Link download full: Solution Manual for Accounting...

25

Full file Page 1 of 25 http://testbankcollection.com/ Link download full: Solution Manual for Accounting Information Systems 11th Edition by Romney http://testbankcollection.com/download/solution-manual-foraccounting- information-systems-11th-edition-by-romney CHAPTER 2 OVERVIEW OF BUSINESS PROCESSES Instructors Manual Learning Objectives: 1. Explain the basic activities companies engage in, the types of decisions they must make and the types of information they need to make those decisions. 2. Identify the major internal and external parties that an AIS interacts with and they type of information it provides each user. 3. Describe the major transaction cycles present in most companies. 4. Describe the four major steps in the data processing cycle and the major activities in each. 5. Describe the documents and procedures used in an AIS to collect and process transaction data. 6. Describe the ways information is stored in computer-based information systems. 7. Discuss the types of information that an AIS can provide. Questions to be addressed in this chapter include: [Refer to power point slide #2] 1. What are the basic business processes in which an organization engages? – What decisions must be made to undertake these processes? – What information is required to make those decisions? 2. What role does the data processing cycle play in organizing business processes and providing information to users?

Transcript of Link download full: Solution Manual for Accounting...

Full file

Page 1 of 25

http://testbankcollection.com/

Link download full: Solution Manual for Accounting Information

Systems 11th Edition by Romney

http://testbankcollection.com/download/solution-manual-foraccounting-

information-systems-11th-edition-by-romney CHAPTER 2

OVERVIEW OF BUSINESS PROCESSES Instructors Manual

Learning Objectives:

1. Explain the basic activities companies engage in, the types of

decisions they must make and the types of information they need

to make those decisions.

2. Identify the major internal and external parties that an AIS

interacts with and they type of information it provides each

user.

3. Describe the major transaction cycles present in most companies.

4. Describe the four major steps in the data processing cycle and

the major activities in each.

5. Describe the documents and procedures used in an AIS to collect

and process transaction data.

6. Describe the ways information is stored in computer-based

information systems.

7. Discuss the types of information that an AIS can provide.

Questions to be addressed in this chapter include:

[Refer to power point slide #2]

1. What are the basic business processes in which an organization

engages?

– What decisions must be made to undertake

these processes?

– What information is required to make those

decisions?

2. What role does the data processing cycle play in organizing business processes and providing information to users?

http://testbankcollection.com/

Page 2 of 25

3. What is the role of the information system and enterprise

resource planning in modern organizations?

OUTLINE

Introduction

This chapter is divided into two major sections.

Full file

The first major section discusses the basic business activities

an organization engages in.

The second major section discusses the data processing cycle and

its role in organizing business activities and providing

information to users.

Learning Objective One

Explain the basic activities companies engage

in, the types of decisions they must make and

the types of information they need to make those

decisions.

Information Needs and Business Activities

Table 2-1 on Page 29 provides businesses processes, key

decisions and information needs.

Business Processes

1. Acquires capital 6. Sell merchandise

2. Acquire building and equipment 7. Collect payments from customers

3. Hire and train employees 8. Pay employees

4. Acquire inventory 9. Pay taxes

5. Advertising and marketing 10. Pay vendors

Multiple Choice #1

S&S has ten business processes which require information to make

key decisions. Which S&S business process requires a market

analyses?

a. Sell merchandise

b. Advertising and marketing

c. Acquire inventory

d. A and B

e. All of the above

Full file

Page 3 of 25

Multiple Choice #2

S&S has ten business processes which require information to make

key decisions. What is one or more of the key decisions made to

sell merchandise?

a. Which credit cards to accept?

b. What models to carry?

c. How to handle cash receipts?

d. A and B

e. None of the above

http://testbankcollection.com/Learning Objective Two

Identify the major internal and external parties

that an AIS interacts with and the type of

information it provides each user.

Interaction Between External and Internal Parties

Figure 2-1 on Page 30 provides important interactions between external

and internal parties.

