Lending technologies, loan pricing and customer profitability in

Lending Relationships and Loan Rate Smoothing

Sascha Steffen ∗

May 31, 2008

Abstract

Do firms benefit from maintaining strong banking relationships? This paperempirically examines lending relationships in a novel sample of loans extendedto large, private companies drawn from the UK syndicated loan market for thetime period 1996 through 2005. Using borrowers’ public debt market accessas proxy for information asymmetry between borrowers and outside credit mar-kets, I focus on one particular question: Do banks insure their borrowers againstadverse shocks to their creditworthiness? I analyze this question focusing onloan rate smoothing as particular insurance mechanism. Lending relationshipsare accounted for using (continuous) intensity measures. The endogeneity ofbond market access makes it difficult to isolate the causal effect of lending re-lationships on loan spreads. This paper uses determinants of exogenous varia-tion in bond market supply as (plausible) instruments for bond market access toovercome the endogeneity concerns. I find strong evidence that borrowers withclose ties to their banks are insured paying higher interest rates in good timesbut lower interest rates during recessions vis-à-vis non-relationship borrowers,thus are exposed to smoother loan rate movements across the business cycle.

JEL-Classification: G14, G21, G22, G23, G24

Keywords: Syndicated loans; Bonds; Hold-up; Lending relationships

∗Sascha Steffen is Assistant Professor at the Department of Finance, Goethe University Frankfurt(Germany), email: [email protected], and currently visiting the Finance Department,Leonard N. Stern School of Business, New York University, 44 West 4th Street, New York, NY 10012-1126, USA, Phone: 212.998.0377, email: [email protected]. I thank Sreedhar Bharath, ElenaCarletti, Günther Franke, Roman Inderst, Jan Krahnen, Christian Laux, Steven Ongena, Jörg Rocholl,Anthony Saunders, Marcel Tyrell, Mark Wahrenburg and Andrew Winton for valuable comments andsuggestions. All remaining errors are our own.

1 Introduction

Do firms benefit from maintaining strong banking relationships? This question

has been extensively studied over the last two decades with mixed evidence, both in

theoretical and empirical research. Sharpe (1990) and Rajan (1992) propose models

in which banks learn proprietary information over the course of a bank-borrower

relationship which finally locks-in the borrower and yields information rents for the

relationship lender. An alternate view to that effect highlights the benefits asso-

ciated with borrower-specific information: the reduction of adverse selection and

moral hazard (Diamond (1984) and Fama (1985)), information sharing such as de-

tails of R&D (Bhattacharya and Chiesa (1995), renegotiation of loan contracts and

bank discretion (Berlin and Mester (1992), Boot, Greenbaum, and Thakor (1993),

Boot and Thakor (1994) and Petersen and Rajan (1995)). Other papers highlight that

durable and reusable borrower-specific information facilitates implicit risk-sharing

agreements associated with bank loan contracts (Petersen and Rajan (1995), Allen

and Gale (1997) and Berlin and Mester (1999)). A number of empirical papers ana-

lyzes which theory of lending relationships carries out to the data examining small,

privately-held firms. Recent empirical research focuses on large, publicly traded com-

panies. Even for those firms evidence is mixed (Santos and Winton (2006), Bharath,

Dahiya, Saunders, and Srinivasan (2007) and Schenone (2007)).

My paper adds to this literature studying the impact of lending relationships on

loan spreads for loans extended to large, private companies. Overall, these firms

remain rather unnoticed in academic research but represent an important borrower

spectrum, especially in the UK.1 Further, they exhibit characteristics which make

them particularly interesting compared to small, private or large, stock exchange

1Brav (2005) for example provides evidence for the importance of private borrowers in the UK.Using the Financial Analysis Made Easy (FAME) database, he shows that 97 percent of all UK com-panies are private and hold about 70 percent of all assets. He further shows that private firms haveabout 50 percent higher leverage ratios than their public counterparts, that the proportion of shortterm debt relative to long term debt is 50 percent higher for private firms and that private firms havea more passive financial policy, which is more sensitive to operating performance but less sensitiveto traditional determinants of capital structure and are less quick in adjusting to their target capitalratio.

2

listed companies. Large companies are typically associated with less information

asymmetries. This should reduce the monopoly power of relationship lenders. How-

ever, private companies have limited access to external capital. They regularly rely

on bank financing and, to a lesser degree, on public debt. Being extensively bank

dependent might preserve the bank’s ex-post monopoly power, the ability to borrow

in outside credit markets, however, reduces it. A key contribution of my paper in

light of these facts is to answer one particular question: Do banks insure these bor-

rowers against adverse shocks to their creditworthiness? Intertemporal insurance

contracts are only feasible if the bank has an ex-post monopoly in the loan market.

More specifically, I examine whether bank loan rates for firms which borrow repeat-

edly from one bank move smoother over the business cycle compared to loan rates

for firms which switch lenders or engage more in transactional lending. My sample

is drawn from the UK syndicated loan market and comprises both large private and

public companies and, therefore, is ideally suited for this analysis.

My empirical results confirm (a) that even large, private borrowers benefit from

lending relationships through the smoothing of loan rates over the business cycle

and (b) that large borrowers or those with public debt market access benefit paying

lower loan rates than non-relationship borrowers. However, they do not benefit from

intertemporal risk sharing, primarily because of restrictions imposed by loan market

competition.

This paper contributes to previous research of relationship lending and loan rate

smoothing in several ways. First, I use local monopoly power of the relationship

lender in the loan market as measure of the lender’s market power. Petersen and

Rajan (1995) also focus on loan market power but use the concentration of lenders

in local markets as proxy for market power. Further, the timespan in which intertem-

poral smoothing materializes is much longer in Petersen and Rajan (1995). They look

at the lifecycle of the firm, whereas I look at loan rate smoothing over the business

cycle. Their sample is inherently different to mine. They look at loans to small, pri-

vate firms collected from the SSBF in 1988 with an average firm size of roughly USD

3

1.5 million and a median age of 10 years. The firms in my sample are on average

USD 8 billion in size with an average age of 25 years. Since information asymme-

tries are supposed to decline when a firms grows and becomes older, this should

bias me against finding any form of loan rate smoothing in my sample. It is even

more surprising that I do. Berlin and Mester (1999) also examine smoothing over the

business cycle but propose that the ability to smooth interest rates depends on the

bank’s availability of core deposits. They look at competition in the deposit market

and how this feeds back into the loan market. In an even earlier paper, Berger and

Udell (1992) find that loan rates move in a smoother fashion than market rates.

Second, this paper adds to recent empirical research on the impact of lending re-

lationships on loan contract terms which draw their samples from the US syndicated

loan market. Whereas Bharath, Dahiya, Saunders, and Srinivasan (2007) argue that

relationship benefits (which stem from private information of relationship lenders

about their borrowers) dissipate if companies become too large or have public debt

outstanding, I argue that relationship benefits still exist because relationship loans

have more favorable loan terms compared to non-relationship loans. However, the

benefit of loan rate smoothing dissipates because the bank’s ex-post monopoly power

seizes to exist. Santos and Winton (2006) find that banks opportunistically exploit

their borrowers charging higher spreads during recessions to firms which have not

issued public debt. My results show the opposite: firms that do not have issued pub-

lic bonds pay higher interest rates during expansions but lower interest rates dur-

ing recessions. Schenone (2007) finds similar results as Bharath, Dahiya, Saunders,

and Srinivasan (2007) for firms once they went public. Before the IPO, however, she

finds that relationship loans are priced higher than non-relationship loans. Schenone

(2007)’s and Santos and Winton (2006)’s results suggest that banks exploit an infor-

mation monopoly. My results, however, are consistent with models of intertemporal

smoothing and implicit insurance, pinpointing the benefits of relationships for these

borrowers.

The paper proceeds as follows. The next section derives testable hypotheses. Sec-

4

tion three gives an overview about UK company law and describes the datasources,

the sample and the variables used in this study with a focus on the measures of

monopoly power. Section four presents regression results. In section five, I exten-

sively discuss the results accounting for possible endogeneity concerns and show the

results of further robustness tests. Section six concludes.

2 Lending Relationships and Loan Spreads - Theory and

Discussion

2.1 The impact of bond market access and lending relationships on

loan spreads

Various theoretical and empirical studies have investigated costs and benefits

of lending relationships since the early 1990’s. Greenbaum, Kanatas, and Venezia

(1989)), Sharpe (1990) as well as Rajan (1992) analyse the costs of bank-borrower

relationships arising because of the asymmetric evolution of information among re-

lationship lenders and outside investors. In these models, informed lenders accrue

information rents in later stages of the relationship while subsidizing borrowers at

the beginning. A common thread to all models is that a bank acquires proprietary

(albeit imperfect) information in the process of lending to the firm which is unavail-

able to outside lenders and effectively locks-in the borrower. The latter also incurs

additional costs in searching a new lender.2 The inside (relationship) bank has an in-

formational advantage over the competitor banks which allows the former to extract

additional rents from its borrowers. A crucial determinant of the monopoly power is

the uncertainty of the competitor banks about the quality of the borrower. Assuming

that the relationship bank knows that the borrower will fail or succeed with certainty,

it only bids for the loan if the borrower succeeds. If the borrower accepts the offer of

the competitor bank and the loan is priced according to its marginal funding costs,

2For further information about search costs see e.g. Klemperer (1995).

