Letter to Shareholders: FY 2020

25

/

Transcript of Letter to Shareholders: FY 2020

/

Letter to Shareholders: FY 2020

2

Key annual metrics:

Direct Contribution ($m)

Letter to Shareholders: FY 2020

3

Dear Shareholders,

2020 was an unprecedented year by any measure. The first global pandemic in over 100 years profoundly

disrupted the world economy. Increasing social unrest and political instability at home and abroad as the year

progressed amplified the economic uncertainty and the powerful consumer and business headwinds that

began surfacing the world over in the first quarter of 2020. Together, these dynamics resulted in the most

volatile and unpredictable global economic environment in many decades.

Against this challenging backdrop, I am extremely pleased to report that Root finished 2020 stronger and

better positioned to achieve our ambitions of profitably growing our business, continuing to disrupt the

traditional insurance industry, and delivering consistent, long-term value creation for our shareholders.

A few highlights of Root’s FY 2020:

• We grew our Direct Written Premium by 37% to $617 million, despite intentionally throttling back

marketing spend after the pandemic emerged

• We improved our Direct Accident Period Loss Ratio by a full 26 points year-over-year, with only

roughly six points of the improvement attributable to reduced driving due to the pandemic

• We launched our new proprietary loss cost model (or pricing algorithm) and an updated version of our

telematics model, UBI 3.0+, which are together driving considerable loss ratio improvements and have

now been approved by regulators in 20 states

• We became a publicly held company, welcoming new shareholders to the Root family and raising over

$1 billion of proceeds to continue to fuel our future growth

As much progress as we made in 2020, we realize we still have much work to do in the quarters and years

ahead, particularly around improving customer retention, managing customer acquisition costs, and driving

continued improvement in loss ratios. And our teams are laser-focused on delivering meaningful improvement

in each of these areas. In the pages that follow, we lay out our roadmap for success, and Dan and I will provide

additional details on our earnings call today at 5 p.m. ET. We hope you can join us for the call.

We targeted the personal auto insurance sector as the first insurance segment to disrupt for

two compelling reasons:

Letter to Shareholders: FY 2020

4

1. The market is massive–$266 billion in annual premiums in the U.S. alone–and is a mandated purchase

in most jurisdictions.

2. The data is clear that consumers have traditionally been very dissatisfied with their car insurance

experience, describing it as complicated, confusing, unwieldy, and as pleasurable as a trip

to the dentist.

Given these dynamics and the tech-driven shifts in consumer behavior across industries occurring over the last

decade, a revolution in the auto insurance industry was inevitable. Today, consumers are calling out for ease,

fairness, and price transparency to supplant the “black box” model of the last 100+ years. And we believe that

in the years ahead, conventional insurance carriers with antiquated or non-existent tech stacks and those for

whom delivering an “elevated customer experience” is more marketing slogan than core value will be

marginalized or left behind entirely.

Root believes that with our proprietary telematics and clean technology stack, we can deliver uniquely

customized underwriting accuracy, reduced premiums, and a vastly better auto insurance purchase experience

for our target consumer audience. Over time, these factors will enable us to win in the marketplace and drive

revenues and profits by attracting and retaining high-quality customers in an industry typically characterized

by price opaqueness and customer disappointment.

Building a disruptive insurance business that will win over the next 100 years requires determination,

foresight, innovation, and investment. Root is committed to all four. None of us believed that achieving scale in

a market characterized by entrenched, legacy operators spending billions of marketing dollars would occur

overnight. But we are more convinced than ever that with approved licenses in 36 states, proprietary data, and

data science second to none all sitting atop a clean technology stack, Root is ideally positioned to further

leverage its first-mover advantage.

Proprietary data and machine learning are enabling us to build a better business and contribute to building a

better and fairer world. Whether relying on credit scores, education history, or occupation, it’s an open secret

that the variables used in pricing auto insurance today disproportionately and unfairly impact those who can

least afford insurance, perpetuating a vicious cycle of financial hardship.

Letter to Shareholders: FY 2020

5

Root is committed to addressing this unfairness by empowering consumers and leveling the playing field.

We will continue to invest in a range of initiatives—grassroot, marketing, and regulatory—to eliminate

these unfair and discriminatory practices from the industry.

It will take time and investment to change the status quo, no doubt, but we are committed to improving

insurance pricing and practices and the overall insurance customer experience. Root will never be about talking

animals or funny commercials. The Root brand will always be an authentic brand, committed to our values and

our customers. You will see continued brand investment in the quarters and years ahead. And if you haven’t

done so already, please check out Root’s groundbreaking partnership with Bubba Wallace at

https://www.joinroot.com/progress/.

While we still have much work to do, we are passionate and confident about our future. Root occupies a unique

and increasingly relevant position in the personal insurance market. We are a disruptive player in an enormous

global market, where technology, innovation, and data drive our business and our people to improve every day.

With our mobile customer experience and proprietary algorithms, we have developed a better model that will

only continue to improve and create further separation from competitors.

Every piece of data improves our pricing ability. Every customer who uses our app or website delivers valuable

insights to make our interfaces better for the next customer. Ours is not the typical insurance industry

mindset. We believe that by continuing to disrupt and focusing on the long term, Root will become the

industry-defining platform, built to last.

We look forward to continuing our journey with our customers, employees, and investors, and we are

grateful for the confidence and support you have shown us.

