13-1 ©2011 Pearson Education, Inc. Publishing as Prentice Hall.

Upload

toby-masonCategory

view

216download

0

Life and Health Insurance

9-2Copyright © 2010 Pearson Education, Inc. Publishing as Prentice Hall

Learning Objectives

1. Understand the importance of insurance.

2. Determine your life insurance needs and design a life insurance program.

3. Describe the major types of coverage available and the typical provisions that are included.

9-3Copyright © 2010 Pearson Education, Inc. Publishing as Prentice Hall

Learning Objectives

4. Design a health care insurance program and understand what provisions are important to you.

5. Describe disability insurance and the choices available to you.

6. Explain the purpose of long-term care insurance and the provisions that might be important to you.

9-4Copyright © 2010 Pearson Education, Inc. Publishing as Prentice Hall

Introduction

Health insurance is an issue none of us can afford to dismiss.

Most of us avoid thinking about and planning for our deaths—most of us do not seek out a life insurance policy.

When you consider your need for insurance, need to keep in mind its purpose.

9-5Copyright © 2010 Pearson Education, Inc. Publishing as Prentice Hall

The Importance of Insurance

An insurance policy spells out what losses are covered, what the policy costs, and who receives payment.

Health insurance provides protection against devastating medical bills.

Life insurance protects your family if you die.

9-6Copyright © 2010 Pearson Education, Inc. Publishing as Prentice Hall

The Importance of Insurance

Health care is expensive because:no incentive to economize.Medical care is extremely sophisticated.High malpractice insurance costs.

High costs mean limited insurance coverage, no health benefits, and higher out-of-pocket payments for medical bills.

9-7Copyright © 2010 Pearson Education, Inc. Publishing as Prentice Hall

Do You Need Life Insurance?Risk pooling—through insurance, sharing

financial consequences of riskPremiumActuariesFace amount or face of policy - amount of

insurance provided at death.Policy owner or policyholder.Beneficiary – designated to receive the

proceeds.Life insurance doesn’t make sense

without a spouse or dependents

9-8Copyright © 2010 Pearson Education, Inc. Publishing as Prentice Hall

9-9Copyright © 2010 Pearson Education, Inc. Publishing as Prentice Hall

How Much Life InsuranceDo You Need?

Priorities and goals

Crunch the numbers—networth, inflation and future earnings

Earnings Multiple Approach

Needs Approach

9-10Copyright © 2010 Pearson Education, Inc. Publishing as Prentice Hall

Earnings Multiple ApproachReplace a stream of lost annual income.

Tells you a lump-sum needed to replace that stream of annual income

Multiply present annual gross income by the appropriate earnings multiple.

Earnings multiple depends on number of years you need the lost income and rate of return

9-11Copyright © 2010 Pearson Education, Inc. Publishing as Prentice Hall

9-12Copyright © 2010 Pearson Education, Inc. Publishing as Prentice Hall

Needs Approach

Determine the needs of a family after the death of the breadwinner?

Immediate needs at time of deathDebt elimination fundsImmediate transitional fundsDependency expensesSpousal life incomeEducational expenses for childrenRetirement income

9-13Copyright © 2010 Pearson Education, Inc. Publishing as Prentice Hall

Major Types of Life Insurance

Term insurance – pure life insurance that pays beneficiary a specific amount of money if you die while covered.

Cash-value insurance – has a life insurance and a savings plan

9-14Copyright © 2010 Pearson Education, Inc. Publishing as Prentice Hall

9-15Copyright © 2010 Pearson Education, Inc. Publishing as Prentice Hall

Term Insurance and Its FeaturesPays the death benefit if insured dies during

the coverage period.

Has no face value.

Primary advantage is affordability.

Disadvantage is that the cost increases each time the policy is renewed.

9-16Copyright © 2010 Pearson Education, Inc. Publishing as Prentice Hall

Term Insurance and Its FeaturesRenewable term insurance

Decreasing term insurance

Group term insurance

Credit and mortgage group life insurance

Convertible term life insurance

9-17Copyright © 2010 Pearson Education, Inc. Publishing as Prentice Hall

Cash-Value Insuranceand Its Features

Provides both a death benefit and an opportunity to accumulate cash value.

Permanent—pay the premiums and eventually you will get paid.