5

the competitor bank earns a negative expected profit (winner’s curse). Therefore,

the outside bank will adjust the offer according to its belief about the quality of the

borrower.. The higher the outside bank’s conjectured probability that the borrower

is of high quality, the lower the lending rate because the outside bank bids more ag-

gressively. Vice versa, the lower this probability, the higher the lending rate because

outside banks are less willing to bid for these loans, thus reducing competition which

gives the inside bank an opportunity to extract additional rents from its borrower.3

Even though competition ensures that these rents extracted at a later stage of the

relationship are reflected in ex-ante lower loan rates Rajan (1992)), this distorts a

firm’s investment decisions limiting the firm’s gains from successful projects.4

The literature proposes a mix of public and private debt claims to avoid the lock-in by

relationship banks.5 Diamond (1991) and Rajan (1992) show that this distortion can

be avoided if the relationship bank’s bargaining power is reduced by issuing public

debt.6 Hauswald and Marquez (2003) develop a model of asymmetric information to

analyze how technological progress affects competition in financial services which

can be easily accommodated to our setting. They show that technological progress

in a sense of easier dissemination of information to investors levels the playing field

between informed and uninformed investors. Issuing public debt resembles this ad-

vance in information technology: A considerable amount of information is revealed

by firms registering public securities. Competing lenders receive some of the previ-

ously private information which reduces asymmetric information between borrowers

3There is extensive empirical research on the added value lending relationships James (1987),Lummer and McConnell (1989), Slovin, Sushka, and Polonchek (1993), Billett, Flannery, and Garfinkel(1995) and others documented that the existence of lending relationships adds value, wherease.g. Petersen and Rajan (1994) and Berger and Udell (1995) analyze the link between relationshipsstrength (measured as relationship duration) and this added value. This literature is reviewed inOngena and Smith (1998).

4However, other models derive conditions under which borrowers are not held-up by theirlenders, but loan contract terms rather improve over the course of the relationship Petersen andRajan (1995) and Boot and Thakor (1994).

5Multiple bank relationships are also a way to avoid the lock-in which is not focus of this paperand is therefore not discussed here (see e.g. Ongena and Smith (2000)). However, large syndicatesresemble multiple-bank relationships, especially since spillover effects on syndicate members arisedue to the fiduciary duty of the lead bank to pass through information about the borrower. We willtake this into account at a later stage in our framework.

6Empirical work by Houston and James (1996) shows that multiple bank relationship and publicdebt market access help to mitigate hold-up problems.

6

and outside credit markets and consequently reduces potential information rents.

This can be summarized in the following hypothesis:

HYPOTHESIS 1: Loan spreads should, on average, be higher for relationship loans

if borrowers have no access to public bond markets.

2.2 Lending relationships and loan rate smoothing

Who benefits from having strong bank-relationships? Suppose that the econ-

omy is in recession. Following Rajan (1992)’s model, the bank’s monopoly power

increases, since the probability of failure of the borrower is higher (as perceived by

outside lenders), which finally results in a markup on the risk-adjusted loan spread.

According to the reasoning described above, this should only be the case if the bor-

rower has not access to public bond markets. Santos and Winton (2006) test this

theory and find significant information rents for loans extended to borrowers with-

out public debt market access during recessions.

Berlin and Mester (1999) test a model of competitive loan markets, in which banks

with access to core deposits are able to smooth out loan rates for their customers.

Banks that have to refinance themselves at market rates cannot accomplish this in-

surance function. In Petersen and Rajan (1995)’s model, smoothing occurs over the

lifetime of the borrower. They show that competition is detrimental to bank insur-

ance without explicitly modelling credit risk shocks. In an overlapping generations

model, Allen and Gale (1997) document the benefits of long-term relationships par-

ticularly strengthening the advantages of intertemporal smoothing and risk sharing

between customers and banks within a bank-based system.

I test the opposing theoretical predictions using relationship intensity measures

to measure local monopoly power of the lending bank and analyze the loan spread

over the business cycle as a function of these relationship measures. 7 Specifically, I

test the following hypothesis:

7These measures are described in detail in Section 3 of this paper

7

HYPOTHESIS 2: Loan spreads should, on average, be lower for relationship bor-

rowers than for non-relationship borrrowers in recessions, if they don’t have access to

public debt.

2.3 Discussion

2.3.1 Competition in the loan market

I focus on market power in the loan market as the source of loan rate smoothing.

More specifically, I claim that a local monopoly obtained by the bank from frequent

interacting with the borrower over the course of the lending relationship enables

the relationship lender to smooth loan rates and insure the borrower against credit

shocks. However, focusing on local monopoly power involves three major issues.

Firstly, the market power is based on private information about the borrower col-

lected over the course of the relationship. To account for that, I use direct relation-

ship proxies as measure of monopoly power. Secondly, the market power crucially

depends on the degree of information asymmetry between the borrower and outside

credit markets. The market power dissipates, if the information advantage of the re-

lationship lender decreases. I use borrowers’ public debt market access as measure

for this information asymmetry. Thirdly, local monopoly power is endogenous. A

firm may deliberately choose to borrow repeatedly from one lender because it is de-

nied credit elsewhere giving monopoly power to the lender. Furthermore, as good as

public bond market access may approximate information asymmetry between bor-

rower and outside lenders, it is also endogenous. It is likely, that particularly good

borrowers choose to finance themselves with public debt.

In the following paragraphs, I discuss in detail how local monopoly power is mea-

sured. Discussion of the treatment of endogeneity concerns and the choice of appro-

priate instruments is relayed to section 5.

8

2.3.2 The value of information in syndicated loans

Linking the literature of ’relationship lending’ with the literature of ’syndicated

loans’ necessarily meets criticism. Whereas the first strand of research is primarily

associated with small, private companies, is the latter associated with huge loans and

large companies. And as a matter of fact, this criticism is justified. I omit a broad

and thorough discussion of this issue here because Santos and Winton (2006) have a

lucid account in their paper. However, I will discuss the main points with relevance

to this paper.

Private information matters in syndicated loans as shown by Sufi (2007). Most

of the companies in his analysis had publicly traded equity. But still, private infor-

mation on the lead arranger level was shown to be the key determinant of syndicate

structures: the lead arranger structures the syndicate, he is responsible for the mon-

itoring of the borrower on behalf of the participants and, which is the crucial results

in the paper, structures the syndicate to reduce moral hazard keeping a larger share

of the loan if information asymmetries between borrowers and participants are high.

In an earlier paper, Bosch and Steffen (2007) found consistent results for the UK

syndicated loan market, which is also the market of interest in this paper.

3 Data and Sample

3.1 Regulation: UK company law for private and public companies

Since only a limited number of papers are concerned with the UK market and dif-

ferences between private and public companies in particular, I provide some further

information on Uk company law in this section.8

All limited liability companies are formed by incorporation with the Companies

House in the UK and registered as public or private companies.9 Public companies

8This section is primarily based on the discussion in Ball and Shivakumar (2005) and Brav (2005).Please refer to these papers for further details and for exact refereces to the specific sections in theUK Companies Act to Ball and Shivakumar (2005).

9The main functions of Companies House are to "incorporate and dissolve limited

9

must incorporate ’public limited company’ or ’plc’ in their name, private limited com-

panies need only include ’limited’. Public companies must have a minimum share

capital of GBP 50,000 before they start doing their business. There is no minimum

share capital requirement for private companies.

The most important distinction between private and public companies is in their

ability to raise funds from the general public. A public company has unrestricted

rights to offer shares or debentures to the public, but such offerings are prohibited

for private companies. In this paper, I do not distinguish between private and public,

not listed companies. The primary reason is that both types of firms (at least in my

sample) do not differ in terms of their disclosure requirements 10 and I am primarily

interested in the effect of public debt issues on loan terms.

Prior to 1967, only public companies were required to file their financial state-

ments with the Registrar of Companies House. The Companies Act of 1967 requires

all companies, private and public, to file their financial statements annually with the

Registrar. Certain small or medium-sized companies may prepare accounts for their

members under the special provisions of sections 246 and 246A of the Companies

Act 1985.11 In addition, they may prepare and deliver abbreviated accounts to the

Registrar. Public companies and certain companies in the regulated sectors cannot

qualify as small or medium-sized companies.12 Similarly, companies which are part

of a group which has members who are public companies or certain companies in the

regulated sector cannot qualify as small or medium-sized. For the other companies,

to be classified as small (medium), they must fulfill two of the following criteria for

companies; [to] examine and store company information delivered under the Compa-nies Act and related legislation; and [to] make this information available to the pub-lic."(http://www.companieshouse.gov.uk/about/functionsHistory.shtml)

10I provide more details on UK disclosure requirements further below.11The Companies Act 1985 was amended in 1989. The Companies Act 2006 overrules the Com-

panies Act 1989 and, even though intends to simply regulations, could not be implemented im-mediately but continued through 2007. The new Act makes public companies subject to morestringent regulation whereas relaxes the requirements for private companies. However, sincethis paper needs information about UK companies only until 2004, the changes associated withthis Act do not apply to this paper and are therefore not further discussed. (For further ref-erence to the Companies Act 2006, please visit the Office of Public Sector Information in UKhttp://www.opsi.gov.uk/acts/acts2006/).