Multiple Choice #3

The AIS at S&S interacts with many external parties. Which

external party or parties receive financial statements?

a. Government agencies

b. Investors

c. Customers

d. Banks

e. A and B

Multiple Choice #4

The AIS at S&S interacts with many external parties. Which

external party receives an invoice from S&S?

a. Vendor

b. Customers

c. Creditors

http://testbankcollection.com/

Page 4 of 25

Business Processes

Figure 2-2 on Page 32 provides an overview of the business processes.

A transaction is an agreement between two entities to exchange

goods or services or any other event that can be measured in

economic terms by an organization.

Another definition that is not in this book: In order to operate

from day to day, a firm conducts a number of business events

called transactions.

The process that begins with capturing transaction data and

ends with an informational output such as the financial

statements is called transaction processing.

d. None of the above

Learning Objective Three

Identify the major transaction cycles present in

most companies.

Full file http://testbankcollection.com/

Page 5 of 25

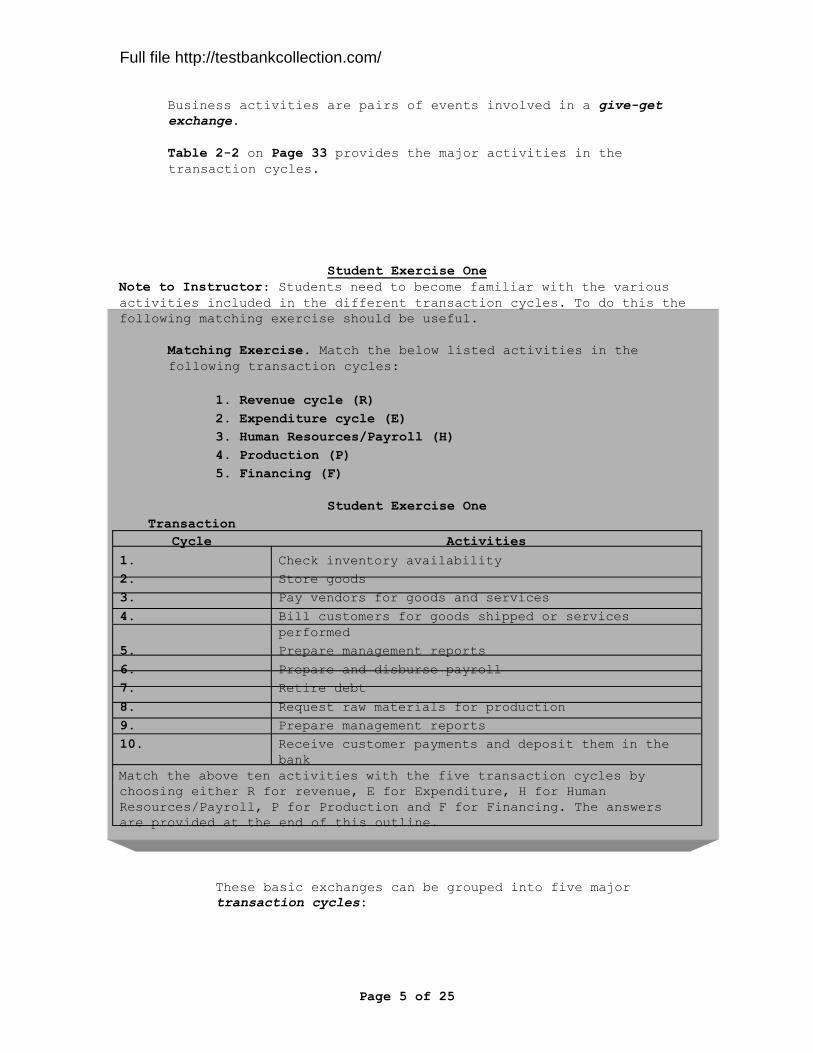

Business activities are pairs of events involved in a give-get

exchange.

Table 2-2 on Page 33 provides the major activities in the

transaction cycles.

Student Exercise One

Note to Instructor: Students need to become familiar with the various

activities included in the different transaction cycles. To do this the

following matching exercise should be useful.

