Level 41 242 Exhibition Street The Manager MELBOURNE VIC … · 2013-10-22 · Driving value from...

66

Telstra Corporation Limited ACN 051 775 556 ABN 33 051 775 556 23 October 2013 The Manager Company Announcements Office Australian Securities Exchange 4 th Floor, 20 Bridge Street SYDNEY NSW 2000 Office of the Company Secretary Level 41 242 Exhibition Street MELBOURNE VIC 3000 AUSTRALIA General Enquiries 08 8308 1721 Facsimile 03 9632 3215 ELECTRONIC LODGEMENT Dear Sir or Madam Investor Day – Media Release and Slide Presentations In accordance with the Listing Rules, I attach a copy of a media release and the presentations to be delivered at Telstra’s Investor Day, for release to the market. Yours faithfully Damien Coleman Company Secretary For personal use only

Transcript of Level 41 242 Exhibition Street The Manager MELBOURNE VIC … · 2013-10-22 · Driving value from...

Telstra Corporation Limited ACN 051 775 556

ABN 33 051 775 556

23 October 2013 The Manager Company Announcements Office Australian Securities Exchange 4th Floor, 20 Bridge Street SYDNEY NSW 2000

Office of the Company Secretary Level 41 242 Exhibition Street MELBOURNE VIC 3000 AUSTRALIA General Enquiries 08 8308 1721 Facsimile 03 9632 3215

ELECTRONIC LODGEMENT Dear Sir or Madam Investor Day – Media Release and Slide Presentations In accordance with the Listing Rules, I attach a copy of a media release and the presentations to be delivered at Telstra’s Investor Day, for release to the market. Yours faithfully

Damien Coleman Company Secretary

For

per

sona

l use

onl

y

Follow Telstra online:

exchange.telstra.com | www.facebook.com/telstra | www.twitter.com/telstra | www.youtube.com/telstracorp

MEDIA RELEASE 23 October 2013 TELSTRA REFINES STRATEGY, REALIGNS KEY BUSINESS UNITS Telstra today announced a refined long term strategy supported by business unit changes aligning senior leaders to growth opportunities in Australia and overseas. Telstra CEO David Thodey said the realignment would ensure Telstra focused on the critical areas of customer service excellence, core revenue and growth. Speaking at a Telstra investor day in Sydney, Mr Thodey said Telstra must continue to focus on its core Australian business while exploring new opportunities domestically and internationally, particularly across the Asia region. Telstra’s strategy now has three pillars evolving from the previous four pillars – Improve customer advocacy; Drive value from the core; and Build new growth businesses.

“Our strategy is simpler and more impactful. It makes our ambitions clearer and shows where shareholders can expect us to continue building value,” Mr Thodey said. “We must serve our global customers at international scale, leveraging our expertise into Asia and other regions, while seeking to deliver outstanding customer service every day in every home, street and business around Australia. “This strategy provides greater organisational clarity around our growth portfolios. New businesses such as global applications and platforms, cloud solutions and e-health were not opportunities three years ago and can play important roles as we head towards 2020 and beyond.” The investor day reviewed Telstra’s performance in key growth areas such as Network Applications and Services, mobile network expansion, digital media and global applications and ventures. Full presentation materials are available at http://www.telstra.com.au/abouttelstra/investor/ Telstra strategy refinements Telstra’s three-pillar strategy simplifies the previous strategic framework developed in 2010, reflecting the company’s evolution in its customer-focused journey and identification of new opportunities. Improving customer advocacy reflects progress from customer satisfaction and retention and is a

stand-alone proposition across the company. There are four major sub-pillars: Telstra’s use of the Net Promoter System, product differentiation, process improvement focus and creating a uniquely positive customer service experience.

Driving value from the core concentrates on customer and revenue growth, network superiority and driving productivity through simplifying the business. This pillar has four key focus areas in 2013-14: mobiles, fixed broadband, transitioning Sensis to a digital business and broader productivity improvements through simplification plans.

Building new growth business is centred on network services, Asian expansion, e-health and longer term growth opportunities such as digital media and global applications and platforms. These will change over time while the focus on growth opportunities remains constant.

For

per

sona

l use

onl

y

Follow Telstra online:

Blog exchange.telstra.com | www.facebook.com/telstra | www.twitter.com/telstra_news | www.youtube.com/telstracorp

Telstra’s capital management framework, announced by the company in 2012, remains unchanged. The framework guides management decisions according to a set of criteria and provides transparency for shareholders. Telstra portfolio changes Following Telstra’s new strategic pillars, key portfolio changes in the business include – Global Enterprise and Services: Brendon Riley appointed Group Executive of a new $5 billion

revenue business unit operating as a global scale, industry-based services and solutions business. Riley’s responsibilities will include Network Application Services worldwide, Global Applications and Platforms, a new cloud division, Telstra Ventures, Telstra Enterprise and Government and Defence. The unit reflects rapid growth in key portfolio areas and the global market in which these services are provided.

Telstra Operations: Kate McKenzie appointed Chief Operations Officer, now including the Chief Technology Office and innovation portfolios to better integrate technology development and implementation. The function’s leadership was reorganised in an operational review earlier this year. Telstra Operations will lead Telstra’s ongoing technical excellence across fixed and mobile networks; and

Telstra Retail: Gordon Ballantyne appointed Group Executive bringing together key retail-facing segments including Telstra Consumer and Telstra Business, products, National Broadband Network product, sales and marketing, Telstra Country Wide and the Chief Marketing Office. Ballantyne will also have responsibility for growth through the new e-health division. He will have key aspects of Customer Sales & Service and Innovation, Products & Marketing portfolios.

Chief Financial Officer Andrew Penn will work with Mr Thodey and Telstra International Group President and Group Executive Tim Chen to enhance Telstra’s Asia strategy, drawing on Mr Penn’s extensive experience across Asia Pacific markets. Group Executive Corporate Affairs Tony Warren will again lead Telstra’s negotiations with the Federal Government on the National Broadband Network. All portfolio changes will be effective Monday 28 October. Other CEO leadership team members reporting to Mr Thodey remain unchanged: Rick Ellis, Group Executive Telstra Media Group; Tracey Gavegan, Group Executive Human Resources; Stuart Lee, Group Executive Telstra Wholesale; Carmel Mulhern, Group General Counsel; and Robert Nason, Group Executive Business Support and Improvement. “These changes make sense because they reflect our business needs and the exciting and rapidly moving environment around us,” Mr Thodey said. “Structure follows strategy so we have asked some of our most senior leaders to take on new or expanded opportunities to ensure we deliver on these promises. Each executive has considerable experience inside the industry as well as other industry sectors or global markets.” Media contacts: Jason Laird 0488 126823, Nicole McKechnie 0429 004617 Email: [email protected] www.telstra.com.au/abouttelstra/media-centre/ Reference: 249/2013

For

per

sona

l use

onl

y

CEO INVESTOR DAY SPEECH DRAFT V8 – CHECK AGAINST DELIVERY Page 1

CEO SPEECH NOTES

TELSTRA INVESTOR DAY

23 OCTOBER 2013

SLIDE 1: OPENING SLIDE

• Good morning and welcome...

• The purpose of today is to:

o Update you on our strategy;

o Hear from senior management about how we will

execute this strategy; and

o Give you an opportunity to ask questions.

• I recognise you may have questions about the National

Broadband Network and what impact the change of

Government policy will have. As you know, NBN Co has

just begun a 60 day strategic review so there is very little

we can add at this time.

• However, Kate McKenzie (Group Executive Director

Telstra Innovation Products and Marketing) and Tony

Warren (Group Managing Director of Corporate Affairs)

will talk briefly on the NBN later this morning and you

will have a chance to ask questions then.

For

per

sona

l use

onl

y

CEO INVESTOR DAY SPEECH DRAFT V8 – CHECK AGAINST DELIVERY Page 2

SLIDE 2: MAJOR INDUSTRY TRENDS

• Increasingly, smart technology is at the forefront of

everything we do.

o Think of the smart home; smart workplaces; smart

transportation; smart education; smart health; smart

cities; smart states etc.

• This presents tremendous new opportunities for our

industry.

• This morning I want to highlight some of the major

trends shaping the way we think about our business:

1. Exponential Growth in Connectivity: We are driving

to a world where everything will be connected,

wherever you are and whenever you want to be

connected. This will require different network design

and configurations... and different business models.

2. Demand for bandwidth: The growth in connected

devices and use of the network is driving an

extraordinary increase in demand for bandwidth, across

fixed and mobile networks (e.g. entertainment;

equipment monitoring and maintenance; environmental

controls etc). This is driving a new age of innovation.

Telcos must remain ahead of this demand curve but

what a wonderful industry to be in with such demand.

3. Consumer behaviour is changing and expectations

are increasing: Consumers are more informed, more

For

per

sona

l use

onl

y

CEO INVESTOR DAY SPEECH DRAFT V8 – CHECK AGAINST DELIVERY Page 3

demanding and less patient than at any other time. Not

only are they more informed about the products and

services they require, they have higher expectations

about the services they receive. We must continue to

improve our service and products.

4. Smarter networks and improved user interfaces:

The intelligence that now exists in networks has

improved functionality. New generation human to

machine interfaces like Suri and Google Now allow

technology to be used more simply and by more

people. Machine intelligence, gesture recognition and

new user interfaces mean millions of people are able to

participate in this digital revolution.

5. New network dependent, innovative applications

continue to grow very quickly: There are now billions of

mobile and fixed network applications available around

the world and an innovative software industry has been

born. Each one of these applications is dependent on

the network and is both driving network usage and

creating new opportunities.