12For detailed explanatory notes on reporting requirements and disclosure exemptions pleaserefer to http://www.companieshouse.gov.uk/about/gbhtml/gba3.shtml#three).

10

two consecutive year: annual turnover must be GBP 5.6 million (GBP 22.8 million) or

less; the balance sheet total must be GBP 2.8 million (GBP 11.4 million) or less; the

average number of employees must be 50 (250) or fewer.13

The financial statements of private (public) companies must be filed within ten

(seven) months of their fiscal year. Failure to file is a criminal offense. All financial

statements must be prepared in accordance with UK accounting standards, whether

the firm is private or public. They must be audited if annual sales exceed GBP 1

million. 14

UK tax laws likewise do not descriminate between public and private firms. Lon-

don Stock Exchange listing rules require additional disclosures for public companies,

but the rules do not mandate accounting standards for financial reporting. In all im-

portant respects, the UK regulatory regimes governing financial reporting for public

companies and all but the smallest private companies are equivalent.

3.2 Data sources and sample selection

The body of the data for this study is obtained from several sources - the Dealscan

database from the Loan Pricing Corporation (LPC), Thomson’s Financial Securities

Data Corporation (SDC) Platinum database, Thomson Financial Datastream, UK Com-

panies House, and the Centre for Economic Policy Research (CEPR).

I examine syndicated loans over the time period 1996 through 2005 for UK domi-

ciled borrowers. Loan information (i.e. borrower identity, lenders, spreads (plus

fees), origination date, loan amount, maturity, loan purpose and loan type) are ex-

tracted from LPC’s Dealscan database. This database has been documented exten-

sively in the literature.15 LPC reports loans both on a "deal" and a "facility" level. One

deal regularly consists of several facilities with different price and non-price loan

terms and lender composition. This study therefore uses a loan facility as unit of ob-

13For fiscal years ending earlier than January 30th, 2004, the following criteria were valid: annualturnover must be GBP 2.8 million (GBP 11.4 million) or less; the balance sheet total must be GBP 1.4million (GBP 5.6 million) or less; the average number of employees must be 50 (250) or fewer.

14Before June 2000, the threshold was GBP 350,000. Less than 1 percent of the companies in mysample don’t have audited financial statements.

15See e.g. Carey, Post, and Sharpe (1998) for a detailled discussion of this database.

11

servation.16 However, all results hold on the deal level using the largest and earliest

facility as approximation. Matching the loan data to other databases is a trouble-

some task since unique identifiers for both borrowers and lenders are not available.

I carefully hand-match borrowers in Dealscan to issuers in SDC and company names

obtained from Companies House. Companies House stores all company information

provided under UK’s Companies Act 1985. All accounting data (and information on

industry affiliation and firm age) are from company reports and I use fiscal year t-1

data for all firms.

For UK based borrower, Dealscan contains information on 5,063 syndicated loans

issued between 1996 and 2005 involving 1,481 different firms. We drop loans that

are "not fully confirmed" (112), loans to borrowers of regulated and financial indus-

tries (617), as well as loans with structural inconsistencies (10). For all observations

included, I require the joint availability of borrower, firm and loan characteristics.

This matching process results in a final sample used in the regressions with detailed

financial data for 1,277 syndicated loan transactions representing 361 different UK

based borrowers for the time period 1996 to 2005.

(Bond) Underwriting information comes from the SDC database. The sample of

bonds used in this study include only bonds issued in the UK by UK domiciled firms

consistent with our loan data. I use information on bond issues since 1962 in order

to identify which borrower from our loan sample has tapped the bond market before

issuing the loan, first time issues and the frequency of bond issues. In calculating

the relationship variables, however, I start the measurement period in 1991. My loan

sample starts in 1996 and I regularly use a look-back window of 5 years in defining

the relationship measures.17 I further rely on this database to get information on

bond ratings and the issue type (public bond versus private placement).

I identify recessions using the EuroCOIN Index provided by the Centre of Eco-

16Especially in the context of lending relationships, it is important to differentiate between com-mitment loans (which are so-called "relationship" loans) and term loans ("transaction loans") asnoted e.g. by Berger and Udell (1995).

17The main reason is that the average maturity of the loan facility is about 5 years. I relay a furtherdiscussion of the measurement period to section 5 of this paper.

12

nomic Policy Research (CEPR) as indicator for economic activity. EuroCOIN is the

leading coincident indicator of the Euro area business cycle available in real time.

The indicator provides an estimate of the monthly growth of Euro area GDP - after

the removal of measurement errors, seasonal and other short-run fluctuations. In

other words, the index represents only the cyclical component of GDP growth.18 The

index started in January 1988. Over the lifetime of the index, the quarterly growth

rate averaged 0.59. Based on definitions in earlier research, I define that an economy

is in recession, when the EuroCOIN Index is below its long run average for at least

four consecutive quarters.19 Based on this definition, I identify the following periods

of recession: 1995:03 through 1996:08 (my sample period starts in 1996:01), 2000:12

through 2002:02, 2002:06 through 2003:06 and 2004:07 through 2005:08.20

3.3 Bond and loan markets

I measure a borrower’s public debt market access and possible spillover effects on

the loan market with a set of variables related to the bond issue. All variables have

been used in prior literature and have proven to be relevant information proxies in

the bond market.21 The first measure (Public Bond) is a broad proxy for bond market

access capturing whether the borrower has issued a public bond prior to the loan

origination.22 This variable is supplemented by the number of public bonds issued

18EuroCOIN is constructed using a dataset covering about 1,000 monthly variables from the sixlargest economies of the Euro area. Variables included are industrial production, consumer andproducer prices, trade variables, money, stock prices and exchange rates, interest rates, labor marketrelated variables and surveys among others.

19The EuroCOIN Index is based on an extension of the Stock-Watson XCI methodology, which wasone of the leading coincident indicators for the US market until 2003. Its direct successor for the USeconomy is the Chicago Fed National Activity Index (CFNAI) which is also an extension of the Stock-Watson XCI methodology. Other researchers using the Stock-Watson index to measure economicactivity relying on our definition of recession include Santos and Winton (2006).

20Four consecutive quarters of below average growth in GDP indicates long-term economic weak-ness which is in line with methods used for US Stock-Watson indices in earlier literature. However,note that my analysis does not hinge on the classification "recession versus expansion" as describedhere. All I want to show is that economic uncertainties in general increase the cost of relationshiplending. In unreported results, I employ further proxies using credit spreads and stock volatilitiesto support the empirical methodology. All results remain unchanged.

21Variables have been used (among others) by Hale and Santos (2006) and Santos and Winton(2006).

22The measure is "broad" because it only says that the borrower has accessed the bond market atany time between 1991 (the beginning of our measurement period) before the loan was issued but

13

by the firm prior to the loan (Number of Bonds). Both proxies measure transparency

of the borrower and the availability of public debt for this borrower.23 The second

measure focuses on the most recent access to public debt (Last Bond Public) and

takes the value of one if the most recent bond issued by the borrower was public.

Santos and Winton (2006) prefer this measure because it is a closer measure of how

many informed investors the borrower can tap in the bond market. I supplement

this measure using a variable that captures the time since the last public bond issue

and the loan origination date (Time since Last Bond Public). My third measure of

information asymmetry in outside debt markets is related to the most recent bond

issue. Some bonds are rated by one or more of the major rating agencies. Following

the literature on bond markets which show the effect of ratings on bond spreads, I

include the rating of the most recent (public) bond issue to examine the impact on

subsequent loan spreads.

3.4 Previous lending relationships and local monopoly power

An important part in the empirical approach is to identify measures for the extent

of local monopoly power of the relationship lenders. On this account, I measure

the existence and intensity of the relationship. I follow Bharath, Dahiya, Saunders,

and Srinivasan (2007) and Ljungqvist, Marston, and Wilhelm (2006) in defining the

"loan lending relationship" measures. I follow these studies and exclude all banks

described as "participants" in Dealscan to focus only on the lead role bank which have

an information production function in the syndicate.24 Second, I carefully account for

merger & acquisition activities among banks and, following Ljungqvist, Marston, and

Wilhelm (2006), assume that the acquiring bank inherits both lender characteristics

there might have been private placements between that bond issue and the loan origination, or thebond has matured long ago. The information effect of this variable is supposed to be small or evenquestionable.

