Lippo Karawaci · PDF fileLPKR operates 43 malls throughout Indonesia with total gross ......

18

PLEASE SEE ANALYST CERTIFICATIONS AND IMPORTANT DISCLOSURES & DISCLAIMERS BEGINNING ON PAGE 13. Lippo Karawaci (LPKR) The integrated property developer The most integrated property company Lippo Karawaci (LPKR) has several lines of business streams which separates the company from the rest. Other than its core property business, the company is also exposed to healthcare business, hotel management and funeral homes (non-core businesses). LPKR has property assets in Lippo Village, Lippo Cikarang and Tanjung Bunga, and Makassar (South Sulawesi). In our view, LPKR’s non-core businesses complement the company’s overall performance and act as fat buffers amid unfavorable property market situations. The contribution from healthcare business is becoming larger every year, despite relatively stagnant performances from its hotel and funeral home businesses. The next growth engine: Hospital business Growing health awareness motivates LPKR to drive its healthcare business further. The company is in its early stage of developing 46 hospitals under the brand name “Siloam Hospital”. Due to slowing property market growth (both residential and commercial), LPKR’s performance improvement is strongly supported by healthcare business which is evident by its increasing portion to its total revenue. As of 9M15, healthcare business contributed IDR3r to the company’s revenue (an increase by 24.8% YoY), compared to the total revenue growth of 10.4% YoY to IDR6.8tr. Healthcare business contribution to total revenue came in at 45% in 9M15 compared to 39% a year earlier. Stable revenue growth with CAGR of 28% LPKR delivered revenue growth of 28% CAGR (excluding assets sold to REITS) over the last 4 years (2010 ~ 2014). Healthcare business growth posted a solid 34% CAGR during the same period. We see that LPKR optimizes its healthcare business for complementing its overall business model and buffering earnings volatility stemming from its property business. Initiate coverage with a Trading Buy call We initiate LPKR on Trading Buy rating with target price of IDR1,175 by using DCF method (16.3% upside potential), with WACC of 11.1%. Key risk to our recommendation is lower than expected growth of property sales. FY (Dec) 12/12 12/13 12/14 15/15F 12/16F Revenue (IDRbn) 6,160 6,666 11,655 9,475 11,765 OP (IDRbn) 1,549 1,943 3,809 2,551 3,147 OP Margin (%) 25.1 29.1 32.7 26.9 26.7 NP (IDRbn) 1,060 1,228 2,547 1,508 1,867 EPS (IDR) 46.5 53.9 111.9 65.3 80.9 ROE (%) 9.9 9.6 16.3 8.3 9.8 P/E (x) 21.7 18.7 9.0 15.5 12.5 P/B (x) 2.2 1.8 1.5 1.3 1.2 Note: All figures are based on consolidated basis; NP refers to net profit attributable to controlling interests Source: Company data, KDB Daewoo Securities Research estimates Property Initiation report January 12, 2016 (Initiate) Trading Buy Target Price (12M, IDR) 1,175 Share Price (1/11/16 IDR) 1,010 Expected Return 16.3% Market Cap (IDRbn) 23,308.8 Shares Outstanding (mn) 23,077.7 52-Week Low (IDR) 975 52-Week High (IDR) 1,460 (%) 1M 6M 12M Absolute -10.2 -15.8 -3.3 Relative -11.9 -7.7 11.1 PT Daewoo Securities Indonesia Developers Maxi Liesyaputra +62-21-515-1140 [email protected]

Transcript of Lippo Karawaci · PDF fileLPKR operates 43 malls throughout Indonesia with total gross ......

PLEASE SEE ANALYST CERTIFICATIONS AND IMPORTANT DISCLOSURES & DISCLAIMERS BEGINNING ON PAGE 13.

Lippo Karawaci (LPKR)

The integrated property developer

The most integrated property company

Lippo Karawaci (LPKR) has several lines of business streams which separates the

company from the rest. Other than its core property business, the company is also

exposed to healthcare business, hotel management and funeral homes (non-core

businesses). LPKR has property assets in Lippo Village, Lippo Cikarang and Tanjung

Bunga, and Makassar (South Sulawesi). In our view, LPKR’s non-core businesses

complement the company’s overall performance and act as fat buffers amid unfavorable

property market situations. The contribution from healthcare business is becoming

larger every year, despite relatively stagnant performances from its hotel and funeral

home businesses.

The next growth engine: Hospital business

Growing health awareness motivates LPKR to drive its healthcare business further. The

company is in its early stage of developing 46 hospitals under the brand name “Siloam

Hospital”. Due to slowing property market growth (both residential and commercial),

LPKR’s performance improvement is strongly supported by healthcare business which is

evident by its increasing portion to its total revenue. As of 9M15, healthcare business

contributed IDR3r to the company’s revenue (an increase by 24.8% YoY), compared to

the total revenue growth of 10.4% YoY to IDR6.8tr. Healthcare business contribution to

total revenue came in at 45% in 9M15 compared to 39% a year earlier.

Stable revenue growth with CAGR of 28%

LPKR delivered revenue growth of 28% CAGR (excluding assets sold to REITS) over the

last 4 years (2010 ~ 2014). Healthcare business growth posted a solid 34% CAGR during

the same period. We see that LPKR optimizes its healthcare business for complementing

its overall business model and buffering earnings volatility stemming from its property

business.

Initiate coverage with a Trading Buy call

We initiate LPKR on Trading Buy rating with target price of IDR1,175 by using DCF

method (16.3% upside potential), with WACC of 11.1%. Key risk to our recommendation

is lower than expected growth of property sales.

