Limits to arbitrage during the crisis: funding liquidity ... · funding liquidity constraints &...

37

Angelo Ranaldo, s/bf-HSG 09.11.2012 # 1 Swissquote conference 2012 Limits to arbitrage during the crisis: funding liquidity constraints & covered interest parity Tommaso Mancini-Griffoli & Angelo Ranaldo Swissquote Conference 2012 on Liquidity and Systemic Risk EPFL Lausanne, Friday, 9th November 2012

Transcript of Limits to arbitrage during the crisis: funding liquidity ... · funding liquidity constraints &...

Angelo Ranaldo, s/bf-HSG 09.11.2012 # 1Swissquote conference 2012

Limits to arbitrage during the crisis:

funding liquidity constraints & covered

interest parity

Tommaso Mancini-Griffoli & Angelo Ranaldo

Swissquote Conference 2012 on Liquidity and Systemic Risk

EPFL Lausanne, Friday, 9th November 2012

Angelo Ranaldo, s/bf-HSG 09.11.2012 # 2Swissquote conference 2012

Research aims

To document deviations from the Covered Interest Rate

Parity (CIP) during the Crisis

To explain them

Angelo Ranaldo, s/bf-HSG 09.11.2012 # 3Swissquote conference 2012

Main findings

Keynes, J. M. (1923): A tract on monetary reform. “Floating capital normally available for the purpose of

taking advantage of arbitrage profits is by no means unlimited in amount“ (p. 129)

“The abnormal discount can only disappear when the high profit of arbitrage between spot and forward has drawn fresh capital into the arbitrage business” (p. 130)

Angelo Ranaldo, s/bf-HSG 09.11.2012 # 4Swissquote conference 2012

Related literature: FX arbitrage

FX arbitrage Prachowny (1970), Frenkel and Levich (1975, 1977) CIP: Taylor (1989), Rhee and Chang (1992), Akram, Rime, and

Sarno (2008) and Fong, Valente, and Fung (2010) On the crisis: Baba, Packer, and Nagano (2008), Baba and Packer

(2009b, 2009a), Coffey, Hrung, and Sarkar (2009), Genberg, Hui, Wong, and Chung (2009) and Jones (2009).

Angelo Ranaldo, s/bf-HSG 09.11.2012 # 5Swissquote conference 2012

Related literature: limits to arbitrage Limits of arbitrage

Surveys: Gromb and Vayanos (2010); Brunnermeier and Oehmke(2012)

Funding constraints: e.g. Brunnermeier and Pedersen (2009), Garleanu and Pedersen (2011), Gromb and Vayanos (2002), Kondor (2009)

Agency problems: e.g. Shleifer and Vishny (1992, 1997), Allen and Gorton (1993)

Heterogeneous beliefs: e.g. Miller (1977), Scheinkman and Xiong (2003)

Time horizons: e.g. Dow and Gorton (1994) Moral hazard: e.g. Acharya and Viswanathan (2011) Risk aversion: e.g. Xiong (2001) Slow-Moving Capitals: Duffie (2011)