With gratitude,

Letter to Shareholders: FY 2020

6

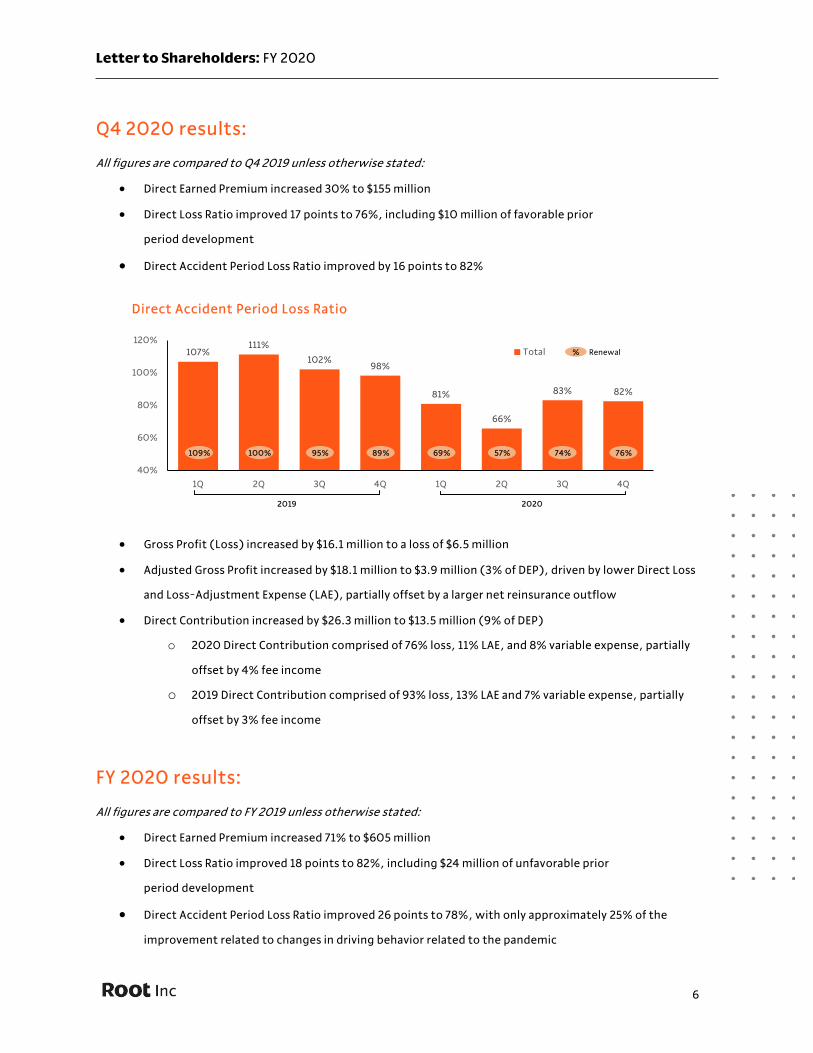

Q4 2020 results:

All figures are compared to Q4 2019 unless otherwise stated:

• Direct Earned Premium increased 30% to $155 million

• Direct Loss Ratio improved 17 points to 76%, including $10 million of favorable prior

period development

• Direct Accident Period Loss Ratio improved by 16 points to 82%

• Gross Profit (Loss) increased by $16.1 million to a loss of $6.5 million

• Adjusted Gross Profit increased by $18.1 million to $3.9 million (3% of DEP), driven by lower Direct Loss

and Loss-Adjustment Expense (LAE), partially offset by a larger net reinsurance outflow

• Direct Contribution increased by $26.3 million to $13.5 million (9% of DEP)

o 2020 Direct Contribution comprised of 76% loss, 11% LAE, and 8% variable expense, partially

offset by 4% fee income

o 2019 Direct Contribution comprised of 93% loss, 13% LAE and 7% variable expense, partially

offset by 3% fee income

FY 2020 results:

All figures are compared to FY 2019 unless otherwise stated:

• Direct Earned Premium increased 71% to $605 million

• Direct Loss Ratio improved 18 points to 82%, including $24 million of unfavorable prior

period development

• Direct Accident Period Loss Ratio improved 26 points to 78%, with only approximately 25% of the

improvement related to changes in driving behavior related to the pandemic

Direct Accident Period Loss Ratio

2019 2020

107%111%

102%98%

81%

66%

83% 82%

40%

60%

80%

100%

120%

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q

Total

109% 100% 76%74%57%69%89%95%

% Renewal

Letter to Shareholders: FY 2020

7

1. Proprietary segmentation: improved risk segmentation in pricing through telematics UBI model and pricing algorithm

2. State management: state-level pricing and underwriting adjustments

3. Tenure mix: impact to blended loss ratio from proportion of premium in each term tenure, loss ratio improves with each subsequent term,

with largest impact first term to first renewal

4. COVID-19: exposure associated with COVID-19

• Gross Profit (Loss) increased by $69.3 million to a loss of $14.2 million

• Adjusted Gross Profit increased by $75.2 million to $21.0 million (3% of DEP), driven by lower Direct

Loss and LAE and a net reinsurance inflow from higher ceding commissions

• Direct Contribution increased by $76.3 million to $18.9 million (3% of DEP)

o 2020 Direct Contribution comprised of 82% loss, 10% LAE and 8% variable expense, partially

offset by 3% fee income

o 2019 Direct Contribution comprised of 100% loss, 12% LAE and 7% variable expense, partially

offset by 3% fee income

2020 Direct Accident Period Loss Ratio improvement

104%

78%

-8%-7%

-5%-6%

2019Loss ratio

Proprietarysegmentation

Statemanagement

Tenuremix

COVID-19 2020Loss ratio

Letter to Shareholders: FY 2020

8

Telematics and data science advantage

In the auto insurance business, price is king. It has traditionally been the #1 reason a consumer selects or rejects

an auto insurance product. We are focused on driving better and more accurate pricing by continuing to scale

our data sets and by constantly improving our pricing algorithms. As we get better at segmenting risk, we grow

faster, create highly satisfied, loyal customers, and drive a profitable business.