Matching Exercise. Match the below listed activities in the

following transaction cycles:

1. Revenue cycle (R)

2. Expenditure cycle (E)

3. Human Resources/Payroll (H)

4. Production (P)

5. Financing (F)

Student Exercise One

Transaction

Cycle Activities

1. Check inventory availability

2. Store goods

3. Pay vendors for goods and services

4. Bill customers for goods shipped or services

performed

5. Prepare management reports

6. Prepare and disburse payroll

7. Retire debt

8. Request raw materials for production

9. Prepare management reports

10. Receive customer payments and deposit them in the

bank

Match the above ten activities with the five transaction cycles by

choosing either R for revenue, E for Expenditure, H for Human

Resources/Payroll, P for Production and F for Financing. The answers

are provided at the end of this outline.

These basic exchanges can be grouped into five major

transaction cycles:

Full file http://testbankcollection.com/

Page 6 of 25

The revenue cycle, where goods and services are sold

for cash or a future promise to pay cash.

The expenditure cycle, where companies purchase

inventory for resale or raw materials to use in

producing products in exchange for cash or a future

promise to pay cash.

The production cycle, where raw materials are

transformed into finished goods.

The human resources/payroll cycle, where employees

are hired, trained, compensated, evaluated, promoted

and terminated.

The financing cycle, where companies sell shares in

the company to investors and borrow money and where

investors are paid dividends and interest is paid on

loans

Figure 2-2 on Page 32 gives a good overview of the give-get

exchange and the general ledger and reporting system.

The general ledger and reporting system is used to

generate information for both management and external

parties.

Table 2-2 on Page 33 gives a great listing of activities within

the Revenue, Expenditure, Human Resources/Payroll, Production

and Financing Cycles.

Notice that the last activity listed in Table 2-2 for each

transaction cycle is “send appropriate information to the other

cycles.”

Multiple Choice #5

Give cash and get raw materials is an event in the _______

cycle, and give labor and get finished goods is an event

in the _______ cycle.

a. Expenditure, production

b. Financing, human resources

c. Revenue, production

d. Expenditure, production

Multiple Choice #6

Which business cycle does not involve cash?

a. Revenue

b. Production

Full file http://testbankcollection.com/

Page 7 of 25

c. Human resources

d. Expenditure

Transaction Processing: The Data Processing Cycle

Four Major Steps in The Data Processing Cycle [Figure 2-3 on Page

35]:

1) Data Input

2) Data Storage

3) Data Processing

4) Information Output

The first step in processing transaction is to capture the

data for each transaction that takes place and enter them into

the system.

Data Inputs

Data must be collected about three facets of each business

activity:

1. Each activity of interest

2. The resource(s) affected by each activity

3. The people who participate in each activity

For example, collect the following data about a sales

transaction:

o Date and time of day the sale occurred

e. Financing

Learning Objective Four

Describe the four major steps in the data

processing cycle and the major activities in

each.

Full file http://testbankcollection.com/

Page 8 of 25

o Employee who made the sale and the checkout clerk who

processed the sale

o Checkout register where the sale was processed

o Item(s) sold

o Quantity of each item sold

o List price and actual price of each item sold

o Total amount of the sale

o For credit sales: delivery instructions, customer bill-to and

ship-to addresses, customer name

Multiple Choice #7

Accountants have a significant role in the data processing

cycle. Accountants interact with system analyst to answer

questions that include:

a. What report should be used to portray the goals in

financial terms?

b. What data should be entered and stored by the

organization?

c. How should the information be organized, updated,

stored, accessed and retrieved?

d. B and C

e. None of the above

Multiple Choice #8

The most frequent transaction in the revenue cycle is a

a. purchase of inventory

b. sale

c. credit approval

d. customer payments

Learning Objective Five

Describe the documents and procedures used in an

AIS to collect and process transaction data.

Full file http://testbankcollection.com/

Page 9 of 25

Source Documents – documents used to collect data about their

business activities. Source documents are also used to support

the validity of the business activities.