Angelo Ranaldo, s/bf-HSG 09.11.2012 # 6Swissquote conference 2012

Related literature: crisis measures

Unconventional monetary policies

CIP and unconventional monetary policies

Angelo Ranaldo, s/bf-HSG 09.11.2012 # 7Swissquote conference 2012

CIP arbitrage

Angelo Ranaldo, s/bf-HSG 09.11.2012 # 8Swissquote conference 2012

How to perform CIP arbitrage

Secured arbitrage Unsecured arbitrage

Angelo Ranaldo, s/bf-HSG 09.11.2012 # 9Swissquote conference 2012

CIP arbitrage: unsecured

Lender L Borrower B

FX Counterparty

Spot Forward

1W – 1M

OIS contracts

Angelo Ranaldo, s/bf-HSG 09.11.2012 # 10Swissquote conference 2012

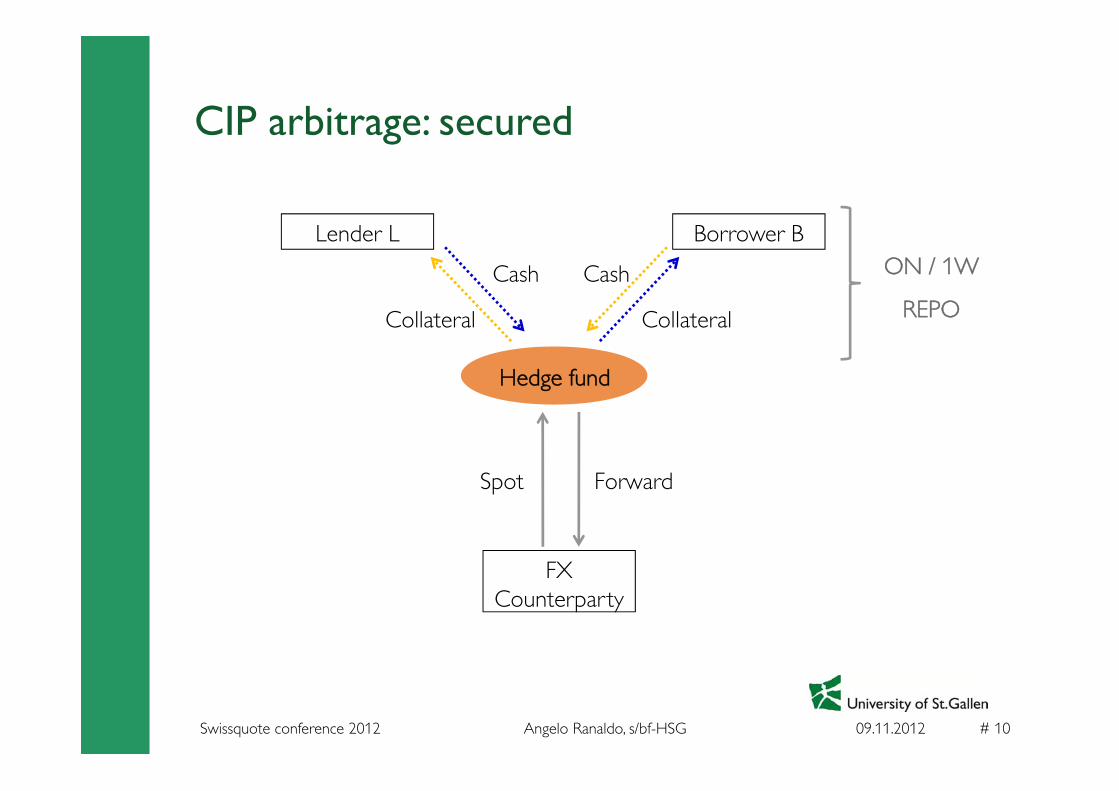

CIP arbitrage: secured

Lender L Borrower B

Hedge fund

FX Counterparty

Spot Forward

Cash

Collateral Collateral

Cash ON / 1W

REPO

Angelo Ranaldo, s/bf-HSG 09.11.2012 # 11Swissquote conference 2012

Replicating the CIP arbitrage

Our method to compute CIP takes into account:

1. Transaction costs pure profits2. Synchronicity no time bias3. Actual prices no mismeasurement4. Secured money market rates minimum risk

