Lieh ming luo

16

Click here to load reader

-

Upload

teguh-hadi-santoso -

Category

Economy & Finance

-

view

106 -

download

1

description

Transcript of Lieh ming luo

Valuation of money-backguarantees for retail goods: a testof the real-option perspective

Lieh-Ming LuoDepartment of Finance and International Business,Fu Jen Catholic University, New Taipei City, Taiwan

Abstract

Purpose – The paper aims to develop an alternative valuation model for money-back guarantees(MBG) using a real-option approach and examine the validity of the proposed model with anexperimental design. This study attempts to address how retailers appropriately price MBG from aconsumer value-based viewpoint.

Design/methodology/approach – The study defines the perceived post-purchase product value asa stochastic underlying process, and then MBG option value could be theoretically determined by thereal-option pricing approach. For the test of the real-option perspective on MBG, a 2 £ 2 £ 2 factorialexperimental design is conducted to examine the empirical effects.

Findings – With model specification, the study investigated the effects of three key factors, i.e. pricelevel, perceived risk level, and consumers’ risk-aversion, which are characterized by a two-sided effecton MBG option value. The relationships among those factors also are clarified through theoreticalanalyses. The empirical results could be explained well by the proposed model.

Originality/value – Faced with increasingly competitive market, retailers typically need moresophisticated pricing strategies. The study can offer retailers a more comprehensive understanding ofconsumers’ perceived value of MBG in various situations and thereby suggest some managementimplications for the MBG pricing issue.

Keywords Management, Risk management, Mathematical modelling, Money-back guarantees,Real-option approach, Retail goods, Stochastic process

Paper type Research paper

1. IntroductionRetailing industries used money-back guarantee offers as a mechanism to reduceconsumers’ perceived risk in buying the products, thereby increasing the product’s valuein consumer’s perception. Most retailers apply a unified and non-differential MBG policyfor all product items in the store. However, the added value that MBG can create forconsumers could depend on product characteristics and consumer preference. Especiallywhen faced with intensive price competition, firms need to clarify the MBG value of aproduct in order to price it adequately. Thus, it is important that retailers know how toset the MBG optimally to fulfill consumers’ expectations while making a fair profit. Thisstudy attempts to propose an alternative valuation model for MBG using a real-optionapproach, and to investigate the effects of key factors on the MBG value based on thatmodel. From a real-option perspective, we provide a different insight into the

The current issue and full text archive of this journal is available at

www.emeraldinsight.com/0368-492X.htm

This study was supported by the National Science Council under project grant NSC97-2410-H-030-050-MY2. The author would like to thank the National Science Council for theirfinancial support.

Received 24 March 2013Revised 24 March 2013

Accepted 6 June 2013

KybernetesVol. 42 No. 5, 2013

pp. 815-830q Emerald Group Publishing Limited

0368-492XDOI 10.1108/K-03-2013-0054

Valuationof MBG forretail goods

815

consumer-perceived value of MBG and clarify the relations among the influencingfactors. This work offers some management implications for retailers pricing policies forMBG, and guides them to improve product-pricing decisions.

Consumers in general are concerned about whether the received value of a productafter purchase meets the value expected before purchase. They face the risk that whatthey pay for a product exceeds its expected value. Typically, this risk is related touncertainties about product performance, durability, and fit (Roselius, 1971; Heiman et al.,2001a, b). Even though consumers can evaluate a product before purchase based onexternal cues, such as brand, store name and price, their evaluation can be onlyapproximate. To reduce consumer-perceived risk, retailers can offer MBGs. MBG is apost-sale learning mechanism that enables consumers to experience the product, butwith the option to return it if they are unsatisfied. Thus, retailers can enhance consumers’purchase intentions by providing MBG. In fact, the great majority of leading retailers inthe USA have been offering full MBGs (McWilliams and Gerstner, 2006).

MBG are a put option by buyers because MBGs lets buyers sell a product backto retailers at a predetermined price. Heiman et al. (2002) use the option pricing theory(OPT) to build a framework for retailers to optimize the price of MBG under variousmarket conditions. They show that binding an MBG with a product could beprofitable when customers have a low variance in their valuation of a product but varygreatly in the likelihood of product fit. In contrast to their seminal study, this work triesto adopt a pure real-option approach to valuing MBG and to offer a different insightinto MBG practice. Typical real-option approaches assume that an underlying assetof options follows a specific stochastic process, and then determine possible payoffsat each time if the options are exercised. For example, a gold-mining project cancontain several types of real options, such as abandonment, deferment and expandingoptions. To evaluate that project, the real-option pricing methods can treat themarket price of gold as the underlying asset and assume it follows a specific stochasticprocess.

Similarly, we can treat the product value after purchase as an underlying variableand model it as a specific stochastic process. The reason is that various factors caninfluence product valuation by consumers, and hence the product value after purchasecan change over time. Unlike previous research (Heiman et al., 2002), this researchapplies the concept of a stochastic underlying process from conventional real optiontechniques to fully describe the uncertainties associated with product valuation byconsumers. By building an alternative valuation model for MBG from a purereal-option perspective, this research theoretically investigates how a retailer can makeprice for MBG optimally under various conditions, and how model parameters affectthe MBG value. The research also uses a factorial experimental design to examine theempirical effects of the model parameters. The outcomes of the empirical study areconsistent with the model prediction. The results can serve as a reference to helpmanagers to more accurately evaluate consumers’ benefits from MBGs and thereby toimprove their pricing practice.