If paper documents are exchanged with customers or suppliers,

data input accuracy and efficiency is improved by using

turnaround documents, which are records of company data sent to

an external party and then returned to the system as input.

Table 2-3 on Page 36 provides an excellent listing of Common

Business Activities and Source Documents for the revenue,

expenditure and human resources cycles that students should

become familiar with.

Source Data Automation is yet another means to improve the

accuracy and efficiency of data input. An example would be once

the sale of merchandise is rung up on the cash register it would

be interfaced with accounting to automatically record the sale

and also interfaced with the warehouse to automatically reduce

the level of inventory for the item that was sold. This would

also be interfaced with purchasing in which the purchase order

would automatically be printed out for delivery to the vendor.

The second step in processing transactions is to make sure

captured data are accurate and complete.

One way to increase accuracy and completeness is to use

well-designed turnaround documents and data entry screens,

as well as source data automation.

Multiple Choice #9

The source document used to request that items be purchased

is a

a. purchase order

b. purchase budget

c. purchase requisition

d. A and C

e. all of the above

Multiple Choice #10

A customer returns merchandise to a company. The source

document that should be used is:

a. credit memo

b. adjustment memo

c. remittance advice

Full file http://testbankcollection.com/

Page 10 of 25

Data Storage

A company’s data are one of its most important resources.

Accountants need to know how to manage data for maximum corporate

use.

Ledgers

General Ledger contains summary-level data for every

asset, liability, equity, revenue and expense

account of the organization.

Subsidiary Ledger. Records all the detailed data for

any general ledger account that has many individual

subaccounts.

These subsidiary ledgers would be used for accounts

receivable and accounts payable.

Accounts receivable subsidiary ledger would

record detailed data for customers whom buy

products or services on credit.

The accounts receivable subsidiary ledger would

support the accounts receivable general ledger

controlling account.

Accounts payable subsidiary ledger would record

detailed data for the individual vendor credit

purchases of merchandise/supplies made by the

company.

The accounts payable subsidiary ledger would

support the accounts payable general ledger

controlling account.