3 basic types:Whole LifeUniversal LifeVariable Life

9-18Copyright © 2010 Pearson Education, Inc. Publishing as Prentice Hall

Whole Life Insuranceand Its Features

death benefit when the insured dies, turns 100, or reaches the maximum stated age.

Cash-value—policyholder’s savings

Nonforfeiture Right—gives the policyholder the right to choose the policy’s cash value in exchange for giving up the death benefit.

Different premium payment patterns

9-19Copyright © 2010 Pearson Education, Inc. Publishing as Prentice Hall

Universal Life Insuranceand Its Features

Combines term insurance with tax-deferred savings with flexible premiums and benefits.

Flexible—premiums can vary

Mortality charge or term insurance, cash value or savings, administrative expenses.

May not end up with the anticipated amount of savings.

9-20Copyright © 2010 Pearson Education, Inc. Publishing as Prentice Hall

9-21Copyright © 2010 Pearson Education, Inc. Publishing as Prentice Hall

Term Versus Cash-ValueLife Insurance

For most individuals, term insurance is the better alternative:low costhigh cash-value premiums can lead to less

coverage than you actually need

Cash-value insurance has tax advantages.Growth of the cash-value is tax-deferred.Life insurance is not considered part of

your estate.

9-22Copyright © 2010 Pearson Education, Inc. Publishing as Prentice Hall

Fine-Tuning Your Policy:Contract Clauses, Riders, and

Settlement OptionsContract Clauses:Beneficiary ProvisionCoverage Grace PeriodLoan ClauseNonforfeiture ClausePolicy Reinstatement ClauseChange of Policy ClauseSuicide ClausePayment Premium ClauseIncontestabilty Clause

9-23Copyright © 2010 Pearson Education, Inc. Publishing as Prentice Hall

Fine-Tuning Your Policy:Contract Clauses, Riders, and

Settlement OptionsRiders:Waiver of Premium for Disability RiderAccidental Death Benefit Rider or Multiple

IndemnityGuaranteed Insurability RiderCost-of-Living Adjustment (COLA) RiderLiving Benefits Rider

9-24Copyright © 2010 Pearson Education, Inc. Publishing as Prentice Hall

Fine-Tuning Your Policy:Contract Clauses, Riders, and

Settlement OptionsSettlement or Payout Options:Lump-Sum SettlementInterest-Only SettlementInstallment-Payments SettlementLife Annuity SettlementStraight Life AnnuityPeriod Certain AnnuityRefund AnnuityJoint Life and Survivorship Annuity

9-25Copyright © 2010 Pearson Education, Inc. Publishing as Prentice Hall

Buying Life Insurance

Choose an efficiently run life insurance company that will be around when your policy matures.

Selecting an AgentMost agents make living through

commissions

9-26Copyright © 2010 Pearson Education, Inc. Publishing as Prentice Hall

Buying Life Insurance

Choose an efficiently run life insurance company that will be around when your policy matures.

Selecting an AgentMost agents make living through commissionsBe aware of agent’s professional designationList of prospects from good companiesInterview the agents and get a quote

9-27Copyright © 2010 Pearson Education, Inc. Publishing as Prentice Hall

9-28Copyright © 2010 Pearson Education, Inc. Publishing as Prentice Hall

Buying Life Insurance

Comparing CostsTraditional Net Cost (TNC) method—sums up

premiums over a stated period (usually 10 to 20 years) and subtracts from this the sum of all dividends over that same period.

Interest-Adjusted Net Cost (IANC) method—incorporates the time value of money

9-29Copyright © 2010 Pearson Education, Inc. Publishing as Prentice Hall

Buying Life Insurance

Making a Purchase: The Net or an AdvisorShop for term life insurance on the Web

Check at least 2 Web quote services and call an independent insurance agent

More complicated to compare cash-value policies—different features and assumptions

Still get quotes on the Web for different cash-value policies

9-30Copyright © 2010 Pearson Education, Inc. Publishing as Prentice Hall

Health InsuranceEmployer-sponsored health care coverage

Your choices limited to what employer offers

Additional coverage, make additional payments

Pick insurance with only types of coverage you need.