Many studies relating to MBG are being done in the marketing field. Researchershave shown that MBG is valuable to consumers because it can reduce the purchaserisk, especially when they seek for a good quality product (McWilliams and Gerstner,2006; Mann and Wissink, 1988, 1990; Heiman et al., 2001a, b). Thus, consumers arewilling to pay a higher price for the product accompanied by MBG (Fruchter and

K42,5

816

Gerstner, 1999; de Groot et al., 2009). The study by Davis et al. (1995) indicates thatwhen there is fit uncertainty, offering an MBG can help increase profit if the seller cansalvage a returned product better than the buyer can. In addition, many researcherssuggest that MBG can have a greater impact on risk reduction than either brand name orprice reduction (Hawes and Lumpkin, 1986; Roselius, 1971; Akaah and Korgaonkar,1988; d’Astous and Guevremont, 2008). In particular, MBG can play an important role ininsuring the consumer against losses in the event that product quality is below anacceptable level in selling channels, such as the internet and catalog sales, whereconsumers cannot experience products before purchase (Van den Poel and Leunis, 1999).

However, some aspects of MBG can be a disadvantage for retailers. For example,retailers may incur an additional risk when offering MBG because some customersmight buy products with the intention of freely using them before asking for a refund.But retailers can discourage such “free renting” by imposing hassle costs on customerswho return used products (Davis et al., 1995), or by offering only partial refunds andtaking the non-refundable portion as rent for using the product (Chu and Chu, 1994;Mann and Wissink, 1990). The present work concentrates in particular on quantitativelydeveloping a consumer value-based model for MBG with financial tools, and empiricallytesting the proposed model by a factorial experimental design. This approach provides atechnical foundation for the valuation of real options embedded in general products suchas product exchange guarantees, leasing and warranties.

The remainder of the paper flows as follows. Section 2 develops a theoreticalvaluation framework for MBG that treats the post-purchase product value perceivedby consumers as a stochastic process, allowing an accurate valuation of the MBG putoption using conventional option pricing techniques. Section 3 then provides theapplications of our theoretical model in marketing pricing practices for differentscenarios. Section 4 is devoted to empirically testing the model by means of a factorialexperimental design. The conclusion follows.

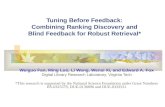

2. The valuation framework for MBG2.1 Defining the underlying variable of the MBG optionConsumers are uncertain whether the product can fulfill their expectation or fully fittheir need before buying the product. Even after they have bought the product, theycannot be sure how much it is worth; they may keep evaluating the product. Manyfactors can influence consumer valuation of the product after purchase, for example,changes in fashion or a friend’s comments on the product. Or product valuation mayvary due to features of the product itself such as durability or performance. Consumersmay obtain additional value from the product because they find that the product hasadditional functions; or they may lower the valuation because of some unexpectedinconvenience in using it. Consequently, consumer-perceived product value may movedownward or upward at any time point during the use, and consumers cannot knowthe exact product value until the end of its use.

Given the uncertainties in consumer-perceived value, we can assume that thepost-purchase product value follows a stochastic process. Suppose that the useduration of the product is T (years). To describe the stochastic process, we divide thehorizon of product use-duration into N periods of equal length, where each period isT/N, denoted by Dt. The value of the product at the end of the tth period is denoted byvt, which is a random variable. For simplicity, we model the valuation process as

Valuationof MBG forretail goods

817

a binomial lattice model that is typically used to describe the stochasticity of financialassets or real assets in the financial economics field.

For a fixed volatility coefficient s, this process is accompanied by an upwardmultiple, u ¼ exp(sD0.5), and a downward multiple, d ¼ 1/u, as a typical setting. Thus,vt will become either uvt (for up) or dvt (for down) in the next period, for t ¼ 0, 1, 2, . . . ,N 2 1. The binomial lattice is shown in Figure 1. We assume that the probability of anupward movement from any node is pR and the probability of a downward movementis 1 2 pR. Therefore, the probability measures for all possible paths,{vt;j ¼ v0u

t2jd jj1 # t # N ; 0 # j # t}, can be defined by the sequence, P ¼ {Pt;jj1 #t # N ; 0 # j # t} with:

Pt; j ¼t

j

!pt2jR ð1 2 pRÞ

j:

2.2 Consumers’ perceived value of MBG optionApplying the stochastic process as described above, the expected consumer-perceivedvalue of a product can be calculated. If consumers are risk-neutral, theconsumer-expected benefit (henceforth CEB) can be obtained simply by CEB ¼E P ½vN �: However, CEB can be generally affected by buyers attitude toward risk. Forthe same product, CEB will decrease with the degree of consumers’ risk-reversion, andtherefore consumers’ risk preference should be taken into account when evaluating theproduct’s expected benefit. The level of consumer-perceived risk can be measured bythe volatility coefficient (s) of the stochastic valuation process.

Hence the volatility coefficient (s) can represent the overall level of product risk. Forexample, a newly introduced product or a product with applications of a new technologywould have a larger volatility coefficient because consumers will be more uncertainabout how much utility those products offer. For a certain risk level of a specific product(i.e. s is fixed), a consumer with greater risk-aversion would perceive less value from theproduct. So the product valuation needs to be adjusted to consumers’ risk attitude. Usingthe value function in a dynamic decision problem (Bellman, 1957), we set value functionV( y, s). Hence CEB ¼ V ðE P ½vN �;sÞ: For simplicity, we set V( y, s) ¼ yD(s). Here D(s)is used to represent the consumers’ attitude toward risk, which is a decreasingfunction of s with the property, dD=ds , 0. Obviously, D(s) , 1 for a general case.