FY (Dec) 12/12 12/13 12/14 15/15F 12/16F

Revenue (IDRbn) 6,160 6,666 11,655 9,475 11,765

OP (IDRbn) 1,549 1,943 3,809 2,551 3,147

OP Margin (%) 25.1 29.1 32.7 26.9 26.7

NP (IDRbn) 1,060 1,228 2,547 1,508 1,867

EPS (IDR) 46.5 53.9 111.9 65.3 80.9

ROE (%) 9.9 9.6 16.3 8.3 9.8

P/E (x) 21.7 18.7 9.0 15.5 12.5

P/B (x) 2.2 1.8 1.5 1.3 1.2

Note: All figures are based on consolidated basis; NP refers to net profit attributable to controlling interests

Source: Company data, KDB Daewoo Securities Research estimates

Property

Initiation report

January 12, 2016

(Initiate) Trading Buy

Target Price (12M, IDR) 1,175

Share Price (1/11/16 IDR) 1,010

Expected Return 16.3%

Market Cap (IDRbn) 23,308.8

Shares Outstanding (mn) 23,077.7

52-Week Low (IDR) 975

52-Week High (IDR) 1,460

(%) 1M 6M 12M

Absolute -10.2 -15.8 -3.3

Relative -11.9 -7.7 11.1

PT Daewoo Securities Indonesia

Developers

Maxi Liesyaputra

+62-21-515-1140

Lippo Karawaci

2

January 12, 2016

KDB Daewoo Securities Indonesia Research

Company description

Lippo Karawaci was formed through the merger of 8 property and property related

companies in 2004. The company has two basic revenue streams, consisting of

development revenue and recurring revenue. For the development revenue, the company

develops 7 locations throughout Indonesia, which are Lippo Village in Karawaci, Lippo

Cikarang (combination of industrial area and residence), Holland Village in Makassar and

Central Jakarta, Tanjung Bunga in Makassar, St. Moritz in West Jakarta and San Diego Hills,

a memorial park and funeral homes.

For recurring revenue stream, one unique thing is that LPKR operates hospitals under the

brand of “Siloam Hospitals”. Currently LPKR operates 20 hospitals (total 4,790 beds) in

locations throughout Indonesia, with outstanding specialty in each hospitals. For example,

Siloam Hospitals Lippo Village has good track record in the areas of cardiology,

neuroscience, orthopedics and emergency, while MRCCC Siloam Semanggi has strength in

the fields of cancer, liver and emergency. In short to mid-term, LPKR will build additional

Siloam hospitals in Bogor, Jember, Labuan Bajo, Lubuk Linggau, Bangka Belitung, Ambon,

Makassar and Central Jakarta.

Another business from recurring revenue is through the operations of Aryaduta Hotels

with average occupancy rate of 66% as of June 30, 2015 and total 1,684 rooms from 8

hotels in Sumatra, Java and Sulawesi. The largest is hotel Aryaduta in Central Jakarta with

302 rooms, followed by hotel Aryaduta Semanggi (South Jakarta) with 274 rooms.

LPKR operates 43 malls throughout Indonesia with total gross floor area (GFA) of 3.1mn

sqm. Among the operating malls are Lippo Mall Puri, PX Pavillion and Maxxboxx Karawaci.

The company also has two malls under development, which are Lippo Plaza Mampang and

Lippo Plaza Pangrango.

Figure 1. LPKR corporate structure

Source: Company, KDB Daewoo Securities Research

Source: Company, KDB Daewoo Securities Research

Figure 2. Shareholding structure

Source: Company, KDB Daewoo Securities Research

Lippo Karawaci

3

January 12, 2016

KDB Daewoo Securities Indonesia Research

Figure 3. Projects and land banks

Source: Company, KDB Daewoo Securities Research

Potential earnings upside in FY16, supported by healthcare

Heading into 2016, we expect to see increasing earnings contribution from its healthcare

business. We do not expect significant earnings contribution growth from its core

property business, as we believe that domestic property market is yet to fully recover this

year. Even if we strip off the assets sold to REITS in 2014, we believe the company will not

be able to meet its marketing sales target (company target: IDR4tr vs. ours IDR3.5tr) in

2015. This trend is likely to continue heading into this year, in our view.

We believe that LPKR will be very cautious in launching its new property products given

unsupportive market backdrop. The company may expect positive catalyst from the

implementation of new luxury tax on property which defines luxury landed house with

price at least IDR20bn per unit and apartment of at least IDR10bn per unit. Previously

regulation considered a house “luxury” if it had total building area of 350sqm or more. The

previous regulation also stated that for apartments, it is considered luxury if it has a total

building area of 150sqm or more.

Apart from its property business, LPKR is optimistic on healthcare business growth, in

conjunction with the hospital’s rapid expansion. In 2016 LPKR is expected to open 6 new

hospitals located in Labuan Bajo, Bau-bau, Sorong, Bogor, Jember and Bangka Belitung.

The company is also in the developing stage of 18 new hospitals which will be located in

Sumatra, Java, Kalimantan and Sulawesi.

Lippo Karawaci

4

January 12, 2016

KDB Daewoo Securities Indonesia Research

Figure 4. Marketing sales trend

Source: Company, KDB Daewoo Securities Research

Figure 5. Marketing sales by category

Marketing sales

IDRbn 2011 2012 2013 2014 9M15

Township total 1,882 3,064 2,400 2,115 1,476

Condominium total 1,161 1,501 1,034 2,677 1,452

Office total 124 100 671 388 11

Retail space 11 18 11 5 0

Sub total 3,178 4,683 4,116 5,185 2,940

Asset sold to REITS 0 2,077 1,482 3,330 0

Total 3,178 6,760 5,598 8,515 2,940

Source: Company, KDB Daewoo Securities Research

Launching clusters in FY15

In FY15 LPKR launched seven projects (both landed houses and high rise residential). For

landed houses, the company launched Le Freya (May 2015) and Cosmo Terrace

(September 2015) in Lippo Cikarang (both were 100% sold) and Holland Village in Manado

in June 2015 (83% sold). For the high-rise residential projects, the company launched

Pasadena Suites (the third tower in Orange County, Lippo Cikarang, 100% sold) in March

2015, Monaco Bay (a mixed-use project in Manado, 85% sold) in May 2015 and the

Burbank Suit (the whole fourth residential tower in Lippo Cikarang to a single Japanese

investor) in June 2015.