Accurate pricing has always been at the core of Root’s mission. We believe the rapid and dramatic

transformation of data and machine learning will result in increasingly more informed underwriting models.

Pricing improvements, however, take time to be approved by regulators and earn through our book.

We believe that Root’s proprietary data science-driven telematics and pricing algorithm models are superior to

competitive models, given the predictive power of our telematics and our ability to correlate variables in the

pricing algorithm. Carriers that source a UBI score from a third party are disadvantaged because they are limited

to layering in predefined scores on top of a preexisting pricing model, vastly reducing the model’s power and

effectiveness. Competitor models also lack our integrated claims experience data—data that meaningfully

improves the quality of our telematics.

Internally developing our telematics and pricing algorithms also enables us to move much more quickly than

competitors to iterate on our proprietary models. As a result and for context, while many top-20 carriers have

a material loss cost model refresh every 3–5 years, if not longer, we routinely change pricing and fine-tune our

models, with a complete rebuild of our pricing algorithms on average every nine months. And each successive

iteration enables us to deliver meaningful loss-prediction improvements.

To isolate the long-term benefits of our proprietary technologies and demonstrate the improvements they are

driving, we have created a metric of seasoned states. A seasoned state is defined as a state where (1) the

regulator has approved our data science-driven telematics and pricing models and (2) we have been writing

policies in the state for a minimum of one year with a minimum of two pricing filings.

Applying the above criteria, at the start of 2020 Root had only three states that were “seasoned,” but by the

end of 2020, that figure had increased to 20 states. As a result, our percentage of earned premium written in

seasoned states increased throughout the year, totaling 60% in the second half of 2020 compared to 18% in

the first half of 2020. Most importantly and as expected, our loss ratio in seasoned states was 15 points below

unseasoned states during the second half of 2020, demonstrating the impact of our iterative improvements in

Letter to Shareholders: FY 2020

9

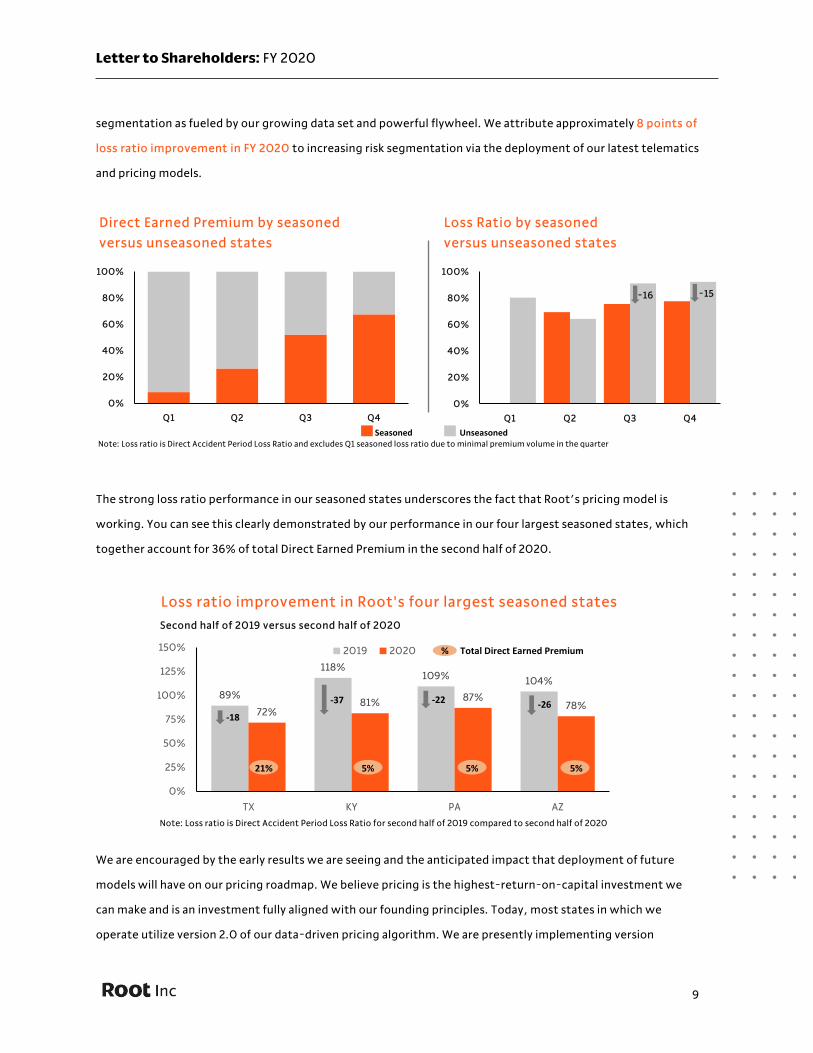

segmentation as fueled by our growing data set and powerful flywheel. We attribute approximately 8 points of

loss ratio improvement in FY 2020 to increasing risk segmentation via the deployment of our latest telematics

and pricing models.

The strong loss ratio performance in our seasoned states underscores the fact that Root’s pricing model is

working. You can see this clearly demonstrated by our performance in our four largest seasoned states, which

together account for 36% of total Direct Earned Premium in the second half of 2020.