Figure 1.The valuation processof post-purchaseas a binomial lattice

t = 0 t = 1 t = 2 t = 3 t = 4

…

…

…

…

…

V0u4

V0

V0u2

V0u3

V0u2

V0u V0u

V0 V0

V0d2

V0d4

V0d

V0d3

V0d

V0d2

K42,5

818

Therefore, CEB ¼ E P ½vN �DðsÞ is to express the consumer-expected benefit (CEB)incorporating consumers’ risk adjustment. Let s denote the total purchase cost thatincludes the monetary cost, that is, the price (p) and the other transaction costs.So obviously it follows that s . p. Consequently, the consumer-perceived value (CPV),that is, consumer-expected benefit minus total purchase cost, is derived by:

CPV ¼ E P ½vN �DðsÞ2 s: ð1Þ

Now, consider MBG in the valuation model. MBG gives consumers an option to returna product for a refund. The value of such guarantees relates to both the MBG’s durationand the return cost. In practice, the MBG duration can range from 30 to 90 days(Heiman et al., 2002). The return costs can include traveling to the store, waiting in line,and any possible discomfort during the return process. Also, return conditions specifiedby retailers, such as proof of purchase or original packing, may increase return costs.The stricter the requirements imposed by the retailers, the higher the return cost. Returnconditions also can reduce or prevent potential ethical problems that may arise whenconsumers buy an MBG product intending to return it for a refund. For example,retailers can minimize such opportunism by imposing hassle costs, or by offering onlypartial refunds on returns. The added cost to consumers resulting from such conditionsis a part of the total return cost.

Since consumers might think of MBG as a put option value, they may treat the MBGas a contingent claim in the stochastic valuation process described above. Consumerscan exercise this option when their valuation is lower than a determined level withinthe duration of the MBG contract. Assume the MBG duration is Tm (obviouslyTm , T) and it contains Nm (¼ Tm/Dt) sub-periods. In this span, Tm, the consumerscan return the product at the purchase price once they find that the product cannot fittheir need or that its post-purchase value is not sustained at a satisfactory level.

The MBG provision allows consumers an early exercise option that is anAmerican-type put option. However, the MGB provision is a European option for twomain reasons: first, because the European option has a closed-form solution which is notyet the case with the American option, and second, because the values of the two optiontypes do not differ significantly when the contract duration is not long (mostly less than30 days). Since this paper aims to provide a simple model to investigate the MBG optionvalue, using the European option can fulfill this need and thus simplify analyses.

According to the option pricing property, in order to achieve value maximum, a putoption will not be exercised until the end of the MBG duration. Thus, the maximumvalue of the put option can be obtained by fixing the option-exercise time to thedue date of the MBG. It is reasonable to take that maximum value as the addedvalue the consumer can receive from the MBG. If consumers return the product, theycan receive the original sale price ( p) but need to meet the total return cost (c). So thecorresponding exercise price of the option should be p 2 c. Based on OPT, the putoption value of MBG, denoted by POVMBG; can be calculated as:

POVMBG ¼ E Q½maxð p2 c2 vNm; 0Þ� ð2Þ

where Q represents the risk-neutral probability measure (see the Appendix).Theoretically, the put option value of MBG, denoted by POVMBG; is a function ofseveral variables, such as the initial value of the underlying process (v0), exercise price

Valuationof MBG forretail goods

819

( p 2 c), duration of MBG contract (Tm), and volatility coefficient (s). Thus, we expressPOVMBG by a function form as POVMBG ¼ putðv0; p2 c;Tm;sÞ; where v0 ¼ E P ½vN �is the initial valuation of the product before purchase.

OPT estimates the aforementioned put option value of MBG under a risk-neutralworld. However, the consumers’ risk attitude, denoted by D(s), also could affect theconsumers’ perceived value of MBG. In the study of Towse and Garrison (2010), MBGcan be regarded as a risk-sharing mechanism for adopting a new product, and theperception of MBG put option value may depend on the degree of risk aversion. Whileregarding MBG as a hedging mechanism, a highly risk-averse consumer will putgreater value-added on MBG. Thus, for the same product, a consumer with greater riskaversion can perceive a higher value of MBG. Based on this argument, consumers’perceived value of MBG is denoted by VMBG ¼ V ðPOVMBG;DðsÞÞ: For simplicity, weset VMBG ¼ POVMBGFðDÞ: Hence F(D) is a decreasing function of D, i.e. dF=dD , 0. Itfollows that greater risk aversion can produce a greater value of VMBG Consequently,the consumer-perceived value (CPV) of the product with MBG, represented byCPVMBG, may be written as:

CPVMBG ¼ CPV þ VMBG ð3Þ

From the relationship of equation (3), we provide a theoretical evaluation frameworkfor MBG. Through this model, how those relevant factors can influence the MBG putoption value is clarified. In the following section, we investigate the relations amongthe factors in more details from a theoretical economic viewpoint.

3. Applications of the valuation model in MBG pricing3.1 Theoretical analyses for the MBG option valueFrom the real-option perspective, we can evaluate the consumers’ perceived value ofMBG adequately with the proposed model. In order to analyze the effects of some keyparameters of the model on the MBG’s value in various situations, the three scenariosare presented below to express the applications of the theoretical model to retailerspricing practices.