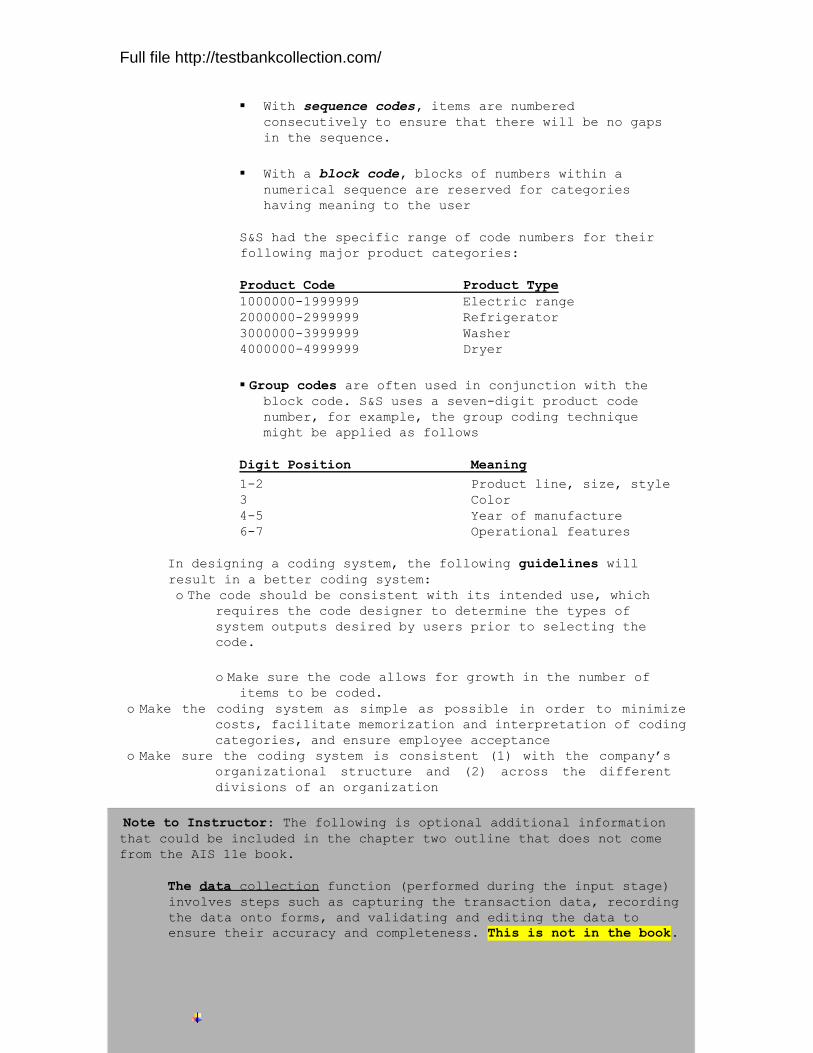

Coding Techniques

Coding is the systematic assignment of numbers or letters

to items to classify and organize them

d. none of the above

Learning Ob jective Six

Describe the ways information is stored in

computer - based information systems.

Full file http://testbankcollection.com/

Page 11 of 25

With sequence codes, items are numbered

consecutively to ensure that there will be no gaps

in the sequence.

With a block code, blocks of numbers within a

numerical sequence are reserved for categories

having meaning to the user

S&S had the specific range of code numbers for their

following major product categories:

Product Code Product Type

1000000-1999999 Electric range

2000000-2999999 Refrigerator

3000000-3999999 Washer

4000000-4999999 Dryer

Group codes are often used in conjunction with the

block code. S&S uses a seven-digit product code

number, for example, the group coding technique

might be applied as follows

Digit Position Meaning

1-2 Product line, size, style

3 Color

4-5 Year of manufacture

6-7 Operational features

In designing a coding system, the following guidelines will

result in a better coding system:

o The code should be consistent with its intended use, which

requires the code designer to determine the types of

system outputs desired by users prior to selecting the

code.

o Make sure the code allows for growth in the number of

items to be coded.

o Make the coding system as simple as possible in order to minimize

costs, facilitate memorization and interpretation of coding

categories, and ensure employee acceptance

o Make sure the coding system is consistent (1) with the company’s

organizational structure and (2) across the different

divisions of an organization

Note to Instructor: The following is optional additional information that could be included in the chapter two outline that does not come

from the AIS 11e book.

The data collection function (performed during the input stage)

involves steps such as capturing the transaction data, recording

the data onto forms, and validating and editing the data to

ensure their accuracy and completeness. This is not in the book.

Full file http://testbankcollection.com/

Page 12 of 25

Also, this is not in the book. The data maintenance function

(performed during the processing stage) involves steps like the

following:

Classifying, or assigning collected data to pre-established

categories

Transcribing, or copying/reproducing the data onto another

document or medium

Sorting, or arranging data elements according to one or more

characteristics

Batching, or gathering together groups of transactions of a

similar nature

Merging, or combining two or more batches or files of data.

Multiple Choice #11

Purchase orders would use _______ codes, while coding for major

product categories would use a _______ code.

a. account and ledger

Full file http://testbankcollection.com/

b. block and sequence

c. group and sequence

d. sequence and block

Multiple Choice #12

In designing a coding system, the following guidelines will

results in a better coding system:

a. The second digit in each account code should represent

the primary financial subaccounts within each category.

b. The code should be consistent with its intended use,

which requires the code designer to determine the types

of system outputs desired by users after selecting the

code.

c. Make sure the coding system is consistent (1) with the

company’s organizational structure and (2) across the

different divisions of an organization.

d. A and C

Chart of Accounts

A chart of accounts is a list of all general ledger accounts an

organization uses with each general ledger account being

assigned a specific number.

Full file http://testbankcollection.com/

Page 14 of 25

Student Exercise Two

Note to the Instructor: To familiarize the students with completing a

chart of accounts, especially if you are going to assign problem 2.2

on pages 51 and 52 as part of the homework assignment; the following

exercise would be helpful.

