Lesson 1 Financial Instruments Bonds Institute of Economic Studies Faculty of Social Sciences...

13

Lesson 1 Essentials of bond pricing Financial Instruments Bonds Institute of Economic Studies Faculty of Social Sciences Charles University in Prague

-

Upload

ellen-lyons -

Category

Documents

-

view

214 -

download

0

Transcript of Lesson 1 Financial Instruments Bonds Institute of Economic Studies Faculty of Social Sciences...

Lesson 1

Essentialsof bond pricing

Financial Instruments

Bonds

Institute of Economic StudiesFaculty of Social SciencesCharles University in Prague

Essentials of bond pricing 2

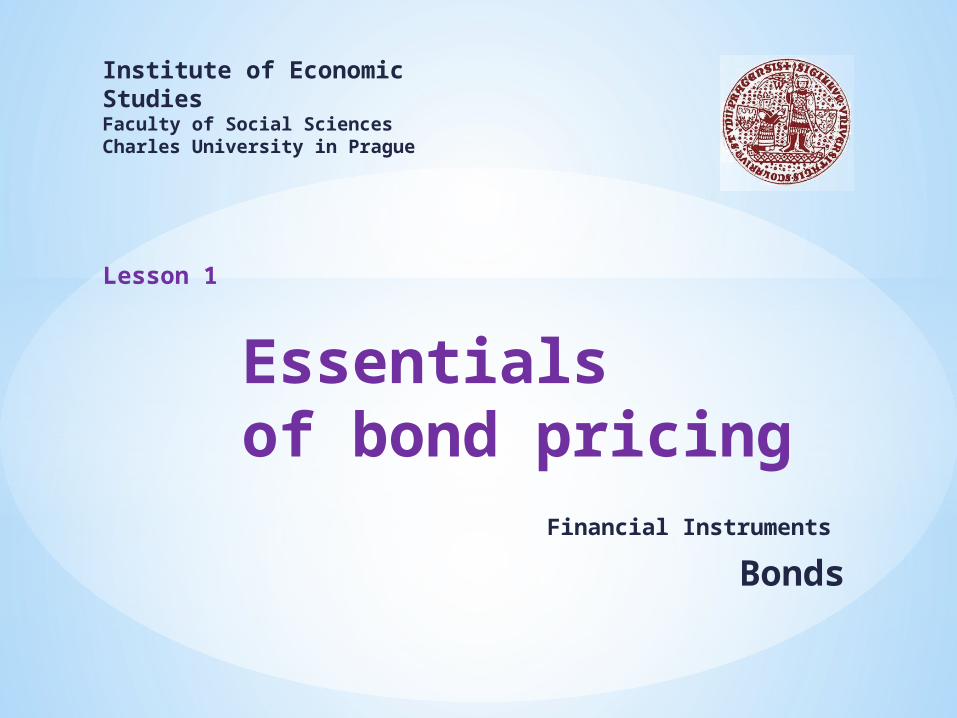

Straight bond

1 2 3 T-1 T

𝐶1 𝐶2

𝑃0

… issuing price of the bond

… maturity of the bond… nominal value of the coupon (t = 1, 2, … T)

𝐶𝑇 −1 𝐶𝑇

𝑀

… principal (face or par value) of the bond𝐶𝑡=𝑐×𝑀

… coupon rate (percentage)

Parties of a bond contract Issuer (borrower, debtor) obtains funds from the sale of the security and pays the interest rate called the coupon rate Holder (lender, creditor) invests funds in the purchase of the security and earns coupons Properties of a straight (plain vanilla) bond

Essentials of bond pricing 3

Diversities in bond contracts (1)

1 2 . . . Tsemi-annual bond zero-coupon bond Size of coupon payments

1 2 . . . T?

variable-coupon bond (inflation-linked bond, floating-rate bond) Redemption date

1 2 . . . perpetual bond, consol 1 2 . . . Tcallable bond

Frequency of coupon payments1 2 . . . T

?