6. Data Analytics: To deliver the type of experience

customers are demanding requires the analysis of vast

amounts of data. Data analytics have always been a

part of our world. Our ability to use this data to

improve the customer experience is an essential part of

our future.

For

per

sona

l use

onl

y

CEO INVESTOR DAY SPEECH DRAFT V8 – CHECK AGAINST DELIVERY Page 4

7. The last trend I want to mention is that of the Asian

century. The Asian region presents a huge market

opportunity with its growing middle class; rapid

urbanisation; and unprecedented economic growth. Half

of the world’s internet users live in Asia, and their

influence in the online world is only set to grow.

• These trends place telecommunications companies at

the heart of a societal and economic change taking

place around the world — we must capitalise upon this

opportunity as we can create tremendous value for our

customers.

SLIDE 3: THREE CRITICAL TECHNOLGIES FOR TELSTRA

• There are three technological changes that are critical

for our future:

o The Mobile Internet is enabling a new generation

of applications and solutions which in turn is enabling

individuals, businesses, governments, industries and

societies in ways we could never have imagined. This

rate of technological innovation will only accelerate.

o Cloud solutions (the use of computer hardware and

software resources delivered over a network or the

Internet) are becoming an essential part of business.

There are already over two billion global users of

cloud based email services like Gmail, Yahoo! and

For

per

sona

l use

onl

y

CEO INVESTOR DAY SPEECH DRAFT V8 – CHECK AGAINST DELIVERY Page 5

Hotmail. This is now extending to business critical

applications. The rate of innovation in building

seamless end-to end solutions to meet business

needs is accelerating.

o The third technology is what we call “the internet

of things” (also known as the Industrial Internet or

Machine to Machine) where everything

communicates. This is growing rapidly – and goes

beyond phones and devices connected to the

internet. These changes are happening now (for

example, in e-health, smart meters, vehicle tracking)

and will drive a fundamental change in our

landscape. As you will hear today, we recently past

the one million mark for our Machine to Machine

services.

• I believe Telstra is well placed to leverage its strengths

and be a serious competitor in each of these areas.

• You will hear more about these opportunities throughout

the course of the day. With that in mind let me now turn

to our strategy.

SLIDE 4: OUR STRATEGY HAS SERVED US WELL

• Since 2010 we have been focused on four strategic

priorities:

o Improving customer satisfaction;

For

per

sona

l use

onl

y

CEO INVESTOR DAY SPEECH DRAFT V8 – CHECK AGAINST DELIVERY Page 6

o Retaining and growing our customer numbers;

o Simplifying the business; and

o Building new growth businesses.

• As our results demonstrate, these priorities have served

us well:

o For the past three years, we have delivered top line

growth.

o We continue to hold operating costs, having

delivered around $2.7B in productivity benefits over

the past three years.

o Last financial year our earnings per share grew

12%.

o Our efforts have translated into strong shareholder

returns.

• Telstra is a great Australian telecommunications

company, focused on enabling our customers to utilise

network connectivity to improve their quality of life,

enhance business productivity and enable industries and

governments to achieve their ambitions. We are focused

on providing connectivity to enable new capabilities. We

will progressively expand these capabilities through Asia.

For

per

sona

l use

onl

y

CEO INVESTOR DAY SPEECH DRAFT V8 – CHECK AGAINST DELIVERY Page 7

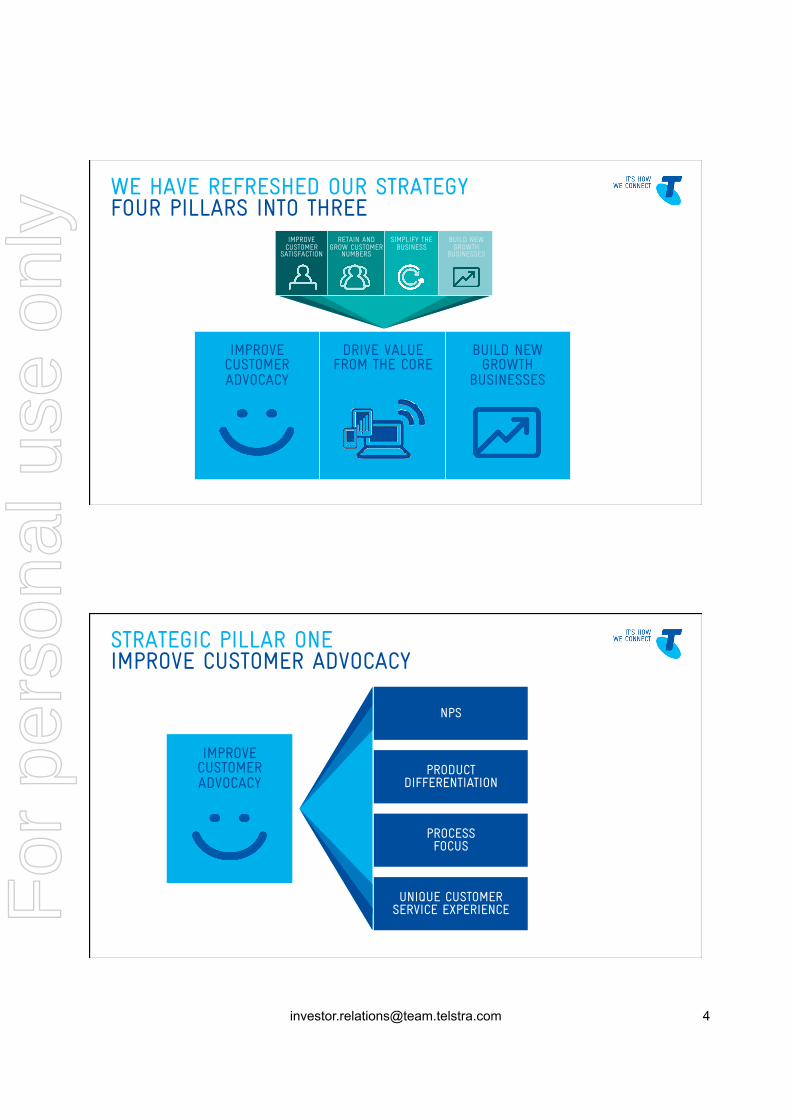

SLIDE 5: WE HAVE REFRESHED OUR STRATEGY

• We regularly review our long-term strategy with a

view to ensuring we have the right focus on how to deliver

long-term value.

• As a result, we have made some subtle but important

changes to our strategic priorities which we think better

reflect the way we think about managing and growing our

business.

• Our refreshed strategy is centred around three

priorities:

o Improving customer advocacy;

o Driving value from the core business; and

o Building new growth businesses.

• Today we are going to explore each of those priorities.

• You will notice a shift in emphasis but the foundations

of our strategic framework remain strong.

SLIDE 6: IMPROVING CUSTOMER ADVOCACY

• We are moving from a focus on satisfying our customers

to driving customer advocacy. Why? The evidence

suggests that turning customers into advocates translates

into shareholder value.

• Let me explain this. Advocates:

For

per

sona

l use

onl

y

CEO INVESTOR DAY SPEECH DRAFT V8 – CHECK AGAINST DELIVERY Page 8

o Buy more;

o Churn less;

o Recommend more often; and

o Generate fewer complaints and call volumes.

• To do this, we need to change:

o We are embedding the Net Promoter System

into our business and improving our interactions with

customers;

o We are investing in product differentiation and

bundling:

o We are focusing on getting our processes right;

and

o We’re providing customers with a unique service

experience.

• While the industry has followed Telstra’s lead on

customer service, I’m pleased to say our data indicates

we are improving faster than the industry as a whole...

and we have really only begun the journey.

• While our focus on improving our core service delivery

remains, our attention has shifted to broadening our

service relationship with our customers.

o We are approaching customer loyalty in ways that

differentiate us from our competitors.

For

per

sona

l use

onl

y

CEO INVESTOR DAY SPEECH DRAFT V8 – CHECK AGAINST DELIVERY Page 9

o Our approach to bundling telecommunication

services, entertainment and shared data is opening

up new service paradigms for consumers.

o We are now part of the productivity agenda for

other businesses and our offerings allow us to

establish true customer service partnerships with

small, medium and large business.

• This morning Gordon Ballantyne will lead the discussion

into this strategic priority.

SLIDE 7: DRIVING GREATER VALUE FROM THE CORE

• Our second priority is to drive greater value from the

core.

• We define the core as our key domestic products,

services and costs that comprise the bulk of our

portfolio today.

• Our focus on retaining and growing customer

numbers remains a priority but the emphasis has

expanded to delivering organic revenue growth; as

well as maintaining our network leadership and

driving productivity by simplifying the business.

• As at the end of September we have:

• 15.3 million mobile customers (having added

243,000 customers in the first quarter);

For

per

sona

l use

onl

y

CEO INVESTOR DAY SPEECH DRAFT V8 – CHECK AGAINST DELIVERY Page 10

• 2.8 million fixed broadband customers (having

added 41,000 customers in the first quarter); and

• 1.7 million customers with a fixed broadband

bundle (having added 51,000 customers this

quarter).

• This morning you will hear more about this priority from

Kate McKenzie; Warwick Bray (Group Executive

Director Mobile and Wireline); Philip Jones (Executive

Director Data IP Network Application and Services) and

Robert Nason.

• Driving value from the core is important because the

scale of our core business is so significant in terms of

customers, revenue and networks.

• We continue to invest in our networks to maintain our

network leadership.

• We believe there is enormous potential for growing

revenue and returns in our core business.

• As you know, last week at our Annual General Meeting we

reaffirmed our financial guidance for FY13 which

includes low single digit income and EBITDA growth.