Tom Jones is a sole proprietor that owns and manages a music store

that sells music CDs and DVD music videos.

Use the following information to design and complete a chart of

accounts:

1. Customers cannot use commercial credit cards, but Tom has

in-house credit.

2. Cash in the bank includes a checking account, savings

account, change fund and petty cash fund.

3. Tom pays for rent and insurance in advance.

4. When Tom started the business he purchased land, a building

used for the store, furniture and fixtures, and computer

equipment. There have been no additional purchases.

5. The are no short-term or long-term investments

6. Tom issued a 90 day note to a customer that could not pay

the amount owed that was recorded in accounts receivable.

There are no notes payable.

Full file http://testbankcollection.com/

Page 15 of 25

Table 2-4 on Page 39 provides the chart of accounts for S&S

Note that the various categories of accounts all start with the

same first number. For example, current assets all start with

the number 1. The 2nd and 3rd number identifies the specific

account. For example, cash 101, where the first number 1

identifies the category of current assets and the 2nd & 3rd

numbers 0 and 1 identifies the checking account.

7. Toms earns interest on boPage 11 of

th the checking account

and the 19

savings account.

8. Tom has two employees that are paid hourly wages. The

Full file http://testbankcollection.com/

Page 16 of 25

employees do not receive any benefits.

Journals

Sales Journal (SJ) – Credit Sales

Cash Receipts Journal (CR) – Cash Sales & Cash Collected

From Customers’ Accounts Receivable

Purchase Journal (PJ) – Credit Purchases

Cash Payments Journal (CP) – All Cash Payments

General Journal (GJ) – Adjusting Entries and Closing

Entries

Table 2-5 at the bottom of Page 40 provides an example of

the Sales Journal. Students should remember that the

column on the far right in this journal represents the

debits to accounts receivable and credit to sales.

Students should also remember that credit sales are

recorded daily in the Sales Journal and also recorded in

the Accounts Receivable Subsidiary Ledger. Then at the end

of the month the column total in the Sales Journal is then

posted to the general ledger accounts for accounts

receivable and sales.

Figure 2-4 on Page 41 provides the flow of Recording and

Posting Credit Sales.

Students should note that transactions are recorded daily

in the sales journal and accounts receivable subsidiary

ledger. Students should also remember that SJ1 means Sales

Journal Page 1, CR4 means Cash Receipts Journal Page 4 and

SJ5 means Sales Journal Page 5.

Audit Trail The accounting data and records should provide a

trail starting with the source document that supports the

transaction (for example, lets use credit sales) all the way

through to the final posting in the general ledger accounts

to the financial statements. An audit trail provides a means

to check the accuracy and validity of ledger postings.

In auditing, this technique would be called Tracing. In the

opposite direction; from the general ledger to the journals &

subsidiary ledgers to the source document; this is called

Vouching for auditors. This is covered in more detail in

Auditing Theory and Practice courses.

Multiple Choice #13

Full file http://testbankcollection.com/

Page 17 of 25

The journal that records cash collections from customers

is the:

a. Sales journal

b. Cash receipts journal

c. General journal

d. A and B

e. None of the above

Multiple Choice #14

Posting references and _______ numbers provides what is

known as a(n) _______.

a. Document and general ledger control account

b. Account and Audit trail balance

c. Transaction and subsidiary ledger

d. Document and audit trail

Computer-Based Storage concepts

An entity is something about which information is stored.

For example, employees, inventory items and customers.

Each entity has attributes, or characteristics of

interest, which need to be stored. For example an

employee’s hourly rate of pay, unit cost of an inventory

item and a customer’s address.

Figure 2-5 on Page 42 provides examples of data storage

elements:

Data values are stored in a physical space called a

field. In the figure the fields are Customer number,

Customer name, Address, Credit limit and Balance

The sect of fields that contain data about various

attributes of the same entity forms a record. In the

figure that records are represented by each of the

three rows; so there are three records.

The contents of each field within a record are

called a data value. Sometimes, not mentioned in

this book, the contents of each field are called a

specific data element which contains value the data.