Scenario 1: risk-level effect. According to the valuation model of MBG described inthe previous section, we use the risk-adjustment factor (D) to represent consumers’ riskattitude toward the focus product, and risk level (s) to represent the risk characteristicof the product. Clearly the value of D will decrease with risk level (s). Hence therisk level can have a negative impact on the value of CPVMBG. On the other hand, therisk level may have a positive impact on CPVMBG since the put option value ofMBG will increase with s. Thus, the volatility coefficient (s) can have two effects onthe consumers’ perceived value of the product: one negative stemming from therisk-aversion property, and one positive, that is, the option value-creation effect. If theconsumers’ risk attitude is given (i.e. the function form of risk-adjustment factor D isgiven) and all else is equal, CPVMBG can vary with risk level (s). The relationshipbetween CPVMBG and s is shown in Figure 2. This relationship will depend on thevalues of both D and p since CPV can be sensitive to D and the MBG option value canbe sensitive to p. It can be expected that the value creation from MBG will be offset inlarge part by the negative effect of perceived risk if the risk level is relatively high. Thefact implies that an optimal level of product-risk level (s) can have the greatestvalue-creation effect when the product carries MBG. The above analyses indicate that

K42,5

820

the risk characteristic of a specific product category should be regarded as a significantfactor in retailer’s pricing strategies about MBG products.

Scenario 2: price-level effect. When making decisions about appropriate pricing of afocus product, retailers need to determine beforehand how much value they want tooffer to the customers. In the following scenario, a retailer would like to implement avalue-offering policy for a product to a certain market segment. Suppose that theretailer can classify the market segments using different consumers’ attitudes towardrisk. Thus, a certain group of consumers can be characterized with the risk-adjustmentfactor, D. To provide a certain perceived-value, denoted by CPV*, how can the retailerfairly price the product for the target market segment? The retailer needs to know therelationship between product price and CPVMBG for the target segment. Assume that Dof the target market segment and s of the product are known. Without considering theMBG put value, CPV would decrease with the price level ( p) because p is the directmonetary cost. However, when incorporating MBG, the MBG option value wouldincrease with p because a higher exercise price ( p 2 c) can generate a greater putoption value based on the option properties. Consequently, the price level can also havetwo kinds of effect on consumers’ perceived product value: the monetary cost effect andthe option value-creation effect. Figure 3 shows the relationship between CPVMBG

and p. It is seen that different price levels can provide different levels of CPVMBG whenthe product is accompanied by BMG. Accordingly, when a retailer seeks to provide aproduct to market segment at a predetermined level of perceived value, the pricingpolicy for MBG must take account of the effect of price level.

Figure 2.Consumer-perceived value(CPV), MBG option value(VMBG) and risk levels (s)

Value

Risk level (σ)

VMBG

Low High

CPV

CPVMBG

Figure 3.Consumer-perceived value(CPV), MBG option value(VMBG) and price level ( p)

Value

Price level (p)

VMBG

Low High CPV

CPVMBG

Valuationof MBG forretail goods

821

Scenario 3: risk-aversion effect. According to equation (3), the consumers’ risk attitudealso can play an important role in determining consumers’ perceived product valuewhen MBG is incorporated. Consumers with greater risk aversion will typicallyperceive a lower value for a certain product than those with less risk aversion.But when MBG is tied to the product, the high degree of risk aversion can augment theperceived value of MBG option as shown in equation (3). Consequently, consumers’attitude toward risk also has a dual effect on the consumers’ perceived value of theproduct with MBG: a negative effect which can decrease CPV, and a positive effectwhich can increase the perceived value of the MBG option. Here consider a scenario inwhich a retailer is implementing a market-penetration pricing strategy in a new targetmarket, to express the effects of consumers’ risk attitude. Retailers typically use pricereduction as a tool to attract more customers and stimulate sales growth. Consumers atthe introductory stage of the product life cycle generally are less risk-averse to the newproduct than the later adopters. When the new product enters the growth stage,manufactures can use the price-cutting policy to increase revenues and therebycapitalize on economics of scale.

Suppose that there exist two market segments with different consumers’ attitudestoward risk (D(s)), that is, high and low degrees of risk-aversion. For the same product,the customers with higher risk aversion would typically demand a lower price tocompensate for their greater perceived loss due to uncertainty. Now suppose theexisting market segment is characterized by a lower degree of risk-aversion. Theretailer would like to implement a price-reduction strategy to attract another segment,one that is more risk-averse. Assume that the retailer imposes a fixed value-offeringpolicy for an item to offer consumers a certain perceived value, denoted by CPV* asbefore. Manager should use care in setting the value-offering level (CPV*), since it canbe transformed into consumers’ purchase intentions.

To receive a given perceived value, CPV *, different customer segments would liketo pay different levels of price for the same product, as shown in Figure 4. If retailersattempt to penetrate into the greater risk-aversion segment using a price-cutting policy,the price should be reduced more while MBG is not yet attached. On the other hand, ifMBG is tied to the product, retailers must reduce price by less. That is the positiveeffect of consumer risk aversion on MBG option value, which can offset its negativeeffect on the consumers’ perceived value (Figure 4).