SLIDE 8: BUILDING NEW GROWTH BUSINESSES

• Turning to our third priority of building new growth

businesses. We have adjusted our focus to reflect more

For

per

sona

l use

onl

y

CEO INVESTOR DAY SPEECH DRAFT V8 – CHECK AGAINST DELIVERY Page 11

accurately the way we look at our business and the

growth opportunities that exist.

• When we talk about growth we are talking about:

o The more immediate opportunities in our Network

Applications and Services business and Asia; as

well as

o Emerging opportunities including Digital Media,

Global Applications and Platforms and eHealth.

• You will hear about these opportunities during the

breakout sessions this afternoon. You will have the

chance to select three of the five growth areas I just

mentioned.

• Our strategic growth opportunities focus on leveraging

our current strengths. We believe we can provide

customers with a unique service experience that makes it

compelling to choose Telstra.

SLIDE 9: ORGANISATIONAL ALIGNMENT

• It is important that our organisation is aligned to our

strategy, especially our growth agenda and value from the

core.

• As a result of the changes we have made to our strategy,

we have made some important changes to the

For

per

sona

l use

onl

y

CEO INVESTOR DAY SPEECH DRAFT V8 – CHECK AGAINST DELIVERY Page 12

structure of our leadership team. We have a strong

leadership team. The depth of capability is evident.

• We have asked some of our most senior leaders to take

on new or expanded opportunities to ensure we

deliver on our strategy.

• Each executive has considerable experience inside the

industry as well as other industry sectors or global

markets.

• Let me step you through the changes.

• We are establishing a new business unit, Global

Enterprise and Services, in what will be a $5 billion

revenue business unit from day one. This business has

exciting growth opportunities.

o Brendon Riley will lead this business unit, bringing

together Network Application Services on a

worldwide basis, Global Applications and Services, a

new cloud division, Telstra Ventures, Telstra

Enterprise and Government and Defence contract.

o This will be an industry-based services and solutions

business, operating at a global scale,

• Now to Telstra Operations:

o Kate McKenzie is our new Chief Operations Officer,

including the Chief Technology Office and innovation

For

per

sona

l use

onl

y

CEO INVESTOR DAY SPEECH DRAFT V8 – CHECK AGAINST DELIVERY Page 13

portfolios to better integrate technology development

and implementation.

o Telstra Operations will lead Telstra’s ongoing

technical excellence across fixed and mobile

networks.

o As you know, Kate was most recently responsible for

Innovation, Products and Marketing.

• Turning to Telstra Retail:

o Gordon Ballantyne will lead a new group that will

consolidate our key retail-facing segments including

Telstra Consumer and Telstra Business; retail

products management; National Broadband Network

retail roll-out; Telstra Country Wide and the Chief

Marketing Office. Gordon will also have responsibility

for growth through the new eHealth division.

• In addition, I’ve asked Andy Penn to work with me and

Tim Chen to enhance our Asia strategy, drawing on Andy’s

extensive experience across Asia Pacific markets.

• Tony Warren will again lead Telstra’s negotiations with

the Federal Government on the National Broadband

Network.

• Other CEO leadership team members remain

unchanged.

For

per

sona

l use

onl

y

CEO INVESTOR DAY SPEECH DRAFT V8 – CHECK AGAINST DELIVERY Page 14

• These changes become effective next Monday, 28

October.

SLIDE 10: SUMMARY

• Before I hand over to Gordon Ballantyne to lead the

discussion on the first of our strategic priorities, customer

advocacy, let me summarise our focus for today:

o We have a clear strategy in place and we are

focused on delivering against that strategy.

o We have made some subtle but important

refinements to our strategy to reflect where the

business is heading.

o We have made some organisational changes to

align the organisation to our strategy.

• Our strategy is centred around three priorities:

o Improving customer advocacy;

o Driving value from the core; and

o Building new growth businesses.

• Thank you.

[END]

For

per

sona

l use

onl

y

TELS

TRA T

EM

PLATE 4

X3 B

LUE B

ETA

|

TELP

PTV4

TELSTRA INVESTOR DAY 0CTOBER 2013

TELS

TRA

TEM

PLA

TE 4

X3

BLU

E B

ETA

| T

ELP

PTV

4

DISCLAIMER

! These presentations include certain forward-looking statements that are based on information and assumptions known to date and are subject to various risks and uncertainties. Actual results, performance or achievements could be significantly different from those expressed in, or implied by, these forward-looking statements. Such forward-looking statements are not guarantees of future performance and involve known and unknown risks, uncertainties and other factors, many of which are beyond the control of Telstra, which may cause actual results to differ materially from those expressed in the statements contained in these presentations. For example, the factors that are likely to affect the results of Telstra include general economic conditions in Australia; exchange rates; competition in the markets in which Telstra will operate; the inherent regulatory risks in the businesses of Telstra; the substantial technological changes taking place in the telecommunications industry; and the continuing growth in the data, internet, mobile and other telecommunications markets where Telstra will operate. A number of these factors are described in Telstra’s Annual Report dated 8 August 2013 and 2013 Debt Offering Circular lodged with the ASX and available on Telstra’s Investor Centre website www.telstra.com/investor.

! All forward-looking figures in this presentation are unaudited and based on A-IFRS. Certain figures may be subject to rounding differences. All market share information in this presentation is based on management estimates based on internally available information unless otherwise indicated.

! All amounts are in Australian Dollars unless otherwise stated.

! ® ™ Registered trademark and trademark of Telstra Corporation Limited (ACN 051 775 556) and its subsidiaries. Other trademarks are the property of their respective owners.

For

per

sona

l use

onl

y

DAVID THODEY CHIEF EXECUTIVE OFFICER

TRENDS IN THE GLOBAL TELCO INDUSTRY

GROWTH IN CONNECTIVITY

DEMAND FOR BANDWIDTH

CHANGING CONSUMER BEHAVIOUR AND INCREASING EXPECTATIONS

SMARTER NETWORKS AND IMPROVED USER INTERFACES

NETWORK DEPENDENT, INNOVATIVE APPLICATIONS

DATA ANALYTICS

THE ASIAN CENTURY For

per

sona

l use

onl

y

KEY INFLUENCING TECHNOLOGIES

OUR STRATEGIC FRAMEWORK HAS SERVED US WELL THE FOUR PILLARS

IMPROVE CUSTOMER

SATISFACTION

RETAIN AND GROW CUSTOMER

NUMBERS

SIMPLIFY THE BUSINESS

BUILD NEW GROWTH

BUSINESSES

For

per

sona

l use

onl

y

IMPROVE CUSTOMER ADVOCACY

DRIVE VALUE FROM THE CORE

BUILD NEW GROWTH

BUSINESSES

IMPROVE CUSTOMER

SATISFACTION

RETAIN AND GROW CUSTOMER

NUMBERS

SIMPLIFY THE BUSINESS

BUILD NEW GROWTH

BUSINESSES

WE HAVE REFRESHED OUR STRATEGY FOUR PILLARS INTO THREE

STRATEGIC PILLAR ONE IMPROVE CUSTOMER ADVOCACY

NPS

PRODUCT DIFFERENTIATION

PROCESS FOCUS

UNIQUE CUSTOMER SERVICE EXPERIENCE

IMPROVE CUSTOMER ADVOCACY

For

per

sona

l use

onl

y

STRATEGIC PILLAR TWO DRIVE VALUE FROM THE CORE

CUSTOMER AND REVENUE GROWTH

NETWORK LEADERSHIP

DRIVE PRODUCTIVITY THROUGH SIMPLIFYING

THE BUSINESS

DRIVE VALUE FROM THE CORE

STRATEGIC PILLAR THREE BUILD NEW GROWTH BUSINESSES

NAS

ASIA

EMERGING OPPORTUNITIES • eHEALTH • GLOBAL APPLICATIONS &

PLATFORMS • DIGITAL MEDIA

BUILD NEW GROWTH

BUSINESSES

For

per

sona

l use

onl

y

ORGANISATIONAL ALIGNMENT DAVID THODEY

CHIEF EXECUTIVE OFFICER

GORDON BALLANTYNE GROUP EXECUTIVE TELSTRA RETAIL

RICK ELLIS GROUP EXECUTIVE

TELSTRA MEDIA GROUP

ANDREW PENN CHIEF FINANCIAL OFFICER

FINANCE & STRATEGY

CARMEL MULHERN GROUP GENERAL COUNSEL

LEGAL SERVICES

TRACEY GAVEGAN GROUP EXECUTIVE

HUMAN RESOURCES

KATE MCKENZIE CHIEF OPERATIONS OFFICER

TELSTRA OPERATIONS

BRENDON RILEY GROUP EXECUTIVE

GLOBAL ENTERPRISE & SERVICES

TONY WARREN GROUP EXECUTIVE

CORPORATE AFFAIRS

ROBERT NASON GROUP EXECUTIVE

BUSINESS SUPPORT & IMPROVEMENT

TIM CHEN PRESIDENT & GROUP EXECUTIVE TELSTRA INTERNATIONAL GROUP

STUART LEE GROUP EXECUTIVE

TELSTRA WHOLESALE JENNIFER CRICHTON

CHIEF OF STAFF

OUR STRATEGY IS CENTRED AROUND THREE PRIORITIES 1. IMPROVING CUSTOMER ADVOCACY 2. DRIVING VALUE FROM THE CORE 3. BUILDING NEW GROWTH BUSINESSES