In turn, data elements/data value is composed of

characters such as letters, numbers and symbols.

Related records are grouped to form a file.

Full file http://testbankcollection.com/

Page 18 of 25

Two basic types of files exist:

o A master file is conceptually similar to a

ledger in a manual AIS

o The second basic type of file is called a

transaction file, which is conceptually similar

to a journal in a manual AIS

Data Processing

Once data bout a business activity have been collected and

entered into the system they must be processed.

Data processing implies the execution of a certain procedures,

usually involving a series of tasks.

There are four different types of file processing:

1. Updating data previously stored about the activity, the

resources affected by the activity , or the people who

performed the activity

Figure 2-6 on Page 41 provide The Accounts Receivable

File Update Process

2. Changing data, such as changing a customer’s address

when they move or their credit limit when their

financial situation changes

3. Adding data, such as adding a new employee to the

payroll master file or data-base after they have been

hired

4. Deleting data, such as purging the vendor master file

of all vendors that the company no longer does business

with

Periodic updating of data is referred to as batch processing.

This approach may be combined with either the off-line or on-

line entry of data.

Under the on-line entry/batch processing method of processing,

individual transactions are entered directly into the computer

via a terminal as they occur.

Updating as each transaction occurs is referred to as on-line,

real-time processing.

Full file http://testbankcollection.com/

Page 19 of 25

The on-line entry/on-line processing method differs from on-

line entry/batch processing in the following two respects: (1)

master files are updated concurrently with data entry and (2) a

transaction log is produced that consists of a chronological

record of all transactions.

Figure 2-7 on Page 45 summarizes the three different types of

processing data.

Multiple Choice #15

The file that is similar to a journal in an manual AIS is

a. Journal file

b. Transaction file

c. Data file

d. Master file

This is the final step in the data processing cycle.

Forms of Information Output

Documents are records of transaction or other

company data. For example, checks and invoices.

Documents generated at the end of transaction

processing activities are called operational

documents to distinguish them from source documents,

which are used at the beginning of the process.

Reports are prepared for both internal and external

users. We are all familiar with the external reports

called financial statements.

Information needs cannot always be satisfied

strictly by documents or periodic reports. Instead,

problems and questions constantly arise that need

rapid action or answers. To respond to this problem,

personal computers or terminals are used to query

the system.

When the queried information is displayed on the

computer monitor, the output is referred to as a

“soft copy.” When it is printed out on paper, it is

referred to as a “hard copy.”

Information Output

Learning Objective Seven

Discuss the types of information that an AIS can

provide.

Full file http://testbankcollection.com/

Page 20 of 25

Purpose of Output

There are four main types of financial reports that were

covered in Principles of Accounting I & II courses, the

balance sheet, income statement, statement of owner’s

equity or statement of stockholder’s equity and the

statement of cash flows. Sometimes a statement of retained

earnings is used instead of the statement of stockholder’s

equity. These financial statements are used by both

external and internal users.

Budgets are used by management of the firm. Budgets

require estimating future revenue/sales, cost and

expenses. This is the operational budget. There are also

cash budgets and capital expenditure budgets.

Behavioral Implications of Managerial Reports

Employees focus their efforts primarily on those tasks that are

measured and evaluated.

This can be either good or bad.

For example, the task of customer complaint resolution.

The organization wants to satisfy its customers to the

greatest extent possible, at the lowest possible cost.

If customer service representatives are evaluated solely

based on the number of complaints resolved.

Then there two possible problems that could arise:

The customer service representatives may be focused on

quickly resolving each complaint in the store’s favor

that may alienate some customers, or

Customer service representatives may “give away the

store” just to keep the customer happy.

Role of the AIS

Traditionally, the AIS has been referred to as a transaction

processing system because its only concern was financial data

and accounting transactions. Consequently, many organizations

developed additional information systems to collect, process,

store and report information not contained in the AIS.

Enterprise resource planning (ERP) systems are designed to

overcome these problems as they integrate all aspects of a

company’s operations with its traditional AIS.