ARTtk

BRTtjA

t

BTt

t rrSFz ,

...,,...,

...,4 11

Angelo Ranaldo, s/bf-HSG 09.11.2012 # 12Swissquote conference 2012

Data

Asset Synch Maturity Bid / Ask Source

FX spt Snaps / All spot Yes TP / EBS

FX fwd Yes, snaps ON-2Y Yes TP

OIS Yes, snaps 1W-2Y Yes TP

REPO USD Snaps ON-3M Price ICAP

REPO EUR All trades ON-1Y Yes EUREX

REPO CHF All trades ON-3M Yes EUREX

EURUSD, USDJPY, GBPUSD, USDCHF, EURCHF

2006-20012

Angelo Ranaldo, s/bf-HSG 09.11.2012 # 13Swissquote conference 2012

Documenting CIP deviations

Angelo Ranaldo, s/bf-HSG 09.11.2012 # 14Swissquote conference 2012

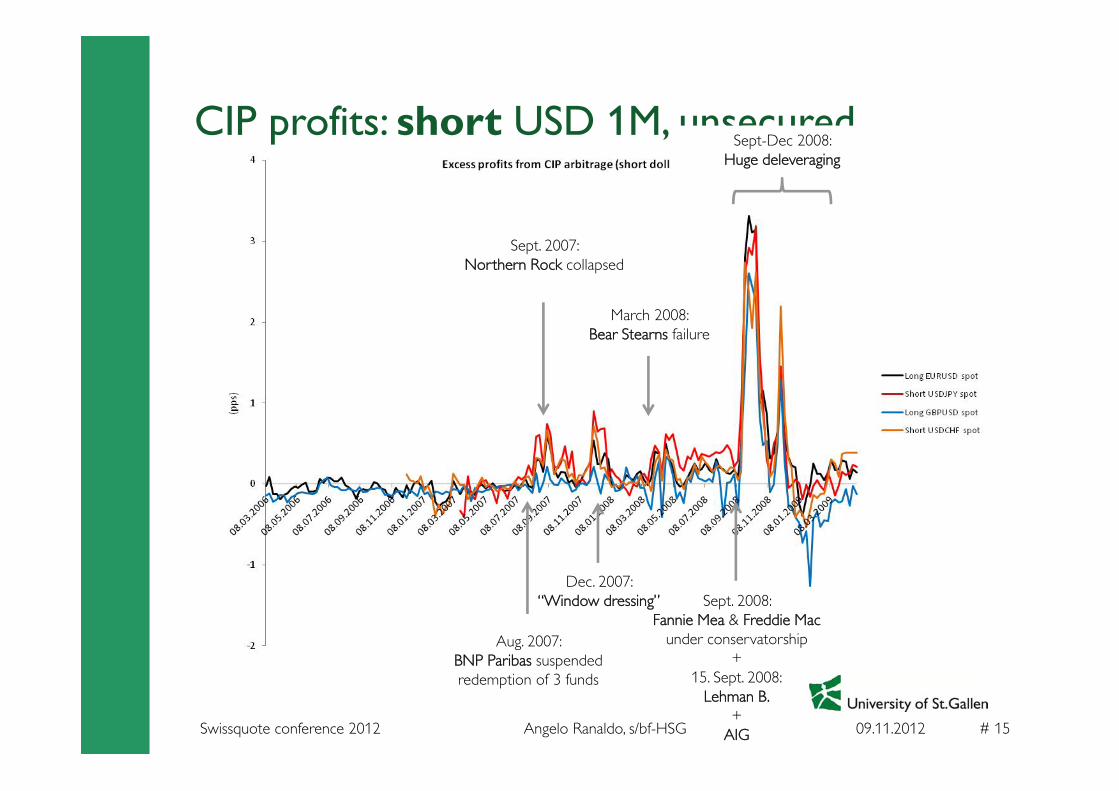

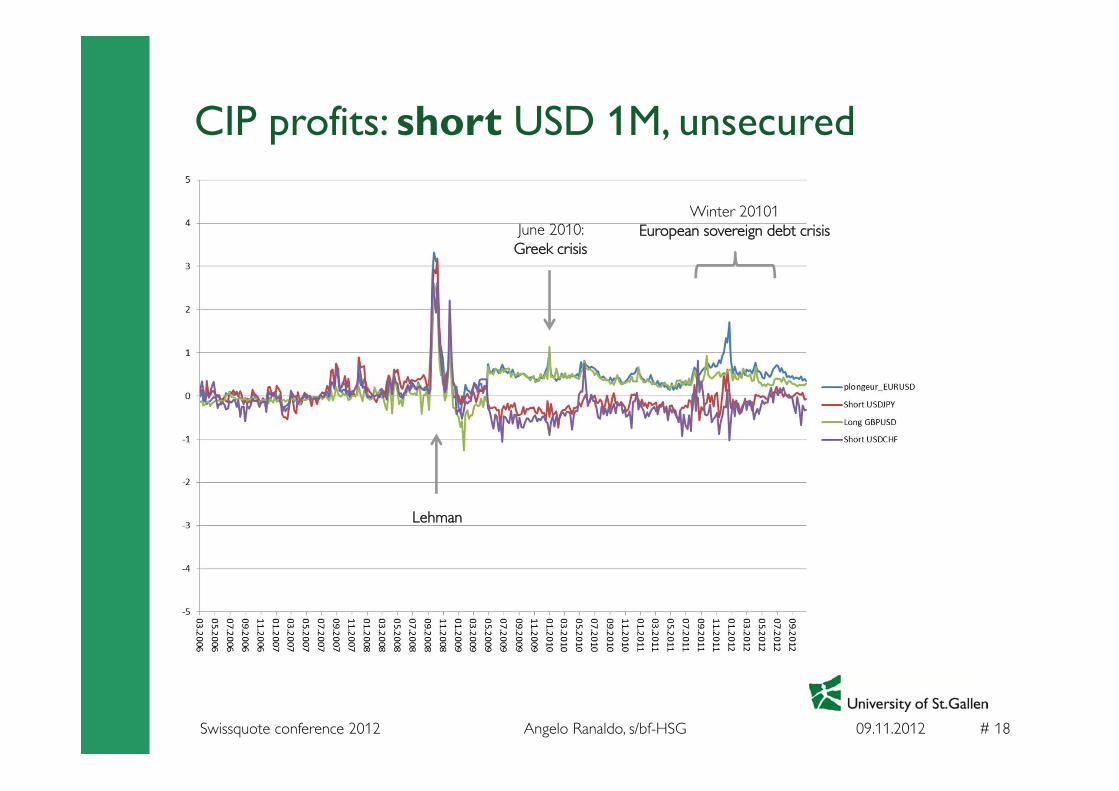

CIP profits: short USD 1M, unsecured

Angelo Ranaldo, s/bf-HSG 09.11.2012 # 15Swissquote conference 2012

CIP profits: short USD 1M, unsecured

Aug. 2007: BNP Paribas suspended redemption of 3 funds

Sept. 2007: Northern Rock collapsed

Dec. 2007: “Window dressing”