WE HAVE MADE SOME ORGANISATIONAL CHANGES TO ALIGN THE ORGANISATION TO OUR STRATEGY

WE HAVE MADE SOME SUBTLE BUT IMPORTANT REFINEMENTS TO OUR STRATEGY TO BETTER REFLECT WHERE THE BUSINESS IS HEADING

SUMMARY

WE HAVE A CLEAR STRATEGY IN PLACE AND ARE FOCUSED ON DELIVERING AGAINST THAT STRATEGY

For

per

sona

l use

onl

y

TELS

TRA T

EM

PLATE 4

X3 B

LUE B

ETA

|

TELP

PTV4

CUSTOMER ADVOCACY GORDON BALLANTYNE, CHIEF CUSTOMER OFFICER

TELS

TRA

TEM

PLA

TE 4

X3

BLU

E B

ETA

| T

ELP

PTV

4

FOCUSING ON THE THINGS THAT MATTER FOR OUR CUSTOMERS

INSIGHTS MATTER INNOVATION MATTERS SIMPLICITY MATTERS Connecting us to what’s important

for our customers In our products, our services, our

networks, and in recognising loyalty Making it easy for our customers to

do business with us

Voice of the Customer

11 million NPS surveys in FY13

Voice of the Customer in our operations, our conversations and our celebrations

! Top 16 Processes covering all aspects of Telstra’s operations

! Our Customer Connection 2 – 75 events for 7500 participants

! 4000 T-Time Meetings each month ! Open and honest conversation on

internal social network, Yammer ! Telstra Employee Referral ! Zing! Recognition and reward F

or p

erso

nal u

se o

nly

TELS

TRA

TEM

PLA

TE 4

X3

BLU

E B

ETA

| T

ELP

PTV

4

FOCUSING ON THE THINGS THAT MATTER FOR OUR CUSTOMERS

INSIGHTS MATTER INNOVATION MATTERS SIMPLICITY MATTERS Connecting us to what’s important

for our customers In our products, our services, our

networks, and in recognising loyalty Making it easy for our customers to

do business with us

Making it easy to do business with us ! 40% of store transactions completed in 3 minutes ! First Call Resolution improved again in FY13 ! 8% reduction in TIO complaints in FY13 ! Consumer contact centre volumes per SIO reduced by 16%

since FY11

And customers are embracing digital like never before:

! >2.5 million downloads of the 24/7 app, and 1m regular users ! 1.5 million MyAccount regular users ! 2.5 million customers receive only electronic bills ! LiveChat: >600% growth in inbound chats during FY13

TELS

TRA

TEM

PLA

TE 4

X3

BLU

E B

ETA

| T

ELP

PTV

4

FOCUSING ON THE THINGS THAT MATTER FOR OUR CUSTOMERS

INSIGHTS MATTER INNOVATION MATTERS SIMPLICITY MATTERS Connecting us to what’s important

for our customers In our products, our services, our

networks, and in recognising loyalty Making it easy for our customers to

do business with us

$1.2B INVESTED IN OUR MOBILE

NETWORK in FY13

4G NETWORK NOW COVERS 66% OF THE POPULATION AND WILL REACH 85% BY DEC ‘13

Roaming alerts Entertainer Bundles Game-changing Returns & Repairs No Lock-In Plans ‘Thanks’ TM program F

or p

erso

nal u

se o

nly

TELS

TRA

TEM

PLA

TE 4

X3

BLU

E B

ETA

| T

ELP

PTV

4

MAINTAINING OUR COURSE Broad benefits built on Customer agenda

FY10 FY11 FY12 FY13

DELIVERING MARKET RESULTS Creating advocates and winning customers

EXECUTING ON WHAT MATTERS Changing the way we run our business

Customers are voting with their feet ! In FY13 1.3 million retail mobile

customers added, and 238,000 new bundled customers bringing the total to 1.6 million

Our advocacy agenda has changed: ! Operating rhythm, meetings, culture ! Investment decisions ! Allocation of human capital resources ! Our approach to product development

WE’RE EXECUTING ON WHAT MATTERS AND SEEING THE RESULTS

Since introducing NPS a year ago, we’ve made considerable progress but there’s much more to do

Q4 FY12 Q1 FY13 Q2 FY13 Q3 FY13 Q4 FY13

NPS

Scor

e Mov

emen

t

Making us values-led, customer-led: ! Making it easier to do business ! Maintaining Network Leadership ! Simple Products and Pricing ! Telstra “Thanks” Loyalty Program

$9.6B

$10.7B

10.8%

0.4m

1.6m

FY10 FY11 FY12 FY13

FY10 FY11 FY12 FY13

Telstra Consumer Segment Income

Fixed Bundles

Postpaid Handheld Churn

16.2%

TELS

TRA T

EM

PLATE 4

X3 B

LUE B

ETA

|

TELP

PTV4

Q&A

For

per

sona

l use

onl

y

TELS

TRA T

EM

PLATE 4

X3 B

LUE B

ETA

|

TELP

PTV4

DRIVING VALUE FROM THE CORE KATE MCKENZIE, GROUP MANAGING DIRECTOR INNOVATION PRODUCTS AND MARKETING

TELS

TRA

TEM

PLA

TE 4

X3

BLU

E B

ETA

| T

ELP

PTV

4

DRIVING VALUE FROM THE CORE

CUSTOMER AND REVENUE GROWTH

NETWORK LEADERSHIP

DRIVE PRODUCTIVITY THROUGH SIMPLIFYING

THE BUSINESS

DRIVE VALUE FROM THE CORE

For

per

sona

l use

onl

y

TELS

TRA

TEM

PLA

TE 4

X3

BLU

E B

ETA

| T

ELP

PTV

4

OUR DOMESTIC CORE IS A KEY ASSET WE INTEND TO LEVERAGE FOR GROWTH

“Companies have a four to six times better chance of success if they seek a solution for tomorrow’s growth based

on their ‘hidden assets’ in the core”

Chris Zook, Bain and Company

TELS

TRA

TEM

PLA

TE 4

X3

BLU

E B

ETA

| T

ELP

PTV

4

FOUR OF OUR TOP PRIORITIES TO DRIVE VALUE FROM THE CORE

MARKET MAKER IN MOBILITY

Growth in services through continued network differentiation and new adjacent services such as M2M

GROWING IN DATA & IP

Growth in core data and IP services through increasing product differentiation for our business and enterprise customers

EXTENDING OUR PRODUCTIVITY

Extending our productivity drive to include our new and growth businesses, as well as improving capital efficiency and asset base effectiveness

WINNING IN BROADBAND

Making the NBN migration experience as simple as possible for our consumer and business customers

For

per

sona

l use

onl

y

TELS

TRA T

EM

PLATE 4

X3 B

LUE B

ETA

|

TELP

PTV4

MOBILES WARWICK BRAY, GROUP EXECUTIVE DIRECTOR MOBILE AND WIRELINE

TELS

TRA

TEM

PLA

TE 4

X3

BLU

E B

ETA

| T

ELP

PTV

4

MOBILES IMPORTANT TO TELSTRA’S GROWTH

FIXED MEDIA MOBILES NAS DATA & IP OTHER1 INTERNATIONAL

-2.2%

$520m

$224m

+17.7%

+16.2% +26.1%

$78m $243m

+2.4% EX CLEAR

FY12 EX TELSTRACLEAR

-$205m

-2.7%

-7.8%

+6.0% -$186m

-$67m

FY13 EX TELSTRACLEAR

$25,338m

$24,731m

1. Other includes revenue for the NBN Information Campaign and Migration Deed and miscellaneous fee revenue

For

per

sona

l use

onl

y

TELS

TRA

TEM

PLA

TE 4

X3

BLU

E B

ETA

| T

ELP

PTV

4

36% 32% 36% 38% MARGIN

CONTINUED GROWTH

REVENUE ($B)

2009

6.8

2010

7.3

2011

8.0

2012

8.7

2013

9.2

2009

10.2

2010

10.6

2011

12.2

2012

13.8

2013

15.1

2009

2.4

2010

2.6

2011

2.6

2012

3.1

2013

3.5

SIOs (M) EBITDA ($B)

6.4% 10.1% 8.5% 6.0% GROWTH 0.364 1.668 1.592 1.257 GROWTH 36%

TELS

TRA

TEM

PLA

TE 4

X3

BLU

E B

ETA

| T

ELP

PTV

4

CONTINUED MOMENTUM

FY12 & FY13 REVENUE ($M)

MOBILES REVENUE* ($ MILLIONS)

2011/12 2012/13

FY12 H1 H2 FY13

JUN-12 PCP GROWTH DEC-12 PCP

GROWTH JUN-13 PCP GROWTH JUN-13 PCP

GROWTH

Postpaid handheld 4,672 6.0% 2,377 0.3% 2,427 5.4% 4,804 2.8%

Prepaid handheld 654 2.7% 351 7.7% 376 14.6% 727 11.2%

Total handheld 5,326 5.5% 2,728 1.2% 2,803 6.6% 5,531 3.8%

Mobile broadband 1,018 10.8% 576 16.8% 620 18.1% 1,196 17.5%

Machine to Machine (M2M) 80 15.9% 44 10.0% 46 15.0% 90 12.5%

Satellite 12 0.0% 7 0.0% 6 20.0% 13 8.3%

Mobile services revenue - retail 6,436 6.5% 3,355 3.7% 3,475 8.6% 6,830 6.1%

* From 5 year P&L sheet of Full Year 2013 Financial Results supporting Material spreadsheet

For

per

sona

l use

onl

y

TELS

TRA

TEM

PLA

TE 4

X3

BLU

E B

ETA

| T

ELP

PTV

4

ARPU DECLINE SLOWING

FY12 & FY13 ARPUs ($)

TELSTRA GROUP 2011/12 2012/13

FY12 H1 H2 FY13 $ PCP $ $ PCP $ $ PCP $ $ PCP $

SIO ARPUs

Postpaid Handheld $61.51 ($2.44) $58.88 ($4.50) $58.29 ($0.75) $58.80 ($2.71)