Full file http://testbankcollection.com/

Page 21 of 25

A key feature of ERP systems is the integration of financial

with other nonfinancial operating data.

ANSWERS to Multiple Choice Questions:

Multiple

Choice

Number

Multiple

Choice

Answer

Multiple

Choice

Number

Multiple

Choice

Answer

1 C 9 C

2 A 10 A

3 B 11 D

4 B 12 C

5 D 13 B

6 B 14 D

7 B 15 B

8 B

References Used:

1 The idea of modeling an AIS as a set of “Give and Take” exchanges

was developed in Cheryl L. Dunn and

William E. McCarthy, “Conceptual Models of Economic Exchange

Phenomena:

History’s Third Wave of

Accounting Systems,” Collected Papers of the Sixth World Congress of

Accounting Historians, Vol. 1, Kyoto,

Japan. pp. 133–164; and in Guido Geerts and William E. McCarthy,

“Modeling Business Enterprises as Value-Added

Process Hierarchies with Resource-Event-Agent Object Templates,”

Business Object Design and

Implementation: OOPSLA 1995 Workshop Proceedings (October 16, 1995),

Austin, TX: Springer.

Figure 2-2 The AIS and Its Subsystems Source :Adapted from classroom

materials originally developed by Julie Smith David at Arizona State

University and based on ideas developed in the sources listed in

footnote 1.

Answers To Student Exercise One

Transaction

Cycle Activities

1. R Check inventory availability

2. E Store goods

3. E Pay vendors for goods and services

4. R Bill customers for goods shipped or services performed

5. R Prepare management reports

6. H Prepare and disburse payroll

7. F Retire debt

8. P Request raw materials for production

Full file http://testbankcollection.com/

Page 22 of 25

9. E Prepare management reports

10. R Receive customer payments and deposit them in the bank

Match the above ten activities with the five transaction cycles by

entering either R for revenue, E for Expenditure, H for Human

Resources/Payroll, P for Production and F for Financing. The answers

are provided at the end of this outline.

Full file http://testbankcollection.com/

Student Exercise Two Answers

Account

Code Account Name

100-199 Current Assets

101 Checking Account

102 Savings Account

103 Change Fund

104 Petty Cash

110 Accounts Receivable

115 Allowance for Doubtful Accounts

120 Interest Receivable

130 Notes Receivable

150 Inventory

160 Supplies

170 Prepaid Rent

180 Prepaid Insurance 200-299

Noncurrent Assets

200 Land

210 Buildings

215 Accumulated Depreciation – Buildings

220 Furniture and Fixtures

225 Accumulated Depreciation

- Furniture and Fixtures

230 Computer Equipment

235 Accumulated Depreciation

- Computer Equipment

Student Exercise Two Answers Concluded

300-399 Liabilities

300 Accounts Payable

310 Wages Payable

321 FWT Taxes Payable

322 FICA Tax Payable

323 Federal Unemployment Tax Payable

324 State Unemployment Tax Payable

330 Current Portion of Mortgage Payable

350 Long-Term Mortgage Payable

400-499 Equity Accounts

400 Tom Jones, Capital

Full file http://testbankcollection.com/

410 Tom Jones, Withdrawals

500-599 Revenues

500 Cash Sales – Music CDs

501 Cash Sales – DVD Music Videos

502 Credit Sales – Music CDs

Page 18 of 19

503

510

511

520

530

Credit Sales – DVD Music Videos

Sales Returns & Allowances

Sales Discounts

Interest Revenue

Miscellaneous Revenue

600 - 799 Expenses

600

611

612

613

620

630

701

702

703

710

720

Cost of Goods Sold

Wages Expen ses

Payroll Tax Expense

Rent Expense

Supplies Expense

Bad Debt Expense

Depreciation Expense – Buildings

Depreciation Expense – Furniture and Fixtures

Depreciation Expense – Computer Equipment

Income Tax Expense

Miscellaneous Expense

900 - 999 Summary Accoun ts

910 Income Summary

Full file http://testbankcollection.com/

Page 19 of 19