Most recently, on December 5, 2015, LPKR conducted the grand preview of luxurious

condominium of Glendale Park Orange County in Lippo Cikarang, which was completely

sold out. From the launching, LPKR is expected to add IDR540bn to its marketing sales

which support the company to achieve its 2015 marketing sales target of IDR4tr (9M15

marketing sales of IDR2.94tr).

We conclude that every project launched in Lippo Cikarang was absorbed very well, due to

its positioning as an integrated industrial area.

Improving healthcare business to support performance growth

Indonesia healthcare industry still has big potential room to grow compared to other

countries in the region. Hospital bed per 10,000 is only 9, compared to Singapore of 20

and China of 38. Physician per 10,000 people remains low at 2, compared to Malaysia at 12.

Lippo Karawaci

5

January 12, 2016

KDB Daewoo Securities Indonesia Research

Figure 6. Comparison health statistics

Source: WHO 2015, KDB Daewoo Securities Research

Total healthcare spending as a % of GDP stood at 3%, compared to South Korea of 7.6%

and USA of 17.0%. Even for total expenditure per capita on healthcare, Indonesia only

spends USD273 compared to Malaysia of USD894 and much smaller than Singapore of

USD3,215.

Figure 7. Comparison health statistics of GDP

Source: WHO 2015, KDB Daewoo Securities Research

The private sector contributed more in hospital developments, along with district

government and army/police. This is strongly required to complement the limited budget

flexibility by the central government.

Figure 8. Hospitals in Indonesia

Source: Ministry of Health, KDB Daewoo Securities Research

Lippo Karawaci

6

January 12, 2016

KDB Daewoo Securities Indonesia Research

Seizing the opportunity in healthcare business, LPKR continuously optimizes its healthcare

business. The company’s healthcare business shows continuous growth, in line with its

hospital expansion. In 9M15, healthcare revenue grew by 25% YoY to IDR3tr, which is

higher than the total revenue growth of 10% YoY. The portion to the total revenue also

improved to 46% in 9M15 from 39% in 9M14. The urban development business only

showed growth of 13% YoY. On the other hand, large scale integrated development

declined by 17% YoY to IDR890bn.

Figure 9. List of Siloam Hospitals

No Locations Beds No Locations Beds

1 Lippo Village 308 11 Cinere 40

2 Kebon Jeruk 283 12 Palembang 357

3 Surabaya 162 13 Bali 283

4 Cikarang 109 14 TB Simatupang 269

5 MRCCC 334 15 Kuta 21

6 Jambi 100 16 Nusa Dua 20

7 Balikpapan 232 17 Purwakarta 210

8 Tangerang (General) 640 18 Asri 40

9 Manado 230 19 Kupang 405

10 Makassar 360 20 Medan 388

Source: Company, KDB Daewoo Securities Research

For comparison, in FY14 healthcare business also showed solid revenue improvement by

33% YoY to IDR3.3tr. The highest business growth contribution came from the urban

development business which grew by two folds to IDR5.6tr. However, we note that this

figure includes the sale of Kemang Village mall to REIT (IDR3.37tr). If we peel away the

one-off sales to REIT, urban development growth would have picked up 21% YoY to

IDR2.7tr. In the period of 2011 ~ 2014, healthcare business showed significant revenue

improvement with CAGR of 38.3%.

We believe the healthcare business will continue to grow in conjunction with hospital

expansions throughout Indonesia. In FY16, we expect healthcare business to grow by 24%

YoY, in line with our expected FY15 growth of 25% YoY.

Figure 10. MRCCC Siloam Semanggi

Source: Company, KDB Daewoo Securities Researc

Lippo Karawaci

7

January 12, 2016

KDB Daewoo Securities Indonesia Research

Figure 11. Healthcare business revenue

Source: Company, KDB Daewoo Securities Research

Limited land bank in Lippo Cikarang

At present, the company has total land bank of 445ha in Lippo Cikarang (157ha for

residential, 288ha for industrial). To manage the limited land bank, LPKR launched high

residential project namely Orange County with 4 towers (Westwood Suites, Irvine Suites,

Pasadena Suites and Burbank Suites). Irvine and Westwood were launched in 2014, while

Pasadena and Burbank were launched in 2015

Figure 12. Orange Country residential towers

Source: Company, KDB Daewoo Securities Research

We believe that LPKR still needs to acquire big land for improving its land bank, mainly

for industrial area. Every manufacturing plant requires sizeable area to support its

production activities, such as for inventory space, plant machine, waste management,

etc. Lippo Cikarang still has rights to acquire another 588ha for its industrial area.

SWOT analysis

According to our SWOT analysis, we conclude that LPKR has a strong point its well-

diversified business. Entering the healthcare business increases the company’s ability to still

have growth, especially when domestic property market is facing slower pace.

Strength

Supported by various business types with significant contribution from non-core

Lippo Karawaci

8

January 12, 2016

KDB Daewoo Securities Indonesia Research

businesses (healthcare, hospitality and infrastructure, memorial park). The

diversified contribution from various businesses of the company cushions LPKR’s

financial performance during unfavorable property market environment. We

conclude that LPKR is the most integrated business property company in Indonesia.