Postpaid Handheld ex MRO $65.42 $0.06 $64.75 ($1.73) $65.39 $1.70 $65.33 ($0.09)

Prepaid Handheld $16.87 ($0.02) $17.79 $1.03 $18.44 $1.77 $17.94 $1.07

Total Mobile Broadband $31.26 ($8.96) $29.75 ($2.75) $29.93 $0.09 $29.80 ($1.46)

Machine to Machine (M2M) $9.09 ($0.45) $8.66 ($0.94) $8.30 ($0.20) $8.46 ($0.63)

Blended ARPU including interconnect and MRO $46.08 ($2.81) $44.29 ($3.42) $43.47 ($0.47) $43.84 ($2.24)

* From 5 year P&L sheet of Full Year 2013 Financial Results supporting Material spreadsheet

TELS

TRA

TEM

PLA

TE 4

X3

BLU

E B

ETA

| T

ELP

PTV

4

MOBILE PRIORITIES (FROM LAST YEAR)

IMPROVE CUSTOMER

SATISFACTION

RETAIN AND GROW

CUSTOMERS

SIMPLIFY THE BUSINESS

DEVELOP NEW GROWTH

BUSINESSES

! Call volumes and “right first time” ! Self service (online) ! Reduce bill shock (alerts & excess) ! Device excellence

! Promote network advantage ! Promote customer service improvements

! Operating costs and SARC ! Best practice ARPU ! Targeted network CAPEX

! MBB ! M2M ! Business applications

INCREASE ADVOCACY

WHY TELSTRA?

IMPROVE MARGINS

GROWTH For

per

sona

l use

onl

y

TELS

TRA

TEM

PLA

TE 4

X3

BLU

E B

ETA

| T

ELP

PTV

4

• LTE 66% population coverage • Expanded LTE bandwidth to

15MHz Syd/Melb, 20 MHz Bris/Adel/Per

• Trial 900MHz LTE and 900+1800 LTE-A Carrier Aggregation.

• Bought 2x20MHz of 700MHz and 2x40MHz 2.5GHz spectrum

• Leading approach to network planning

• $1.2B of mobile CAPEX

NETWORK LEADERSHIP

NETWORK AIMS FY13 ACHIEVEMENTS FY14 FOCUS

Superior Coverage & Depth* • More sq kms • Fewer dead spots • Fewer dropped calls • More reliable speed experience

• LTE 85% population by Christmas

• Launch LTE-A 900+1800 CA device with Cat 4

• Re-farm 900MHz & selectively deploy 900+1800 LTE-A

• Promote & grow the APT700 ecosystem.

• Trial 700+1800MHz LTE-A Carrier Aggregation at 300 Mbps.

• Source Cat 6 devices in bands to enable above.

• Trial LTE-B & small cells for capacity & functionality

• ~$1.2B of mobile CAPEX

* In an environment of growing demand.

TELS

TRA

TEM

PLA

TE 4

X3

BLU

E B

ETA

| T

ELP

PTV

4

THE NETWORK WITHOUT EQUAL CAMPAIGNS

For

per

sona

l use

onl

y

TELS

TRA

TEM

PLA

TE 4

X3

BLU

E B

ETA

| T

ELP

PTV

4

IMPROVING ADVOCACY

INITIATIVES OUTCOMES

DEVICE REPLACEMENT

24X7

ADVOCACY

DIGITAL ENHANCEMENTS

REDUCE BILL SHOCK

SERVICE CALLS/ CUSTOMER

TIO COMPLAINTS

TELS

TRA

TEM

PLA

TE 4

X3

BLU

E B

ETA

| T

ELP

PTV

4

BAD DEBT & REBATES

MOBILE MARGIN OUTCOMES

NO. OF EVENTS • TENURE • PROPENSITY

MIX

BYOD UNIT SUBSIDIES

COST OF NON-QUALITY

NO. OF SERVICE CALLS

PREPAY RECHARGE

SARC MARGIN

For

per

sona

l use

onl

y

TELS

TRA

TEM

PLA

TE 4

X3

BLU

E B

ETA

| T

ELP

PTV

4

WORKING WITH INDUSTRY SOLUTION PARTNERS IN M2M

AGRICULTURE / ENVIRONMENT

INDUSTRIAL & MANUFACTURING HEALTHCARE BUSINESS

SERVICES CONSUMER

ELECTRONICS

SOLUTION & APPLICATION PROVIDERS

REFERRAL VALUE ADDED RESELLER

PARTNERS

HARDWARE PROVIDERS / OEMS

M2M PLATFORM PARTNER

SYSTEM INTEGRATORS & DEVELOPERS

PUBLIC SAFETY & SECURITY

TRANSPORT / LOGISTICS

RETAIL / FINANCIAL SERVICES ENERGY & UTILITIES

TELS

TRA

TEM

PLA

TE 4

X3

BLU

E B

ETA

| T

ELP

PTV

4

IMPROVING BUSINESS PRODUCTIVITY THROUGH CONNECTED TABLETS

SALES FORCE TRADES PEOPLE FIELD FORCE

• Mobile access to CRM tools • Collaboration • Access to Collateral • Expenses • Analytics • Training

• Job Dispatch & Management • Mobile digital forms • Invoicing

• Logging work & issues • Rich data (GPS / Photography) • OH&S Monitoring

ARISapp Empower your mobile

teams in real time

CANVAS Escape the paper chase

GeoOP Job Dispatch and Management

KONY Same App, Any Screen

Launched May FY13 Launched May FY13 Launched June FY13 Coming in 1H FY14

For

per

sona

l use

onl

y

TELS

TRA

TEM

PLA

TE 4

X3

BLU

E B

ETA

| T

ELP

PTV

4

• Call volumes and “right first time” • Self service (online) • Reduce bill shock

IMPROVE CUSTOMER ADVOCACY

BE THE MARKET MAKER IN MOBILE IN FY14

MONETISE DATA

SERVICE INITIATIVES

• Increase and promote network advantage

• Increase and promote customer service improvements

DRIVING VALUE FROM THE CORE WHY TELSTRA?

• Operating costs and SARC • Best practice ARPU • Targeted network CAPEX

DRIVING VALUE FROM THE CORE IMPROVE

MARGINS

• MBB • M2M • Business applications

BUILD NEW GROWTH

BUSINESSES BUSINESS PRODUCTIVITY

BUSINESS CONNECTED DEVICES

MARKET MAKER

TELS

TRA

TEM

PLA

TE 4

X3

BLU

E B

ETA

| T

ELP

PTV

4

CONCLUSION

INVESTMENT OUTCOMES

NETWORK

SERVICE

MARKETING

NEW BUSINESS

GROWTH

ADVOCACY

For

per

sona

l use

onl

y

TELS

TRA T

EM

PLATE 4

X3 B

LUE B

ETA

|

TELP

PTV4

APPENDICES

TELS

TRA

TEM

PLA

TE 4

X3

BLU

E B

ETA

| T

ELP

PTV

4

Reduce installation & set up time of a new kiosk and link all the locations to meet demand.

In 2002 Move Yourself pioneered self-service kiosks for trailer hire, reducing the need to for service station assistants. It now operates from more then 1000 locations in Australia.

IMPROVING PRODUCTIVITY IN LOGISTICS WITH M2M

AUTOMATION OF ‘MOVE YOURSELF TRAILER HIRE’ POWERED BY M2M

COMPANY PROFILE BUSINESS CHALLENGE

“We chose Telstra because the Next G network offers the most reliable connection and the Telstra M2M Control Centre gives us control of our plan’”

“Telstra M2M technology means our system has all the facts, movements and performance of all our products and agents by the minute”.

MOVE YOURSELF TRAILER HIRE, M.D. Bill Cowie

WHY TELSTRA & MOVE YOURSELF TRAILER

“The big efficiency gain has been the control of the SIM cards and the Next G connection”.

“We have seen $140,000 pa operational savings”

MOVE YOURSELF TRAILER HIRE, M.D. Bill Cowie For

per

sona

l use

onl

y

TELS

TRA

TEM

PLA

TE 4

X3

BLU

E B

ETA

| T

ELP

PTV

4

MOBILE BUSINESS APPS TO MONITOR OH&S COMPLIANCE IN FIELD WORKFORCE

Over 500 vehicles, with a paper based crew manual which holds important occupational health and safety information for field staff that work near powerlines every day. Business was spending up to $75,000 to update manual 4 times per year.

