Life Sciences Licensing — Trends and Issues

41

Life Sciences Licensing 2015 – Trends and Issues October 7, 2015 Paul Armitage*, Partner *Law Corporation

-

Upload

this-account-is-closed -

Category

Law

-

view

9.548 -

download

6

Transcript of Life Sciences Licensing — Trends and Issues

Life Sciences Licensing

2015 – Trends and Issues

October 7, 2015

Paul Armitage*, Partner *Law Corporation

2

Financial terms

Financial components of licenses - % of deals*

• Upfront payment: 75%

• Technology access fee: 5%

• Equity investment: 22%

• R&D funding: 33%

• Development milestones: 68%

• Sales milestones: 52%

*LES, Global “Life Sciences” Royalty Rates & Deal Terms Survey 2014 (for years 2012-2014)

Financial terms

Royalty rate structure - % of deals*

• Flat royalty: 64%

• Reflects overall trend of early stage of licensing (see

later) - flat royalty most common for preclinical deals

• Tiered royalties: 17%

• No royalty: 19%

* LES, Global “Life Sciences” Royalty Rates & Deal Terms Survey 2014 (for years 2012-2014)

3

Financial terms

Tiered royalties*

• Usually 3 tiers (2 or 5 tiers next most common)

• Tiered royalties more likely to be used with greater

peak sales potential

• $0-100m: 80% of deals are flat royalty

• >$100m: approx. 50% of deals are tiered royalties

Tiered royalties: associated with more complex

payment designs (biobucks, equity, funding,

etc.)

* LES, Global “Life Sciences” Royalty Rates & Deal Terms Survey 2014 (for surveys 2008, 2009,

2012, 2014)

4

Financial terms

What are royalties paid-on? - % of deals*

• Net sales: 76%

• Gross sales: 13%

• Units: 3%

* LES, Global “Life Sciences” Royalty Rates & Deal Terms Survey 2014 (for years 2012-2014)

5

Financial terms

Profit-sharing / co-promotion - % of deals*

• Profit-sharing component: 29%

• No profit-sharing component: 71%

• Co-promotion: 7%; additional 3% with opt-in

• Lack of profit-sharing and lack of co-promotion go hand-

in-hand

* LES, Global “Life Sciences” Royalty Rates & Deal Terms Survey 2014 (for years 2012-2014)

6

Financial terms

Average flat royalty by stage of development*

* LES, Global “Life Sciences” Royalty Rates & Deal Terms Survey 2014 (for surveys 2008, 2009,

2012, 2014)

7

Preclinical through IND-filed: 4.6%

Phase I enrolling through Phase II enrolling: 5%

Phase II completed through Phase III completed:

i.e., royalties double with proof of concept established

10.2%

NDA submitted through to launched:

12.5%

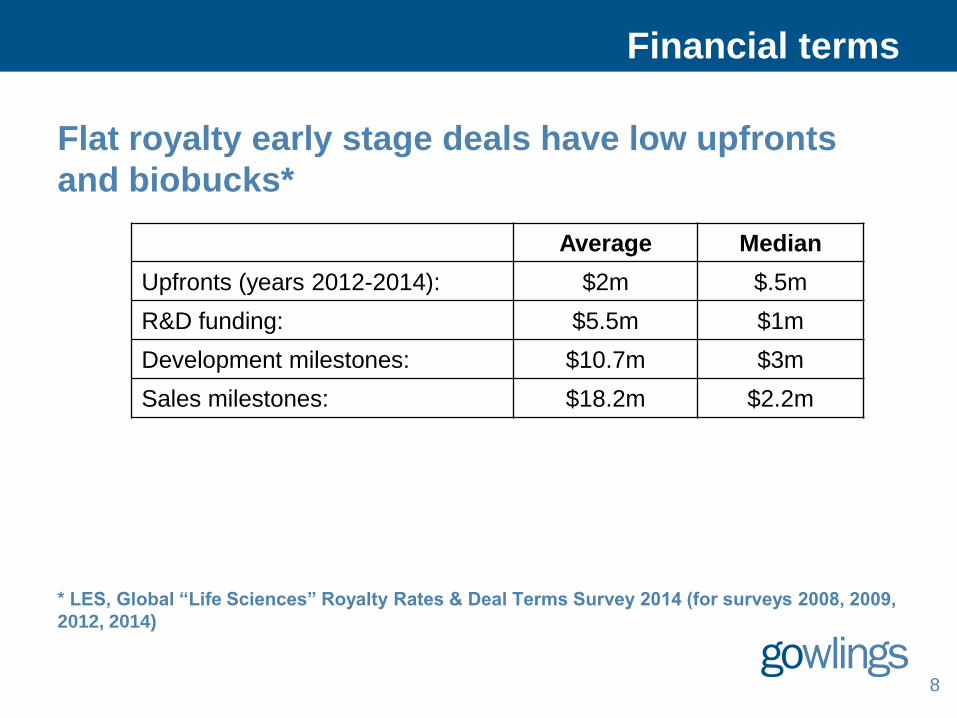

Financial terms

Flat royalty early stage deals have low upfronts

and biobucks*

* LES, Global “Life Sciences” Royalty Rates & Deal Terms Survey 2014 (for surveys 2008, 2009,