We are encouraged by the early results we are seeing and the anticipated impact that deployment of future

models will have on our pricing roadmap. We believe pricing is the highest-return-on-capital investment we

can make and is an investment fully aligned with our founding principles. Today, most states in which we

operate utilize version 2.0 of our data-driven pricing algorithm. We are presently implementing version

Direct Earned Premium by seasoned Loss Ratio by seasonedversus unseasoned states versus unseasoned states

Note: Loss ratio is Direct Accident Period Loss Ratio and excludes Q1 seasoned loss ratio due to minimal premium volume in the quarter

0%

20%

40%

60%

80%

100%

Q1 Q2 Q3 Q40%

20%

40%

60%

80%

100%

Q1 Q2 Q3 Q4Seasoned Unseasoned

-15-16

Loss ratio improvement in Root's four largest seasoned statesSecond half of 2019 versus second half of 2020

Note: Loss ratio is Direct Accident Period Loss Ratio for second half of 2019 compared to second half of 2020

89%

118%109% 104%

72%81% 87%

78%

0%

25%

50%

75%

100%

125%

150%

TX KY PA AZ

2019 2020 % Total Direct Earned Premium

-18

-37 -22 -26

21% 5% 5% 5%

Letter to Shareholders: FY 2020

10

3.0+, with version 4.0 deep into development and expected to be commercialized later in 2021. Likewise, our UBI 4.0 telematics model is targeted to be rolled out in a similar timeframe. Each UBI model update has

delivered meaningful improvements in predictive power and segmentation, a trend we fully expect to continue into the future.

The “Insur” in InsurTech

Risk segmentation is only one part of the insurance pricing architecture. While our telematics model is

developing as anticipated, other rating variables add value to the equation. With each state overseeing

regulation of insurance, nearly every state has its own pricing regulations and critical trends that impact

loss cost.

To address this, we launched a team in 2020 whose focus is managing the nuances of each individual state. And

over the course of the year, our new team filed 33 rate changes in existing states, while also launching in one

new state. While that may be “off the charts” in comparison to mature industry incumbents, for a young,

disruptive auto insurer rolling out new segmentation models every nine months, this performance underscores

our ability to deploy learnings quickly and our commitment to improving the consumer experience in order to

build a loyal and profitable customer base. And the results speak for themselves, with approximately 7 points

of loss ratio improvement in 2020 attributable to our new state management initiatives and the distribution

of state loss ratios transformed versus 2019.

As discussed on our Q3 2020 earnings call, last November we acquired a shell underwriting entity with 48

personal auto state licenses, enabling us to expand into new states with materially reduced regulatory hurdles.

Loss ratio distribution by state

Note: based on Direct Accident Period Loss Ratio

23

12

5

34

2

87

8

5

'19 '20 '19 '20'19 '20 '19 '20 '19 '20 '19 '20 '19 '20 '19 '20

<60% >120%60-69% 70-79% 80-89% 90-99% 100-109% 110-119%

Letter to Shareholders: FY 2020

11

Also last year, we shared a plan to fully leverage that acquisition in order to operate nationally by the end of

2021. We recently revisited that plan and are now targeting the addition of regulatory approval in seven new

states in 2021 for a total of 37 states representing 85% of the U.S. addressable market by year’s end. You will

see the impact of this strategic decision reflected in our 2021 top-line and unit economic guidance.

While our growth ambitions for 2021 remain high, given recent learnings and the meaningful benefits we are

driving in seasoned states, we have decided to focus and sequence our expansion investments on states where

our pricing and telematics models have already been approved by the regulator, as opposed to launching all

states simultaneously. Our seasoned state cohort analysis reinforces that our business works best when the

state regulator approves our pricing models and we incorporate learnings from prior states. Thus, while we

remain fully committed to building a nationwide footprint, over the next quarters we will be focusing our

capital and resources on accelerating growth, improving operations, and prioritizing regulatory efforts in our

expanding market. Thereafter, our strategy when launching a new state will be to have our pricing model

approved and tested in the state before investing heavily to drive customer acquisition. Once we know the unit

economics are sound and supported, we will quickly and efficiently ramp marketing spend to drive growth.

We are confident that, in time, we will be able to shorten the new state entry process given our learnings

with existing states.

Growth and profitability

As a management team, we regularly focus on the balance between growth and profitability. Growth

generates valuable data, creating a natural moat around our business, widening our lead over competitors, and

feeding our flywheel because more data leads to better pricing, which drives faster growth and even more

data. Growth makes us smarter, and with each new learning, we create better products and better prices.

But we are very mindful of the importance of throttling ,up or down, the capital we are deploying to fuel our

growth based on exigent circumstances. For example, in 2020, given the macro-economic and regulatory

uncertainty resulting from COVID-19, we made the decision to selectively throttle back on our

marketing spend.

As we reaccelerate marketing investments in 2021, we are focusing on driving sustainable growth and

delivering sustainable profit in those markets where we have implemented our proven models, while

continuing to test in markets that we believe will drive profitable future growth. New investments in 2021 will

include targeted new state expansion, new product launches, and expansion of marketing channels. And while

Letter to Shareholders: FY 2020

12

our 2021 investments may cause near-term fluctuations in our KPIs and results, we believe these investments

are appropriate and will ultimately increase our long-term returns and shareholder value.