March 2008: Bear Stearns failure

Sept. 2008: Fannie Mea & Freddie Mac

under conservatorship+

15. Sept. 2008:Lehman B.

+AIG

Sept-Dec 2008: Huge deleveraging

Angelo Ranaldo, s/bf-HSG 09.11.2012 # 16Swissquote conference 2012

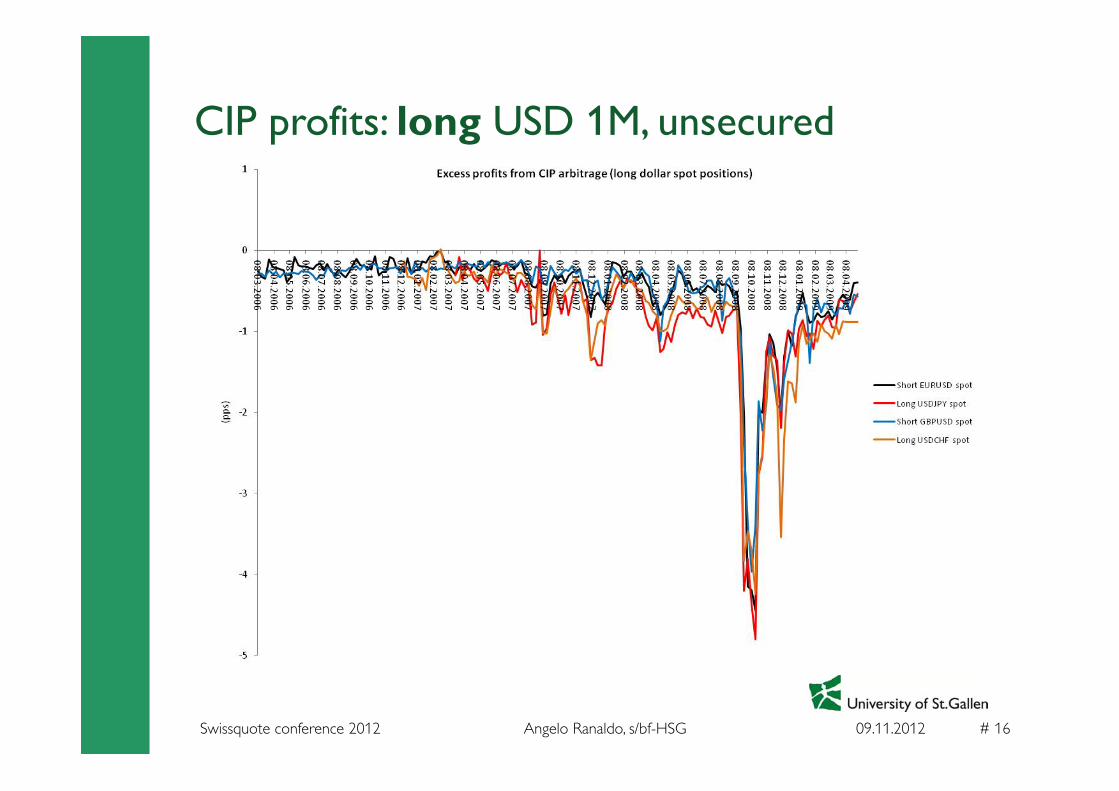

CIP profits: long USD 1M, unsecured

Angelo Ranaldo, s/bf-HSG 09.11.2012 # 17Swissquote conference 2012

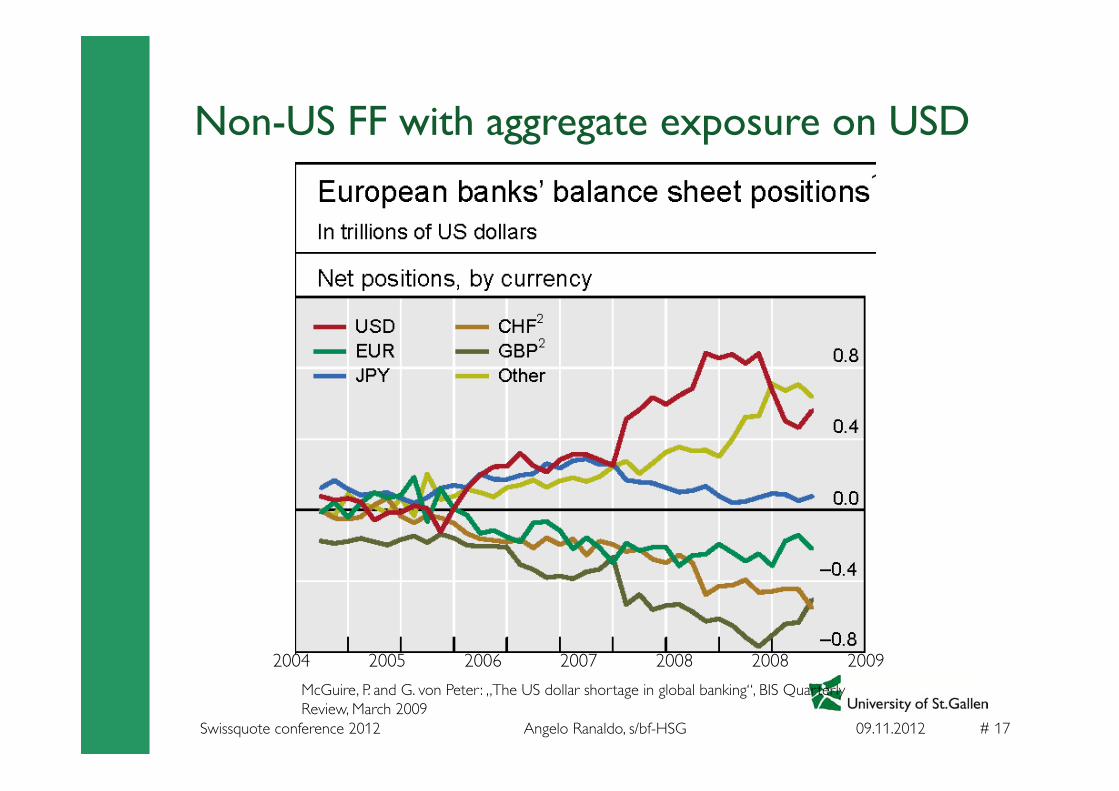

Non-US FF with aggregate exposure on USD

McGuire, P. and G. von Peter : „The US dollar shortage in global banking“, BIS Quarterly Review, March 2009