Continuing expansion in healthcare business. LPKR expands the healthcare business

through the development of new Siloam Hospitals in many strategic areas across

Indonesia.

Weakness

High USD exposure. The company issued global bond of USD803.3mn as of

September 2015 (represents all of its total foreign debt)

Dependency on asset sold to REITS to boost marketing sales. In FY14 LPKR posted

IDR3.3tr worth of assets sold to REITS, which drove its total marketing sales to

reach IDR8.5tr for the year. If we strip away the assets sold, LPKR only booked

marketing sales of IDR5.2tr. Assets sold to REITS represented 39% to total

marketing sales in FY14.

High dependency on healthcare business to stimulate growth. The company’s total

revenue grew by CAGR of 30.7% in 2011 ~2014, lower than healthcare business

CAGR of 38.3% in the same period. Although LPKR’s revenue jumped in FY14 on

the back of sales of its asset to REITS, the company only posted growth of 8.2%

YoY in FY13 revenue.

Opportunities

Growing awareness of health. Siloam Hospital is expected to benefit from the

increasing awareness of health. The healthcare business grabs the opportunity by

developing more hospitals throughout Indonesia

Improving demand for Lippo Cikarang - an integrated industrial area. LPKR enjoys

rising position of Lippo Cikarang as an integrated industrial area. Every launching in

the area has been well absorbed.

Threats

Slowing property demand. Factoring in the slow property demand, LPKR slashed its

marketing sales target to IDR4tr from previous IDR6tr (excluding planned asset

sold to REIT of IDR1.5tr) in FY15.

Heightened competition in obtaining customers. Related to slowing absorption of

domestic property products, LPKR should have a unique strategy to attract more

customers than its competitors.

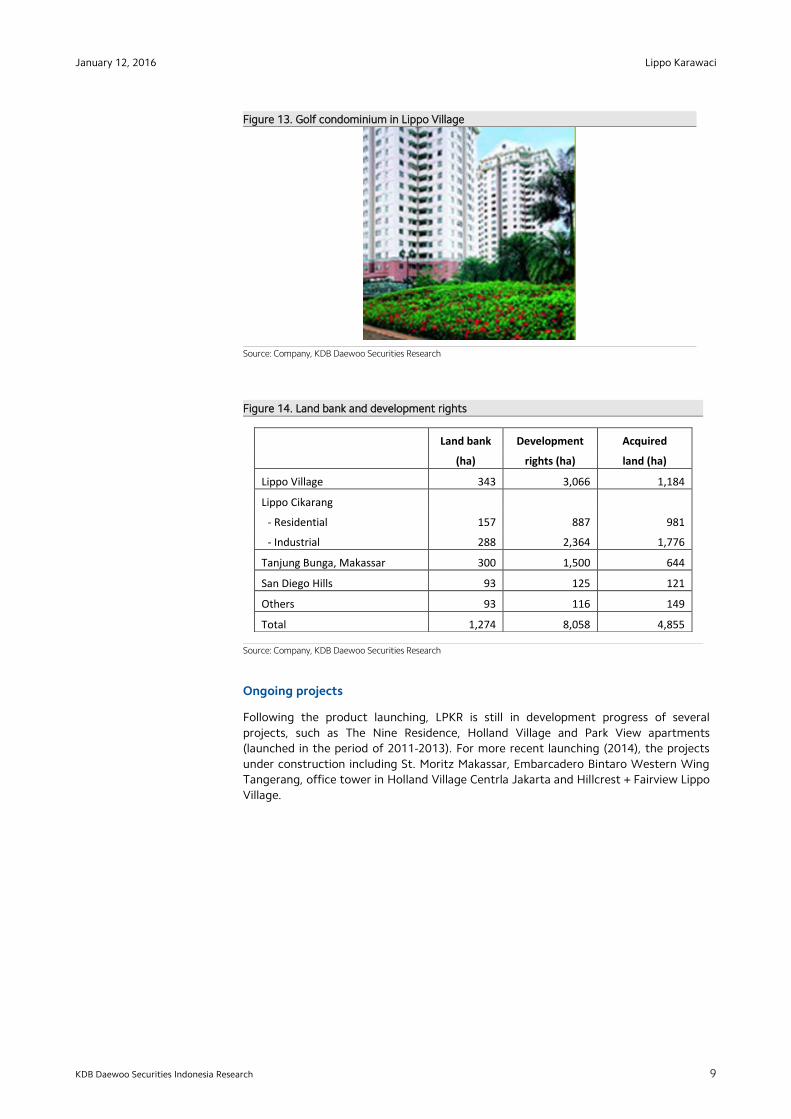

Diversified location

LPKR develops property in many areas throughout Indonesia with sizeable development

rights. There is still big room for the company to expand through land acquisition further,

although there will be problems for the action, such as society resistance and the price is

getting higher more than expected.

Lippo Village has only acquired less than half of its development rights. Tanjung Bunga

Makassar and Lippo Cikarang (for industrial) still have much room for more land acquisition.

In total, LPKR still has room to acquire another 3,200ha (currently the company only

acquired 60% of its development rights).

Lippo Karawaci

9

January 12, 2016

KDB Daewoo Securities Indonesia Research

Figure 13. Golf condominium in Lippo Village

Source: Company, KDB Daewoo Securities Research

Figure 14. Land bank and development rights

Land bank Development Acquired

(ha) rights (ha) land (ha)

Lippo Village 343 3,066 1,184

Lippo Cikarang

- Residential 157 887 981

- Industrial 288 2,364 1,776

Tanjung Bunga, Makassar 300 1,500 644

San Diego Hills 93 125 121

Others 93 116 149

Total 1,274 8,058 4,855

Source: Company, KDB Daewoo Securities Research

Ongoing projects

Following the product launching, LPKR is still in development progress of several

projects, such as The Nine Residence, Holland Village and Park View apartments

(launched in the period of 2011-2013). For more recent launching (2014), the projects

under construction including St. Moritz Makassar, Embarcadero Bintaro Western Wing

Tangerang, office tower in Holland Village Centrla Jakarta and Hillcrest + Fairview Lippo

Village.