ETS is Australia’s largest Vegetation Management Company with over 1000 field staff across 18 locations across Australia. 90% of customers are utilities where they cut the trees around power lines

TELSTRA + ARIS FOR EASTERN TREE SERVICES

COMPANY PROFILE BUSINESS CHALLENGE

Deployed Tablets with ARIS Mobile Business Application connected to the Telstra Next G network • Saved significant costs on updating paper based manuals. • Monitor what version crew manuals staff are using and update

in real-time. • Send quizzes down to field staff so they can complete online

training in the field. • Ensure only qualified staff are allocated to jobs

WHY TELSTRA & ARIS

“We recently won some more work in Tasmania where we got the whole state awarded to us. The client gave us feedback that our tablet solution was innovative and it was a key factor in awarding us this extra work.” “If we can make people safer and make them think about what they are doing that’s our main aim.” Paul Tymensen, Chief Financial Officer – ETS

TELS

TRA T

EM

PLATE 4

X3 B

LUE B

ETA

|

TELP

PTV4

WINNING IN BROADBAND KATE MCKENZIE, GROUP MANAGING DIRECTOR TELSTRA INNOVATION, PRODUCTS AND MARKETING

For

per

sona

l use

onl

y

TELS

TRA

TEM

PLA

TE 4

X3

BLU

E B

ETA

| T

ELP

PTV

4

WINNING IN FIXED BROADBAND

$1,987

$2,087

FY12 FY13

FIXED BROADBAND REVENUE ($m)

+5%

Fixed broadband includes fixed broadband and NBN data revenue

Retail fixed broadband customers up 173,000 to 2.8 million in FY13 (additional 41k in Q1 of FY14)

Bundled customers up 238,000 in FY13 to 1.6 million, representing 59% of our fixed broadband customer base

Launched “Entertainer Bundles” with mobility inclusions

Launched online desktop application (My Online Toolkit) to improve assurance experience on ADSL

FY13 KEY HIGHLIGHTS

TELS

TRA

TEM

PLA

TE 4

X3

BLU

E B

ETA

| T

ELP

PTV

4

WINNING IN NBN: THE LAST 12 MONTHS

TELSTRA MOMENTUM CONTINUES TO BUILD AS TELSTRA CONNECTS CUSTOMERS TO FIBRE AND FIXED WIRELESS ON THE NBN

Key Milestones in the last 12 months

NBN Co announced disconnection dates for the first 15 markets (November 2012)

Telstra launched Business Plans on the NBN (December 2012)

Casual Plans from Telstra launched (April 2013)

Fixed Wireless Telstra launch (July 2013)

Telstra launched battery backed up voice services on NBN (July 2013)

Self Install for Greenfields launch (September 2013) For

per

sona

l use

onl

y

TELS

TRA

TEM

PLA

TE 4

X3

BLU

E B

ETA

| T

ELP

PTV

4

WE ARE WELL PLACED TO COMPETE: ~700 MICRO MARKETS

* NBN Co Fibre and Fixed Wireless premises as at 21/10/2013

NBN MARKET CONTINUES TO GROW REACHING 370K PREMISES* ACROSS 685 SITES

TELSTRA IS ACTIVE IN ALL MARKETS PROVIDING NBN SERVICES OVER FIBRE AND FIXED WIRELESS

NEW OPPORTUNITIES OPENING UP WITHIN THE GREENFIELDS MARKET - APARTMENT BLOCKS, HOUSE & LAND AND AGED CARE MARKET SEGMENTS

17%

59%

7%

17%

Fibre (Brownfield Sites)

Fibre (Multi Dwelling Units)

Fibre (New Housing Estates)

Fixed Wireless

TELS

TRA

TEM

PLA

TE 4

X3

BLU

E B

ETA

| T

ELP

PTV

4

THE NBN IS A LOCAL CONVERSATION

• Telstra is an active member of local communities and has been for over 100 years

• Telstra is committed to helping customers understand what the NBN means for them and making the move simple

• Our local teams are active in each community helping customers, developers, builders and the wider community unlock the potential of the NBN

For

per

sona

l use

onl

y

TELS

TRA

TEM

PLA

TE 4

X3

BLU

E B

ETA

| T

ELP

PTV

4

WINNING IN THE MARKET WITH CUSTOMER BASED OFFERS

TELSTRA HAS BEEN OFFERING A RANGE OF VOICE, BROADBAND AND ENTERTAINMENT SERVICES ON THE NBN FOR 2 YEARS

Responding to customer feedback we have extended this range to include:

• Launch of casual plans for the rental market and self install options

• “Move in Day” offers for customers in apartment blocks

• Launch of Digital Office Technology (DOT) for business customers

• Introduction of NBN ready plans on cable and ADSL

TELS

TRA

TEM

PLA

TE 4

X3

BLU

E B

ETA

| T

ELP

PTV

4

NBN IS PART OF OUR CONNECTED HOME STRATEGY FOR BROADBAND

For

per

sona

l use

onl

y

TELS

TRA T

EM

PLATE 4

X3 B

LUE B

ETA

|

TELP

PTV4

NBN AGREEMENTS TONY WARREN GROUP MANAGING DIRECTOR CORPORATE AFFAIRS

TELS

TRA T

EM

PLATE 4

X3 B

LUE B

ETA

|

TELP

PTV4

Q&A

For

per

sona

l use

onl

y

TELS

TRA

TEM

PLA

TE 4

X3

BLU

E B

ETA

| T

ELP

PTV

4

DATA & IP PHILIP JONES, EXECUTIVE DIRECTOR DATA & IP

TELS

TRA

TEM

PLA

TE 4

X3

BLU

E B

ETA

| T

ELP

PTV

4

• Consumerisation of IT/ BYOD

• Mobility, Wireless, Smart Devices

• Cloud Delivery Models

TECHNOLOGY Demands speed &

innovation

• Social, Mobile & Global • Flexible Working • Security, Privacy & Control • Everything-as-a-Service • New Non-IT Decision

Makers

CUSTOMER New ways of working for individuals & businesses

Data & IP • Dynamics remain unchanged

NAS • Fragmented with competition

from diverse players: System Integrators, Global Telco’s, Over-the-top players, Niche players

COMPETITION Broader portfolio results

in new competitors

Data & IP • Market Share:

NAS • 47% of TEG IP Access

customers have NAS products • 250K T-Suite SaaS TB SIOs

MARKET DIPNAS is outperforming

the market across all portfolios

TEG TB

MARKET DYNAMICS CREATE A UNIQUE GROWTH OPPORTUNITY

For

per

sona

l use

onl

y

TELS

TRA

TEM

PLA

TE 4

X3

BLU

E B

ETA

| T

ELP

PTV

4

OUR DATA & IP NETWORKS ARE AN ENABLER FOR NAS GROWTH

NETWORKS

Drive IP differentiation

Mobile

Fixed & Broadband

IP

Internet

MANAGED NETWORK SERVICES

Deliver enhanced network service levels

Managed Mobility

Data Centre

WAN

LAN

SECURITY

Secure customers’ entire solution

Device Security

Security Apps

Network Security

Managed Security

CLOUD SERVICES

Deliver applications & infrastructure globally

IaaS & SaaS

Unified Comms & Collaboration

Enterprise Apps

UNIFIED COMMS

Enable collaboration with VAS

Telephony

Conferencing

Contact Centres

Bus & Mobile Apps

INDUSTRY SOLUTIONS

Media Retail Emergency Mining Financial Education Health

INTEGRATED SERVICE MANAGEMENT

Online Portals & Reporting

Service Desks & Support

Professional Services

Achieve Customers’ Business Objectives

21% FY13 Growth:

33% 18%

5% 29%

TELS

TRA

TEM

PLA

TE 4

X3

BLU

E B

ETA

| T

ELP

PTV

4

WE ARE HELPING OUR CUSTOMERS TRANSFORM THEIR BUSINESSES

CONTACT CENTRE VIDEO SOCIAL

ENTERPRISE VIDEO

CONFERENCING IP

TELEPHONY

ANY OFFICE

HEAD OFFICE

BRANCH OFFICE

DATA CENTRE

Converged IP Network Platform Integrated with Cloud & Apps TRADITIONAL COMMS

TRADITIONAL COMMS

ENTERPRISE APPS

BANDWIDTH UPGRADES

DATA CENTRE

RESULT IP ACCESS BANDWIDTH UPGRADES

ISDN & OTHER CALLING REVENUE MIGRATING TO

NAS

INCREASING IMPORTANCE OF NETWORK & VAS

TO: FROM:

For

per

sona

l use

onl

y

TELS

TRA

TEM

PLA

TE 4

X3

BLU

E B

ETA

| T

ELP

PTV

4

WE ARE CREATING ADVANTAGE TO DELIVER VALUE

Customers

Increasing Scale: Core capacity 75Tbps to 100Tbps

Increasing Coverage: 756 Australian and 85 global on-net POPs

Improving: Network security & intelligence

Integrating: Mobile, IP Network and Cloud products

Strengthening our differentiators... ...in order to deliver value for our customers and shareholders

Telstra

Converged IP platform to enable business transformation

Enabling productivity gains

Fostering innovation on the network and the cloud

Establishing long-term customer relationships

Increasing our addressable market

Delivering share gains and overall portfolio growth

TELS

TRA T

EM

PLATE 4

X3 B

LUE B

ETA

|

TELP

PTV4

PRODUCTIVITY AND BUSINESS IMPROVEMENT ROBERT NASON, GROUP MANAGING DIRECTOR BUSINESS SUPPORT AND IMPROVEMENT

For

per

sona

l use

onl

y

TELS

TRA

TEM

PLA

TE 4

X3

BLU

E B

ETA

| T

ELP

PTV

4

PROJECT NEW WAS ESTABLISHED TO DRIVE CROSS-COMPANY BUSINESS IMPROVEMENT

Bad volumes and

Duplicated activity

Complex Operating Model and Structures

Inefficient channels and limited online interactions

Under-leveraged

partnerships and vendors

Simplify

New Lean Operating

Model

A New Customer Focussed Culture

End-To-End Customer Process Improvement

Sales & Services Channel

Enhancements

Simplified Pricing

Third Party Spend & Productivity Improvement Program

Serve Save

Telstra before Project New Project New Focus Areas

Source: FY10 Investor day presentation

TELS

TRA

TEM

PLA

TE 4

X3

BLU

E B

ETA

| T

ELP

PTV

4

FROM FY11-FY13, WE REPORTED PRODUCTIVITY SAVINGS OF OVER $2.5B

In FY11 we reported OPEX Productivity Benefits of $0.6b ...

...in FY12 we reported $1.1b ...