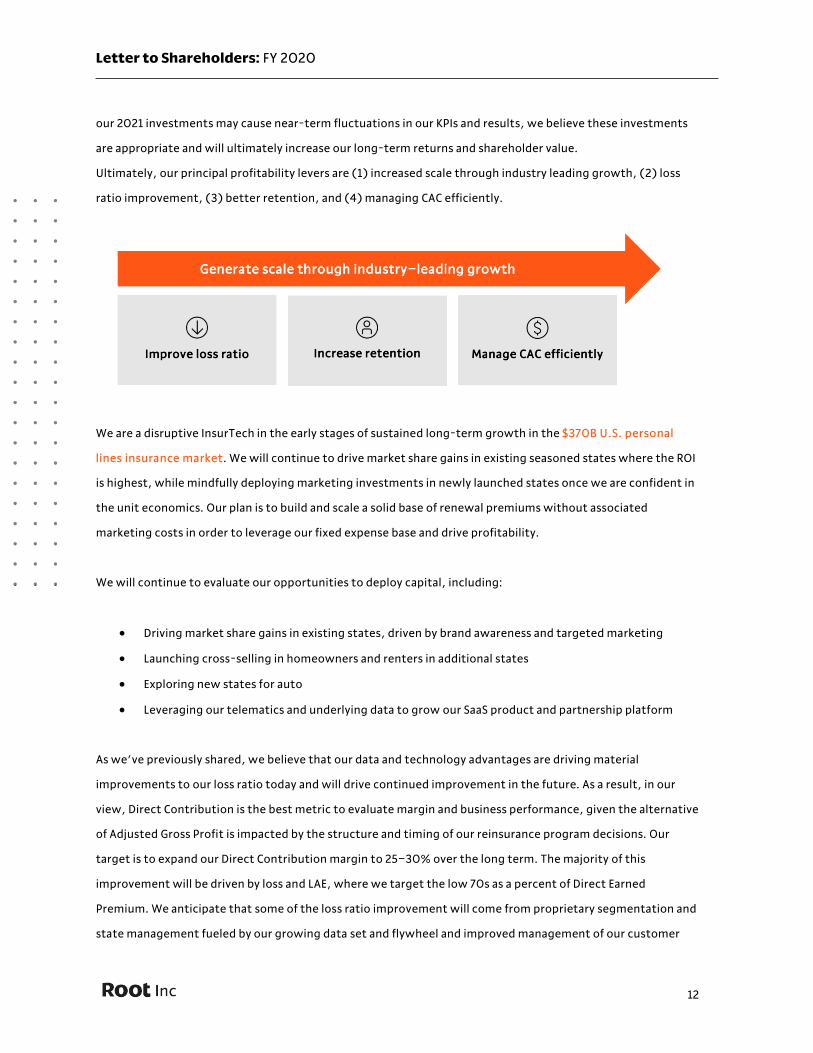

Ultimately, our principal profitability levers are (1) increased scale through industry leading growth, (2) loss

ratio improvement, (3) better retention, and (4) managing CAC efficiently.

We are a disruptive InsurTech in the early stages of sustained long-term growth in the $370B U.S. personal

lines insurance market. We will continue to drive market share gains in existing seasoned states where the ROI

is highest, while mindfully deploying marketing investments in newly launched states once we are confident in

the unit economics. Our plan is to build and scale a solid base of renewal premiums without associated

marketing costs in order to leverage our fixed expense base and drive profitability.

We will continue to evaluate our opportunities to deploy capital, including:

• Driving market share gains in existing states, driven by brand awareness and targeted marketing

• Launching cross-selling in homeowners and renters in additional states

• Exploring new states for auto

• Leveraging our telematics and underlying data to grow our SaaS product and partnership platform

As we’ve previously shared, we believe that our data and technology advantages are driving material

improvements to our loss ratio today and will drive continued improvement in the future. As a result, in our

view, Direct Contribution is the best metric to evaluate margin and business performance, given the alternative

of Adjusted Gross Profit is impacted by the structure and timing of our reinsurance program decisions. Our

target is to expand our Direct Contribution margin to 25–30% over the long term. The majority of this

improvement will be driven by loss and LAE, where we target the low 70s as a percent of Direct Earned

Premium. We anticipate that some of the loss ratio improvement will come from proprietary segmentation and

state management fueled by our growing data set and flywheel and improved management of our customer

Letter to Shareholders: FY 2020

13

funnel and test drive experience. The remaining improvement will come from our maturing book (positive

tenure mix), with more policies in later terms producing lower loss ratios.

Our blended loss ratio will gradually improve over time as we season additional states, iterate future UBI and

pricing models, build our renewal premium base, and reduce the pre-telematics loss ratio. This last point is a

unique element of our business model: to seek out lower-risk drivers and retain them as customers.

We identify low-risk drivers during the test drive, which for some customers happens after an initial policy

bind, subject to a price adjustment during their underwriting period to reflect their driving risk. We can

improve our pre-telematics loss ratio by iterating on our traditional underwriting variables and more efficiently

managing the test drive to quickly eliminate the highest-risk drivers. We have made progress in reducing the

impact of the pre-telematics period over the past two years. Pre-telematics loss ratios are approximately 20

points higher than post-telematics loss ratios, and we are continuing to identify and target opportunities for

further improvement.

Our reduction in marketing spend in Q2 2020 slowed our growth in the second half of 2020 and dramatically

increased our proportion of renewal premiums. We estimate that this positive tenure mix drove approximately

5 points of improvement on the loss ratio in 2020. As we resume marketing spend levels and reaccelerate

growth in 2021, the proportion of renewal premiums should drop back below 50% by the end of 2021, having a

negative tenure mix impact on loss ratio versus 2020. Over the long term, as we build the base of renewal

premiums in the book and our scale increases, the proportion of premiums from renewal terms will build again.

