AND AUDIT QUALITY: INITIAL PUBLIC OFFERINGS AS A NATURAL EXPERIMENT Ramgopal Venkataraman Carlson School of Management University of Minnesota [email protected] Joseph Weber Sloan School of Management Massachusetts Institute of Technology [email protected] Michael Willenborg School of Business University of Connecticut [email protected] We thank Nick Dopuch, Ron King, James McKeown, Mark Peecher, Martin Wu and seminar participants at the 2004 AAA Annual Meeting, University of Illinois and Washington University. This paper was previously titled “What if auditing was not a ‘low-margin’ business? Auditors and their IPO clients as a natural experiment.” February 17, 2005

-

Upload

nguyendieu -

Category

Documents

-

view

213 -

download

0

Transcript of LITIGATION RISK, AUDIT FEES AND ... - assets.csom…assets.csom.umn.edu/assets/37726.pdf ·...

LITIGATION RISK, AUDIT FEES AND AUDIT QUALITY:

INITIAL PUBLIC OFFERINGS AS A NATURAL EXPERIMENT

Ramgopal Venkataraman Carlson School of Management

University of Minnesota [email protected]

Joseph Weber Sloan School of Management

Massachusetts Institute of Technology [email protected]

Michael Willenborg School of Business

University of Connecticut [email protected]

We thank Nick Dopuch, Ron King, James McKeown, Mark Peecher, Martin Wu and seminar participants at the 2004 AAA Annual Meeting, University of Illinois and Washington University. This paper was previously titled “What if auditing was not a ‘low-margin’ business? Auditors and their IPO clients as a natural experiment.”

February 17, 2005

LITIGATION RISK, AUDIT FEES AND AUDIT QUALITY:

INITIAL PUBLIC OFFERINGS AS A NATURAL EXPERIMENT

Abstract We use the IPO setting to examine the relation between the auditor’s exposure to legal liability, audit fees and audit quality. We find that auditors earn higher fees for IPO engagements than for post-IPO engagements, and that these higher fees are strongly associated with our proxy for the auditor’s higher exposure under the 1933 Act (the size of the IPO). In regard to audit quality, we find that pre-IPO accruals are negative and less than post-IPO accruals, particularly when the issuer’s IPO prospectus refers to the existence of an audit committee. In contrast to the inference in the extant literature, our findings provide scant support for the view that auditors acquiesce to opportunistic pre-issuance earnings management by IPO issuers. Taken together, and consistent with the effect that an increase in litigation exposure likely has on auditor incentives, our results suggest that audit fees and audit quality are higher in a higher litigation (1933 Act) regime. Given present-day interest in auditor litigation reform, our paper may be of interest to legislators and standard setters.

Keywords: Abnormal accruals, audit committees, audit fees, audit quality, auditor litigation, earnings management, initial public offerings

“Are the Big Four accounting firms members of an endangered species, destined to die from litigation? … the firms yearn for legal protection …In Britain, their plea for a cap on damage awards was rejected by the government this week. This may be a case of Catch-22. If auditors are doing a good job, they deserve to be protected from lawsuits that could put them out of business. But without the threat of such suits, will they do a good job?” (Norris 2004)

1. Introduction

As it concerns the audit profession, blame for recent accounting scandals has largely been

affixed to four culprits, ranging from the alleged misdeeds of one firm to more systemic causes

involving an erosion in independence, the inadequacy of self regulation and the diminished legal

threat. During 2002, in the wake of certain of these scandals, two major events took place: the

U.S. Justice Department’s indictment (and consequent demise) of Arthur Andersen and the U.S.

Congress’ passage of the Sarbanes-Oxley Act. Nowadays, public company management and, for

the most part, their four international audit firms are more accountable under a new structure of

expanded duties and heightened scrutiny. To a large extent, auditors cannot serve as consultants

to companies whose books they examine and a new regulator, the PCAOB, oversees auditors of

SEC registrants. In terms of likely culprits, these events address three of four, leaving untouched

the diminished litigation environment. Despite the introduction of legislation (Comprehensive

Investor Protection Act of 2002), there has been no change to what many critics consider to be a

fundamental cause for these scandals: the reduction in auditor legal liability during the mid-to-

late 1990’s.1 To the contrary, conceding their inability to price litigation risk, audit “firms yearn

[again] for legal protection”. The issue distills to whether lawmakers should decrease auditor

litigation risk to protect an “endangered species”, or retain / increase it to enforce a “Catch 22”.

In this paper, we conduct a series of tests to address the issue of auditor litigation reform.

Our primary interests are to assess whether audit fees and audit quality appear to be higher in 1 Two recent examples are: “… Enron is part of a pattern. As the liabilities faced by auditors declined in the 1990’s and as the incentives auditors perceived to acquiesce in management’s desire to manage earnings increased over the same period (because of opportunities to earn highly lucrative consulting revenues), there has been an apparent erosion in the quality of financial reporting. Assertive as this conclusion may sound, a burgeoning literature exists on earnings management, which indicates that earnings management is conscious, widespread and tolerated by auditors within, at least, very wide limits. “ (Coffee 2002); and “[b]ack in 1995, Congress enacted the Private Securities Litigation Reform Act (PSLRA), which … reduced accountability of auditors who bless phony financial statements … Then, in a second law, the Securities Litigation Uniform Standards Act of 1998 (SLUSA), Congress mandated that securities class-action suits be tried in federal courts. Give the devil its due: Both PSLRA and SLUSA were meant to curb abusive plaintiffs’ suits. But the laws were massive overkill. In essence, they gave auditors and companies a license to steal. They have exercised that license - - and then some.” (Bauder 2002, C-3)

2

higher litigation environments. Our tests focus on auditors and their IPO clients. This setting

offers two advantages for archival study of the effect of litigation risk on audit fees and quality.

For one, extant literature (Beatty 1993; Willenborg 1999; Mayhew and Wilkins 2003) suggests

that IPOs are a setting wherein audit fees may somewhat reflect the auditor’s litigation exposure.

For another, auditing a company as it goes from private to public ownership cleanly captures a

litigation regime change for auditors. As is well known, when companies register their IPO, they

file under the Securities Act of 1933 (1933 Act). Then, after going public, companies file under

the Securities Exchange Act of 1934 (1934 Act). While the Private Securities Litigation Reform

Act of 1995 (PSLRA of 1995) amends them both, the shift from 1933 Act to 1934 Act still

represents a dramatic regime change for auditors with respect to legal liability. Following Dye

(1993), which demonstrates conditions under which an auditor’s wealth serves as a bond for

audit quality and that the audit’s price includes this option on the auditor’s wealth, we expect

variation across the 1933 Act – 1934 Act threshold with regard to audit fees and audit quality.

Since litigation risk (and the potential claim on the auditor’s wealth) is substantially higher in the

1933 Act regime, auditors should receive higher fees and provide higher quality for IPO audits.

We utilize recent proxy statement disclosures of audit fees to construct a balanced panel

dataset of newly-public companies. Across the threshold from 1933 Act to 1934 Act, we study

audit fees and audit quality. First, we compare the audit fees that companies pay to go public

with those they pay once they are public. Second, using signed abnormal accounting accruals to

proxy for audit quality, we examine pre-IPO accruals (i.e., from financial statements prior to the

IPO) on both a stand-alone basis and in contrast with post-IPO accruals (i.e., from financial

statements subsequent to the IPO). In summary, we find that auditors receive higher fees for IPO

engagements and that pre-IPO abnormal accounting accruals are negative and less than post-IPO

levels. That auditors receive higher fees and appear more conservative when auditing IPOs is

consistent with the effect that an increase in litigation exposure should have on their incentives.

We start by collecting a sample of IPO companies for 2000–2002 for which both pre- and

post-IPO audit fee information is available from proxy statements. We study audit fees in both

3

levels and changes. In terms of our levels analysis, and despite a high correlation between IPO

proceeds and pre-IPO assets, we confirm the strong positive association between IPO proceeds

and pre-IPO audit fees. An economic interpretation of the elasticity between IPO proceeds and

pre-IPO audit fees suggests that, about the mean of these variables, each additional $1 million in

IPO proceeds is associated with an increase in pre-IPO audit fees of approximately $1,200. Our

changes analysis reinforces the importance of deal size in explaining audit fees in our setting.

We find that almost 90% of our sample companies pay lower audit fees as public companies than

they do to go public, and the extent of this change is strongly inversely related with the amount

of fees raised in the IPO. Simply put, we find that the greater the IPO proceeds, the greater the

decline in post-IPO audit fees. Because the 1933 Act establishes proceeds as an upper limit on

damages, the amount an IPO raises is a proxy for the implicit insurance coverage auditors

provide to investors. Following this, the extent (removal) of this coverage helps to explain the

level of pre-IPO audit fees (the decline from pre-IPO audit fees to post-IPO audit fees). Overall,

we conclude that audit fees appear to be higher in a higher litigation (1933 Act) regime.