23Faulkender and Petersen (2006) use a firm’s debt rating as a proxy for debt market access. Therationale is a high correlation between the company having a rating and public debt outstanding.This correlation, however, is rather low for the companies in our sample (i.e. 33 percent). Therefore,the availability of a rating alone is a rather sketchy measure for public debt market access.

24See e.g. Madan, Sobhani, and Horowitz (1999). I comment on further tests related to this speci-fication in section 5.

14

and lending relationships.

The first measure (Relationship Dummy) is a dummy variable capturing whether

the loan is a relationship loan or not. The facility is assigned the value of 1, if the

lead bank in the current lending syndicate has been lead lender in a previous loan

issued by the same borrower. In those cases where there is more than one lead bank,

the facility is assigned the value of 1, if at least one lead bank is a relationship bank

according to this definition. (Relationship Amount ) measures the amount lent by

the lead bank relative to the total amount borrowed by the firm. This measure is

calculated for each lead bank and the highest value is assigned to the loan facility.

The third measure (Relationship Number ) captures how many loans have been given

by a lead bank relative to the number of loans the borrower has issued over the last

years. Again, if there is more than one lead bank, this measure is calculated for each

lead bank and the highest value is assigned to the loan facility.

3.5 Loan and borrower characteristics

All loan data comes from the LPC Dealscan database. Following a vast amount of

literature, I use the All in Spread Drawn (AISD) as the measure of interest rate for a

loan, which is the total annual spread paid over LIBOR for each dollar drawn. The

AISD is defined as the coupon spread on the drawn amount plus any annual fee. I

further control for several loan terms which were shown to have an impact on loan

spreads, i.e. maturity25, covenants, loan purpose controls, facility size, loan type and

some others. A complete list of controls is given in the appendix.

Accounting data for borrower come from companies’ annual reports filed with

Companies House. I control for borrower risk using the following variables: Log

(Total Assets) is the natural logarithm of the borrower’s total assets. Larger firms

25Log (Maturity) is also used as control variable because borrowers might trade longer maturitiesfor higher spreads. However, it might also be the case that only creditworthy borrowers get longermaturities. The overall effect on spread is therefore ambiguous. This indicates that there might be asimultaneity problem in regressing spread on maturity. I address this concern using a simultaneousequation framework as an (unreported) robustness check. The overall results in terms of bondmarket access and lending relationship continue to hold, but we get a clearer picture on the impactof maturity on spread. I find only weak results for the hypothesis that longer maturities are tradedagainst higher spreads by the borrower.

15

are supposed to be less risky and I expect a negative correlation with spread. A

similar argument applies to Tangibles which is the ratio of tangibles over total assets.

Tangibles can be used to repay debt in the event of financial distress and higher ratios

imply lower risk. Interest Coverage Ratio is the natural logarithm of one plus interest

coverage ratio. A higher ratio implies less risk for lenders to be repaid on the debt

and high ratios therefore should decrease loan spreads. Leverage measures the ratio

of long term debt over total assets. High levels of debt are associated with higher risk

and I expect a positive correlation between leverage and spread. I further control for

industry specific factors using the one-digit SIC code.

3.6 Sample characteristics

Our loan data is taken from LPC’s Dealscan database and contains loans issued

to private firms for the years 1996 through 2005. The final dataset comprises 1,277

loans issued by 361 borrowers.

[Figure 1]

Figure 1 shows the percentage of firms with prior public debt market access across

all years. On average, 17 percent of firms have access to public debt. This number

varies across the years. At the end of the 1990s and in the end of the upswing in the

European economy, almost 20 percent of loan issuers have issued public bonds prior

to the loan origination date. During the recession periods after 2000, a decreasing

percentage of firms accessed public debt markets. E.g. in 2004, less than 10 per-

cent of firms could tap investors in this market. A similar picture is given by the

percentage of loan amounts extended to borrowers. At the peak in 2000, 53 percent

of total loan amounts were extended to borrower with public debt market access,

whereas in 2004, this was only the case for 24 percent of loan amounts. During

economic downturns, monitoring by banks seems to become more valuable. Table

I shows descriptive statistics for the sample separately for loans to bank and non

16

bank dependent firms (where the term ’bank dependent’ is used synonymously for

borrowers without public debt market access).

[Table I]

Firms with public debt market access are larger and older than bank dependent

firms. They have on average USD 19 billion total assets compared to USD 1.7 bil-

lion of bank dependent firms and are 3 years older. Comparing operating revenues

and EBITDA gives similar results. Interestingly, leverage ratios do not differ signif-

icantly between these firms, which contradicts empirical findings in the US market.

Faulkender and Petersen (2006), for example, find that even after controlling for firm

characteristics, firms with public debt market access have 35 percent higher leverage

ratios. Further, bank dependent firms are more profitable than non bank dependent

firms.

Loans to bank dependent firms have on average 57 bps higher spreads and 24 months

longer maturities (both significant at the one percent level). Further, these loans are

significantly smaller and less likely to include performance pricing provisions. Bank

dependent firms are more likely to borrow through institutional term loans (i.e. non

amortizing term loans) and for corporate control purposes. With regard to syndi-

cate structures, the descriptive statistic is consistent with findings in Sufi (2007) and

Bosch and Steffen (2007) who show that syndicates are systematically driven by infor-

mational opaqueness. Mandated arrangers retain a 15 percent larger share of loans

to firms without public debt market access. Syndicates of these loans have on av-

erage 7 lenders less and are significantly more concentrated. Non-bank lenders are

more likely to be present in loans to non-bank dependent firms.

17

4 Empirical Results

4.1 Multivariate Analysis of Hypothesis 1

AISD = β0 + β1(LendingRel)+∑βi(BorrowerCharacteristicsi)

+∑βj(LoanCharacteristicsj)+

∑βk(Controlsk)

The dependent variable is the AISD, the key explanatory variables are my relation-

ship proxies. Table II - Panel A presents the results for this model with appropriate

controls. The standard errors are robust accounting for within firm correlation (Pe-

tersen (2007)).

[Table II]

Across models 1 through 3, my relationship proxies are highly significant and

the coefficients are of similar magnitude. Prior bank borrower relationships in the

loan market increase the spread of subsequent loans by 20 to 25 bps depending on

the relationship proxy. This finding is highly interesting because it runs counter to

most US evidence. Furthermore, it gives prove for the existence of the relationship

specific nature of the UK syndicated loan market. Theories on informational scope

economies or the reduction of asymmetric information borrowing repeatedly from

one bank which finally reduces the loan spread do not apply to the UK syndicated loan

market. On the contrary, I find evidence consistent with the theory of relationship

lenders extracting monopoly rents from their borrowers. Model 4 uses the time since

the first contact with the lead bank as measure of relationship strength measured

in days. For each unit increase in this measure, borrowers pay 0.041 bps higher

spreads compared to non-relationship borrowers. E.g. a borrower with an average

relationship length with the lead bank (the average is 2 years) pays 27 bps higher

spreads compared to a borrower without lending relationships.

18

The control variables are generally highly significant with the signs of the coef-

ficients as expected. Last Bond Public controls for asymmetric information between

borrower and outside lenders. A value of 1 means less information asymmetry and,

as expected, reduces loan spreads by 39 bps spreads compared to borrowers with

high information asymmetry. In the following, I will discuss the impact of bond

market access in more detail and then analyze whether bond market access causes

sufficient competition in the loan market that monopoly power (and rents) fade away.

I estimate an OLS model for the costs of corporate borrowing using the following

specification:

AISD = β0 + β1(PublicBond)+ β2(Recession)+ βi(BorrowerCharacteristicsi)

+∑βj(LoanCharacteristicsj)+

∑βk(Controlsk)

The dependent variable is the AISD, the key explanatory variables are the measures

for public debt market access. The results for this estimation are reported in Panel

B of Table II. Standard errors are clustered at the borrower level.

We also include Recession as an important variable to analyze hold-up problems

and bank-borrower relationships in our setting. Recession takes the value of one,

if the loan is issued in a period of recession as defined by the EuroCoin index. For

each model, I further control for specific loan and borrower characteristics as well as

time and industry effects. I do not report the coefficients for time, industry and loan

purpose controls for brevity. All models are heteroscedasticity robust with clustered

standard errors.