2004 2005 2006 2007 2008 2008 2009

Angelo Ranaldo, s/bf-HSG 09.11.2012 # 18Swissquote conference 2012

CIP profits: short USD 1M, unsecured

Lehman

June 2010: Greek crisis

Winter 20101European sovereign debt crisis

Angelo Ranaldo, s/bf-HSG 09.11.2012 # 19Swissquote conference 2012

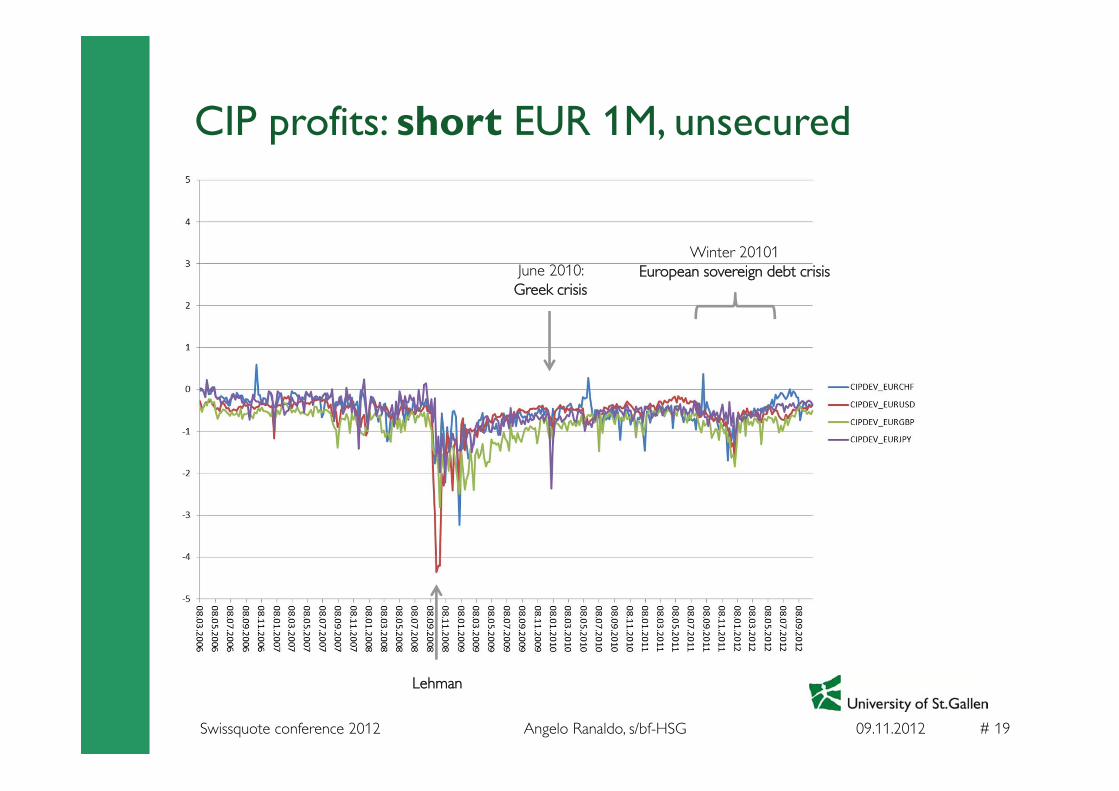

CIP profits: short EUR 1M, unsecured

Lehman

June 2010: Greek crisis

Winter 20101European sovereign debt crisis

Angelo Ranaldo, s/bf-HSG 09.11.2012 # 20Swissquote conference 2012

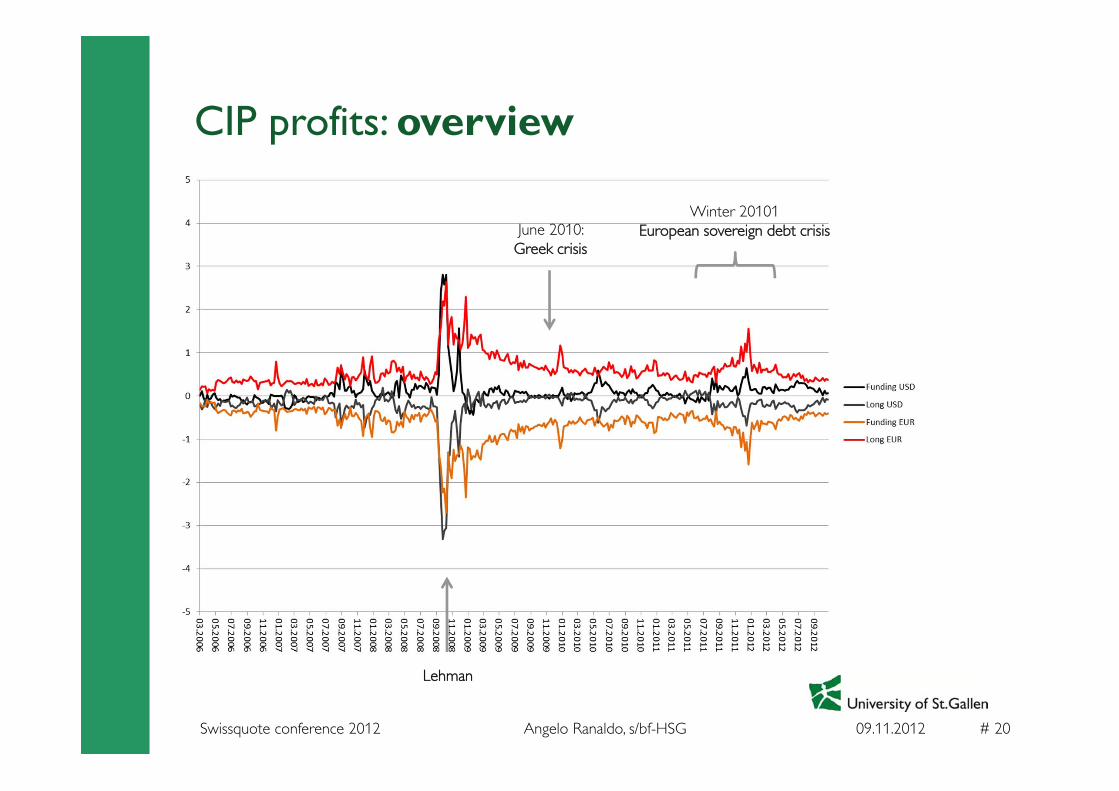

CIP profits: overview

June 2010: Greek crisis

Winter 20101European sovereign debt crisis

Lehman

Angelo Ranaldo, s/bf-HSG 09.11.2012 # 21Swissquote conference 2012

Takeaways

1. Excess profits are currency-specific2. Excess profits are directional: only when the USD (EUR) is the

funding (investment) currency3. Same picture for any trading strategy

Angelo Ranaldo, s/bf-HSG 09.11.2012 # 22Swissquote conference 2012

Explanations

Angelo Ranaldo, s/bf-HSG 09.11.2012 # 23Swissquote conference 2012

Why?