Our findings are consistent with studies of audit production (O’Keefe, Simunic and Stein

1994; Stein, Simunic and O’Keefe 1994; and Bell, Landsman and Shackleford 2001) that find

auditor effort is increasing in partner assessments of inherent and business risk. In our IPO

setting, it seems reasonable that auditors expend effort in accordance with their litigation

exposure, which we proxy with proceeds. In addition, our conversations with partners at large

and small firms confirm that they usually earn a higher percentage of their standard billing rates

for IPO audits (i.e., “realization rates” are higher for IPO audits than for annual audits). As such,

it also seems plausible that they receive higher hourly fees for the heightened exposure to

litigation risk that an IPO audit portends. One interpretation is that the higher pre-IPO fees we

observe represent compensation for litigation risk reduction procedures involving substantially

more hours, for which audit firms collect somewhat higher hourly rates. Absent audit firm data

on hours and billing rates (both standard and actual), we cannot disentangle these. Overall, as

with Pratt and Stice’s (1994, p. 640) field experiment of 243 (then) Big 6 partners and managers,

4

we interpret our findings as consistent with the view that “audit fees reflect both the amount of

audit evidence collected and an additional premium to cover litigation risk … suggesting that

auditors may be charging clients to insure against future litigation losses”.

We then examine whether an increase in litigation risk is associated with an increase in

audit quality. We first examine whether pre-IPO accruals are negative. Second, using each firm

as its’ own control, we compare pre-IPO accruals with post-IPO accruals. We stress that, in

contrast to Teoh, Welch and Wong (1998) and Teoh, Wong and Rao (1998), we use pre-IPO

financial statements to calculate pre-IPO accruals and post-IPO financial statements to calculate

post-IPO accruals. We compute total accruals, and Jones (1991) and modified-Jones (Dechow,

Sloan and Sweeney 1995) abnormal accruals. For each of these three measures of signed

accruals, we use balance sheet and statement of cash flows approaches to obtain total accruals.2

For each of these six measures, both mean and median pre-IPO accruals are negative.

This suggests that the typical company in our samples is unlikely to be engaging in income

increasing, pre-IPO earnings management. Beyond this, pre-IPO accruals are smaller (generally

more negative) than post-IPO accruals. Taken together, these findings imply that auditors are

more conservative in a higher (the 1933 Act) litigation regime. While over 95% of our

observations have Big5 auditors (thereby precluding meaningful analysis of the effects of audit

firm type on accruals), our sample offers ample variation with respect to the point in time when

the audit committee is in existence. In over 70% of our IPOs, the prospectus makes reference to

specific individuals as being current members of an audit committee of the board of directors.3

The formation of the audit committee shifts whom the auditor reports to, from the managers to

the audit committee, and provides additional discipline on the audit and financial reporting

2 Our findings and inferences do not change when we compute abnormal accruals in accordance with the methods that Teoh, Wong and Rao (1998) / Teoh, Welch and Wong (1998) and Kothari, Leone and Wasley (2005) use. 3 Per Klein (2002b), starting in December 1999, all NYSE and NASDAQ companies must have audit committees containing at least three independent directors. Since our sample starts with companies that successfully went public during January 2000, all of our observations must comply with this requirement, once their shares begin to trade. Our interest is whether the audit committee exists prior to the IPO date (i.e., during the 1933 Act regime) and the relation between the existence of an audit committee and audit quality.

5

process. For issuers that refer to the existence of an audit committee in their prospectus, pre-IPO

accruals are both significantly negative and much smaller than post-IPO accruals. Moreover,

pre-IPO accruals are more negative for issuers that refer to an audit committee in their

prospectus in contrast those that do not state this reference. Overall, our results support the view

that auditors, particularly when an audit committee exists, afford issuers less accounting

discretion in their pre-IPO financial statements. In other words, audit quality seems higher in a

higher litigation regime.

In addition to the policy importance of auditor litigation reform, our paper contributes to

the accounting, corporate governance, finance and legal literatures. For one, we provide U.S.-

based support for the “litigation risk-audit fee hypothesis” (Seetharaman, Gul and Lynn 2002) as

we find audit fees are increasing in auditor litigation exposure. Our setting enables us to study

audit fee in both levels and changes, each of which demonstrates the importance of considering

the auditor’s liability exposure. For another, we extend Klein (2002b), which documents an

inverse relation between audit committee independence and the absolute value of abnormal

accruals for a sample of large, publicly traded firms. We consider a pre-public setting, wherein

companies have incentives to overstate earnings, and report evidence of an inverse relation

between the presence of an audit committee and signed abnormal accruals.

We also contribute to the literature on earnings management in IPOs (Teoh, Wong and

Rao 1998; and Teoh, Welch and Wong 1998). In general, these papers find that accruals for

issuing firms are unusually high and suggest that earnings are opportunistically inflated and

investors are systematically misled. These papers argue that constraints on manager’s incentives

to manage earnings are imperfect; particularly auditors, who are hamstrung when confronted

with earnings management within the boundaries of GAAP. However, the probability of auditor

litigation is likely increasing in positive accruals (Heninger 2001) and, for an IPO audit,

securities laws place an extra onus on auditors. Consistent with this alternative view, we find

that pre-IPO accruals are negative and less than post-IPO accruals.

6

Our paper also has some implications for the legal literature on “issuer choice”. This

research challenges the federal securities regime, proposing instead a “system of competitive

federalism” (Romano 1998; Tung 2002). Advocates contend that issuers should have the choice

of regulatory regime, arguing for a competitive market wherein companies choose a “sovereign”

(federal or state government or foreign country) to regulate transactions in their securities.

Romano (1998, p. 2372, 2428) criticizes the current federal regime:

“The difficulty of discerning an affirmative impact on investors from the federal regime…supports abandoning its exclusivity…the near total absence of measurable benefits from the federal regulatory apparatus surely undermines blind adherence to the status quo…The mandatory federal securities regime has been in place for over sixty years, but the theoretical support for it is thin, and there is no empirical evidence indicating that it is effective in achieving its stated objective.” (italic emphasis added)

Our findings suggest that the liability regime under the 1933 Act and conditions in the

IPO market may be more conducive to high-quality audits than the liability regime under the

1934 Act and market conditions for regular audits. By documenting evidence consistent with

higher quality for IPO audits, we offer some empirical support for the federal securities system

put in place by the 1933 Act (at least as it differs from the 1934 Act regime).

The remainder of this paper is as follows: Section 2 surveys relevant institutional details

and literature, Section 3 details the sample and descriptive statistics, Sections 4 and 5 provides

our analyses of audit fees and accounting accruals (respectively), and Section 6 concludes.

2. Background and Motivation

This section contains four sub-sections. Section 2.1, summarizes the differences between

the Securities Act of 1933 (the 1933 Act) and the Securities Exchange Act of 1934 (the 1934

Act) in terms of the auditor’s responsibilities and legal liability. Section 2.2 reviews the

literature examining the audit fees / auditor’s legal liability relation and its applicability to our

IPO setting. Section 2.3 discusses the connection between litigation risk, audit fees and audit

quality. Section 2.4 discusses literature pertaining to earnings management in IPOs.

7

2.1 AUDITOR RESPONSIBILITIES AND LIABILITIES UNDER FEDERAL SECURITIES LAWS

While the auditor’s primary responsibility, in either an IPO or non-IPO engagement, is to

express an opinion on the financial statements, there are some notable differences in auditor

responsibilities for 1933 Act filings. For one, the independent accountants’ responsibility for the

financial statements does not end as of the date of their report, but extends until the effective date

of the registration statement (the “keeping current” requirement). For another, the auditor must

read the entire registration statement to ensure its textual portions are not in conflict with the

financial statements and disclosures and that all material facts that could affect a potential

investor are properly disclosed. Lastly, the auditor usually provides a “comfort letter” to the

underwriter. Underwriters request such letters, as part of their due diligence activities, to obtain

assurance from the auditor regarding financial information in the registration statement that is

not covered by the auditor’s report and on events subsequent to the audit report date.

In addition to these differences in responsibilities, the external auditor’s legal exposure is

more severe under the 1933 Act than under the 1934 Act. While the auditor liability differences

between these two securities acts are numerous, the heightened exposure under the 1933 Act is

largely due to: 1) the auditor’s above-mentioned requirement to “keep current”; 2) a shift in the

burden of proof from plaintiff to (auditor) defendant; 3) that neither privity with the plaintiff nor

their reliance on the financial statements is a necessary condition to bring suit; and, lastly 4) that

“ordinary negligence” is a basis for liability to 3rd parties.