Direct Contribution

Note: Other includes LAE and variable cost efficiencies as well as fee income expansion driven by increasing cross-sell and our SaaS Enterprise product

3%

Current Long-termtarget

25-30%

Tenuremix

OtherProprietary pricingmodel

Letter to Shareholders: FY 2020

14

The final approximately 6 points of positive impact on the loss ratio in 2020 was related to the claims

frequency reduction associated with COVID-19. As stated previously, we saw a pronounced impact on driving

behavior in the period of March–May 2020, driving 15 to 17 points of loss ratio benefit for that period. We saw

varying trends in the second half of the year by state and month, with some pronounced reduction in

November, but overall a minimal impact in the second half. Our footprint drove these results, in part, as we are

not actively writing in high-commuting states that had extended COVID-19 restrictions such as California,

New York, New Jersey, and Massachusetts. We are monitoring operations closely to determine if we will see a

complete reversion to pre-pandemic driving behavior or if recent dynamics represent a new normal.

While we see a clear path to increasing direct contribution, we are equally focused on driving retention

improvements to extend this contribution margin for multiple years across our customer base. Root is a new

auto insurance product market entrant that understandably will not yet have the retention levels of a legacy

carrier with decades-long customers in its base. Core to our business model is a disruptive technology and an

underwriting model that will deliver lower prices to consumers and value to shareholders by entirely avoiding

or actively culling the worst drivers from our customer base.

That said, our management team is succeeding in reducing churn and increasing customer retention by:

• Reducing price volatility: Our unique ability to fine-tune our pricing with regularity can cause short-

term noise for some consumers, particularly at renewal in unseasoned states. We remain focused on

the long-term learnings in our pricing algorithms, and we are working to reduce short-term pricing

volatility for our existing customers

• Boomerang: Among Root’s major advantages over competitors is our widely distributed mobile app.

If a customer leaves Root, they generally continue to retain our mobile app on their device, and

Renewal premium % of Direct Earned Premium

2019 2020 2021E

0%10%20%30%40%50%60%70%80%

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q

Letter to Shareholders: FY 2020

15

tapping on that app is the path of least resistance to get reinsured. Last year, we invested in a product

feature called Boomerang, which allows customers to quickly reinstate themselves as policyholders

within a few button taps. Since launch, more than 21,000 customers have reinstated their policies,

adding $18.7M in DWP. We plan to expand this functionality to more customers in the coming months

• Bundling: As we expand home and renters product throughout our footprint, we will drive retention

through deeper customer relationships and the ability to attract more longer-retaining customers

who wish to bundle into our funnel

• Attracting better drivers: Much of retention comes down to price. We know that better drivers retain

longer with Root. As our loss and telematics model updates feed our flywheel with better pricing for

better drivers, it will lead to improved retention

• Improving the customer experience: We are focused on constantly elevating our customer experience

and recently promoted Hemal Shah into our Chief Product Officer role. Hemal joined Root in 2019

following product roles at Instagram, Facebook, and Twitter. He is taking ownership of retention, and

his team will build products designed to add value to our customers and increase their engagement

• Improving claims processing: We are making significant strides in claims automation and in applying

advanced machine learning techniques to estimate loss expense, which will allow us to pay out claims

faster, driving higher customer satisfaction and reducing claims severity

Letter to Shareholders: FY 2020

16

• Targeting our marketing: While we plan for an elevated level of churn associated with our business

model of underwriting out those drivers we view as disproportionately high risk, we will reduce this

particular impact over time by identifying good driver characteristics and attracting more of the right

customer segments into the top of our funnel

We expect that retention will improve steadily in the quarters and years ahead. Of note, because we typically

write 6-month policies, recently introduced products and underwriting fixes tend not to have immediate-term

impact on customer retention metrics.

We see a clear path to significantly expanding customer lifetime value (LTV) through improved pricing and

customer retention. Our goal is to maintain CAC at historic levels while we scale the business significantly. To

manage CAC while scaling, we will continue to build our advantage in mobile and partnership channels while

establishing new demand generation channels. We are simultaneously increasing our brand investment to drive

CAC efficiency in all channels as awareness grows. And we will continue to leverage our data science capabilities

to drive target customer mix and optimize spend across channels. Increased awareness of our pricing

advantage will both accelerate our growth and meaningfully improve our customer acquisition efficiency.

We are confident our data science and technology advantage, our team, and the maturation of our book

will generate a lifetime value return significantly in excess of our customer acquisition costs.

Letter to Shareholders: FY 2020

17

Guidance

Our current outlook for FY 2021 is as follows:

• Direct Written Premium in the range of $805–$855 million

• Direct Earned Premium in the range of $685–$715 million

• GAAP Total Revenue in the range of $270–$300 million

• Direct Contribution in the range of $25–$35 million

• Operating Income in the range of $(555)–$(505) million

Our guidance is based upon the following:

• Marketing spend: As outlined, we plan to more than double sales and marketing investments in 2021

following a COVID-driven pullback last year

• Growth: While our modified approach to state expansion in 2021 has deferred some of our written

premium growth to 2022 we are still targeting significant growth acceleration during the year

• Inflation: The auto insurance market historically has annual embedded price increases. Our guidance

does not include any inflation assumption in 2021 given the uncertainty around COVID-19 and our

competitor pricing levels

• Retention: We may experience areas of increased customer churn as we implement our pricing and

telematics models in unseasoned states

• Loss ratio: Importantly, our state expansion adjustment allows us to improve our expected Direct Loss

Ratio outlook (and Direct Contribution) for the year as we reduce the impact of new, unseasoned

states on our loss performance. Our 2021 guidance does not assume any material impact from COVID-

19, whereas we believe that 2020 included ~6 points of annualized loss ratio improvement related to

the pandemic

• Reinsurance: Due to positive loss ratio trends, we elected to postpone extension of our January 1

treaty until April 1, when we expect to obtain superior terms. We believe this will drive higher GAAP

Total Revenue as we retain more premium in the first half, but it has a negative impact on Operating

Income due to reduced ceding commissions

Root is a long-term-focused company and management team, and we are just getting

started. We look forward to transparent and active engagement with our investors and

keeping you updated on our progress as we continue this exciting journey together.