9-31Copyright © 2010 Pearson Education, Inc. Publishing as Prentice Hall

Basic Health Insurance

Most health insurance—combination of hospital, surgical, and physician expense insurance

Hospital insuranceSurgical insurancePhysician expense insuranceMajor medical expense insurance

9-32Copyright © 2010 Pearson Education, Inc. Publishing as Prentice Hall

Health Insurance

Dental and Eye Insurance—coverage for minor and regular dental, eye examinations, glasses, and contact lenses

Dread Disease and Accident Insurance—additional coverage for specific disease like cancer insurance or accident

Provide protection against major catastrophes—make policy comprehensive

9-33Copyright © 2010 Pearson Education, Inc. Publishing as Prentice Hall

Basic Health Care Choices

Traditional fee-for-service – reimbursed for medical expenditures and choice of doctor.

Managed health care – most expenses covered but limited choice of doctors, hospitals, and clinics.

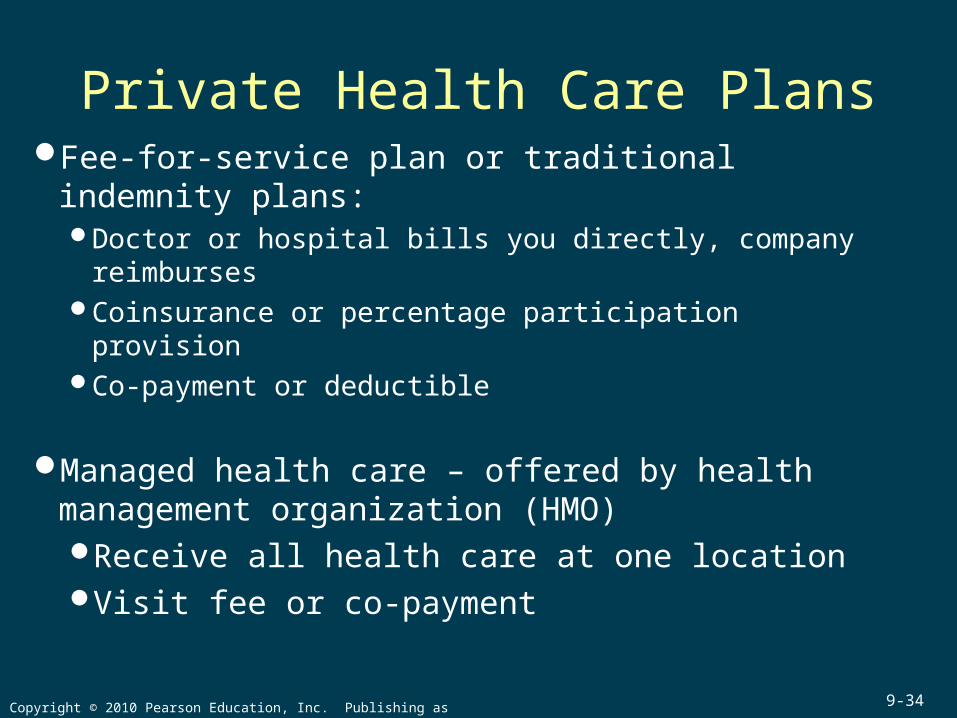

9-34Copyright © 2010 Pearson Education, Inc. Publishing as Prentice Hall

Private Health Care PlansFee-for-service plan or traditional indemnity

plans:Doctor or hospital bills you directly, company

reimbursesCoinsurance or percentage participation provisionCo-payment or deductible

Managed health care – offered by health management organization (HMO)Receive all health care at one locationVisit fee or co-payment

9-35Copyright © 2010 Pearson Education, Inc. Publishing as Prentice Hall

9-36Copyright © 2010 Pearson Education, Inc. Publishing as Prentice Hall

Private Health Care Plans

Managed Health Care: HMOsIndividual practice association plan (IPA)Group practice planPoint-of-service plan