The first of these, the accountant’s requirement to “keep current”, mandates that auditors

ensure that the financial statements are fairly stated up until the effective date of the registration

statement. Per Section 8(a) of the 1933 Act, a registration statement becomes “effective” twenty

days following its initial filing, though each time the registrant amends the filing a new twenty-

day waiting period begins. This requirement to keep current dramatically expands the auditor’s

liability (e.g., the 1968 case of Escott et al. v. BarChris Construction Corporation). The second

of these, the shift in the burden of proof, is unique within common or statutory law. Whereas in

a Rule 10b-5 of the 1934 Act action, the burden of proof that the auditor acted fraudulently rests

8

with the plaintiff, under Section 11 of the 1933 Act, the burden of proof that the auditor was not

culpable rests with the defendant-auditor. Thus, as this relates to the third and fourth auditor

liability differences: under the 1933 Act, a lawsuit may be brought by any IPO investor, and the

auditor must respond by demonstrating that an adequate audit was conducted; in the sense that

there was not an absence of due diligence (i.e., that they are not guilty of ordinary negligence).

2.2 THE LITIGATION RISK — AUDIT FEES RELATION

A stream of accounting literature, dating back 25 years, relates audit fees with the

auditor’s exposure to losses from legal liability. To begin, Simunic (1980) proposes a model

wherein audit fees are a linear combination of the marginal cost of auditing plus expected losses

from litigation. The two components are interrelated, in that additional effort increases the

resource-based cost of performing the audit while decreasing expected litigation losses. As

Simunic and Stein (1996) discuss in their survey of the U.S. literature, this inverse relation

occurs for two reasons. By expending greater effort, auditors are more likely to detect material

misstatements and satisfy GAAS, thereby mitigating each of the conditions necessary to bring

successful litigation against auditors. Overall, while Simunic and Stein (p. 126) conclude that

the evidence is generally consistent with a positive relation between audit fees and litigation risk,

they emphasize that this relation “… is statistically not very strong.” This absence of strong

evidence accords with the common refrain from audit practitioners that they typically cannot

adequately price litigation risk, a recent example of which is:

“Auditors claim they bear the brunt of any financial damages sought because they have deep pockets and are often ‘the last man standing’, says Sam DiPiazza, chief executive of PWC. In effect, auditors have become the insurers of financial statements, writing what Mr. Fusco [a partner with Grant Thornton] likens to a naked (ie, unhedged) option: ‘You get unlimited exposure for a limited reward’ he says.” (The Economist 2004)

As Simunic and Stein (1996) also discuss, Beatty (1993, p. 296) is the first paper to focus

on the connection between litigation risk and audit fees; a relation he characterizes as “…the

legal liability hypothesis…that as the expected losses from imposition of legal liability increase,

the audit fee will increase, ceteris paribus”. Beatty reports a positive relation between all non-

underwriting expenses (a proxy for IPO audit fees) and three ex post measures of exposure to

9

legal liability: security delisting, company bankruptcy and lawsuits. Willenborg (1999) extends

Beatty (1993) with an ex ante measure, by showing that pre-IPO audit fees are increasing in the

amount of money the IPO raises. Because the 1933 Act establishes proceeds as an upper limit on

damages, Willenborg (1999, p. 226) suggests this association provides “…support for the notion

that audit firms adjust their fees for situations which (definitionally) involve increased insurance

exposure”. That is, IPO proceeds provide an ex ante measure of the implicit insurance coverage

auditors provide to investors. Seetharaman, Gul and Lynn (2002) examine audit fees paid by

U.K. companies that sell their securities in U.S. equity markets. They report evidence consistent

with the “litigation risk-audit fee hypothesis”, in that audit fees are adjusted upward to reflect the

increase in litigation liability present in the U.S. for auditors of these U.K.-based companies.

As with Seetharaman et al. (2002), we exploit differences between litigation liability

regimes, though within a national context. We compare audit fees paid by the same company, as

it transitions from 1933 Act to 1934 Act liability regimes, enabling us to extend the literature

with a capital markets test of the litigation risk-audit fee hypothesis in both levels and changes.

2.3 THE CONNECTION BETWEEN LITIGATION RISK, AUDIT FEES AND AUDIT QUALITY

The prediction that audit fees reflect differences across litigation regimes has implication

for audit quality. If auditors respond to an increase in liability exposure with an increase in

effort, this should decrease expected litigation losses (Simunic 1980). Dye (1993) formalizes the

relation between litigation liability exposure, audit quality and audit fees. Dye models the audit

as consisting of both informational and liability components and demonstrates conditions under

which the auditor’s wealth serves as a bond to ensure a high-quality audit. He provides an

equilibrium audit pricing equation that combines the market for auditors with the market for the

companies that hire them. In addition to showing that audit quality is a function of the auditor’s

at-risk wealth, Dye (1993) provides the conditions under which audits are priced such that they

contain a component relating to the option that financial statement users have on this wealth.

10

The relation between audit fees, audit quality and the claim on the auditor’s wealth that

financial statement users have in the case of an audit failure motivates our paper. If audit fees

are a nested function of audit quality and litigation exposure, then the 1933 Act – 1934 Act

threshold suggests certain empirical predictions. Because of the additional liability that the 1933

Act imposes on auditors, and the corresponding increase in the extent to which the auditor’s

wealth serves as a bond, both quality and fees should be higher for IPO audits. Alternatively,

given the decline in the auditor’s litigation liability exposure, both audit fees and audit quality

should decline for newly-public companies. We test these relations using recent proxy statement

disclosures of audit fees, the 1933 Act to 1934 Act decrease in the auditor’s exposure to potential

litigation, and abnormal accounting accruals as a proxy for audit quality.

2.4 ACCOUNTING ACCRUALS AT THE TIME A COMPANY RAISES INITIAL EQUITY CAPITAL

Our use of accruals as a proxy for audit quality has implications for papers (Teoh, Wong

and Rao 1998; Teoh, Welch and Wong 1998) that report companies going public have unusually

high abnormal accruals in the fiscal year of their IPO (issue-year accruals). As Teoh, Welch and

Wong (1998, p. 1937-1938) argue, “[t]he IPO process is particularly susceptible to earnings

management, offering entrepreneurs both motivation and opportunities to manage earnings … If,

as we hypothesize, investors are unable to understand fully the extent to which IPO firms engage

in earnings management by borrowing from either the past or the future, high reported earnings

would translate directly into a higher offering price.” These papers note that the limitations on

these motivations are not perfect, particularly the extent to which the auditor can constrain the

IPO entrepreneur’s earnings management. The auditor’s primary responsibility is to express an

opinion on whether the financial statements are in accordance with GAAP and that “sufficient

flexibility may be permitted within GAAP to allow for substantial earnings management …

auditors, in turn, generally defer to management’s judgement on discretionary accrual items that

do not explicitly violate GAAP” (Teoh, Wong and Rao 1998, p. 178).

11

While this argument has merit, it neglects two concerns: first, auditors are held to a

higher legal standard when conducting an IPO engagement vis-à-vis a post-IPO engagement; and

second, consistent with Heninger (2001), the probability that the auditor is named in a lawsuit is

likely increasing in client abnormal accruals. As such, following Dye’s (1993) connection

between audit quality and the investor’s claim on the auditor’s wealth, the degree to which

auditors accede to management’s within-GAAP aggressiveness on discretionary accruals should

vary (increase) across the going-public threshold.

It is also important to emphasize that Teoh, Wong and Rao (1998) and Teoh, Welch and

Wong (1998) do not use pre-IPO financial statement information to calculate accruals. Arguing

that incentives exist to motivate entrepreneurs to continue to book income-increasing accruals

during the period after the offering and up until the company’s year-end, both of these papers

conduct large-sample studies of accruals in the fiscal year of the company’s IPO (i.e., accruals

data are from the issuer’s first public financial statement). In contrast, we use pre-IPO financial

statement information to compute pre-IPO accruals; which we compare to post-IPO accruals,

which we compute using post-IPO financial statement information. Put another way, because we

focus on the auditor’s work across the going-public threshold, we trade off the costs of a

somewhat smaller sample for the benefits of an arguably cleaner measure.

To summarize Section 2, given the heightened litigation risk that an IPO portends and its

effects on audit quality and audit fees, we expect that when conducting an IPO audit, auditors

should receive higher fees and the ensuing financial statements should be of higher quality.

3. Sample and descriptive statistics

In this section, we discuss the sample and descriptive statistics for our analysis of

companies that clearly provide proxy statement disclosure of both pre- and post-IPO audit fees.

12

3.1 DATA COLLECTION

Our objective is to collect a sample of companies for which we can reliably identify the

amount of their audit fees for both their IPO audit and their subsequent annual audit. We start

with firms that go public on or after January 1, 2000 because the SEC mandates disclosure of

information about the fees that registrants pay to their certifying accountant beginning with

proxy statements filed on or after February 5, 2001 (SEC 2000). We end with firms that go

public on or before December 31, 2002 because our accruals analysis requires that we compute

post-IPO accruals. We begin by identifying the 454 firm-commitment IPOs from January 2000

to December 2002 from the Securities Data Corporation (SDC) database with valid cusip

identification numbers. We then search the Lexis/Nexis database and obtain the first proxy

statement that, subsequent to the IPO, the company files with the SEC. From these proxy

statements, we then hand-collect both pre-IPO and post-IPO audit fee information. To be in the

final sample for our audit fees analysis, a company must file a proxy statement that clearly

discloses both the fee for the IPO audit and the fee for the 1st post-IPO annual audit.4 We

emphasize this because proxy statement disclosure of the IPO audit fee is voluntary. We use this

sample to examine the determinants of, and changes in, audit fees across the pre-IPO to post-IPO

threshold. We then analyze pre- versus post-IPO accruals for the subset of these observations

with sufficient data. To provide assurance that the results of this analysis are not subject to a

selection bias, we also analyze pre- versus post-IPO accruals for these IPOs in combination with

IPOs with sufficient accruals and other data that we do not include in our audit fees analysis.