2012, 2014)

8

Average Median

Upfronts (years 2012-2014): $2m $.5m

R&D funding: $5.5m $1m

Development milestones: $10.7m $3m

Sales milestones: $18.2m $2.2m

Financial terms

Tiered royalty rates increase with stage of

development*

* LES, Global “Life Sciences” Royalty Rates & Deal Terms Survey 2014 (for surveys 2008, 2009,

2012, 2014)

9

Preclinical through IND-filed: 6% through 8% tiers

Phase I enrolling through Phase II enrolling: 10% through 14% tiers

Phase II completed through Phase III

completed:

11% through 15% tiers

Tiered royalty deals have greatest biobucks

immediately pre-proof of concept*

This shows that pre-proof of concept, the licensor

shoulders more risk

* LES, Global “Life Sciences” Royalty Rates & Deal Terms Survey 2014 (for surveys 2008, 2009,

2012, 2014)

Financial terms

Upfronts

Development

Milestones

Sales

Milestones

Preclinical through IND-filed $2m $30m $35m

Phase I enrolling through

Phase II enrolling $4m $125m $135m

Phase II completed through

Phase III completed $5m $12m $42m

10

Financial terms

Deal terms – diagnostics*

• Typical deal - % of deals

• Small upfront payment: 46%

• Royalty: main component

• 75% based on net sales; 10.3% based on gross sales, 6.9%

based on units

• 50% of deals had royalty rate of <5%

• 25% of deals had a royalty rate equal to or greater than 11%

• R&D funding: 17%

• Development milestones: 20%

• Sales milestones: 17%

* LES, Global “Life Sciences” Royalty Rates & Deal Terms Survey 2014 (for surveys 2008, 2009,

2012, 2014)

11

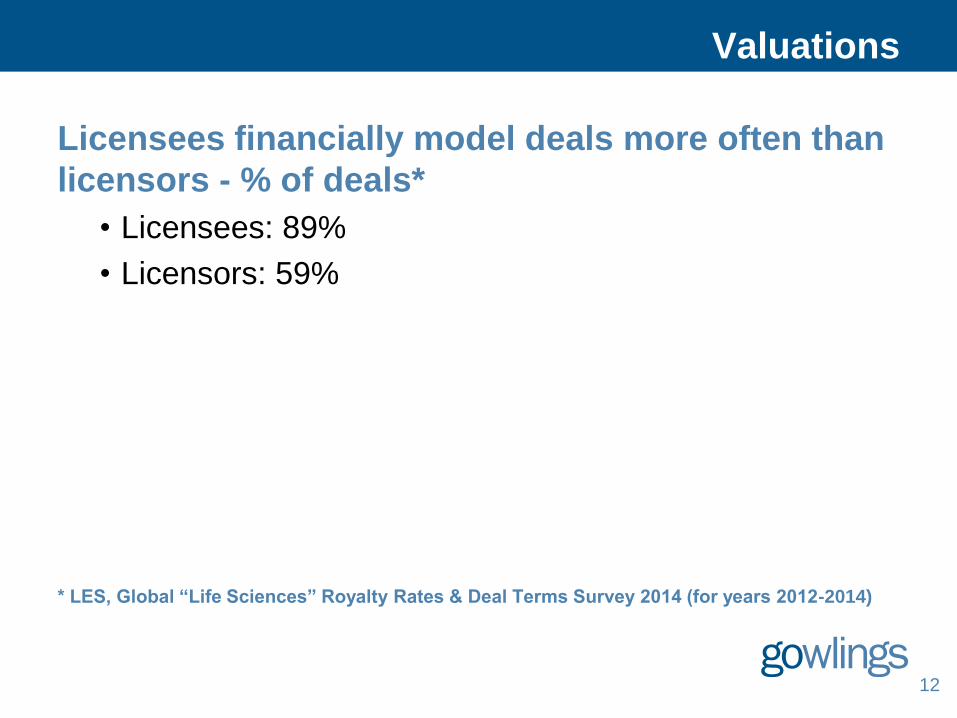

Valuations

Licensees financially model deals more often than

licensors - % of deals*

• Licensees: 89%

• Licensors: 59%

* LES, Global “Life Sciences” Royalty Rates & Deal Terms Survey 2014 (for years 2012-2014)