HMOs are cost efficient

Service can be too quick, waits long

Lack of choice can be too restricting

9-37Copyright © 2010 Pearson Education, Inc. Publishing as Prentice Hall

9-38Copyright © 2010 Pearson Education, Inc. Publishing as Prentice Hall

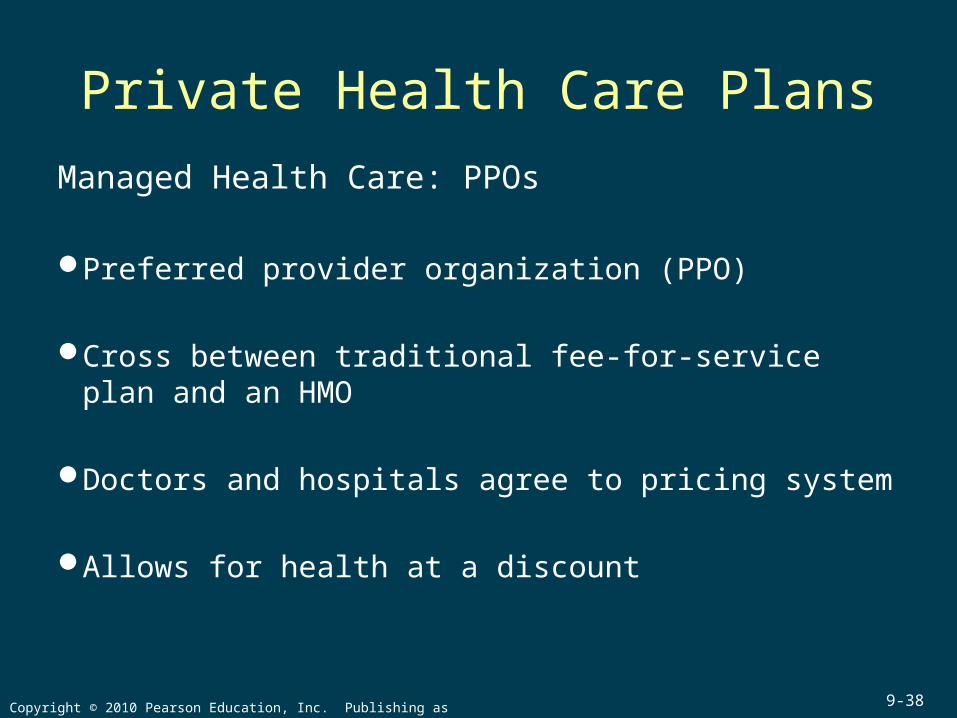

Private Health Care Plans

Managed Health Care: PPOs

Preferred provider organization (PPO)

Cross between traditional fee-for-service plan and an HMO

Doctors and hospitals agree to pricing system

Allows for health at a discount

9-39Copyright © 2010 Pearson Education, Inc. Publishing as Prentice Hall

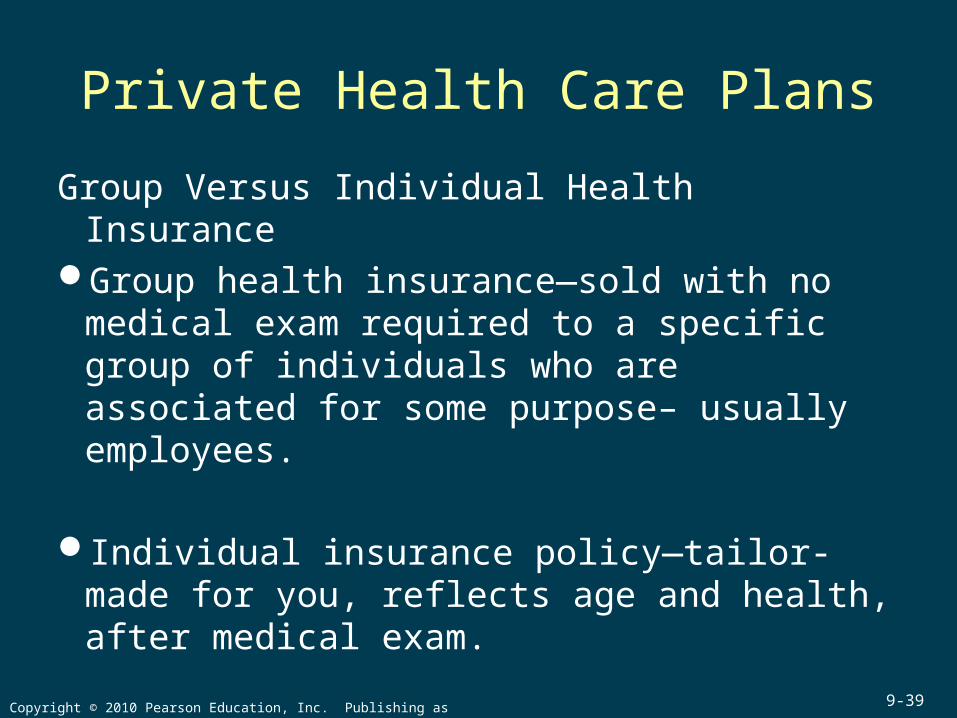

Private Health Care Plans

Group Versus Individual Health Insurance Group health insurance—sold with no

medical exam required to a specific group of individuals who are associated for some purpose– usually employees.