Figure 4.Consumer-perceived value(CPV), MBG option value(VMBG) and risk-aversiondegree (D)

Value

Risk-Aversion Degree (D)

VMBG

Low HighMarket-Penetration Pricing

CPV

CPVMBG

Price Reduction

K42,5

822

3.2 Theoretical implicationsFollowing the theoretical analyses aforementioned, this subsection is devoted todiscussing management implications for MBG option value. First, the risk level (s) canplay an important role in determining the MBG option value. There are many sourcesof uncertainty about post-purchase product value, including technology development,consumers’ taste, and product performance, among others. As with the market price ofstocks, there are many influencing factors, such as interest rate, oil price or governmenteconomic policy. Thus, as with the expression of the uncertainty about stock price, weuse the volatility parameter (s) to universally describe the risk level of a product.A high volatility parameter (s) may cause a decrease in product value due toconsumers’ risk aversion, but may imply the greater potential benefits embedded in theproduct. That is, in market equilibrium, an asset with high risk generally isaccompanied by high return. Consumers can pay an additional price margin for MBGand use MBG to capture the potential benefits. From this viewpoint, in some cases,MBG can offer significant added value to consumers, but in some cases, it cannot. Forexample, when the risk level is extremely high, the MBG option value would be eatenaway by the negative effect of a risk-averse attitude. On the other hand, when the risklevel is extremely low, the MBG option value would be rendered valueless. So retailersneed to assess carefully both the positive and negative effects of risk level (s) whenspecifying product pricing policy for MBG.

Consumers typically regard the sale price (p) as a direct monetary cost. A higher pricemeans that consumers face a higher potential loss and hence have a larger risk exposure.For example, buying a house would involve higher risk than buying a car. Thus, a higherprice can partially decrease consumers’ perceived value due to the greater monetary costand higher risk. However, from the option-value viewpoint, the MBG option valuecan increase with price level (p). Particularly if price level is extremely high relative toreturn cost, MBG could create much higher value for consumers. For example, forfamous-brand clothes that have a high price but also have high taste-fitness risk, MBGcould be very valuable to consumers because of the very low return cost (where travelingcost is not high). On the other hand, if the price is very low, MBG would becomevalueless, because the return cost (c) could eat up a large portion of the return benefit(the sale price). Especially when the return requirement is very strict and traveling cost(including time cost) is high, the MBG option value would be largely offset by the returnefforts. For various price levels and transaction conditions, the MBG option value cancontribute differentially to the consumers’ perceived value.

Since MBG can mitigate consumers’ perceived risk, consumers’ attitude toward riskis an important factor in discussing the MBG option value. Hence managers canclassify consumers according to risk aversion degree (D) when considering effect ofconsumers’ risk attitude. Great risk aversion means that risk level can have a morenegative impact on the consumer’s perceived value; consumers with a high degree ofrisk aversion worry more about the potential loss in value. Because MBG can eliminatevalue-loss risk exposure, MBG generally is more valuable to highly risk-averseconsumers. For various market segments classified by risk attitudes, MBG can havedifferent value-creation effects. We have presented an example about pricing policy forvarious segments, as shown in Figure 4. As is well known, price cutting probably canstimulate sales growth, but it may erode profit. For retailers, one advantage of MBG isto prevent excessive erosion of profit when they implement a market-penetration

Valuationof MBG forretail goods

823

pricing strategy for expanding their target market. Managers can take this analyticframework as a guild for determining the optimal price-reduction margin for such apricing strategy. Thus, the pricing policies for MBG may be different in different marketsegments. In an extreme case, a consumer group with risk-loving characteristics willnot appreciate the value-creation effect of MBG (in this case, D is very high and hencea is very low). On the other hand, MBG option value also would be offset greatly ifconsumers are very highly risk averse. Through our model, retailers can clarify therelationship among those key factors of the MBG option value and hence can fairly priceMBG. In the following section, we try to examine how the MBG option value can relatethose key factors empirically through an experimental design.

4. Experimental test for MBG option value4.1 Experimental design and data collectionThis section describes empirical testing of the theoretical model proposed in this studyby means of a 2 £ 2 £ 2 factorial experimental design. 198 undergraduate businessstudents at Chaoyang University of Technology in Taiwan participated in theexperiments to earn extra course credits. The key variables considered in theexperiments are product-price level, product-risk level and consumers’ risk-aversionlevel, as discussed in the previous section. The stimuli for the first two variables weretreated in a booklet that contains an introduction, description of a scenario, and surveyquestions. The key information in this scenario was manipulated to control forproduct-price level (high price vs low price) and product-risk level (high perceived riskvs low perceived risk). As for the third variable, consumers’ risk attitude toward thefocus product, subjects were asked a series of questions to determine the degree ofconsumers’ risk-aversion. The details of manipulating the risk-averseness measure aregiven in the next subsection.

In order to choose appropriate product stimuli, the study conducted a preliminarytest with 16 students. We choose ten considered product items and asked the studentsto assess the perceived risk levels of those ten items. We set prices within a appropriaterange for all the product items so as to ensure that the prices are affordable to mostcollege students. According to the results of the preliminary test, we select twoproducts with a significant difference of perceived risk level. One is a desk lamp, theproxy for low risk level products, and the other is a new style cell phone, the proxy forhigh risk level products. The well-known brands were used for the selected products(Philips and Nokia, respectively) to avoid a situation in which subjects evaluate theproducts as being poor because they have never heard of the brand.

The procedure first shuttled the booklets with the four controlled conditions (twoprice levels, $50 vs $65, and two risk levels, desk lamp vs cell phone), and thenrandomly distributed them to subjects in four groups of approximately 50 each. Allbooklets looked exactly the same so that subjects were unaware of the manipulation ofinformation in the scenario. Subjects were told that the study would investigate howconsumers evaluate and respond to the MBG provision. They were asked to read thescenario assuming that they had just decided to purchase the assigned product from anunnamed chain store. They were informed that the sale price was determined bycurrent market prices and thus would be fair. After reading a brief description ofproduct features, subjects were to evaluate the MBG provision and indicate theirvaluation of MBG. The experiment lasted about 15 minutes.