... and $0.8b in FY13

Source: Telstra Investor Presentations

For

per

sona

l use

onl

y

TELS

TRA

TEM

PLA

TE 4

X3

BLU

E B

ETA

| T

ELP

PTV

4

OUR FOCUS HAS BEEN ON THREE KEY BUSINESS IMPROVEMENT AREAS

42%

32%

26%

FY11 - FY13 Total Benefits

Benefits FY11 – FY13

Structural Change

Service Improvements

Process, System, Network

Selected Measures FY11 – FY13

Service Improvements • TIO complaints reduced by 32%

• Consumer contact centre volumes reduced by 16% per SIO

• Bad debt expenditure reduced by 38%

• Error provisioning rate reduced by 62%

• Reduced number of suppliers by 33%

• Total cumulative sourcing / contracts savings of $1.1b

• Online billing has increased ten-fold to 2.5m a month

• Reduced headcount

• EBITDA contribution per FTE increased by 13%

Process, System, Network

Structural Change

TELS

TRA

TEM

PLA

TE 4

X3

BLU

E B

ETA

| T

ELP

PTV

4

FUTURE OPPORTUNITIES New Businesses – Improving profit of new businesses

• Adjust for global service ambitions

• Target the current labour and contractor cost

• Implement revised outsourcing arrangements

• Address NBN

Asset Effectiveness/Capital Efficiency – Improving investment and asset management

Service Improvement – Increasing self service and reduce failure cost

Structural Change - Adapting to global competition

• Improve margins on new and high growth businesses (e.g. NAS, International, Digital Media)

• Improve management of strategic and non-strategic assets across our $20b asset base

• Improve efficiency of investment in new assets

• Move to online self service model to reduce call volumes. 51m calls per annum currently received

• Reduce failure costs (e.g. error provisioning, assurance and network management ) of $2.3b

• Develop IP-based service delivery architecture

For

per

sona

l use

onl

y

TELS

TRA T

EM

PLATE 4

X3 B

LUE B

ETA

|

TELP

PTV4

Q&A

TELS

TRA T

EM

PLATE 4

X3 B

LUE B

ETA

|

TELP

PTV4

BUILD NEW GROWTH BUSINESSES BREAKOUT SESSIONS

For

per

sona

l use

onl

y

TELS

TRA T

EM

PLATE 4

X3 B

LUE B

ETA

|

TELP

PTV4

TELS

TRA T

EM

PLATE 4

X3 B

LUE B

ETA

|

TELP

PTV4

NETWORK APPLICATIONS & SERVICES REALISING OUR NAS OPPORTUNITY

NETWORK APPLICATIONS & SERVICES A PORTFOLIO OF ENTERPRISE & BUSINESS SERVICES

Single to fully integrated end to end solutions to achieve business objectives

Build Service Foundations

World class network infrastructure and network access foundations

1

3G/4G Mobile

Fixed & Broadband Networks

IP Networks

Internet Access

End To End Managed Networks

End-to-end management of mobile or data network, to agreed service levels

2

Managed Mobility

Data Centre

WLAN

LAN

Security

24 x 7 and end-to-end protection

3

Device Security

Security Apps

Network Security

Managed Security

Outsource Infrastructure

4

The freedom to focus on core business

Cloud / XaaS

Unified Comms & Collaboration

Industry Solutions

Integrate Your Workspace

Enable workforce mobility, collaboration & business functions.

5

Devices

Comms

Web services

Bus & Mobile Apps

Integrated Service Management

6

Online Portals & Reporting

Service Desks & Support

Profess’l Services

BYOD

Carriage (DIP) NAS products and services

For

per

sona

l use

onl

y

EXPAND service portfolio (Cloud, Mobility & Service Integration)

GROW VALUE

from existing offers

INTERNATIONAL Expansion

GROWING NAS CONTINUED FOCUS ON THREE KEY AREAS

Australia Asia-Pacific

Grow the core, expand offer roadmap and

GROW INTERNATIONALLY

OUR JOURNEY CONTINUED EVOLUTION

2011 2012 2013

Practices

Global Delivery Model

Digital Office Technology*

* Previously “Digital Business

Customer Delivery Unit

For

per

sona

l use

onl

y

STRONG REVENUE GROWTH ENHANCED CAPABILITIES

AUD $M

1,143 1,263 1,487

FY11 FY12 FY13

+11% +18%

DOMESTIC REVENUE GROWTH OF +18% ACHIEVEMENTS

Delivered record NAS sales and several major deal wins

Strengthened our Australian and Global delivery and operational capabilities

Delivering an improved customer service experience and NPS

Increasing focus on key growth areas such as Cloud Computing and expanding our portfolio of Services

Launched Practices to provide thought leadership to customers in a fast changing and complex market

Market-Leading NAS Capabilities

Strong International Presence

Continued Growth from Australia and Asia

For

per

sona

l use

onl

y

TELS

TRA T

EM

PLATE 4

X3 B

LUE B

ETA

|

TELP

PTV4

GROWTH OPPORTUNITIES IN ASIA MARTIJN BLANKEN TELSTRA INTERNATIONAL GROUP

TELS

TRA

TEM

PLA

TE 4

X3

BLU

E B

ETA

| T

ELP

PTV

4

DOUBLE-DIGIT REVENUE GROWTH OF 16% TO A$1.7B IN FY13 �����

CUSTOMER FOCUS

DRIVING VALUE FROM THE CORE

BUILD NEW GROWTH BUSINESSES

HIGHLIGHTS AND GROWTH STRATEGY

For

per

sona

l use

onl

y

TELS

TRA

TEM

PLA

TE 4

X3

BLU

E B

ETA

| T

ELP

PTV

4

TELSTRA CHINA

SOLIDIFY AUTOHOME’S LEAD AS #1 AUTOMOTIVE PORTAL AND MAXIMISE EQUITY VALUE OF CHINA MEDIA ASSETS

CHINA MEDIA ASSETS DELIVERED REVENUE GROWTH OF 22%

AUTOHOME REVENUE GREW BY 74%

IN CHINA TELSTRA GLOBAL SIGNED MULTIPLE STRATEGIC NETWORK DEALS

TELS

TRA

TEM

PLA

TE 4

X3

BLU

E B

ETA

| T

ELP

PTV

4

CSL

BROADEN MARKET LEADERSHIP WITH SUPERIOR CUSTOMER EXPERIENCE AND LEVERAGE LTE NETWORK AND SPECTRUM ADVANTAGE

#1 HONG KONG MOBILE OPERATOR IN SERVICE REVENUE AND EBITDA, WITH 17% REVENUE GROWTH

WORLD’S FIRST LTE ROAMING PACT

#1 IN HONG KONG WITH 3.9M CUSTOMERS, GAINED 425,000 CUSTOMERS IN FY13

OPERATES A DISTINCTIVE MULTI-BRAND STRATEGY THROUGH BRANDS 1O1O, ONE2FREE AND NEW WORLD MOBILITY

For

per

sona

l use

onl

y

TELS

TRA

TEM

PLA

TE 4

X3

BLU

E B

ETA

| T

ELP

PTV

4

TELSTRA GLOBAL

GROW GLOBAL CONNECTIVITY BUSINESS THROUGH INVESTMENTS, PORTFOLIO AND NAS EXPANSION, TARGETED SEGMENT FOCUS AND STRATEGIC CUSTOMER DEALS, UNDERPINNED BY A CUSTOMER-CENTRIC APPROACH

MILESTONE INTERNATIONAL NAS CONTRACT WITH JETSTAR

STRENGTHENED CLOUD OFFERINGS WITH DATA CENTRE IN SINGAPORE, CLOUD-ENABLED NODES IN SINGAPORE, HONG KONG AND LONDON

NEW LICENSES IN TAIWAN AND INDIA; 17 LICENSES WORLDWIDE

REVENUE GROWTH OF 9% IN FY13

NETWORK EXPANSION WITH OVER 1,400 POINTS-OF-PRESENCE IN 230 COUNTRIES AND TERRITORIES

TELS

TRA T

EM

PLATE 4

X3 B

LUE B

ETA

|

TELP

PTV4

TELSTRA HEALTH SHANE SOLOMON, HEAD OF HEALTH

For

per

sona

l use

onl

y

TELS

TRA

TEM

PLA

TE 4

X3

BLU

E B

ETA

| T

ELP

PTV

4

WHY IS TELSTRA ENTERING THE HEALTH INDUSTRY?

TOTAL HEALTH SYSTEM EXPENDITURE SET TO DOUBLE IN A DECADE

MAJOR SUSTAINABILITY CHALLENGES POINT TO NEED FOR eHEALTH SOLUTIONS

THE eHEALTH MARKET CONSISTS OF MANY VALUABLE BUT DISCONNECTED TECHNOLOGIES

TELS

TRA

TEM

PLA

TE 4

X3

BLU

E B

ETA

| T

ELP

PTV

4

CREATING A SAFER, EFFICIENT AND MORE CONVENIENT PHARMACY SYSTEM

IMPROVING INTEGRATION OF HEALTH INFORMATION

REDUCING HOSPITAL AND AGED CARE ADMISSIONS

PROVIDING CONSUMERS WITH GREATER CONTROL OF THEIR HEALTH & WELLNESS

INCREASING ACCESS TO HEALTHCARE REGARDLESS OF LOCATION

IMPROVING EFFICIENCY AND PRODUCTIVITY ACROSS THE HEALTH SYSTEM

TELSTRA WILL BE AT THE HEART OF THIS TRANSFORMATION

For

per

sona

l use

onl

y

TELS

TRA

TEM

PLA

TE 4

X3

BLU

E B

ETA

| T

ELP

PTV

4

WE WILL LEAD THE MARKET WITH A COMPLETE ECOSYSTEM BUILT THROUGH INVESTMENT & STRATEGIC PARTNERSHIPS

TELS

TRA

TEM

PLA

TE 4

X3

BLU

E B

ETA

| T

ELP

PTV

4

CREATING A SAFER, EFFICIENT AND MORE CONVENIENT PHARMACY SYSTEM

IMPROVING INTEGRATION OF HEALTH INFORMATION

REDUCING HOSPITAL AND AGED CARE ADMISSIONS

1,2. DOHA. 2012. PBS Trends in Expenditure and Prescriptions, 2011-12 | 3, 4. NEHTRA Annual Report, 2012 | 5. Average based on: Dilworth, S. 2009. A Literature Review: Readmission of Older Patients to the Acute Care Setting | 6. See for example: Medical Journal of Australia 2006: 184(8) | 7.Figures provided by Ontario Telemedicine Network