4 Our sampling approach, to collect IPO audit fees from an issuer’s first proxy statement, differs from the extant literature (e.g., Beatty 1993; Willenborg 1999; Mayhew and Wilkens 2003) that surrogates IPO audit fees using information issuers report to the SEC regarding either all non-underwriting expenses or accounting fees they pay in connection with the issuance and distribution of the IPO securities. Per SEC guidelines, this amount may combine all payments to the registrant’s audit firm and, moreover, may be estimates. We obtain these amounts, available from SDC, for 122 of our sample 142 IPOs. For these 122 observations, the Pearson correlation between our proxy-statement based measure of IPO audit fees and the amount of accounting fees per SDC is 0.88. We also run the Equation (1c) regression using these 122 observations, substituting the dependent variable between our proxy-statement based measure and the SDC measure. When we compare the parameter estimates some differences exist; in particular, Leverage emerges as (unexpectedly) negatively associated with the SDC-based measure of audit fees. All in all, we believe that our proxy-statement based measure of IPO audit fees has less measurement error than the SDC-based measure; however, this point seems relatively minor with respect to the findings in the extant literature.

13

Of these 454 IPOs: 32 companies either do not have a proxy statement available on the

Lexis/Nexis database or have a proxy but it does not disclose audit fee information; 10

companies have proxy statements that disclose audit fee information, but combine audit fees for

the 1st post-IPO annual audit with those for the IPO audit; 124 companies have proxy statements

that disclose audit fee information for the 1st post-IPO annual audit, but not for the IPO audit5;

139 companies have proxy statements that disclose audit fee information, but combine audit fees

for the IPO with non-audit fees for the IPO.6 Of the remaining 149 companies, data was either

missing or insufficient from Compustat with regard to the covariates for our audit fee analysis

for seven companies. The final sample for our audit fees analysis consists of 142 companies that

went public during the 2000-2002 period for which we are able to reliably ascertain both the pre-

and post-IPO audit fees they pay for external auditing (Table 1).

3.2 DESCRIPTIVE STATISTICS – AUDIT FEES ANALYSIS OBSERVATIONS

Table 2 presents descriptive statistics for these 142 companies. As we discuss, we hand

collect audit fees from the 1st proxy statement that the company files with the SEC. We obtain

financial statement information from Compustat and, for the pre-IPO (post-IPO) year, we ensure

that this information is from the most-recent (first-available) financial statements prior to (after)

the day of the company’s IPO. We hand collect much of the remaining information (e.g., audit

firm type, change in auditors, registration form type) from the issuer’s final prospectus.

As per Table 2, audit fees for the IPO are higher than audit fees for the first, post-IPO

annual audit. Moreover, as per our analysis of audit fee changes in Section 4.2, audit fees

decline in the post-IPO period for almost 90% (127 of 142) of our sample. Table 2 also provides

information on the covariates in the audit fee analysis to follow. The increase in total assets,

from pre-IPO to post-IPO, corresponds with the descriptive statistics on proceeds. Moreover, as

5 Mean (median) post-IPO AuditFees for these 124 companies are $222.0 ($167.5) million, somewhat smaller than mean (median) $297.9 ($176.5) million post-IPO AuditFees for the 142 companies in our final sample (see Table 2). 6 To ensure that we do not bias our findings towards higher fees for IPOs, we include firms in our sample when we can clearly identify the amount of the IPO audit fee. Many of the 139 firms that we exclude disclose the auditing, consulting and tax advisory fees for the IPO, but do so by grouping them together as IPO-related accounting fees.

14

of the post-IPO year, companies have less debt and sustain smaller bottom-line losses. More

than one-quarter of our sample (26.1%) disclose either a change in audit firm or more than one

audit firm in the “experts” section of their final IPO prospectus.7 Lastly, for over 70% (100 of

142) of our sample companies, the IPO prospectus refers to the existence of an audit committee.

Typically, we locate this reference in the “Management” section of the IPO prospectus wherein

the issuer states that certain directors presently serve on an audit committee of the Board.

4. Audit fee analysis — pre and post IPO

4.1 AUDIT FEE LEVELS

We begin by examining audit fee levels for companies as they cross the 1933 Act – 1934

Act threshold. Following the extant audit-fee literature (e.g., Beatty 1993; Menon and Williams

2001; Seetharaman et al. 2002), we control for company size, the percentage of assets in

inventories and receivables, leverage, profitability and auditor type. Because we focus on the

connection between litigation risk (as it varies by securities act) and audit fees, we control for

whether the company operates in a litigious industry (Francis, Philbrick and Schipper 1994).8

Equation (1a) provides our baseline regression. We then append it with an indicator variable for

whether or not the audit engagement pertains to the company’s IPO, as per equation (1b).

Ln(AuditFees)i,t = β0 + β1Ln(Assets)i,t + β2InvReci,t + β3Leveragei,t + β4ROAi,t + β5Lossi,t + β6LitRiski,t + β7Big5i,t + εi,t (1a)

Ln(AuditFees)i,t = β0 + β1Ln(Assets)i,t + β2InvReci,t + β3Leveragei,t + β4ROAi,t + β5Lossi,t + β6LitRiski,t + β7Big5i,t + β8IPOi,t + εi,t (1b)

Where: Ln(AuditFees) = Ln(Audit fees) Ln(Assets) = Ln(Total assets)

7 See Menon and Williams (1991) for a study of pre-IPO auditor changes, which occurs for 14% (20 of 142) of our sample. In addition, 21% (30 of 142) of our sample companies mention more than one audit firm in the “experts” section of their prospectus. Because the Spearman correlation between these two is 0.435 (e.g., a registrant may change their audit firm for the most recent audited financial statements in the prospectus, but the older statements in the prospectus are audited by their previous audit firm), we combine them to specify our New/n>1Auditors variable. 8 We do not specify control variables for the number of subsidiaries or whether the company has foreign operations because these likely do not vary from pre-IPO to post-IPO. In addition, only one of the 142 companies in our sample went public with a going-concern audit opinion; and coefficients change very little when we exclude this observation. As such, we do not consider an audit opinion variable in our audit fee and accounting accrual analyses.

15

InvRec = (Inventory + Receivables) / Total assets Leverage = Debt / Total assets ROA = Net income / Total assets Loss = One if negative Net income and zero otherwise LitRisk = One if firm’s primary SIC is 2833-2836, 3570-3577, 3600-3674, 5200-5961, or 7370-

7374 and zero otherwise (i.e., whether the company operates in one of four industries – biotechnology, computers, electronics and retailing – with a high incidence of accounting-related litigation)

Big5 = One if a Big5 audit firm and zero otherwise IPO = One if the IPO year and zero otherwise

The results of estimating the equation (1a) and (1b) regressions, as columns one and two

of Table 3 show, are consistent with extant literature. Audit fees are positively associated with

total assets (Ln(Assets)) and the percentage of audit-intensive assets (InvRec); and inversely

associated with company profitability (ROA). Consistent with Table 2, audit fees are higher for

IPO engagements vis-à-vis subsequent year-end engagements. Considering whether the audit

pertains to the IPO engagement increases the regression’s adjusted R2 from 27.0% to 50.4%.

That audit fees are higher for IPOs is likely due to increases in auditor responsibilities

and auditor litigation exposure. To pursue this, we focus on the IPO year and supplement

equation (1a) with five covariates. We include an indicator variable (IPOAC) for whether the

IPO prospectus refers to the existence of an audit committee. While we do not have a directional

expectation for IPOAC’s coefficient, we anticipate that the remaining four covariates will be

positively associated with IPO audit fees. The first of these is whether the prospectus discloses a

change in the registrant’s audit firm or mentions more than one audit firm in the “Experts”

section (New/n>1Auditors). The next two, whether the issuer files an S-1 registration statement

(S-1) and the natural logarithm of number of registration statement amendments (Ln(#Amend)),

proxy for the extra work that an IPO audit requires (e.g., the “keeping current” requirement).

The fourth variable (Ln(Proceeds)) is a proxy for the auditor’s litigation risk exposure for IPO

audits. As IPO proceeds increase, so does the amount at risk in a possible securities suit, and

IPO size is a measure of the insurance coverage auditors provide to investors (Willenborg 1999).