K42,5

824

4.2 MeasuresThe questionnaire was composed of three parts. The experimental stimuli appeared inthe first part. They were presented in the form of high-quality color photographs with ashort text stating the product category, the brand name, the MBG provision, and theperiod of time within which the product could be returned after purchase. No measureswere used to check manipulations since they were clearly controlled in various scenariosas mentioned in the previous subsection. In the second part of the questionnaire, threekey dependent measures immediately followed the stimuli and included purchaseintention, change of purchase intention from MBG offers to no-MBG offers, andperceived value of MBG. Note that the first dependent measure indicates consumers’whole evaluation of the product and the second represents the difference in productvaluation with MBG and without MBG. They mainly constitute the second part ofthe questionnaire. Subjects were asked to indicate their purchase intention to theproduct shown in the booklet if they need such the product, using a seven-point Likertscale (1 – being trivial and 7 – significant). We can assume that consumers’ overallevaluation of a product will be reflected in their purchase intention. We also used aseven-point Likert scale to measure how subjects’ purchase intention can change ifthe MBG provision was removed. Lastly, the subjects were asked to indicate what extentthe price should be reduced so that the original purchase intention can be sustained if theMBG provision was removed. We listed various amounts of price reductions rangingfrom $0 to $20 to allow the subjects to choose from. It is reasonable to assume that theamount of the price reduction would be equal to the consumers’ perceived value of MBG.In order to check that all conditions specified in the experiment appeared equally realisticto subjects, subjects additionally were asked to indicate whether the MBG provisionlooked common or unusual (1 – being common and 7 – unusual). The third and finalpart of the questionnaire contained typical questions on the risk-aversion measure,which is adopted from Burton et al. (1998). Using the results of risk aversionmeasurement, the subjects were ranked and then classified by degree of risk aversion.We took the top 40 percent as a consumer group of relatively great risk aversion, whilethe bottom 40 percent is regarded as having relatively low risk aversion. The analysesused a dummy variable, “1”, to represent a high degree of risk-aversion and a “0” torepresent a low degree. In order to dearly distinguish the two groups by risk attitude, theremaining 20 percent, the middle part (39 subjects), was neglected. Consequently, only159 subjects are incorporated for further analysis.

4.3 Results and discussionTable I presents the means and standard deviations of all measures by treatmentconditions. Subjects indicated that these MBG offers were relatively common(mean ¼ 2.87, SD ¼ 1.45). We used a three-way ANOVA to analyze subjects’perception of the MBG value. Table II summarizes the findings for each measure. Thetwo independent variables, price level and risk aversion degree, tend to affect purchaseintention negatively for the product with MBG, but only the effect of price level issignificant; the risk-level effect tended to be positive. As predicted in the theoreticalmodel, those variables can have a two-directional effect on product evaluation whilethe product carries MBG. For example, a high risk level may lower product valuationdue to consumer’s risk aversion, but can be offset by an increase in the MBG put optionvalue. Checking the effects of those variables on the MBG value separately may clarify

Valuationof MBG forretail goods

825

the interactive relations. Table II clearly shows that all the three independent variablestend to have positive effects on the perceived value of MBG, but the effects of risklevel are more significant than either price level or risk-aversion (although both wereclose to significant). The results also are consistent with the model prediction. Thisexperimental study used the change of purchase intention from MBG-offering tono-MBG-offering to measure how the product evaluation is changed if MBG is removedfrom the product. As observed in Table II, the effect of risk level on purchase intentionchanges is significantly positive, but on original purchase intention is not significant.The negative effect of risk level on product evaluation appears to be offset by thevalue-creation effect of risk level on MBG option value. And in this case, thevalue-creation effect is more apparent than the negative effect of risk level, so that neteffect of risk level on product valuation tends to be positive but not significant. Theprice-level effect on product valuation differed from the risk level effect. The studyresult showed that price level has a significantly negative effect on overall productvaluation, but on the other hand, can create added value by enhancing MBG put optionvalue (even if it merely approaches significant level). But in this case, the negativeeffect of price level on product valuation is offset in part by its value-creating effect onMBG option value, and hence the net effect of price level still tends to be negative. Asfor the risk-aversion effect, it is similar to the price effect. The net effect of risk aversionon purchase intention is slightly negative, but its effect on purchase intention change ispositive. In other words, the negative effect of risk aversion on product evaluation was

High risk aversion degree Low risk-aversion degreeHigh price Low price High price Low price

Measures Mean SD Mean SD Mean SD Mean SD

High riskOriginal purchase intention 3.00 0.88 3.20 1.06 2.75 0.97 3.40 0.82Perceived value of MBG 7.58 2.17 7.70 2.54 8.20 1.94 6.10 1.77Change of purchase intention 3.84 1.01 3.90 1.25 4.15 0.99 3.10 0.85Low riskOriginal purchase intention 2.71 0.72 2.95 0.94 2.65 0.81 3.21 0.85Perceived value of MBG 6.00 2.19 6.60 2.06 6.00 1.84 5.05 2.04Change of purchase intention 3.10 1.00 3.30 1.03 3.10 0.97 2.63 1.07

Table I.Cell means and standarddeviations

Dependent variablesOriginal purchase

intentionPerceived value of

MBGChange of purchase

intention

Risk level (high vs low) 0.2051ns 1.4900 * * 0.7206 * *

(0.1443) (0.0000) (0.0000)Price level (high vs low) 20.4112 * 0.5772ns 0.3123 ns

(0.0037) (0.0883) (0.0609)Risk-aversion degree (high vslow)

20.0362ns 0.6273ns 0.2874 ns

(0.7958) (0.0642) (0.0845)

Notes: Significant at: *p , 0.05 and * *p , 0.01; the numbers in parentheses denote p-value; ns – notsignificant

Table II.Summary of significantfindings and effect sizes

K42,5

826

only partly offset by its value-creating effect on MBG value, and thus the net effectremains negative. Except for the aforementioned main effects, we observed nointeraction effects between any two independent variables.