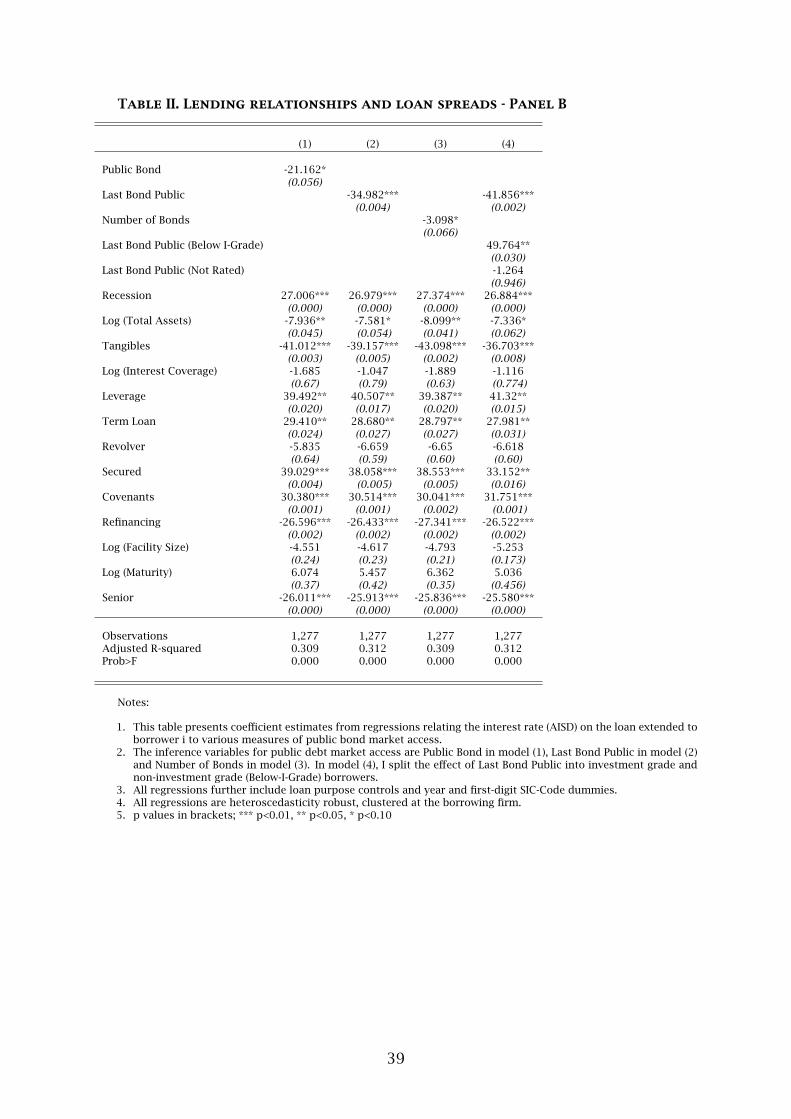

Across all models, the bond market variables are highly significant. Having issued

a public bond (Public Bond) prior to the loan activation date reduces loan spreads by

21 bps (however, significant only at the 10 percent level). Having issued a public

bond right before the loan (Last Bond Public) has a higher impact on the spread as

expected, which is 35 bps lower compared to spreads on loans to bank dependent

borrowers and significant at the one percent level. However, the number of public

bonds (Number of Bonds) issued prior to the loan has only a small impact on spreads

19

reducing the spread by 3 bps (only significant at the 10 percent level). Bond ratings

also substantially alter the spread on subsequent loans. I introduce a dummy variable

equal to one if the last bond was public and had a rating below investment grade (Last

Bond Public (Below I-Grade)) and a dummy variable equal to one if the last bond was

public but not rated (Last Bond Public (Not Rated)). If both dummy variables are zero,

the variable Last Bond Public equals the impact of an investment grade rated bond

on the loan spread. The coefficient on Last Bond Public (Below I-Grade) is significant

at the one percent level. Having issued a junk-bond prior to the loan increases the

spread on subsequent loan roughly about 8 bps (adding also the coefficient of Last

Bond Public). In other words, only investment grade borrowers benefit from issuing

a public bond prior to the loan. This finding is consistent with empirical evidence in

Hale and Santos (2006) and the theoretical arguments in Rajan (1992). A bond rating

below investment grade makes the realization of a bad state more likely and, ulti-

mately, increases the bank’s monopoly power. A higher loan spread might therefore

already point at the existence of hold-up problems.

In recession, loan spreads are on average 27 bps higher across all model specifica-

tions Our other control variables are regularly statistically significant, their signs as

expected and in line with prior literature and the magnitude of the coefficients does

not vary across the different models.

To establish the existence of monopoly pricing more clearly, I show that the mark-

up in pricing exists only for opaque firms. Following the theory, a borrower is more

known to investors if it has issued a public bond prior to the loan. These borrowers

should not be subject to hold-up problems as they can tap public debt markets more

easily.

I change the model specification to address this issue.

20

AISD = β0 + β1(LendingRel)+ β2(LastBondPublic)

+ β3(LendingRel∗ LastBondPublic)+∑βi(BorrowerCharacteristicsi)

+∑βj(LoanCharacteristicsj)+

∑βk(Controlsk)

The results are reported in Panel C of Table II. All regressions include firm and

year effects and the results are heteroscedasticity robust, clustered at the borrowing

firm.

The results give strong support for my hypothesis with regard to the relationship

intensity measures. Prior lending relationships reduce the spread on a subsequent

loan issuance for non-bank dependent firms as shown in models 1 through 3. If the

relationship intensity with regard to the ratio of loan amounts to the total amount

borrowed is in the upper quartile of its distribution, prior lending relationships re-

duce the costs of borrowing by approximately 30 bps (obtained by summing the

coefficient on the relationship variable and the interaction term in model 2).26 Mea-

suring relationship intensity with regard to the number of loans underwritten by the

lead bank relative to the total number of loans obtained by the borrower, I find that

prior lending relationships reduce the spread by 30bps as well (model 3). 27

In model 4 and 5, I use alternative proxies for informational transparency. Total

assets is the first proxy. It is well established in prior literature that size is a good

proxy for transparency. A borrower at the 75th percentile of size (measured by total

assets) pays 27 bps (ln(1,379)-ln(107)) multiplied by the coefficient on the interaction

term) less on a similar loan than a borrower at the 25th percentile of size, ceteris

paribus. If a borrower has high tangible assets, the spread is about 26 bps lower all

else equal. However, being large or having high tangible assets does not reduce loan

26The results hold if Relationship Amount (and Relationship Number) are used instead of thedummy variables employed in the regression, but the interaction terms are more difficult to interpretand therefore remain unreported.

27Analogously, non-bank dependent firms pay lower spreads if they have a longer relationshipwith the lead bank. This effect, however, is statistically but not economically significant and remainunreported.

21

spreads conditional on the loan being provided by a relationship bank (the sum of

the coefficients of the relationship proxy and the interaction term remains positive

in both models).

I find evidence that lending relationships induce hold-up problems for borrowers

facing costs of switching lenders. Borrowers who have outside funding options and

who are known to the market in turn may benefit from lending relationship obtaining

cheaper loans. However, the benefits of lending relationships are not conclusive and

will be more broadly discussed in the next section.

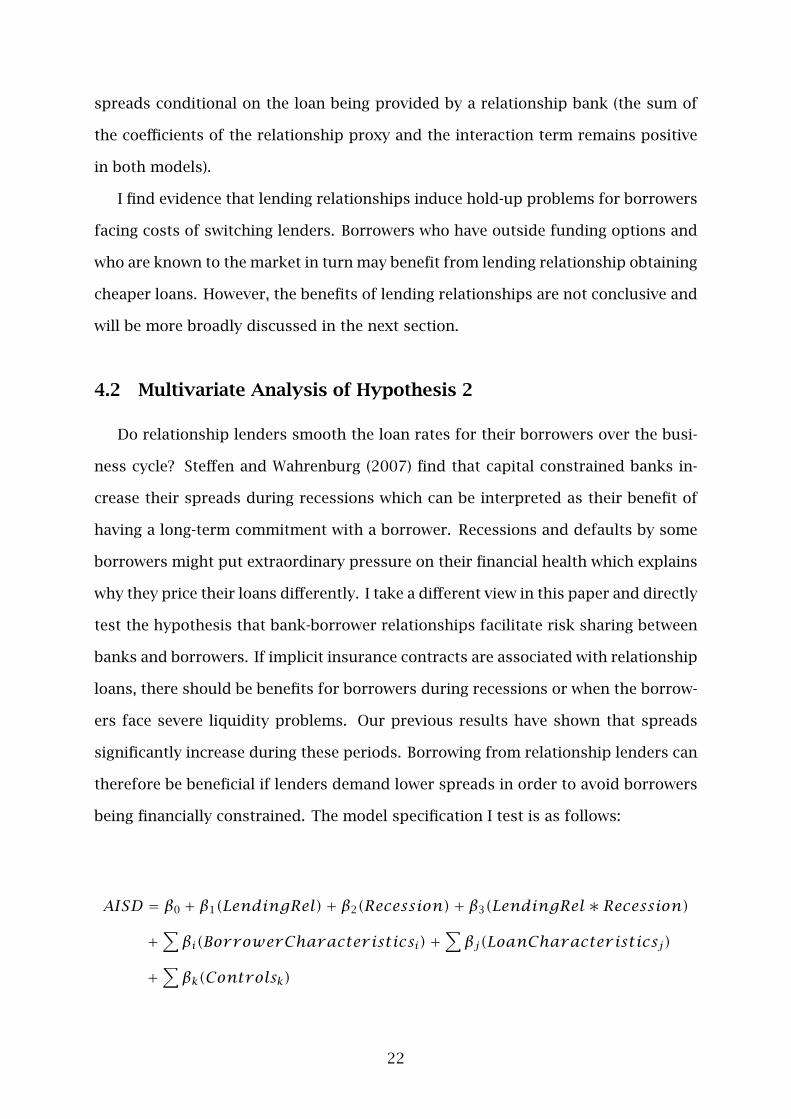

4.2 Multivariate Analysis of Hypothesis 2

Do relationship lenders smooth the loan rates for their borrowers over the busi-

ness cycle? Steffen and Wahrenburg (2007) find that capital constrained banks in-