Ln(AuditFees)i,t = β0 + β1Ln(Assets)i,t + β2InvReci,t + β3Leveragei,t + β4ROAi,t + β5Lossi,t + β6LitRiski,t + β7Big5i,t + β8IPOACi,t + β9New/n>1Auditorsi,t + β10S-1i,t + β11Ln(#Amend)i,t + β12Ln(Proceeds)i,t + εi,t (1c)

16

Where: IPOAC = One if the IPO prospectus refers to the presence of an audit committee and zero otherwise New/n>1Auditors = One if the IPO prospectus either discloses a change in the registrant’s auditor or mentions

more than one auditor in the “experts” section and zero otherwise S-1 = One if IPO issuer files an S-1 SEC registration statement and zero otherwise Ln(#Amend) = Ln(Number of SEC registration statement amendments that IPO issuer files) Ln(Proceeds) = Ln(Gross proceeds from the IPO)

Column four of Table 3 shows the results of estimating equation (1c). For comparability,

we estimate equation (1a) for these IPO observations (column three). Both New/n>1Auditors

and Ln(Proceeds) are positively associated with IPO audit fees.9 Moreover, the coefficient on

Ln(Proceeds) is more than three times that of Ln(Assets), and its significance is despite a Pearson

correlation with Ln(Assets) of 0.842. Because equation (1c) is a double-log specification, the

coefficients on Ln(Assets) and Ln(Proceeds) are elasticity estimates (i.e., the % change in audit

fees divided by the % change in either assets or proceeds). An economic interpretation of the

elasticity between IPO proceeds and IPO audit fees suggests that, about the mean of these

variables, a 1% increase in average IPO proceeds (per Table 2, $182.349 million * 0.01 or

$1,823,500) is associated with a 0.352% increase in average pre-IPO audit fees (per Table 2,

$612.240 thousand * 0.00352 or $ 2,155) increase in pre-IPO audit fees. That is, each additional

$1 million in IPO proceeds is associated with an increase in IPO audit fees of approximately

$1,200. Column five shows the results of estimating equation (1a) using the post-IPO year

observations and, consistent with the extant literature, much of this regression’s explanatory

power stems from the association between company size and audit fees.

In summary, the Table 3 results show that pre-IPO audit fees are higher than post-IPO

audit fees, ceteris paribus, and document the strong positive association between IPO proceeds

and IPO audit fees (Willenborg 1999; Mayhew and Wilkins 2003). Because the 1933 Act

establishes proceeds as an upper limit on damages, the amount an IPO raises is a proxy for the

implicit insurance coverage auditors provide to investors. Following this, we show that pre-IPO

audit fees are strongly, positively associated with the auditor’s litigation exposure. 9 Despite the audit extra effort (e.g., examining two balance sheets and three income statements) that it proxies for, the variable S-1 is not statistically significant in the equation (1c) estimation results. This is likely because, as Table 2 shows, 93% (132 of 142) of the companies in our sample file an S-1 registration statement.

17

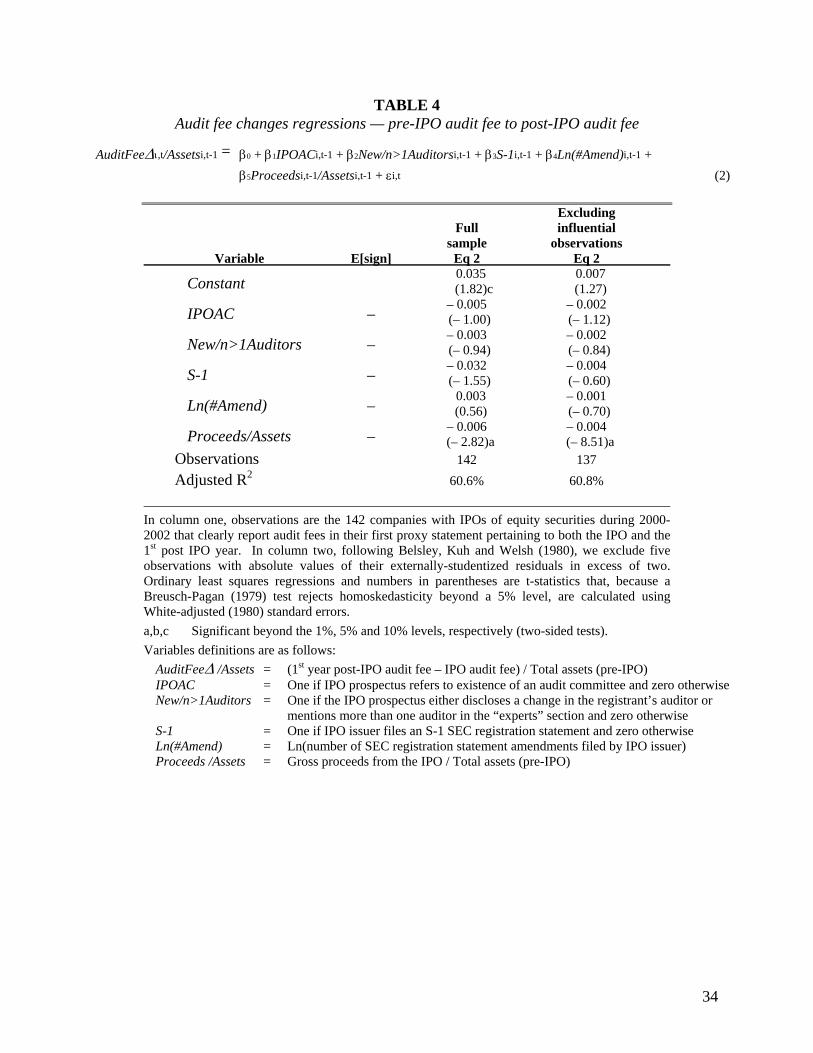

4.2 AUDIT FEE CHANGES

An arguably stricter test of the litigation risk-audit fee hypothesis in our setting is to

analyze the change in fees, from IPO audit to post-IPO audit. The above analysis shows that

audit fees are considerably higher for the IPO and are positively associated with variables that

proxy the extra effort and litigation exposure that such audits involve. It does not test whether

the change in audit fees is associated with variables that proxy for this effort and exposure.

As we mention in Section 3.2, audit fees decline for almost 90% (127 of 142) of our

sample companies. Figure 1 presents a histogram of audit fee changes (post-IPO audit fee minus

IPO audit fee). As this figure shows, of the 127 newly public companies with lower post-IPO

audit fees, two companies (Accenture and Agere Systems) experience very substantial decreases.

These two offerings are among the very largest, in terms of gross proceeds, in our sample. That

they are among the largest IPOs and experience large declines in audit fees is consistent with the

litigation risk-audit fee hypothesis. Put another way, because these IPOs are very large, their

audit fee include a large (1933 Act) litigation risk component. However, large companies often

have large IPOs. Indeed, these two companies are also among the very largest, in terms of pre-

IPO assets, in our sample. As such, they also illuminate the importance of scale effects; in that,

because they are among largest companies in our sample, it seems reasonable that they might be

among the companies with the largest changes in audit fees. Because large companies pay large

audit fees, large companies are obvious candidates for large decreases in audit fees.

To study the relation between audit fee changes (from IPO audit to post-IPO audit) and

the extra auditor responsibilities and litigation exposure that are associated with IPO audits, we

specify equation (2). The right-hand side variables are those extra variables that we specify in

equation (1c) as being particular to the IPO engagement. To accommodate the scale effects that

we discuss above, we deflate both the change in audit fees and IPO proceeds by pre-IPO assets.

To the extent that IPO proceeds serve as an adequate ex ante proxy for the auditor’s litigation

exposure, this is an arguably stronger test of the litigation risk-audit fee hypothesis.

18

AuditFee∆ i,t/Assetsi,t-1 = β0 + β1PreIPOACi,t-1 β2New/n>1Auditorsi,t-1 + β3S-1 i,t-1 + β4Ln(#Amend) i,t-1 + β5Proceeds i,t-1/Assets i,t-1 + εi,t (2)

Where: AuditFee∆ /Assets = (1st year post-IPO audit fee – IPO audit fee) / Total assets (pre-IPO) Proceeds /Assets = Gross proceeds from the IPO / Total assets (pre-IPO)

Column one of Table 4 presents the results of estimating the equation (2) regression. A

Breusch-Pagan (1979) test indicates a high degree of heteroskedasticity and White-adjusting

(1980) the standard errors has a dramatic effect on the significance of Proceeds/Assets. Prior to

adjustment, the t-statistic for Proceeds/Assets is –14.69, whereas afterwards, it is –2.82 (Table

4). Further diagnostics reveal five influential observations that, following Belsley, Kuh and

Welsh (1980), have absolute values of their externally-studentized residuals in excess of two.

Column 2 of Table 4 re-estimates the equation (2) regression after excluding these observations.

While Proceeds/Assets’s coefficient changes from –0.006 to –0.004, elimination of these outliers

leads to a more precise estimate, as its White-adjusted t-statistic changes from –2.82 to –8.51. In

summary, almost 90% of our sample companies pay lower audit fees as first-year public

companies than they do to go public, and the extent of this change in audit fees is strongly

correlated with our proxy for ex ante litigation risk exposure, IPO proceeds.