Lippo Karawaci

10

January 12, 2016

KDB Daewoo Securities Indonesia Research

Figure 15. Holland Village Central Jakarta

Source: Company, KDB Daewoo Securities Research

Financial analysis

In the period of 2011 ~ 2014, LPKR exhibited gradual increase in both revenue and net profit.

A significant financial performance jump occurred in FY14 following the sales of assets to

REITS worth IDR3.3tr. This was the largest asset sold to REITS, compared to 2013 worth

IDR1.48tr and 2012 worth IDR2.08tr. Net profit in 2014 also jumped 107.4% YoY to

IDR2.55tr. Gross margin was relatively stable between 45% and 46%. Net margin was also

relatively stable in the period, except for FY14 which recorded a very high net margin (29%)

compared to approximately 17% ~ 18% in 2011 ~ 2013 along with high value in asset sold to

REITS (IDR3.3tr). Entering 2016, we believe that LPKR still has potential revenue growth of

24% YoY to IDR11.8tr with high contribution from healthcare business and urban

development.

Figure 16. LPKR financial performance

Source: Company, KDB Daewoo Securities Research

Lippo Karawaci

11

January 12, 2016

KDB Daewoo Securities Indonesia Research

Figure 17. LPKR margins

Source: Company, KDB Daewoo Securities Research

The hotel brand, Aryaduta

To complement LPKR’s business portfolio, the company also owns and manages hotels under

the brand name of Aryaduta. However, revenue growth from its hotel business is still far

from satisfying (IDR223.5bn in 2011 vs. IDR293.1bn in 2014). Looking into more detail,

revenue in FY14 declined by 6.3% YoY. Actually the hotel locations are in prime areas, such as

Aryaduta Jakarta in the heart of the city and Aryaduta Semanggi, located in near Jakarta

CBD. This is contrary with increasing foreign tourists coming to Indonesia by 7.2% YoY to

10.2mn people in FY14. In 2016, we expect there will be no significant improvement in hotel

performance. Besides, the revenue contribution of hotel operation to total revenue,

approximately of 3%. The number shows decline tendency from 5.3% in 2011 to 2.5% in

2014.

Figure 18. Hotel revenue

Source: Company, KDB Daewoo Securities Research

Lippo Karawaci

12

January 12, 2016

KDB Daewoo Securities Indonesia Research

Figure 19. Incoming foreign tourists to Indonesia

Source: BPS, KDB Daewoo Securities Research

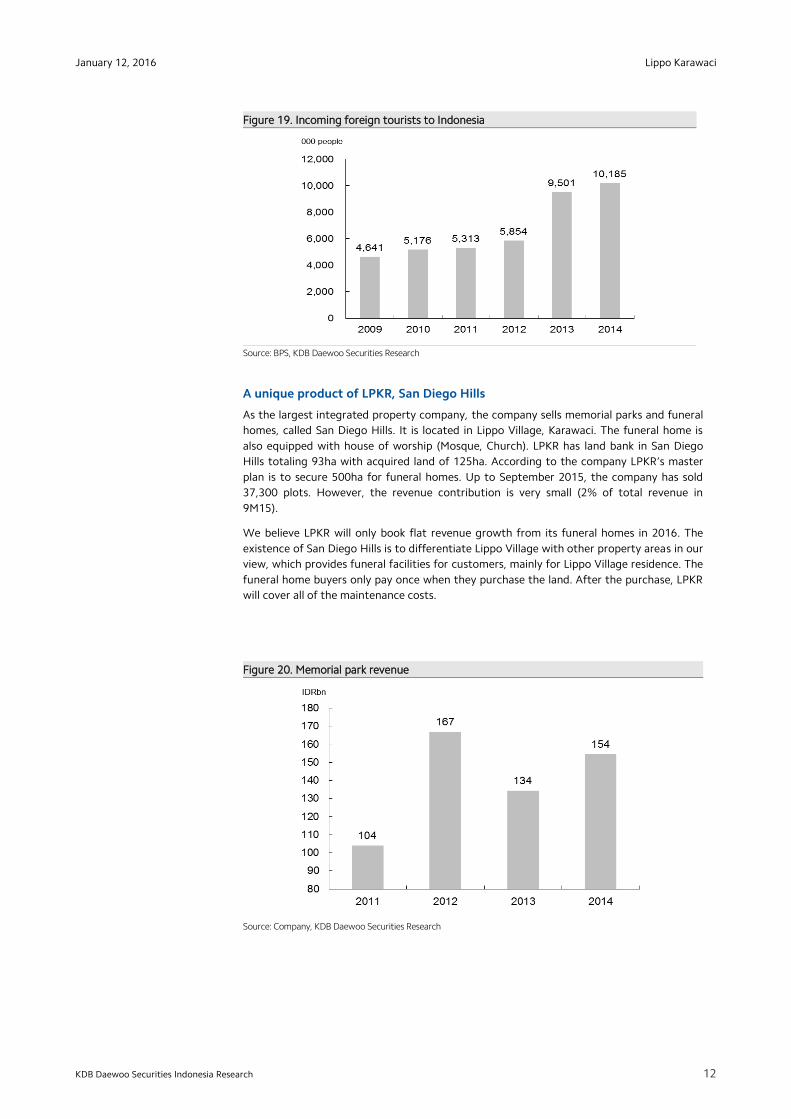

A unique product of LPKR, San Diego Hills

As the largest integrated property company, the company sells memorial parks and funeral

homes, called San Diego Hills. It is located in Lippo Village, Karawaci. The funeral home is

also equipped with house of worship (Mosque, Church). LPKR has land bank in San Diego

Hills totaling 93ha with acquired land of 125ha. According to the company LPKR’s master

plan is to secure 500ha for funeral homes. Up to September 2015, the company has sold

37,300 plots. However, the revenue contribution is very small (2% of total revenue in

9M15).