crease their spreads during recessions which can be interpreted as their benefit of

having a long-term commitment with a borrower. Recessions and defaults by some

borrowers might put extraordinary pressure on their financial health which explains

why they price their loans differently. I take a different view in this paper and directly

test the hypothesis that bank-borrower relationships facilitate risk sharing between

banks and borrowers. If implicit insurance contracts are associated with relationship

loans, there should be benefits for borrowers during recessions or when the borrow-

ers face severe liquidity problems. Our previous results have shown that spreads

significantly increase during these periods. Borrowing from relationship lenders can

therefore be beneficial if lenders demand lower spreads in order to avoid borrowers

being financially constrained. The model specification I test is as follows:

AISD = β0 + β1(LendingRel)+ β2(Recession)+ β3(LendingRel∗ Recession)

+∑βi(BorrowerCharacteristicsi)+

∑βj(LoanCharacteristicsj)

+∑βk(Controlsk)

22

The dependent variable is the AISD, the key explanatory variables are the rela-

tionship proxies and Recession. All regressions include the same borrower and loan

controls as described before and we control for industry and time effects. All regres-

sions are heteroscedasticity robust with clustered standard errors. The results are

reported in Table III.

[Table III]

I use two proxies to capture liquidity problems or even distressed situations of

borrowers, i.e. situations in which an implicit insurance contract would be triggered.

First, I use Recession to describe the state of the economy. Second, I use the dummy

variable Leverage High equal to 1 if the borrowers’ long term debt to asset ratio

exceeds the 75 percent quartile of the distribution. In models 1 through 6, I inter-

act each proxy for relationship intensity with Recession and Leverage High and find

similar results across all models. The variables are all highly significant (at the one

percent level) in the models using the recession proxy. My overall results confirm

that prior loan lending relationships increase loan spreads again pointing at the ex-

istence of monopoly rents. In recessions, however, borrowers pay between 6 bps

and 12 bps lower spreads conditional on the loan being provided by a relationship

bank (obtained by summing the coefficient on the relationship proxy and the inter-

action term). The benefits of having bank relationships are also apparent for highly

leveraged borrowers reducing loan spreads by approximately 22 bps (models 4 and 6)

vis-à-vis non-relationship borrowers. Public debt market access reduces loan spreads

by 40 bps throughout all models. A junk-bond rating on a previous public bond is-

suance increases subsequent loan spreads by roughly 55 bps supporting my earlier

results. Loans issued in recessions carry 40 bps to 43 bps higher spreads as expected.

The results emphasize the economic relevance of lending relationships facilitat-

ing risk sharing between borrowers and lenders showing that borrowers receive more

favourable spreads during recessions when they have strong bank relationships. In

addition to loan terms, there are further possibilities to make transfers between

banks and borrowers when the insurance is triggered. One way e.g. is to increase

23

the credit availability for borrowers. This, however, is not tested in this paper. Boot

(2000) and Allen and Gale (1999) emphasize the structural differences between the

US and Europe that might facilitate both hold-up as well as the existence of implicit

contracts. My results support this view but are naturally not conclusive. They do

give, however, fist time evidence for the risk sharing arguments put forth by Allen

and Gale (1999).28

5 Identification and Robustness

5.1 Instrumental variable estimation

It is likely, that bond market access is positively correlated with the residuals of

the spread equation, potentially inducing a bias in the estimates of the coefficient.

Firms that issue public bonds possibly have a common set of characteristics which

firms without bond market access do not possess. My results can therefore be driven

by unobservable risk factors, i.e. firms with public debt market access might be less

risky than firms that do not have access to bond markets. The objective of this

section is therefore to establish the causal link between bond market access and

loan spreads. To assess this question empirically, I follow Santos and Winton (2006)

and Faulkender and Petersen (2006) and use a two step procedure focussing on the

variation in public debt market access arising from heterogeneity in bond market

demand. Plausible instruments determine the access to public debt markets, but

do not directly affect loan spreads other than through bond market access. If the

exclusion of our instruments from the spread equation is valid, however, two-stage

least squares estimation using these instruments will lead to consistent estimates.

Following earlier literature, the instruments are chosen to increase firm or indus-

try visibility, which facilitates the access to public debt and, at the same time, do not

correlate with firm risk. I select these instruments based on economic intuition. The28Further empirical evidence and explanations for hold-up in Europe is e.g. given in Degryse and

Cayseele (2000) and Kracaw and Zenner (1998).

24

first instrument is a dummy variable equal to one if the firm is contained in more

than one stock index (Multiple Indices). This should increase the visibility of the firm

among investors. Even though these firms may be less risky in a way I have not con-

trolled for, this variable is less problematic than a stock exchange listing which is

clearly a choice variable and associated with similar concerns as public debt market

access. The second instrument is the age of the company (Log (Date of Incorpora-

tion). In prior (unreported) tests I have seen that age does not directly affect the loan

spread. Older firms, however, should be more known in the market and therefore

have a higher probability to access the bond market. Another instrument is the Num-

ber of Shareholders (respective number of owners if the company is privately held). A

larger number of shareholders also proxies for firm visibility. Following Faulkender

and Petersen (2006) and Santos and Winton (2006), I also include SIC Fraction (2 digit)

which measures the percentage of borrowers with the same first-two digit industry

code. The measure is a proxy for industry visibility and a larger fraction should also

facilitate bond issues by a borrower within the same industry. However, as also ex-

plained in the paper cited above, this measure could be correlated with unobserved

risk factors (common to firms within the same industry) I have not controlled for

but which directly affect loan spread. However, I also control for one digit industry

code in the second stage which might alleviate this effect. My last instrument is the

percentage of borrowers with public debt market access in the particular year (Total

Bond Market Access). The higher this ratio, the more firms have access to the public

bond market which should facilitate bond issues for all firms. Table IV shows the

regression results.

[Table IV]

The first column presents the results from the first stage regression. All variables

are highly significant showing the expected signs. If the instruments are only weakly

correlated with the endogenous variable, the IV estimates are biased towards those of

OLS (Bound, Jaeger, and Baker (1995), Staiger and Stock (1997), and Stock and Watson

(2003)). The F-statistic for the hypothesis that the coefficients on the instruments are

25

jointly zero is large and statistically significant suggesting that the IV estimates are

unlikely to be biased.

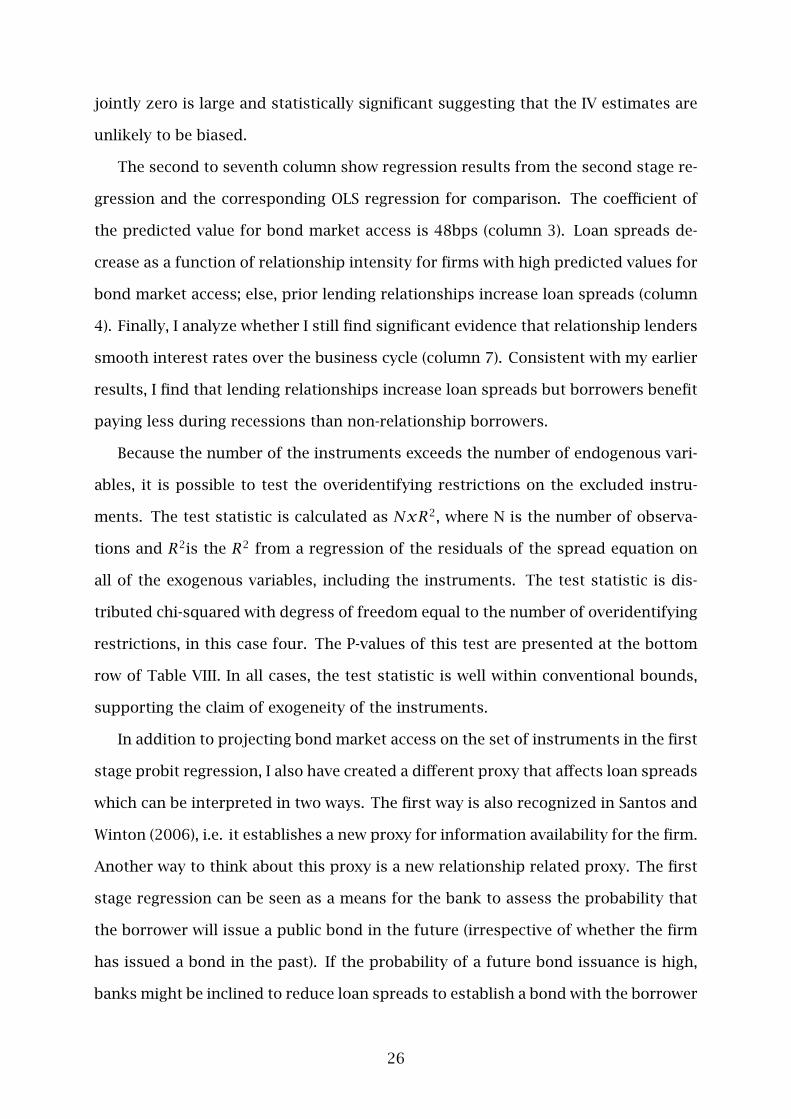

The second to seventh column show regression results from the second stage re-

gression and the corresponding OLS regression for comparison. The coefficient of

the predicted value for bond market access is 48bps (column 3). Loan spreads de-

crease as a function of relationship intensity for firms with high predicted values for

bond market access; else, prior lending relationships increase loan spreads (column