Overall, the findings in Section 4 support the view that, in the IPO market, conditions are

such that auditors receive higher fees for the heightened exposure to litigation risk that the 1933

Act portends. Following this, the extent (removal) of this exposure helps to explain the level of

IPO audit fees (the decline from IPO audit fees to post-IPO audit fees). Consistent with Dye

(1993), the increase in the option on the auditor’s wealth that an IPO audit implies increases the

audit’s price. In addition, our findings are consistent with the empirical literature on audit

production (O’Keefe, Simunic and Stein 1994; Stein, Simunic and O’Keefe 1994; and Bell,

Landsman and Shackelford 2001), that both report auditor hours increasing in partner

assessments of inherent and business risk. In our setting, it seems plausible that auditors expend

effort in accordance with their litigation liability risk exposure (which we proxy with proceeds).

19

5. Accounting accruals analysis — pre-IPO and post-IPO

The scope of Dye (1993) extends beyond formalizing the connection between audit fees

and the investor’s option on the auditor’s wealth. He also demonstrates conditions under which

the auditor’s wealth serves as a bond for audit quality. Following this, and given the increase in

litigation exposure for auditor when conducting an IPO audit (in terms of the investor’s claim on

the auditor’s wealth in the event of an audit failure), we also test for differences across the 1933

Act – 1934 Act threshold with regard to audit quality. We conduct two types of tests to

determine whether audit firms allow their IPO clients an increase in accounting discretion. First,

we test whether signed pre-IPO abnormal accruals statistically differ from zero. Second, we

compare pre-IPO versus post-IPO signed abnormal accruals. Each of these tests has strengths

and weaknesses.10 By conducting both types of tests, we can better examine the impact of IPO-

related litigation risk on audit quality; assessing, in particular, whether abnormal accruals in the

pre-IPO period appear to be opportunistic or conservative. In addition, for reasons we discuss

below, we also partition our samples by whether the IPO prospectus refers to the existence of an

audit committee and by whether the company reports a profit for the pre-IPO period.

We calculate total accruals and abnormal accruals per the Jones (1991) and modified-

Jones (Dechow, Sloan and Sweeney 1995) models. We use both balance sheet and statement of

cash flows approaches (Hribar and Collins 2002) to obtain total accruals.11 Given the increase in

assets that accompany going public, choice of a scaler is not clear. In particular, the practice of

deflating accruals by lagged assets is problematic because it results in many values in excess of

10 By examining whether signed pre-IPO abnormal accruals are statistically different from zero, we can test whether IPO company accounting choices appear, on the whole, conservative or opportunistic. However these tests suffer from the concern that IPO companies are inherently different from non-IPO companies, and that abnormal accruals for IPO companies are noisy. By examining accruals for the same companies, at two different points in time (pre-IPO and post-IPO) we allay the criticism, particularly relevant for studies of earnings management at the time of security issuance, that issuing firms are growth firms and accrual measures commingle performance with discretion. However, these tests suffer from the concern that accruals are likely to be negatively serially correlated. 11 We also compute accruals in accordance with the methodology that Teoh, Wong and Rao (1998) and Teoh, Welch and Wong (1998) use (i.e., we split total current accruals into a non-discretionary component, via an out-of-sample estimation approach, and a discretionary component). Though, in contrast to these papers, we use pre-IPO financial statement information to compute pre-IPO accruals. When we do this, our findings and inferences do not change (e.g., we continue to find that both total current accruals and discretionary current accruals are smaller, more negative, in the pre-IPO period).

20

100% (e.g., scaling accruals from post-IPO financial statements using assets from pre-IPO

financial statements). Because of this, we deflate by average assets in Tables 5 and 6.12

Of the 142 companies in our audit-fees sample, 113 have necessary data to compute our

measures of accruals.13 Table 5 presents accrual information and tests: Panel A relates to all 113

companies; Panel B parses these companies into sub-samples by whether the IPO prospectus

does or does not refer to the existence of an audit committee; and Panel C parses these

companies into sub-samples by whether the company reports a profit on their most-recently

audited Income Statement in the pre-IPO period.

As Panel A shows, for all six measures of accruals, mean and median pre-IPO accruals

are significantly negative. In addition, pre-IPO accruals are significantly less than first-year

post-IPO accruals, which are typically also negative. Put another way, abnormal accruals are

negative overall and even more so in the pre-IPO period. While our balanced-panel design treats

each company as its own control, the measures of accounting accruals that we display in Table 5

do not otherwise address the difficulty of benchmarking “normal” accruals for a firm in an IPO

setting. These are firms with an unusual inflow of cash, typically needed to fund investments for

growth. We know from the literature that “discretionary” accruals tend to be high for high-

growth firms as they build capacity (e.g., build up inventory). It would not be surprising to find

an increase in abnormal accruals after the IPO, even with no earnings management in any year.

To address this, we compute abnormal accruals in accordance with Kothari, Leone and Wasley’s

(2005) performance-matching approach. While pre-IPO accruals continue to be negative and

less than post-IPO accruals, these post-IPO accruals are positive.

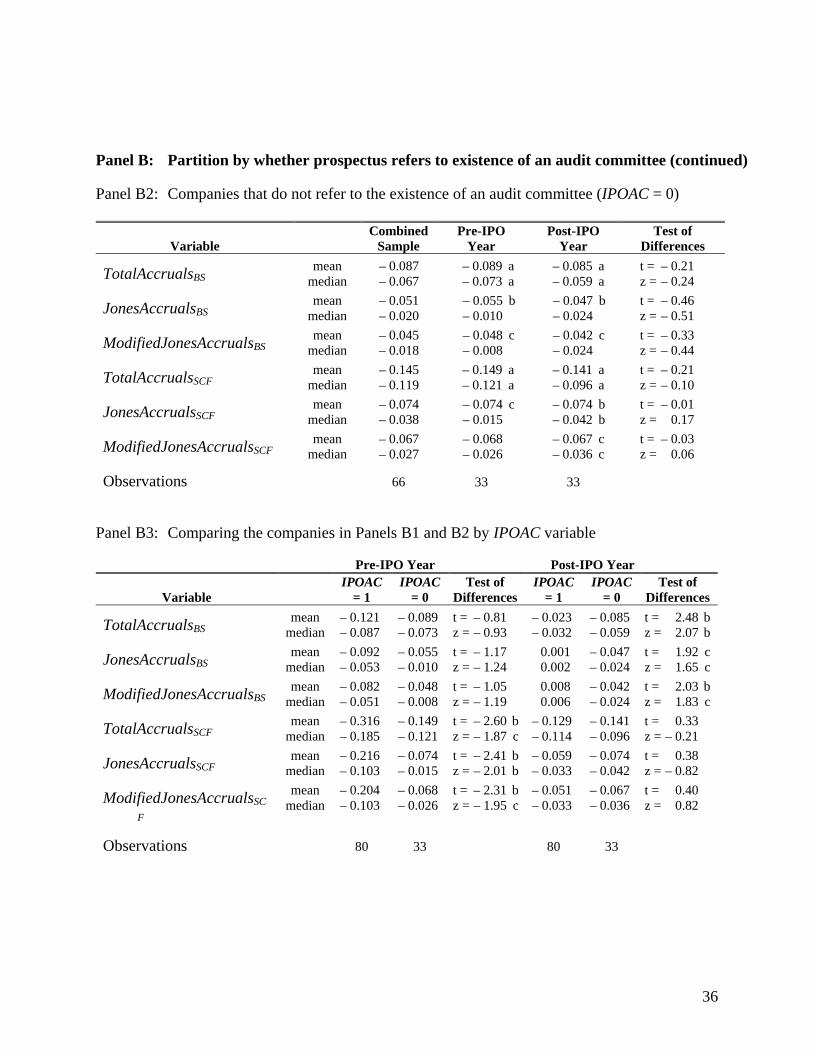

As we discuss, over 70% (100 of 142) of the observations in our audit fees analysis refer,

in their prospectus, to the existence of an audit committee. The presence of an audit committee

12 We note that, regardless of whether we deflate by average assets or lagged assets, we do not find evidence of statistically higher accruals in the pre-IPO period vis-à-vis the post-IPO period. 13 Of these 29 companies that we exclude from this analysis: 14 are financial companies (i.e., SIC 6xxx); three are companies that provide only one balance sheet in their prospectus; and Compustat does not provide (i.e., backfill) the necessary two years of pre-IPO data for the remaining 12 companies.

21

shifts whom the auditor reports to, from management to the audit committee, and safeguards the

independence of the auditor and imposes discipline on the financial reporting processes (Carcello

and Neal 2000). Per Klein (2002a, p. 436-437), “[a]ccording to the Blue Ribbon Committee

Report, the audit committee is the ‘ultimate monitor’ of the financial accounting reporting

system (NYSE and NASD 1999, 7)”. Of the 113 IPOs (of 142) with necessary data to compute

our accrual measures, 80 (33) refer (do not refer) to the existence of an audit committee in their

IPO prospectus. Panels B1 and B2 of Table 5 present accrual information and tests for these 80

and 33 companies, respectively (i.e., by whether the IPOAC variable equals one or zero). Panel

B1 reports findings very similar to those in Panel A. That is, as Panel B1 shows, for issuers that

refer to the existence of an audit committee in their prospectus, pre-IPO accruals are both

significantly negative and less than post-IPO accruals. As for issuers that do not refer to the

existence of an audit committee in their prospectus, Panel B2 reports some evidence of negative

pre-IPO accruals, but these pre-IPO accruals are not more negative than post-IPO accruals.