We believe LPKR will only book flat revenue growth from its funeral homes in 2016. The

existence of San Diego Hills is to differentiate Lippo Village with other property areas in our

view, which provides funeral facilities for customers, mainly for Lippo Village residence. The

funeral home buyers only pay once when they purchase the land. After the purchase, LPKR

will cover all of the maintenance costs.

Figure 20. Memorial park revenue

Source: Company, KDB Daewoo Securities Research

Lippo Karawaci

13

January 12, 2016

KDB Daewoo Securities Indonesia Research

Valuation and recommendation

As an integrated developer company, LPKR has the capacity to provide complete range of

property products and services, complemented by healthcare services. This differentiates

LPKR with other domestic property companies, in our opinion. We believe that the strategy

for business diversification is suitable for weathering turbulence in slowing property market

environment. Also, LPKR sells and leases back its asset to REITS for improving revenue and

cash flow.

Figure 21. Peers comparison

Source: Bloomberg, KDB Daewoo Securities Research

The location of LPKR’s property areas in western part of Java and south Sulawesi is good

for location portfolio. The objective is to capture middle up customers in different regions

in Indonesia.

Currently LPKR is traded at 2016F PER of 12.5x. We initiate coverage LPKR with Trading

Buy call. The target price for LPKR is IDR1,175 with 16.3% upside potential by using DCF

method (WACC of 11.1%).

Figure 22. DCF assumption

Source: KDB Daewoo Securities Research

Lippo Karawaci

14

January 12, 2016

KDB Daewoo Securities Indonesia Research

Figure 23. P/E band

Source: Bloomberg, KDB Daewoo Securities Research

LPKR share price is quite volatile, although still always higher than the industry movement.

Investors pay big attention to LPKR since it has the largest market capitalization among the

property companies and has integrated business portfolio.

Figure 24. LPKR vs JAKPROP

Source: Bloomberg, KDB Daewoo Securities Research

Lippo Karawaci

15

January 12, 2016

KDB Daewoo Securities Indonesia Research

Figure 24. NAV calculation

Source: Company, KDB Daewoo Securities Research

Ownership (%) Land area (ha) Assets value (IDRbn)

Urban development

Lippo Village 100 407 26,662

Lippo Cikarang 54.4 645 14,113

Tanjung Bunga 50.3 243 3,875

San Diego Hills 100 98 2,442

Micro suburbs 100 20 297

Sub total 47,389

Large scale integrated development

City of Tomorrow 85 5 725

Kemang Village 92 7 1,832

St Moritz 100 11 6,918

14 new projects 91 6,214

Others 100 2,458

Sub total 18,147

Retail malls

3 malls 1,756

Retail space inventory 673

Sub total 2,429

Hotels

2 hotels FREIT 681

Hotels 100 1,674

Sub total 2,355

REIT units 5,279

Hospitals 10,129

Estimated total asset value 85,728

Add Cash 1,584

Less Debt 12,283

Less Advances from customers 4,891

Estimated NAV 70,137

Issued shares (bn) 23

NAV/share (IDR) 3,039

Lippo Karawaci

16

January 12, 2016

KDB Daewoo Securities Indonesia Research

Indofood C Lippo Karawaci (LPKR/Trading Buy/TP: IDR1,175)

Income Statement (Summarized) Balance Sheet(Summarized)

(IDRbn) 12/13 12/14 12/15F 12/16F (IDRbn) 12/13 12/14 12/15F 12/16F

Revenue 6,666 11,655 9,475 11,765 Cash and equivalents 1,855 3,529 1,740 1,158

Cost of revenue (3,620) (6,258) (5,032) (6,176) Accounts & notes receivable 772 951 1,354 1,681

Gross profit 3,047 5,397 4,443 5,589 Inventories 13,894 16,553 20,129 22,233

Operating expenses (1,104) (1,589) (1,892) (2,442) Other current assets 7,492 8,929 10,422 12,534

Operating profit 1,943 3,809 2,551 3,147 Net fixed assets 2,811 3,209 3,530 3,706

Finance expense 94 65 43 29 Investment properties 306 310 310 310

Finance income (18) (114) (231) (275) Land for development 1611 1136 1250 1312

Net non-operating losses (gains) 1,925 3,695 2,320 2,872 Other long-term assets 580 719 843 992

Pre-tax profit (332) (560) (348) (431) Total assets 31,300 37,761 42,842 47,448

Tax expenses 94 65 43 29 Accounts payable 398 395 725 771

Minority interest 364 588 464 574 Short-term borrowings 17 186 307 396

Attributable net profit 1,228 2,547 1,508 1,867 Other short-term liabilities 300 407 407 407

Growth (%) Long-term borrowings 7,791 9,811 10,789 11,865

Revenue 8 75 (19) 24 Other long-term liabilities 2,297 2,763 3,099 4,185

Cost of revenue 8 73 (20) 23 Total liabilities 17,123 20,115 22,463 26,135

Gross profit 8 77 (18) 26 Paid in capital 2,308 2,308 2,308 2,308

Operating expenses (13) 44 19 29 Additional paid in capital 4,063 4,063 4,063 4,063

Operating profit 25 96 (33) 23 Retained earnings 4,748 6,976 7,730 8,663

Interest expense (91) 441 196 11 Total equity attributable parent 12,801 15,605 18,065 18,998