4). Finally, I analyze whether I still find significant evidence that relationship lenders

smooth interest rates over the business cycle (column 7). Consistent with my earlier

results, I find that lending relationships increase loan spreads but borrowers benefit

paying less during recessions than non-relationship borrowers.

Because the number of the instruments exceeds the number of endogenous vari-

ables, it is possible to test the overidentifying restrictions on the excluded instru-

ments. The test statistic is calculated as NxR2, where N is the number of observa-

tions and R2is the R2 from a regression of the residuals of the spread equation on

all of the exogenous variables, including the instruments. The test statistic is dis-

tributed chi-squared with degress of freedom equal to the number of overidentifying

restrictions, in this case four. The P-values of this test are presented at the bottom

row of Table VIII. In all cases, the test statistic is well within conventional bounds,

supporting the claim of exogeneity of the instruments.

In addition to projecting bond market access on the set of instruments in the first

stage probit regression, I also have created a different proxy that affects loan spreads

which can be interpreted in two ways. The first way is also recognized in Santos and

Winton (2006), i.e. it establishes a new proxy for information availability for the firm.

Another way to think about this proxy is a new relationship related proxy. The first

stage regression can be seen as a means for the bank to assess the probability that

the borrower will issue a public bond in the future (irrespective of whether the firm

has issued a bond in the past). If the probability of a future bond issuance is high,

banks might be inclined to reduce loan spreads to establish a bond with the borrower

26

and afterwards be chosen as underwriter in the bond syndicate.29 In either case, the

IV results support my main hypotheses.

5.2 Further robustness test

5.2.1 Sample selection concerns

One concern associated with using LPC Dealscan as loan database is that cover-

age of loans increased over time which implies a possible sample selection bias in my

sample. Since many loans are not included in earlier years, I might not dentify re-

lationships between borrowers and banks properly and the likelihood of identifying

relationships increases over time. This further relates to the question how to define

a reasonable horizon over which to define relationships and over which to define

the "durability" of proprietary information of a relationship lender.30 I address this

concern in two ways: First, I reduce the look-back window to identify lending rela-

tionships to 3 years and rerun the regressions. Second, I drop the first half of my

sample (i.e. all loans prior to 2001), recalculate the relationship measure and rerun

all regressions. As expected, all results remain unchanged.31

To ensure that results are not driven by the smallest firms, I exclude the smallest

quartile of firms using (1) total assets and (2) revenues as proxies. Applying method

(1), I drop all loans to borrowers with an asset size smaller than USD 174 million,

leaving 1,019 observations for the regression. Under method (2), I drop all loans

to borrowers with revenues below USD 146 million and my sample size is reduced

to 966 observations. I re-run the regressions but the results remain qualitatively

unchanged (and are not reported for brevity). The statistical significance for the

effect that lending relationships reduce spreads for non-bank dependent borrowers

Relationship Number*Last Bond Public=1) is weaker at the 12 percent level. All other

29Interviews with practitioners revealed that deliberate mispricing of loan spreads is a commonrelationship driven aspect in the corporate loan market.

30However, I do not believe that this is a problem in the methodology. Since I do not focus onrelationship duration but rather on relationship intensities, information generated once and yearsbefore the loan is extended is assigned a much smaller weight than information frequently generatedand is likely to drop out of my models when I assign the highest intensity to the loan facility.

31All results are available upon request.

27

results remain significant at the one percent level.

I described earlier in the paper, that I use subjective criteria to identify the lead

banks in the syndicate. Until now, I dropped all lenders with "participant" role as

assigned to the lender in Dealscan, calculated the relationship variables for all lead

role banks and assigned the highest value to the loan facility. The upside of this

approach is clearly that I focus only on bank-borrower relationships to identify the

lead bank (which is the bank with the highest relationship intensity). The downside

of the approach is that I might neglect information about the "lender role" as given

by Dealscan (which are the roles that have been reported to LPC and are used to

assign league table credit for the lenders). I therefore modify the definition of the

lead bank. I follow earlier studies that used LPC as loan information provider and

define the mandated arranger as lead bank whenever available. In all other cases, I

go down the list of administrative agent, book runner, lead arranger, lead manager,

agent, and arranger.32 However, there are still cases, where the same role is assigned

to more than one bank. In this case, I use two different approaches: First, I chose the

bank with the highest relationship intensity measure as lead bank. Second, I rank

the remaining lead banks by asset size and choose the bank with the biggest balance

sheet. Balance sheet strength can be a good proxy for bargaining power among the

banks in the syndicate. I re-run all regressions with the three different methodolo-

gies described and obtain very similar results to the ones reported. I am therefore

confident not to introduce a sample selection bias by focusing on the relationship

strength as indicator for the lead bank of the syndicate.

5.2.2 Additional macroeconomic and risk proxies

In further (unreported) tests, I address whether banks price the term structure

environment and credit spreads when originating the loan following Angbazo, Mei,

32I focus on the lead bank because they regularly hold the largest share of the loan (see Krosznerand Strahan (2001)) and has the fiduciary duty vis-à-vis other syndicate members to monitor andprovide timely information about the borrower. The lead bank is responsible for several tasks whichclearly identify it as relationship lender (see Madan, Sobhani, and Horowitz (1999) and Bharath,Dahiya, Saunders, and Srinivasan (2007)).

28

and Saunders (1998) and Gupta, Singh, and Zebedee (2007). These papers use the

spread as percentage of LIBOR as dependent variable. I substitute the AISD over

LIBOR as dependent variable and rerun our tests. My hypotheses are supported by the

results. The R2 are higher in the relative spread model giving support to the notion

that banks price some factors into loan spreads that are not explicitly considered in

the relative spread models. I also change the model specification and include LIBOR

as additional independent varibale. I further add a proxy for the term structure of

interest rates (the difference between a 30 year and a 5 year treasury bond) and credit

spreads calculated as the difference between Moody’s AAA corporate bond and Baa

corporate bond (middle) rates. Again, my results find strong support.

6 Conclusion

This paper sheds some light on the importance of lending relationships in pric-

ing syndicated loans. Using a novel dataset and combining bond and loan data for

large private borrowers, I find evidence for loan rate smoothing if borrowers have

no access to public debt. For non-bank dependent borrowers, loan spreads decline

in the strength of the relationship. In periods of recession, borrowers with strong

relationships pay less on newly issued loans, ceteris paribus. This is the first paper

to explicitly address this issue. One reason might be that the European loan market

is considerably more relationship driven than the US market. This suggests that ana-

lyzing European loan deals even further is an interesting task to find more conclusive

evidence for benefits of lending relationships.

29

References

Allen, F., and D. Gale, 1997, “Financial markets, intermediaries, and intertemporal

smoothing,” Journal of Political Economy, 105, 523–546.

, 1999, “Innovations in financial services, relationships and risk sharing,” Man-

agement Science, 45(9), 1239–1253.

Angbazo, L. A., J. Mei, and A. Saunders, 1998, “Credit spreads in the market for

highly leveraged transaction loans,” Journal of Banking and Finance, 22(10-11),

1249–1282.

Ball, R., and L. Shivakumar, 2005, “Earnings quality in UK private firms: comparative

loss recognition timeliness,” Journal of Accounting and Economics, 39, 83–128.

Berger, A. N., and G. F. Udell, 1992, “Some Evidence on the Empirical Relevance of

Credit Rationing,” Journal of Political Economy, 100, 1047–1077.

, 1995, “Relationship Lending and Lines of Credit in Small Firm Finance,” The

Journal of Business, 68(3), 351–381.

Berlin, M., and L. J. Mester, 1992, “Debt Covenants and Renegotiation,” Journal of

Financial Intermediation, 2, 95–133.

, 1999, “Deposits and Relationship Lending,” Review of Financial Studies, 12(3),

579–607.