Letter to Shareholders: FY 2020

18

Non-GAAP financial measures

This letter and statements made during the above referenced webcast may include information relating to

Adjusted Gross Profit (Loss) and Direct Contribution, which are "non-GAAP financial measures." These non-

GAAP financial measures have not been calculated in accordance with generally accepted accounting principles

in the United States, or GAAP, and should be considered in addition to results prepared in accordance with

GAAP and should not be considered as a substitute for, or superior to, GAAP results.

In addition, Adjusted Gross Profit (Loss) and Direct Contribution should not be construed as indicators of our

operating performance, liquidity, or cash flows generated by operating, investing and financing activities, as

there may be significant factors or trends that they fail to address. We caution investors that non-GAAP

financial information, by its nature, departs from traditional accounting conventions. Therefore, its use can

make it difficult to compare our current results with our results from other reporting periods and with the

results of other companies.

Our management uses these non-GAAP financial measures, in conjunction with GAAP financial measures, as an

integral part of managing our business and to, among other things: (1) monitor and evaluate the performance

of our business operations and financial performance, (2) facilitate internal comparisons of the historical

operating performance of our business operations, (3) facilitate external comparisons of the results of our

overall business to the historical operating performance of other companies that may have different capital

structures and debt level, (4) review and assess the operating performance of our management team, (5)

analyze and evaluate financial and strategic planning decisions regarding future operating investments,

and (6) plan for and prepare future annual operating budgets and determine appropriate levels of

operating investments.

We have not reconciled Adjusted Gross Profit (Loss) and Direct Contribution outlook to GAAP Gross Profit

(Loss) because we do not provide an outlook for GAAP Gross Profit (Loss) due to the uncertainty and potential

variability of factors used to calculate GAAP Gross Profit (Loss). Because we cannot reasonably predict such

items, a reconciliation of the non-GAAP financial measure outlook to the corresponding GAAP measure is not

available without unreasonable effort. We caution, however, that such items could have a significant impact on

the calculation of GAAP Gross Profit (Loss).

For more information regarding the non-GAAP financial measures discussed in this release, please see “Non-

GAAP financial measures” and “Reconciliation of GAAP to non-GAAP financial measures” below.

Letter to Shareholders: FY 2020

19

Forward-looking statements

This letter contains—and statements made during the above-referenced webcast will contain—forward-

looking statements relating to, among other things, the future performance of Root and its consolidated

subsidiaries that are based on Root’s current expectations, forecasts, and assumptions and involve risks and

uncertainties. These include, but are not limited to, statements regarding:

• Our expected financial results for 2021

• Our ability to retain existing customers, acquire new customers and expand our customer reach

• Our ability to remove the use of credit score from our rating variables no later than 2025

• Our expectations regarding our future financial performance, including Total Revenue, Gross Profit

(Loss), Adjusted Gross Profit (Loss), Direct Contribution, Direct Loss Ratio, marketing costs and costs

of customer acquisition, direct LAE ratio, quota share levels and expansion of our renewal premium

base

• The impact of the COVID-19 pandemic on our business and financial performance

• Our goal to be licensed in all states in the United States and the timing of obtaining additional licenses

and launching in new states

• The accuracy and efficiency of our telematics and behavioral data, and our ability to gather and

leverage additional data

• Our ability to materially improve retention rates

• Our ability to release new products and features and the timing of those releases, including our new

Algorithm Version 4.0

• Our ability to underwrite risks accurately and charge profitable rates

• Our ability to drive improved conversion and decrease the costs of customer acquisition

• Our ability to operate a “capital-light” business and obtain and maintain reinsurance contracts

• Our ability to realize economies of scale and grow margins

• Our ability to expand our distribution channels through additional partnership relationships, digital

media, and referrals

• Our ability to protect our intellectual property and any costs associated therewith

• Our ability to expand domestically and internationally

Root’s actual results could differ materially from those predicted or implied by such forward-looking

statements, and reported results should not be considered as an indication of future performance.

Letter to Shareholders: FY 2020

20

Factors that could cause or contribute to such differences also include, but are not limited to, those

factors that could affect Root’s business, operating results, and stock price included under the captions

“Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of

Operations” in Root’s Registration Statement on Form S-1, our Quarterly Report on Form 10-Q, or Annual

Report on Form 10-K at http://ir.joinroot.com or the SEC’s website at www.sec.gov.

Undue reliance should not be placed on the forward-looking statements in this letter or the above-

referenced webcast, which are based on information available to Root on the date hereof. Such forward-

looking statements do not include the potential impact of any acquisitions or divestitures that may be

announced and/or completed after the date hereof. We assume no obligation to update such statements.