According to the results shown in Table II, the net effect of risk level is significantlypositive. The result implied that the risk level of a product seems to have a greatereffect on the perceived value of MBG because its positive effect can exceed its negativeeffect on product valuation. That phenomenon may be more apparent when theperceived risk level is much higher, for example, in the purchase of an entirely newproduct that consumers have never encountered before. Consistent with modelprediction, MBG can create a greater value for a higher risk product. The results alsoindicate that the price level of a product has a significant but not very strong effect onthe perceived value of MBG. The net effect of price level is greatly affected by the directmonetary cost effect of price level. In this experiment we manipulate different pricelevels for the same product, $50 vs $65 (note that the subjects are informed that the saleprice is fairly determined in terms of current market prices); hence the direct monetarycost effect of price level would reasonably be expected to exceed its value-added effecton MBG option value. Consequently, the negative effect of price level on productvaluation dominates but can be greatly offset by its value-added effect, in part becausewith MBG consumers can return the product for any reason, including dissatisfactionwith the price after purchase. In other words, MBG can mitigate not only therisks about product quality and consumers’ taste match, but also the price risk(the possibility of finding a lower price elsewhere after purchase). So we can reasonablyexpect that the result may be somewhat different if the price level is set higher. Notsurprisingly, consumers will still be more concerned over the monetary cost effect ofprice level than the MBG option value-added effect. However, if the experimentalcondition is set so that the higher price level corresponds to higher product qualitylevel, the value-added effect might be sufficient to offset the cost effect, and the neteffect of price level on product valuation might thus be positive. In addition, the resultsshowed that the effect of risk aversion was relatively less important, perhaps becausemost subjects were rather risk-averse so that the distribution of the risk-aversiondegree of all subjects is not very dispersive. The results thus show that therisk-aversion degree does not generate a significant effect either on overall productvaluation or on MBG put option value. One may wonder whether an interaction effectmight occur between risk level or price level and risk aversion since a highlyrisk-averse consumer may tend to be more concerned about sale price or product risk.But the experimental results show no interaction effects among those variables.Generally speaking, the experimental results fulfill the model prediction. Thus, theresults of the empirical testing indicate that the theoretical model may well explainconsumers’ product valuation and their perception of the MBG value.

5. ConclusionConsumers who are dissatisfied with purchased products can return for a full refund forany reason under MBG. Since MBG is popularly used for mitigating consumers’ riskperception in retailing industries, retailers should clearly understand the value of MBGso as to price it properly. To deal with increasingly competitive market, firms typicallyneed more useful and sophisticated pricing strategies. In the real option approach,consumers can obtain additional put option value if MBG accompanies a product.

Valuationof MBG forretail goods

827

This research has developed an alternative pricing model for MBG with a real-optionapproach from a consumer value-based viewpoint. In particular, the post-purchaseproduct value perceived by consumers is modeled as a stochastic process and MBG isthen treated as a contingent claim underlying the stochastic process. According to theoption pricing property, the model can fairly determine the MBG value, which dependson product’s properties and consumers’ characteristics. In the theoretical model, weconsider three main factors, which are characterized by a two-sided effect on productvaluation: price level, perceived risk level, and consumers’ risk-aversion. This study alsoimplements an experimental design to test the effects of the three factors on consumers’product valuation when the product is accompanied by MBG. The results of the testcoincide generally with the model prediction. These results of the model can helpretailers to understand consumers’ perceived value of MBG in various situations andenable them to make better pricing decisions for MBG.

The limitations of this research include the parameter assumptions regarding thestochastic process of perceived product value. This restriction typically appears in areal-option model for the valuation of a project or a real asset because a real asset(or project) often has more complicated features than financial assets. Anotherrestriction is that because managers typically cannot observe historical data on thevolatility parameter of the underlying value (i.e. risk level), it may not possible toestimate it accurately. Hence applications of this model have to rely on the judgment ofsenior management or on some heuristic approaches to estimate an objective value ofthe volatility parameter.

References

Akaah, I.P. and Korgaonkar, P.K. (1988), “A conjoint investigation of the relative importanceof risk relievers in direct marketing”, Journal of Advertising Research, Vol. 28 No. 4,pp. 38-44.

Bellman, R.E. (1957), Dynamic Programming, Princeton University Press, Princeton, NJ.

Black, F. and Scholes, M. (1973), “The pricing of options and corporate liabilities”, Journal ofPolitical Economy, Vol. 81 No. 3, pp. 637-659.

Burton, S., Lichtenstein, D.R., Netemeyer, R.G. and Garretson, J.A. (1998), “A scale for measuringattitude toward private label products and an examination of its psychological andbehavioral correlates”, Academy of Marketing Science, Vol. 26 No. 4, pp. 293-306.

Chu, W. and Chu, W. (1994), “Signaling quality by selling through a reputable retailer:an example of renting the reputation of another agent”, Marketing Science, Vol. 13 No. 2,pp. 177-189.

Cox, J.C., Ross, S.A. and Rubinstein, M. (1979), “Option pricing: a simplified approach”, Journal ofFinancial Economics, Vol. 7 No. 3, pp. 229-263.

d’Astous, A. and Guevremont, A. (2008), “Effects of retailer post-purchase guarantee policies onconsumer perceptions with the moderating influence of financial risk and productcomplexity”, Journal of Retailing and Consumer Services, Vol. 15 No. 4, pp. 306-314.