∞

Essentials of bond pricing 4

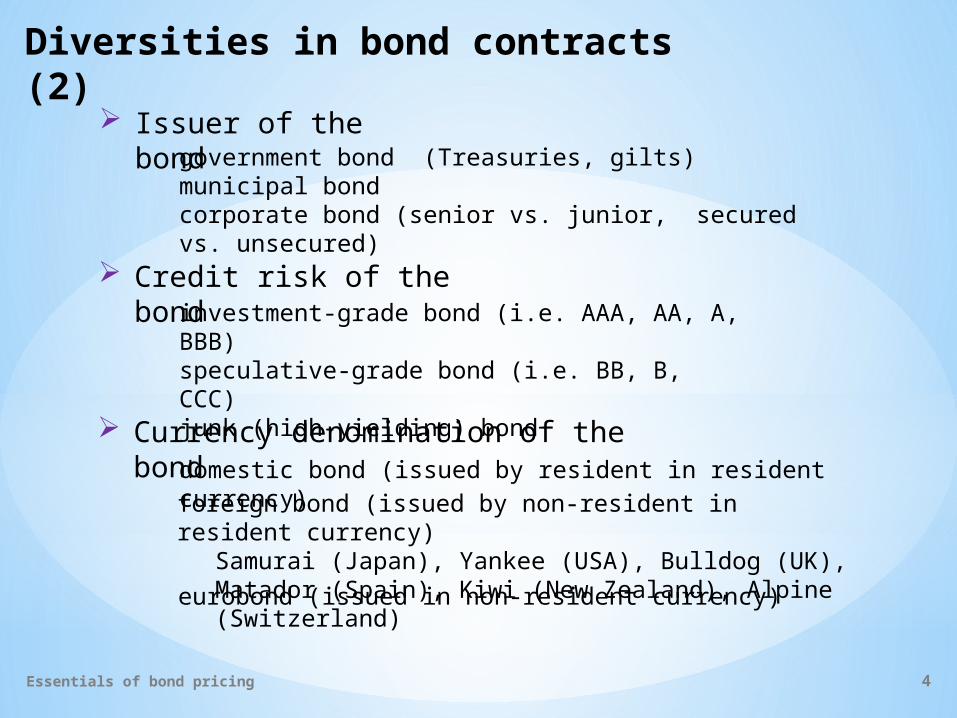

Diversities in bond contracts (2)

Credit risk of the bond Currency denomination of the bond

Issuer of the bondgovernment bond (Treasuries, gilts)municipal bondcorporate bond (senior vs. junior, secured vs. unsecured)investment-grade bond (i.e. AAA, AA, A, BBB)speculative-grade bond (i.e. BB, B, CCC)junk (high-yielding) bonddomestic bond (issued by resident in resident currency)foreign bond (issued by non-resident in resident currency)Samurai (Japan), Yankee (USA), Bulldog (UK), Matador (Spain), Kiwi (New Zealand), Alpine (Switzerland) eurobond (issued in non-resident currency)