Pre-tax profit 22 92 (37) 24 Non-controlling interest 1,377 2,041 2,315 2,315

Tax expenses 31 68 (38) 24 Total shareholders’ equity 14,178 17,646 20,380 21,313

Attributable net profit 16 107 (41) 24

Key performance indicators

12/13 12/14 12/15F 12/16F

Per share data

EPS (IDR) 53.9 111.9 -65.3 80.9

EPS growth (%) 16.0 107.4 -41.6 23.8 Balance sheet growth rate

BPS (IDR) 554.7 676.2 782.8 823.2

12/13 12/14 12/15F 12/16F

BPS growth (%) 20.1 21.9 15.8 5.2 Cash and equivalents (44.4) 90.2 (50.7) (33.4)

DPS (IDR) 14.1 16.7 16.7 16.7 Accounts & notes receivable 29.8 23.3 42.3 24.2

Key ratios Inventories 32.3 19.1 21.6 10.5

ROE 9.6 16.3 8.3 9.8 Other current assets 48.6 19.2 16.7 20.3

ROA 3.9 6.7 3.5 3.9 Net fixed assets 26.5 14.2 10.0 5.0

Gross profit margin 45.7 46.3 46.9 47.5 Investment properties 1.5 1.3 0.0 0.0

OP margin 29.1 32.7 26.9 26.7 Land for development 73.4 (29.5) 10.0 5.0

Net profit margin 18.4 21.9 15.9 15.9 Other long-term assets 23.9 24.0 17.2 17.7

Tax rate 17.3 15.1 15.0 15.0 Total assets 25.9 20.6 13.5 10.8

Debt/equity 133.8 128.9 124.3 137.6 Accounts payable (30.9) (0.7) 83.5 6.3

Assets/equity 245 242 237 250 Short-term borrowings 4.0 1,012. 65.3 28.8

Current ratio 5.0 5.2 5.0 4.5 Other short-term liabilities 67.2 35.6 0.0 0.0

Payout ratio 26.0% 14.9% 25.5% 20.6% Long-term borrowings 29.9 25.9 10.0 10.0

Other long-term liabilities 3.1 20.3 12.2 35.0

Total liabilities 27.8 17.5 11.7 16.3

Paid in capital 0.0 0.0 0.0 0.0

Additional paid in capital 0.0 0.0 0.0 0.0

Retained earnings 25.3 46.9 10.8 12.1

Total equity attributable parent 20.1 21.9 15.8 5.2

Non-controlling interest 69.1 48.3 13.4 0.0

Total shareholders’ equity 23.6 24.5 15.5 4.6

Source: Company data, KDB Daewoo Securities Research estimates

Lippo Karawaci

17

January 12, 2016

KDB Daewoo Securities Indonesia Research

Important Disclosures & Disclaimers

Stock Ratings Industry Ratings

Buy Relative performance of 20% or greater Overweight Fundamentals are favorable or improving

Trading Buy Relative performance of 10% or greater, but with volatility Neutral Fundamentals are steady without any material changes

Hold Relative performance of -10% and 10% Underweight Fundamentals are unfavorable or worsening

Sell Relative performance of -10%

* Ratings and Target Price History (Share price (----), Target price (----), Not covered (■), Buy (▲), Trading Buy (■), Hold (●), Sell (◆))

* Our investment rating is a guide to the relative return of the stock versus the market over the next 12 months.

* Although it is not part of the official ratings at Daewoo Securities, we may call a trading opportunity in case there is a technical or short-term material

development.

* The target price was determined by the research analyst through valuation methods discussed in this report, in part based on the analyst’s estimate of

future earnings.

The achievement of the target price may be impeded by risks related to the subject securities and companies, as well as general market and economic

conditions.

Analyst Certification

The research analysts who prepared this report (the “Analysts”) are registered with the Indonesian jurisdiction and are subject to Indonesian securities

regulations. They are neither registered as research analysts in any other jurisdiction nor subject to the laws and regulations thereof. Opinions expressed in

this publication about the subject securities and companies accurately reflect the personal views of the Analysts primarily responsible for this report. Except

as otherwise specified herein, the Analysts have not received any compensation or any other benefits from the subject companies in the past 12 months and

have not been promised the same in connection with this report. No part of the compensation of the Analysts was, is, or will be directly or indirectly related

to the specific recommendations or views contained in this report but, like all employees of PT Daewoo Securities Indonesia, the Analysts receive

compensation that is impacted by overall firm profitability, which includes revenues from, among other business units, the institutional equities, investment

banking, proprietary trading and private client division. At the time of publication of this report, the Analysts do not know or have reason to know of any

actual, material conflict of interest of the Analyst or PT Daewoo Securities Indonesia except as otherwise stated herein.

Disclaimers

This report is published by PT Daewoo Securities Indonesia (“Daewoo”), a broker-dealer registered in the Republic of Indonesia and a member of the