Individual insurance policy—tailor-made for you, reflects age and health, after medical exam.

9-40Copyright © 2010 Pearson Education, Inc. Publishing as Prentice Hall

Government-SponsoredHealth Care Plans

State Plans—provide for work-related accidents and illness

Worker’s Compensation

Federal Plans—Medicare, Medicaid

9-41Copyright © 2010 Pearson Education, Inc. Publishing as Prentice Hall

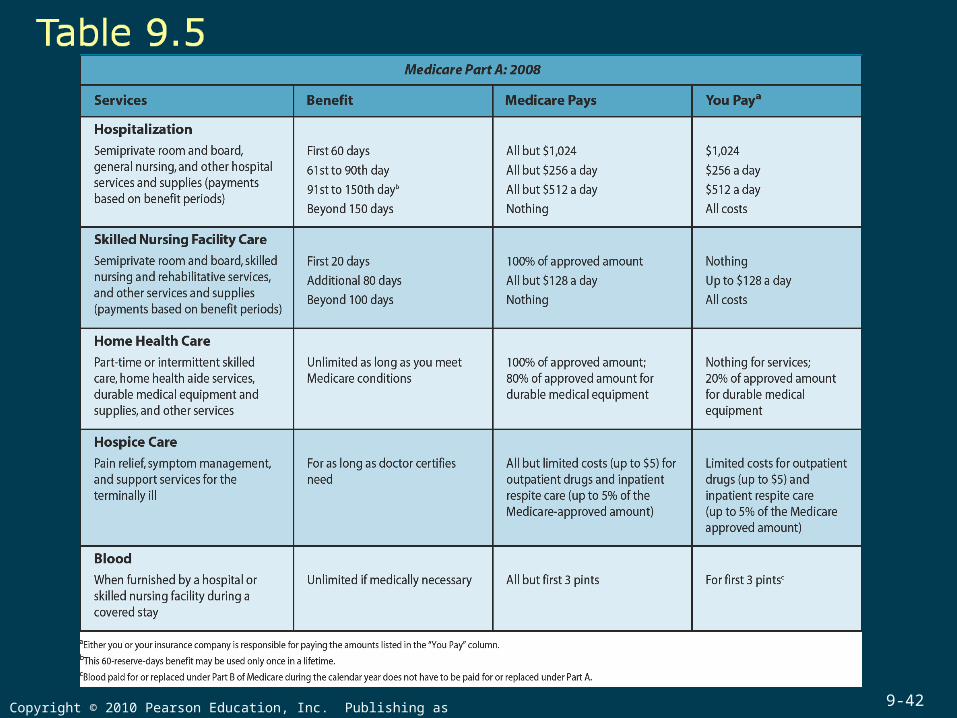

MedicareMedicare Part A—Hospital Insurance

Medicare Part B—Supplemental Medical Insurance

Medicare Part C—Medicare Advantage Plans

Medicare Part D—Medicare Prescription Drug Coverage

Medigap Plans

9-42Copyright © 2010 Pearson Education, Inc. Publishing as Prentice Hall

9-43Copyright © 2010 Pearson Education, Inc. Publishing as Prentice Hall

Medicaid

Government medical insurance plan for needy families—as well as aged, blind, and disabled.

Joint federal and state program

Some covered by Medicaid also covered by Medicare.

Limited in scope

9-44Copyright © 2010 Pearson Education, Inc. Publishing as Prentice Hall

Controlling Health Care Costs

Flexible Spending Accounts

Health Savings Accounts (HSAs)

COBRA and Changing Jobs

Choosing No Coverage—or “Opting Out”

9-45Copyright © 2010 Pearson Education, Inc. Publishing as Prentice Hall

9-46Copyright © 2010 Pearson Education, Inc. Publishing as Prentice Hall

Finding the Perfect Plan

Important Provisions in Health Insurance Policies:

Who’s Covered? Terms of PaymentPreexisting conditions Guaranteed Renewability ExclusionsEmotional and Mental Disorders

9-47Copyright © 2010 Pearson Education, Inc. Publishing as Prentice Hall

Disability Insurance

Health insurance that provides payments to the insured in the even that income is interrupted by illness, sickness, or accident

Sources of Disability Insurance

How much disability coverage should you have?