1. Market illiquidity

2. Funding constraints

3. Risk

Angelo Ranaldo, s/bf-HSG 09.11.2012 # 24Swissquote conference 2012

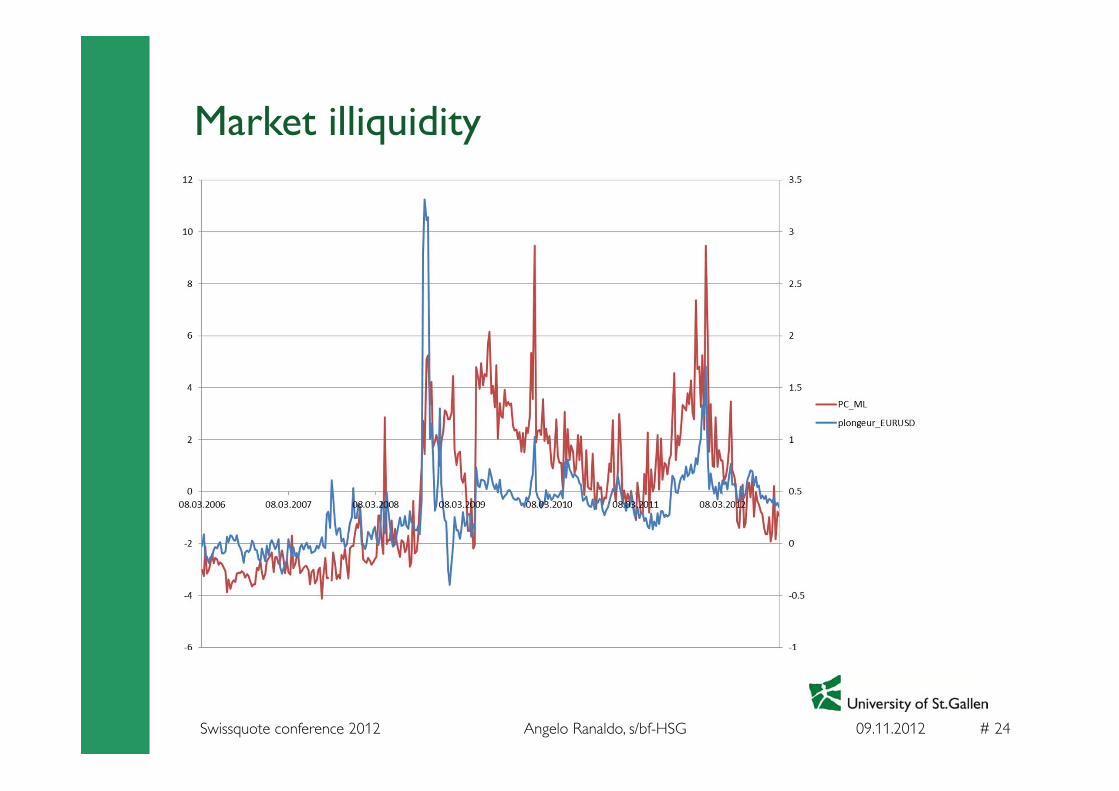

Market illiquidity

Angelo Ranaldo, s/bf-HSG 09.11.2012 # 25Swissquote conference 2012

Market illiquidity

Mancini, Ranaldo and Wrampelmeyer (JF, 2012)