Letter to Shareholders: FY 2020

21

Financial statements

Letter to Shareholders: FY 2020

22

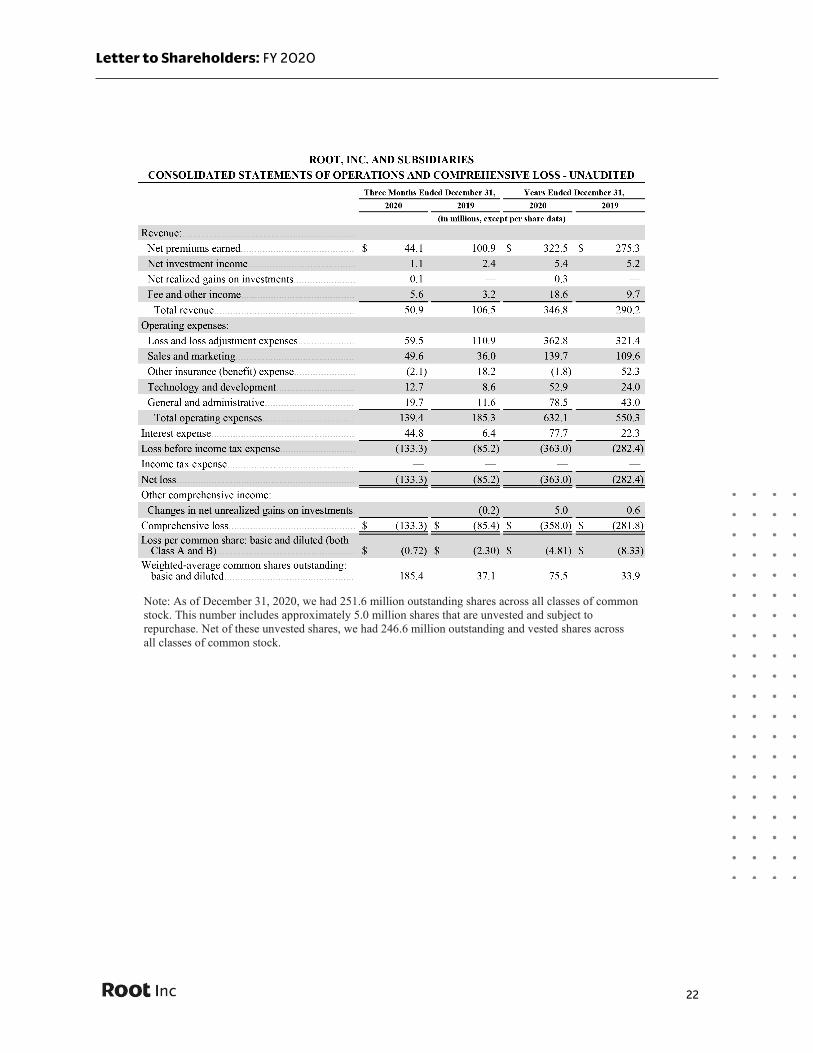

Note: As of December 31, 2020, we had 251.6 million outstanding shares across all classes of common stock. This number includes approximately 5.0 million shares that are unvested and subject to repurchase. Net of these unvested shares, we had 246.6 million outstanding and vested shares across all classes of common stock.

Letter to Shareholders: FY 2020

23

Letter to Shareholders: FY 2020

24

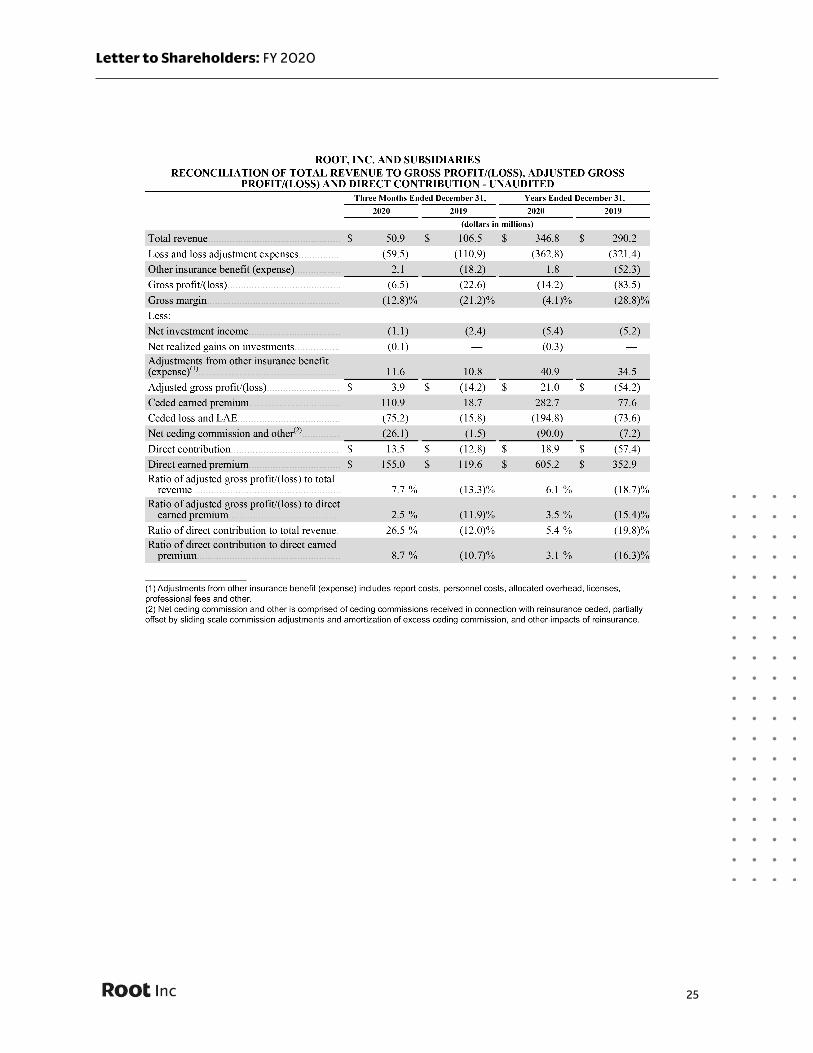

Supplemental financial information

Letter to Shareholders: FY 2020

25