9-48Copyright © 2010 Pearson Education, Inc. Publishing as Prentice Hall

Disability Features ThatMake Sense

Definition of Disability

Residual or Partial Payments

Benefit Duration

Waiting Period

Waiver of Premium

Noncancelable

Rehabilitation Coverage

9-49Copyright © 2010 Pearson Education, Inc. Publishing as Prentice Hall

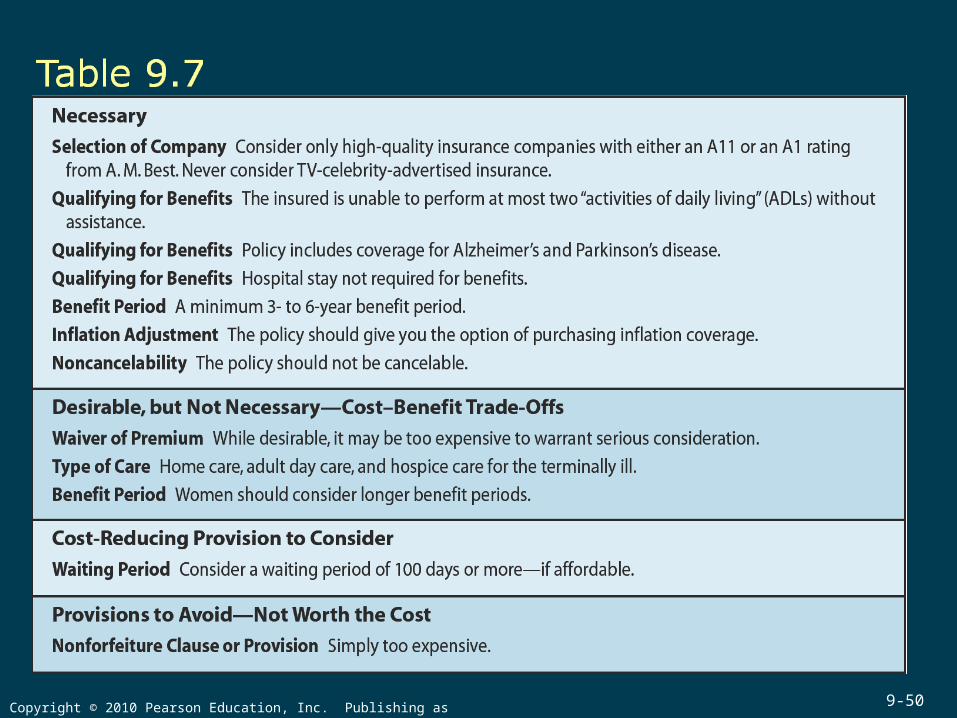

Long-Term Care Insurance

Pays nursing home expenses and home health care.

Covers costs associated with long-term care for thoseagainst the financial costs of Alzheimer’s, strokes, or chronic diseases.

Requires that insured cannot perform “activities of daily living” (ADLs)

9-50Copyright © 2010 Pearson Education, Inc. Publishing as Prentice Hall

9-51Copyright © 2010 Pearson Education, Inc. Publishing as Prentice Hall

Long-Term Care InsuranceType of Care – nursing home, adult day care,

or hospice care for terminally ill.

Benefit Period - can range from 1 year to lifetime.

Waiting Period – 0 days – 1 year.

Inflation Adjustment – protected from inflation.

Waiver of Premium – insurance stays in force while receiving benefits.

9-52Copyright © 2010 Pearson Education, Inc. Publishing as Prentice Hall

Summary

Life insurance controls the financial effect on your family when you die.

There are two types of life insurance—term and cash-value.

Basic health insurance provides combination of hospital, surgical, and physician expense insurance.

9-53Copyright © 2010 Pearson Education, Inc. Publishing as Prentice Hall

Summary

Major medical expense insurance covers medical costs not covered by basic health insurance.

Disability insurance provides income in the event of a disability.

Long-term care insurance covers the cost of long-term nursing home care

9-54Copyright © 2010 Pearson Education, Inc. Publishing as Prentice Hall

All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, in any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of the publisher. Printed in the United States of America.