Essentials of bond pricing 5

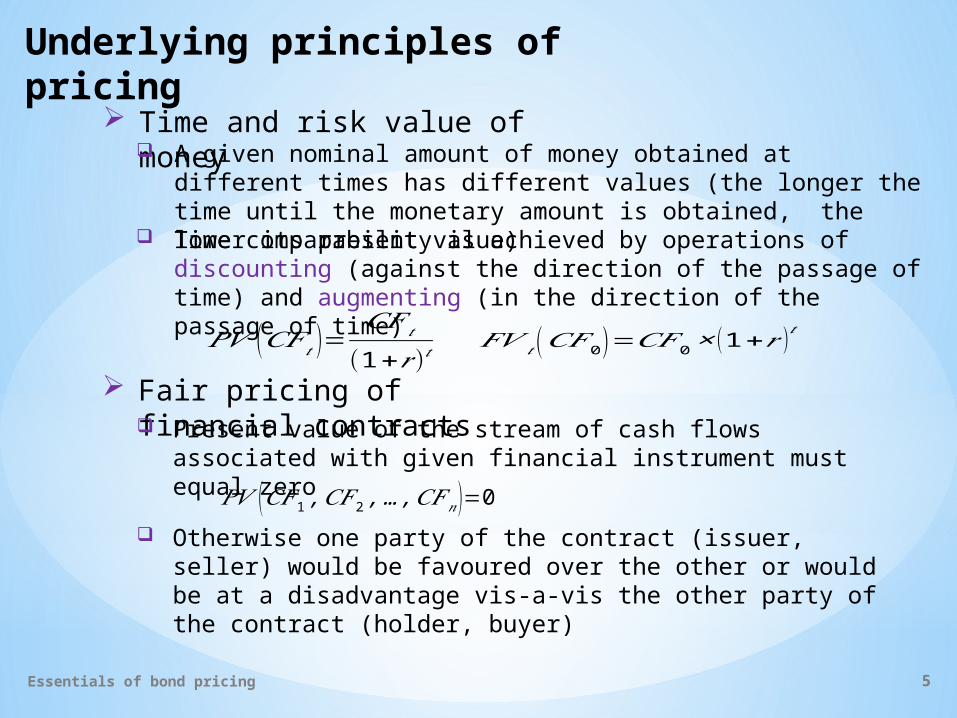

Underlying principles of pricing

Fair pricing of financial contracts

Time and risk value of money

𝐹𝑉 𝑡 (𝐶𝐹 0 )=𝐶𝐹 0× (1+𝑟 )𝑡𝑃𝑉 (𝐶𝐹 𝑡 )=𝐶𝐹 𝑡

(1+𝑟 )𝑡

A given nominal amount of money obtained at different times has different values (the longer the time until the monetary amount is obtained, the lower its present value) Time comparability is achieved by operations of discounting (against the direction of the passage of time) and augmenting (in the direction of the passage of time)

Otherwise one party of the contract (issuer, seller) would be favoured over the other or would be at a disadvantage vis-a-vis the other party of the contract (holder, buyer)

Present value of the stream of cash flows associated with given financial instrument must equal zero𝑃𝑉 (𝐶𝐹 1 ,𝐶𝐹 2 ,…,𝐶𝐹𝑛)=0

Essentials of bond pricing 6

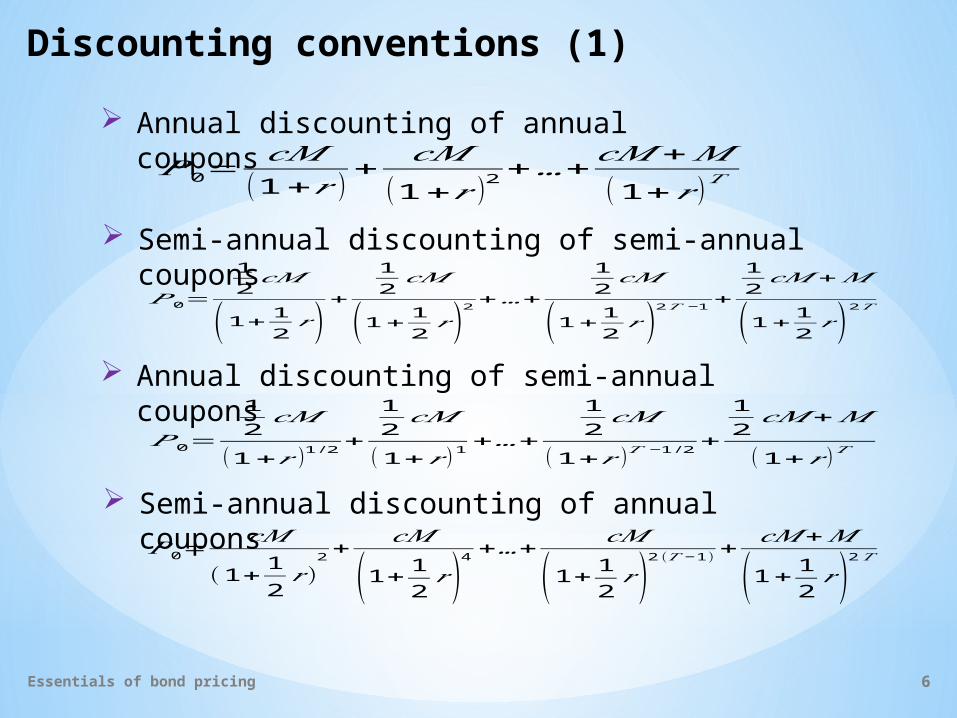

Annual discounting of annual coupons𝑃0=𝑐𝑀

(1+𝑟 )+𝑐𝑀

(1+𝑟 )2+…+

𝑐𝑀+𝑀(1+𝑟 )𝑇

Semi-annual discounting of semi-annual coupons𝑃0=

12𝑐𝑀

(1+ 12 𝑟 )+

12𝑐𝑀

(1+ 12 𝑟 )2+…+

12𝑐𝑀

(1+ 12 𝑟 )2𝑇 −1+

12𝑐𝑀+𝑀

(1+ 12 𝑟 )2𝑇

Annual discounting of semi-annual coupons Semi-annual discounting of annual coupons𝑃0=