Panel B3 compares pre-IPO and post-IPO accruals by the IPOAC variable, and shows that

(particularly with a statement of cash flows approach to compute total accruals) pre-IPO accruals

are more negative for companies that refer to an audit committee in their prospectus.

As Table 2 show, the majority (101 of 142, or 71%) of companies in our audit fees

sample sustain pre-IPO bottom-line losses. This begs the question of whether it is reasonable to

expect unprofitable companies to engage in income-increasing earnings management. Of the

113 IPOs (of 142) with necessary data to compute our accrual measures, 26 (87) report a pre-IPO

profit (loss) on the most-recently audited Income Statement in their prospectus. Panels C1 and

C2 of Table 5 present accrual information and tests for these 26 and 87 companies, respectively

(i.e., by whether the ROA variable is positive or negative for the pre-IPO year). As Panel C1 of

Table 5 shows, even for pre-IPO profitable companies, we report scant evidence to support the

view that pre-IPO abnormal accruals are unusually high (Teoh, Wong and Rao 1998). As Panel

C2 of Table 5 shows, for companies that report losses in their pre-IPO Income Statement

22

abnormal accruals are negative and statistically significant in both the pre- and post-IPO periods

and pre-IPO accruals are significantly more negative than post-IPO accruals.14

The sample of companies for which we analyze accounting accruals in Tables 5 is a

subset of the sample of companies for which we analyze audit fees in Section 4. And, as we

discuss in Section 3, these are companies that clearly provide proxy statement disclosure of both

pre-IPO and post-IPO audit fees. It is therefore possible that, because proxy statement disclosure

of pre-IPO audit fees is voluntary and we require that all disclosures unambiguously refer to

audit fees, there is a selectivity bias in this sample of companies (e.g., perhaps they are both

forthright in their proxy statement disclosures and conservative in their accounting accruals). To

address this concern, we replicate the Table 5 analysis for all IPO companies with necessary data

to compute our various measures of accounting accruals. In other words, we no longer exclude

companies because they do no not clearly provide proxy statement disclosure of audit fees. Of

the 312 companies that we exclude in our Table 1 data screens (i.e., 454 minus 142), 252 have

the necessary data to compute our measures of accounting accruals and to discern whether their

prospectus refers to the existence of an audit committee. We combine these 252 companies with

the 113 companies in Table 5 and, in Table 6, report results consistent with those we show in

Table 5 and discuss above.

It is important to discuss that, we report some evidence of positive abnormal accruals in

the post-IPO period for pre-IPO profitable companies (Panels C1 of both Tables 5 and 6). This

is consistent with the literature that finds performance is associated with abnormal accruals

(Kothari, Leone and Wasley 2005) and that computes “issue-year” accruals (i.e., using post-IPO

financial statement information). For example, Teoh, Wong and Rao (1998) report positive

“issue-year” accruals for their sample of over 1,500 IPOs from 1980-1990. However, 76% of

their observations have “issue-year” return on sales greater than zero. In contrast, as we

14 As we discuss, certain IPOs in our sample change their audit firm. Given this, we also compare our accruals measures across the pre-IPO to post-IPO threshold, for these companies in contrast to those of companies that do not disclose a change in their auditor. Regardless of whether a company discloses a change in their audit firm, we find that pre-IPO accruals are more negative than post-IPO accruals.

23

mention, the majority of our sample reports losses. As such, the relevant comparison between

recent published papers and our dataset arguably relates to the sub-sample of our observations

that report profits. However, the focus of our paper is on the threshold from pre-IPO to post-IPO

(and the impact of this regime change on audit quality). In this regard, it is important to

emphasize that, while we observe some evidence of positive accruals in the pre-IPO financial

statements of profitable companies, these accruals are not more positive in the post-IPO year. It

seems plausible that accruals are abnormally positive in the fiscal year of the company’s IPO, yet

not abnormally positive in the pre-IPO year. This is because if auditors respond to the increase

in litigation risk and encourage their clients to make conservative (income-decreasing) accruals

in the pre-IPO year, then the negative serial correlation that arises when accruals reverse may

cause accruals in the fiscal year of the IPO to be positive. However, the inference from this is

not that companies are acting opportunistically to inflate their IPO proceeds. Instead, this

implies that auditors are acting conservatively in the pre-IPO period; and that the presence of

positive post-IPO (i.e., fiscal year of the IPO) accruals is an artifact of this pre-IPO conservatism

and the properties of accruals.15

To summarize, in contrast to the inference that issuers opportunistically inflate accruals

(Teoh, Wong and Rao 1998), our findings do not suggest that IPO companies systematically

engage in earnings management. Our results suggest that auditors, particularly when they report

to an audit committee, afford issuers less discretion in their pre-IPO financial statements.

Overall, our findings support the view that, consistent with their incentives, auditors do not

afford their IPO clients more financial reporting discretion. Put another way, and consistent with

Dye (1993), the 1933 Act appears to be associated with an increase in audit quality.

15 We also note that a recent paper by Li (2004, p. 7) concludes that the Teoh, Welch and Wong (1998) anomaly (i.e., the effect of discretionary current accruals on the pricing of IPOs) is “…a non-pervasive sample- and period-specific phenomenon.”

24

6. Conclusion

We draw from the IPO setting and the recent availability of proxy disclosures of audit

fees to study the relation between the auditor’s exposure to legal liability, audit fees and audit

quality. We examine audit fees and accounting accruals across an exogenous change in litigation

risk (i.e., in our setting, from 1933 Act to 1934 Act). To summarize our findings, in regard to

IPO engagements (where securities law imposes an extra onus on auditors) we find that auditors

receive higher fees and that the financial statements appear to be of higher quality.

Our paper contributes to the U.S.-based audit fee literature by providing evidence that

audit fees reflect litigation risk differences across liability regimes. Of note, the audit fee

difference between the IPO engagement and the post-IPO engagement varies with our proxy for

the insurance coverage that auditors provide to IPO investors. By finding support for the

litigation risk-audit fee hypothesis, our results are consistent with the view that IPO litigation

risk is priced. In addition, we contribute to the corporate governance / earnings management

literature, extending Klein (2002b) with a pre-public setting wherein there are incentives to

overstate earnings. We document a strong inverse relation between the presence of a pre-IPO

audit committee and pre-IPO signed abnormal accruals. Perhaps most importantly, we also

contribute to the recent literature on earnings management in IPOs (Teoh, Wong and Rao 1998;

and Teoh, Welch and Wong 1998). These widely-cited papers show that accruals for IPO firms

are unusually high, suggesting that earnings are opportunistically inflated around the time of the

offering and investors are misled. For some, this inference is troubling; “… the … interpretation

… as indicating that intentional earnings management at the time of security issuance is

successful in misleading investors, makes me uncomfortable … [because it] implies that

financial statement fraud is pervasive at the time of issuance” (Beneish 1998, p. 209-210). In

contrast to these papers, we use pre-IPO financial statements (i.e., dated prior to the date the

company goes public) to compute pre-IPO accruals and report scant evidence to suggest that pre-

IPO accruals are opportunistically high. Our findings support the view that, consistent with the

25

increase in litigation liability they face and audit fees they receive, auditors do not afford their

IPO clients greater accounting discretion.

Our paper may also provide some insights regarding present-day interest in reforming

auditor litigation laws. As we discuss in the Introduction (and provide examples in footnote 1),

some critics argue that the PSLRA of 1995 is a primary source of the recent accounting scandals.

Another example, per Representative Edward J. Markey’s (D-MA) statement to the

Congressional Oversight and Investigations Subcommittee hearing on Andersen’s admission of

shredding, “…this ill-advised law [PSLRA of 1995] has directly contributed to a rising tide of

accounting failures, culminating in the Enron-Arthur Anderson [sic] fiasco. The types of internal

checks and balances that a healthy concern about litigation risk used to create within each

accounting firm has been undermined”. One interpretation of our findings is that, at least in the

context of an IPO audit, there may still be healthy concern about litigation risk.

26

References

Bauder, D. 2002. “Congress can’t complain about securities laws it spawned.” The San Diego Union Tribune February 22, 2002: C3.

Beatty, R. 1993. “The economic determinants of auditor compensation in the initial public offerings market.” Journal of Accounting Research 31(Autumn): 294-302.

Bell, T., W. Landsman and D. Shackelford. 2001. “Auditors’ perceived business risk and audit fees: Analysis and evidence.” Journal of Accounting Research 39(June): 35-43.