12

Valuations

Operating companies with >250m in revenue are

more likely to model deals - % of deals*

• >250m in revenue: 92%

• <250m in revenue: 71%

* LES, Global “Life Sciences” Royalty Rates & Deal Terms Survey 2014 (for years 2012-2014)

13

Valuations

Modeling more likely as stage of development

advances - % of deals*

* LES, Global “Life Sciences” Royalty Rates & Deal Terms Survey 2014 (for years 2012-2014)

14

Preclinical through IND-filed: 63%

Phase I enrolling through Phase II enrolling: 67%

Phase II completed through Phase III completed: 100%

NDA submitted through to launched: 100%

Valuations

How do companies financially model deals? All

models used*

• NPV: 65%

• Comparables: 53%

• Peak revenue: 41%

• IRR: 31%

• rNPV: 29%

• Multiples: 7%

• Other: 5%

* LES, Global “Life Sciences” Royalty Rates & Deal Terms Survey 2014 (for years 2012-2014)

15

Valuations

How do companies financially model deals?

Primary model used*

• NPV: 31%

• Comparables: 31%

• rNPV: 14%

• IRR: 10%

• Peak revenue: 9%

* LES, Global “Life Sciences” Royalty Rates & Deal Terms Survey 2014 (for years 2012-2014)

16

Valuations

How do companies financially model deals?*

• Early stage deals are more likely to look at

comparables

• Later stage deals are more likely to include other

valuation techniques

* LES, Global “Life Sciences” Royalty Rates & Deal Terms Survey 2014

17

Valuations

Does modeling make a difference?*

• Financially modeled deals have higher fixed royalties

• Modeled deals: 9% royalty

• Not modeled deals: 6.7% royalty

• Final deal structure reflected pre-negotiation valuation

66% of the time for compounds

* LES, Global “Life Sciences” Royalty Rates & Deal Terms Survey 2014 (for years 2012-2014)

18

The continuing saga of the patent cliff

• 2015: pharma industry will replace by nearly

x4 lost sales due to patent expiries*

• This trend will continue to 2020 (x5 sales replacement

forecast)

• Compare to 2011: new sales replacement roughly

equalled sales lost due to patent expiries

• Top line sales bolstered by growing proportion of drug

sales comprised of biologics

• 2014: 40% of new drugs approved by U.S.

FDA were new biologics (1 biosimilar to

date)**

* Pharma & Biotech 2015 Preview, EvaluatePharma

** World Preview 2015, Outlook to 2020, EvaluatePharma

19

The continuing saga of the patent cliff

• 2014*:

• U.S. FDA: 41 novel medicines approved (2nd highest all-

time next to 53 in 1996)

• 40% are specialty drugs for rare diseases (typically

have easier regulatory pathway and lower clinical trial

costs)

• EMA: 82 new medicines (including generics), compared

to 79 in 2013 and 57 in 2012

• 2015**: U.S. FDA on track for up to 50 novel

medicines * “Pharma and biotech on a roll as drug approvals hit 18-year high,” Business News, January 5,

2015

** 2015 Pharma and Biotech Half-Year Review, Evaluate

20

The continuing saga of the patent cliff

• 2016 R&D spending in biopharmaceutical and

health care industries: $145b*

• 6% increase from 2013

• R&D increasing due to need to increase the number of

new drugs and replace lost sales due to patent

expiries

* “Quintiles projects increase in biopharma R&D spending,” Triangle Business Journal,

February 20, 2014

21

The continuing saga of the patent cliff

U.S. more aggressive in trade negotiations to expand

protection of U.S. pharma industry* – TPP and data

exclusivity

• Canada’s hot button issue is dairy, Japan’s is rice, U.S.’ is

pharmaceuticals**

• 12 TPP countries: 5,600 medicines in development in total, of

which 3,372 are in the U.S. including >900 biologics. Pharma

industry contributes $800b to U.S. economy each year

• U.S.: pushed for 12 years of data exclusivity for biologics (matching

current U.S. domestic law); other countries wanted 8 years or fewer

(Australia, with nationalized health that covers drugs, wanted 5)

• Compromise is hybrid solution of 8 or 5 years, plus up to 3 more

years * “With protections set to lapse on advanced drugs, U.S. presses strict rules overseas,” The

Washington Post, March 17, 2014

** “Patent Protection for Drugs Puts Pressure on U.S. in Trade Talks”, New York Times, July 30,

2015

22

“More payer pressure, more commercialization risk”

Question: what’s the biggest deduction from Net

Sales calculations?