Bharath, S., S. Dahiya, A. Saunders, and A. Srinivasan, 2007, “Lending Relationships

and Loan Contract Terms: Does Size Matter?,” Working Paper.

Bhattacharya, S., and G. Chiesa, 1995, “Proprietary Information, Financial Intermedi-

ation and Research Incentives,” Journal of Financial Intermediation, 4(328-357).

Billett, M. T., M. J. Flannery, and J. A. Garfinkel, 1995, “The Effect of Lender Identity

on a Borrowing Firm’s Equity Return,” The Journal of Finance, 50(2), 699–718.

30

Boot, A. W. A., 2000, “Relationship Banking: What Do We Know?,” Journal of Financial

Intermediation, 9(1), 7–25.

Boot, A. W. A., S. I. Greenbaum, and A. V. Thakor, 1993, “Reputation and Discretion

in Financial Contracting,” American Economic Review, 83(5), 1165–1183.

Boot, A. W. A., and A. Thakor, 1994, “Moral Hazard and Secured Lending in an In-

finitely Repeated Market Game,” International Economic Review, 35, 899–920.

Bosch, O., and S. Steffen, 2007, “Informed Lending and the Structure of Loan Syndi-

cates - Evidence from the European Syndicated Loan Market,” Working Paper, SSRN

eLibrary.

Bound, J., D. Jaeger, and R. Baker, 1995, “Problems with Instrumental Variables Es-

timation When the Correlation between the Instruments and the Endogenous Ex-

planatory Variabels is Weak,” Journal of American Statistical Association, XC, 443–

450.

Brav, O., 2005, “How Does Access to the Public Capital Market Affect Firms’ Capital

Structure?,” Working Paper, University of Pennsylvania.

Carey, M., M. Post, and S. A. Sharpe, 1998, “Does Corporate Lending by Banks and

Finance Companies Differ? Evidence on Specialization in Private Debt Contracting,”

The Journal of Finance, 53(3), 845–878.

Degryse, H., and P. v. Cayseele, 2000, “Relationship Lending within a Bank-Based

System: Evidence from European Small Business Data,” Journal of Financial Inter-

mediation, 9, 90–109.

Diamond, D. W., 1984, “Financial Intermediation and Delegated Monitoring,” Review

of Economic Studies, 51, 393–414.

, 1991, “Monitoring and Reputation: The Choice between Bank Loans and

Directly Placed Debt,” The Journal of Political Economy, 99(4), 689–721.

31

Fama, E. F., 1985, “What’s different about banks?,” Journal of Monetary Economics,

15(1), 29–39.

Faulkender, M., and M. A. Petersen, 2006, “Does the Source of Capital Affect Capital

Structure?,” Review of Financial Studies, 19(1), 45–79.

Greenbaum, S. I., G. Kanatas, and I. Venezia, 1989, “Equilibrium loan pricing under

the bank-client relationship,” Journal of Banking and Finance, 13(2), 221–235.

Gupta, A., A. K. Singh, and A. A. Zebedee, 2007, “Liquidity in the Pricing of Syndicated

Loans,” Journal of Financial Markets, April 2007.

Hale, G., and J. A. C. Santos, 2006, “Evidence on the Costs and Benefits of Bond IPOs,”

Federal Reserve Bank of San Francisco Working Paper Series, 2006-42.

Hauswald, R., and R. Marquez, 2003, “Information Technology and Financial Services

Competition,” Review of Financial Studies, 16(3), 921–948.

Houston, J., and C. James, 1996, “Bank Information Monopolies and the Mix of Private

and Public Debt Claims,” The Journal of Finance, 51(5), 1863–1889.

James, C., 1987, “Some evidence on the uniqueness of bank loans,” Journal of Finan-

cial Economics, 19(2), 217–235.

Klemperer, P., 1995, “Competition when Consumers have Switching Costs: An

Overview with Applications to Industrial Organization, Macroeconomics, and In-

ternational Trade,” The Review of Economic Studies, 62(4), 515–539.

Kracaw, W., and M. Zenner, 1998, “Bankers in the boardroom: Good News or Bad

News?,” Unpublished Working Paper, University of North Carolina.

Kroszner, R. s., and P. E. Strahan, 2001, “Throwing good money after bad? Board

connections and conflicts of interest,” Working Paper.

Ljungqvist, A., F. Marston, and W. Wilhelm, 2006, “Competing for Securities Under-

writing Mandates: Banking relationships and Analyst Recommendations,” Journal

of Finance, 61, 301–340.

32

Lummer, S. L., and J. J. McConnell, 1989, “Further evidence on the bank lending pro-

cess and the capital-market response to bank loan agreements,” Journal of Finan-

cial Economics, 25(1), 99–122.

Madan, R., R. Sobhani, and K. Horowitz, 1999, “Syndicated Lending,” Paine Webber

Equity Research Report.

Ongena, S., and D. C. Smith, 2000, “What determines the Number of Bank Relation-

ships? Cross-Country Evidence,” Journal of Financial Intermediation, 9, 26–56.

Ongena, S. R., and D. C. Smith, 1998, “Bank Relationships: A Review,” Working Paper.

Petersen, M. A., 2007, “Estimating standard errors in finance panel data sets: Com-

paring approaches,” Review of Financial Studies (forthcoming).

Petersen, M. A., and R. G. Rajan, 1994, “The Benefits of Lending Relationships: Evi-

dence from Small Business Data,” The Journal of Finance, 49(1), 3–37.

, 1995, “The Effect of Credit Market Competition on Lending Relationships,”

The Quarterly Journal of Economics, 110(2), 407–443.

Rajan, R., 1992, “Insiders and Outsiders: The Choice Between Informed and Arm’s

Length Debt,” The Journal of Finance, XLVII(4).

Santos, J. A. C., and A. Winton, 2006, “Bank Loans, Bonds, and Information Monopolies

across the Business Cycle,” Journal of Finance (forthcoming).

Schenone, C., 2007, “Lending Relationships and Information Rents: Do Banks Exploit

Their Information Advantages?,” Working Paper.

Sharpe, S. A., 1990, “Asymmetric Information, Bank Lending and Implicit Contracts:

A Stylized Model of Customer Relationships,” Journal of Finance, 45, 1069–1087.

Slovin, M. B., M. E. Sushka, and J. A. Polonchek, 1993, “The Value of Bank Durability:

Borrowers as Bank Stakeholders,” Journal of Finance, 48(1), 247.

33

Staiger, D., and J. H. Stock, 1997, “Instrumental Variables Regression with Weak In-

struments,” Econometrica, LXV, 557–586.

Steffen, S., and M. Wahrenburg, 2007, “Syndicated Loans, Lending Relationships and

the Business Cycle,” Working Paper.

Stock, J. H., and M. W. Watson, 2003, Introduction to Econometrics. Addison Wesley,

Boston, MA.

Sufi, A., 2007, “Information Asymmetry and Financing Arrangements: Evidence from

Syndicated Loans,” The Journal of Finance, 62(2), 629–668.

34

Appendix. Variable Definition

Variable Description Source

Loan Contract Variables

All-in spread drawn (AISD) AISD is defined as the coupon spread on the drawn amount plus any annualfee.

LPC Dealscan

Log (Maturity) Log (Maturity) is the natural logarithm of one plus the loan tenor (measuredin months)

Log (Facility Size) Log (Facility Size) is the natural logarithm of the loan amount (measured in$MM)

LPC Dealscan

Performance Pricing Performance Pricing is a dummy variable equal to one if the loan includesperformance pricing provisions.

LPC Dealscan

Refinancing Refinancing is a dummy variable equal to one if the loan is refinanced andnot a first loan issue.

LPC Dealscan

Covenants Covenants is a dummy variable equal to one if the loan contract includescovenants.

LPC Dealscan

Secured Secured is a dummy variable equal to one, if the loan was secured with col-lateral.

LPC Dealscan

Senior Senior is a dummy variable equal to one if the loan was senior. LPC DealscanTerm Loan Term Loan is a dummy variable equal to one if the loan type was a (non

amortizing) term loan.LPC Dealscan

Revolver Revolver is a dummy variable equal to one if the loan was either a revolvingcredit facility or an amortizing loan.

LPC Dealscan

Syndicate Structure

Relationship Variables

Relationship Dummy Relationship Dummy is a dummy variable capturing whether the loan is arelationship loan or not. The facility is assigned the value of 1, if the leadbank in the current lending syndicate has been lead lender in a previous loanissued by the same borrower (using a five year look-back window). In thosecases where there is more than one lead bank, the facility is assigned thevalue of 1, if at least one lead bank is a relationship bank according to thisdefinition.

LPC Dealscan

Relationship Number Relationship Number captures how many loans have been given by a leadbank relative to the number of loans the borrower has issued over the lastyears. Again, if there is more than one lead bank, this measure is calculatedfor each lead bank and the highest value is assigned to the loan facility.

LPC Dealscan