Belsley, D., E. Kuh and R. Welsh. 1980. Regression diagnostics. Wiley: New York, New York.

Beneish, M. 1998. “Discussion of: Are accruals during Initial Public Offerings Opportunistic?” Review of Accounting Studies 3 (May): 209-221.

Breusch, T. and A. Pagan. 1979. “A simple test for heteroskedasticity and random coefficient variation.” Econometrica 47 (September): 1287-1294.

Carcello, J. and T. Neal. 2000. “Audit committee composition and auditor reporting.” The Accounting Review 75 (October): 453-467.

Coffee, J. 2002. “Auditors and analysts: An analysis of the evidence and reform proposals in light of the Enron experience.” Prepared statement at the oversight hearing on “Accounting and investor protection issues raised by Enron and other public companies” of the U. S. Senate Committee on Banking, Housing and Urban Affairs (March 5).

Dechow, P., R. Sloan and A. Sweeney. 1995. “Detecting earnings management.” The Accounting Review 70 (April): 193-225.

Dye, R. 1993. “Auditing standards, legal liability, and auditor wealth.” Journal of Political Economy 101 (October): 887-914.

Heninger, W. 2001. “The association between auditor litigation and abnormal accruals.” The Accounting Review 76 (January): 111-126.

Hribar, P., Collins, D., 2002. “Errors in estimating accruals: Implications for empirical research.” Journal of Accounting Research 40 (March): 105–134.

Francis, J., D. Philbrick and K. Schipper. 1994. “Shareholder litigation and corporate disclosures.” Journal of Accounting Research 32 (Autumn): 137-164.

Jones, J., 1991. “Earnings management during import relief investigations.” Journal of Accounting Research 29 (Autumn): 193–228.

Klein, A. 2002a. “Economic determinants of audit committee independence.” The Accounting Review 77 (April): 435-452.

27

Klein, A. 2002b. “Audit committee, board of director characteristics, and earnings management.” Journal of Accounting and Economics 33 (August): 375-400.

Kothari, S.P., Leone, A. and C. Wasley. 2005. “Performance matched discretionary accrual measures.” Journal of Accounting and Economics 39 (January)

Li, X. 2004. “Behavioral explanation for mispricing of IPOs’ discretionary current accruals and impact of firm’s information environment on the information asymmetry.” Unpublished doctoral dissertation, Massachusetts Institute of Technology (June).

Mayhew, B. and M. Wilkins. 2003. “Audit firm industry specialization as a differentiation strategy: Evidence from fees charged to firms going public.” Auditing: A Journal of Practice & Theory 22 (September): 33-52.

Menon, K. and D. Williams. 1991. “Auditor credibility and initial public offering.” The Accounting Review 66 (April): 313-332.

Menon, K. and D. Williams. 2001. “Long-term trends in audit fees.” Auditing: A Journal of Practice & Theory 20 (March): 115-136.

Norris, F. 2004. “Will Big Four audit firms survive in a world of unlimited liability?” The New York Times (September 10): D1

New York Stock Exchange and National Association of Securities Dealers. 1999. Report and Recommendation of the Blue Ribbon Committee on Improving the Effectiveness of Corporate Audit Committees. New York, NY: NYSE and NASD.

O’Keefe, T., Simunic, D. and M. Stein. 1994. “The production of audit services: Evidence from a major public accounting firm.” Journal of Accounting Research 32 (Autumn): 241-261.

Pratt, J. and J. Stice. 1994. “The effects of client characteristics on auditor litigation risk judgments, required audit evidence, and recommended audit fees.” The Accounting Review 69 (October): 639-656.

Romano, R. 1998. “Empowering investors: A market approach to securities regulation.” The Yale Law Journal 107 (June): 2359-2430.

Securities and Exchange Commission. 2000. Final Rule: Revision of the Commission’s Auditor Independence Requirements. File No. S7-13-00. Washington, D.C.: Government Printing Office.

Seetharaman, A., F. Gul and S. Lynn. 2002. “Litigation risk and audit fees: Evidence from UK firms cross-listed on US markets.” Journal of Accounting and Economics 33 (February): 91-115.

Simunic, D. 1980. “The pricing of audit services: Theory and evidence.” Journal of Accounting Research 18 (Spring): 161-190.

28

Simunic, D. and M. Stein. 1996. “The impact of litigation risk on audit pricing: A review of the economics and the evidence.” Auditing: A Journal of Practice & Theory 15 (Supplement): 119-134.

services.” Auditing: A Journal of Practice & Theory 13 (Supplement): 128-142

Teoh S., I. Welch and T. J. Wong. 1998. “Earnings management and the long-run performance of Initial Public Offerings.” Journal of Finance 53 (December): 1935-1974.

Teoh S., T. J. Wong and G. Rao. 1998. “Are accruals during Initial Public Offerings Opportunistic?” Review of Accounting Studies 3 (May): 175-208.

The Economist. 2004. “Called to account: The auditing industry has yet to recover from the damage inflicted by an era of corporate scandals.” (November 20): 73.

Tung, F. 2002. “From monopolists to markets? A political economy of issuer choice in international securities regulation.” Wisconsin Law Review 6: 1363-1433.

White, H., 1980. “A heteroskedasticity-consistent covariance matrix estimator and a direct test for heteroskedasticity.” Econometrica (May): 817–838.

Willenborg, M. 1999. “Empirical analysis of the economic demand for auditing in the Initial Public Offerings market.” Journal of Accounting Research 37 (Spring): 225-238.

29

FIGURE 1 Histogram of audit fee changes — pre-IPO audit fee to post-IPO audit fee

-3000000 -2250000 -1500000 -750000 0

10

20

30

40

50

AuditFeeChange

Figure 1: Sample histogram of AuditFeeChange, the audit fee for the 1st post-IPO year minus the audit fee for the IPO. The number of observations is 142 and the “counts” for each histogram bar (going from left to right are: 1, 1, 2, 2, 4, 4, 3, 8, 26, 44, 32, 9, 4, 1, 1). Each bar represents a $150,000 change in audit fees.

30

TABLE 1

Sample selection

Number of Companies IPOs 2000 – 2002 companies (per SDC database) with valid Cusip numbers 454 less: Companies without a proxy statement (per Lexis/Nexis database), or with a

proxy statement but it does not disclose any audit fee information

32 less: Companies with proxy statements that disclose audit fees, but combine audit

fees for the 1st post-IPO annual audit with those for the IPO audit

10 less: Companies with proxy statements that disclose audit fees for the 1st post-IPO

annual audit, but not for the IPO audit

124 less: Companies with proxy statement that disclose audit fees, but combine audit fees

for the IPO with non-audit fees for the IPO they pay to their audit firm

139 less: Companies with missing or insufficient Compustat data for audit fees analysis 7

Sample of companies for audit fee analysis (Tables 2-4) 142 less: Companies with insufficient data for accruals analysis 29

Sample of companies, with audit fee data, for accruals analysis (Table 5) 113 plus: Companies without audit fee data, yet with sufficient data for accruals analysis 252

Sample of companies, with or without audit fee data, for accruals analysis (Table 6) 365

31

TABLE 2 Sample descriptive statistics —by pre/post-IPO time periods

Variable

Pre-IPO Year (n 142)

Post-IPO Year (n 142)

AuditFees ($thousands)

mean median standard deviation

612.240 413.100 713.768

297.937 176.500 382.590

Assets ($millions)

mean median standard deviation

871.175 40.620

4,631.590

970.508 129.825

4,133.080

InvRec

mean median standard deviation

0.249 0.186 0.223

0.169 0.118 0.171

Leverage

mean median standard deviation

0.251 0.106 0.383

0.090 0.005 0.179

ROA

mean median standard deviation

– 0.489 – 0.180

0.920

– 0.159 – 0.063

0.391

Loss mean 0.711 0.648

LitRisk mean 0.570 0.570

Big5 mean 0.958 0.958

New/n>1Auditor mean 0.261 n/a

S-1 mean 0.930 n/a

IPOAC mean 0.704 n/a

#Amendments

mean median standard deviation

4.923 5.000 2.067

n/a

Proceeds ($millions)

mean median standard deviation

182.349 70.950

490.462

n/a

Observations are the 142 companies with IPOs of equity securities during 2000-2002 that clearly report audit fees in their first proxy statement pertaining to both the IPO and the 1st post-IPO year. Variables definitions are as follows:

AuditFees = Audit fees, as per company proxy statement ($ thousands) Assets = Total assets ($ millions) InvRec = (Inventory + Receivables) / Total assets Leverage = Long-term debt / Total assets ROA = Net income / Total assets Loss = One if net income is negative and zero otherwise LitRisk = One if firm’s primary SIC is 2833-2836, 3570-3577, 3600-3674, 5200-5961, or 7370-

7374 and zero otherwise (Francis, Philbrick and Schipper 1994) Big5 = One if a Big5 audit firm and zero otherwise New/n>1Auditors = One if the IPO prospectus either discloses a change in the registrant’s auditor or mentions