𝑐𝑀

(1+ 12𝑟 )

2+𝑐𝑀

(1+ 12 𝑟 )4 +…+

𝑐𝑀

(1+ 12 𝑟)2(𝑇− 1) +

𝑐𝑀+𝑀

(1+ 12 𝑟 )2𝑇

𝑃0=

12𝑐𝑀

(1+𝑟 )1/2+

12𝑐𝑀

(1+𝑟 )1+…+

12𝑐𝑀

(1+𝑟 )𝑇−1 /2+

12𝑐𝑀+𝑀

(1+𝑟 )𝑇

Discounting conventions (1)

Essentials of bond pricing 7

Discounting conventions (2)

Valuation date differs from the issuance or the coupon payment date𝑃𝑛𝑐=𝑐𝑀+

𝑐𝑀(1+𝑟 )

+𝑐𝑀

(1+𝑟 )2+…+

𝑐𝑀+𝑀(1+𝑟 )𝑇

𝑃0=1

(1+𝑟 )𝑛365

×𝑃𝑛𝑐 number of days to the nearest coupon payment day

Price of the bond on the nearest coupon payment day () Price of the bond on the valuation day ()

Day/year conventions ACT/365, 30/360, ACT/ACT

ACT .. .actual number of calendar days in the period

8Essentials of bond pricing

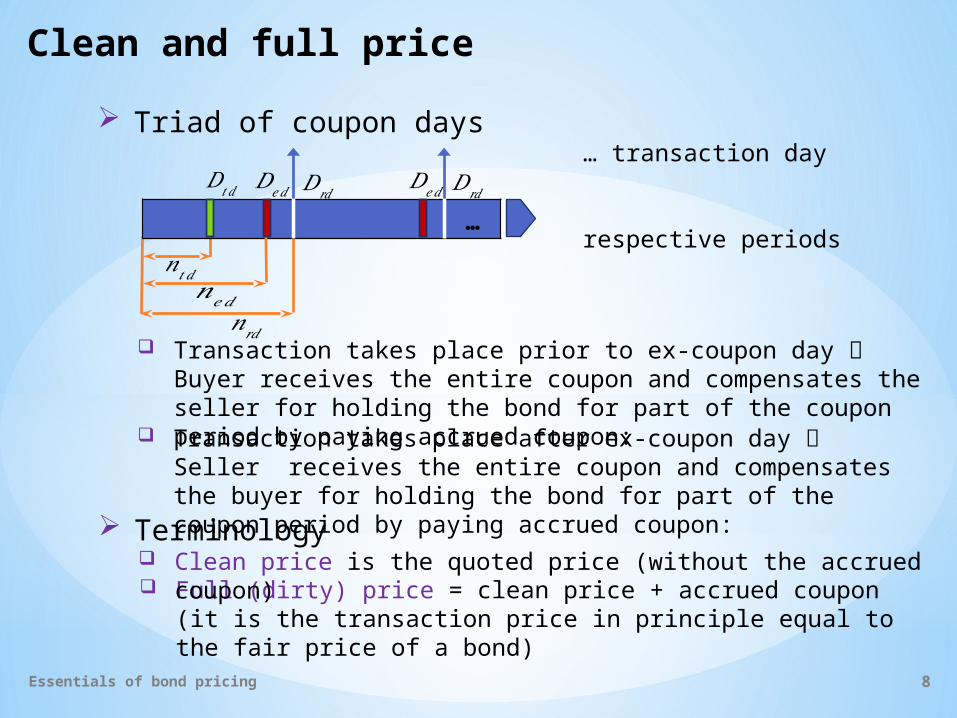

𝐷𝑒𝑑𝐷𝑒𝑑𝐷𝑡 𝑑

Full (dirty) price = clean price + accrued coupon (it is the transaction price in principle equal to the fair price of a bond) Clean price is the quoted price (without the accrued coupon) Terminology Transaction takes place after ex-coupon day Seller receives the entire coupon and compensates the buyer for holding the bond for part of the coupon period by paying accrued coupon:

Transaction takes place prior to ex-coupon day Buyer receives the entire coupon and compensates the seller for holding the bond for part of the coupon period by paying accrued coupon:

Triad of coupon days

𝑛𝑟𝑑

𝑛𝑒𝑑

𝑛𝑡 𝑑

…

𝐷𝑟𝑑 𝐷𝑟𝑑

… transaction dayrespective periods

Clean and full price

Essentials of bond pricing 9

Price-yield relationship

Summation formula

< 0 downward-sloping curve

c … coupon ratem … coupon frequencyr … required yield Properties of price-yield relationship

> 0 convex curve (par bond)r

P

Essentials of bond pricing 10

Price–maturity relationship

Price of a bond may change simply because the bond is heading to maturity clean bond price remains constant

T

𝑃 premium bonddiscount bond

par bond𝑀

Economic jargon bond is selling at a premium bond is selling at par

clean price converges to the face value from above price converges to the face value from below

bond is selling at a discount

Essentials of bond pricing

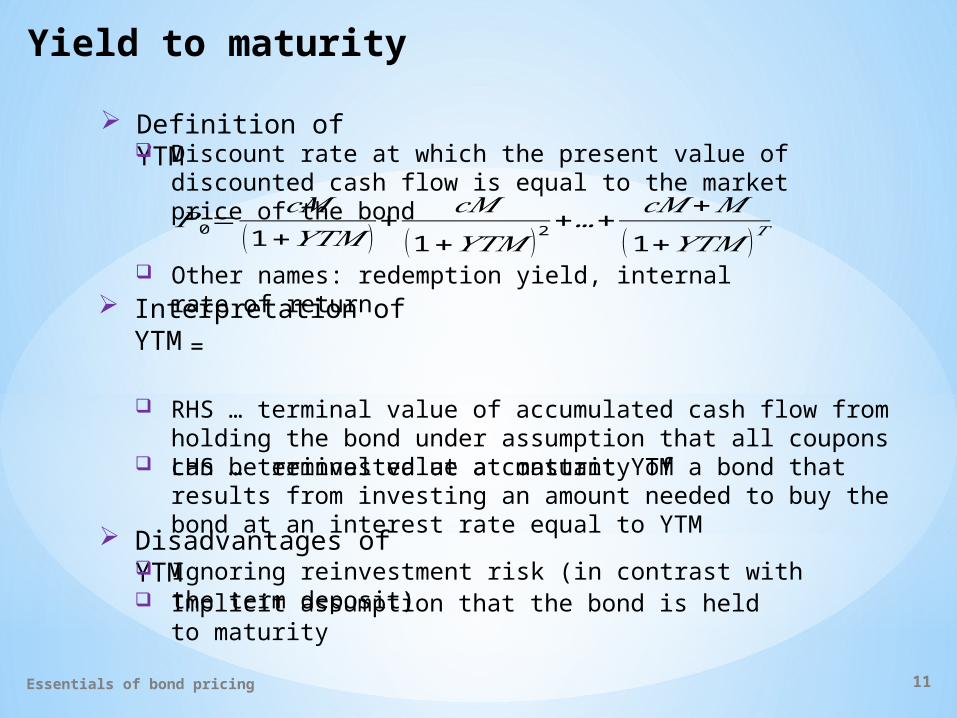

Definition of YTM𝑃0=

𝑐𝑀(1+𝑌𝑇𝑀 )

+𝑐𝑀

(1+𝑌𝑇𝑀 )2+…+

𝑐𝑀+𝑀(1+𝑌𝑇𝑀 )𝑇

= Interpretation of YTM

Disadvantages of YTM Ignoring reinvestment risk (in contrast with the term deposit) Implicit assumption that the bond is held to maturity

Discount rate at which the present value of discounted cash flow is equal to the market price of the bond

LHS … terminal value at maturity of a bond that results from investing an amount needed to buy the bond at an interest rate equal to YTM RHS … terminal value of accumulated cash flow from holding the bond under assumption that all coupons can be reinvested at a constant YTM

Other names: redemption yield, internal rate of return

11

Yield to maturity

Essentials of bond pricing 12

Other yield measures

= Holding period yield Current (flat, running) yield

Generalized YTM which takes into account buying price (, selling price ( and different rollover rates ( HPY must make assumptions about future values that are uncertain

= Exact YTM for perpetual bonds, approximate measure for other bonds (finite maturity, ignorance of capital gains and losses)

Used for bonds that are approaching maturity in order to ensure comparability with money market instruments

Simple yield to maturity = CY + Smoothing capital gains/losses over the remaining life of the bond Money market yield

See you in the next lecture

© O. D. LECTURING LEGACY

13Essentials of bond pricing