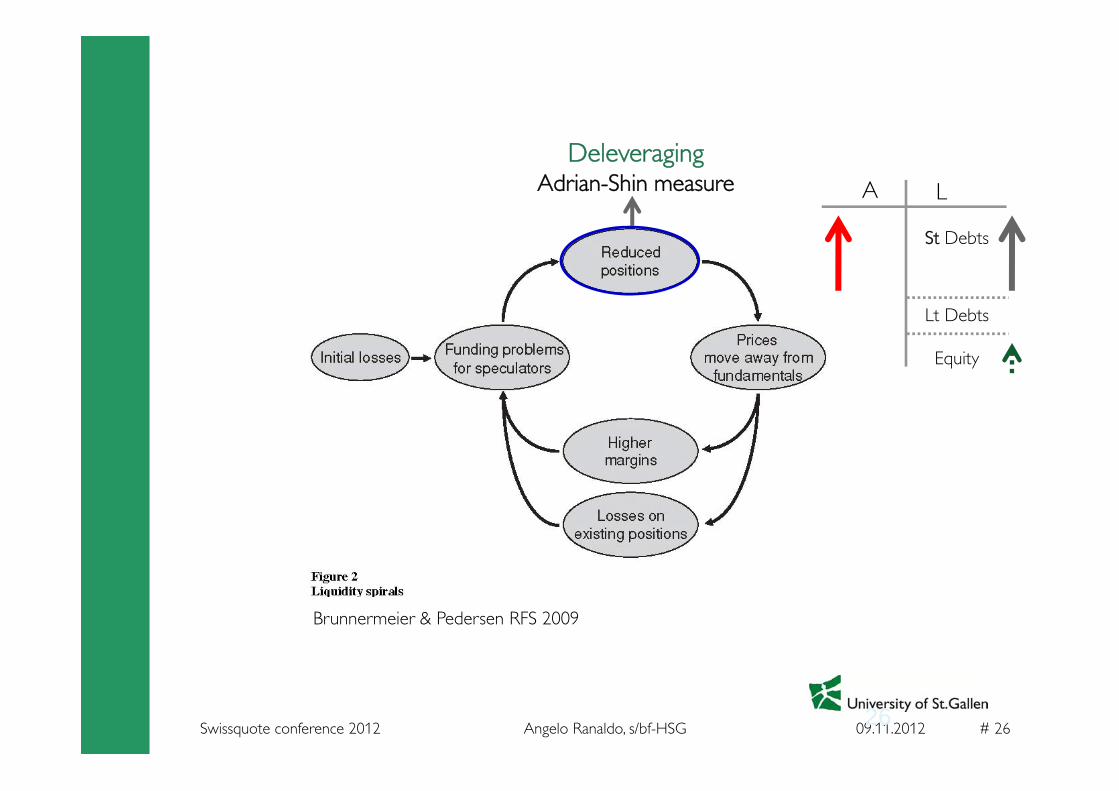

Angelo Ranaldo, s/bf-HSG 09.11.2012 # 26Swissquote conference 2012 26

DeleveragingAdrian-Shin measure A L

St Debts

Lt Debts

Equity

Brunnermeier & Pedersen RFS 2009

Angelo Ranaldo, s/bf-HSG 09.11.2012 # 27Swissquote conference 2012 27

Prudential hoardingbank deposits left at the FED NY

A L

St Debts

Lt Debts

Equity

St AssetsCash USD

Lt Assets

Angelo Ranaldo, s/bf-HSG 09.11.2012 # 28Swissquote conference 2012 28

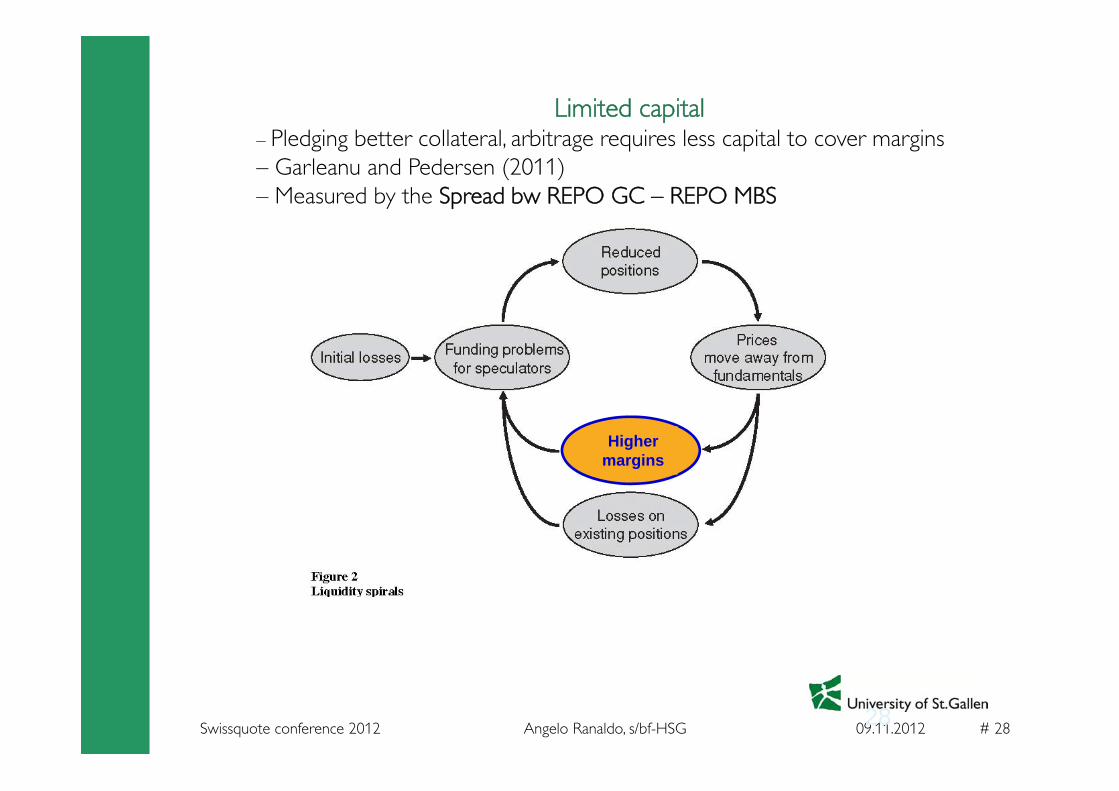

Higher margins

Limited capital– Pledging better collateral, arbitrage requires less capital to cover margins– Garleanu and Pedersen (2011)– Measured by the Spread bw REPO GC – REPO MBS

Angelo Ranaldo, s/bf-HSG 09.11.2012 # 29Swissquote conference 2012

Risk: 3 elements

Lender L Borrower B

Trader

FX Counterparty

Spot Forward

Counterparty Default Risk

Measured by CDS banks

Contract Risk

Measured by option-implied FX volatility

Roll-over Risk

Measured by interest-rate

spreads

Angelo Ranaldo, s/bf-HSG 09.11.2012 # 30Swissquote conference 2012

Empirical analysis

Angelo Ranaldo, s/bf-HSG 09.11.2012 # 31Swissquote conference 2012 31

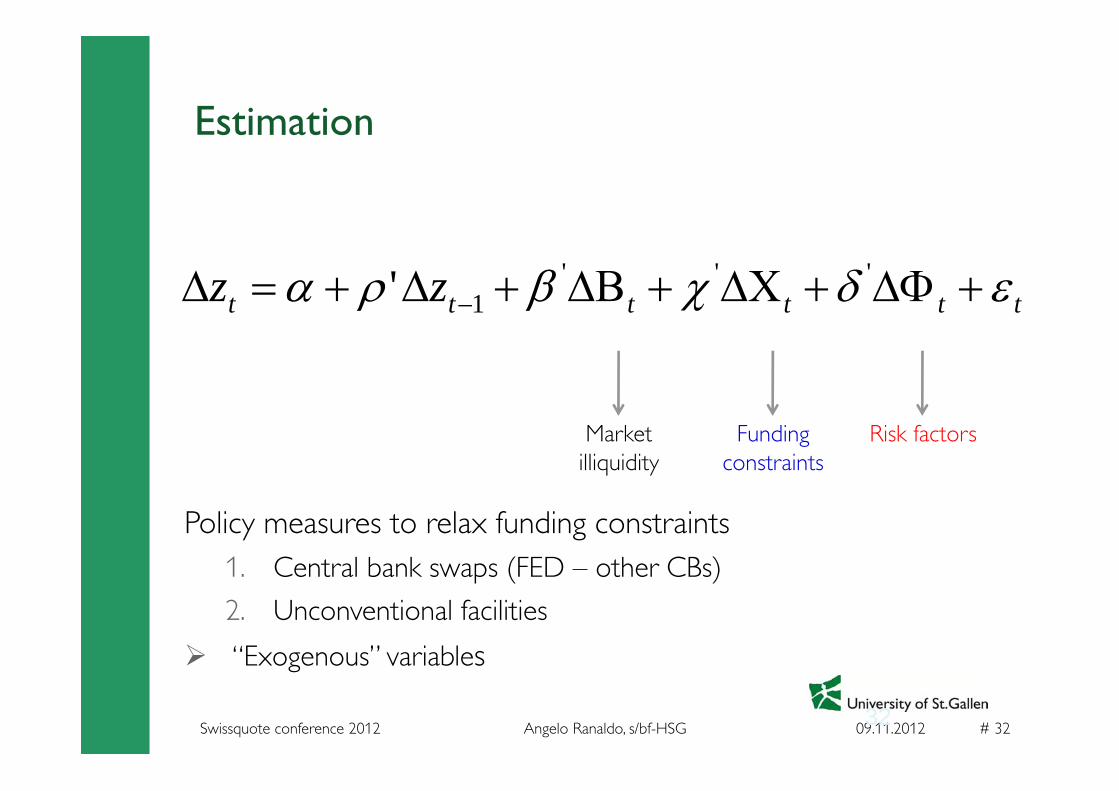

Estimation

tttttt zz '''