• Health service providers don’t have the information to know what other health professionals are doing for the patient

• Even hospitals mostly do not have a single patient record

• 1 in 6 hospital admissions run duplicate tests - pathology and radiology4

• 200 million PBS prescriptions per year in Australia1

• Approx.100 million Australian prescriptions are for routine repeat prescriptions of drug groups for chronic health conditions, e.g. cholesterol lowering2

• 1 in 5 medical errors due to incomplete patient information3

• Approx. 20% of elderly patients re-admitted to hospital within a month of discharge5

• ‘Frequent flyer’ patients consume 40% of health resources6

• Ontario achieved 70% reduction in ED attendances and 60% reduced hospitalisation through home monitoring and care co-ordination7

For

per

sona

l use

onl

y

TELS

TRA

TEM

PLA

TE 4

X3

BLU

E B

ETA

| T

ELP

PTV

4

PROVIDING CONSUMERS WITH GREATER CONTROL

INCREASING ACCESS TO SPECIALIST CARE IN RURAL AREAS

IMPROVING EFFICIENCY AND PRODUCTIVITY

8. Kaiser Permanente Annual Report 2012 | 9. Teladoc, National Healthcare Innovation Summit, 2013 | 10. MBS Item numbers report 2012-13 | 11. Figures provided by Ontario Telemedicine Network | 12. AIHW, Frost & Sullivan | 13. Generally agreed industry estimate. Example DOHA, 2007, ‘The use of SMS text messaging to improve outpatient attendance’

• 135 million doctor appointments each year – only 21,000 done through videoconferencing10

• Ontario Telemedicine Network saved $60 million in patient travel grants to people in rural areas through use of telehealth videoconferencing11

• Many health transactions can now be done online

• US insurer Kaiser Permanente, does 12m online consultations per year8

• US telehealth company Teladoc does 11,600 telehealth medical consultations per month9

• Health spending up from 8% GDP a decade ago to nearly 10% now, projected to reach 15% in next decade12

• 20% of public hospital outpatients are ‘no-shows’13

• While people can wait 2 years for an outpatient appointment in some hospitals

TELS

TRA

TEM

PLA

TE 4

X3

BLU

E B

ETA

| T

ELP

PTV

4

OUR INTEGRATED eHEALTH ECOSYSTEM AVAILABLE TO MILLIONS OF AUSTRALIANS

Telstra Health combines the trust of an iconic Australian brand with specialised expertise and capabilities in health care to bring an integrated eHealth ecosystem to millions of Australians:

• Our investments leverage experience in complex industries and infrastructure

• Our strategy builds on world-class capabilities in connectivity, technology and cloud

• We connect more households than any other in Australia

WHY TELSTRA WILL SUCCEED IN eHEALTH

For

per

sona

l use

onl

y

TELS

TRA T

EM

PLATE 4

X3 B

LUE B

ETA

|

TELP

PTV4

GLOBAL APPLICATIONS AND PLATFORMS CHARLOTTE YARKONI, EXECUTIVE DIRECTOR TELSTRA APPLICATIONS

TELS

TRA

TEM

PLA

TE 4

X3

BLU

E B

ETA

| T

ELP

PTV

4

By Marc Andreessen

WHY SOFTWARE IS EATING THE WORLD

80

THE SOFTWARE IMPERATIVE

For

per

sona

l use

onl

y

TELS

TRA

TEM

PLA

TE 4

X3

BLU

E B

ETA

| T

ELP

PTV

4

BUILDING A SOFTWARE BUSINESS KEY CHARACTERISTICS

• High margin at scale • Low CAPEX • High initial investment,

then very low marginal costs

• Multiple competitors initially, few will capture significant market share

• Talent-driven business • Requires sustained

commitment over time • Product development

different than IT-oriented solution development

• Ecosystem where partnerships are required with other parts of the value chain

FINANCIAL CULTURAL BUSINESS

TELS

TRA

TEM

PLA

TE 4

X3

BLU

E B

ETA

| T

ELP

PTV

4

APPLICATION GROWTH INITIATIVES

SCOPE OF ENGAGEMENT SCALE OF INVESTMENT

APPLICATIONS BUSINESS UNIT

Deal flow to Ventures

Follow on investments in Accelerator graduates

Incorporate Ventures investments into Applications

VENTURES

ACCELERATOR

Applications business unit identifies strategic areas of

interest

INTERRELATED ACTIVITIES

For

per

sona

l use

onl

y

TELS

TRA

TEM

PLA

TE 4

X3

BLU

E B

ETA

| T

ELP

PTV

4

GLOBAL APPLICATIONS AND PLATFORMS

A SOFTWARE BUSINESS UNIT THAT ADDRESSES THE SHIFT TOWARDS BUSINESSES AND INDUSTRIES BEING RUN ON SOFTWARE AND DELIVERED AS ONLINE SERVICES

RATIONALE • The future is in the software layer and

there is an application for absolutely everything.

• Enterprise orientation • Start in Australia but not limited to

Australia • Three year effort to build the unit • Operate like a start-up

OPPORTUNITY LANDSCAPE • Cloud-enabled software solutions • Digital entertainment • Software-as-a-Service • Mobile Internet • Internet of things • Big Data

TELS

TRA

TEM

PLA

TE 4

X3

BLU

E B

ETA

| T

ELP

PTV

4

• Window into technology leaders in Silicon Valley

• Accelerate Telstra’s roadmap • Increased vendor knowledge • Better market insights • Investment returns

TELSTRA VENTURES SERVES TELSTRA’S BUSINESS UNITS BY PROACTIVELY INVESTING IN MARKET LEADING, HIGH-GROWTH COMPANIES THAT ARE STRATEGICALLY RELEVANT TO TELSTRA

KEY BENEFITS FOR TELSTRA

VENTURES

CURRENT INVESTMENT PORTFOLIO

For

per

sona

l use

onl

y

TELS

TRA

TEM

PLA

TE 4

X3

BLU

E B

ETA

| T

ELP

PTV

4

MURU-D ACCELERATOR

• Standalone identity powered by Telstra • Applicants apply online for a 6-month

program • Help talent develop the business model and

business plan through world class mentoring and domain expertise

MURU-D PROVIDES LEADERSHIP IN ACCELERATING INNOVATION AND CREATIVITY FOR THE AUSTRALIAN DIGITAL ECONOMY TO CULTIVATE AUSTRALIAN DIGITAL TALENT SO THEY DON’T HAVE TO GO OFFSHORE TO SUPPORT THEIR INNOVATION

TM

TM

TELS

TRA T

EM

PLATE 4

X3 B

LUE B

ETA

|

TELP

PTV4

DIGITAL MEDIA RICK ELLIS, GROUP MANAGING DIRECTOR TELSTRA MEDIA GROUP

For

per

sona

l use

onl

y

TELS

TRA

TEM

PLA

TE 4

X3

BLU

E B

ETA

| T

ELP

PTV

4

• Massive growth in Smartphone penetration

• Almost 75% of Smartphone users accessing the internet daily on their device

• 50% of Smartphone users have a tablet

CHANGING CONSUMPTION PATTERNS

A MARKETPLACE READY FOR MEDIA GROWTH

THEN

• Video will account for 80% of global consumer data traffic by 2017

• And 66% of global mobile data traffic by 2017

CONSUMERS HAVE MORE POWER THAN EVER BEFORE

NOW

TELS

TRA

TEM

PLA

TE 4

X3

BLU

E B

ETA

| T

ELP

PTV

4

DELIVERING PREMIUM CONTENT BY PARTNERING LEADING BRANDS

For

per

sona

l use

onl

y

90

A better entertainment experience for each Australian, every day

Better viewing experience

Multiple platforms

True customer focus

Compelling, distinctive

content offering

Our vision

For

per

sona

l use

onl

y

Premium content

Best of Global Brands

Foxtel Networks

Compelling, distinctive content offering

[working title]

For

per

sona

l use

onl

y

iQ3 – The Entertainment Hub

‘Full’ Foxtel

Multiple platforms for different customer segments

Presto

Foxtel Play

Enga

gem

ent w

ith T

V

Price sensitivity For

per

sona

l use

onl

y

Foxtel Play

Entertainment Documentary Movies Kids Drama Sport

1 Pick: $25 2 Picks: $35 3 Picks: $45 4 Picks: $50 1 Pick: $25 2 Picks: $50

Build your own entertainment pack Add premium packs

Bonus (included with every package) Complimentary access to All picks for $100

Presto – a new way for Australians to access movies

• An online entertainment subscription service targeting movie lovers, with access to movie content delivered over the internet across a range of devices

• Live & On Demand access to the biggest box office releases of 2012 at launch and all 7 live Foxtel Movies channels.

• Monthly pass to stream Foxtel Movies with no lock-in contract.

• Launching late 2013 on PC, MAC, iOS and Android tablets

Presto. Powered by Foxtel

For

per

sona

l use

onl

y

Investing in customer service

Digital Advocacy

Driving customer advocacy

For

per

sona

l use

onl

y