Davis, S., Gerstner, E. and Hagerty, M. (1995), “Money back guarantees in retailing: matchingproducts to consumer tastes”, Journal of Retailing, Vol. 71 No. 1, pp. 7-22.

de Groot, I.M., Antonides, G., Read, D. and van Raaij, W.F. (2009), “The effects of directexperience on consumer product evaluation”, The Journal of Socio-Economics, Vol. 38No. 3, pp. 509-518.

K42,5

828

Fruchter, G.E. and Gerstner, E. (1999), “Selling with satisfaction guaranteed”, Journal of ServiceResearch, Vol. 1 No. 4, pp. 313-323.

Hawes, J.M. and Lumpkin, J.R. (1986), “Perceived risk and the selection of a retail patronagemode”, Journal of the Academy of Marketing Science, Vol. 14 No. 4, pp. 37-42.

Heiman, A., McWilliams, B. and Zilberman, D. (2001a), “Demonstrations and money-backguarantees: market mechanisms to reduce uncertainty”, Journal of Business Research,Vol. 54 No. 1, pp. 71-84.

Heiman, A., McWilliams, B. and Zilberman, D. (2001b), “Reducing purchasing risk withdemonstrations and money-back guarantees”, Journal of Marketing Management, Vol. 11No. 1, pp. 58-72.

Heiman, A., McWilliams, B., Jinhua, Z. and Zilberman, D. (2002), “Valuation and management ofmoney-back guarantee options”, Journal of Retailing, Vol. 78 No. 3, pp. 193-205.

McWilliams, B. and Gerstner, E. (2006), “Offering low price guarantees to improve customerretention”, Journal of Retailing, Vol. 82 No. 2, pp. 105-113.

Mann, D.P. and Wissink, J.P. (1988), “Money-back contracts with double moral-hazard”, RandJournal of Economics, Vol. 19 No. 2, pp. 285-292.

Mann, D.P. and Wissink, J.P. (1990), “Money-back warranties vs replacement warranties:a simple comparison”, American Economic Review, Vol. 80 No. 2, pp. 432-436.

Roselius, T. (1971), “Consumer ranking of risk reduction methods”, Journal of Marketing, Vol. 35No. 1, pp. 56-61.

Towse, A. and Garrison, L.P. Jr (2010), “Can’t get no satisfaction? Will pay for performancehelp?”, Pharmacoeconomics, Vol. 28 No. 2, pp. 93-102.

Van den Poel, D. and Leunis, J. (1999), “Consumer acceptance of the internet as a channel ofdistribution”, Journal of Business Research, Vol. 45 No. 3, pp. 249-256.

AppendixAs described in the text, the study adopted a binomial lattice model to describe the stochasticbasis of post-purchase product valuation by consumers. Cox et al. (1979) initially propose such amodel (abbreviated CRR model) to price the financial options using the contingent claimanalyses. We use the binomial option-pricing model in this research for some of the reasonsbelow. First, we try to apply a basic financial valuation tool to the MBG evaluation issue in themarketing field. We hope that the proposed model will be as intuitive as possible so as to be moreaccessible to marketing audiences. Second, as is well known, the discrete binomial model may beviewed as an approximation of the model of Black and Scholes (1973) for its convergingasymptotically properties, so there may be no significant difference in the valuation results fromthe two models. Third, because the MBG term is often rather short (seven to 90 days, usually less30 than days), it would be reasonable to fix the volatility level as constant for this case. For ageneral retail good, which unlike financial assets has no long-term series data, we do not need tocapture the changing volatility effect over a short time. Therefore, the discrete binomial modelseems to be able to sufficiently describe the stochastic properties of a consumer good.

In this model, we take the random variable vt to denote the product value at the end ofthe tth period. The risk-free interest rate, r, is assumed constant. According to the CRR model,there exists a unique risk-neutral probability (or martingale measure), which is conditionalon the information to time t, derived as q ¼ ½ð1 þ rÞD 2 d�=ðu2 d Þ and 1 2 q ¼ ½u2 ð1 þ rÞD�=ðu2 d Þ, for {vtþ1 ¼ uvt} and {vtþ1 ¼ dvt}, respectively. Therefore, the unique risk-neutralprobability measure is defined by the sequence:

Q ¼ {Qt;jj1 # t # N ; 0 # j # t} ðA1Þ

Valuationof MBG forretail goods

829

for all possible paths {vt;j ¼ v0ut2jd jj1 # t # N ; 0 # j # t} with:

Qt;j ¼t

j

!q t2jð1 2 qÞ j:

According to the option property, the fair value of the focus asset in the underlying process,Yf, that has payoffs, ft, at time t for t ¼ 1, 2, . . . , N, may be calculated as:

Yf ¼ E QXNt¼1

ð1 þ rÞ2tDf t

" #ðA2Þ

where E Q is the conditional expectation operator with respect to the risk-neutral probabilitymeasure in equation (A1). In this case, the payoff at the end of MBG duration that a consumerwith the returning option can receive is maxð p2 c2 vNm

; 0Þ. For simplicity, we take the interestrate as zero since our discussion concentrates on consumption goods. This setting will not affectthe generality. Consequently, we can derive the put option value of MBG by E Q½maxð p2 c2vNm

; 0Þ� based on the relationship described in equation (A2).

Corresponding authorLieh-Ming Luo can be contacted at: [email protected]

K42,5

830

To purchase reprints of this article please e-mail: [email protected] visit our web site for further details: www.emeraldinsight.com/reprints