1'

Market illiquidity

Funding constraints

Risk factors

Angelo Ranaldo, s/bf-HSG 09.11.2012 # 32Swissquote conference 2012 32

Estimation

tttttt zz '''

1'

Market illiquidity

Funding constraints

Risk factors

Policy measures to relax funding constraints1. Central bank swaps (FED – other CBs)

2. Unconventional facilities

“Exogenous” variables

Angelo Ranaldo, s/bf-HSG 09.11.2012 # 33Swissquote conference 2012

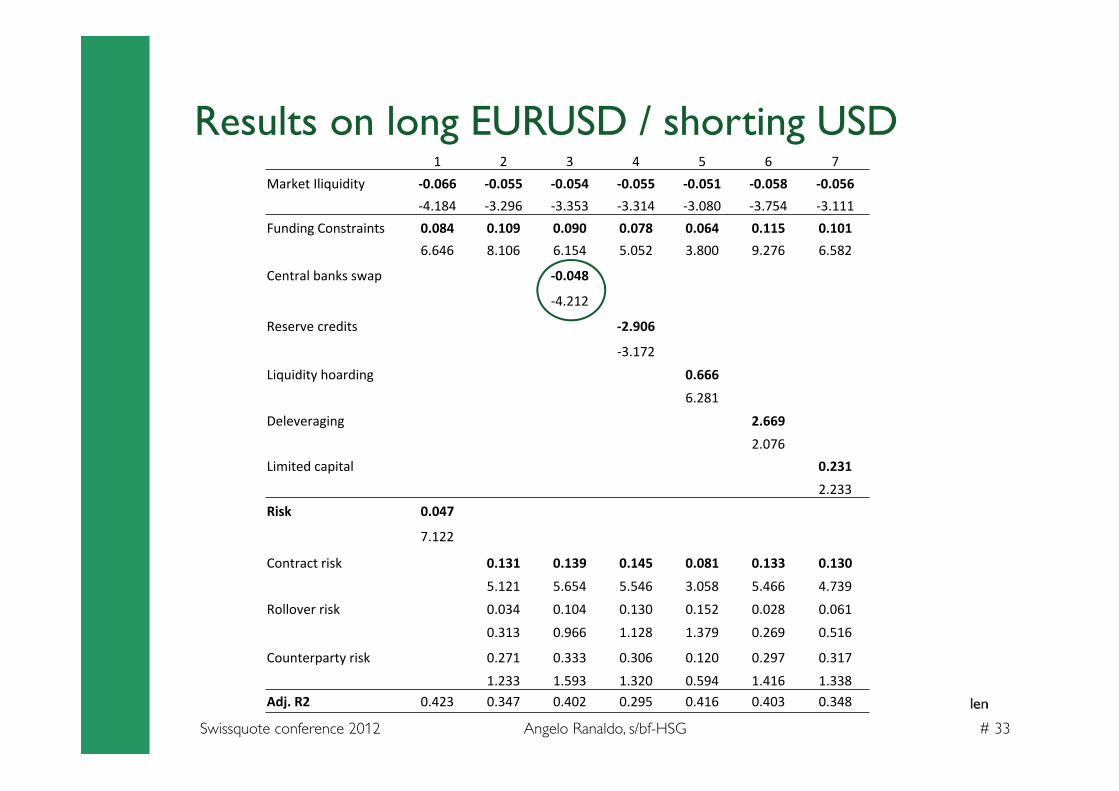

Results on long EURUSD / shorting USD1 2 3 4 5 6 7

Market Iliquidity ‐0.066 ‐0.055 ‐0.054 ‐0.055 ‐0.051 ‐0.058 ‐0.056‐4.184 ‐3.296 ‐3.353 ‐3.314 ‐3.080 ‐3.754 ‐3.111

Funding Constraints 0.084 0.109 0.090 0.078 0.064 0.115 0.1016.646 8.106 6.154 5.052 3.800 9.276 6.582

Central banks swap ‐0.048

‐4.212

Reserve credits ‐2.906

‐3.172

Liquidity hoarding 0.666

6.281

Deleveraging 2.669

2.076Limited capital 0.231

2.233Risk 0.047

7.122

Contract risk 0.131 0.139 0.145 0.081 0.133 0.130

5.121 5.654 5.546 3.058 5.466 4.739

Rollover risk 0.034 0.104 0.130 0.152 0.028 0.061

0.313 0.966 1.128 1.379 0.269 0.516

Counterparty risk 0.271 0.333 0.306 0.120 0.297 0.317

1.233 1.593 1.320 0.594 1.416 1.338Adj. R2 0.423 0.347 0.402 0.295 0.416 0.403 0.348

Angelo Ranaldo, s/bf-HSG 09.11.2012 # 34Swissquote conference 2012 34

FED measures

AMLFDiscount Window

MBS purchase

PDCF CPCB swap

linesTAF

Total USD Trillion 0.22 15.76 1.85 8.95 0.74 10.06 3.82

US % 100% 65% 48% 94% 44% 0% 45%

FGN % 0% 35% 52% 6% 56% 100% 55%

Angelo Ranaldo, s/bf-HSG 09.11.2012 # 35Swissquote conference 2012 35

Additional tests & robustness

1. Panel regressions

2. No endogeneity problems

– Hausman tests

– Structural VAR

3. Sub-samples

– The results are not biased by Lehman

4. Other maturities

5. Other intraday snaps

Angelo Ranaldo, s/bf-HSG 09.11.2012 # 36Swissquote conference 2012

Conclusion

Angelo Ranaldo, s/bf-HSG 09.11.2012 # 37Swissquote conference 2012 37

Conclusion

Limits to arbitrage

Funding liquidity constraints

Unconventional monetary policies