Indonesia Exchange. Information and opinions contained herein have been compiled from sources believed to be reliable and in good faith, but such

information has not been independently verified and Daewoo makes no guarantee, representation or warranty, express or implied, as to the fairness,

accuracy, completeness or correctness of the information and opinions contained herein or of any translation into English from the Bahasa Indonesia. If this

report is an English translation of a report prepared in the Indonesian language, the original Indonesian language report may have been made available to

investors in advance of this report. Daewoo, its affiliates and their directors, officers, employees and agents do not accept any liability for any loss arising

from the use hereof. This report is for general information purposes only and it is not and should not be construed as an offer or a solicitation of an offer to

effect transactions in any securities or other financial instruments. The intended recipients of this report are sophisticated institutional investors who have

substantial knowledge of the local business environment, its common practices, laws and accounting principles and no person whose receipt or use of this

report would violate any laws and regulations or subject Daewoo and its affiliates to registration or licensing requirements in any jurisdiction should receive

or make any use hereof. Information and opinions contained herein are subject to change without notice and no part of this document may be copied or

reproduced in any manner or form or redistributed or published, in whole or in part, without the prior written consent of Daewoo. Daewoo, its affiliates and

their directors, officers, employees and agents may have long or short positions in any of the subject securities at any time and may make a purchase or sale,

or offer to make a purchase or sale, of any such securities or other financial instruments from time to time in the open market or otherwise, in each case

either as principals or agents. Daewoo and its affiliates may have had, or may be expecting to enter into, business relationships with the subject companies to

provide investment banking, market-making or other financial services as are permitted under applicable laws and regulations. The price and value of the

investments referred to in this report and the income from them may go down as well as up, and investors may realize losses on any investments. Past

performance is not a guide to future performance. Future returns are not guaranteed, and a loss of original capital may occur.

Disclosures

As of the publication date, PT Daewoo Securities Indonesia, and/or its affiliates do not have any special

interest with the subject company and do not own 1% or more of the subject company's shares

outstanding.

Lippo Karawaci

18

January 12, 2016

KDB Daewoo Securities Indonesia Research

Distribution

United Kingdom: This report is being distributed by Daewoo Securities (Europe) Ltd. in the United Kingdom only to (i) investment professionals falling within

Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (the “Order”), and (ii) high net worth companies and other

persons to whom it may lawfully be communicated, falling within Article 49(2)(A) to (E) of the Order (all such persons together being referred to as “Relevant

Persons”). This report is directed only at Relevant Persons. Any person who is not a Relevant Person should not act or rely on this report or any of its

contents.

United States: This report is distributed in the U.S. by Daewoo Securities (America) Inc., a member of FINRA/SIPC, and is only intended for major institutional

investors as defined in Rule 15a-6(b)(4) under the U.S. Securities Exchange Act of 1934. All U.S. persons that receive this document by their acceptance

thereof represent and warrant that they are a major institutional investor and have not received this report under any express or implied understanding that

they will direct commission income to Daewoo or its affiliates. Any U.S. recipient of this document wishing to effect a transaction in any securities discussed

herein should contact and place orders with Daewoo Securities (America) Inc., which accepts responsibility for the contents of this report in the U.S. The

securities described in this report may not have been registered under the U.S. Securities Act of 1933, as amended, and, in such case, may not be offered or

sold in the U.S. or to U.S. persons absent registration or an applicable exemption from the registration requirements.

Hong Kong: This document has been approved for distribution in Hong Kong by Daewoo Securities (Hong Kong) Ltd., which is regulated by the Hong Kong

Securities and Futures Commission. The contents of this report have not been reviewed by any regulatory authority in Hong Kong. This report is for

distribution only to professional investors within the meaning of Part I of Schedule 1 to the Securities and Futures Ordinance of Hong Kong (Cap. 571, Laws

of Hong Kong) and any rules made thereunder and may not be redistributed in whole or in part in Hong Kong to any person.

All Other Jurisdictions: Customers in all other countries who wish to effect a transaction in any securities referenced in this report should contact Daewoo or

its affiliates only if distribution to or use by such customer of this report would not violate applicable laws and regulations and not subject Daewoo and its

affiliates to any registration or licensing requirement within such jurisdiction.

KDB Daewoo Securities International Network

Daewoo Securities Co. Ltd. (Seoul) Daewoo Securities (Hong Kong) Ltd. Daewoo Securities (America) Inc.

Head Office

14, Eunhaeng-ro, Yeongdeungpo-gu

Seoul 150-973

Korea

Suites 2005-2012

Two International Finance Centre

8 Finance Street, Central

Hong Kong

320 Park Avenue, 31st Floor.

New York, NY 10022

United States

Tel: 82-2-768-3026 Tel: 85-2-2514-1304 Tel: 1-212-407-1000

Daewoo Securities (Europe) Ltd. Daewoo Securities (Singapore) Pte. Ltd. Tokyo Representative Office

41st Floor, Tower 42

25 Old Broad Street

London EC2N 1HQ

United Kingdom

Six Battery Road #11-01

Singapore, 049909

7F, Yusen Building, 2-3-2

Marunouchi, Chiyoda-ku

Tokyo 100-0005

Japan

Tel: 44-20-7982-8000 Tel: 65-6671-9845 Tel: 81-3- 3211-5511

Beijing Representative Office Shanghai Representative Office Ho Chi Minh Representative Office

2401A, 24th Floor. East Tower

Twin Tower, B-12 Jianguomenwai Avenue

Chaoyang District, Beijing 100022

China

Room 38T31, 38F SWFC

100 Century Avenue, Pudong New Area,

Shanghai, 200120

China

Suites 901B. Centec Tower

72-74 Nguyen Thi Minh Khai St, Ward 6

District 3, HCMC

Tel: 86-10-6567-9699 Tel: 86-21-5013-6392 Tel: 84-8-3910-6000

Daewoo Investment Advisory (Beijing) Co., Ltd PT. Daewoo Securities Indonesia Daewoo Securities (Mongolia) LLC

2401B,24th Floor. East Tower

Twin Tower, B-12 Jianguomenwai Avenue

Chaoyang District, Beijing 100022

China

Equity Tower 50th Floor

Jl.Jend Sudirman, SCBD Lot 9

Jakarta 12190

#406, Blue Sky Tower, Peace Avenue 17

1 Khoroo, Sukhbaatar District

Ulaanbaatar 14240

Mongolia

Tel: 86-10-6567-9699 Tel: 62-21-2553-1000 Tel: 976-7011-0807