“Net Sales” means the gross amount invoiced by

Licensee, its affiliates and sublicensees for products

sold, less the following deductions:

(i) trade, quantity and cash discounts;

(ii) refunds, returns, recalls;

(iii) rebates;

(iv) tariffs, duties, taxes; and

(v) freight and insurance.

23

“More payer pressure, more commercialization risk”

Discounts/rebates are now the largest

commercial cost to pharma*

• Average discounts/rebates

• 2007 (all branded drugs): 17%

• 2013 (all branded drugs): 29%

• 2015 (HCV): 45%

* RealEndpoints 2015

24

“More payer pressure, more commercialization risk”

New, expensive specialty drugs are driving

growth in health costs*

• Growth in spending 2014:

• Traditional drugs: up 6%

• Speciality drugs: up 30%

* RealEndpoints 2015

25

“More payer pressure, more commercialization risk”

Responses by payers (government, private

insurers, employers)*

• Stricter management of drug benefits

• e.g., patient co-pay, prior authorization, quantity limits

• Notice from B.C. government: “Effective January 1,

2015. BC PharmaCare is limiting the number of

blood glucose strips it covers for a patient each

calendar year...”

* RealEndpoints 2015

26

“More payer pressure, more commercialization risk”

Responses by payers (government, private

insurers, employers)*

• Purchasing pressure*

• Relative value - cost-benefit analysis: does the

(incremental) benefit justify the (higher) cost?

• Traditional drugs (established drugs in older product

categories where competition has long existed) will face

less price pressure; BUT new entrants where there are

traditional drugs will face strong price pressure

* RealEndpoints 2015

27

“More payer pressure, more commercialization risk”

Responses by payers (government, private

insurers, employers)

• Purchasing pressure*

• Payers pit suppliers against each other to drive

discounts/rebates: payers will look to add competitive

products on formulary and require discounts from all

suppliers in order to be listed

• Prices fall in competitive classes:

• HCV 2013 (1 treatment, Sovaldi): $90+G

• HCV 2019 projected (5 treatments): $35G

* RealEndpoints 2015

28

“More payer pressure, more commercialization risk”

Responses by payers (government, private

insurers, employers)

• Purchasing pressure*

• Payers may restrict access until competitive products

appear

• Biosimilars will also have a role in creating competition in

specialty drugs and therefore controlling biologics spending

(although biosimilars are typically only 20-30% cheaper

than branded biologics, compared with generics being 80-

90% cheaper)

• First-in-class entrants therefore may be less valuable as

payers seek to delay widespread adoption until

competitive products emerge

* RealEndpoints 2015

29

Licensing as a commercialization strategy

No. of licenses and JVs continues to rise*

2012: 528

2013: 690

2014: 739

2015 Q1: 213

* Allicense 2015

30

Licensing as a commercialization strategy

Early stage licensing continues to dominate*

• 2014:

• Discovery/lead, preclinical (2/3s discovery): 66%

• Clinical/approved: 34%

• Fairly consistent over last 5 years, with discovery stage

licensing intensifying

* Allicense 2015

31

Licensing as a commercialization strategy

Early stage licensing continues to dominate*

• Discovery/pre-IND: 66%

• IND-filed/approved: 34%

* LES, Global “Life Sciences” Royalty Rates & Deal Terms Survey 2014 (for years 2012-2014)

32

Licensing as a commercialization strategy

Worldwide rights deals: almost 70%*

• Total number of regional deals (ex-U.S.) is increasing**

• 2007 – 2010 EU, Japan/Asia, other: average of 51 per year

• 2011 – 2014 EU, Japan/Asia, other: average of 95 per year

* LES, Global “Life Sciences” Royalty Rates & Deal Terms Survey 2014 (for years 2012-2014)

** Allicense 2015

33

Licensing as a commercialization strategy

2014 life sciences dealmaking*

• Deal volume (no. of deals):

• Licenses, JVs: 25%

• M&A, asset purchase: 19%

• Deal dollars:

• Licenses, JVs: 5%

• M&A, asset purchases: 92%

* Allicense 2015

34

Licensing as a commercialization strategy

2015 Q1 life sciences dealmaking*

• Deal volume (no. of deals):

• Licenses, JVs: 27%

• M&A, asset purchase: 9%

• Deal dollars:

• Licenses, JVs: 15%

• M&A, asset purchases: 83%

* Allicense 2015

35

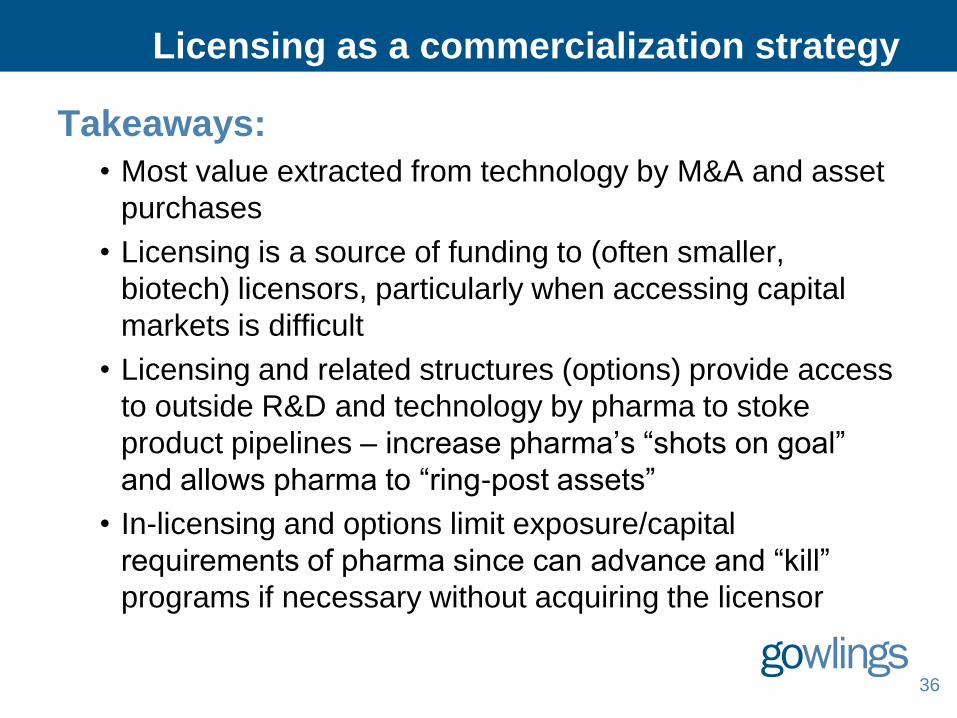

Licensing as a commercialization strategy

Takeaways:

• Most value extracted from technology by M&A and asset

purchases

• Licensing is a source of funding to (often smaller,

biotech) licensors, particularly when accessing capital

markets is difficult

• Licensing and related structures (options) provide access

to outside R&D and technology by pharma to stoke

product pipelines – increase pharma’s “shots on goal”

and allows pharma to “ring-post assets”

• In-licensing and options limit exposure/capital

requirements of pharma since can advance and “kill”

programs if necessary without acquiring the licensor

36

Licensing as a commercialization strategy

• Licensing/partnering early stage, non-core assets

while maintaining rights to lead programs can be a

viable strategy*

• Allows company to focus on lead programs, which are

left unencumbered

• Provides non-dilutive capital to allow for further

development of lead programs

• Validates platform

• Regional licensing allows for similar strategies

* Locust Walk Partners 2015

37

Academic to industry licensing

Typical deal*

• Stage of deal: 65% are for preclinical through IND filed

assets

• Stage of licensee: 44% have a pre-commercial

licensee

* LES, Global “Life Sciences” Royalty Rates & Deal Terms Survey 2014

38

Academic to industry licensing

Deal terms*

• Academic licensor to pre-commercial licensee: 70%

use flat royalties

• Valuation technique typically used is comparable deals

• Pre-commercial sub-licensor to large company

licensee: 60% use tiered royalties

• Use of tiered royalties reflects later stage licensing: as

expected product revenue increases, tiered royalty

structures are used more often

* LES, Global “Life Sciences” Royalty Rates & Deal Terms Survey 2014

39

Academic to industry licensing

Who creates and captures value in academic to

industry licensing?*

• Small companies that in-license preclinical through IND-

filed assets from academic institutions create and then

capture substantial value from the asset if they advance

the assets to Phase I

• rNPV royalty/biobucks to academic licensor: $3.5m

• rNPV royalty/biobucks to small company sub-licensor: $26.7m

* LES, Global “Life Sciences” Royalty Rates & Deal Terms Survey 2014

40

Thank You

montréal ottawa toronto hamilton waterloo region calgary vancouver beijing moscow london

Paul Armitage

Tel: 604-891-2779

Email: [email protected]